Asymptotics of Yule’s nonsense correlation for Ornstein-Uhlenbeck paths: a Wiener chaos approach.

Abstract

In this paper, we study the distribution of the so-called "Yule’s nonsense correlation statistic" on a time interval for a time horizon , when is large, for a pair of independent Ornstein-Uhlenbeck processes. This statistic is by definition equal to :

where the random variables , are defined as

We assume and have the same drift parameter . We also study the asymptotic law of a discrete-type version of , where above are replaced by their Riemann-sum discretizations. In this case, conditions are provided for how the discretization (in-fill) step relates to the long horizon . We establish identical normal asymptotics for standardized and its discrete-data version. The asymptotic variance of is . We also establish speeds of convergence in the Kolmogorov distance, which are of Berry-Esséen-type (constant*) except for a factor. Our method is to use the properties of Wiener-chaos variables, since and its discrete version are comprised of ratios involving three such variables in the 2nd Wiener chaos. This methodology accesses the Kolmogorov distance thanks to a relation which stems from the connection between the Malliavin calculus and Stein’s method on Wiener space.

1 Introduction

In this paper, we study the normal asymptotics in law of the so-called “Yule’s nonsense correlation statistic” on a time interval when the time horizon tends to infinity, for two independent paths of the Ornstein-Uhlenbeck (OU) stochastic processes. This statistic is defined as:

| (1) |

where the random variables , are given by

| (2) |

and is a pair of two independent OU processes with the same known drift parameter , namely solves the linear SDE, for

| (3) |

with , , where the driving noises , are two independent standard Brownian motions (Wiener processes). We also study the asymptotic law of a discrete-data version of , denote by for observations, where the Riemann integrals in (2) are replaced by Riemann-sum approximations.

It has been known since 1926 that a discrete version of the statistic , which is the Pearson correlation coefficient, does not behave the same way when the data from and are i.i.d. and as when they are the discrete-time observations of a random walk. As is universally known for i.i.d. data, and also holds for shorter-memory models, converges in probability to under all but the most extreme circumstances (data coming from a distribution with no second moment), but G. Udny Yule showed in [12] that when the data come from a random walk, does not concentrate, and has a law which seems to converge instead to a diffuse distribution on . The exact variance and other statistical properties of this law remained unknown with mathematical precision, though a 1986 paper [5] by P.C.B. Phillips showed that the limiting law of with simple symmetric random-walk data rescaled to the time interval is the same as the law of for two independent Wiener processes, which is indeed necessarily diffuse and fully supported on . This advance prompted several talented prominent probabilists to look for ways of computing statistics of , if even only its variance, but this remained elusive until 2017, when Ph. Ernst and two collaborators (one posthumous) provided a closed-form expression for in [1]. Since then, other advances on the moments of have been made, particularly [2], and recent progress was recorded in [3] on how to compute the momens of when the paths are independent Gaussian simple-symmetric random walks. In all cases mentioned in this paragraph, the asymptotic behavior of in law (scaled appropriately in time) is necessarily that of for two independent Wiener processes.

This leaves open the question of what happens to when the paths deviate substantially from Wiener paths or random walks. Wiener (resp. random walk) paths have the property of exact (resp. approximate) self-similarily. We take up the question of using different kinds of paths, with the simplest possible example of a clear alternative to self-similar processes, namely the ubiquitous mean-reverting OU processes. The property of mean reversion is so distinct from self-similarily, that the behavior of changes drastically from one to the other. Note that these two classes of processes are simply those satisfying (3) with (Wiener process) or (OU process). To illustrate the point of how distinct these processes are, let us extend the scope of this paper momentarily, to include all processes defined by (3) (with or without ), by replacing with a fractional Brownian motion (fBm) denoted by , for some . Like the Wiener process, which corresponds to , the self-similar property of simply states that for any fixed real constant , in law. By using this property with via the change of variable in the Riemann integrals defining , we obtain immediately the equality in law

and therefore

In fact, we only used the property of self-similarity to get the above. In other words, for any pair of self-similar processes, the law of the nonsense correlation is constant as the time horizon increases. In stark contrast, in this paper, we show that, for a pair of OU processes, the law of converges to the Dirac mass at 0. As mentioned, we show more: a central limit theorem for (the mean of is always 0), with asymptotic variance equal to , and a speed of convergence of to in Kolmogorov metric at the rate .

