Mean Field Game of Optimal Relative Investment with

Jump Risk

Abstract

This paper studies the -player game and the mean field game under the CRRA relative performance on terminal wealth, in which the interaction occurs by peer competition. In the model with agents, the price dynamics of underlying risky assets depend on a common noise and contagious jump risk modelled by a multi-dimensional nonlinear Hawkes process. With a continuum of agents, we formulate the MFG problem and characterize a deterministic mean field equilibrium in an analytical form under some conditions, allowing us to investigate some impacts of model parameters in the limiting model and discuss some financial implications. Moreover, based on the mean field equilibrium, we construct an approximate Nash equilibrium for the -player game when is sufficiently large. The explicit order of the approximation error is also derived.

Mathematics Subject Classification (2010): 91A15, 91G80, 91G40, 60G55

Keywords: Relative performance, contagious jump risk, mean field game with jumps, mean field equilibrium, approximate Nash equilibrium

1 Introduction

The Model Setup. In this paper, we consider a financial market model with agents. Each agent invests in a common riskless bond and one individual stock . The common time horizon for all agents is denoted by . For , the price process of the th stock follows the following SDE:

| (1.1) |

with the given parameters , . Here, represents the riskless interest rate, and is an -dimensional Brownian motion under the filtered probability space with the reference filtration satisfying the usual conditions. The Brownian motion appears in all price dynamics, which represents a common noise in the financial market. The Brownian motion , specified to each individual risky asset, stands for the idiosyncratic noise. In addition, each stock is subject to the downward jump risk and the jump contagion among all stocks is allowed. In particular, we denote as an -dimensional mutually exciting point process modelled by a nonlinear Hawkes process with a (bounded, Lipschtiz and differentiable) jump rate function .111For example, it is referred as the jump function in Chevallier (2017) in the context of generalized Hawkes processes; and it is called the spiking rate function by Löcherbach (2018) in the context of interacting neurons. The intensity process is defined by , and the compensated process of , defined by , , is an -dimensional -martingale, where . Namely, for each , for is a scalar -martingale.

The global market filtration is defined by as the right-continuous augmentation by null sets (see Karatzas and Shreve (1991), Definition 7.2 in Chapter 2). By Bo and Capponi (2018), the Brownian motion under is also a Brownian motion under , i.e., the immersion property holds. It is assumed in the present paper that the vector intensity process is governed by

| (1.2) |

where is the mean-reverting level of the underlying intensity factor of stock with speed , describes the scaled jump size effect to the intensity factor of stock , and measures the contagion effect on the intensity factor of stock by the jump of stock . The contagious risk is then captured because the downward jump of one stock increases the jump intensity of all other stocks, leading to a higher risk of default clustering (see Bo et al. (2019a)).

Let the -predictable process be the proportion of wealth that the agent allocates in the stock at time . The self-financing wealth process of agent under the control is given by

| (1.3) |

where denotes the initial wealth of agent . The portfolio vector is denoted by . Let us denote the set of admissible controls for the agent . We say a control process is admissible if is -predictable and satisfies for some constant and positive constant (both and depend on the control) such that the non-bankruptcy condition holds a.s. for . Note that the pure jump martingale has the jump size of one. In view of (1.3), the wealth process must be positive a.s. if the initial wealth level because the admissible control is constrained to satisfy for all .

Each agent in the market aims to maximize the expected utility with a competition component represented by the geometric average of the terminal wealth from all peers. The objective function of the th agent is given by

| (1.4) |

in which the utility function of the th agent is of the CRRA type that

| (1.5) |

where is a power utility that . It is assumed in the present paper that all risk aversion parameters and all competition weight parameters .

Remark 1.1.

The above relative investment preference is motivated by the fact that peer competition sometimes has notable impacts on fund manager’s decision making. The parameter of the agent represents how competitive the agent is towards the relative performance with her peers. The small (resp. large) value of implies a low (resp. high) relative performance concern. In the extreme case, the utility with reduces to the standard utility on her own absolute wealth; while the utility with indicates that the agent is extremely sensitive to her relative performance with other peers and no absolute performance is concerned.

Due to the presence of inside the utility, the optimal decision of the agent is coupled with optimal controls by other peers, which makes the game problem challenging especially when there are jump risk contagion and common noise. In the present paper, we aim to provide an approximate Nash equilibrium to the -player game problem, which is defined in the following sense.

Definition 1.1 (Approximate Nash Equilibrium (ANE)).

Let the objective functional be defined in (1.4). An admissible strategy is called a Nash equilibrium if, for all with , it holds that

| (1.6) |

If there exists a constant satisfying , and it holds that

| (1.7) |

we call an -approximate Nash equilibrium.

To this end, we will first take advantage of the simplified structure of the mean field game (MFG) when , in which the impact of an individual agent on the aggregated wealth of the whole population becomes negligible. That is, comparing with in (1.4) for agents, we now consider (with being the set of -adapted processes that are right continuous with left limits) as the geometric average wealth of the continuum of agents, which is the competition component in the utility of a representative agent. The MFG problem is to find a pair that solves the utility maximization problem for a representative agent similar to (1.4) that

where (resp. ) is the utility function (resp. the wealth process under an arbitrary control ) of the representative agent, and is the wealth process under the control . In addition, the geometric average wealth of the population coincides with the geometric mean of the wealth process of the representative agent that . The precise formulation of the MFG problem and the definition of mean field equilibrium are given in Section 2. Using the stochastic maximum principle, we are able to characterize one deterministic mean field equilibrium in analytical form. Based on the information and the structure of this mean field equilibrium, we can then construct the -Nash equilibrium for the -player game as described in Definition 1.1.

