Risk Bounds and Calibration for a Smart Predict-then-Optimize Method

University of California, Berkeley††thanks: {heyuan_liu, pgrigas}@berkeley.edu

)

Abstract

The predict-then-optimize framework is fundamental in practical stochastic decision-making problems: first predict unknown parameters of an optimization model, then solve the problem using the predicted values. A natural loss function in this setting is defined by measuring the decision error induced by the predicted parameters, which was named the Smart Predict-then-Optimize (SPO) loss by Elmachtoub and Grigas (2021). Since the SPO loss is typically nonconvex and possibly discontinuous, Elmachtoub and Grigas (2021) introduced a convex surrogate, called the SPO+ loss, that importantly accounts for the underlying structure of the optimization model. In this paper, we greatly expand upon the consistency results for the SPO+ loss provided by Elmachtoub and Grigas (2021). We develop risk bounds and uniform calibration results for the SPO+ loss relative to the SPO loss, which provide a quantitative way to transfer the excess surrogate risk to excess true risk. By combining our risk bounds with generalization bounds, we show that the empirical minimizer of the SPO+ loss achieves low excess true risk with high probability. We first demonstrate these results in the case when the feasible region of the underlying optimization problem is a polyhedron, and then we show that the results can be strengthened substantially when the feasible region is a level set of a strongly convex function. We perform experiments to empirically demonstrate the strength of the SPO+ surrogate, as compared to standard and squared prediction error losses, on portfolio allocation and cost-sensitive multi-class classification problems.

1 Introduction

The predict-then-optimize framework, where one predicts the unknown parameters of an optimization model and then plugs in the predictions before solving, is prevalent in applications of machine learning. Some typical examples include predicting future asset returns in portfolio allocation problems and predicting the travel time on each edge of a network in navigation problems. In most cases, there are many contextual features available, such as time of day, weather information, financial and business news headlines, and many others, that can be leveraged to predict the unknown parameters and reduce uncertainty in the decision making problem. Ultimately, the goal is to produce a high quality prediction model that leads to a good decisions when implemented, such as a position that leads to a large return or a route that induces a small realized travel time. There has been a fair amount of recent work examining this paradigm and other closely related problems in data-driven decision making, such as the works of Bertsimas and Kallus (2020); Donti et al. (2017); Elmachtoub and Grigas (2021); Kao et al. (2009); Estes and Richard (2019); Ho and Hanasusanto (2019); Notz and Pibernik (2019); Kotary et al. (2021), the references therein, and others.

In this work, we focus on the particular and important case where the optimization problem of interest has a linear objective with a known convex feasible region and where the contextual features are related to the coefficients of the linear objective. This case includes the aforementioned shortest path and portfolio allocation problems. In this context, Elmachtoub and Grigas (2021) developed the Smart Predict-then-Optimize (SPO) loss function, which directly measures the regret of a prediction against the best decision in hindsight (rather than just prediction error, such as squared error). After the introduction of the SPO loss, recent work has studied its statistical properties, including generalization bounds of the SPO loss function in El Balghiti et al. (2019) and generalization and regret convergence rates in Hu et al. (2020). Moreover, since the SPO loss is not continuous nor convex in general (Elmachtoub and Grigas, 2021), which makes the training of a prediction model computationally intractable, Elmachtoub and Grigas (2021) introduced a novel convex surrogate loss, referred to as the SPO+ loss. Elmachtoub and Grigas (2021) highlight and prove several advantages of the SPO+ surrogate loss: (i) it still accounts for the downstream optimization problem when evaluating the quality of a prediction model (unlike prediction losses such as the squared loss), (ii) it has a desirable Fisher consistency property with respect to the SPO loss under mild conditions, and (iii) it often performs better than commonly considered prediction losses in experimental results. Unfortunately, although a desirable property of any surrogate loss in this context, Fisher consistency is not directly applicable when one only has available a finite dataset, which is always the case in practice, because it relies on full knowledge of the underlying distribution. Motivated thusly, it is desirable to develop risk bounds that allow one to translate an approximate guarantee on the risk of a surrogate loss function to a corresponding guarantee on the SPO risk. That is, risk bounds (and the related notion of calibration functions) answer the question: to what tolerance should the surrogate excess risk be reduced to in order to ensure that the excess SPO risk is at most ? Note that, with enough data, it is possible in practice to ensure a (high probability) bound on the excess surrogate risk through generalization and optimization guarantees.

The main goal of this work is to provide risk bounds for the SPO+ surrogate loss function. Our results, to the best of our knowledge, are the first risk bounds of the SPO+ loss, besides the analysis of the -dimensional scenario in Ho-Nguyen and Kılınç-Karzan (2020). Our results consider two cases for the structure of the feasible region of the optimization problem: (i) the case of a bounded polyhedron, and (ii) the case of a level set of a smooth and strongly convex function. In the polyhedral case, we prove that the risk bound of the SPO+ surrogate is , where is the desired accuracy for the excess SPO risk. Our results hold under mild distributional assumptions that extend those considered in Elmachtoub and Grigas (2021). In the strongly convex level set case, we improve the risk bound of the SPO+ surrogate to by utilizing novel properties of such sets that we develop, namely stronger optimality guarantees and continuity properties. As a consequence of our analysis, we can leverage generalization guarantees for the SPO+ loss to obtain the first sample complexity bounds, with respect to the SPO risk, for the SPO+ surrogate under the two cases we consider. In Section 5, we present computational results that validate our theoretical findings. In particular we present results on entropy constrained portfolio allocation problems which, to the best of our knowledge, is the first computational study of predict-then-optimize problems for a strongly convex feasible region. Our results on portfolio allocation problems demonstrate the effectiveness of the SPO+ surrogate. We also present results for cost-sensitive multi-class classification that illustrate the benefits of faster convergence of the SPO risk in the case of strongly convex sets as compared to polyhedral ones.

Starting with binary classification, risk bounds and calibration have been previously studied in other machine learning settings. Pioneer works studying the properties of convex surrogate loss functions for the 0-1 loss include Zhang et al. (2004); Bartlett et al. (2006); Massart et al. (2006) and Steinwart (2007). Works including Zhang (2004); Tewari and Bartlett (2007) and Osokin et al. (2017) have studied the consistency and calibration properties of multi-class classification problems, which can be considered as a special case of the predict-then-optimize framework (El Balghiti et al., 2019). Most related to the results presented herein is the work of Ho-Nguyen and Kılınç-Karzan (2020), who study the uniform calibration properties of the squared loss, and the related work of Hu et al. (2020), who also develop fast sample complexity results for the SPO loss when using a squared surrogate.

Notation.

