Predicting the Last Zero before an exponential time of a Spectrally Negative Lévy Process

Abstract

Given a spectrally negative Lévy process, we predict, in a sense, the last passage time of the process below zero before an independent exponential time. This optimal prediction problem generalises Baurdoux and Pedraza, (2020) where the infinite horizon problem is solved. Using a similar argument as that in Urusov, (2005), we show that this optimal prediction problem is equivalent to solving an optimal prediction problem in a finite horizon setting. Surprisingly (unlike the infinite horizon problem) an optimal stopping time is based on a curve that is killed at the moment the mean of the exponential time is reached. That is, an optimal stopping time is the first time the process crosses above a non-negative, continuous and non-increasing curve depending on time. This curve and the value function are characterised as a solution of a system of non-linear integral equations which can be understood as a generalisation of the free boundary equations (see e.g. Peskir and Shiryaev, (2006) Chapter IV.14.1) in the presence of jumps. As an example, we calculate numerically such curve in the Brownian motion case and a compound Poisson process with exponential sized jumps perturbed by a Brownian motion.

Keywords: Lévy processes, optimal prediction, optimal stopping.

Mathematics Subject Classification (2000): 60G40, 62M20

1 Introduction

The study of last exit times has received much attention in several areas of applied probability, e.g. risk theory, finance and reliability in the past few years. Consider the Cramér–Lundberg process, a process consisting of a deterministic drift and a compound Poisson process with only negative jumps (see Figure 1), which is typically used to model the capital of an insurance company. Of particular interest is the moment of ruin, which is defined to refer to the first moment when the process becomes negative. Within the framework of the insurance company having sufficient funds to endure negative capital for a considerale amount of time, another quantity of interest is the last time, that the process is below zero. In a more general setting, we can consider a spectrally negative Lévy process instead of the classical risk process. Several studies, for example Baurdoux, (2009) and Chiu and Yin, (2005) studied the Laplace transform of the last time before an exponential time that a spectrally negative Lévy process is below some given level.

Last passage time is increasingly becoming a vital factor in financial modeling as shown in Madan et al., 2008a and Madan et al., 2008b where the authors concludes that the price of a European put and call options, modelled by non-negative and continuous martingales that vanish at infinity, can be expressed in terms of the probability distributions of some last passage times.

Another application of last passage times is in degradation models. Paroissin and Rabehasaina, (2013) propose a spectrally positive Lévy process to model the ageing of a device in which they consider a subordinator perturbed by an independent Brownian motion. A motivation for considering this model is that the presence of a Brownian motion can model small repairs of the device and the jumps represent major deterioration. In the literature, the failure time of a device is defined as the first hitting time of a critical level . An alternative approach is to consider instead, the last time that the process is under the level since the paths of this process are not necessarily monotone and this allows the process to return below the level after it goes above .

The aim of this work is to predict the last time a spectrally negative Lévy process is below zero before an independent exponential time where the terms “to predict” are understood to mean to find a stopping time that is closest (in sense) to this random time. This problem is an example of the optimal prediction problems which have been widely investigated by many. Graversen et al., (2001) predicted the value of the ultimate maximum of a Brownian motion in a finite horizon setting whereas Shiryaev, (2009) focused on the last time of the attainment of the ultimate maximum of a (driftless) Brownian motion and proceeded to show that it is equivalent to predicting the last zero of the process in this setting. The work of the latter was generalised by du Toit et al., (2008) for a linear Brownian motion. Bernyk et al., (2011) studied the time at which a stable spectrally negative Lévy process attains its ultimate supremum in a finite horizon of time and this was later generalised by Baurdoux and van Schaik, (2014) for any Lévy process in infinite horizon of time. Investigations on the time of the ultimate minimum and the last zero of a transient diffusion process were carried out by Glover et al., (2013) and Glover and Hulley, (2014) respectively within a subclass of functions.

