Proof of non-convergence of the short-maturity expansion for the SABR model

Alan L. Lewis111Newport Beach, California, USA; email: alewis@financepress.com

and Dan Pirjol222School of Business,

Stevens Institute of Technology, Hoboken, NJ 07030; email:dpirjol@gmail.com

(26 July 2021)

Abstract

We study the convergence properties of the short maturity expansion of option

prices in the uncorrelated log-normal () SABR model.

In this model the option time-value can be represented as an integral of the form

with a “payoff

function” which is given by an integral over the McKean kernel .

We study the analyticity properties of the function in the complex

-plane and show that it is holomorphic in the strip . Using this result

we show that the -series expansion of and implied volatility are asymptotic (non-convergent for any ).

In a certain limit which can be defined either as the large volatility limit at fixed , or the small vol-of-vol limit limit at fixed , the short maturity -expansion for the implied volatility

has a finite convergence radius .

1 Introduction and motivation

The SABR model is a versatile stochastic volatility model which has proved

very popular with practitioners since its introduction almost 20 years ago [5].

It was originally introduced to model interest rate volatilities,

but its application has been extended later also to other asset classes,

such as FX and commodities.

The model is described by the diffusion

(1)

(2)

where are standard Brownian motions correlated with correlation

.

The volatility of volatility (vol-of-vol) parameter determines the curvature of the implied volatility, and the backbone function is introduced such that the model captures the smile dynamics of the ATM (“at-the-money”) implied volatility

under spot price changes.

In the original SABR paper [5] the backbone function was chosen

as a power function (CEV-like) with .

In practice more complicated forms are

used, such as the three-regime backbone of de Guillaume, Rebonato and Pogudin [4], reflecting the empirically observed backbone behavior of swaption volatilities. Since in the academic literature the SABR model is typically defined with CEV-like backbone, we also use the same convention and refer to the values of

in the SABR model implied as the CEV backbone.

The leading order in the short maturity expansion for the implied volatility for the SABR model was obtained in [5].

The subleading correction was also computed in this paper at the ATM point. The result has a simple analytical form, and is easily implemented in practice for model simulation and calibration. This feature contributed to the widespread adoption and popularity of the model.

Higher order corrections to the short maturity expansion of the implied volatility in the SABR model were obtained by Henry-Labordére [6] and Paulot [14]. The complete contribution

was obtained in [14], although its evaluation involves numerical integration for some terms.

A systematic algorithm for expanding the implied volatility in a double series expansion in log-strike and maturity was mentioned in [8], and is used here once to generate (1) below. (However, none of our subsequent results rely upon this algorithm.)

Throughout, we work with the so-called “log-normal” SABR model: .

The (Black-Scholes) implied volatility in this model has the

full parametric dependence .

Here , so ATM means , and is the time to option maturity.

For reference purposes we give here the expansion of the ATM implied volatility to (to our knowledge the full term is new [9]):

(3)

From here on, we work with ;

the general case can be recovered as

(4)

With and (suppressing the display of all three parameters), a second reference expansion is:

(5)

Although efficient numerical techniques are available for option pricing with general strike and maturity [8, 1], series expansions are very convenient. Thus, it is useful to explore their limits of applicability. We address the following questions: what is the nature of the short-maturity expansion of the implied volatility around the ATM point? Is it strictly asymptotic or convergent? If convergent, is there a finite radius of convergence?

In this note, we show that the full expansion underlying

(5) is strictly asymptotic, via a careful analysis of the (closed-form) SABR option value . Briefly, the argument is as follows. We show in (12) below that the value function can be put into the form

, calling a “payoff function”.

Our key result, Theorem 2, establishes that

) admits an analytic continuation to the strip in the complex -plane. This function has singularities at .

Theorem 2 may be of separate interest because itself is given by a non-trivial integral. From Theorem 2, the non-convergence of (5) for all follows from term-by-term integration of ’s power series in .

Arguably, non-convergence may have been the expected result. However,

there is a curious and interesting “large scaling limit” – where the convergence story changes. This limit was introduced and first studied in [15].

In that limit, under our current setup, take

and , holding fixed.

(Under general this limit corresponds to taking at fixed and arbitrary , holding fixed.)