Literature Review. Optimal investment under relative performance for a finite number of agents and a continuum of agents has been an important research topic in recent years. In a Black-Scholes model, Espinosa and Touzi (2015) and Bielagk et al. (2017) formulate and study the -player game under the CARA relative performance using the coupled quadratic BSDE system when the equilibrium pricing and portfolio constraints are also incorporated. In a log-normal market model with deterministic parameters and common shock together the asset specialization to each agent, Lacker and Zariphopoulou (2019) consider the -player game and MFG problems under both CARA and CRRA relative performance on terminal wealth. Thanks to the simplified structure of the asset specialization, the constant equilibrium is obtained therein for both the -player game and MFG problems. In the same framework, Lacker and Soret (2020) generalize the problems to examine optimal relative performance on consumption under CRRA utilities. Fu et al. (2020) consider the generalization of the market model in Lacker and Zariphopoulou (2019) by allowing random return and volatility parameters and solve the -player game and MFG problems using the FBSDE approach when the exponential relative performance on terminal wealth is concerned. Dos Reis and Platonov (2021) study the MFG under forward relative performance utilities of CARA type. Kraft et al. (2020) formulate and solve some -player games in a general stochastic volatility price model (Heston and Chacko-Viceira stochastic-volatility models as special cases) with unhedgeable stochastic factors. Under the exponential relative performance on terminal wealth, Hu and Zariphopoulou (2022) recently investigate the -player game and MFG in the incomplete Itô-diffusion market model and also in the case with random risk tolerance coefficients.

To the best of our knowledge, the -player games and MFGs under relative performance when the underlying price dynamics exhibit jumps have not been studied before. On the other hand, the importance of considering defaultable risky assets, especially after the systemic failure caused by the global financial crisis, has attracted a lot of attention; see, for example, Bélanger et al. (2004), Yu (2007) and references therein. To better understand the impact of systemic default risk on dynamic portfolio management, abundant recent works have considered optimal investment problems when jumps of risky assets are contagious. See, for example, Bo and Capponi (2018), Bo et al. (2019a), Bo et al. (2019b), Shen and Zou (2020), Bo et al. (2022) among others that are based on the interacting intensity framework, allowing the credit default in one risky asset to increase the default intensities of other surviving names. See also Jin et al. (2021) in the context of optimal dividend control for an insurance group. The present paper aims to enrich the study of the -player games and MFGs under relative performance by featuring the jump risk. In particular, the jump risk in price dynamics is modelled by an -dimensional mutually exciting Hawkes process, whose componentwise intensity process satisfies the specific form of (1.2). As a result, the contagion phenomenon can be depicted in the model with agent because the jump of one stock leads to a larger jump intensity of all other stocks. Meanwhile, we adopt the asset specialization framework in Lacker and Zariphopoulou (2019) with a common noise and focus on the CRRA relative performance utility. The presence of contagious jumps in price dynamics give rise to the controlled jump component.

Starting from the seminal works by Lasry and Lions (2007) and Huang et al. (2006), MFGs have been actively studied and widely applied in economics, finance and engineering. Giving a full list of references is beyond the scope of this paper. For some recent developments in theories and applications, we refer to Guéant et al. (2011), Bensoussan et al. (2013), Carmona (2016), Carmona and Delarue (2018) and references therein. However, we also note the majority of existing research has focused on models when the controlled state processes have continuous paths, and the study of MFGs with controlled jumps is relatively rare. In the simple setting of inhomogeneous Poisson process, Nutz and Zhang Nutz and Zhang (2019) consider the rank-based mean field competition when each agent controls the intensity of the Poisson project process. Yu et al. (2021) further extend the model to some two-layer mean field competitions based on teamwork formulations, in which team members collaborate to control the intensity of the Poisson project process. Gomes et al. (2013) and Neumann (2020) examine some MFGs with continuous time Markov chains. Hafayed et al. (2014) considers the McKean-Vlasov stochastic control problems. Recently, Benazzoli et al. (2020) study MFGs with controlled jump-diffusion processes, in which the jump component is driven by a Poisson process with a time-dependent intensity function. The existence of a Nash equilibrium is obtained therein by using relaxed control and martingale problem arguments. Building upon results in Benazzoli et al. (2020), Benazzoli et al. (2019) further verify that the mean field equilibria can be used to construct an approximate Nash equilibrium in the -player game when is large enough.

Our Contributions. Although our targeted MFG is in the realm of MFGs with controlled jump-diffusion processes, our model and methodology differ from the ones in Benazzoli et al. (2020) (see also Benazzoli et al. (2019)). To be precise, the MFG problem in Benazzoli et al. (2020) stems from a symmetric nonzero-sum -player game, in which the Poisson jump process for each player has the same deterministic intensity and all players have the same objective function. In contrast, our -player game is formulated for heterogeneous agents with different underlying processes and relative performance utilities. The contagious jump risk is a new feature of our -player game and a common noise appears in all risky assets, which are not concerned by Benazzoli et al. (2020). Our mathematical contribution is two-fold. First, we model the contagious jump risk in the -player game by a mutually exciting Hawkes process, which enables us to formulate a tractable MFG problem with controlled jumps under the assumption of constant type vector (see (2.1) in the assumption below). The strong control approach can be applied and we can characterize a deterministic mean field equilibrium in an analytical form by using the stochastic maximum principle argument; see Theorem 2.2. Some quantitative properties of the obtained mean field equilibrium are examined, yielding some interesting financial implications. Second, despite the lost tractability in the -player game, we can use the mean field equilibrium to construct an -approximate Nash equilibrium in the model with finite agents when is sufficiently large. We highlight that the explicit convergence rate of the approximation error is also obtained; see Theorem 4.4. The constructed approximate Nash equilibrium using the mean field equilibrium can efficiently help to reduce the dimensionality of the -player game in practical applications.

The rest of the paper is organized as follows. In Section 2, we formulate the MFG problem in the limiting model and obtain a time-dependent deterministic mean field equilibria. Section 3 presents some quantitative properties and numerical sensitivity results on the mean field equilibrium. Section 4 establishes an approximate Nash equilibrium for an -player game problem. Some conclusion remarks and future directions are given in Section 5. Finally, the proofs of some auxiliary results and arguments to derive the mean field limit of the default intensity are reported in A and B, respectively.