In Baurdoux and Pedraza, (2020) the last zero of a spectrally negative Lévy process in a infinite horizon setting is predicted. It is shown that the an optimal stopping time that minimises the last zero of a spectrally negative Lévy process with drift is the first time the Lévy process crosses above a fixed level which is characterised in terms of the cumulative distribution of the overall infimum of the process. As is in the case in the Canadisation of American type options (see e.g. Carr, (1998)), given the memoryless property of the exponential distribution, one would expect that the generalisation of the aforementioned problem to an exponential time horizon would result in an infinite horizon optimal prediction problem, and hence have a non time dependent solution. However, it turns out that this is not the case. Indeed, we show the existence of a continuous, non-increasing and non-negative boundary such that an optimal stopping time is given by the first passage time, before the median of the exponential time, above such curve. The proof relies on solving an equivalent (finite horizon) optimal stopping problem that depends on time and the process itself. Moreover, based on the ideas of du Toit et al., (2008) we characterise the boundary and the value function as the unique solutions of a system of non-linear integral equations. Such system can be thought as a generalisation of the free boundary equation (see e.g. Peskir and Shiryaev, (2006), Section 14) allowing for the presence of jumps. We consider two examples where numerical calculations are implemented to find the optimal boundary.

This paper is organised as follows. In Section 2 we introduce some important notation regarding Lévy processes and we outline some known fluctuation identities that will be useful later. We then formulate the optimal prediction problem and we prove that it is equivalent to an optimal stopping problem. Section 3 is dedicated to the solution of the optimal stopping problem. The main result of this paper is stated in Theorem 3.9 and its proof is detailed in Section 3.1. The last section makes use of Theorem 3.9 to find numerical solution of the optimal stopping problem for the Brownian motion with drift case and a compound Poisson process perturbed by a Brownian motion.

2 Prerequisites and Formulation of the Problem

We start this section by introducing some important notations and we give an overview of some fluctuation identities of spectrally negative Lévy processes. Readers can refer to Bertoin, (1998), Sato, (1999) or Kyprianou, (2014) for more details about Lévy processes.

A Lévy process is an almost surely càdlàg process that has independent and stationary increments such that . Every Lévy process is also a strong Markov -adapted process. For all , denote as the law of when started at the point , that is, . Due to the spatial homogeneity of Lévy processes, the law of under is the same as that of under .

Let be a spectrally negative Lévy process, that is, a Lévy process starting from with only negative jumps and non-monotone paths, defined on a filtered probability space where is the filtration generated by which is naturally enlarged (see Definition 1.3.38 in Bichteler, (2002)). We suppose that has Lévy triplet where , and is a measure (Lévy measure) concentrated on satisfying .

Let be the Laplace exponent of defined as

Then exists in , it is strictly convex and infinitely differentiable with and . From the Lévy–Khintchine formula, we know that takes the form

for all . Moreover, from Lévy–Itô decomposition, we know that there exists a Brownian Motion and an independent Poisson random measure on with intensity such that for each ,

Denote as the first time the process is above the level , i.e.,

Then it can be shown that its Laplace transform is given by

| (1) |

where corresponds to the right inverse of , which is defined by

for any .

Now we introduce the scale functions. This family of functions is the key to the derivation of fluctuation identities for spectrally negative Lévy processes. The notation used is mainly based on Kuznetsov et al., (2013) and Kyprianou, (2014) (see Chapter 8). For , the function is such that for and is characterised on as a strictly increasing and continuous function whose Laplace transform satisfies

We further define the function by

Denote as the first passage time of of the set , that is,

It turns out that the Laplace transform of can be written in terms of the scale functions. Specifically,

| (2) |

for all and . It can be shown that the paths of are of finite variation if only if

In such case, we may write

where

| (3) |

Note that monotone processes are excluded from the definition of spectrally negative Lévy processes so we assume that when is of finite variation. The value of at zero depends on the path variation of . In the case where is of infinite variation we have that , otherwise

| (4) |

For any and , the -potential measure of killed upon entering the set is absolutely continuous with respect to the Lebesgue measure. A density is given for all by

| (5) |

Let be the last passage time below zero before an exponential time, i.e.

| (6) |

where is an exponential random variable with parameter . Here, we use the convention that an exponential random variable with parameter is taken to be infinite with probability . In the case of , we simply denote .

Note that -a.s. for all . However, in the case where , could be infinite. Therefore, we assume that throughout this paper. Moreover, we have that has finite moments for all .

Remark 2.1.

Since is a spectrally negative Lévy process, we can exclude the case of a compound Poisson process and hence the only way of exiting the set is by creeping upwards. This tells us that in the event of and that holds -a.s.

Clearly, up to any time the value of is unknown (unless is trivial), and it is only with the realisation of the whole process that we know that the last passage time below has occurred. However, this is often too late: typically, at any time , we would like to know how close we are to the time so we can take some actions based on this information. We search for a stopping time of that is as “close” as possible to . Consider the optimal prediction problem

| (7) |

where is the set of all stopping times.