Substituting in (5), one sees that

(6)

Mechanically, large scaling has the effect of (i) suppressing all the odd -powers in (5) and

(ii) keeping only the largest power of in each even -power.

In the Appendix, we present a (new) derivation of the closed-form relation for ,

a relation first obtained in [15] by a time discretization argument.

The series in (6) has a finite (non-zero) convergence radius in the complex -plane (see Sec. 6).

2 The SABR value function

Our starting point is the exact representation of the (time) value of call option prices in the uncorrelated SABR model. From Eq. (3.103) in [1]:

(7)

with .

This expression assumes . This parameter can be restored to a general value by replacing and as in

(4).

The function is related to the McKean heat kernel

[11] for the Brownian motion on the Poincaré hyperbolic plane

. The precise relation is

.

The function is given explicitly by

(8)

Geometrically, suppose is the hyperbolic distance between two points and

in .

Then, is the transition density for a hyperbolic Brownian particle,

starting at , to reach the point after time . Thus is similar to a

complementary distribution function – the tail probability for the particle to move a hyperbolic distance greater than at time . (See [1] for further discussion.)

A similar integral expression to (7) holds in the uncorrelated

SABR model with , with different upper and lower integration limits,

and a different form for the sine factor.

We study here the case for definiteness.

Combining (7) with the integral representation of in

Eq. (8) and exchanging the order of

integration, the option time value can be put into the form

(9)

with

(10)

(11)

At the ATM point we have and the expression (9) simplifies as

(12)

with

(13)

We study the analyticity of in the complex variable.

It is instructive to first generalize the situation.

3 Analyticity of a class of general value functions

Consider the analyticity of general value functions in the complex -plane

which can be represented in the form

(14)

and where is any “analytic payoff function”. Here are two model-dependent constants,

irrelevant for analyticity. We introduce the following definition.

A payoff function is said to be an analytic payoff function if there exists a function of the

complex variable which is regular (analytic and single-valued) in the circle and a constant

such that for .

We call the analytic continuation of .333 Our definition is in the spirit of Lukacs [10] for “analytic characteristic functions”. A difference is that the agreement between and need only hold here for (an interval of) the positive real axis. When , then is entire.

A further adopted restriction, very convenient for our problem, assumes an odd function:

. As it turns out, this antisymmetry holds for analytic continuations under both

SABR and Black-Scholes (BS) models, with and

respectively. There is an important (subtle) point regarding oddness. As it’s seen in the BS case

in an elementary way, consider that first.

With , a generic call option value function , with the strike price,

using . Here is the set of initial conditioning information: in the BS model,

in the SABR model, etc.

Under BS, follows geometric Brownian motion

with . Here denotes a normal distribution with mean and variance , and (for this section alone) “” denotes “is distributed as”. Taking ATM with ,

showing a well-known result using the error function. Thus, , odd as advertised. But, of course the “original” payoff

function was defined for () and vanishes there. Arguably,

, certainly not odd.

Yet, given the representation (14), we find

admits an analytic continuation , an odd function. Thus, for real negative ,

a possibility already hinted at in footnote 3.

We belabor the point because a similar thing happens with the SABR model. Manifestly from (13), , easily confirmed from a plot. But, the power series (33) below is an odd series. The resolution of the apparent discrepancy is that the analytic continuation of

, to the negative real axis via , is not found by mechanically taking a negative value of in the

integral of (13), even though that (extended) integral technically exists. (Indeed, a mechanical plot of

(13) over an interval , with , shows a function not even differentiable at ). Instead, the analytic continuation enforces the antisymmetry of the power series for . That should motivate part of our

key Theorem 2 below. That theorem will establish that is indeed an analytic payoff function

with finite convergence radius .

Small-maturity expansion of the value function.

Under our assumptions, for some

sequence of coefficients

, as long as . We allow finite , or for entire functions.

Integrating term-by-term gives a formal expansion of a “normalized value function” ,

defined by

(16)

differs from by a and the pre-factors of (14).

Our issue is the convergence or not, of the power series for . Consider three cases:

1.

analytic with .

(Example: SABR with . This will be shown below in Sec.4.).

2.

entire and of exponential type . (Example: BS with .).

3.

entire of order 2 and type .

