Liquidity Provision with Adverse Selection and Inventory Costs

Abstract

We study one-shot Nash competition between an arbitrary number of identical dealers that compete for the order flow of a client. The client trades either because of proprietary information, exposure to idiosyncratic risk, or a mix of both trading motives. When quoting their price schedules, the dealers do not know the client’s type but only its distribution, and in turn choose their price quotes to mitigate between adverse selection and inventory costs. Under essentially minimal conditions, we show that a unique symmetric Nash equilibrium exists and can be characterized by the solution of a nonlinear ODE.

Mathematics Subject Classification: (2010) 91A15, 91B26, 91B54, 49J55

JEL Classification: C61, C72, C78, G14

Keywords: liquidity provision, Nash competition, adverse selection, inventory costs

1 Introduction

Trades in financial markets are typically executed either to profit from superior information or for idiosyncratic “liquidity reasons”, e.g., to offload certain risks by hedging. As succinctly summarized by Treynor (1971), “the essence of market making, viewed as a business, is that in order for the market maker to survive and prosper, his gains from liquidity-motivated transactors must exceed his losses to information motivated transactions.” Designated market makers have mostly been replaced by either centralized limit-order books or OTC markets comprised of discretionary dealers. Nevertheless, this basic tradeoff between exposure to adverse selection through counterparties with superior information and rents earned by servicing liquidity trades remains at the heart of liquidity provision.

The other main risk that liquidity providers are exposed to is “inventory risk”, incurred from “uncertainty about the return on their inventory but also from the uncertainty about when future transactions will occur (which affects how long they must bear return uncertainty)” (Ho and Stoll, 1981).

This paper studies several strategic liquidity providers (“dealers”), who compete for the business of a liquidity-taking “client” by quoting price schedules, which indicate at what prices the dealers stand ready to fill orders of different sizes. As in the seminal works of Biais, Martimort, and Rochet (2000, 2013); Back and Baruch (2013), we assume that clients trade either because they have private information about the payoff of the risky asset, for liquidity reasons (because they are exposed to some idiosyncratic risk), or due to a mix of both trading motives.

When quoting their price schedules, the dealers do not know the clients’ type, but can only mitigate their adverse selection risk based on its distribution. In addition, as in Bielagk, Horst, and Moreno-Bromberg (2019), the dealers also take into account inventory risk through a quadratic cost on their post-trade positions.111The case of zero inventory costs studied in Biais et al. (2000, 2013); Back and Baruch (2013) is natural in markets with very short holding times such as equities or currencies; inventory costs become increasingly important in markets with longer holding times such as (exotic) options. Bielagk et al. (2019) incorporate convex holding costs into a model with a single dealer and a dark pool; we add such inventory costs to a Nash competition between several strategic dealers as in Biais et al. (2000).

In this setting, we show that there is a unique symmetric Nash equilibrium, where the dealers’ optimal price schedules are characterized by a nonlinear ODE. The corresponding equilibrium prices naturally exhibit a bid-ask spread between the best buying and selling prices; as a result, only clients with sufficiently strong trading motives end up engaging with the dealers. Furthermore, we show that convexity of equilibrium price schedules for several competing dealers is endogenous, and does not have to be assumed a priori as in Glosten (1989); Biais et al. (2000, 2013); Back and Baruch (2013). While markets organized as limit-order books do not allow dealers to offer discounts for large quantities, justifying this assumption, we are therefore able to show that such discounts are also not optimal in other dealer-based markets. In contrast, quantity discounts can be optimal for markets dominated by a monopolist dealer.

We establish existence and uniqueness of a symmetric Nash equilibrium under very weak sufficient conditions on the distribution of clients. To wit, we consider general log-concave distributions for the client-type supported on the whole real line. In concrete examples with Gaussian or Exponential distributions, the characteristic ODE can be analyzed directly and optimality can in turn be verified by a direct verification argument (Back and Baruch, 2013). We show that a unique solution of the ODE exists in general, despite the lack of natural boundary conditions, complementing results of Biais et al. (2000, 2013) for type distributions with compact support. Our proof of existence is constructive in that it puts forward explicit upper and lower solutions. Using these as boundary conditions, standard ODE solvers for uniformly Lipschitz equations directly yield very tight upper and lower bounds of the optimal price schedule on any finite interval.

As pointed out by Back and Baruch (2013); Biais et al. (2013), a well-behaved solution of the characteristic ODE (derived from the dealers’ first-order conditions) is generally not sufficient to produce a Nash equilibrium. Instead, for risk-neutral dealers, sufficiently strong adverse selection by informed clients is required to guarantee that the solution of the ODE indeed leads to an equilibrium. We show that the dealers’ inventory costs (relative to the clients’) serve as a partial substitute for this, in that the solution of the ODE leads to an equilibrium if a combination of adverse selection and inventory costs is sufficiently large. Sharp conditions are expressed in terms of the solution of the characteristic ODE; sufficient conditions in terms of primitives of the model can be derived from explicit upper and lower solutions. In the special case of Gaussian client-type distributions and risk-neutral dealers, this recovers the adverse-selection bounds of Back and Baruch (2013).

From a mathematical perspective, the main challenges are that we do not work on compact type intervals as in Biais et al. (2000, 2013), and that we do not make any convexity assumptions, neither for the clients’ problem as in Back and Baruch (2013) nor the dealer’s problem as in Biais et al. (2000). Also, we cannot rely on special properties of the Gaussian distribution as in Back and Baruch (2013).

