Competition and Recall in Selection Problems 111222The authors gratefully acknowledge funding from ANITI ANR-3IA Artificial and Natural Intelligence Toulouse Institute, grant ANR-19-PI3A-0004, and from the ANR under the Investments for the Future program, grant ANR-17-EURE- 0010. J. Renault also acknowledges the support of ANR MaSDOL-19-CE23-0017-01.

Abstract

We extend the prophet inequality problem to a competitive setting. At every period , a new

sample from a known distribution arrives, which is publicly observed. Then two players simultaneously decide whether to pick an available value

or to pass and wait until the next period (ties are broken uniformly at random).

As soon as a player gets one sample, he leaves the market and his payoff is the value of this item.

In a first variant, namely “no recall” case, the agents can only bid in period for the current

value .

In a second variant, the “full recall” case, the agents can also bid at period for any of the previous samples with values ,…, which has not been already selected.

For each variant, we study the subgame-perfect Nash equilibrium payoffs of the corresponding game, as a function of the number of periods and the distribution .

More specifically, we give a full characterization in the full recall case, and show in particular that both players always get the same payoff at equilibrium, whereas in the no recall case the set of equilibrium payoffs typically has full dimension. Regarding the welfare at equilibrium, surprisingly it is possible that the best equilibrium payoff a player can have is strictly higher in the no recall case than in the full recall case. However, symmetric equilibrium payoffs are always better when the players have full recall.

Finally, we show that in the case of 2 arrivals and arbitrary distributions on , the prices of Anarchy and Stability in the no recall case are at most 4/3, and this bound is tight.

Keywords: Optimal stopping, Competing agents, Recall, Prophet inequalities, Price of anarchy, Price of stability, Subgame-perfect equilibria, Game theory.

1 Introduction

1.1 Context

The theory of optimal stopping has a vast history and is concerned with the problem of a decision-maker who observes a sequence of random variables arriving over time and has to decide when to stop optimizing a particular objective. Probably, the two best-known problems in optimal stopping are the Secretary Problem and the Prophet Inequality. In the classical model of the former, introduced in the ‘60s, a decision-maker observes a sequence of values arriving over time and has to pick one in a take-it-or-leave-it fashion maximizing the probability of picking the highest one. In other words, after observing an arrival, he has to decide whether to pick this value (and gets a reward equals to the value picked) or to pass and continue observing the sequence. Once a value is picked, the game ends and the goal of the decision-maker is to maximize the probability of getting the highest value. Lindley [14] proves that an optimal stopping rule for this problem consists in rejecting a particular amount of values first and then accepting the first value higher than the maximum observed so far. When the number of arrivals goes to infinity, the probability of picking the best value approaches to . Since then, several variants have been studied in the literature (see, e.g., [6, 8, 11]).

Related to the secretary problem is the optimal selection problem where the decision-maker knows not only the total number of arrivals but also the distribution behind them, and he has to decide when to stop, with the goal of maximizing the expected value of what he gets. Instead of looking at this problem as an optimal stopping problem, in the ‘70s researchers started to answer the question of how good can a decision-maker play compared to what a prophet can do, where a prophet is someone who knows all the realizations of the random variables in advance and simply picks the maximum. These inequalities are called Prophet Inequalities and it was in the ’70s when Krengel and Sucheston, and Garling [13] proved that the decision-maker can get at least 1/2 of what a prophet gets, and that this bound is tight. Later, in 1984 Samuel-Cahn [17] proved that instead of looking at all feasible stopping rules, it is enough to look at a single threshold strategy to get the 1/2 bound. These results are for a general setting where the random variables are independent but not necessarily identically distributed, and then one natural question that arose was if this bound could be improved assuming i.i.d. random variables. Kertz [12] answered this question positively and provided a lower bound of roughly 0.7451. Quite recently, Correa et al. [4] proved that this bound is tight. A lot of work has appeared considering different model variants (infinitely many arrivals, feasibility constraints, multi-selection, etc) but it was since the last decades that this problem gained particular attention due to its surprising connection with online mechanisms (see, e.g., [3, 5, 10]).

1.2 Our paper

In the i.i.d. setting of the prophet inequality problem, there is a decision-maker who observes an i.i.d. sample distributed according to a known distribution . Only one value can be selected, and the banchmark is . After each arrival, the decision-maker must make an immediate and irrevocable decision whether to pick this value or not. If he selects it, he leaves the market and the game ends, otherwise he continues observing the next arrival. This problem is commonly motivated by applications to online auction theory, where at each time period a seller, who wants to sell an item, receives an offer from a potential buyer and has to decide whether to accept it and sell the item or to reject it and wait for the next offer. Most of the work on the prophet inequality problem relies in the fact that there is only one decision-maker and in that the decision must be taken immediately after observing the offer. However, in some situations of interest– a person who wants to buy a house, a company hiring an employee, among others– it seems reasonable to allow more than one decision-maker, as well as to be able to make the decision later on time. Driven by this fact, in this paper we study two variants of the classic setting. More specifically, on one hand, we consider the setting where two decision-makers compete to get the best possible value, and we call it competitive selection problem with no recall. On the other hand, we consider the problem where the two decision-makers are allowed to select any available value that appeared in the past and not only the one just arrived, and we call it competitive selection problem with full recall.

For each variant, we study the two-player game induced by the optimal stopping problem, focusing on subgame-perfect Nash equilibria (SPE for short).

The main contributions of this paper can be divided into three lines, which are summarized in what follows.

Description of the subgame-perfect equilibrium payoffs.

The first stream of contributions refers to the study of the set of SPE payoffs (SPEP) for both settings. Regarding the full recall case, we fully characterize the set of SPEP (Theorems 1 and 2) and we obtain that each such payoff is symmetric, meaning that every SPE gives the same payoff to both players.

In the no-recall case, the set of SPEP is clearly symmetric with respect to the diagonal but contains points outside of the diagonal, inducing different payoffs for the players. In this case we give in Theorem 3 recursive formulas to compute the best and the worst SPEP payoffs (in terms of sum of payoffs of the players), as well as the worst payoff a single player can get at a subgame-perfect equilibrium.

To illustrate these results, in Section 3.5 we provide a detailed study of the particular case where is the uniform distribution on .

Comparison of the two variants.

The second stream of results is focused on comparing the highest SPEP in both settings. Surprisingly, an example (see Section 3.1) shows that the best SPEP a player can obtain may be higher in the no recall case than in the full recall case. This can be explained by the possible existence of an asymmetric SPE in the no recall case which significantly favors one player at the expense of the other, who picks a value early in the game. However, if we restrict our attention to symmetric SPEP, we show in Theorem 4 that players are always better off in the variant with recall. More precisely, we prove that for every number of periods and continuous distribution , if is a SPEP of the game with full recall and is a SPEP of the game without recall, then . Furthermore, this advantage can be significant: If is the uniform distribution on and , the payoff of players in the full recall case is at least higher than in the no recall case.

Efficiency of equilibria.

To analyze efficiency, we use in Section 3.4 the standard notions of Price of Anarchy and Price of Stability, and we introduce the notion of Prophet Ratio, defined as the sum of payoffs a team of prophets would obtain, divided by the best sum of payoffs at equilibrium. When is uniform on , we find numerically that equilibria are quite efficient and that having full recall gives a small advantage to the players, in terms of having a payoff closer to the one obtained by playing the best possible feasible strategy in the corresponding setting. We also show that both the prices of Anarchy and Stability are maximized in the no recall case with , and the intuition is that it is the case maximizing the probability that a player will get nothing. The Prophet Ratio in the same context is maximized for , which is less intuitive. Finally we consider the case without recall, and let be any distribution with support contained in [0,1]. We prove in Theorem 5 that both the prices of anarchy and stability are not greater than 4/3, and that this bound (reminiscent of the bound for routing problems with linear latencies, see [16]) is tight in both cases.

It is worth noting that, although competition and recalling variants have already been considered in the literature for some optimal stopping problems (as we will discuss in the next section), to the best of our knowledge, our paper is the first considering them from a Game Theory perspective with a focus on the study of the set of SPEP, and then it constitutes a good starting point for future research work of interest cross academic communities in Operations Research, Computer Science, and Economics.

