empty

Weighted asymmetric least squares regression with fixed-effects

Abstract

The fixed-effects model estimates the regressor effects on the mean of the response, which is inadequate to summarize the variable relationships in the presence of heteroscedasticity. In this paper, we adapt the asymmetric least squares (expectile) regression to the fixed-effects model and propose a new model: expectile regression with fixed-effects The model applies the within transformation strategy to concentrate out the incidental parameter and estimates the regressor effects on the expectiles of the response distribution. The model captures the data heteroscedasticity and eliminates any bias resulting from the correlation between the regressors and the omitted factors. We derive the asymptotic properties of the estimators and suggest robust estimators of its covariance matrix. Our simulations show that the estimator is unbiased and outperforms its competitors. Our real data analysis shows its ability to capture data heteroscedasticity (see our R package, github.com/AmBarry/erfe).

Keywords: Expectile regression, quantile regression, fixed-effects, within-transformation, endogenous model, panel data.

1 Introduction

The fixed-effects model is commonly used in econometric to analyze panel data. The model has the ability to account for the correlation between the regressors and the omitted (unmeasured) factors which is common in many applications. For example, in econometrics, the education level is known to be correlated with the individual unobserved ability (Card,, 2001). In perinatal studies, the birth weight is influenced by maternal genetic (Warrington et al.,, 2019), which is usually a missing information. Therefore, in such context—where the unmeasured factors are correlated with the regressors, the estimator (within-estimator) is unbiased, consistent and computationally efficient (Cornwell and Rupert,, 1988).

Several quantile regression -based methods (Koenker,, 2004; Galvao and Montes-Rojas,, 2010; Lamarche,, 2010) have been proposed to overcome the heteroscedasticity problem in the framework. However, they fail to extend the favorable properties of the within-estimator and suffer from two significant limitations. First, the fixed-effects -based methods do not extend the within-transformation strategy to solve the incidental parameter problem. Thus, the fixed-effects -based methods simultaneously estimate the parameter of interest and the incidental parameter which results in a computationally demanding algorithm. Additionally, the covariance of the -based methods is based on the random error density function which further adds a computational burden and certain numerical issues (Chen et al.,, 2004; Yin and Cai,, 2005; Kocherginsky et al.,, 2005). Second, the fixed-effects -based method do not control for the correlation between the individual effects and the regressors. Thus, in the presence of such correlations, the fixed-effects -based method yields biased and inconsistent estimates.

In this paper, we rely on expectiles to successfully generalize the within-estimator and take into account the heteroscedasticity present in the panel data under the framework. To the best of our knowledge, this is the first approach that estimates the marginal effect of the regressors on the response distribution, and generalizes the within transformation strategy in the framework.

The expectiles are statistics that characterize the distribution function of a random variable (Girard et al.,, 2021). The expectiles and the expectile regression were introduced in the seminal paper by Newey and Powell, (1987). The expectiles and quantiles play similar statistical roles, except that expectiles are weighted averages while quantiles are order statistics. This interpretation difference offers significant computational advantages. In other words, quantiles focus on the ordering of the observations while the expectiles target their values. For instance, the mean is a particular expectile as the median is a particular quantile. The research on expectiles is very active and for further details we refer to Barry et al., (2020).

Typically quantiles are more robust than expectiles, but as mentioned earlier, the proposed -based fixed-effects models can not extend the within transformation strategy to solve the computational challenges raised by the incidental parameter problem efficiently. Further, the -based fixed-effects models fail to control for the correlation between the individual effects and the regressors. Therefore, the expectile-based approach could be an effective alternative for inference in the framework.

In this paper, we combine the weighted asymmetric least squares regression and the model to propose a new panel model that we call: expectile regression for fixed-effects model The model retains the attractive properties of the model, while accounting for the heteroskedasticity present in the panel data. We derive its asymptotic properties and propose a heterogeneous, consistent, and robust estimator of its variance-covariance matrix. We share our code as a free R package available on GitHub (github.com/AmBarry/erfe) to simplify its implementation.

Our main contributions are: i. Extension of the within-transformation strategy in the framework to solve the incidental parameter problem, offering a significant computational advantage particularly with the advent of high dimensional data, where the sample size can be very large; ii. Elimination of any bias that might result from the correlation between the individual effects and the regressors; iii. Derivation of the asymptotic properties of the estimators; iv. Proposition of an estimator of its variance-covariance matrix for inference.

Our model accounts for the omitted time-invariant factors and their correlation with the regressors present in the model. It also captures the heteroskedasticity present in the panel data by estimating the effects of the regressors at the conditional expectiles of the response distribution. Indeed, in the presence of heteroskedasticity, the parameters of the model are function of the asymmetric points, and in this case the model captures the heteroskedasticity by estimating several regression coefficient vectors at different locations of the conditional response distribution. The model provides a detailed overview of the regressor effects on the response distribution without making any assumption about the random error distribution. Our model is computationally efficient and easy to implement, with its available R package. We believe that it will be a useful tool for addressing the heteroskedasticity present in the panel data.

In Section 2, we introduce the expectile function and the expectile regression model, and then present the expectile regression with fixed-effects (ERFE) model. In Section 3, we derive the asymptotic properties of the ERFE estimator, and propose an estimator of its variance-covariance (VC) matrix. We present the sample performance of the ERFE estimator in Section 4 and its application to a real dataset in Section 5. The conclusions is in Section 6 and detail of the proofs are in the Supplementary material.