2 Mean Field Game Problem

To avoid the complexity of the coupled controls in the -player game problem (1.4), one can consider the limiting model that enjoys the decentralized structure and the impact of an individual agent on the whole population is negligible. That is, we can first solve a stochastic control problem for a representative agent against a fixed environment (assuming that the geometric average wealth of the population is ) and derive its best response portfolio strategy (as a functional of ). We then apply this best response strategy to generate the wealth process of the representative agent. Finally, as all agents should behave the same in the mean field model, the geometric mean of the wealth process (as a functional of ) of the representative agent should coincide with the geometric average wealth of the whole population, which gives the consistency condition to characterize a mean field equilibrium. The mathematical formulation of the MFG problem and the precise definition of a mean field equilibrium are given as follows.

For , let us denote the type vector and the space . Let (resp. ) be the Borel -algebra generated by the open sets of (resp. the set of probability measures on ).

For mathematical tractability, the following assumption is imposed throughout the paper.

-

: There exists a constant vector

(2.1) denoting the type vector of the limiting model such that

(2.2) where denotes the Dirac measure on the constant vector and the convergence holds with the order of and “” denotes the weak convergence, i.e., as for every bounded continuous function on . In addition, it is assumed that as , where .

Under the assumption that the type vector is a constant vector in the mean field model, the arguments provided in B yield that the mean field limit of the intensity process is a continuous deterministic function, which satisfies

| (2.3) |

In the mean field model when , the wealth process of a representative agent is governed by

| (2.4) |

where is a scalar Brownian motion under that is independent of Brownian motion . The pure jump martingale satisfies the decomposition that

where is a Poisson point process with the deterministic intensity process .

For sufficiently large, in view of the common noise in the wealth process , we may approximate the geometric mean by a càdlàg -adapted process (i.e., ). Let denote the smallest filtration satisfying the usual conditions, in which , , are adapted. We denote the set of admissible controls when is -predictable and satisfies with some constant and positive constant (depending on the control) such that has no bankruptcy.

Let us first give the definition of mean field equilibrium.

Definition 2.1 (Mean Field Equilibrium (MFE)).

For a given -adapted process , let be the best response solution to the stochastic control problem (2.5). The strategy is called a mean field equilibrium (MFE) if it is the best response to itself such that , , where is the wealth process in (2.4) under the control . Moreover, if is deterministic, we call a deterministic MFE.

Based on the above definition, finding a MFE of the mean field game problem is to solve the two-step problem:

Step 1. For a fixed -adapted process , we solve a stochastic control problem for a representative agent against the fixed environment that

| (2.5) |

where the wealth process satisfies (2.4) with the risk aversion parameter and the competition parameter . The best response strategy for the representative agent is denoted by , and stands for the wealth process in (2.4) under the control .

Step 2. We next derive a MFE by the consistency condition, which is to find the fixed point to the equation for all . The MFE is then given by .

To facilitate the proof of the main theorem in this section, we first present the next auxiliary lemma, whose proof is reported in A.

Lemma 2.1.

Define the function with and that

| (2.6) |

Then, for each fixed , there exists a unique such that

| (2.7) |

Moreover, there exists an small enough such that . Equivalently, for satisfying (2.7), there exists a unique continuous and decreasing function such that

| (2.8) |

where has a continuous partial derivative with respect to .

We can now establish the main result of this section that gives a time-dependent deterministic mean field equilibrium in the MFG problem as a function of the deterministic limiting intensity process.

Theorem 2.2.

There exists one deterministic MFE strategy that satisfies

| (2.9) |

Equivalently, this deterministic MFE strategy can be written by

| (2.10) |

Here, and are given in Lemma 2.1. In addition, let be the wealth process under the deterministic MFE . The associated fixed point satisfying the consistency condition for is characterized by

| (2.11) |

where the function is given by, for ,

| (2.12) |

Here, is given by (2.3).

Remark 2.3.

Note that if there is no contagious jump risk in price dynamics, i.e., (i.e., the jump rate function ), the function defined in (2.6) is reduced to

It follows that

| (2.13) |

which is a constant mean field Nash equilibrium that coincides with the result in Theorem of Lacker and Zariphopoulou (2019). Therefore, the obtained MFE given in (2.10) is a generalization of the constant MFE in Lacker and Zariphopoulou (2019) to incorporate the jump risk.

Proof of Theorem 2.2.

First, for a given process , we aim to solve the mean field stochastic control problem via the stochastic maximum principle; see Øksendal and Sulem-Bialobroda (2005). To this end, we first note that the Hamiltonian function corresponding to the control problem (2.5) is given by

| (2.14) |

for with the policy space .

Let be an arbitrary admissible strategy that may depend on , and be the corresponding wealth process under . Then, the adjoint forward-backward SDEs (corresponding to ) are given by

where (resp. ) denotes the partial derivative of w.r.t. (resp. ). In view of (2.14), we get that

| (2.15) |

We next solve FBSDE (2.15) in terms of explicitly. To do this, it follows from (2.15) that

| (2.16) | ||||

Recall that is the filtration generated by the Brownian motion . Taking conditional expectations on both sides of (2.16) w.r.t. for , and using Lemma B.2 in Giesecke et al. (2015), we can deduce that

| (2.17) | ||||

Let us denote for . It follows from Itô’s lemma that

| (2.18) | ||||

where we have used the notation

To solve the FBSDE (2.15), we consider the ansatz that

| (2.19) |

where is a deterministic function of class , which satisfies the terminal condition . First, note that holds trivially. Applying Itô’s lemma to , we can obtain that

| (2.20) | ||||

Comparing the expressions of in (2.15) and (2.20), we have that

| (2.21) |

Let be a candidate optimal control that may depend on , and be the wealth process under . For the solution of FBSDE (2.15) with replaced by , we have from (2.14) that, for any ,

| (2.22) |

It can be observed from (2) that is linear in . It is then natural to make the coefficient of vanish, i.e., for ,

| (2.23) |

We first apply the relation in (2.21) to have that

| (2.24) |

Plugging (2.24) into (2.23), we get that the candidate best response satisfies the equation:

| (2.25) |

Next, we focus on a deterministic MFE and assume that is deterministic. Therefore, the condition (2.25) reduces to

| (2.26) |

As for in (2.3) is deterministic and bounded, by Lemma 2.1, we can easily get that, for , there exits a unique such that . Equivalently, for , we have that

| (2.27) |

where is a Lipschitz continuous function. We can easily verify that . This yields a best (deterministic) response control for . We observe that as the coefficients in (2.26) do not depend on (so is the function defined by (2.6)), is independent of . Hence, we can write as , i.e., for .