Note that the random time is only measurable so it is not immediately obvious how to solve the optimal prediction problem by using the theory of optimal stopping. Hence, in order to find the solution (and hence prove Theorem 2.3) we solved an equivalent optimal stopping problem. In the next Lemma we establish an equivalence between the optimal prediction problem (7) and an optimal stopping problem. This equivalence is mainly based on the work of Urusov, (2005).

Lemma 2.2.

Suppose that is a spectrally negative Lévy process. Let be the last time that is below the level zero before an exponential time with , as defined in (6). Consider the optimal stopping problem given by

| (8) |

where the function is given by for all . Then the stopping time which minimises (7) is the same which minimises (8). In particular,

| (9) |

Proof.

Fix any stopping time . We have that

From Fubini’s theorem and the tower property of conditional expectations, we obtain

Note that in the event of , we have so that

On the other hand for , as a consequence of Remark 2.1, the event is equal to (up to a -null set). Hence, we get that for all that

where the last equality follows from the lack of memory property of the exponential distribution and the Markov property for Lévy process. Hence, we have that

where for all , . Then, since is independent of , we have that for ,

where the last equality follows from equation (2). Thus,

Therefore,

The conclusion holds. ∎

Note that evaluating , the function coincides with the gain function found in Baurdoux and Pedraza, (2020) (see Lemma 3.2 and Remark 3.3). In order to find the solution to the optimal stopping problem (8) (and hence (7)), we extend its definition to Lévy process (and hence strong Markov process) in the following way. Define the function as

| (10) |

So that

The next theorem states the solution of the optimal stopping theorem (10) and hence the solution of (7).

Theorem 2.3.

Let be any spectrally negative Lévy process and an exponential random variable with parameter independent of . There exists a non increasing and continuous curve such that , where and the infimum in (10) is attained by the stopping time

where . Moreover, the function is uniquely characterised as in Theorem 3.9.

3 Solution to the optimal stopping problem

In this section we solve the optimal stopping problem (10). The proof relies on showing that defined in Theorem 2.3 is indeed an optimal stopping time by using the general theory of optimal stopping and properties of the function . Hence, some properties of are derived. The main contribution of this section (Theorem 3.9) characterises and as the unique solution of a non-linear system of integral equations within a certain family of functions.

Recall that the is given by

From the proof of Lemma 2.2 we note that can be written as,

where is the distribution function of the positive random variable given by

| (11) |

for all . Now we give some intuitions about the function . Recall that for all , and are continuous and strictly increasing functions on such that and for . From the above, equation (11) and from the fact that is a distribution function, we have that for a fixed , the function is strictly increasing and continuous in with a possible discontinuity at depending on the path variation of . Moreover, we have that for all . For and , we have that the function takes the form . Similarly, from the fact that for all , we have that for a fixed the function is continuous and strictly increasing on . Furthermore, from the fact that , we have that the function is bounded by

| (12) |

which implies that . Recall that is defined as the median of the random variable , that is,

Hence from (12) we have that for all and . The above observations tell us that, to solve the optimal stopping problem (10), we are interested in a stopping time such that before stopping, the process spends most of its time in the region where is negative, taking into account that can live in the set and then return back to the set . The only restriction that applies is that if a considerable amount of time has passed, then for all .

Recall that the function is defined as

| (13) |

Hence, we can see that the function is a non-increasing continuous function on such that and for . Moreover, from the fact that for , we have that for all .

In order to characterise the stopping time that minimises (10), we first derive some properties of the function .

Lemma 3.1.

The function is non-drecreasing in each argument. Moreover, for all and . In particular, for any with and for all .

Proof.

First, note that follows by taking in the definition of . Moreover, since on we have that vanishes on . The fact that is non-decreasing in each argument follows from the non-decreasing property of the functions and as well as the monotonicity of the expectation. Moreover, using standard arguments we can see that .

Next we will show that for all and for all . Note that if and only if . Then for all we have that

Hence, for all and

The term in the last integral is non-negative, so we obtain for all and that

∎

By using a dynamic programming argument and the fact that vanishes on the set we can see that

so that (since ) we have that for all and ,

Moreover, as a consequence of the properties of we have that the function is upper semi-continuous we can see that is upper semi-continuous (since is the infimum of upper semi-continuous functions). Therefore, from the general theory of optimal stopping (see Peskir and Shiryaev, (2006) Corollary 2.9) we have that an optimal stopping time for (10) is given by

| (14) |

where is a closed set.

