Abstract

We propose the relaxation bootstrap method for the numerical solution of multi-matrix models in the large limit, developing and improving the recent proposal of H.Lin. It gives rigorous inequalities on the single trace moments of the matrices up to a given “cutoff” order (length) of the moments. The method combines usual loop equations on the moments and the positivity constraint on the correlation matrix of the moments. We have a rigorous proof of applicability of this method in the case of the one-matrix model where the condition of positivity of the saddle point solution appears to be equivalent to the presence of supports of the eigenvalue distribution only on the real axis and only with positive weight. We demonstrate the numerical efficiency of our method by solving the analytically “unsolvable” two-matrix model with interaction and quartic potentials, even for solutions with spontaneously broken discrete symmetry. The region of values for computed moments allowed by inequalities quickly shrinks with the increase of the cutoff, allowing the precision of about 6 digits for generic values of couplings in the case of symmetric solutions. Our numerical data are checked against the known analytic results for particular values of parameters.

Analytic and Numerical Bootstrap for One-Matrix Model and “Unsolvable” Two-Matrix Model

Vladimir Kazakov and Zechuan Zheng

Laboratoire de Physique de l’École Normale Supérieure,

CNRS,

Université PSL, Sorbonne Universités,

24 rue Lhomond, 75005 Paris, France

1 Introduction

Matrix integrals play an important role in numerous physical and mathematical subjects, such as multi-component quantum field theory tHooft:1973alw (see Migdal:1983qrz for the review), two-dimensional quantum gravity and string theory David:1984tx ; Kazakov:1985ea ; Kazakov:1985ds ; Kazakov:1987qg , mesoscopic physics PhysRevLett.52.1 , algebraic geometry Dijkgraaf:2002fc ; Dijkgraaf:2002pp ; Eynard:2007kz ; Kontsevich:1992ti , number theory montgomery1973pair , etc. A rather general class of matrix integrals has the form

| (1) |

where are Hermitian matrices with invariant integration measure and the potential is an analytic function (often a polynomial) of the variables . The partition function is a function of parameters (couplings) of the potential. The typical “physical” quantities to study are various correlators of traces of “words” built out of products of matrices , computed w.r.t. the measure represented by the expression under the integral:

| (2) |

The limit, with the appropriately adjusted parameters of the potential and of the averaged quantity, is of a special importance in multiple applications since it describes the thermodynamical limit of macroscopically many degrees of freedom for various physical systems. Such a limit deals with the infinite number of integrals, thus the matrix integral becomes a functional integral.

A particularly interesting limit, for the potential scaled as , where the function contains only finite, -independent parameters, is usually called the ’t Hooft, or planar limit. Among many important matrix models of this kind there is the so called Eguchi-Kawai -matrix integral equivalent, in the ’t Hooft limit, to the multicolor Quantum Chromodynamics Eguchi:1982nm . The ’t Hooft limit is characterized by the perturbative expansions given in terms of planar Feynman graphs (-expansion appears to be a topological expansion: the “fat” graphs of a given genus are weighted with the factor ). This allows the counting of such planar graphs Brezin:1977sv ; Itzykson:1979fi ; Mehta:1981xt and enables the introduction and exact solution of statistical mechanical models on random planar dynamical lattices – Ising model on random triangulations Kazakov:1986hy ; Boulatov:1986sb and various generalizations Kazakov:1987qg ; Kostov:1988fy ; Daul:1994qy ; Kazakov:1988ch .

The direct analytic computation of a majority of such multi-matrix integrals is virtually impossible, apart from some trivial, albeit important, cases, such as the quadratic potential leading to the gaussian integral.111Expansions w.r.t. parameters around the gaussian point lead in the ’t Hooft limit to the perturbation theory formulated in terms of planar Feynman graphs. It can help to study the model in a specific, narrow domain of the parameter space.

For a sub-class of such integrals with specific potentials the problem can be reduced to integrations over a smaller number of variables than . For example, sometimes the problem can be reduced to the integrations or summation only over variables, such as eigenvalues of the matrices. Then, in the large limit, the problem can be reduced to the saddle point calculation, significantly simplifying the problem of computation of that functional integral.222An (incomplete) review of such solvable matrix models can be found in Kazakov:2000aq . The basic example of such a simplification is the one matrix model

| (3) |

solvable for any potential . Once we have two or more matrix integration variables in (1) the problem usually gets much more complicated. Generically, such models are unsolvable, i.e. the number of degrees of freedom cannot be efficiently reduced, and the saddle point approximation is inappropriate since the characteristic “energy” and entropy of the integration variables are both of the order . Here comes the question whether we can study these integrals at least numerically.

Virtually the only universal general method of numerical computation of functional integrals is the Monte-Carlo method. It has been applied to some matrix integrals with more or less of success. Its main drawbacks are well known: i) the result comes with a statistical error; ii) it is sometimes difficult to reach the numerical equilibrium state in a reasonable time; iii) MC is bad for the systems with sign-changing Boltzmann weights or non-local interactions; iv) the size of the system (the number of integrals) is limited by computational facilities v) The precision is usually rather modest, maximum about 3-4 digits.

Do we have any alternative?

In the 1980’s, in a series of papers Jevicki:1982jj ; Jevicki:1983wu ; Rodrigues:1985aq , the authors formulated the problem of large N matrix integral and large N quantum mechanics in the loop space (space of moments). The authors attempted the numerical study for the loop variables by minimizing an effective action. They were the first to stress the importance of positive semi-definiteness conditions for certain matrices of loop variables in getting physically meaningful results.

Recently, an important progress has been made in the computations of multi-point correlators in conformal field theories in various dimensions, due to the conformal bootstrap method 2008JHEP…12..031R . The method uses various properties of correlators, such as crossing and positivity, to “bootstrap” numerically their values and the values of the critical exponents. It appeared to be far more efficient and precise then other numerical approaches, giving the critical exponents of 3d Ising model with the record 6-digits precision 2017JHEP…03..086S . An appealing property of this method is the absence of any statistical error in the results, which are given within rigorously established margins.

Inspired by this success a few authors applied the philosophy of the numerical bootstrap to the computations of various matrix integrals 2020JHEP…06..090L ; 2020PhRvL.125d1601H and even of the lattice multi-color QCD and SYM theory 2017NuPhB.921..702A . Instead of the direct study of the matrix integrals they proposed to study the large Schwinger-Dyson equations which are often also called loop equations, in analogy with their applications to QCD Makeenko:1979pb . They are easily obtained by the obvious Ward identities resulting from insertion of the full matrix derivative under the matrix integral:

| (4) |

where the matrix derivative inside the trace acts on all -matrices, including the potential. All other loop equations correspond to all possible “words” of matrices under the trace and to all insertions of various matrix derivatives at any place in the “words”.333 In the ’t Hooft limit, the single trace “words” are enough due to the factorization property which we will describe in the next section. Then the positivity conditions are imposed stating that the inner product444Here inner product of an operator means . of any operator with itself is positive. Rigorous bounds on the dynamical quantities of the theory can be derived from these positivity conditions and loop equations.

This new approach, compared to the previous work of loop variables Jevicki:1982jj ; Jevicki:1983wu ; Rodrigues:1985aq , imposes the large Schwinger-Dyson equations (loop equations) explicitly, rather than getting loop equations as a result of effective action minimization. In parallel with the philosophy of conformal bootstrap, this approach focuses more on the geometry of the space of loop variables under sensible physical constraints, which guarantees the rigorousness of the bounds on physical quantities.

In the inspiring work of Lin 2020JHEP…06..090L the method was rather successfully applied to the one-matrix model mentioned above, to the exactly solvable two-matrix model with interaction Mehta:1981xt ; Itzykson:1979fi describing the Ising model on planar graphs Kazakov:1986hy as well as to the model with interaction, presented there as a case of “unsolvable” matrix model 555We will demonstrate in the Appendix A that, in fact, all two-matrix models with cubic interactions, including this one, are solvable in the above-mentioned sense. . Lin uses the non-linear equations (4) to bootstrap the loop averages up to the positive semi-definite matrix of size .