Let represent element-wise multiplication between two vectors. For any positive integer , let denote the set . Let denote the by identity matrix for any positive integer . For and a positive semi-definite matrix , let denote the normal distribution . We will make use of a generic given norm on , as well as its dual norm which is defined by . For a positive definite matrix , we define the -norm by . Also, we denote the diameter of the set by .

2 Predict-then-optimize framework and preliminaries

We now formally describe the predict-then-optimize framework, which is widely prevalent in stochastic decision making problems. We assume that the problem of interest has a linear objective, but the cost vector of the objective, , is not observed when the decision is made. Instead, we observe a feature vector , which provides contextual information associated with . Let denote the underlying joint distribution of the pair . Let denote the decision variable and assume that we have full knowledge of the feasible region , which is assumed to be non-empty, compact, and convex. When a feature vector is provided, the goal of the decision maker is to solve the contextual stochastic optimization problem:

| (1) |

As demonstrated by (1), for linear optimization problems the predict-then-optimize framework relies on a prediction of the conditional expectation of the cost vector, namely . Let denote a prediction of the conditional expectation, then the next step in the predict-then-optimize setting is to solve the deterministic optimization problem with the cost vector , namely

| (2) |

Depending on the structure of the feasible region , the optimization problem can represent linear programming, conic programming, and even (mixed) integer programming, for example. In any case, we assume that we can solve to any desired accuracy via either a closed-form solution or a solver. Let denote a particular optimization oracle for problem (2), whereby is an optimal solution of . (We assume that the oracle is deterministic and ties are broken in an arbitrary pre-specified manner.)

In order to obtain a model for predicting cost vectors, namely a cost vector predictor function , we may leverage machine learning methods to learn the underlying distribution from observed data , which are assumed to be independent samples from . Most importantly, following (1), we would like to learn the conditional expectation and thus can be thought of as an estimate of . We follow a standard recipe for learning a predictor function where we specify a loss function to measure the quality of predictions relative to the observed realized cost vectors. In particular, for a loss function , the value represents the loss or error incurred when the cost vector prediction is (i.e., ) and the realized cost vector is . Let denote the the risk of given loss function and let denote the optimal -risk over all measurable functions . Also, let denote the empirical -risk. Most commonly used loss functions are based on directly measuring the prediction error, including the (squared) and the losses. However, these losses do not take the downstream optimization task nor the structure of the feasible region into consideration. Motivated thusly, one may consider a loss function that directly measures the decision error with respect to the optimization problem (2). Elmachtoub and Grigas (2021) formalize this notion in our context of linear optimization problems with their introduction of the SPO (Smart Predict-then-Optimize) loss function, which is defined by

where is the predicted cost vector and is the realized cost vector. Due to the possible non-convexity and possible discontinuities of the SPO loss, Elmachtoub and Grigas (2021) also propose a convex surrogate loss function, the SPO+ loss, which is defined as

Importantly, the SPO+ loss still accounts for the downstream optimization problem (2) and the structure of the feasible region , in contrast to losses that focus only on prediction error. As discussed by Elmachtoub and Grigas (2021), the SPO+ loss can be efficiently optimized via linear/conic optimization reformulations and with (stochastic) gradient methods for large datasets. Elmachtoub and Grigas (2021) provide theoretical and empirical justification for the use of the SPO+ loss function, including a derivation through duality theory, promising experimental results on shortest path and portfolio optimization instances, and the following theorem which provides the Fisher consistency of the SPO+ loss.

Theorem 1 (Elmachtoub and Grigas (2021), Theorem 1).

Suppose that the feasible region has a non-empty interior. For fixed , suppose that the conditional distribution is continuous on all of , is centrally symmetric around its mean , and that there is a unique optimal solution of . Then, for all it holds that

Moreover, if , then .

Notice that Theorem 1 holds for arbitrary , i.e., it employs a nonparametric analysis as is standard in consistency and calibration results, whereby there are no constraints on the predicted cost vector associated with . Under the conditions of Theorem 1, given any , we know that the conditional expectation is the unique minimizer of the SPO+ risk. Furthermore, since is also a minimizer of the SPO risk, it holds that the SPO+ loss function is Fisher consistent with respect to the SPO loss function, i.e., minimizing the SPO+ risk also minimizes the SPO risk. However, in practice, due to the fact that we have available only a finite dataset and not complete knowledge of the distribution , we cannot directly minimize the true SPO+ risk. Instead, by employing the use of optimization and generalization guarantees, we are able to approximately minimize the SPO+ risk. A natural question is then: does a low excess SPO+ risk guarantee a low excess SPO risk? More formally, we are primarily interested in the following questions: (i) for any , does there exist such that implies that ?, and (ii) what is the largest such value of that guarantees the above?

Excess risk bounds via calibration.

The notions of calibration and calibration functions provide a useful set of tools to answer the previous questions. We now review basic concepts concerning calibration when using a generic surrogate loss function , although we are primarily interested in the aforementioned SPO+ surrogate. An excess risk bound allows one to transfer the conditional excess -risk, , to the conditional excess -risk, . Calibration, which we now briefly review, is a central tool in developing excess risk bounds. We adopt the definition of calibration presented by Steinwart (2007) and Ho-Nguyen and Kılınç-Karzan (2020), which is reviewed in Definition 2.1 below.

Definition 2.1.

For a given surrogate loss function , we say is -calibrated with respect to if there exists a function such that for all , , and , it holds that

| (3) |

Additionally, if (3) holds for all , where is a class of distributions on , then we say that is uniformly calibrated with respect to the class of distributions .

A direct approach to finding a feasible function and checking for uniform calibration is by computing the infimum of the excess surrogate loss subject to a constraint that the excess SPO loss is at least . This idea leads to the definition of the calibration function, which we review in Definition 2.2 below.

Definition 2.2.

For a given surrogate loss function and true cost vector distribution , the conditional calibration function is defined, for , by

Moreover, given a class of joint distributions , with a slight abuse of notation, the calibration function is defined, for , by

If the calibration function satisfies for all , then the loss function is uniformly -calibrated with respect to the class of distributions . To obtain an excess risk bound, we let denote the biconjugate, the largest convex lower semi-continuous envelope, of . Jensen’s inequality then readily yields , which implies that the excess surrogate risk of a predictor can be translated into an upper bound of the excess SPO risk . For example, the uniform calibration of the least squares (squared ) loss, namely , was examined by Ho-Nguyen and Kılınç-Karzan (2020). They proved that the calibration function is , which implies an upper bound of the excess SPO risk by . In this paper, we derive the calibration function of the SPO+ loss and thus reveal the quantitative relationship between the excess SPO risk and the excess surrogate SPO+ risk under different circumstances.

