Bi-Directional Grid Constrained Stochastic Processes’ Link to Multi-Skew Brownian Motion

Abstract.

Bi-Directional Grid Constrained (BGC) stochastic processes (BGCSPs) constrain the random movement toward the origin steadily more and more, the further they deviate from the origin, rather than all at once imposing reflective barriers, as does the well-established theory of Itô diffusions with such reflective barriers. We identify that BGCSPs are a variant rather than a special case of the multi-skew Brownian motion (M-SBM). This is because they have their own complexities, such as the barriers being hidden (not known in advance) and not necessarily constant over time. We provide a M-SBM theoretical framework and also a simulation framework to elaborate deeper properties of BGCSPs. The simulation framework is then applied by generating numerous simulations of the constrained paths and the results are analysed. BGCSPs have applications in finance and indeed many other fields requiring graduated constraining, from both above and below the initial position.

Key words and phrases:

Wiener Processes, Itô Processes, Reflecting Barriers, Stochastic Differential Equation (SDE), Stopping Times, First Passage Time (FPT), Multi-Skew Brownian Motion (M-SBM)Notation

| Term | Description |

|---|---|

| BGC | Bi-Directional grid constrained |

| BGCSP | BGC stochastic process |

| M-SBM | Multi-skew Brownian motion |

| Stochastic process over time | |

| Brownian motion over time | |

| Wiener process over time | |

| Time | |

| , | Drift coefficient of over |

| , | Diffusion coefficient of over |

| BGC coefficient of over | |

| Sign function of | |

| Lower barrier | |

| Upper barrier | |

| Stopping time when is hit | |

| Absolute value of |

1. Introduction

In Taranto et al., [33], the concept of Bi-Directional Grid Constrained (BGC) stochastic processes (BGCSPs) was introduced, and the impact of BGC on the iterated logarithm bounds of the corresponding stochastic differential equation (SDE) was derived. In the subsequent paper (Taranto and Khan, 2021b [32]), the hidden geometry of the BGC process was examined, in particular how the hidden reflective barriers are formed, the various possible formulations that can be formed, and an algorithm to simulate BGCSPs was provided. BGCSPs were also compared to the Langevin equation, the Ornstein-Uhlenbeck process (OUP), and it was shown how BGCSPs are more complex due to a more general framework that does not always admit an exact solution. In this paper, we examine in what respects a BGCSP resembles and in what respect it differs from a type of multi-skew Brownian motion (M-SBM).

Before we do this, we recall that the BGC term , from now onwards simply , unless required to be fully expressed, has been defined as impacting the term as in [33] or the term to a lesser extent as in [32]. Here, we notice that even if this term is placed as a factor outside the sum of the and terms, it will still constrain the Itô diffusion in a slightly different, yet fundamentally the same way. Since is continuous and differentiable, we require to include the infinitessimal , giving . We thus provide the following third alternative definition of the BGCSP.

Definition 1.1.

(Definition III of BGC Stochastic Processes). For a complete filtered probability space and a (continuous) BGC function , , is the drift coefficient, is the diffusion coefficient, is the BGC function. , and are convex functions and is the sign function defined in the usual sense,

Then, the corresponding BGC Itô diffusion is defined as follows,

| (1.1) |

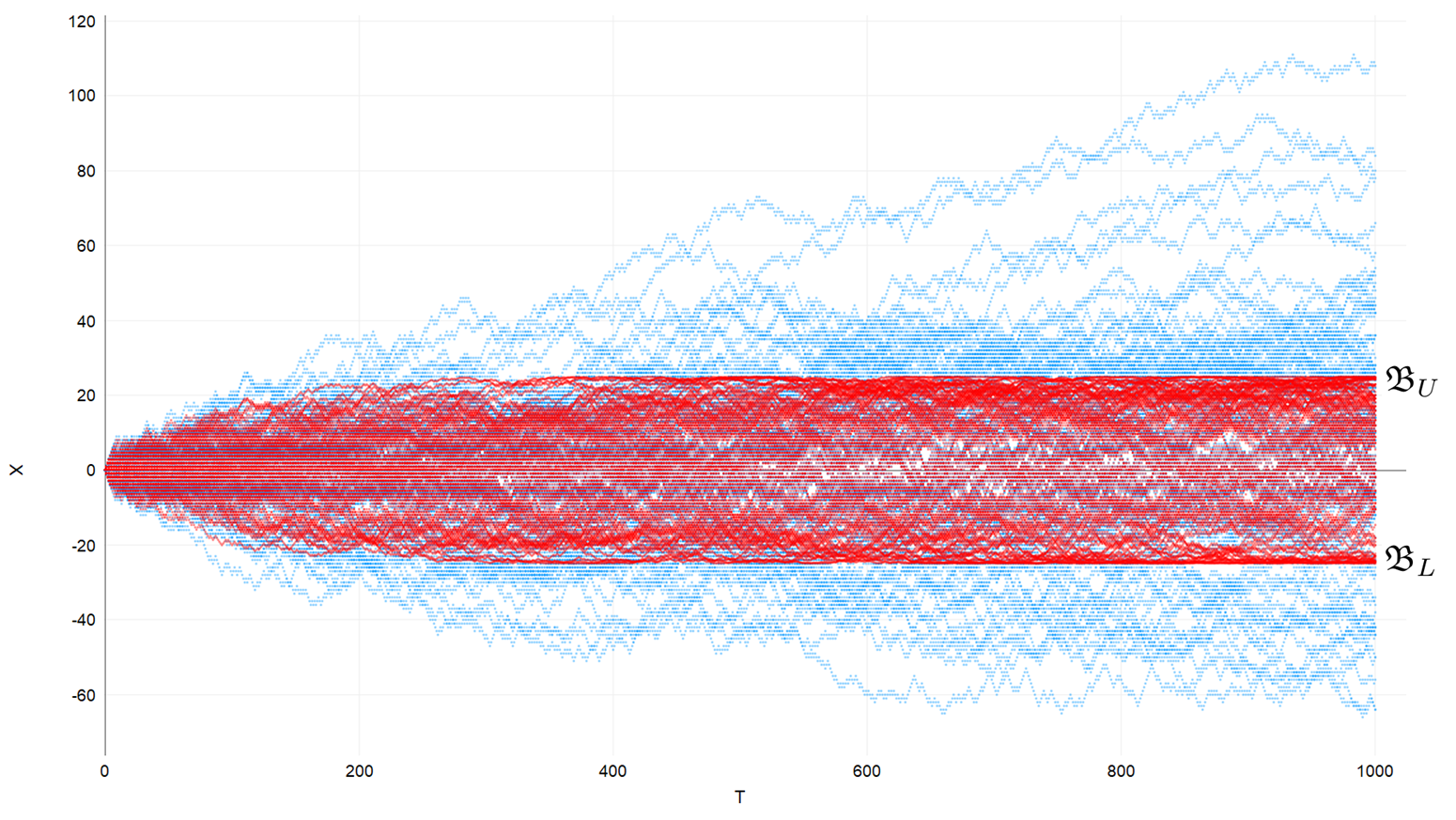

By choosing to be a ‘suitable’ parabolic cylinder function in relation to the underlying Itô diffusion, as shown in [32], namely , the hidden barriers become visible when enough simulations hit them. Figure 1 shows that (1.1) is simulated 1,000 times for both with and without BGC, together with the hidden lower reflective barrier and the hidden reflective upper barrier also being displayed.

An even more specialized case that is of great interest, due to its simplicity, is where drift function is set to , and similarly, the diffusion function is set to , . One can even define and in a more gradual manner such that in the limit they approach the typical constant expressions for the drift and diffusion coefficients,

| (1.2) |

Depending on whether the generalized and are used, or whether the simplified and are used, then the resulting reflective boundary theorems will either have more complexity, or less complexity, respectively.

Before proceeding to the Methodology section, (1.1) is discussed within a multi-Dimensional context with some examples, which will help explain the multidimensionality of M-SBMs.

Remark 1.2.

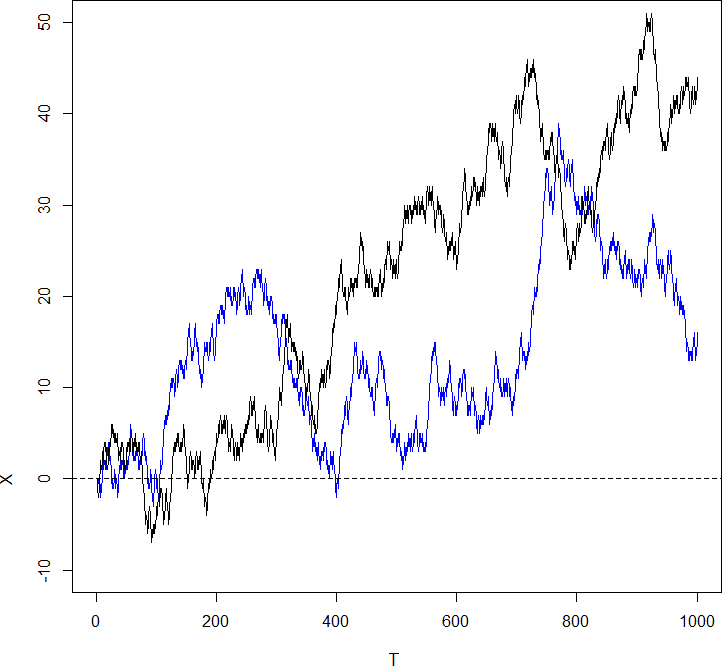

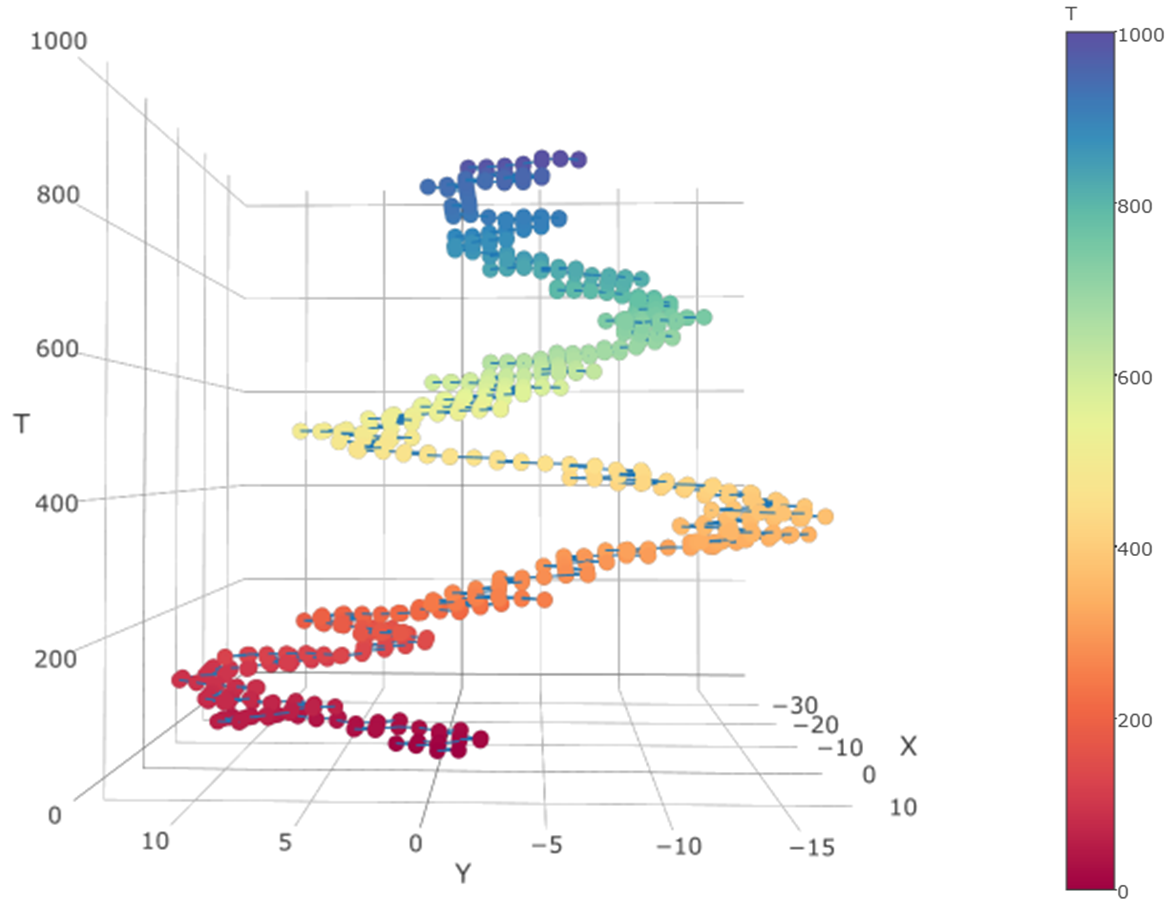

By multi-Dimensional diffusion, we are not referring to the usage in papers such as Sacerdote et al., [27] in which each dimension is reserved for each possible path or simulation, as shown in Figure 2(a).

