Adaptively Optimize Content Recommendation Using Multi Armed Bandit Algorithms in E-commerce

Abstract.

E-commerce sites strive to provide users the most timely relevant information in order to reduce shopping frictions and increase customer satisfaction. Multi armed bandit models (MAB) as a type of adaptive optimization algorithms provide possible approaches for such purposes. In this paper, we analyze using three classic MAB algorithms, -greedy, Thompson sampling (TS), and upper confidence bound 1 (UCB1) for dynamic content recommendations, and walk through the process of developing these algorithms internally to solve a real world e-commerce use case. First, we analyze the three MAB algorithms using simulated purchasing datasets with non-stationary reward distributions to simulate the possible time-varying customer preferences, where the traffic allocation dynamics and the accumulative rewards of different algorithms are compared. We find all three algorithms can adaptively optimize the recommendations, and under this simulated scenario UCB1 surprisingly slightly outperforms the most popular TS algorithm. Second, we compare the accumulative rewards of the three MAB algorithms with more than 1,000 trials using actual historical A/B test datasets. We find that the larger difference between the success rates of competing recommendations the more accumulative rewards the MAB algorithms can achieve. In addition, we find that TS shows the highest average accumulative rewards under different testing scenarios. Third, we develop a batch-updated MAB algorithm to overcome the delayed reward issue in e-commerce and enable an online content optimization on our App homepage. For a state-of-the-art comparison, a real A/B test among our batch-updated MAB algorithm, a third-party MAB solution, and the default business logic are conducted. The result shows that our batch-updated MAB algorithm outperforms the counterparts and achieves 6.13% relative click-through rate (CTR) increase and 16.1% relative conversion rate (CVR) increase compared to the default experience, and 2.9% relative CTR increase and 1.4% relative CVR increase compared to the external MAB service.

1. Introduction

E-commerce offers customer convenience and large assortment options compared to physical stores. But it also creates unique challenges, e.g. how to surface the most relevant information to a customer among massive contents on a limited 2D screen? The most used approach today in e-commerce is to perform an A/B test and pick the winner among a few hypothesized design choices. However, in many cases, a sensible goal might not be to choose a fixed winner among competing experiences. For example, if the underlying composition of user population or intent changes dramatically with time, there might not exist a definite winner design for all situations. In addition, under some circumstances, the opportunity cost of assigning some users to an inferior experience might be very high and often not reported. The constant traffic allocation framework required by an A/B test seems too rigid. To deal with these problems, recently more and more internet companies start using a continuous optimization framework, multi armed bandit (MAB), to maximize the relevancy of their content recommendation dynamically.

MAB is a type of algorithm that belongs to the reinforcement learning category, or a simple version of reinforcement learning without state transition. It was first posed by researcher Thompson (Thompson, 1933) as a concept of clinical trial design, and later on studied by Robbins (Robbins, 1952) and Bellman (Bellman, 1956) in a more general format referred to as sequential design of experiments. The name MAB first appeared in the publications during 1950s such as Neyman (Neyman, 1951) and Bush et al (Bush and Mosteller, 1953). It describes a gambling situation, where in a gambling room there are multiple slot machines, and each machine has its own success distribution. The gambler has to decide by trying and observing which arm of the slot machine to pull, in order to maximize the total money received.

MAB algorithms are extensively studied (Berry and Fristedt, 1985; Slivkins, 2019; Lai and Robbins, 1985; Agrawal, 1995; Auer et al., 2002) in a wide range of applications (Huo and Fu, 2017; Villar et al., 2015; Schwartz et al., 2017; Yu et al., 2015; Sutton et al., 1998). In this paper, we mainly focus on three classical multi armed bandit algorithms, -greedy (Sutton et al., 1998), Thompson sampling (Russo et al., 2017), and upper confidence bound 1 (UCB1) (Auer et al., 2002). More details of these algorithms are given later as we introduce the problem formulations. We analyze these MAB algorithms for content recommendation in the e-commerce settings, where we may face some different issues than what the original MAB algorithms are designed for or the assumptions they use.

For example, in a typical MAB algorithm, it is assumed that the success distribution of each slot machine, or an arm, is fixed. In the e-commerce setting using MAB for content recommendations implies the slot machine’s response is an analogy for customers’ feedback. However, oftentimes customers’ feedback is non-stationary as their preferences may change over time. In addition, after pulling an arm of a slot machine, the response is usually available instantaneously. However, this may not be the case in e-commerce, where the customers may take minutes, hours, or even longer to provide feedback, such as a purchase.

In recent years, some studies provide theoretical analysis of MAB performance in terms of regrets under mathematically tractable non-stationary reward distributions (Besbes et al., 2014; Slivkins and Upfal, 2008; Garivier and Moulines, 2008; Cao et al., 2019) and some others proposed different algorithms that can handle the delayed issue either theoretically (Joulani et al., 2013; Guha et al., 2010) or practically (Grover et al., 2018; Liu et al., 2019). In this paper, we do not focus on the theoretical analysis part. Instead, we analyze the performance and properties of using the MAB algorithms first on simulated non-stationary distributed user purchasing datasets, and then we evaluate the MAB algorithms offline using datasets logged in real-world A/B tests of a large e-commerce site. Lastly, we propose a batch-update MAB framework to tackle some of the practical data delay issues, and provide a real online A/B test performance of adaptively optimizing the sequence of content cards on the homepage of a major e-commerce App.

The rest of the paper is organized as follows. Section 2 introduces the three MAB algorithms to be studied in this paper. Section 3 analyzes the performance of the three MAB algorithms in the simulated non-stationary scenarios. Section 4 provides the offline evaluation of the three algorithms using actual historical A/B testing datasets. Section 5 illustrates our batch-updated MAB framework with a real three-way online A/B test. Section 6 concludes the paper and provides certain future directions.

