Efficient approximation of SDEs driven by countably dimensional Wiener process and Poisson random measure

Abstract.

In this paper we deal with pointwise approximation of solutions of stochastic differential equations (SDEs) driven by infinite dimensional Wiener process with additional jumps generated by Poisson random measure. The further investigations contain upper error bounds for the proposed truncated dimension randomized Euler scheme. We also establish matching (up to constants) upper and lower bounds for -complexity and show that the defined algorithm is optimal in the Information-Based Complexity (IBC) sense. Finally, results of numerical experiments performed by using GPU architecture are also reported.

Key words: countably dimensional Wiener process, Poisson random measure, stochastic differential equations with jumps, randomized Euler algorithm, lower error bounds, complexity

MSC 2010: 65C30, 68Q25

1. Introduction

We investigate strong pointwise approximation of solutions of the following stochastic differential equations

| (1) |

where , , , and is a countably dimensional Wiener process on a complete probability space , i.e., an infinite sequence of independent scalar Wiener processes defined on the same probability space. We also assume that is a Poisson random measure with an intensity measure , where is a finite Lévy measure on . We assume that and are independent. In the sequel we will also impose suitable regularity conditions on the coefficients and .

Analytical properties and applications of such SDEs are widely investigated in [5] and [11]. It follows that the case of countably dimensional Wiener process naturally extends the well-known case when only finite dimensional is considered. It allows us to model much more complicated structure (in fact, infinite dimensional) of noise but we do not have to use (somehow involved) theory of stochastic partial differential equations. However, in most cases exact solutions of the underlying SDEs are not known (even when only finite dimensional Wiener process is considered) and efficient approximation of solutions, together with implementation of developed algorithms, is of main interest.

The topic of approximation of jump-diffusion SDEs driven by finite dimensional Wiener and Poisson processes has been widely investigated in the literature in recent years, see, for example, [2], [7], [8], [9], [13], [14], [15], [31], and [27], which is a standard book reference. Lower error bounds and optimality issues have been raised in [10], [16], [18], [29], [30]. The growing popularity of SDEs with jumps follows from their wide applications in, for example, mathematical finance, modelling energy markets etc., see [27], [32], [33].

In this paper we define so-called truncated dimension randomized Euler scheme and we use it to approximate the value of , where the error is measured the -norm. In particular, the algorithm uses only finite dimensional evaluations of . This algorithm can be seen as a generalisation of the randomized Euler method investigated in [23], [24] for SDEs driven by a finite dimensional Wiener process. (See also [19], [25] where the authors defined randomized version of the Milstein algorithm.) Recall that randomization in the drift coefficient allows us to handle discontinuities wrt the time variable , since we assume that is only Borel measurable in the variable . We investigate properties of the method such as: error bounds and their dependence on the parameters ; its cost optimality in certain classes of coefficients and among algorithms that use only finite number of evaluations of , , and finite number of samples from the Poisson random measure . Moreover, we propose effective implementation of this algorithm in C programming language with CUDA application programming interface (API).

In summary, the main contributions of the paper are as follows:

-

•

derivation of upper error bounds for proposed truncated dimension randomized Euler algorithm together with its convergence rate (Theorem 1),

- •

-

•

effective implementation of the method which utilises GPU architecture, and numerical experiments that confirm our theoretical findings (Section 5).

The structure of the paper is as follows. In Section 2 we describe the main problem and provide necessary notations, and definitions. In Section 3 we define the truncated dimension Euler algorithm and show its upper error bounds. Then, in Section 4 we deal with lower error bounds in the class of algorithm under consideration. We also provide complexity bounds and establish optimality of the previously defined algorithm in some particular subclasses of the input data. Our theoretical results are supported by numerical experiments described in Section 5. There, we also provide the key elements of our current algorithm implementation in CUDA C. Finally, auxilliary lemmas together with their proofs are presented in Appendix.

2. Preliminaries

Let We treat a real –dimensional vector as a –dimensional matrix. By we denote Frobenius norm for matrices respectively. In case by we understand the Hilbert-Schmidt norm for infinite dimensional matrices. The norms appearing in the paper will be clear from the context. We also set

where , . Let be a complete probability space and . For a random vector we write , . Let be a Lévy measure on , i.e., is a measure on that . We further assume that . Let be a countably dimensional Wiener process and let be a Poisson random measure, both defined on the space . We assume that and are independent of each other. Let be a filtration on that satisfies the usual conditions, i.e., and is right-continuous, see [28]. We assume that is an -Wiener process and is an -Poisson measure with the intensity measure . Then, by Theorem 1.4.1 in [21], there exists a scalar Poisson process with intensity and an iid sequence of -valued random variables with the common distribution such that the Poisson random measure can be written as follows for . The -dimensional compound Poisson process, associated with the Poisson measure , is defined as . We also set , , , and we define , for any . Of course and are independent for any . Moreover, for all , the -fields and are independent. For a càdlàg process by we mean its càglàd modification. We refer to Chapter 2.9. in [1] for further properties of càdlàg mappings.