Hence, from Lemma 3.1, we derive that , where the function is given by

for each . It follows from Lemma 3.1 that is non-increasing and for all . Moreover, for , since for all and , giving us . In the case that , we have that is finitely valued as we will prove in the following Lemma.

Lemma 3.2.

Let . The function is finitely valued for all .

Proof.

For any and fix , consider the optimal stopping problem,

where is the set of all stopping times of bounded by . From the fact that for all and , and that (under for all ), we have that

| (15) |

for all . Hence it suffices to show that there exists (finite) sufficiently large such that for all .

It can be shown that an optimal stopping time for is , the first entry time before to the set . We proceed by contradiction, assume that , then . Hence, by the dominated convergence theorem and the spatial homogeneity of Lévy processes we have that

which is a contradiction. Therefore, we conclude that for each , there exists a finite value such that . ∎

Remark 3.3.

From the proof of Lemma 3.2, we find an upper bound of the boundary . Define, for each , . Then it follows that is a non-increasing finite function such that

for all .

Next we show that the function is continuous.

Lemma 3.4.

The function is continuous. Moreover, for each , is Lipschitz on and for every , is Lipschitz on .

Proof.

First, we are showing that, for a fixed , the function is Lipschitz on . Recall that if , for all so the assertion is clear. Suppose that . Let and define . Since is optimal in (under ) we have that

Define the stopping time

Then we have that (since is a non-increasing function). From the fact that is non-decreasing, we obtain that for ,

Using Fubini’s theorem and a density of the potential measure of the process killed upon exiting (see equation (5)) we get that

where in the last inequality, we used the fact that is strictly increasing and non-negative and that vanishes at . By an integration by parts argument, we obtain that

Moreover, it can be checked that (see Kuznetsov et al., (2013) lemma 3.3) the function is a continuous function in the interval such that

This implies that there exist a constant such that for every , . Then we obtain that for all ,

On the other hand, since for all we have that for all , . Hence we obtain that for all and ,

| (16) |

Therefore we conclude that for a fixed , the function is Lipschitz on .

Using a similar argument and the fact that the function is Lipschitz continuous on we can show that for any ,

and therefore is Lipschitz continuous for all . ∎

In order to derive more properties of the boundary , we first state some auxiliary results. Recall that if , the set of real bounded functions on with bounded derivatives, the infinitesimal generator of is given by

| (17) |

Let be the continuation region. Then we have that the value function satisfies a variational inequality in the sense of distributions. The proof is analogous to the one presented in Lamberton and Mikou, (2008) (see Proposition 2.5) so the details are omitted.

Lemma 3.5.

Fix . The distribution is non-negative on . Moreover, we have that on .

We define a special function which is useful to prove the left-continuity of the boundary . For , we define an auxiliary function in the set . Let

| (18) |

From the fact that vanishes on and that is finite on sets of the form for we can see that for all . Moreover, by the Lemma above and the properties of and , it can be shown that is strictly positive, continuous and strictly increasing (in each argument) in the interior of .

Now we are ready to give further properties of the curve in the set .

Lemma 3.6.

The function is continuous on . Moreover we have that .

Proof.

The method proof of the continuity of in is heavyly based on the work of Lamberton and Mikou, (2008) (see Theorem 4.2, where the continuity of the boundary is shown in the American option context) so is omitted.

We then show that the limit holds. Define . We obtain since for all . The proof is by contradiction so we assume that . Note that for all , we have that and . Moreover, we have that

in the sense of distributions on . Hence, by continuity, we can derive, for , that on the interval . Hence, by taking we obtain that

in the sense of distributions, where we used the continuity if and , the fact that for all and that for all . Note that we have got a contradiction and we conclude that . ∎

Define the value

| (19) |

Note that in the case where is a process of infinite variation, we have that the distribution function of the random variable , , is continuous on , strictly increasing and strictly positive in the open set with . This fact implies that the inverse function of exists on and then function can be written for as

Hence we conclude that for all . Therefore, when is a process of infinite variation, we have for all and hence . For the case of finite variation, we have that which implies that for all and for all . In the next lemma, we characterise its value.

Lemma 3.7.

Let and be a process of finite variation. We have that for all and ,

Moreover, for any Lévy process, is given by

| (20) |

where is given by

for all and .