2. Multi Armed Bandit Algorithms

Consider we have competing experiences (i.e., arms), denoted by set , and a decision strategy such that for every customer’s visit at time , the strategy can decide which one of the experiences, , to show. After showing the experience , we will see a feedback or reward, denoted by , from the customer who received the experience. The feedback could either be binary () such as the experience being click or not, and a purchase being made or not, or continuous () such as the total price of the order etc.

An MAB problem is described that assuming at each visit time , for any experience being shown, i.e., , the corresponding rewards are drawn independently from an unknown distribution , then how we can decide the experience to show at each time in order to maximize the total rewards . A main challenge in this problem is that for the experiences that are not shown before, their reward distribution is unknown. Hence a common exploration-exploitation dilemma arises, i.e., we want to explore the unknown distributions hoping to find a better experience with higher rewards, but this is on the cost of giving up exploiting the current best experience we have learned so far.

To deal with this problem, many strategies or the MAB algorithms, are proposed and analyzed. In this paper, we mainly focus on the three MAB algorithms, i.e., -greedy, Thompson sampling, and upper confidence bound 1 (UCB1).

1) -greedy: the -greedy algorithm (Sutton et al., 1998) is a strategy which assigns at each visit time a small probability for exploration (i.e., randomly selecting an experience to show) and with the probability to exploit the current winner experience (i.e., showing the experience that currently generates the highest average reward based on what it has learned so far).

2) Thompson Sampling (TS): different from the -greedy using a fixed exploration rate, Thompson sampling (Russo et al., 2017) keeps adjusting exploration rate based on its current estimation on the reward distributions . The approach usually starts from assigning an initialized beta distribution to each experience , which is used to gradually approximate the true average reward distribution of the experience. At every visit time, the model generates a sample from the currently learned beta distributions of all experiences, and the experience with the largest sample is shown to the customer. Then based on the customer’s feedback, the model updates the beta distribution related to that shown experience. For binary rewards , this update can be very efficient, i.e., , . (the beta distributions of unselected experiences remain the same.)

3) Upper Confidence Bound 1 (UCB1): This algorithm balances the exploration and exploitation by using upper confidence bounds of the current average rewards for each experience (Auer et al., 2002). At each visit time the experience with the highest upper confidence bound is shown to the customer. An upper confidence bound of an experience at time consists of two parts, the current average reward of the experience , and an upper confidence range (with high probability) , where is the number of times experience is shown by time .

The theoretical analysis of these three algorithms in terms of their expected total rewards, or usually equivalently measured by the expected regrets, and their asymptotic relationship with time steps, can be found in (Slivkins, 2019). In this paper we mainly focus on the application and performance analysis of these algorithms.

3. Performance of MAB in simulated non-stationary scenarios

3.1. Simulated Datasets and Methodology

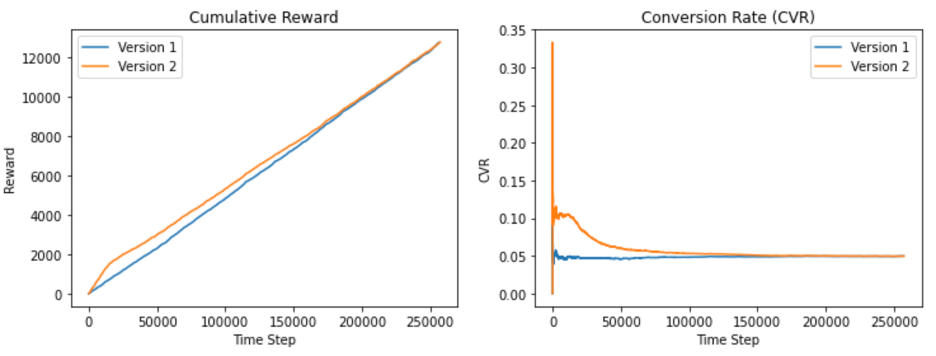

In order to illustrate how the different MAB algorithms work under a non-stationary scenario while protecting data privacy, we created a simulated dataset to represent a common and challenging practical situation where one or more distributions are non-stationary. Specifically, we added some disturbance. One experience (v2) has a higher local conversion rate (CVR) than the other (v1) at the beginning of the test, but a lower local CVR (than v1) later on, so that the two experiences finally converge to the same CVR (average conversion over the whole time range). The cumulative reward (purchases) and CVR of the simulated dataset are presented in Figure 1.

Since the simulated datasets are generated with a uniformly random logging policy, i.e., at each time step a version is chosen uniformly, we can use the unbiased offline evaluation method proposed by Li et. al (Li et al., 2011), to test the performance of the three MAB algorithms and the A/B test sampling strategy with the simulated dataset.