(a). (b).

Notice that in Figure 2(b), the BGCSP exhibits a ‘skew’ and can be considered as a 2-SBM -which will be elaborated in the Methodology section. Instead of the usage in Figure 2(a), we use the standard interpretation and generally accepted usage of the term ‘multi-Dimensional diffusion’ in which each dimension is reserved for each co-ordinate of the multivariate Itô process, as shown in Figure 3.

(a). 2-D Itô Diffusion as seen from (b). 2-D Itô Diffusion as seen from

We also note that the Methodology, Results and Discussion sections are either directly multi-Dimensional or can be extended to multi-Dimensional expressions.

We now have a more geometric understanding of how BGCSPs can be constrained along multiple dimensions, to be in a better position to express (1.1) in a more generalized -Dimensional framework in (1.3).

Definition 1.3.

(Definition IV - Multi-Dimensional BGC Stochastic Processes). Let defined on a probability space be an Itô diffusion satisfying the conditions given in the definition of the 1-Dimensional Itô process for each , , then we can form 1-Dimensional Itô processes in an SDE of the form,

|

|

(1.3) |

where is an -Dimensional Wiener process and and are the drift and diffusion fields respectively. For a point , let denote the law of given initial datum , and let denote expectation with respect to . Now, (1.3) can also be expressed in matrix notation as,

| (1.4) |

where,

|

|

|

|

for vectors , , and matrix .

Having reviewed the multi-Dimensional nature of unconstrained and BGC Itô diffusions, the paper is structured as follows; Section 2 provides the Literature Review, Section 3 the Methodology, Section 4 the Results and Discussion, and finally, Section 5 the Conclusion.

2. Literature Review

2.1. Constraining Stochastic Processes by Reflective Barriers

The constraining of stochastic processes in the form of discrete random walks and continuous Wiener processes has been researched for many decades. By reviewing Weesakul, [34] and the references therein, we see an established and rigorous analysis of random walks between a reflecting and an absorbing barrier. Lehner, [16] extended this to 1-Dimensional random walks with a partially reflecting (semipermeable) barrier. Gupta, [9] generalised this concept further to random walks in the presence of a multiple function barrier (MFB) where the barrier can either be partially reflective, absorptive, transmissive or hold for a moment, but not terminating or killing the random variable. Dua et al., [7] extended the work of [16] to random walks in the presence of partially reflecting barriers in which the probability of a random variable or datum reaching certain states was determined. Lions and Sznitman, [20] extended the research on reflecting boundary conditions through the refinement to SDEs. Percus, [24] considered an asymmetric random walk, with one or two boundaries, on a 1-Dimensional lattice. At the boundaries, the walker is either absorbed or reflected back to the system. Budhiraja and Dupuis, [5] considered the large deviation properties of the empirical measure for 1-Dimensional constrained processes, such as reflecting Wiener processes, the M/M/1 queue, and discrete-time analogs. L’epingle, [18] examined stochastic variational inequalities to provide a unified treatment for SDEs existing in a closed domain with normal reflection and (or) singular repellent drift. When the domain is a polyhedron, he proved that the reflected-repelled Wiener process does not hit the non-smooth part of the boundary. Bramson et al., [4] examined the positive recurrence (to the origin) of reflecting Wiener processes in 3-Dimensional space. Ball and Roma, [3] examined the detection of mean reversion within reflecting barriers with an application to the European exchange rate mechanism (EERM).

2.2. Multi-Skew Brownian Motion

The concept of skew Brownian motion (SBM) was first introduced in the book by Itô and McKean, [13] as a diffusion with a drift represented by a generalized function, which solves an SDE involving its symmetric local time. Specifically, an SBM is the solution of,

where is a standard Brownian motion (BM). However, standard Brownian motion is oftentimes abbreviated as SBM, so to reduce any possible confusion and to eliminate any reference to the original botanical context of Robert Brown -to which the term ‘Brownian motion’ is attributed -we will express in the rest of this paper in the more mathematically precise context as a Wiener process . is the symmetric local time at . Note that for , the above equation is reduced to a Wiener process. Harrison and Shepp, [10] then considered diffusions with a discontinuous local time. The literature on SBMs was consolidated by Harrison and Shepp, [10] and later by Lejay, [17]. Applications of SMBs were extended by Ramirez, [26] by applying multi-SBM (M-SBM) and diffusions in layered media that involve advection flows. Appuhamillage and Sheldon, [1] linked SBMs to existing research by deriving the first passage time (FPT) of SBM. In 2015, the multiple barrier research of [26] was extended by Atar and Budhiraja, [2], Ouknine et al., [23] who collapsed barriers to an accumulation point, and by Dereudre et al., [6] who derived an explicit representation of the transition densities of SBM with drift and two semipermeable barriers. Mazzonetto, [21] extended her prior research [6] on SBMs by deriving exact simulations of SBMs and M-SBMs with discontinuous drift in her Doctoral dissertation. Gairat and Shcherbakov, [8] applied SBMs and their functionals to finance. Krykun, [14] also extended the convergence of SBM with local times at several points that are contracted into a single one. Mazzonetto, [22] has also recently examined the rates of convergence to the local time of oscillating and SBMs.

3. Methodology

Before proceeding to the main result of this paper, it is instructive to establish a theoretical foundation by considering the key research for Itô diffusions constrained by two reflective barriers and then examining the necessary extensions that need to be derived for M-SBM constrained Itô diffusions.

3.1. Itô Diffusions Constrained by Two Reflective Barriers

Given a filtered probability space with the filtration , then the reflected diffusion with two-sided barriers , at , respectively can be defined as,

| (3.1) |

Remark 3.1.

The process and are known in the literature as ‘regulators’ for the points and , however, we believe that a better term is ‘detectors’ because they mainly detect or count how many times reaches and .

Here, the drift is Lipschitz continuous, the diffusion is strictly positive and Lipschitz continuous. , with are given real numbers, and is the 1-Dimensional standard Wiener process on . The processes and are the minimal non-decreasing and non-negative processes, which restrict the process . More precisely, the processes and increase only when hits the boundary and , respectively, so that , is the characteristic function of the set and,

| (3.2) |

Furthermore, the processes and are uniquely determined by the following properties (Harrison, [11]),

-

(1)

both and are nondecreasing processes,

-

(2)

and increase only when and , respectively, that is and , for .

