Kurtosis control in wavelet shrinkage with generalized secant hyperbolic prior

Abstract

The present paper proposes a bayesian approach for wavelet shrinkage with the use of a shrinkage prior based on the generalized secant hyperbolic distribution symmetric around zero in a nonparemetric regression problem. This shrinkage prior allows the control of the kurtosis of the coefficients, which impacts on the level of shrinkage on its extreme values. Statistical properties such as bias, variance, classical and bayesian risks of the rule are analyzed and performances of the proposed rule are obtained in simulations studies involving the Donoho-Johnstone test functions. Application of the proposed shrinker in denoising Brazilian stock market dataset is also provided.

1 Introduction

Wavelet shrinkers has been succesfully applied as estimators to wavelet coefficients in denoising data problems, such as nonparametric curve estimation, time series analysis, image processing, among others, see Donoho e Johnstone (1994, 1995), Donoho et al. (1995, 1996), Vidakovic (1998, 1999) for more details about wavelet shrinkage methods. In a bayesian setup, the assumption of a shrinkage prior distribution allows us to incorporate prior information about the wavelet coefficients of the wavelet transformed unknown function, such as sparsity, support (if they are bounded), local features, and others. Several priors have been proposed along the years, see Angelini et al. (2004), Remenyi et al. (2015), Karagiannis et al. (2015), Bhattacharya et al. (2015), Torkamani et al. (2017), Griffin et al. (2017), among others.

Although the already proposed priors are well succeeded to describe important features of the wavelet coefficients, as mentioned above, there is no available prior that allows us to incorporate prior kurtosis information of the coefficients. Kurtosis control can be interesting to model heavy tailed distributed coefficients and to perform wavelet shrinkage under this context. This work addresses to this problem, with the use of a particular prior distribution that allows kurtosis control of the coefficients by convenient choice of its hyperparameters.

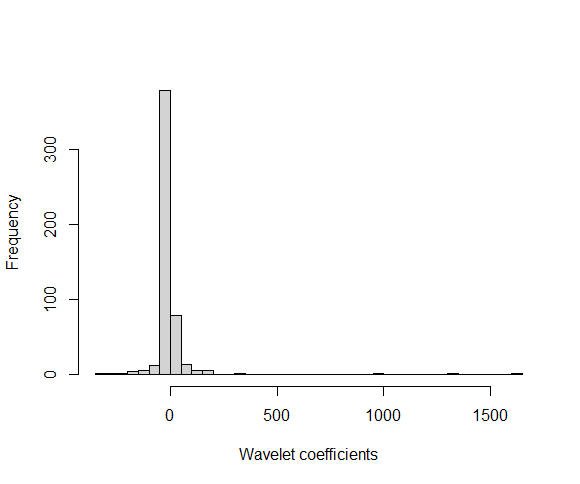

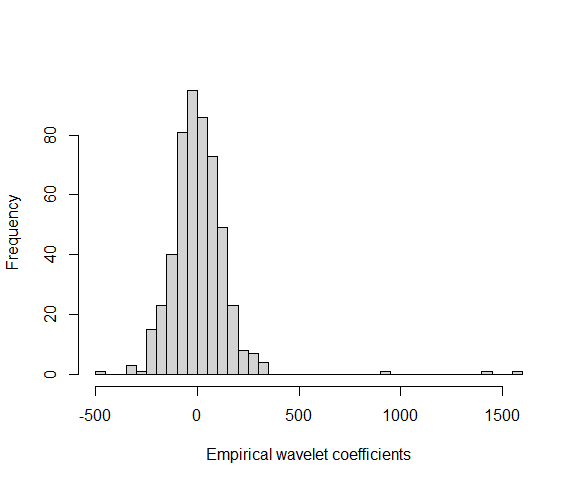

As a motivational example, we generated 512 wavelet coefficients from a heavy tailed distribution and show them by the histogram in Figure 1.1 (a). Note that most of the coefficients are zero or near from zero, once the wavelet coefficients vector of a function under certain conditions is typically sparse but there are some coefficients with high magnitudes, one of them greater than 1500 for instance. In real datasets, one observes noisy versions of wavelet coefficients, called empirical wavelet coefficients. Figure 1.1 (b) shows the histogram of associated empirical coefficients, which are the wavelet coefficients with normal noises added. The goals of a wavelet shrinker are to remove noise effect present on empirical coefficients and estimate the wavelet coefficients of Figure 1.1 (a). Once the wavelet coefficients are heavy tailed distributed, it is necessary a bayesian wavelet shrinker that takes the kurtosis of the distribution into account in the shrinkage process to have a good estimation performance.

