Probabilistic methods for approximate archetypal analysis

Abstract

Archetypal analysis is an unsupervised learning method for exploratory data analysis. One major challenge that limits the applicability of archetypal analysis in practice is the inherent computational complexity of the existing algorithms. In this paper, we provide a novel approximation approach to partially address this issue. Utilizing probabilistic ideas from high-dimensional geometry, we introduce two preprocessing techniques to reduce the dimension and representation cardinality of the data, respectively. We prove that provided the data is approximately embedded in a low-dimensional linear subspace and the convex hull of the corresponding representations is well approximated by a polytope with a few vertices, our method can effectively reduce the scaling of archetypal analysis. Moreover, the solution of the reduced problem is near-optimal in terms of prediction errors. Our approach can be combined with other acceleration techniques to further mitigate the intrinsic complexity of archetypal analysis. We demonstrate the usefulness of our results by applying our method to summarize several moderately large-scale datasets.

lternating minimization, Approximate convex hulls, Archetypal analysis, Dimensionality reduction, Random projections, Randomized SVD

1 Introduction

Archetypal analysis (AA) is an unsupervised learning method introduced by Cutler and Breiman in 1994 [10]. For fixed , the method finds a convex polytope with vertices, referred to as archetypes, in the convex hull of the data that explains the most variation of the data. Equivalently, given , AA can be formulated as the following optimization problem:

| (1.1) |

where denotes the Frobenius norm, and ‘cs’ stands for column stochastic matrices, which are entry-wise nonnegative matrices with each column summing to 1. The normalizing factor is introduced for convenience later. To understand this formulation, note that the columns of are the expected archetypes, and the columns of correspond to the projection coefficients of the columns of to the convex hull of the archetypes. Consequently, the objective defined in (1.1) represents the (average) variation of the data that cannot be explained by the convex combinations of the archetypes.

AA is closely related to other unsupervised learning methods such as the -means, principal component analysis (PCA) and nonnegative matrix factorization (NMF) [19, 22]. In fact, AA can be seen as an interpolation between the -means and PCA; it has more geometry than the former while it is more restrictive than the latter due to additional convexity constraints. This allows AA to produce more interpretable results in many applications, e.g., in evolutionary biology [38], meanwhile raising additional questions of increased computational complexity. Under suitable assumptions, the consistency and convergence of AA have recently been established in [33], laying the foundation for AA to be applicable to large-scale inference.

Despite offering interpretable results, AA did not gain equal attention compared to its alternatives. One possible reason, as pointed out in [6], is due to the lack of efficient computational resources for applying AA to large-scale datasets, which are becoming increasingly ubiquitous in the big-data era. Indeed, the optimization defined in (1.1) is non-convex, and one common approach to solving (1.1) is based on an alternating minimization algorithm [10], which will be reviewed in Section 2. The subproblems in the alternating minimization scheme are equivalent to quadratic programming problems (see Section 2), which makes the full loop for solving AA computationally intensive for moderately large dimension and cardinality .

The scope of this paper is to provide a promising perspective for addressing the theoretical computational challenges encountered by the AA. Instead of focusing on optimizing the subproblem solvers to accelerate computation, we introduce two separate dimensionality reduction techniques to downsize the problem before applying optimization methods to solve (1.1). We show that under appropriate conditions, a solution of the reduced AA (i) well-approximates the solution of the original problem (1.1) in terms of projection error and (ii) can be obtained significantly faster than the original solution. Our approach relies on a few fundamental results in high-dimensional geometry. Note that our proposed method is a data preprocessing procedure by nature, and complements the many existing methods to further accelerate computation.

1.1 Related work

Making archetypal analysis practical for large-scale data analysis has been an active area of research in recent years. Various approaches have been proposed to attack the problem from different perspectives. For example, feasible optimization techniques such as projected gradients [31], active-subsets [6], and the Frank-Wolfe method [4] are considered for accelerating solving the quadratic programming problem in the alternating minimization scheme. Relaxation methods including decoupling [30] and sparse projections [1] are concerned with relaxing the alternating minimization into problems that enjoy better scalability properties. Another direction of work is centered around approximately solving AA by first reducing the cardinality of the data via sparse representation [40, 27]. Although these approaches are demonstrated to work well empirically, they either do not address the intrinsic complexity of the problem or lack theoretical guarantee on the quality of approximation. In the recent work [28], the authors proposed to use the coreset of the data to reduce the computational complexity of the objective function and theoretically quantified the approximation error.

Using approximate isometric embedding to reduce dimensionality is a fruitful idea in data analysis. The technique has been successfully applied to a variety of problems including least-squares regression [12, 2], clustering [5, 8, 29], low-rank approximation [41, 7, 18], nonnegative matrix factorization [14, 34], and tensor decomposition [44, 3].

1.2 Contributions of this paper

This paper proposes two novel dimensionality reduction techniques which can be combined with existing approaches to mitigate the inherent complexity of archetypal analysis. Both techniques come with theoretical guarantees on their approximation accuracy. In particular,

-

•

We introduce a data compression technique based on a randomized Krylov subspace method [32] to reduce data dimension. This procedure allows us to circumvent frequent queries to high-dimensional data and is new in the context of archetypal analysis.

-

•

We propose to use random projections to compute an approximate convex hull of the data to reduce the cardinality of the dictionary to represent archetypes.

-

•

We theoretically analyze the approximation accuracy and time complexity for both techniques. In particular, we show that the reduced archetypal analysis gives a near-optimal solution but has significantly reduced complexity provided that the data is low-dimensional and approximately described by a few extreme patterns.

Our results yield an approximate algorithm that is capable of dealing with data that is large both in size and dimension. Numerical experiments are provided which support and illustrate our theoretical findings.

