1 Introduction

Divisions of a large firm frequently act as independent profit maximizing agents. In this paper we consider a firm with several production and sales divisions. The firm management can settle internal prices for the produced commodities to coordinate the division activities. The production (resp., sales) division should sell (resp., buy) commodities at these transfer prices, which are valid only within the firm. The aim of such pricing system is to stimulate agent behavior, resulting in the profit maximization of the whole firm. The problem of constructing such pricing policies was formulated in 1950s Hirshleifer1956 . Now the literature on transfer pricing has is quite rich. We refer to the reviews Gox2006 , Baldenius2009 , (Labro2019, , Chap. 13). The most influential papers related to the topic of transfer pricing were recently collected in Eden2019 .

In Schuster2015 three major types of transfer prices are highlighted: market-based, cost-based and negotiated. Among cost based transfer prices the marginal ones are mathematically most natural, since under the convexity assumption they stimulate the firm-optimal solution. However, this pricing method is frequently criticized as follows: to get the transfer price one should find the firm-optimal solution, which is impossible in practice. Moreover, if for some reason such solution is known, then its related components can simply be communicated to each division by the firm manager. So, there is no need in any pricing system.

In the present paper the revenue and cost functions of the divisions are assumed to be unknown. Instead, the firm manager gets the division responses for the transfer prices. So, the transfer pricing is the only way to indirectly access the agent revenue and cost function. Is it possible, using only the agent responses, to find transfer prices stimulating approximately firm-optimal solutions? Roughly speaking, we give an affirmative answer with some quantitative estimates.

Dual gradient descent algorithms, which we utilize for this purpose, are widely used for resource allocation in communication networks Low1999 ; Beck2014 ; Wu2019 ; Rokhlin2021 . In these algorithms the link prices are updated on the basis of user (or processor) reactions to current prices. The firm profit maximization corresponds to the network utility maximization problem, formulated in Kelly1998 . Note, however, that usually the mentioned algorithms need some information concerning the user utilities, like Lipschitz constants or strong convexity parameters. In the present paper we try to avoid using such information (note that the intention of Rokhlin2021 was similar). To this end, we apply the SOLO FTRL algorithm of Orabona, Pál Orabona2018 to the dual problem. The resulting updating rule for the transfer price does not depend on any parameters, and requires no information on the production and cost functions.

The paper is organized as follows. In Section 2 we formally describe the static problem, where the revenue and cost functions of the divisions are unknown but fixed. Under convexity and compactness assumptions we show that the firm-optimal solution is stimulated by some transfer price vector (Theorem 2.1). This is a simple and standard result.

Then, similarly to Beck2014 , we apply Nesterov’s fast gradient descent algorithm to the dual problem and obtain the estimates of order in the number of iterations for optimality and feasibility residuals (Theorem 2.2). After this we apply the mentioned SOLO FTRL algorithm. Its convergence rate is slower: the same residuals are of order (Theorem 2.3), but it uses only the information on division reactions to current prices.

In Section 3 we consider the dynamic problem, where the revenue and cost functions depend on a sequence of i.i.d. random variables. To evaluate the quality of transfer prices we use the average regret: the quantity which is standard in the online learning theory. The main result of the paper (Theorem 3.1) states that the price sequence generated by the SOLO FTRL algorithm ensures no-regret learning with respect to the best possible plan sequence, and the equilibrium between the supply and demand is satisfied on average. It also states that the stochastic bounds of order . Note that the best possible plan sequence is a rather strong comparator.

