Optimal Consumption with Loss Aversion and Reference to Past Spending Maximum

Abstract

This paper studies an optimal consumption problem for a loss-averse agent with reference to past consumption maximum. To account for loss aversion on relative consumption, an S-shaped utility is adopted that measures the difference between the non-negative consumption rate and a fraction of the historical spending peak. We consider the concave envelope of the utility with respect to consumption, allowing us to focus on an auxiliary HJB variational inequality on the strength of concavification principle and dynamic programming arguments. By applying the dual transform and smooth-fit conditions, the auxiliary HJB variational inequality is solved in closed-form piecewisely and some thresholds of the wealth variable are obtained. The optimal consumption and investment control can be derived in the piecewise feedback form. The rigorous verification proofs on optimality and concavification principle are provided. Some numerical sensitivity analysis and financial implications are also presented.

Keywords: Loss aversion, optimal relative consumption, path-dependent reference, concave envelope, piecewise feedback control

Mathematical Subject Classification (2020): 91B16, 91B42, 93E20, 49L20

1 Introduction

Optimal portfolio-consumption via utility maximization has been one of the fundamental research topics in mathematical finance. In the seminal works of Merton [24, 25], the feedback optimal investment and consumption strategy is first derived by resorting to dynamic programming arguments and the solution of the associated HJB equation. Since then, abundant influential results and methodology have been rapidly developed to accommodate more general financial market models, trading constraints and other factors in decision making. Giving a complete list of references is beyond the scope of this paper. To partially explain the smooth consumption behavior, it has been suggested in the literature to take into account the past consumption decision in the measurement of the utility function. By considering the relative consumption with respect to a reference that depends on the past consumption, the striking changes in consumption can essentially be ruled out from the optimal solution. The widely used habit formation preference (see Abel [1], Constantinides [6], Detemple and Zapatero [10]) recommends the utility maximization problem as

where stands for the habit formation process taking the form with discount factors and the initial habit . That is, the satisfaction and risk aversion of the agent depend on the relative deviation of the current consumption from the weighted average of the past consumption integral. Along this direction, some recent developments can be found in Schroder and Skiadas [28], Detemple and Karatzas [9], Englezos and Karatzas [13], Yang and Yu [30], Yu [31, 32] and references therein. One notable advantage of the habit formation preference is its linear dependence on consumption, which enables one to consider as an auxiliary control in a fictitious market model so that the path-dependence can be hidden. This insightful transform, first observed in [28], reduces the complexity of the problem significantly. The martingale and duality approach can be applied by considering the adjusted martingale measure density process essentially based on Fubini theorem; see Detemple and Karatzas [9] and Yu [31, 32].

Another stream of research on the consumption reference focuses on its historical maximum level. Indeed, a large expenditure might signal the turning point of one’s standard of living and is usually a decision after careful thought and consideration. Such historical high spending moments are consequent on adequate wealth accumulation and often give rise to some long term subsequent consumption decisions such as maintenance, repairs and upgrade. To take into account the impact of the past consumption maximum, some previous studies incorporate the ratcheting or drawdown constraints that into the Merton optimal consumption problem where stands for the consumption running maximum process with the initial level and captures the degree of adherence towards the reference level . In particular, the case accounts for the ratcheting consumption constraint as studied in Dybvig [12], and the case depicts the consumption drawdown constraint as discussed in Arun [3] and Angoshtari et al. [2]. Meanwhile, it is also of great importance to understand the consumption behavior when the past spending maximum appears inside the utility. By taking the multiplicative form of reference, Guasoni et al. [14] and Li et al. [20] adopt the Cobb-Douglas utility with a zero discount factor and study the problem

Recently, Deng et al. [8] investigate an optimal consumption problem bearing the impact of the past spending maximum in the same form of the habit formation preference, which is defined by

The exponential utility is considered therein and the non-negative consumption constraint is enforced, yielding more regions for different consumption behavior. Although the running maximum term complicates the objective functional, the optimal consumption problems in both Guasoni et al. [14] and Deng et al. [8] can be tackled successfully under the umbrella of dynamic programming. The associated HJB variational inequalities and the feedback optimal controls can be solved in closed-form piecewisely in different regions, and some explicit and interpretable thresholds of the wealth are obtained. One key feature in Guasoni et al. [14] and Deng et al. [8] is their allowance of the agent to strategically consume below the reference level. Nevertheless, from the behavioral finance perspective, one shortcoming in these studies is their incapability to distinguish agent’s different risk aversion on the same-sized overperformance and falling behind with respect to the reference process. Instead, loss aversion depicts the agent’s proclivity to prefer avoiding losses to acquiring equivalent gains, naturally leads to different left and right derivatives of the utility function at the reference point. In particular, it is an open problem how the loss aversion on consumption with respect to the past consumption peak will affect the optimal investment and consumption behavior.

The loss aversion with a reference point has been studied in behavioral finance predominantly on terminal wealth optimization, see among Berkelaar et al. [4], Jin and Zhou [21], He and Zhou [17, 18], He and Strub [15], He and Yang [16] and references therein. Only a handful of papers can be found to encode that the agent may hurt more when the consumption is falling below a reference, especially when the reference level is endogenously generated by past decisions. Recently, Curatola [7] studies a utility maximization problem on consumption for a loss averse agent under an S-shaped utility when the reference is chosen as a specific integral of the past consumption process. Later, van Bilsen et al. [29] consider a similar problem under a two-part utility when the reference process is defined as the conventional consumption habit formation process. By imposing some artificial lower bounds on consumption control, the martingale and duality approach together with the concavification principle can be employed in both papers.

By contrast, the present paper investigates the optimal consumption behavior of a loss-averse agent who feels differently when the consumption is over-performing and falling below the past spending maximum. As the first attempt to combine the loss-aversion on relative consumption and the reference to historical consumption peak, the mathematical problem is formulated by

where is described by the conventional two-part power utility (see Kahneman and Tversky [22]) that

| (1.1) |

Here, stands for the loss aversion degree, and it is assumed in the present paper that , which represent the risk aversion parameters over the gain domain and the loss domain , respectively. The utility is an S-shaped function on . The parameter again reflects the degree of adherence towards the reference level , which now affects the expected utility directly.