For we consider a class of all functions satisfying the following conditions:

-

(A1)

is Borel measurable,

-

(A2)

for all ,

-

(A3)

for all , .

Let be a positive, strictly decreasing sequence, converging to zero and let , . We consider the following class of functions , where , . Namely, iff it satisfies the following conditions:

-

(B1)

,

-

(B2)

for all and ,

-

(B3)

for all and ,

-

(B4)

for all and , where is the following projection operator

We denote and then for all . We also set , so for all .

Let , and let be the Lévy measure as above. We say that a function belongs to the class if and only if

-

(C1)

is Borel measurable,

-

(C2)

,

-

(C3)

for all , ,

-

(C4)

for all , .

Finally, we define the following class

As a set of admissible input data we consider the following class

The constants together with , the Lévy measure , and the sequence are referred to as parameters of the class . Except for , the parameters are not known and cannot be used by an algorithm as input parameters.

Since is a finite random (counting) measure, and , differ on at most countable number of time points, the equation (1) can be written as

| (2) |

where

is the compensated Poisson measure, and

| (3) |

Moreover,

is the stochastic Itô integral wrt the countable dimensional Wiener process , see pages 427-428 in [5]. (See also [11] where even more general setting than (2) is considered.) In the case when is countably dimensional Wiener process the above stochastic Itô integral can be understood as a stochastic integral wrt cylindrical Wiener process in the Hilbert space , see pages 289-290 in [5] and Remark 3.9 in [6]. Alternatively properties of such stochastic integrals were widely described and proved in [3], [22]. From [5] and the papers [3], [22] it follows that the stochastic Itô integral wrt the countably dimensional Wiener process has analogous properties as in the case finite dimensional case - in particular, we can use the Burkholder’s inequality, Itô formula etc. Moreover, by the Fact 2 and Lemma 17.1.1 in [5] for any there exists a unique strong solution of the equation (2) (and therefore also (1)).

The aim of this paper is to construct an efficient scheme that approximates , i.e., the value of solution of (1) at the final time point . We consider algorithms that use only finite dimensional evaluations of at finite number of points in . The idea of approximating the solution of is as follows. For a fixed as a first approximation of we use the process - a unique strong solution of the following SDE

| (4) |

Since for any

the SDE (2) can be equivalently viewed as a finite dimensional SDE driven by the -dimensional Wiener process . Again, by rewriting the equation (2) analogously as in (2) we get by Fact 2 and Lemma 17.1.1 in [5] that for all and every the equation (2) has a unique strong solution . From the uniqueness of solution for any we have , and for .

In the following lemma and proposition we gathered results on moments bound, -regularity of , and main approximation property of . The proofs are postponed to the Appendix.

Lemma 1.

There exist depending only on the parameters of the class such that for every and we have

| (5) |

and for all the following holds:

-

(i)

if then

-

(ii)

if and then

-

(iii)

if and then

Note that the cases (i) and (ii) coincide only when . Moreover, we stress that in Lemma 1 do not depend on the truncation parameter .

Proposition 1.

There exist , such that for any it holds

| (6) |

and for any we have

| (7) |

Hence,

| (8) |

as .

The next step is to approximate via truncated dimension randomized Euler scheme . In the next section we provide definition and analysis of the algorithm . Moreover, in some subclasses of we establish complexity bounds and optimality of the truncated dimension randomized Euler scheme by using Information-Based Complexity (IBC) framework, see [34]. Finally, we show efficient implementation of the method and present result of numerical experiments performed on GPU.

Unless otherwise stated all constants appearing in estimates and in the ”O”, ””, ”” notation will only depend on the parameters of the class . Moreover, the same letter might be used to denote different constants.