3 Risk bounds and calibration for polyhedral sets

In this section, we consider the case when the feasible region is a bounded polyhedron and derive the calibration function of the SPO+ loss function. As is shown in Theorem 1, the SPO+ loss is Fisher consistent when the conditional distribution is continuous on all of and is centrally symmetric about its mean . More formally, the joint distribution lies in the distribution class . In Example 3.1, we later show that this distribution class is not restrictive enough to obtain a meaningful calibration function. Instead, we consider a more specific distribution class consisting of distributions whose density functions can be lower bounded by a normal distribution. More formally, for given parameters and , define . Intuitively, the assumptions on the distribution class ensure that we avoid a situation where the density of the cost vector concentrates around some “badly behaved points.” This intuition is further highlighted in Example 3.1. Theorem 2 is our main result in the polyhedral case and demonstrates that the previously defined distribution class is a sufficient class to obtain a positive calibration function. Recall that denotes the diameter of and define a “width constant” associated with by . Notice that whenever has a non-empty interior.

Theorem 2.

Suppose that the feasible region is a bounded polyhedron and define . Then the calibration function of the SPO+ loss satisfies

| (4) |

Theorem 2 yields an uniform calibration result for the distribution class . The dependence on the constants is also natural as it matches the upper bound given by the cases with a -like unit ball feasible region and standard multivariate normal distribution as the conditional probability . Please refer to Example B.1 in the Appendix for a detailed discussion. Let us now provide some more intuition on the parameters involved in the definition of the distribution class and their roles in Theorem 2. In the definition of , is a lower bound on the ratio of the density of the distribution of the cost vector relative to a “reference” standard normal distribution. When is larger, the distribution is behaved more like a normal distribution and it leads to a better lower bound on the calibration function (4) in Theorem 2. The parameter is an upper bound on the standard deviation of the aforementioned reference normal distribution, and the lower bound (4) naturally becomes worse as increases. The parameter measures how the conditional mean deviates from zero relative to the standard deviation of the reference normal distribution. If this distance is larger then the predictions are larger on average and (4) becomes worse. The width constant measures the near-degeneracy of the polyhedron ( is degenerate) and the bound becomes meaningless as . When the feasible region is near-degenerate, i.e., the ratio is close to zero, we tend to have a weaker lower bound on the calibration function, which is also natural.

We now state a remark concerning an extension of Theorem 2 and we describe the example that demonstrates that it is not sufficient to consider the more general distribution class .

Remark 3.1.

In Theorem 2, we assume that the conditional distribution is lower bounded by a normal density on the entire space . We can extend the result of Theorem 2 to the case when is lower bounded by a normal density on a bounded set but the constant is more involved. For details, please refer to Theorem 5 in the Appendix.

Example 3.1.

Let the feasible region be the ball and consider the distribution class . For a fixed scalar , let and . Let the conditional distribution be a mixture of Gaussians defined by for any , and we have . Let the predicted cost vector be , then the excess conditional SPO risk is . Then it holds that the excess conditional SPO+ risk when , and hence we have .

The intuition of Example 3.1 is that the existence of a non-zero calibration function requires the conditional distribution of given to be “uniform” on the space , but not concentrate near certain points. Example 3.1 highlights a situation that considers one such “badly behaved” case where a limiting distribution of a mixture of two Gaussians leads to a zero calibration function.

By combining Theorem 2 with a generalization bound for the SPO+ loss, we can develop a sample complexity bound with respect to the SPO loss. Corollary 3.1 below presents such a result for the SPO+ method with a polyhedral feasible region. The derivation of Corollary 3.1 relies on the notion of multivariate Rademacher complexity as well as the vector contraction inequality of Maurer (2016) in the -norm. In particular, for a hypothesis class of cost vector predictor functions (functions from to ), the multivariate Rademacher complexity is defined as , where are Rademacher random vectors for . Please refer to Appendix A for a detailed discussion of multivariate Rademacher complexity and the derivation of Corollary 3.1.

Corollary 3.1.

Suppose that the feasible region is a bounded polyhedron, the optimal predictor is in the hypothesis class , and there exists a constant such that . Let denote the predictor which minimizes the empirical SPO+ risk over . Then there exists a constant such that for any and , with probability at least , it holds that

Notice that the rate in Corollary 3.1 is . However, the bound is with respect to the SPO loss which is generally non-convex and is the first such bound for the SPO+ surrogate. Hu et al. (2020) present a similar result for the squared surrogate with a rate of , and an interesting open question concerns whether the rate can also be improved for the SPO+ surrogate.

4 Risk bounds and calibration for strongly convex level sets

In this section, we develop improved risk bounds for the SPO+ loss function under the assumption that the feasible region is the level set of a strongly convex and smooth function, formalized in Assumption 4.1 below.

Assumption 4.1.

For a given norm , let be a -strongly convex and -smooth function for some . Assume that the feasible region is defined by for some constant .

The results in this section actually hold in more general situations than Assumption 4.1. In Appendix C, we extend the results of this section to allow the domain of the strongly convex and smooth function in Assumption 4.1 to be any set defined by linear equalities and convex inequalities (Assumption C.1). Herein, we consider the simplified case where the domain is for ease of exposition and conciseness. The results of this section and the extension developed in Appendix C allow for a broad choice of feasible regions, for instance, any bounded ball for any and the probability simplex with entropy constraint. The latter example, which can also be thought of as portfolio allocation with an entropy constraint, is considered in the experiments in Section 5.

As in the polyhedral case, the distribution class is not restrictive enough to derive a meaningful lower bound on the calibration function of the SPO+ loss. We instead consider two related classes of rotationally symmetric distributions with bounded conditional coefficient of variation. These distribution classes are formally defined in Definition 4.1 below, and include the multi-variate Gaussian, Laplace, and Cauchy distributions as special cases.

Definition 4.1.

Let be a given positive definite matrix. We define as the class of distributions with conditional rotational symmetry in the norm , namely

Let denote the conditional expectation . For constants and , define

and

Under the above assumptions, Theorem 3 demonstrates that the calibration function of the SPO+ loss is , significantly strengthening our result in the polyhedral case. Theorem 6 in Appendix C extends the result of Theorem 3 to the aforementioned case where the domain of may be a subset of , which includes the entropy constrained portfolio allocation problem for example.

Theorem 3.

Suppose that Assumption 4.1 holds with respect to the norm for some positive definite matrix . Then, for any , it holds that and .

Let us now provide some more intuition on the parameters involved in the definitions of the distribution classes and and their roles in Theorem 3. In both cases, controls the concentration of the distribution of cost vector around the conditional mean. The more concentrated the distribution is, the better the bounds in Theorem 3 are. In the case of , relates to the probability that the cost vector is “relatively close” to the conditional mean. When is larger, the cost vector is more likely to be close to the conditional mean and the bound will be better.