Our aim is to solve this stochastic control problem by dynamic programming arguments and the PDE approach. However, the non-concave utility causes new troubles in solving the HJB variational inequality heuristically. In response to this, we propose to focus on the realization utility for each fixed and the control constraint and consider the concave envelope of only with respect to the variable on the strength of concavification principle. Similar to Deng et al. [8], by considering both the wealth level and reference level as state variables, we can derive the auxiliary HJB variational inequality in the piecewise form based on the decomposition of the domain when the feedback optimal consumption: (i) equals 0; (ii) lies between 0 and past spending maximum; (iii) coincides with the past spending peak. By utilizing the dual transformation only with respect to the wealth variable and treating the reference variable as a parameter, we arrive at a piecewise dual ODE problem in different regions. Together with some intrinsic boundary conditions and smooth-fit conditions, we are able to solve the piecewise ODE problem. In contrast to the exponential utility in Deng et al. [8], the concave envelope function in the current setting has no explicit form, which complicates the smooth fit arguments significantly. As a direct consequence, all coefficient functions in the solution to the dual ODE contain are implicit functions of the reference variable . After the inverse transform, all boundary curves separating different regions can still be expressed as thresholds of the wealth variable, albeit implicitly. The feedback optimal controls can also be derived analytically in terms of and , in which the optimal consumption may exhibit jumps. On account of the specific feedback form of optimal consumption in each region, the verification theorem on the optimality and concavification principle can be rigorously proved, giving the desired equivalence between the original problem and the auxiliary one using the concave envelope of the realization utility. When in (1.1) is an S-shaped utility, it is interesting to observe that the optimal consumption exhibits a jump and it is either zero or above the reference . That is, because the agent is risk-loving in the loss domain, she can never tolerate any positive consumption below the reference when the wealth is not sufficient and will prefer to stop consumption right away to accumulate more capital from the financial market to sustain her future high consumption.

The rest of the paper is organized as follows. Section 2 introduces the market model and the optimal consumption problem under the two-part utility with reference to past spending maximum. By considering the concave envelope of the utility function, we transform the original problem into an equivalent control problem. In Section 3, we solve the auxiliary HJB variational inequality. The optimal controls for the original problem are obtained in piecewise feedback form across different regions and all boundary curves are derived analytically. Section 4 presents some quantitative properties of the optimal controls and some numerical sensitivity analysis and their financial implications. In Section 5, we prove the verification theorem on optimality and concavification principle as well as some auxiliary results in previous sections.

2 Model Setup and Problem Formulation

2.1 Market Model and Preference

Let be a filtered probability space and satisfies the usual conditions. The financial market consists of one riskless asset and one risky asset. The riskless asset price follows , where is the interest rate. The risky asset price is governed by the SDE

where is a -adapted Brownian motion, and and stand for the drift and volatility. It is assumed that and the Sharpe ratio is denoted by .

Let be the amount of wealth that the agent allocates in the risky asset, and let represent the consumption rate. The self-financing wealth process satisfies

with the initial wealth . The control pair is said to be admissible if is -predictable and non-negative, is -progressively measurable, both satisfy the integrability condition a.s. for any as well as the no bankruptcy condition holds that a.s. for . We use to denote the set of admissible controls .

It is assumed in the present paper that the agent is loss averse on relative consumption in the sense that the agent feels more pain when the consumption is falling below the reference than the same-sized gain. The reference level is chosen as a fraction of the consumption running maximum process , where depicts the degree towards the reference, denotes the past spending maximum, and is the initial reference level. The utility maximization problem is defined by

| (2.1) |

where is the S-shaped utility defined in (1.1) with different risk-aversion parameters and on gains and losses of the relative consumption, and is the subjective discount rate to guarantee the convergence of the value function.

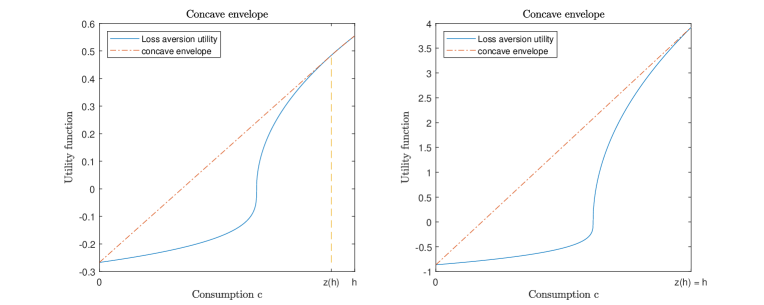

Two main challenges in solving (2.1) are the path-dependence of on the control and the non-concavity of the S-shaped utility . As a remedy, we propose to consider the concave envelope of the realization utility on consumption by first assuming the validity of concavification principle (see, for example, Reichlin [26] and Dong and Zheng [11]). Later, we plan to characterize the optimal control under the concave envelope function and then verify that the optimal control also attains the value function in the original problem, i.e., the concavification principle indeed holds. To be precise, for each fixed , let us consider as the concave envelope of with respect to the variable on a constrained domain. That is, for each fixed , let be the smallest concave function on such that holds for all .

2.2 Concave envelope of the realization utility

To emphasize the concave envelope only with respect to while keeping the variable fixed, let us consider an equivalent bivariate function

on the domain . Define and and denote and . Note that as . As when , we have two different subcases:

Subcase (i): If , there exists a unique solution to the equation

| (2.2) |

That is, is the tangent point of the straight line at to the curve for . Note that does not admit an explicit expression in this subcase.

Subcase (ii): If , we simply let . The concave envelope of on corresponds to the straight line through two points and .

Remark 2.1.

The condition of Subcase (ii) is fulfilled if and only if and model parameters satisfy one of the following three conditions that

Similar to Dong and Zheng [11], we can define the concave envelope of for by

| (2.3) |

Figure 1 illustrates two subcases of the concave envelope of the S-shaped utility . We stress that the function is implicit in as is an implicit function in general. To simplify the future presentation, let us also define

| (2.4) |

Hence, if , then , i.e., .