1.3 Outline

The rest of the paper is organized as follows. In Section 2, we review the standard alternating minimization algorithm for solving archetypal analysis as well as the corresponding computational challenges. In Section 3 and 4, we introduce two separate randomized techniques to reduce the data dimension and representation cardinality of the archetypes, respectively. We also quantify the approximation accuracy and the computational complexity for both techniques. In Section 5, we combine the ideas in Section 3 and 4 to devise an approximate algorithm for archetypal analysis. We show that the proposed algorithm gives a near-optimal solution meanwhile having significantly reduced computational complexity for datasets that are approximately embedded in a low-dimensional subspace and well summarized via a few extreme points. We numerically verify our results in Section 6.

1.4 Notation

In the rest of the paper, denotes the data matrix. We always use to denote a minimizer to (1.1), and the corresponding optimum value.

Denote . For a matrix , we denote by the -th largest singular value of , and the Moore-Penrose pseudoinverse of . For and , we use notation , , , and to denote the submatrices formed by taking the rows of with indices in , the rows of with indices in , the columns of with indices in , and the columns of with indices in , respectively. When talking about subspace embedding for , we view as points in the column space of , i.e., . We use and to represent the convex hull of the columns of and the corresponding extreme points, respectively.

Moreover, , and are standard notation in complexity theory, where the implicit constants do not depend on the indices .

2 An alternating minimization algorithm for archetypal analysis

In this section, we review an alternating minimization algorithm for solving AA, due to Cutler and Breiman [10].

Note that (1.1) is a non-convex optimization. However, when fixing or and solving for the other, the problem becomes convex. This observation gives rise to the following alternating minimization algorithm for computing a stationary solution for (1.1).

The loop in Algorithm 1 updates and alternatingly. To analyze the computational complexity of these subroutines, we formulate the optimization problems in steps and more explicitly as follows.

In step 3, is fixed and needs to be updated. If we let , then the optimization is equivalent to computing the projection coefficients for each column in to . In particular, we need to solve independent -dimensional quadratic programming problems:

In step 4, is fixed and , or equivalently, , needs to be updated. Using the Pythagorean theorem, one can first compute the least-squares solutions

then update each column of by projection:

| (2.1) |

Alternatively, one can use a Gauss-Seidel approach to update the columns of sequentially to accelerate computation [33]. Since the rest of the paper uses the Gauss-Seidel technique in the subroutine of solving reduced AA, we derive the optimization problems resulting from the procedure; more details can be found in [33, Appendix B].

The Gauss-Seidel method updates the identified archetypes (i.e. the columns of ) one at a time. In the -th step, the procedure optimizes over the -th column of with the rest kept fixed. It can be verified from direct computation that for ,

where and collects the terms that do not depend on . Since , minimizing is equivalent to solving

| (2.2) |

Either (2.1) or (2.2) involves solving quadratic programming problems with variable dimension .

For small and large , the computation time in step 3 scales linearly in (assuming solving a -dimensional quadratic programming problem takes constant time). For step 4, the computation time is approximately equal to a multiplicative constant () times the complexity of solving an -dimensional quadratic programming problem, which can be computationally infeasible for large . We will provide a theoretically justified accelerated scheme for step 4 in Section 4. Moreover, when is large, taking repeated numerical operations on is inconvenient. We will introduce a data dimensionality reduction technique to address this issue in Section 3.

3 Data dimensionality reduction

We first consider the scenario where the data dimension is large. This may happen, for instance, when each data point is obtained from the discretization of a continuous function (time series) or encodes a high-resolution image. In this case, directly working with the data is inconvenient. Instead, we can embed in a lower dimensional space while maintaining the convexity structure of . This compression will save us from frequently querying the columns of in the iterative process for solving (1.1), which can be computationally expensive. A straightforward idea for embedding is via singular value decomposition (SVD), which we recall below:

Definition 3.1.

Suppose . The singular value decomposition (SVD) of is given by , where are the left and right singular vector matrices, respectively, and is a diagonal matrix with diagonal entries arranged in non-increasing order.

Under the columns of , provides a sparse representation for (since ). If we first embed in using SVD and apply AA to , then for every feasible , by the unitary invariance of Frobenius norm,

| (3.1) |

which establishes the equivalence between (1.1) and the AA under the SVD representation.

In fact, if has full rank but possesses low-rank structure, one may use a truncated SVD to further reduce the data dimension at a minor cost of accuracy, as made precise in the following theorem:

Theorem 3.1.

Suppose . Denote by the first columns of and , respectively, and the top submatrix of . Let be a solution to the AA for the truncated SVD representation of at -th level:

Then,

| (3.2) |

Proof.

Let

| (3.3) |

By the Eckart–Young theorem [13], is the best rank- approximation for in the spectral norm, with approximation error . Let be a solution to (1.1). Consequently,

| (3.4) |

Since are column stochastic matrices, so are and . It follows from direct computation and Cauchy-Schwarz inequality that

| (3.5) |

Similarly,

| (3.6) |

Plugging (3.5) and (3.6) into (3.4) and dividing by yields

completing the proof. ∎

Thus, for data that admits a good low-rank approximation, AA applied to the truncated SVD representation yields a near-optimal solution in terms of prediction errors. In this case, the data dimension can be significantly reduced to streamline computation. However, to obtain truncated SVD representations, one often needs to compute the full SVD of , which has complexity . For large and , this procedure is computationally intensive and thus can be restrictive in practice. To address this issue, we consider an approximate version of the best rank- approximation without taking the SVD of .

Definition 3.2.

A matrix is a rank- approximation to if and

| (3.7) |

where is the best rank- approximation to as defined in (3.3).

Before turning to discuss how to find such an , we consider a few consequences assuming its existence. Similar to the previous discussion, we can apply AA to , which can be efficiently represented using the SVD. As will be seen shortly, computing the SVD of is much cheaper than when is small. On the other hand, let be the SVD of and define

| (3.8) |

The following theorem quantifies the approximation error if we use in place of for archetypal analysis:

Theorem 3.2.

