Neural network approximation for superhedging prices

Abstract

This article examines neural network-based approximations for the superhedging price process of a contingent claim in a discrete time market model. First we prove that the -quantile hedging price converges to the superhedging price at time for tending to , and show that the -quantile hedging price can be approximated by a neural network-based price. This provides a neural network-based approximation for the superhedging price at time and also the superhedging strategy up to maturity. To obtain the superhedging price process for , by using the Doob decomposition it is sufficient to determine the process of consumption. We show that it can be approximated by the essential supremum over a set of neural networks. Finally, we present numerical results.

Keywords: Deep learning; Superhedging; Quantile hedging

Mathematics Subject Classification (2020): 91G15, 91G20, 60H30

JEL Classification: C45

1 Introduction

In this paper we study neural network approximations for the superhedging price process for a contingent claim in discrete time.

Superhedging was first introduced in [12] and then thoroughly studied in various settings and market models. It is impossible to cover the complete literature here, but we name just a few references. For instance, in continuous time, for general càdlàg processes we mention [20], for robust superhedging [21], [27], for pathwise superhedging on prediction sets [1], [2], or for superhedging under proportional transaction costs [6], [11], [18], [25], [26]. Also in discrete time there are various studies in the literature, like the standard case [14], robust superhedging [8], [23], superhedging under volatility uncertainty [22], or model-free superhedging [5]. The superhedging price provides an opportunity to secure a claim, but it may be too high or reduce the probability to profit from the option. In order to solve this problem, quantile hedging was introduced in [13], where the authors propose to either fix the initial capital and maximize the probability of superhedging with this capital or fix a probability of superhedging and minimize the required capital. In this way a trader can determine the desired trade-off between costs and risk.

In certain situations it is possible to calculate explicitly or recursively the superhedging or quantile hedging price, see e.g. [7], but in general incomplete markets it may be complicated to determine superhedging prices or quantile hedging prices. In this article we investigate neural network-based approximations for quantile- and superhedging prices. Neural network-based methods have been recently introduced in financial mathematics, for instance for hedging derivatives, see [4], determining stopping times, see [3], or calibration of stochastic volatility models, see [10], and many more. For an overview of applications of machine learning to hedging and option pricing we refer to [24] and the references therein.

This paper contributes to the literature on hedging in discrete time market models in several ways. First, we prove that the -quantile hedging price converges to the superhedging price for tending to . Further, we show that it is feasible to approximate the -quantile hedging and thus also the superhedging price for by neural networks. We extend our machine learning approach also to approximate the superhedging price process for . By the first step we obtain an approximation for the superhedging strategy on the whole interval up to maturity. By using the uniform Doob decomposition, see [14], we then only need to approximate the process of consumption to generate the superhedging price process. We prove that can be obtained as the the essential supremum over a set of neural networks. Finally, we present and discuss numerical results for the proposed neural network methods.

The paper is organized as follows. In Section 2, we present the discrete time market model of [14] and recall essential definitions and results on superhedging. Section 3 contains the study of the superhedging price for . More specifically, in Section 3.1 we prove in Theorem 3.4 that the -quantile hedging price converges to the superhedging price as tends to . We also present a similar result in Corollary 3.9 in Section 3.1.2, where -quantile hedging is given in terms of success ratios. In Section 3.2 we show in Theorem 3.11 that the superhedging price can be approximated by neural networks. This concludes the approximation for . Then, we consider the case for in Section 4. In Section 4.1, we explain how the uniform Doob decomposition can be used to approximate the superhedging price process. In that account, we prove an explicit representation of the process of consumption, see Proposition 4.1. Proposition 4.3 and Theorem 4.4 show that the process of consumption and thus the superhedging price process can be approximated by neural networks. The numerical results are presented in Section 5. The section is divided in the case , see Section 5.1, and , see Section 5.2. We present details on the algorithm and the implementation. Appendix A contains a version of the universal approximation theorem, derived from [16].

2 Preliminaries

In this section we introduce the discrete time financial market model from [14] and recall some basic notions on superhedging.

Consider a finite time horizon . Let be a probability space endowed with a filtration . We assume for and for some -valued process for some , and write for . Further, we suppose that and that is constant P-a.s. Then .

In our market model on the asset prices are modeled by a non-negative, adapted, stochastic process

with , . In particular, . Further, we assume that

and define to be the numéraire. The discounted price process is given by

A probability measure is called an equivalent martingale measure if is equivalent to P and is a -martingale. We denote by the set of all equivalent martingale measures for and assume . By Theorem 5.16 of [14] this is equivalent to the market model being arbitrage-free.

Definition 2.1.

A trading strategy is a predictable -valued process

The (discounted) value process associated with a trading strategy is given by

A trading strategy is called self-financing if

A self-financing trading strategy is called an admissible strategy if its value process satisfies .

By we denote the set of all admissible strategies and by the associated value processes, i.e.,

By Proposition 5.7 of [14], a trading strategy is self-financing if and only if

with . In particular, given a -valued predictable process and , the pair uniquely defines a self-financing strategy.

Remark 2.2.

By Theorem 5.14 of [14], P-a.s. implies that P-a.s. for all , where denotes the value process of a self-financing strategy. More precisely, Theorem 5.14 of [14] guarantees that if is a self-financing strategy and its value process satisfies , then is a -martingale for any . In particular, in the proof the martingale property of and Proposition 5.7 of [14] is used successively in the following way:

A discounted European contingent claim is represented by a non-negative, -measurable random variable such that

Definition 2.3.

Let be a European contingent claim. A self-financing trading strategy whose value process satisfies

is called a superhedging strategy for . In particular, any superhedging strategy is admissible since by definition.

The upper Snell envelope for a discounted European claim is defined by

Corollary 2.4 (Corollary 7.3, Theorem 7.5, Corollary 7.15, [14]).