2 Models and Methods

2.1 Expectile and expectile regression

The expectile of level of a random variable is defined as the unique solution of

| (1) |

where is the asymmetric square loss function that assigns weights and to positive and negative deviations, respectively.

The expectiles summarize the cumulative distribution function of a random variable. In this regard, the expectiles play a similar statistical role to the quantiles, except that quantiles are order statistics while expectiles are weighted averages, and this interpretation difference is accompanied by significant computational advantages. The expectiles generalize the mean which corresponds to the expectile of level and assigns the same weight to positive and negative deviations. The expectiles are location and scale equivariant, that is for A detailed study of the expectiles can be found in (Newey and Powell,, 1987).

Once the optimization problem of equation (1) is solved, for a fixed the expectile of the random variable can be defined as a weighted average:

where is the check function. The only subtlety is that the weights are random. Given a random sample, the corresponding -th sample expectile

| (2) |

is the weighted mean, where the weights depend on the sample data. For a fixed equation (2) is derived as the solution which minimizes the following empirical risk function:

| (3) |

In addition to the expectiles, Newey and Powell, (1987) introduced the expectile linear regression as a tool to study the regressor effects on the response distribution and capture the heteroscedasticity present in the data. Consider the following linear regression model

| (4) |

where is a vector of regressors, and are respectively the response variable and the random error with unspecified distribution function. The parameter of interest is unknown and needs to be estimated. The assumption, ensures that the random error is centered on the -th expectile. The corresponding model, for a fixed is given as:

| (5) |

Therefore, the estimator for a fixed can be derived by minimizing the following objective function:

over Since the loss function is continuously differentiable, we have through the first order condition:

| (6) |

where is the check function. The estimator can be computed as an iterated weighted least squares estimators. For the special case of is the classical ordinary least squares (OLS) estimator and this makes the a natural complement of the OLS regression.

2.2 Fixed-effects model for panel data

Consider the standard linear fixed-effects model for panel data

| (7) |

where is the scalar response variable, the vector is the vector of regressors measured on subject at time the parameter is the subject-specific effects parameter, and the variable is a random error with unspecified distribution function. The equation model (7) is conveniently represented in individual notation as:

| (8) |

where are vectors, is an design matrix and is an incidence matrix and is an subject-specific effects vector. We can also stack all the data and represent the equation model (8) as:

| (9) |

where and are vectors, and are respectively and matrices with The incidence matrix identifies the distinct subjects of the sample.

The fixed-effects of model equation (9) is infinite in nature and is potentially correlated with the regressors of the model. The traditional estimation method used to overcome this issue is the within-transformation strategy. This technique consists of pre-multiplying both sides of equation model (9) by the idempotent matrix to eliminate the infinite-dimensional parameter, and then applies the ordinary least squares (OLS) regression to the transformed data. The model that results from this transformation is represented as:

| (10) |

where and are defined similarly. The OLS estimator of the fixed-effects model, known as the within-transformation estimator, is given as:

| (11) |

The within-transformation estimator is consistent and asymptotically normally distributed (Greene,, 2011). The within-transformation estimator is computationally efficient and is not affected by any bias resulting from the correlation between the individual effects and the regressors. The within-transformation technique does not allow estimation of the time-invariant regressors which could be seen as a limitation. However, this can be a strength when the number of time-invariant confounders is large, and when the collection of some of these variables (genetic factor) is complex and costly (Brüderl and Ludwig,, 2014). In the following subsection, we present the expectile regression for fixed-effects model and derive the iterative-within-transformation estimator.

2.3 ERFE model for panel data

The model of the linear fixed-effects model is defined, for fixed as:

| (12) |

In this setting the parameter captures the influence of the regressors on the location, scale, and shape of the conditional distribution of the response variable The subject-specific effects is assumed to be independent of across the percentiles and to have a pure location-shift effect on the conditional expectile of the response. Assuming a -dependency of the subject-specific effects implies estimating its distribution with number of within-subject observations, which is relatively small in most applications. Take note that no assumption is made about the shape of the response distribution.

The corresponding estimator of model equation (12) is defined as the vector minimizing the following objective function:

| (13) |

Since the loss function is continuously differentiable, we can apply the first-order condition and derive the resulting estimator , which is defined as:

| (14) |

where the diagonal check function matrix is:

| (15) |

The projection matrix and its complement are idempotent matrices and are defined as:

The function defined in equation (15) depends on the subject-specific parameter estimator which, by the first-order condition of equation (13), verifies the relationship:

| (16) |

Now, using equation (16), the argument of the check function matrix can be written as

| (17) |

Therefore, the incidental parameter estimate is eliminated from the expression of equation (14) of the estimator. Now, using the following relationship:

and the idempotent property of the projection matrix we can rewrite the estimator as:

| (18) |

In summary, the within-estimator is extended to the framework. The strategy is derived by applying the projection matrix to the initial data to eliminate the subject-specific effects parameter. Additionally, like the estimator in equation (6), the within estimator can be computed iteratively using the iterative weighted least squares algorithm. The detailed algorithm for computing the iterative-within-transformation estimator is summarized in the following stepwise procedures.

-

1.

-

2.

-

3.

-

4.

-

5.

The parameter is the convergence tolerance and the default value in our code implementation is set to In practice, Algorithm 1 is computationally efficient and usually the number of iterations required to achieve convergence is between 3 and 5. Note that when we have and the iterative within-transformation estimator is nothing else than the OLS within-transformation estimator.

