On Modelling of Crude Oil Futures in a Bivariate State-Space Framework

Abstract

We study a bivariate latent factor model for the pricing of commodity futures. The two unobservable state variables representing the short and long term factors are modelled as Ornstein-Uhlenbeck (OU) processes. The Kalman Filter (KF) algorithm has been implemented to estimate the unobservable factors as well as unknown model parameters. The estimates of model parameters were obtained by maximising a Gaussian likelihood function. The algorithm has been applied to WTI Crude Oil NYMEX futures data111Data provided by Datascope - https://hosted.datascope.reuters.com.

1 Introduction

In this paper, the OU two-factor model is used for modelling of short and long equilibrium commodity spot price levels. Our motivation is driven by the development of a robust KF algorithm which will be used for joint estimation of the model parameters and the state variables. In a different setup, the parameter estimation problem for bivariate OU process using KF has been studied in favetto2010parameter and KutoyantsYuryA.2019Opeo .

In ChengBenjamin2018Polc the KF is used to study the effect of stochastic volatility and interest rates on the commodity spot prices using the market prices of long-dated futures and options. In peters2013calibration the Kalman technique has been applied to calibration, jointly with filtering, of partially unobservable processes using particle Markov Chain Monte Carlo approach. The extended KF was developed in ewald2019calibration for estimation of the state variables in the two-factor model from schwartz1997stochastic for the commodity spot price and its convenience yield.

In Sect. 2, we will derive the linear partially observable system specific for commodity futures prices developed in the two-factor model, which represents an extension of schwartz2000short , in the risk-neutral setting. In Sect. 3, the model will be applied to WTI Crude Oil NYMEX futures prices over 2001-2005, 2005-2009 and 2014-2018 time periods.

2 Two-Factor Model with Risk Premium Parameters

We propose the two-factor model of pricing of commodity futures which represents an extension of schwartz2000short , where the spot price is modelled as the sum of two unobservable factors and ,

| (1) |

where is the short-term fluctuation in prices and is the long-term equilibrium price level. We assume that follows an OU equation and its expected value converges to 0 as ,

| (2) |

The changes in the equilibrium level of are expected to persist and is also assumed to be a stationary OU process

| (3) |

where and are correlated standard Brownian motions processes with ; and are the volatilities; and are the speed of mean-reversion parameters of and processes respectively; is a long-run mean for . In schwartz2000short , only one factor had a mean-reverting property. In this work, both and are modelled as the mean-reverting processes. The parameters and in (2) and (3) were introduced as adjustments for market price of risk. The approach stems from the risk-neutral futures pricing theory developed in black1976pricing . Given the initial values and , and are jointly normally distributed. Therefore the logarithm of the spot price, which is the sum of and , is normally distributed. Hence, the spot price is log-normally distributed and

| (4) |

where and represent the expectation and variance taken with respect to the risk-neutral distribution, and

| (5) |

Let be the current market price of the futures contract with maturity . For eliminating arbitrage, the futures prices must be equal to the expected spot prices at the asset delivery time . Hence, under the risk-neutral measure, we have

After discretization, we will obtain the following AR(1) dynamics for bivariate state variable

| (6) |

where

and is a column vector of uncorrelated normally distributed random variables with and

is the time step between and . The relationship between the state variables and the observed futures prices is given by

| (7) |

where

is -dimensional vector of uncorrelated normally distributed random variables, , and are the futures maturity times. In Sect. 3, we assume that is a diagonal matrix with non-zero diagonal entries , i.e. the variance of the error term for the first contract is and for all other remaining contracts. Let be - algebra generated by the futures contract up to time . The prediction errors are supposed to be multivariate normally distributed, then the log-likelihood function of can be written as

| (8) |

where the set of unknown parameters , is the number of time instances, . Given , the maximum likelihood estimate (MLE) of is obtained by maximising the log-likelihood function from (8). Both quantities and are computed within the KF.