The discrete-observation part of this paper simply replaces the Riemann integrals by the Riemann sums, for instance replacing the first integral in by where and . We denote the resulting empirical correlation by rather than . It is convenient to note that can be thought of as depending on , and we will systematically emphasize this by denoting . It is assumed that the discretization step converges to while tends to , which means that in our asymptotics. We provide a full range of speeds of convergence in central limit theorem depending on how fast converges to We find in fact that we must have as and we also note that , as well it should. Our convergence result, which immediately implies the central limit theorem , is

From this, we can immediately read off that a rather optimal rate of sampling of our discrete data is one for which the two terms in the max are of the same order, i.e. , which is equivalent to requiring that be of order , which in turn, since , is equivalent to of order . This is explained in more detail in the conclusion of the section on discrete data. In any case, in Kolmogorov distance, we see that the best rate of convergence of to is of order , which is exactly the same rate as in the case of continuous data, and which occurs for a relatively frequency of observations of order over unit intervals. Lower frequency of observations lead to slower convergence rate in Kolmogorov distance in the scale of the time horizon compared to continuous observation. Higher frequency of observation leads to the same rate as with continuous observations, but this can be considered wasteful since the same rate was achieved at the optimal frequency of per unit time. It is worth stating again that these results in discrete time, pertaining to the convergence rate in the CLT for , are a second-order result compared to the CLT itself, i.e.

which holds in law identically in both the discrete and continuous data cases.

As mentioned, we use techniques from analysis on Wiener chaos to prove the above results. Some of these results are technical and novel, and we provide here a few points in the hopes of enlightening the methods. A key element comes from the connection discovered by I. Nourdin and G. Peccati (see [8]) between the Malliavin calculus and Stein’s method. In that connection, the distance in law between a random variable and the standard normal law can be measured to some extent by comparing the Hilbert-space norm of the Malliavin derivative to the value , which is the value one would find for the norm of the Malliavin derivative of a standard normal variable under any reasonable coupling of and i.e. under any reasonable representation of on Wiener space. The question of how to represent on Wiener space is typically trivial when dealing with functionals of stochastic processes based on Wiener processes, and this is certainly the case in our paper. The question of whether is an adeqate functional of to make the comparison with is less trivial. The original work in [4] noted that it is sufficient for variables on Wiener chaos, and used an auxiliary random variable which is slightly more involved than to establish broader convergence in law beyond fixed chaos. That same random variable was used in [9] to characterize laws on Wiener chaos at the level of densities, and was used specifically in [6, Theorem 2.4] to measure distances between laws in the Kolmogorov metric. We use that theorem herein, by applying it separately to all three Wiener chaos components which are used to calculate , noting as in [4] that .

The above elements are explained in the preliminary section on analysis on Wiener space below. They are used herein via standard computations of variances and differentiation and product rules for variables on Wiener chaos which are represented as double Wiener integrals with respect to the ’s, leading to computing the asymptotic variance of the rescaled numerator , namely , and the speed of convergence of the variances to this limit, including precise estimations of the constants in this rate of convergence as functions of . It turns out that the rescaled denominator does not have normal fluctuations, but rather converges to the constant . We establish this too. Adding to this that the numerator, as a second-chaos variable, has mean zero, this indicates that the entire rescaled fraction should converge in law to Finding a presumably sharp rate of this convergence in Kolmogorov metric is the main technical issue we tackle in this paper. Establishing this for the numerator alone is a key quantitative estimate. We use [6, Theorem 2.4] and our ability to compute the norm of the Malliavin derivative of the first double Wiener integral in the expression for and we find a rate of normal convergence of order . However, we must also handle the second term in , which is the (rescaled) product of two independent normal variables, which are both non-independent from the first part of . For this, we appeal to a 1971 theorem of Michel and Pfanzagl [11] which allows us to decouple the dependence of a sum (resp. a ratio) of two variables when comparing them to a normal law in Kolmogorov distance. We specialize this theorem to the case when the second summand (resp. the denominator) is a product normal variable (resp. the root of a product normal), establishing an optimal use of it in this special case. See Proposition 5, Corollary 7, Proposition 8 and estimate (29), and estimate (37).

This optimal use of this decoupling technique comes at the very small cost of adding a factor of to our rate of convergence. We believe this factor is optimal given our use of [11], and is determined by the weight of the tail of a product normal law, which is asymptotically the same as the tail of a chi-square variable with one degree of freedom, which in logarithmic scale, is the same as an exponential tail . The interested reader can check that any use of Holder’s inequality or similar methods based on moments, cannot achieve this more efficient method, leading instead to a rate of convergence of for . The reader will also observe our use of the fine structure of the second Wiener chaos as a separable Hilbert space, to deal with the tail distribution of ’s denominator terms. This structure is documented for instance in [8, Section 2.7.4] where it is shown that every second-chaos variable can be represented as a series where is a sequence of i.i.d. mean-zero chi-square variables with one degree of freedom, and is in . In our case, the reader will observe that the terms in the denominator of also contain non-zero expectations, that their ’s are positive and in , and that the expectations equal . This fact is essential to us being able to control the denominator.