Let . Suppose is a rank- approximation to , and is the representation of under the left singular vectors. Let be a solution to the AA applied to :

| (3.9) |

Then,

Proof.

Theorem 3.2 implies that for with small best rank- approximation error, using the SVD representation of will only result in a small impact on prediction accuracy. The following algorithm, due to Musco and Musco [32], provides a way to compute (i.e., ) via randomized block Krylov methods. The details of the algorithm are given in Algorithm 2:

For moderately large , with high probability, returned by Algorithm 2 is a good approximation to :

Lemma 3.1 ([32]).

Proof.

Lemma 3.1 is a probabilistic version of [32, Theorem 1] where a fixed probability (0.99) is used instead of for an arbitrary . Nevertheless, the proof is the similar except one needs to apply sharp concentration inequalities to bound extreme singular values of Gaussian matrices [43, Corollary 7.3.3], [36, Theorem 1.2] to control the failure probability. ∎

Remark 3.1.

Other randomized low-rank approximation algorithms may also be used in place of Algorithm 2. For example, one can use the randomized simultaneous iteration to compute [18, 45]. Under the same approximation error and failure probability , the sample complexity of this method has a slightly worse dependence on (i.e. ) than (3.10). As such theoretical discrepancy was also manifested in several empirical studies in [32], we use Algorithm 2 to compute in this article.

Remark 3.2.

The desired low-rank approximation is computed under the spectral norm, which is necessary in the derivation of approximation error in Theorem 3.2. Other randomized algorithms based on oblivious sketching [37, 45, 8] or leverage score sampling [9] only produce low-rank approximations under the Frobenius norm. Since an error bound under the Frobenius norm does not imply a similar bound under the spectral norm, these methods do not directly work for the problem considered in this paper.

To apply Theorem 3.2, we need to compute the SVD representation of the low-rank approximation matrix , that is, , rather than itself; see (3.8). Since the output of Algorithm 2 is the full low-rank matrix , finding its SVD representation may incur additional computational cost for our purpose. However, in Algorithm 2, can be read off the shelf as , where and are computed in step 4. Thus, the total cost for is the computational complexity for the first four steps in Algorithm 2.

Theorem 3.3.

Let be the SVD representation of in Algorithm 2. Then, the computational complexity for is .

Proof.

We only sketch the proof; more details can be found in [32]. Step 1 in Algorithm 2 generates a random Gaussian matrix which takes time . Step 2 computes the Krylov subspace basis which takes time . The QR decomposition of in step 3 takes time . In step 4, we first compute , which takes time , then compute the SVD of , which takes time . Computing takes time . ∎

Remark 3.3.

When , the computational complexity of becomes , which is significantly smaller than .

Theorem 3.4.

Remark 3.4.

Fixing small, say , . The computational complexity of is . Consequently, for data that can be well approximated via low-rank matrices with approximation rank , using Algorithm 2 can effectively reduce the dimension of AA.

4 Representation cardinality reduction

We now consider the situation where the dataset has a large cardinality, i.e., . In this case, to reduce computational complexity, we propose to use a parsimonious subset of points in to approximately represent , i.e., we wish to find a small subset such that

| (4.1) |

where and will be made rigorous later. We will refer to as an approximate convex hull of .

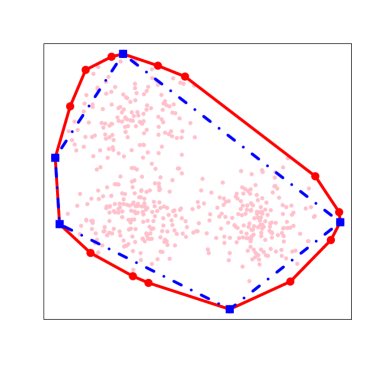

The idea of using subsets of (i.e. extreme points) to represent has been considered in [40, 27], where exact equality in (4.1) is expected. Here we only ask for approximate representation of (allowing for a small approximation error), so that it is possible to further reduce the cardinality of the representation set for the archetypes (Figure 1).

Similar to the discussion in the previous section, we first give a few consequences assuming exists.

Definition 4.1.

We say that is an -approximate convex hull of if

| (4.2) |

where is the Hausdorff distance.

Theorem 4.1.

For and , suppose is a -approximate convex hull of . Consider the following AA optimization problem constrained to :

| (4.3) |

Then, the archetype points given by the solution of provide a -approximation to the solution for (1.1) in terms of prediction errors:

Proof.

For an optimal solution of (1.1) that resides on the boundary of (such a solution always exists [10]), consider the projection of each column of to , and denote the projected points as . Note that is well-defined as . By the triangle inequality, the distance between each column of and is bounded by the sum of the distance between the column of and and . Since gives an -approximate convex hull of ,

| (4.4) |

It follows from direct computation that

where the last inequality follows from (4.4) and Cauchy-Schwarz inequality. Taking the square root on both sides completes the proof. ∎

Theorem 4.1 establishes an approximate equivalence between the solutions of (4.3) and (1.1) in terms of objective values. Compared to (1.1), the dimension of is significantly reduced provided , while the dimension of stays unchanged.

To see the computational gain from solving (4.3) instead of (1.1), recall the alternating minimization in Section 2. When is fixed and is updated, one needs to solve quadratic programming problems with variable dimensions equal to the number of rows of . For certain optimization methods such as the ellipsoid method, the complexity of quadratic programming problems with positive-definite quadratic matrix has weakly polynomial time (of the variable dimension) [24]. Thus, when , a notable acceleration is expected for the subroutine of updating , which justifies the significance of using a parsimonious subset of points to represent the archetypes.