2.3 Equivalent problem

We now consider the auxiliary stochastic control problem

| (2.5) |

The equivalence between problems (2.1) and (2.5) is given in the next proposition. Its proof is deferred to Section 5.4 after we first establish the verification proof on optimality.

Proposition 2.1 (Concavification Principle).

For problem (2.5), we can derive the auxiliary HJB variational inequality that

| (2.6) |

for and . The free boundary condition will be specified later. Our goal is to find the optimal feedback control and . If is in , the first order condition gives the optimal portfolio in a feedback form by . This implies that the HJB variational inequality (2.6) can be simplified to

| (2.7) |

3 Derivation of the Solution

For ease of presentation and technical convenience, we only consider the case that in the present paper. Computations in general cases that and can be conducted similarly. However, some additional sufficient assumptions on model parameters are needed to facilitate the proofs of the verification theorem. Given the implicit concave envelope in (2.3), we can still solve the HJB variational inequality in the analytical form. In particular, we plan to characterize some thresholds (depending on ) for the wealth level such that the auxiliary value function, the optimal portfolio and consumption can be expressed analytically in each region.

Let us first introduce the boundary curves by

| (3.1) | ||||

where and are defined in Section 2.2. Here, and are derivatives of the concave envelope at and respectively, which are used to simplify the expression of when the maximum occurs at and . We also use to describe the free boundary curve . Note that if , we have as by (2.2); on the other hand, if , we have , yielding that as .

Similar to Deng et al. [8], we can heuristically decompose the domain into several regions based on the first order condition of and express the HJB equation (2.7) piecewisely. However, the concave envelope of the S-shaped utility complicates the computations here, in which the previous in (3.1), , will serve as the boundaries of these regions. We can then separate the following regions:

Region I: on the set is decreasing in , implying that and the HJB equation (2.7) becomes

| (3.2) |

Region II: on the set is increasing on and concave on , implying that and the HJB equation (2.7) becomes

| (3.3) |

Region III: on the set , is increasing in on , implying that . To distinguish whether the optimal consumption updates the past maximum process in this region, one can heuristically substitute in (2.7) and apply the first order condition to with respect to and derive the auxiliary singular control . We then need to split Region III further into three subsets:

Region III-(i): on the set , it is easy to see a contradiction that , and therefore the optimal consumption does not equal to and we should follow the previous feedback form , in which is a previously attained maximum level. The HJB variational inequality is written by

| (3.4) |

Region III-(ii): on the set , we get and the feedback optimal consumption is . This corresponds to the singular control that creates a new peak for the whole path that for any . We then impose the free boundary condition in this region, and the HJB equation follows the same PDE in (3.4).

Region III-(iii): on the set , we get . The optimal consumption is again a singular control , which pulls the associated upward to the new value , in which is the solution of the HJB equation on the set . This suggests that for any given initial value in the set , the feedback control pushes the value function jumping immediately to the point on the boundary set .

In summary, it is sufficient to consider the effective domain defined by

| (3.5) | ||||

and can only occur at the initial time .

Therefore, the HJB variational inequality (2.7) can be written to

| (3.6) | |||

where

To solve the above equation, some boundary conditions are also needed. First, to guarantee the global regularity of the solution, we need to impose smooth-fit conditions along two free boundaries that and . Next, if we start with 0 initial wealth, to avoid bankruptcy, the optimal investment and the consumption rate should be 0 at all times. Therefore, we have that

| (3.7) |

On the other hand, when the initial wealth tends to infinity, one can consume as much as possible, leading to an infinitely large consumption rate. In addition, a small variation of initial wealth will only lead to a negligible change of the value function. It follows that

| (3.8) |

We also note that, as the initial value is large enough, we have and thus Intuitively, our problem will be similar to the Merton problem [24] along the free boundary , in which the optimal consumption is asymptotically proportional to the wealth. Therefore, we expect to have that

| (3.9) |

for some constant . This condition will be verified later in Corollary 4.1.

To tackle the nonlinear HJB equation (3.6), we employ the dual transform only with respect to the variable and treat the variable as a parameter; see similar dual transform arguments in Deng et al. [8] and Bo et al. [5]. That is, we consider , . For a given , let us define the variable and it holds that . We can further deduce that , , and . The nonlinear ODE (3.6) can be linearized to

| (3.10) |

and the free boundary condition is transformed to . As can be regarded as a parameter, we can study the above equation as an ODE problem of the variable . Based on the dual transform, the boundary conditions (3.8) can be written as

| (3.11) |

The boundary condition (3.9) becomes

| (3.12) |

along the boundary curve . The boundary condition (3.7) is equivalent to

| (3.13) |

It holds by the dual transform that , and one can derive that . The free boundary condition (3.6) is translated to

| (3.14) |

Although the dual ODE problem looks similar to the one in Deng et al. [8], we emphasize that the boundary curves and are implicit functions of that contains the implicit function . As a result, it becomes more complicated to apply smooth-fit conditions to derive the solution analytically and to prove the verification theorem. It is inevitable that all coefficient functions (in terms of ) in the solution will involve . In particular, the following assumption on model parameters is needed, which is used is showing that the obtained solution is convex in and in the verification proof of the optimal control.

Assumption (A1) , , where and are two roots to the equation .

Note that implies that , , for .

Proposition 3.1.

Let Assumption (A1) hold. Under boundary conditions (3.11), (3.12), (3.13), the free boundary condition (3.14), and the smooth-fit conditions with respect to along and , ODE (3.10) in admits the unique solution that

| (3.15) |

where , is defined in (2.4), and are given in Assumption (A1), and are given in (3.1), and functions , , are defined by

| (3.16) |

Remark 3.1.

Note that all , , are implicit functions of . In particular, , and are written in the integral form. and are written in terms of implicit functions and . Some technical efforts are needed to handle these semi-analytical functions in the later verification proof.

Theorem 3.1 (Verification Theorem).

Let , and , where stands for the initial wealth, is the initial reference level, and is the effective domain (3.5). Let Assumption (A1) hold. For , let us define the feedback functions that

| (3.17) |

and

| (3.18) | ||||

We consider the process , where is the discounted rate state price density process, and is the unique solution to the budget constraint with

The value function can be attained by employing the optimal consumption and portfolio strategies in the feedback form that and for all , where and .