Our analysis for the calibration function (the proof of Theorem 3) relies on the following two lemmas, which utilize the special structure of strongly convex level sets to strengthen the first-order optimality guarantees and derive a “Lipschitz-like” continuity property of the optimization oracle . The first such lemma strengthens the optimality guarantees of (2) and provides both upper and lower bounds of the SPO loss.

Lemma 1.

Suppose that Assumption 4.1 holds with respect to a generic norm . Then, for any , it holds that

and

The following lemma builds on Lemma 1 to develop upper and lower bounds on the difference between two optimal decisions based on the difference between the two normalized cost vectors.

Lemma 2.

Suppose that Assumption 4.1 holds with respect to a generic norm . Let be such that , then it holds that

and

Note that the lower bound of in Lemma 1 and the upper bound of in Lemma 2 match bounds developed by El Balghiti et al. (2019). Indeed, although El Balghiti et al. (2019) study the more general case of strongly convex sets, the constants are the same since Theorem 12 of Journée et al. (2010) demonstrates that our set is a -strongly convex set. However, the upper bounds in Lemmas 1 and 2 appear to be novel and rely on the special properties of strongly convex level sets. It is important to emphasize that we generally do not expect all of the bounds in Lemmas 1 and 2 to holds for polyhedral sets. Indeed, for a polyhedron the optimization oracle is generally discontinuous at cost vectors that have multiple optimal solutions. The properties in Lemmas 1 and 2 drive the proof of Theorem 3 and hence lead to the improvement from in the polyhedral case to in the strongly convex level set case.

By following similar arguments as in the derivation of Corlloary 3.1, Corollary 4.1 presents the sample complexity of the SPO+ method when the feasible region is a strongly convex level set.

Corollary 4.1.

Suppose that Assumption 4.1 holds with respect to the norm for some positive definite matrix . Suppose further that the optimal predictor is in the hypothesis class , and there exists a constant such that . Let denote the predictor which minimizes the empirical SPO+ risk over . Then there exists a constant such that for any and , with probability at least , it holds that

5 Computational experiments

In this section, we present computational results of synthetic dataset experiments wherein we empirically examine the performance of the SPO+ loss function for training prediction models, using portfolio allocation and cost-sensitive multi-class classification problems as our problem classes. We focus on two classes of prediction models: (i) linear models, and (ii) two-layer neural networks with 256 neurons in the hidden layer. We compare the performance of the empirical minimizer of the following four different loss function: (i) the previously described SPO loss function (when applicable), (ii) the previously described SPO+ loss function, (iii) the least squares (squared ) loss function , and (iv) the absolute () loss function . For all loss functions, we use the Adam method of Kingma and Ba (2015) to train the parameters of the prediction models. Note that the loss functions (iii) and (iv) do not utilize the structure of the feasible region and can be viewed as purely learning the relationship between cost and feature vectors.

Entropy constrained portfolio allocation.

First, we consider the portfolio allocation (Markowitz, 1952) problem with entropy constraint, where the goal is to pick an allocation of assets in order to maximize the expected return while enforcing a certain level of diversity through the use of an entropy constraint (see, e.g., Bera and Park (2008)). This application is an instance of our more general theory for strongly convex level sets on constrained domains, developed in Appendix C. Alternative formulations of portfolio allocation, including when is a polyhedron or a polyhedron intersected with an ellipsoid, have been empirically studied in previous works (see, for example Elmachtoub and Grigas (2021); Hu et al. (2020)). The objective is to minimize where is the negative of the expected returns of different assets, and the feasible region is where is a user-specified threshold of the entropy of portfolio . Note that, due to the differentiability properties of of the optimization oracle in this case (see Lemma 15 in the Appendix), it is possible to (at least locally) optimize the SPO loss using a gradient method even though SPO loss is not convex.

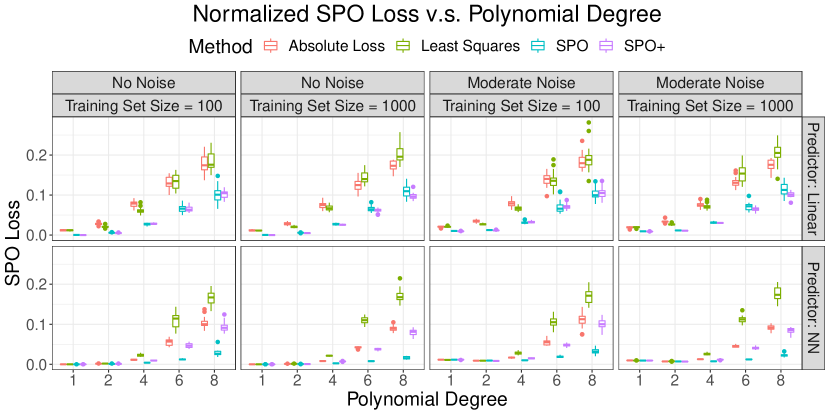

In our simulations, the relationship between the true cost vector and its auxiliary feature vector is given by , where is a polynomial kernel mapping of degree deg, is a fixed weight matrix, and is a multiplicative noise term. The features are generated from a standard multivariate normal distribution, we consider assets, and further details of the synthetic data generation process are provided in Appendix D. To account for the differing distributions of the magnitude of the cost vectors, in order to evaluate the performance of each method we compute a “normalized” SPO loss on the test set. Specifically, let denote a trained prediction model and let denote the test set, then the normalized SPO loss is defined as , where is the optimal cost in hindsight. We set the size of the test set to . In all of our experiments, we run independent trials for each setting of parameters.

Figure 1 displays the empirical performance of each method. We observe that with a linear hypothesis class, for smaller values of the degree parameters, i.e., , all four methods perform comparably, while the SPO and SPO+ methods dominate in cases with larger values of the degree parameters. With a neural net hypothesis class, we observe a similar pattern but, due to the added degree of flexibility, the SPO method dominates the cases with larger values of degree and SPO+ method is the best among all surrogate loss functions. The better results of the loss as compared to the squared loss might be explained by robustness against outliers. Appendix D also contains results showing the observed convergence of the excess SPO risk, in the case of polynomial degree one, for both this experiment and the cost-sensitive multi-class classification case.

Cost-sensitive multi-class classification.

