May2020 \degreefieldPh.D. \copyrightholderLiao Zhu

The Adaptive Multi-Factor Model and the Financial Market

Abstract

Modern evolvements of the technologies have been leading to a profound influence on the financial market. The introduction of constituents like Exchange-Traded Funds, and the wide-use of advanced technologies such as algorithmic trading, results in a boom of the data which provides more opportunities to reveal deeper insights. However, traditional statistical methods always suffer from the high-dimensional, high-correlation, and time-varying instinct of the financial data. In this dissertation, we focus on developing techniques to stress these difficulties. With the proposed methodologies, we can have more interpretable models, clearer explanations, and better predictions.

We start from proposing a new algorithm for the high-dimensional financial data – the Groupwise Interpretable Basis Selection (GIBS) algorithm, to estimate a new Adaptive Multi-Factor (AMF) asset pricing model, implied by the recently developed Generalized Arbitrage Pricing Theory, which relaxes the convention that the number of risk-factors is small. We first obtain an adaptive collection of basis assets and then simultaneously test which basis assets correspond to which securities. Since the collection of basis assets is large and highly correlated, high-dimension methods are used. The AMF model along with the GIBS algorithm is shown to have significantly better fitting and prediction power than the Fama-French 5-factor model.

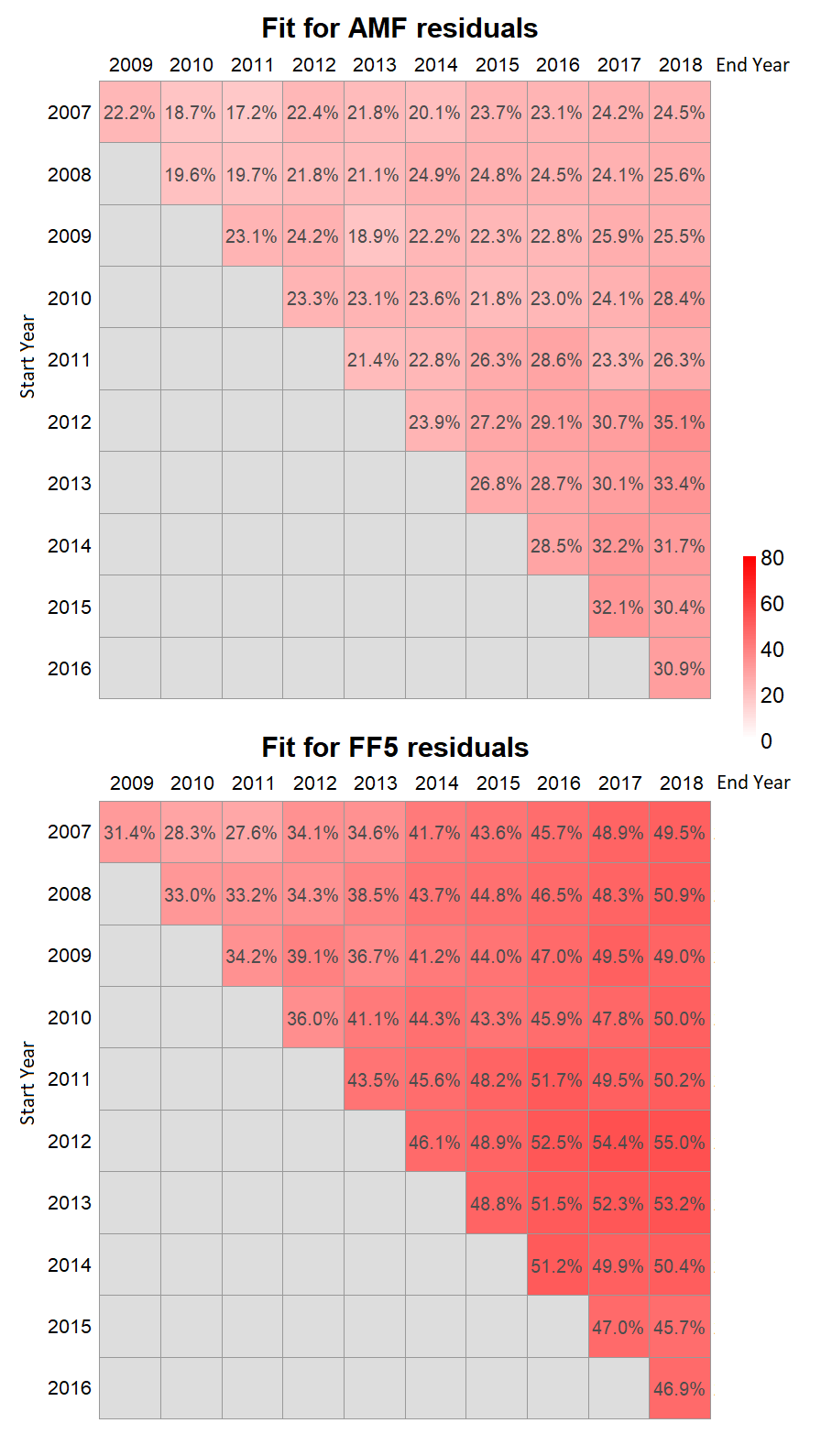

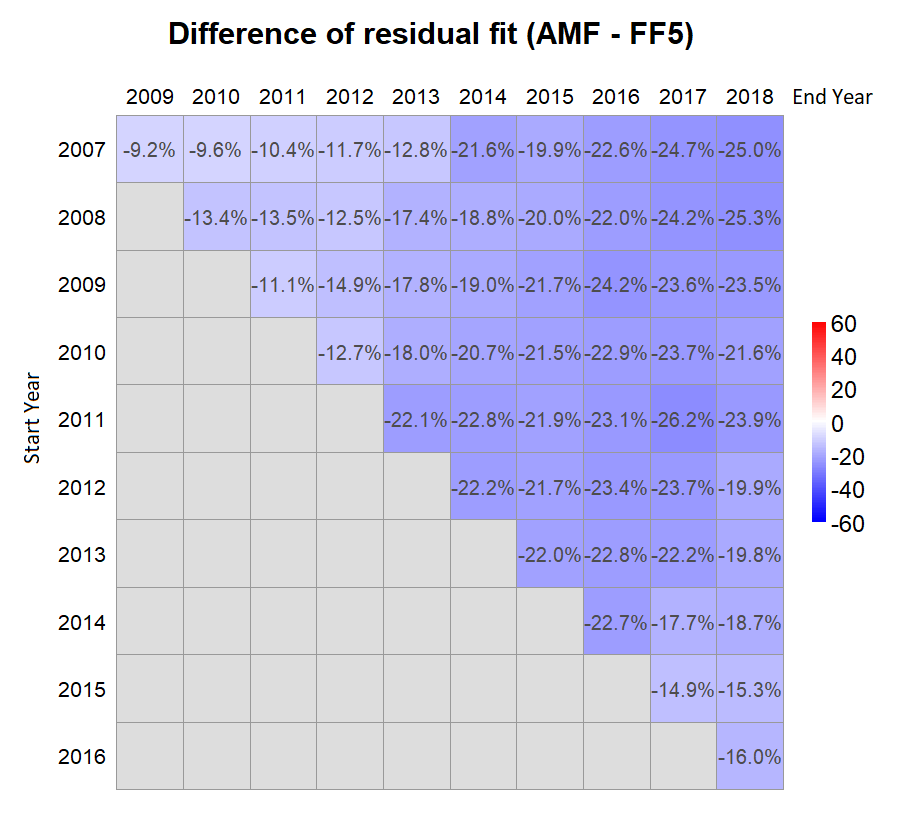

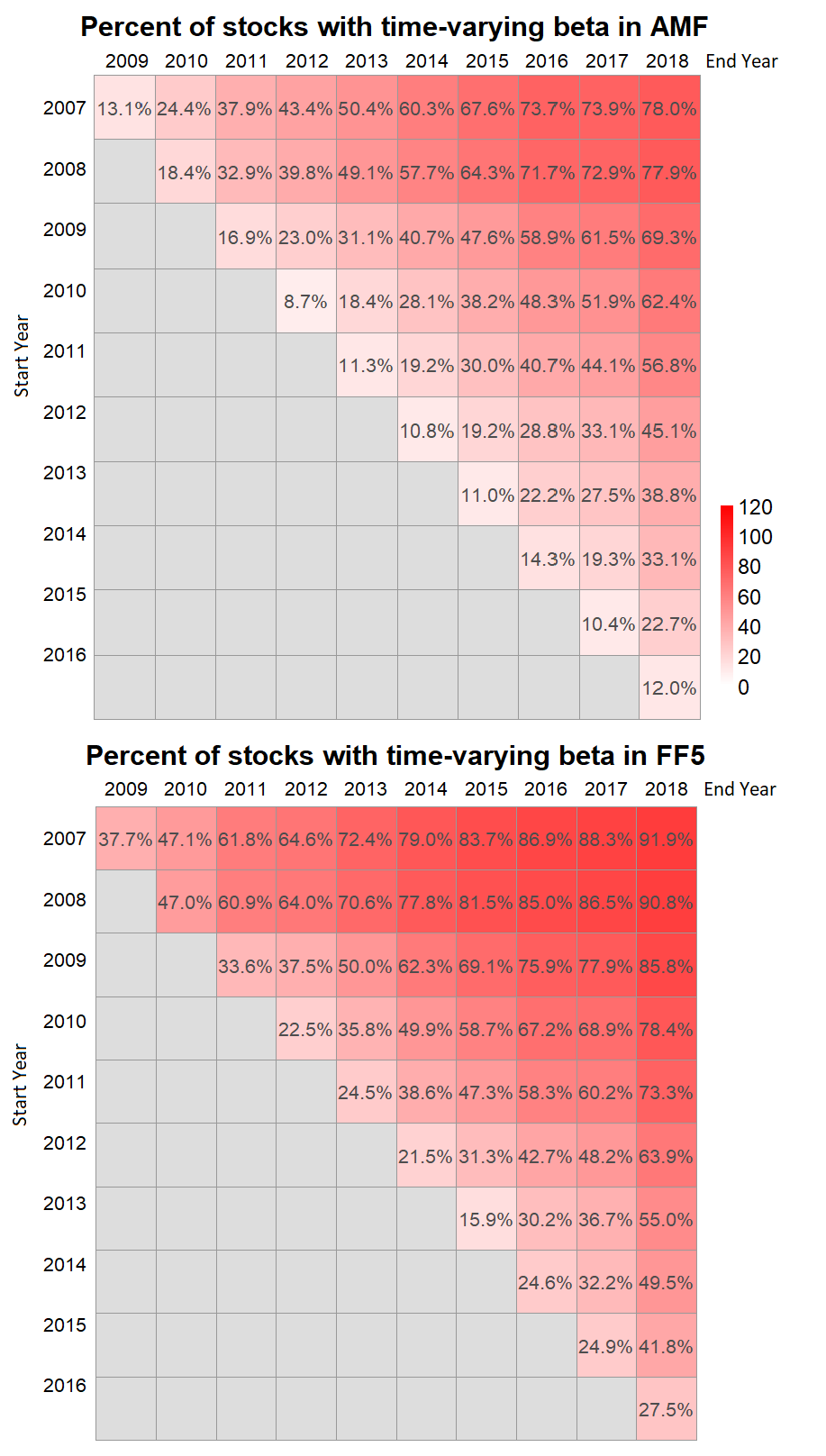

Next, we do the time-invariance tests for the ’s for both the AMF model and the FF5 in various time periods. We show that for nearly all time periods with length less than 6 years, the coefficients are time-invariant for the AMF model, but not the FF5 model. The coefficients are time-varying for both AMF and FF5 models for longer time periods. Therefore, using the dynamic AMF model with a decent rolling window (such as 5 years) is more powerful and stable than the FF5 model.