The process

is the smallest -supermartingale whose terminal value dominates . Furthermore, there exists an adapted increasing process with and a -dimensional predictable process such that

| (2.1) |

Moreover, and

| (2.2) |

The process in (2.1) is sometimes called process of consumption, see [20]. Equations (2.1) and (2.2) yield

| (2.3) |

Set

| (2.4) |

Corollary 2.5 (Corollary 7.18, [14]).

Suppose is a discounted European claim with

Then

3 Superhedging price for

In this section we approximate the superhedging price for in two steps. In the first part, we introduce the theory of quantile hedging, see [13]. In Theorem 3.4 we prove that the quantile hedging price for converges to the superhedging price as tends to . Analogously, in Corollary 3.9 we prove that for tending to also the success ratios for converge to the superhedging price.

In the second part, we prove in Theorem 3.11 that the superhedging price and the associated strategies can be approximated by neural networks.

3.1 Quantile hedging

3.1.1 Success sets

In incomplete markets perfect replication of a contingent claim may not be possible. Superhedging offers an alternative hedging method but it presents two main disadvantages. From one hand the superhedging strategy not only reduces the risk but also the possibility to profit. On the other hand, the superhedging price may result to be too high.

Quantile hedging was proposed for the first time in [13] to address these problems. Fix . Given probability of success we consider the minimization problem

| (3.1) |

Here is called the shortfall probability. Quantile hedging may be considered as a dynamic version of the value at risk concept.

For an admissible strategy with associated value process we call

the success set.

Remark 3.1.

Proposition 3.2 below provides an equivalent formulation of the quantile hedging (3.1), see also [13].

Proposition 3.2.

Fix . Then

Proof.

: Take such that . We prove that

| (3.2) |

By the well-known superhedging duality, see Theorem 7.13 of [14], we have that

and that there exists a superhedging strategy for with initial value , i.e.,

| (3.3) |

In particular, by (3.3) we get for that

This implies (3.2) and hence

: Take and denote by the corresponding strategy such that

Define the set by

Clearly and . By construction we have that

and because is assumed to be admissible, we have

In particular, and by Theorem 7.13 of [14] we obtain

| (3.4) |

That is, for an arbitrary we have constructed a set such that (3.4) holds. Therefore,

∎

Corollary 7.15 of [14] guarantees that there exists a superhedging strategy with initial value . In contrast, there might be no explicit solution to the quantile hedging approach (3.1). If a solution to the quantile hedging approach exists, then Proposition 3.2 states that it is given by the solution of the classical hedging formulation for the knockout option for some suitable . However, such a set does not always exist. In particular, quantile hedging does not always admit an explicit solution in general. The Neyman-Pearson lemma suggests to consider so-called success ratios instead of success sets. We will briefly discuss success ratios below. For further information we refer the interested reader to [13].

We now show that the superhedging price , can be approximated by the quantile hedging price for tending to .

Definition 3.3.

For we define

Theorem 3.4.

The -quantile hedging price converges to the superhedging price as tends to , i.e.,

Proof.

We first note that, using Proposition 3.2 it suffices to prove

Let be an increasing sequence such that converges to as tends to infinity. Note that

| (3.5) |

because . Therefore, the limit of exists because the sequence is monotone and bounded. Let be arbitrary. For each exists such that

| (3.6) |

Then, by Lemma111For random variables we denote by the convex hull of which is defined -wise.

Lemma (Lemma 1.70, [14]).

Let be a sequence in such that P-a.s. Then there exists a sequence of convex combinations

which converges P-almost surely to some .

1.70 of [14] there exists a sequence , , which converges P-a.s. to some . Note that it is not clear if is an indicator function of some -measurable set. We will show that P-a.s. For , is of the form

| (3.7) |

for some such that . By dominated convergence and (3.7) we obtain

| (3.8) |

Because and by the definition of the limes inferior, equation (3.8) yields

| (3.9) |

Since , it follows that P-a.s. By (3.6) and with similar arguments as in (3.8) and (3.9) using the supremum instead of the infimum, we obtain by dominated convergence for any that

| (3.10) |

Since the limit on the left hand side in (3.10) exists by (3.5) and (3.10) holds for all , we get

| (3.11) |

Thus, we observe that (3.5) and (3.11) yields

As was arbitrary this implies that

∎

3.1.2 Success ratios

Let be the set of randomized tests. For we denote by the set

We now consider the following minimization problem

| (3.12) |

In a first step, we prove that this problem admits an explicit solution. In a second step, we show that the solution is given by the so-called success ratio, see Definition 3.6 below. In particular, (3.12) can be formulated in terms of success ratios, see also [13]. In Proposition 3.5 and 3.8 we provide a proof for some result of [13] for the sake of completeness.

Proposition 3.5.

There exists a randomized test such that

and

| (3.13) |

Proof.

Take a sequence such that

| (3.14) |

By Lemma 1.70 of [14] there exists a sequence of convex combinations converging P-a.s. to a function because for all . Clearly for each . Hence, dominated convergence yields that

| (3.15) |

and we get that . In the following we use similar arguments as in the proof of Theorem 3.4. In particular, is of the form

| (3.16) |

for some such that . By (3.16) we obtain for any that

| (3.17) |

where we used monotone convergence. Moreover, we obtain by (3.14), (3.17) and dominated convergence that

| (3.18) |

Since (3.18) holds for all we obtain

Furthermore, by (3.15) yields

So is the desired minimizer.

We now show that holds. If , then we can find such that , and

| (3.19) |

which contradicts the minimality property of . Thus,

∎

Definition 3.6.

For an admissible strategy with value process we define its success ratio by

| (3.20) |

For we denote by the set

Remark 3.7.

Note that for we have that P-a.s. In particular, and hence (3.20) is well-defined.

In the following, we formulate the optimization problem (3.1) in terms of success ratios and prove that it is equivalent to (3.12), see Proposition 3.8 below.

Consider the minimization problem

| (3.21) |

Proposition 3.8.

Proof.