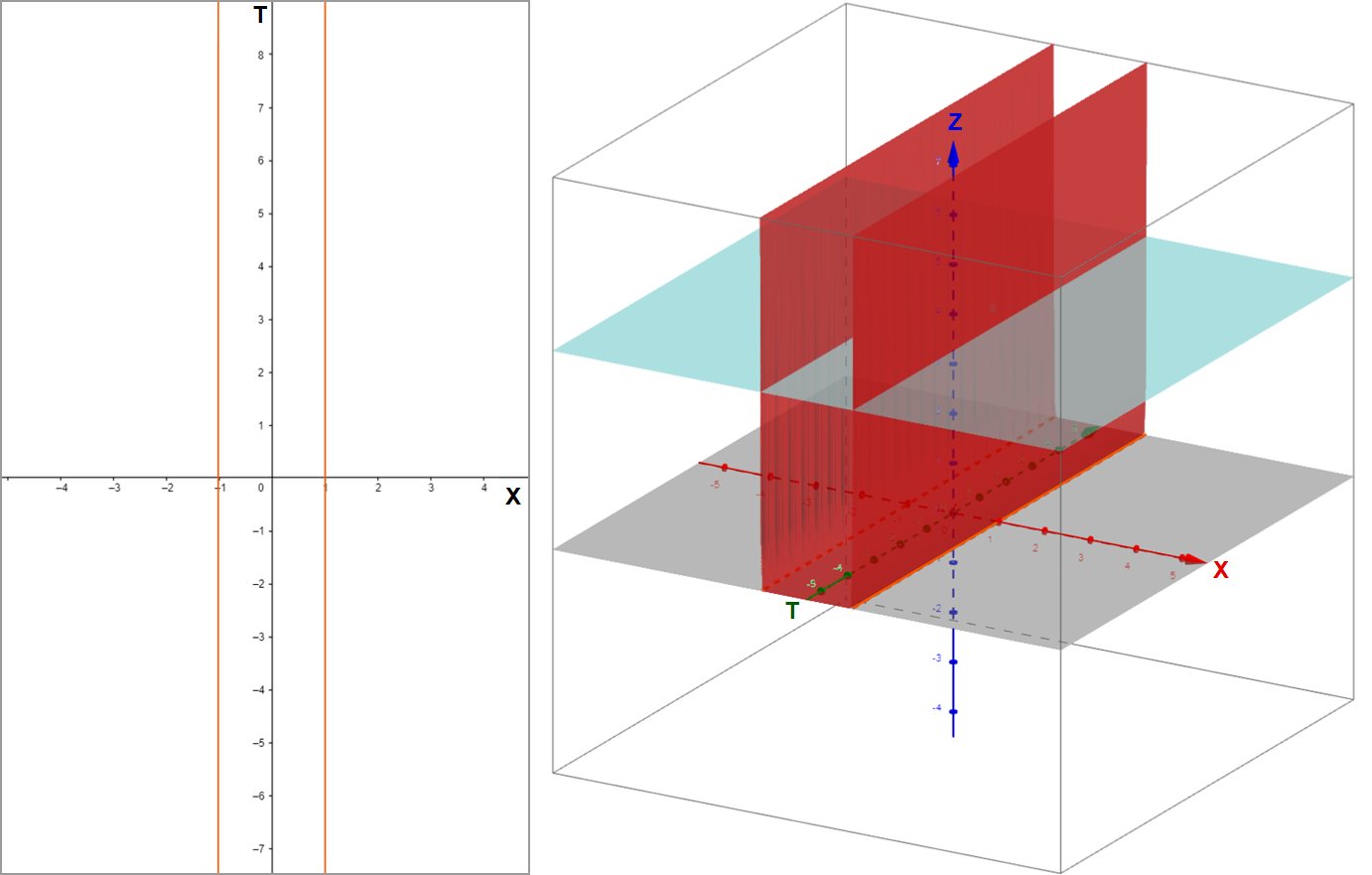

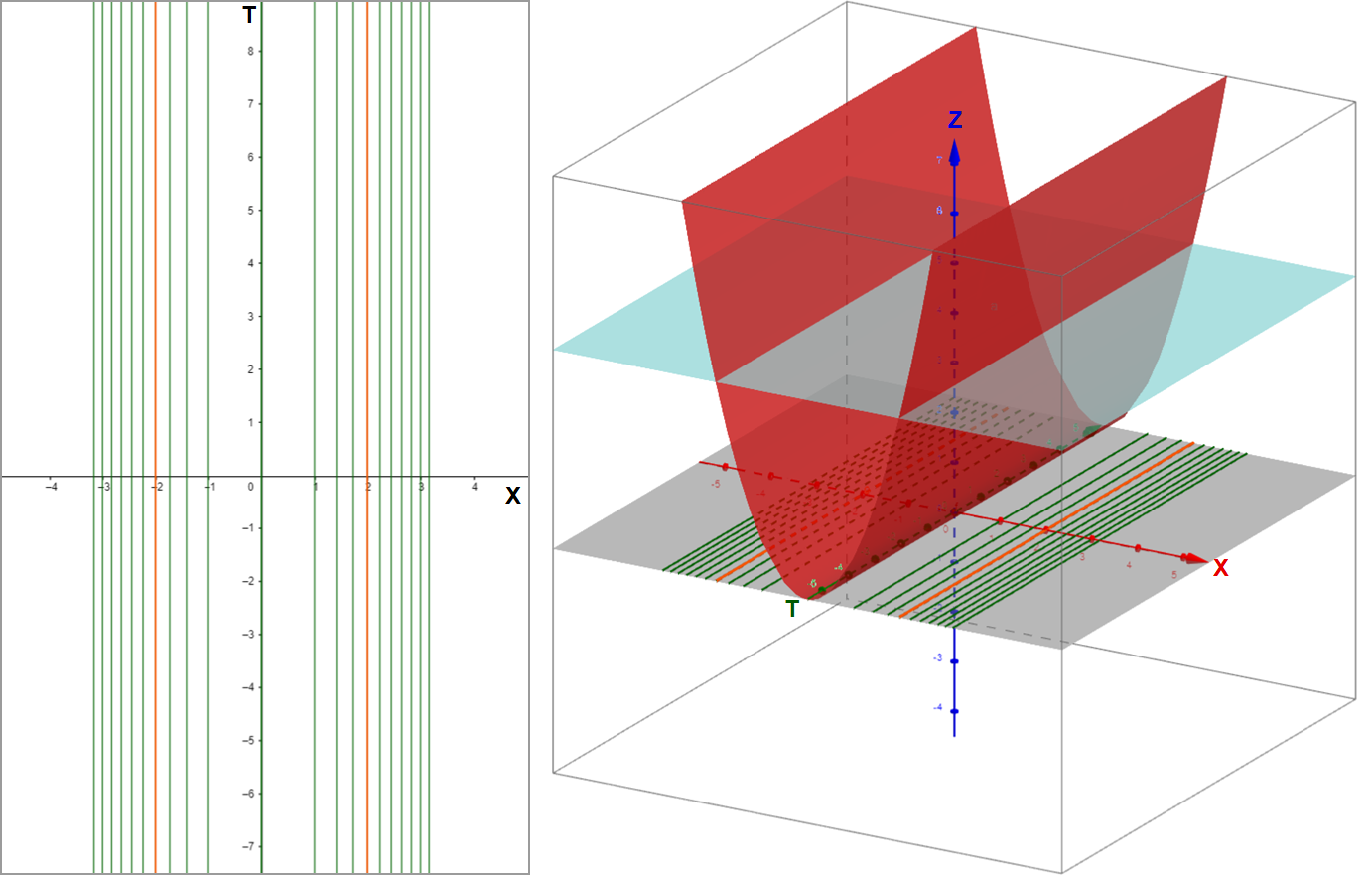

We can consider the two reflective barriers as forming a 2-SBM. Furthermore, it is instructive for BGCSP to see the two barriers and in , shown in Figure 4(a) as embedded in by a governing BGC surface , as shown in Figure 4(b).

(a). Barriers in - Contour plot (b). Barriers in - Contour & surface plot

Remark 3.2.

3.2. Multi-Skew Brownian Motion

Having examined Itô diffusions constrained by two reflective barriers, we now consider the so-called multi-skew Brownian motion, constrained by multiple barriers of varying degrees of reflectiveness.

Definition 3.3.

(M-SBM). A multi-skew Brownian motion (M-SBM) represented (adapted from Mazzonetto, [21]) by -SBM, or more simply by -SBM with semipermeable barriers of varying permeability coefficients, respectively , is the starting position, the coefficients , barriers , local times , and is the set of all parameters of the M-SBM, then the M-SBM is expressed as,

Remark 3.4.

The term has been added to the [21] definition so that the process can fit a wider range of models. We require that . The cases when are said to exhibit zero permeability (i.e. impermeability or full reflectiveness), and when the process is said to exhibit partial reflectiveness (i.e. semi permeability). Note that a 0-SBM is simply a Wiener process and a -SBM is a positively/negatively reflected Wiener process. The definition of M-SBM is illustrated in Figure 6, representing a typical example of M-SBM. The standard definition of a skew Brownian motion has a drift term making it no longer, strictly speaking, Brownian motion.

The M-SBM of Definition 3.3 allows any barrier combination to be either fully reflective or semipermeable.

Remark 3.5.

If the permeability is at the barrier for some and the initial position is , then the lower barriers will almost surely be never reached [21]. For this to happen, it must be that , so that as the Itô diffusion descends (down) to , it is fully reflected back (up). This of course assumes that the diffusion coefficient is ‘relatively small’ and so allows the Itô diffusion to be ‘well behaved’ and never ‘jump over’ and go below the barrier, as also illustrated in Figure 6.

Theorem 3.6.

(Multiple Barriers of M-SBM Merging to One, adapted from Mazzonetto, [21]). Before expressing the skewness parameter for a general number of barriers , we derive for the first two simplest scenarios.

If , , and , . Let,

Let us denote by the -SBM with drift , barriers , and denote by the 1-SBM with drift , and barrier . Let us assume , then converges to in the following sense,

The same holds in the case of barriers merging. In this case is the -SBM with drift , skewness parameters and barriers , .

The skewness parameter of the limit -SBM is given by,

| (3.3) |

If is even,

| (3.4) |

If is odd,

| (3.5) |

The M-SBM framework also only considers one half-plane at a time, so that the transition density (or distribution) of the upper plane is assumed to be the same for the lower half plane, which is not always the case (except for BGCSP). We show below that whilst BGCSPs are a special case of M-SBMs, they have some unique properties that make them of particular interest among the larger class.

3.3. Constructing BGC Stochastic Processes

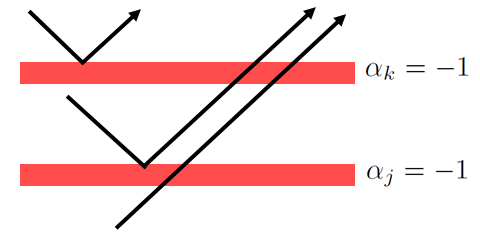

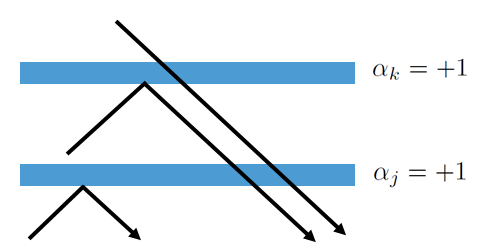

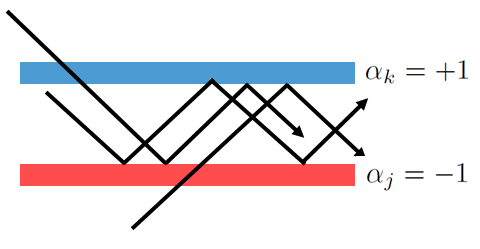

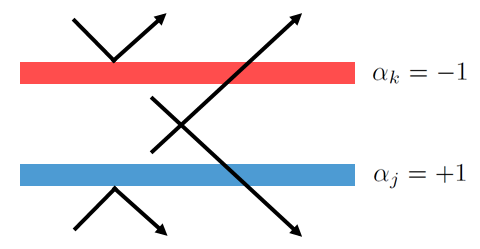

We can compliment Mazzonetto by condensing all possible local barrier combinations to the following four possible global barrier combinations that comprise a lower barrier and an upper barrier , as shown in Figure 7.

(a). (b).

(c). (d).

The diagrammatic summary of possible cases represented in Figure 7 is formally stated as Lemma 3.7 which is then used in Theorem 3.8. This Theorem formally expresses that the barriers of an M-SBM merge to a 1-SBM, to which the process converges.

Lemma 3.7.

Proof.

We first assume that there exists only one reflective barrier and semipermeable barriers . We then consider the two SDEs;

| (3.6) |

where is an unconstrained Itô diffusion and is a constrained Itô diffusion according to the above barrier constraints. Let , so or .

If , then will dominate as it will vanish (i.e. ) such that,

If , then will dominate and merge (i.e. ) such that,

Next, assume that there exist two fully reflective barriers , and semipermeable barriers . (3.6) now equates to,

| (3.7) |

If , then and (or) will dominate and as it will vanish (i.e. ) and if , then will dominate and (or) hence merge to and , such that and , respectively.

Finally, if there are more than fully reflective barriers and semipermeable barriers, then the new barriers will effectively be a linear combination of any two possible combinations in Figure 7, depending on how the fully reflective barriers of are defined, completing the proof for all scenarios. ∎

To contrast Figure 4 for two reflective constant barriers, for BGCSP we have two hidden reflective barriers which also constrain the interior between the boundaries, as shown in Figure 8, where (a) shows the multiple barriers in , and (b) shows how the multiple barriers are projected from .