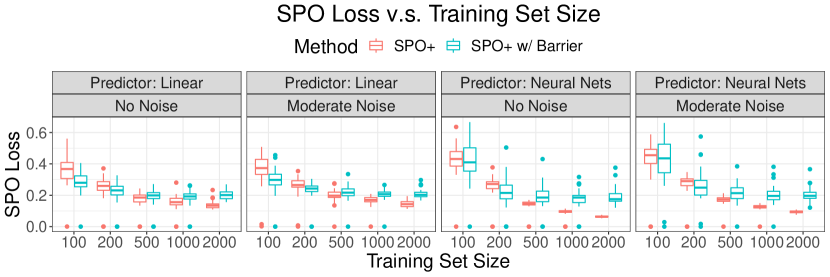

Here we consider the cost-sensitive multi-class classification problem. Since this is a multi-class classification problem, the feasible region is simply the unit simplex We consider an alternative model for generating the data, whereby the relationship between the true cost vector and its auxiliary feature vector is as follows: first we generate a score , where is a degree-deg polynomial kernel, is a fixed weight vector, is a multiplicative noise term, and is the logistic function. Then the true label is given by and the cost vector is given by for . The features are generated from a standard multivariate normal distribution, and further details of the synthetic data generation process are provided in Appendix D. Since the scale of the cost vectors do not change as we change different parameters, we simply compare the test set SPO loss for each method. We still set the size of the test set to and we run independent trials for each setting of parameters. In addition to the regular SPO+, least squares, and absolute losses, we consider an alternative surrogate loss constructed by considering the SPO+ loss using a log barrier (strongly convex) approximation to the unit simplex. That is, we consider the SPO+ surrogate that arises from the set for some . Details about how we chose the value of are provided in Appendix D.

Herein we focus on the comparison between the standard SPO+ loss and the “SPO+ w/ Barrier” surrogate loss. (We include a more complete comparison of all the method akin to Figure 1 in Appendix D.) Figure 2 shows a detailed comparison between these alternative SPO+ surrogates as we vary the training set size. Note that the SPO loss is always measured with respect to the standard unit simplex and not the log barrier approximation. Interestingly, we observe that the “SPO+ w/ Barrier” surrogate tends to perform better than the regular SPO+ surrogate when the training set size is small, whereas the regular SPO+ surrogate gradually performs better as the training set size increases. These results suggest that adding a barrier constraint to the feasible region has a type of regularization effect, which may also be explained by our theoretical results. Indeed, adding the barrier constraint makes the feasible region strongly convex, which improves the rate of convergence of the SPO risk. On the other hand, this results in an approximation to the actual feasible region of interest and, eventually for large enough training set sizes, the regularizing benefit of the barrier constraint is outweighed by the cost of this approximation.

6 Conclusions and future directions

Our work develops risk bounds and uniform calibration results for the SPO+ loss relative to the SPO loss, and our results provide a quantitative way to transfer the excess surrogate risk to excess true risk. We analyze the case with a polyhedral feasible region of the underlying optimization problem, and we strengthen the results when the feasible region is a level set of a strongly convex function. There are several intriguing future directions. In this work, we mainly focus on the worst case risk bounds of the SPO+ method under different types of feasible regions, and we consider the minimal possible conditions to guarantee the risk bounds. In many practical problems, it is reasonable to assume the true joint distribution of satisfies certain “low-noise” conditions (see, for example, Bartlett et al. (2006); Massart et al. (2006); Hu et al. (2020)). In such conditions, one might be able to obtain improved risk bounds and sample complexities. Also, developing tractable surrogates and a corresponding calibration theory for non-linear objectives is very worthwhile.

Acknowledgments

The authors are grateful to Othman El Balghiti, Adam N. Elmachtoub, and Ambuj Tewari for early discussions related to this work. PG acknowledges the support of NSF Awards CCF-1755705 and CMMI-1762744.

References

- Bartlett and Mendelson [2002] P. L. Bartlett and S. Mendelson. Rademacher and gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3(Nov):463–482, 2002.

- Bartlett et al. [2006] P. L. Bartlett, M. I. Jordan, and J. D. McAuliffe. Convexity, classification, and risk bounds. Journal of the American Statistical Association, 101(473):138–156, 2006.

- Bera and Park [2008] A. K. Bera and S. Y. Park. Optimal portfolio diversification using the maximum entropy principle. Econometric Reviews, 27(4-6):484–512, 2008.

- Bertsimas and Kallus [2020] D. Bertsimas and N. Kallus. From predictive to prescriptive analytics. Management Science, 66(3):1025–1044, 2020.

- Donti et al. [2017] P. Donti, B. Amos, and J. Z. Kolter. Task-based end-to-end model learning in stochastic optimization. In Advances in Neural Information Processing Systems, volume 30, 2017.

- El Balghiti et al. [2019] O. El Balghiti, A. N. Elmachtoub, P. Grigas, and A. Tewari. Generalization bounds in the predict-then-optimize framework. In Advances in Neural Information Processing Systems, volume 32, 2019.

- Elmachtoub and Grigas [2021] A. N. Elmachtoub and P. Grigas. Smart “predict, then optimize”. Management Science, 2021.

- Estes and Richard [2019] A. Estes and J.-P. Richard. Objective-aligned regression for two-stage linear programs. Available at SSRN 3469897, 2019.

- Ho and Hanasusanto [2019] C. P. Ho and G. A. Hanasusanto. On data-driven prescriptive analytics with side information: A regularized nadaraya-watson approach. URL: http://www. optimization-online. org/DB FILE/2019/01/7043. pdf, 2019.

- Ho-Nguyen and Kılınç-Karzan [2020] N. Ho-Nguyen and F. Kılınç-Karzan. Risk guarantees for end-to-end prediction and optimization processes. arXiv preprint arXiv:2012.15046, 2020.

- Hu et al. [2020] Y. Hu, N. Kallus, and X. Mao. Fast rates for contextual linear optimization. arXiv preprint arXiv:2011.03030, 2020.

- Journée et al. [2010] M. Journée, Y. Nesterov, P. Richtárik, and R. Sepulchre. Generalized power method for sparse principal component analysis. Journal of Machine Learning Research, 11(Feb):517–553, 2010.

- Kao et al. [2009] Y.-h. Kao, B. Roy, and X. Yan. Directed regression. Advances in Neural Information Processing Systems, 22:889–897, 2009.

- Kingma and Ba [2015] D. P. Kingma and J. L. Ba. Adam: A method for stochastic gradient descent. In ICLR: International Conference on Learning Representations, pages 1–15, 2015.

- Kotary et al. [2021] J. Kotary, F. Fioretto, P. Van Hentenryck, and B. Wilder. End-to-end constrained optimization learning: A survey. arXiv preprint arXiv:2103.16378, 2021.

- Markowitz [1952] H. Markowitz. Portfolio selection. The Journal of Finance, 7(1):77–91, 1952. ISSN 00221082, 15406261. URL http://www.jstor.org/stable/2975974.

- Massart et al. [2006] P. Massart, É. Nédélec, et al. Risk bounds for statistical learning. The Annals of Statistics, 34(5):2326–2366, 2006.