Note that

and thus

| (3.23) |

By Proposition 3.5, we know that the left hand side of (3.23) admits a solution . We prove that there exists such that

Define the the modified claim

By Theorem 7.13 of [14] there exists a minimal superhedging strategy with value process for such that

First, can be assumed to be admissible by Remark 3.1 and hence . Now, we show that . We have

| (3.24) |

where we used that is the value process of the minimal superhedging strategy of and . Therefore, we get

so and . It is left to show that P-a.s. By (3.24) we obtain . For the reverse direction we first show that is also a minimizer of the problem (3.13), i.e.,

Indeed, since is the value process of an admissible strategy, is a -martingale for all by Theorem 5.14 of [14] and thus we get that

| (3.25) |

where we used in the last equality that is the superhedging price of . In particular, is a minimizer. By the same arguments as in (3.19) it follows that

| (3.26) |

Thus, we get by (3.19) and (3.26) that

i.e., . Together with (3.24), this implies P-a.s. We have proved that and

In particular, solves (3.22) and the quantile hedging formulations of (3.12) and (3.21) are equivalent. ∎

Corollary 3.9.

The following convergence holds:

where denotes the success ratio associated to a portfolio as in (3.20).

Proof.

The proof is similar to the one of Theorem 3.4 and is omitted. ∎

3.2 Neural network approximation for

We now study how to approximate the superhedging price at by using neural networks.

We recall the following definition, see e.g. [4]. Common choices for below are and .

Definition 3.10.

Consider with , measurable and for any , let be an affine function. A function defined as

is called a (feed forward) neural network. Here the activation function is applied componentwise. denotes the number of layers, denote the dimensions of the hidden layers and , the dimension of the input and output layers, respectively. For any the affine function is given as for some and . For any the number is interpreted as the weight of the edge connecting the node of layer to node of layer . The number of non-zero weights of a network is , i.e. the sum of the number of non-zero entries of the matrices , , and vectors , .

For we denote the set of all possible neural network parameters corresponding to neural networks mapping by

With we denote the neural network with parameters specified by , see Definition 3.10. Recall that for , and for some -valued stochastic process . Then, any -measurable random variable can be written as for some measurable function . Using Theorem A.1, can be approximated by a deep neural network in a suitable metric.

The approximate superhedging price is then

|

|

(3.27) |

For the approximate -quantile hedging price is then

|

|

(3.28) |

For we also define the truncated approximate superhedging price and the truncated approximate -quantile hedging price with

|

|

(3.29) |

and

| (3.30) |

where the maximum and minimum are taken componentwise.

Assumption 1.

Suppose that

|

|

where denotes the -norm.

The next result shows that can be used as an approximation of the superhedging price .

Theorem 3.11.

Assume is bounded and non-constant. Further, suppose Assumption 1 is fulfilled. Then for any there exists and such that

| (3.31) |

Proof.

By Assumption 1 we can consider instead of . Set . Then for there exists a predictable strategy such that and Define by

| (3.32) |

Further, for define by

First, we prove that the limit of for tending to exists and that

| (3.33) |

Let be a sequence such that as tends to infinity. Then, since

and therefore , where , for . Thus, the limit is well-defined and . Furthermore, for and , there exists predictable such that and

| (3.34) |

For , define by

Then and hence as tends to infinity. Since for all we get by Theorem 5.14 of [14] for any that

| (3.35) | ||||

| (3.36) |

Recall that is a -dimensional -martingale, , and thus for all

Furthermore, converges to in probability as tends to infinity, since for any we have

because of (3.34). By dominated convergence we obtain that

and

Note that for dominated convergence, it is sufficient that converges only in probability. Taking to infinity in (3.35) and (3.36) yields

|

|

(3.37) |

As (3.37) holds for all we get by the superhedging duality that

Because was arbitrary, this implies

To conclude the proof of (3.33), we note that by definition and that . This implies that , and

hence (3.33) follows. We observe that for all . Furthermore, by (3.33) for there exists such that

| (3.38) |

which proves the second inequality in (3.31).

To prove the first inequality in (3.31), let be given. Consider

for . Then and therefore by continuity from below

Thus, we may choose such that . As is predictable, for each there exists a measurable function such that . By the universal approximation theorem [16, Theorem 1 and Section 3], see also Theorem A.1 in the appendix, with measure given by the law of under P, for each there exists such that

| (3.39) |

Define

By the definition of in (3.32), we get that

On we have for that

and hence on . Conversely, for such that

we get for that

and hence . In particular,

|

|

for all . Therefore, we get that with

and

On we have

and therefore

This inclusion and the Fréchet inequalities222For it holds that . yield

| P | |||

This proves the left inequality of (3.31). ∎

Remark 3.12.

Note that in the proof of Theorem 3.11 we compute both the price at and the superhedging strategy for the complete interval.

Remark 3.13.

Thanks to the universal approximation theorem in [16], we could in fact restrict our attention to neural networks with one hidden layer and the result in Theorem 3.11 remains valid. Thus, for each we could fix , , and consider instead the simpler parameter sets

Note the simpler form of , which is due to the fact that all one-hidden layer networks with hidden nodes can be written as one-hidden layer networks with hidden nodes and appropriate weights set to .

4 Superhedging price for

In this section we establish a method to approximate superhedging prices for . Using a version of the uniform Doob decomposition, see Theorem 7.5 of [14], the problem reduces to the approximation of the so-called process of consumption. In the first part, we build the theoretical basis for this approach. In the second part we prove that this method can be used to approximate the superhedging price for by neural networks.

4.1 Uniform Doob Decomposition

We briefly summarize some results on superhedging in discrete time in Corollary 2.4 below. For a more detailed overview we refer to Chapter 7 of [14].

Recall that denotes a discounted European claim satisfying

The superhedging price at , and the associated strategy can be calculated as in Section 3 and so we consider them as known. The remaining unknown component is the process of consumption given by (2.1). By Corollary 2.4,

is the smallest -supermartingale whose terminal value dominates . Consider the stochastic process defined as and for ,

| (4.1) |

where

| (4.2) |

Proof.