On the other hand, when is fixed and is updated, one needs to compute the projection of each column of to . This step is the same in both (1.1) and (4.3) and consists of independent quadratic programming problems with variable dimension . In this case, it is possible to take an additional step of acceleration via parallelization combined with the coreset approximation [28], which reduces the computation of projection coefficient vectors to a small subset of points in with appropriate weights, similar to the ideas of quadrature. Indeed, given a coreset and appropriate weight diagonal matrix , one can approximate the objective function in (1.1) with . Note the complexity of the subproblem for updating in the alternating minimization algorithm is proportional to the number of points in the objective function. Therefore, when , the step of solving the -subproblem can be significantly accelerated. Combining the idea of coreset with (4.4) yields an approximate objective function , which has significantly reduced complexity when solved by the alternating minimization algorithm. The details are not discussed here.

We next discuss how to find a “small” subset such that (4.2) is satisfied. Note that to represent , it suffices to consider the extreme points of . In other words, we will find a subset whose convex hull can well approximate . As will be seen below, this procedure can be effectively implemented by taking random projections. Indeed, random projections are linear maps whose inverse image of the extreme points of a convex set are a subset of the extreme points of the inverse image of that convex set [25]. Similar ideas have been used in the empirical study of archetypal analysis to seek extreme points [40, 11].

Finding all the extreme points of may itself be computationally demanding unless is small. When can be well approximately using a few extreme points, it is desired to single them out to further shrink the complexity of the problem at a small sacrifice of accuracy. To this end, we need to know which extreme points are more important than the others in terms of composing . The following result, which originally appeared in [17], is precisely what is needed here.

Observe that under a random projection , the points in have projected values , which with probability one have a unique maximum. The inverse image of the maximum is an element in . Thus, throwing away a null set, we can partition the unit sphere as follows:

For , its curvature is defined as

which is the relative area of the directions that distinguish as the maximum to the unit sphere in . By definition, points with larger curvature are more likely to be sampled if is uniformly drawn from ; in fact, they are also more ‘important’ as specified by the following lemma [17, Theorem 3.4]:

Lemma 4.1.

Let . Suppose that both and are non-degenerate (i.e., with nonempty interior), and . Then,

| (4.5) |

As a result, to compute a sparse approximate convex hull, it suffices to use high-curvature points to approximately represent . To find high-curvature points, we apply a Monte-Carlo (MC) procedure to estimate the curvature of each point and then truncate at some thresholding parameter. The details are given in Algorithm 3:

A similar MC method based on a different truncation rule has been proposed [17, Algorithm 1], where points are removed whenever their estimated curvatures are below some fixed threshold. To ensure that the remaining points have large cumulative curvature, this algorithm requires the thresholding parameter to be overly small, leaving most points unremoved. To facilitate parsimony, Algorithm 3 first sorts points based on their estimated curvatures, then truncates based on the estimated cumulative curvatures.

The computational complexity of Algorithm 3 can be easily obtained from direct computation:

Theorem 4.2.

The computational complexity for Algorithm 3 is .

Proof.

We will show that for large , with high probability, the output of Algorithm 3 satisfies (4.2) with . Without loss of generality, in the following discussion we assume and

| (4.6) |

We have the following theorem:

Theorem 4.3.

Let be the subset returned by Algorithm 3, and . Suppose is non-degenerate for every with . Denote as the smallest integer such that :

| (4.7) |

and the truncation gap

If

| (4.8) |

then with probability at least , and

| (4.9) |

Remark 4.1.

Setting the upper bound in (4.9) equal to yields

which has an unpleasant but expected exponential dependence on (curse of dimensionality). For datasets with low-dimensional structure, i.e., well approximated via rank- matrices with , it is possible to use ideas in Section 3 to improve the exponential dimension dependence to (Algorithm 4).

Proof of Theorem 4.3.

Note that step 9 in Algorithm 3 ensures that is non-degenerate. Therefore, to show (4.9), by (4.5), it suffices to show , or equivalently, .

We first show that for satisfying (4.8), with high probability, the estimated curvatures are close to their expectations for all reasonably large . Note for every , is a sum of independent Bernoulli random variables with parameter , and the tail sum is a sum of independent Bernoulli random variables with parameter . Thus, by Hoeffding’s inequality [20],

Taking a union bound over and combining the two inequalities yields

| (4.10) |

The right-hand side in (4.10) can be further lower bounded by if satisfies (4.8).

We next show that for large , with high probability, the largest terms of , i.e., , coincide with . Particularly, denoting the index of as , we will show . Note that if and only if the following probabilistic event occurs:

Since for every and , is a sum of i.i.d. random variables , where with probability , with probability , and otherwise. Thus, we can bound the probability of from below with another application of Hoeffding’s inequality:

which is lower bounded by if satisfies (4.8). Taking a union bound, for satisfying (4.8), both the event in (4.10) and occur with probability at least .

5 An approximate AA algorithm

Putting results in Section 3 and 4 together, we have the following approximate algorithm for archetypal analysis (AAA):

Under appropriate assumptions on the input parameters, we have the following guarantee for the solutions computed by Algorithm 4:

Theorem 5.1.

Under the same assumptions in Theorem 4.3 and , if

| (5.1) | |||||

| (5.2) | |||||

where is the same constant as in Theorem 3.4, is the optimum value of (1.1), , are the same as defined in Theorem 4.3, then with probability at least , , and the approximate archetypes as well as the coefficient matrix returned by Algorithm 4 satisfy

Remark 5.1.

According to Theorem 3.3 and Theorem 4.2, the computational complexity of data dimensionality reduction (step 1 to step 5) and representation cardinality reduction (step 6) is and , respectively. With probability at least , step 6 solves the reduced problem which has data dimension and representation cardinality . Thus, the overall complexity for Algorithm 4 is small if both and are small and is away from . This corresponds to the scenario where is approximately low-rank and has most of the curvature concentrated on a small subset.

Proof of Theorem 5.1.