For the client’s problem, the lack of compactness implies that existence and continuity properties of the optimizer do not follow from Berge’s theorem. Since – unlike the extant literature – we do not assume convexity a priori (but prove it for the oligopolistic case), establishing sufficient and necessary conditions for price schedules to be admissible is rather delicate. As a remedy, we combine the precise structure of the aggregated goal function (which is linear in the type variable of the client) with the a priori -regularity of the goal function in the optimisation variable, and the necessary and sufficient first-order conditions of interior optimizers to gradually derive more and more structure for the optimizer as a function of the type variable.

For the dealers’ problem, the lack of compactness implies that the candidate ODE in the oligopolistic case has no boundary conditions. To obtain existence and to apply numerical schemes, we therefore need to construct explicit upper and lower solutions with appropriate properties. Combining these with a taylor-made Grönwall estimate in turn also allows to prove uniqueness. The lack of convexity for the dealer’s goal functional implies that to verify optimality (both in the monopolistic and the oligopolistic case), we cannot rely on second-order conditions but rather have to work with first-order conditions which are more general but delicate to establish, in particular, since the optimal price schedules exhibit a nontrivial bid-ask spread.

This article is organized as follows. In Section 2, we study the liquidity-taking clients’ problem, taking the price schedules quoted by the dealers as given. With the clients’ optimal demand function at hand, we then turn to the dealers’ problem in Section 3. As a benchmark, we first study in Section 3.1 the (most tractable) case of a single monopolistic dealer. Then, in Section 3.2, we analyze the symmetric Nash competition between an arbitrary number of identical dealers. For better readability, all proofs are collected in the appendices.

2 The Client’s Problem

We consider symmetric dealers who compete for the orders of a client in a Stackelberg-type game: the dealers “lead” by quoting price schedules that describe at what prices they are willing to trade various quantities. The client “follows” by choosing her optimal trade sizes.

As is customary for Stackelberg equilibria, we start by analyzing the optimal response function of the “follower”. In the present context, this means that we first focus on the client and study her optimal trade sizes given the price schedules quoted by the dealers. This analysis needs to be carried out for heterogenous price schedules, even though we focus on identical dealers who quote the same price schedules in equilibrium. The reason is the Nash competition between the dealers that we will analyze in Section 3: for a Nash equilibrium, one needs to verify that unilateral deviations are suboptimal. Accordingly, the response function of the client is required for heterogeneous off-equilibrium price schedules, even if the equilibrium itself is symmetric.

For the client’s problem, the prices quoted by the dealers are fixed. To wit, dealer quotes a price schedule , i.e., a continuous function that satisfies and is twice continuously differentiable on .222This means that prices are a smooth function of trade sizes except for a potential “bid-ask spread” between buying and selling prices. The equilibrium we construct in Section 3 will be of this form. This means that shares of the risky asset can be bought from dealer for units of cash. The client has inventory costs , an initial position in the risky asset, and receives a signal about its payoff :

Here, the mean-zero error term , the signal , and the client’s initial position are independent. The client observes the realizations and of her signal and inventory ; in contrast, the dealers only know the distributions of these random variables. Setting

the client then chooses her trades

to maximize her expected profits penalized for quadratic inventory costs (if the error term is normally distributed as in Biais et al. (2000), then one could equivalently assume that the client maximizes her expected exponential utility):

| (2.1) |

Here, the first term is the expected payoff of the client’s post-trade position, conditional on her information set and . The second term collects the cash payments to the dealers, and the last term describes the inventory cost of the client’s post-trade position.

We make the following standing assumption on the distribution of type variables; the standard example are normal distributions as in, e.g., Glosten (1989), but many other common distributions such as two-sided exponential or gamma distributions also fall into this framework. In the appendix, we prove our results under weaker but less intuitive conditions; these also allow to cover other distributions, e.g., of Pareto type.333Distributions with compact support are studied in Biais et al. (2000) or Cetin and Waelbroeck (2021), for example; discrete types are analyzed by Attar et al. (2019).

Assumption 2.1.

The distributions of the type variables and have positive densities and on that are log-concave, i.e., and are concave functions

While the client’s problem apparently depends on the two type variables and , their impact on the client’s problem can in fact be summarized by a single “effective” type as already observed by Glosten (1989):

Indeed, for each realization , maximizing (2.1) over is equivalent to maximizing the “normalized” goal functional

| (2.2) |

We denote the density of the effective type variable by . Assumption 2.1 implies that is log-concave and continuously differentiable with bounded derivative; see Proposition D.2(a). The corresponding cumulative distribution function and survival function are denoted by

Remark 2.2.

The client’s optimization only depends on her effective type . We nevertheless impose log-concavity on both and , which implies log-concavity of , rather than assuming this directly as in Biais et al. (2000). This provides an intuitive condition in terms of the primitives of the model – as pointed out by Miravete (2002), only assuming log-concavity of either or does not guarantee log-concavity of . Moreover, log-concavity of both signals and inventories already ensures that most other regularity conditions required for the subsequent analysis hold automatically. For example, by Proposition 3.1, log-concavity of the primitives already implies the bounds on the sensitivity of the expected asset payoff conditional on the client’s effective type assumed directly in (Biais et al., 2000, p. 807).

As a minimal requirement for unique symmetric Nash equilibria (with pure strategies), we impose that dealers only quote price schedules for which a symmetric quote gives rise to a unique solution of the clients’ problem (2.2) for all realizations of the type :

Definition 2.3.

A price schedule is admissible (for dealers) if – for every type and given that all dealers quote the price schedule – the client’s goal function

has a unique maximizer .444Note that if and a unique maximizer exists, then it follows from symmetry of the function in that .

The following lemma collects the properties of the client’s optimal trade sizes for identical, admissible price schedules quoted by all dealers.