3.2. Traffic Allocation Patterns

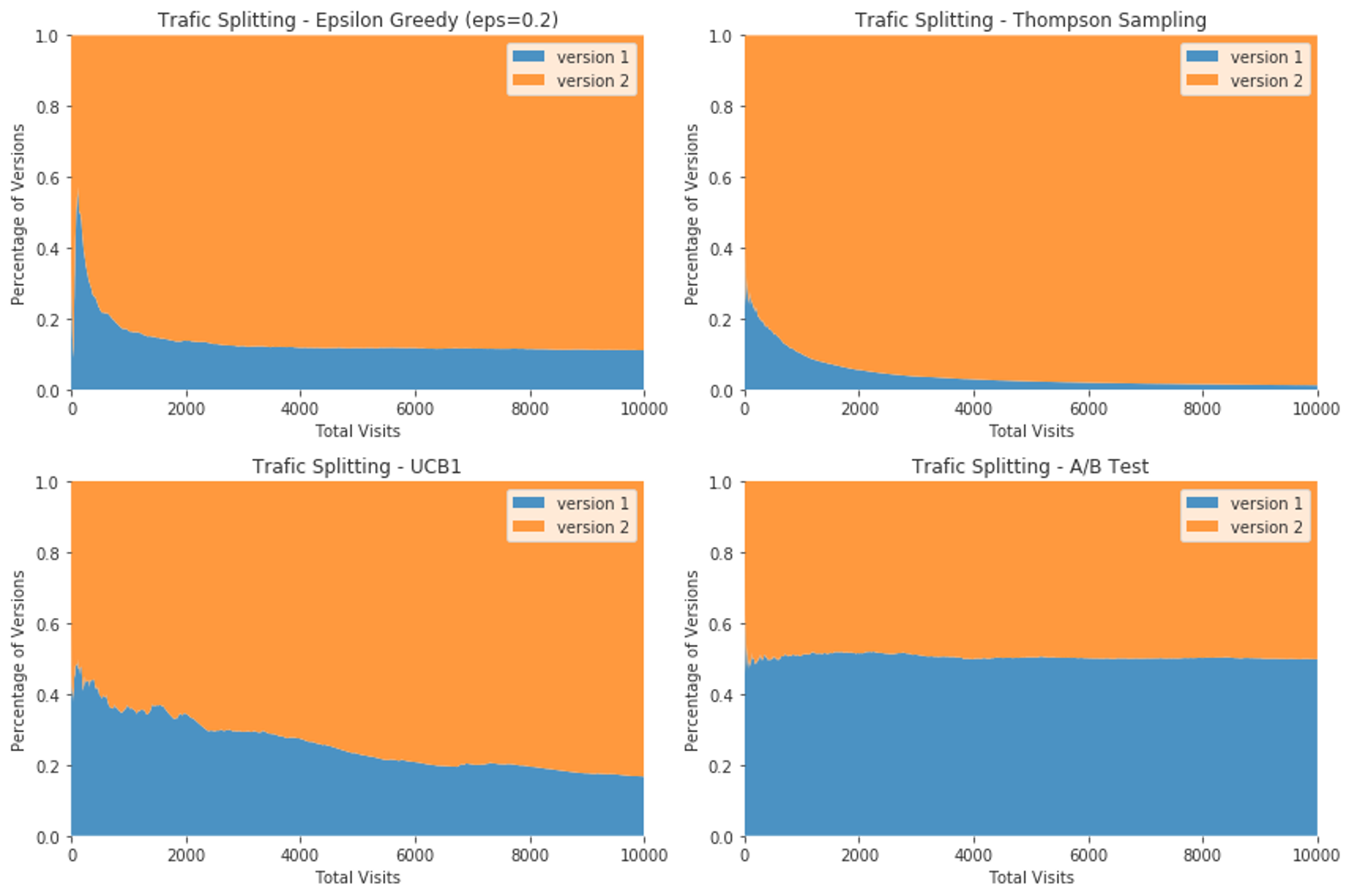

We first analyzed the traffic allocation dynamics for these 4 different strategies, which are shown in Fig. 2. In the figure, we see that compared to the A/B test strategy all the three MAB algorithms can adjust the traffic allocation earlier, i.e., gradually increasing the traffic amount for the winner experience (v2) and lowering the traffic amount for the under-performed experience (v1).

and typical A/B testing

For the tested three MAB algorithms, -greedy algorithm () shows the highest traffic changing speed at the beginning. However, after detecting a relatively stable winner, its traffic allocation for the winner is maintained around the level. Thompson sampling not only shows a high adjustment speed at the beginning, but also continuously shows an aggressive allocation of traffic towards the winning experience. It is the only one that keeps the currently detected winner (version 1) at a very dominate level (around of the total traffic) while keeps the losing version traffic only around . The traffic allocation dynamics for UCB1 seems more ”moderate”, i.e., the changing speed is relatively lower than the other two MAB algorithms.