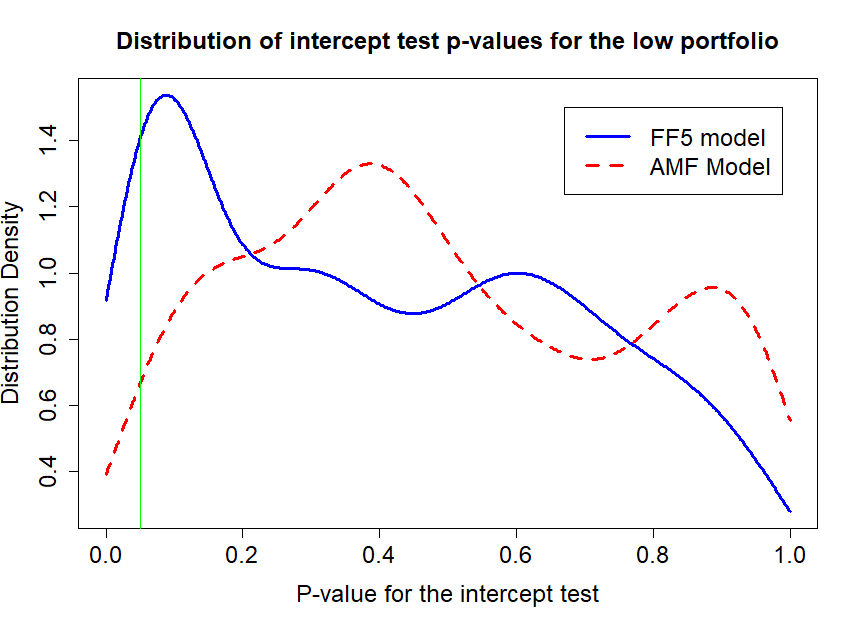

We also successfully provide a new explanation of the well-known low-volatility anomaly which pervades in the finance literature for a long time. We use the Adaptive Multi-Factor (AMF) model estimated by the Groupwise Interpretable Basis Selection (GIBS) algorithm to find those basis assets significantly related to low and high volatility portfolios. These two portfolios load on very different factors, which indicates that volatility is not an independent risk, but that it is related to existing risk factors. The out-performance of the low-volatility portfolio is due to the (equilibrium) performance of these loaded risk factors. For completeness, we compare the AMF model with the traditional Fama-French 5-factor (FF5) model, documenting the superior performance of the AMF model.

Liao Zhu is a Ph.D. in the Department of Statistics and Data Science, Cornell University. Before that he was in the School of Gifted Young, the University of Science and Technology of China, where he finished his B.S. degree majoring statistics in 2015.

This document is dedicated to all Cornell graduate students.

Acknowledgements.

I would like to thank my advisor - professor Martin Wells and my co-advisor - professor Robert Jarrow for their encouragements, insights and supports during my Ph.D. career. I am extremely grateful to their mentorship, which has a long-last influence to my life. I would also like to thank my committee members, professor David Mimno, David Matteson and David Ruppert for their generous support and advice. I would like to thank Dr. Manny Dong for helping with the data access. Thanks to my collaborators, professor Sumanta Basu, Dr. Rinald Murataj, etc. Thanks to my parents, my friends, and all the supports from Cornell University.Chapter 1 Introduction

Modern evolvements of the technologies have been leading to a profound influence on the financial market. The introduction of constituents like Exchange-Traded Funds, and the wide-use of advanced technologies such as algorithmic trading, results in a boom of the data which provides more opportunities to reveal deeper insights. However, traditional statistical methods always suffer from the high-dimensional, high-correlation, and time-varying instinct of the financial data. In this dissertation, we focus on developing techniques to stress these difficulties. With the proposed methodologies, we can have more interpretable models, clearer explanations, and better predictions.

We start from proposing a new algorithm for the high-dimensional

financial data, the Groupwise Interpretable Basis Selection (GIBS) algorithm to estimate a new Adaptive Multi-Factor (AMF) asset pricing model, implied by the generalized arbitrage pricing theory (APT) recently developed by Jarrow and Protter (2016) [35] and Jarrow (2016) [34]. 111The Appendix A provides a brief summary of the generalized APT. This generalized APT is derived in a continuous-time, continuous trading economy imposing only the assumptions of frictionless markets, competitive markets, and the existence of a martingale measure.222By results contained in Jarrow and Larsson (2012) [36], this is equivalent to the economy satisfying no free lunch with vanishing risk (NFLVR) and no dominance (ND). See Jarrow and Larrson (2012) [36] for the relevant definitions. As such, this generalized APT includes both Ross’s (1976) [54] static APT and Merton’s (1973) [50] inter-temporal CAPM as special cases.

Compared to PCA based methods that construct risk-factors from linear combinations of various stocks, which are consequently often difficult to interpret, our GIBS algorithm consists of a set of interpretable and tradeable basis assets. The new model explains more variation in realized returns. It is important to note here that in a model of realized returns, some of the basis assets will reflect idiosyncratic risks that do not earn a non-zero risk premium. Those basis assets that have non-zero excess expected returns are the relevant risk-factors identified in the traditional estimation methodologies. While a few recent papers adopt high-dimensional estimation methods for modeling the cross-section of expected returns and an associated parsimonious representation of the stochastic discount function [13, 21], our empirical test is specifically designed to align with the generalized APT model’s implications using basis assets and realized returns.

To test the generalized APT, we first obtain the collection of all possible basis assets. Then, we provide a simultaneous test, security by security, of which basis assets are significant for each security. However, there are several challenges that must be overcome to execute this estimation. First, in the security return regression using the basis assets as independent variables, due to the assumption that the regression coefficients (’s) are constant, it’s necessary to run the estimation over a small time window because the ’s are likely to change over longer time windows. This implies that the number of sample points may be less than the number of independent variables (). This is the so-called high-dimension regime, where the ordinary least squares (OLS) solution no longer holds. Second, the collection of basis assets selected for investigation will be highly correlated. And, it is well known that large correlation among independent variables causes difficulties (redundant basis assets selected, low fitting accuracy, etc., see [26, 63]) in applying the Least Absolute Shrinkage and Selection Operator (LASSO). To address these difficulties, we propose a novel and hybrid algorithm – the GIBS algorithm, for identifying basis assets that are different from the traditional variance-decomposition approach. The GIBS algorithm takes advantage of several high-dimensional methodologies, including prototype clustering, LASSO, and the “1se rule” for prediction.

We investigate Exchange-Traded Funds (ETFs) since they inherit and aggregate the basis assets from their constituents. In recent years there are more than one thousand ETFs, so it is reasonable to believe that one can obtain the basis assets from the collection of ETFs in the CRSP database, plus the Fama-French 5 factors. Consider the market return, one of the Fama-French 5 factors. It can be duplicated by ETFs such as the SPDR S&P 500 ETF, the Vanguard S&P 500 ETF, etc. Therefore, it is also reasonable to believe that the remaining ETFs can represent other basis assets as well. The AMF model along with the GIBS algorithm is shown to have significantly better fitting and prediction power than the Fama-French 5-factor model.

Next, we do the time-invariance tests for the ’s for both the AMF model and the FF5 in various time periods. The intercept (arbitrage) tests show that there are no significant non-zero intercepts in either AMF or FF5 model, which validates the 2 models. We show that the constant-beta assumption holds in the AMF model in all time periods with length less than 6 years and is quite robust regardless of the start year.

However, even for short time periods, FF5 sometimes gives very unstable estimation, especially in the financial crisis. This indicates that AMF is more insightful and can capture the risk-factors to explain the market shift during the financial crisis.

For time periods with length longer than 6 years, both AMF and FF5 fail to provide time-invariance ’s. However, the ’s estimate by the AMF is more time-invariant than the FF5 for nearly all time periods. This shows the superior performance of the AMF model.

Considering the two results above, using the dynamic AMF model with a decent rolling window (such as 5 years) is more powerful and stable than the FF5 model.

We also successfully provides a new explanation of the well-known low-volatility anomaly which pervades in the finance literature for a long time. The low-risk anomaly contradicts accepted APT or CAPM theories that higher risk portfolios earn higher returns. The low-risk anomaly is not a recent empirical finding but an observation documented by a a large body of literature dating back to the 1970s. Despite its longevity, the academic community differs over the causes of the anomaly. The two main explanations are: 1) it is due to leverage constraints that retail, pension and mutual fund investors face which limits their ability to generate higher returns by owning lower risk stocks, and 2) it is due to behavioral biases ranging from the lottery demand for high beta stocks, beating index benchmarks with a limit to arbitrage, and the sell-side analysts over-bias on high volatility stocks’ earnings.

In this paper, we study the low-volatility anomaly from a new perspective based on the Adaptive Multi-Factor (AMF) model proposed in the paper by Zhu et al. (2018) [69] using the recently developed Generalized Arbitrage Pricing Theory (see Jarrow and Protter (2016) [35]). In Zhu et al. (2018) [69], basis assets (formed from the collection of Exchange Traded Funds (ETF)) are used to capture risk factors in realized returns across securities. Since the collection of basis assets is large and highly correlated, high-dimension methods (including the LASSO and prototype clustering) are used. This paper employs the same methodology to investigate the low-volatility anomaly. We find that high-volatility and low-volatility portfolios load on different basis assets, which indicates that volatility is not an independent risk. The out-performance of the low-volatility portfolio is due to the (equilibrium) performance of these loaded risk factors. For completeness, we compare the AMF model with the traditional Fama-French 5-factor (FF5) model, documenting the superior performance of the AMF model.

Chapter 2 High Dimensional Estimation, Basis Assets, pand Adaptive Multi-Factor Models

2.1 Introduction

The purpose of this paper is to proposes a new algorithm for the high-dimensional

financial data, the Groupwise Interpretable Basis Selection (GIBS) algorithm to estimate a new Adaptive Multi-Factor (AMF) asset pricing model, implied by the generalized arbitrage pricing theory (APT) recently developed by Jarrow and Protter (2016) [35] and Jarrow (2016) [34]. 111The Appendix A provides a brief summary of the generalized APT. This generalized APT is derived in a continuous time, continuous trading economy imposing only the assumptions of frictionless markets, competitive markets, and the existence of a martingale measure.222By results contained in Jarrow and Larsson (2012) [36], this is equivalent to the economy satisfying no free lunch with vanishing risk (NFLVR) and no dominance (ND). See Jarrow and Larrson (2012) [36] for the relevant definitions. As such, this generalized APT includes both Ross’s (1976) [54] static APT and Merton’s (1973) [50] inter-temporal CAPM as special cases.