3 Crude Oil Futures

The unknown parameters were estimated 222The Appendix containing the initial values and parameter estimates along with their standard errors can be found at https://github.com/peilun-he/MAF-Conference-September-2020 by maximising the log-likelihood function (8). Then, the state variables were estimated using the KF and Kalman Smoother (KS), harvey1990forecasting and de1989smoothing . Given all observations until time and the current time , , KF only uses the observations up to , while KS uses all the available observations up to . In this section, “in-sample” and “out-of-sample” performances of KF and KS are analysed using the RMSE criterion.

We used the historical data of WTI Crude Oil NYMEX futures prices over different time intervals from 1996 to 2019. The data comprised the prices of 20 monthly futures contracts with duration up to 20 months.

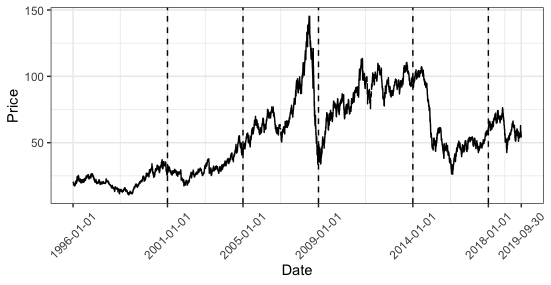

Figure 1 shows the WTI Crude Oil futures prices from 1996 to 2019. It is obvious that the prices dropped dramatically during the Global Financial Crisis (GFC) in 2008. For studying the “in-sample” and “out-of-sample” forecasting performances, the three separate time periods were selected, 01/01/2001 - 01/01/2005, 01/01/2005 - 01/01/2009, and 01/01/2014 - 01/01/2018.

| Period | 2001-2005 | 2005-2009 | 2014-2018 | |||||

|---|---|---|---|---|---|---|---|---|

| \svhline Estimation | Filter | Smoother | Filter | Smoother | Filter | Smoother | ||

| \svhline In-Sample | C4 | 0.003264 | 0.003268 | 0.002219 | 0.002244 | 0.002180 | 0.002181 | |

| C9 | 0.002289 | 0.002304 | 0.001612 | 0.001616 | 0.001646 | 0.001668 | ||

| C13 | 0.004155 | 0.004163 | 0.003959 | 0.003986 | 0.003516 | 0.003494 | ||

| \svhline Out-of-Sample | C14 | 0.005959 | 0.005955 | 0.005569 | 0.005591 | 0.005215 | 0.005181 | |

| C20 | 0.018585 | 0.018579 | 0.018002 | 0.018006 | 0.020331 | 0.020265 | ||

Table 3 provides the RMSE over the selected time periods. “In-sample” forecasting performance has been evaluated on the first 13 contracts (C1-C13), while “out-of-sample” performance has been evaluated on the 14th to the 20th contracts (C14-C20). Overall, the “in-sample” forecasting errors were less than “out-of-sample” errors as seen in Table 1. The “out-of-sample” forecasting errors were consistently increasing with respect of maturity times from C14 to C20 contracts. The RMSE are consistent across the three time intervals, even over 2005 - 2009, where the futures prices plummeted during the GFC. In summary, for each specified time period, the RMSE calculated through KF is smaller for short maturity contracts, which provides evidence that the KF performed better in predicting prices for short maturity contracts, whilst KS outperformed KF in the pricing of longer maturity futures.