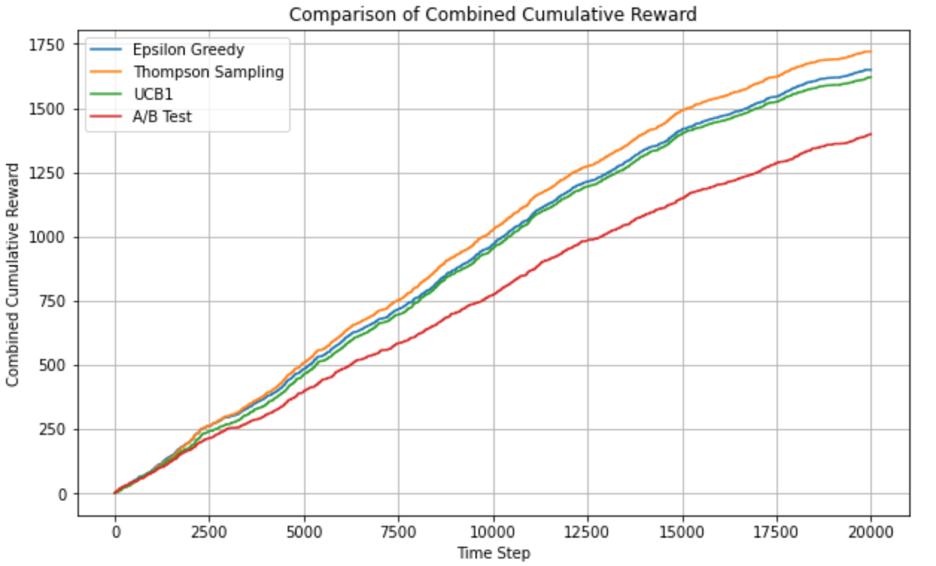

3.3. Reward and Empirical Regret Comparison

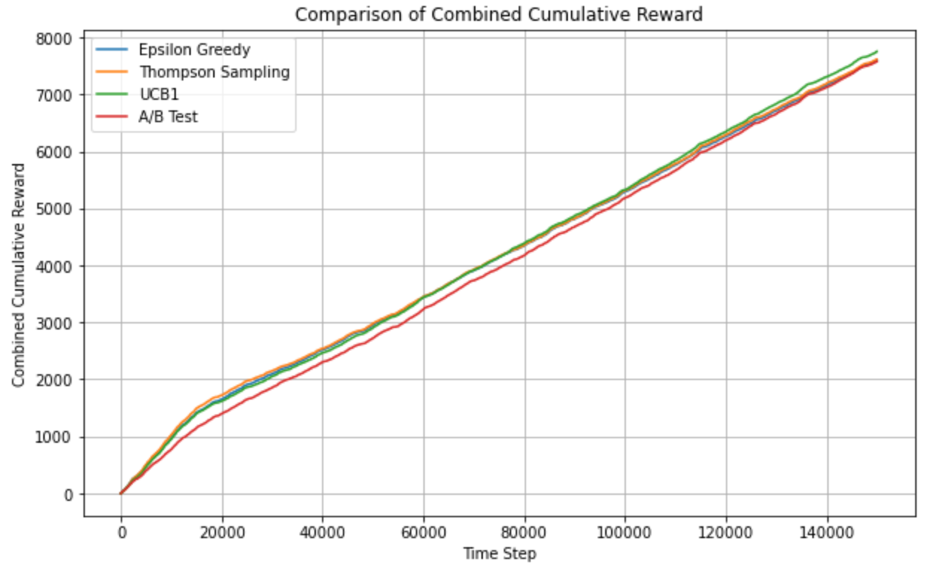

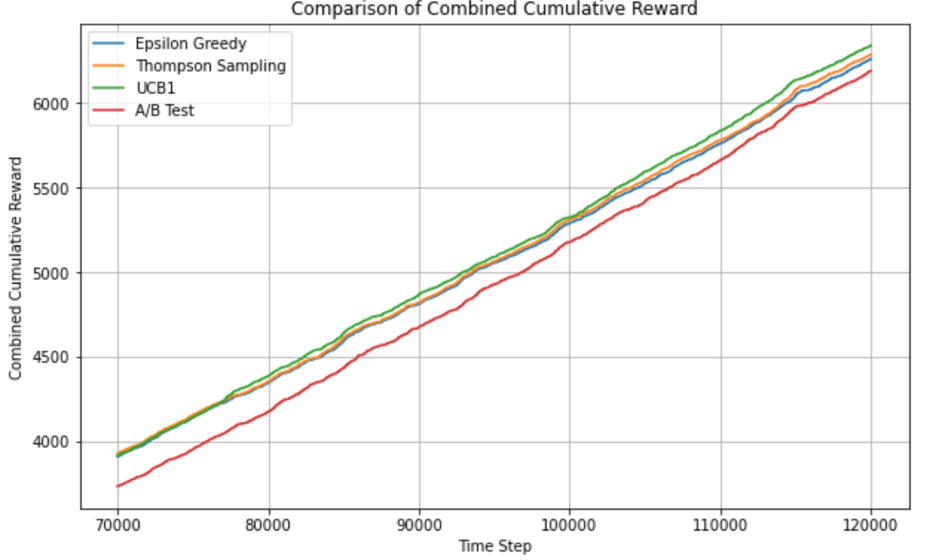

The total rewards for different algorithms over the dynamic recommendations are shown in Fig. 4, where we see Thompson sampling achieves a higher total rewards than the others in the early half, as shown in the zoom-in plot Fig. 6, while interestingly UCB1 achieves the highest total rewards in the later half thus outperforms TS as displayed in the zoom-in plot Fig 6. This result is interesting as Thompson sampling recently has gain wide popularity because of its strong performance as demonstrated both empirically and analytically, which seems to suggest that TS would always be the top choice. However, this simulation generates an opposite result. We would like to highlight that the result here does not mean in general or more practical cases TS is definitely worse than UCB1 (in fact we provide a more comprehensive comparison in the later section under industrial datasets that TS does show a better performance). This simulation result can be regarded as an ”adversarial” case, where the fast-and-aggressive traffic adjustment pattern of TS, happens to be a weaknesses here, since TS does not detect the higher local CVR of version 1 in the later half and still assigns the dominate traffic to version 2 according to the whole time CVR. This implies that no MAB algorithm can always be the ”perfect” algorithm; thus the choice should depend on the real use cases.

early-half zoom-in

later-half zoom-in

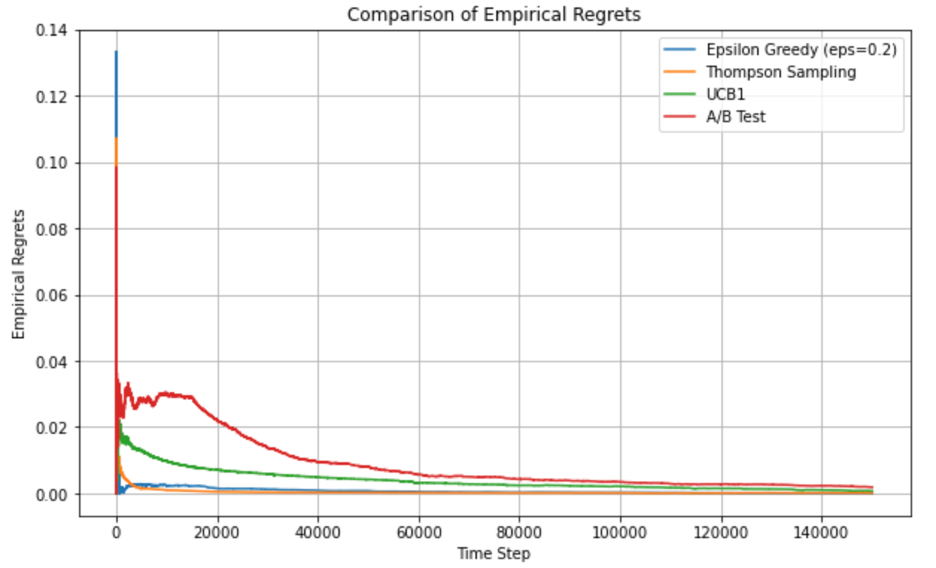

We also compare the empirical average regrets of the three different algorithms, as shown in figure 4, since ”regrets” are also commonly used metrics for evaluating MAB algorithms. However, different from the theoretical average regrets at a given time , i.e.,

