Sparse estimation for generalized exponential marked Hawkes process

Abstract

We established a sparse estimation method for the generalized exponential marked Hawkes process by the penalized method to ordinary method (P-O) estimator. Furthermore, we evaluated the probability of the correct variable selection. In the course of this, we established a framework for a likelihood analysis and the P-O estimation when there might be nuisance parameters, and the true value of the parameter might be at the boundary of the parameter space. Finally, numerical simulations are given for several important examples.

1 Introduction

The Hawkes process is a self-exciting point process introduced by [13] and has a wide range of applications including seismic (see [16]), finance (see [1]), and web data analysis (see [11]). For the properties as a stochastic process, a class with exponential kernels has attracted much attention since its intensity process has Markov, geometric ergodic, and mixing properties, for example, see [7] and [10]. As an extension of the Hawkes process, the marked Hawkes process is known. By the marked Hawkes process, it is possible to consider a model that adds the scale of the event and other characteristics to the occurrence times of the events. The properties of the marked Hawkes process were investigated by [6], and in which an important class called the generalized exponential marked Hawkes process (GEMHP) was introduced. The GEMHP is a marked Hawkes process whose kernel has the flexible form, which is generated by terms multiplying , where , by a polynomial or trigonometric function. The GEMHP can be represented in terms of a Markov process, and we can establish the geometric ergodicity of the GEMHP. Moreover, the convergence of moments for the quasi maximum likelihood estimator (QMLE) and the quasi Bayesian estimator (QBE) was established, in [6], for a class of the GEMHP with a linear intensity. In particular, a polynomial type large deviation inequality was established for the quasi-likelihood of the GEMHP in the application of the results of the quasi-likelihood analysis in [21]. The GEMHP with a linear intensity has been used for the models of earthquakes marked with the magnitude (see [16]), the limit order book in financ (see [18]), etc. In this paper, we introduce the Hawkes process marked by ”topic” as an example of the GEMHP with a linear intensity.

Model selection is one of the most important topics in statistical inference. In particular, sparse estimation methods like the least absolute shrinkage and selection operator (LASSO) in [20], the elastic net in [24], and so on, have been widely studied starting from linear regression problems. By the sparse estimation method, we can execute parameter estimation and variable selection simultaneously. Let be the true parameter of a parameter for . Moreover, let and . We write for a vector and an index set . The following two properties are called the oracle properties (see [9]) that the sparse estimator should satisfy:

-

•

Selection consistency: ,

-

•

Asymptotic normality: ,

as for some positive definite matrix , where represents an observation time, and we omit in the expression and . We focus on the penalized method to ordinary method (P-O) estimator proposed in [19]. The P-O estimation is a sparse estimation method using the least-squares approximation method given a prior estimator with the consistency, and retuning using an ordinary estimation method such as the maximum likelihood estimator. It satisfies the oracle properties under the suitable conditions. Moreover, we can evaluate the probability of the correct variable selection.

A sparse estimation for the multivariate Hawkes process is useful to identify disconnections in networks. It is also possible to identify which marks do not affect the trend by a sparse estimation for the marked Hawkes process. Furthermore, it is also important that a sparse estimation prevents the overfitting of the model. In a previous study applying a sparse estimation to the Hawkes process, [12] proposed an adaptive -penalized methodology for the nonparametric case and evaluated the oracle inequality. In the parametric case, there are several studies with respect to the Hawkes process using the exponential kernel. In [22], they designed the log-likelihood function penalized by the nuclear and norm and an algorithm ADM4 for their estimation method, while they investigated the performance of their method through numerical experiments. In [4], they proposed the least-squares method with the entry-wise weighted nuclear and norm penalization and proved a sharp oracle inequality for their procedure. In [11], they introduced a hybrid method combined with the QMLE and the -penalized QMLE and investigated the accuracy of model selection and the asymptotic normality through numerical experiments. However, the oracle properties have not been established even for the exponential Hawkes process with no marks.

We apply the P-O estimation to the GEMHP, and we prove the oracle properties and evaluate the probability of the correct variable selection. In this application, when the GEMHP contains zero parameters, it is often necessary to assume the existence of nuisance parameters. For example, let be a -dimensional exponential Hawkes process with the intensity process

| (1.1) |

where , , and are parameters for . Then, is undefined, that is, is a nuisance parameter, when . We confirm that the polynomial type large deviation inequality for the quasi-likelihood of the GEMHP with nuisance parameters holds and thus that the consistency for the QMLE and the QBE holds. Furthermore, in most cases of statistical inference, the true value of a parameter is represented as an interior point on a compact set. However, when the true value of a parameter in the GEMHP is zero, it might be at the boundary of the parameter space. For an example of an exponential Hawkes process with the intensity (1.1), ’s are often assumed to take value in a compact subset in . Then, is realized on the boundary of the parameter space. We prove that the P-O estimator works well even in such a situation where the true value is on the boundary.

We explain the GEMHP and its properties in Section 2. In Section 3, we discuss the P-O estimator under the condition that some parameters are nuisance parameters and the true parameter is possibly on the boundary of the parameter space. The main results about the application of the P-O estimation to the sparse GEMHP are in Section 4. Finally, Section 5 presents the results of some numerical experiments. We introduce the Hawkes process marked by ”topic” in this section. The proofs of each statement are given in Appendix A. Moreover, we give Additional numerical experiments in Appendix B.

2 Generalized exponential marked Hawkes process

In this section, we review the theory in [6]. In particular, we define the generalized exponential marked Hawkes process (GEMHP). The GEMHP is a class of marked Hawkes processes that satisfies the Markov, ergodic, and mixing properties under the stability conditions. In this article, we only focus on the GEMHP with the linear form intensity for our application in Section 4. On the other hand, we note that the Markov, ergodic, and mixing properties are proved for more general non-linear (sub-linear) form intensities.

2.1 Marked point process

First, we define the general marked point process. Let be a stochastic basis, and be a measurable space. For , we consider a sequence of couples . Suppose that ’s are -stopping times such that almost surely and as hold for each , and ’s are -valued -measurable random variables. We define the -dimensional marked point process as a family of random measures on such that . Moreover, we call a random measure the compensator of when is a local martingale for any , see Theorem 1.8 in [14].

2.2 Generalized exponential marked Hawkes process

We use the same notations in Subsection 2.1. We write the counting process associated with as and jump times of the global counting process as . Furthermore, let be a permutation of similar to the relationship between jump times and . Then, we define the mark process as a piecewise constant and right continuous stochastic process such that for where and . The marked Hawkes process is defined as below.