The proof follows by induction. For we have by definition. For the induction step assume that P-a.s. for some . First we observe that because is increasing and by the assumption of the induction step. In addition, by (2.3) we obtain

| (4.3) |

In particular, and thus P-a.s. Assume that . Then define by

First, we note that

and thus by Theorem 5.14 of [14] we have for any that

is -martingale for all . Further, by (4.3) and (2.1) we obtain

and

implies that for all and all . In particular, since is increasing and non-negative, we can conclude that is a -supermartingale for all . Furthermore, we show that P-a.s. for all . To this end, let be arbitrary, then we have by the -supermartingale property that

The terminal value of dominates by construction and since for all , we have

Then we obtain

which contradicts the fact that is the smallest -supermartingale whose terminal value dominates . Thus P-a.s. This concludes the proof. ∎

Remark 4.2.

In the definition of (4.1) we can equivalently consider , where

for . This is due to the fact that, on the one hand for all . On the other hand, for we have that and P-a.s. Therefore, for all .

4.2 Neural network approximation for

We now study a neural network approximation for the superhedging price process for . Throughout this section we use the notation of Section 3. For we define the set

where is the consumption process for introduced in (2.1). We now construct an approximation of by neural networks.

Proposition 4.3.

Assume is bounded and non-constant. Then for any there exist neural networks such that for all and

In particular, there exists a sequence of neural networks with for all and for all such that

Proof.

Fix and . Note that by definition. Let be given by the representation (4.1). Observe that the set from (4.2) is directed upwards. By Theorem A.33 of [14] there exists an increasing sequence

such that converges P-almost surely to as tends to infinity. Since almost sure convergence implies convergence in probability, there exists such that

| (4.4) |

For all there exist measurable functions such that . Fix . By the universal approximation theorem [16, Theorem 1 and Section 3], see also Theorem A.1 in the appendix, (with measure given by the law of under P) there exists and such that

By the triangle inequality and by De Morgan’s law we obtain that

In particular, we obtain by sub-addidivity that

Next, we show that . For this purpose, we note that

Therefore, we have that

|

|

which implies that . We set for and consider the neural network

where is given by (4.4). Then, for all and for all . Further, we have

which implies convergence in probability, i.e.,

By passing to a suitable subsequence, convergence also holds P-a.s. simultaneously for all . ∎

Let . Recursively, we define the set

| (4.5) | ||||

for , and the approximated process of consumption by and

| (4.6) |

Theorem 4.4.

Assume is bounded and non-constant. Then

Proof.

We prove the statement by induction. For we have by definition . Assume now that

for some . First we note that by (4.5) and (4.6), and because it follows that for all . Let and such that

Then, we can easily see that

We now prove that

| (4.7) |

On the one hand we have

which by Remark 4.2 implies that

On the other hand, let

and define . Then P-a.s. and

which implies that

and hence (4.7) follows. Further, we also have that

Therefore, we obtain by (4.7) that

and hence

| (4.8) |

For the converse direction let . By the proof of Proposition 4.3 there exists a neural network such that

Define the sets by

and

Then, . Note that by the assumption of the induction

For we have by construction,

For we get that

and

For we have

and

Thus, using that that and we get

| (4.9) |

Then, (4.9) implies

| (4.10) |

Because was arbitrary, it follows that P-a.s. by (4.10). By (4.8) and (4.10) we conclude that P-a.s. for all . ∎

5 Numerical results

In this section, we present some numerical applications for the results in Section 3 and 4. Combining Theorem 3.4 and 3.11, we obtain a two-step approximation for the superhedging price at . Then, we use Theorem 4.4 to simulate the superhedging process for .

5.1 Case

5.1.1 Algorithm and implementation

Let denote a fixed batch size. For fixed we implement the following iterative procedure: for each iteration step we generate i.i.d. samples of and consider the empirical loss function

with and denoting the squared rectifier function, i.e.,

We then calculate the gradient of at and use it to update the parameters from to according to the Adam optimizer, see [19]. After sufficiently many iterations , the parameter should be sufficiently close to a local minimum of the loss function

| (5.1) |

Note that is constant and hence is a constant. We obtain a small value for the first term of if representing the superhedging price is small. On the other side, the second summand in (5.1) is equal when the portfolio dominates the claim . Thus, minimizing the second summand in (5.1) corresponds to maximizing the superhedging probability. The weight offers the opportunity to balance between a small initial price of the portfolio and a high probability of superhedging. In particular, if is the minimum for the loss function , then is close to the minimal price required to superhedge the claim with a certain probability, i.e., to the quantile hedging price for a certain . In view of Theorem 3.11 we thus expect for large enough.

Also other choices for in (5.1) are possible. We considered the scaled sigmoid function for in (5.1). In this case, however, we did not obtain stable results.

The algorithm is implemented in Python, using Keras with backend TensorFlow to build and train the neural networks. More precisely, we create a Sequential object to build the models and compile with a customized loss function.

We use a Long-Short-Term-Memory network (LSTM), see [15], with the following architecture: the network has two LSTM layers of size , which return sequences and one dense layer of size . Between the layers the swish activation function is used. The activation functions within the LSTM layers are set to default, i.e., activation between cells is tanh and the recurrent activation is the sigmoid function. The kernel and bias initializer of the first LSTM layer are set to truncated normal, i.e., the initial weights are drawn from a standard normal distribution but we discard and re-draw values, which are more than two standard deviations from the mean. This gives trainable parameters. The training is performed using the Adam optimizer with a learning rate of or . We generate samples, which we split in for the training set and for the test set. The batch size is set to . We apply the procedure described above in two examples, which we present in the following.

5.1.2 Trinomial model

We consider a discrete time financial market model given by an arbitrage-free trinomial model with and

where is -measurable for , and takes values in with equal probability, where . Here, we set , , and and yielding possible paths. In this model, we want to superhedge a European Call option with strike price . For this choice of parameters the theoretical superhedging price is , as it can be easily obtained by the results of [9].