Remark 3.2.

Note that the optimal consumption has a jump when and whenever . Meanwhile, we note that the running maximum process still has continuous paths for . Indeed, from the feedback form, jumps only when and we also have that after the jump, i.e., the jump will never increase . Therefore, both and still have continuous paths.

By the dual representation, we have that . Define as the inverse of , then . Note that the function should have a piecewise form across different regions. The invertibility of the map is guaranteed by the next lemma.

Lemma 3.1.

Let Assumption (A1) hold. The function is convex in all regions so that the inverse Legendre transform is well defined. Moreover, it implies that the feedback optimal portfolio .

Proof.

The proof is given in Section 5.5. ∎

Thanks to Lemma 3.1, we can apply the inverse Legendre transform to the solution in (3.15). Similar to Section 3.1 in [8], we can derive the following three boundary curves and that

| (3.19) | ||||

and it holds that the feedback function of the optimal consumption satisfies: (i) when ; (ii) when ; (iii) when . In particular, the condition in the effective domain can be explicitly expressed as . Moreover, the following inverse function is well defined that

| (3.20) |

Along the boundary , the feedback form of the optimal consumption in (3.23) is presented by . Using the dual relationship and Proposition 3.1, the function can be implicitly determined as follows:

Corollary 3.1.

For , , and , under Assumption (A1), let us define the piecewise function

The value function in (2.5) can be written by

where the free boundaries , , and are given explicitly in (3.19). The feedback optimal consumption and portfolio can be expressed in terms of primal variables that

| (3.23) |

where is given in (3.20), and

| (3.24) | ||||

Moreover, for any initial value , the stochastic differential equation

| (3.25) |

has a unique strong solution given the optimal feedback control as above.

Proof.

The proof is given in Section 5.3. ∎

4 Properties of Optimal Controls

First, comparing with the main results in the standard Merton’s problem with power utility (see [24]), our optimal feedback controls and are fundamentally different, which are expressed as the piecewise implicit nonlinear functions of both variables and . In particular, our optimal consumption process exhibits jumps when the wealth level crosses the threshold . The more complicated solution structure is rooted in the path-dependent reference process inside the utility and the S-shaped utility accounting for the loss aversion.

Moreover, based on Corollary (3.1), we can show some asymptotic results on the optimal consumption-wealth ratio and the optimal portfolio-wealth ratio , whose proof is given in Section 5.6.

Corollary 4.1.

As , the asymptotic behavior of large wealth is equivalent to . We then have that

for some constants and . In addition, as , two limits and coincide with the asymptotic results in the infinite-horizon Merton’s problem [24] with power utility . As a result, the boundary conditions (3.9) and (3.12) hold valid in our problem.

Remark 4.1.

As the wealth level gets sufficiently large, both the optimal consumption and the optimal portfolio amount are asymptotically proportional to the wealth level that and , in a similar fashion to the asymptotic results in the standard Merton’s problem with the power utility. However, it is important to note that our asymptotic limits differ significantly from the ones in the Merton’s problem, which now sensitively depends on the reference degree parameter and risk aversion parameters from the S-shaped utility. One can see that, even when the agent’s wealth level is very high, the impacts from the reference level and the loss aversion preference will not fade out in our model due to the fact that the large consumption rate will also lift up the reference to a new high level. Only in the extreme case when the reference degree , i.e., there is no reference process, our asymptotic results will coincide with the ones in the standard Merton’s problem under the power utility.

Next, we can characterize the average fraction of time that the agent expects to stay in each region.

Corollary 4.2.

The following properties hold:

-

1.

The long-run fraction of time that the agent stays in the region equals the value of .

-

2.

The long-run fraction of time that the agent stays in the region equals the value of .

-

3.

Starting from , let us consider the first hitting time of zero consumption that . We have that

where and satisfy:

-

4.

Starting from , let us define the first hitting time to update the historical consumption maximum . We have that

We next present some numerical examples of the thresholds and the optimal feedback functions and discuss some financial implications.

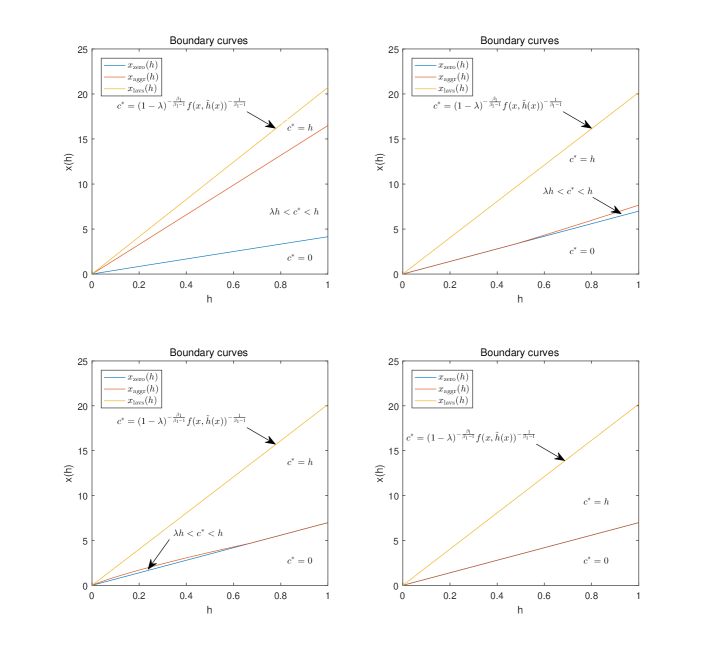

We first plot in Figure 2 the boundary curves , and as functions of , separating the regions for different feedback forms of the optimal consumption. First, comparing with Figure 1 in Deng et al. [8], it is interesting to note that we need to take into account of four different cases in total depending on whether two boundary curves and may coincide or not. To be more precise, we know by definition that if and only if , where and are given in (3.1). In view of Remark 2.1, in three different scenarios. The upper left panel in Figure 2 corresponds to the case that two boundaries and are completely separated for all , i.e., for (with parameters , , , , , , ); the upper right panel in Figure 2 corresponds to the case that two boundaries when the reference level is low that for some critical point (with parameters , , , , , , ); the lower left panel in Figure 2 corresponds to the case that two boundaries when the reference level is high that for some (with parameters , , , , , , ); and the lower right panel in Figure 2 corresponds to the case that for all (with parameters , , , , , , ).