From the above development, the multiplication of a vector (say ) by the matrix deviates that vector from its expectile as shown by the following expression:

We can see, from this expression, how the projection matrix eliminates the subject-specific effects parameter and any other time-invariant regressors from the initial model. For a matrix, like the design matrix the transformation is applied column-wise.

ERFE model for a sequence of expectiles

The preceding development shows that the classical within-transformation strategy can be generalized in the framework. Now, we present the estimator for a sequence of expectiles using the transformed data. The sequence of expectiles, for example the mean and a few expectiles above and below it, is necessary in the description of the conditional distribution of the response variable and for capturing the data heteroscedasticity. In addition, the simultaneous estimation allows the multiple expectiles to share strength among each other and to gain better estimation accuracy than individually estimated expectile functions (Liu and Wu,, 2011).

The iterative within-transformation estimator for a sequence of asymmetric points is defined as the minimum of the following objective function:

| (19) |

The vector is the vector of weights controlling the relative influence of the q asymmetric points and it choice depends on the research question. For a sequence of expectiles, the iterative within-transformation estimator is defined as:

| (20) |

where and the transformed data is obtained by pre-multiplying the matrix to the initial data The projection matrix is defined as and

3 Asymptotic

In this section, the asymptotic properties of the estimator are presented. As stated by Koenker, (2004), the presence of the incidence parameter, which has an infinite dimension, can raise some challenges. For this reason, we present first the asymptotic results of the estimator in the simplest case, namely for a single We then present the asymptotic properties of the estimator for a simultaneous sequence of asymmetric points The section ends with the suggestion of an estimator of the covariance matrix for the estimator. All the proofs are available in the Supplementary file.

3.1 Asymptotics for the ERFE estimator

Asymptotics for a single expectile

In the following, the asymmetric square-loss function of the model,

is replaced in term of optimization by the equivalent loss function

where Now, observe that the following estimator

minimizes the new objective function

| (21) |

The asymptotic theory of the estimator is derived using this new objective function (21) and under the following assumptions.

A1. The data are independent across and,

where and

A2. The limiting forms of the following matrices are positive definite

where

A3. The norm of the regressors is bounded by a positive constant

The stated assumptions A1-A3 are standard for panel data models (Koenker,, 2004). Condition A1 ensures independence across individuals, but allows a within-subject dependency and heterogeneity across individuals. Condition A2 is a full rank condition and is used to invoke the Lindeberg-Feller Central Limit Theorem. We observe that, when then simplifies and Condition A2 reduces to a condition on the matrices and Condition A3 is useful both for the application of the Lindeberg-Feller Central Limit Theorem and for ensuring the finite dimensional convergence of the objective function.

Theorem 1.

Assume conditions A1-A3 are met, with for some Then the components of the minimizer, converge in distribution to a Gaussian random vector with mean zero and variance-covariance matrix given by the lower right block of the matrix In others words

To show the closed form of the above matrix assume that the limiting forms of the following matrices are positive definite

where

Under the above conditions and the conditions of Theorem 1 it follows that:

Lemma 1.

Asymptotics for several expectiles

The asymptotic properties of the estimator for a sequence of asymmetric points are derived using the transformed data, where Both projection matrices are idempotent and are defined as:

where

A robust estimator of the covariance matrix is also proposed. Assume the following conditions.

B1. The data are independent across and,

where and

B2. The limiting forms of the following matrices are positive definite

B3. The norm of the regressors is bounded by a positive constant

Theorem 2.

Suppose conditions B1-B3 are satisfied, and that If then

In order to use the estimator to make inference, an estimator of its covariance matrix is presented in Theorem 3. This will make it possible to construct large sample confidence intervals or hypothesis tests. The proposed covariance matrix estimator is robust and consistent, and is a generalization of the commonly advocated covariance matrix estimator proposed by White, (1980).

Theorem 3.

Let the matrices and defined as:

where the transformed data is obtained by pre-multiplying the initial data with the projection matrix and

Then, for every fixed, we have:

We end this section with the result for a single

Corollary 1.

Let the matrices and defined as:

with the corresponding projection matrices

Then, under the above conditions and for every fixed we have

4 Simulations

In this section we conducted a simulation study to evaluate the performance of the estimator. We started by presenting the simulation design, then the metrics to evaluate the estimators and the results.

4.1 Design

The random samples were generated from the following linear model:

| (22) |

We considered two versions of model equation (22) according to the heteroscedastic parameter The value of corresponds to a location shift model where the regressors are uncorrelated to the random error. The model is used to assess the performance of the estimators for a homoscedastic scenario. In contrast, when the value of then there is a correlation between the predictor and the random error. In that case, the model is a location-scale shift model and is set to assess the performance of the estimators in the presence of heteroscedasticity.

In the location shift scenario, the model corresponds to where only the intercept term, varies with and the expectile functions are parallel lines. In the location-scale shift scenario, the related model is defined as: where the intercept and Therefore, in the presence of heteroscedasticity both the intercept and the slope of the predictor vary with

The parameters are set to and and the corresponding regressors are generated from a non-central student distribution with 3 degree of freedom and a normal distribution respectively. The individual-specific effects parameter is generated from a normal distribution and is correlated to the predictor Indeed, in real data applications it is more likely that omitted factors are correlated with regressors in the model. The random error of the model equation (22) is generated from three different distributions: normal distribution Student distribution with 3 degrees of freedom, and chi-squared distribution with degrees of freedom. We have set the sample size and the repeated measurements to The extensive simulation was carried out with 400 replications. In each case the focus is on the regressor effects at the asymmetric points

All simulations were conducted using high performance computing clusters provided by Calcul Quebec and Compute Canada. All computations were performed with the R (v3.6.0) statistical programming language R Core Team, (2021). The implemented R package erfe that comes with this manuscript is publicly available on GitHub at https://github.com/AmBarry/erfe.