(a). Barrier in - Contour plot (b). Barrier in - Contour & surface plot

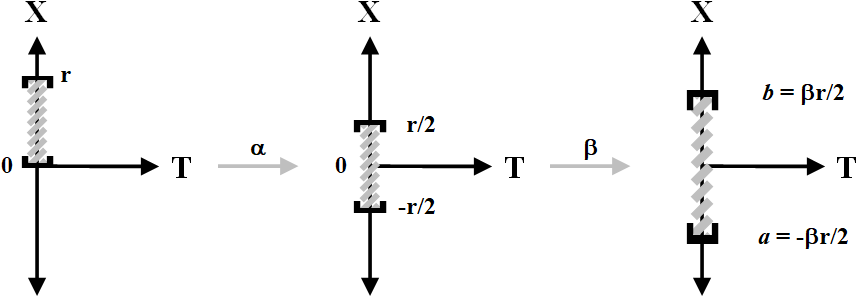

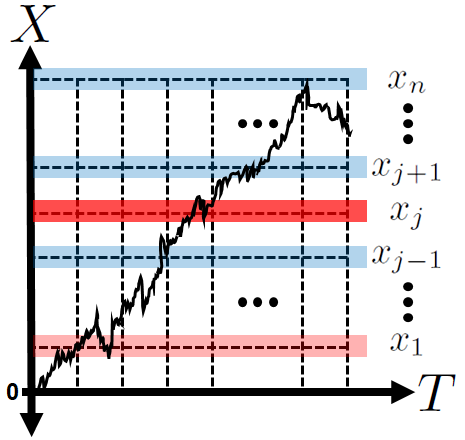

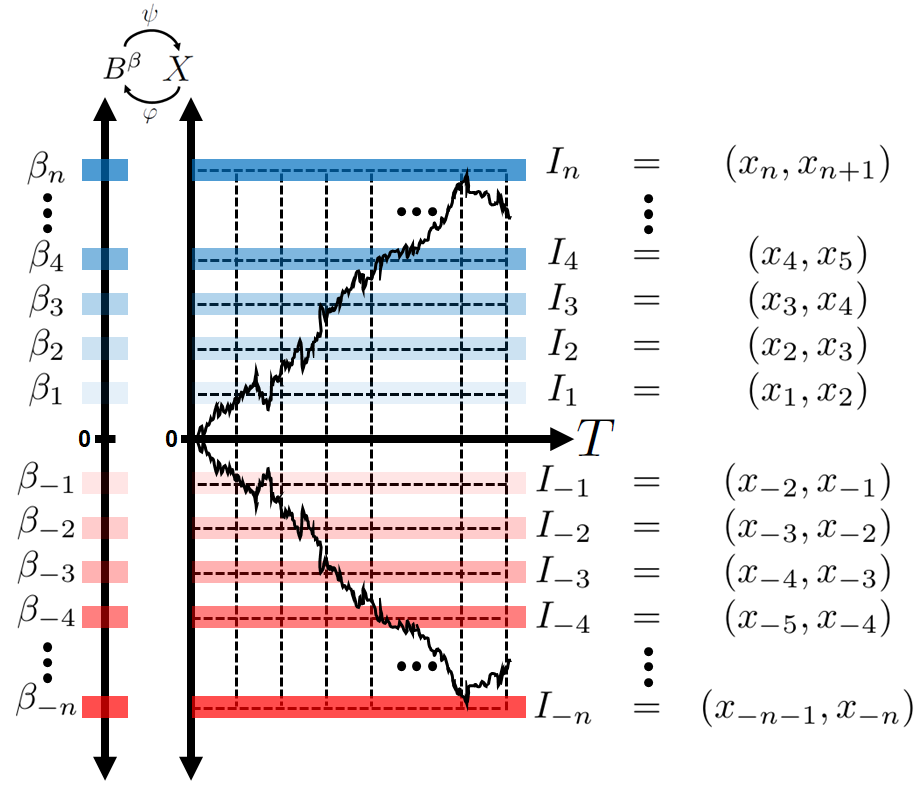

Leveraging the work of Ramirez, [26], we partition into countably infinite intervals , forming the sequence such that the standard conditions are met; , and . We wish to shrink the size of each interval to zero as we apply more and more intervals, where and . This is because we wish to constrain the Itô diffusion by the BGC function .

In terms of BGC stochastic processes, we effectively have a -SBM and will express it as,

| (3.8) |

as illustrated in Figure 9.

Theorem 3.8.

(Skewness Parameter of BGC Stochastic Processes). Let us denote by the -SBM with drift and barriers , and denote by the 2-SBM (i.e. -SMB) with drift , diffusion and barrier . Let us assume , then converges to in the following sense,

The same holds in the case of barriers merging. In this case is the -SBM with drift , diffusion , skewness parameters and barrier , . Then .

Proof.

In contrast to the skewness parameter of the limit -SBM in (3.3), the corresponding skewness parameter of the limit -SBM for BGCSP is given by (3.9),

| (3.9) |

Noting that due to the symmetry of BGCSP about the origin,

which allows the terms to factor out in (3.9) giving,

which expands to,

| (3.10) |

It is clear that the numerator equates to 0 and so , completing the proof. ∎

Remark 3.9.

Theorem 3.10.

(Cylindrical BGCSPs are 2-SBMs). For a complete filtered probability space and a BGC function , , then the corresponding BGC Itô diffusion is defined as follows,

| (3.11) |

where is the drift coefficient, is the diffusion coefficient, is the usual sign function, , , are convex functions and the 2-SBM is defined by,

| (3.12) |

then, almost surely.

Proof.

It is conceivable that under general non-constant and and some generalized BGC function that could modulate such that it is bounded above and below by a constant barrier at and , respectively, where . For this theorem, we are required to prove that constant over time (i.e. cylindrical) BGC functions will converge almost surely to a 2-SBM. We know from at least Krykun, [14] that if , , there exists a strong solution to (3.12). Since the BGC functions are convex, there exists some value for both a hidden lower barrier and a hidden upper barrier that are induced by . For BGCSP, there is no fully reflective barrier defined in advance as there is with M-SBM. However, there are still two fully reflective barriers in BGCSP because the BGC term will enable the constrained Itô process to eventually be overtaken by the underlying unconstrained Itô process such that giving,

| (3.13) |

| (3.14) |

For this to be true, it must be shown that exists. We create a small neighborhood about the initial point of radius such that . As , and will eventually lie in .

If , then such that .

If , then such that .

If , then such that .

Hence exists and its value is for some function . Having found , we know that the reflectiveness at , i.e. , and before , i.e. , . Hence, for must be scaled for by and since is strictly convex and symmetrical about the origin, then the ordering is preserved,

| (3.15) |

(3.15) ensures that a strong solution to BGCSP exists within a 2-SBM framework, completing the proof. ∎

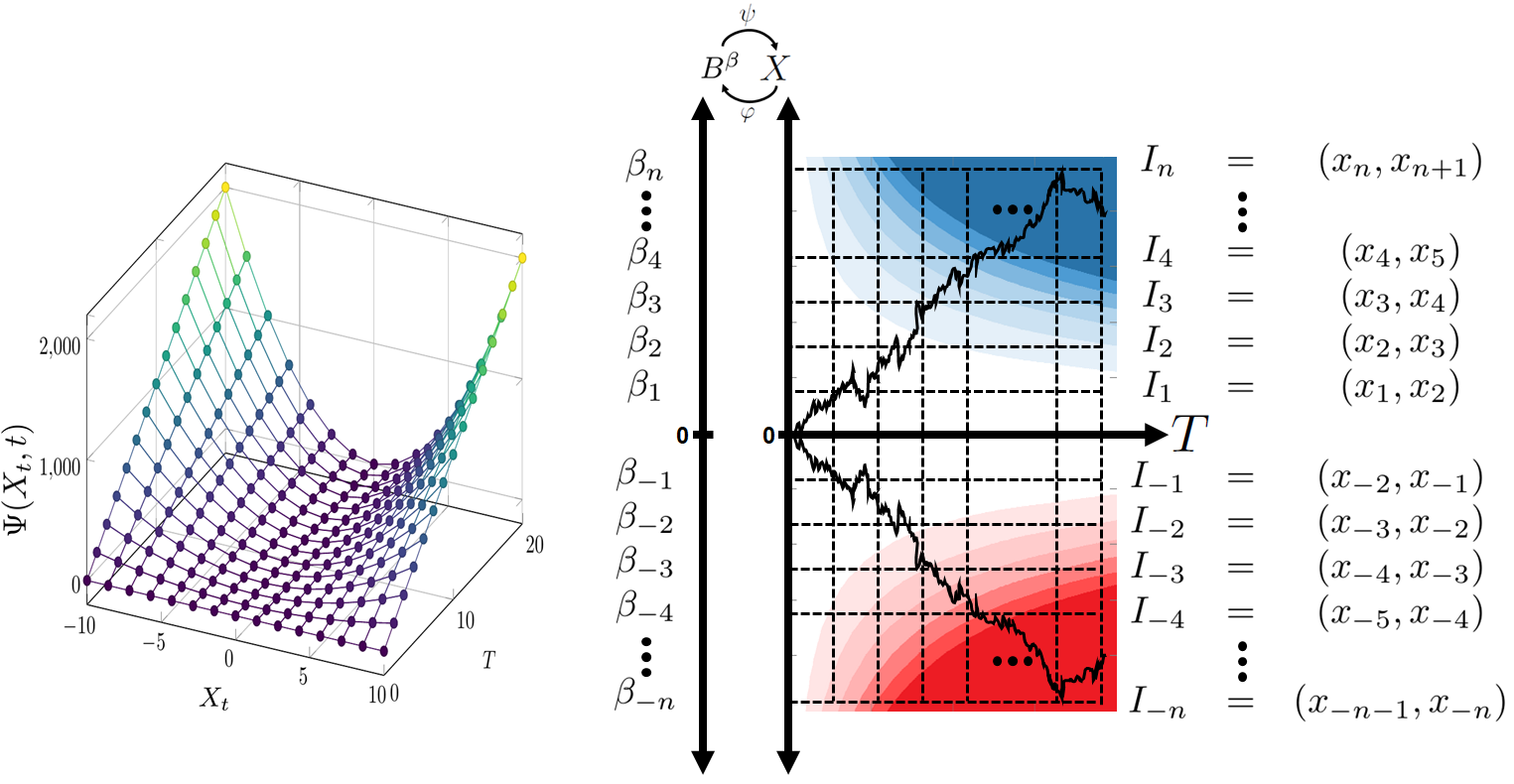

So far, our formulations of BGC functions have been expressed in the general form , but we have considered BGC barriers induced by time-independent convex surfaces which can be specified by just , hence M-SBM is related to BGCSPs with . However, since the barriers have been specified to be able to change not only under space (distance) but over time as well, we demonstrate this additional complexity of BGCSPs in Figure 10.

Having developed the M-SBM and 2-SBM frameworks for BGCSP, we can now support this by numerical simulations in the Results and Discussion section.

4. Results and Discussion

In the following simulations, the underlying unconstrained Itô diffusions have drift and diffusion , resulting in just the Wiener process. This is so that the subsequent impact of BGC can be easily compared. Despite this, we still refer to these as the more general Itô diffusions because these parameters can be modified for one’s specific requirements.

To validate the existing M-SBM research and to support our comparison of BGCSP with M-SBM, we develop Algorithm 1 which is used to progressively introduce additional reflective barriers. In the subsequent series of simulations, we introduce 2, 4, 8, 16 and finally 32 semipermeable barriers, with increasing reflectiveness (i.e. decreasing permeability) the further the Itô diffusion is from the origin, which are simulated via Algorithm 1.

(a). 1,000 Simulations, (b). 10,000 Simulation Density

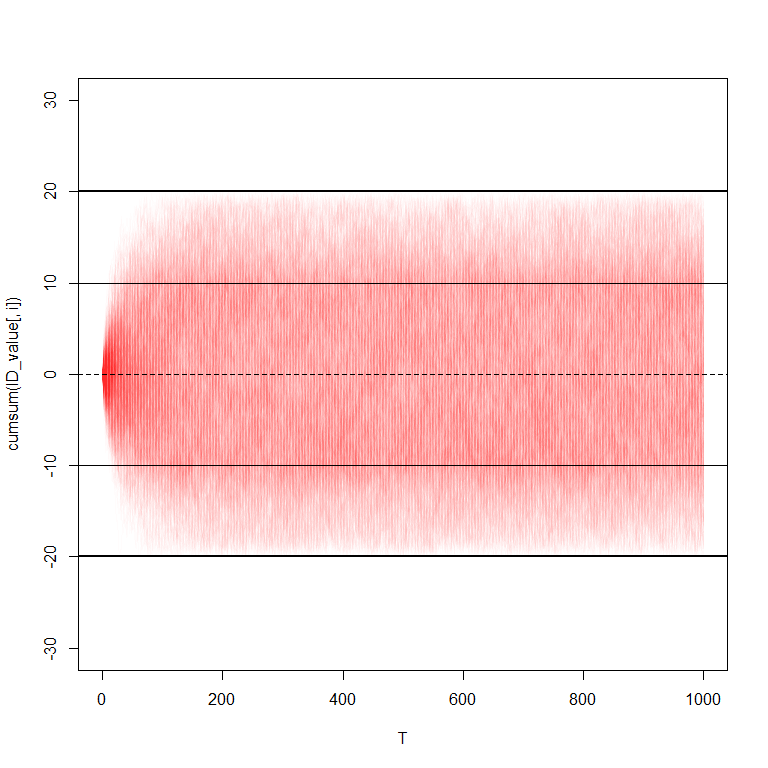

Figure 11 has 2 fully reflective barriers at generated using Algorithm 1. This was then increased to 4 barriers (2 fully reflective and 2 semipermeable) as shown in Figure 12.