The techniques used to establish results in the case of discrete observations are similar to those in the continuous case. Additional ingredients include the rate of convergence of the Riemann-sum version of the first integral in to its limit. This rate turns out to be where, as mentioned, is the number of observations in and the regular mesh is . The use of the aforementioned Michel-Pfanzagl theorem from [11] to deal with the product-normal term in the numerator has to be optimized against this dicretization error; this is where the term comes from, whereas the term is none other than the same convergence rate for the numerator in Kolmogorov distance as in the continuous case. See Lemma 11 and Proposition 13. The use of the sum version of the Michel-Pfanzagl theorem from our Corollary 7 leads again to a leading log correction factor . The denominator terms also require a careful analysis, though no additional ideas are needed beyond what was already established in the continuous case.

With this roadmap summary complete, the structure of this paper should appear as straightforward. We begin with a section of preliminaries presenting the tools needed from analysis on Wiener space, followed by a section covering the convergence in the continuous case, and then a section dealing with the case of discrete data. The final section provides some numerics to illustrate the convergence rates in practice, wherein we find that in discrete time, the time-scaled does indeed behave in distribution largely like a normal with variance , even without using the optimal observation frequency.

2 Preliminaries

2.1 Elements of Analysis on Wiener space

With denoting the Wiener space of a standard Wiener process , for a deterministic function , the Wiener integral is also denoted by . The inner product will be denoted by .

-

•

The Wiener chaos expansion. For every , denotes the th Wiener chaos of , defined as the closed linear subspace of generated by the random variables where is the th Hermite polynomial. Wiener chaos of different orders are orthogonal in . The so-called Wiener chaos expansion is the fact that any can be written as

(4) for some for every . This is summarized in the direct-orthogonal-sum notation . Here denotes the constants.

-

•

Relation with Hermite polynomials. Multiple Wiener integrals. The mapping is a linear isometry between the symmetric tensor product (equipped with the modified norm ) and . Hence, for and its Wiener chaos expansion (4) above, each term can be interpreted as a multiple Wiener integral for some .

-

•

Isometry Property-Product formula. For any integers and and , we have

(8) For any integers , and symmetric integrands and ,

(9) where is the contraction of order of and which is an element of defined by

while denotes its symmetrization. More generally the symmetrization of a function is defined by where the sum runs over all permutations of . The special case for in (9) is particularly handy, and can be written in its symmetrized form:

(10) where means the tensor product of and .

-

•

Hypercontractivity in Wiener chaos. For , the multiple Wiener integrals , which exhaust the set , satisfy a hypercontractivity property (equivalence in of all norms for all ), which implies that for any (i.e. in a fixed sum of Wiener chaoses), we have

(11) The constants above are known with some precision when : by Corollary 2.8.14 in [8], .

-

•

Malliavin derivative. For any function with bounded derivative, and any , the Malliavin derivative of the random variable is defined to be consistent with the following chain rule:

A similar chain rule holds for multivariate . One then extends to the so-called Gross-Sobolev subset by closing inside under the norm defined by All Wiener chaos random variable are in the domain of . In fact this domain can be expressed explicitly for any as in (4): if and only if .

-

•

Generator of the Ornstein-Uhlenbeck semigroup. The linear operator is defined as being diagonal under the Wiener chaos expansion of : is the eigenspace of with eigenvalue , i.e. for any , . We have ( , the constants. The operator is the negative pseudo-inverse of , so that for any , .

-

•

Kolmogorov distance. Recall that, if are two real-valued random variables, then the Kolmogorov distance between the law of and the law of is given by

If , with and , then (Theorem 2.4 in [6]), then

If moreover, for some , , then , and thus in this case

(12)

Lemma 1

Let . Let be a sequence of random variables. If for every there exists a constant such that for all ,

then for all there exists a random variable which is almost surely finite such that

for all . Moreover, for all .

3 Continuous observations

In this section, we compute the asymptotic variance of and its normal fluctuations for large by working with each of the three terms which appear in its definition. For the sake of convienence and compactness of notation, we construct a two-sided Brownian motion from the two independent Brownian motions and as follows :

The following lemma will be convenient in the sequel.

Lemma 2

Let , , then

where , in are defined by

Proof.

Using the product formula of multiple integrals, we have

which completes the proof. ∎

3.1 Asymptotic distribution of :

The numerator of can be written as follows

| (13) |

where . Using the notation for the Wiener integral with respect to , since = , where we can write using Lemma 2

| (14) | ||||

with is given

| (15) |

On the other hand, we have

Note that the kernel is not symmetric, in the sequel we will denote its systematization defined by . We are now ready to compute the asymptotic variance of the main term in the numerator of .

Lemma 3

Proof.

We have

where

and

∎

Proposition 4

Let and , then we have

where . Consequently as .

Proof.