Next, we just need to solve the function in the ansatz solution (2.19) so that the adjoint processes are well defined. Comparing the drift term of (associated with ) in (2.15) and (2.20), we have that

| (2.28) | ||||

Plugging (2.19) and (2.24) into (2.28), we obtain that

| (2.29) |

with the terminal condition . We stress here that depends on for . We can then deduce that , where for is defined by (2.12), i.e.,

By solving the ODE problem (2), we have that

| (2.30) |

It then follows from (2.15) that the adjoint processes corresponding to can be rewritten by

| (2.31) |

where is the wealth process under .

Finally, using the consistency condition in Step 2 that with , we next derive the expression of . To this purpose, let us recall the process in (2.18) satisfies for , where is the wealth process under an arbitrary strategy . Then, we have that for and it follows that is given by (2.11). We therefore conclude that for is a deterministic MFE, which completes the proof. ∎

Remark 2.4.

We emphasize that the assumption with a constant limiting type vector is needed to guarantee the existence of a deterministic MFE strategy in Theorem 2.2 in the model with both common noise and contagious jump risk. We focus on a deterministic MFE strategy not only because it exhibits clean and interpretable analytical form, but it also crucially simplifies some future proofs to show the validity of a contructed approximate Nash equilibrium in the -player game and to analyze its explicit convergence rate.

3 Discussions of the Mean Field Equilibrium

We present in this section some quantitative properties and sensitivity results of the deterministic MFE strategy obtained in Theorem 2.2. First, Lemma 3.1 (proved in A) summarizes some monotonicity results on several model parameters.

Lemma 3.1.

For each fixed , let us use the notation to highlight the dependence of the deterministic MFE strategy on the model parameters . Then, we have that

-

(i)

is increasing;

-

(ii)

both and are decreasing;

-

(iii)

both and are decreasing.

Note that items (i) and (ii) in Lemma 3.1 are consistent with our intuition that the higher return and lower volatility in the limiting market model will incentivize the agent to invest more in the risky asset account in the mean field equilibrium strategy. When the representative agent is more risk averse, item (iii) implies that the representative agent becomes more conservative and invests less in the risky asset. It is also interesting to see that for , the mean field Nash equilibrium has no short-selling and a higher competition parameter leads to a lower investment proportion in the risky asset. That is, in the equilibrium state, a more competitive agent with the risk aversion will prefer to invest more in the riskless bond account. Here, we note that both and are parameters for the whole population (as all agents are symmetric in the mean field model). If the risk tolerance of the population is high with ( for all agents, when the whole population becomes more competitive as increases, the representative agent actually behaves less competitively in a highly competitive environment. This can be explained via a game theoretical thinking. Suppose other agents initially hold large long positions in the stock, there are essentially two strategies for the representative agent: She can also hold a large long position in the stock and hope to outperform other peers when the price goes up. However, as all peers are very competitive and allocate large amount of wealth into the stock, the chance to outperform others is actually slim because other peers may receive even higher wealth return. Or the representative agent can reduce her allocation in the stock and take advantage of the risk that the stock price may diffuse down or jump downward frequently such that her terminal wealth in riskless asset can significantly outperform other peers whose wealth drop due to default risk. If the representative agent can tolerate some risk and is highly concerned with the relative performance, she will adopt the second strategy, leading to the reduction of investment in the stock. Similarly, as all other peers are as competitive as the representative agent, all of them will also reduce the investment in the stock and aim to outperform others when the default jump occurs or the price goes down. Therefore, for , a higher actually leads to a lower equilibrium allocation in the stock in this mean field game.

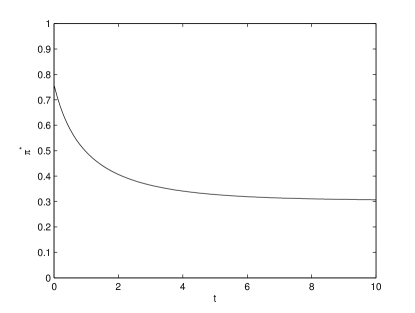

We next numerically illustrate the sensitivity results of with respect to jump risk parameters. We first note that the jump contagion effect among all stocks becomes negligible in the mean field model. However, the jump intensity process in the mean field model comes from the model with contagion effect in the -player game model. That is, the larger contagion effect among stocks in the -player model with larger and will lead to a larger jump intensity process in the mean field model. Therefore, our numerical examples can partially reflect how the contagion effect in the -player game affects the equilibrium behavior when there are infinitely many agents. Recall that the function is decreasing in by Lemma 2.1. Here, we take a differentiable and Lipschitz function such that when , while when for positive constants . It is also clear that the limiting intensity factor admitting the explicit form when (this can be achieved by taking appropriate parameter values listed in Table 1 together with large enough). In the following numerical simulation, we take and . It is increasing in time if and it is decreasing in time otherwise. Thanks to the analytical structure of , if model parameters satisfy that , the deterministic MFE strategy is decreasing in time indicating that the representative agent in the mean field game will reduce the portfolio in the risky asset as time evolves because of the increasing probability of the downward jump risk. To numerically illustrate this case, we choose parameters from Table 1 except the time variable . We then plot the function in Figure 1, which is shown to be a decreasing function of .