(a). 1,000 Simulations, (b). 10,000 Simulation Density

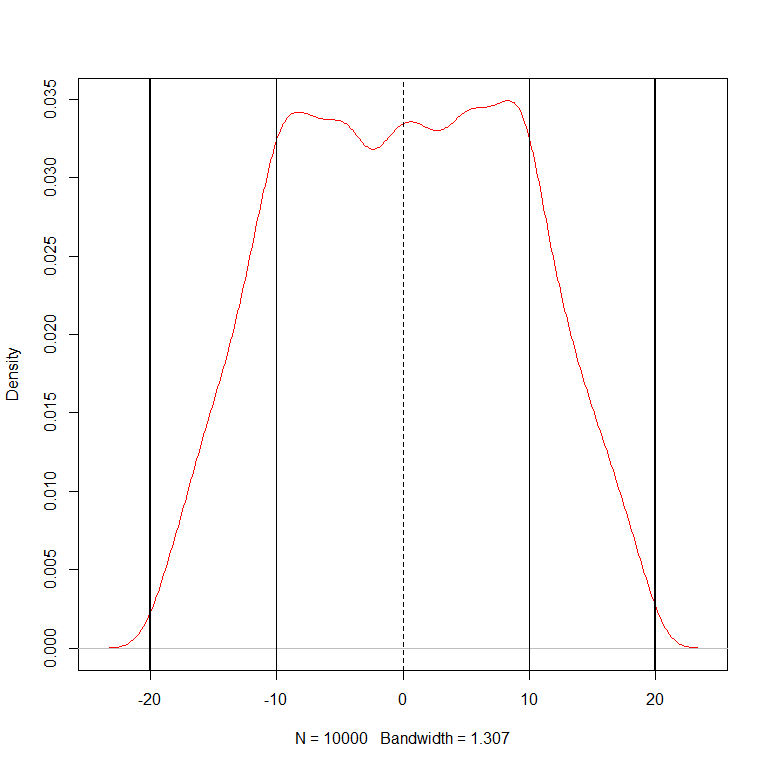

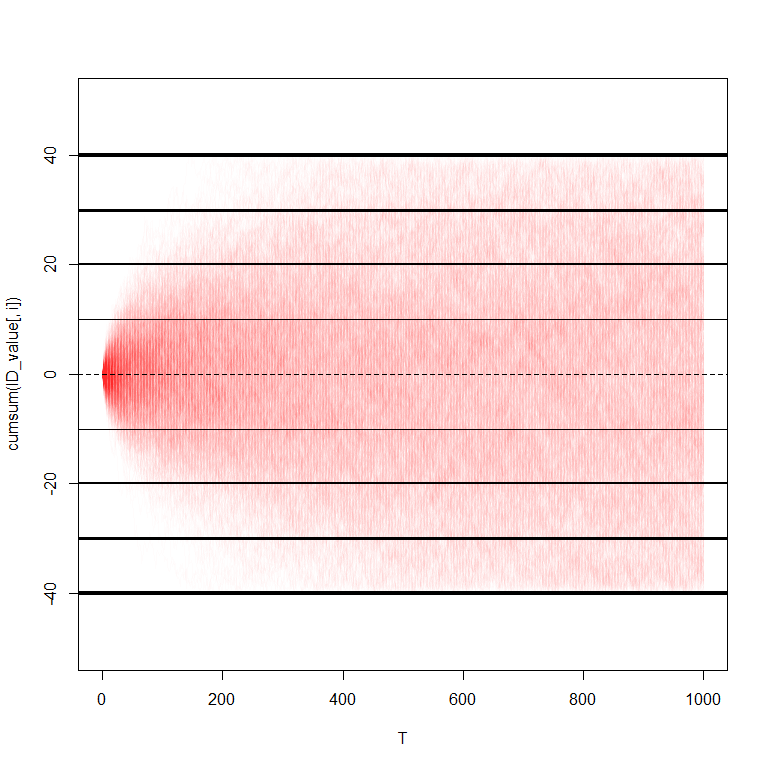

In Figure 12, we make the barriers at fully reflective and the barriers at now to be semipermeable. Although it may not yet be apparent due to the thickness of the drawn barriers, we have and will continue to increase the thickness of the barriers to highlight the increasing reflectiveness (and decreasing semipermeability) the further the Itô diffusions are from the origin. The total number of barriers was doubled again to result in 8 barriers (2 fully reflective and 6 semipermeable), as shown in Figure 13.

(a). 1,000 Simulations, (b). 10,000 Simulation Density

In Figure 13(b), we start to notice a corrugation or ‘crinkling’ of the density due to 2 fully reflective barriers and 6 semipermeable barriers. This was doubled again to 16 barriers (2 fully reflective and 14 semipermeable), as shown in Figure 14.

(a). 1,000 Simulations, (b). 10,000 Simulation Density

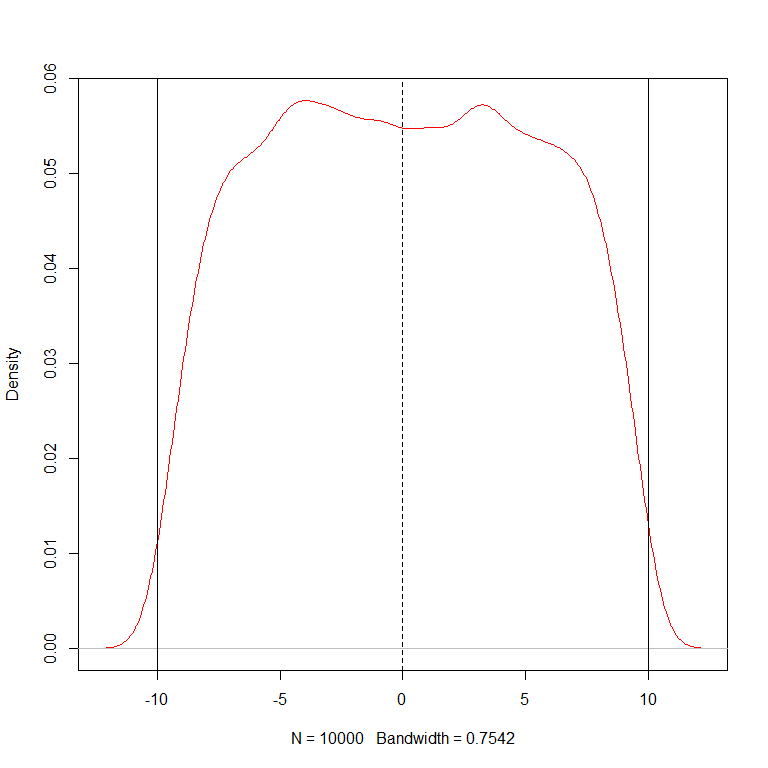

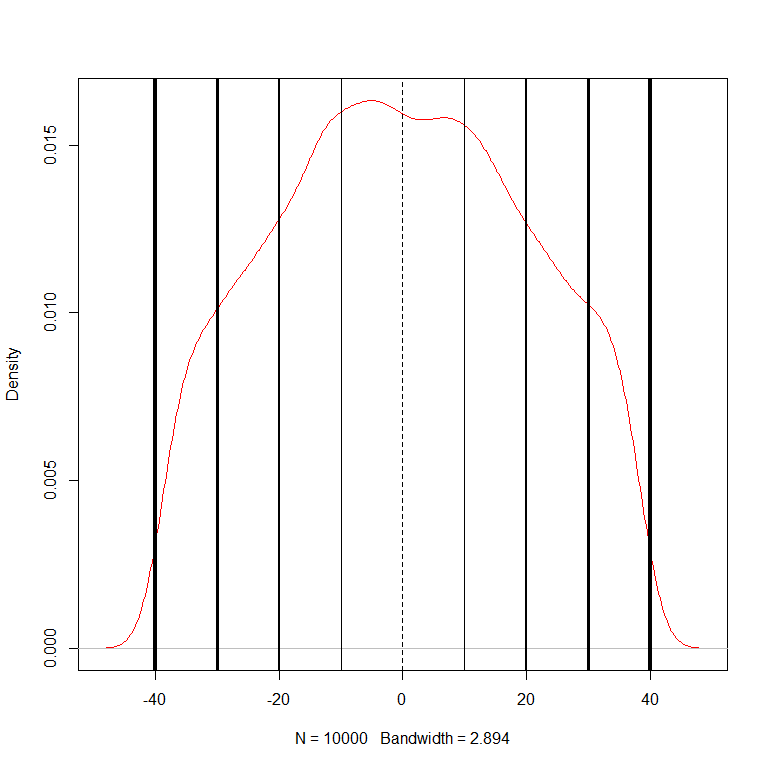

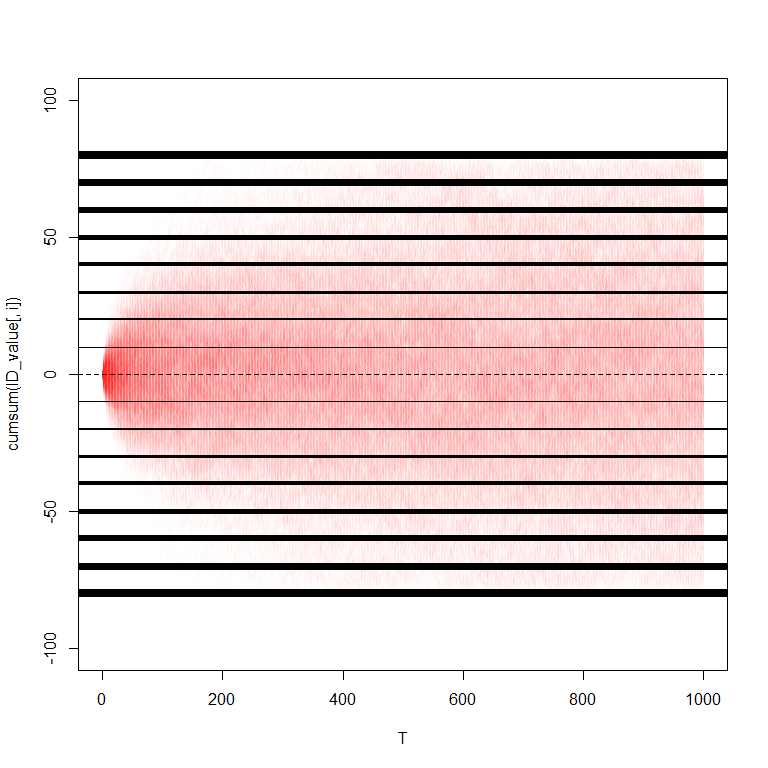

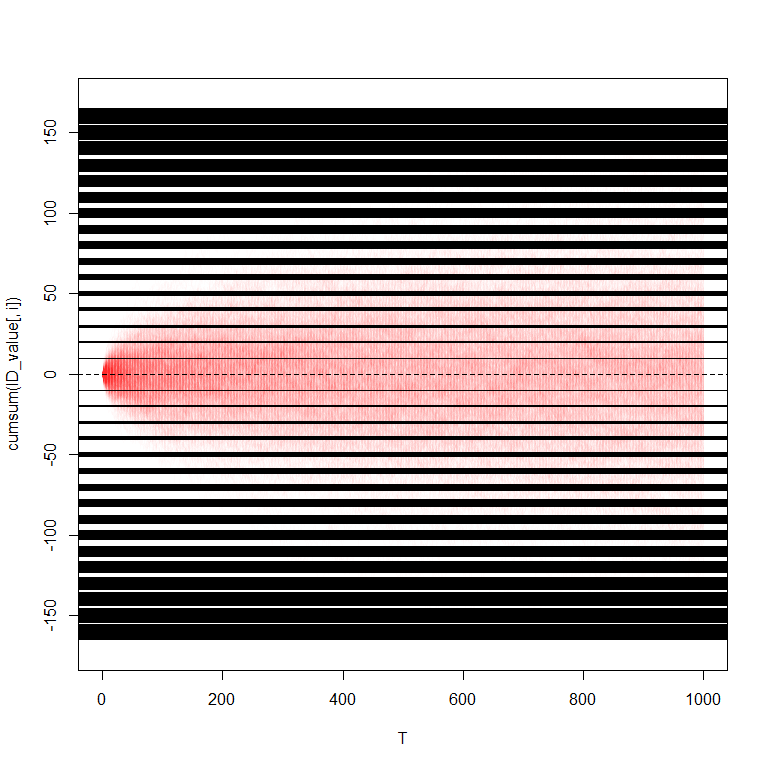

In Figure 14(b), we notice that the corrugation effect has become more pronounced due to another doubling of the number of barriers. This was doubled again to 32 barriers (2 fully reflective and 30 semipermeable), as shown in Figure 15.