This new approach has, in our opinion, a great potential for the precision computations of physically important matrix integrals in the ’t Hooft limit. But at the same time it is very much perfectible at this stage.

Firstly, the numerical matrix bootstrap approach of 2017NuPhB.921..702A ; 2020JHEP…06..090L ; 2020PhRvL.125d1601H , based on the loop equations and positivity constraint, is not well understood analytically. Its efficiency, and the power of positivity, still looks quite mysterious. It is not even fully understood why we need the positivity condition. Secondly, the matrix bootstrap has a very distinguished feature comparing to most of the other bootstrap problems we dealt with so far: it is in general non-convex. The non-convexity comes from the quadratic terms in the loop equation, which is a result of large factorization. In optimization theory, this is called Nonlinear SDP (semi-definite programing) and all the solvers for it are not mature enough compared with the highly developed SDP solvers dealing with linear problems. In 2017NuPhB.921..702A ; 2020JHEP…06..090L ; 2020PhRvL.125d1601H , the authors tried to bootstrap the matrix models by the Nonlinear SDP directly, and this non-linearity limited the bootstrap capabilities to very simple models, or to more complex models but only up to very small lengths of operators.

1.1 Main results

In this work, we advance the matrix bootstrap approach trying, on the one hand, to understand analytically the role of positivity conditions, and on the other hand, to overcome, at least partially, the above-mentioned limitations of the method.

First, we derive a necessary and sufficient condition for the positivity of bootstrap for large one-matrix model, to clarify how this method is working. Namely, we show that the positivity is equivalent to the condition for the resolvent to have the cuts only on the real axis, with the positive imaginary part corresponding to the positive density of eigenvalue distribution. This condition actually enables us, in principle, to analytically solve the bootstrap problem for any one-matrix model. For the illustrative purposes, we will apply the new positivity condition to the one-matrix model with quartic potential:

| (5) |

where we normalized the quadratic term to . We will use the analytic bootstrap to completely classify the admissible set of solutions of the loop equations and positivity conditions, and to locate the critical value of symmetry breaking.

So far, we could solve exactly a very limited set of bootstrap problems, and most of them correspond to very simple theories, such as Sine-Gordon theory in S-matrix bootstrap 2017JHEP…11..143P and 1d mean field theory in conformal bootstrap 2019JHEP…02..162M . Since this method appears to be applicable to any one-matrix model and generalized to some solvable multi-matrix models, it provides us with a big new family of exactly solvable bootstrap problems. Hopefully these solvable bootstrap models will give us more of intuition about the way the bootstrap method works.

The other new result of this work is a new bootstrap scheme for the study of non-linear SDP for multi-matrix integrals, which appears to be numerically much more efficient than those proposed in the past. The main ingredient of the method is the introduction of relaxation matrix in the place of non-linearity of the loop equation. Namely, we treat the quadratic terms as independent variables and impose the positivity condition on these variables. Surprisingly, it seems enough to bootstrap the region of admissible values of the computed quantity that is quickly shrinking with the increase of the “cutoff” – the maximal length of “words” in the involved operators.

As a particular example of analytically unsolvable matrix integral we will study by this method the following two-matrix model

| (6) |

Various versions of this model have been studied in the past in connection to certain supersymmetric Yang-Mills theories 1999NuPhB.557..413K . In the particular case the model is solvable and it will serve us as an important check of applicability and efficiency of our relaxation bootstrap method. Our results show a very good precision: up to 6 digits with the maximal cutoff equal to 22 for the words under averages. We were also able to establish with a reasonable accuracy the phase structure of the model in the coupling space, i.e. the positions of critical lines corresponding to the convergence radius of planar perturbative expansion, as well as to the spontaneous symmetry breaking.

The two-matrix model (6) considered in this paper serves mostly for the illustration of the power of our method, though it could have in principal some physical applications, such as the statistical mechanics on dynamical planar graphs, in the spirit of Kazakov:1998qw ; Kostov:1999qx ; Zinn-Justin:1999chi .

This article is organized as follows. The next Section 2 serves as a retrospect of the Hemitian matrix integral and the numerical bootstrap technique developed for it so far. Then in Section 3 we propose our equivalent condition for the positivity condition described in Section 2. This condition will justify the numerical bootstrap method and enable us to analytically solve the corresponding bootstrap problem. in Section 4, we will describe the way our relaxation method works for analytically unsolvable large multi-matrix integrals. We test this relaxation method in Section 5 on the concrete unsolvable model (6). We will see that our relaxation method is able to largely meet our expectations, with remarkable precision. In the last section, after short conclusions, we will briefly discuss possible applications of our method to some more physical problems, such as the multicolor lattice Yang-Mills theory.

Note: The main results of this work are compared with the later Monte Carlo(MC) results Jha:2021exo . This comparison convinces us that the bootstrap method is more efficient than MC regarding the large N two-matrix model calculation.

2 Hermitian one-matrix model bootstrap

In this section we will revisit several basic facts about large limit Hermitian one-matrix model and the related numerical bootstrap proposed in 2020JHEP…06..090L . We will be mainly focused here on the aspects of this model which are crucial for the theoretical development in the next section and provide us with important intuition. The reader can refer to numerous works and reviews, some already cited above (see e.g. Eynard:2004mh for a good state-of-art description of results on Hermitian one-matrix model).

2.1 Hermitian one-matrix model in the planar limit and loop equations

The Hermitian one-matrix model is defined by matrix integral:

| (7) |

where the invariant Hermitian measure is . The potential is usually taken polynomial 666We believe that our final conclusion can be generalized to non-polynomial potentials, but there may be some subtleties.:

| (8) |

The main “physical observable” is the -th moment:

| (9) |

This model is solvable in the planar limit for arbitrary polynomial potentials Brezin:1977sv . There exist several methods for that: direct recursion relations for planar graphs, orthogonal polynomials, saddle point approximation for the eigenvalue distribution, loop equations (see Migdal:1983qrz ; DiFrancesco:1993cyw for a review). The loop equations will play the crucial role in our bootstrap method.

To derive them we simply use the Schwinger-Dyson method by writing

| (10) |

since the expression under the integral is a total derivative. The boundary terms are absent assuming that the highest power of the potential is even and its coefficient is positive . 777For the “unstable” potentials, which do not satisfy one of these conditions, the matrix integral might still exist with appropriate deformation of the integration contour. The large solutions can exist even independently of the contour deformation since they correspond to local minima of the effective potential for the eigenvalues.

Applying explicitly the matrix derivative in (10) we write the loop equation in terms of the moments:888Here for the conciseness, we introduce the normalized trace , so that

| (11) |

In the limit we can use the factorization property:

| (12) |

Then the loop equation reduces to

| (13) |

The simplest way to solve (13) is to introduce the generating function of moments - the resolvent - as a formal power series in terms of :

| (14) |

We have not yet assumed anything about the convergence of the series. Multiplying (13) by and summing from to we represent the loop equation in a compact form as a quadratic equation for the resolvent.

| (15) |

The function comes from carefully collecting in the summation the terms with small ’s . It can be written compactly as:

| (16) |

This is a polynomial of and a linear function of . For example, if , then we have . We can solve (15), picking the relevant branch of the root which reproduces the leading behavior of the resolvent at infinity:

| (17) |

This result will play an important role in our work, so we make several comments on it:

-

1.