| Model Parameter | Financial Meaning | Value |

|---|---|---|

| is the upper bound of strategy | ||

| is the degree of relative risk aversion | ||

| competition weight | 0.5 | |

| limiting volatility of stock price | 0.3 | |

| common volatility | 0.2 | |

| return premium of stock | 0.2 | |

| initial default intensity | 0.1 | |

| long-term default intensity level | 0.6 | |

| adjustment speed of intensity toward long-term level | 0.5 | |

| limiting jump weight of default intensity | 0.4 | |

| limiting jump weight of default intensity | 0.2 | |

| the current time level | 3 |

With the parameter values given in Table 1, another interesting observation is that the limiting intensity process converges to a long-run steady level as tends to when the parameters satisfy . In this case, it follows from the explicit solution of that

| (3.1) |

Thus, using the continuity of (see Lemma 2.1), we can also derive the long-run behavior of the deterministic MFE (given the time horizon is sufficiently large) that

| (3.2) |

For the given parameters, it is observed from Figure 1 that this long run steady value of the deterministic MFE is approximately .

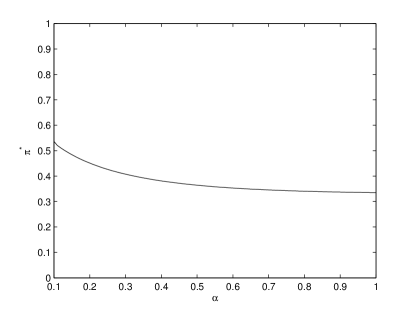

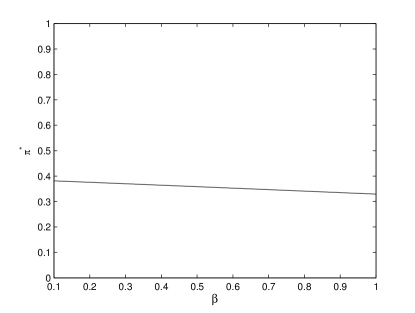

Let us then examine the sensitivity of the mean field equilibrium w.r.t. the mean recovery speed parameter in the mean field model. To this end, we choose and fix parameters as in Table 1 apart from the parameter , and plot the function of in terms of the parameter in Figure 2 on the interval . For the given , we can observe that the equilibrium is decreasing in the parameter . For the chosen parameters, it is easy to see that a larger leads to a larger default intensity of the risky asset. Consequently, to avoid the higher probability of default, the agent prefers to invest less in the risky asset account. Similarly, we plot in Figure 3 the mean filed equilibrium as a function in terms of the parameter from the intensity process . We choose and fix other parameters as in Table 1 apart from the parameter . For the given , the mean field equilibrium is decreasing in the parameter . We also note that and are symmetric in the definition of , the sensitivity result of the mean filed equilibrium w.r.t. the parameter is similar to the case w.r.t. the parameter . Again, from the definition of , one can see that the intensity value is increasing in terms of and . Therefore, as or increases, the agent invests less in the risky asset due to the higher probability of default.

4 Approximate Nash Equilibrium in the -Player Game

The goal of this section is to show that the mean field equilibrium obtained in Theorem 2.2 can help us to construct an approximate Nash equilibrium in the game with a sufficiently large but finite number of agents. Furthermore, the explicit order of the approximation error can also be derived, which will facilitate the practical implementations of the mean field approximation in finite population game applications.

Recall that the intensity process follows the dynamics that

| (4.1) |

with the speed parameter , the mean-reverting level , and the jump risk contagion effect parameter . To avoid the possible ambiguity in notation, we will keep the superscript in this section. Hereafter, denotes the state space of , which is a bounded set and is independent of since the jump rate function is bounded (c.f. (4.1)).

Next, before constructing an -Nash equilibrium in the -player game, we first introduce an auxiliary problem based on the limiting case, whose best response strategy will help us to construct an approximate Nash equilibrium. Let us define the auxiliary control problem ) by

| (4.2) |

subjecting to

| (4.3) |

Here, we recall that is the fixed point given by (2.11), is the deterministic MFE characterized by (2.9) in Theorem 2.2, and is a -martingale for . The following lemma characterizes the optimal strategy of the auxiliary control problem . The proof is reported in A.

Lemma 4.1.

Let for be the optimal (feedback) strategy of the auxiliary control problem . Then, we have that

| (4.4) |

where the function is defined by

| (4.5) |

and is the deterministic MFE given in Theorem 2.2. Moreover, there exists a pair independent of such that .

Intuitively, it can be seen from (4.4) in Lemma 4.1 that, as tends to infinity, the optimal feedback strategy converges to some , where satisfies . The following lemma characterizes the zero point of . The proof is similar to that of Lemma 2.1, and we hence omit it.

Lemma 4.2.

For the function defined by (4.5), we have that, for any , there exists a unique such that where is a pair of constants that are independent of . Moreover, there exists a unique continuous function such that

| (4.6) |

where also has a continuous partial derivative with respect to .

The above function in (4.6) also plays an important role in the construction of an approximating Nash equilibrium. More precisely, for , we consider a strategy of the agent that

| (4.7) |

where is given in (4.3). It follows from Lemma 4.2 that for some in view that is bounded. Then, the corresponding wealth process of agent under the strategy is governed by

| (4.8) |

Remark 4.3.

Comparing in (4.5) for the -player game and in (2.1) for the MFG, we note that the approximate Nash equilibrium in (4.7) is constructed specifically based on the analytical form of the mean field equilibrium when parameters in are modified to and the term is replaced by the term depending on the mean field equilibrium . That is, we propose a construction of based on the mean field equilibrium both implicitly (via the analytical form of in (2.1)) and explicitly (via the term in (4.5)).

We can now present the main result of this section, which gives the approximate Nash equilibrium for the -player game.

Theorem 4.4.

To prove Theorem 4.4, we first introduce the following auxiliary results, whose proofs are given in A.