We propose the use of the generalized secant hyperbolic distribution defined by Vaughan (2002) as prior to the wavelet coefficients in a nonparametric curve estimation problem. The great advantage is the control of the kurtosis along the resolution levels as prior knowledge, which impact on the degree of shrinkage on the extremes of the empirical wavelet coefficients distribution throw convenient hyperparameters elicitation. We organize the paper defining the model in Section 2, the shrinkage rule under the generalized secant hyperbolic prior and its statistical properties are described in Section 3 and its hyperparameters elicitation discussed in Section 4. A simulation study to evaluate the performance of the proposed shrinker and compare it with standar techniques is presented in Section 5. Application of the shrinker under generalized secant hyperbolic prior in a Brazilian stock market index dataset is done in Section 6. Finally, conclusions are in Section 7.

2 Statistical model description

Let is consider the nonparametric regression problem of the form

| (2.1) |

where , , , and , , are zero mean independent normal random variables with unknown variance . In vector notation, we have

| (2.2) |

where , and . The goal is to estimate de unknown function . The standard procedure is to apply a discrete wavelet transform (DWT) on (2.2), represented by an orthogonal matrix , to obtain the following model in the wavelet domain,

| (2.3) |

where , and . For a specific coefficient of the vector , we have the simple model

| (2.4) |

where is the empirical wavelet coefficient, is the wavelet coefficient to be estimated and is the normal random error with unknown variance . Since the method works coefficient by coefficient, we extract the typical resolution level and location subindices of , and for simplicity. Note that, according to the model (2.4), and then, the problem of estimating a function becomes a normal location parameter estimation problem in the wavelet domain for each coefficient, with posterior estimation of by the inverse discrete wavelet transform (IDWT), i.e, .

For bayesian estimation of , we propose the following shrinkage prior distribution for ,

| (2.5) |

where , is the point mass function at zero and is the generalized secant hyperbolic (GSH) distribution symmetric around zero defined by Vaughan (2002), for and as