3. Truncated dimension randomized Euler algorithm

We define the truncated dimension randomized Euler algorithm that approximates the value of . Let , , . We denote by where for . Let be a sequence of independent random variables, where each is uniformly distributed on , . We also assume that is independent of . For we set

| (9) |

The truncated dimension randomized Euler algorithm is defined by

In order to analyse the truncated dimension randomized Euler scheme we define its time-continuous version denoted by . Set

and

| (10) |

for . Due to the fact that is a finite Lévy measure, there are only finitely many jumps of in every subinterval and

for . Hence, it can be shown by induction that

| (11) |

Note that the trajectories of are càdlàg. As in [24] we consider the extended filtration , where . Since and are independent, the process is still -Wiener process while is -Poisson random measure.

Lemma 2.

Let and . Then the process is -progressively measurable.

The proof easily follows from induction and the well-known fact that adapted càdlàg processes are progressive. We now state the upper error bound on the error of the truncated dimension randomized Euler algorithm.

Theorem 1.

There exists a positive constant , depending only on the parameters of the class , such that for every and it holds

For the proof of Theorem 1 we need the following result.

Proposition 2.

There exists a positive constant , depending only on the parameters of the input data class , such that for every and it holds

In particular, if and then

when , we have

while if , then

Proof.

We deliver the proof in general case with drift, diffusion and jump coefficients being non-zero. Firstly, we can rewrite (2) for all as follows

| (12) |

with

Moreover, we define three auxiliary functions

and by (10) we have for all that

| (13) |

Due to Lemma 2 all stochastic integrals involved in (13) are well-defined. By (12) and (13), we get for that

| (14) |

where

Moreover, we have for all

where

The Lemma 1 together with the Hölder inequality yields

Proceeding analogously as in the proof of inequality (71) in [23] we get by Lemma 1 that

Again by the Hölder inequality for every it holds

Finally, we obtain the following estimate

| (15) |

By the Burkholder inequality we have for every that

Therefore

| (16) |

where

By Fact 2 and Lemma 1 (iii) we get

| (17) |

Moreover,

| (18) |

Finally for we get

| (19) |

Combining (16), (17), (18), and (19) we have for that

| (20) |

Now we estimate the jump part in (14). By the Kunita inequality (see, for example, Theorem 2.11 in [20]) we have

Hence, we have for all that

with

Thanks to Lemma 1 together with the fact that we obtain

| (21) |

Again by Lemma 1, we obtain

| (22) |

The following also holds for

| (23) |

In view of (3), (22), and (23) we can see that

| (24) |

Finally, by (14), (15), (20), and (24) the following holds for

where depend only on the parameters of the class . Moreover, from Lemma 8 and (5), the function is Borel (as a non-decreasing function) and bounded. An application of the Gronwall’s lemma yields then

where depends only on the parameters of the class .

In other cases, when some of the coefficients vanish, we use the same proof technique. Note that the -regularity of a solution might increase due to Lemma 1, which results in different, usually higher, convergence rates. ∎

4. Lower error bounds and complexity

In this section we provide some insight on lower error bounds and complexity bounds of numerically solving (1). We consider the following subclasses of the main class

for , where

Note that , see Remark 3. For the class we additionally impose the following assumption on the Lévy measure

which assures that is non-empty, see Remark 4. Moreover, for all

Both classes , are important from a point of view of possible applications in finance, see, for example, [4], [27].

We consider a class of algorithms that are parametrized by the pair , where is a discretization parameter while is a truncation dimension parameter. In a subclass we assume that any uses only finite dimensional discrete information about the coefficients , the Wiener process and the process . Namely, the vector of information used by is of the following form

where (if ) or (if ), and is the -dimensional Wiener process. We assume that , for , are given and such that

| (25) |

is a -valued random vector on , such that the -fields and are independent. Furthermore, ,

, are given discretization points such that , , , for . The evaluation points for the spatial variables , , of , and can be given in adaptive way with respect to , , and . It means that there exist Borel measurable functions , , such that the successive points are computed in the following way

and for

By the (informational) cost of computing the information we mean the total number of scalar (finite dimensional) evaluations of , and . Hence, for all and for all trajectories of and it is equal to

if and

if . However, by (25) in both cases the cost is .

An algorithm , using , that approximates is given by

| (26) |

for some Borel measurable function

when and

if . The error of for a fixed , where , is defined as

The worst-case error of in is given by

see [34]. For we define the -complexity in as follows

Note that we consider complexity only for the worst-case error measured in -norm (i.e., for ). Moreover, we narrow our attention to algorithms for which , which in turn implies that the cost of any such algorithm is . Such assumption is not too restrictive and is often satisfied by algorithm used in practice, for example, for .

In order to establish upper bound on the complexity we need the following corollary that directly follows from Theorem 1.

Corollary 1.