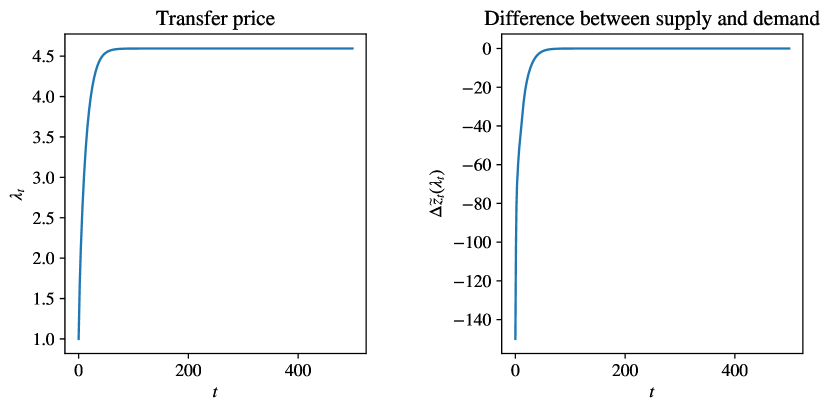

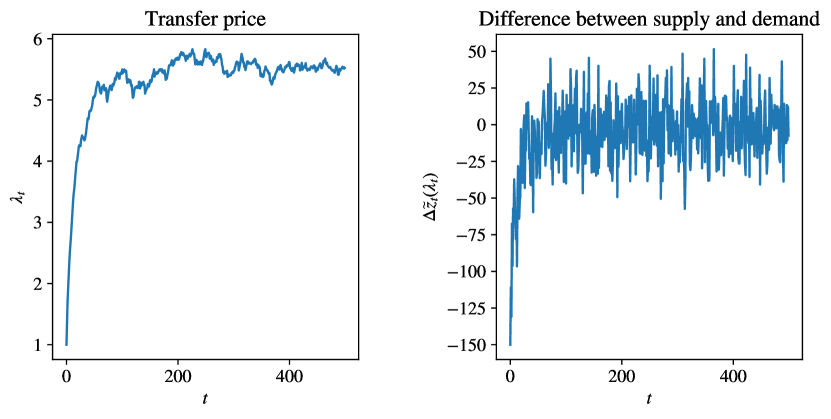

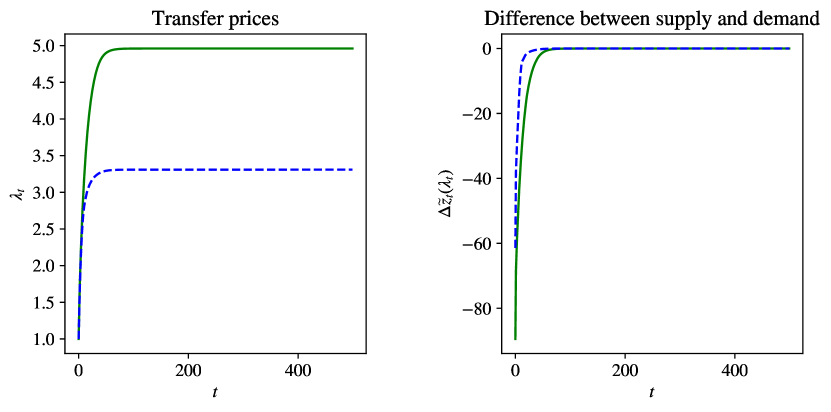

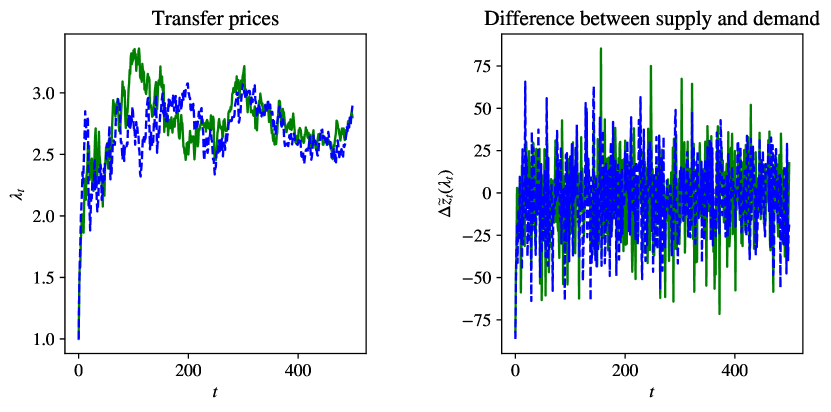

In Section 4 we present two computer experiments with one and two commodities. In the static case the transfer prices and the difference between the supply and demand demonstrate fast stabilization. In the dynamic case the same quantities fluctuate around equilibrium values after a short transition phase.