(a). 1,000 Simulations, (b). 10,000 Simulation Density

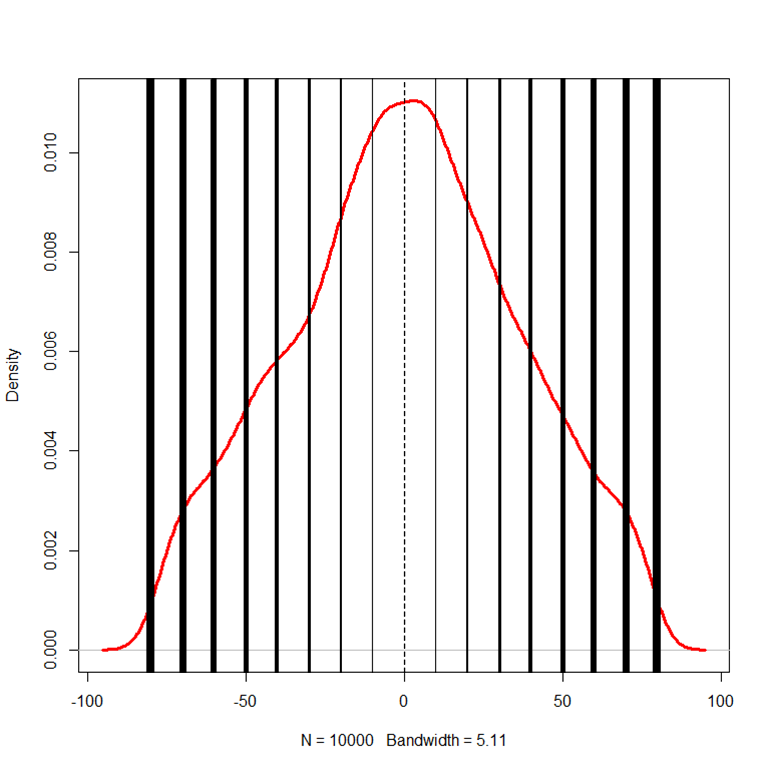

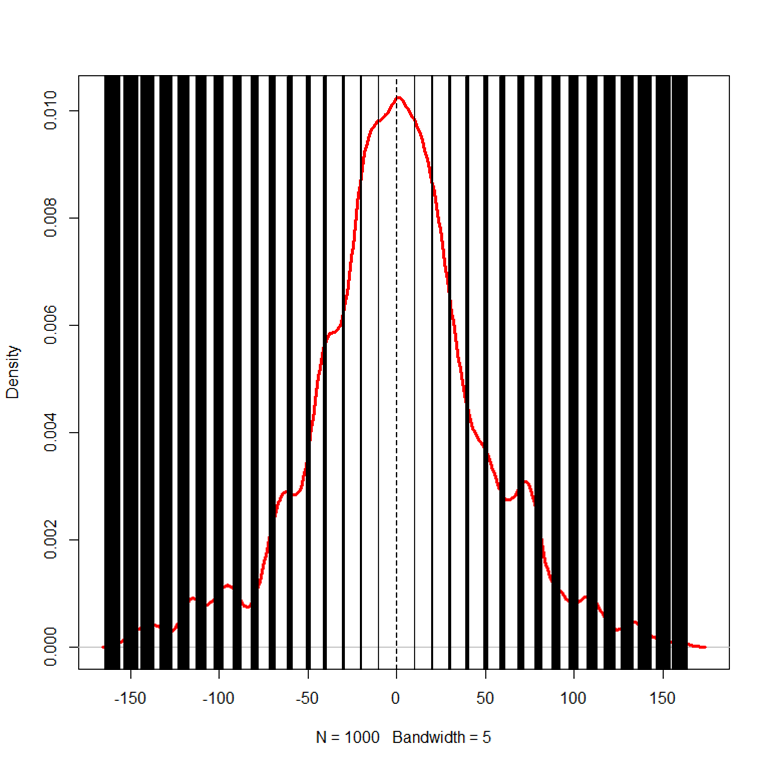

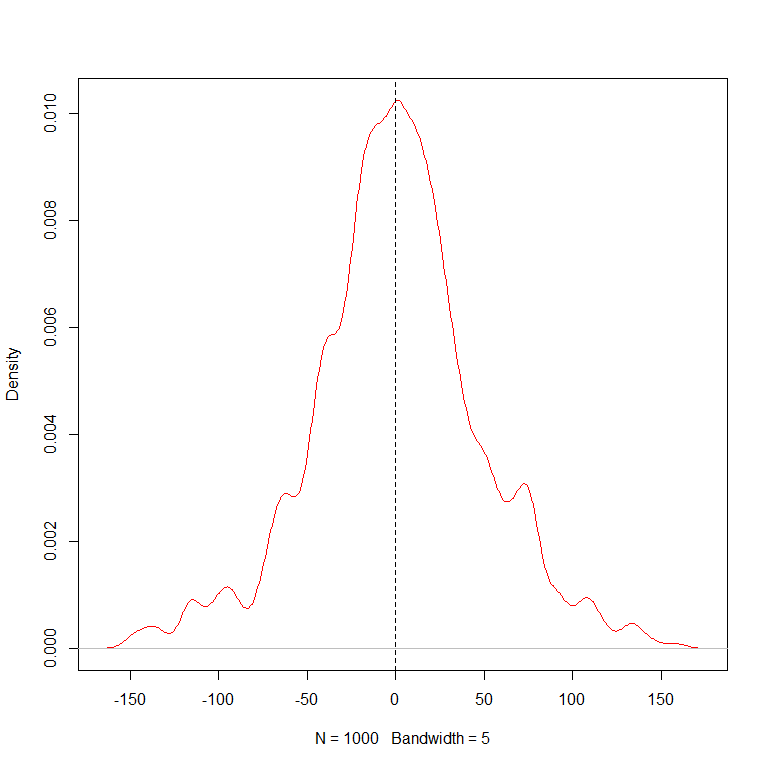

Finally, in Figure 15(b), we notice the most amount of the corrugation effect due to yet another doubling of the number of semipermeable barriers. Due to the importance of this density as a sufficient approximation of BGC densities, we plot the density again in Figure 16 without the barriers depicted and slightly larger.