Proof.

Assume that is a process of finite variation. We first show that

for all and . The case is straightforward since for all . The case follows from the Lipschitz continuity of the mapping , that is finite on intervals away from zero and since when is of finite variation. Moreover, from Lemma 3.5, we obtain that

on in the sense of distributions, where the last inequality follows since is non-decreasing in each argument and is defined in (3). Then by continuity of the functions and (recall that is at least continuous on and right-continuous at points of the form for ) we can derive

| (21) |

for all .

Next, we show that the set is non empty. We proceed by contradiction, assume that for all so that . Taking in (21) and applying dominated convergence theorem, we obtain that

where the strict inequality follows from since is of finite variation. Therefore, we observe a contradiction which shows that . Moreover, by the definition, we have that .

Next we find an expression for when and . Since for all , we have that

| (22) |

where the first equality follows since for all and for all . Hence, in particular, we have that for all and .

We show that (20) holds. From the discussion after Lemma 3.5, we know that

for all and . Then by taking , making use of the right continuity of , continuity of (see Lemma 3.4) and applying dominated convergence theorem, we derive that

In particular, if , (20) holds since (for all ) and are non-decreasing functions. If , taking in (21) gives us

Hence, we have that with (20) becoming clear due to the fact that is non-decreasing. If is a process of infinite variation, we have that for all and therefore for all and which implies that

∎

Now we prove that the derivatives of exist at the boundary for those points in which is strictly positive.

Lemma 3.8.

For all , the partial derivatives of at the point exist and are equal to zero, i.e.,

Proof.

First, we prove that the assertion in the first argument. Using a similar idea as in Lemma 3.4, we have that for any , and ,

where is the optimal stopping time for and the second inequality follows since is non increasing. Hence, by (1) and continuity of we obtain that

Now we show that the partial derivative of the second argument exists at and is equal to zero. Fix any time , and (without loss of generality, we assume that ). By a similar argument that as provided in Lemma 3.4, we obtain that

Dividing by , we have that for and that

where

By using that and are non-decreasing, that (and hence ) has left and right derivatives and the dominated convergence theorem we can show that for , for each . Hence, we have that

proving that is differentiable at with for .

∎

The next theorem looks at how the value function and the curve can be characterised as a solution of non-linear integral equations within a certain family of functions. These equations are in fact generalisations of the free boundary equation (see e.g. Peskir and Shiryaev, (2006) Section 14.1 in a diffusion setting) in the presence of jumps. It is important to mention that the proof of Theorem 3.9 is mainly inspired by the ideas of du Toit et al., (2008) with some extensions to allow for the presence of jumps.

Theorem 3.9.

Let be a spectrally negative Lévy process and let be as characterised in (20). For all and , we have that

3.1 Proof of Theorem 3.9

Since the proof of Theorem 3.9 is rather long, we split it into a series of Lemmas. This subsection is entirely dedicated for this purpose. With the help of Itô formula and following an analogous argument as in Lamberton and Mikou, (2013) (in the infinite variation case), we prove that and are solutions to the integral equations listed above. The finite variation case is proved using an argument that considers the consecutive times in which hits the curve .

Proof.

Recall from Lemma 3.7 that, when , the value function satisfies equation (25) for and . We also have that equation (3.9) follows from (3.9) by letting and using that .

We proceed to show that solves equation (3.9). First, we assume that is a process of infinite variation. We follow an analogous argument as Lamberton and Mikou, (2013) (see Theorem 3.2). Consider a regularized sequence of non-negative functions with support in such that . For every , define the function by

for any . Then for each , the function is a bounded function (since is bounded). Moreover, it can be shown that on when and that (see Lamberton and Mikou, (2008), proof of Proposition 2.5),

| (26) |

where is the infinitesimal generator of given in (3) and . Let , such that and . Applying Itô formula to , for , we obtain that for any ,

where is a zero mean martingale. Hence, taking expectation and using (26), we derive that

where we used the fact that is finite for all and that for all and when is of infinite variation (see Sato, (1999)). Taking , using the fact that for all and letting (by the dominated convergence theorem), we obtain that (3.9) holds for any . The case when follows by continuity.