Lemma 4.5.

Let the assumption hold. Then, we have that

- (i)

-

(ii)

Let for , and the mean field intensity be given by (2.3). We have that

(4.11) -

(iii)

Denote by the geometric mean wealth process at , where is defined in (4.8), and in the limiting model is obtained in Theorem 2.2. We have that, for all ,

(4.12)

Based on all previous preparations, we can give the proof of Theorem 4.4.

Proof of Theorem 4.4.

Recall that is defined by (4.8). For ease of presentation, let us denote

Here, satisfies the wealth dynamics (1.3) under the strategy . We recall the objective functional defined by (1.4). Then, we have that

Next, we proceed to prove (4.9) by using the introduced auxiliary problem in (4.2)-(4.3). Note that

| (4.13) |

For the first term of RHS of (4), we have that

For the term , we deduce that

Note that implies that . Using the inequality for all , we can derive that

We only give the detailed proof on the event , and skip similar arguments on the event . It follows from that

This yields that

For , let . Then . We have from the Hölder’s inequality and the estimate (4.10) in Lemma 4.5 that

| (4.14) |

where the constant is independent of . Thus we have that

| (4.15) |

Similarly, for the term , we can apply Hölder inequality and the estimate (4.12) in Lemma 4.5 to get that, for some constant independent of ,

| (4.16) | ||||

For the second term of r.h.s. of (4), we can follow similar argument in proving (4.16) to get that

| (4.17) |

We next claim that

| (4.18) |

where we recall the definition of in (4.7). It follows from (4.7) that, -a.s.

Recall that the best response solution of the auxiliary control problem () satisfies (4.4) in Lemma 4.1. Let and it holds that, -a.s.

| (4.19) |

For any , by Lemma 4.1, we have -a.s. that for constants , which are independent of . Using (4.19) and the mean value theorem, we arrive at

| (4.20) |

Building upon the estimate (4.20), we next focus on the proof of (4.18). In fact, by virtue of (4.3), it follows from Itô’s formula that, for any admissible strategy ,

| (4.21) |

with . This is equivalent to

Let us recall that, for ,

Therefore, for any , it holds that

| (4.22) |

with .

Let and be the wealth processes corresponding to the strategies and , respectively. Using the representation (4) with replaced by and respectively, we deduce that

| (4.23) |

After a straightforward calculation, the term can be further rewritten as:

| (4.24) |

Applying the Cauchy-Schwarz inequality to (4) results in

| (4.25) |

It follows from (4.10) in Lemma 4.5 that is bounded and the bound is independent of . Then, by (4), in order to verify (4.18), we need to show that

| (4.26) |

We introduce the density process satisfying the following SDE under the original probability measure that

| (4.27) |

In view that , the density process is in fact a martingale. We then define a probability measure by

| (4.28) |

Using the change of measure and (4.20), we obtain the existence of a constant independent of such that

Here, denotes the expectation operator under . This shows the validity of (4). It then follows from (4) and (4) that (4.18) holds. Combining (4.15)-(4.18), we can conclude the desired estimation that . Thus, we complete the proof of the theorem. ∎

5 Conclusions

This paper revisits the MFG and the -player game under CRRA relative performance by allowing risky assets to have contagious jumps, which are modelled by a multi-dimensional mutually exciting nonlinear Hawkes process. As a first attempt to such problems to accommodate controlled jumps, it is assumed for tractability in the present paper that the limiting model has constant parameters. By using the FBSDE and stochastic maximum principle arguments, a deterministic Nash equilibrium for the MFG can be characterized as a function of the deterministic limiting intensity process. Furthermore, using the information of the MFE, we are able to construct a good approximation of the Nash equilibrium for the large but finite population game and the order of the approximation error is explicitly obtained.

Based on our current study, some future research directions can be considered. First, it will be attractive to consider both -agent model and the limiting model with general random parameters. A deterministic mean field equilibrium may no longer exist. The existence of a mean field equilibria and the verification of an approximate Nash equilibrium for the -player game will require different mathematical arguments. Second, our work may pave the way to consider other sophisticated default intensity processes. For example, the default intensity of each risky asset may depend on the asset price itself or other stochastic factors. Some novel analysis for the mean field FBSDE with jumps are in demand to tackle the MFG problem.

Acknowledgements We sincerely thank two anonymous referees for their helpful comments on the presentation of this paper. L. Bo is supported by Natural Science Basic Research Program of Shaanxi (Program No. 2023-JC-JQ-05) and National Natural Science Foundation of China (Grant No. 11971368). S. Wang is supported by the Fundamental Research Funds for the Central Universities (Grant No. WK3470000024). X. Yu is supported by the Hong Kong Polytechnic University research (Grant No. P0031417 and No. P0039251).

References

- Bélanger et al. (2004) A. Bélanger, S. E. Shreve, and D. Wong (2004). A general framework for pricing credit risk. Math. Financ., 14(3), 317-350.

- Benazzoli et al. (2019) C. Benazzoli, L. Campi and L. Di Persio (2019): -Nash equilibrium in stochastic differential games with mean-field interaction and controlled jumps. Stat. Probab. Lett., 154, 108522.

- Benazzoli et al. (2020) C. Benazzoli, L. Campi and L. Di Persio (2020): Mean field games with controlled jump-diffusion dynamics: Existence results and an illiquid interbank market model. Stoch. Proc. Appl., 130, 6927-6964.

- Bensoussan et al. (2013) A. Bensoussan, J. Frehse and P. Yam (2013): Mean Filed Games and Mean Field Type Control Theory. Springer-Verlag, New York, 2013.

- Bielagk et al. (2017) J. Bielagk, A. Lionnet and G. Dos Reis (2017). Equilibrium pricing under relative performance concerns. SIAM J. Financ. Math., 8, 435-482.

- Bo et al. (2015) L. Bo and A. Capponi (2015): Systemic risk in interbanking networks. SIAM J. Finan. Math., 6(1), 386-424.