where is the true success rate of the winner experience, here we use empirical regrets, defined by,

where is the empirical success rate of the winner experience based on what the model has learned up to time , to simulate the real situations where we have no prior knowledge of the reward distribution. (thus the regret can only be estimated based on the experience). From the figure 4, we can see that UCB1 has a relatively higher empirical regret per trial, which seems ”opposite” to its good performance in terms of the total rewards obtained. This is because the empirical regrets are purely determined by the best distribution at the current step the agent has learned so far and each agent learns in a different way.

To illustrate how higher rewards do not always correlate with lower empirical regrets, we show a toy example in Table 1. In this example, two different arms are tested against each other using two different algorithms. In this case, we assume conversion rate for Arm 2 starts off lower then increases at a later stage during the test. Algorithm 1 more aggressively shifts traffic to Arm 1 at the beginning of the test while Algorithm 2 adapts to this change and gives a more balanced traffic allocation. In this example, both algorithms achieve the same regret but Algorithm 1 has higher rewards.

| Algorithm 1 | Algorithm 2 | ||

|---|---|---|---|

| Trials | 800 | 500 | |

| Arm 1 | Wins | 400 | 240 |

| CTR | 0.5 | 0.48 | |

| Trials | 200 | 500 | |

| Arm 2 | Wins | 20 | 160 |

| CTR | 0.1 | 0.32 | |

| Empirical Regret | 80 | 80 | |

| Reward | 420 | 400 | |

4. Offline Evaluation of MAB algorithms on Industrial Datasets

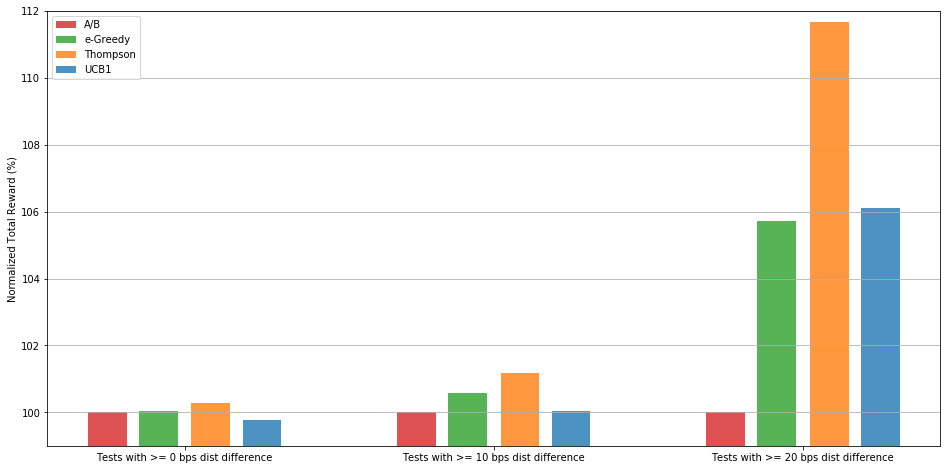

In order to estimate the performance of using each MAB algorithm in industrial settings, we evaluate their performance on the historical A/B testing datasets of a major e-commerce website based on the unbiased offline evaluation method (Li et al., 2011) with around 1000 offline trials, where all test durations are longer than 2 weeks and the visits are in the order of 10 thousands or millions. The performance is shown in figure 7.

In the above figure, there are three types of testing scenarios, where the first one on the left area is for the performance of the tests where the true success rate difference (computed based on the whole datasets) between the control and treatment groups are larger than or equal to 0 basis point (BPS) , while the tests in the middle are for the true success rate difference larger than or equal to 10 BPS, and the last tests on the right are for the success rate difference 20 BPS. The y axis describes the relative total reward. To protect confidential information, we normalize the average reward for A/B testing to as a general benchmark. It can be seen that as the true success rate difference (or ”gap”) increases, the performance of the MAB algorithms also improves. Also we noticed that Thompson sampling shows the highest average reward improvements in all three scenarios. Thus it has the strongest performance based on the offline evaluation. Epsilon greedy algorithm also performs better than A/B test in the three scenarios (thus also robust), even though it does not show the best performance as Thompson sampling does. UCB1 on the other hand, performs the worst in the first scenario, but as the ”gap” increases it outperforms A/B tests or even epsilon greedy under the largest difference scenario.