By (17), the resolvent is understood as a genuine analytic function, at least in the neighborhood of infinity point. So the formal series defined in (14) has a finite radius of convergence. As a consequence, there must be an exponential bound for the moments999Strictly speaking the radius of convergence is the inverse of the module of largest root of the polynomial under the square root in (17), unless two of such roots merge. Here it is enough for us that it is bounded exponentially.:

(18) -

2.

It is clear from this formula, that all the moments are determined by several low-order moments in and the couplings:

(19) This is what the loop equation tells us. But the loop equation doesn’t tells us how to fix the low-order moments involved in . Those can be fixed only by additional assumptions on the solution, such as for example the single support solution for the eigenvalues (single cut on the physical sheet of ). We will see how to classify the solutions which are picked up by the bootstrap method.

To have more intuitive ideas of possible large solutions it is useful to reduce the matrix integration (7) to the integration over the eigenvalues of the Hermitian matrix. Namely, if we represent it as where is the diagonal matrix of eigenvalues and is the diagonalizing unitary matrix, the matrix integral reduces to only integrations over the eigenvalues Brezin:1977sv :

| (20) |

where the square of the Vandermonde determinant represents the Jacobian of the change of integration variables (Dyson measure). Here the integrand is of the order whereas the number of variables is reduced to . This allows for the application of the saddle point approximation, giving the BIPZ saddle point equations (SPE) Brezin:1977sv

| (21) |

It looks as the condition of electrostatic equilibrium of two-dimensional point-like electric charges (of the same sign) with coordinates on a line, locked in the potential (see the Fig 1. )

The possible physical solutions correspond to filling minima of such a potential with fractions of these charges, such that . The eigenvalues then form a continuous distribution with finite supports along the real axis.

The SPE describes all extrema of the effective potential

| (22) |

not only the minima but also the maxima. For the solutions with the filling of some maxima of the potential the linear supports of distributions around the maxima should inevitably turn into the complex plane, with the complex conjugate endpoints, as shown in Fig 1. We will call such solutions “unphysical”. The values of fractions are in one-to-one correspondence with the values of first moments and they completely fix the algebraic curve of the solution Dijkgraaf:2002fc ; Dijkgraaf:2002pp . The solutions where we fill only the minima of the effective potential will be called "physical". The supports for such solutions will be located only on the real axis, with positive weight for the distribution of the eigenvalues.

In the large limit, the distribution of eigenvalues converges to a continuous function and the corresponding SPE actually becomes the quadratic equation for resolvent (15). In this limit, the resolvent function, the eigenvalue distribution and the series of moments are closely related.

The moments can be computed via the resolvent (14) by a simple contour integration formula:

| (23) |

where the contour must encircle all branch points of (see Dijkgraaf:2002fc ; Dijkgraaf:2002pp for the details). We introduced here the “cut-function” – the square root of the discriminant – by the formula

| (24) |

The roots of the discriminant become the branch points of the cut-function. Their number is always even. For real couplings in the potential the branch points lay only on the real axis or come in complex conjugate pairs. Note that it is easy to relate the eigenvalue fractions to these branch points:

| (25) |

where the contour encircles anticlockwise only the branch points , and can be in principal of either sign.

The eigenvalue density is expressed as the discontinuity of the cut function :

| (26) |

and the moments can be expressed by the eigenvalue density:

| (27) |

2.2 Bootstrap method for the large one matrix model

As we stated above, the loop equation (13),(15) has in general a continuum of solutions of the form (17) labeled by a finite number of parameters – the lowest moments which can take a priori arbitrary values. But not all of these solutions are “physical”, i.e. rendering all moments real and compatible with the finite Hermitian matrix ensemble. For example, the physical even moments should be positive, but this condition is not the only one.

A more general physical condition on a solution is the positivity of inner product for the matrix integral. This condition states that, for any operator of the form and for any , we have the positive semi-definite quadratic form101010Here we assume that all the expectation values we study are real. This is actually a non-trivial result from the symmetry of the potential. Since this symmetry is always present for all the models considered in this article, we will implicitly assume this to be always true.:

| (28) |

Here we introduced the matrix which will be called below for convenience the correlation matrix. The above condition is equivalent to the positive definiteness of correlation matrix111111Here we slightly abused the notations: sometimes means the matrix with finite size, involving only the moment up to a certain order (“cutoff”), and sometimes it means the infinite dimensional matrix. But the positive semi-definiteness is always well defined as a positivity of the corresponding quadratic form.:

| (29) |

The condition (28) is obvious for a finite matrix model with converging integral (7), i.e. when is even and in the potential (8), since the moments are just given by the integration of positive definite functions with a positive measure. In addition, at finite there exists only one solution for the moments 121212To define the matrix integral for unstable potentials, when odd or/and one usually deforms appropriately the integration contours. Then the the questions of positivity become less obvious for finite . But we will see on the example of quartic potential that at infinite we can still have positivity for certain solutions, even for such, globally unstable, potentials. . But it is far from trivial in large limit, where we have to understand what solutions from the continuum are really physical.

To do numerical bootstrap, we set a finite cutoff , i.e. the highest moment in the correlation matrix and loop equations is and the size of the correlation matrix is . We can use the loop equations to express the higher moments through a certain number of the lower moments and substitute them into the correlation matrix as functions of lower moments. Then the positivity of the correlation matrix provides us with algebraic inequality on these lower moments. In general, we expect to get the inequalities for each of the lower moments both from above and from below, for example:

| (30) |

at a cutoff . In practice, the allowed region shrinks fast as we increase , giving us tight bounds on .

We exemplify this approach on the case of quartic potential . We plot in Fig 2 the region for the allowed values of function under the assumption of symmetry of the solution, i.e. . Under this assumption, all the higher moments are polynomials in terms of and . The positivity of the correlation matrix reduces to a list of algebraic inequalities on .131313To depict the allowed region, maybe the simplest way is the Mathematica RegionPlot function. Although not really numerically efficient, it is already good enough for the simplest quartic one-matrix model.

It is a bit surprising that the bootstrap scheme described above for Hermitian one-matrix model is generally analytically solvable, considering that it is usually non-trivial to solve an infinite series of algebraic inequalities. In the next section we will propose a necessary and sufficient condition for the positivity constraint (29) by virtue of a result of solution of Hamburger moment problem. By this condition we can not only generally solve the bootstrap problem analytically but also justify why the numerical bootstrap process excludes the unphysical solutions of SPE described in Section 2.1.

3 Hamburger moment problem and positivity of resolvent

As it should be clear from the previous section, the bootstrap method for one-matrix model has two main ingredients: 1. The Schwinger-Dyson loop equations for the moments of the random matrix variables; 2. The positive definiteness of the correlation matrix of these moments. We will rigorously prove that the second ingredient, in virtue of the Hamburger moment problem reed1975ii , picks up in the planar limit the solutions of loop equations only with real-positive supports of the matrix eigenvalue distribution. We will employ this condition to analytically solve the bootstrap condition.

3.1 Hamburger problem versus the positivity condition on resolvent

The loop equation (13) renders all possible large , saddle point solutions of the Hermitian one matrix model. Some of them “look” physical, i.e. corresponding to the stable equilibrium in the Coulomb gas picture for the eigenvalues locked in the effective potential (22). For the other, the stable solution corresponds to “unphysical” picture when the supports of eigenvalue distribution become complex. What are the solutions captured by our bootstrap procedure?

As we just reviewed, numerical bootstrap of one matrix model consists of two ingredients: loop equation and positivity of correlation matrix. It sets a cutoff on both constraints and gets a rigorous bound on the physical quantities we are interested in. Analytically all the information contained in the loop equations is encoded in the quadratic equation of resolvent (15), which has a simple solution (17). It describes the hyper-elliptic algebraic curve parameterized by complex variable . It is natural to ask the question: can the positivity of correlation matrix also be expressed as a simple condition on the resolvent? The answer is, luckily and a bit surprisingly, yes.