Let and be solutions to (1.1) and

| (5.3) |

respectively. Under the assumptions on and , Theorem 4.1 and Theorem 4.3 together imply that with probability at least , and

| (5.4) |

Let and , where is the left singular vector matrix of the low-rank approximation given by Algorithm 2. For satisfying (5.1), it follows from Lemma 3.1 that with probability at least ,

| (5.5) |

where is the best rank- approximation for . Thus, both (5.4) and (5.5) hold with probability . Conditioning on (5.4) and (5.5), the rest of the proof is similar to the computation in (3.4):

Dividing both sides by yields the desired result. ∎

6 Numerical experiments

In this section, we apply the proposed algorithm (Algorithm 4) to compute the archetypes for three real datasets, including a time series dataset and two image datasets. When implementing the alternating minimization algorithm for solving AA, we use the -means to find an initial guess for the archetypes; the subproblems are solved using the existing package ‘quadprog’ [42] in R [35]. The algorithm stops if the relative objective decrease falls below 1e-3. We will compare the computation time and accuracy of the following algorithms:

-

•

(SVD-AA): Alternating minimization applied to the reduced singular value representation of as in (3.1), where truncation keeps of the variance of the data. SVD is implemented using the built-in function ‘svd’ in R.

-

•

(AAA): Approximate archetypal analysis (Algorithm 4), with .

- •

To ensure comparability of the results, we do not include other accelerated algorithms such as the active-subset solver [6] and the coreset approximation [28], which have a different focus than our methods. All reported results in this section were obtained on a Macbook Air with an M1 processor and 8GB of RAM.

6.1 S&P 500 cumulative log-returns

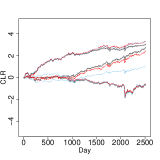

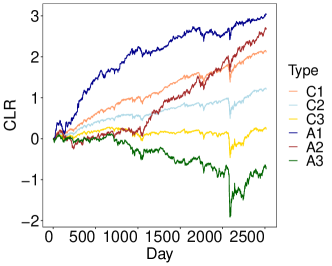

The Standard and Poor’s 500 (S&P 500) is a stock market index consisting of 500 large companies listed on stock exchanges in the United States. It is one of the most commonly used equity indices to evaluate the financial market as well as the economy. The companies that are selected for the S&P 500 index are changing with time. In this example, we consider a dataset comprised of companies that are currently in the S&P 500 index by January 2022, with close price recorded from December 2011 to December 2021. We compute for each column in a -dimensional time series representing the cumulative log-return (CLR) of a company over ten years. The CLR is calculated on a daily basis using the adjusted prices of stocks. Visualization of the dataset is given in the first plot in Figure 2. In the rest of the section, we assume that the CLR of each company in the S&P 500 index can be decomposed with respect to a few distinct growth patterns that can be identified via AA.

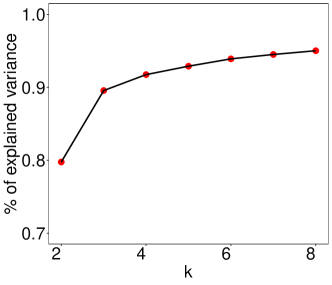

To apply AA, we need to first determine the number of archetypes . Like other unsupervised learning methods such as the -means and PCA, there is no principled rule to find the correct number of for real-life datasets. A more practical solution is to follow the heuristic “elbow rule” [39] to choose approximately. In this case, we apply SVD-AA to find such a . In particular, we plot the variance of the dataset explained by the archetypes given by SVD-AA as a function of (see Figure 2) and choose to be the point where the curve starts to plateau, which is around .

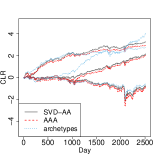

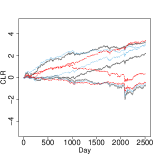

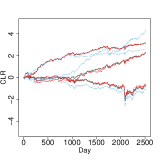

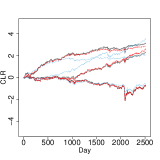

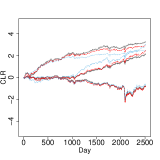

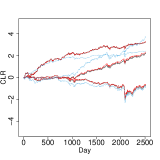

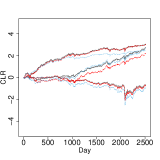

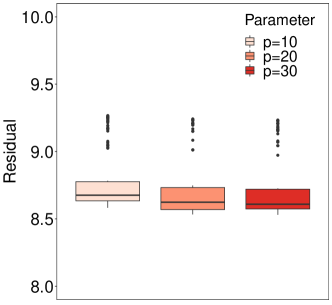

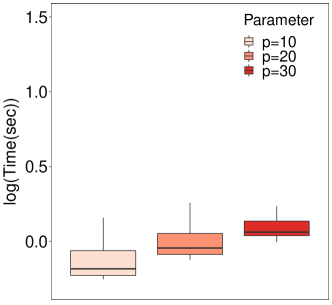

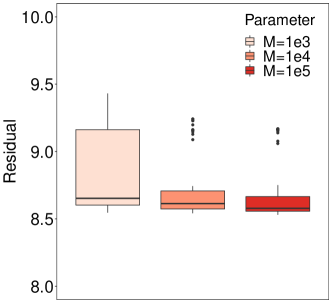

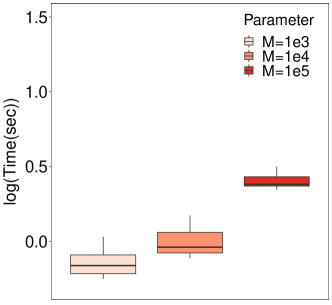

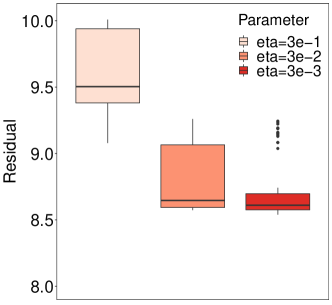

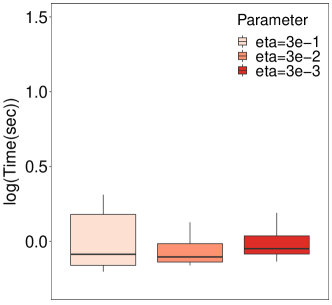

Setting , we apply SVD-AA, AAA, and archetypes to compute the archetypes for . The parameters , and in AAA are set as , and (so that ), respectively. Each experiment is repeated times, with the learned archetypes (in the first 10 experiments), the running times (elapsed time computed using the ‘system.time()’ function in R) and residuals reported in Figure 3 and Figure 4, respectively.