- Maurer [2016] A. Maurer. A vector-contraction inequality for rademacher complexities. In International Conference on Algorithmic Learning Theory, pages 3–17. Springer, 2016.

- Notz and Pibernik [2019] P. M. Notz and R. Pibernik. Prescriptive analytics for flexible capacity management. Available at SSRN 3387866, 2019.

- Osokin et al. [2017] A. Osokin, F. Bach, and S. Lacoste-Julien. On structured prediction theory with calibrated convex surrogate losses. arXiv preprint arXiv:1703.02403, 2017.

- Steinwart [2007] I. Steinwart. How to compare different loss functions and their risks. Constructive Approximation, 26(2):225–287, 2007.

- Tewari and Bartlett [2007] A. Tewari and P. L. Bartlett. On the consistency of multiclass classification methods. Journal of Machine Learning Research, 8(5), 2007.

- Zhang [2004] T. Zhang. Statistical analysis of some multi-category large margin classification methods. Journal of Machine Learning Research, 5(Oct):1225–1251, 2004.

- Zhang et al. [2004] T. Zhang et al. Statistical behavior and consistency of classification methods based on convex risk minimization. The Annals of Statistics, 32(1):56–85, 2004.

Appendix A Rademacher complexity and generalization bounds

Herein we briefly review Rademacher complexity, a widely used concept in deriving generalization bounds, and how it applies in our analysis. For any loss function and a hypothesis class of cost vector predictor functions, the Rademacher complexity is defined as

where are independent Rademacher random variables and are independent samples from the joint distribution for . The following theorem provides a classical generalization bounds based on the Rademacher complexity.

Theorem 4 (Bartlett and Mendelson [2002]).

Let be a hypothesis class from to and let . Then, for any , with probability at least , for all it holds that

Moreover, we define the multivariate Rademacher complexity [Maurer, 2016, Bertsimas and Kallus, 2020, El Balghiti et al., 2019] of as

where are Rademacher random vectors for . In many cases of hypothesis classes, such as linear functions with bounded Frobenius or element-wise norm, the multivariate Rademacher complexity can be bounded as where is a constant that usually depends on the properties of the data, the hypothesis class, and mildly on the dimensions and . Detailed examples of such bounds have been provided by El Balghiti et al. [2019], Bertsimas and Kallus [2020].

When the loss function is additionally -Lipschitz continuous with respect to the -norm in the first argument, namely for all , then by the vector contraction inequality of Maurer [2016] we have . It is also easy to see that the the SPO+ loss function is -Lipschitz continuous with respect to the -norm for any and therefore we can leverage the vector contraction inequality of Maurer [2016] in this case. Combined with Theorem 4, this yields a generalization bound for the SPO+ loss which, when combined with Theorems 2 and 3 yields Corollaries 3.1 and 4.1, respectively. The full proofs of these corollaries are included below.

Proof of Corollary 3.1 and 4.1.

Let . For any , with probability at least , for all , it holds that

Since and , we know that there exists some universal constant such that

for all and . Since minimizes the empirical SPO+ risk , we have . and therefore, with probability at least , it holds that

Recall Theorem 2, the biconjugate of is for and for . Then if the assumption in Corollary 3.1 holds, with probability at least , it holds that

for some universal constant . Also, since the calibration function in Theorem 6 is linear and thus convex, then if the assumption in Corollary 3.1 holds, with probability at least , it holds that

for some universal constant . ∎

Appendix B Proofs and other technical details for Section 3

B.1 Additional definitions and notation

Recall that is polyhedral and let denote the extreme points of . We assume, for simplicity, that for all , but our results can be extended to allow for other possibilities in the case when there are multiple optimal solutions of . For any , we use to represent the unit vector whose -th entry is and others are all zero. Given a vector and a scalar , let denote the vector . For fixed and when ranges from negative infinity to positive infinity, the corresponding optimal solution will sequentially take different values in , and we let denote this sequence. Let denote the last element of vector for . Also, for , we define phase transition location such that , and additionally, we define and . When there is no confusion, we will omit and only use for simplicity.

Based on the above definition, for all , it holds that . Also, it holds that .

B.2 Detailed derivation for Example 3.1

Let the feasible region be the ball and consider the distribution class . Let be fixed, be a fixed scalar, and . Let the conditional distribution be a mixture of normals defined by for some . The condition mean of is then and the distribution is centrally symmetric around ; therefore . Let and , which yields that the excess conditional SPO risk is . Also, for all , we may assume that and hence . Therefore, using , it holds that

when , and hence we have .

B.3 Proofs and useful lemmas

Lemma 3 provides the relationship between excess SPO risk and the optimal solution of (2) with respect to the difference between the predicted cost vector and the realized cost vector .

Lemma 3.

Let be given and define . Let and , and let and denote the last elements of and , respectively. If , then it holds that . Additionally, if for some , then it holds that .

Proof of Lemma 3.

First we have , and therefore it holds that . Also, since and , we have . Moreover, when for , we have and , and therefore, it holds that . ∎

Lemma 4.

Suppose that with and for some . Then for all , it holds that

Proof.

Let and . For all , we have

for . Therefore, for all it holds that

Also, we have , and . Then, for all , it holds that . ∎

Lemma 5.

Let be given with , and let , , and be the corresponding optimal solution sequence and phase transition location sequence as described in Section B.1. Let and . Then it holds that

where .

Proof.

Let be the first element of . Suppose for some , then it holds that for and for . Therefore, we know that

Also, we have and . Therefore, by the result in Lemma 4, we have

∎

Lemma 6 provide a lower bound of the conditional SPO+ risk condition on the first element of the realized cost vector.

Lemma 6.

Let be a fixed vector and , be fixed scalars. Let a random variable satisfying for all . Let , and sequence , defined as in Section B.1. Let denote the last element of vector for . Let for . Suppose for some , then for all , it holds that

Proof of Lemma 6.

Let as defined in Section B.1, and suppose and for some . By the definition of , we know that and . Therefore, it holds that

where denotes the last element of for all . When follows the normal distribution , it holds that

for all . Therefore, it holds that

∎

Lemma 7 provide a lower bound of the conditional SPO+ risk when the distribution of is well behaved.

Lemma 7.

Let be a fixed vector and , be fixed scalars. Let be a random vector satisfying for all , and let be a random variable satisfying for all . Define . Suppose for some , then for all , it holds that

Proof of Lemma 7.

Now we present a general version of Theorem 2. For given parameters and , define . By introducing the constant , we no longer require the conditional distribution be lower bounded by a normal distribution on the entire vector space . Instead, we only need has a lower bound on a bounded -ball.

Theorem 5 (A general version of Theorem 2).