Second, Figure 2 illustrates again that the positive optimal consumption can never fall below the reference level, i.e., we must have if so that there exists a jump when the wealth process crosses the boundary curve . In particular, for some value of such that hold, the optimal consumption may jump from to the current maximum level immediately, indicating that the agent consumes at the historical maximum level if the agent starts to consume. This differs substantially from the continuous optimal consumption process derived in Deng et al. [8]. The jump of consumption is caused by the risk-loving attitude over the loss domain in the S-shaped utility, which corresponds to the linear piece of the concave envelop. In this wealth region, the agent prefers to stop the current consumption if it cannot surpass the reference level. Therefore, our result under the S-shaped utility can depict the extreme behavior of some agents who cannot endure any positive consumption plan below the current reference. We emphasize that, all the boundary curves in Figure 2 are generally nonlinear functions of , featuring the necessity of two dimensional state processes of and in our control problem. Only in the extreme case when , the boundary curves can be expressed in a linear manner, and the dimension reduction can be conducted.

Remark 4.2.

When risk aversion parameters satisfy , our problem has a homogeneous property that , and it is sufficient to consider the function to reduce the dimension. In this case, the boundary curves degenerate to boundary points for the new state variable .

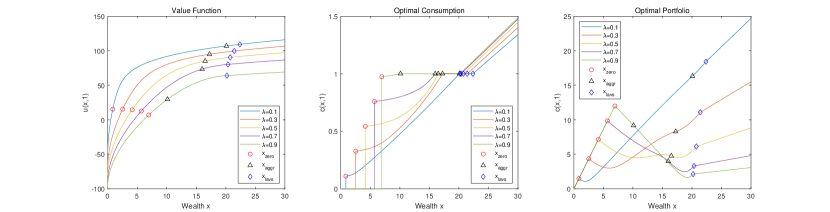

We now fix the model parameters that , , , , , , , and reference level . We will numerically illustrate the sensitivity with respect to the reference degree . Let us choose . The value function, the optimal feedback consumption, and the optimal feedback portfolio together with marked boundaries , and are plotted in Figure 3. From all panels, one can observe that the boundary curve is increasing in , while boundary curves and are both decreasing in . On one hand, one can explain that, when the agent has higher reference with the larger and the current wealth is low, it is more likely that the optimal consumption falls below the reference, leading to zero consumption. Therefore, the threshold for positive consumption is getting larger for a larger . On the other hand, when the wealth is sufficiently large, larger reference degree will result in more aggressive consumption (see the middle panel) and it is more likely that the agent will lower the threshold to consume at the global maximum level even by reducing the portfolio amount. Moreover, when increases, we can also observe that actually increases faster than the consumption during the life cycle, which leads to a drop of and a decline in the value function from the left panel. From the right panel, when wealth decreases to the region , the optimal consumption stays at 0 due to the linear piece of the concave envelop, but the optimal portfolio is increasing in with a large slope. This can be interpreted by the fact that the agent needs to invest very aggressively to pull the wealth level back to the threshold driven by the strong desire of positive consumption under the loss aversion preference. When wealth starts to surpass the threshold , the agent chooses the positive consumption above the reference level , and we can see from the right panel that the agent will strategically withdraw some wealth from the risky asset account to support the high consumption plan. In addition, the higher reference degree is, the more drastic decreasing in portfolio with respect to can be observed. When wealth tends to be further larger, both the optimal consumption and optimal portfolio become increasing in . By comparison from the right panel, when wealth is very large, the optimal portfolio is decreasing in the reference degree , which is consistent with the fact that the agent needs more cash to support the more aggressive consumption as increases.

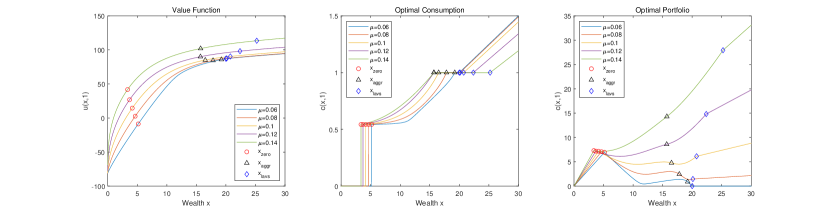

Finally, we numerically illustrate the sensitivity with respect to the expected return of the risky asset. Let us fix model parameters that , , , , , , , and consider . The value function and the optimal feedback controls together with marked boundaries are plotted in Figure 4. First, from the left panel, one can observe that the value function increases in , which matches with the intuition that the better market performance guarantees the higher wealth and the larger consumption plan. From all panels, it is also interesting to observe that both boundaries and are decreasing in , while the boundary is increasing in . On one hand, the higher return from the financial market secures the better wealth growth, leading to lower thresholds for the agent to start the positive consumption and the consumption at the historical peak level. On the other hand, higher return rate also motivates the agent to invest more in the risky asset as one can see the optimal portfolio is increasing in from the right panel. As a result, the agent will not blindly lower the threshold to create the new global consumption peak as it becomes more beneficial in the long run to invest more cash into the risky asset when is sufficiently large. Therefore, the threshold is actually increased with an increased parameter . One can also observe that for , as the expected return increases, the agent will gradually shift from the willingness of high consumption plan by sacrificing the portfolio to the more aggressive investment behavior to accumulate the larger wealth. Combing Figure 3 and Figure 4, we also note that the optimal portfolio is decreasing in but increasing in when is large, suggesting that some agents with the large reference degree will only be motivated to invest more wealth in the financial market when the expected return is excessively high. This is consistent to and may partially help to explain the equity premium puzzle (see Mehra and Prescott [23]) that the market premium needs to be very high to attract some agents (possibly those agents with the large reference degree if they adopt our proposed preference on consumption performance) to actively invest in the risky asset.