For convenience, we make the following definition: a resolvent satisfies the positivity condition if the corresponding eigenvalue density (26) is supported on the real axis and is positive on its support. Our main conclusion of this section will be:

| (31) |

We prove the necessity first. The proof is based on a well-known mathematical conclusion that will play an important role in our demonstration – the result of the solution of the Hamburger moment problem reed1975ii :

For a given series of real numbers , there exists a positive Borel measure such that:

| (32) |

if and only if the matrix is positive semi-definite. Moreover, if there exist the constants and , such that , the measure is unique.

Applying the result of Hamburger momentum problem (42), we have for each moment . We notice from the exponential bound condition (18) that must be supported in a finite region , since otherwise, if we have , such that , then

| (33) |

which contradicts the exponential bound (18).

Consequently for :

| (34) |

The exchange of infinite sum and integration is justified by Fubini’s theorem. Due to this equation, is analytic in the region outside of the disk . The last equality in (34) enables us to analytically continue to the whole region . So the function must be analytical away from the real line, which eliminates the possibility of cuts between complex branch points. Comparing with (17) and (26), we come to the conclusion that all supports of function must be located on the real line. For the positivity of eigenvalue density, we note that we can extract by contour deformation the coefficient of the series in (14):

| (35) |

By the uniqueness of solution of the Hamburger momentum problem, we must have i.e. they are equal in terms of positive measure.141414We note that the uniqueness is not strictly necessary here. To see this, the reader can combine Stone-Weierstrass theorem and the fact that compactly supported continuous function is dense in . Then if is not positive almost everywhere then the positivity of correlation matrix is violated. So we have real supported and positive. This concludes our proof of necessity for (31).

The proof of sufficiency is straightforward. It is already true because the sufficiency is a part of the result of the solution of Hamburger moment problem. For a more direct argument, suppose we have a resolvent that satisfies the positivity condition, i.e. (27) with . We notice that the matrix is trivially positive semi-definite for real , so that if we integrate the matrix w.r.t. the positive measure , it stays positive semi-definite as well. The result of the integration is actually our correlation matrix . This concludes the proof of sufficiency and hence of the equivalence (31).

It is easy to demonstrate by the direct computation that in the presence of complex branch points in the corresponding correlation matrix is not positive definite. A simple example is the resolvent for the matrix model with the unstable potential , which is . We see that so that the correlation matrix is not positive definite.

This suggests the validity of the numerical bootstrap approach at least in the case of the one-matrix model: by imposing the positive semi-definiteness condition on the solutions of loop equations, at least for a finite cutoff , we exclude the “unphysical” large solutions with the eigenvalue distributions having complex or negative supports, i.e. violating the hermiticity of the matrix measure.

The result of the present section actually enables us to analytically solve the bootstrap constraints, since the infinite series of inequalities from the positivity of the correlation matrix have been proven to be equivalent to the positivity property of resolvent. As an example, in the next subsection we will present the analytic result of solving the bootstrap problem of quartic one-matrix model.

The application of numerical bootstrap to the multi-matrix models, such as the one studied in Section 5, has not as strong theoretical basis as the one presented in this section for the one-matrix model. However the arguments presented here give a good intuition why the numerical bootstrap can work even in the multi-matrix model case. In the following sections we will demonstrate its viability empirically, by showing its numerical efficiency for a specific, “unsolvable” matrix model.

3.2 Classification of physical solution of quartic one-matrix model

In Fig 2, we saw that as we increase the allowed region converges to the analytic solution. One may ask whether the allowed region will ultimately exclude all other solutions as increases, or it will stabilize to a very tiny island which will not shrink further. The results of the current section will support the first of these options.

In this section, we will apply the positivity of resolvent to the one-matrix model with quartic potential

| (36) |

in order to fully classify all physical solutions. This is equivalent to solving the positivity condition of one-matrix bootstrap analytically. Since in the previous subsection we have already formulated this problem as a precise mathematical theorem, we will not present the formal mathematical derivation here. For the details the reader can refer to the Appendix B.

For the bootstrap problem we are trying to solve, we will not assume the symmetry of the solutions. This symmetry would mean . We will see that there exist solutions that break this symmetry. In fact, for solutions we find numerically the breakdown or preservation of symmetry will be established dynamically and not necessarily imposed as an input. Alternatively, if we assume symmetry from the beginning, the numerical efficiency for such solutions considerably increases.

For the specific potential (36) the positivity condition for the resolvent

| (37) |

translates into the condition that it has a only real positive eigenvalue distribution. This condition can be solve rigorously, namely:

-

1.

and : .

-

2.

and , there is no possible solution.

-

3.

and , there is no possible solution.

-

4.

and : .

-

5.

and : This situation is a bit involved. The bootstrap solution is a curve segment parametrized by . Explicitly, the solution is a branch of the algebraic equation:

(38) The physical branch of solution is selected by the one passing through ,151515Actually for and , the symmetry preserving solution is just . So the first discontinuity of at happens for second derivative. with .

For ,

(39) and for ,

(40)

This reproduces the exact solution of quartic one-matrix model. In Fig 2 we have already compared the exact solution and the numerical bootstrap result for . A typical comparison for case is Fig 3.

In Fig 3 we take a representative from each phase and compare it with the above analytic solutions. We see that the numerical bootstrap results converge quickly to the analytic result. A distinguishable feature of these figures is that the allowed region is not guaranteed to be convex. This is very different from the convex optimization problems which we encountered in CFT bootstrap and S-matrix bootstrap. Generally, the large-scale non-convex problem is hard and usually unsolvable. We will discuss in the next section how to overcome this difficulty.

3.3 Comments

Here we present several comments on the results of this section:

-

1.

There may exist certain doubts on particular choices of the positivity condition of the correlation matrix in numerical bootstrap. In the work 2017NuPhB.921..702A ; 2020JHEP…06..090L , the authors showed that in some cases one only needs the positivity of even moments to make bootstrap converging to the analytically known solution. But in general one should be careful about the choices of the positivity condition. For example, consider the model with . Under the assumption of the symmetry, the loop equations of this model read:

(41) We see that the positivity condition on even moments only provides us with the constraint , evident by induction in loop equations. In this situation we can bootstrap the physical solution only with the positivity condition on the full correlation matrix. This fact explains to some extent why the convergence in Fig 3 is not as fast as for the model with positive quadratic coefficient.

-

2.

For the one-matrix integral with integration over the unitary matrix instead of the Hermitian matrix, we can establish and justify a similar bootstrap method. This enables us with the analytic solution of such bootstrap problems. The main difference in this case comparing to the Hermitian integral is that the correlation matrix is of the form . It is called the Toeplitz matrix in linear algebra161616For the Hermitian integral the correlation matrix is of the form of the Hankel matrix.. For this correlation matrix, we have the following result of solution, this time for trigonometric moment problem:

For a given series of real numbers such that , there exists a positive Borel measure on such that:

(42) if and only if the matrix is positive semi-definite.

Applying this result to our unitary matrix integral, we come to the conclusion that the positivity of correlation matrix for large unitary matrix integral is equivalent to the positivity of the eigenvalue density which is supported on the unit circle in the complex plain.

4 Relaxation bootstrap method

Now we turn to the discussion of the bootstrap method for multi-matrix models. We will see that a naive generalization of the previous one-matrix model bootstrap will lead to a Non-linear SDP 171717SDP means semi-definite programming. But it is widely known that a general large-scale Non-linear SDP cannot be solved efficiently. In this section we will propose a systematic numerical bootstrap procedure to solve the large multi-matrix models via SDP.