Suppose the feasible region is a polyhedron and define . Then the calibration function of the SPO+ loss satisfies

| (6) |

Additionally, when , we have and therefore

Proof of Theorem 5.

Without loss of generality, we assume . Otherwise, the constant will be zero and (6) will be a trivial bound. Let and be an orthogonal matrix such that for . We implement a change of basis and let the new basis be . With a slight abuse of notation, we keep the notation the same after the change of basis, for example, now the vector equals to . Since the excess SPO risk of is at least , we have . Let . Then it holds that . By Lemma 7, we know that

where is the first elements of , is the last element of , and . Then we can conclude that

Furthermore, since , we have

∎

B.4 Tightness of the lower bound in Theorem 5.

Herein we provide an example to show the tightness of the lower bound in Theorem 5.

Example B.1.

For any given , we consider the conditional distribution for some constants to be determined. For some , let the feasible region be . Although is not polyhedral, it can be considered as a limiting case of a polyhedron and the argument easily extends, with minor complications, to the case where the sphere is replaced by an -gon for sufficiently large. Let , we have . Also, for the excess conditional SPO+ risk we have

when . Therefore, let , we have and

for some large enough, and therefore the lower bound in Theorem 5 is tight up to a constant.

Appendix C Proofs and other technical details for Section 4

C.1 Extension of Theorem 6 and Lemma 8 and 9.

Let us first present a more general version of Assumption C.1 that allows the domain of the strongly convex function to be a subset of . In particular, we define the domain set by , where and for , and are convex functions for . Clearly, when , the set is the entire vector space . Also, let the closure of be , and with a slight abuse of notation, let the (relative) boundary of be . For any function defined on , we consider the (relative) lower limit be , where the distance function is defined as .

Assumption C.1 (Generalization of Assumption 4.1).

For a given norm , let be a -strongly convex function on for some . Assume that the feasible region is defined by for some constant satisfying . Additionally, assume that is -smooth on for some .

Let denote the linear subspace defined by the linear combination of all , namely , and let denote its orthogonal complement, namely . Also, for any , let denote its projection onto . Theorem 6 provides an lower bound of the calibration function of two different distribution classes, which include the multi-variate Gaussian, Laplace, and Cauchy distribution. Theorem 3 is a special instance of Theorem 6 when (and thus ).

Theorem 6 (Generalization of Theorem 3).

Suppose that Assumption C.1 holds with respect to the norm for some positive definite matrix . Then, for any , it holds that and .

Our analysis for the calibration function relies on the following two lemmas, which utilize the property of the feasible region to strengthen the “first-order optimality” and provide a “Lipschitz-like” continuity of the optimization oracle. We want to mention that some of the results in the following two lemmas generalize the results in El Balghiti et al. [2019] to the cases where the feasible region is defined on a subspace of rather than an open set in . The following lemma provides both upper and lower bound of SPO-like loss.

Lemma 8 (Generalization of Lemma 1).

Suppose Assumption C.1 holds with respect to a generic norm . Then, for any , it holds that

| (7) |

and

| (8) |

The two constants are the same since Theorem 12 in Journée et al. [2010] showed that set is a -strongly convex set. The following lemma provides a lower bound in the difference between two optimal decision based on the difference between the two normalized cost vector.

C.2 Proofs and useful lemmas

From now on, for any vector , we will use to represent the projection for simplicity. Likewise, when we shorten this notation even further to .

First we provide some useful properties in the following lemma.

Lemma 10.

If is -strongly convex on , the for all , it holds that

Proof.

First, for all and , it holds that

Since is -strongly convex, it holds that for all . Therefore, it holds that

∎

Lemma 11.

If is -smooth on , then for all , it holds that

Proof.

If , then the statement holds. Otherwise, there exists such that and . Let , we have and . Let

Since is continuous and for all , we have and since is continuous, we have . Since is -smooth on , it holds that

Therefore, we have . Moreover, since , then it holds that . Now we know that , and

Therefore, it holds that . ∎

Proof of Lemma 8.

Let and . Since is -strongly convex on , it holds that

Since the Slater condition holds, the KKT necessary condition indicates that there exists scalar such that and . When , we additionally have . Therefore, it holds that

where the last inequality holds since . Therefore, it holds that

| (9) |

Since is -smooth on , it holds that , and hence we have

By applying the above inequality to (9), we can conclude that

On the other hand, it holds that

where the last inequality holds since . Therefore, it holds that

| (10) |

Since is -strongly convex on , it holds that , and hence we have

By applying the above inequality to (10), we can conclude that

∎

Proof of Lemma 9.

Without loss of generality we assume . Let and . By KKT condition there exists such that and for . Also, since is -strongly convex, it holds that

for . Then, it holds that

Moreover, since is -smooth, it holds that

∎

In the rest part of this section, without loss of generality we assume . Also, since and for all , we will ignore the notation and assume all . In Theorem 7 we provide a lower bound of an SPO-like loss.

Theorem 7.

When and , it holds that

When the norm we consider is -norm defined by for some positive definite matrix , additionally we have

Moreover, if , it holds that

Proof of Theorem 7.

The following lemma provides a necessary condition on such that the excess SPO loss of is at least .

Lemma 12.

Suppose the excess SPO loss of is at least , that is, . Then it holds that

When the norm we consider is -norm defined by for some positive definite matrix , additionally we have

Proof of Lemma 12.

From Theorem 7 and Lemma 12, we know that have a lower bound , where and

Moreover, the excess SPO risk of is at least implies that where and

Let . We know that the calibration function has a lower bound which defined as

| (11) | ||||

| s.t. |

Here we first provide two properties of random variable when .

Proposition 1.

Suppose . If for some , it holds that

Proposition 2.

Suppose . When , for any constant , it holds that

Proof of Proposition 2.

For simplicity we just assume from now on and ignore the conditional probability. Let . Since , we have

By the fact that , it holds that and hence

Therefore, we further get

where . For any such that , we have

Also, when , we have . Then we can conclude that

∎

By first-order necessary condition we know that is an optimal solution to (11) only if

| (12) |

for some . Also, for any fixed , it holds that

and

The following lemma simplifies .

Lemma 13.

Suppose . Then there exists a unique function such that for all , it holds that

Also, is a non-decreasing function.

Proof.

