Distributed inference for tail risks

Abstract

For measuring tail risk with scarce extreme events, extreme value analysis is often invoked as the statistical tool to extrapolate to the tail of a distribution. The presence of large datasets benefits tail risk analysis by providing more observations for conducting extreme value analysis. However, large datasets can be stored distributedly preventing the possibility of directly analyzing them. In this paper, we introduce a comprehensive set of tools for examining the asymptotic behavior of tail empirical and quantile processes in the setting where data is distributed across multiple sources, for instance, when data are stored on multiple machines. Utilizing these tools, one can establish the oracle property for most distributed estimators in extreme value statistics in a straightforward way. The main theoretical challenge arises when the number of machines diverges to infinity. The number of machines resembles the role of dimensionality in high dimensional statistics. We provide various examples to demonstrate the practicality and value of our proposed toolkit.

Keywords: Oracle property, Tail empirical process, Tail quantile process, KMT inequality

1 Introduction

Financial risk management requires risk forecasting for rare but high-impact events, typically referred to as extreme events. Extreme value analysis, statistical methods for analyzing the tail of a distribution, is recognized as a useful tool for modeling and analyzing such extremes. In this paper, we consider tail risk analysis using a large dataset that is distributedly stored at various locations.

While the availability of large datasets in general benefits statistical analysis, such as extreme value analysis, it also presents at least three practical challenges to implementing conventional statistical procedures. Firstly, a combined dataset might not be available to one end user due to privacy concerns. For example, consider analyzing insurance claims from various insurance companies. Since insurance firms are contracted for protecting privacy of their customers, it is impossible to combine all claims from different insurers into one massive dataset. Secondly, the computation cost to analyze a massive dataset can be expensive when implementing statistical procedures involving an optimization algorithm, such as maximum likelihood or loss minimization. Thirdly, storage constraints can arise when dealing with massive datasets, for instance, when the size of a dataset exceeds a computer’s memory. Another example is to analyze online stream data, where data become available in a sequential manner (Gama et al.,, 2013).

One solution to overcome these challenges is to handle the massive datasets in batches, sometimes referred to as “distributedly stored”. Divide and Conquer (DC) algorithms are often invoked when data are distributedly stored in multiple machines. One first estimates a desired quantity or parameter based on part of the data stored on each machine and then combines the results obtained from all machines to calculate an aggregated estimate, often by a simple average. DC algorithms have at least three advantages. Firstly, DC algorithms help to preserve privacy. For example, insurance firms can share some statistical results provided that that other companies cannot infer client level data from the shared results. Moreover, DC algorithms can significantly improve computational efficiency by utilizing parallel computing. Lastly, DC algorithms can overcome the challenge of storage constraint by analyzing the dataset in batches.

Theoretically a DC algorithm can be applied to a given statistical procedure only if it possesses the so-called oracle property: the aggregated estimator by averaging achieves the same statistical efficiency as the imaginary estimator using all observations. The latter is often referred to as the oracle estimator. The validity of applying a DC algorithm is not obvious for many statistical procedures, and often requires additional conditions, see Fan et al., (2019) for principal component analysis, Volgushev et al., (2019) for quantile regression and Li et al., (2013) for kernel density estimation, among others.

The validity of a DC algorithm to extreme value analysis may fail. For example, considering a distribution with a finite endpoint, a natural estimator for the endpoint is the sample maxima. If an oracle sample maxima cannot be obtained, one may consider collecting the maxima from data stored in each machine. Clearly, to obtain the oracle estimator, one needs to take the maximum of the machine-wise maxima instead of taking average. Therefore, in this specific example, the standard DC algorithm based on averaging may lead to an estimator that fails the oracle property. Since estimators in extreme value analysis are often based on high order statistics, the oracle property of the DC algorithm for such estimators are yet to be established. The goal of this paper is to fill in this gap.