We will use the estimate (12) recalled in the preliminaries in order to prove this proposition. We have , , hence

where we used the product formula (10) and the fact that the kernel is symmetric. Thus

| (16) |

We have,

Hence

| (17) | |||

On the other hand by Fubini’s theorem

Using the fact that the other term of (17) can be treated similarly and that , , we get

On the other hand, since for , , where , we get

| (18) | |||

| (19) | |||

| (20) | |||

| (21) |

where and we used the change of variables , . Therefore, applying Young’s inequality, we can conclude

| (22) | |||||

The desired result follows using (12) and the estimates (16), (22) and Lemma 14. ∎

We will need the following Proposition due to Michel and Pfanzagl (1971) [11] in the sequel which gives upper bounds for Kolmogorov’s distance between respectively the sum and the ratio of two random variables and a standard Gaussian random variable.

Proposition 5

Let , and be three random variables defined on a probability space such that . Then, for all , we have

-

1.

.

-

2.

where

Proposition 6

Let be a r.v. such that where and two independent Gaussian r.v defined on a probability space . Then, there exists a constant such that

Moreover, there exists a constant such that .

Proof.

By the independence of and , it’s easy to check that for any , we have

Thus the constraint implies that should be such that . On the other hand since , thus there exists a constant such that . ∎

Corollary 7

Let , be two r.v. defined on a probability space such that where and . Then, there exists a constant such that

Proof.

To prove the convergence in law of , recall that We can write , where and we have for

| (23) |

Hence by the independence of and and denoting , we get

| (24) |

Then in virtue of Proposition 6 and Corollary 7, there exists a constant with such that

On the other hand, since the function is increasing on , we have for large enough

The following proposition follows.

Proposition 8

There exists a constant depending only on , such that

In particular, as .

Having just completed the study of the convergence in law of the numerator in , in order to study the convergence in law of , we will use Proposition 5 assertion 2 and the fact that

| (25) |

to show in the next subsection that the denominator concentrates to the value 1, and that the behavior of is thus given by that of the numerator above.

3.2 The denominator term

Let us denote the denominator term

| (26) |

According to Proposition 5 assertion 2. we need to estimate for instance for . Using the fact that a.s. then a.s. Now using the shorthand notation , , thus, we have a.s.

| (27) |

Thus, using the fact that and are equal in law, we get for any ,

| (28) |

We lighten the notation by writing instead of , therefore by Proposition 5 assertion 2. applied to in (25), we get

| (29) |

where .

The next step is to control the term . We have :

where

and

Then we immediately get the mean concentration around 1:

| (30) |

For the term , in a similar way to the calculus in the proof of Proposition 3 and since is symmetric, we get

Therefore, we have , since

Finally, by equation (23), . On the other hand, we can write

where

By the product formula (9), the r.v. belongs to the second Wiener chaos while is deterministic. Moreover, we have

| (31) |

where we used the hypercontractivity property (11) on Wiener chaos for , since and . The last estimate plus the estimate (30) on established earlier imply that

| (32) |

With all those estimates in place, we return to our main target to control for some , Or

Of course second chaos r.v. are not symmetric, but since we do not know the sign of and second Wiener chaos can be skewed in either direction, there is no loss of efficiency to treat and in the same fashion. Recall the from Proposition 2.7.13 of [8] that any second chaos r.v. has the following representation

where is a sequence of reals for which is decreasing and are independent standard Gaussian random variables and

Moreover, by the product formula (9), if is a quadratic functional of a Gaussian process, then is the expectation of that functional. Therefore with , there exists and iid , such that

One immediately checks that the expression to be added to to make it a quadratic functional is which is equal to . Therefore, the sequence satisfies

From the representation we just established, we will set a general global tail for any r.v. in the second Wiener chaos, which is convenient for our purposes. Let let and . Assume that . Let which is a constant to be chosen later. Then by Markov’s inequality, we have for all

| (33) |

This formula requires that for all , but since the sign of is unknown and decreases, it is sufficient to require that . Since , we can say that . Therefore, to be completely safe we require that .We must also check that the product in (33) converges. In fact, notice that since , thus as , for all , we have

Thus, we get

| (34) |

where we used the fact that ( see Proposition 2.7.13 of [8])

where denotes the third cumulant of . Since is centered then this cumulant is equal to the third moment: .

Applying inequality (34) to where

we can pick any , thus we can chose . This implies that . On the other hand, since is in the second Wiener chaos, then by the hypercontractivity property in Section 2, , and consequently . Finally, since , thus we get the following:

| (35) |

where

We now replace by . Note that we must also evaluate but since the signs of and are not known, this will yield exactly to the same estimate as . Thus from the estimate (35), we get

Let us denote , we must choose . Let

| (36) |

where is some constant to be chosen as well. Thus since we proved in (32) that , we get

For large enough, for instance for , we have

so that

and hence

Thus it’s sufficient to choose , obtaining

| (37) |

Summarizing, with and , for , then according to inequality (27), with the choice for in (36) with , we have the following estimate for the denominator term defined in (26), as follows

Thus, from inequalities (29) and (37), we get the following theorem for the convergence in law of Yule’s statistic as .