SDP, unlike the Nonlinear-SDP which is directly applicable in the case of large matrix model bootstrap 2020JHEP…06..090L ; 2017NuPhB.921..702A , has a long history in academic research as well as in applied sciences. The standard primal form of SDP is181818There exists also the dual form of these problems, which will be discussed in Appendix C. We also note that in some literature different conventions for dual and primal for SDP are used.:

| (43) |

Here denotes the space of real symmetric matrices. As long as we can transform our bootstrap problem to the form (43), we can get rigorous bounds on the physical quantities of interest – linear functions of – by efficiently solving the SDP problem (43).

So the problem reduces to the question how to efficiently transform our matrix integral problem into the constraints of the form (43). Then the original physical problem is transformed into a purely numerical SDP problem.

In this section we will describe our relaxation bootstrap method on the example of single trace moments in a large two-matrix model with the partition function191919The generalization to multi-matrix models with more matrices is straightforward.:

| (44) |

where is assumed to be a so far general polynomial in and , to make the loop equations more tractable. In the next section we will apply it to a model with a concrete potential, generally unsolvable by the known analytic methods. We will see that our method has four types of constraints: loop equations, global symmetries, positivity of correlation matrix and positivity of relaxation matrix (which will be explained later).

4.1 Physical constraints

To make this section as self-contained as possible, we briefly review here the terminology already introduced in the previous sections and show how the constraints of the type (43) are specified in the two-matrix model.

The positivity of correlation matrix is still at the heart of our method. Since we are doing numerical analysis, we set the cutoff to the length of operators that we are considering, i.e. to the length of “words” built from two “letters” – the matrices and : . For any word of the length, we assume:

| (45) |

The set of words with length is a vector space spanned by all the words constructed from two letters with the length cutoff . This is a set of elements which we denote as , where runs from to . For example, when the basis of this vector space reads:

| (46) |

We can expand the equation (45) w.r.t. this base:

| (47) |

Let us introduce the correlation matrix which consists of expectation values of operators with the lengths up to . Since (45) is true for all operators, the condition (47) holds for all , i.e. the semi-definite positivity of correlation matrix is ensured:

| (48) |

This correlation matrix condition can be directly applied to the two-matrix model. We see that the main difference with the one-matrix model is that the dimension of correlation matrix grows exponentially with .

Another important ingredient for our bootstrap method is the loop equations. For the two-matrix model it can be schematically represented as:

| (49) |

where “Word” means the matrix word built by arbitrary finite product of matrices and . 202020Note that “word” is not yet traced, so that generically it is not cyclically symmetric: a cyclic transformation gives in general a new word. The differentiation can be either w.r.t. the matrix or w.r.t. the matrix .

The loop equations for large multi-matrix model in general close on all words.212121Here we mean that there is generally no infinite subset of loop equations and operators closed among themselves. This fact will be explored further in Section F. Schematically, they have the following quadratic form:

| (50) |

which is a direct generalization of (13) of the one-matrix model. Here are the words obtained by cutting the word in two words whenever one has the matrix on the -th place in . The matrix factor in the l.h.s. comes from the derivative of the exponential factor in (49), which generically renders a sum over single trace operators with lengths from to (the degree of polynomial is assumed to be ). So we expect that a loop equation of length involves quadratic relations of operators with lengths up to . In the next section we will precise all these steps on a particular example of the two-matrix model.

The set of all loop equations can be efficiently generated by applying the derivatives in to any word of the length less than a certain cutoff222222We will discuss the detail of the choice of the cutoff in the Appendix D.. However, the loop equations obtained in this way are not all independent, which means that there may exist linear dependence and/or algebraic dependence among them. It turns out that these redundancies are numerically crucial when applying the SDP solver to the constraints of our system, but they are not important at this stage of explanation. We will discuss these technicalities in Appendix D.

If the model has some discrete symmetries, such as or , it is not necessary to assume them from the beginning in our bootstrap scheme, but factoring it out will significantly increase our numerical efficiency if we are only interested in the symmetry preserving solution. Generally, the symmetry assumptions not only simplify the loop equation by reducing the number of operators232323For example, if the potential has symmetry , we could identify all the operators identical by transformation. but in certain cases they make the correlation matrix block diagonal, thus greatly simplifying our problem. We will encounter this situation in the next section for a concrete model.

At last, we identify all the operators related by cyclicity of trace and the reversion of the word. These transformations also reduce considerably the number of unknowns in our scheme.

In summary, for the two-matrix integral (44), assuming the global symmetries or not, we set up all the physical constraints. A natural question is what is the solution of these constraints. But this is not a good question since generally, apart from some solvable models where the loop equations close on a very limited subclass of operators (like in a two-matrix model Kazakov:1989bc ; Staudacher:1993xy or some -matrix models Kazakov:1987qg ; Daul:1994qy ; Kostov:1988fy ), the number of operators grows faster than the number of constraints, which means that the solution is a region in an extremely high dimensional space. A constructive question at this stage is: given a cutoff to the length , what is the minimal or maximal possible value of a physical quantity? This amounts to asking what is the allowed interval when the region allowed by the constraints is projected on the linear subspace corresponding to the specific physical quantity.

Rephrasing it in the language of optimization theory, we deal with the problem of the form:

| minimize | (51) | |||

| subject to | ||||

| and |

where is a vector defining the dynamical quantity we want to optimize and is the column vector of all our operator expectations , up to the length . The quadratic loop equation (in the middle) is written in the vector form, where is the quadratic form encountered in the th equation; linear and constant terms are represented accordingly. The matrix inequality is the expansion of the correlation matrix in terms of the operator expectations. This is certainly not equivalent to the standard SDP which we introduced by (43) since the quadratic equations represent non-convex conditions. One of the conventional methods to deal with it is relaxation.

4.2 Relaxation matrix

The constraints discussed in the last section define a problem which is called Non-Linear SDP in optimization theory. There are indeed some solvers specialized for it but, from our limited trials, they are not mature enough to solve large-scale problems such as the ones we encountered in matrix bootstrap. To improve the situation, we propose to modify the problem (51) by relaxing the non-convex conditions involving the non-linear loop equations, into convex ones. Our intuition here is that we don’t really need all of the loop equation constraints for our bootstrap method to converge as increases.

To see how our method works, let us begin with a simple example which will provide us with a heuristic argument. Suppose we have only three quadratic “loop equations”:

| (52) |

Here denote linear combinations of some other variables . These equations are of course non-convex. But we can relax them to make them convex by replacing with or, in the positive semi-definite matrix form,

| (53) |

We can do the same thing with the second equation , to relax it to a convex condition. But the same operation cannot be reproduced for equation , since neither nor is convex 242424Because the bilinear form is not positive semi-definite.. It is tempting to consider the positive semi-definite combinations:

| (54) |

It is not very elegant to implement (54) by introducing extra parameters like , although numerically this is viable. Can we write instead of (54) a condition that does not contains explicitly ? In fact yes. Since , we only need the discriminant of (54) w.r.t. to be non-positive, to exclude the existence of real solution for when (54) becomes an equality. That means

| (55) |

is equivalent to (54) for all . In its turn, it is equivalent to:

| (56) |

Combining (53) and (56) we come to the conclusion that:

| (57) |

This is mathematically more elegant and numerically more efficient.

To apply this relaxation method to the case of our loop equations is a simple generalization of what we just proposed. We make in the loop equation the substitution , or in matrix notations:

| (58) |

where again is the column vector whose components are . Formally, this changes the loop equations in (51) to a linear form:

| (59) |

To apply the relaxation method sketched above, we relax (58) by imposing the inequality:

| (60) |

which is equivalent to:

| (61) |

By Schur’s complement, this can be re-arranged into a more compact form:

| (62) |

Here we introduced the relaxation matrix by and . This step concludes our translation of the nonlinear bootstrap problem into an SDP. This SDP takes now a numerically much more tractable, convex form:

| minimize | (63) | |||

| such that | ||||

| and | ||||

| and |

It has now two types of variables to bootstrap: a column vector variable and a symmetric matrix variable .