Definition 2.1.

A -dimensional marked point process is called a -dimensional marked Hawkes process if the intensity process of the associated counting process has the form

where is a continuous function and is a measurable function for each .

Then, the linear GEMHP is defined by restricting the form of the function and the kernel function . For , we denote the Frobenius inner product on a real matrix space as .

Definition 2.2.

A -dimensional marked Hawkes process is called a -dimensional linear generalized exponential marked Hawkes process if the function and the kernel function have the representations, for ,

and

where and are measurable functions, for some , and is the matrix exponential for each . That is, its intensity process has the form

for .

The temporal part of the kernel is represented as a linear combination of terms , where and are constants, and is a polynomial for and some , see Proposition 3.1 of [6].

The remainder of this section is devoted to the explanation of the sufficient conditions of Theorem 2.3. We restrict the distribution of the mark process to maintain the Markov structure of the intensity process. Let be labels of the jumps of the global counting process , i.e., is a -valued random variable such that for . We write . Then, we assume that there exists a family of Feller transition kernels on such that

| (2.1) |

for any and . For the stability of the process, we assume that has eigenvalues with positive real parts. We define and for . refers to the conditional expectation of the long-run effect of the excitation on the intensity process after a jump. refers to the conditional expectation of a jump size in when jumps. By the assumption on , we have the representation for any .

Let

| (2.2) |

for and . obviously drives the intensity process of the GEMHP. We write the transition kernel of the global mark process by . It satisfies

where and for and , see Proposition 3.2 of [6]. We call a non-negative function a norm-like function if as holds. The following statements are the sufficient conditions for the geometric ergodicity and the geometric mixing property of the GEMHP.

- [L1]

-

There exist norm-like functions and such that

(2.3) (2.4) (2.5) and there exists such that

(2.6) - [L2]

-

There exist with positive coefficients and such that, component-wise, .

- [ND1]

-

There exist such that and for any .

- [ND2]

-

The transition kernel admits a reachable point . Moreover, for any , the transition kernel admits a sub-component , such that there exist a lower semi-continuous function and a non-trivial measure on , such that

-

for any non-empty open set ,

-

and for any and .

-

We write the transition kernel of as for . Finally, the -norm of a measure on a measurable space is defined as

for a positive function , where the supremum is taken over all the measurable functions such that for all . The following theorem is the main theorem in this section, which is shown in Theorem 3.7 of [6].

Theorem 2.3.

(Theorem 3.7 in [6]) Under [L1]-[L2] and [ND1]-[ND2], is -geometrically ergodic, i.e., there exist a unique invariant measure and constants such that for any and

where . Moreover, is -geometrically mixing, i.e., there exist positive constants , such that for any and measurable functions with ,

3 P-O estimator with nuisance parameter

The penalized method to ordinary method (P-O) estimator was introduced by [19]. The P-O estimator allows us to execute parameter estimation and variable selection simultaneously. In this section, we extend the applicable condition of the P-O estimation to the case where nuisance parameters might exist, and the true parameter might be at the boundary of the parameter space. In general, a parameter that is not subject to estimation is called a nuisance parameter. In particular, we admit a nuisance parameter whose true value might be undefined.

Let be a parameter, where , and are open convex bounded subsets of , and for , respectively. is a parameter that might take the value for some . is a non-zero parameter. is a nuisance parameter that might take the value for some . is a nuisance parameter that takes a non-zero value. Note that and might not have the true value. Suppose that is the true parameter, and let and . We write . We remark that might be on the boundary of .

Example 3.1.

Let be a GEMHP with the intensity : Here, for ,

where are non-negative parameters and is the true parameters with nuisance parameters. We can consider the situation where some and might be besides and are always positive. In this case, and are undefined parameters, and thus nuisance parameters, when for all . In other words, we can write , , , and , where . Then, we can rewrite .

Let be an observation time index. We often consider the case where with discrete time observation or with continuous time observation. For convenience of explanation, we consider two objective functions and . For example, and are log-likelihood functions multiplied by . The objective function will be defined later. We denote the -th component of each estimator as by omitting . If is realized at multiple points, we take one of them arbitrarily. The P-O estimation is done in the following three steps:

- Step 1.

-

We obtain the first estimator of by

- Step 2.

-

We obtain the second estimator of by

where the objective function depends on the first estimator .

- Step 3.

-

We obtain the third estimator of by

where , , , and .

We call the P-O estimator. The sparse model selection is derived from Step 2. The objective function is constructed by using the first estimators as below:

| (3.1) |

where , and are deterministic sequences. We remark that and depend on . We often choose and to converge to as , see Remark 3.4. Let and .

We retune the estimator in Step 3. We rewrite the notation in Step 3 to describe the properties of components with the non-zero true values in the third estimator. Without loss of generality, we can assume that and its true value . Let and

By contrary, we write . We call a stochastic process is -bounded if holds for all . We introduce sufficient conditions for the oracle properties of the above P-O estimator. Note that the following assumptions demand the properties of the first and third-step estimators. In other words, it is not necessary to assume the objective functions and to establish the oracle properties of the P-O estimator.

Assumption 3.2.

-

(i)

is -consistent, that is, as .

-

(i)′

is -bounded.

-

(ii)

and as .

-

(iii)

as , where is a positive definite matrix for any , and is a -dimensional standard Gaussian random vector.

-

(iv)

There exists such that as .

-

(v)

is -bounded.

Remark 3.3.

Assumption 3.2 (i)′ is obviously a stronger condition than (i). We need (i)’ to evaluate the probability of a correct variable selection for the P-O estimator. In the case where and are the quasi log-likelihood functions, (i)’ and (v) are satisfied if the polynomial type large deviation inequality for the quasi likelihood ratio random field holds, see Proposition 1 in [21].

Remark 3.4.

Assumptions 3.2 (ii) and (iv) are conditions on the weight of the penalty term. These conditions are satisfied, for example, in the following setup under Assumption 3.2 (i). We take for given and . Moreover, we take positive deterministic sequences that satisfy and . Then, as ,

and

Moreover, as holds for .

The following theorem is the main theorem in this section. The statement (i) means the selection consistency in Step 2. Moreover, the statements (ii) and (iv) say that the probability of a correct variable selection converges to in a polynomial decay as . The statement (iii) is about the asymptotic normality of the P-O estimator. In particular, the statements (iii) and (iv) mean the oracle properties of the P-O estimator. Compared to the result of [19], each statement is extended to in the situation where nuisance parameters might exist and the true parameter might be at the boundary of the parameter space.