It can be seen from Figure 4 that SVD-AA, as expected, gives the best-computed archetypes in terms of the residual on average; however, its computation time is significantly longer than the other two methods. The built-in function archetypes has the worst performance, and its computation time is between the other two methods. The AAA, which first reduces the dimension of the dataset before applying the alternating minimization, achieves competitive results with SVD-AA (despite a few outliers) but takes much less time (more than times faster than SVD-AA). This may be because is essentially low-dimensional and admits a parsimonious approximation for its convex hull. A numerical justification for this argument can be seen from the spectral decay of the sample covariance matrix of as well as the scatterplot of the reduced representation of with respect to the first two principal components (PCs), as illustrated in Figure 5.

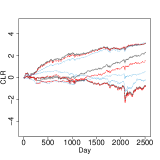

To implement AAA, it is necessary to choose the input parameters in advance. The optimal choice for the parameters is problem-dependent and often there is no universal tuning strategy for it. The Krylov subspace parameter is set as deterministically. We investigate the accuracy/running time dependence on , and . In particular, we will use the same parameters as in the previous simulation. Whenever we test the dependence on one parameter, the other two are set fixed. We will test and at three different values, respectively, i.e., , and . The results are given in Figure 6.

Figure 6 shows that for the S&P 500 dataset, the accuracy of AAA has a strong dependence on , which measures the missing proportion of curvature in the approximate convex hull construction. The number of random projections mostly influences the running time while having only a mild impact on the accuracy when . The approximation rank , as long as set reasonably large, is sufficient to give a good approximation result.

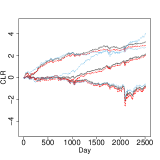

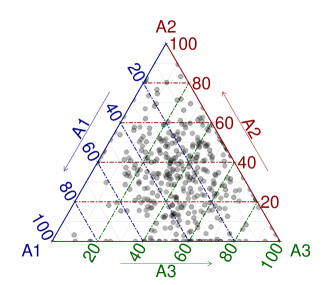

In this example, we compare the three archetypes with the same number of centers identified by the -means; see the first plot in Figure 7. It can be seen that the archetypal curves are visually more illustrative than the centers of the -means, which share a similar growth pattern with differing slopes. Indeed, the percentage of variance explained by AA is around ; the same number for the -means and PCA are and , respectively. Visualization of the convex coefficients for each data point with respect to the three archetypes is given in the ternary plot in Figure 7. In this case, most of the data fall in the interior of the simplex, suggesting the S&P dataset can be well summarized using a polytopic structure.

To further understand the meanings of the three archetypes, for each archetype, we single out the tickers of the top five companies having the largest component in the direction:

-

•

A1: NFLX: , STZ.B: , ILMN: , REGN: , FLT: ;

-

•

A2: AMD: , FTNT: , ISRG: , LRCX: , CPRT: ;

-

•

A3: MRO: , DVN: , OXY: , APA: , MOS: .

All the five companies in A3 are in the energy industry (oil, mining, etc.), representing the traditional aspect of the financial market. Companies in A1 and A2 leave more room for interpretation. In particular, for A1, NFLX is an entertainment company, STZ.B is a food company (beer and wine), ILMN is a biotechnology company, REGN is a pharmaceutical company, FLT is a financial service company; for A2, both AMD and LRCX are in the semiconductor industry, FTNT is a cybersecurity company, ISRG is a surgical equipment design company, and CPRT is a company that provides online vehicle auction and remarketing services. According to the quant ratings on https://seekingalpha.com/ between 2021 and 2022, all these companies have high profitability; each of these companies has consecutively ranked above A- and many have been A+ in the three latest reports (the factor grade ranges from A+ to F). This feature is also manifested in the upward trend in the archetypal curves associated with A1 and A2. Moreover, they are more resilient than the traditional industries when unexpected events occur (e.g. Covid-19 pandemic in early 2020), as can be seen from the “V” shape of these curves near Day in the first plot in Figure 7. The difference between A1 and A2 is more difficult to corroborate using recent financial data. From a macroscopic perspective, A1 represents the more established highly profitable industries in the market; they maintain a steady pace of CLR growth over time. A2 represents the emerging industries that, while not as profitable as A1, possess relatively more growth potential. This conclusion can be numerically inspected by comparing the slope of the A1 and A2 curves in Figure 7.

6.2 Intel Image

The Intel Image dataset [21] has been used for multi-class classification in machine learning, and consists of images representing different categories of the scene: Buildings, Forest, Glacier, Mountain, Sea, and Street. Each image is a pixel color image, which corresponds to a -dimensional vector through vectorization and stacking of the pixel matrices (). We randomly select samples in the training dataset () and apply AAA to extract representative patterns. Note we could have used the full dataset; however, this would require using a more efficient optimization solver for the subproblems to ensure the computation is done in a reasonable time. Since there are different categories of images, we set . The input parameters for AAA are chosen as , and . We compare the computed archetypes given by AAA with the clustering centers given by the -means in Figure 8.

In this experiment, the instance running time is s (s for data dimensionality reduction, s for representation cardinality reduction and s for solving the reduced problem using Algorithm 1) for AAA, and s for the -means. In this case, the cardinality of the extreme points used to build up the approximate convex hull is . The archetypes account for about of the variance of the dataset, as opposed to explained by the -means. The other two methods, SVD-AA, and archetypes cannot be implemented within a reasonable time.