In this paper, we provide general tools to establish the oracle property for distributed estimators in extreme value statistics. Chen et al., (2022) adapts a particular extreme value estimator, the Hill estimator, to the DC algorithm and proposes the distributed Hill estimator to estimate the extreme value index for the case . They study the asymptotic behavior of the distributed Hill estimator and show sufficient, sometimes also necessary, conditions under which the distributed Hill estimator possesses the oracle property. The proof therein relies on the specific construction of the Hill estimator, and cannot be generalized to validate the oracle property of other estimators for the extreme value index, let alone that of other estimators for practically relevant quantities such as high quantile, tail probability and endpoint. By contrast, using the tools in this paper, the oracle property for most estimators extreme value statistics based on the peak-over-threshold (POT) approach can be established in a straightforward way.

In classical extreme value statistics, two key tools for establishing asymptotic theories are the tail empirical process and the tail quantile process. Let be an intermediate sequence such that as , . The tail empirical process is defined as

where and denotes the empirical cumulative distribution function . Here and are suitable versions of and , respectively. Drees et al., (2006) shows a weighted approximation of the tail empirical process (see Section 2 below) under some mild conditions. The approximation of the tail empirical process is a useful tool in a wider context. For example, Drees et al., (2006) proposes a test for the extreme value condition, de Haan and Ferreira, (2006, Example 5.1.5) establishes the asymptotic normality of the Hill estimator, both by using this result.

Analogous to the tail empirical process, Drees, (1998) shows a weighted approximation of the tail quantile process (see Section 3 below). The tail quantile process is defined as

where are the order statistics of the sample . Here and thereafter, we use to denote the largest integer less than or equal to . Note that the POT approach in extreme value statistics often uses high order statistics . Consequently, compared to the tail empirical process, the tail quantile process is more straightforward for proving asymptotic theory for estimators in extreme value statistics based on the POT approach. By writting such estimators as a functional of and using the weighted approximation of the tail quantile process, one can derive their asymptotic behavior. Examples of estimators for the extreme value index based on the POT approach are the probability weighted moment estimator (Hosking and Wallis,, 1987), the maximum likelihood estimator (Drees et al.,, 2004) and the Pickands estimator (Pickands III,, 1975). In addition, the asymptotic behavior for the estimators of high quantile, tail probability and endpoint can be derived from the approximation of the tail quantile process as well, see e.g. Chapter 4 in de Haan and Ferreira, (2006).

In this paper, we establish weighted approximations of tail empirical processes and tail quantile processes for the distributed subsamples in a joint manner, with linking these approximations to that for the oracle sample. Such results lead to the oracle properties of many distributed estimators in extreme value statistics based on the POT approach, with some straightforward proofs. Mathematically, we show a stronger result than the classical oracle property: the difference between the distributed estimator and the oracle estimator diminishes faster than the speed of convergence of the oracle estimator. Note that Chen et al., (2022) only shows that the limiting distribution of the distributed Hill estimator coincides with that of the oracle estimator, whereas asymptotic behavior of the difference between the two estimators cannot be derived using the method therein. Daouia et al., (2021) achieves such result for the Hill estimator. However, the proof in Daouia et al., (2021) cannot be generalized to other estimators in extreme value statistics since it relies on the specific structure of the Hill estimator.

The main challenge for handling tail empirical process arises when the number of machines diverges to infinity. The number of machines resembles the role of dimensionality in high dimensional statistics. Observing that with equal subsample sizes across different machines, the tail empirical process for the oracle sample is the average of the tail empirical processes based on the distributed subsamples, it seems trivial that they can be approximated by the same asymptotic limits. However, to aggregate the tail empirical processes in different machines, we need to make sure that the approximation errors in different machines are uniformly negligible. We achieve this mathematically difficult result by invoking Komlós-Major-Tusnády type inequalities (see e.g. Komlós et al., (1975)). Linking the weighted approximation of the tail empirical process based on the oracle sample to those of the tail empirical processes on each machine is an important intermediate step towards establishing similar links between the corresponding tail quantile processes.

By contrast, when handling tail quantile processes, we cannot follow similar steps as for tail empirical processes. The main difference is that the average of the tail quantile processes based on distributed subsamples in different machines is not equal to the tail quantile process based on the oracle sample. Linking the approximations of the tail quantile processes based on the distributed subsamples to that based on the oracle sample poses an additional layer of technical difficulty, which we will handle in Section 3.