The generalized APT has four advantages over the traditional APT and the inter-temporal CAPM. First, it derives the same form of the empirical estimation equation (see Equation (2.13) below) using a weaker set of assumptions, which are more likely to be satisfied in practice.333The stronger assumptions in Ross’s APT are: (i) a realized return process consisting of a finite set of common factors and an idiosyncratic risk term across a countably infinite collection of assets, and (ii) no infinite asset portfolio arbitrage opportunities; in Merton’s ICAPM they are assumptions on (i) preferences, (ii) endowments, (ii) beliefs and information, and (iv) those necessary to guarantee the existence of a competitive equilibrium. None of these stronger assumptions are needed in Jarrow and Protter (2016) [35]. Second, the no-arbitrage relation is derived with respect to realized returns, and not with respect to expected returns. This implies, of course, that the error structure in the estimated multi-factor model is more likely to lead to a larger and to satisfy the standard assumptions required for regression models. Third, the set of basis assets and the implied risk-factors are tradeable under the generalized APT, implying their potential observability. Fourth, since the space of random variables generated by the uncertainty in the economy is infinite dimensional, the implied basis asset representation of any security’s return is parsimonious and sparse. Indeed, although the set of basis assets is quite large (possibly infinite dimensional), only a finite number of basis assets are needed to explain any assets’ realized return and different basis assets apply to different assets. This last insight is certainly consistent with intuition since an Asian company is probably subject to different risks than is a U.S. company. Finally, adding a non-zero alpha to the no-arbitrage relation in realized return space enables the identification of arbitrage opportunities. This last property is also satisfied by the traditional APT and the inter-temporal CAPM.

The generalized APT is important for practice because it provides an exact identification of the relevant set of basis assets characterizing a security’s realized (emphasis added) returns. This enables a more accurate risk-return decomposition facilitating its use in trading (identifying mispriced assets) and for risk management. Taking expectations of this realized return relation with respect to the martingale measure determines which basis assets are risk-factors, i.e. which basis assets have non-zero expected excess returns (risk premiums) and represent systematic risk. Since the traditional models are nested within the generalized APT, an empirical test of the generalized APT provides an alternative method for testing the traditional models as well. One of the most famous empirical representations of a multi-factor model is given by the Fama-French (2015) [20] five-factor model (FF5), see also [19, 18]. Recently, Harvey, Liu, and Zhu (2016) [25] reviewed the literature on the estimation of factor models, the collection of risk-factors employed, and argued for the need to use an alternative statistical methodology to sequentially test for new risk-factors. Our paper provides one such alternative methodology using the collection of basis assets to determine which of these earn risk premium.

Since the generalized APT is a model for realized returns that allows different basis assets to affect different stocks differently, an empirical test of this model starts with slightly different goals than tests of conventional asset pricing models (discussed above) whose implications are only with respect to expected returns and risk-factors. First, instead of searching for a few common risk-factors that affect the entire cross-section of expected returns, as in the conventional approach, we aim to find an exhaustive set of basis assets, while maintaining parsimony for each individual stock (and hopefully for the cross-section of stocks as well), using the GIBS algorithm we propose here. This alternative approach has the benefit of increasing the explained variation in our time series regressions. Second, as a direct implication of the estimated realized return relation, the cross-section of expected returns is uniquely determined. This implies, of course, that the collection of risk-factors will be those basis assets with non-zero expected excess returns (i.e. they earn non-zero risk premium).444An investigation of the cross-section of expected returns implied by the generalized APT model estimated in this paper is a fruitful area for future research.

In addition, compared to PCA based methods that construct risk-factors from linear combination of various stocks, which are consequently often difficult to interpret, our GIBS algorithm consists of a set of interpretable and tradeable basis assets. The new model explains more variation in realized returns. It is important to note here that in a model of realized returns, some of the basis assets will reflect idiosyncratic risks that do not earn non-zero risk premium. Those basis assets that have non-zero excess expected returns are the relevant risk-factors identified in the traditional estimation methodologies. While a few recent papers adopt high-dimensional estimation methods for modeling the cross-section of expected returns and an associated parsimonious representation of the stochastic discount function [13, 21], our empirical test is specifically designed to align with the generalized APT model’s implications using basis assets and realized returns.

To test the generalized APT, we first obtain the collection of all possible basis assets. Then, we provide a simultaneous test, security by security, of which basis assets are significant for each security. However, there are several challenges that must be overcome to execute this estimation. First, in the security return regression using the basis assets as independent variables, due to the assumption that the regression coefficients (’s) are constant, it’s necessary to run the estimation over a small time window because the ’s are likely to change over longer time windows. This implies that the number of sample points may be less than the number of independent variables (). This is the so-called high-dimension regime, where the ordinary least squares (OLS) solution no longer holds. Second, the collection of basis assets selected for investigation will be highly correlated. And, it is well known that large correlation among independent variables causes difficulties (redundant basis assets selected, low fitting accuracy etc., see [26, 63]) in applying the Least Absolute Shrinkage and Selection Operator (LASSO). To address these difficulties, we propose a novel and hybrid algorithm – the GIBS algorithm, for identifying basis assets which are different from the traditional variance-decomposition approach. The GIBS algorithm takes advantage of several high-dimensional methodologies, including prototype clustering, LASSO, and the “1se rule” for prediction.

We investigate Exchange-Traded Funds (ETFs) since they inherit and aggregate the basis assets from their constituents. In recent years there are more than one thousand ETFs, so it is reasonable to believe that one can obtain the basis assets from the collection of ETFs in the CRSP database, plus the Fama-French 5 factors. Consider the market return, one of the Fama-French 5 factors. It can be duplicated by ETFs such as the SPDR S&P 500 ETF, the Vanguard S&P 500 ETF, etc. Therefore, it is also reasonable to believe that the remaining ETFs can represent other basis assets as well.

We group the ETFs into different asset classes and use prototype clustering to find good representatives within each class that have low pairwise correlations. This reduced set of ETFs forms our potential basis assets. After finding this set of basis assets, we still have more basis assets than observations (), but the basis assets are no longer highly correlated. This makes LASSO an appropriate approach to determine which set of basis assets are important for a security’s return. To be consistent with the literature, we fit an OLS regression on each security’s return with respect to its basis assets (that are selected by LASSO) to perform an intercept () and a goodness of fit test. The importance of these tests are discussed next.

As noted above, the intercept test can be interpreted as a test of the generalized APT under the assumptions of frictionless, competitive, and arbitrage-free markets (more formally, the existence of an equivalent martingale measure). The generalized APT abstracts from market microstructure frictions, such as bid-ask spreads and execution speeds (costs), and strategic trading considerations, such as high-frequency trading. To be consistent with this abstraction, we study returns over a weekly time interval, where the market microstructure frictions and strategic trading considerations are arguably less relevant. Because the generalized APT ignores market microstructure considerations, we label it a “large-time scale” model.

If we fail to reject a zero alpha, we accept this abstraction, thereby providing support for the assertion that the frictionless, competitive, and arbitrage-free market construct is a good representation for “large time scale” security returns. If the model is accepted, a goodness of fit test quantifies the explanatory power of the model relative to the actual time series variations in security returns. A “good” model is one where the model error (the difference between the model’s predictions and actual returns) behaves like white noise with a “small” variance. The adjusted provides a good metric of comparison in this regard. Conversely, if we reject a zero alpha, then this is evidence consistent with either: (i) that microstructure considerations are necessary to understand “large time scale” models, or (ii) that there exist arbitrage opportunities in the market. This second possibility is consistent with the generalized APT being a valid description of reality, but where markets are inefficient. To distinguish between these two alternatives, we note that a non-zero intercept enables the identification of these “alleged” arbitrage opportunities, constructed by forming trading strategies to exploit the existence of these “positive alphas”. The implementation of these trading strategies enables a test between these two alternatives.

Here is a brief summary of our results.

-

•

The AMF model gives fewer significant intercepts (alphas) as compared to the Fama-French 5-factor model (percentage of companies with non-zero intercepts from 6.22% to 3.86% ). For both models, considering the False Discovery Rate, we cannot reject the hypothesis that the intercept is zero for all securities in the sample. This implies that historical security returns are consistent with the behavior implied by “large-time scale” models.

-

•

In an Goodness-of-Fit test comparing the Fama-French 5-factor and the AMF model, the AMF model has a substantially larger In-Sample Adjusted and the difference of goodness-of-fit of two models are significant. Furthermore, the AMF model increased the Out-of-Sample for the prediction by . This supports the superior performance of the generalized APT in characterizing security returns.

-

•

As a robustness test, for those securities whose intercepts were non-zero (although insignificant), we tested the AMF model to see if positive alpha trading strategies generate arbitrage opportunities. They do not, thereby confirming the validity of the generalized APT.

-

•

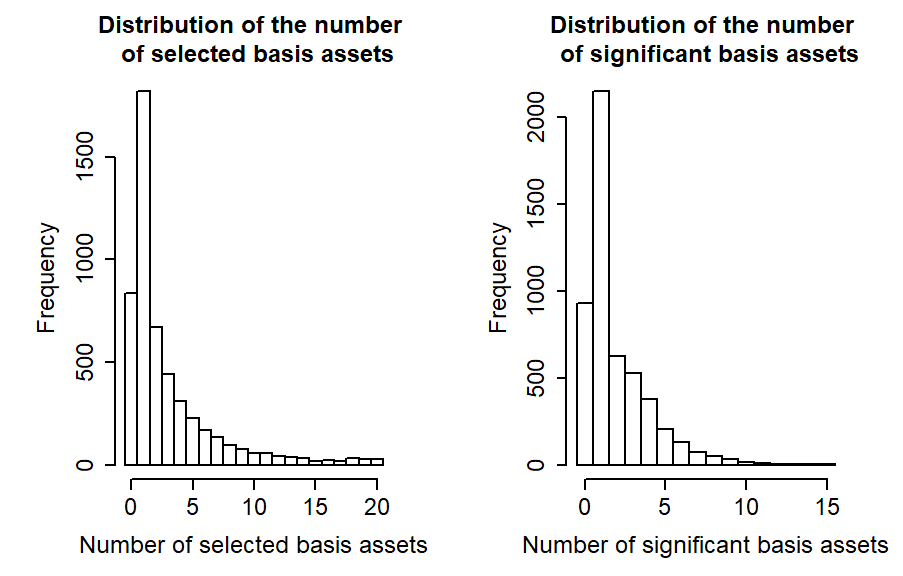

The estimated GIBS algorithm selects 182 basis assets for the AMF model. All of these basis assets are significant for some stock, implying that a large number of basis assets are needed to explain security returns. On average each stock is related to only 2.98 basis assets, with most stocks having between significant basis assets. Cross-validation results in the Section 2.6 are consistent with our sparsity assumption. Furthermore, different securities are related to different basis assets, which can be seen in Table 2.2 and the Heat Map in Figure 2.2. Again, these observations support the validity of the generalized APT.

-

•

To identify which of the basis assets are risk-factors, we compute the average excess returns on the relevant basis assets over the sample period. These show that 77.47% of the basis assets are risk-factors, earning significant risk premium.

-

•

Comparison of GIBS with the alternative methods discussed in Section 2.6 shows the superior performance of GIBS. The comparison between GIBS and GIBS + FF5 shows that some of the FF5 factors are overfitting noise in the data.