2 Static problem

Consider a firm consisting from production and sales divisions. There are commodities produced by each production division. The same commodities are sold by each sales division. In this section we consider the static problem where , are the revenue functions of the sales divisions, , are the cost functions of the production divisions, and , are some convex subsets of . A vector describes the amounts of commodities to be sold by -th sales division, and describes the amounts of commodities to be produced by -th production division. Under an unrealistic assumption that the functions , are completely known, the firm manager can solve the profit maximization problem

|

|

|

(1) |

|

|

|

(2) |

and ensure an optimal firm performance by assigning to each division the related component of an optimal solution. The constraint requires that the total production equals to the total sales in each commodity: an equilibrium between the supply and demand at the firm level.

Under convexity assumptions there is also a more economic way to achieve the same goal. The firm can announce the commodity transfer price vector with the obligation to buy the commodities at these prices from the production divisions, and sell them to the sales divisions. Let us introduce the standing assumptions that will be used in the rest of the paper.

Recall that a function , defined on a convex set is called -strongly convex (with some ) if

|

|

|

for all , . By we always denote the usual Euclidean norm.

- Assumption 1.

-

The sets , are convex, compact, and

|

|

|

with some , .

- Assumption 2.

-

The functions (resp., ) are -strongly concave (resp., -strongly convex), non-decreasing in each argument, and .

- Assumption 3.

-

The functions (resp., ) are -Lipschitz (resp., -Lipschitz).

The optimal division (agent) reactions are uniquely defined by

|

|

|

|

(3) |

|

|

|

|

(4) |

where is the usual scalar product. We will say that the plan is stimulated by the transfer price vector . The next elementary result shows that the problem (1), (2) is equivalent to finding a price vector, stimulating an equilibrium.

Theorem 2.1

An admissible point is an optimal solution of the problem (1), (2) if and only if it is stimulated by some transfer price vector : .

Proof

Consider the Lagrange function

|

|

|

(5) |

If , then it is an optimal solution of (1), (2):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(6) |

Conversely, if is an optimal solution of the mentioned problem, then by a version of the Karush-Kuhn-Tucker theorem (Rockafellar1970, , Corollary 28.3.1), there exists a vector such that is a saddle point of the Lagrange function:

|

|

|

From the right inequality, which is similar to (6), it follows that . If has a negative component , then

|

|

|

for the same components , of the vectors , , since the functions , are non-decreasing in each variable. But this contradicts to the equilibrium condition (in commodity ), which should satisfy. Thus, . The proof is complete.

The price vector , mentioned in Theorem 2.1, is an optimal solution of the dual minimization problem

|

|

|

(7) |

where and are Fenchel convex and concave conjugates of and respectively (Barbu2012, , Chap. 2):

|

|

|

The dual problem (7) is solvable and there is no duality gap: (Beck2017, , Theorem A.1).

Is is easy to see that the function is strongly convex on with parameter

|

|

|

(8) |

The Lagrange function (5) is -strongly concave in . Hence, for

|

|

|

we have (see (Beck2017, , Theorem 5.25))

|

|

|

Since , , by putting , we get

|

|

|

(9) |

Furthermore, is -Lipshitz:

|

|

|

|

(10) |

|

|

|

|

(11) |

From (10), (9) it follows that

|

|

|

(12) |

Recall that a function is called -smooth if

|

|

|

From Assumption 2, by Theorem 5.26 of Beck2017 , it follows that the functions are -smooth, and are -smooth. It easily follows that is also smooth with the smoothness parameter

|

|

|

(13) |

Therefore (see (Beck2017, , Theorem 5.8)),

|

|

|

(14) |

Furthermore, since

|

|

|

(15) |

(see (Beck2017, , Corollary 4.21)), we have

|

|

|

Putting , from (14) we get

|

|

|

(16) |

since , .