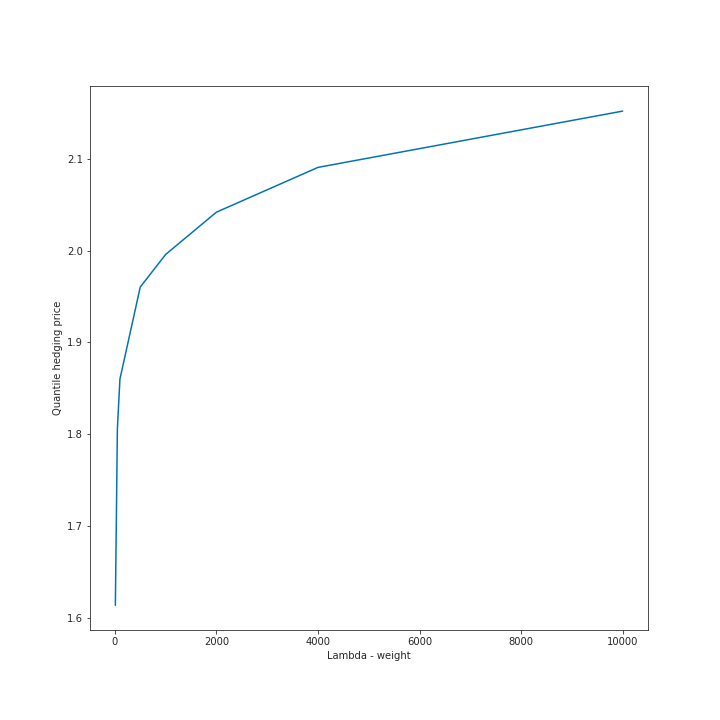

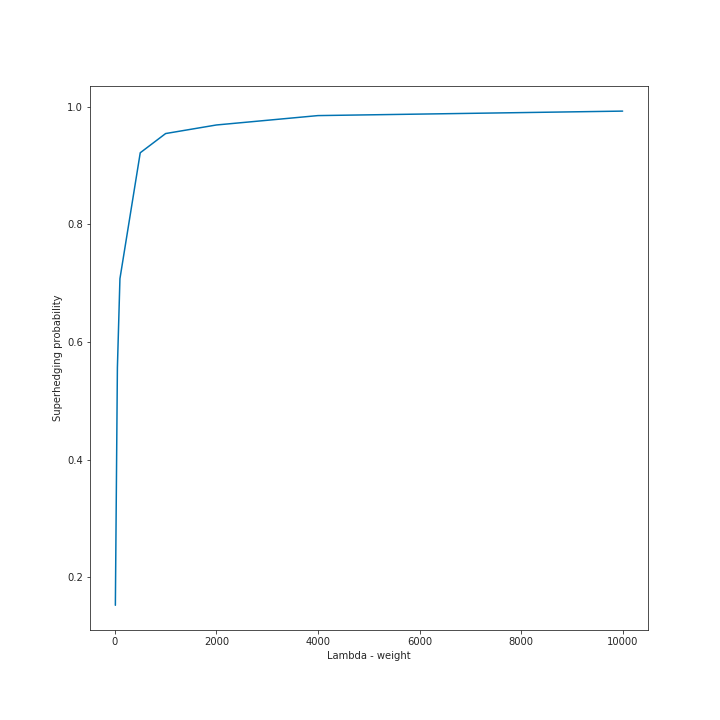

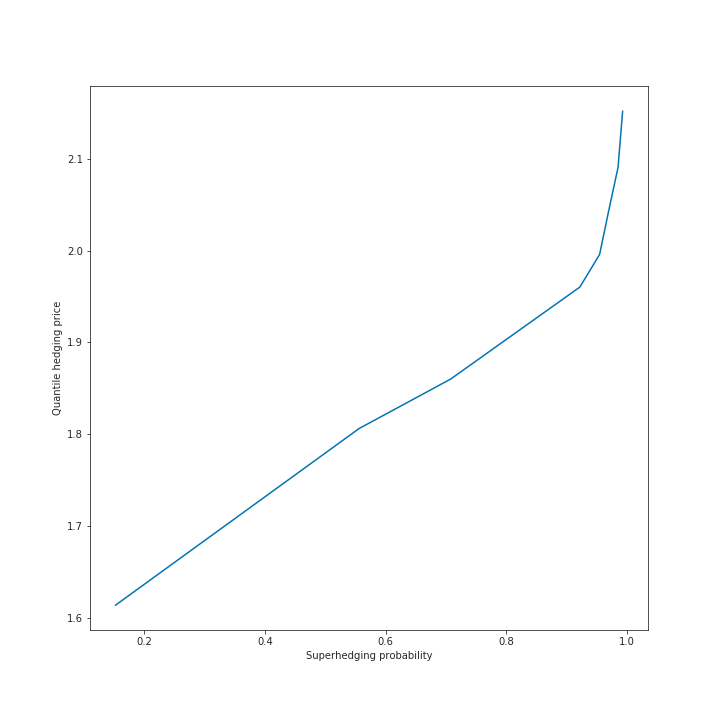

The network is trained and evaluated for different to illustrate the impact of in (5.1) and the relation between and the corresponding -quantile hedging price. More precisely, we consider . For each the network is trained over epochs.

