A Theoretical Analysis of the Stationarity of an Unrestricted Autoregression Process

Abstract

The higher dimensional autoregressive models would describe some of the econometric processes relatively generically if they incorporate the heterogeneity in dependence on times. This paper analyzes the stationarity of an autoregressive process of dimension having a sequence of coefficients multiplied by successively increasing powers of . The theorem gives the conditions of stationarity in simple relations between the coefficients and in terms of . Computationally, the evidence of stationarity depends on the parameters. The choice of sets the bounds on and the number of time lags for prediction of the model. 111 Initial paper Acknowledgements: Thanks to Prabha Sharma, Ajit Iqbal Singh

1 Introduction

Autoregression models of time series represent stochastic dynamical systems. They are commonly used by econometricians as techniques to predict economic indicators based on the values in previous times. The randomness in the time evolution impacts the predictability and the number of lagged time steps included in the model. Some mathematical economists (Chiang and Wainwright, Im et al, Box et al, Judge et al, Samuelson)[1, 2, 3, 4, 5] have investigated the time series properties of stationarity, ergodicity and causality theoretically to understand the dynamics of autoregressive models. In general, AR denotes an autoregressive model of dimension . The research in this area has often addressed the theory of lower dimensional AR processes more than that of the higher dimensional models [6]. In this paper, I analyze the stationarity conditions of a particular case of the unrestricted AR (), model.

Previous research has focused on the stationarity of AR process with identical coefficients. In econometrics, there are, however, situations conforming to different kinds of AR) models. Consider the autoregressive model predicting the time evolution of a quantity or economic indicator when there are individuals or entities in the system showing varying levels of dependence on the previous values in time. For instance, the formation of inflationary expectations and the information propagation through the economy are heterogenous processes.

A prediction through an AR process may involve an unequal dependence on the different time lags, usually diminishing with increasing lags. The heterogeneity of the time dependence in this model maybe related to the asymmetry of information, inequality, or some other kind of phenomenon, and this may result in different models and their estimations.

This paper analyzes an unrestricted AR model wherein the coefficients of the first two time lags are equal, and the coefficients of the times beyond decrease sequentially with the number of previous time steps taken.

2 Model

The model is given as

| (1) |

where denotes the innovation term such that it has mean and variance as . And small so that . Choosing a suitable and generalizes . Also , .

The system in Eq.(1) describes a situation when there can be any number of past time steps or lags considered in the model with respect to the current time so that the term of the series would be at least equal to a chosen arbitrarily small number . This restricts the permissible number of terms in the model, however, given that by choice, the variation in the number of terms can be very large.

In a dimensional system, one may associate the coefficients with the proportions of individuals or firms in a population or economy according to their dependence or the relative importance placed on the values of the economic time series in the previous times. In this context, I consider the first two coefficients denoting two different categories as being equal whereas all the other coefficients as proportionate to them.

The system in Eq(1) is equivalent to

| (2) |

where , and .

In this paper, I find the bound on the coefficient that satisfies the condition to achieve convergence to stationarity of the unrestricted AR system defined in Eq.(2). Researchers have solved this for AR process with equal coefficients (or weights), but the case presented in this paper is unique in the sense that the coefficients in the system bear a sequential relation. Every coefficient is discounted in proportion to the coefficient at previous time step.

3 Analysis and proof

The rest of this paper analyses the system and provides the proof. It depends on some well known results and theorems.

The AR process in Eq.(1) has a characteristic polynomial of degree associated with it and (in accordance with algebraic theorem) every such polynomial has roots.

The conditions on stationarity of AR () process defined above in (1) are equivalent to those of the convergence of a polynomial (Box et al, Judge et al, Samuelson, Carmichael). From Eq.1

| (3) |

In particular, the unrestricted AR process is stationary if the polynomial polynomial has roots beyond the unit circle. This implies the condition that the roots of

| (4) |

would be lower than 1. In other words, the roots of (3) should be lower than 1 for AR() process to converge to stationarity.