4.2 Performance measures

We compared our model to the quantile regression with fixed-effects model proposed by Koenker, (2004). The model estimated the parameter of interest and the nuisance parameter of the model which could be computationally demanding as the sample size increased. We also considered the expectile regression model and the quantile regression model which ignored the individual fixed-effects parameter. Given that expectile and quantile of the same level were generally different, we carried out the appropriate conversions between the asymmetric points and the percentiles to ensure that the expectile-based regressions and the quantile-based regressions estimated the same statistics (that is quantiles and expectiles are identical). For example, the Gaussian quantiles of level are identical to the Gaussian expectiles of level In other words, the based-model and the based-model estimate the same locations of the response distribution.

We evaluated the quality of the estimators by reporting the distribution of their coefficient estimate as box-plots. We also evaluated the performance of the asymptotic standard error presented in Theorem 3 by reporting the distribution of the ratio between the asymptotic standard error and the Monte Carlo standard deviation defined as:

where

4.3 Results

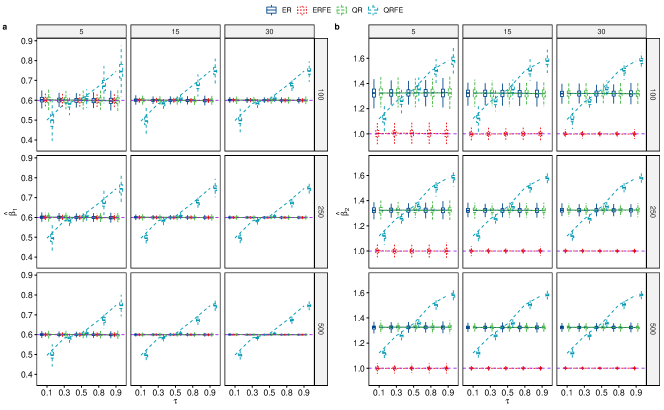

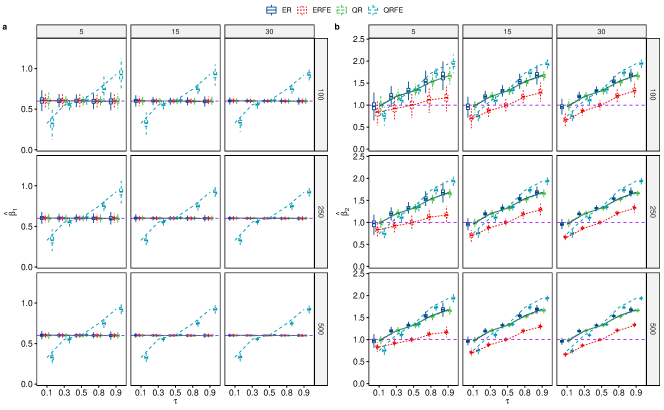

We present here the results related to the Gaussian random error and we brought the results for the Student and Chi-square random errors in the Supplementary file. Figure 1 and Figure 2 report the distribution of the coefficient estimates in the location-shift and location-scale-shift scenarios, respectively.

In the location-shift scenario, we observe that the coefficient estimates of our model are centered around the true value of the parameters with a small interquartile range. We also observe that the coefficient estimate of the and models are centered around the true value for the parameter only. We notice that the coefficient estimates of the model are not close to the true value of the parameters except when for the parameter only. In other words our model performs well in estimating the parameter coefficients of the model in the location-shift scenario. The and models perform similarly in the location-shift scenario, with an unbiased estimator for the parameter and a biased estimator for the parameter The and models do not account for the individual fixed-effects which are correlated to the regressor which could explain the bias for the parameter In contrast, the model performed poorly in estimating the parameter coefficients of the model in the location-shift scenario. The model includes the individual fixed-effects in its specification but, similarly to the random-effect model, it did not account for the dependence between the individual fixed-effects and the regressors of the model. This could explained the poor performance of the

Indeed, similar to the within-estimator, the model transforms the data by subtracting the person-specific expectile of level from the observed values of each variable and then applied the method to the de-expectilized model given by:

| (23) |

where and are defined similarly. This transformation concentrated out the individual fixed-effects and any bias that could result from its association with the regressors.

The and models do not take into account the individual fixed-effects parameter, which is included in the random error component. Since, the individual fixed-effects parameter is correlated to the predictor then the random error of the model equation (22) is also correlated to the predictor of the model. Hence, the coefficient estimate of the and methods for the parameter is biased.

Consider, the reformulation of model equation (22) in the location-shift scenario:

where is the quantile of the individual fixed-effects of level and the new random variable. The corresponding model, for a fixed can be specified as: where (since the individual fixed-effects are correlated to the regressors). Thus, in this context, the coefficient estimates of the model would be biased.

Figure 2 report the distribution of the coefficient estimates in the location-scale-shift scenario. Again, we observe that the model performs well in estimating the parameter coefficients of the model and outperformed its competitors. The apparent bias of the estimator for the parameter is due to the effect of the heteroscedasticity in this formulation of the model and is not surprising. Indeed, in the location-scale-shift scenario, because of the correlation between the predictor and the error term, the parameter of the predictor is function of the asymmetric point and then different to except when for the symmetric distributions (Normal and Student), where the expectile of level is zero. The same remark could be applied to the other methods which in addition did not account for the individual fixed-effects or its correlation with the regressors We observed similar results for the Student and Chi-square random errors (results are available in the Supplementary file).