Theorem 9

There exists a constant depending only on such that for large enough, we have

In particular,

Remark 10

From expression at the end of the calculation preceding Theorem 9, and similar estimates elsewhere above, a detailed analysis of how these constants depend on show that for ,

where is a universal constant. This analysis is omitted for conciseness. In particular, as .

4 Discrete observations

We assume now that the pair of Ornstein-Uhlenbeck processes is observed at equally spaced discrete time instants , where is the observation mesh and is the length of the “observation window”. We assume and , as . The aim of this section is to prove a CLT for the following statistic which can be considered as a discrete version of Yule’s nonsense correlation statistic , defined by

| (38) |

where , are the Riemann-type discretization of defined as follows

| (39) |

with denoting the empirical mean-process of , , namely

As in the continuous case, we make use of the following expression of along with Proposition 5 in order to prove its convergence in law to a Gaussian distribution:

| (40) |

4.1 Convergence in law of

From the expression of given in (39), we can write

| (41) |

where

We also defined the following random sequence

where is defined in (14). The following lemma holds.

Lemma 11

Assume that as and that , then, there exists a constant , such that

In particular if as , , as .

Proof.

We have

By Cauchy Schwartz inequality and the fact that , , we get

where we used the fact that and are two Gaussian processes equal in law. On the other hand since , . Recall that , . We get

where

We will use in the sequel the fact that the increments of the process satisfies , . For the first sequence we have

where we used the change of variables , . For , we have

Similarly, we have

For the last sequence , we get

The desired result following using the previous inequalities and the fact that as . ∎

Remark 12

One possible mesh that satisfies the assumptions of Lemma 11 is with .

Proposition 13

There exists a constant such that

In particular, if as , we get

as .

Proof.

On the other hand, from the decomposition (41), Corollary 7, Proposition 5, there exists a constant such that , and such that

| (42) |

Let us now compute ,

with . Thus similarly to a previous calculation, we have

| (43) |

where for the last equality we used the fact that

Recall that , where , . Moreover,

We deduce that there exists a constant , such that

Therefore, from equation (42) and the fact that the function on , we have for large enough

The following proposition follows.

Theorem 14

There exists a constant depending only on such that

In particular, if as ,

as .

Example 15

If with , then we have

Consequently,

as .

4.2 The denominator term

We denote the denominator term in by , i.e.

| (44) |

According to Proposition 5 assertion 2, we need to estimate for instance for . Thus, denoting , then similarly to the calculations performed in the continuous case, i.e. (27), we get

Writing instead of , by Proposition 5 assertion 2 applied to , we get

| (45) |

where . It remains to control the term . we have

| (46) |

where

| (47) |

Lemma 16

Consider defined in (47), then for every large , we have

Proof.

The sequence can be written as follows :

where . Thus

For the right hand partial sum, we can write

Moreover,

For every large . The desired result follows since . ∎

For the sequence , we have

| (48) |

For every large , . Therefore, following exactly the same analysis done for the denominator term in the continuous case and choosing , we get the existence of a constant , such that for large enough

| (49) |

The previous estimates will allow to prove first a Strong law result by showing that converges to almost surely as , then the convergence in law of the statistic given with its rate of convergence as .

Proposition 17

Assume that , for , then we have almost surely

Proof.

We can write as follows

For the numerator term, we have by the decomposition (41),

For the sequence , we have

Then by Lemma 11, we get , and by the hypercontractivity property and Lemma 1, we obtain , a.s. as . By the same argument, and using Lemma 3, we obtain , and we then get , a.s. as . Consequently, we have a.s. as , For the sequence , , thus a.s. as . Finally,

a.s. as For the denominator term, we will need the following proposition

Proposition 18

For every , there exists a constant depending on and , such that

Proof.

Using the fact that if p.s. then we have for every , then by the notation , , we get

Moreover, since by the decomposition (46), , where and are defined in (47), we get

where we used the hypercontractivity property (11), Lemma 16 and the estimate (48), with

The result of Proposition 18 is therefore established. ∎

By Proposition 18, we have for all ,

for any , it follows from Borel-Cantelli’s Lemma that

almost surely as , which finishes the proof. ∎

Remark 19

The previous proposition was proved in the scale , for , for ease of presentation, but one can also show that it holds for any mesh satisfying:

-

•

, a.s. for some as .

-

•

for any .