Researchers in economics and mathematics have shown that in order to ascertain the convergence of temporal paths, the conditions are derivable without the estimation of the roots of the characteristic equation. They have achieved this by utilizing some of the theorems including those of algebra, Rouche and Hurwitz theorems in complex analysis and Cauchy resulting in bounds and relations between roots and coefficients (Chiang and Wainwright, Samuelson, Carmichael)[1, 5, 7]. In accordance with the Schur theorem, it is necessary and sufficient for the degree polynomial to have roots lower than unity, that all of its determinants are positive. Hence in this case, we rewrite the polynomial in Eq. (4)

| (5) |

This polynomial in Eq. (5) has coefficients as a geometric sequence. is a matrix of the structure of the blocks

These blocks consist of matrices and and their transposes, which can be identified in A. In this context, the AR process is stationary if and only if , .

is a square matrix of dimension matrix characterizing the polynomial wherein the coefficients are multiplied by the sequence of constants .

Evidently, if then the matrix represents the case of equal coefficients that has been studied previously (Im et al) [2]. The spectral analysis of that system yields multiple eigenvalues of same magnitude indicating the inherent instability particularly for large . Here, , and the sequence of constants alters the matrix of coefficients and its properties while rendering the analysis of the matrix intricate. The triangularization of through Schur technique is algorithmic which may require a lot of numerical analysis, particularly as the size of the matrix becomes greater than 3. However, one may observe that as the dimension increases, the matrix A tends to get sparser. In addition, since is small, it creates a sparser matrix . This has a simpler approximation if obtained through perturbation of the matrix and its properties. It gives a circle around eigenvalues as a range of stability and the deviation depends on the size and nature of the perturbation.

In accordance with the procedure for obtaining eigenvalues delineated earlier (Im et al)[2], can be written in terms of a square block matrix , identity matrix and matrix obtained by taking the Hadamard product. If is defined as , taking as a lower triangular matrix such that if

and otherwise.

Then . whenever and , and otherwise. is a square matrix of same dimension such that the elements of are identical to those of but without the coefficients in the elements. The matrix is a matrix of same dimension as A () and is a matrix with all elements as . is the Hadamard product. The eigenvalues of A, therefore, are bounded and dependent on the product of these matrices. (If all elements of are 1, then it reduces to the all equal coefficients system studied previously). However, this is merely a slight perturbation to the system and therefore the eigenvalues should not be very different from those of and I incorporate this using an additive perturbed matrix, instead. is defined as

where

and

The original matrix can now be expressed as

or

| (6) |

taking

Any vector can be an eigenvector of the Identity matrix with eigenvalue 1. Thus the eigenvalues of A are equal to where denotes the eigenvalues of . According to a well known Bauer-Fike theorem, the eigenvalues of will be inside the circle surrounded by eigenvalues of of radius as constant . In particular,

and where is the constant defined as

and , being the matrix of eigenvectors of .

Remark.

The number of terms of previous times in the AR model is bounded.

The remark statement is consistent with the definition and specification of parameters. In general, the term of the sequence converges as such that . This is a Cauchy sequence and so the series can be truncated after some of the previous times. In other words, it specifies the starting point of the model. Therefore, is constrained by , . It means that the number of terms and the dependence on the previous time steps diminishes depending on and other parameters.

Lemma 1.

is finite

Proof:

is the norm of the matrix and we show here that it is bounded. The norm is

This becomes upon simplification

.

This expands to

and converges to

Thus,

| (7) |

It must be noted that, , and so on.

The polynomial in the square brackets under square root sign in Eq. (7) depends on constant functions and the parameter nonlinearly (increasing). The behavior of dominates that of the constant functions of and, therefore, . It is evident that . At fixed levels of , , the value of depends only on . But is constrained to be around a certain value set by the choice of and . Hence, remains finite within the realm of this context. Thus according to the lemma, this indicates that the eigenvalues are constrained to a finite range of stability.

Lemma 2.

The eigenvalues of , satisfy

Proof

To find the eigenvalues of , we can use a similarity transformation as shown earlier in the case of equal coefficients [2]. According to this transformation, with the matrix defined as

and

Therefore

and eigenvalues of are same as those of which means, . Here, .

Now for and for . So,

for , for , and for

First consider the case of lower than or equal to inequality which yields

Then the second case of greater than or equal to as

Theorem.