1.3 Related literature

As it was aforementioned, the literature in optimal stopping theory is extensive and mainly focused on finding optimal or near-optimal policies for the different model variants, as well as on studying the guarantees of some simple strategies, such as single threshold strategies, even when they are not optimal. However, this paper introduces a game-theoretic approach for a model with competition and where recall is allowed. In what follows, we revisit some of the existing literature regarding optimal stopping problems with some of these two particular features.

Optimal Stopping with competition.

Abdelaziz and Krichen [1] survey the literature on optimal stopping problems with more than one decision-maker until 2000s. More recently, Immorlica et al. [11] and Ezra et al. [6] study the secretary problem with competition. The former considers a classical setting where decision are made in a take-it-or-leave-it fashion and ties are broken uniformly at random, and they show that as the number of competitors grows, the moment at which “accept” is played for the first time in an equilibrium decreases. The latter incorporates the recalling option, and studies the structure and performance of equilibria in this game when the ties are broken uniformly at random or according to a global ranking.

Our paper considers a different model, since the problem is more related to the prophet inequality setting. In this sense, the work closest to ours is the recent paper by Ezra et al. [7], who introduce, independently of our paper, the no recall case, again with the two variants for tie breaking. However, the novelty of our paper is the incorporation of recalling in addition to the competition between players. Moreover, instead of studying the reward guarantees under single-threshold strategies, we focus on the study of equilibria of the game.

Optimal Stopping with recall.

Allowing decision-makers to choose between any of the values arrived so far

is a variant of the classic problem that may have interesting applications.

If this extension is considered without competition, it is easy to see that the optimum is just to wait until the end and pick the best value. However, adding competition in the model makes the problem interesting and characterizing the set of equilibrium payoff and studying their efficiency are challenging questions we address in this paper.

Notice that this notion of recalling is not new for some optimal stopping problems. For example, Yang [19] considers a variant of the secretary problem, where the interviewer is allowed to make an offer to any applicant already interviewed. In his model, the applicant reject the offer with some probability that depends on when the offer is made and he studies the optimal stopping rules in this context. Thereafter, different authors have been studying other variants of the secretary problem with recall (see, e.g., [6, 15, 18]).

Our work differs from most of them not only in the model we consider but also in terms of questions since we are more interested in a game-theoretic approach of the problem.

1.4 Roadmap

The remainder of this paper is organized as follows: We start presenting the model in Section 2, including the description of the games for the full recall and no recall cases in Section 2.1. The results of our paper are presented formally in Section 3. This section is divided into four parts: In Section 3.2, we study the set of SPEP, starting with its computation for a very simple example (see Section 3.1), and making then a complete analysis for the full recall case (see Section 3.2.1) and for the no recall case (see Section 3.2.2). In Section 3.3 we present the results concerning the comparison of the two variants, whereas in Section 3.4 we study the efficiency of equilibria. In Section 3.5 we make a detailed analysis of the case where is uniform on . Finally, we close the paper with the proofs of the results, which are relegated to Section 4.

2 Model

Consider a sequence of samples ,…, of a random variable distributed according to a c.d.f. with support included in [0,1]. 333We assume the support of included in to not overload the notation but the results can be easily extended to the general case. There are two players, or decision-makers, competing to select the highest value among ,…,. More explicitly, at each time period , the decision-makers – who know the distribution – observe and simultaneously decide whether or not to select one value in the current feasible set . Once a decision-maker chooses a value , he leaves the market obtaining a payoff of and this value no longer belongs to the feasible set. Decision-makers must decide when to stop, maximizing the expected value of their payoff. If at time both agents want to select the same value, we break the tie uniformly at random. That is, each of them gets the value with probability , and the decision-maker who gets it leaves the market, whereas the other passes to the next period.

It remains to specify what are the sets of feasible values, distinguishing the two cases we will consider. In the first one, namely full recall case, the set of feasible elements at time consists of all the periods that have not yet been selected by a decision-maker, and a feasible action represents a probability distribution over the set , where represents the action of not selecting anything. In this case, the game ends when all decision-makers choose an element, and then it could be later than if both players are still present at period . We assume that at stage all players who are present select the element corresponding to the highest value. If both players are present, there is a tie, and the player who losses the toss gets the second best value.

The second variant we consider is the no recall case. In this case, a take-it-or-leave-it decision is faced by the decision-makers at each time period. That is, after observing the sample just arrived they should decide whether to take it or not. Independently of their decision, the value cannot be chosen later. Thus, the set of feasible elements at time is just given by and a feasible action is a probability distribution on where represents the action of represents the action of not selecting anything. Notice that in the 1-player case (decision problem), the optimal strategy with full recall is simply to wait until the end and to pick the element which corresponds to the maximum of . And in the 1-player case with no recall we have a standard prophet problem, with value smaller than the expectation of the maximum of . Obviously, having the possibility of getting a sample observed in the past is beneficial to the player. In our multiplayer setting, we cannot say a priori that the full recall case is beneficial to the players, as there are examples where having more information or more actions decreases the sum of the payoffs of the players at equilibrium. This motivated us to ask how important is to have the power of being able to choose a value observed in the past. To answer this question we study the games behind the two model variants described above. In particular, we study the set of SPEP as well as the Price of Anarchy (PoA) and the Price of Stability (PoS).

We remark here that throughout the paper we will “the decision-maker selects value ” to refer to the decision-maker selecting element from .

2.1 Description of the games

We now formally describe the games induced by the full recall case and the no recall case, denoted by and , respectively. Then, we specify the notions of equilibrium that will be used throughout the paper.

-

1.

Full recall case. Game

For each we denote by the set of possible histories up to stage . only contains the empty history. contains what happens at stage 1, i.e., the sample , who tried to get and who got (possibly nobody). contains everything that happened at stages 1 and 2, and so on.

As usual a strategy for player is an element where is a measurable map which associates to every history in an available action, that is a probability distribution over . A strategy profile induces a probability distribution over the set of possible plays , and the payoff (or utility) of each player is defined as the expectation of the value he gets, with the convention that getting none of the samples yields a payoff of .

-

2.

No recall case. Game

Here, the set of available elements at stage is , and we only need to consider histories for where contains everything that happened up to stage under the no recall assumption. A strategy for player is an element where is a measurable map which associates to every history in an available action, that is a probability distribution over . A strategy profile induces a probability distribution over the set of possible plays , and payoffs are defined as in the full recall case.

-

3.

Equilibrium notions. We recall here the usual notions of Nash equilibrium (NE) and subgame perfect equilibrium (see, e.g., [9]). The following definitions apply to both games and .

Definition 1.

A strategy profile is a Nash equilibrium (NE) of the game if for every agent and every strategy , player’s utility when is played is not greater than the one obtained if is played.

Given a stage number and a finite history mentioning everything that happened up to stage , we can define the continuation game after .

Definition 2.

A strategy profile is a subgame perfect equilibrium (SPE) if it induces a NE for every proper subgame of the game (i.e. for any continuation game after a finite history).

When studying SPE, we will assume w.l.o.g. that as soon as a player is alone in the game, he plays optimally in the remaining decision problem. By best (resp. worse) equilibrium, we mean an equilibrium maximizing (resp. minimizing) the sum of the payoffs of the players.

3 Results

The goal of this section is to present the main results of the paper. First, we study the structure of the sets of SPEP. We start by introducing a simple example, where the computation for both the recall and no recall cases is easy. Then, we present our main result in the full recall case which fully characterizes the set of SPEP. Regarding the no recall case, we provide recursive formulas to compute the the worst payoff a player can get in equilibrium, as well as the sum of payoffs of players for both the best and worst SPE, when the distribution function is continuous. After that, we move on to understand what is the relationship between the payoff a player gets in both problems. In other words, we answer the question: Is the recall case always beneficial for the players? Finally, we study the efficiency of equilibria for the full recall and no recall cases. We leave the proofs of the results to Section 4.

3.1 Motivating example.

Let us consider the particular instance of the problem where samples of arrive sequentially over time, where the law of is defined by:

We compute the set of SPEP in the full recall and no recall case, denoted by and , respectively.