Overall, the model outperforms its competitor and extends the favorable properties of the fixed-effects model. The model accounts for the time-invariant omitted variables and for the heteroscedasticity present in the data.

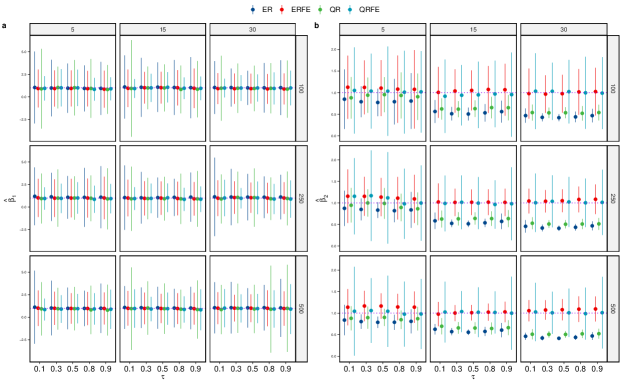

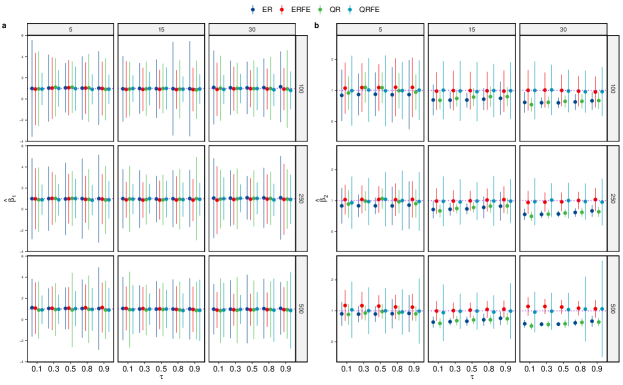

To evaluate the asymptotic standard error of the parameter estimates, we use the Monte Carlo standard deviation as a benchmark and present the distribution of the ratio as an error plot centered at the mean, Figure 3 and Figure 4. In general the error plots of the model and the model are centered around 1, which means that on average the asymptotic standard error and the Monte Carlo standard deviation are identical. However, we observe that the error plots of the model and the model are not centered around the mean for the parameter and the range of their error plot is generally larger. Similar performances were observed for the Student and Chi-Squared random error which results can be found in the Supplementary file.

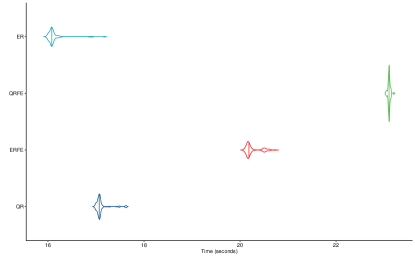

We end this section by comparing the run-times of the -based algorithms and the -based algorithms. We fitted the methods to a dataset generated by a location-shift model with a Gaussian random error. We used the microbenchmark package (Mersmann,, 2019) with 100 replications to evaluate the computation time of the different algorithm. The results in Figure 5 show that the cross-sectional algorithms and are the fastest algorithms, and our algorithm is faster than the algorithm. We also performed the comparison for a larger sample size but the algorithm stopped due to a shortage of memory for the algorithm. This problem has also been reported by Canay, (2011).

5 Application

Returns to schooling also known as returns to education is a topic widely studied in empirical economics. It is often presented in standard econometric textbooks (Baltagi,, 2008; Greene,, 2011; Cameron and Trivedi,, 2005) as an example of an endogeneity model. Indeed, there is a potential correlation between individual’s ability and the other regressors such as education. In the presence of endogeneity, the model is often preferred than other mean regression models for panel data. Despite the fact that it does not estimate the effect of the time-invariant regressors, the estimator is consistent even if the individual effects are correlated with the regressors of the model (Baltagi,, 2008).

In this section, we replicated Baltagi and Khanti-Akom, (1990)’s study using the Panel Study of Income Dynamics (PSID) dataset. The dataset is a cohort of 595 individuals observed over the period 1976–1982. The respondents, aged between 18 and 65 in 1976, are those who reported a positive wage in private non-farm employment for all 7 years, (Cornwell and Rupert,, 1988).

The log wage is the dependent variable and is regressed on weeks worked (WKS), years of full-time work experience (EXP), occupation (OCC=1, if the individual is in a blue-collar occupation), residence (SOUTH = 1, SMSA = 1, if the individual resides in the South, or in a standard metropolitan statistical area), marital status (MS = 1, if the individual is married), industry (IND = 1, if the individual works in a manufacturing industry), and union coverage (UNION = 1, if the individual’s wage is set by a union contract).

We fitted the model to the PSID dataset. In addition to the regressor effects on the average salary (Baltagi,, 2008; Baltagi and Khanti-Akom,, 1990; Cornwell and Rupert,, 1988), the model captures the regressor effects on the entire wage distribution. Consequently, the model controls for the endogeneity resulting from unmeasured factors and captures the heterogeneity present in the data. The corresponding Mincer equation of the model, for a fixed is specified as:

where the initial model is transformed to eliminate the individual effects.