Lemma 2.4.

Let be an admissible price schedule for dealers and denote by

the set of types for which trading is optimal. Then:

-

(a)

The function is continuous;

-

(b)

There are such that ;

-

(c)

The function is increasing on with and satisfies

Properties (b) and (c) in Lemma 2.4 show that when facing identical admissible price schedules, client types are divided into three categories. To wit, clients optimally sell to the dealers if their type is sufficiently small (i.e., they either receive signals indicating sufficiently unfavorable payoffs, or hold large initial inventories that need to be reduced to limit inventory costs). Conversely, clients with large type purchase risky shares since they expect favorable payoffs or because they start with a negative inventory that they wish to reduce. Clients with an intermediate type in turn prefer not to trade with the dealers. Moreover, Property (c) shows that there is no limit on what the client will buy or sell if their type is sufficiently small or large. Property (a) asserts that the dependence of the trade size on the type is smooth.

With competition between two or more dealers, admissibility in the sense of Definition 2.3 is equivalent to convexity of the price schedules, which is often assumed a priori (Biais et al., 2000, 2013; Back and Baruch, 2013). In contrast, admissible price schedules for a monopolistic dealer need not be strictly convex and can in fact be strictly concave (compare (Biais et al., 2000, Section 4.2)):

Lemma 2.5.

-

(a)

A price schedule is admissible for dealers if and only if it is strictly convex.

-

(b)

A price schedule is admissible for dealer if and only if is strictly convex on and satisfies .

Remark 2.6.

-

(a)

By Lemma 2.5, admissible price schedules for dealers are also admissible for a monopolist. By contrast, admissibility for a monopolist does not necessarily imply admissibility for two or more dealers.

-

(b)

For a monopolist dealer (), admissible price schedule can be concave, and more concave if the client is more inventory averse.

Admissibility of a price schedule in the sense of Definition 2.3 requires that the client’s problem has a unique solution for all types given that all dealers post . This is a natural minimal requirement for symmetric equilibria, but not sufficient to analyse Nash competition between the dealers. Indeed, if one of the dealers unilaterally deviates from a symmetric Nash equilibrium, then the client will face asymmetric price schedules. Whence, her optimization problem is no longer guaranteed to have a (unique) solution even if the price schedules in the equilibrium are admissible. A natural way out is to focus on deviations for which the asymmetric price schedules remain “compatible”, in that the client’s problem still has a solution at least for some type:

Definition 2.7.

Admissible price schedules for dealers are compatible if the client’s (normalized) problem has a solution for some type . (Uniqueness then follows automatically since the strict convexity of the admissible price implies that the client’s goal functional is strictly concave, cf. the proof of Theorem 2.8.)

Note that compatibility of the price schedules (and whence existence for some client types) can fail even if the price schedules are integrals of increasing marginal prices as in Biais et al. (2000), cf. Example A.1.

For not necessarily identical but compatible price schedules, all clients’ problems are still well posed. The next result provides a simple criterion for compatibility in terms of limiting marginal prices and collects the properties of the corresponding optimal trade sizes:

Theorem 2.8.

Let be admissible price schedules for dealers and set

| (2.3) |

Then are compatible if and only if

| (2.4) |

Moreover, in this case, setting , we have the following properties:

-

(a)

For every type , the client’s (normalized) problem has a unique solution ;

-

(b)

For each , the function is continuous, nondecreasing, and increasing on ;

-

(c)

For each , , where if .

As for the symmetric case, Theorem 2.8(b) and (c) show that – for each dealer – clients with sufficiently negative type sell, clients with sufficiently positive type buy, and clients with intermediate types do not trade at all. However, unlike in the symmetric case, each of these three intervals (“buy”, “no-trade” and “sell”) can now be empty for a given dealer. In particular, part (c) shows that there may be a limit on what the client will buy or sell from a given dealer irrespective of their type. Note, however, that compatibility ensures that at least one of the buy, no-trade and sell intervals is nonempty for each dealer, and there exists a at last one dealer where there is no limit on how much the client will buy if their type is large enough (if ) and there is at last one dealer where there is no limit on how much the client will sell if their type is small enough (if ).

3 The Dealers’ Problem

3.1 Monopolistic Case

As a benchmark, we first consider the most tractable case of a single monopolistic dealer, which has been studied by Glosten (1989) for risk-neutral preferences and Gaussian primitives. Generally, the monopolistic dealer chooses an admissible price schedule to maximise expected profits penalized for quadratic inventory costs:555Here, we use the convention that the integral equals minus infinity if its negative part is not integrable.

| (3.1) |

The first term on the right-hand side of (3.1) are the cash payments received from the clients for selling the risky asset. The second term describes the corresponding payoff of the risky assets, and the third is a quadratic cost levied on the post-trade inventory. For example, in the context of exotic options, the inventory cost can be a multiple of the portfolio variance after hedging the option.

As the clients’ optimal response function from Section 2 only depends on their effective type , the relevant statistic for the payoff of the risky asset is its corresponding conditional expectation . For log-concave client types as in Assumption 2.1, this conditional-mean function has the following properties:

Proposition 3.1.

The expected payoff of the risky asset conditional on the clients’ type,

| (3.2) |

is continuously differentiable with for all .

The properties and mean that the agents’ type has some positive correlation with the asset payoff, but is not perfectly informative. This is assumed in (Biais et al., 2000, p. 807) but in fact holds automatically if the densities of both signals and inventories are log concave.

Example 3.2.

Suppose the client’s inventory and signal are both normally distributed with means and and variances and , respectively. Then is also normally distributed with mean and variance . Moreover, the conditional mean is a linear function of the client’s type:

| (3.3) |

Example 3.3.