Theorem 20

There exists a constant such that for large enough, we have

In particular, if as ,

as .

Remark 21

The results obtained in Theorem 20 can be as efficient as those of Theorem 9, as long as one picks a step size very precisely. In fact, Theorem 20 allows us to identify an optimal step size immediately, by requiring that is of the same order as . By equating these two terms, we immediately find that it is optimal to choose on the order of . When choosing , one then immediately finds that , which means that the speed in the Kolmogorov metric in Theorem 20 is bounded above by up to a constant. Therefore, in terms of , the rate of convergence is of the order of . We obtain therefore the same speed as in the continuous case in Theorem 9. It is in this sense that the convergence rate in Theorem 20 is as efficient in Theorem 9.

5 Numerical results

This section contains a numerical study of some of the properties of the discrete version of Yule’s nonsense correlation statistic, which we denoted by in (38). We first simulate the OU processes and according to the following steps :

-

1.

Set the values of , the sample size and the mesh , .

-

2.

Generate two independent Brownian motions and .

-

3.

Set , for and simulate the observations , , …, , where following the Euler scheme :

-

4.

We obtain a simulation of the sample paths of and based on , , by approximating and using the linear process linking the points for as follows

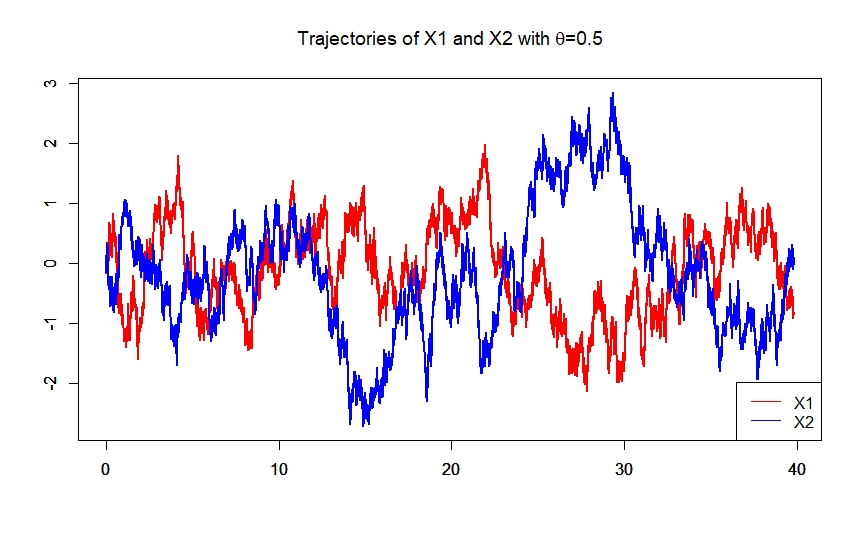

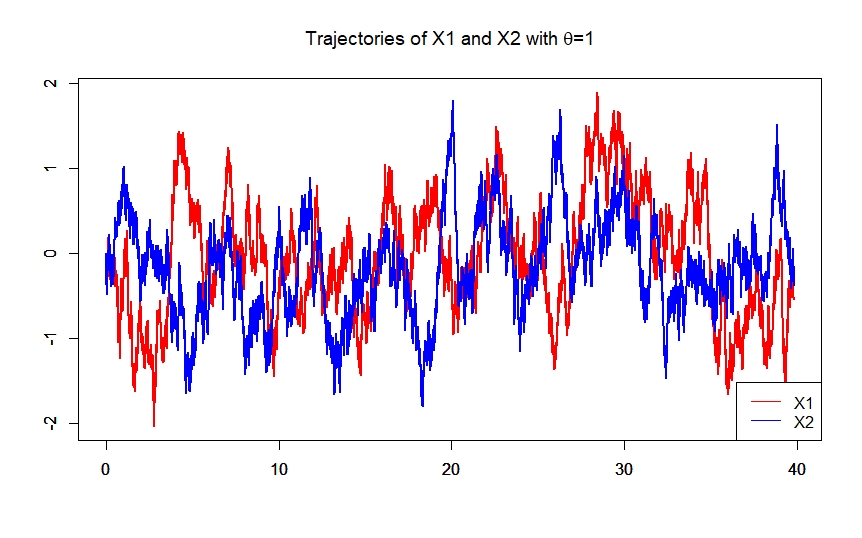