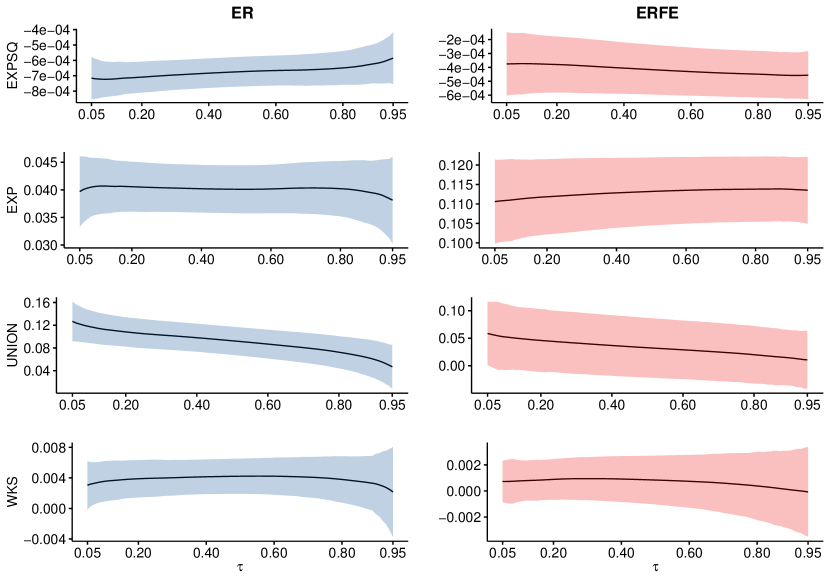

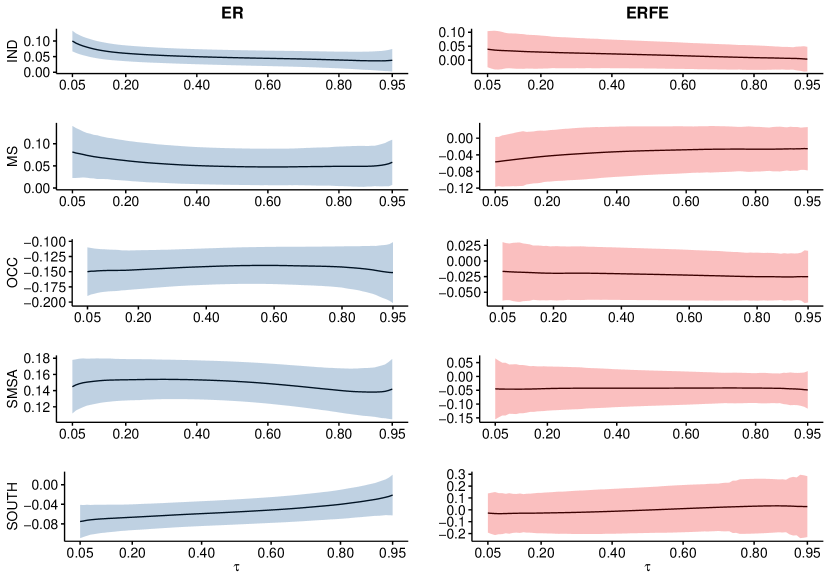

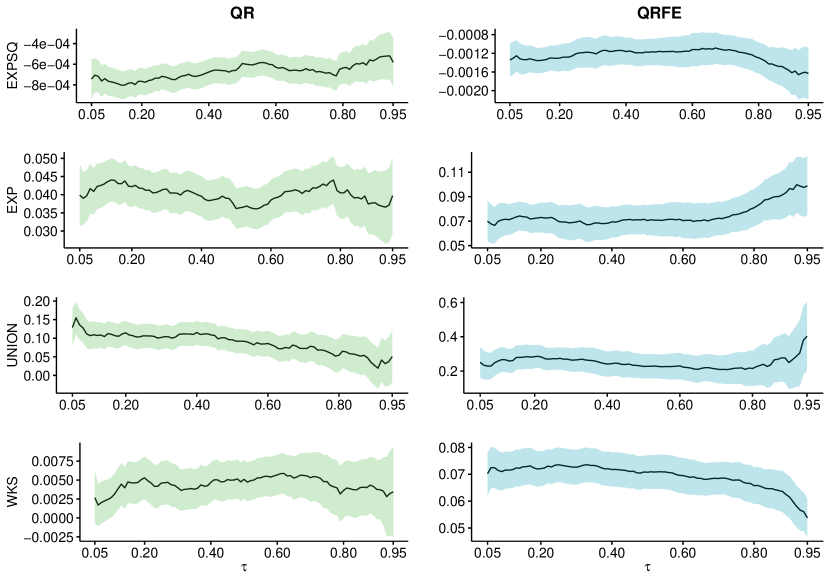

We estimated the conditional expectiles of the log wage distribution using 91 asymmetric points We generated the confidence intervals using the asymptotic standard error of the model. For comparison, we also fitted the model, the model and the model. Notice that the covariance matrix of the -based method depends on the random error density function which add a computational burden and some numerical issues (Chen et al.,, 2004; Yin and Cai,, 2005; Kocherginsky et al.,, 2005). We used a kernel estimate of the sandwich as proposed by Barnett et al., (1991) to compute the standard error of the estimates and the generalized bootstrap of Bose and Chatterjee, (2003) to compute the standard error of the estimates. Moreover, since an expectile of level is not necessarily equal to a quantile of the same level, the comparison between the -based results and the -based results must be done globally.