5. Online Optimization Using a Batch-Update MAB Framework

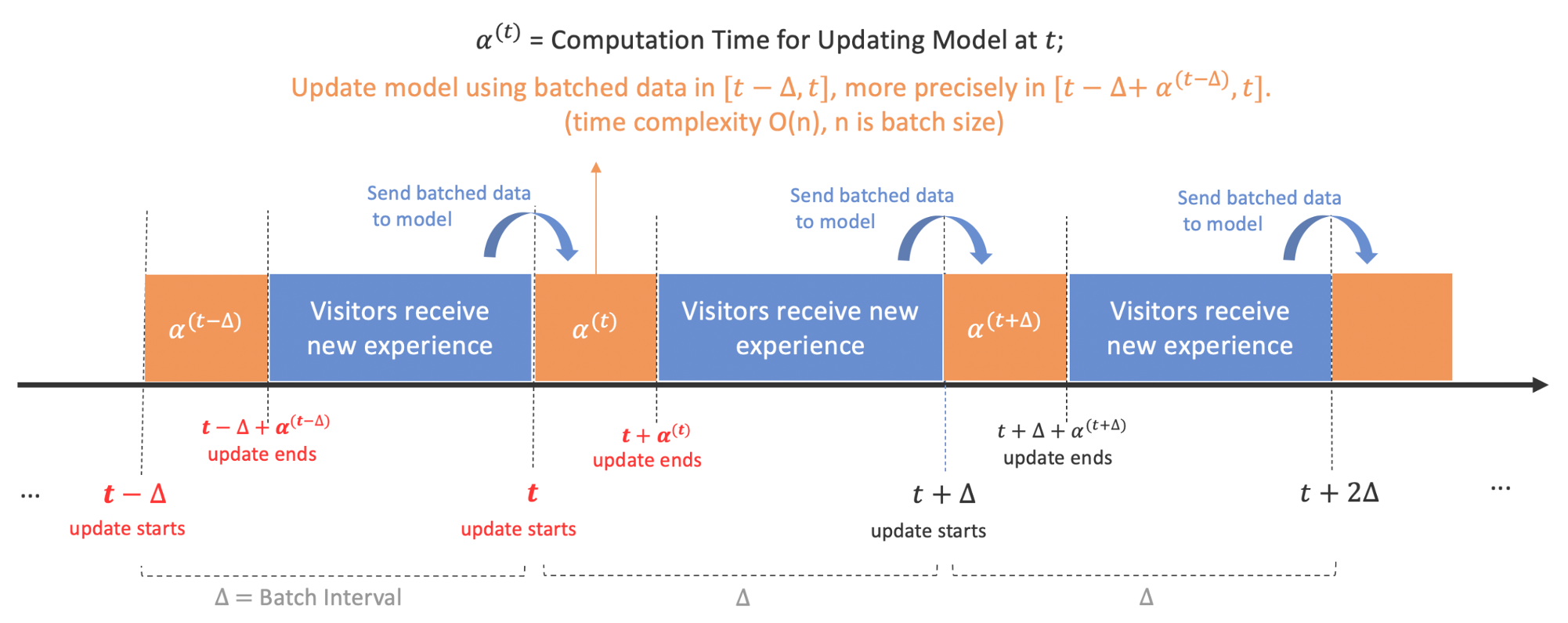

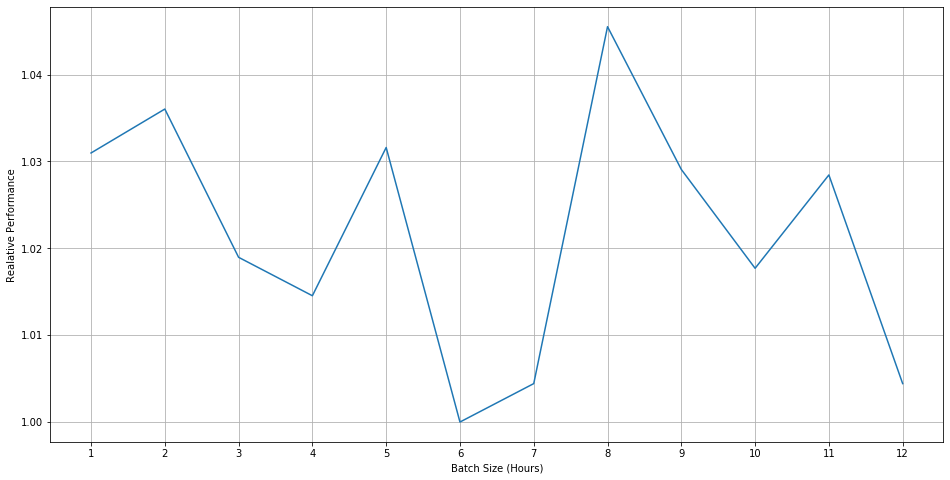

As mentioned before in some e-commerce use cases with possible time-varying customer preferences and considerable opportunity cost, a continuous optimization of the content recommendation is probably a better choice than deciding a fixed winner. Hence MAB algorithms provide possible solutions in these use cases. However, one of the big challenges to implement MAB algorithm for content recommendation in a large e-commerce platform like in The Home Depot is to deal with the data latency issue. The data latency issue is two-folds: 1) data refresh delay due to existed data platform configuration. 2) reward data delay due to customers’ late feedback for the experience they receive. To solve the issue, we design a batch-update MAB framework, which is shown in figure 8. The lower bound of the batch update should be the data fresh latency. With the lower bound, a practical and good choice of batch size can be decided by offline evaluations on the historical datasets that are related to the business cases under consideration. As an example, figure 9 shows the performance of using different batch-size with -greedy algorithms (), where in this case 8-hour batch size shows the best performance.