Full recall case. Note that in this case, the unique SPE is to bid at any time if and to pass otherwise until the last period, where the best available value is chosen. Then, if all samples take the value the players obtain a payoff of ; if only one sample is equal to , both players bid for this value and then they obtain with probability and with probability ; and if more than one realization of has value both players obtain a payoff of . Thus, the expected payoff of a player in equilibrium, namely , can be computed as follows

where denotes the maximum of i.i.d. samples of . The probabilities above are easy to compute, having that , and . Putting all together we conclude that with

No recall case. Because we are considering an instance with time periods and the random variable only takes two possible values, for the first arrivals, at equilibrium, players bid if and only if the sample has value . Therefore, at equilibrium: if at least two samples have value up to time , players obtain ; if only one samples have value up to time , each player obtain with probability and the expected value of with probability ; and if all samples up to are , the players obtain an expected payoff . Note that is the value of the decision problem in a standard prophet setting with two arrivals from , and thus . Therefore, an expected payoff of player 1 can be computed as

whereas for player 2 we have

Again, the probabilities above are easy to compute, having , and . Thus, we obtain that an expected payoff of player is given by:

| (1) |

It remains to compute the set To this end, for we consider the game, called , defined as but with an initial available value . That is, there is a time period “zero” where players choose between selecting the value or pass, before observing the value of the single sample of the game. We denote by the set of SPEP of the game . Notice that

| (2) |

and then can be easily computed from To study we consider the payoffs matrix for the game represented in Table 1.

| Player | |||

|---|---|---|---|

| Player | |||

Observe that if , is the unique NE with payoff , and thus . Otherwise, if , there are three NE: and a symmetric mixed equilibrium in which both agents play with probability and pass with probability . The equilibrium payoffs are and , respectively, and then We now can compute the set by using (2), obtaining

Finally, we go back to equations (1) and we conclude that is the three-elements set

| (3) |

with

Note that and represent the best and worst possible payoff of a player in equilibrium, respectively, whereas represents the payoff in between.

Recall that and therefore Moreover . The latter means that the sum of equilibrium payoffs of the players in the full recall case is equal to the sum of the payoffs of players in the no recall case if an asymmetric equilibrium is played. Otherwise, i.e., if in the no recall case the symmetric equilibrium is played, then the sum of payoffs of the players is strictly lower than in the full recall case, which is somehow not surprising.

However, for this example we observe that, surprisingly, the best payoff a single player can obtain at equilibrium is strictly higher in the no recall case than in the full recall case. Intuitively, what happens here is that the lack of recalling power implies that with positive probability one player will take the “bad” value in period and therefore it gives an advantage to the other player, who is now alone in the game.

A natural question is to ask how efficient are the equilibria of the games compared with the best feasible strategy. We use the well known notions of Price of Stability (PoS) and Price of Anarchy (PoA) which are defined as the ratio between the maximal sum of payoffs obtained by players under any feasible strategy and the best and worst sum of payoffs of SPEs respectively. For the example, this analysis is easy to do, and we start by noting that in both model variants, there exist a feasible strategy (not the same for both problems) where players obtain the first and the second best values. This implies that the numerator of PoA and PoS will be the same and equal to , where denotes the second best sample, which is given by Observe that this value is exactly and and then PoS is 1 for both settings and PoA is 1 for the full recall case, meaning that in the full recall case the resulting equilibria is efficient. On the other hand, the PoA for the no recall case is given by which is strictly greater to 1 but it converges fast to one when grows.

This example highlights the relevance of our work in three ways. First, even in this case where the random variable only takes two possible values, we observe that the computation of the SPEP requires a detailed analysis and then computing these sets for a general probability distribution, even under some mild assumptions, seems difficult and challenging. On the other hand, this example shows us that the power of recalling is not always favorable to all players, and then it is an interesting question to try to understand under which assumptions one can ensure that the payoff of a player in the full recall case in equilibria will be at least as good as the one in the no recall case. Finally, we see in this example that the SPEP are efficient and it motivates us to study if that still holds for a general distribution.

3.2 Description of the subgame-perfect equilibrium payoffs

Here we will fully characterize the set of SPEP for the full recall case. For the no recall case, we provide recursive formulas to compute the best and worst sum of SPEP.

3.2.1 Full recall case

We go back to the general case and study here the game with full recall, that is, at time , any of the values so far arrived that has not been selected before can be selected.

We introduce a two-player game , where for each natural number and , is defined as with samples to arrive and and two available values present at the beginning of the game. That is, we have a time period “zero” where players choose between getting or pass, before the sequential arrival of the samples. We denote by the set of the SPEP of the game Note that the set of the SPEP of the game is just the set .

The next theorem states that the set of SPEP for the defined auxiliary game is contained in the diagonal, i.e., at each SPE both players get the same payoff. We see this as a surprising result.

Theorem 1.

Consider an instance of the game , for real numbers such that and . The set of SPE payoffs is contained in the diagonal, that is .

Furthermore, if we define the projection of to , we have and , where and are defined recursively as follows:

-

i)

-

ii)

for :

where , med denotes the median, and and are defined by:

Using the theorem above, we can prove the following result which fully characterizes the set of SPEP of the games when is continuous (i.e. when the corresponding distribution is atomless).

Theorem 2.

Assume is continuous. Then, for , the set of SPE payoffs of the game is the segment:

That is, is convex, contained in the diagonal, and its extreme points are and , where and are defined in the statement of Theorem 1.

3.2.2 No recall case

We now consider the no recall variant, where players can only play in a take-it-or-leave-it fashion, without being able to select a sample arrived in the past. In this section, we assume that is continuous, which ensures that the set of SPEP is convex, and allows us to derive explicit recursive formulas for the support function of this set in particular directions.

We introduce here the two-player game , where for each natural number and , is defined as with samples to arrive, but with an available value present at the beginning. That is, we have a time period “zero” where players choose between getting or pass, before the sequential arrival of the samples.

Calling the set of SPEP of the game , we have that the set of the SPEP of is just where

Below we present a technical result, stating that the set of SPE payoffs for the no recall case is symmetric with respect to the diagonal, and when is continuous, it is also convex and compact.

Proposition 1.

For each natural number , the set of the SPE payoffs is is symmetric with respect to the diagonal. If is continuous, is convex compact.

Although the set of SPEP for the no recall case is convex and symmetric with respect to the diagonal, it will not be a subset of the diagonal. The recursive structure of the SPEP in the no recall case is more complex than the full recall case. However, in the main result of this section we give explicit recursive formulas to compute the sum of the SPE payoffs for the best and worst equilibria under the no recall setting. Recall that by best (resp. worst) equilibrium we mean a SPE which maximizes (minimizes) the sum of the payoffs of the 2 players.

Before presenting the result, we introduce some necessary notation. We first define by induction (with ):

Note that is the value of the decision problem in a standard prophet setting.

On the other hand, we denote by () the smallest (highest) coordinate value of a point on belonging to the diagonal, and by the smallest coordinate of a point belonging to . That is, , and (see Figure 1). It is easy to see that:

Theorem 3.

Assume is continuous. In the game , the following holds:

-

a)

the worst payoff a player can get at equilibrium is , where for :

-

b)

the sum of payoffs for the best SPE is , where for :

-

c)

the sum of payoffs for the worst SPE is , where for :

3.3 Comparison of the two model variants

We now come back to the general case and no longer assume that is continuous, and want to compare the SPEP obtained by the players with and without recalling power.

We have that the best SPE payoff of a player under full recall is defined recursively in Theorem 1. We now denote by

the best possible SPEP of a player under no-recall.

We know from the simple example presented in Section 3.1 that we may have: , that is the best possible SPE payoff for a player may be strcitly higher under no recall than under full recall. Unsurprisingly this is not a general result, and we will give here one example when and one example when .

Then, we will consider the maximal sum of the payoffs of the players at equilibrium. In the the full recall case, we know that the best SPE payoff is and the worst SPE payoff is . In the no-recall case when is continuous, the SPE payoff set is convex, compact and symmetric with respect to the diagonal, hence the best sum of payoffs is obtained at the symmetric equilibrium . Theorem 4 will show that , implying that when is continuous, at a symmetric equilibrium payoff, players are always better off under full recall than under no recall.