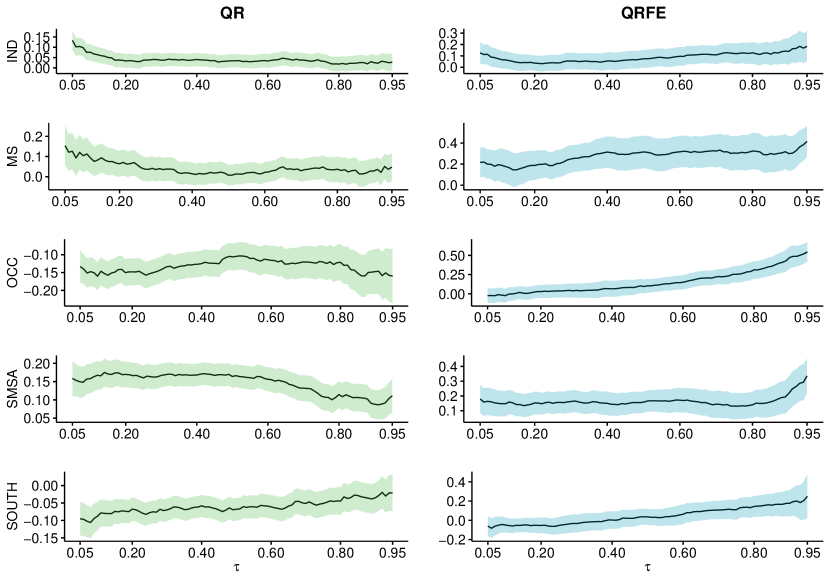

Figure 6(a) and Figure 6(b) display the coefficient estimates of the regressors obtained by fitting the -based methods while Figure 7(a) and Figure 7(b) display the coefficient estimates of the regressors obtained by fitting the -based methods. The overall results show the potential of both -based and -based methods to reveal the heterogeneous regressor effects on the response distribution and therefore to capture the heteroscedasticity present in the data. We observe that the parameter estimates of some regressors (UNION, IND and SOUTH, for example) vary with respect to the asymmetric points or percentiles suggesting the presence of heteroscedasticity in the data. For example, we observe that the parameter estimates of the UNION variable decrease with respect to the asymmetric points or percentiles suggesting that individuals with low salary have more advantage of being unionized than individuals with high salary. We also observe that the parameter estimates of some regressors may vary a little or not at all with respect to the asymmetric points, suggesting that the mean effect of these regressors would be enough to summarize their relationship with the response variable.

We also observe that the curves of the -based results are smoother than those from the -based method which seem to be more wiggly and unstable. Indeed, the -based results is more volatile and it is more difficult to identify an overall trend of the heterogeneity of the regressor effects. For example, the parameter estimates of the IND variable is decreasing between the percentiles 0.1 and 0.25, and then increasing between the percentiles 0.25 and 0.9.

Despite the similar trend, the parameter estimates of the different methods have different statistical properties. The coefficient estimates of the and have similar range and are biased upward. For example, the and coefficient estimates of the WKS variable fluctuate between 0.0025 and 0.005. While the coefficient estimates of the WKS variable vary between 0.06 and 0.07, 10 times higher than that of the parameter estimates. Therefore, the coefficient estimates is severely biased because of its inability to account for the correlation between the individual fixed-effects and some regressors in the model.

This results are in line with the simulation results, where we observed that the and the estimates have similar and lower bias than the estimates which have higher bias particularly when the individual fixed-effects is correlated to the regressors in the model.

In summary, the data analysis shows that some parameter estimates vary according to the asymmetric points or the percentiles. Therefore, we need to consider beyond the mean or median regression in order to capture the heterogeneity present in the data. The model, like other methods that estimate the mean effect, is not sufficient to analyze the returns to schooling because the impact of most of the regressors vary across the wage distribution.

6 Conclusion

We introduced the model which inherits the attractive properties of the weighted asymmetric least squares regression and the model. As with the model, the ERFE model is an endogenous model that takes into account the possible correlation between the omitted time-invariant variables and the regressors included in the model. In addition, the model estimates the regressor effects on the conditional expectiles of the response distribution allowing to study the influence of the regressors on the location, scale, and shape of the conditional response distribution.

We derived the asymptotic properties of the estimator and suggest an estimator of its variance covariance matrix. We showed that the estimator is an iterative-within-transformation estimator. That is, the estimator can be derived by using iteratively the within-transformation strategy to concentrate out the incidental parameter from the model. The model is computationally efficient and easy to implement. See our GitHub for a free R package that simplifies the implementation (github.com/AmBarry/erfe).

The exhaustive simulations showed that the estimator outperformed its competitors, including the estimator in the location-shift and location-scale-shift scenarios. These results are not surprising because our estimator inherits the properties of the within-estimator which is simply an estimator of level The real data application showed that some parameter estimates vary according to the asymmetric points signaling the presence of heteroscedasticity in the data. Therefore we need to go beyond the mean regression to capture unobserved heterogeneity of the data and provide an overview of the relationship between the regressors and the dependent variables for a better decision making.

Our model suffers from the same limitations as the model which corresponds to the model of level The model estimates only the effects of the time-variant regressors. The model ignores also the between-subject variations which can affect the efficiency of its standard error. The model is a weighted mean regression and as such it is sensitive to aberrant values. Fortunately, there is a large number of regression diagnostic tools available to mitigate their influence.