Now, by the root test for

convergence, if converges,

its radius of convergence is .

Here . Freely invoking Stirling’s approximation,

we obtain the following convergence properties for each of the cases enumerated.

Case 1. Since is analytic with radius , . Thus, the convergence radius of is

In words, the -series for , under Case 1, has zero radius of convergence.

Case 2. Since and at ,

for large , . Now

Thus, under Case 2, is entire. This agrees with the BS result from (3): since is entire and odd, is an entire function of .

Case 3. If at , for large , . Now

For order 2, type payoffs, the series converges for .

4 Analyticity of the SABR payoff function

In this section we study the extension of the function defined by the integral

(13) to complex values of .

The integral (13) is well defined along the real axis .

We would like to construct a holomorphic function which reduces to along the positive real axis, and determine its maximal domain of holomorphicity.

The limitations of this domain are due to the singularities of the factor in the denominator. Defining this factor as a single-valued function for complex requires some care in the choice of the branch cut of the square root. We will choose to define the square root with a cut along the real positive axis, and denote it as . Specifically, if denotes the standard square-root with a branch-cut along the negative

real axis, then

(19)

This choice is guided by the following lemma.

Lemma 1.

The equation with and real has no solutions in the half-strip .

Proof.

Writing we have with

(20)

(21)

We distinguish the two cases:

i) . We have and for all , so the

equation clearly does not have a solution.

ii) . Fix and vary in .

We will show that if has a zero at , then

, which proves the statement of the lemma.

Step 1.

For we have the lower bound

(22)

since is increasing on .

We used here which holds for all .

This implies that if has a zero then it must lie in

.

Step 2.

For , the function is negative. This follows

from the upper bound

(23)

since is decreasing on .

We used here and .

∎

We rely subsequently upon two textbook results for analytic continuation. The first is the classic Schwarz reflection principle.

The second is the analyticity of certain functions defined via an integration.

For ease of reference we state the result below, in the formulation of Stein and Shakarchi [17].

Theorem 1(Stein and Shakarchi [17], Th. 5.4 Ch. 2).

Let be defined for , where is an open set in ℂ.

Suppose satisfies the following properties:

(i) is holomorphic in for each .

(ii) is continuous on .

Then the function defined on by is holomorphic.

We shall construct a function which is holomorphic

in the entire strip , and which reduces to the function

defined by the integral in (13) along the real positive axis.

Definition 1.

First, using , define in the interior

and boundaries of the upper half-strip in the first quadrant

as the integral

(24)

Elsewhere in the strip, the function is defined by combined application of the odd symmetry property in and Schwarz reflection principle

(28)

Theorem 2.

is holomorphic (and hence analytic) in .

Proof.

The -integral in (13) is well defined for positive real .

We would like to define an analytic continuation of this integral to the complex

-plane, in the strip , which agrees with the original integral for positive real .

With , along the upper side of the cut (the positive real axis),

is positive and real, and reproduces the denominator in (13).

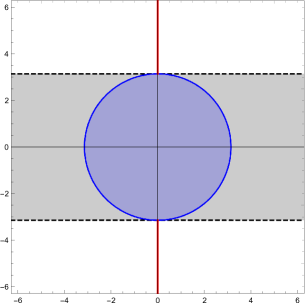

Figure 1: The function is holomorphic in the strip . The convergence domain of the series expansion for is the disc ,

and the closest singularities to are the branch points at .

Next introduce the integral defined as in (24)

for . This can be written equivalently as

(30)

The integrand is a holomorphic function for for each

and is jointly continuous in .

Continuity follows by Lemma 1 which ensures that the argument of the square root never crosses the cut for all .

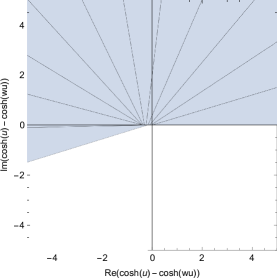

This property is illustrated graphically in Figure 2

which shows the mapping of the half-strip by the function at fixed . As is varied in the image of the half-strip does not cross the real positive axis, which ensures continuity of in .

Figure 2: The mapping of the half-strip

by the function with . Lines of constant are mapped to the radial curves extending from the center outwards.