| (2.6) |

where for ,

and for ,

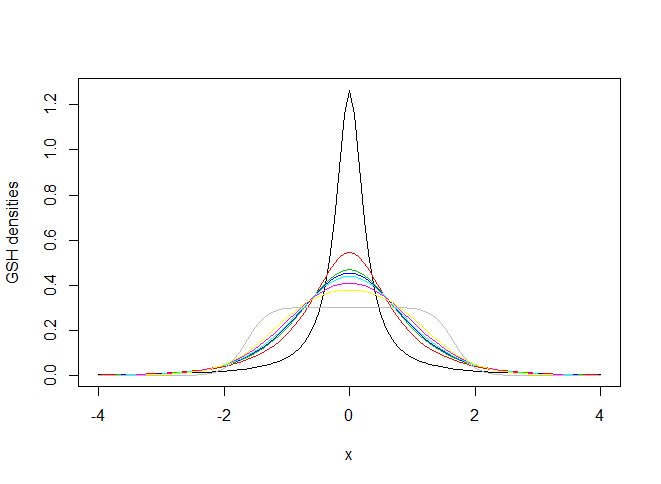

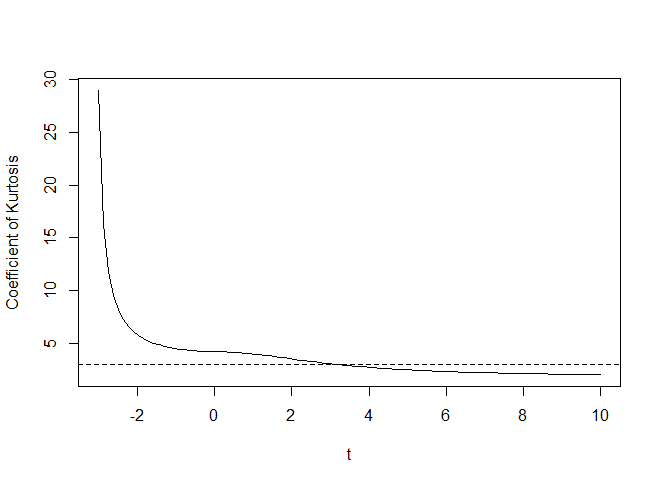

where is the indicator function. Note that for , the GSH is equivalent to the usual secant hyperbolic distribution, for , GSH tends to the logistic distribution and when , GSH tends to the uniform distribution. In fact, the hyperparameter controls the kurtosis of the distribution. Vaughan shows that if is the usual coefficient of kurtosis of the GSH with zero mean and , then for and for . As t increases, the coefficient of kurtosis decreases. This allows us to control the level of shrinkage of the wavelet coefficients on the extremes values of the empirical wavelet coefficients . The hyperparameters and control the shrinkage level for empirical wavelet coefficients sufficiently close to zero. Figure 2.1 (a) and (b) shows some densities of the GSH distribution defined in (2.6) and the coefficient of kurtosis as function of the parameter respectively.

3 The shrinkage rule and its properties

To obtain the bayesian shrinkage rule under the prior (2.5), , we assume the quadratic loss function . It is well known that, under this loss function, the Bayes rule is the posterior expected value of , i.e, . Simple calculation proves the following proposition.

Proposition 1.

If the prior distribution of is of the form , where is a density function with support in , then the shrinkage rule under the quadratic loss function and model (2.4) is

| (3.1) |

where is the standard normal density function.

Proof.

If is the likelihood function and substituting , we have

∎

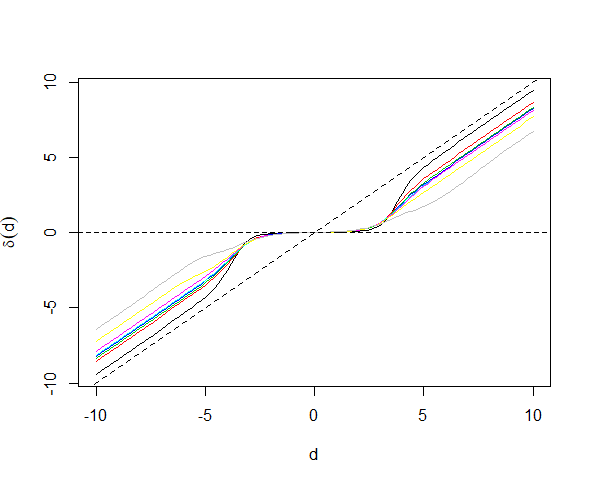

Figure 3.1 (a) shows the shrinkage rule under GSH prior (2.5) and (2.6) obtained numerically for some values of in the interval , and . As the hyperparameter increases, the rule shrinks more the coefficients on the extremes, once the kurtosis of the GSH decreases. In the curve estimation point of view, the impact of higher level of shrinkage on the extreme empirical wavelet coefficients occurs in the local features of the curve, such peaks estimation for example. In general, one can see the and hyperparameters as usual controllers of the regularity of the curve and hyperparameter as local feature controller of the curve to be estimated, which is a novelty in terms of bayesian wavelet shrinkage.