Example 1.

An example with . Consider the following discrete random variable:

We will show that the expected payoff of a player at equilibrium in the full recall case is always higher than the expected payoff of a player at equilibrium in the no recall case, when there are 2 samples of arriving sequentially. In other words, we will prove that .

Let us start with the full recall case. In this setting, the only SPE is to bid in the first stage if and only if . Then, the expected payoff of a player playing SPE is given by:

In the no recall case, Table 2 represents the matrix of expected payoff for the game if the first arrival is .

| Player | |||

|---|---|---|---|

| Player | |||

Note that if , is the unique NE with payoff , and if , is the unique NE with payoff . Then, the SPE payoff of each player is This means that , and we then conclude that .

Example 2.

An example with . Let us now consider the game with two samples of arriving sequentially over time, with .

Using Theorem 1 we can easily obtain that , and then in this case we have .

Regarding the no recall case, Table 1 represents the expected payoffs matrix if the first arrival is . We now compute the set of NE depending on the value of :

-

Case 1.

If , is the unique NE and the payoff is given by .

-

Case 2.

If , is the unique NE with payoff .

-

Case 3.

If , and are the pure NE with payoff and , respectively, and there is also a mixed NE with payoff .

Therefore we have that,

Note that the maximum possible expected payoff for one player is obtained if he passes for every , and the payoff obtained is given by

concluding that .

Symmetric equilibrium payoffs. From the examples above, we conclude that it is not true that at equilibrium players always take advantage of the recalling power. However, restricting the set of SPE in the no recall case to the symmetric SPE, holds that the expected revenue of a player in the full recall case is always at least the one obtained in the no recall case. We state this result formally in Theorem 4.

Theorem 4.

Assume that is continuous. Let be a SPE payoff under full recall, and be a symmetric SPE payoff under no recall. Then .

The proof in Appendix 4.2 will use the following technical lemma, which gives a lower bound for a SPEP of a player in the full recall case.

Lemma 1.

Let be a positive real number such that . If denotes the expected payoff of one player in some SPE in , then

where is the value of the decision problem in the no recall case with one decision-maker and arrivals.

3.4 Efficiency of equilibria

The goal of this section is to study how efficient are the SPE payoffs. To this end, we define as usual the Price of Anarchy and Price of Stability, and we introduce what we call the Prophet Ratio of the game. Given an instance of a game, the first two notions refers to the ratio between the maximal sum of payoffs obtained by players under any feasible strategy and the sum of payoffs for the worst and best SPEs, respectively. On the other hand, we define the Prophet Ratio of an instance of the problem as the ratio between the optimal Prophet value of the problem (that is, the expected sum of the two best values) and the sum of payoffs for the best SPE. We call this quantity Prophet Ratio because we are comparing the best sum of payoffs obtained by playing a SPE strategy with what a prophet would do if he knows all the values of the samples in advance.

Next, we formally introduce these definitions.

Definition 3.

Consider an instance or , where samples from a distribution arrive sequentially over time. Denote by the set of all feasible strategy pairs and by SPE the set of subgame-perfect equilibria. We call:

-

a)

Price of Anarchy of this game instance– and we denote it by – to the following ratio

-

b)

Price of Stability of this game instance– and we denote it by – to the following ratio

-

c)

Prophet Ratio of this game instance– and we denote it by – to the following ratio

where and represent the first and second order statistics from the sequence of samples .

Clearly, by definition it holds that for each and

Notice that is usually called competitive ratio for the two-sample optimal selection problem.

For each , we define the Price of Anarchy, Price of Stability and Prophet Ratio of our competitive selection problems as the worst case ratio over all possible value distributions . That is:

In what follows, we study this quantities for each of the model variants, and at the end of the section, we consider the case where the number of arrivals is two, and we present a tight bound for the ratios in Theorem 5.

3.4.1 Full recall case

Note that in this case, the maximal feasible sum of payoffs obtained by the players is simply the expected value of the two best samples (they can wait until the end of the horizon and pick the best and second best values). Thus, here, the notions of Price of Stability and Prophet Ratio are equivalent.

By Theorem 2, the sum of payoffs for the worst SPE is given by and for the best SPE is , and therefore given an instance of the game we have in this setting:

Notice that if , that is, we have only two arrivals, each sample will be eventually picked by a player, so that for every value distribution .

On the other hand, if goes to infinity, then we also have that both the Price of Anarchy and Price of Stability goes to 1. Then, the interesting question is what happen with these ratios when is finite and greater than 2.

Although we have a general characterization of the ratios for any value of and distribution , these quantities are not always easy to compute for any even if we fix the distribution .

3.4.2 No recall case

If , picking the two best samples is a feasible strategy since player one can get and player two , and then . However, for , as soon as the support of has at least three points, picking almost surely the two best samples is no longer feasible and

Note that in this case, the maximal feasible strategy is the same as the strategy of one player selecting two values among in the classical online selection problem. The following Lemma gives us a recursive formula for the expected sum of payoffs of the maximal feasible strategy.

Lemma 2.

Assume we are in the no recall case with arrivals following a distribution with mean . Let denote a random variable with law , and the value of the decision problem in the no recall case with one decision-maker and arrivals. Then, the expected maximal feasible sum of payoffs satisfies

-

a)

if ,

-

b)

if ,

-

c)

if

If the ratios are equal to 1 and if we take going to infinity, we also obtain that the ratios goes to 1. Then, as in the full recall case, the interesting cases are the ones in between.

Recall that from Theorem 4 we have that for every and every continuous distribution , and therefore . However, the comparison is not direct for PoA and PoS as the numerators are different in the full recall and the no recall cases.

3.4.3 Two arrivals case

To conclude this section, we study the efficiency of SPE when we fix the number of arrivals at two and we look at the worst case ratios over . In the case with full recall all ratios are 1 and the question is trivial, so we consider the no recall case here. In other words, we consider the game and we want to study how bad it may be to play the best or worst SPE, in terms of the sum of payoffs obtained, compared with the maximal feasible sum of payoffs.

We obtain the following result, which states that both the Price of Anarchy and Price of Stability are upper bounded by , and that this bound tight.

Theorem 5.

If , under the no recall case it holds that for every distribution ,

Furthermore, this bound is tight for both the price of stability and price of anarchy.

3.5 Example: Uniform distribution

In this section, we apply the results obtained in the former sections to the particular case where the samples are from a random variable uniformly distributed on [0,1].

3.5.1 Computation of SPEP

We start by the computation of the SPEP. To this end, we divide the analysis according to whether we are under the full recall or no recall case. For the former, We compute to illustrate how to apply Theorem 1. For the latter, we implement the recursive formulas for , and .

Full recall case.

We now compute the set of SPEP of the game , when we have three samples arriving from a uniform distribution.

Using the notation introduced in Theorem 1:

If and , we have:

To compute , we need to compute . The expected value of the maximum between random variables and a constant is given by:

and therefore .

We have:

We obtain:

In particular, so that .

Now, we compute . We have

where is the unique root of . We deduce that

We conclude that

What is played at equilibrium? In the best equilibrium, both players pick if and only if , whereas in the worst equilibrium, both players pick if and only if . Competition induces the players to pick with relatively low values in the worst equilibrium, and this decreases the sum of expected payoffs.

No recall case.

Now, we turn to reduce the formulas obtained in Theorem 3 for the particular case where the values are uniformly distributed in the interval . Recall that , for and . To obtain the expressions of and for the uniform case, we use the following technical result.

Lemma 3.

If , then .

Proof.

It is enough to show that . We prove that by induction on .

Notice that and thus . On the other hand, and putting all together we have that

and then the Lemma holds for

Let us assume now that the inequality holds for and we prove that it also holds for that is:

By Theorem 3, we have that

where the second equality and the inequality follow by the induction hypothesis.