-

(i)

There exists a positive constant , depending only on the parameters of the class , such that for every and it holds

-

(ii)

Let . There exists a positive constant , depending only on the parameters of the class , such that for every and it holds

For the both classes the (informational) cost of is .

In the following part of the section we deal with suitable lower error bounds in , . For a better clarity the proof is divided into number of auxiliary lemmas stated below.

Lemma 3.

(Lower error bound for the Lebesgue integration) For and for any algorithm it holds that

Proof.

We consider the following class

with

For we have . Since for , , by Theorem 4.2.1 from Chapter 11 in [34] we obtain the thesis. ∎

In the sequel we will make use of the following lemma.

Lemma 4.

Let . There exists , depending only on the parameters of the class , such that for all and any -measurable random vector it holds

| (27) |

where , and

Proof.

Firstly, note that for all we have that .

Let and let us consider any -measurable . If then and the first inequality in (27) is obvious. If then by the projection property of conditional expectation we get for all that

Since is -measurable, is -measurable, and , we get

This ends the proof of the first inequality in (27).

Let us consider the function

| (28) |

where for all and . Note that there exists such that for all we have . Moreover,

which ends the proof. ∎

Lemma 5.

(Lower error bound for the stochastic Itô integration) Let . There exist positive constants , , depending only on the parameters of the class , such that for every , and we have the following lower bound

| (29) |

Proof.

We split the proof into two parts corresponding to different components of the lower bound (29). Firstly, we define the following class

where for . For any we have

Hence, from Proposition 5.1. (i) in [23] and by the fact that we get that for any that

| (30) |

(Note that by the results of [12] the lower bound (30) holds also in case when the evaluation points for are chosen in an adaptive way.)

In order to establish a lower bound (29) dependent on we consider the following class

where for . For every we have

By Lemma 4 we have that there exists such that for all , , and any algorithm the following holds

| (31) |

since by (26) we have that for . Since by (30) and (4) we get

This completes the proof. ∎

Lemma 6.

(Lower error bound in the class for the stochastic integration wrt Poisson random measure) There exist positive constants and , depending only on the parameters of the class , such that for every , and for every algorithm it holds

Proof.

Let us consider the following class

where

and . If we consider the input vector then it holds

Let By using suitably chosen bump functions we can construct two mappings such that , , and for , where . (The construction of such mappings is well-known and widely used in the literature when establishing lower bounds, see, for example, [26]). Then we have that , and by Lemma 6.1 (i) in [10] we get

This ends the proof. ∎

The analogous lower bound can be obtained in class .

Lemma 7.

(Lower error bound in the class for the stochastic integration wrt Poisson random measure) Let . There exist positive constants and , depending only on the parameters of the class , such that for every , and for every algorithm we have

Proof.

Let

where

We have . Furthermore, for every it holds

where the last integration is with respect to –dimensional compound Poisson process and are iid -valued random variables with the common distribution By it holds for all , and that Since we have that . Therefore, there exists such that , although it might happen that

The next part follows analogous proof technique as in the proof of Lemma 6. Let We construct two mappings such that , , whenever , and for with . Consequently, we obtain and

For the notational brevity we denote . By the martingale and isometry properties for stochastic integral driven by the cádlág martingale (see, for example, Theorem 88, page 53 in [33])

which results in the following inequality

and the proof is completed. ∎

Remark 1.

Since , we have to show lower bounds in Lemmas 6, 7 separately for each class and . Furthermore, see also [10] where the authors established lower error bounds for approximate stochastic integration wrt homogeneous Poisson process but in different class of integrands and in the so-called asymptotic setting.

Theorem 2.

-

(i)

There exist positive constants , depending only on the parameters of the class , such that for all and for every method it holds

-

(ii)

Let . There exist positive constants , depending only on the parameters of the class , such that for all and for every method it holds

4.1. Complexity bounds

We are ready to establish the optimality of previously defined Euler algorithm (9) in the class and for .

Theorem 3.

Let .

-

(i)

There exist positive constants , depending only on the parameters of the class , such that for all the following holds

-

(ii)

Let . There exist positive constants , depending only on the parameters of the class , such that for all the following holds

Proof.

Let us define

By Corollary 1 we have that for sufficiently small

for . To bound from above it is sufficient to take the value of with the minimal such that

This gives upper bound for . For the proof of lower bounds consider an arbitrary algorithm , such that . Then the informational cost of computing of is . If then by Theorem 2 we get

and hence

This implies the lower bound for . ∎

Remark 2.