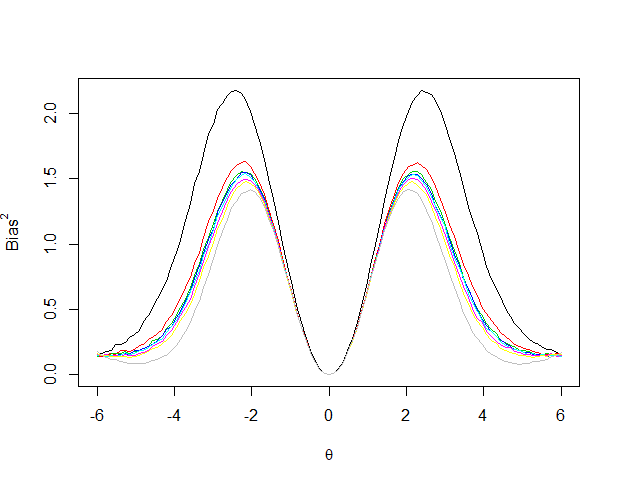

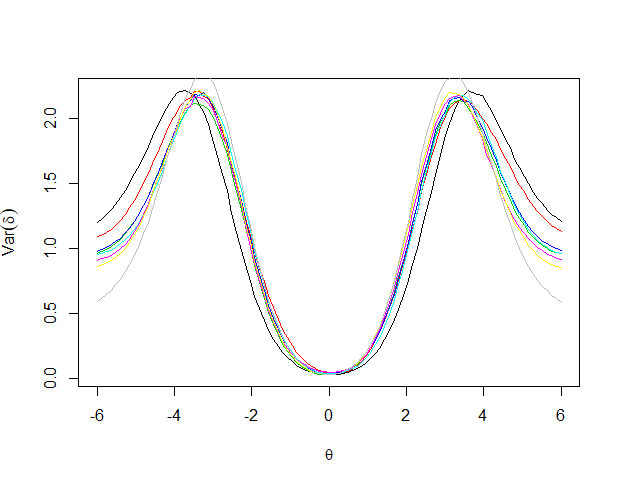

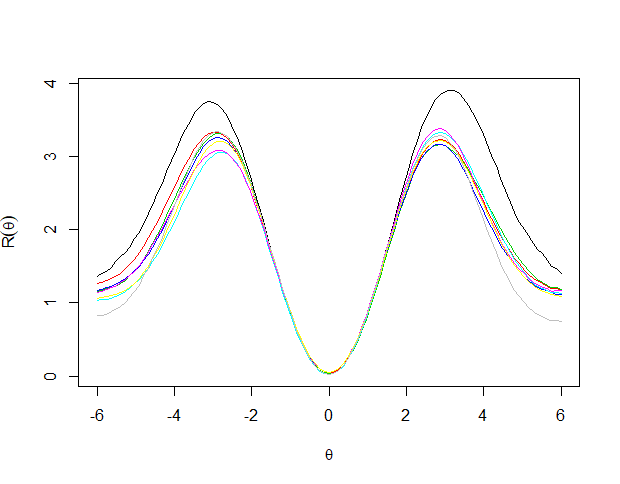

Figures 3.1 (b) and 3.2 show the squared biases, variances and classical risks of the shrinkage rules considered in Figure 3.1 (a). The properties have the same graphical symmetric behaviour, i.e, they are close to zero for close to zero, then there are peaks at the points when the shrinkage rule stops to shrink close to zero the empirical coefficients (in the plot, when is between 3 and 4) and finally they decrease and stabilize.

Tables 3.1 and 3.2 show the bayes risks of the shrinkage rules for some values of and respectively. In both cases, there is not a monotonical relationship observed between the risk and the considered hyperparameters but the risks themselves are close to zero for the hyperparameters values considered.

| -3 | -2 | -1 | 0.1 | 1 | 2 | 3 | 10 | |

|---|---|---|---|---|---|---|---|---|

| 0.125 | 0.329 | 0.223 | 0.235 | 0.183 | 0.221 | 0.240 | 0.247 |

| 0.6 | 0.7 | 0.8 | 0.9 | 0.99 | |

| 0.744 | 0.762 | 0.129 | 0.245 | 0.03 |

4 Parameters elicitation

The elicitations of the hyperparameters , and and the parameter are crucial to our bayesian procedure be well succeed. In fact, there already are propositions well accepted in the area for values of and . Based on the fact that much of the noise information present in the data can be obtained on the finest resolution scale, for the robust estimation, Donoho and Johnstone (1994) suggested the robust estimator

| (4.1) |

Angelini et al. (2004) suggested the hyperparameter be dependent on the resolution level according to the expression

| (4.2) |

where is the primary resolution level and . They also suggested that in the absence of additional information, can be adopted.

For the hyperparameter , we suggest using its relationship with the coefficient of kurtosis obtained by Vaughan, but adopting the sample coefficient of kurtosis of the empirical wavelet coefficients as estimator of the kurtosis, i.e,

| (4.3) |

where is the sample coefficient of kurtosis of the empirical wavelet coefficients, i.e, .

The hyperparameter has the same impact as the hyperparameter in the shrinkage procedure, since it controls the shape of the GSH distribution around zero in our context. In this sense, we consider and control the level of shrinkage for empirical coefficients around zero by elicitation in our study.

5 Simulation studies

Simulation studies were done to evaluate the performance in terms of averaged mean square error (AMSE) of the shrinkage rule under GSH prior and compare it with well known methods in the literature and practice. To this goal, the so called Donoho and Johnstone test functions, Bumps, Blocks, Doppler and Heavisine, see Donoho and Johnstone (1994), were used to simulate data in three sample sizes, and three signal to noise ratios (SNR), SNR . The Daubechies wavelets with ten null moments (Daub10) were applied to the generated data.