Therefore, we have that and the proof is completed. ∎

Notice that by definition, for all , and therefore, by Lemma 3 we conclude that if then . Thus, applying Theorem 3, the sum of payoffs for the worst SPE for is

If the samples are uniformly distributed in the interval , the recursive formulas given in Theorem 3 are easy to implement numerically,

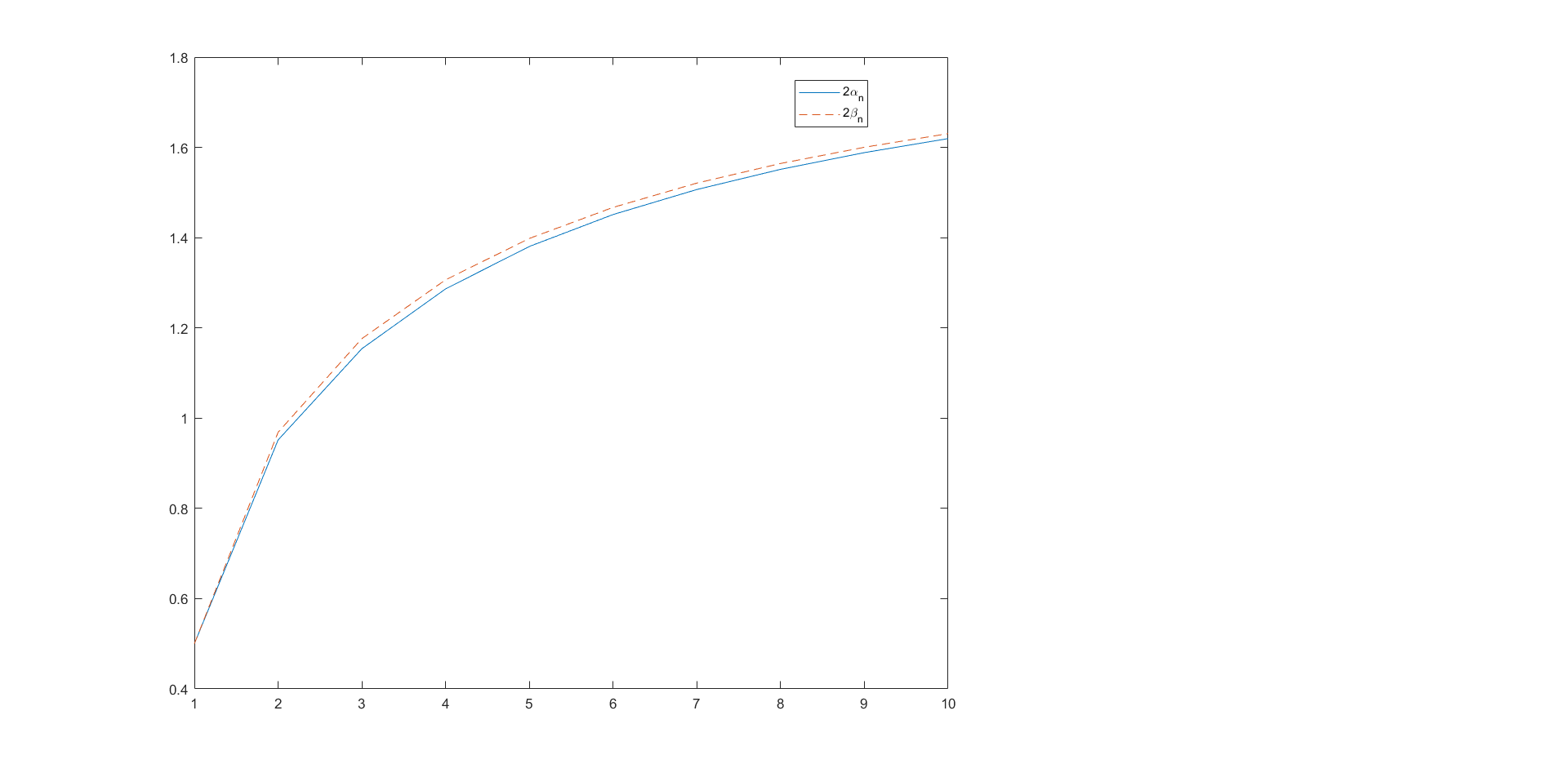

In Table 3 we expose the values of and for from 1 to 4 and , whereas in Figure 2 we compare the sum of payoffs for the best and worst SPE for up to 10.

| n=1 | 0.25 | 0.25 | 0.25 |

| n=2 | 0.4688 | 0.4759 | 0.4844 |

| n=3 | 0.5747 | 0.5803 | 0.5881 |

| n=4 | 0.6419 | 0.6465 | 0.6533 |

3.5.2 Comparison of model variants

We know by Theorem 4 that for every , meaning that having full recall is advantageous to the players. We quantify this difference for small values of numerically,

In Table 4 we present the values of and for arrivals. The values corresponding to the no recall case were computed using the formulas obtained in the former section, whereas for the full recall case, for the values were obtained explicitely and for numerically via discretization.

From the values of Table 4 we can see that under the full recall case, each player has an advantage compare to the no recall case of between 3 and 5 for , between and for , between and for and between and for .