The rest of this paper is organized as follows. Section 2 shows the weighted approximations of the tail empirical processes based on the distributed subsamples in a joint manner and links that to the weighted approximation of tail empirical process based on the oracle sample. Section 3 shows the analogous result for the weighted approximations of the tail quantile processes. We provide various examples in Section 4 to show how these tools can be used to prove the oracle property of extreme value estimators such as the estimators of extreme value index, high quantile, tail probability and endpoint. Section 5 extends the theoretical results to the case of heterogeneous subsample sizes. A real data application is given in Section 6. A concluding remark is made in Section 7. The technical proofs are deferred to the Supplementary Material, along with a simulation study showing the performance of the distributed estimators for the extreme value index and the high quantile.

Throughout the paper, means that as ; means that both and are as .

2 Distributed Tail Empirical Process

Let be independently and identically distributed (i.i.d.) random variables with distribution function , which is in the maximum domain of attraction of an extreme value distribution with index , i.e. there exist a positive function and a real function such that,

for all . We denote this assumption as , where is the so called extreme value index. Extreme value statistics considers estimating the extreme value index , the functions and , as well as other practically relevant quantities such as high quantile of . For established results in extreme value statistics, we refer interested readers to monographs such as de Haan and Ferreira, (2006) and Resnick, (2007).

Write , where ← denotes the left-continuous inverse function. Then the necessary and sufficient condition for with is

| (1) |

for all . In this paper, we focus on the distributions which satisfy the second order refinement of condition (1) as follows (de Haan and Stadtmüller,, 1996): there exists an eventually positive or negative function with and a real number such that for all ,

| (2) |

Under this condition, one can find suitable normalizing functions such that the convergence in (2) holds uniformly as follows, see Corollary 2.3.7 in de Haan and Ferreira, (2006). There exists functions , and such that, for any , there exists such that, for all ,

| (3) |

where

For the details of the expression of and , see Corollary 2.3.7 in de Haan and Ferreira, (2006).

Let be an intermediate sequence such that as , . The tail empirical process for the oracle sample is defined as

where and denotes the empirical cumulative distribution function .

Under the second order condition (2) and as , Drees et al., (2006) shows that, under proper Skorokhod construction, there exists a sequence of Brownian motions , such that, for any ,

| (4) | ||||

where and are defined in Theorem 1 below.

The result (4) is based on the oracle sample. We intend to provide an analogous result for the tail empirical processes based on the distributed subsamples in a joint manner. Assume that the observations are distributedly stored in machines with observations in each machine and then . We will extend our analysis to the case of heterogeneous subsample size in Section 5. The tail empirical process based on the observations in machine is defined as

where and denotes the empirical distribution function based on the observations in machine . Here is an intermediate sequence such that and , as .

We intend to relate the asymptotics of and where . Without causing any ambiguity, we use the simplified notation and for the tail empirical processes based on the oracle sample and the sample in machine , respectively.

Throughout this paper, let be sequences of integers such that, and as . We assume the following conditions for the sequences and :

-

(A1)

as .

-

(A2)

.

-

(A3)

as .

Remark 1.

Note that . Condition (A1) is a typical condition assumed in extreme value analysis to guarantee finite asymptotic bias in the oracle estimator. Condition (A2) states that, the number of machines () should be smaller than the number of observations used in each machine (). Similar conditions are assumed in the literature of distributed inference for other statistical procedures, see e.g. Corollary 3.4 in Volgushev et al., (2019) and Theorem 4 in Zhu et al., (2021). Condition (A3) is an additional technical condition, which requires that the number of observations () in each machine is at a sufficiently high level for given and .

Remark 2.

The following theorem shows the weighted approximations of the tail empirical processes based on the distributed subsamples in a joint manner.

Theorem 1.

Suppose that the distribution function satisfies the second order condition (2) with and . Let be sequences of integers satisfying conditions (A1)-(A3) and . Then under suitable Skorokhod construction, there exist independent sequences of Brownian motions , such that for any , as ,

where

Moreover, as ,

where is a version of the Brownian motion in (4).