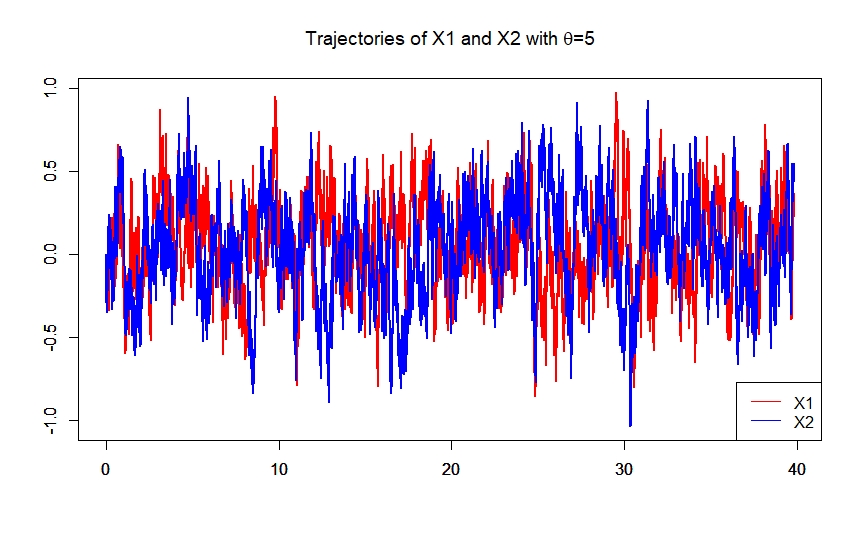

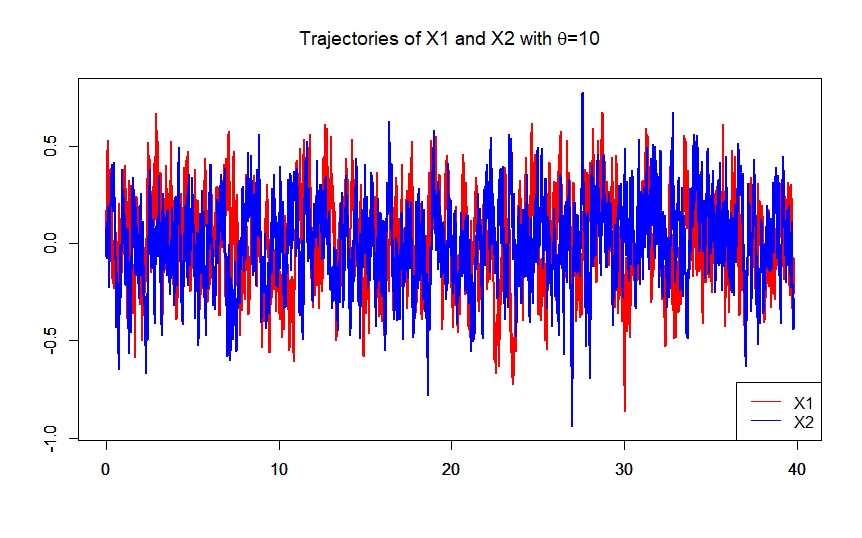

The figures below are an example of four sample paths of and for different values of the drift parameter .

Figure 1: Sample paths of X1 and X2 for different values of .

The simulation of the Ornstein-Uhlenbeck sample paths and is done for different values of the parameter , for a sample size and a mesh () which corresponds to a time horizon . One can see from the figures above how the drift parameter value impacts the variability and raggedness of OU sample paths. The next step is to illustrate numerically Proposition 17. The table below shows the mean, the median and standard deviation values for for different values of , using 500 Monte-Carlo replications for three different values of the drift parameter .

| Mean | -0.01022 | 0.00667 | 0.00377 | |||||||||

| Median | -0.00725 | 0.00873 | 0.00168 | |||||||||

| S.Dev | 0.14990 | 0.10162 | 0.10898 | |||||||||

| Mean | 0.00296 | 0.00130 | 0.00088 | |||||||||

| Median | 0.00136 | 0.00214 | -0.0011 | |||||||||

| S.Dev | 0.05237 | 0.06892 | 0.04602 | |||||||||

| Mean | -0.00258 | -0.00038 | 0.00015 | |||||||||

| Median | -0.00147 | 0.00036 | 0.00035 | |||||||||

| S.Dev | 0.04935 | 0.03641 | 0.03156 |

Table 1 above shows that approaches zero for large values of the sample size which confirms Proposition 17, even for moderate , and even though is not an inordinately large value. To investigate the asymptotic normal distribution of empirically, we need to compare the distribution of the statistic