We compare the shrinkage rule under GSH prior (GSH rule) with fixed and and according to (4.2) and (4.3) with the methods Cross Validation (CV) of Nason (1996), False Discovery Rate (FDR) of Abramovich and Benjamini (1996), Stein Unbiased Risk Estimator (SURE) of Donoho and Johnstone (1995), Large Posterior Mode (LPM) of Cutillo et al. (2008) and Amplitude-scale invariant Bayes Estimator (ABE) of Figueiredo and Nowak (2001).

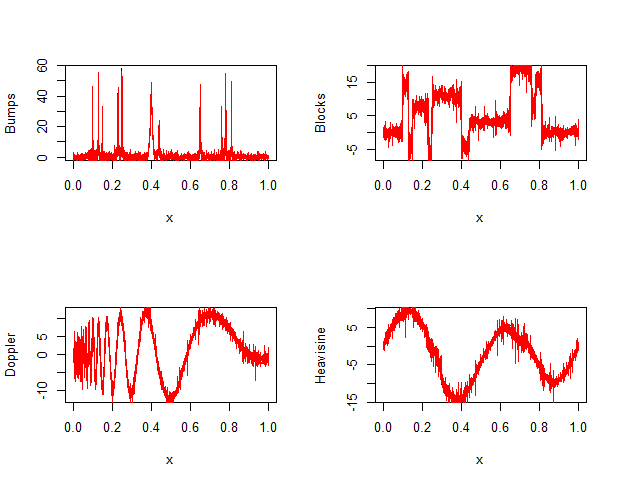

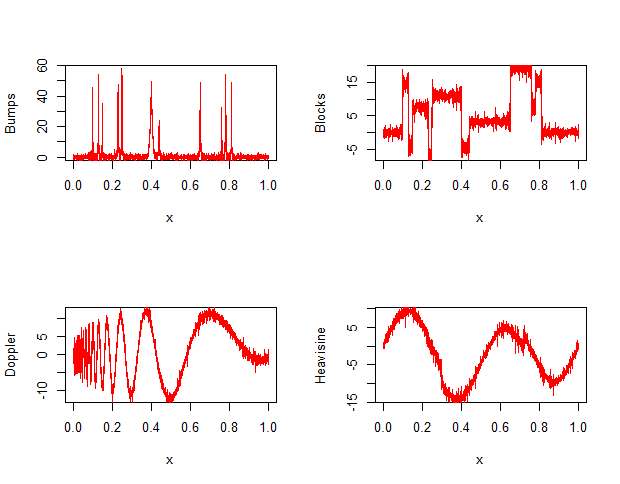

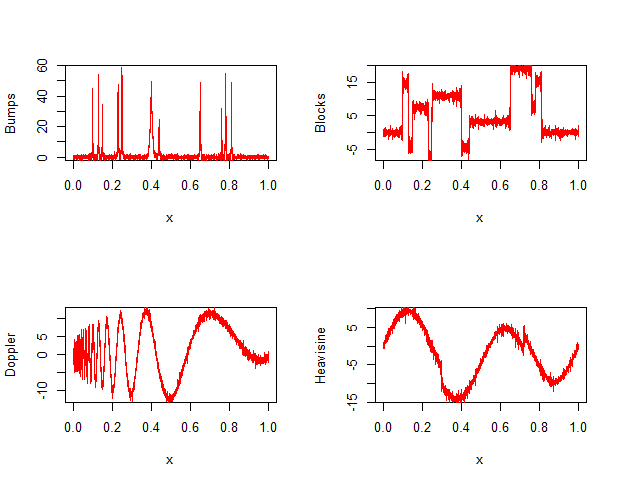

We used the mean squared error (MSE), as performance measure of the shrinkage rules. For each function, the process was repeated times and a comparison measure, the average of the obtained MSEs, , was calculated for each rule as shown in Tables 5.1 and 5.2. The estimates of the curves by the shrinkage rules for are shown in Figure 5.1.