More recently, insightful papers by Kozak, Nagel, and Santosh (2017, 2018) [45, 44] proposed alternative methods for analyzing risk-factors models. As Kozak et al. (2018) [45] note, if the “risk-factors” are considered as a variance decomposition for a large amount of stocks, one can always find that the number of important principal components is small. However, this may not imply that there are only a small number of relevant risk-factors because the Principal Component Analysis (PCA) can either mix the underlying risk-factors together or separate them into several principal components. It may be that there are a large number of risk-factors, but the ensemble appears in only a few principal components. The sparse PCA method used in [45] removes many of the weaknesses of traditional PCA, and even gives an interpretation of the risk-factors as stochastic discount risk-factors. However all these methods still suffer from the problems (low interpretability, low prediction accuracy, etc.) inherited from the variance decomposition framework. An alternative approach, the one we use here, is to abandon variance decomposition methods and to use high-dimensional methods instead, such as prototype clustering to select basis assets as the “prototypes” or “center” of the groups they are representing. The proposed GIBS method gives much clearer interpretation, and much better prediction accuracy.

A detailed comparison of alternative methods that address the difficulties of high-dimension and strong correlation id given in Section 2.6 below. Other methods include Elastic Net or Ridge Regression to deal with the correlation. Elastic Net and Ridge Regression handle multicollinearity by adding penalties to make the relevant matrix invertible. However, neither of these methods considers the underlying cluster structure, which makes it hard to interpret the selected basis assets. This is the reason for the necessity of prototype clustering in the first step, since it gives an interpretation of the selected basis assets as the “prototypes” or the “centers” of the groups they are representing. After the prototype clustering, we use a modified version of LASSO (use in the GIBS algorithm) instead of either Elastic Nets or Ridge Regression. The reason is that, compared to GIBS, alternative methods achieve a much lower prediction goodness-of-fit (see Table 2.5), but select more basis assets (see Figure 2.7), which overfits and makes the model less interpretable.

The tuning parameter that controls sparsity in LASSO, , is traditionally selected by cross-validation and with this , the model selects an average of 15.66 basis assets for each company. However, as shown in the comparison Section 2.6, this overfits the noise in the data when compared with the GIBS algorithm with respect to Out-of-Sample . The reasons for the poor performance of this cross-validation is discussed in Section 2.6 below. Consequently, to control against overfitting, we use the “1se rule” along with the threshold that the number of basis assets can not exceed 20.

The Adaptive Multi-Factor (AMF) model estimated by the GIBS algorithm in this paper is shown to be consistent with the data and superior to the Fama-French 5-factor model. An outline of this paper is as follows. Section 2.2 describes the high-dimensional statistical methods used in this paper and Section 2.3 presents the Adaptive Multi-Factor (AMF) model to be estimated. Section 2.4 gives the proposed GIBS algorithm to estimate the model and Section 2.5 presents the empirical results. Section 2.6 discusses the reason we chose our method and provide a detailed comparison over alternative methods. Section 2.7 discusses the risk premium of basis assets and Section 2.8 presents some illustrative examples. Section 2.9 concludes. All codes are written in R and are available upon request.

2.2 High-Dimensional Statistical Methodology

Since high-dimensional statistics is relatively new to the finance literature, this section reviews the relevant statistical methodology.

2.2.1 Preliminaries and Notations

Let denote the standard norm of a vector of dimension , i.e.

Suppose is also a vector with dimension , a set , then is a vector with i-th element

Here the index set is called the support of , in other words, . Similarly, if is a matrix instead of a vector, for any index set , use to denote the the columns of indexed by . Denote as a vector with all elements being 1, and . denotes the identity matrix with diagonal 1 and 0 elsewhere. The subscript is always omitted when the dimension is clear from the context. The notation means the number of elements in the set .

2.2.2 Minimax Prototype Clustering and Lasso Regressions

This section describes the prototype clustering to be used to deal with the problem of high correlation among the independent variables in our LASSO regressions. To remove unnecessary independent variables, using clustering methods, we classify them into similar groups and then choose representatives from each group with small pairwise correlations. First, we define a distance metric to measure the similarity between points (in our case, the returns of the independent variables). Here, the distance metric is related to the correlation of the two points, i.e.

| (2.1) |

where is the time series vector for independent variable and is their correlation. Second, the distance between two clusters needs to be defined. Once a cluster distance is defined, hierarchical clustering methods (see [42]) can be used to organize the data into trees.

In these trees, each leaf corresponds to one of the original data

points.

Agglomerative hierarchical clustering algorithms build trees

in a bottom-up

approach, initializing each cluster as a single point,

then merging the two closest clusters at each successive stage. This

merging is repeated until only one cluster remains. Traditionally,

the distance between two clusters is defined as either a complete

distance, single distance, average distance, or centroid distance.

However, all of these approaches suffer from interpretation difficulties

and inversions (which means parent nodes can sometimes have a lower

distance than their children), see Bien, Tibshirani (2011)[9].

To avoid these difficulties, Bien, Tibshirani (2011)[9]

introduced hierarchical clustering with prototypes via a minimax linkage

measure, defined as follows. For any point and cluster ,

let

| (2.2) |

be the distance to the farthest point in from . Define the minimax radius of the cluster as

| (2.3) |

that is, this measures the distance from the farthest point which is as close as possible to all the other elements in C. We call the minimizing point the prototype for . Intuitively, it is the point at the center of this cluster. The minimax linkage between two clusters and is then defined as

| (2.4) |

Using this approach, we can easily find a good representative for each cluster, which is the prototype defined above. It is important to note that minimax linkage trees do not have inversions. Also, in our application as described below, to guarantee interpretable and tractability, using a single representative independent variable is better than using other approaches (for example, principal components analysis (PCA)) which employ linear combinations of the independent variables.

The LASSO method was introduced by Tibshirani (1996) [59] for model selection when the number of independent variables () is larger than the number of sample observations (). The method is based on the idea that instead of minimizing the squared loss to derive the Ordinary Least Squares (OLS) solution for a regression, we should add to the loss a penalty on the absolute value of the coefficients to minimize the absolute value of the non-zero coefficients selected. To illustrate the procedure, suppose that we have a linear model

| (2.5) |

is an matrix, and are vectors, and is a vector.

The LASSO estimator of is given by

| (2.6) |

where is the tuning parameter, which determines the magnitude of the penalty on the absolute value of non-zero ’s. In this paper, we use the R package glmnet [23] to fit LASSO.

In the subsequent estimation, we will only use a modified version of LASSO as a model selection method to find the collection of important independent variables. After the relevant basis assets are selected, we use a standard Ordinary Least Squares (OLS) regression on these variables to test for the goodness of fit and significance of the coefficients. More discussion of this approach can be found in Zhao, Shojaie, Witten (2017) [67].

2.3 The Adaptive Multi-Factor Model

This section presents the Adaptive Multi-Factor (AMF) asset pricing model that is estimated using the high-dimensional statistical methods just discussed. Given is a frictionless, competitive, and arbitrage free market. In this setting, a dynamic generalization of Ross’s (1976) [54] APT and Merton’s (1973) [50] ICAPM derived by Jarrow and Protter (2016) [35] implies that the following relation holds for any security’s realized return:

| (2.7) |

where at time , denotes the return of the i-th security for (where is the number of securities), denotes the return used as the j-th basis asset for , is the risk free rate, denotes the vector of security returns, is a column vector with every element equal to one, and .

This generalized APT requires that the basis assets are represented by traded assets. In Jarrow and Protter (2016) [35] the collection of basis assets form an algebraic basis that spans the set of security payoffs at the model’s horizon, time . No arbitrage, i.e. the existence of a martingale measure, implies that this same basis set applies to the returns over intermediate time periods , which yields the basis asset risk-return relation given in Equation (2.7). It is important to emphasize that this no-arbitrage relation is for realized returns, not expected returns. Realized returns are the objects to which asset pricing estimation is applied. Secondly, the no-arbitrage relation requires the additional assumptions of frictionless and competitive markets. Consequently, this asset pricing model abstracts from market micro-structure considerations. For this reason, this model structure is constructed to understand security returns over larger time intervals (days or weeks) and not intra-day time intervals where market micro-structure considerations apply.

Consistent with this formulation, we use traded ETFs for the basis assets. In addition, to apply the LASSO method, for each security we assume that only a small number of the coefficients are non-zero ( has the sparsity property). Lastly, to facilitate estimation, we also assume that the coefficients are constant over time, i.e. . This assumption is an added restriction, not implied by the theory. It is only a reasonable approximation if the time period used in our estimation is not too long (we will return to this issue subsequently).

To empirically test our model, both an intercept and a noise term are added to Equation (2.7), that is,

| (2.8) |

where and .

The error term is included to account for noise in the data and “random” model error, i.e. model error that is unbiased and inexplicable according to the independent variables included within the theory. If our theory is useful in explaining security returns, this error should be small and the adjusted large. The intercept is called Jensen’s alpha. Using the recent theoretical insights of Jarrow and Protter (2016) [35], the intercept test can be interpreted as a test of the generalized APT under the assumptions of frictionless, competitive, and arbitrage-free markets (more formally, the existence of an equivalent martingale measure). As noted above, this approach abstracts from market microstructure frictions, such as bid-ask spreads and execution speeds (costs), and strategic trading considerations, such as high-frequency trading. To be consistent with this abstraction, we study returns over a weekly time interval, where the market microstructure frictions and strategic trading considerations are arguably less relevant. If we fail to reject a zero alpha, we accept this abstraction, thereby providing support for the assertion that the frictionless, competitive, and arbitrage-free market construct is a good representation of “large time scale” security returns. If the model is accepted, a goodness of fit test quantifies the explanatory power of the model relative to the actual time series variations in security returns. The adjusted provides a good test in this regard. The GRS test in [24] is usually an excellent procedure for testing intercepts but it is not appropriate in the LASSO regression setting.

Conversely, if we reject a zero alpha, then this is evidence consistent with either: (i) that microstructure considerations are necessary to understand “large time scale” as well as “short time scale” returns or (ii) that there exist arbitrage opportunities in the market. This second possibility is consistent with the generalized APT being a valid description of reality, but where markets are inefficient. To distinguish between these two alternatives, we note that a non-zero intercept enables the identification of these “alleged” arbitrage opportunities, constructed by forming trading strategies to exploit the existence of these “positive alphas.”

Using weekly returns over a short time period necessitates the use of high-dimensional statistics. To understand why, consider the following. For a given time period , letting , we can rewrite Equation (2.8) using time series vectors as

| (2.9) |

where , and

| (2.10) |

| (2.11) |

| (2.12) |

Recall that we assume that the coefficients are constants. This assumption is only reasonable when the time period is small, say three years, so the number of observations given we employ weekly data. Therefore, our sample size in this regression is substantially less than the number of basis assets .

We fit the GIBS algorithm to select the basis assets set ( is derived near the end). Then, the model becomes

| (2.13) |

Here, the intercept and the significance of each basis asset can be tested, making the identifications and in Equation (2.5). Goodness of fit tests, comparisons of the in-sample adjusted , and prediction out-of-sample [14] can be employed.