The inequalities (12), (16) show that the difference controls the optimality gap as well as the feasibility residual of the plan , stimulated by . So, to get an approximately optimal performance, it is enough to approximately solve the dual problem.

Let us consider the gradient descent algorithm with some step sizes :

|

|

|

(17) |

Observing the agent reactions to the transfer price vector , the firm manager can iteratively update according to the law of supply and demand: if , then the supply in -th commodity is greater than the demand and the price decreases, and if , the price goes up.

The are many results concerning the rate of convergence of the gradient descent method, but they require some additional knowledge concerning , and hence the revenue and cost functions of the agents. To get fast convergence rate let us apply Nesterov’s fast gradient descent algorithm Nesterov1983 in the form considered in Su2016 :

|

|

|

|

(18) |

|

|

|

|

(19) |

Note that this algorithm comes from a slightly general family than (17). If then (see Su2016 )

|

|

|

(20) |

From (12), (16), (20) we get the following result.

Theorem 2.2

If , then for the transfer price sequence , generated by the fast gradient descent algorithm (18), (19), we have

|

|

|

|

|

|

|

|

where the constants , , are defined by (8), (11), (13).

To implement the algorithm (18), (19) one needs to know the smoothness parameter of . However, in practice it is unknown. In what follows we show that it is possible to construct a convergent algorithm without any parameter knowledge by sacrificing a large amount of convergence rate. To this end consider the SOLO FTRL (Scale-free Online Linear Optimization Follow The Regularized Leader) algorithm of Orabona2018 :

|

|

|

|

|

|

|

|

(21) |

|

|

|

|

Solving the optimization problem (21), we get

|

|

|

(22) |

Note that if , then is an optimal solution, which is not the case for our problem.

In the online learning theory the quantity

|

|

|

is called the regret of an algorithm, generating , with respect to a fixed decision .

Using the convexity of , we can bound the regret as follows:

|

|

|

This simple and well-known linearization argument reduces any online convex optimization problem to the online linear optimization problem. According to (Orabona2018, , Theorem 1) we have the following bound for the regret of the algorithm (22):

|

|

|

(23) |

Let us estimate :

|

|

|

|

|

|

|

|

(24) |

Here we used (15) and Assumption 1, which allows to estimate the diameter of any set , by . For

|

|

|

(25) |

using the convexity of and the inequalities (23), (24), we get

|

|

|

|

|

|

|

|

(26) |

From the last inequality and (12), (16) we obtain the following result.

Theorem 2.3

For the average transfer price vector (25), generated by the SOLO FTRL algorithm (22), we have

|

|

|

|

|

|

|

|

So, for optimality and feasibility residuals we have the estimates of order instead of the estimates of order of the fast gradient descent algorithm. However the SOLO FTRL algorithm requires no knowledge about the revenue and cost functions, and contains no parameters.

In addition, the following lemma show that the iterations are uniformly bounded. This result will be useful in the next section.

Lemma 1

The iterations (21) satisfy the inequalities

|

|

|

Proof

The inequalities are true for . Assume that they are satisfied for .

(i) Lower bound. Let . Since the functions , are non-decreasing in each argument, from the definitions of , it follows that

|

|

|

Note that and

|

|

|

(27) |

Hence,

If , then from (27) we get

|

|

|

(ii) Upper bound. Let . Without loss of generality assume that . If , then

|

|

|

and we get a contradiction: , since

|

|

|

|

|

|

|

|

Thus, and . Now from (27) it follows that .

If , then again from (27) we get

|

|

|

3 Dynamic problem

Consider a sequence of time dependent revenue and cost functions

|

|

|

and the sequence of profit maximization problems

|

|

|

where is defined by (2). For notational simplicity we assume that , do not depend on . Furthermore, we assume that the Assumptions 1 – 3 are still satisfied for , instead of , , wherein all constants , , , , , are independent of .