For each archetype, we find the image that has the largest component with respect to it in the dataset. We also identify the images closest to the -means centers. The results are reported in Figure 8. According to the label information, the images on the top and bottom panels in Figure 8 (from left to right) correspond to “Forest”, “Buildings”, “Glacier”, “Glacier”, “Street”, “Sea” and “Mountain”, “Mountain”, “Mountain”, “Sea”, “Glacier”, “Forest”, respectively. Despite an approximate algorithm, AAA produces more diversified results than the -means in terms of image content. The only repetition occurs in the third and fourth pictures, where both the snow mountains are classified as Glacier.

6.3 MNIST dataset

The MNIST database [26] is a large database of handwritten digits that is commonly used for both classification and clustering tasks. Each data point in MNIST is a gray-scale image (i.e. a -dimensional vector) representing handwritten digits from to . The total size of the training dataset is 42000.

In this experiment, we use both the -means and AA to analyze the data structure in each label class separately. We first split the training data into 10 different datasets corresponding to labeled digits , respectively, each having a size of around 4000. We apply both the -means and AAA to the split datasets to identify the typical patterns and the archetypes, respectively. After running the “elbow inspection” for the -means at different labels, we found to be a reasonable choice on average. To be consistent, we also use for AAA. Moreover, the other parameters in AAA are set as , and . As before, in each label class, we find the images in the corresponding datasets that are closest to the -means centers as well as have the largest convex combination coefficients with respect to the archetypes. The results are reported in Figure 9.

In general, the -means centers are the images that are representative of each label class. They are more standard and usually can be distinguished using raws eyes. On the flip side, the approximate archetypes found by AAA are more extreme in terms of size, shape, position, etc.

Acknowledgements

We would like to thank the anonymous referees for their very helpful comments which significantly improved the presentation of the paper. We would like to thank Yu Zhu for providing us with the S&P 500 dataset and helping clarify some related questions related to interpretation. We also thank Akil Narayan for reading through an early version of the draft, and for providing several comments that improved the presentation of the manuscript. Y. Xu would like to thank the organizers of the MSRI Summer Graduate School on Mathematics of Big Data: Sketching and (Multi-) Linear Algebra for motivating discussions.

Funding

R. Han is supported by the Direct Grant for Research from The Chinese University of Hong Kong, Hong Kong under Grant No. 4053474. B. Osting is supported by the National Science Foundation under Grant No. DMS-1752202. D. Wang is supported by the National Natural Science Foundation of China grant 12101524 and the University Development Fund from The Chinese University of Hong Kong, Shenzhen under Grant No. UDF01001803. Y. Xu is supported by the National Science Foundation under Grant No. DMS-1848508.

References

- [1] Vinayak Abrol and Pulkit Sharma “A geometric approach to archetypal analysis via sparse projections” In International Conference on Machine Learning, 2020, pp. 42–51 PMLR

- [2] Haim Avron, Petar Maymounkov and Sivan Toledo “Blendenpik: Supercharging LAPACK’s least-squares solver” In SIAM J. Sci. Comput. 32.3 SIAM, 2010, pp. 1217–1236

- [3] Casey Battaglino, Grey Ballard and Tamara G Kolda “A practical randomized CP tensor decomposition” In SIAM J. Matrix Anal. Appl. 39.2 SIAM, 2018, pp. 876–901

- [4] Christian Bauckhage, Kristian Kersting, Florian Hoppe and Christian Thurau “Archetypal analysis as an autoencoder” In Workshop New Challenges in Neural Computation, 2015, pp. 8 Citeseer

- [5] Christos Boutsidis, Anastasios Zouzias and Petros Drineas “Random Projections for -means Clustering” In Advances in Neural Information Processing Systems 23, 2010, pp. 298–306

- [6] Yuansi Chen, Julien Mairal and Zaid Harchaoui “Fast and robust archetypal analysis for representation learning” In Proceedings of the IEEE Conference on Computer Vision and Pattern Recognition, 2014, pp. 1478–1485

- [7] Kenneth L Clarkson and David P Woodruff “Low-rank approximation and regression in input sparsity time” In J. ACM 63.6 ACM New York, NY, USA, 2017, pp. 1–45

- [8] Michael B Cohen, Sam Elder, Cameron Musco, Christopher Musco and Madalina Persu “Dimensionality reduction for k-means clustering and low rank approximation” In Proceedings of the forty-seventh annual ACM symposium on Theory of computing, 2015, pp. 163–172

- [9] Michael B Cohen, Cameron Musco and Christopher Musco “Input sparsity time low-rank approximation via ridge leverage score sampling” In Proceedings of the Twenty-Eighth Annual ACM-SIAM Symposium on Discrete Algorithms, 2017, pp. 1758–1777 SIAM

- [10] Adele Cutler and Leo Breiman “Archetypal analysis” In Technometrics 36.4 Taylor & Francis, 1994, pp. 338–347

- [11] Anil Damle and Yuekai Sun “A geometric approach to archetypal analysis and nonnegative matrix factorization” In Technometrics 59.3 Taylor & Francis, 2017, pp. 361–370

- [12] Petros Drineas, Michael W Mahoney, Shan Muthukrishnan and Tamás Sarlós “Faster least squares approximation” In Numer. Math. 117.2 Springer, 2011, pp. 219–249

- [13] Carl Eckart and Gale Young “The approximation of one matrix by another of lower rank” In Psychometrika 1.3 Springer, 1936, pp. 211–218

- [14] N Benjamin Erichson, Ariana Mendible, Sophie Wihlborn and J Nathan Kutz “Randomized nonnegative matrix factorization” In Pattern Recognition Letters 104 Elsevier, 2018, pp. 1–7

- [15] Manuel J. A. Eugster and Friedrich Leisch “From Spider-Man to Hero – Archetypal Analsis in R” In Journal of Statistical Software 30.8, 2009, pp. 1–23 URL: http://www.jstatsoft.org/v30/i08/

- [16] Manuel J. A. Eugster and Friedrich Leisch “Weighted and Robust Archetypal Analysis” In Comput. Statist. Data Anal. 55.3, 2011, pp. 1215–1225 URL: http://www.sciencedirect.com/science/article/pii/S0167947310004056