An example of Equation (2.13) is the Fama-French (2015) [20] five-factor model where all of the basis assets are risk-factors, earning non-zero expected excess returns. Here, the five traded risk-factors are: (i) the market portfolio less the spot rate of interest (), (ii) a portfolio representing the performance of small (market capital) versus big (market capital) companies (), (iii) a portfolio representing the performance of high book-to-market ratio versus small book-to-market ratio companies (), (iv) a portfolio representing the performance of robust (high) profit companies versus that of weak (low) profits (), and (v) a portfolio representing the performance of firms investing conservatively and those investing aggressively (), i.e.

| (2.14) |

The key difference between the Fama-French five-factor and Equation (2.13) is that Equation (2.13) allows distinct securities to be related to different basis assets, many of which may not be risk-factors, chosen from a larger set of basis assets than just these five. In fact, we allow the number of basis assets to be quite large (e.g. over one thousand), which enables the number of non-zero coefficients to be different for different securities. As noted above, we also assume the coefficient vector to be sparse. The traditional literature, which includes the Fama-French five-factor model, limits the regression to a small number of risk-factors. In contrast, using the LASSO method, we are able to fit our model using time series data when , as long as the coefficients are sparse and the basis assets are not highly correlated. As noted previously, we handle this second issue via clustering methods.

2.4 The Estimation Procedure (GIBS algorithm)

This section discusses the estimation procedure for the basis asset implied Adaptive Multi-Factor (AMF) model. To overcome the high-dimension and high-correlation difficulties, we propose a Groupwise Interpretable Basis Selection (GIBS) algorithm to empirically estimate the AMF model. The details are given in this section, and the sketch of the GIBS algorithm is shown in Table 2.1 at the end of this section.

The data consists of security returns and all the ETFs available in the CRSP database over the three year time period from January 2014 to December 2016. The same approach can be used in other time periods as well. However, in earlier time periods, there were less ETFs. In addition, in the collection of basis assets we include the five Fama-French factors. A security is included in our sample only if it has prices available for more than 80% of all the trading weeks. For easy comparison, companies are classified according to the first 2 digits of their SIC code (a detailed description of SIC code classes can be found in Appendix B).

Suppose that we are given tradable basis assets . In our investigation, these are returns on traded ETFs, and for comparison to the literature, the Fama-French 5 factors. Using recent year data, the number of ETFs is large, slightly over 1000 (). Since these basis assets are highly-correlated, it is problematic to fit directly on these basis assets using a LASSO regression. Hence, we use the Prototype Clustering method discussed in Section 2.2.2 to reduce the number of basis assets by selecting low-correlated representatives. Then, we fit a modified version of the LASSO regression to these low-correlated representatives. This improves the fitting accuracy and also selects a sparser and more interpretable model.

For notation simplicity, denote

| (2.15) |

where the definition of are in equation (2.9 - 2.12). Let denote the market return. It is easy to check that most of the ETF basis assets are correlated with (the market return minus the risk free rate). We note that this pattern is not true for the other four Fama-French factors. Therefore, we first orthogonalize every other basis asset to before doing the clustering and the LASSO regression. By orthogonalizing with respect to the market return, we apvoid choosing redundant basis assets similar to it and meanwhile, increase the accuracy of fitting. Note that for OLS, projection does not affect the estimation since it only affects the coefficients, not the estimated . However, in the LASSO, projection does affect the set of selected basis assets because it changes the magnitude of shrinking. Thus, we compute

| (2.16) |

where denotes the projection operator. Denote the vector

| (2.17) |

Note that this is equivalent to the residuals after regressing other basis assets on the market return minus the risk free rate.

The transformed ETF basis assets contain highly correlated members. We first divide these basis assets into categories based on their financial interpretation. Note that . The list of categories with more descriptions can be found in Appendix C. The categories are (1) bond/fixed income, (2) commodity, (3) currency, (4) diversified portfolio, (5) equity, (6) alternative ETFs, (7) inverse, (8) leveraged, (9) real estate, and (10) volatility.

Next, from each category we need to choose a set of representatives. These representatives should span the categories they are from, but also have low correlation with each other. This can be done by using the prototype-clustering method with distance defined by equation (2.1), which yield the “prototypes” (representatives) within each cluster (intuitively, the prototype is at the center of each cluster) with low-correlations.

Within each category, we use the prototype clustering methods previously discussed to find the set of representatives. The number of representatives in each category can be decided according to a correlation threshold. (Alternatively, we can also use the PCA dimension or other parameter tuning methods to decide the number of prototypes. Note that even if we use the PCA dimension to suggest the number of prototypes to keep, the GIBS algorithm does not use any linear combinations of factors as PCA does). This gives the sets with for . Denote . Although this reduction procedure guarantees low-correlation between the elements in each , it does not guarantee low-correlation across the elements in the union . So, an additional step is needed, which is prototype clustering on to find a low-correlated representatives set . Note that . Denote . The list of all ETFs in the set is given in Appendix D Table LABEL:tab:_amf_etf_representatives. This is still a large set with .

Recall from the notation Section 2.2.1 that means the columns of the matrix indexed by the set . Since basis assets in are not highly correlated, a LASSO regression can be applied. By equation (2.6), we have that

| (2.18) |

where denotes the complement of . However, here we use a different compared to the traditional LASSO. Normally the of LASSO is selected by the cross-validation. However this will overfit the data as discussed in Section 2.6. So here we use a modified version of the select rule and set

| (2.19) |

where is the selected by the “1se rule”. The “1se rule” gives the most regularized model such that error is within one standard error of the minimum error achieved by the cross-validation (see [23, 56, 60]). Further discussion of the choice of can be found in Section 2.6.

Therefore we can derive the the set of basis assets selected as

| (2.20) |

Next, we fit an Ordinary Least Squares (OLS) regression on the selected basis assets. Since this is an OLS regression, we use the original basis assets rather than the orthogonalized basis assets with respect to the market return . In this way, we construct the set of basis assets .

Note that here we can also add the Fama-French 5 factors into if not selected, which will be also discussed in Section 2.6 as the GIBS + FF5 model. This is included to compare our results with the literature. However, the comparison results between the GIBS and the GIBS + FF5 model in Section 2.6 show that adding back Fama-French 5 factors into results in overfitting and should be avoided. Hence, the GIBS algorithm emplyed herein doesn’t include the Fama-French 5 factors if they are not selected in the procedure above.

The following OLS regression is used to estimate , the OLS estimator of in

| (2.21) |

Note that . The adjusted is obtained from this estimation. Since we are in the OLS regime, significance tests can be performed on . This yields the significant set of coefficients

| (2.22) |

Note that the significant basis asset set is a subset of the selected basis asset set. In another word,

| (2.23) |

To sum up, the sketch of the GIBS algorithm is shown in Table 2.1. Recall from the notation Section 2.2.1 that for an index set , means the columns of the matrix indexed by the set .

| The Groupwise Interpretable Basis Selection (GIBS) algorithm |

|---|

| Inputs: Stocks to fit and basis assets . |

| 1. Derive using and the equation (2.16, 2.17). |

| 2. Divide the transformed basis assets into k groups by a |

| financial interpretation. |

| 3. Within each group, use prototype clustering to find prototypes . |

| 4. Let , use prototype clustering in B to find prototypes . |

| 5. For each stock , use a modified version of LASSO to reduce |

| to the selected basis assets |

| 6. For each stock , fit linear regression on . |

| Outputs: Selected factors , significant factors , and coefficients in step 6. |

It is also important to understand which basis assets affect which securities. Given the set of securities is quite large, it is more reasonable to study which classes of basis assets affect which classes of securities. The classes of basis assets are given in Appendix C, and the classes of securities classified by the first 2 digits of their SIC code are in Appendix B. For each security class, we count the number of significant basis asset classes as follows.

Recall that is the number of securities. Denote to be the number of security classes. Denote the security classes by where . Recall that the number of basis assets is . Let the number of basis asset classes be . Let the basis asset classes be denoted where and is the number of basis assets which were significant for at least one of the security i. Also recall that in equation (2.22). Denote the significant count matrix to be where

| (2.24) |

That is, each element of matrix is the number of significant basis assets in basis asset class , selected by securities in class . Finally, denote the proportion matrix to be where

| (2.25) |

In other words, each element of matrix is the proportion of significant basis assets in basis asset class selected by security class among all basis assets selected by security class . Note that the elements in each column of sum to one.

2.5 Estimation Results

Our results show that the GIBS algorithm selects a total of 182 basis assets from different sectors for at least one company. And all of these 182 basis assets are significant in the second stage OLS regressions after the GIBS selection for at least one company. This validates our assumption that the total number of basis assets is large; much larger than 10 basis assets, which is typically the maximum number of basis asset with non-zero risk premiums (risk-factors) seen in the literature (see Harvey, Liu, Zhu (2016) [25]).

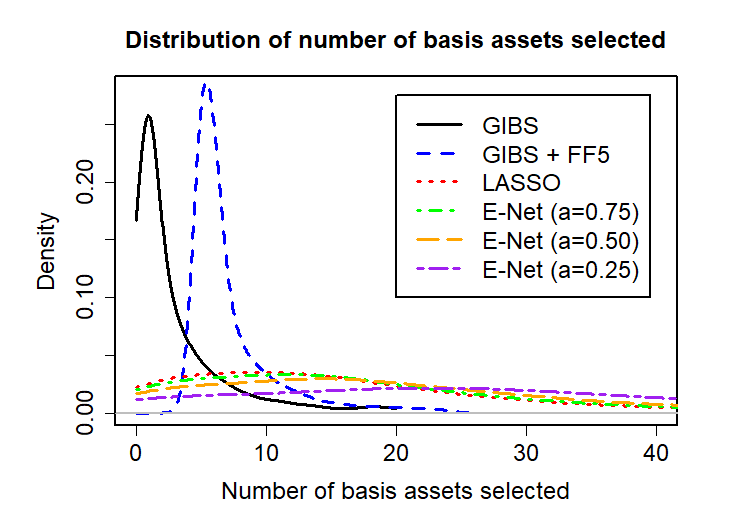

In addition, the results validate our sparsity assumption, that each company is significantly related to only a small number of basis assets (at a 5% level of significance). Indeed, for each company an average of 2.98 basis assets are selected by GIBS and an average of 1.92 basis assets show significance in the second stage OLS regression. (Even using the traditional cross-validation method with overfitting discussed in Section 2.6, only an average of 15.66 basis assets are selected.) In other words, the average number of elements in (see Equation 2.20) is 2.98 and the average number of elements in (see Equation 2.22) is 1.92. Figure 2.1 shows the distribution of the number of basis assets selected by GIBS and the number of basis assets that are significant in the second stage OLS regression. As depicted, most securities have between significant basis assets. Thus high dimensional methods are appropriate and necessary here.