As in the static case, put ,

|

|

|

|

|

|

|

|

Applying the SOLO FTRL algorithm (22) to instead of , by (Orabona2018, , Theorem 1) we get the estimate similar to (2):

|

|

|

(28) |

since still satisfies (24)

|

|

|

(29) |

We want to estimate the regret with respect to the best possible plan sequence :

|

|

|

Note, that in (28) is fixed, but optimal solutions of the dual problems

|

|

|

(30) |

|

|

|

depend on . Thus, we cannot apply (12), (16) to pass to the regret, related to the residuals in the primal problem, as in the proof of Theorem 2.3.

Recall that the notation , where are random variables, is a probability measure, and are constants, means that the sequence is stochastically bounded. That is, for any there exists , such that

|

|

|

It is easy to see that Lemma 1 is still holds true for the iterations

|

|

|

(31) |

constructed for time-dependent functions , . By this lemma the sequence is uniformly bounded:

|

|

|

(32) |

Theorem 3.1

Assume additionally that the revenue and cost functions are of the form

|

|

|

where is a sequence of i.i.d. random vectors such that

|

|

|

(33) |

Then the price sequence (31) generated by the SOLO FTRL algorithm, ensures no-regret learning with respect to the best possible plan sequence :

|

|

|

(34) |

and the estimate

|

|

|

(35) |

The equilibrium between the supply and demand is satisfied on average:

|

|

|

(36) |

|

|

|

(37) |

Proof

(1) From the definition (30) of the dual objective functions we get

|

|

|

Since , and is a minimum point of , using the strong duality we obtain the inequality

|

|

|

|

|

|

|

|

|

for any . Take the average:

|

|

|

|

|

|

(38) |

(2) Let us prove the existence of , satisfying the equation

|

|

|

(39) |

From (33) it follows that , since ,

|

|

|

Put

|

|

|

|

|

|

where is the standard basis of . Then

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

It follows that as . Furthermore, since are non-negative:

|

|

|

we can apply Fatou’s lemma to get

|

|

|

This implies the existence of a (global) minimum point of the function . Note that we can take independent of , since are identically distributed, and does not depend on .

As is uniformly bounded, we can interchange the expectation and differentiation (see (Asmussen2007, , Proposition 2.3)):

.

By the optimality criterion we get (39):

|

|

|

(3) Assume that are defined on some probability space . Let be the -algebra generated by , , and put . Then forms the martingale difference sequence with respect to the filtration :

|

|

|

We used the fact that is -measurable, and is independent from . Since, by (29), (32),

|

|

|

the martingale is bounded in . It follows that converges a.s. (Williams1991, , Chap. 12). From the Kronecker lemma (Shiryaev1996, , Chap IV, §3) we get the strong law of large numbers:

|

|

|

(40) |

Consider the inequality (14):

|

|

|

(41) |

Applying the relations (28) and (40), noting that the last one also holds true with instead of , we get

|

|

|

(42) |

We see that the assertion (34) follows from (38), (40), (42), since are uniformly bounded.

The “average equilibrium“ property (36) also follows immediately. We have

|

|

|

The first term conveges to zero a.s. by the mentioned strong law of large numbers. The second term converges to zero a.s. by (42):

|

|

|

(4) To prove (35) we again use (38). Since are uniformly bounded: , for any we have

|

|

|

|

|

|

By the inequalities (41) and (28) the condition

|

|

|

(43) |

implies that

|

|

|

|

|

|

(44) |

for sufficiently large :

|

|

|

Hence,

|

|

|

|

|

|

(45) |

Furthermore, in view of the estimate

|

|

|

we can apply by the Azuma-Hoeffding inequality (see (Lange2010, , Proposition 10.5.1)):

|

|

|

(46) |

Applying this inequality to each term in the right-hand side of (45), we get

|

|

|

|

|

|

|

|

for sufficiently large . This implies (35).

(5) To prove (37) consider the representation

|

|

|

Since are i.i.d. and , from the central limit theorem it follows that

|

|

|

To get the estimate

|

|

|

(47) |

we note that the inequatilty

|

|

|

implies the inequality similar to (43):

|

|

|

Applying the inequalities similar to (44), (46), we get (47). The proof is complete.