Theorem 3.5.

4 Application to GEMHP

In this section, we apply the penalized method to ordinary method (P-O) estimator to the generalized exponential marked Hawkes process (GEMHP).

For tractability, we restrict the intensity of the GEMHP to a linear form, that is, for any . When is sub-linear, more involved formulations for the conditions [AH1]-[AH2] below are needed, and we let it aside for future works as in Section 4 of [6]. We set a parameter as in Section 3. For some , we assume that is a -dimensional GEMHP with the following intensity process:

| (4.1) |

for , where , are measurable functions, and the real parts of the eigenvalues of are dominated by some independently of , for some and each . We assume that there exist the Feller transition kernels of the mark process similar to (2.1). Moreover, we restrict the structure of the mark transition kernel . We assume that there exists a dominating measure on which induces the density , i.e.,

for any and . Then, we have the following representation of the compensator of :

where is the mark process defined as in Subsection 2.1. We write . Let be an observation time index. We consider the quasi log-likelihood function with respect to the above GEMHP:

| (4.2) | |||||

Here, is the part related to the counting process and to the mark process . We remark that is actually equivalent to the log-likelihood function related to if the filtration satisfies the appropriate condition, see the condition (2.12) and Theorem 5.43 in [14]. However, we call the ”quasi” log-likelihood function since we allow here to take a more general filtration . We consider the P-O estimator whose first and third objective functions are set to this quasi log-likelihood function. The quasi maximum likelihood estimator (QMLE) is defined as a quantity satisfying

and we set this QMLE as the first-step estimator. Similar to as in Section 3, we set the second-step estimator of by

and the third-step estimator of by

where is the same as (3.1), and are defined in Step 3 of the P-O estimator in Section 3.

Remark 4.1.

The results in this section also hold if we consider the quasi Bayesian estimator (QBE)

instead of the QMLE by changing notations in Step 1 and Step 3 in Section 3, where is a continuous prior density with .

We define the quasi likelihood ratio random field as

| (4.3) |

As mentioned in Remark 3.3, if satisfies the polynomial type large deviation inequality (PLD), we can show that Assumption 3.2 (i)’ and (v) holds for the above P-O estimator. Therefore, to obtain the PLD, we prepare additional conditions [AH1]-[AH3] beside the conditions [L1]-[L2], [ND1]-[ND2]. We sometimes rewrite as , where and . We also write , where is the true value and is an arbitrary point in . We call that is of class for some if is of class and its derivatives admit continuous extensions on .

- [AH1]

-

-

(i)

For any and , , , , , are in .

-

(ii)

For any and , if and only if

-

(i)

- [AH2]

-

For any , , and , there exists which may depend on such that

-

(i)

,

-

(ii)

,

where is a norm-like function in [L1], and is a positive constant in Theorem 2.3.

-

(i)

The conditions [AH1] and [AH2] are sufficient conditions to leads the conditions [A1]-[A3] in Appendix A.2. [AH1] is the regularity condition for the intensity process, which leads to [A1]. [AH2] is closely related to [A2] and is used for the evaluation of moments of the quasi log-likelihood process. Let the quasi log-likelihood random field be

The -geometric ergodicity of the GEMHP and [AH1]-[AH2] guarantee the existence of the limit field

where is the density of the predictable compensator of the stationary version at time , see Lemma 4.1 in [6]. For this , we consider the following identifiability condition.

- [AH3]

-

.

Moreover, we write .

Remark 4.2.

is of class by the condition [A3] in Appendix. Then, the condition [AH3] is equivalent to the two following conditions:

-

(i)

for any and .

-

(ii)

is positive definite uniformly in .

Let and . The following theorem says that the quasi likelihood ratio random field satisfies the PLD.

Theorem 4.3 (Polynomial type large deviation inequality).

Under [L1]-[L2], [ND1]-[ND2], and [AH1]-[AH3], for any , there exists such that

where is defined in (4.3). In particular, is -bounded.

5 Examples and Simulation Results

In this section, we show the numerical simulation result for Theorem 4.4. Experiments in the scenario with no zero parameters and a comparison with previous studies are presented in Appendix B. All experiments are done by using Python3.111The code is available on the GitHub page https://github.com/goda235/Sparse-estimation-for-GEMHP. We consider the same notations and restrictions in Section 4. Moreover, let be as in Section 2. We write , where is the mark process and is the generalized elementary excitation process defined by (2.2). The value of the GEMHP’s intensity process is updated based on the value of for as follows:

for . Then, a path of the GEMHP can be simulated by using the above computation and Ogata’s method, see [17]. In the following subsections, we see the oracle properties of the P-O estimator for the GEMHP via numerical experiments for two basic models. For each model, we calculate the QMLE and the P-O estimator 300 times, respectively, while changing the observation time to , and . Here, all optimizations are done by the limited memory Broyden-Fletcher-Goldfarb-Shanno method for bound-constrained (L-BFGS-B), see [23].

5.1 Multivariate Exponential Hawkes process

First, we focus on the non-marked, however, quite important, Hawkes process.

5.1.1 Definition

We consider the multivariate exponential Hawkes process with the intensity

| (5.1) |

for , where is a parameter, is the true value, and is an open convex bounded parameter space. We assume the following conditions.

Assumption 5.1.

-

(i)

Some might be besides all and are positive. Moreover, .

-

(ii)

The spectral radius of is less than .

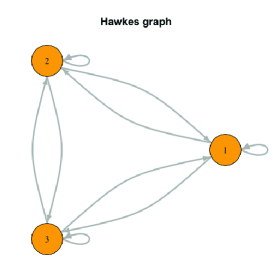

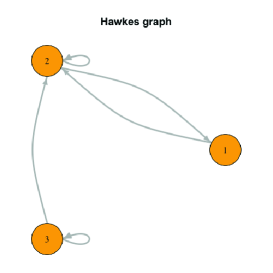

In (i), we assume that are away from to control the oscillation of the nuisance parameter. (ii) is a stability condition related to [L2]. We write , , and . The multivariate exponential Hawkes process has been used in various fields, for example, a model of limit order books in finance (see [1]), a model of the time of posting texts on social media (see [11]), etc. The directed graph whose each vertice corresponds to the value of and each edge corresponds to the excitability value of is called the Hawkes graph, see [8]. The Hawkes graph allows visualizing the structure of the mutual excitations in a model. The means that the effect of an event on the probability of the occurrence of an event is zero, i.e., the edge from to is disconnected in a Hawkes graph, see Figure 1.