- Bo and Capponi (2018) L. Bo and A. Capponi (2018): Portfolio choice with market-credit risk dependencies. SIAM J. Control Optim., 56, 3050-3091.

- Bo et al. (2019a) L. Bo, A. Capponi and P. C. Chen (2019): Credit portfolio selection with decaying contagion intensities. Math. Financ., 29, 137-173.

- Bo et al. (2019b) L. Bo, H. Liao and X. Yu (2019): Risk sensitive portfolio optimization with default contagion and regime-switching. SIAM J. Control Optim., 57, 366-401.

- Bo et al. (2022) L. Bo, H. Liao and X. Yu (2022): Risk-sensitive credit portfolio optimization under partial information and contagion risk. Ann. Appl. Probab., 32(4), 2355-2399.

- Carmona (2016) R. Carmona (2016): Lectures on BSDEs, Stochastic Control, and Stochastic Differential Games with Financial Applications. Society for Industrial and Applied Mathematics, Philadelphia, PA, 2016.

- Carmona and Delarue (2018) R. Carmona and F. Delarue (2018): Probabilistic Theory of Mean Field Games with Applications I-II, Springer Nature, 2018.

- Chevallier (2017) J. Chevallier (2017): Mean-field limit of generalized Hawkes processes. Stoch. Process. Appl. 127(12), 3870-3912.

- Delong and Klüppelberg (2008) L. Delong and C. Klüppelberg (2008): Optimal investment and consumption in a Black-Scholes market with Lévy-driven stochastic coefficients. Ann. Appl. Probab. 18, 879-908.

- Dos Reis and Platonov (2021) G. Dos Reis and V. Platonov (2021): Forward utilities and mean-field games under relative performance concerns. In: Bernardin, C., Golse, F., Gonçalves, P., Ricci, V., Soares, A.J. (eds) From Particle Systems to Partial Differential Equations. ICPS ICPS ICPS 2019 2018 2017. Springer Proceedings in Math. Stats., vol. 352. Springer, Cham.

- Espinosa and Touzi (2015) G. E. Espinosa and N. Touzi (2015): Optimal investment under relative performance concerns. Math. Financ., 25(2), 221-257.

- Fu et al. (2020) G. Fu, X. Su and C. Zhou (2020): Mean field exponential utility game: A probabilistic approach. Preprint, available at arXiv:2006.07684.

- Giesecke et al. (2015) K. Giesecke, K. Spiliopoulos, R.B. Sowers and J.A. Sirignano (2015): Large portfolio asymptotics for loss from default. Math. Finance 25(1), 77-114.

- Gomes et al. (2013) D. A. Gomes, J. Mohr and R. R. Souza (2013): Continuous time finite state mean field games. Appl. Math. Optim., 68(1), 99-143.

- Guéant et al. (2011) O. Guéant, J. M. Lasry and P. L. Lions (2011): Mean Field Games and Applications. Paris-Princeton Lectures on Math. Finance 2010, 205-266.

- Hafayed et al. (2014) M. Hafayed, A. Abba and S. Abbas (2014): On mean-field stochastic maximum principle for near-optimal controls for Poisson jump diffusion with applications. Int. J. Dyn. Control, 2(3), 262-284.

- Hu and Zariphopoulou (2022) R. Hu and T. Zariphopoulou (2022): -player and mean-field games in Itô-diffusion markets with competitive or homophilous interaction. Stochastic Analysis, Filtering, and Stochastic Optimization, Edited by G. Yin and T. Zariphopoulou. pp. 209-237, Springer-Verlag, New York.

- Huang et al. (2006) M. Huang, R. Malhamé and P. E. Caines (2006): Large population stochastic dynamic games: closed-loop McKean-Vlasov systems and the Nash certainty equivalence principle. Commun. Inf. Syst., 6, 221-252.

- Jin et al. (2021) Z. Jin, H. Liao, Y. Yang and X. Yu (2021): Optimal dividend strategy for an insurance group with contagious default risk. Scand. Actuar. J., 2021(4), 335-361.

- Karatzas and Shreve (1991) I. Karatzas and S. E. Shreve (1991): Brownian Motion and Stochastic Calculus, 2nd Edition. Springer-Verlag, New York.

- Kraft et al. (2020) H. Kraft, A. Meyer-Wehmann and F. T. Seifried (2020): Dynamic asset allocation with relative wealth concerns in incomplete markets. J. Econ. Dyn. Control, 113, 103857.

- Lacker and Soret (2020) D. Lacker and A. Soret (2020): Many-player games of optimal consumption and investment under relative performance criteria. Math. Financ. Econ., 14, 263-281.

- Lacker and Zariphopoulou (2019) D. Lacker and T. Zariphopoulou (2019): Mean field and -agent games for optimal investment under relative performance criteria. Math. Financ., 29, 1003-1038.

- Lasry and Lions (2007) J. M. Lasry and P. L. Lions (2007): Mean field games. Jpn. J. Math., 2, 229-260.

- Löcherbach (2018) E. Löcherbach (2018): Spiking neurons: interacting hawkes processes, mean field limits and oscillations. ESAIM: Proceedings & Surveys 60, 90-103.

- Neumann (2020) B. A. Neumann (2020): Stationary equilibria of mean field games with finite state and action space. Dyn. Games Appl., 10, 845-871.

- Nutz and Zhang (2019) M. Nutz and Y. Zhang (2019): A mean field competition. Math. Opers. Res., 44, 1245-1263.

- Øksendal and Sulem-Bialobroda (2005) B. K. Øksendal and A. Sulem-Bialobroda (2005): Applied Stochastic Control of Jump Diffusions (Vol. 498). Springer-Verlag, Berlin.

- Shen and Siu (2013) Y. Shen and T. K. Siu (2013): The maximum principle for a jump-diffusion mean-field model and its application to the mean-variance problem. Nonlinear Anal. Theor., 86, 58-73.