Several comments are in order:

-

•

One of the primary questions to the method is: does the relaxed SDP generate the same bounds as the previous Non-linear SDP problem? Generally, the answer is “no”. It is obvious that when the optimal solution of the relaxed problem satisfies the constraint of the original problem the relaxed problem will generate the same bound as the original one. From our experience, this is not the case for any finite . 252525More precisely, if the relaxation is saturated for the optimal solution, we expect that the relaxation matrix will only have one non-zero eigenvalue. But practically, we always observe multiple non-zero eigenvalues for the relaxation matrix. But as we increase the cutoff , the mismatches for the quadratic conditions are tending to zero. So we are tempted to believe that for infinite , the relaxed problem and the original problem give the same result for most of the questions we are interested in. This indicates that the non-linear constraints in the loop equations are somehow contained in the positivity conditions for correlation matrix and relaxation matrix.

-

•

One can regard our relaxation scheme as a numerical compromise: doing relaxation we replace the nonlinear equalities by linear inequalities but we can thus explore the correlation matrices of a much higher order since we can significantly increase the length cutoff . This enable us to embrace more information from correlation matrix. Our numerical results in the next section will show that this is a worthy trade-off.

-

•

There is another point of view on our relaxation formulation (63). The problem (63) is actually the dual of the dual of the problem of (51). Although this fact is in principle simple to show its proof is quite lengthy, so we put it into the Appendix C. In that appendix, we also briefly review the definition and basic facts about the dual formulation. As it is known, the dual problem of any general optimization problem is always convex boyd_vandenberghe_2004 , so the double dual is guaranteed to be convex. In some sense, this point of view is more general and universal.

-

•

We believe that the key condition for the relaxation method to work well is that, under our bootstrap assumption, there is a unique exact solution.262626Here exact solution means bootstrap solution with infinite cutoff. Then since a single point (corresponding to the solution of bootstrap) is convex, our relaxation procedure leading to convex constraints will not make the results too different even for a finite but sufficiently large . However, we observed in Section 3.2 that the set of exact solutions may become non-convex in the presence of a symmetry breaking. In such situation, we need further assumptions to make the exact solution unique. We will further discuss these aspects in the next section when bootstrapping the symmetry breaking solutions.

5 Bootstrap for “unsolvable” two-matrix model with interaction

In this section, we implement the relaxation bootstrap method described in the previous section to the case of generically unsolvable large two-matrix model:

| (64) |

where the integration goes over Hermitian matrices and . This model is unsolvable analytically for generic parameters and , at least with the known methods, such as reduction to eigenvalues or the character expansion. It is still analytically solvable for some particular values: for it can be reduced to a specific one-matrix model and solved via saddle point method or via the reduction to a KP equation 1982PhDT……..32H ; 1999NuPhB.557..413K ; for it reduces to two decoupled one-matrix models; for we have and it reduces again explicitly to another eigenvalue problem. These particular solvable cases are useful to test the power of our numerical method.

The present section is organized as follows: The bootstrap results for the model (64) with particular choice of parameters (which represent a generic analytically "unsolvable" example) are shown in Section 5.1. Then in Section 5.2 we compare the bootstrap result for the analytically solvable cases or with the corresponding analytic solution, to test our method. In Section 5.3, we explore the phase diagram of the this model and make several comments about the convergence rate in different regions. At last, in Section 5.4, we investigate the symmetry breaking in the model by our relaxation bootstrap method.

5.1 Bootstrap solution for a generic choice of

In this subsection, we present the results of the bootstrap for the model (64) where we specify, for definiteness, the parameters: . We stress that this choice has nothing specific for the properties of the model and it is made mostly for the demonstrative reasons, as an example of generic values of parameters. The method appears to be very efficient almost everywhere in the physical domain of parameters , except when we approach the critical lines where it is less efficient. We will discuss in the next subsection the phase structure of the model in the plane.

The symmetry of this model can be described by the Dihedral Group 272727Actually we implicitly assume the which basically means that all the moments are real. We will assume throughout this paper that this symmetry cannot be broken. At least intuitively, this is unlikely to happen in our model 64. , with generator:

| (65) |

We saw already on the example of the one matrix model that in the large limit there could be a multitude of saddle point solutions, many of them breaking this kind of symmetries. We begin with the study of symmetric large solutions. Later we will discuss the solutions with broken symmetries as well.

In the fully symmetric solutions, only the operators with even number of and even number of can be non-vanishing, and we should identify the operators under the exchange . Obviously this assumption of symmetry of solution is in principle not necessary for our bootstrap method to work. However, assuming this symmetry we gain a lot in the efficiency since we are left with approximately of operators comparing to a general non-symmetric setup. It also happens that the symmetry assumption simplifies the correlation matrix by much. Namely, when constructing the correlation matrix, only the words with the same parity in both and can appear in the inner product for a non-vanishing correlator. So our correlation matrix break into 4 block-diagonal matrices, corresponding to parities in and : even-even, even-odd, odd-even, odd-odd. By symmetry, the even-odd and odd-even blocks are actually the same. So the original correlation matrix can be reduced to three block diagonal matrices: even-even, even-odd, and odd-even.

Here we bootstrap the allowed region for the first two non-vanishing operators , 282828Here we give up the notation for the moments we used in one-matrix model since for two-matrix model the moments cannot be characterize by a single positive number.. According to (63), this corresponds to setting the objective function of the optimization problem as:

| (66) |

Scanning it in the interval we can fix the allowed region for these two operators. Using the general method described in the last section we can use the SDP solvers to solve these problem. The readers interested in the details of the implementation can refer to the Appendix D, where we gather all the technical detail of numerical implementations. We also demonstrated in Appendix E our numerical procedure explicitly, step by step, on the example of the system with cutoff.

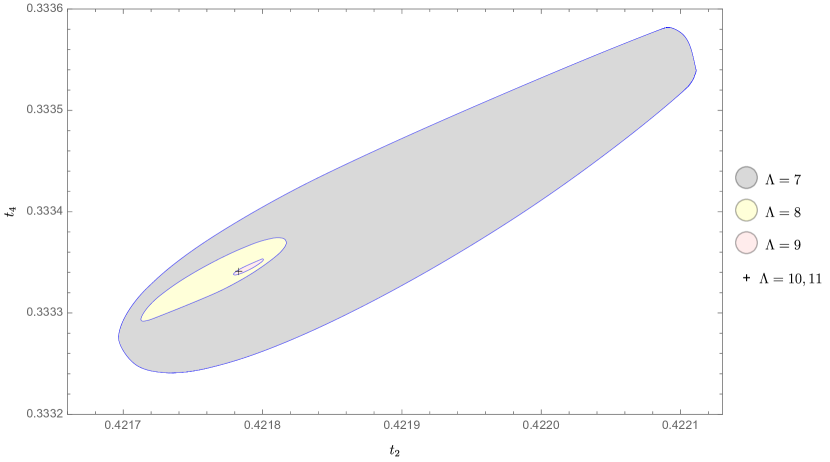

Let us demonstrate our results for various values of the length cutoff . We summarized the allowed regions for the first two correlators and in Fig 4. The regions for and are too small to be plotted on the figure, so we give here the upper and lower bound of and . For :

| (67) |

and for :

| (68) |

We see here that for we already have a six digits precision at . The calculation is the largest problem in this work, it is done with SDPA-dd, a solver in SDPA family with the double-double float type. The input to SDPA has variables, with the correlation matrix size: even-even , odd-odd , even-odd , and with relaxation matrix size . We note that this is still within the capability of a single laptop, it only takes CPU time for a single maximization cycle. We also stress that these inequalities, unlike the Monte Carlo methods, are exact: increasing the cutoff we can only improve the margins.