Linear functions as in Example (3.2) arise more generally if the client’s signal and inventory are both generated using iid copies of the same distribution. To wit, suppose that and , where and all random variables are iid and have the same log-concave distribution. Then, by symmetry, the conditional mean is indeed affine linear in the type:

For log-concave distributions of the client types as in Assumption 2.1, the cumulative distribution functions and survival function of the effective type are log-concave as well (cf. Proposition D.1(a)). In particular, both and are nondecreasing. Denoting by the identity function, this implies via Proposition 3.1 that the functions and are increasing and continuously differentiable with positive derivatives. In particular, their inverses are well defined, increasing and continuously differentiable. They in turn determine the monopolistic dealer’s optimal price schedule in closed form:

Lemma 3.4.

Remark 3.5.

Note that log-concavity of the client types is the only assumption needed for this result. In particular, no parameter constraints are required for Gaussian primitives, for example. If one additionally wants to guarantee that the optimal price schedule is convex (which is natural for a limit-order book, but not necessarily for a market dominated by a monopolist dealer) then additional conditions are needed. To wit, differentiation of (3.4) shows that the optimal price schedule for the monopolist is convex if and only if

| (3.5) | ||||

| (3.6) |

For normally distributed inventories and signals as in Example 3.2, this can be translated into explicit parameter constraints. Suppose for simplicity as in Back and Baruch (2013) that the dealer has no inventory costs (). Then the optimal price schedule for the monopolist is convex if and only if

| (3.7) |

where and denote the cumulative distribution function and the probability density function of the standard normal distribution, respectively, and

In particular if , then and (3.7) specializes to the condition of Back and Baruch (2013):

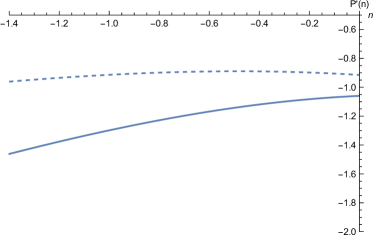

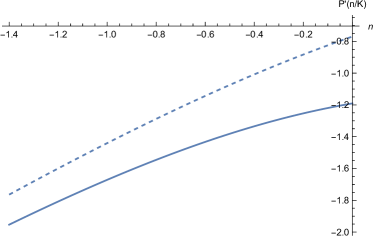

This parameter constraint means that there is sufficient adverse selection to discourage the monopolist from offering quantity discounts for large trades. For inventories with non-zero mean, the second part of the corresponding condition (3.7) has the same interpretation. The first part additionally requires that client inventories are not too large on average. If they are, then large trades are likely enough to come from uninformed traders so that quantity discounts may be optimal. The crossover from convex optimal price schedules (i.e., increasing marginal prices ) to locally concave ones is illustrated in Figure 3.1. If the dealer is sufficiently inventory-averse relative to the client, then (3.5), (3.6) show that this effect disappears.

The right panel in Figure 3.1 displays the dependence of the monopolist’s optimal marginal prices on the corresponding inventory costs. The bid-ask spread is independent of the inventory costs here and (3.4) shows that this in fact holds in general. Whereas monopolist spreads remain invariant, larger inventory costs of the dealer lead to steeper marginal price curves and hence (more) convex price schedules. Differentiation of (3.4) shows that this also holds in general.

3.2 Oligopolistic Case

We now turn to competition between several identical, strategic dealers. To identify a symmetric Nash equilibrium, we suppose without loss of generality that the dealers post the same admissible price schedule and dealer then chooses an admissible price schedule such that is compatible. The common price schedule in turn is a Nash equilibrium if dealer has no incentive to deviate, in that the common price schedule is also optimal for her.

After fixing the price schedules of the other dealers, the goal functional of dealer 1 is

This is of the same form as the goal functional (3.1) of the monopolistic dealer, except that the trade that the client conducts with dealer 1 now depends on the price schedules quoted by all dealers through the clients’ optimal response function from Section 2.

Our first result shows that if a Nash equilibrium exists, then the corresponding marginal prices have to satisfy a nonlinear first-order ODE, derived from the dealers’ first-order conditions for pointwise optimality. Note that unlike for the distributions with compact support considered in Biais et al. (2000, 2013), there are no natural boundary conditions here.

Lemma 3.6.

Suppose Assumption 2.1 is satisfied. If is a Nash equilibrium for dealers, then the corresponding marginal prices satisfy the following ODE:

| (3.8) |

(In particular, it is part of the assertion that the denominators never vanish.)

We next establish existence and uniqueness of a solution to the ODE (3.8). Compared to the monopolistic case from Section 3.1, this requires an additional assumption. To wit, log-concavity of the client types as in Assumption 2.1 guarantees that on by Proposition 3.1. However, for well-posedness of the ODE, we need that this also remains true in the limit .

Assumption 3.7.

The function from (3.2) satisfies .

For normally distributed type variables s in Example 3.2 (or, more generally, if inventories and signals are generated from the same distributions as in Example 3.3), is just a linear function with slope equal to the projection coefficient. Therefore Assumption 3.7 is evidently satisfied in this case.

Theorem 3.8.

Remark 3.9.

Note that uniqueness for (3.8) holds despite the absence of natural boundary conditions. For distributions with compact support, such boundary conditions are derived from a local analysis of the corresponding ODEs near the boundary points by Biais et al. (2000). For distributions with support on the entire real line, monotonicity and finiteness of the solution suffice to guarantee uniqueness: there is only one value of the left and right derivatives at zero for which the solution remains increasing and finite on the entire real line.