For the multivariate exponential Hawkes process, the oracle properties of the P-O estimation holds by Theorem 4.4.

5.1.2 Simulation Results

Let be a -dimensional exponential Hawkes process with the following parameters:

where means a non-definite value. We set the hyperparameters of the P-O estimator in Remark 3.4 to be , the observation times , and the number of the Monte Carlo simulation . Table 1 shows the fraction of trials in which the parameter ’s are estimated to be completely zero. We can see that the variable selection is performed more accurately by the P-O estimator than by the QMLE as becomes larger.

| QMLE: T=100 | |||||

|---|---|---|---|---|---|

| 71.7% | 11.7% | 52.7% | |||

| 5.67% | 51.3% | 5.00% | |||

| 60.0% | 58.3% | 26.7% | |||

| QMLE: T=500 | |||||

| 62.7% | 0.00% | 54.0% | |||

| 0.00% | 11.3% | 0.00% | |||

| 58.7% | 54.7% | 0.00% | |||

| QMLE: T=3000 | |||||

| 58.0% | 0.00% | 50.0% | |||

| 0.00% | 0.00% | 0.00% | |||

| 54.3% | 57.0% | 0.00% | |||

| P-OE: T=100 | |||||

|---|---|---|---|---|---|

| 84.3% | 30.7% | 66.3% | |||

| 27.3% | 67.3% | 11.0% | |||

| 80.3% | 82.0% | 42.0% | |||

| P-OE: T=500 | |||||

| 83.3% | 3.67% | 72.7% | |||

| 1.67% | 34.0% | 0.00% | |||

| 84.7% | 83.7% | 6.33% | |||

| P-OE: T=3000 | |||||

| 87.7% | 0.00% | 79.0% | |||

| 0.00% | 3.33% | 0.00% | |||

| 87.3% | 88.7% | 0.00% | |||

Remark 5.3.

In Table 1, the QMLE asymptotically correctly estimates about 50% of the zero parameters. This phenomenon is derived from the local asymptotic normality on the restricted parameter space to a positive region, see [11] for an intuitive but more detailed explanation. There are few studies of the maximum likelihood method on the constrained parameter space using as a variable selection method. In an i.i.d. case, the asymptotic behavior of the maximum likelihood estimator is discussed under general assumptions where we can consider such a constrained parameter space, see [15]. The same phenomenon is observed in Table 3 below.

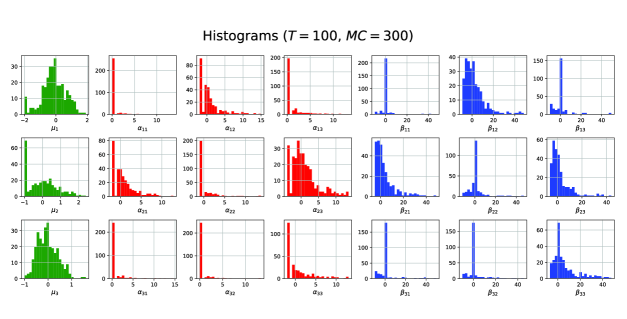

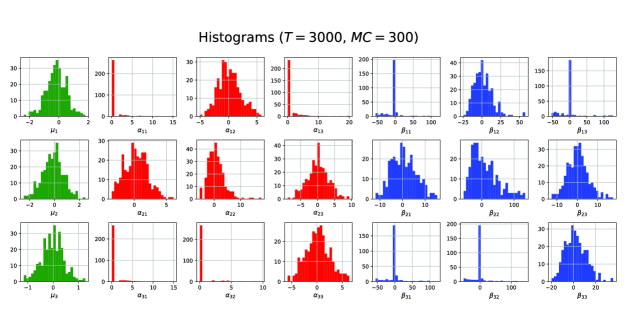

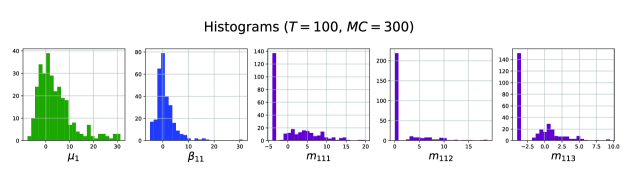

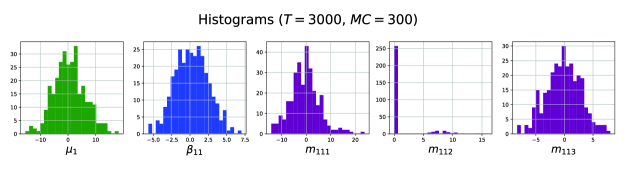

Figure 2 shows histograms of the error distribution of the P-O estimator, that is, histograms of the values of . It seems that the distribution is close to the normal distribution as becomes larger.

Table 2 shows the averages of squared errors of the QMLE and the P-O estimator . For non-zero parameters, owing to the asymptotic normality, both the QMLE and the P-O estimator have asymptotically the same level of variance. For zero parameters, we can guess that the P-O estimator asymptotically has a smaller error than the QMLE, due to the accurate model selection. However, when the observation time is small, the performance of the QMLE is better due to the miss model selection of the P-O estimator.

| Method | |||||||

|---|---|---|---|---|---|---|---|

| 100 | QMLE | 6.80e-03 | 5.63e-03 | 3.09e-03 | 5.90e-01 | 1.15e-00 | 4.89e-00 |

| P-OE | 5.79e-03 | 6.73e-03 | 1.80e-03 | 6.34e-01 | 1.19e-00 | 5.01e-00 | |

| 500 | QMLE | 1.58e-03 | 1.81e-03 | 8.06e-04 | 1.61e-02 | 1.41e-02 | 1.03e-01 |

| P-OE | 1.24e-03 | 1.80e-03 | 3.62e-04 | 2.16e-02 | 1.39e-02 | 9.51e-02 | |

| 3000 | QMLE | 2.59e-04 | 2.44e-04 | 1.84e-04 | 1.81e-03 | 1.28e-03 | 4.19e-03 |