| n=1 | 0.25 | 0.25 | 0.25 | 0.25 |

| n=2 | 0.5 | 0.5 | 0.4759 | 0.4844 |

| n=3 | 0.6244 | 0.6245 | 0.5803 | 0.5881 |

| n=4 | 0.6989 | 0.699 | 0.6465 | 0.6533 |

| n=5 | 0.7484 | 0.7486 | 0.6932 | 0.6991 |

3.5.3 Efficiency of equilibria

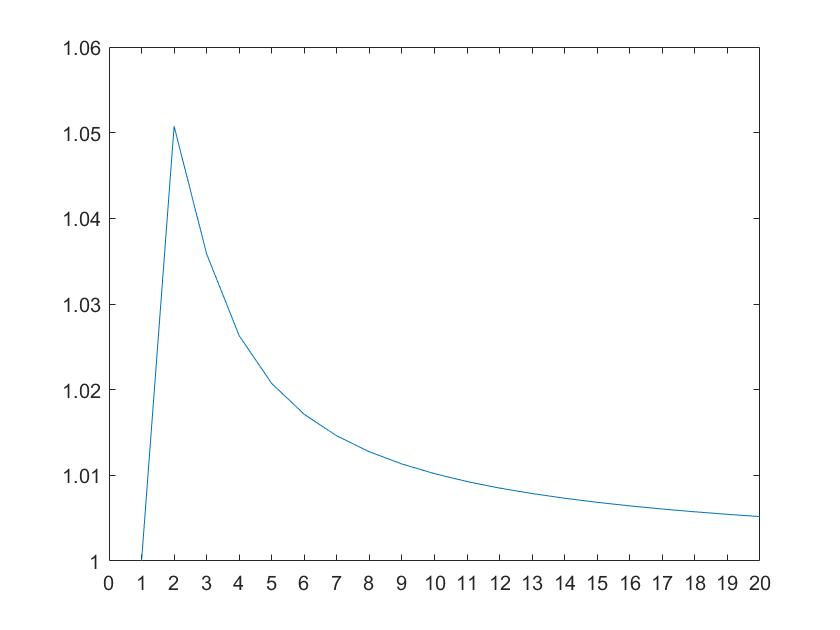

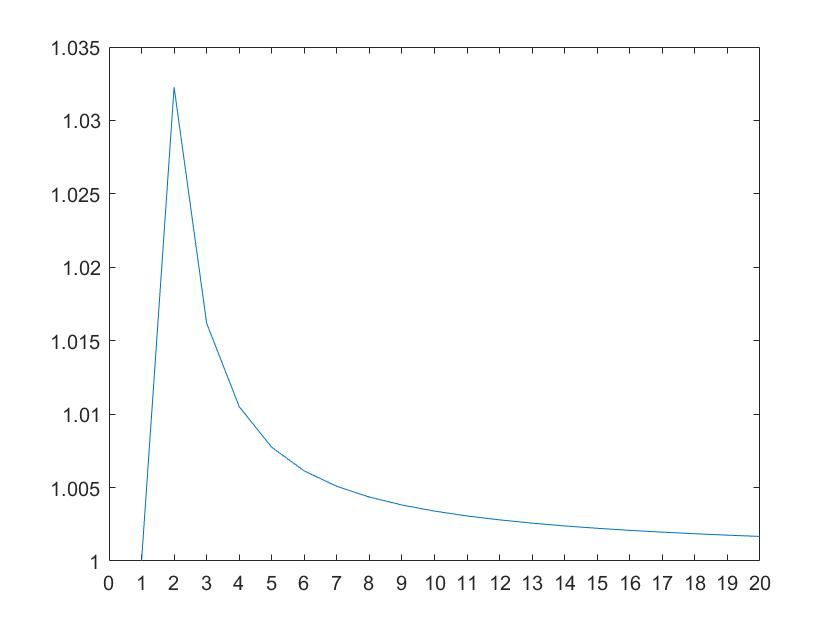

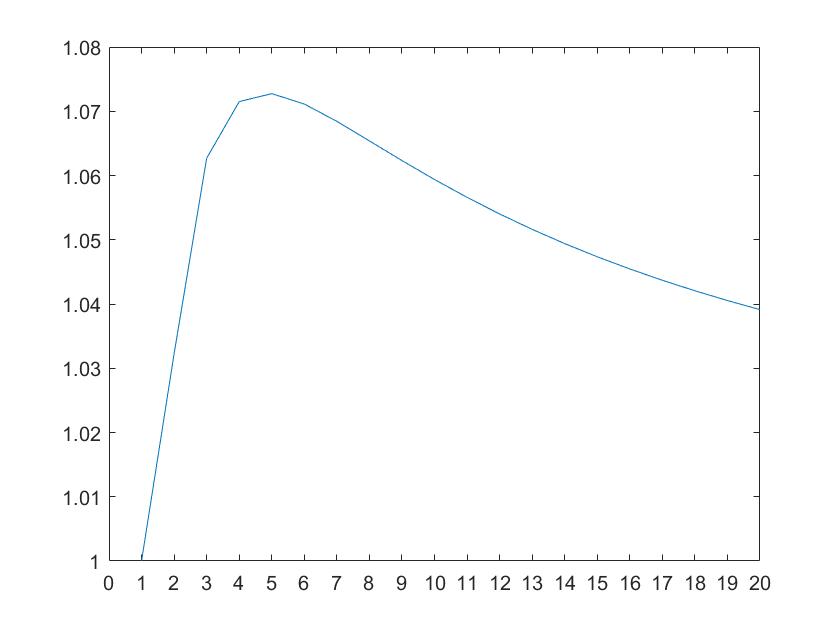

We represent in Table 5 the values of the ratios and for and up to 5 in both settings. We notice that the ratios are close to 1, i.e. equilibria are close to be efficient in both model variants, being more efficient in the full recall case. We highlight here that these ratios are a measure of efficiency of equilibria for each game, but not between the two different games. That is to say, it is not correct to say that one setting is better than the other by comparing the PoA or PoS, because for each game, these ratios are computed in a different way (the numerator are different). For such a comparison, we could use the value of PR, but comparing the PR for both problems is equivalent to compare and , which is a comparison we already made.

| PoAn(F) | PoSn(F) | PRn(F) | ||||

|---|---|---|---|---|---|---|

| Full Recall | No Recall | Full Recall | No Recall | Full Recall | No Recall | |

| n=2 | 1 | 1.0507 | 1 | 1.0323 | 1 | 1.0323 |

| n=3 | 1.000823 | 1.0299 | 1.0008 | 1.0161 | 1.0008 | 1.0627 |

| n=4 | 1.00157 | 1.0212 | 1.00143 | 1.0105 | 1.00143 | 1.0714 |

| n=5 | 1.0021 | 1.0164 | 1.00187 | 1.0077 | 1.00187 | 1.0728 |

Another question we address here is the number of arrivals that gives the worst gaps, in the no recall case for which the numerics are easier. We obtain that, for both the Price of Anarchy and Price of Stability, the ratios reach their maximum when , see Figures 3(a) and 3(b). This result is somehow intuitive: as we are in the no recall case, there exists a positive probability of getting nothing and then the smaller the number of arrivals, the more likely this seems to happen. Regarding the Prophet Ratio, we also compute it as a function of (see Figure 3(c)), and we obtained that the maximum is reached when . Here, the result is more surprising.

4 Proofs

In this section we provide the proofs omitted in Section 3.

4.1 Omitted proofs from Section 3.2

Full recall case.

In this section, we prove Theorems 1 and 2. Before that, we need some preliminary results stating properties of the game defined in Section 3.2. Recall that this game is defined as with arrivals but with two initial values already present in the market.

At first, in order to study the SPEP of , note that this game has the same SPEP as the game which is identical to and terminates at the first time a player gets an item or at stage . If the game terminates because one player did get an item, the payoff of the other player is the value of the one-player continuation problem, and the payoff of the players if none of them did stop strictly before stage is the expected payoff given by the pair of strategies ”bid for the best available item”. Indeed, it is easy to check that in both these situations the SPEP in the continuation games are unique and correspond to the payoffs of this auxiliary game. In the following, we assume that is the auxiliary game. In this game, an history is just a sequence of values and the strategy of player at time is a measurable map from histories into the probabilities over . We use the same identification for the game .

Given an history of length , let denote the subgame of starting at stage after observing in which the two players are still present and the set of SPEP of this game.

In the following, variables will denote independent variables with distribution , and .

Without loss of generality, we assume that (otherwise the set of equilibrium payoffs is reduced to ).

We state now without proofs some properties of SPEP which follow easily from usual arguments in dynamic game theory. Recall that if is a set-valued map, is defined by

Lemma 4.

The following properties hold:

-

1.

-

2.

If is an history of length , then where and denote the first and second largest items in respectively.

-

3.

with if and only if there exists such that is a mixed Nash equilibrium payoff of the finite game with payoff matrix:

Player Player Table 6: Payoff matrix of . -

4.

Similarly, is a pair of first-stage strategies of some SPE in with payoff in if and only if there exists such that is a mixed Nash equilibrium of the matrix game with payoff .

The first point follows from the fact that any strategy in any subgame of which bids with positive probability for one of the two initial items with value is strictly dominated by the modified strategy which waits until the last stage and bids for the best available item whenever the initial strategy bids for an item with value zero. Therefore such strategies are not played in any equilibrium in and the result follows easily. The other points can be proven by induction on using the recursive structure of SPE, the one-shot deviation principle and measurable selection arguments.

In the following proposition, we prove that if a player prefers to pass instead of take given that the other player takes , then he prefers to pass instead of take if the other player passes.

Proposition 2.

Let , and . If then and . Similarly, if then and .

By the symmetry of the game, it is enough to prove the inequality for , then the same arguments will hold for .

To prove the Proposition, we need the following two lemmas.

Lemma 5.

If are integrable random variables and a real number such that (resp. ), then it holds that (resp. ).

Proof.

Let us first prove that if are real numbers, then

| (4) |

Indeed, we show that for the four possible cases:

Then, defining the random variable and using the inequality above,

| (5) |

Take and , then by (5) we have that

| (6) |

But

-

i)

,

-

ii)

, and

-

iii)

and thus (6) means that

which is equivalent to

In particular, the later implies that

and due to , we conclude that

and the result follows. The case with strict inequalities is similar. ∎

Lemma 6.

Under the same notation and assumptions as in Proposition 2, we have

where is a random variable with distribution , and for some i.i.id sequence of samples of .

Proof.

By assumption, for some measurable function such that is the expected payoff of player 1 in some SPE in . We will obtain a lower bound for by providing a lower bound for the payoff associated to a particular strategy in .

To this end, suppose that Player 1 plays the following strategy:

-

1.

If , bid for .

-

2.

If , wait until the end and get at least the second best item.

Define , . Since the second best item in has expected value , we deduce that the payoff of player , independently of the strategy of player , is at least if and if . We deduce that

Note that the last term is at least because for . Therefore, we conclude that

and the result follows. ∎

Proof of Proposition 2.

Take with distribution independent of some i.i.d sequence of variables distributed according to , and . Then , and applying Lemma 5 we have

On the other hand, by independence and since , we have

By Lemma 6 . Putting all together we obtain and the proof is completed. The case with the strict inequality is similar. ∎

The next result allows to reduce the analysis of to a smaller matrix game.