5 Proofs

5.1 Proof of Proposition 3.1

It is straightforward to see that the linear ODE (3.10) admits the general solution

where are functions of to be determined.

The free boundary condition in (3.13) implies that . Together with free boundary conditions in (3.13) and the formula of in the region , we deduce that . To determine the remaining parameters, we consider the smooth-fit conditions with respect to the variable along and that

| (5.1) | ||||

The equations in (5.1) can be treated as linear equations for , , and and . By solving the system of equations, we can obtain

Therefore, to can be expressed by (3.1). To solve and , we will find first, and and can then be determined.

Indeed, as , we get in the region , and the boundary condition (3.12) leads to , where is a positive constant. Along the free boundary, we have . It follows from that as . Therefore, we can deduce that . By Lemma 5.1 and the definition , it follows that

as , where the last equation holds because

From Assumption (A1), it follows that . Therefore, we can write . We then apply the free boundary condition (3.14) at that

which implies the desired result of in (3.1).

5.2 Proof of Theorem 3.1 (Verification Theorem)

The proof of the verification theorem boils down to show that the solution of the auxiliary HJB variational inequality (2.6) coincides with the value function, i.e. there exists such that . For any admissible strategy , we have by the supermartingale property and the standard budget constraint argument, see Karatzas et al. [19].

Let be regarded as parameters, the dual transform of with respect to in the constrained domain that defined in (3.10). Moreover, can be attained by the construction of the feedback optimal control in (3.17).

In what follows, we distinguish the two reference processes, namely and that correspond to the reference process under an arbitrary consumption process and under the optimal consumption process with an arbitrary . Note that the global optimal reference process will be defined later by with to be determined. Let us now further introduce

| (5.2) |

where is the discounted martingale measure density process.

For any admissible controls , recall the reference process , and for all , we see that

| (5.3) | ||||

the third equation holds because of Lemma 5.3, and the last equation is verified by Lemma 5.2. In addition, Lemma 5.4 guarantees the equality with the choice of , in which satisfies that for a given and . In conclusion, we have that

Then we prove some auxiliary results that have been used above. We first need some asymptotic results on the coefficients in Proposition 3.1.

Lemma 5.1.

Proof.

We first discuss the asymptotic results of and . It is easy to see that and thus , . Moreover, if , we have ; if , indicating that , thus we have and . Therefore, we have and .

To obtain the asymptotic properties of to , we need to derive the asymptotic property of . If , the equation (2.2) indicates that

| (5.4) |

where , , and . We shall obtain the asymptotic property of in two cases: and respectively. In the sequel of the proof below, let be a generic positive constant independent of , which may be different from line to line. If , as , the second term of equation (5.4) goes to infinity, yielding and thus ; as , the second term goes to 0, yielding and thus . If , we can similarly obtain that and as goes to infinity and 0 respectively. Together with the fact that , we deduce that

If , then , and . If , then , , and thus and . In summary, we have and .

We further discuss the asymptotic property of . If , it is obvious that . Otherwise, we have

Since , we can derive that , , , and .

Based on the asymptotic property of and , we shall find the asymptotic results of to . let us begin with and . It is easy to see that

Note that

and

where to are discriminant constants in each equation. Then by , , , , , , , and , we have

and

where to are discriminant constants, and thus

Recall that

We can get the asymptotic property of that

Finally, it follows that

and

in view that . ∎

Following similar proofs of Lemma 5.1 and Lemma 5.2 in Deng et al. [8] and using asymptotic results in Lemma 5.1, we can readily obtain the next two lemmas.

Lemma 5.2.

Lemma 5.3.

Let , , and be the same as in Lemma 5.2, then for all , we have , , and hence

Let us then continue to prove some other auxiliary results.

Lemma 5.4.

The inequality in (5.3) becomes equality with , , with as the unique solution to

| (5.5) |

Proof.

By the definition of , it is obvious that for all , . Moreover, the inequality becomes an equality with the optimal feedback . Thus, it follows that

To turn (5.3) into an equality, the equality of (5.5) needs to hold with some to be determined later, and

| (5.6) |

also needs to hold. Hence, we choose to employ , where

It follows from definition that: (i) If , then and , it indicates that ; (ii) If , then and , it indicates that . The existence of can thus be verified if is continuous in .

Indeed, let , then exists and is continuous in , and

Therefore, is also continuous in . ∎

Lemma 5.5.

The following transversality condition holds that for all ,

Proof.

Recall that . In this proof, the results in Lemma 5.7 and Lemma 5.8 are applied repeatedly, therefore, we omit the illustrations if there is no ambiguity. In more details, we use Lemma 5.7 with , and use Lemma 5.8 with and since , which can be obtained by some simple computations.

Let us firstly consider the case . We first write that

| (5.7) |

in which the second term converges to 0 as due to Lemma 5.7. For the first term in (5.7), since , we have

We then consider the case . In this case, , and thus

| (5.8) | ||||

We consider asymptotic behavior of the above equation term by term as .

The third term in (5.8) clearly converges to 0 by Lemma 5.7. For the fourth term in (5.8), since , we have

which also vanishes as by Lemma 5.7.

Let us continue to consider the terms containing and in equation (5.8). Because of the constraint due to which is discussed in the proof of Remark (5.1), we can deduce that

which converges to 0 by Lemma 5.8.

Finally, we consider the case and write that

| (5.9) | ||||

In this case, similar to the discussion for (5.8), we have

Lemma 5.6.

For any , we have

| (5.10) |

Proof.

By the definition of , for all , we have , and thus

Therefore, we have that , . Together with the fact that by Assumption (A1), we will show the order of in cases when , , and .

Lemma 5.7.

For , we have

| (5.11) |

Proof.

It is obvious that

and it is clear that as .

Let us define with its running maximum . It follows that

where , , , and . Note that , thanks to the Corollary A.7 in Guasoni et al. [14], we have that

and therefore

where . It thus holds that

as . Thanks to Assumption (A1), we have . It follows that and thus

which tends to 0 as . ∎

Lemma 5.8.

For any , we have

| (5.12) |

Proof.