(ii) The limits of along the axes bordering are continuous with the interior values. Along the real axis this follows from the equality for real positive , and along the imaginary axis from Lemma 1.

Combining (i) and (ii), the Schwarz reflection principle provides the analytic extension of to . This gives the last line in (28).

Enforcing the odd property and applying the Schwarz principle again provides

the remaining continuations to and , and thus to the entire

open strip .

∎

Comments.

By construction, along the real positive axis, reproduces the integral in

(13). In addition, approaches continuously as approaches the real axis from below

(31)

Of course, we more generally have that is both continuous and continuously differentiable

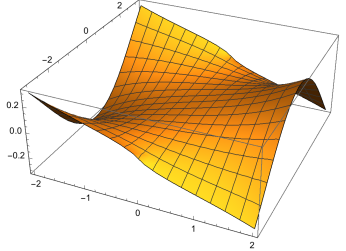

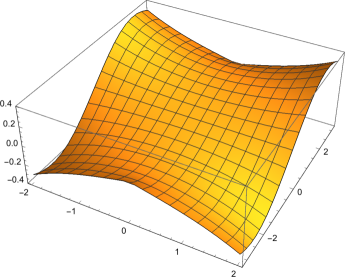

as any axis is crossed in , since is analytic there. Along the negative real axis we have by the odd symmetry in . All of this smoothness is evident in Fig. 3, which shows plots of both the real

and imaginary parts of in a rectangle.

Figure 3: Plots of (left) and (right) for ,

with in the ranges .

4.1 The power series

By Theorem 2, the function can be expanded in a power series around which is convergent for .

As advertised, the series contains only odd powers

(32)

The first few terms are

(33)

4.2 Singularity structure

The function has logarithmic

singularities on the imaginary axis of the form

(34)

In order to study this singularity, take along the imaginary

axis with . Denoting the integration variable and neglecting the factor which is regular as , the integral is approximated as

(35)

The convergence domain of the Taylor series of around is restricted by this singularity to the open disk . See Fig. 1.

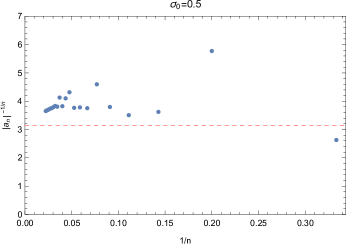

The root test – see Fig. 4 – confirms convergence of the series expansion

for with a convergence radius .

Figure 4: Root test for the convergence of the series expansion (32)

for , showing the reduced coefficients vs .

The horizontal line is at .

.

Application of “transfer results” in Flajolet and Sedgewick (see equation (26) in Ch.VI.2 of [3]) gives the leading large- order asymptotics of the coefficients in the series expansion (32)

It’s worth revisiting the non-convergence argument with the improved knowledge from (36).

Now, the large- asymptotics of the coefficients have the form

(38)

Again the root test shows that the -series for the ATM option price has zero radius of convergence.

4.4 Non-convergence of the short-maturity expansion of the implied volatility function

This is our title result. Consider the expansion for the implied volatility . This is related to the ATM option price as

(39)

We prove that a finite convergence radius of the series for the implied variance implies a finite convergence radius of the option price

. Since the latter series is non-convergent we conclude that the previous series must be non-convergent.

The proof proceeds in two steps.

Step 1. First we observe that the function is entire. This follows from the application of the root test for convergence to its Taylor expansion

. The root test gives that the convergence radius of this series expansion is infinite, which proves that is entire.

Step 2.

Suppose is an analytic function with finite convergence radius and denote the radius of the largest disk centered on which is mapped by to a region which does not include the origin.

Then has the convergence radius . This follows from writing as the composition of with . The analyticity domain of is limited either by the analyticity domain of , or by the branch cut of starting at the point where , and is thus the same as the disk .

From the non-convergence of the series for , it follows that the series for also has zero convergence radius.

5 Numerical illustrations and error estimates

The asymptotic nature of the -expansion of option prices and implied volatility for the SABR model requires a careful application for practical use.

The -series (37) for the value function must be truncated to some finite order . Two issues must be addressed in relation to the use of asymptotic series: i) what is the optimal truncation order , and ii) estimate the best attainable error of the series ,

where is the truncation error.