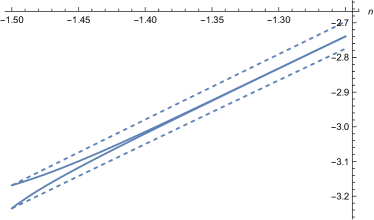

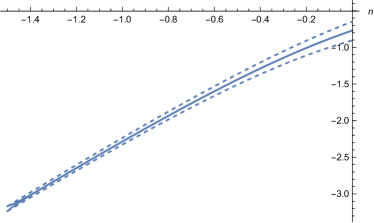

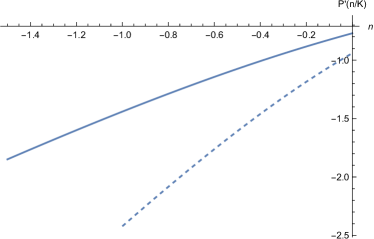

Solving the equation numerically by a grid search for these derivatives is evidently extremely unstable. In contrast, the ODE can be solved in a stable manner (with concrete error bounds) by starting from the upper and lower solutions that we construct for the existence part of the proof of Theorem 3.8, and then solving the equation backwards, cf. Remark B.6. For standard normal primitives, this is illustrated in Figure 3.2, which plots the numerical solutions of the ODE (3.8) starting from the upper and lower solutions. Evidently, the convergence is very fast (as illustrated by the left panel that zooms in near the boundary points). Moreover, the right panel shows that the corresponding values of the solutions at zero (which are required for verifying Assumption 3.10) are indistinguishable.

Lemma 3.6 and Theorem 3.8 show that there is at most one symmetric Nash equilibrium. However, as pointed out by Back and Baruch (2013), existence of a well-behaved solution to the ODE (3.8) is not enough to identify a Nash equilibrium. The reason is that the ODE corresponds to the dealers’ first-order conditions for pointwise optimality, which are not generally sufficient for global optimality here due to the absence of convexity in the dealers’ optimization problems.

As a way out, Biais et al. (2013) impose additional restrictions on the primitives of the model that guarantee this convexity. Conditions of this type rule out standard examples like exponential or normal types, so we instead follow Back and Baruch (2013) in assuming that there is sufficient adverse selection in the market, in that the client’s type has a sufficiently strong relation with the asset payoff. More specifically, our next result shows that if adverse selection and the dealer’s inventory costs (relative to the client’s) are large enough, then the solution to the ODE (3.8) indeed identifies the unique symmetric Nash equilibrium.

Assumption 3.10.

Theorem 3.11.

Assumption 3.10 is analogous to the conditions (3.5)-(3.6) for convexity of the optimal price schedules quoted by a monopolistic dealer. The only difference is the range of marginal prices on which these constraints need to be imposed. In the monopolistic case, these are given by the range of (the inverse of) an explicit function; here they are instead determined by the solution of the ODE (3.8). Using the explicit upper and lower solutions from the existence proof in Theorem 3.8 as boundary values, upper and lower bounds can readily be computed numerically using standard solvers for (uniformly Lipschitz) ODEs.

Alternatively, sufficient conditions in terms of model primitives can be derived directly from upper and lower solutions of the ODE. For standard normal client inventories and signals and risk-neutral dealers, these conditions are satisfied if the projection coefficient from Example 3.2 is bigger than . However, the numerical solution of the corresponding ODEs suggests that (3.5)-(3.6) are in fact already satisfied for for two dealers () and for if the number of dealers is very large.

The bound coincides with the sufficient condition of Back and Baruch (2013), which can be derived by exploiting the specific properties of the normal distribution. To wit, in this case, the competitive price schedule of Glosten (1989) yields a smaller upper solution on and a larger lower solution on for ODE (3.8), that is still known in closed form for normally-distributed types. This in turn provides an explicit sufficient condition for our general condition (3.9)–(3.10). The same argument can also be applied to general non-centered Gaussian types as in Example (3.2):

Remark 3.12.

For normally distributed types as in Example 3.2, suppose that and

| (3.11) |

Here, and denote the cumulative distribution function and the probability density function of the standard normal distribution, respectively, and

Then Assumptions (3.9)–(3.10) are satisfied. In particular, if , then and (3.11) specialises to the sufficient condition of Back and Baruch (2013).666The boundary case can be treated with a limiting argument.

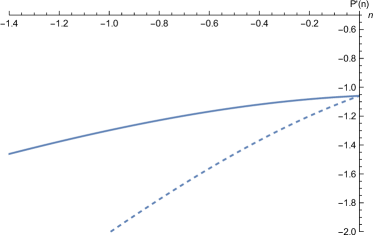

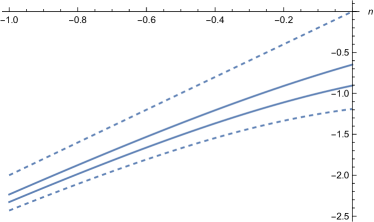

For Gaussian primitives as in Glosten (1989); Back and Baruch (2013), the left panel in Figure 3.3 displays the impact of the dealers’ inventory costs on the optimal price schedules with competition. Unlike in the monopolistic case, bid-ask spreads no longer remain invariant but instead increase with the dealers’ inventory costs.

The right panel of Figure 3.3 compares the monopolistic marginal prices from Lemma 3.4 to the marginal prices of the aggregate price schedule quoted by symmetric oligopolistic dealers, cf. Theorem 3.11. We see that competition between the dealers leads to both tighter bid-ask spreads (as in Ho and Stoll (1981)) and flatter price schedules (i.e., “deeper” markets). Both properties follow directly from the fact that, by the proof of Theorem 3.8, the marginal prices of the monopolist on are a lower solution to the ODE for the marginal prices quoted in the oligopolistic case.