For the finite variation case, we define the auxiliary function

for all . We then prove that . First, note that from the discussion after Lemma 3.5 we have that for all . Then we have that for all ,

where we used that in the last inequality. For each , we define the times at which the process hits the curve . Let and for ,

where in this context, we understand that . Taking and and gives us

where the last equality follows from the strong Markov property applied at time and , respectively, and the fact that is optimal for . Using the compensation formula for Poisson random measures (see Kyprianou, (2014) Theorem 4.4), it can be shown that

Hence, for all , we have that

Using an induction argument, it can be shown that for all and ,

| (27) |

where the last equality follows since for all . Since is of finite variation, it can be shown that for all , -a.s. Therefore, from (27) and taking , we conclude that for all ,

where the last inequality follows from the dominated convergence theorem. On the other hand, if we take and we have, by the strong Markov property applied to the filtration at time , that

where we used the fact that is an optimal stopping time for and that vanishes on . So then (3.9) also holds in the finite variation case.

∎

Next we proceed to show the uniqueness result. Suppose that there exist a non-positive continuous function and a continuous function on such that and for all . We assume that the pair solves the equations

| (28) |

and

| (29) |

when and . For and , we assume that

| (30) |

In addition, we assume that

| (31) |

Note that solving the above equations means that for all and for all . Denote as the “stopping region” under the curve , i.e., and recall that is the “stopping region” under the curve . We show that vanishes on in the next Lemma.

Lemma 3.11.

We have that for all .

Proof.

Since the statement is clear for , we take and . Define to be the first time that the process is outside before time , i.e.,

where in this context, we understand that . From the fact that for all and the strong Markov property at time , we obtain that

where the last equality follows since for all and for all . Then, applying the compensation formula for Poisson random measures (see Kyprianou, (2014) Theorem 4.4) we get

Hence for all as we claimed. ∎

The next lemma shows that can be expressed as an integral involving only the gain function stopped at the first time the process enters the set . As a consequence, dominates the function .

Lemma 3.12.

We have that for all ,

Proof.

Note that we can assume that because for , we have that and for , for all . Consider the stopping time

Let , using the fact that for all and the strong Markov property at time , we obtain that

| (32) |

where the second equality follows since creeps upwards and therefore for and for all . Then from the definition of (see (10)), we have that

Therefore on . ∎

We proceed by showing that the function is dominated by . In the upcoming lemmas, we show that equality indeed holds.

Lemma 3.13.

We have that for all .

Proof.

The statement is clear for . We prove the statement by contradiction. Suppose that there exists a value such that and take . Consider the stopping time

Applying the strong Markov property to the filtration at time , we obtain that

where we used the fact that for all . From Lemma 3.12 and the fact that (by assumption), we have that for all and , . Hence, by the compensation formula for Poisson random measures, we obtain that

Recall from the discussion after Lemma 3.5 that the function is strictly positive on . Hence, we obtain that for all ,

The assumption that together with the continuity of the functions and mean that there exists such that for all . Consequently, the probability of spending a strictly positive amount of time (with respect to Lebesgue measure) in this region is strictly positive. We can then conclude that

This is a contradiction and therefore we conclude that for all . ∎

Note that the definition of on (see equation (30)) together with condition (31) imply that

for all and . The next Lemma shows that and coincide.

Lemma 3.14.

We have that for all and hence .

Proof.

We prove that by contradiction. Assume that there exists such that . Since for all , we deduce that . Let be the stopping time

With the Markov property applied to the filtration at time , we obtain that for any

where the second inequality follows from the fact that (see Lemma 3.12) and the last equality follows as is the optimal stopping time for . Note that since creeps upwards, we have that . Hence,

However, the continuity of the functions and gives the existence of such that for all . Hence, together with the fact that for all we can conclude that

which shows a contradiction.

∎

4 Examples

4.1 Brownian motion with drift

Suppose that is a Brownian motion with drift. That is for any , , where and . In this case, we have that

for all . Then

It is well known that has exponential distribution (see e.g. Borodin and Salminen, (2002) pp251 or Kyprianou, (2014) pp 233) with distribution function given by

Denote as the distribution function of a Normal random variable with mean and variance , i.e., for any ,