Let denote . First we show that has the same direction as . Let denote the affine transform . We have and for all . It leads to and hence

Now we let

and we want to show that if . Since , there exists a matrix such that and . Let be a random variable depending on where . It holds that , which implies that and therefore . Also, we have , which implies that and therefore

Moreover, since , it holds that

Therefore,

Therefore, we know that is a well-defined function based on the above property of . Now we are going to prove that is a non-decreasing function. Pick arbitrary , we have and , where for . Therefore,

It is sufficient to show that

| (13) |

for all when . We divide the proof into three cases. When , (13) is equivalent to

When , we know that left hand side of (13) is non-negative and right hand side is non-positive. When , (13) is equivalent to

∎

Following the results in Lemma 13 we have

Hence, (12) is equivalent to

Since and are linearly independent, (12) is further equivalent to

which is also equivalent to

| (14) |

Lemma 14.

Proof.

Based on the above property, we provide a lower bound of calibration function.

Theorem 8.

Proof.

First we know that . Also, Lemma 14 shows that for optimal , it holds that . By the definition of , we have

Since , Proposition 1 shows that . Therefore, it holds that

where the last inequality holds since . Based on the result in Proposition 2, we have

Also, let . In the constraint we have

and hence . Since , it holds that . This implies that . Therefore, we conclude that

∎

We are now ready to complete the proof of Theorem 6.

Appendix D Experimental details

For both problems, we ran each instance on one core of Intel Xeon Skylake 6230 @ 2.1 GHz.

D.1 Excess risk comparison

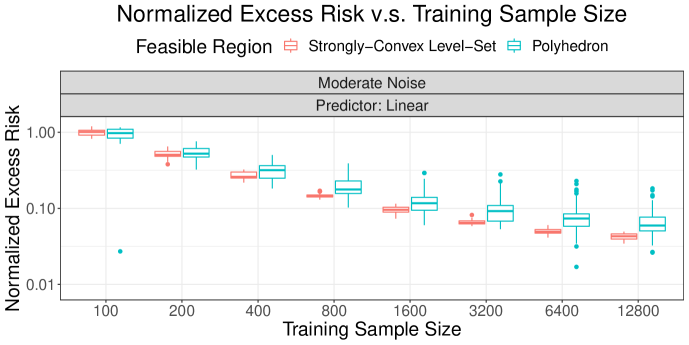

In Figure 3, we provide the empirical excess risk comparison of the cases with polyhedral and level-set feasible regions. The case with polyhedral feasible region are the cost-sensitive multi-class classification instances with simplex feasible region, and the case with level-set feasible region are the entropy constrained portfolio optimization problems. The main metric we use in Figure 3 is the normalized excess risk, which for each case, is defined as the excess risk over the averaged excess risk with sample size . For each type of feasible region, the excess risk is calculated by the difference between the SPO risk of the predictions given by the trained model and the true model. Also, we set polynomial degree equals to one with moderate noises, which means the true model is in the hypothesis class. The main purpose of this plot is not checking if the order of the calibration matches the theoretical results, as these are only worst case guarantees, but qualitatively comparing the convergence of excess risk with different types of feasible regions.

D.2 Additional plots on the cost-sensitive multi-class classification instances

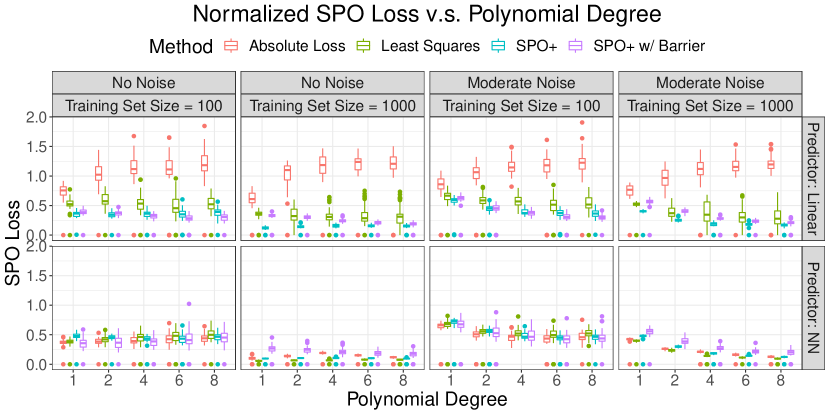

In Figure 4, we provide a complete comparison of all the method on the cost-sensitive multi-class classification instances. We can observe a similar pattern as in Figure 1.

D.3 Technical details

In Lemma 15 we show that the optimization oracle is differentiable when the projection of the predicted cost vector is not zero for the entropy constrained portfolio optimization example.

Lemma 15.

Let denote the interior of the probability simplex. For any vector , let denote the projection of onto . Let denote the entropy function. For some scalar , let . Let . Then it holds that is differentiable when where is the projection of onto the subspace .

Proof.

Let denote the softmax function, namely

Using KKT condition, we know that for any such that , there exists some scalar such that , and therefore . Since the softmax function is differentiable and is differentiable with respect to , we only need to show that the function is also differentiable with respect to . Indeed, when , we have , which is equivalent to . Let . Since is a decreasing function for , by inverse function theorem we have , and hence is also differentiable with respect to . ∎

In the cost-sensitive multi-class classification problem, we consider the SPO+ method using a log barrier approximation to the unit simplex. For the choice of the threshold , according to Assumption C.1 we will need and . In this log barrier scenario, we have and . Therefore, we pick the threshold . Of course, one may consider a more careful tuning of this hyper-parameter. Nevertheless, even with our simplistic approach for setting it we observe benefits of the SPO+ loss that uses a log barrier approximation to the unit simplex.

D.4 Data generation processes

In the next two paragraphs we discuss the detailed data generation process of each problem.

Portfolio allocation problems.

Let us describe the process used for generating the synthetic data sets for portfolio allocation instances. In this experiment, we set the number of assets and the dimension of feature vector . We first generate a weight matrix , whereby each entry of is a Bernoulli random variable with the probability . We then generate the training data set and the test data set independently according to the following procedure.

-

1.

First we generate the feature vector from the standard multivariate normal distribution, namely .

-

2.

Then we generate the true cost vector according to for , where is the -th row of matrix . Here deg is the fixed degree parameter and , the multiplicative noise term, is a random variable which independently generated from the uniform distribution for a fixed noise half width . In particular, is set to for “no noise” instances and for “moderate noise” instances.

Cost-sensitive multi-class classification problems.

Let us describe the process used for generating the synthetic data sets for cost-sensitive multi-class classification instances. In this experiment, we set the number of class and the dimension of feature vector . We first generate a weight vector , whereby each entry of is a Bernoulli random variable with the probability . We then generate the training data set and the test data set independently according to the following procedure.

-

1.

First we generate the feature vector from the standard multivariate normal distribution, namely .

-

2.

Then we generate the score according to , where is the logistic function. Here , the multiplicative noise term, is a random variable which independently generated from the uniform distribution for a fixed noise half width . In particular, is set to for “no noise” instances and for “moderate noise” instances.

-

3.

Finally we generate the true class label and the true cost vector is given by for .