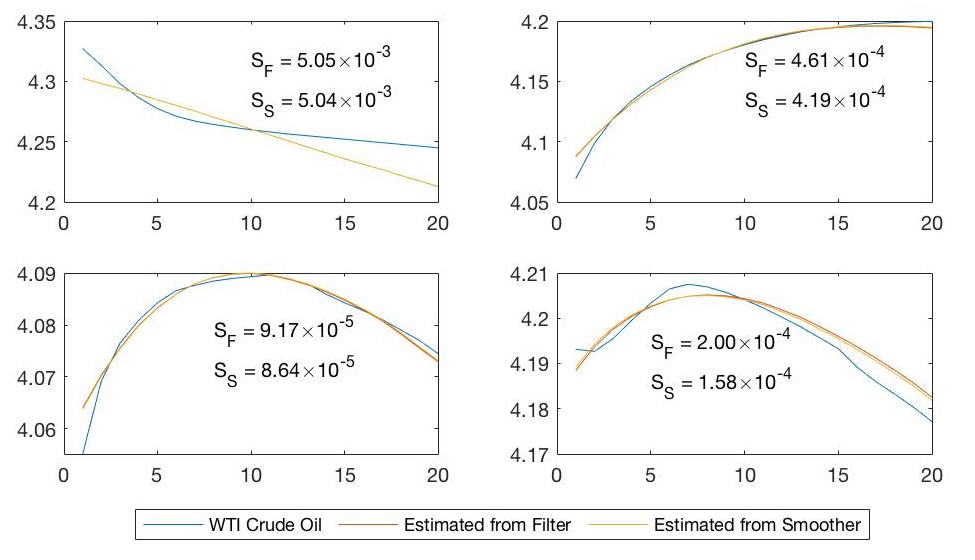

Figure 2 gives the cross-sectional data plots of the logarithms of futures prices and their forecasts obtained by KF and KS on four different days. The plots exhibit the distinct patterns of futures curves, 05/09/2007, 10/10/2006, 14/11/2005 and 20/09/2005. The horizontal axis represents the number of contracts from 1 to 20 and the logarithm of futures prices are presented on the vertical axis. The RMSE for the curve with backwardation pattern (top left) appears larger than RMSE of that with contango pattern (top right)333Backwardation represents the situation where the futures prices with shorter maturities are higher than the futures prices with longer maturities, while contango refers to the reverse situation. .

4 Conclusion

In this paper, we have developed the two-factor model which can be used for pricing of oil futures and forecasting their term structure which remains a most significant challenge, Cort2019 . The KF algorithm has been robustified by the grid-search add-on which has been implemented to estimate the hidden factors jointly with unknown model parameters. The model has been applied to WTI Crude Oil futures market prices from 1996 to 2019. The model “in-sample” and “out-of-sample” forecasting performances were evaluated using the RMSE criterion. Moreover, we observed that KF gives a better estimate of state vector for shorter maturity contracts, while KS performs better for contracts with longer maturities.

References

- (1) Black, F.: The pricing of commodity contracts. Journal of Financial Economics 3, 167–179 (1976)

- (2) Cheng, B., Nikitopoulos, C.S., Schlögl, E.: Pricing of long-dated commodity derivatives: Do stochastic interest rates matter? Journal of Banking and Finance 95, 148–166 (2018)

- (3) Cortazar, G., Millard, C., Ortega, H., Schwartz, E.S.: Commodity Price Forecasts, Futures Prices, and Pricing Models. Management Science 65, 4141–4155 (2019)

- (4) De Jong, P.: Smoothing and interpolation with the state-space model. Journal of the American Statistical Association 84, 1085–1088 (1989)

- (5) Ewald, C.O., Zhang, A., Zong, Z.: On the calibration of the Schwartz two-factor model to WTI crude oil options and the extended Kalman Filter. Annals of Operations Research 282, 119–130 (2019)

- (6) Favetto, B., Samson, A.: Parameter estimation for a bidimensional partially observed Ornstein-Uhlenbeck process with biological application. Scandinavian Journal of Statistics 37, 200–220 (2000)

- (7) Harvey, A.C.: Forecasting, structural time series models and the Kalman filter. Cambridge (1990)

- (8) Kutoyants, Y.A.: On parameter estimation of the hidden Ornstein-Uhlenbeck process. Journal of Multivariate Analysis 169, 248–263 (2019)

- (9) Peters, G.W., Briers, M., Shevchenko, P., Doucet, A.: Calibration and filtering for multi factor commodity models with seasonality: incorporating panel data from futures contracts. Methodology and Computing in Applied Probability 15, 841–874 (2013)

- (10) Schwartz, E.S.: The stochastic behavior of commodity prices: Implications for valuation and hedging. The Journal of Finance 52, 923–973 (1997)

- (11) Schwartz, E.S., Smith, J.E.: Short-term variations and long-term dynamics in commodity prices. Management Science 46, 893–911 (2000)