For , a similar but simpler result is given as follows.

Theorem 2.

Suppose that the distribution function satisfies the second order condition (2) with and . Let be sequences of real numbers that satisfy conditions (A1)-(A3) and . Then under suitable Skorokhod construction, there exist independent sequences of Brownian motions , such that for any , as ,

Moreover, as ,

where .

To prove these theorems, we need a fundamental inequality to bound the approximation error of the tail empirical process to the Gaussian process in machine , which is of independent interest. Consider a positive sequence as , satisfying

| (5) | |||||

| (6) | |||||

| (7) |

Proposition 1.

Suppose that the distribution function satisfies the second order condition (2) with and . Let be a sequence of real numbers satisfying conditions (5)-(7) and . Then for sufficiently large , under suitable Skorokhod construction, there exist independent sequences of Brownian motions and a constant such that, for any ,

where

and is defined by .

3 Distributed Tail Quantile Processes

Drees, (1998) provides a weighted approximation of the tail quantile process. Assume the second order condition (2) and as , with the same Brownian motions in (4), we have that, for any ,

Again, this result is based on the oracle sample. We intend to provide weighted approximations of the tail quantile processes based on the distributed subsamples in a joint manner. The tail quantile process based on the observations in machine is defined as

where are the order statistics of the observations in machine .

We aim at linking the asymptotics of and where . Again, without causing any ambiguity, we use the simplified notation and for the tail quantile process based on the oracle sample and the sample in machine , respectively. Since the average of the tail quantile processes based on distributed subsamples in machines is not equal to the tail quantile process of the oracle sample, we cannot follow similar steps as in Section 2. Instead, we achieve our goal by “inverting” the result for the tail empirical processes. More specifically, we intend to replace in Theorem 1 by for .

The following theorem shows that, with the same sequences of Brownian motions defined in Theorem 1: , , the approximation errors of the tail quantile processes are uniformly negligible for .

Theorem 3.

For , a similar but simpler result is given as follows.

Theorem 4.

The following corollary, which is a direct consequence of Theorem 4 with applying the Cramér’s delta method, can be used for proving asymptotic theory of the distributed Hill estimator.

Corollary 1.

Assume the same conditions as in Theorem 2. By the Cramér’s delta method, we can obtain that, as ,

Theorem 3 provides a useful tool for establishing the oracle property of some extreme value estimators based on the POT approach. For example, using Theorem 3, one can immediately show that, the distributed Pickands estimator achieves the oracle property since the distributed Pickands estimator is a functional of the tail quantile processes at three points and . We leave this to the readers. Instead, we focus on some other estimators, for which Theorem 3 alone may not be sufficient for proving their oracle property. We use the probability weighted moment (PWM) estimator as an example to explain the remaining issue.

The PWM estimator in machine is defined as

where

The distributed PWM estimator is defined as the average of the estimates from each machine:

To establish the asymptotic theory for , we need to handle the asymptotic expansion of and for in a joint manner. For , define

| (8) |

Then we can write as

The three terms and can be handled in a similar way as handling analogous terms in the oracle PWM estimator. The integral can be handled using Theorem 3. However, handling the last integral requires some additional tools to deal with the “corner” of the tail quantile processes. Similarly, for , we need to handle a different integral in the “corner”: To complete the toolkit for our purpose, we provide a general result regrading the joint asymptotic behavior of weighted integrals of the tail quantile processes in the corner area .

Proposition 2.

Assume the same conditions as in Theorem 1. Assume that a function defined on (0,1) satisfies with . Then, there exists a sufficiently small constant , such that, as ,

4 Application

4.1 Distributed inference for the Hill estimator

In this subsection, we apply the approximations of the tail empirical processes based on the distributed subsamples to establish the oracle property of the distributed Hill estimator. The Hill estimator in machine is defined as

The distributed Hill estimator is defined as the average of the estimates from each machine: . And the oracle Hill estimator using the top exceedance ratios is

Corollary 2.