| P-OE | 1.68e-04 | 2.43e-04 | 6.17e-05 | 1.72e-03 | 1.26e-03 | 4.76e-03 |

| Method | |||||||

|---|---|---|---|---|---|---|---|

| 100 | QMLE | 3.78e-01 | 1.38e-00 | 1.47e-00 | 1.66e-00 | 5.75e-01 | 4.73e-01 |

| P-OE | 4.89e-01 | 1.51e-00 | 1.77e-00 | 1.77e-00 | 1.06e-00 | 6.64e-01 | |

| 500 | QMLE | 9.07e-03 | 1.01e-01 | 2.26e-02 | 8.13e-03 | 5.51e-02 | 1.87e-02 |

| P-OE | 9.26e-03 | 1.02e-01 | 2.20e-02 | 8.17e-03 | 5.50e-02 | 1.86e-02 | |

| 3000 | QMLE | 1.09e-03 | 3.81e-03 | 3.15e-03 | 1.07e-03 | 1.82e-03 | 1.95e-03 |

| P-OE | 1.09e-03 | 3.96e-03 | 3.13e-03 | 1.03e-03 | 1.77e-03 | 1.91e-03 |

| Method | |||||||

|---|---|---|---|---|---|---|---|

| 100 | QMLE | * | 4.07e+02 | * | 6.88e+01 | 2.77e+02 | 5.97e+01 |

| P-OE | * | 4.17e+02 | * | 7.79e+01 | 2.81e+02 | 8.79e+01 | |

| 500 | QMLE | * | 1.70e-00 | * | 1.84e-01 | 1.37e+01 | 1.30e-01 |

| P-OE | * | 1.51e-00 | * | 1.67e-01 | 1.36e+01 | 1.38e-01 | |

| 3000 | QMLE | * | 5.67e-02 | * | 1.04e-02 | 6.99e-00 | 8.98e-03 |

| P-OE | * | 5.13e-02 | * | 1.01e-02 | 6.94e-00 | 8.88e-03 |

| Method | ||||

|---|---|---|---|---|

| 100 | QMLE | * | * | 4.66e+01 |

| P-OE | * | * | 6.24e+01 | |

| 500 | QMLE | * | * | 1.76e-00 |

| P-OE | * | * | 1.65e-00 | |

| 3000 | QMLE | * | * | 3.58e-02 |

| P-OE | * | * | 3.14e-02 |

5.2 Hawkes process marked with ”Topic”

Second, we introduce the marked Hawkes process useful in the field of natural language processing.

5.2.1 Definition

We consider a web service where types of users post texts while reading each other’s posts, like social network services such as Twitter and Facebook, product reviews on Amazon, and so on. In this subsection, we model a sequence of posting times by using a GEMHP. Since we can consider the distribution of future posting times naturally depends on the content of the previous posts, we will regard the content of texts as marks.

Techniques to quantify the amount of ”topic” in a sentence have been studied in the field of natural language processing. For example, Latent Dirichlet Allocation (LDA) is a hierarchical Bayesian model in which a sentence consisting of words is generated by a conditional multinomial distribution given a ”topic” , see [5]. The topic in the LDA model is a -valued random variable (where is the number of topics), and its distribution is a conditional multinomial distribution whose parameters are generated by the Dirichlet distribution. Conversely, we can consider the conditional probabilities , and it can be assumed as a proportion of each topic in a sentence .

For and , let be the -th post by the -th user, where is the number of words in a post . We assume that the conditional probabilities are given for a -valued random topic . Then, we regard as a mark .

Now, we consider the model for the above sequence of a couple . Let be the GEMHP with the intensity

| (5.2) |

for , and suppose that its mark process takes values on the -simplex222The -simplex is the set . and has the transition kernel

where is a parameter, is the true value, and is an open convex bounded parameter space. For a vector , we write as a tensor . Recall that we write . When we have the geometric ergodicity of the above model, we can consider the stationary version of and write it as . The following assumptions are sufficient conditions for [L1]-[L2], [ND1]-[ND2], and [AH1]-[AH3].

Assumption 5.4.

-

(i)

Some might be besides all and are positive. Moreover, .

-

(ii)

The spectral radius of is less than uniformly in , where

-

(iii)

The transition kernel admits a reachable point . Moreover, there exists a lower semi-continuous function such that admits a sub-component with and for any and .

-

(iv)

For any , the mark process is not almost surely constant. Moreover, for any , and are distinguishable333That is, ..

-

(v)

For any , , and ,

holds, where is a norm-like function in [L1], and is a positive constant in Theorem 2.3. Moreover, for any and , the transition densities ’s satisfy the following conditions.

-

(i)

If there exists such that , then .

-

(ii)

If there exists such that , , then .

-

(iii)

Almost surely,

-

(i)

Remark 5.5.

(i) is a constraint on the parameters, in particular, requiring to be away from to control the oscillation of the nuisance parameter. (ii) and (iii) are assumptions for the sake of [L2] and [ND2], respectively. (iv) ensures the identifiability of the parameters. (v) is an assumption related to the probability density of marks to guarantee [AH2] and [AH3]. For this model, the oracle properties of the P-O estimation holds by Theorem 4.4.

Proposition 5.6.

Remark 5.7.

Referring to the expression of the quasi log-likelihood function in (4.2), for the above model, the intensity’s parameters and the mark’s parameter are only included in and , respectively. Therefore, we can obtain the estimator by optimizing and independently. Then, Assumption 5.4 (v) is irrelevant to the estimation for .

5.2.2 Simulation Results

As a simple case, suppose that only one user posts texts and set the number of topics in texts to . Moreover, we assume that the proportion of each topic in a text follows simply the Dirichlet distribution, although it has a more complicated distribution in the LDA model.

Let be the -dimensional GEMHP whose intensity is

where its marks independently and identically follow the -dimensional Dirichlet distribution with a parameter . Here, we only estimate the parameters since is estimated as the conventional MLE, see Remark 5.7. Furthermore, we assume that only parameters ’s can take the zero value, i.e., we set and . Then, we can immediately confirm the conditions in Assumption 5.4. We set the hyperparameters of the P-O estimator in Remark 3.4 to be , the observation times , and the number of the Monte Carlo simulation .

Table 3 shows the fraction of trials in which the parameters , and are estimated to be completely zero. We can see that the variable selection is performed more accurately by the P-O estimator than by the QMLE as becomes larger.

| QMLE: | |||||

|---|---|---|---|---|---|

| 30.0% | 58.7% | 18.0% | |||

| QMLE: | |||||

| 6.00% | 54.0% | 0.00% | |||

| QMLE: | |||||

| 0.00% | 51.7% | 0.00% | |||

| P-OE: | |||||

|---|---|---|---|---|---|

| 45.3% | 73.0% | 50.3% | |||

| P-OE: | |||||

| 19.7% | 77.3% | 7.33% | |||

| P-OE: | |||||

| 0.00% | 85.7% | 0.00% | |||

Figure 3 show histograms of the error distribution of the P-O estimator, that is, histograms of the values of . It seems that the distribution is close to the normal distribution as becomes larger.