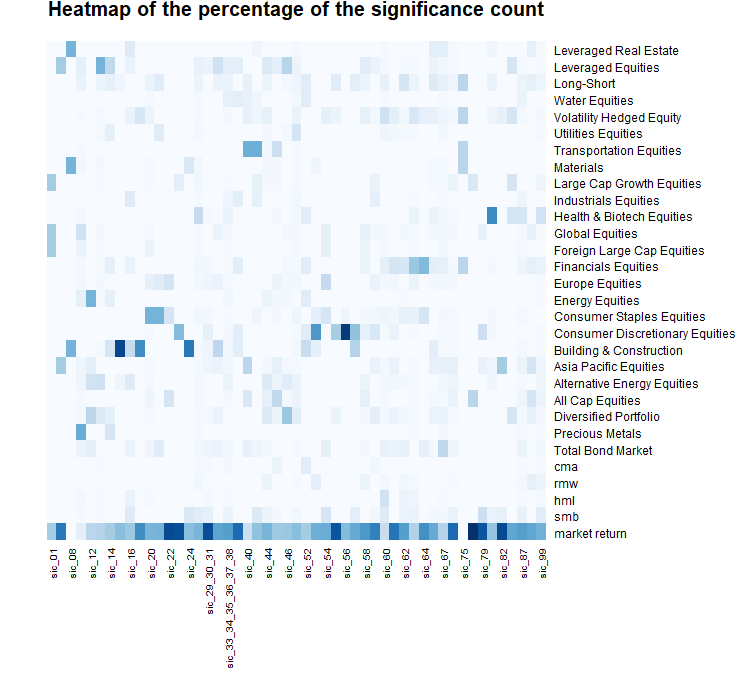

Table 2.2 provides the matrix in percentage. Each grid is where is defined in equation (2.25). Figure 2.2 is a heat map from which we can visualize patterns in Table 2.2. The darker the grid, the larger the percentage of significant basis assets. As indicated, different security classes depend on different classes of basis assets, although some basis assets seem to be shared in common. Not all of the Fama-French 5 risk-factors are significant in presence of the additional basis assets in our model. Only the market portfolio shows a strong significance for nearly all securities. The emerging market equities and the money market ETF basis assets seem to affect many securities as well. As shown, all of the basis assets are needed to explain security returns and different securities are related to a small number of different basis assets.

ETF Class SIC First 2 digits 01 07 08 10 12 13 14 15 16 17 20 21 22 23 24 25-28 29-31 market return 25 50 0 7 20 21 25 30 26 44 32 33 62 62 30 33 62 smb 0 0 0 1 0 1 0 0 9 0 0 0 0 0 10 8 6 hml 0 0 0 1 0 1 0 0 4 0 1 0 0 0 0 1 2 rmw 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 3 0 cma 0 0 0 0 0 1 0 0 0 0 0 0 0 0 0 1 2 Total Bond Market 0 0 0 4 7 0 0 0 4 0 3 8 0 0 0 2 3 Precious Metals 0 0 0 36 0 0 12 0 0 0 0 0 0 0 0 1 0 Diversified Portfolio 0 0 0 2 20 9 6 0 0 0 1 0 0 0 0 1 2 All Cap Equities 0 0 0 1 0 0 0 0 0 0 3 0 12 0 0 2 0 Alternative Energy Equities 0 0 0 3 13 14 0 3 9 0 2 0 0 0 0 2 0 Asia Pacific Equities 0 25 0 3 7 0 0 0 0 0 1 0 0 0 0 1 3 Building & Construction 0 0 33 0 0 1 12 63 17 44 0 0 0 0 50 2 3 Consumer Discrtnry. Equities 0 0 0 0 0 0 0 0 0 0 2 0 0 31 0 0 6 Consumer Staples Equities 0 0 0 0 0 0 0 0 0 0 33 33 12 0 0 3 2 Energy Equities 0 0 0 6 33 1 6 0 0 0 0 0 0 0 0 0 0 Europe Equities 0 0 0 2 0 2 0 0 0 0 6 8 12 0 0 2 3 Financials Equities 0 0 0 1 0 1 6 0 4 0 0 0 0 0 0 2 2 Foreign Large Cap Equities 25 0 0 4 0 1 0 0 0 0 4 0 0 0 0 1 0 Global Equities 25 0 0 14 0 2 0 0 0 0 2 0 0 0 0 1 0 Health & Biotech Equities 0 0 0 1 0 0 0 0 0 0 0 0 0 0 0 17 2 Industrials Equities 0 0 0 0 0 1 0 0 9 0 0 0 0 0 0 1 0 Large Cap Growth Equities 25 0 0 0 0 1 0 0 0 0 1 0 0 8 0 2 0 Materials 0 0 33 2 0 2 0 0 0 0 1 0 0 0 10 2 0 Transportation Equities 0 0 0 1 0 0 0 0 0 0 0 0 0 0 0 1 0 Utilities Equities 0 0 0 0 0 1 6 0 0 0 0 8 0 0 0 2 0 Volatility Hedged Equity 0 0 0 1 0 1 0 0 4 11 4 0 0 0 0 1 0 Water Equities 0 0 0 0 0 0 0 0 0 0 1 0 0 0 0 1 0 Long-Short 0 0 0 4 0 4 6 3 0 0 4 8 0 0 0 4 0 Leveraged Equities 0 25 0 7 0 33 19 0 4 0 0 0 0 0 0 5 5 Leveraged Real Estate 0 0 33 0 0 0 0 0 9 0 0 0 0 0 0 0 0

ETF Class SIC First 2 digits 32 33-38 39 40 42 44 45 46 47-51 52 53 54 55 56 57 58 59 market return 38 40 54 15 28 33 26 27 30 25 34 35 60 30 36 42 48 smb 0 4 0 0 9 4 2 0 2 0 0 12 0 0 7 0 2 hml 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 rmw 0 0 0 0 0 4 0 0 1 0 7 0 0 0 0 4 0 cma 0 2 0 0 0 0 4 0 0 8 0 0 0 0 0 0 2 Total Bond Market 5 2 0 5 3 2 0 0 1 0 0 6 0 0 0 2 0 Precious Metals 0 0 0 0 0 0 0 0 1 0 0 0 0 0 0 0 0 Diversified Portfolio 5 0 0 0 0 10 4 27 7 0 0 0 4 0 0 2 7 All Cap Equities 0 2 0 10 0 6 19 2 4 0 0 0 0 0 0 6 0 Alternative Energy Equities 0 4 0 0 0 10 4 8 5 0 0 0 0 0 0 4 0 Asia Pacific Equities 5 2 0 20 0 2 6 2 1 0 0 0 0 0 0 0 4 Building & Construction 19 3 8 0 0 0 0 0 2 17 7 0 0 0 21 0 0 Consumer Discrtnry. Equities 0 2 8 0 0 0 0 0 1 8 41 0 24 67 29 6 11 Consumer Staples Equities 0 1 0 0 3 0 2 0 3 0 7 12 0 3 0 2 2 Energy Equities 0 2 0 0 0 4 2 2 0 8 0 0 0 0 0 0 0 Europe Equities 5 1 0 0 0 0 4 2 3 0 0 18 0 0 0 0 4 Financials Equities 0 1 8 0 0 0 0 2 1 8 0 0 0 0 0 4 0 Foreign Large Cap Equities 0 1 0 0 0 0 0 0 2 0 0 6 0 0 0 4 0 Global Equities 5 1 0 0 0 0 0 2 2 0 0 6 0 0 0 6 2 Health & Biotech Equities 0 5 0 0 0 0 2 0 2 8 0 0 0 0 0 0 0 Industrials Equities 0 3 8 0 6 0 0 0 2 0 0 0 0 0 0 0 7 Large Cap Growth Equities 0 1 0 0 6 2 2 0 1 0 0 0 0 0 0 0 4 Materials 0 0 0 0 0 2 2 0 1 0 3 0 0 0 0 0 0 Transportation Equities 0 0 0 35 34 2 15 0 1 0 0 0 0 0 0 0 0 Utilities Equities 0 0 0 0 0 2 0 2 12 0 0 0 0 0 0 0 0 Volatility Hedged Equity 0 2 0 5 3 6 0 0 4 0 0 6 4 0 0 6 2 Water Equities 0 6 8 5 3 0 0 0 2 8 0 0 0 0 0 0 0 Long-Short 5 5 0 5 0 4 0 2 3 8 0 0 8 0 7 4 0 Leveraged Equities 14 7 8 0 0 10 8 21 4 0 0 0 0 0 0 8 4 Leveraged Real Estate 0 0 0 0 3 0 0 0 2 0 0 0 0 0 0 0 0

ETF Class SIC First 2 digits 60 61 62 63 64 65 67 70-73 75 78 79 80 82 83 87 89 99 market return 16 51 40 22 44 36 21 55 0 70 60 27 62 38 40 38 34 smb 10 0 4 5 0 2 2 4 0 0 15 5 6 0 5 0 8 hml 14 0 4 3 0 0 1 0 0 0 0 0 0 0 1 0 1 rmw 3 0 3 1 0 0 1 1 0 0 0 0 0 0 2 6 4 cma 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1 0 1 Total Bond Market 5 5 5 0 6 2 19 3 0 0 0 0 0 0 4 0 3 Precious Metals 0 0 1 1 0 0 2 0 0 0 0 0 0 0 2 0 1 Diversified Portfolio 2 5 3 1 0 4 4 1 0 0 0 0 0 12 1 6 2 All Cap Equities 1 0 0 1 0 2 1 4 0 20 0 0 0 0 3 12 4 Alternative Energy Equities 2 2 2 1 0 0 2 3 0 0 0 3 0 0 1 0 3 Asia Pacific Equities 2 5 1 1 0 5 6 6 0 0 5 3 25 0 4 12 3 Building & Construction 0 0 0 0 0 7 1 1 0 0 0 0 0 0 2 0 1 Consumer Discrtnry. Equities 1 5 1 1 0 0 1 1 0 0 15 2 0 0 0 0 1 Consumer Staples Equities 3 2 6 5 12 0 1 1 0 0 0 2 0 0 2 0 1 Energy Equities 0 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 1 Europe Equities 2 2 1 4 0 2 2 2 0 0 0 0 0 0 0 0 1 Financials Equities 7 12 11 27 31 7 6 2 20 0 0 2 0 0 3 6 4 Foreign Large Cap Equities 2 0 0 1 0 0 2 1 0 0 0 0 0 0 2 0 1 Global Equities 2 0 2 1 0 2 2 1 0 0 5 0 0 0 1 6 1 Health & Biotech Equities 1 0 0 4 0 4 1 1 0 0 0 45 0 12 11 0 13 Industrials Equities 0 0 0 1 0 0 1 0 0 0 0 0 0 0 3 0 0 Large Cap Growth Equities 0 0 0 0 0 2 1 4 0 10 0 0 0 12 0 0 3 Materials 0 0 1 0 0 2 1 0 20 0 0 0 0 0 0 0 1 Transportation Equities 0 0 0 0 0 0 0 1 20 0 0 0 0 0 0 0 1 Utilities Equities 3 2 1 1 0 0 3 0 0 0 0 0 0 0 0 0 1 Volatility Hedged Equity 15 7 3 11 6 5 3 2 20 0 0 3 6 12 2 0 2 Water Equities 1 0 0 0 0 0 1 0 0 0 0 0 0 0 4 0 1 Long-Short 5 0 12 4 0 9 5 3 20 0 0 5 0 0 4 6 3 Leveraged Equities 2 0 1 1 0 4 2 1 0 0 0 0 0 12 1 0 1 Leveraged Real Estate 1 0 1 0 0 7 7 1 0 0 0 3 0 0 0 6 1

2.5.1 Intercept Test

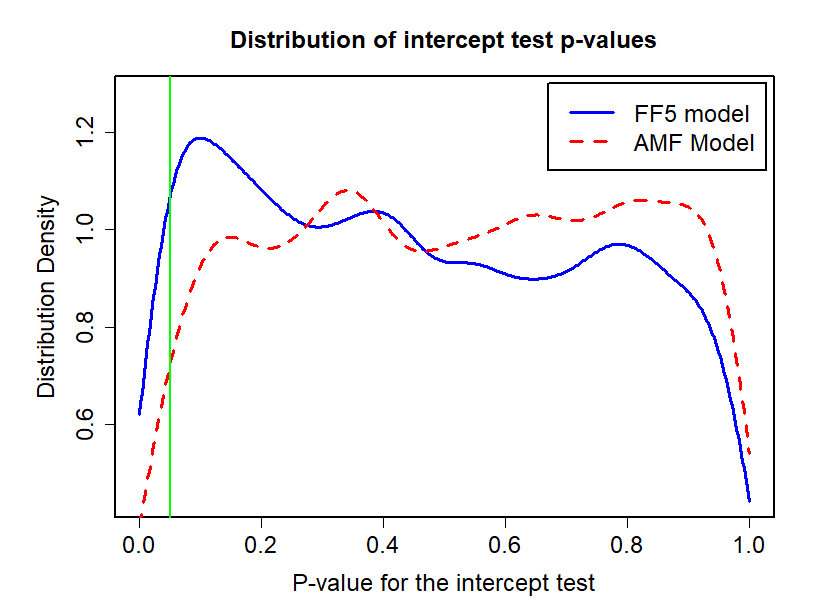

This section provides the tests for a zero intercept. Using the Fama-French 5-factor model as a comparison, Figure 2.3 compares the intercept test p-values between our basis asset implied Adaptive Multi-factor (AMF) model and Fama-French 5-factor (FF5) model. As indicated, 6.22% (above 5%) of the securities have significant intercepts in the FF5 model, while 3.86% (below 5%) of the securities in AMF have significant ’s. This may suggests that the AMF model is more insightful than the FF5 model, since AMF reveals more relevant factors and makes the intercept closer to 0.