In fact, we have that

which converges to 0 in view that by Assumption (A1). ∎

5.3 Proof of Corollary 3.1

To conclude the main results in Corollary 3.1, it is sufficient to prove that the SDE (3.25) has a unique strong solution for any initial value . To this end, we can essentially follow the arguments in the proof of Proposition 5.9 in [8]. However, due to more complicated expressions of - in (3.1) and different feedback functions, we need to prove the following auxiliary lemmas to conclude Corollary 3.1.

Lemma 5.9.

The function is within each of the subsets of and , and it is continuous at the boundary of and . Moreover, we have that

| (5.13) | ||||

and

| (5.14) |

Proof.

The proof is the same as Lemma 5.6 in [8], so we omit it. ∎

Lemma 5.10.

The function is Lipschitz on .

Proof.

By (3.17), (3.18) and the inverse transform, we can express and in terms of the primal variables as in (3.23) and (3.24). Combining the expressions of and with Proposition 3.1 which implies that the coefficients are , Lemma 5.9 which implies that the regularity of , together with the continuity of at the boundary between the three regions, we can draw the conclusion that and are locally Lipschitz on .

(i) Boundedness of .

First using in (3.24), we have

| (5.15) | ||||

Note that the first line is constant and hence bounded. For the second line, by differentiating (3.21) and using the fact that , we have that

Plugging this back to , we can obtain

Combining with Lemma 5.9, we can obtain , where

| (5.16) | ||||

We will show that and , and is bounded. We only need to discuss the case that , because the second region will reduce to a point for any fixed if . Indeed, it is obvious that since according to the proof of Lemma 3.1 and . Moreover, we have that

where is some positive constant. For , according to the proof of Lemma 3.1, we have that

where is some positive constant. Therefore, for some positive constant independent of , and thus in the second line of (5.15) is bounded.

For the third line, by differentiating (3.22) and using the fact that , we have that . Putting this back to the third line of (5.15), we can obtain where

| (5.17) | ||||

by combining with the results of Lemma 5.9. In fact, by the proof of Lemma 3.1, we have and , therefore, and . Moreover, we have that

and thus

, indicating that is bounded in the third line.

(ii) Boundedness of .

First, using equations (5.13) and (5.14) and the definition of , we have

We analyze the derivative in different regions separately. In the region , , hence it is bounded. In the region , we also only need to discuss the case that , and

By differentiating (3.21) and using the fact that , we have that

Putting this back to the previous expression of , we can obtain that

| (5.18) | ||||

where is defined in (5.16). In (5.18), the third term is a constant. For the second term, by the proof of Lemma 3.1, we first have , and

In the sequel of the proof below, let be a generic positive constant independent of , which may be different from line to line. Hence, we have that

Therefore, the second term is bounded.

For the first term in (5.18), by virtue of , it is enough to show that for some positive constant . Indeed, we have that , where is defined in (5.16). As and are bounded, it is sufficient to show that is bounded. As , let be a generic constant that may differ from line to line, we have that

where the first inequality holds because of . Similarly, let be the constant that may differ from line to line, it follows that

which is bounded as .

In the region , similar computations yield that

where is defined in (5.17). For the term , due to , we have that which is bounded as , where is chosen such that . Moreover, for the term , similar to the proof in the region , it is enough to check that is bounded. Indeed, we can obtain

which is shown to be bounded. Putting all the pieces together completes the proof. ∎

5.4 Proof of Proposition 2.1 (Concavification Principle)

To prove this proposition, we claim that under the optimal controls and , it holds that all the time. In fact, for any , according to the definition of concave envelop of in in (2.3), we can easily see that if , where is defined in Section 2.2. We will interpret the claim in all the regions of the wealth .

If , then , indicating that .

If , yielding the existence of the solution for equation (2.2) with . Moreover, the optimal consumption satisfies that , where is defined in Corollary 3.1. This leads to the fact that and thus .

If , then , indicating that .

Therefore, we have verified that the optimal consumption rate always leads to . Thus, given the optimal portfolio and for the stochastic control problem (2.5), based on the fact that everywhere and corresponding , we have

that is, , and the optimal portfolio and consumption for (2.1) are the same as (2.5).

5.5 Proof of Lemma 3.1

We prove in three regions: , , and , respectively.

(i) In the region , .

As , we only need prove and . We shall separate the proof into two cases: the case that and that . If , we can deduce that

and

therefore, we have .

We next prove that , and hence . It is easy to see that , and hence , where the second inequality follows from

thanks to and .

Along the free boundary condition (3.14), we have , therefore, we can deduce that .

We then consider the case that in which we have that

and . Thus, it holds that , implying that when .

(ii) In the region , we only need to consider the case that , otherwise the second-order derivative of in will be trivial because this region will reduce to a point.

Because , , , we can deduce that

where the last inequality holds because , , and . Moreover, we have that

Thus, we can deduce that .

(iii) In the region , . Since , we only need to prove that . We shall also discuss for two cases that or respectively.

If , indicating that we have . Similar to the proof of , we have

If , similar to the proof of , we can obtain that .

5.6 Proof of Corollary 4.1

Proof.

We first have that

by L’Hpital’s rule. To compute , we need to consider two cases that and .

We first consider the case that as , indicating that and in condition (S2) or (S3), therefore, , and thus

Therefore, we can derive that

and

Let us then consider the other case when . If , the second term in (5.4) converges to 0, and thus converges to a constant . If , the second term in (5.4) equals a constant, and becomes a constant that is the unique solution to . Otherwise, if , the second term in (5.4) goes to infinity as , indicating that converges to 0.

Thus, we always have that

where . It holds that

Then we can deduce that

and

where

Recall that and in the Merton’s problem. In our setting, as , it is obvious that . On the other hand, similar to the discussion of the limit of as , we have that as , and thus as in all three scenarios when as . Therefore, we can deduce that

and

which complete the proof. ∎

5.7 Proof of Corollary 4.2

Proof.

Let us consider the auxiliary process and defined in Theorem 3.1.

(i) The long-run fraction of time that the agent stays in the region can be computed by

where the last equation holds by the same argument to prove Theorem 5.1 in [14].