Table 4 shows the averages of squared errors of the QMLE and the P-O estimator . For non-zero parameters, owing to the asymptotic normality, both the QMLE and the P-O estimator have asymptotically the same level of variance. For zero parameters, we can guess that the P-O estimator asymptotically has a smaller error than the QMLE, due to the accurate model selection. However, when the observation time is small, the performance of the QMLE is better due to the miss model selection of the P-O estimator.

| Method | ||||||

|---|---|---|---|---|---|---|

| 100 | QMLE | 3.22e-01 | 1.56e-00 | 2.59e-01 | 1.42e-01 | 8.29e-02 |

| P-OE | 7.52e-01 | 2.67e-00 | 3.27e-01 | 1.74e-01 | 1.10e-01 | |

| 500 | QMLE | 6.09e-02 | 1.16e-02 | 6.11e-02 | 3.44e-02 | 1.98e-02 |

| P-OE | 6.40e-02 | 1.19e-02 | 7.97e-02 | 3.88e-02 | 2.65e-02 | |

| 3000 | QMLE | 1.07e-02 | 1.74e-03 | 1.17e-02 | 4.74e-03 | 3.11e-03 |

| P-OE | 1.07e-02 | 1.73e-03 | 1.16e-02 | 3.61e-03 | 3.04e-03 |

Acknowledgment

I am deeply grateful to Professor Yoshida. Without his guidance and help, I could not have completed this article. This research was supported by the FMSP program of The University of Tokyo and Japan Science and Technology Agency CREST JPMJCR14D7.

Appendix A Proofs

A.1 Proofs of Section 3

Proof of Theorem 3.5 (i).

By considering similarly to the proof of Theorem 1 in [19], we obtain the -consistency of from Assumption 3.2 (i) and (ii). Let

and

Then we obtain . From the consistency of ,

| (A.1) |

holds as , where . On the other hand, to handle the case where the true value is at the boundary of the parameter space, we consider the following sets:

and

where and . Then, holds. The consistency of immediately yields

| (A.2) |

as . On , is differentiable at with respect to some -th component. Thus, the same way as the proof of Theorem 2 in [19] leads

| (A.3) | |||||

From the equations (A.1), (A.2), and (A.3), we get the conclusion. ∎

We write for a sequence and a positive constant if there exists a positive constant such that for all .

A.2 Proofs of Section 4

Let , and be a set of functions such that:

-

(i)

is of class on ,

-

(ii)

and are polynomial growth in for ,

-

(iii)

.

The sufficient conditions for the PLD are proposed by [6]. Here, modifying the conditions [A1]-[A3] in [6] to allow the model with nuisance parameter, we consider the following conditions. Here, we again call that is of class for some if is of class and its derivatives admit continuous extensions on .

- [A1]

-

For any ,

-

(i)

is a predictable on for any ,

-

(ii)

is almost surely in for any ,

-

(iii)

if and only if for any and .

-

(i)

- [A2]

-

For any and ,

-

(i)

,

-

(ii)

-

(iii)

,

-

(iv)

.

-

(i)

- [A3]

-

There exist , , and such that

as for any and , and

as for any .

In [A1], which is a regularity condition to ensure the existence of the quasi log-likelihood process, we extended the differentiability of each function to the boundary of the parameter space. [A2] gives moment and smoothness conditions, and here, we consider the finiteness uniformly in . [A3] is the condition for the ergodicity of and uniformly in . These conditions are derived from the ergodicity of the GEMHP and the conditions [AH1]-[AH2].

Lemma A.1.

Under [L1]-[L2], [ND1]-[ND2], and [AH1]-[AH2], the conditions [A1]-[A3] hold.

Proof.

We write and . Furthermore, we decompose , , and as

and

For the proof of Theorem 4.3, we prepare the following lemmas.

Lemma A.2.

Under [A1]-[A3], we have, for any ,

Proof.

Lemma A.3.

Under [A1]-[A3], we have, for any ,

Proof.

By applying Sobolev’s inequality of Theorem 4.12 in [2], we can choose such that

where the last convergence is a consequence of the condition [A3]. Similarly, we get

as , and thus we have the conclusion. ∎

Proof of Theorem 4.3.

We only have to check that the conditions (A1”), (A4’), (A6), (B1), and (B2) in Theorem 3 (c) in [21] are satisfied. Note that the nuisance parameter in [21] is replaced by in our literature. Set , and for satisfying (A4’). By Lemma A.1, we have

| (A.5) |

as , for any in the same way as Theorem 2.2 in [6]. Thus, (A.5) and Lemma A.2 lead to (A6). Moreover, we have

| (A.6) |

for any by Sobolev’s inequality, Hölder’s inequality, and [A2]. Now (A1”) is satisfied by (A.6) and Lemma A.3. Finally, from [AH3], we see that the conditions (B1) and (B2) follow immediately; see Remark 4.2. ∎

A.3 Proofs of Section 5

Proof of Proposition 5.2.

Since there are no marks, we can assume that , , and for all . Then, the conditions [L1], [ND1], and [ND2] hold, for example, for and . The condition [L2] holds by the Perron-Frobenius’ theorem and the assumption that the spectral radius of is less than . Thus, the multivariate exponential Hawkes process with sparse structure has geometric ergodicity.

Since each takes a positive value, the conditions [AH1] and [AH2] hold. Finally, the condition [AH3] is satisfied in the same way as Lemma A.7 in [7]. To obtain [AH3], we prove that if there exists a vector such that . In this proof, we use Assumption 5.1 (i) to take positive realizing the infimum. ∎

Proof of Proposition 5.6.

Let

and

and then we can write

We check the conditions [L1]-[L2] and [ND1]-[ND2] for this GEMHP. First, the condition [ND1] obviously holds. Let and for , where we extend the first domain of as for . Then, we can easily check the condition [L1]. The conditions [L2] and [ND2] are assumed in Assumption 5.4 (ii) and (iii). Thus, this model has geometric ergodicity.

Now, we consider the conditions [AH1]-[AH3]. We define , and then we can write

[AH1] obviously holds, and [AH2] follows from Assumption 5.4 (v). We write as in Section 4. Finally, for the sake of the condition [AH3], we only have to show that (i) for any and , and (ii) is positive definite uniformly in , see Remark 4.2. Let there be and such that . We have

Since each term on the right-hand side is non-negative, we have

and

Thus, we obtain and Then, we get by Assumption 5.4 (v-a). On the other hand, we have

| (A.7) | |||||

for any . Since the left-hand side is constant, the right-hand side must only have jumps of size zero. Then, by Assumption 5.4 (iv), we get for all , and . By taking the derivative with respect to , we have

and thus, we get for all and such that for some by Assumption 5.4 (iv). Finally, the right-hand side of (A.7) becomes zero, and holds. Therefore, holds and contradicts .