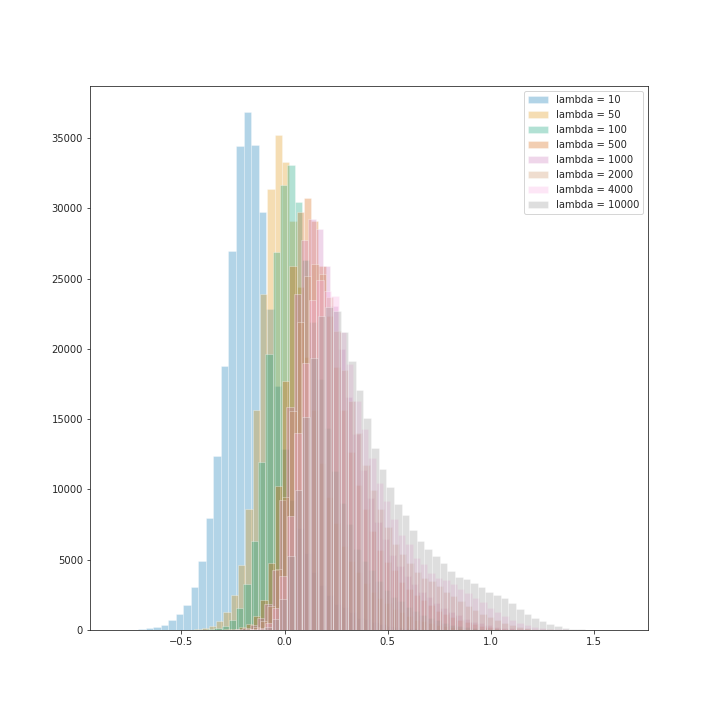

In Figure 1(a)-(c), we see that as well as the -quantile hedging price increase in , and that the -quantile hedging price increases in . Figure 1(d) shows the superhedging performance on the test set for all ’s, i.e., samples of

| (5.2) |

for each . Table 1 summarizes the values for , and the -quantile hedging price. In particular, for we obtain a numerical price of and .

| -quantile hedging price | ||

|---|---|---|

5.1.3 Discretized Black Scholes model

Here we consider a discrete time financial market given by a discretized Black-Scholes model for the asset price . We consider a Barrier Up and Out Call option with strike and upper bound such that and . We set , and . We assume to have trading days per year and a time horizon of trading days with daily rebalancing. In particular, for a European contingent claim the time until expiration for the option is .

The weight of the loss function is set to in order to obtain a high superhedging probability. Indeed, we obtain a superhedging probability of on the training set as well as on the test set with an approximate price of . By [7], the theoretical superhedging price is given by

In the Black-Scholes model the asset price process at time has unbounded support and thus the additional error, which arises from the discretization of the probability space, is non-negligible. Although the Barrier option artificially bounds the support of the model, the numerical price still significantly deviates from the theoretical price.

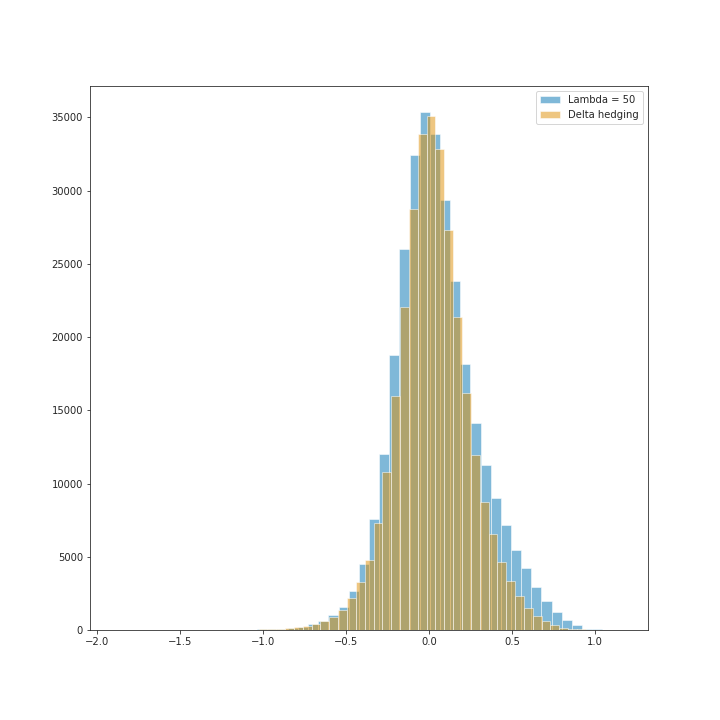

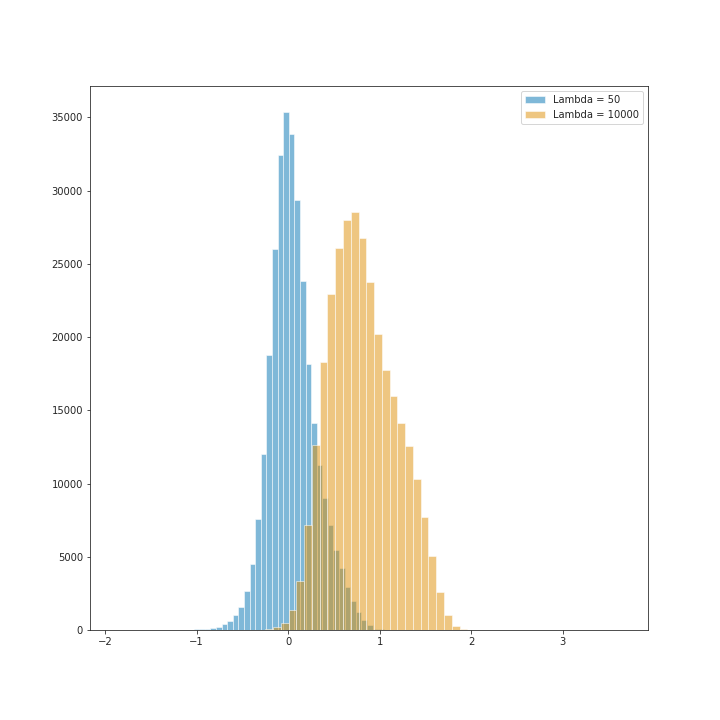

Finally, we consider a European call option with strike and parameters , and . By [7] the theoretical price of for the discrete time version of the Black-Scholes model is equal to . The theoretical price of in a standard Black-Scholes model in the continuous time is , and by following the -hedging strategy we superhedge with a probability of . Here we consider in (5.1) in order to compare the result to the discretized -hedging strategy of the Black-Scholes model, and in order to obtain a high superhedging probability. For , we obtain an approximate price of and a superhedging probability of . In Figure 2(a) we compare the -hedging strategy with the approximated superhedging strategy obtained for . Further, in Figure 2(b) we compare the results for and , respectively. For , the superhedging probability on the test set is with an approximated price of .