In general, the performance of the shrinkage rule under GSH prior was great in the simulations, with the lower or the second lower AMSE in almost all the scenarios. The rule sometimes lost to ABE method, mainly for Bumps and Blocks functions, but for Doppler and Heavisine, our rule had the best performance in terms of AMSE. Further, the AMSE decreased as the SNR decreased and/or de sample size increased, as expected.

| Signal | n | Method | SNR = 3 | SNR = 5 | SNR =7 | Signal | n | Method | SNR = 3 | SNR = 5 | SNR =7 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Bumps | 512 | Univ | 11.114 | 5.178 | 3.027 | Blocks | 512 | Univ | 6.928 | 3.676 | 2.262 |

| CV | 11.466 | 9.488 | 6.297 | CV | 2.555 | 1.247 | 0.843 | ||||

| FDR | 9.290 | 4.323 | 2.633 | FDR | 5.904 | 2.919 | 1.747 | ||||

| SURE | 3.666 | 1.562 | 0.892 | SURE | 2.812 | 1.224 | 0.691 | ||||

| LPM | 5.446 | 1.948 | 1.000 | LPM | 5.417 | 1.959 | 0.995 | ||||

| ABE | 2.713 | 1.055 | 0.577 | ABE | 2.289 | 0.930 | 0.480 | ||||

| GSH rule | 3.150 | 1.120 | 0.598 | GSH rule | 2.979 | 1.186 | 0.567 | ||||

| 1024 | Univ | 7.556 | 3.576 | 2.142 | 1024 | Univ | 4.879 | 2.488 | 1.548 | ||

| CV | 2.942 | 1.935 | 1.739 | CV | 1.794 | 0.842 | 0.537 | ||||

| FDR | 5.608 | 2.543 | 1.478 | FDR | 3.888 | 1.867 | 1.125 | ||||

| SURE | 2.512 | 1.060 | 0.592 | SURE | 1.900 | 0.843 | 0.484 | ||||

| LPM | 5.469 | 1.969 | 0.999 | LPM | 5.457 | 1.964 | 1.005 | ||||

| ABE | 1.879 | 0.751 | 0.401 | ABE | 1.549 | 0.644 | 0.349 | ||||

| GSH rule | 2.158 | 0.814 | 0.425 | GSH rule | 1.910 | 0.760 | 0.407 | ||||

| 2048 | Univ | 5.056 | 2.349 | 1.392 | 2048 | Univ | 3.423 | 1.775 | 1.103 | ||

| CV | 1.606 | 0.734 | 0.480 | CV | 1.304 | 0.589 | 0.352 | ||||

| FDR | 3.594 | 1.598 | 0.920 | FDR | 2.681 | 1.292 | 0.766 | ||||

| SURE | 1.659 | 0.699 | 0.390 | SURE | 1.359 | 0.602 | 0.341 | ||||

| LPM | 5.442 | 1.959 | 0.999 | LPM | 5.425 | 1.953 | 0.996 | ||||

| ABE | 1.253 | 0.497 | 0.267 | ABE | 1.141 | 0.464 | 0.250 | ||||

| GSH rule | 1.335 | 0.508 | 0.271 | GSH rule | 1.298 | 0.531 | 0.278 |

| Signal | n | Method | SNR = 3 | SNR = 5 | SNR =7 | Signal | n | Method | SNR = 3 | SNR = 5 | SNR =7 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Doppler | 512 | Univ | 2.639 | 1.383 | 0.885 | Heavisine | 512 | Univ | 0.565 | 0.403 | 0.302 |