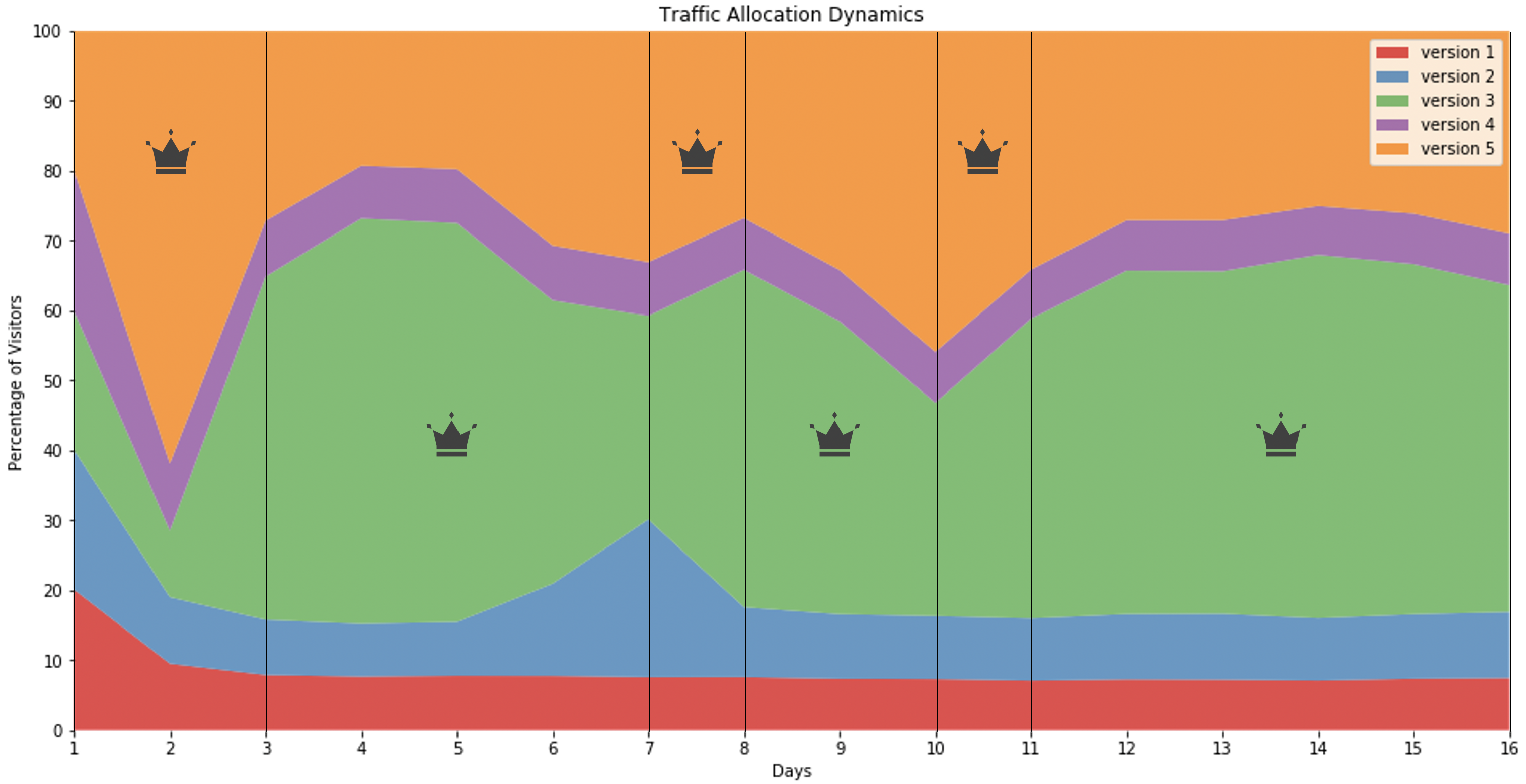

To test the performance of the batch-update MAB framework, we apply it on the homepage of our App to optimize the order of content cards (widgets) and maximize its click through rate or conversation rate. On our homepage, there are five different orders of content cards (i.e., five different experiences). Our goal is to continuously find the best experience to fit the needs of the user population at the moment. For a state-of-the-art comparison, a real A/B test of our batch-updated MAB algorithm, a third-party MAB solution, and the default business logic were conducted. With millions of visits from real online shoppers who engaged with the App homepage, we saw 6.13% relative increase in the click-through-rate (CTR) and 16.1% relative increase in the conversion rate (CVR) compared to the default experience, and 2.9% relative CTR increase and 1.4% relative CVR increase compared to the external MAB service. Moreover, we do observe that our user base behaves differently on different days of the test, and MAB allocates different proportions of visits to different design choice according to their performance at the time. The traffic dynamics (in percentage) and the detected winner experience are shown in figure 10.

The details of the test design and metrics values are confidential thus are not disclosed here.

6. Conclusion

In this paper, we analyze using the three classic MAB algorithms, -greedy, Thompson sampling (TS), and upper confidence bound 1 (UCB1) for dynamic content recommendation. Under simulated purchasing datasets with non-stationary reward distributions, we find

-

•

All the three MAB algorithms can adaptively adjust traffic and achieve a higher total rewards compared to random sampling in A/B testing.

-

•

TS shows the most aggressive traffic allocations among all three algorithms, while UCB1 shows the most moderate traffic allocations.

-

•

TS can be outperformed by UCB1 in the non-stationary reward distribution case (e.g the ”adversarial” case here).

Second, in the offline evaluation based on industrial datasets, we find that

-

•

The larger difference between the competing experiences in terms of the success rate, the more total rewards the MAB algorithms can achieve.

-

•

TS shows the strongest performance in terms of the total rewards obtained under different offline testing scenarios.

Last, a batch-updated MAB algorithm is proposed to overcome the practical data latency issues and enable the real world content optimization on the homepage of a major e-commerce App. The real A/B test shows our batch-updated MAB algorithm outperformed the counterparts and achieved 6.13% increase in click-through rate and 16.1% increase in conversion rate.

Future directions include designing new MAB algorithms that can achieve higher rewards by considering personalization potentials under the possible time-varying customer preferences and feedback delays, and designing new adaptive optimization algorithms that are compatible with more general business success metrics other than click through rate and conversion rate etc. to increase the flexibility of a content recommendation framework.

7. Acknowledgement

We thank Kevin Abdo’s continuous support allowing us to apply and test our MAB framework in the App homepage use case. We thank Sarfaraz Hussein for providing the testing variants. We thank Priyanka Kommidi and Achal Dalal for the effort and support in the A/B test. We thank Weiyu Li, Varun Vohra, Shradha Mani, Evan Bailey and people who contributed in the data platform development and deployment process.