Appendix A Proofs for Section 2

Proof of Lemma 2.4.

Since all dealers quote the same price schedule in the context of this lemma, the client’s goal functional (2.2) simplifies. Indeed, the client’s optimal trade , then is the unique maximizer of the scalar function

| (A.1) |

(a) Fix and let be a sequence in with . For , set . We have to show that . Denote by the set of all accumulation points in of the sequence . As , it suffices to show that .

First, we show that . We only establish the claim for ; the corresponding assertion for follows from a similar argument. Seeking a contradiction, suppose that . Then there exists a subsequence, again denoted by for convenience, such that . By maximality of each for and continuity of ,

Together with maximality of for and the definition of in (A.1), this leads to the desired contradiction:

It remains to show that . Seeking a contradiction, suppose there is . Then there exists a subsequence, again denoted by for convenience, such that . Recall that is the unique maximizer of , is continuous in both variables, and each is maximal for . Whence, we again arrive at a contradiction:

We conclude that the function is continuous as asserted.

(b) To prove this part of the lemma, we only show the following formally weaker claim:

(b’) There are and such that .

We will then use only (b’) to establish (c) and argue in (c) that . Since , we have , where

These sets are both nonempty, because

| (A.2) |

Observe that if , then for all and also for all in a (sufficiently small) neighbourhood of . Set . The previous argument implies that . Similarly, set . Then .

(c) For , we have so that is differentiable in at . Hence, maximality of for implies the following first-order condition (FOC):

| (A.3) |

We now use this to show that for all , there is an open neighbourhood of such that for all ,

| (A.4) |

Fix and set . As is the unique maximum of , there exists an open neighbourhood of such that, for all , we have

| (A.5) |

As is continuous, there exists an open neighbourhood of such that . Now, if with , then (A.3) and the definition of give

Together with (A.5), this implies . Similarly, if with , then . Therefore, (A.4) indeed holds on a suitable neighbourhood of .

We proceed to show that (A.4) together with (b’) and Lemma C.1 implies that is increasing on . First, if , then and the claim follows directly from Lemma C.1. Otherwise, if , Lemma C.1 implies that is increasing on and on . Since is zero on and continuous on , it follows that is negative on and positive on . Hence, is also increasing on .

Finally, we show that and . Recall that is continuous on (cf. (a)), increasing and nonzero on (as shown above) and zero on by definition. Therefore, the limits at in turn yield that , and .

We only spell out the argument for ; the corresponding argument for is similar. Set . As is increasing on and for , it follows that is well defined and valued in . Seeking a contradiction, suppose that . We distinguish two cases. First, assume that . Then for all . In particular for all , by maximality of for and the definition of , we obtain

Hence, it follows that

which contradicts (A.2). Next, assume that . Then there exists such that for all . By the FOC (A.3), we have

As is continuous on , taking limits as yields

This contradicts . In summary, we conclude that as claimed. ∎

Proof of Lemma 2.5.

(a) “”: Suppose is admissible for dealer. To establish strict convexity of , it suffices to show that is increasing on . So fix with . Recall that by the first-order condition (A.3),

and is increasing on by Lemma 2.4(c). As a consequence,

Hence, is increasing on , and is in turn strictly convex. Finally, as by (A.3) for all , Lemma 2.4(c) yields .

Conversely, suppose is strictly convex on with . By (Bertsekas, 1999, Proposition B.22(b)), the function has left and right derivatives for all , denoted by and (which coincide with for ). Moreover, for each fixed , the function is strictly concave on . Hence it has at most one maximum, and by (Bertsekas, 1999, Proposition B.24(f)), is a maximum of if and only if

Here, denotes the subdifferential of at . Concavity of the functions , continuous differentiability of on , and imply that for each . Hence, for each , there exists such that .

(b) “”: Let be an admissible price schedule for dealers. We first show that is convex. To this end, it suffices to check that for all . So fix and set , so that is the unique maximum of the function . As , is twice differentiable in and the second-order necessary optimality condition in turn implies that

(Here, .) Hence, all eigenvalues of are nonnegative. Using the matrix determinant lemma, it is not difficult to verify that the matrix has the eigenvalue with algebraic multiplicity and the eigenvalue with algebraic multiplicity . Whence, for , we have so that is indeed convex.

We proceed to show that the price schedule is even strictly convex. To this end, it suffices to show that is increasing on . Seeking a contradiction, suppose that there are with such that . Since is nondecreasing on by convexity of on , it follows that for all . Set

Then , we have , and is constant on . As a consequence, for all . Let , choose such that , and set . Then

Hence, the function has at least two maximizers, contradicting the admissibility of .

Proof of Theorem 2.8.

First, assume that are compatible. Then there is such that the client’s problem has a solution . Since the price schedules are admissible, they are strictly convex by Theorem 2.5(b). As a consequence, the client’s (normalized) goal function is strictly concave and therefore has only one maximizer. Moreover, is a maximizer of if and only if . Hence, for each , we have

Since is increasing on by strict convexity of , this is equivalent to

As this holds for any , it follows that . This in turn yields (2.4).

Conversely, assume that (2.4) is satisfied. We proceed to show that then (b) and (c) and in turn (a) are satisfied. The latter also implies a fortiori that are compatible.