- [17] Robert Graham and Adam M Oberman “Approximate Convex Hulls: sketching the convex hull using curvature” In arXiv preprint arXiv:1703.01350, 2017

- [18] Nathan Halko, Per-Gunnar Martinsson and Joel A Tropp “Finding structure with randomness: Probabilistic algorithms for constructing approximate matrix decompositions” In SIAM Rev. 53.2 SIAM, 2011, pp. 217–288

- [19] Trevor Hastie, Robert Tibshirani and Jerome Friedman “The Elements of Statistical Learning”, Springer Series in Statistics New York, NY, USA: Springer New York Inc., 2001

- [20] Wassily Hoeffding “Probability Inequalities for Sums of Bounded Random Variables” In J. Amer. Statist. Assoc. 58.301, 1963, pp. 13–30

- [21] Intel “Intel image classification challenge” Public dataset available at https://www.kaggle.com/puneet6060/intel-image-classification

- [22] Hamid Javadi and Andrea Montanari “Nonnegative matrix factorization via archetypal analysis” In J. Amer. Statist. Assoc. 115.530 Taylor & Francis, 2020, pp. 896–907

- [23] Donald Ervin Knuth “The art of computer programming” Pearson Education, 1997

- [24] Mikhail K Kozlov, Sergei Pavlovich Tarasov and Leonid Genrikhovich Khachiyan “Polynomial solvability of convex quadratic programming” In Doklady Akademii Nauk 248.5, 1979, pp. 1049–1051 Russian Academy of Sciences

- [25] Peter D Lax “Functional Analysis. John Wiley&Sons” In Inc. Publication, 2002

- [26] Yann LeCun “The MNIST database of handwritten digits” In http://yann. lecun. com/exdb/mnist/, 1998

- [27] Sebastian Mair, Ahcene Boubekki and Ulf Brefeld “Frame-based data factorizations” In International Conference on Machine Learning, 2017, pp. 2305–2313 PMLR

- [28] Sebastian Mair and Ulf Brefeld “Coresets for Archetypal Analysis” In Advances in Neural Information Processing Systems 32, 2019, pp. 7247–7255

- [29] Konstantin Makarychev, Yury Makarychev and Ilya Razenshteyn “Performance of Johnson-Lindenstrauss transform for k-means and k-medians clustering” In Proceedings of the 51st Annual ACM SIGACT Symposium on Theory of Computing, 2019, pp. 1027–1038

- [30] Jieru Mei, Chunyu Wang and Wenjun Zeng “Online dictionary learning for approximate archetypal analysis” In Proceedings of the European Conference on Computer Vision (ECCV), 2018, pp. 486–501

- [31] Morten Mørup and Lars Kai Hansen “Archetypal analysis for machine learning and data mining” In Neurocomputing 80 Elsevier, 2012, pp. 54–63

- [32] Cameron Musco and Christopher Musco “Randomized block Krylov methods for stronger and faster approximate singular value decomposition” In Advances in Neural Information Processing Systems 2015, 2015, pp. 1396–1404

- [33] Braxton Osting, Dong Wang, Yiming Xu and Dominique Zosso “Consistency of archetypal analysis” In SIAM J. Math. Data Sci. 3.1 SIAM, 2021, pp. 1–30

- [34] Yuqiu Qian, Conghui Tan, Nikos Mamoulis and David W Cheung “Dsanls: Accelerating distributed nonnegative matrix factorization via sketching” In Proceedings of the Eleventh ACM International Conference on Web Search and Data Mining, 2018, pp. 450–458

- [35] R Core Team “R: A Language and Environment for Statistical Computing”, 2020 R Foundation for Statistical Computing URL: https://www.R-project.org/

- [36] Mark Rudelson and Roman Vershynin “The Littlewood–Offord problem and invertibility of random matrices” In Adv. Math. 218.2 Elsevier, 2008, pp. 600–633

- [37] Tamas Sarlos “Improved approximation algorithms for large matrices via random projections” In 2006 47th Annual IEEE Symposium on Foundations of Computer Science (FOCS’06), 2006, pp. 143–152 IEEE

- [38] Oren Shoval, Hila Sheftel, Guy Shinar, Yuval Hart, Omer Ramote, Avi Mayo, Erez Dekel, Kathryn Kavanagh and Uri Alon “Evolutionary trade-offs, Pareto optimality, and the geometry of phenotype space” In Science 336.6085 American Association for the Advancement of Science, 2012, pp. 1157–1160

- [39] Robert L Thorndike “Who belongs in the family” In Psychometrika, 1953

- [40] Christian Thurau, Kristian Kersting, Mirwaes Wahabzada and Christian Bauckhage “Convex non-negative matrix factorization for massive datasets” In Knowledge and information systems 29.2 Springer, 2011, pp. 457–478

- [41] Joel A Tropp, Alp Yurtsever, Madeleine Udell and Volkan Cevher “Practical sketching algorithms for low-rank matrix approximation” In SIAM J. Matrix Anal. Appl. 38.4 SIAM, 2017, pp. 1454–1485

- [42] Berwin A. Turlach and Andreas Weingessel “quadprog: Functions to solve Quadratic Programming Problems.” R package version 1.5-4, 2011 URL: http://CRAN.R-project.org/package=quadprog

- [43] Roman Vershynin “High-dimensional probability: An introduction with applications in data science” Cambridge university press, 2018

- [44] Yining Wang, Hsiao-Yu Tung, Alexander J Smola and Anima Anandkumar “Fast and guaranteed tensor decomposition via sketching” In Advances in neural information processing systems 28, 2015

- [45] David P Woodruff “Sketching as a Tool for Numerical Linear Algebra” In Foundations and Trends® in Theoretical Computer Science 10.1–2 Now Publishers Inc. Hanover, MA, USA, 2014, pp. 1–157