- Shen and Zou (2020) Y. Shen and B. Zou (2020): Mean-variance portfolio selection in contagious markets. Preprint, available at www.researchgate.net/publication/340049920.

- Yu (2007) F. Yu (2007): Correlated defaults in intensity-based models. Math. Financ., 17, 155-173.

- Yu et al. (2021) X. Yu, Y. Zhang and Z. Zhou (2021): Teamwise mean field competitions. Appl. Math. Optim., 84, 903-942.

Appendix A Proofs of Some Auxiliary Results

Proof of Lemma 2.1.

Recall the definition of in (2.6). As , the partial derivative is given by, for ,

which implies that is monotonically decreasing with respect to . Note that and . It is deduced that there exists a unique such that , where the constant is small enough. Moreover, as for all , it follows from the implicit function theorem that, there exists a unique continuous function such that , and has a continuous partial derivative with respect to . We also note that

and for some constant independent of . The desired result follows that the function is decreasing in and is Lipschitz continuous with respect to . ∎

Proof of Lemma 3.1.

Note that the mean filed equilibrium in Theorem 2.2 is a positive deterministic function that for . For each fixed , by straightforward computations, we can derive the derivatives that

Thus, the claimed monotonicity results follow directly. ∎

Proof of Lemma 4.1.

Let be the admissible control set starting with any time . Then, we can define the value function of the auxiliary control problem given by, for ,

| (A.1) |

where for . The value function (A.1) is then associated with the HJB equation that

with the terminal condition . Here, denotes the -dimensional column vector whose -th entry is and remaining ones are . Let us consider the decoupled form that , where solves the following equation:

| (A.2) |

where the terminal condition is given by , and corresponds to the Hamiltonian operator that

| (A.3) |

It follows from Theorem 4.1 in Bo et al. (2019a) and Proposition 4.3 in Delong and Klüppelberg (2008) that (A) admits a unique (positive) classical solution. By applying the first-order condition to with respect to , we obtain that the optimum in Eq. (A) satisfies

| (A.4) |

By the assumption , it holds that

This yields the desired result (4.4).

It follows from the assumption and (4.4) that, there exist a constant independent of such that . Note that is continuous and decreasing, and . We get the existence of some independent of such that . We next prove that there exists a pair , which is independent of such that and . In fact, by the monotonicity of , it follows that

Thanks to the assumption , we have that

This yields that

Similarly, we also have that

It holds that . Therefore, we obtain that

which completes the proof. ∎

Proof of Lemma 4.5.

(i) By (4.7), we have that . Also recall that the wealth process satisfies (4.8). The conclusion clearly holds when . It suffices to prove the result when . By Itô formula, we have that

| (A.5) |

It follows that

| (A.6) |

Here, is defined by , where satisfies SDE under that

| (A.7) |

Note that both of and are bounded. The desired estimate (4.10) follows from (A).

(ii) Note that the mean field intensity factor process reduces to

| (A.8) |

and the intensity process takes the form that

| (A.9) |

It follows from (A.8) and (A.9) that

Applying Itô’s lemma, we obtain that

Taking the integral from to and then taking expectations on both sides, we arrive at

It follows from the Lipschitz continuity of that, there exists a constant independent of such that

By using Gronwall’s inequality, we conclude that

Applying Jensen inequality and the Lipschitz continuity property, it holds that

The desired claim (4.11) then holds.

(iii) Recall that where is defined by (4.8), and the geometric mean process satisfies (2.11). Let us define and

It follows from (4.8) that

| (A.10) |

We denote , which satisfies that

| (A.11) |

Note that

To prove the claim (4.12), by the boundedness of , it is sufficient to prove that, for any

| (A.12) |

To this end, for , we introduce the auxiliary SDE that

and

For some positive constants for satisfying , we can derive by generalized Hölder inequality that

| (A.13) | ||||

For the first term on the RHS of (A.13), we have that

For the second term on the RHS of (A.13), we have that

where is a positive constant independent of . By the assumption , we have that

For the third term on the RHS of (A.13), it holds that

We then claim that

| (A.14) |

Recall that in (4.7) satisfies the equation that

and given by Theorem 2.2 is the solution to

We introduce an auxiliary control , which satisfies

From the proof of Lemma 4.5-(ii) and the assumption , we have that as , and there exists a constant independent of such that

Moreover, the order of the term is the same to the order of because the function is Lipschitz continuous in , which proves that the claim (A.14) holds. Putting all the pieces together completes the proof. ∎

Appendix B Arguments to Derive in the Mean Field Model

Let us first recall that the default intensity process for agent satisfies SDE (1.2), for ,

| (B.1) |

where , , is a -martingale. For , recall that the type vector of the default intensity model is , and the space . We then define the following empirical measure-valued process on by

| (B.2) |

We next claim that, under the assumption , the mean field limit of the default intensity process satisfies that

| (B.3) |

where is the constant vector in the assumption for the mean field model. In fact, by applying Itô’s formula to an arbitrary (a test function that is w.r.t. ), we obtain

| (B.4) |

where for . It follows from mean value theorem that . Thus, we arrive at

| (B.5) |

We define for any . Then, Eq. (B) can be read as:

| (B.6) |

where we defined the operators for , for , and for . Let be the weak limit point of as . Then, the 4th term of RHS of Eq. (B) converges to as , a.s. On the other hand, as is a martingale, it follows from the martingale limit theorem that the martingale sequence converges to zero, as , a.s.. Hence, as , we have from Eq. (B) that the limit point satisfies

| (B.7) |

We next claim that for . In fact, it follow from Itô’s formula that

| (B.8) |

Note that, if , then and . Moreover, it holds that

Plugging the above equality into (B.8), we have that for indeed satisfies Eq. (B.7). Moreover, it follows from the uniqueness of Eq. (B.7) (c.f. Bo et al. (2015) by using martingale problem) that the limit point of is given by for . This yields that the mean field limit of described as (B.1) is given by in Eq. (B.3).