(ii) The long-run fraction of time that the agent stays in the region can be computed by

(iii) Let be the solution to the following PDE:

where . It holds that , where and satisfy

Applying It’s formula to , and integrating from 0 to , we have that

Note that , the stochastic integral is square-integrable and thus a martingale with zero mean, and only increases when , implying . Together with the fact that , we can finally deduce that .

(iv) Before time , the historical consumption peak does not increase, and

Then, by equation (9.1) in [27], let , , , it follows that for any : . Then, it holds that

∎

Acknowledgements

We thank two anonymous referees for their helpful comments on the presentation of this paper. X. Li is partially supported by the Hong Kong General Research Fund under grants 15215319, 15216720 and 15221621. X. Yu is supported by the Hong Kong Polytechnic University research grant under no. P0031417.

References

- [1] A. B. Abel. Asset prices under habit formation and catching up with the joneses. The American Economic Review, 80(2):38–42, 1990.

- [2] B. Angoshtari, E. Bayraktar and V. Young. Optimal dividend distribution under drawdown and ratcheting constraints on dividend rates. SIAM Journal on Financial Mathematics, 10(2):547-577, 2019.

- [3] T. Arun. The Merton problem with a drawdown constraint on consumption. Preprint, arXiv:1210.5205, 2012.

- [4] A. B. Berkelaar, R. Kouwenberg, and T. Post. Optimal portfolio choice under loss aversion. Review of Economics and Statistics, 86(4):973–987, 2004.

- [5] L. Bo, H. Liao and X. Yu. Optimal tracking portfolio with a ratcheting capital benchmark. SIAM Journal on Control and Optimization, 59(3):2346–2380, 2021.

- [6] G. M. Constantinides. Habit formation: A resolution of the equity premium puzzle. Journal of Political Economy, 98(3):519–543, 1990.

- [7] G. Curatola. Optimal portfolio choice with loss aversion over consumption. The Quarterly Review of Economics and Finance, 66:345–358, 2017.

- [8] S. Deng, X. Li, H. Pham and X. Yu. Optimal consumption with reference to past spending maximum. Finance and Stochastics, 26:217-266, 2022.

- [9] J. Detemple and I. Karatzas. Non-addictive habits: Optimal consumption-portfolio policies. Journal of Economic Theory, 113:265–285, 2003.

- [10] J. Detemple and F. Zapatero. Optimal consumption-portfolio policies with habit formation. Mathematical Finance, 2(4):251–274, 1992.

- [11] Y. Dong and H. Zheng. Optimal investment with S-shaped utility and trading and value at risk constraints: An application to defined contribution pension plan. European Journal of Operational Research, 281:341–356, 2020.

- [12] P. H. Dybvig. Dusenberry’s ratcheting of consumption: Optimal dynamic consumption and investment given intolerance for any decline in standard of living. The Review of Economic Studies, 62(2):287–313, 1995.

- [13] N. Englezos and I. Karatzas. Utility maximization with habit formation: Dynamic programming and stochastic PDEs. SIAM Journal on Control and Optimization, 48(2):481–520, 2009.

- [14] P. Guasoni, G. Huberman and D. Ren. Shortfall aversion. Mathematical Finance, 30(3):869-920, 2020.

- [15] X. He and M. Strub. How endogenization of the reference point affects loss aversion: a study of portfolio selection. Operations Research, 70(6):3035-3053, 2022.

- [16] X. He and L. Yang. Realization utility with adaptive reference points. Mathematical Finance, 29(2):409–447, 2019.

- [17] X. He and X.Y. Zhou. Portfolio choice under cumulative prospect theory: An analytical treatment. Management Science, 57(2):315–331, 2011.

- [18] X. He and X.Y. Zhou. Myopic loss aversion, reference point, and money illusion. Quantitative Finance, 14(9):1541–1554, 2014.

- [19] I. Karatzas, J. P. Lehoczky, S. E. Shreve and G. L. Xu. Martingale and duality methods for utility maximization in an incomplete market. SIAM Journal on Control and Optimization, 29:702-730, 1991.

- [20] X. Li, X. Yu and Q. Zhang. Optimal consumption and life insurance under shortfall aversion and a drawdown constraint. Insurance: Mathematics and Economics, 108:25–45, 2023

- [21] H. Jin and X.Y. Zhou. Behavioral portfolio selection in continuous time. Mathematical Finance, 18(3):385–426, 2008.

- [22] D. Kahneman and A. Tversky. Prospect theory: An analysis of decision under risk. In Handbook of the fundamentals of financial decision making: Part I, pages 99–127. World Scientific, 2013.

- [23] R. Mehra and E. C. Prescott. The equity premium: A puzzle. Journal of Monetary Economics, 15(2):145-161, 1969.

- [24] R. C. Merton. Lifetime portfolio selection under uncertainty: The continuous time case. The Review of Economics and Statistics, 51(3):247–257, 1969.

- [25] R. C. Merton. Optimal consumption and portfolio rules in a continuous-time model. Journal of Economic Theory, 3:373–413, 1971.

- [26] C. Reichlin. Utility maximization with a given pricing measure when the utility is not necessarily concave. Mathematics and Financial Economics, 7(4):531–556, 2013.

- [27] L. C. G. Rogers and D. Williams. Diffusions, markov processes and martingales, Volume 1: Foundations. John Wiley & Sons, Ltd., Chichester, 7, 1994.

- [28] M. Schroder and C. Skiadas. An isomorphism between asset pricing models with and without linear habit formation. The Review of Financial Studies, 15(4):1189–1221, 2002.

- [29] S. van Bilsen, R. Laeven and E. Nijman. Consumption and portfolio choice under loss aversion and endogenous updating of the reference level. Management Science, 66(9):3799–4358, 2020.

- [30] Y. Yang and X. Yu. Optimal entry and consumption under habit formation. Advances in Applied Probability, 54(2):433–459, 2022.

- [31] X. Yu. Utility maximization with addictive consumption habit formation in incomplete semimartingale markets. Annals of Applied Probability, 25(3):1383–1419, 2015.

- [32] X. Yu. Optimal consumption under habit formation in markets with transaction costs and random endowments. Annals of Applied Probability, 27(2):960–1002, 2017.