For , set and denote its inverse function by , with the convention that if Then each is nondecreasing on and increasing on . Hence, the function defined by

is continuous and increasing. Moreover, it satisfies and . To wit, there exists at least one such that and at least one such that . For these indices, we then have and by the definition of and in (2.3). Now, for , define the functions by

Then, in view of the properties of the functions and established above, is continuous, nondecreasing on and increasing on . So we have (c). This in turn implies that

and we have (b). To complete the proof, it now remains to establish (a). Let . We need to establish that is the maximizer of . Uniqueness follows as in the first part of the proof by strict convexity of . By (Bertsekas, 1999, Proposition B.24(f)), it suffices show that . So fix . We first consider the case . Then, the definition of and give

so that . Next, we turn to the case . Then,

The definition of in turn yields that zero is an element of this subdifferential also in the second case,

Here, the set membership follows from the definition of and from (which holds by definition of because ). ∎

Example A.1.

The following price schedules are admissible for dealers, but not compatible:

Indeed, and , so that are not compatible by Theorem 2.8. Analogous counterexamples can be constructed for distributions with compact support, which shows that a compatibility condition for unilateral deviations also needs to be imposed in the setting of Biais et al. (2000).

Lemma A.2.

-

(a)

Let be an admissible price schedule for dealer. Then:

(A.6) -

(b)

Let be admissible price schedules for dealers that are compatible and set . Then for all and ,777Here, we use (as always) the convention that if .

(A.7)

Proof.

(a) Fix . It suffices to consider the case . We only consider the case , the case can be argued similarly. Using that the function is increasing on by Lemma 2.4(a), it follows from the mean value theorem that

| (A.8) |

Now, the lower bound in (A.6) follows from the first inequality in (A.8) together with . Finally, using that for and then rearranging the second inequality in (A.8) gives

Now the upper bound in (A.6) follows from the elementary inequality for .

(b) The argument is very similar to the proof of part (a). The only difference is that we now use that

Appendix B Proofs for Section 3

Proof of Proposition 3.1.

Recall that and , where are independent. Because the error term has mean zero, it follows that . Since , it therefore suffices to show that as well as are continuously differentiable with positive derivatives. This follows from Proposition D.3. ∎

B.1 Proof of Lemma 3.4

In this section, we prove Lemma 3.4 about the monopolistic dealer’s optimal price schedule. We do this under weaker (but substantially less intuitive) assumptions than the convenient sufficient condition imposed in Assumption 2.1.

Assumption B.1.

The expected payoff of the risky asset conditional on the clients’ type, is continuously differentiable and of linear growth.

Assumption B.2.

The probability density function of is positive on and satisfies . Moreover, setting

we have:

-

(i)

is continuously differentiable on with positive derivative and nonnegative on ;

-

(ii)

is continuously differentiable on with positive derivative and nonpositive on .

Remark B.3.

Note that since , Assumption B.2 implies in particular that . It is straightforward to check using Proposition 3.1 that log-concavity as in Assumption 2.1 indeed implies Assumptions B.2 and B.1. When the conditional mean function as well as the probability density and cumulative distribution functions of the client’s type are available, e.g., for Gaussian types, then can be computed in a straightforward manner as the roots of explicit scalar functions.

Proof of Lemma 3.4.

We prove the result under the weaker Assumptions B.1 and B.2. In light of the square-integrability of and the estimate (A.6), for all admissible schedules we have and if and only if . So fix an admissible schedule such that and let and be as in Lemma 2.4(b). Define the function by and set and . Moreover, denote the inverse function of on by , set and note that

| (B.1) |

is increasing by Lemma 2.5(a). Then using Lemma 2.4(c), the substitution rule and an integration by parts in the form of Lemma C.2, the monopolist dealer’s goal functional can be rewritten as follows:

and in turn

| (B.2) | ||||

| (B.3) |

We now establish uniqueness of the optimal price schedule. To this end, suppose that is an optimizer of . We seek a formula for , which in turn yields a formula for via (B.1). To this end, we employ a localised calculus of variation argument on (B.2)–(B.3). We only spell this out for (B.2); the argument for (B.3) is analogous. Let be compact and a continuously differentiable function that is supported on (and hence vanishes on ). Using that is increasing, Lemma C.3(b) shows that there exists such that is increasing on and hence the corresponding price schedule is admissible by Lemma 2.5(a) for all . After plugging into (B.2)–(B.3), dividing by and sending (and using that is zero on ), optimality of yields

Since was arbitrary, the continuity of , , , , in turn gives

Thus, it follows that

Since is increasing, both and are nowhere dense sets by Lemma C.3(a). By continuity of , , , and , this implies that

| (B.4) | ||||

| (B.5) |

Rearranging gives (3.4), so if an optimal price schedule exists it has to be of the proposed form.

We now verify that this price schedule is indeed optimal. To this end, note that (B.4) together with positivity of and Assumption B.2 on imply for fixed that

| (B.6) |

Similarly, (B.5) together with positivity of and Assumption B.2 on imply for fixed that

| (B.7) |

Now, let be as above and be any competitor price schedule such that . Then the mean value theorem together with (B.6) and (B.7) implies that

where for each , lies in the interval with the endpoints and . Whence, is indeed optimal as asserted. ∎

Proof of Remark 3.5.

In order to prove that the optimal price schedule for the monopolist is (strictly) convex in the context of Example 3.2 if and only if (3.7) holds, set

Since and are increasing on and , (3.5) and (3.6) are equivalent to

| (B.8) |

Define

Then, using the scaling properties of the normal distribution and the symmetry of , it follows that (B.8) is equivalent to

| (B.9) |

As is increasing on , (B.9) is equivalent to

| (B.10) |

Next, the scaling properties of the normal distribution, the symmetry of and the definition of and show that and are the unique solutions of

Again using that is increasing on , it follows that is the unique solution of

| (B.11) |

If , then it follows that , whence (B.10) cannot be satisfied as . Conversely, if , then it follows that .