For example, if and , , then, by Theorem 3, the complexity is . Hence, if then the minimal cost is , while in the case of finite dimensional the minimal cost is equal to with embedded in the error constant. This example shows that the complexity significantly increases when we switch from finite to infinite dimensional driving Wiener process.

Remark 3.

It turns out that

Remark 4.

If the measure satisfies then , where

and

5. Numerical experiments and implementation issues in CUDA C

In this section we compare the obtained theoretical results with the outputs of performed simulations. Firstly, we consider the jump-diffusion Ornstein–Uhlenbeck process. Next, we focus on Black–Scholes–Merton equation with stochastic integral driven by compound Poisson process . In our analyses we will use the following fact.

Fact 1.

For given let be as follows

Then for some and .

If , , and then from Theorem 3 we get for the randomized Euler algorithm that the optimal (up to constants) choice of is , and hence we can take . The error of , expressed in terms of the informational cost, is . Hence, the slope of regression lines computed for the vs scale should be close to .

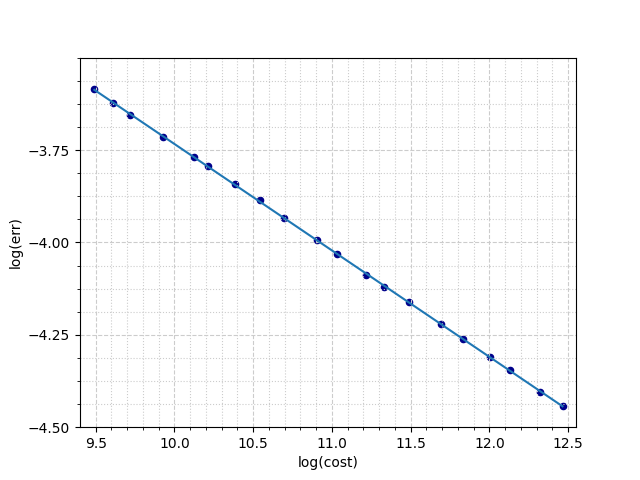

5.1. Ornstein–Uhlenbeck process with jumps

Now we consider the following equation

| (32) |

where and is a bounded sequence of positive real numbers, is a given function, and is a Poisson process with intensity The solution of the equation (32) is of the form of

| (33) |

For the simulation purposes, we set Note that while the analytical formula (33) is known, it involves the stochastic integrals calculation. Therefore, we simultaneously execute schemes and based on common rare grid and fine grid, respectively. We estimate the –error in the following way

| (34) |

with trajectories and By the virtue of Corollary 1 and Fact 1

We take In Figure 1(a) we can see that the obtained slope coefficient almost perfectly matches the predicted one .

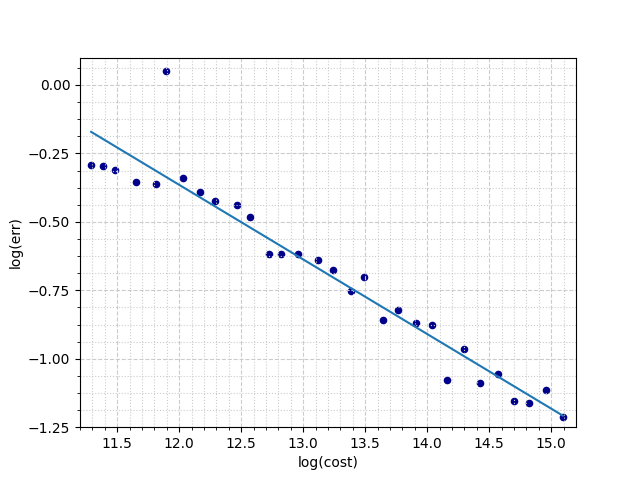

5.2. Merton model

Let us consider the following equation

| (35) |

where is a bounded sequence of positive real numbers, and is a compound Poisson process with intensity and jump heights The solution of the equation (35) can be described by the following formula

For the simulation purposes, we set Let be a sequence of independent random variables that are normally distributed with zero mean and unit variance. We assume that the jump heights sequence of random variables is defined by We estimate the error in the norm in the following way

| (36) |

where is the number of trajectories and is the th sample of We also set where By Corollary 1 and Fact 1

The method in Figure 1(b) exhibits convergence rate equal to

5.3. Details of implementation in CUDA C

In this section we present the crucial parts of the code of algorithm implemented in CUDA C and executed on NVIDIA Titan V GPU (Graphics Processing Unit). The details of CUDA C concept can be found, for instance, in [16]. In addition in [16] the author presented implementation of Milstein scheme (based on equidistant and nonequidistant mesh) and used it for optimal approximation of solutions of SDEs driven by Wiener and Poisson processes. The architecture of GPU enables to significantly decrease computation time by simulating multiple trajectories in parallel for e.g. Monte Carlo approximation; see [17] for performance comparison between CPU (Computer Processing Unit) and GPU. In particular, this refers to the errors estimation as per (34) and (36).