Proof of Corollary 2.

By applying the same techniques used in proving the asymptotic normality of the oracle Hill estimator (cf. Example 5.1.5 in de Haan and Ferreira, (2006)), we have that, as ,

For , note that, as ,

By taking in Theorem 4, we get that, as ,

| (9) |

Thus, as ,

For , since , we obtain that,

We can handle in a similar way and get that,

The Corollary is proved by noting that . ∎

Remark 3.

Chen et al., (2022) only shows that the limiting distribution of the distributed Hill estimator coincides with that of the oracle Hill estimator, but does not investigate the difference between the two estimators.

4.2 Distributed inference for the PWM estimator

In this subsection, we take the distributed PWM estimator as an example to show how to apply Theorem 3 and Proposition 2 to establish its oracle property. The oracle PWM estimator is defined as

where and are counterparts of and based on the oracle sample, respectively.

Corollary 3.

Proof of Corollary 3.

For a continuous function , define an operator

It is obvious that is a linear operator.

Note that, for the oracle PWM estimator using top exceedances, we have that, as ,

see e.g. Section 3.6.1 in de Haan and Ferreira, (2006). By using similar techniques, we obtain that, as ,

Recall that is a linear operator and , we get that

The Corollary is proved provided that, as , and .

For handling , we divide into and . Thus,

We first handle . Note that, for , we can always find a such that . Then, by Theorem 3, as ,

The term can be handled by Proposition 2 as follows. Choose . Since and , the conditions in Proposition 2 hold. The proposition yields that . Hence, we obtain as . The term can be handled in a similar way with choosing . ∎

4.3 Distributed inference for the MLE

The MLE for the extreme value index and the scale parameter based on the sample on machine , is defined as the solution of the following equations:

| (10) | ||||

The distributed MLE for the extreme value index and the scale parameter are defined as

The oracle MLE for the extreme value index and the scale parameter are defined in a similar way by using the oracle sample.

Corollary 4.

The proof is deferred to the Supplementary Material. Solving the likelihood equations (10) involves an optimization algorithm. The computation cost can be high when implementing an optimization algorithm for the oracle sample. We provide a simulation study to compare the computation cost of the oracle MLE and the distributed MLE in the Supplementary Material.

4.4 Distributed inference for the high quantile, endpoint and tail probability

In this subsection, we show how to establish the oracle property of the estimators for the high quantile, endpoint and tail probability. In order to estimate these quantities, we need to estimate the extreme value index , the scale parameter and the location parameter , see e.g. de Haan and Ferreira, (2006, Chapter 4). We focus on the PWM estimators for and as an example. Other estimators based on the POT approach can be treated in a similar way.

We apply the DC algorithm to estimate and based on distributed subsamples. Define the distributed scale estimator as

and the distributed location estimator as

Following similar steps as in proving the oracle property of , we can show that, as ,

4.4.1 High quantile

Let , where as , be the quantile we want to estimate. In finance management, the high quantile is often referred to as value at risk, which is the most prominent risk measure. The detailed procedures of the distributed estimator for high quantile are given as follows:

-

•

On each machine , we calculate and transmit these values to the central machine.

-

•

On the central machine, we take the average of the statistics collected from the machines to obtain .

-

•

On the central machine, we estimate with by

(11)

The oracle high quantile estimator is defined in an analogous way as , with replacing , and by , and in (11), respectively. Following the lines of the proof for the asymptotics of the oracle high quantile estimator, we can obtain the asymptotic normality of . Moreover, since , and possess the oracle property, also achieves the oracle property due to applying the Cramér delta method. We present the result in the following corollary while omitting the proof.

Corollary 5.

4.4.2 Endpoint

Next, we consider the problem of estimating the endpoint of the distribution function . Assume that for some . In this case the endpoint is finite. The endpoint can be treated as a specific case of quantile by regarding as . The distributed endpoint estimator can be defined as

The definition of the oracle endpoint estimator is in an analogous way. Again, the distributed endpoint estimator achieves the oracle property as in the following corollary.

Corollary 6.