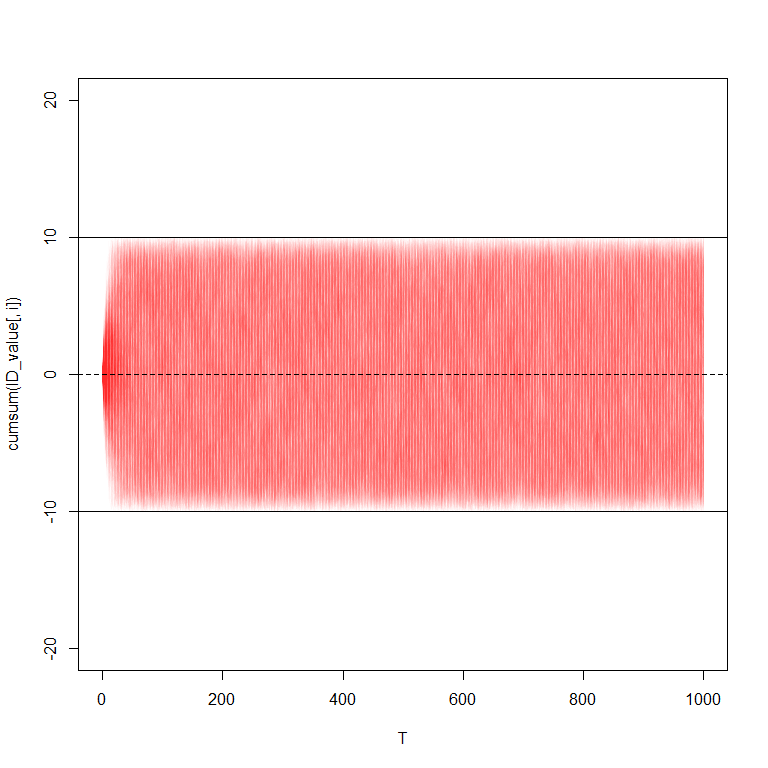

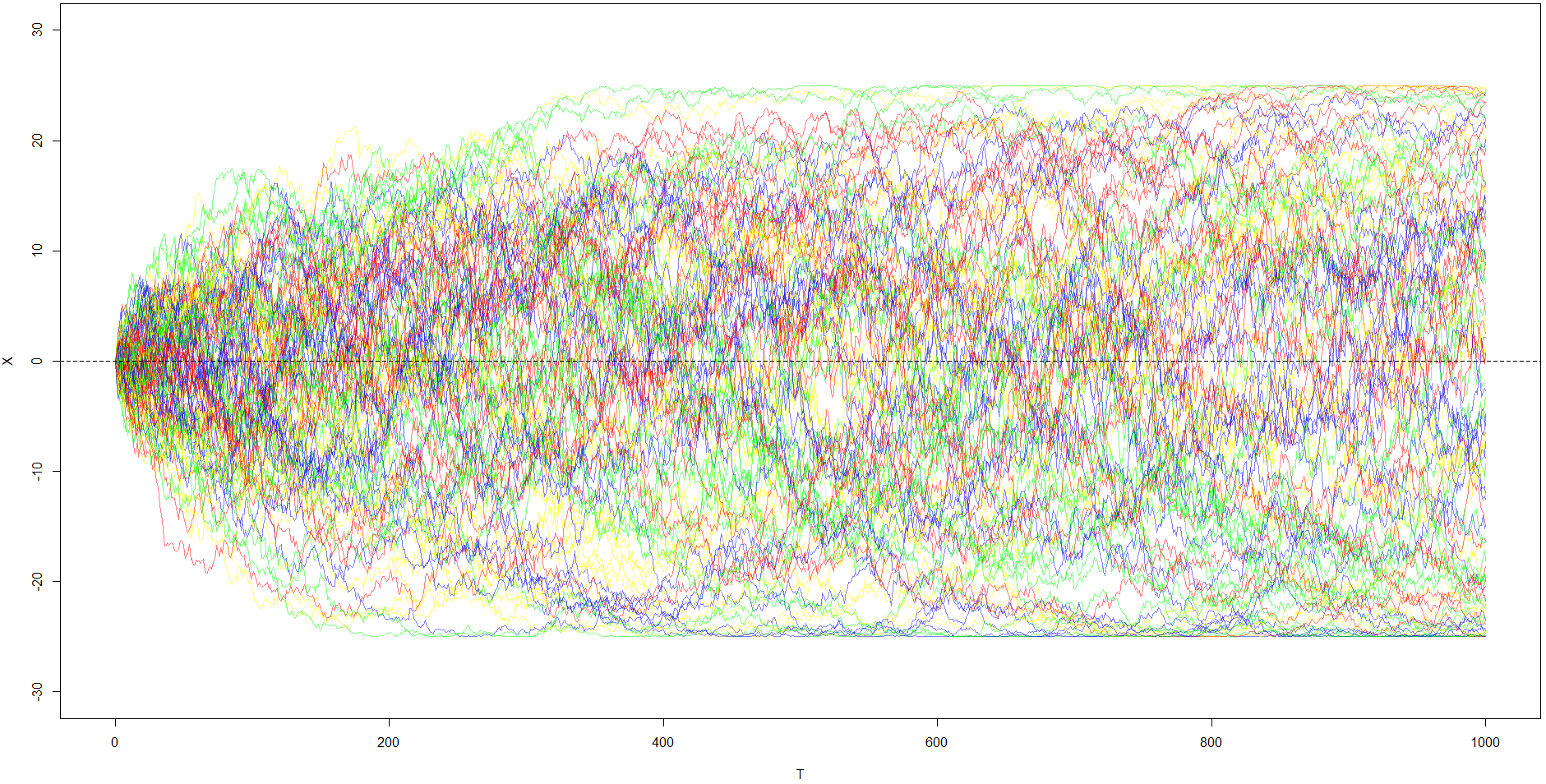

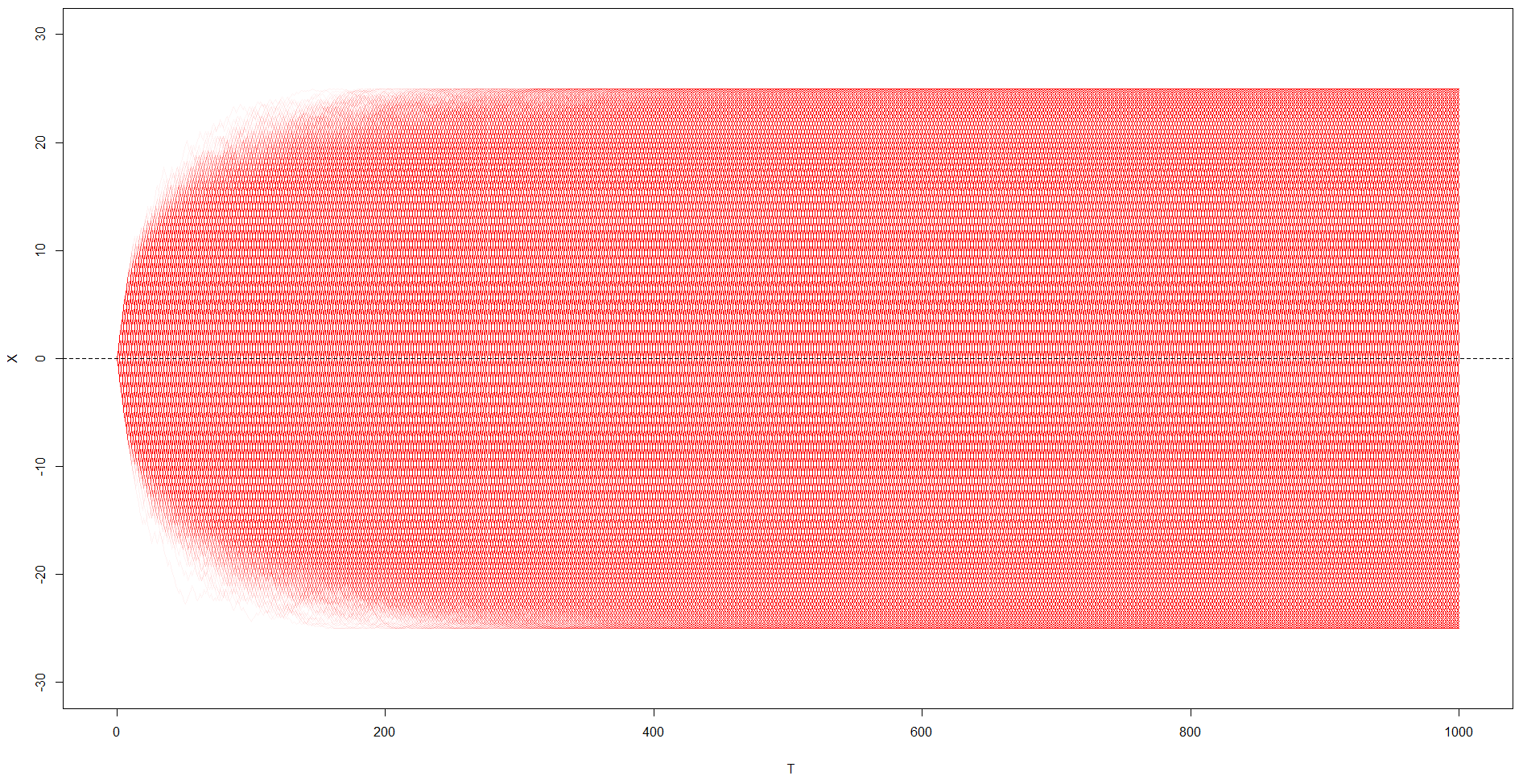

Figure 16 shows that after 32 barriers, we effectively arrive at the typical density of BGC Itô diffusions, which have an infinite number of increasingly reflective barriers, with just 2 fully reflective hidden barriers. If we take the limit of this numerical approximation process, the number of such barriers would approach infinitely many barriers, of smaller and smaller size and hence smaller constraining contribution. These approximation barriers are thus replaced by the main BGC function itself, , as shown in Figure 17, where the algorithm for BGCSP was stated in [32].

(a). 1,000 Simulations, (b). 10,000 Simulation Density

From Figure 17, we see the typical characteristics of BGCSPs; 1). a certain amount of discretization or banding at various local times, 2). the emergence of two hidden reflective barriers that are not known exactly in advance and can only be estimated, 3). the density is ‘corrugated’ or ‘rough’.