A necessary and sufficient condition that the time evolution of the autoregressive model

, , and

, converges to stationarity is that .

Proof

The condition for stationarity is that the determinant . Hence, the determinant as expressed in this equation is given as

| (8) |

The results of lemmas 1 and 2 specify the eigenvalues of and the range depending on the dimension considered. Therefore,

| (9) |

In the first case of lower than inequality

.

It requires that . This results in

| (10) |

Then in the case of greater than inequality, , the lower bound is The condition of stationarity now requires that be chosen so that the right side of the inequality is at least greater than 0. This means

| (11) |

Thus from Eqs. (10) and (11), the condition is and . increases with , and so . If , it simply reduces to .

Thus it is interesting that the stationarity of this unrestricted AR process is given by a simple relation, determined by the coefficients and .

The attempt to reproduce this result on a time series in the appendix shows that the bounds on for obtaining stationarity may not be as strict as given in the theorem. Rather, it manifests clearly in terms of the variation of the strengths of evidence of stationarity within versus outside these bounds. In other words, to obtain a perceptible inference of non stationarity, one should take much greater than specified by this boundary.

Corollary 1.

The stationary of this , model requires sum of all its coefficients to be lower than 1.

Proof:

The theorem specifies the allowed interval around when the AR model is . Therefore, here, the sum of coefficients is

. The sum converges and

| (12) |

Then for the sum to be , I show that . By the construction, when .

And, because has a unitary matrix of eigenvectors as , therefore, and . If we consider the case of a relatively small , then . In particular if , for the stationary AR(2) process, . In case of larger value of , both and increase with or as . increases as a function of and , so and this means that the sum total of the coefficients of the unrestricted AR model is .

Corollary 2.

In the stationary AR model, the lower bound on is dependent on as .

Proof:

We have the AR() model, . If this process converges to stationarity, then for a fixed as constant, according to the theorem, and that . Taking from the Corollary 1, we have

. This establishes the lower bound on . It is consistent with . It is interesting as it indicates that it decreases as increases. Thus the choice of restricts the number of lagged terms in the model. The example of the time series and simulation in the Appendix also demonstrates this.