5.2 Demonstration for analytically solvable cases

It is instructive to apply our numerical method to the analytically solvable cases or , which is a good check for our approach, convincing us that it works well indeed even for the generic parameters, where we have no analytic data to compare with. In this part we will firstly review the analytic solution for both cases and then compare it with the numerical results of our relaxation bootstrap method.

As we mentioned, for this model reduces to two decoupled one-matrix models – the case which we already discussed and studied analytically in Section 3.2. Integrating out one of the decoupled matrices, we expect the operator containing only one matrix to have exactly the same expectation value as for the result in Section 3.2:

| (69) |

For , this model is already solved analytically in 1982PhDT……..32H ; 1999NuPhB.557..413K . Here we simply present the analytic solution derived there in our notations and normalization. To have a compact form, we introduce the short-hand notations , , , where K and E are the complete elliptic integrals of first and second kind:

| (70) |

We introduce the new parameter related with by:

| (71) |

and we can express as:

| (72) |

This formula is valid when . For , we need to analytically continue the solution to the other sheet of Riemann surface of the variable . For that we introduce the analytic continuation of the elliptical integral and :

| (73) |

To make (71) and (72) valid for , we simply replace all the by .

The critical point of the smallest possible for can be defined as the solution of the equation292929We thank Nikolay Gromov for sharing with us his computation of .:

| (74) |

which can be numerically solved as:

| (75) |

The comparison of our numerical results with analytic result is presented on Fig 5 and Fig 6. Indeed, we see that our numerical results nicely agree with the analytic formula (69) and (72). An apparent feature of these plots is that when or , the allowed region is much larger than the one for the positive coupling case, thus giving less of precision. In general we have the worst convergence in the neighborhood of critical value. We will discuss this feature in more details in the next subsection.

There is another fact which is not obvious from the Fig 5. If we compare this figure with Fig 2 in Section 2 we will find that for same values of , the non-relaxed one-matrix bootstrap bound for (denoted by in that section) and our relaxation bootstrap bound for case of the 2-matrix model actually coincides within the error bar. This is a very striking feature of our relaxation method since we relaxed all the quadratic equalities to inequalities but we compensated this with many more mixed operators of two decoupled matrices. So the correlation matrix is much larger in the relaxed case and the final results are basically the same. We will see this feature of relaxation again when we discuss later the bootstrapping of the symmetry breaking solutions. We don’t have a very clear explanation for these phenomena in general.

5.3 Phase Diagram and convergence rate

In this part, we will discuss the phase diagram of the matrix model (64) and the corresponding convergence rate in different regions of the diagram.

In general, for finite matrix integral the potential must be bounded from below to define a sensible integral over Hermitian matrices. But this is not necessary for a large theory, where we only need deep enough local minima to have a stable saddle point solution. Even for the unstable potentials, the tunnelling effects between the local minima, or to the infinity are suppressed exponentially. We saw this in Section 5.2, where the bootstrap procedure allowed the existence of solutions with negative values of and . This provides us with a possibility to study the boundaries of possible and values (we will call the region of possible and values the feasible region in the following) even when the corresponding potential is not bounded from below.

Before going deeper into the technicalities of bootstrapping the boundaries of the feasible region, we can get a rough estimate of them by deriving the parameter region of and which leads to the matrix potential bounded from below. It is obvious that the domain is one part of the region we are looking for. Another, less obvious part is , as in this case we should have:

| (76) |

The union of these two domains represents the maximal region where the matrix potential is bounded from below, since for and we can always find configurations where the potential is not bounded from below. For , one of these configurations is taking and . For , we simply put and to be some constants times generalized Pauli matrices of dimension and , where is a large real number. Then we have:

| (77) |

This must be unbounded from below when .

In conclusion, the region of potential bounded from below is . In addition, the domain is guaranteed to lie within the feasible region. But due to the large effects, we expect the feasible region to be a little bigger than that. Specifically, for analytically solvable cases, when we have and when we have . These facts give us an additional information about the location of the boundary of the feasible region.

To numerically bootstrap the boundary of the feasible region, we can obtain the critical boundary between the allowed and forbidden parameter regions by bisection. Namely, for a given we fix and take two values of , as and . Here is a point that is guaranteed to be forbidden for a given , and is a point that is guaranteed to be allowed. Then we test the geometric average value . If is allowed, then we make the substitution , otherwise we take . In this way we can recursively approach the maximal forbidden value of at fixed . Then we scan over the values of and get the plot shown in Fig 7.

Some explanations for the plot Fig 7 are in order. The gray region is rigorously forbidden as the result of bootstrap at . On the contrary, the white region is not guaranteed to be allowed for any physical large solution. As we increase , the gray region will expand a little. But we have several hints about the position of the exact boundary line:

-

•

We notice the red and green dots on the plot, which are the critical points of the analytic solutions. They are located on the exact boundary of feasible region, i.e. no matter how large is , the gray curve cannot go beyond these two points. From this fact we convince ourselves that our numerical curve in Fig 7 is already very accurate, since the red dot and the green dot are very close to the gray curve.

-

•

The blue region is the region where the potential is strictly bounded from below. It is enclosed by the lines and . Its boundary can be considered as the exact solution in the “classical” limit for this matrix integral, where is the coefficient put in front of the potential. In this case we scale the couplings as . The boundary of the gray will coincide for with the boundary of the blue area on Fig 7. Then inside the blue area we have a well-defined theory even for finite . At large and finite there is a gap between blue region and gray region, as is visible on the Fig 7.

5.3.1 Rate of convergence

As the reader may have noticed already in Section 5.2, when or the convergence is very bad compared to the case and . From our experience, this is a generic situation when we are outside of the blue region in Fig 7, which is defined by the region of parameters yielding a potential bounded from below. For example, Fig 8 depicts the allowed region for when we fix and scan over in the neighborhood of . It is clear from this figure that for there is drop in the rate of convergence. Actually, from numerical data, the difference of the upper bound and the lower bound varies between the orders of magnitude from to around when varies from to .

Nonetheless we can get a rather accurate estimate of physical quantities in the region discussed in the last paragraph. We note that in Fig 5 and Fig 6, the analytic solution is very close to the lower bound, comparing to the upper bound303030We believe that the upper bound and the lower bound converge to the same value, but it seems they have rather different convergence behaviors. . Actually, as we increase , the lower bound stabilizes already at rather small . Empirically this is a typical behavior in the unbounded region. Under the assumption that there is a unique solution satisfying the constraint for arbitrarily large , we expect that the optimization results for the maximum and the minimum of will ultimately converge with increasing to the same value. This has been proven for some parameters of the one-matrix model in Section 3.2, and we have strong numerical evidence to believe it will hold for our model (64) as well. So we can simply bootstrap the physical quantities by the minimization of in this region (in the following, we will call this procedure the minimization scheme as opposed to the maximization scheme). Comparing it to the analytically solvable particular cases we learned that this method can yield especially accurate estimate of physical quantities. However, we lost the rigorous margin in the region with good convergence (blue region in Fig 7). 313131This situation is similar to that of the early days of conformal bootstrap when people used the kink of a plot to estimate the dimension of operators in the Ising model, c.f. ElShowk:2012ht

There exists a region in the phase diagram Fig 7 where the bootstrap is valid only for very high cutoff : it is . The Fig 9 shows the allowed region when we fix and vary . For the lower bound of pink region , there are some numerical instabilities for . From careful inspection of our data at various values of it seems that the lower bound at should stabilize in this region at the value if no numerical instabilities happened in our SDP solver. We notice a few very distinguishable features of this plot:

-

1.

For a fixed , there is a region where is slightly larger than and not bounded from above. In other words, the dual SPD problem for the upper bound is infeasible. In this bad region of parameter space, the bootstrap with such essentially tells us nothing about the right physical values. Luckily, the “bad” region is shrinking when we increase , and hopefully it will disappear when we have a high enough cutoff.