We illustrate these issues on the example of the value function defined by taking . This situation corresponds to the small volatility regime , when the factor is well approximated by a constant for

.

For this case the integral in (13) can be evaluated exactly as

(40)

where is the elliptic integral of the first kind.

The value function is defined by (14) with the replacement

.

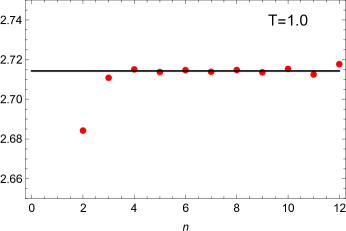

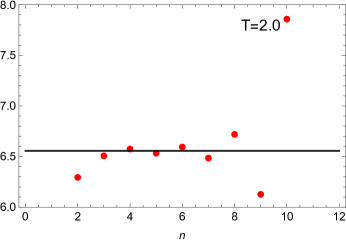

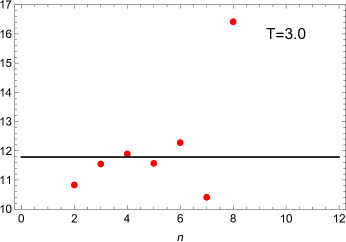

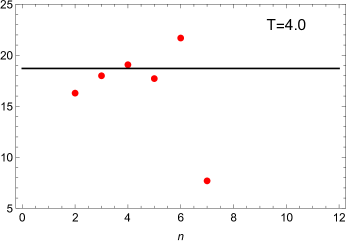

Figure 5 shows the numerical evaluation of from the series expansion (37) truncated to order , plotted as a function of , compared with numerical evaluation of using the exact result (40) for the integrand. The different plots correspond to several values of the parameter.

Figure 5: Dots: The partial sum of from the series expansion (37) keeping terms up to , vs .

Horizontal black line: numerical evaluation of .

We note from these plots that the truncated series agrees best with the numerical evaluation at that order where the last neglected term reaches a minimum. This agrees with the typical behavior of asymptotic series [2]. The optimal truncation order can be estimated from the large-order asymptotics (38) of the coefficients as

.

decreases as increases, and approaches unity for

.

These arguments show that the asymptotic series has a maximum range of validity and breaks down for too large .

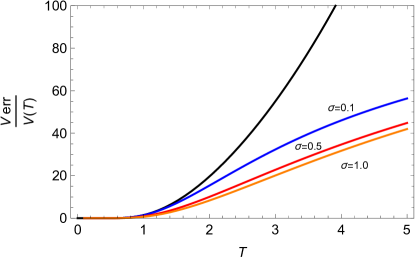

An upper bound on the optimal truncation error of the series can be obtained from a bound on the contribution to the integral (14) from the region .

Denoting

(41)

we have

(42)

with the CDF of the standard normal distribution.

Figure 6: The best attainable error (in percent), measured by the ratio of the contribution to from the region where the series is not convergent to the complete integral. The relative error increases with maturity , and decreases with . The black curve corresponds to

) and the colored curves correspond to .

Proof.

The error bound (42) follows from an upper bound on :

for any , we have

(43)

It is sufficient to prove this bound for defined by setting in the

definition (13), since we have .

The argument of the square root in the denominator is a concave function of and thus is bounded from below as

. This gives the upper bound

The bound (43) can be used to obtain an upper bound on the truncation error but the analytical result is lengthy. The simpler result (42)

is obtained from a weaker bound .

∎

The bound (42) shows that the optimal truncation error is

exponentially suppressed as for .

For the error may be still small, but the

bound (42) is not strong enough to guarantee it.

Numerical simulations

suggest that this error bound overestimates the actual error for larger .

Numerical evaluations of the error term in Fig. 6

confirm that the relative error is negligibly small for and increases rapidly

with . We also note that the error decreases with . This effect is due to the factor which is fast oscillating at a rate which increases with . For very large the oscillations have an effect of suppressing the contribution from the integration region , and thus decreases the error of the asymptotic series.

6 The large scaling limit

In the large volatility limit the function approaches a simple form

.

This follows from the limit in distribution sense

.

Here is defined by , with some test function defined on the positive axis. Taking into the definition (13), the integral is trivially evaluated with the result shown.