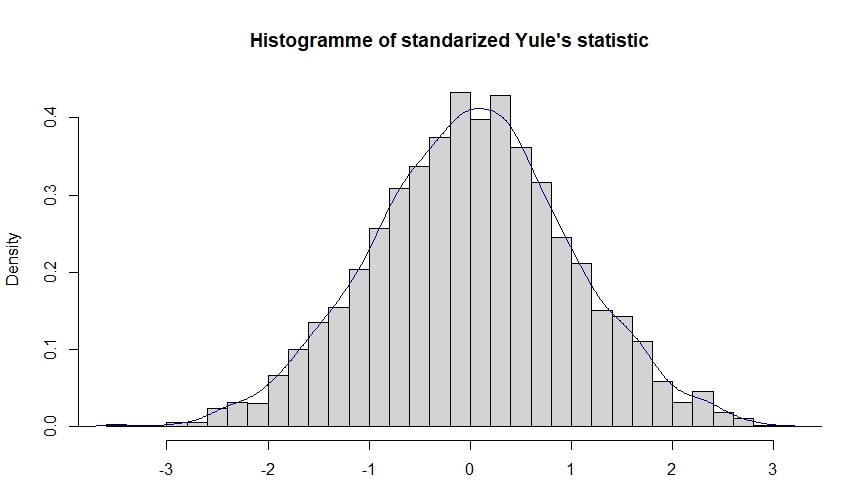

with the standard Gaussian distribution . For this aim, we chose , , and based on 3000 replications, we obtained the following histogram :

The histogram (2) shows visually that the normal approximation of the distribution of the statistic is reasonable for the sampling size and time horizon . Moreover, the results of the next table below show a comparison of statistical properties between and (0,1) with the same parameters as in Figure 2, we can see that the empirical mean, median and standard deviation of and (0,1) are quite close, which illustrates well our theoretical results.

| Statistics | Mean | Median | Standard Deviation |

|---|---|---|---|

| (0,1) | 0 | 0 | 1 |

| 0.00832 | 0.01206 | 0.99691 |

We can also illustrate numerically the rate of convergence in law of the statistic to the standard Gaussian distribution, by approximately computing the Kolmogorov distance between and . For this aim, we approximate the cumulative distribution function using an empirical cumulative distribution function based on 500 replications of the computation of for . The figure below shows the empirical and standard normal cumulative distribution functions.

![[Uncaptioned image]](/html/2108.02857/assets/kolmo-3000.jpeg)

Based on Remark 21, when the mesh for , we expect that

In fact, with our choice of and a sample size , the time horizon . The mesh size is larger than the optimal size yielding a larger time horizon than under the optimal observation frequency. The Kolmogorov distance between the two laws, which equals the sup norm of the difference of these cumulative distribution functions, computes to approximately 0.01974, which implies that is greater than . We could have chosen the optimal mesh

yielding a rate of order , but in this case in order to have the same time horizon , we would have needed data points, which is a large number. In practical applications, the cost of higher-frequency observations, if known, is to be balanced with desired precision on the Kolmogorov distance, which may well point to a lower frequency for a fixed time horizon.

References

- [1] Ersnt, P. Shepp, L. and Wyner, A. (2017) Yule’s "nonsense correlation" solved ! The Annals of Statistics, Vol. 45, No. 4, 1789-1809 DOI: 10.1214/16-AOS1509.

- [2] Ernst, P. Rogers, L.C.G and Zhou, Q. (2020) The distribution of Yule’s "nonsense correlation", https://arxiv.org/pdf/1909.02546.pdf.

- [3] Ernst, P. Huang, D. and Viens, F. Yule’s "nonsense correlation" for Gaussian random walks. (2021) https://arxiv.org/pdf/2103.06176.pdf.

- [4] Nourdin, I. and Peccati, G. (2009). Stein’s method on Wiener chaos. Probability Theory and Related Fields, 145, 75-118.

- [5] Phillips, P.C.B. (1986). Understanding spurious regressions in econometrics. J. Econometrics, 33: 311-340.

- [6] Nourdin, I. and Peccati, G.(2009). Stein’s method and exact Berry Esseen asymptotics for functionals of Gaussian fields. The Annals of Probability, 37(6), 2231-2261.

- [7] Nourdin, I. and Peccati, G. (2015). The optimal fourth moment theorem. Proc. Amer. Math. Soc. 143, 3123-3133.

- [8] Nourdin, I. and Peccati, G. (2012). Normal approximations with Malliavin calculus : from Stein’s method to universality. Cambridge Tracts in Mathematics 192. Cambridge University Press, Cambridge.

- [9] Nourdin, I., Viens, F. (2009). Density Formula and Concentration Inequalities with Malliavin Calculus. Electron. J. Probab. 14, 2287-2309.

- [10] Nualart, D. (2006). The Malliavin calculus and related topics. Springer-Verlag, Berlin.

- [11] Michel, R., Pfanzagl, J. (1971) The accuracy of the normal approximation for minimum contrast estimates. Z. Wahrscheinlichkeitstheorie verw Gebiete 18, 73?84. https://doi.org/10.1007/BF00538488.

- [12] Yule, G.U. (1926) Why do we sometimes get nonsense-correlations between time-series? A study in sampling and the nature of time-series. Journal of the Royal Statistical Society, 89(1): 1-63.