Next, we assume that there exists such that . We write , where and are related to and , respectively, and denotes non-nuisance parameters . From Assumption 5.4 (v-c), we have

and then it is necessary that almost surely

| (A.8) |

and

| (A.9) |

hold for any and . Then, (A.9) and Assumption 5.4 (v-b) lead to . On the other hand, from Assumption 5.4 (i), the infimum in (A.8) for each path is realized by some positive , and we again write this point as . Then, for ,

where , and are components of corresponding to non-nuisance parameters , and , respectively. Differentiating both sides -times with respect to , we almost surely get

| (A.10) | |||||

Let , where represents the first jump time of the counting process . We easily see . By taking the limit in (A.10) on the set , we obtain

and thus we get since holds for some by the definition of . Then, we immediately obtain by Assumption 5.4 (iv), and thus also holds. Now , and we get the conclusion. ∎

Appendix B Additional numerical experiments

B.1 Scenario with no zero coefficients

We considered scenarios with no zero coefficients to see if the P-O estimator and QMLE perform similarly. Here, we deal with the Hawkes process marked with ”Topic” introduced in Section 5.2. Let be the -dimensional GEMHP whose intensity is

where its marks independently and identically follow the -dimensional Dirichlet distribution with a parameter . Same as Subsection 5.2.2, we estimate the parameters and assume that only parameters ’s can take the zero value, i.e., we set and . We also set the hyperparameters of the P-O estimator to be , the observation times , and the number of the Monte Carlo simulation .

Table 5 shows the fraction of trials in which the parameters , and are estimated to be completely zero. We see that both methods asymptotically make correct model selections, but that the probability of incorrectly estimating zero is higher for the P-O estimator.

| QMLE: | |||||

|---|---|---|---|---|---|

| 22.0% | 35.3% | 16.7% | |||

| QMLE: | |||||

| 3.67% | 12.0% | 0.33% | |||

| QMLE: | |||||

| 0.00% | 1.67% | 0.00% | |||

| P-OE: | |||||

|---|---|---|---|---|---|

| 35.3% | 57.3% | 44.0% | |||

| P-OE: | |||||

| 11.0% | 36.3% | 6.00% | |||

| P-OE: | |||||

| 0.00% | 7.33% | 0.00% | |||

Table 6 shows the averages of squared errors of the QMLE and the P-O estimator . When the observation time is small, we see that the QMLE perform better than the P-O estimator due to the miss model selection of the P-O estimator. However, the difference becomes smaller as the observation time is longer. We note that both the QMLE and the P-O estimator have asymptotic normality with the same variance.

| Method | ||||||

|---|---|---|---|---|---|---|

| 100 | QMLE | 3.69e-01 | 4.20e-02 | 2.81e-01 | 1.97e-01 | 7.09e-02 |

| P-OE | 7.58e-01 | 8.85e-01 | 5.45e-01 | 2.40e-01 | 9.63e-02 | |

| 500 | QMLE | 7.41e-02 | 5.30e-03 | 8.55e-02 | 5.39e-02 | 2.01e-02 |

| P-OE | 7.54e-02 | 5.43e-03 | 1.00e-01 | 6.80e-02 | 2.58e-02 | |

| 3000 | QMLE | 1.13e-02 | 7.02e-04 | 1.32e-02 | 1.28e-02 | 3.36e-03 |

| P-OE | 1.12e-02 | 7.00e-04 | 1.39e-02 | 1.53e-02 | 3.51e-03 |

B.2 Comparison with previous studies

In this subsection, we compare the performance of the P-O estimator with the mixed method of Lasso and nuclear regularization, introduced in [22], and the elastic net. These classical methods are implemented in tick library444The documentation is available here https://x-datainitiative.github.io/tick/. in Python3, see [3], and work only for an exponential Hawkes model whose decay parameter is given.

Here, we consider the -dimensional exponential Hawkes process , see Eq. (5.1), whose intensity with the following parameters:

and the decay parameter is given by for all . We only estimate the parameters and assume that only parameters can take the zero value, i.e., we set and .

The mixed method of [22] is defined by

| (B.1) |

where and are hyperparameters, is the nuclear norm of a matrix, which is defined to be the sum of its singular value, is the norm, and is the log-likelihood process of the Hawkes process. On the other hand, the elastic net is given by

| (B.2) |

where and are hyperparameters, is the norm, and is the least-squares function for the Hawkes process, that is,

We set the hyperparameters in Eqs. (B.1) and (B.2) to be , , and , and the hyperparameters of the P-O estimator to be . Let the observation times and the number of the Monte Carlo simulation .

Table 7 shows the fraction of trials in which the parameter ’s are estimated to be completely zero. Here, we regarded estimated values less than 1.0e-8 as zero by taking into account the numerical error in the tick library. We can see that the variable selection is performed more accurately by the P-O estimator than by the other methods.

| Mixed Method in [22] | |||||||

| 0.00% | 40.3% | 40.3% | 40.0% | ||||

| 0.00% | 43.7% | 39.7% | 40.3% | ||||

| 32.0% | 0.00% | 0.00% | 0.00% | ||||

| 41.7% | 0.00% | 0.00% | 0.00% | ||||

| Elastic Net | |||||||

| 0.00% | 56.7% | 59.7% | 61.0% | ||||

| 0.00% | 60.3% | 60.7% | 60.0% | ||||

| 55.0% | 0.67% | 0.00% | 0.00% | ||||

| 57.7% | 0.00% | 0.00% | 0.00% | ||||

| P-O Estimator | |||||||

| 0.00% | 93.3% | 92.3% | 93.0% | ||||

| 0.33% | 92.7% | 95.3% | 95.7% | ||||

| 90.3% | 4.33% | 1.00% | 1.00% | ||||

| 90.3% | 3.00% | 2.00% | 2.00% | ||||

Table 8 shows the averages of squared errors of each method. For non-zero parameters, each method has almost the same level of variance. For zero parameters, we get a smaller error by the P-O estimator than by the other methods due to the accurate model selection.