For any and , define the function

Then it can be easily shown that

Thus, we have that satisfies the non-linear integral equation

for all and the value function is given by

for all . Note that we can approximate the integrals above by Riemann sums so a numerical approximation can be implement. Indeed, take sufficiently large and define . For each , we define . Then the sequence of times is a partition of the interval . Then, for any and for we approximate by

where the sequence is a solution to

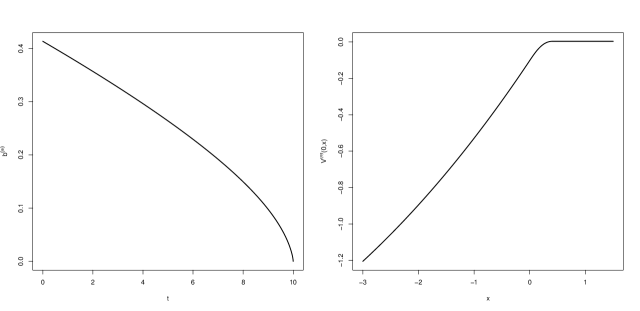

for each . Note that the sequence is a numerical approximation to the sequence (for sufficiently large) and can be calculated by using backwards induction. In the Figure 3, we show a numerical calculation of the equations above. The parameters used are and , whereas we chose .

4.2 Brownian motion with exponential jumps

Let be a compound Poisson process perturbed by a Brownian motion, that is

| (33) |

where is a standard Brownian motion, is Poisson process with rate independent of , , and the sequence is a sequence of independent random variables exponentially distributed with mean . Then in this case, the Laplace exponent is derived as

Its Lévy measure, given by is a finite measure and is a process of infinite variation. According to Kuznetsov et al., (2013), the scale function in this case is given for and by,

where and are the three real solutions to the equation , which satisfy . The second scale function, , takes the form

Note that since we have exponential jumps (and hence ), we have that for all and ,

Then, for any , equation (3.9) reads as

where for any , and ,

Note that the equation above suggest that in order to find a numerical value of using Theorem 3.9 we only need to know the values of the function and not the values of for all and . The next Corollary confirms that notion.

Corollary 4.1.

Let . Assume that is of the form (33) with , . Suppose that and are continuous functions on such that and for all . For any we define the function

Further assume that there exists a value such that for any and . If is a non-positive function, we have that and .

Proof.

First note that, since is of infinite variation, for all such that and . Hence, by continuity of and , and by dominated convergence theorem, we have that is continuous. By means of Theorem 3.9 is enough to show that satisfies the integral equation,

where for all and in the last equality we used the explicit form of . Then it suffices to show that for all .

Let . For any , consider the stopping time

Note that for any we have that and in the event . Then using the strong Markov property at time , we have that for any ,

where in the last equality we used the fact that for all , the continuity of and that can only cross above by creeping. By using the compensation formula for Poisson Random measures, we obtain that

Hence we conclude that for any ,

| (34) |

and hence,

By continuity of and we obtain that

Moreover, from equation (34) we conclude that for all and the conclusion holds. ∎

Hence, for any , we can write

where for any , and ,

Take a value sufficiently small. Hence the functions and satisfy the integral equations

for all . We can approximate the integrals above by Riemann sums so a numerical approximation can be implement. Indeed, take sufficiently large and define . For each , we define . Then the sequence of times is a partition of the interval . Then, for any and , we approximate by

where the sequence is a solution to

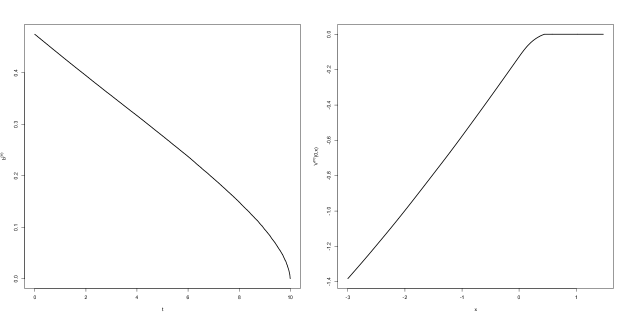

for each . Note that, for sufficiently large, the sequence is a numerical approximation to the sequence (provided that ) and can be calculated by using backwards induction. The functions and can be estimated using simulation methods. In the figures below we include a plot of the numerical calculation of and using the parameters , , .

References

- Baurdoux, (2009) Baurdoux, E. J. (2009). Last Exit Before an Exponential Time for Spectrally Negative Lévy Processes. Journal of Applied Probability, 46(2):542–558.

- Baurdoux and Pedraza, (2020) Baurdoux, E. J. and Pedraza, J. M. (2020). Predicting the last zero of a spectrally negative lévy process. In López, S. I., Rivero, V. M., Rocha-Arteaga, A., and Siri-Jégousse, A., editors, XIII Symposium on Probability and Stochastic Processes, pages 77–105, Cham. Springer International Publishing.