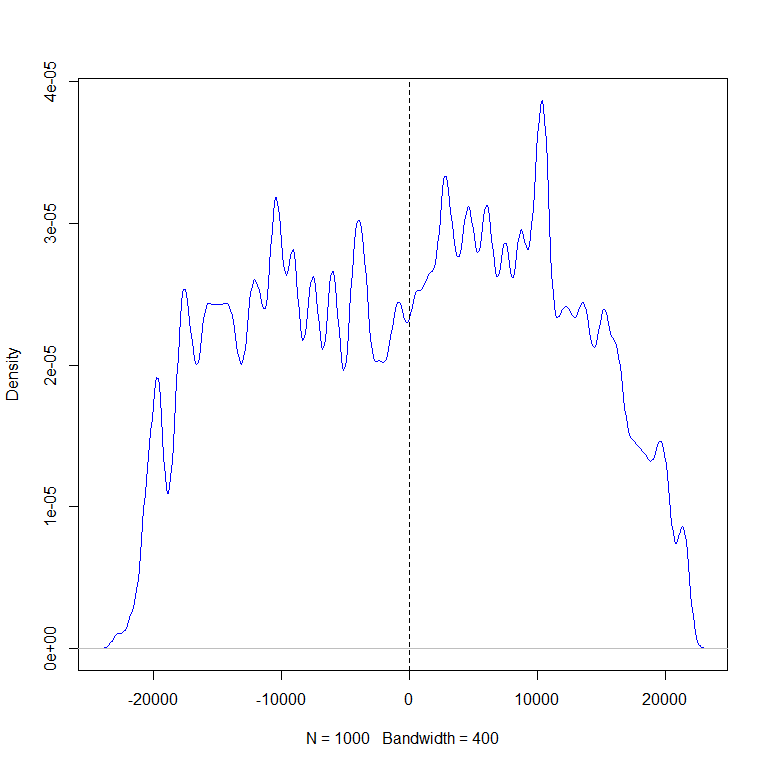

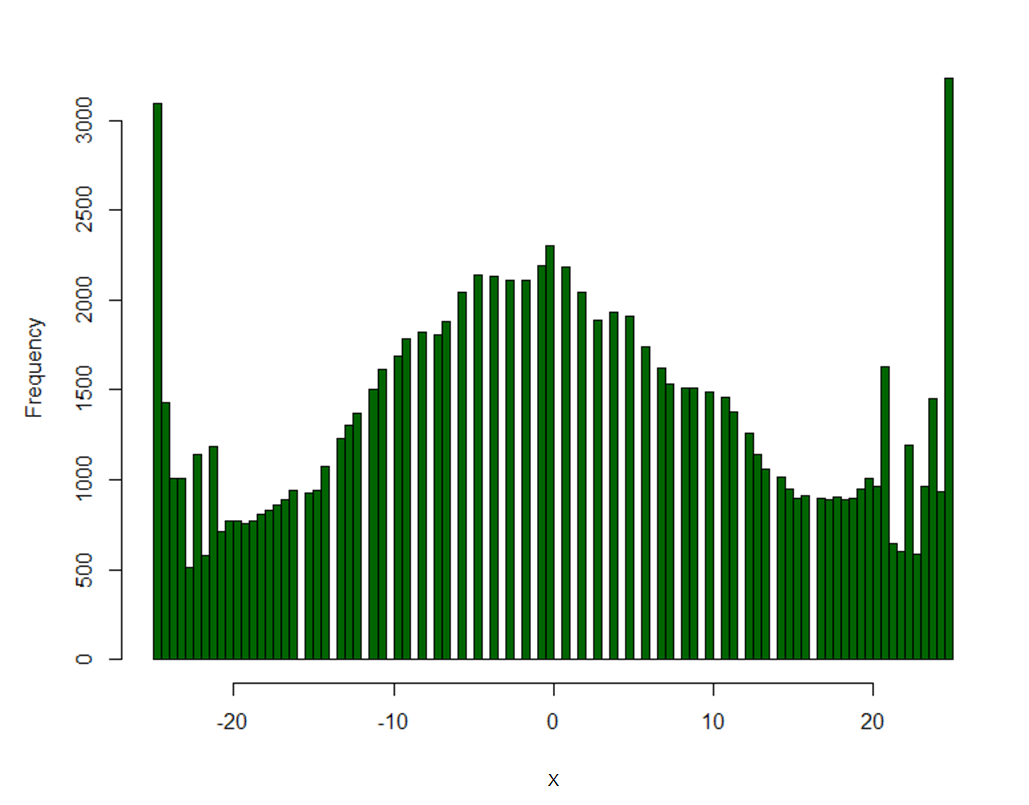

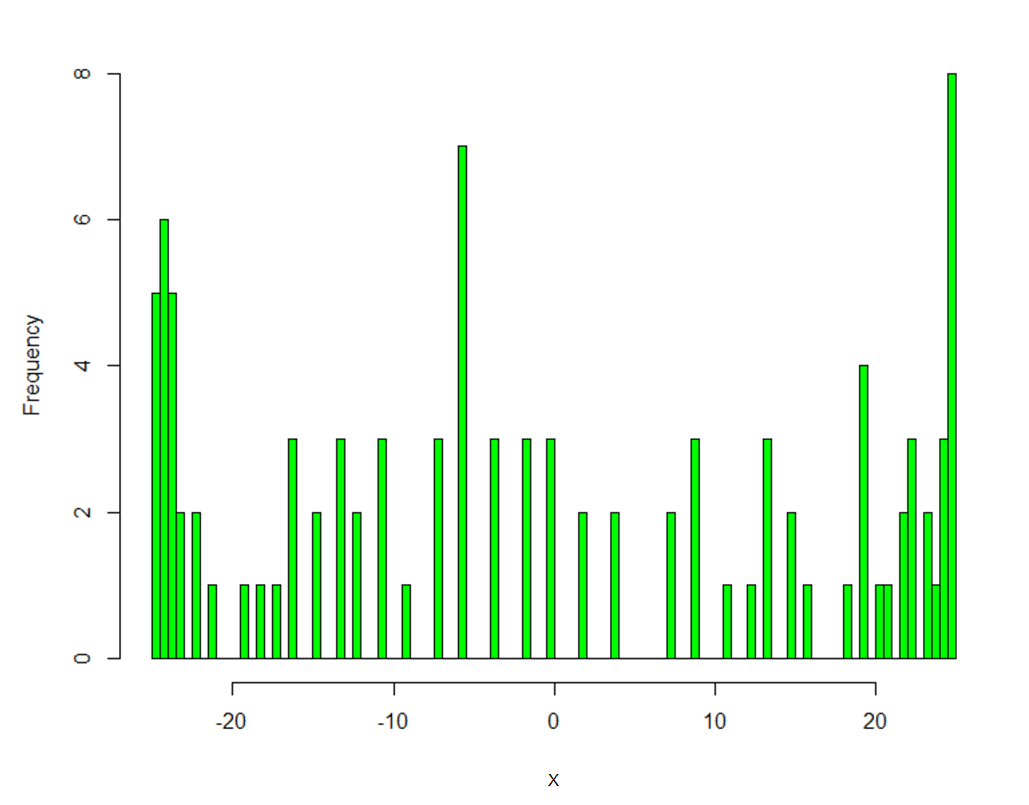

The random component of the Itô diffusions, i.e. the term is sampled from a standard normal distribution that is then constrained by BGCSP. The density of Figure 17(b) has no discontinuities. However, if we sample the path increments from a discrete binary (i.e. binomial) random distribution, we obtain a random walk that is then constrained by BGCSP. When a histogram is derived for the corresponding simulated data rather than fitting a density through the distribution, we obtain Figure 18, which shows the discontinuities, also evident in [33].

(a). , (b). .

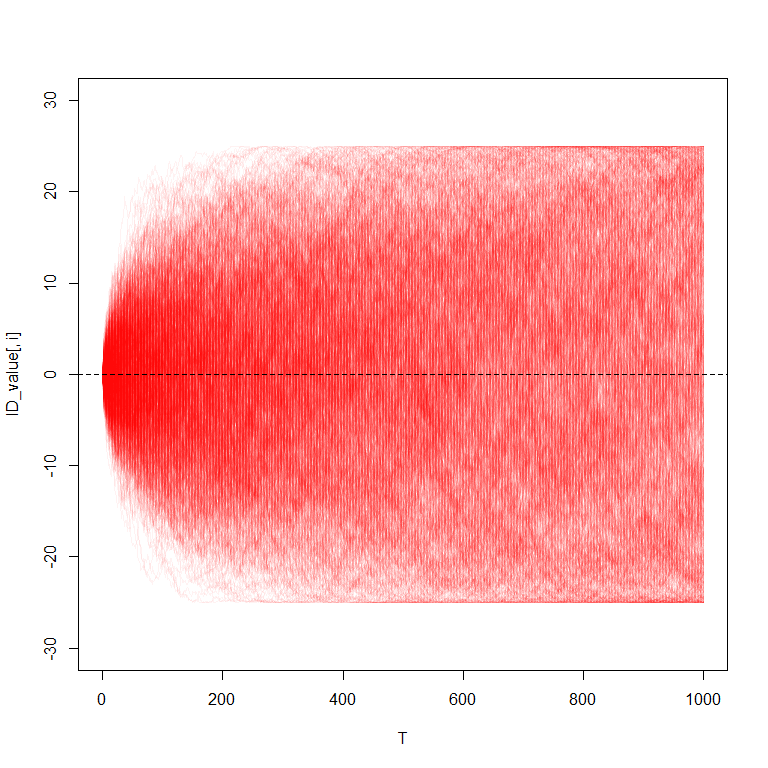

Figure 18 shows that 1). reflection occurs at the barriers as seen by the peaks on either side of the distribution (more prominent in (a)), and 2). discretization or banding occurs at prominent local times that are contracted together due to the BGC function . Figure 18(a) shows similar ‘corrugation’ as in the continuous case in Figure 16. Figure 18(b) shows that at , the BGC Itô diffusion is less likely to be at the origin and more likely to be near the barrier(s). To further demonstrate the characteristics of BGCSP, a detailed plot of 10,000 simulations are shown in Figures 19 and 20.

5. Conclusions

This paper has extended the previous theoretical research on BGCSP by comparing them to a type of multi-skew Brownian motion (M-SBM). This was achieved both theoretically by leveraging existing research, and heuristically by generating new simulations. Working within the M-SBM framework, we proved one Lemma and two Theorems for BGCSPs. This research provides a richer framework in which the semipermeable barriers are modulated in a non-constant manner over distance , allowing for a new constraining regime that is more complex than the Ornstein-Uhlenbeck process (OUP) and yet still related to it. BGCSPs have applications in many fields requiring the constraining of the underlying stochastic process in a gradual manner where the two ultimate reflective barriers are not known in advance.

References

- Appuhamillage and Sheldon, [2012] Appuhamillage, T. and Sheldon, D. (2012). First passage time of skew brownian motion. J. Appl. Probab., 49(3):685–696.

- Atar and Budhiraja, [2015] Atar, R. and Budhiraja, A. (2015). On the multi-dimensional skew brownian motion. Stochastic Process. Appl., 125(5):1911–1925.

- Ball and Roma, [1998] Ball, C. A. and Roma, A. (1998). Detecting mean reversion within reflecting barriers: application to the european exchange rate mechanism. Applied Mathematical Finance, 5(1):1–15.

- Bramson et al., [2010] Bramson, M., Dai, J., and Harrison, J. (2010). Positive recurrence of reflecting brownian motion in three dimensions. The Annals of Applied Probability, 20(2):753–83.

- Budhiraja and Dupuis, [2003] Budhiraja, A. and Dupuis, P. (2003). Large deviations for the emprirical measures of reflecting brownian motion and related constrained processes in r+. Electronic Journal of Prob., 8.

- Dereudre et al., [2015] Dereudre, D., Mazzonetto, S., and Roelly, S. (2015). An explicit representation of the transition densities of the skew brownian motion with drift and two semipermeable barriers. arXiv preprint arXiv:1509.02846.

- Dua et al., [1976] Dua, S., Khadilkar, S., and Sen, K. (1976). A modified random walk in the presence of partially reflecting barriers. J. Appl. Prob., 13:169–175.

- Gairat and Shcherbakov, [2017] Gairat, A. and Shcherbakov, V. (2017). Density of skew brownian motion and its functionals with application in finance. Mathematical Finance, 27(4):1069–1088.

- Gupta, [1966] Gupta, H. (1966). Random walk in the presence of a multiple function barrier. Journ. Math. Sci., 1:18–29.

- Harrison and Shepp, [1981] Harrison, J. and Shepp, L. (1981). On skew brownian motion. Ann. Probab., 9(2):309–313.

- Harrison, [1986] Harrison, M. (1986). Brownian Motion and Stochastic Flow Systems. John Wiley & Sons.

- Hu et al., [2012] Hu, Q., Wang, Y., and Yang, X. (2012). The hitting time density for a reflected brownian motion. Computational Economics, 40(1):1–18.

- Itô and McKean, [1965] Itô, K. and McKean, H. (1965). Diffusion Processes and Their Sample Paths. Springer, New York.

- Krykun, [2017] Krykun, I. (2017). Convergence of skew brownian motions with local times at several points that are contracted into a single one. Journal of Mathematical Sciences, 221(5):671–678.

- LeGall, [1984] LeGall, J. (1984). One-dimensional stochastic differential equations involving the local times of the unknown process. Springer, Berlin, Heidelberg.

- Lehner, [1963] Lehner, G. (1963). One-dimensional random walk with a partially reflecting barrier. Ann. Math. Stat., 34:405–412.

- Lejay, [2006] Lejay, A. (2006). On the constructions of the skew brownian motion. Probab. Surv., 3:413–466.

- L’epingle, [2009] L’epingle, D. (2009). Boundary behavior of a constrained brownian motion between reflecting-repellent walls.

- Linetsky, [2005] Linetsky, V. (2005). On the transition densities for reflected diffusions. Advances in Applied Probability, 37(2):435–460.

- Lions and Sznitman, [1984] Lions, P. and Sznitman, A. (1984). Stochastic differential equations with reflecting boundary conditions. Communications on Pure and App. Maths, 37(4):511–537.

- Mazzonetto, [2016] Mazzonetto, S. (2016). On the exact simulation of (skew) Brownian diffusions with discontinuous drift (Doctoral dissertation, Universität Potsdam).

- Mazzonetto, [2019] Mazzonetto, S. (2019). Rates of convergence to the local time of oscillating and skew brownian motions. arXiv preprint arXiv:1912.04858.

- Ouknine et al., [2015] Ouknine, Y., Russo, F., and Trutnau, G. (2015). On countably skewed brownian motion with accumulation point. Electron. J. Probab., 20(82):1–27.

- Percus, [1985] Percus, O. (1985). Phase transition in one-dimensional random walk with partially reflecting boundaries. Adv. Appl. Prob., 17:594–606.

- Portenko, [1976] Portenko, N. (1976). Generalized diffusion processes. Springer, Berlin.

- Ramirez, [2011] Ramirez, J. (2011). Multi-skewed brownian motion and diffusion in layered media. Proceedings of the American Mathematical Society, 139(10):3739–3752.

- Sacerdote et al., [2016] Sacerdote, L., Tamborrino, M., and Zucca, C. (2016). First passage times of two-dimensional correlated processes: Analytical results for the wiener process and a numerical method for diffusion processes. Journal of Computational and Applied Mathematics, 296:275–292.

- [28] Taranto, A. and Khan, S. (2020a). Bi-directional grid absorption barrier constrained stochastic processes with applications in finance and investment. Risk Governance & Control: Financial Markets & Institutions, 10(3):20–33.

- [29] Taranto, A. and Khan, S. (2020b). Drawdown and drawup of bi-directional grid constrained stochastic processes. Journal of Mathematics and Statistics, 16(1):182–197.

- [30] Taranto, A. and Khan, S. (2020c). Gambler’s ruin problem and bi-directional grid constrained trading and investment strategies. Investment Management and Financial Innovations, 17(3):54–66.

- [31] Taranto, A. and Khan, S. (2021a). Application of bi-directional grid constrained stochastic processes to algorithmic trading. Journal of Mathematics and Statistics, 17(1):22–29.

- [32] Taranto, A. and Khan, S. (2021b). Hidden geometry of bi-directional grid constrained stochastic processes. arXiv preprint.

- Taranto et al., [2020] Taranto, A., Khan, S., and Addie, R. (2020). Iterated logarithm bounds of bi-directional grid constrained stochastic processes. arXiv Preprint: Modern StochAstic Models & ProbleMs Of Actuarial MaTHematics (MAMMOTH) Conference, pages 1–21.

- Weesakul, [1961] Weesakul, B. (1961). The random walk between a reflecting and an absorbing barrier. Ann. Math. Statist., 32:765–769.