The current implementation solution consists of several separate .cu and .cuh files in order to maintain the code brevity. The input data (including model choice, solution formula if available, input parameters’ values) is sourced from input.cu file. In main function located within kernel.cu the user defines whether exact solution is known or rare/fine grid approach should be leveraged, as well as whether the underlying Wiener process is countably dimensional. Note that the user may also specify the relation between parameters Consequently, investigate_error_w_exact or investigate_error_w_unknown function is executed. Moreover, the jumps sequence (if applicable) for a single trajectory is generated within jumps.cu file.

We provide three listings which illustrate the critical parts of our code together with relevant comments. The comments linked to one particular line are appended at the end of this line while the comments referring to a certain part of the code are appended before the corresponding code fragment.

-

(1)

Dividing given number of trajectories into MAX_TR_BLOCKS number of blocks that run in parallel for the specified number of iterations.

-

(2)

Initializing pseudo-random number generator (PRN).

-

(3)

Starting performance measurement by creating so called time events which will return elapsed time of GPU computation.

-

(4)

Allocating memory for the kernel function output (partial results computed in parallel).

-

(5)

Choosing at most 65535 of the available blocks, which is the number determined by the GPU architecture.

-

(6)

Copying the results from device to host and finishing performance measurement.

-

(7)

Calculating the average error for all trajectories.

-

(8)

Releasing memory allocated for the kernel function output and the results copied from the GPU.

-

(9)

Printing the current set of parameters together with execution time for the user convenience.

-

(10)

Returning the value of Monte Carlo estimator for the scheme error in the -th norm.

-

(1)

Assigning every single trajectory to the separate kernel function block in order to be run in parallel.

-

(2)

Obtaining distinct random numbers per simulation and trajectory by initializing our PRN generator with particular seed (current time) and trajectory index.

-

(3)

Allocating memory for the truncated Wiener process increments generated on rare and fine grid, and for the head of jumps list.

-

(4)

Independently generating sequence of jump times for the current trajectory.

-

(5)

Initialising step size per grid.

-

(6)

Starting the outer loop (indexed with ’i’) in order to iterate through rare grid points. The inner loop (indexed with ’j’) iterates through fine grid points.

-

(7)

Assigning every rare Wiener increment coordinate value equal to zero.

-

(8)

Retrieving subsequent jump time given the previously located jump.

-

(9)

Assigning the value of truncated Wiener increment on the fine grid. For this purpose, we use CUDA C sampling from normal distribution.

-

(10)

Calculating the randomized Euler scheme’s single step in order to find the approximated value of scheme in the current time point.

-

(11)

Calculating and saving the -th power of the absolute difference between approximated solution on rare and dense grid.

-

(12)

Releasing previously allocated memory.

-

(13)

If the number of trajectories is greater than the number of blocks, we assign another trajectory to the currently running kernel function block and start another simulation.

-

(1)

Adding drift-related term.

-

(2)

Adding diffusion-related term.

-

(3)

Adding jump part-related term.

6. Conclusions

We investigated complexity bounds in certain input data classes for the pointwise approximation of the systems of SDEs which contain integrals with respect to countably dimensional Wiener process and random Poisson measure. We presented the implementable truncated dimension randomized Euler scheme , derived its convergence rate together with optimality in the class of input data which are important from the point of view of possible applications. Our theoretical results are supported by numerical experiments performed in CUDA architecture embedded into high level programming language C. The usage of GPU in this case is justified by high dimensionality and complexity of intermediate computations. Finally, we conjecture that the lower error bound in the considered setting also depends on , i.e., should also be present in the exponent of the error bound.

7. Appendix

The proof of following fact is straightforward, so we skip the details.

Fact 2.

-

(i)

If then for all

-

(ii)

If then for all

-

(iii)

Let . Then for all we have that and for all

-

(iv)

Let . Then for any .

-

(v)

If then for all

- (vi)

Proof of Lemma 1. The proof of (5) follows the usual localization argument, see, for example, [33], [7]. The main part of the proof consists of use of the Burkholder and Kunita inequalities and the fact that the constant in the linear growth bound for does not depend on . Since we were not able to find a direct reference in literature that covers the case considered in this paper, for a convenience of the reader we provide a complete argumentation.