Since we replicate this test for about 5000 stocks in the CRSP database, it is important to control for a False Discovery Rate (FDR) because even if there is a zero intercept, a replication of 5000 tests will have about 5% showing false significance. We adjust for the false discovery rate using the Benjamini-Hochberg (BH) procedure [7] and the Benjamini-Hochberg-Yekutieli (BHY) procedures [8]. The BH method does not account for the correlation between tests, while the BHY method does. In our case, each test is done on an individual stock, which may have correlations. So the BHY method is more appropriate here.

Chordia et al. (2017) [15] suggests that the false discovery proportion (FDP) approach in [53] should be applied rather than a false discovery rate procedure. The BH approach only controls the expected value of FDP while FDP controls the family-wise error rate directly. There is another test worth mentioning, which is the GRS test. The GRS test in [24] is usually an excellent procedure for testing intercepts. However, these two tests are not appropriate in the high-dimensional regression setting as in our case. To be specific, these tests are implicitly based on the assumption that all companies are only related to the same small set of basis assets. Here the “small” means there are many fewer basis assets than observations. Our setting is more general since we may have more basis assets than observations, although each company is related to only a small number of basis assets, different companies may be related to different sets of basis assets. The GRS is unable to handle setting.

As noted earlier, Table 2.3 shows that 3.86% of stocks in the multi-factor model have p-values for the intercept t-test of less than 0.05. While in the FF5 model, this percentage is 6.22%. After using the BHY method to control for the false discovery rate, we can see that the q-values (the minimum false discovery rate needed to accept that this rejection is a true discovery, see [57]) for both models are almost 1, indicating that there are no significant non-zero intercepts. All the significance shown in the intercept tests is likely to be false discovery. This is the evidence that both models are consistent with the behavior of “large-time scale” security returns.

| Value Range | Percentage of Stocks (%) | |||

|---|---|---|---|---|

| FF5 p-val | AMF p-val | FF5 FDR q-val | AMF FDR q-val | |

| 0 - 0.05 | 6.22 | 3.86 | 0.00 | 0.00 |

| 0.05 - 0.9 | 84.88 | 85.33 | 0.02 | 0.00 |

| 0.9 - 1 | 8.90 | 10.81 | 99.98 | 100.00 |

2.5.2 In-Sample and Out-of-Sample Goodness-of-Fit

This section tests to see which model fits the data best. Figure 2.4 compares the distribution of the adjusted ’s (see [58]) between the AMF and the FF5 model. As indicated, the AMF model has more explanatory power. The mean adjusted for the AMF model is 0.319 while that for the FF5 model is 0.229. The AMF model increases the adjusted by 39.2% compared to the FF5.

We next perform an F-test, for each security, to show that there is a significant difference between the goodness-of-fit of the AMF and the FF5 model. Since we need a nested comparison for an F-test, we compare the results between FF5 and GIBS + FF5 (which is including FF5 factors back to GIBS for fitting if any of the FF5 factors are not selected). In our case, the FF5 is the restricted model, having degrees of freedom and a sum of squared residuals , where . The AMF is the full model, having degrees of freedom (where is the number of basis assets selected in addition to FF5) and a sum of squared residuals . Under the null-hypothesis that FF5 is the true model, we have

| (2.26) |

There are 5132 stocks in total. For 1931 (37.63%) of them, the GIBS algorithm only selects some of the FF5 factors, so for these stocks, GIBS + FF5 does not give extra information. However, for 3201 (62.37%) of them, the GIBS algorithm does select ETFs outside of the FF5 factors. For these stocks, we do the F test to check whether the difference between the two models are significant, in other words, whether AMF gives a significantly better fit. As shown in Table 2.4, for 97.72% of the stocks, the AMF model fits better than the FF5 model.

Again, it is important to test the False Discovery Rate (FDR). Table 2.4 contains the p-values and the false discovery rate q-values using both the BH method and BHY methods. As indicated, for most of the stocks, the AMF is significantly better than the FF5 model, even after considering the false discovery rate. For 97.72% of stocks, the AMF model is better than the FF5 at the significance level of 0.05. After considering the false discovery rate using the strict BHY method which includes the correlation between tests, there is still 90.16% of stocks significant with q-values less than 0.05. Even if we adjust our false discover rate q-value significance level to 0.01, there is still 83.29% of the stocks showing a significant difference. As such, this is strong evidence supporting the multi-factor model’s superior performance in characterizing security returns.

| Value Range | Percentage of Stocks | ||

|---|---|---|---|

| p-value | BH q-value | BHY q-value | |

| 93.44% | 93.06% | 83.29% | |

| (Significant) | 97.72% | 97.53% | 90.16% |

| (Non-Significant) | 2.28% | 2.47% | 9.84% |

Apart from the In-Sample goodness of fit results, we also compare the Out-of-Sample goodness of fit of the FF5 and AMF model in the prediction time period. We use the two models to predict the return of the following week and report the Out-of-Sample for the prediction (see Table 2.5). The Out-of-Sample (see [14]) is used to measure the predictive accuracy of a model. The Out-of-Sample for the FF5 is , while that for the AMF is . That is, the AMF model increased the Out-of-Sample by compared to the FF5 model. The AMF model shows its superior performance by giving a more accurate prediction using an even lower number of factors, which is also strong evidence against overfitting. The AMF model provides additional insight when compared to the FF5.

2.5.3 Robustness Test

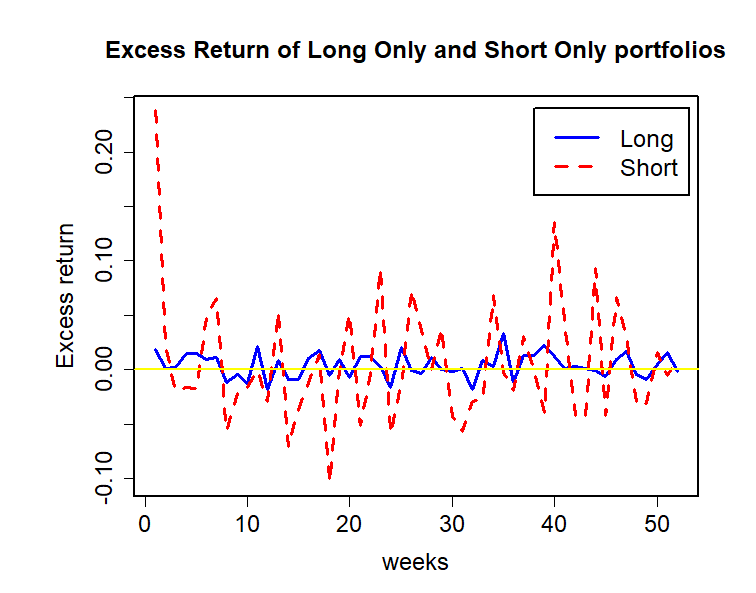

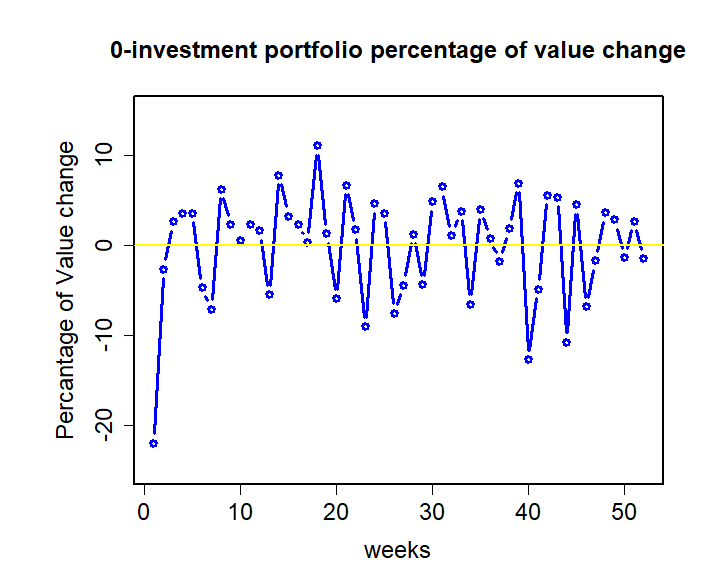

As a robustness test, for those securities whose intercepts were non-zero, we tested the basis asset implied multi-factor model to see if positive alpha trading strategies generate arbitrage opportunities. To construct the positive alpha trading strategies, we use the data from the year 2017 as an out-of-sample period. Recall that the previous analysis was over the time period 2014 to 2016. As explained above, we fit the AMF model using the data up to the last week of 2016. We then ranked the securities by their alphas from positive to negative. We take the top 50% of those with significant (p-val less than 0.05) positive alphas and form a long-only equal-weighted portfolio with $1 in initial capital. Similarly, take the bottom 50% of those with significant negative alphas and form a short-only equal-weighted portfolio with -$1 initial capital. Then, each week over 2017, we update the two portfolios by re-fitting the AMF model and repeating the same construction. Combining the long-only and short-only portfolio forms a portfolio with 0 initial investment. If the alphas represent arbitrage opportunities, then the combined long and short portfolio’s change in value will always be non-negative and strictly positive for some time periods.

The results of the arbitrage tests are shown in Figures 2.5 and 2.6. As indicated, the change in value of the 0-investment portfolio randomly fluctuates on both sides of 0. This rejects the possibility that the positive alpha trading strategy is an arbitrage opportunity. Thus, this robustness test confirms our previous intercept test results, after controlling for a false discovery rate. Although not reported, we also studied different quantiles from 10% to 40% and they give similar results.