Appendix

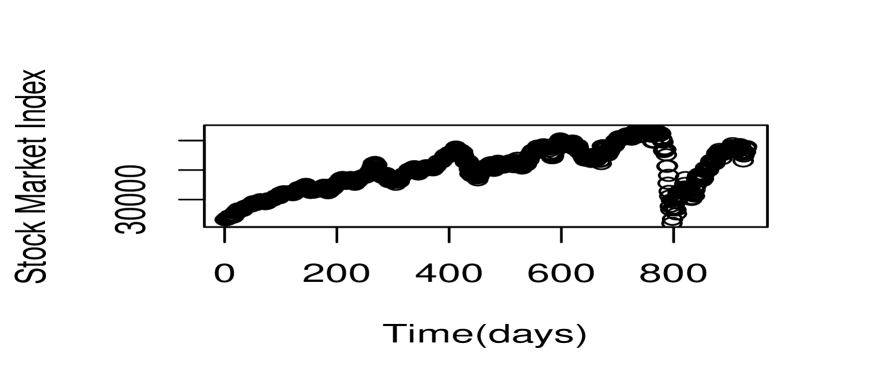

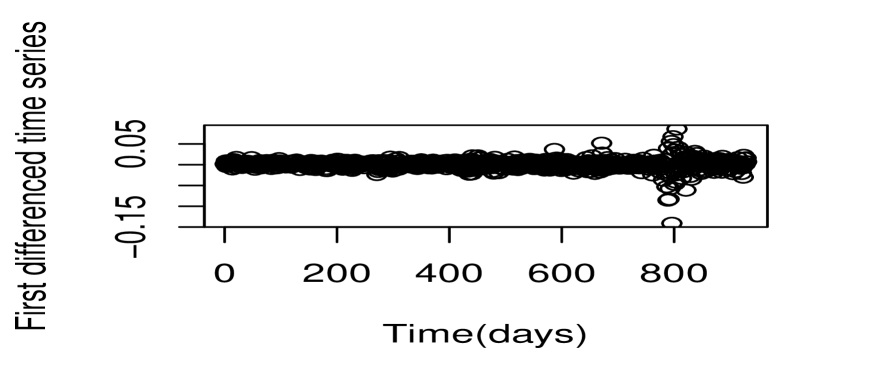

Figure 1 below shows the time series of Bombay Stock Exchange (BSE) market index, called the BSE Sensex. The coefficient of the AR(1) model of the first differenced time series for the first 100 data points (days) estimated through linear regression is less than 1, which implies stationarity of the model. Then the coefficients of the generic model in Eqs. (1,2) computed using linear regression for are used to fit the model for another time period. The Akaike Information Critierion is usually applied to know the number of lags though here we take the coefficients sequentially so that greater time lags terms would diminish gradually. The estimated regression prediction on the next 40 days is not significant, however, it shows reasonably accuracy. Further, the simulated time series using the regression coefficients is non stationary and does not predict significantly.

In accordance with the theorem, the choice of determines for attaining stationarity. The model in Eqs.(1,2) simulated for shows varying strengths of evidence for stationarity (Table 1) based on the Augmented Dickey Fuller test statistic.

| Stationarity | ||

|---|---|---|

| 0.0001 | 0.5 | Highly strong stationarity |

| 0.3 | 0.5 | Moderately stationary |

| 0.35 | 0.5 | Weak stationarity |

| 0.4 | 0.5 | Non stationarity |

| 0.0001 | 0.55 | Highly strong stationarity |

| 0.3 | 0.55 | Moderately stationary |

| 0.35 | 0.55 | Weak stationarity |

| 0.4 | 0.55 | Non stationarity |

| 0.0001 | 0.6 | Stationary |

| 0.3 | 0.6 | Moderately stationary |

| 0.35 | 0.6 | Non stationarity |

| 0.4 | 0.6 | Non stationarity |

| 0.0001 | 0.65 | Stationary |

| 0.3 | 0.65 | Moderately stationary |

| 0.35 | 0.65 | Non stationarity |

| 0.4 | 0.65 | Non stationarity |

| 0.0001 | 0.7 | Weak Stationary |

| 0.3 | 0.7 | Non stationary |

| 0.35 | 0.7 | Non stationarity |

| 0.4 | 0.7 | Non stationarity |

In the simulation, the initial values maybe taken as the consecutive data points from any time period within the time series for computing the model for about 50 time steps in future using different values of . Table 1 shows that as increases beyond ( Theorem), the evidence of stationarity weakens. However, it is very strong when is close to the interval set by the theorem. The simulated model also predicts the BSE Sensex with reasonable accuracy in the time period. The root mean square error for comparing the original data and prediction model: is slightly lower and hence the model computed for prediction is significantly more accurate than the one obtained by using the regression coefficients, an advantage of the model. The boundaries set by the theorem on are, however, relatively flexible on this time series.

References

- [1] A.C Chiang and K. Wainwright, Fundamental Methods of Mathematical Economics, 4th ed, McGraw-Hill, NY, 1980.

- [2] E.I. Im, D. L. Hammes and D.T. Wills, Stationarity Condition for an AR Index Process, Econometric Theory, 2006, 22, 164-168.

- [3] G. E. Box, G. M. Jenkins, G.C. Reinsel and G. M. Ljung, Time series analysis, 5th ed, Wiley, NJ, 2010.

- [4] G. G. Judge, W.E. Griffiths, R.C. Hill, H. Lutkepohl and T.C. Lee, Introduction to the Theory and Practice of Econometrics, 2nd ed, Wiley, NY, 1989.

- [5] P. A. Samuelson, Conditions that the Roots of a Polynomials be Less than Unity in Absolute Value, The Annals of Mathematical Statistics, 1941, 12, 360-364.

- [6] H. Akaike, Fitting autoregressive models for prediction, Ann. Inst. Stat. Math. 1969, 21, 243-247.

- [7] R.D. Carmichael, Elementary Inequalities for the Roots of an Algebraic Equation, Amer. Math. Soc. Bull. 1918, 24, 286-296.