Taking in (12) gives . (The exchange of limit and integration is justified by the Lebesgue dominated convergence theorem, using that is bounded from above as shown in (43).)

What is the approach to this limit? The answer to this question is related to the

asymptotics of the ATM implied volatility .

This asymptotics takes a simple form when considered at fixed product .

Expressed in terms of , the Black-Scholes formula gives

The large asymptotics of the implied volatility function turns out to depend only on , and has a calculable form, given by the following result.

Proposition 1.

We have the limit

(46)

with

(47)

where is the solution of

(48)

Proof.

See the Appendix.

∎

The result (47) reproduces the asymptotic implied volatility in the

SABR model in the uncorrelated limit from [15].

We show next that the convergence properties of the series expansion of are better behaved than expected from the non-convergence of the implied volatility .

For simplicity we consider the series expansion of the implied variance

(49)

The convergence properties of this expansion are given by the following result.

Proposition 2.

The series expansion (49)

converges for with and the positive solution of the equation

.

Proof.

The function is the composition of two functions, with defined by the function on the

right-hand side of (47) and the inverse of in (48).

The function has two branch points of order on the imaginary axis at where and is the positive solution of the equation . This result follows from a study of the critical points of . It is known, see e.g. Theorem 3.5.1 in [16], that the inversion of a complex function around a critical point , gives a multivalued function and thus has a branch point at . See also

Theorem VI.6 in Flajolet and Sedgewick [3]. For a similar application to a more complex case see Sec. 2 in [12].

The critical points of are solutions of the equation . This equation has two types of solutions:

i) Solutions on the imaginary axis. They are at with the positive solution of .

These points are mapped to with .

ii) Infinitely many solutions along the real axis at given by the solutions of

with . These solutions are mapped to which are further away from origin than .

In conclusion the dominant singularities of are the two branch points at .

Since is entire, the singularities of

are the two branch points at , which thus determine the convergence radius of the series (49).

∎

While we have worked throughout with , under general ,

the expansion is in powers of .

Then Prop. 2 implies a corresponding convergence radius for the -series expansion of the implied variance .

7 Summary and discussion

We studied the nature of the short maturity expansion for option prices and implied volatility in the uncorrelated log-normal SABR model, and showed that in general the expansion diverges for any maturity. This implies that the series expansion is asymptotic, and that its application for numerical evaluation has to consider issues such as optimal truncation order. The optimal truncation error is

exponentially suppressed for sufficiently small maturity .

For these maturities the first few terms of the asymptotic series give generally

a good approximation of the exact result, but for longer maturity numerical approaches are preferable to the series expansion evaluation.

Despite the asymptotic nature of the short maturity expansion in this model, it is surprising that essentially a subset of terms in the short maturity expansion of the implied volatility converges, with a finite convergence radius.

This subset corresponds to the large scaling limit at or more generally to the limit at fixed product , and can be summed in closed form.

Although the analysis focused on the ATM option prices and implied volatility, the methods used are more general and may be used also for the study of the short maturity expansion at fixed strike, or in various regimes of joint small maturity-small log-strike.

Acknowledgements. We thank an anonymous referee for helpful suggestions that improved the presentation of the paper.

Appendix – Large asymptotics

There are two components to the asymptotics for the limit.

First, we have the large asymptotics of .

Proposition 3.

The leading asymptotics of the function is

(50)

where .

Proof.

Use Theorem 6.1 in Chapter 4.6 Laplace’s method for contour integrals in Olver [13]. The leading contribution to the asymptotics

comes from the upper boundary of the integration region in (13).

∎

Second, the asymptotics (50) is translated into an asymptotic result for

the integral

(51)

which determines the price of a covered ATM call as

(52)

Substituting the leading approximation (50), the integral (51) can be written equivalently as

where we denoted

(54)

The two integrals can be evaluated using the saddle point method.

They are similar so it is sufficient to consider the first integral

(55)

The function has saddle points given by the solutions of the equation

. This equation has solutions on the imaginary axis. The closest saddle point is at where is the positive solution of the equation

. This establishes (48). At this point we have .

The curves of steepest descent (ascent) from the saddle point are solutions of the equation

(56)

This equation is satisfied along the imaginary axis , and along a curve given by

(57)

where is the solution of .