Lemma 7.

Let in , a positive natural number, and . The game has the same Nash equilibrium payoffs as the game with matrix:

| Player | |||

|---|---|---|---|

| Player | |||

Proof.

We first consider the case .

For both players, the strategy is strictly dominated by mixed strategy consisting on playing with probability and pass with probability . Due to the symmetry of the payoffs’ matrix, it is enough to show that for one player (let us say player 1) the expected payoff if he plays with probability and passes with probability is strictly higher that the expected payoff he obtains if he plays . Note that because we have that:

-

i-

-

ii-

and

-

iii-

where the last inequality follows because . Indeed, in any SPE, player obtains at least the second largest item (otherwise he could deviate to the strategy which does not bid until stage ), which is not smaller than in . We conclude that is a strictly dominated strategy for both players (due to the symmetry of the game), and the result follows.

If , we consider two subcases. If , then Proposition 2 implies that and , so that the strategies and are strictly dominated by . There is a unique Nash equilibrium with payoff . Since the same holds for the matrix game given in table 7, the result follows.

If , the actions and are equivalent in the sense that they induce the same payoffs. Eliminating leads to a matrix game with the same Nash equilibrium payoffs. ∎

Denoting , the payoff matrix introduced in Lemma 7 has the particular form exposed in Table 8. Thus, it is enough to compute the NE of this matrix game where are parameters which correspond to the expected continuation equilibrium payoffs for players.

| Player | |||

|---|---|---|---|

| Player | |||

We are now ready to prove Theorem 1.

Proof of Theorem 1.

Let us first analyze the game with , i.e. the case of continuation payoffs which belong to the diagonal in , given in Table 9 below where .

| Player | |||

|---|---|---|---|

| Player | |||

Let us compute the mixed Nash equilibria of this game. Using Proposition 2, and . We have that:

-

(a)

If , then is the unique NE with payoff .

-

(b)

If , there are two pure NE and and a symmetric mixed equilibrium in which both agents play with probability and pass with probability Furthermore, the equilibrium payoffs are:

-

(c)

If , then is the unique NE, and is the expected payoff.

-

(d)

If or , there are two pure NE and with payoffs:

-

(e)

If , then any profile is a NE with payoff .

From the analysis above we conclude that the set of NE payoffs of the game is contained in the diagonal.

We now prove by induction on that is also a subset of the diagonal, that is:

Ar first, , so the statement is correct for .

Let us assume that the statement is correct for for all pairs . Then, it implies that is also a subset of the diagonal. Therefore, by point 3) of Lemma 4 and the above analysis, we deduce that is a subset of the diagonal.

The first statement of the theorem is proved.

Let us now show that and , where is the projection of to its first coordinate in .

Note that from the analysis done above, we have that if or or , there is only one NE payoff but in the other cases we have multiple equilibrium payoffs. When playing a SPE, the expected payoff of the players when both pass depends on which equilibrium is played in the following stages of the game. It is known that, in general, we cannot assume that if “the worst” or “the best” equilibrium is played at each stage, that results in the worst or best equilibrium of the game. However, below we show that this is indeed true for the game we are considering and then the result will follow just computing the expected payoff corresponding to the best and worst equilibrium.

To this end, it is enough to prove that the expected payoff of a player is increasing in .

Define and consider the multivalued function defined by

Note that if , then

and thus and are respectively the ”best” and the ”worst” equilibrium payoffs for player in . Therefore, represents the ”best” and ”worst” NE payoffs for player in the game represented by Table 9.

We say that the multivalued function is non-decreasing in if for each such that and for , holds that and . Let us see that is non-decreasing in . To show that, fix , and take such that and , . We have the following cases:

-

(a)

If , then for and the result is obvious.

-

(b)

If , then and . Thus, and

-

(c)

If , then and the result is obvious.

-

(d)

If , then and , obtaining .

-

(e)

If , then or and , and the result follows.

Thus, we conclude that is non-decreasing in . The monotonicity property we proved for means that playing a “better” equilibrium in the continuation game gives a “better” equilibrium for and playing a “worse” equilibrium one gives a “worse” equilibrium for .

Precisely, define and by:

and represent the lowest and highest equilibrium expected payoffs of player in . As we aforementioned, we are interested in computing the expected payoff corresponding to the best and the worst NE of the game , which correspond to the extremes values of the set denoted and . Using the monotony of (and thus of and ) with respect to , is the lowest equilibrium payoff of , i.e. , when is the expected continuation payoff obtained by playing the lowest equilibrium in every continuation game, that is:

where . This completes the proof for and a the same analysis applies for . ∎

Remark 1.

Note that we did not use any assumption on the distribution except that it is supported by , therefore Theorem 1 holds when considering discrete distributions.

Proof of Theorem 2.

By Theorem 1, we know that .

Furthermore, and then and belongs to (we obtain them just taking and , respectively). To obtain the result is then enough to prove that the set is convex. To this end, let us define the function by

Notice that is continuous since is atomless, and , then using the intermediate value theorem all values between and are taken by . But belongs to for every by choosing equal to on and to on . Therefore is convex. ∎

No recall case.

We pass now to the no recall case and the goal is to prove Theorem 3.

Recall that the game is defined as , but there are stages: at the first stage, the players can bid for an item with value , and the items for the next stages are randomly drawn as in .

At first, in order to study the SPEP of , note that this game has the same SPEP as the game which is identical to but terminates at the first time a player gets an item (or after stage ). If the game terminates because one player did get an item, the payoff of the other player is the value of the one-player continuation problem. As for the full recall case, it is easy to check that if after a player gets an item, the SPEP in the continuation game are unique and correspond to the payoffs of this auxiliary game. In the following, we assume that is the auxiliary game. In this game, an history is just a sequence of values and the strategy of player at time is a measurable map from histories into the probabilities over . We use the same identification for the game .

Given an history of length , let denote the subgame of starting at stage after observing in which the two players are still present and the set of SPEP of this game.

In the following, variables will denote independent variables with distribution , and .

Without loss of generality, we assume that (otherwise the set of equilibrium payoffs is reduced to ).

As for the full recall case, we state without proofs some properties of SPEP which follow easily from usual arguments in dynamic game theory.

Lemma 8.

The following properties hold:

-

1.

and for , .

-

2.

If is an history of length , then where denotes the largest item in .

-

3.

if and only if there exists such that is a mixed Nash equilibrium payoff of the finite game with payoff matrix:

Player Player Table 10: ;Payoffs matrix of . where denotes the value of the decision problem with stages in a standard prophet setting.

-

4.

Similarly, is a pair of first-stage strategies of some SPE in with payoff if and only if there exists such that is a mixed Nash equilibrium of the matrix game with payoff .

Proof of Proposition 1..

The fact that is is symmetric with respect to the diagonal is a direct consequence of the fact the the game is symmetric.

To prove convexity, we can use the properties of the expectation of a set-valued map, also called the Aumann integral. Theorem 8.6.3 in [2] implies that the expectation of a set-valued map with non-empty closed values and compact graph from to with respect to an atomless measure on is a non-empty convex compact set.

At first, is non-empty compact convex. Then, is a set-valued map with non-empty closed values and compact graph using the classical properties of Nash equilibrium payoffs of matrix games. It follows that is non-empty compact convex. Let us assume that is non-empty compact convex. Let denote the set of Nash equilibrium payoffs of , then is a set-valued map with non-empty closed values and a compact graph, and thus is a set-valued map with non-empty closed values and a compact graph. We conclude that is a non-empty compact convex set. ∎

Below, we prove the theorem.

Proof of Theorem 3..

Given and a natural number, we consider the game defined in Section 3.2. We first analyze the game described in Table 10 with .

One first remark to do regarding this game, is that what a player gets if he stays alone in the game, that is , is at least what he gets if both stay. In other words, and .

Now, we use Table 10 and the remark above to study the NE of the game , depending on the relation between the parameters . It is easy to check that the following holds:

-

(a)

If , is the unique NE with payoff .