5.2 Case

In this section we approximate the process of consumption by neural networks as proposed in Section 4.2. We implement the same iterative procedure as introduced in Section 5.1.1. We define as the difference of the approximated superhedging strategy obtained from Section 5.1 and the claim , i.e.,

|

|

Then, the empirical loss function is given by

where is given by

At a local minimum the two terms of guarantee that is as big as possible but less or equal than .

Here, we also consider a discretized Black-Scholes model as in Section 5.1.3 but only a time horizon of trading days and set , and . For each the neural network consists of two LSTM layers of size and respectively, which return sequences, one LSTM layer of size providing one single value and one dense layer of size . The remaining parameters are chosen as in Section 5.1.1.

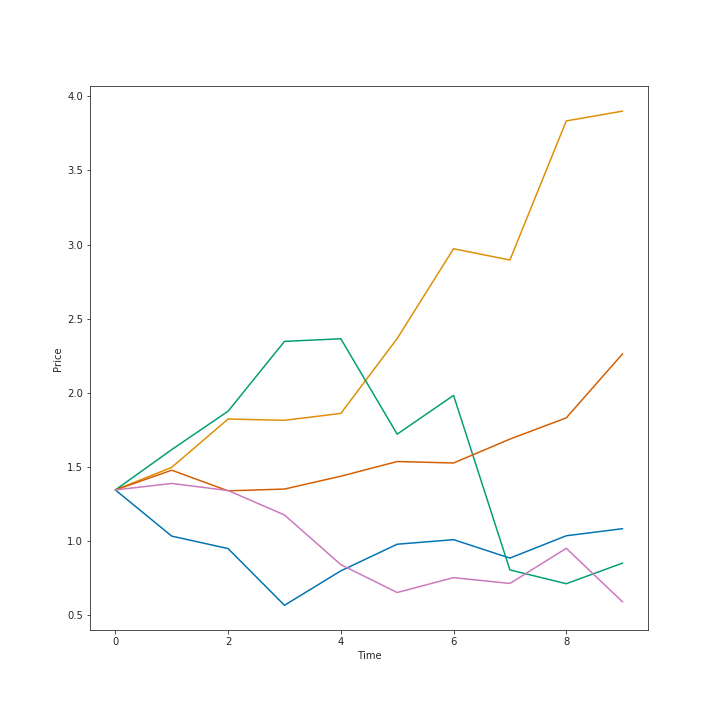

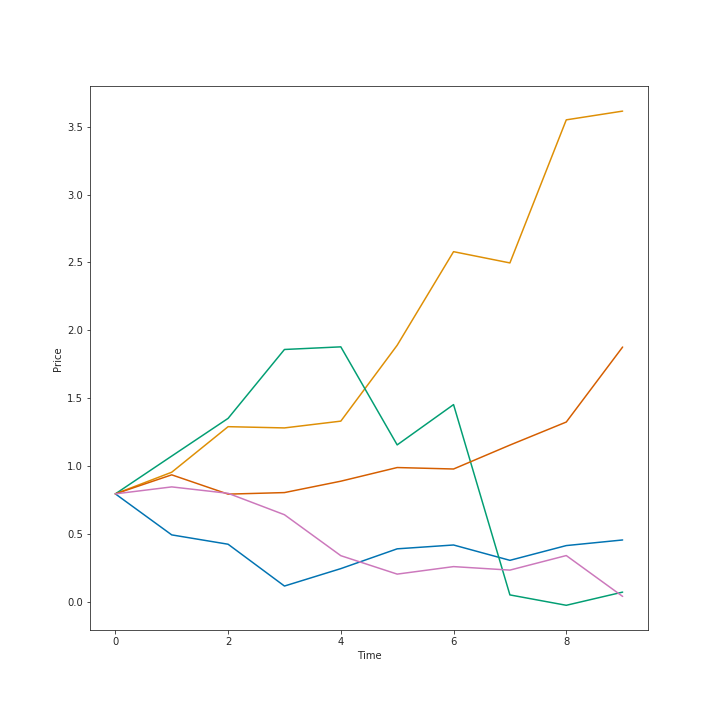

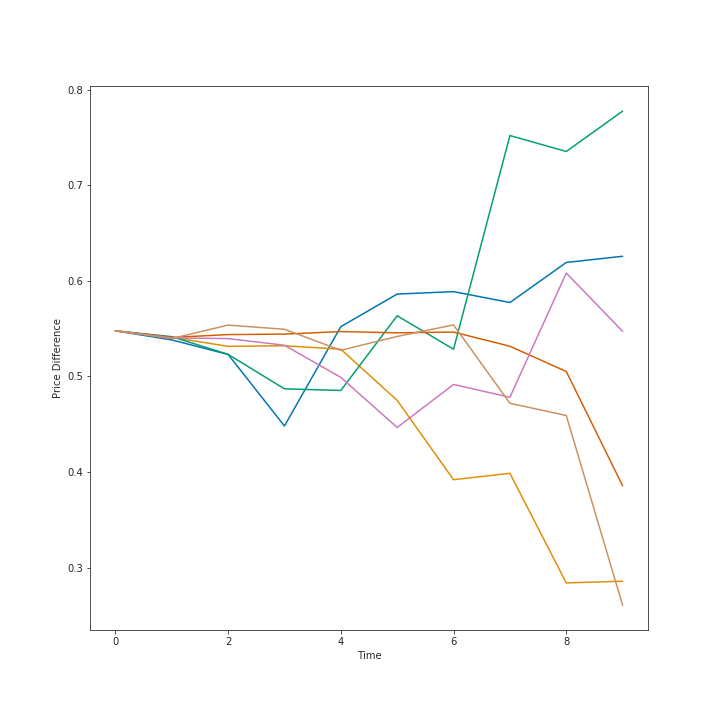

As in Section 5.1.3, we compute an approximated superhedging price and strategy for the complete interval. Setting yields an approximated price of and a superhedging probability of for . For , we choose and then obtain a superhedging probability of . In Figure 3(a), we show trajectories of the approximated superhedging price process generated by this method. Figure 3(b) illustrates paths given by the -hedging strategy of the discretized Black-Scholes model. Finally, we plot the difference of the approximated superhedging price processes and the corresponding price process obtained by the -hedging strategy in Figure 3(c).