Let us fix and define the stopping time , . (Recall that we take ). Since trajectories of are càdlàg, we get

| (37) |

Furthermore, for all . This and Fact 2 imply that for ,

and

Hence, the processes and are -martingales. By using the Burkholder and Kunita inequalities we obtain for all ,

which, in particular, implies that

and

Since the function is bounded and Borel, by the Gronwall’s lemma we get the following (independent of ) bound for all . By applying Fatou’s lemma and (37) we get

| (38) |

By using (38) together with the Hölder, Burkholder and Kunita inequalities we obtain (5). Namely,

We now justify (i)-(iii). By applying the Hölder, Burkholder and Kunita inequalites, Fact 2, and (5), we obtain for all , that

from which (i), (ii), and (iii) follow.

Proof of Proposition 1.

For any , , we have that

where

Firstly, by the Hölder inequality

| (39) |

From (B3), (B4), Lemma 1 and by the Burkholder and Hölder inequalities, we get for that

| (40) |

| (41) |

Finally, from (C3) and by using the Kunita and Hölder inequalities we obtain

| (42) |

Combining (39), (40), (7) and (7) we have for that

By Lemma 1 and Tonelli’s theorem the function is Borel measurable and bounded. Hence, application of the Gronwall’s lemma yields for all

with depending only on the parameters of the class . This implies (6).

Take arbitrary , and any such that for all . Then and by the triangle inequality we have that

| (43) |

In particular, by taking , (defined in (28)) we get , , which together with (7) implies (7). Finally, (8) is a direct consequence of (6), (7), and the Hölder inequality.

Lemma 8.

Let There exists , depending only on the parameters of the class , such that for every and it holds

| (44) |

Proof.

First, we prove by induction that

| (45) |

Let us assume there exists such that (in the case when the thesis is immediate). The set of such indices is non-empty since for we have Therefore, by the Burkholder, Kunita and Hölder inequalities, and Fact 2 the following estimate holds

Hence and, by the rules of induction, the proof of (45) is completed. By (10), (11) and (45), and by using analogous argumentation as above we get for all , that , and hence

| (46) |

Currently constant in the bound (46) depends on . In the second part of the proof we will show, with the help of the Gronwall’s lemma, that we can obtain the bound (44) with that is independent of .

Using the same decomposition as in (13), we obtain that for

| (47) | |||||

By the Kunita and Hölder inequalities, and Fact 2 we get

| (48) |

In analogous way we can obtain for all that

| (49) |

Combining (47), (7), (7) we get for all

| (50) |

where depend only on the parameters of the class . By (46) the mapping is bounded and Borel (as a non-decreasing function). Thus, (50) together with the Gronwall’s lemma imply (44). ∎

References

- [1] D. Applebaum, Lévy Processes and Stochastic Calculus, second ed., Cambridge University Press, Cambridge, 2009.

- [2] E. Buckwar , M.G. Riedler, Runge-Kutta methods for jump-diffusion differential equations, J. Comput. and Appl. Math. 236 (2011), 1155–1182 .

- [3] G. Cao, K. He, On a type of stochastic differential equations driven by countably many Brownian motions, J. Funct. Anal. 203 (2003), 262–285.

- [4] R. Carmona, M. Teranchi, Interest Rate Models: An Infinite Dimensional Stochastic Analysis Perspective, Springer, Berlin, 2006.

- [5] S.N. Cohen, R.J. Elliot, Stochastic calculus and applications, 2nd ed., Probability and its applications, New York, Birkhäuser, 2015.

- [6] R. C. Dalang, L. Quer-Sardanyons, Stochastic integrals for spde’s: A comparison, Expos. Mathem. 29 (2011), 67–109.

- [7] K. Dareiotis, C. Kumar, S. Sabanis, On tamed Euler approximations of SDEs driven by Lévy noise with applications to delay equations, SIAM J. Numer. Anal. 54-3 (2016), 1840–1872.

- [8] S. Deng , W. Fei , W. Liu , X. Mao, The truncated EM method for stochastic differential equations with Poisson jumps, J. Comp. and Appl. Math. 355 (2019), 232–257.

- [9] S. Deng , C. Fei , W. Fei , X. Mao, Generalized Ait-Sahalia-type interest rate model with Poisson jumps and convergence of the numerical approximation, Physica A: Stat. Mech. and its Appl. 533 (2019), 122057.

- [10] J. Dȩbowski, P. Przybyłowicz, Optimal approximation of stochastic integrals with respect to a homogeneous Poisson process, Mediterr. J. Math. 13 (2016), 3713–3727.