2.6 Comparison with Alternative Methods

2.6.1 Are Fama-French 5 Factors Overfitting?

We first test whether the Fama-French 5 factors (FF5) overfit the noise in the data. This can be done by estimating a “GIBS + FF5” model. This model is very similar to GIBS, except that it includes the Fama-French 5 factors to be selected in the last step. That is, if any of the FF5 factors are not selected by GIBS, we add them back to our selected basis asset set and use this set of basis assets to fit and predict the returns. By comparing the In-Sample Adjusted and the Out-of-Sample (see [14]) of GIBS + FF5 model and the GIBS model, we can determine whether FF5 factors are overfitting. The Out-of-Sample (see [14]) is used to measure the accuracy of prediction of a model. Surprisingly, the results show that some of the FF5 factors are over-fitting! As shown in Table 2.5, compared to our GIBS model, the GIBS + FF5 achieves a better in-sample Adjusted , with more significant basis assets, but gives a much worse Out-of-Sample . This indicates that the FF5 factors not selected by GIBS are “false discoveries” - they overfit the training data, but do a poor job in predicting. Therefore, those FF5 factors should not be used for a company if they are not selected by GIBS. Table 2.5 not only provides evidence of the superior performance of GIBS over FF5 by comparing the In-Sample Adjusted and Out-of-Sample of GIBS and FF5 model, but it also indicates an overfitting of FF5 by comparing the In-Sample Adjusted and Out-of-Sample of GIBS and GIBS + FF5.

2.6.2 Comparison with Elastic Net

Since there are a large number of correlated ETFs it is natural to employ the RIDGE, LASSO and Elastic Net (E-Net) methods (by Zou and Hastie (2005) [73]). E-Net is akin to the ridge regression’s treatment of multicollinearity with an additional tuning (ridge) parameter, , that regularizes the correlations. We compare GIBS, LASSO, RIDGE and E-Net with different s. The sparsity inducing parameter in each model is selected by the usual 10-fold cross-validation (by Kohavi et al. (1995) [43]). The comparison results are shown in Table 2.5. The distribution of the number of basis assets selected by each method is shown in Figure 2.7.

From Table 2.5 it is clear that the GIBS model has better prediction than the FF5 model. The GIBS model increased the Out-of-Sample by 24.07% compared to FF5. Across all models, GIBS has the highest Out-of-Sample , which supports the fact that the better In-Sample Adjusted achieved by the other models (LASSO, RIDGE, E-Net etc.) is due to overfitting. Furthermore, from Table 2.5 and Figure 2.7, we see that GIBS selects the least number of factors.

Model Select Signif. In-Sample Adj. Out-of-Sample FF5 5.00 1.78 0.229 (00.00%) 0.030 (00.00%) GIBS 2.98 1.92 0.319 (39.18%) 0.038 (+24.07%) GIBS + FF5 7.20 2.50 0.350 (52.55%) 0.025 (-16.71%) LASSO 15.66 5.72 0.466 (103.46%) 0.018 (-40.97%) E-Net (=0.75) 16.84 5.81 0.470 (105.22%) 0.018 (-40.09%) E-Net (=0.50) 19.28 6.05 0.479 (109.05%) 0.015 (-49.92%) E-Net (=0.25) 26.36 6.51 0.498 (117.20%) 0.009 (-70.33%) Ridge 182.00 NA NA -6 (-2%)

The of LASSO is traditionally selected by cross-validation and with this , the model selects an average of 15.66 factors, as shown in Table 2.5. However, most of the factors selected by cross-validation are “false-positive”. Therefore, instead of the cross-validation, we use the “1se rule” with a hard threshold 20 basis assets at most. The “1se rule” use the largest such that the cross-validation error is within one standard error of the minimum error achieved by the cross-validation. In another word, gives the most regularized model such that error is within one standard error of the minimum error achieved by the cross-validation (see [23, 56, 60]). To further avoid over-fitting, we include the threshold that each company can not be related to more than 20 basis assets. As shown in the Table 2.5, our method used in GIBS works well and achieves the best prediction power. The reason for the superior performance of GIBS compared with the cross-validation LASSO is that cross-validation often overfits, especially when the sample size is small, or when the data is not sufficiently independent and identically distributed. In addition, our results with GIBS are both stable and interpretable.

Our choice of dimension reduction techniques, using a combination of prototype clustering and a modified version of LASSO, was motivated by our desire to select, from a collection of strongly correlated ETFs, a sparse and interpretable set of basis assets that explains the cross-sectional variation among asset returns. These two steps were used as model selection tools to identify basis assets, and we subsequently estimated the model coefficients using OLS. In future research, a more integrative method may be designed to combine the model selection and estimation steps.

The motivation for using prototype clustering is two fold. First, it can be used to derive the cluster structure of the ETFs so that the redundant ones are removed. This reduces the correlation and validates the use of LASSO. Second, this method gives a clear interpretation of the prototypes, which is important for our interpretation of the basis assets. The traditional methods of dealing with empirical asset models are based on variance decomposition of the basis assets (the matrix) as in, for example, the principal component analysis (PCA) approach. More recently, there are modern statistical methods that introduce sparsity and high-dimensional settings in these traditional methods (see Zou et al. (2006) [74]). However, as we argued in the introduction, these methods are not optimal for basis asset models due to their difficulties in interpreting the basis assets. Furthermore, it is the correlation that is important in the determination of the basis assets not the variance itself. Therefore, methods that focus on finding the rotation with the largest variance (like PCA) are not optimal in this setting. Instead, we use correlation as our metric in the prototype clustering step, which gives a clearer interpretation and a direct analysis of the candidate basis assets, rather than linear combinations of the basis assets. For this reason we believe that prototype clustering is preferred to PCA in this setting.

For future work, modern refinements of model-selection and inference methods may be used. For high-dimensional models obtaining valid p-values is difficult. This is in part due to the fact that fitting a high-dimensional model often requires penalization and complex estimation procedures, which implies that characterizing the distribution of such estimators is difficult. For statistical testing in the presence of sparsity a number of new methods are appearing in the literature. One alternative method is the post-selection procedure by Tibshirani et al. (2016) [61]. Another approach for constructing frequentistp p-values and confidence intervals for high-dimensional models uses the idea of de-biasing which was proposed in a series of articles [62, 38, 65]. In the de-biasing method, starting from a regularized estimator one first constructs a de-biased estimator and then makes inference based on the asymptotic normality of low-dimensional functionals of the de-biased estimator. In principle, this approach also provides asymptotically valid p-values for hypotheses testing each of the parameters in the model. However, in our numerical explorations of these methods we found that the confidence intervals are too large for the current application and no meaningful insights could be obtained. The p-values for these methods are also not very stable. So we use the OLS after LASSO instead of the post-selection methods with the theoretical guarantee in the paper by Zhao et al. (2017) [67]. Some details can be found in [69]. Some related work can be found in [70, 71, 72, 37, 46, 12, 64, 32, 30, 29, 31, 48, 66, 17, 51, 68, 40, 47, 41, 39].

2.7 Risk-Factor Determination

We focus on the same three year time period 2014 - 2016 and compute the average annal excess returns on the basis assets to determine which have non-zero risk premium (average excess returns), i.e. which are risk-factors in the traditional sense. In this time period there are 182 basis assets selected, including the Fama-French 5 factors and 177 ETFs. The risk premium of the Fama-French 5 factors are shown in Table 2.6.

| Fama-French 5 Factors | Market Return | SMB | HML | RMW | CMA |

| Annual Excess Return (%) | 10.0 | -2.1 | 1.7 | 1.1 | -1.2 |

Out of the 177 selected ETFs, 136 of them have absolute risk premiums larger than the minimum of that of the FF5 factors (which is the RMW, with absolute risk premium 1.1%). Therefore, at least basis assets are risk factors. Furthermore, 29 out of the 177 selected ETFs have absolute risk premiums larger than 10.0% (the absolute risk premium of the market return, which is the biggest absolute risk premium of all FF5 factors). The list of the 29 ETFs are in Table 2.7.

Risk Pre- ETF name Category mium (%) ProShares Ultra Semiconductors Leveraged Equities 55.1 ProShares Ultra Bloomberg Natural Gas Leveraged Commodities -30.4 ProShares VIX Short-Term Futures ETF Volatility -29.2 ProShares Ultra Real Estate Leveraged Real Estate 26.2 Global X MSCI Nigeria ETF Foreign Large Cap Equities -24.0 Invesco DB Oil Fund Oil & Gas -21.3 Global X FTSE Greece 20 ETF Emerging Markets Equities -20.8 Invesco S&P SmallCap Information Technology ETF Technology Equities 19.7 Direxion Daily Energy Bull 3X Shares Leveraged Equities -17.5 Invesco S&P SmallCap Consumer Staples ETF Consumer Staples Equities 15.8 VanEck Vectors Rare Earth/Strategic Metals ETF Materials -15.5 Global X Uranium ETF Global Equities -15.3 SPDR S&P Health Care Equipment ETF Health & Biotech Equities 15.0 SPDR SSGA US Small Cap Low Volatility Index ETF Volatility Hedged Equity 15.0 Vanguard Utilities ETF Utilities Equities 15.0 VanEck Vectors Egypt Index ETF Emerging Markets Equities -15.0 Global X MSCI Colombia ETF Latin America Equities -14.6 SPDR S&P Insurance ETF Financials Equities 14.2 iShares U.S. Aerospace & Defense ETF Industrials Equities 13.8 iShares North American Tech-Software ETF Technology Equities 13.4 iShares North American Tech-Multimedia Networking ETF Communications Equities 13.3 FLAG-Forensic Accounting Long-Short ETF Long-Short 12.2 SPDR SSGA US Large Cap Low Volatility Index ETF Volatility Hedged Equity 12.0 Global X MSCI Portugal ETF Europe Equities -11.7 Vanguard Consumer Staples ETF Consumer Staples Equities 10.9 VanEck Vectors Poland ETF Europe Equities -10.8 VanEck Vectors Morningstar Wide Moat ETF Large Cap Blend Equities 10.6 Invesco Russell Top 200 Equal Weight ETF Large Cap Growth Equities 10.2 First Trust NASDAQ CEA Smartphone Index Fund Technology Equities 10.1

2.8 Illustrations

In this section we illustrate our multi-factor estimation process and compare the results with the Fama-French 5-factor (FF5) model for three securities: Adobe, Bank of America, and Apple.

2.8.1 Adobe

This section contains the results for Adobe. Using Equation (2.14), we estimate the Fama-French 5 factor (FF5) model as shown in Table 2.8. For our Adaptive Multi-Factor (AMF) model, the final results are shown in Table 2.9 with the description of the ETF basis assets selected by GIBS in Table 2.10. The adjusted for FF5 is 0.38, while the adjusted for AMF is 0.57. From the Tables it is clear that different significant basis assets are selected and the ones selected by GIBS gives much better explanation and prediction power. Only the market return is significant among the FF5 factors. Additionally, Adobe’s returns are related to the iShares North American Tech-Software ETF, indicating that Adobe is sensitive to risks in the technology software sector. For Adobe, both models do not have a significant intercept, indicating that the securities are properly priced.

| SE | t value | P-value | ||

|---|---|---|---|---|

| (Intercept) | 0.002 | 0.002 | 1.227 | 0.222 |

| Market Return | 1.036 | 0.124 | 8.382 | 0.000 |

| SMB | -0.168 | 0.191 | -0.883 | 0.379 |

| HML | -0.480 | 0.247 | -1.942 | 0.054 |

| RMW | -0.378 | 0.310 | -1.217 | 0.226 |

| CMA | -0.234 | 0.424 | -0.551 | 0.583 |