Assume the same conditions as in Corollary 3 and . Then, as ,

4.4.3 Tail probability

Lastly, we consider the dual problem of estimating the high quantile: given a large value of , how to estimate under the distributed inference setup. The detailed procedures for estimating the tail probability are similar to that for estimating the high quantile, except that on the central machine, we estimate the tail probability by

The definition of the oracle tail probability estimator is in an analogous way. Note that is valid only for (cf. Remark 4.4.3 in de Haan and Ferreira, (2006)). The oracle property of is established in the following corollary.

Corollary 7.

Assume the same conditions as in Corollary 3 and . Denote and for . Suppose that and as , then

5 Heterogeneous subsample sizes

In this section, we extend our results to the case of heterogeneous subsample sizes. We assume that the observations are distributedly stored in machines with observations in machine , , i.e. . Moreover, we assume that all , diverge in the same order. Mathematically, that is,

| (12) |

for some positive constants and and all .

The tail empirical process based on the observations in machine is now defined as

where and denotes the empirical distribution function based on the observations in machine .

We choose such that the ratios are homogenous across all the machines, i.e.,

| (13) |

Denote , clearly . Then, we have that,

In other words, the oracle tail empirical process is a weighted average of the tail empirical processes based on the distributed subsamples, where the weights equal to the fraction of the observations on each machine.

Following similar steps as in proving Theorem 1, we obtain the following result.

Theorem 5.

Similar results hold for the tail quantile processes as in Theorem 3. Eventually, we can re-establish the oracle property of the distributed estimators as follows. Suppose the oracle estimator is based on top order statistics in the oracle sample. On each machine, we use the top order statistics in the estimation. By taking a weighted average of the estimates from all machines using the weights , to obtain the distributed estimator, the oracle property holds under the same conditions as in the homogenous case with similar proofs.

6 Real Data Application

We use a dataset containing car insurance claims in five states of United States: Iowa (), Kansas (), Missouri (), Nebraska (), and Oklahoma (). The total sample size is . We work under a hypothesis scenario: each state cannot share its own data to others, but they are willing to share their statistical results. Then one can apply a DC algorithm for conducting extreme value statistics. Our target is to estimate the common extreme value index of the total claim amount. We consider the MLE instead of the Hill estimator considered by Chen et al., (2022) since we do not assume heavy tail at the first place.

Let be the total number of exceedances used by the five states. As suggested in Section 5, we choose as and apply the MLE for each of the five states to obtain , . Then, we combine these five estimates to obtain the distributed MLE by

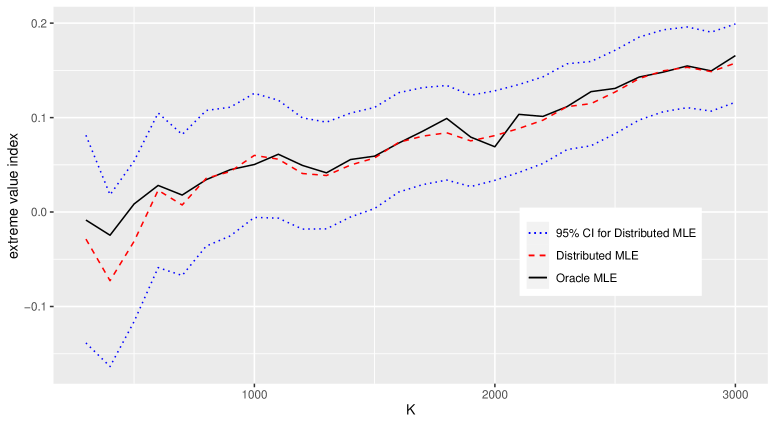

The distributed MLE is plotted against different values of in Figure 1, along with its 95% confidence interval. We also plot the oracle MLE in this figure. The distributed MLE is close to the oracle MLE for almost all levels of and the oracle MLE always falls into the 95% confidence interval constructed based on the distributed MLE.