-

2.

As already stated in the last paragraph, when we are not in the “bad region”, the minimization scheme converges much faster than the maximization scheme. So for a reasonable estimate of the operator expectation we should privilege the minimization scheme.

-

3.

We also notice that for the region , the convergence is excellent as expected, but there is a huge drop in the rate of convergence in the neighborhood of .

5.4 Bootstrapping the symmetry breaking solution

In the previous parts of this section, we always assumed the global symmetry, or in other words, we bootstrapped the symmetry preserving solutions. Here in the following, we will make the first attempt to study the symmetry breaking solutions with our relaxation bootstrap method. Consequently, in this subsection we will not make assumptions on a specific global symmetry of operator expectations. For example, we will assume that it is possible to have:

| (78) |

and any other nonzero expectations containing odd number of letter or , unlike the solutions with such symmetry.

To understand the general features of symmetry breaking solutions, Fig 3 in Section 3.2 is a good source for our intuition. We see on that figure that the exact solution is not unique anymore but there is rather a continuous family of solutions parametrized by . This is a non-convex set of exact solutions, so we don’t expect that our relaxation bootstrap method, as applied in the case of Fig 4, will converge to such a non-convex set as increases. Namely, if we impose the relaxation bootstrap constraint without the assumption of symmetry, then minimize the value of

| (79) |

and then scan over in , we expect to get a convex set instead of the non-convex one, due to the convex nature of the relaxation method.

So to bootstrap the symmetry breaking solutions, new techniques are needed to tackle the non-convexity. We will describe the general method for bootstrapping solutions and then we apply it to the study of our model (64).

5.4.1 Schemes for symmetry breaking bootstrap

The main problems in the study of symmetry breaking solutions in the multi-matrix model of the type considered here are:

-

1.

How to identify the range of parameters for which the model has a possible symmetry breaking solution?

-

2.

How to numerically bootstrap the symmetry breaking solution?

The answer to the first problem is quiet straightforward. We can establish the relaxed constraint without the symmetry assumption, and bootstrap a dynamical quantity which signals the symmetry breaking. For example, for the symmetry breaking solution we take the objective function ( in (63)) as:

| (80) |

and for the symmetry breaking we take the objective function as323232Here in these two situations the dynamical quantity signaling the symmetry breaking is respectively and .:

| (81) |

If the bound of the symmetry breaking expectation is significantly larger than the error bar at the current for a given value of parameters, we believe that this is a strong signal of existence of a symmetry breaking solution.

For the second problem, we propose to transform the non-convex set of exact solutions to a convex one, which means that for the case of Fig 3 we fix by in our bootstrap procedure. For this particular value of we should have at infinite cutoff a unique exact solution for and for other higher moments, which is definitely a convex set. Therefore our relaxation bootstrap method with a finite cutoff will yield a rigorous upper bound and lower bound for . Next we scan over until such values that the problem becomes infeasible. In this way we get the allowed region in plane.

The above method is easily generalizable to the problem of bootstrapping solutions with the other symmetry breaking patterns. Namely, we establish the bootstrap scheme by fixing the dynamical quantity signaling the symmetry breaking, and then we bootstrap the quantities we are interested in. At this step, we expect that after fixing such dynamical quantity, the exact solution of the bootstrap problem is unique. At the next step, we scan over all possible values of the quantity which was fixed in the previous step. In this way we can bootstrap a non-convex set of solutions.

There is another possibile solution for the first problem, i.e. to locate the symmetry breaking region. We can assign to the dynamical quantity signaling the symmetry breaking a specific value and then use the method similar to that of Section 5.3, i.e. using a bisection to approach the maximal possible value of expectation signaling the symmetry breaking. In principle this bisection method could have given us a tighter bound than our initially proposed method. However, from our test, the two methods yield basically the same numerical result, so we will not bother to use the bisection method in what follows.

5.4.2 Numerical results for symmetry breaking solution

Here we apply the method proposed above to the model (64). Our results in this part concern the breaking of the following symmetries:

| (82) |

and

| (83) |

In the bootstrap setup, we don’t impose the global symmetry assumptions for the corresponding symmetries, i.e. that the non-singlet operator expectations of the symmetry vanish. Then we pick up the dynamical quantities signaling the symmetry breaking as:

| (84) |

and

| (85) |

respectively and set them as the objective functions in the corresponding bootstrap problem.

As the result, in the feasible region of Fig 7 we didn’t find any evidence of the existence of a symmetry breaking solution for the model (64). We tried several points in different regions of Fig 7. The results show that the maximized values are always lying within the error bar (typically and , depending on the cutoff and the parameters and ). In particular, for and some generic values of and , we have:

| (86) |

We believe this to be a strong evidence that the two symmetries we investigated are not spontaneously broken for all the regions in Fig 7.

Some other interesting facts:

-

1.

For , i.e. when the quartic coefficient vanishes, the preservation of symmetry is automatic from the loop equation. This fact provides us with the intuition that the commutator square interaction is to some extent not a symmetry-breaking interaction. Regarding that at the model is not in symmetry breaking phase, since it reduces to two decoupled one-matrix models, intuitively it points on the absence of symmetry breaking phase the for model (64) (with positive coefficients in front of quadratic terms).

-

2.

For the region and slightly smaller than zero, we have a very large upper bound for the exposed quantities, sometimes of order , which might signal the symmetry breaking. But we note that the bootstrap convergence is really bad in this region where some bootstrap results for symmetry preserving solution are presented on Fig 9, and the error bar here is almost infinitely big. So we believe this cannot be a reliable evidence that there a symmetry breaking takes place in this region.

As we don’t find evidence for the existence of symmetry breaking solutions for the model (64), we consider the same model but with negative coefficients in front of quadratic terms:

| (87) |

We know from the Section 3.2 that for where we have just two decoupled one-matrix models, we have a symmetry breaking phase for . At such values of we can test our method for bootstrapping the symmetry breaking solutions.

In Fig 10 we compare the results of our relaxation method described above with the exact results and the one-matrix bootstrap plot at the same cutoff and the parameters . We see that our method is indeed able to bootstrap the symmetry breaking solution, even though it is non-convex. It is especially striking that not only our relaxation method converges to the highly non-convex exact solution, but it even coincides with the one-matrix bootstrap at each cutoff within the error bars. It seems that, in spite of some loss of information when applying the relaxation method, we recover this information by considering the positivity condition of the mixed operators containing both matrices, such as . We don’t have yet a good explanation why these two approaches give equal or very close results. We also note that in this case the maximization scheme converges faster than the minimization scheme. Namely, the upper bound (green dots) in the plot is much closer to the exact solution than the lower bound (red dots). This suggests that if we are looking for a good approximation for the exact solution, we should use the upper bound solution as the best approximation.

For generic values of and for the model (87), the convergence is slower than in the analytically solvable particular case. It would be good to understand whether such a situation for solvable versus unsolvable models is typical. In Fig 11 we plot the bootstrap result for . Obviously, it is still a symmetry breaking solution. We expect that taking the upper bound we can get a very accurate estimation of the physical quantities. We didn’t try to further increase the value of , being already satisfied to see that the proposed method works for rather generic values of parameters.

6 Conclusion and discussion

In this work, we develop further the matrix bootstrap method pioneered in the papers 2017NuPhB.921..702A ; 2020JHEP…06..090L and propose a crucial improvement – the relaxation procedure – applicable to a large class of multi-matrix problems and allowing to bootstrap them with a much higher precision. The relaxation transforms a Non-linear SDP, with the non-linearity due to the structure of loop equations, to the usual, linear SDP. We demonstrate the efficiency of our approach on the analytically unsolvable two-matrix model and establish its phase structure with rather high precision. The method appears to work well even for the discrete symmetry breaking large solutions.