- [11] I. Gyöngy, N. V. Krylov, On stochastic equations with respect to semimartingales I., Stochastics 4 (1980), 1–21.

- [12] S. Heinrich, Lower complexity bounds for parametric stochastic Itô integration, J. Math. Anal. Appl., 476 (2019), 177–195.

- [13] D. Higham , P. Kloeden, Numerical methods for nonlinear stochastic differential equations with jumps, Numer. Math. 101 (2005), 101–119 .

- [14] D. Higham , P. Kloeden, Convergence and stability of implicit methods for jump-diffusion systems, Int. J. Numer. Anal. Mod. 3 (2006), 125–140 .

- [15] D. Higham, P.E. Kloeden, Strong convergence rates for backward Euler on a class of nonlinear jump-diffusion problems, J. Comp. and Appl. Math., 205 (2007), 949–956.

- [16] A. Kałuża, Optimal algorithms for solving stochastic initial-value problems with jumps, PhD thesis, AGH University of Science and Technology, Kraków 2020, Click here to access BG AGH repository.

- [17] A. Kałuża, P. M. Morkisz, P. Przybyłowicz, Optimal approximation of stochastic integrals in analytic noise model, Appl. Math. and Comput., 356 (2019), 74–91.

- [18] A. Kałuża, P. Przybyłowicz, Optimal global approximation of jump-diffusion SDEs via path-independent step-size control, Appl. Numer. Math. 128 (2018), 24–42.

- [19] R. Kruse, Y. Wu, A randomized Milstein method for stochastic differential equations with non-differentiable drift coefficients, Discrete Contin. Dyn. Syst. Ser B, 24 (2019), 3475–3502.

- [20] H. Kunita, Stochastic differential equations based on Lévy processes and stochastic flows of diffeomorphisms, In Real and stochastic analysis, pages 305–373, 2004, Springer.

- [21] H. Kunita, Stochastic Flows and Jump–Diffusions, Springer Nature Singapore, 2019.

- [22] Z. Liang, Stochastic Differential Equation driven by countably many Brownian motions with non-Lipschitzian coefficients, Stoch. Anal. Appl. 24 (2006), 501–529.

- [23] P. M. Morkisz, P. Przybyłowicz, Strong approximation of solutions of stochastic differential equations with time-irregular coefficients via randomized Euler algorithm, Appl. Numer. Math. 78 (2014), 80–94.

- [24] P. M. Morkisz, P. Przybyłowicz, Optimal pointwise approximation of SDE’s from inexact information, Journal of Computational and Applied Mathematics 324 (2017), 85–100.

- [25] P. M. Morkisz, P. Przybyłowicz, Randomized derivative-free Milstein algorithm for efficient approximation of solutions of SDEs under noisy information, J. Comput. Appl. Math. 383 (2021), 1–22.

- [26] E. Novak, Deterministic and Stochastic Error Bounds in Numerical Analysis, Lecture Notes in Mathematics, vol. 1349, New York, Springer–Verlag, 1988.

- [27] E. Platen, N. Bruti-Liberati, Numerical Solution of Stochastic Differential Equations with Jumps in Finance. Springer Verlag, Berlin, Heidelberg, 2010.

- [28] P. Protter, Stochastic Integration and Differential Equations, second ed., Springer-Verlag Berlin Heidelberg, 2005.

- [29] P. Przybyłowicz, Optimal sampling design for global approximation of jump diffusion stochastic differential equations, Stochastics: Int. J. Probab. Stoch. Proc. 91 (2019), 235–264.

- [30] P. Przybyłowicz, Efficient approximate solution of jump-diffusion SDEs via path-dependent adaptive step-size control, J. Comp. and Appl. Math. 350 (2019), 396–411.

- [31] P. Przybyłowicz, M. Szölgyenyi, Existence, uniqueness, and approximation of solutions of jump-diffusion SDEs with discontinuous drift, Appl. Math. Comp. 403 (2021), 126191.

- [32] P. Przybyłowicz, Michaela Szölgyenyi, F. Xu, Existence and uniqueness of solutions of SDEs with discontinuous drift and finite activity jumps, Stat. and Probab. Let. 174 (2021), 109072.

- [33] R. Situ, Theory of Stochastic Differential Equations with Jumps and Applications, Springer Science+Business Media, 2005.

- [34] J.F. Traub, G.W. Wasilkowski, H. Woźniakowski, Information-Based Complexity, Academic Press, New York, 1988.