5.3 Discussion

In finite market models as in Section 5.1.2, our methodology delivers an approximation of -quantile hedging and approximated superhedging prices with small approximation error. It is also worth noting, that the predicted superhedging price and the corresponding superhedging probability of the training set are consistent with the values on the test set.

In contrast, in models in which the price process has unbounded support, our numerical results indicate that the additional error caused by the discretization of the probability space cannot be ignored. However, we obtain consistent results of the -quantile hedging price for the training set and test set. Note also that, in Section 5.1.3, the Barrier option can be superhedged with on the training and on the test set.

A further possible application of our methodology is given by superhedging in a model-free setting on prediction sets, see [1], [2], [17], where prediction sets offer the opportunity to include beliefs in price developments or to select relevant price paths.

Appendix A Neural Networks

For the reader’s convenience we recall some results on neural networks. The following result essentially follows from [16, Theorem 1]. For completeness we include its proof here.

Theorem A.1.

Assume is bounded and non-constant. Let be a measurable function and be a probability measure on . Then for any there exists a neural network such that

References

- [1] Bartl, D., Kupper, M., and Neufeld, A. Pathwise superhedging on prediction sets. Finance and Stochastics 24, 1 (2020), 215–248.

- [2] Bartl, D., Kupper, M., Prömel, D. J., and Tangpi, L. Duality for pathwise superhedging in continuous time. Finance and Stochastics 23, 3 (2019), 697–728.

- [3] Becker, S., Cheridito, P., and Jentzen, A. Deep optimal stopping. Journal of Machine Learning Research 20 (2019), 74.

- [4] Buehler, H., Gonon, L., Teichmann, J., and Wood, B. Deep hedging. Quantitative Finance 19, 8 (2019), 1271–1291.

- [5] Burzoni, M., Frittelli, M., Maggis, M., et al. Model-free superhedging duality. Annals of Applied Probability 27, 3 (2017), 1452–1477.

- [6] Campi, L., and Schachermayer, W. A super-replication theorem in kabanov’s model of transaction costs. Finance and Stochastics 10, 4 (2006), 579–596.

- [7] Carassus, L., Gobet, E., and Temam, E. A class of financial products and models where super-replication prices are explicit. In Stochastic Processes and Applications to Mathematical Finance. World Scientific, 2007, pp. 67–84.

- [8] Carassus, L., Obłój, J., and Wiesel, J. The robust superreplication problem: a dynamic approach. SIAM Journal on Financial Mathematics 10, 4 (2019), 907–941.

- [9] Carassus, L., and Vargiolu, T. Super-replication price for asset prices having bounded increments in discrete time.

- [10] Cuchiero, C., Khosrawi, W., and Teichmann, J. A generative adversarial network approach to calibration of local stochastic volatility models. arXiv preprint arXiv:2005.02505 (2020).

- [11] Cvitanić, J., and Karatzas, I. Hedging and portfolio optimization under transaction costs: A martingale approach 1 2. Mathematical Finance 6, 2 (1996), 133–165.

- [12] El Karoui, N., and Quenez, M.-C. Dynamic programming and pricing of contingent claims in an incomplete market. SIAM Journal on Control and Optimization 33, 1 (1995), 29–66.

- [13] Föllmer, H., and Leukert, P. Quantile hedging. Finance and Stochastics 3 (1999), 251–273.

- [14] Föllmer, H., and Schied, A. Stochastic finance: an introduction in discrete time, 4th rev. ed. ed. Walter de Gruyter, 2016.

- [15] Hochreiter, S., and Schmidhuber, J. Lstm can solve hard long time lag problems. Advances in neural information processing systems (1997), 473–479.

- [16] Hornik, K. Approximation capabilities of muitilayer feedforward networks. Neural Networks 4, 1989 (1991), 251–257.

- [17] Hou, Z., and Obłój, J. Robust pricing–hedging dualities in continuous time. Finance and Stochastics 22, 3 (2018), 511–567.

- [18] Kabanov, Y. M., and Last, G. Hedging under transaction costs in currency markets: a continuous-time model. Mathematical Finance 12, 1 (2002), 63–70.

- [19] Kingma, D. P., and Ba, J. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980 (2014).

- [20] Kramkov, D. O. Optional decomposition of supermartingales and hedging contingent claims in incomplete security markets. Probability Theory and Related Fields 105, 4 (1996), 459–479.

- [21] Nutz, M. Robust superhedging with jumps and diffusion. Stochastic Processes and their Applications 125, 12 (2015), 4543–4555.

- [22] Nutz, M., and Soner, H. M. Superhedging and dynamic risk measures under volatility uncertainty. SIAM Journal on Control and Optimization 50, 4 (2012), 2065–2089.

- [23] Obłój, J., and Wiesel, J. Robust estimation of superhedging prices. The Annals of Statistics 49, 1 (2021), 508–530.

- [24] Ruf, J., and Wang, W. Neural networks for option pricing and hedging: a literature review. Journal of Computational Finance, Forthcoming (2020).

- [25] Schachermayer, W. The super-replication theorem under proportional transaction costs revisited. Mathematics and Financial Economics 8, 4 (2014), 383–398.

- [26] Soner, H. M., Shreve, S. E., Cvitanic, J., et al. There is no nontrivial hedging portfolio for option pricing with transaction costs. The Annals of Applied Probability 5, 2 (1995), 327–355.

- [27] Touzi, N. Martingale inequalities, optimal martingale transport, and robust superhedging. ESAIM: Proceedings and Surveys 45 (2014), 32–47.