By choosing , we obtain that the distributed MLE for the extreme value index is about 0.05. And we cannot reject the hypothesis that the extreme value index is under the 5% significance level for this choice of . This result shows that the insurance claims may not be heavy tailed. In turn, the distributed Hill estimator adopted in Chen et al., (2022) may not be suitable for this application.

7 Discussion

In this paper, we investigate the problem of distributed inference in extreme value analysis when the oracle sample are i.i.d.. In fact, the assumption that all the data are drawn from the same distribution can be relaxed. In real applications, observations from different machines may follow different distributions, but nevertheless share some common properties such as the extreme value index.

We assume that all observations are independent, but only observations on the same machine follow the same distribution. Denote the common distribution function of the observations in machine as . We assume that, there exists a continuous function which satisfies the second order condition (2) with . In addition, assume that the series of constants satisfies that for all and , and is a positive regularly varying function with index such that as ,

By restricting that , Chen et al., (2022) gives a theoretical proof for the asymptotic theories of the distributed Hill estimator. Following similar steps, we can also handle tail empirical processes and tail quantile processes. The details are omitted.

Supplementary Material

- Appendix.pdf:

-

The Supplementary Material contains all the technical proofs and simulation studies.

References

- Chen et al., (2022) Chen, L., Li, D., and Zhou, C. (2022). Distributed inference for the extreme value index. Biometrika, 109(1):257–264.

- Daouia et al., (2021) Daouia, A., Padoan, S. A., and Stupfler, G. (2021). Optimal pooling and distributed inference for the tail index and extreme quantiles. arXiv preprint arXiv:2111.03173.

- de Haan and Ferreira, (2006) de Haan, L. and Ferreira, A. (2006). Extreme Value Theory: An Introduction. Springer Science & Business Media.

- de Haan and Stadtmüller, (1996) de Haan, L. and Stadtmüller, U. (1996). Generalized regular variation of second order. Journal of the Australian Mathematical Society, 61(3):381–395.

- Drees, (1998) Drees, H. (1998). On smooth statistical tail functionals. Scandinavian Journal of Statistics, 25(1):187–210.

- Drees et al., (2006) Drees, H., de Haan, L., and Li, D. (2006). Approximations to the tail empirical distribution function with application to testing extreme value conditions. Journal of Statistical Planning and Inference, 136(10):3498–3538.

- Drees et al., (2004) Drees, H., Ferreira, A., and de Haan, L. (2004). On maximum likelihood estimation of the extreme value index. Annals of Applied Probability, 14(3):1179–1201.

- Fan et al., (2019) Fan, J., Wang, D., Wang, K., and Zhu, Z. (2019). Distributed estimation of principal eigenspaces. Annals of Statistics, 47(6):3009–3031.

- Gama et al., (2013) Gama, J., Sebastiao, R., and Rodrigues, P. P. (2013). On evaluating stream learning algorithms. Machine learning, 90:317–346.

- Hosking and Wallis, (1987) Hosking, J. R. and Wallis, J. R. (1987). Parameter and quantile estimation for the generalized pareto distribution. Technometrics, 29(3):339–349.

- Komlós et al., (1975) Komlós, J., Major, P., and Tusnády, G. (1975). An approximation of partial sums of independent rv’-s, and the sample df. i. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 32(1):111–131.

- Li et al., (2013) Li, R., Lin, D. K., and Li, B. (2013). Statistical inference in massive data sets. Applied Stochastic Models in Business and Industry, 29(5):399–409.

- Pickands III, (1975) Pickands III, J. (1975). Statistical inference using extreme order statistics. Annals of statistics, 3(1):119–131.

- Resnick, (2007) Resnick, S. I. (2007). Heavy-tail phenomena: probabilistic and statistical modeling. Springer Science & Business Media.

- Volgushev et al., (2019) Volgushev, S., Chao, S.-K., and Cheng, G. (2019). Distributed inference for quantile regression processes. Annals of Statistics, 47(3):1634–1662.

- Zhu et al., (2021) Zhu, X., Li, F., and Wang, H. (2021). Least squares approximation for a distributed system. Journal of Computational and Graphical Statistics. to appear, https://doi.org/10.1080/10618600.2021.1923517.