References

- (1)

- Agrawal (1995) Rajeev Agrawal. 1995. Sample mean based index policies with O (log n) regret for the multi-armed bandit problem. Advances in Applied Probability (1995), 1054–1078.

- Auer et al. (2002) Peter Auer, Nicolo Cesa-Bianchi, and Paul Fischer. 2002. Finite-time analysis of the multiarmed bandit problem. Machine learning 47, 2 (2002), 235–256.

- Bellman (1956) Richard Bellman. 1956. A Problem in the Sequential Design of Experiments. Sankhyā: The Indian Journal of Statistics (1933-1960) 16, 3/4 (1956), 221–229. http://www.jstor.org/stable/25048278

- Berry and Fristedt (1985) Donald A Berry and Bert Fristedt. 1985. Bandit problems: sequential allocation of experiments (Monographs on statistics and applied probability). London: Chapman and Hall 5, 71-87 (1985), 7–7.

- Besbes et al. (2014) Omar Besbes, Yonatan Gur, and Assaf Zeevi. 2014. Stochastic multi-armed-bandit problem with non-stationary rewards. Advances in neural information processing systems 27 (2014), 199–207.

- Bush and Mosteller (1953) Robert R Bush and Frederick Mosteller. 1953. A stochastic model with applications to learning. The Annals of Mathematical Statistics (1953), 559–585.

- Cao et al. (2019) Yang Cao, Zheng Wen, Branislav Kveton, and Yao Xie. 2019. Nearly optimal adaptive procedure with change detection for piecewise-stationary bandit. In The 22nd International Conference on Artificial Intelligence and Statistics. PMLR, 418–427.

- Garivier and Moulines (2008) Aurélien Garivier and Eric Moulines. 2008. On upper-confidence bound policies for non-stationary bandit problems. arXiv preprint arXiv:0805.3415 (2008).

- Grover et al. (2018) Aditya Grover, Todor Markov, Peter Attia, Norman Jin, Nicolas Perkins, Bryan Cheong, Michael Chen, Zi Yang, Stephen Harris, William Chueh, et al. 2018. Best arm identification in multi-armed bandits with delayed feedback. In International Conference on Artificial Intelligence and Statistics. PMLR, 833–842.

- Guha et al. (2010) Sudipto Guha, Kamesh Munagala, and Martin Pal. 2010. Multiarmed bandit problems with delayed feedback. arXiv preprint arXiv:1011.1161 (2010).

- Huo and Fu (2017) Xiaoguang Huo and Feng Fu. 2017. Risk-aware multi-armed bandit problem with application to portfolio selection. Royal Society open science 4, 11 (2017), 171377.

- Joulani et al. (2013) Pooria Joulani, Andras Gyorgy, and Csaba Szepesvári. 2013. Online learning under delayed feedback. In International Conference on Machine Learning. PMLR, 1453–1461.

- Lai and Robbins (1985) Tze Leung Lai and Herbert Robbins. 1985. Asymptotically efficient adaptive allocation rules. Advances in applied mathematics 6, 1 (1985), 4–22.

- Li et al. (2011) Lihong Li, Wei Chu, John Langford, and Xuanhui Wang. 2011. Unbiased offline evaluation of contextual-bandit-based news article recommendation algorithms. In Proceedings of the fourth ACM international conference on Web search and data mining. 297–306.

- Liu et al. (2019) Larkin Liu, Richard Downe, and Joshua Reid. 2019. Multi-armed bandit strategies for non-stationary reward distributions and delayed feedback processes. arXiv preprint arXiv:1902.08593 (2019).

- Neyman (1951) Jerzy Neyman. 1951. Berkeley symposium on mathematical statistics and probability. University of California Press.

- Robbins (1952) Herbert Robbins. 1952. Some aspects of the sequential design of experiments. Bull. Amer. Math. Soc. 58, 5 (1952), 527 – 535. https://doi.org/bams/1183517370

- Russo et al. (2017) Daniel Russo, Benjamin Van Roy, Abbas Kazerouni, Ian Osband, and Zheng Wen. 2017. A tutorial on thompson sampling. arXiv preprint arXiv:1707.02038 (2017).

- Schwartz et al. (2017) Eric M Schwartz, Eric T Bradlow, and Peter S Fader. 2017. Customer acquisition via display advertising using multi-armed bandit experiments. Marketing Science 36, 4 (2017), 500–522.

- Slivkins (2019) Aleksandrs Slivkins. 2019. Introduction to multi-armed bandits. arXiv preprint arXiv:1904.07272 (2019).

- Slivkins and Upfal (2008) Aleksandrs Slivkins and Eli Upfal. 2008. Adapting to a Changing Environment: the Brownian Restless Bandits.. In COLT. 343–354.

- Sutton et al. (1998) Richard S Sutton, Andrew G Barto, et al. 1998. Introduction to reinforcement learning. Vol. 135. MIT press Cambridge.

- Thompson (1933) William R. Thompson. 1933. On the Likelihood that One Unknown Probability Exceeds Another in View of the Evidence of Two Samples. Biometrika 25, 3/4 (1933), 285–294. http://www.jstor.org/stable/2332286

- Villar et al. (2015) Sofía S Villar, Jack Bowden, and James Wason. 2015. Multi-armed bandit models for the optimal design of clinical trials: benefits and challenges. Statistical science: a review journal of the Institute of Mathematical Statistics 30, 2 (2015), 199.

- Yu et al. (2015) Zhe Yu, Yunjian Xu, and Lang Tong. 2015. Large scale charging of electric vehicles: A multi-armed bandit approach. In 2015 53rd Annual Allerton Conference on Communication, Control, and Computing (Allerton). IEEE, 389–395.