- Baurdoux and van Schaik, (2014) Baurdoux, E. J. and van Schaik, K. (2014). Predicting the Time at Which a Lévy Process Attains Its Ultimate Supremum. Acta Applicandae Mathematicae, 134(1):21–44.

- Bernyk et al., (2011) Bernyk, V., Dalang, R. C., and Peskir, G. (2011). Predicting the ultimate supremum of a stable Lévy process with no negative jumps. Ann. Probab., 39(6):2385–2423.

- Bertoin, (1998) Bertoin, J. (1998). Lévy processes, volume 121. Cambridge university press.

- Bichteler, (2002) Bichteler, K. (2002). Stochastic Integration with Jumps. Encyclopedia of Mathematics and its Applications. Cambridge University Press.

- Borodin and Salminen, (2002) Borodin, A. N. and Salminen, P. (2002). Handbook of Brownian Motion - Facts and Formulae. Birkhäuser Basel.

- Carr, (1998) Carr, P. (1998). Randomization and the American put. The Review of Financial Studies, 11(3):597–626.

- Chiu and Yin, (2005) Chiu, S. N. and Yin, C. (2005). Passage Times for a Spectrally Negative Lévy Process with Applications to Risk Theory. Bernoulli, 11(3):511–522.

- du Toit et al., (2008) du Toit, J., Peskir, G., and Shiryaev, A. N. (2008). Predicting the last zero of Brownian motion with drift. Stochastics, 80(2-3):229–245.

- Glover and Hulley, (2014) Glover, K. and Hulley, H. (2014). Optimal Prediction of the Last-Passage Time of a Transient Diffusion. SIAM Journal on Control and Optimization, 52(6):3833–3853.

- Glover et al., (2013) Glover, K., Hulley, H., and Peskir, G. (2013). Three-dimensional Brownian motion and the golden ratio rule. Ann. Appl. Probab., 23(3):895–922.

- Graversen et al., (2001) Graversen, S. E., Peskir, G., and Shiryaev, A. N. (2001). Stopping Brownian Motion Without Anticipation as Close as Possible to Its Ultimate Maximum. Theory of Probability & Its Applications, 45(1):41–50.

- Kuznetsov et al., (2013) Kuznetsov, A., Kyprianou, A. E., and Rivero, V. (2013). The Theory of Scale Functions for Spectrally Negative Lévy Processes, pages 97–186. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Kyprianou, (2014) Kyprianou, A. E. (2014). Fluctuations of Lévy Processes with Applications. Springer Berlin Heidelberg.

- Lamberton and Mikou, (2008) Lamberton, D. and Mikou, M. (2008). The critical price for the American put in an exponential Lévy model. Finance and Stochastics, 12(4):561–581.

- Lamberton and Mikou, (2013) Lamberton, D. and Mikou, M. A. (2013). Exercise boundary of the American put near maturity in an exponential Lévy model. Finance and Stochastics, 17(2):355–394.

- (18) Madan, D., Roynette, B., and Yor, M. (2008a). From Black-Scholes formula, to local times and last passage times for certain submartingales. working paper or preprint.

- (19) Madan, D., Roynette, B., and Yor, M. (2008b). Option prices as probabilities. Finance Research Letters, 5(2):79 – 87.

- Paroissin and Rabehasaina, (2013) Paroissin, C. and Rabehasaina, L. (2013). First and Last Passage Times of Spectrally Positive Lévy Processes with Application to Reliability. Methodology and Computing in Applied Probability, 17(2):351–372.

- Peskir and Shiryaev, (2006) Peskir, G. and Shiryaev, A. (2006). Optimal Stopping and Free-Boundary Problems. Birkhäuser Basel.

- Sato, (1999) Sato, K.-i. (1999). Lévy processes and infinitely divisible distributions. Cambridge university press.

- Shiryaev, (2009) Shiryaev, A. N. (2009). On Conditional-Extremal Problems of the Quickest Detection of Nonpredictable Times of the Observable Brownian Motion. Theory of Probability & Its Applications, 53(4):663–678.

- Urusov, (2005) Urusov, M. A. (2005). On a Property of the Moment at Which Brownian Motion Attains Its Maximum and Some Optimal Stopping Problems. Theory of Probability & Its Applications, 49(1):169–176.