There are alternatives in the literature that have been proposed to circumvent the lack of inference for the time-invariant regressors (Cornwell and Rupert,, 1988; Baltagi and Khanti-Akom,, 1990), while keeping the favorable properties of the model. Future research should investigate the possibility of adapting these methods to the framework.

In addition to the research avenues mentioned above we are currently exploring different alternatives such as penalizing the individual fixed-effects parameter to solve the incidental parameter problem while allowing inference on the time-invariant regressors.

References

- Baltagi, (2008) Baltagi, B. (2008). Econometric Analysis of Panel Data. John Wiley & Sons.

- Baltagi and Khanti-Akom, (1990) Baltagi, B. and Khanti-Akom, S. (1990). On efficient estimation with panel data: An empirical comparison of instrumental variables estimators. Journal of Applied Econometrics, 5(4):401–06.

- Barnett et al., (1991) Barnett, W. A., Powell, J., and Tauchen, G. E. (1991). Nonparametric and Semiparametric Methods in Econometrics and Statistics: Proceedings of the Fifth International Symposium in Economic Theory and Econometrics. Cambridge University Press. Google-Books-ID: wHTszJdi2H0C.

- Barry et al., (2020) Barry, A., Oualkacha, K., and Charpentier, A. (2020). A new GEE method to account for heteroscedasticity, using asymmetric least-square regressions. arXiv:1810.09214 [stat]. arXiv: 1810.09214.

- Bose and Chatterjee, (2003) Bose, A. and Chatterjee, S. (2003). Generalized bootstrap for estimators of minimizers of convex functions. Journal of Statistical Planning and Inference, 117(2):225–239.

- Brüderl and Ludwig, (2014) Brüderl, J. and Ludwig, V. (2014). Fixed-Effects Panel Regression. In The SAGE Handbook of Regression Analysis and Causal Inference, pages 327–358. SAGE Publications Ltd.

- Cameron and Trivedi, (2005) Cameron, A. and Trivedi, P. (2005). Microeconometrics. Cambridge University Press.

- Canay, (2011) Canay, I. A. (2011). A simple approach to quantile regression for panel data. The Econometrics Journal, 14(3):368–386. Publisher: Wiley.

- Card, (2001) Card, D. (2001). Estimating the Return to Schooling: Progress on Some Persistent Econometric Problems. Econometrica, 69(5).

- Chen et al., (2004) Chen, L., Wei, L.-J., and Parzen, M. I. (2004). Quantile Regression for Correlated Observations, pages 51–69. Springer New York, New York, NY.

- Cornwell and Rupert, (1988) Cornwell, C. and Rupert, P. (1988). Efficient estimation with panel data: An empirical comparison of instrumental variables estimators. Journal of Applied Econometrics, 3(2):149–55.

- Galvao and Montes-Rojas, (2010) Galvao, A. and Montes-Rojas, G. (2010). Penalized quantile regression for dynamic panel data. Journal of Statistical Planning and Inference, 140(11):3476–3497. cited By (since 1996)5.

- Girard et al., (2021) Girard, S., Stupfler, G., and Usseglio-Carleve, A. (2021). Functional estimation of extreme conditional expectiles. Econometrics and Statistics.

- Greene, (2011) Greene, W. H. (2011). Econometric analysis. Prentice Hall, Upper Saddle River, N.J., 7th ed.. edition.

- Kocherginsky et al., (2005) Kocherginsky, M., He, X., and Mu, Y. (2005). Practical Confidence Intervals for Regression Quantiles. Journal of Computational and Graphical Statistics, 14(1):41–55.

- Koenker, (2004) Koenker, R. (2004). Quantile regression for longitudinal data. Journal of Multivariate Analysis, 91(1):74–89.

- Koenker, (2018) Koenker, R. (2018). quantreg: Quantile Regression. R package version 5.36.

- Koenker and Bache, (2014) Koenker, R. and Bache, S. H. (2014). rqpd: Regression Quantiles for Panel Data. R package version 0.6/r10.

- Lamarche, (2010) Lamarche, C. (2010). Robust penalized quantile regression estimation for panel data. Journal of Econometrics, 157(2):396–408.

- Liu and Wu, (2011) Liu, Y. and Wu, Y. (2011). Simultaneous multiple non-crossing quantile regression estimation using kernel constraints. Journal of Nonparametric Statistics, 23(2):415–437.

- Mersmann, (2019) Mersmann, O. (2019). microbenchmark: Accurate Timing Functions. R package version 1.4-7.

- Newey and Powell, (1987) Newey, W. K. and Powell, J. L. (1987). Asymmetric least squares estimation and testing. Econometrica, 55(4):819–47.

- R Core Team, (2021) R Core Team (2021). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Sobotka et al., (2014) Sobotka, F., Schnabel, S., Waltrup, L. S., Eilers, P., Kneib, T., and Kauermann, G. (2014). expectreg: Expectile and Quantile Regression. R package version 0.39.

- Warrington et al., (2019) Warrington, N. M., Beaumont, R. N., and al. (2019). Maternal and fetal genetic effects on birth weight and their relevance to cardio-metabolic risk factors. Nature Genetics, 51(5):804–814.

- White, (1980) White, H. (1980). A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica, 48(4):817–38.

- Yin and Cai, (2005) Yin, G. and Cai, J. (2005). Quantile Regression Models with Multivariate Failure Time Data. Biometrics, 61(1):151–161. _eprint: https://onlinelibrary.wiley.com/doi/pdf/10.1111/j.0006-341X.2005.030815.x.