-

(b)

If , there is a unique NE payoff .

-

(c)

If there are two pure NE and , and a mixed equilibrium; with payoffs and , respectively, with .

-

(d)

If , the NE payoffs are and with .

-

(e)

If , the NE payoffs are and with .

-

(f)

If , the NE payoffs are and with .

-

(g)

If , is the unique NE with payoff .

-

(h)

If , is the unique NE with payoff .

-

(i)

If , is the unique NE with payoff .

-

(j)

If , the NE payoffs are and with .

-

(k)

If , the Ne payoffs are and with .

In particular, we are interested on computing the sum of the expected payoff corresponding to the best and the worst SPEs that is, and , respectively; as well as the worst payoff a player can get at equilibrium, that is .

Due to Proposition 1 we have that

and

Therefore, defining , and , it follows that it is enough to compute , and .

To prove the part of the theorem, we compute a recursive formula for . Define as the minimal NE payoff of player in the family of game when ranges through . It is clear from the previous characterization that . Using our previous analysis, notice that:

Since is atomless, it is sufficient to conclude that for

| (7) | |||||

and the first statement of Theorem 3 is proved.

Next, we compute as a function of and . Define as the maximal sum of payoffs in any NE on the family of game when ranges through , so that . We have:

Since is atomless, it is sufficient to conclude that for

| (8) |

and the second statement of the theorem is obtained.

It remains to compute As before, define as the minimal sum of payoffs in any NE on the family of game when ranges through , so that . Notice that if , the mixed equilibrium gives a worse sum of payoffs than the pure. We have:

Since is atomless, it is sufficient to conclude that for

| (9) |

where and , which is the third statement of the theorem.

Putting together all the foregoing analysis, we obtain the desired result, concluding the proof. ∎

4.2 Omitted proofs from Section 3.3

Proof of Lemma 1..

We assume that one player, let us say player 1, bid in the first stage if , and passes otherwise, where is the realization of the first random variable arrived. Let us show that player 1 obtain an expected payoff, namely , of at least , independently of what player 2 does, and therefore player 1 will obtain a payoff of at least playing any SPE.

We divide the proof in two cases:

Case 1.

Assume that Note that in this case, player 1 bids for and we have that

where is the event player 2 does not bid for M.

Notice that is lower bounded by and by and therefore we have that

where the second inequality holds because due to and the last equality because We conclude that if

Case 2.

Assume that In this case, we have that

where the second equality holds because and the last inequality because both and are at least when . Thus, we conclude that if .

Putting all together we obtain that and the proof is complete. ∎

Proof of Theorem 4.

Note that it is enough to prove that for all , where denotes the lowest SPE payoff in the full recall case and denotes the highest symmetric SPE payoff in the no recall case. To this end, we will prove by induction on that for all and for all , where is defined as in the statement of Theorem 1 and is defined by

where is the value of the decision problem in the no recall case with one decision-maker and arrivals.

First, notice that , and , and thus and for all , concluding that for all .

We assume now that for all and we prove that for all . We divide the proof in two cases depending on if is higher than or not.

Case 1.

Assume that . In this case, we have that because Thus, by the definition of we have that

| (10) |

On the other hand, holds that

| (11) |

where the equality follows from using the definition of when and the inequality hols because .

Case 2.

Assume that To prove that , we show that and that /2. The latter holds by Lemma 1. On the other hand,

where the first equality follows from the definition of for , the first inequality holds due to the monotonicity of the function in both components, the second inequality follows from the induction hypothesis and the last equality from the definition of

Therefore, we conclude that for all .

Putting all together we obtain that for all and the desired result follows. ∎

4.3 Omitted proofs from Section 3.4

The main result in Section 3.4 we prove here is Theorem 5 and then we work on the competitive selection problem with no recall and two arrivals.

Before going to the proof, we obtain an expression for the price of anarchy and price of stability if the random variables are distributed according to , namely and respectively.

Regarding the price of stability, we need to compute

where is obtained from equation (8) by taking . That is:

Now, due to , we have that . Noting that and putting all together we have

On the other hand, and therefore

| (12) |

Regarding the price of anarchy, we need to compute

where follows from equation (9) by taking . After some algebra, we obtain

| (13) | |||||

and thus

| (14) |

Also, we can write the inverse of price of anarchy as follows:

| (15) |

We now prove Theorem 5 using the formulas obtained above.

Proof of Theorem 5..

Regarding the price of anarchy, by equation (14) and using that if , we have

But, and thus

obtaining the desire inequalities.

To prove the tightness of the bound, let us take and two small positive real numbers and consider the random variable , where

Note that when goes to ,

where represents the c.d.f. of , and therefore it is enough to prove that

when goes to .

The c.d.f. of is given by

and the expected value is

Therefore, after some algebra, it follows that

which converges to when , and therefore we obtain price of stability

On the other hand, note that by definition, for each distribution , holds that , and then , where is the upper bound we already prove. Therefore, the bound is tight also for the price of anarchy. ∎

References

- [1] F. B. Abdelaziz and S. Krichen. Optimal stopping problems by two or more decision makers: a survey. Computational Management Science, 4(2):89–111, 2007.

- [2] J.-P. Aubin and H. Frankowska. Set-valued analysis. Springer Science & Business Media, 2009.

- [3] S. Chawla, J. D. Hartline, D. L. Malec, and B. Sivan. Multi-parameter mechanism design and sequential posted pricing. In Proceedings of the forty-second ACM symposium on Theory of computing, pages 311–320, 2010.

- [4] J. Correa, P. Foncea, R. Hoeksma, T. Oosterwijk, and T. Vredeveld. Posted price mechanisms for a random stream of customers. In Proceedings of the 2017 ACM Conference on Economics and Computation, pages 169–186, 2017.

- [5] J. Correa, P. Foncea, D. Pizarro, and V. Verdugo. From pricing to prophets, and back! Operations Research Letters, 47(1):25–29, 2019.

- [6] T. Ezra, M. Feldman, and R. Kupfer. On a competitive secretary problem with deferred selections. arXiv preprint arXiv:2007.07216, 2020.

- [7] T. Ezra, M. Feldman, and R. Kupfer. Prophet inequality with competing agents. arXiv preprint arXiv:2107.00357, 2021.

- [8] P. Freeman. The secretary problem and its extensions: A review. International Statistical Review/Revue Internationale de Statistique, pages 189–206, 1983.

- [9] D. Fudenberg and J. Tirole. Game theory, 1991. Cambridge, Massachusetts, 393(12):80, 1991.

- [10] M. T. Hajiaghayi, R. Kleinberg, and T. Sandholm. Automated online mechanism design and prophet inequalities. In AAAI, volume 7, pages 58–65, 2007.

- [11] N. Immorlica, R. Kleinberg, and M. Mahdian. Secretary problems with competing employers. In International Workshop on Internet and Network Economics, pages 389–400. Springer, 2006.

- [12] R. P. Kertz. Stop rule and supremum expectations of iid random variables: a complete comparison by conjugate duality. Journal of multivariate analysis, 19(1):88–112, 1986.

- [13] U. Krengel and L. Sucheston. On semiamarts, amarts, and processes with finite value. Probability on Banach spaces, 4:197–266, 1978.

- [14] D. V. Lindley. Dynamic programming and decision theory. Journal of the Royal Statistical Society: Series C (Applied Statistics), 10(1):39–51, 1961.

- [15] J. D. Petruccelli. Best-choice problems involving uncertainty of selection and recall of observations. Journal of Applied Probability, 18(2):415–425, 1981.

- [16] T. Roughgarden and É. Tardos. How bad is selfish routing? Journal of the ACM (JACM), 49(2):236–259, 2002.

- [17] E. Samuel-Cahn. Comparison of threshold stop rules and maximum for independent nonnegative random variables. the Annals of Probability, pages 1213–1216, 1984.

- [18] T. Sweet. Optimizing a single uncertain selection by recall of observations. Journal of applied probability, 31(3):660–672, 1994.

- [19] M. C. Yang. Recognizing the maximum of a random sequence based on relative rank with backward solicitation. Journal of Applied Probability, 11(3):504–512, 1974.