| CV | 1.282 | 0.632 | 0.444 | CV | 0.498 | 0.275 | 0.173 | ||||

| FDR | 2.542 | 1.247 | 0.760 | FDR | 0.594 | 0.436 | 0.308 | ||||

| SURE | 1.323 | 0.578 | 0.334 | SURE | 0.568 | 0.414 | 0.313 | ||||

| LPM | 5.472 | 1.956 | 1.005 | LPM | 5.418 | 1.956 | 0.995 | ||||

| ABE | 1.161 | 0.470 | 0.255 | ABE | 0.702 | 0.311 | 0.177 | ||||

| GSH rule | 1.162 | 0.500 | 0.264 | GSH rule | 0.472 | 0.252 | 0.159 | ||||

| 1024 | Univ | 1.632 | 0.848 | 0.533 | 1024 | Univ | 0.455 | 0.313 | 0.230 | ||

| CV | 0.806 | 0.369 | 0.219 | CV | 0.365 | 0.198 | 0.125 | ||||

| FDR | 1.543 | 0.752 | 0.453 | FDR | 0.499 | 0.322 | 0.225 | ||||

| SURE | 0.836 | 0.381 | 0.223 | SURE | 0.459 | 0.320 | 0.238 | ||||

| LPM | 5.443 | 1.959 | 1.000 | LPM | 5.439 | 1.958 | 1.001 | ||||

| ABE | 0.810 | 0.333 | 0.186 | ABE | 0.592 | 0.245 | 0.135 | ||||

| GSH rule | 0.711 | 0.295 | 0.171 | GSH rule | 0.340 | 0.176 | 0.106 | ||||

| 2048 | Univ | 1.160 | 0.583 | 0.367 | 2048 | Univ | 0.362 | 0.235 | 0.166 | ||

| CV | 0.559 | 0.254 | 0.147 | CV | 0.268 | 0.142 | 0.088 | ||||

| FDR | 1.030 | 0.487 | 0.291 | FDR | 0.398 | 0.234 | 0.157 | ||||

| SURE | 0.578 | 0.259 | 0.148 | SURE | 0.365 | 0.239 | 0.170 | ||||

| LPM | 5.431 | 1.955 | 0.997 | LPM | 5.439 | 1.958 | 0.999 | ||||

| ABE | 0.634 | 0.251 | 0.133 | ABE | 0.515 | 0.204 | 0.110 | ||||

| GSH rule | 0.423 | 0.189 | 0.104 | GSH rule | 0.238 | 0.120 | 0.069 |

6 Real data application

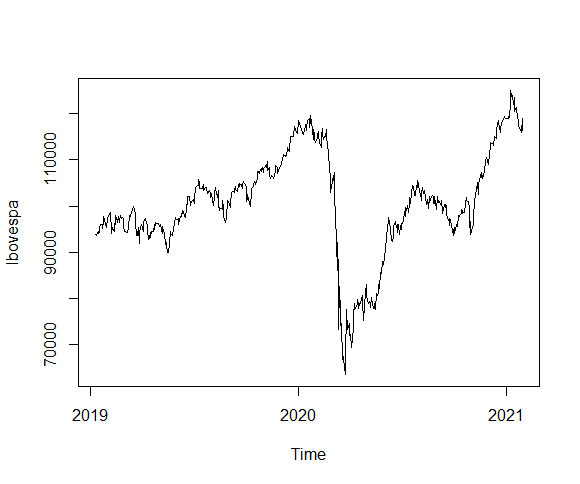

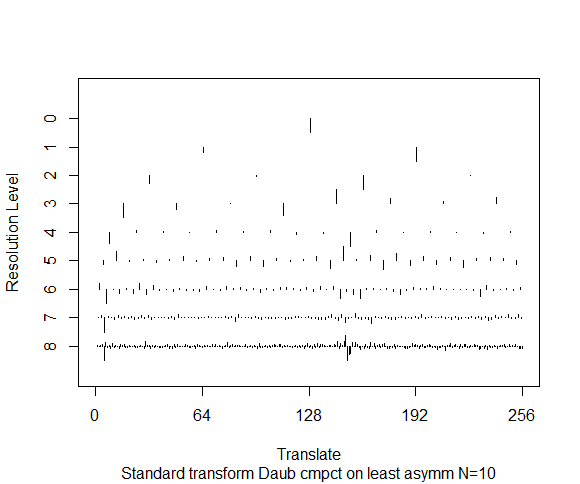

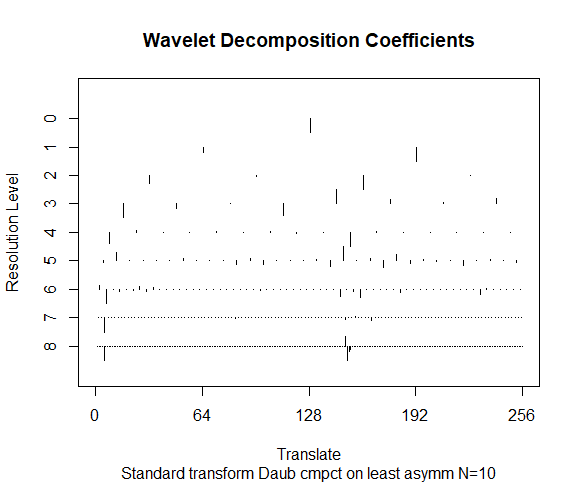

To verify the performance of the GSH shrinkage rule in a real data, we consider a São Paulo stock market index (IBOVESPA) time series collected daily from January, 1st 2019 to January, 29th 2021 (), which is showed in Figure 6.1 (a). After a DWT application, with a Daubechies basis with 10 null moments, we obtain the empirical wavelet coefficients, showed by resolution level in Figure 6.1 (b). Denoising is important in this context to detect sistematic changes of the IBOVESPA. In this sense, wavelet shrinkage is one of the most used denoising tools in time series.