| Method | ||||||

|---|---|---|---|---|---|---|

| Mixed Method | 2.71e-05 | 2.17e-05 | 2.69e-05 | 2.52e-05 | 1.38e-03 | 2.79e-04 |

| Elastic Net | 2.71e-05 | 2.14e-05 | 3.06e-05 | 2.76e-05 | 1.73e-03 | 2.71e-04 |

| P-OE | 2.43e-05 | 2.06e-05 | 2.72e-05 | 2.55e-05 | 1.38e-03 | 1.70e-04 |

| Method | ||||||

|---|---|---|---|---|---|---|

| Mixed Method | 2.67e-04 | 2.77e-04 | 1.47e-03 | 3.39e-04 | 2.15e-04 | 1.78e-04 |

| Elastic Net | 2.32e-04 | 2.56e-04 | 1.81e-03 | 2.38e-04 | 1.88e-04 | 1.45e-04 |

| P-OE | 1.71e-04 | 1.81e-04 | 1.51e-03 | 2.26e-04 | 1.21e-04 | 8.14e-05 |

| Method | ||||

|---|---|---|---|---|

| Mixed Method | 3.98e-04 | 1.36e-03 | 1.09e-03 | 1.16e-03 |

| Elastic Net | 4.14e-04 | 1.71e-03 | 1.24e-03 | 1.27e-03 |

| P-OE | 2.76e-04 | 1.52e-03 | 1.14e-03 | 1.21e-03 |

| Method | ||||

|---|---|---|---|---|

| Mixed Method | 4.02e-04 | 1.31e-03 | 1.21e-03 | 1.09e-03 |

| Elastic Net | 4.15e-04 | 1.46e-03 | 1.37e-03 | 1.29e-03 |

| P-OE | 3.00e-04 | 1.45e-03 | 1.31e-03 | 1.17e-03 |

References

- [1] Frédéric Abergel, Marouane Anane, Anirban Chakraborti, Aymen Jedidi, and Ioane Muni Toke. Limit Order Books. Cambridge University Press, Cambridge, 1st edition, 2016. ISBN: 978-1-107-16398-0.

- [2] Robert A. Adams and John J. F. Fournier. Sobolev Spaces. Academic Press, Cambridge, 2nd edition, 2003. ISBN: 978-0-1204-4143-3.

- [3] Emmanuel Bacry, Martin Bompaire, Philip Deegan, Stéphane Gaïffas, and Søren V. Poulsen. tick: a Python library for statistical learning, with an emphasis on Hawkes processes and time-dependent models. In Journal of Machine Learning Research, volume 18, pages 1–5, 2018.

- [4] Emmanuel Bacry, Martin Bompaire, Stéphane Gaïffas, and Jean François Muzy. Sparse and low-rank multivariate Hawkes processes. Journal of Machine Learning Research, 21(1):1–32, 2020.

- [5] David Meir Blei, Andrew Yan-Tak Ng, and Michael Irwin Jordan. Latent dirichlet allocation. The Journal of Machine Learning Research, 3:993–1022, 2003.

- [6] Simon Clinet. Quasi-likelihood analysis for marked point processes and application to marked Hawkes processes. Statistical Inference for Stochastic Processes, 2021.

- [7] Simon Clinet and Nakahiro Yoshida. Statistical inference for ergodic point processes and application to limit order book. Stochastic Processes and their Applications, 127(6):1800–1839, 2017.

- [8] Paul Embrechts and Matthias Kirchner. Hawkes graphs. Theory of Probability and Its Applications, 62(1):163–193, 2018.

- [9] Jianqing Fan and Runze Li. Variable selection via nonconcave penalized likelihood and its oracle properties. Journal of the American Statistical Association, 96(356):1348–1360, December 2001.

- [10] Masatoshi Goda. Hawkes process and Edgeworth expansion with application to maximum likelihood estimator. Statistical Inference for Stochastic Processes, 24(2):277–325, 2021.

- [11] Masatoshi Goda, Ryosuke Yano, and Takayuki Mizuno. Multivariate Hawkes process analysis of posts on a web service about uncomfortable gender experiences. Journal of Complex Networks, 9(1):1–21, April 2021.

- [12] Niels Richard Hansen, Patricia Reynaud-Bouret, and Vincent Rivoirard. LASSO and probabilistic inequalities for multivariate point processes. Bernoulli, 21(1):83–143, 2015.

- [13] Alan Geoffrey Hawkes. Spectra of some self-exciting and mutually exciting point processes. Royal Statistical Society Publications, 58(1):83–90, 1971.

- [14] Jean Jacod and Albert Nikolayevich Shiryaev. Limit Theorems for Stochastic Processes. Springer-Verlag, Berlin, 2003. ISBN: 978-3-662-05265-5.

- [15] Lucien Le Cam. On the assumptions used to prove asymptotic normality of maximum likelihood estimates. The Annals of Mathematical Statistics, 41(3):802–828, 1970.

- [16] Yosihiko Ogata. Statistical models for earthquake occurrences and residual analysis for point processes. IEEE Transactions on Information Theory, 27(1):23–31, 1981.

- [17] Yosihiko Ogata. On Lewis’ simulation method for point processes. Journal of the American Statistical Association, 83(401):9–27, 1988.

- [18] Marcello Rambaldi, Emmanuel Bacry, and Fabrizio Lillo. The role of volume in order book dynamics: a multivariate Hawkes process analysis. Quantitative Finance, 17(7):999–1020, 2017.

- [19] Takumi Suzuki and Nakahiro Yoshida. Penalized least squares approximation methods and their applications to stochastic processes. Japanese Journal of Statistics and Data Science volume, 3(2):513–541, 2020.

- [20] Robert Tibshirani. Regression shrinkage and selection via the LASSO. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288, 1996.

- [21] Nakahiro Yoshida. Polynomial type large deviation inequalities and quasi-likelihood analysis for stochastic differential equations. Annals of the Institute of Statistical Mathematics, 63:431–479, 2011.

- [22] Ke Zhou, Hongyuan Zha, and Le Song. Learning social infectivity in sparse low-rank networks using multi-dimensional Hawkes processes. In Proceedings of the Sixteenth International Conference on Artificial Intelligence and Statistics, volume 31, pages 641–649, 2013.

- [23] Ciyou Zhu, Richard H. Byrd, Peihuang Lu, and Jorge Nocedal. L-BFGS-B: Fortran subroutines for large-scale bound-constrained optimization. ACM Transactions on Mathematical Software, 23(4):550–560, 1997.

- [24] Hui Zou and Trevor Hastie. Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B, 67(2):301–320, 2005.