Since , the curve approaches as .

intersects the imaginary axis at the saddle point . See Fig. 7 for an illustration for .

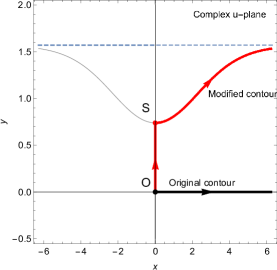

For the application of the saddle point method we deform the contour of integration from the real positive axis such that it passes through the saddle point as shown in Fig. 7 as the red curve.

Along the vertical segment the function increases as and along the curve in the first quadrant, increases further as we move away from the saddle point. We call the latter curve a steepest descent path, and the former a steepest ascent path.

The integration contour can be deformed from the real axis to this path without encountering any singularities of the integrand .

The closest singularities of this function to the origin are branch points at

, which are farther away than the saddle point.

Figure 7: Steepest descent paths for .

The integration contour is deformed from the real axis to the path shown in red. Along the vertical piece of this path the function increases as one approaches , and along the curved portion it increases further as one moves away from the saddle point.

The contribution from the vertical path along the imaginary axis cancels out in the final result. The only contribution appears from the curved path.

The integral is written as a sum of two contributions from the two pieces of the

contour where is the saddle point. The first term is imaginary, and cancels against an identical contribution from . The second integral is dominated by the contribution of the saddle point and is expressed as a Laplace integral by introducing the new integration variable . Since along the contour , the variable is real.

Expanding the integrand as we obtain

(58)

The integral can be evaluated term by term by Watson’s lemma. The leading contribution is

(59)

Collecting all factors gives

(60)

with and

(61)

The same result is obtained for . Adding their contributions reproduces the exponential factor implicitly defined by the arg in (46).

References

[1]

A. Antonov, M. Konikov and M. Spector,

Modern SABR Analytics,

Springer, New York 2019.

[2]

J.P. Boyd,

The Devil’s Invention: Asymptotic, Superasymptotic and Hyperasymptotic Series,

Acta Applicandae Mathematica56 1-98 (1999)

[3]

P. Flajolet and R. Sedgewick,

Analytic Combinatorics,

Cambridge University Press, Cambridge, 2008

[4]

N. de Guillaume, R. Rebonato and A. Pogudin,

The nature of the dependence of the magnitude of rate moves on the level of

rates: A universal relationship,

Quantitative Finance 13, 351-367 (2013)

[5]

P.S. Hagan, D. Kumar, A.S. Lesniewski and D.E. Woodward,

Managing smile risk,

Wilmott Magazine, Sept. 2002.

[6]

P. Henry-Labordére,

Analysis, Geometry and Modeling in Finance: Advanced Methods in Option Pricing,

Chapman and Hall, 2009

[7]

A. Lewis,

Option Valuation under Stochastic Volatility,

Finance Press, Newport 2000

[8]

A. Lewis,

Option Valuation under Stochastic Volatility II,

Finance Press, Newport Beach, 2016

[9]

A. Lewis, unpublished work, using the algorithm described in

[8] (pg. 505).

[10]

E. Lukacs,

Characteristic Functions,

Griffin, Second Edition, 1970

[11]

H. McKean,

An upper bound to the spectrum of on a manifold of negative curvature,

Journal of Differential Geometry 4, 359-366 (1970)

[12]

P. Nándori and D. Pirjol,

On the distribution of the time-integral of the geometric

Brownian motion, 2020.

[13]

F.W.J. Olver,

Asymptotics and Special Functions,

Academic Press 1974.

[14]

L. Paulot,

Asymptotic implied volatility at the second order with application to the SABR model,

arXiv:0906.0658[q-fin.PR]

[15]

D. Pirjol and L. Zhu,

Asymptotics of the time-discretized log-normal SABR model: The implied

volatility surface, arXiv:2001.09850,

Probability in Engineering and Computational Sciences in print,

arXiv:2001.09850[q-fin.MF]

[16]

B. Simon,

A Comprehensive Course in Analysis, II.A Basic Complex Analysis,

American Mathematical Society 2017.

[17]

E. Stein and R. Shakarchi,

Princeton Lectures in Analysis, II Complex Analysis,

Princeton University Press, Princeton 2003