Figures 6.2 (a) and (b) shows denoised IBOVESPA time series after GSH shrinkage rule application and the estimated wavelet coefficients respectively. Observe that most of the empirical coefficients are shrunk to zero or near to zero and only the significative empirical coefficients, in magnitude, remain nonzero after shrinkage process. It minimizes the effect of noise and makes clearer the main features of the time series.

7 Conclusions

The simulation studies showed us that the shrinkage rule under GSH prior had a great performance in terms of averaged mean square error when compared with some of the most used wavelet shrinkage and thresholding techniques nowadays. Further, the advantage of controlling the level of shrinkage on the extreme values of the empirical coefficients through the kurtosis of the GSH distribution allows to include information about local features of the curve to be estimated such peaks, for example. These features can allow the proposed shrinkage rule be considered for practitioners for real data applications.

8 Acknowledgement

This study was financed by the Coordenação de Aperfeiçoamento de Pessoal de Nível Superior – Brasil (CAPES).

References

- [1] Abramovich, F. e Benjamini, Y., (1996) Adaptive thresholding of wavelet coefficients. Comp. Stat. Data Anal., 22, 351–361.

- [2] Angelini, C. e Vidakovic, B. (2004) Gama-minimax wavelet shrinkage: a robust incorporation of information about energy of a signal in denoising applications. Statistica Sinica, 14, 103-125.

- [3] Bhattacharya, A., Pati, D., Pillai, N. and Dunson, D., (2015) Dirichlet-Laplace priors for optimal shrinkage. J. Am. Statatist. Soc.,110 1479-1490.

- [4] Cutillo, L. et. al., (2008) Larger Posterior Mode wavelet Thresholding and Applications. J. of Statistical Planning and Inference, 138, 3758-3773.

- [5] Donoho, D. L. and Johnstone, I. M., (1994) Ideal spatial adaptation by wavelet shrinkage. Biometrika, 81, 425–455.

- [6] Donoho, D. L. e Johnstone, I. M., (1995) Adapting to unknown smoothness via wavelet shrinkage. J. Am. Statist. Ass., 90, 1200–1224.

- [7] Donoho, D. L., Johnstone, I. M., Kerkyacharian, G., and Picard, D. (1995) Wavelet shrinkage: Asymptopia? (with discussion). J. R. Statist. Soc. B, 57, 301–369.

- [8] Donoho, D. L., Johnstone, I. M., Kerkyacharian, G., and Picard, D. (1996) Density estimation by wavelet thresholding. Ann. Statist., 24, 508–539.

- [9] Figueiredo, M.A.T and Nowak, R.D., (2001) Wavelet-based image estimation: an empirical Bayes approach using Jeffrey’s noninformative prior. IEEE Transactions on Image Processing, 10, 1322-1331.

- [10] Griffin,J. and Brown, P., (2017) Hierarquical Shrinkage Priors for Regression Models. Bayesian Analysis,12,Number 1, 135-159.

- [11] Karagiannis,G.,Konomi, B. and Lin, G. (2015) A bayesian mixed shrinkage prior procedure for spatial-stochastic basis selection and evaluation of gPC expansion: applications to elliptic SPDEs. J. Comp. Physics,284, 528-546.

- [12] Nason, G. P. (1996) Wavelet Shrinkage Using Cross-validation. J. R. Statist. Soc. B, 58, 463–479.

- [13] Reményi, N. and Vidakovic, B., (2015) Wavelet shrinkage with double weibull prior. Communications in Statistics: Simulation and Computation, 44, 1, 88-104. .

- [14] Torkamani, R. and Sadeghzadeh, R., (2017) Bayesian compressive sensing using wavelet based Markov random fields. Signal Processing: Image Communication, 58, 65-72.

- [15] Vaughan,D.C., (2006) The generalized secant hyperbolic distribution and its properties. Communications in Statistics: Theory and Methods, 31(2), 219-238.

- [16] Vidakovic, B., (1998) Nonlinear wavelet shrinkage with Bayes rules and Bayes factors. J. Am. Statist. Ass., 93, 173–179.

- [17] Vidakovic, B., (1999) Statistical Modeling by Wavelets. Wiley, New York.