B.2 Proofs for Section 3.2

We now turn to the proofs for the Nash competition between several strategic dealers.

Proof of Lemma 3.6.

We prove this result under the weaker Assumptions B.1 and B.2. Let be a Nash-equilibrium and and be defined as in (2.3). Let be an admissible price schedule for dealers that satisfies

| (B.13) |

Set . Then and defined in (2.4) satisfy and . By Theorem 2.8, this implies that are compatible. In light of the square-integrability of and the estimate (A.7), is always less than and it is greater then if and only if . So assume in addition that is such that . To ease notation, set

Denote the inverse function of on by and note that (with the convention if ),

is increasing and valued in by Theorem 2.8(b) and (c). Now setting and , a change of variable together with an integration by parts in the form of Lemma C.2 allows to rewrite the goal functional of dealer as

| (B.14) | ||||

| (B.15) |

Since is a Nash equilibrium, is a maximizer of . In particular, it is a maximizer among all admissible price schedules that satisfy (B.13). Now using a localised calculus of variations argument separately on (B.14) and (B.15) as in the proof of Lemma 3.4 and noting that the perturbed strategies still satisfy (B.13), we obtain that

and

Rearranging terms gives

| (B.16) | ||||

| (B.17) |

Note that the rearrangement also shows that the numerator and denominator on the right hand sides of (B.16) and (B.17) cannot be zero on and , respectively. Since is increasing by strict convexity of , both and are nowhere dense sets by Lemma C.3(a). By continuity of , , and on , this implies that

| (B.18) | ||||

| (B.19) |

This argument also shows that the denominators on the right hand sides of (B.18) and (B.19) cannot be zero on or , respectively. Indeed, if we multiply (B.16) and (B.17) by the corresponding denominators, we get equations between two continuous functions that hold outside a nowhere dense set, hence everywhere. But this implies that if the denominator in (B.18) and (B.19) can be zero only if the numerator is. But the denominator never vanishes if the corresponding numerator does because and are positive on . ∎

Next, we establish the wellposedness results for the nonlinear ODE (3.8) collected in Theorem 3.8. Again, we do this under weaker (but much less intuitive) assumptions than the convenient sufficient conditions imposed in Assumptions 2.1 and 3.7.

Assumption B.4.

Suppose , are continuously differentiable and there exist such that:

| (B.20) | ||||

| (B.21) | ||||

| (B.22) |

Assumption B.5.

Suppose that and are continuously differentiable and there are and with

| (B.23) |

such that, moreover,

| (B.24) |

Note that Assumptions 2.1 and 3.7 from the body of the paper indeed imply Assumptions B.4 and B.5. To wit, Proposition 3.1 gives (B.20) and (B.21) and (B.22) follows from Proposition D.2(a) and the fact that, fo rlo-concave distributions as in Assumptions 2.1, for all sufficiently small and for all sufficiently large by Proposition D.1(c). Finally, setting , (B.24) follows from Proposition D.1(b) and an integration by parts. However, the above conditions are more general and cover, e.g., two-sided Pareto distributions with sufficiently light tails if the conditional-mean function is linear as in Example LABEL:??.

Proof of Theorem 3.8.

We prove the result under the weaker Assumptions B.4 and B.5. Moreover, we also prove the following two additional claims – part (a) is useful for the analysis of concrete examples and part (b) will be crucial for proving Theorem 3.11.

-

(a)

For any such that

(B.25) (B.26) we have and

(B.27) (B.28) -

(b)

The unique solution to the ODE (3.8) has derivatives that are bounded and bounded away from zero, which implies that and .

The proof is based on constructing explicit upper and lower solutions of the ODE (3.8), and in turn use these to deduce the existence of a solution. The natural candidates for these upper and lower solutions are the functions that make the numerator and denominator in the fractions of the right-hand side of (3.8) vanish.888On , the function corresponding to the numerator is the upper solution and the function corresponding to the denominator is the lower solution; on , the function corresponding to the numerator is the lower solution and the function corresponding to the denominator is the upper solution. Of course, the function that makes the denominator vanish cannot really be used (since it would lead to an infinite derivative) so that another approximation argument is required. Uniqueness follows by a rather delicate Grönwall estimate showing that if there were two solutions between the constructed upper and lower solutions, then the difference between them would grow so fast that at least one of them would cross the upper or lower solution, which is a contradiction.

To ease notation, define the functions by

and set

Then, the ODE (3.8) can be rewritten as

| (B.29) |

Note that

| (B.30) |

This implies that can only be nonnegative if is nonnegative and can only be nonnegative if is negative. Hence, if is increasing, continuously differentiable and satisfies (B.29) (in particular, the denominators do not vanish), then

| (B.31) | ||||

| (B.32) |

Next, if a nondecreasing function satisfies (B.31) and a nondecreasing function satisfies (B.32), then by the fact that is decreasing in by (B.20), it follows that

Thus, the result follows if we can can show that the ODE (B.29) has a unique solution on whose derivatives are bounded and bounded away from zero, and a unique solution on whose derivatives are bounded and bounded away from zero. Then,

| (B.33) |

as well as and .

We only establish the assertion for , the assertion for follows in a similar manner.

We first establish existence of a solution to (B.29) on that has derivatives that are bounded and bounded away from zero. The idea is to construct lower and upper solutions as in Proposition C.4. Given that the right-hand side of the ODE (B.29) on is a (multiple of) the fraction with numerator and denominator , it is natural to consider functions such that and . So define the functions by

| (B.34) | ||||

| (B.35) |

Note that because by the fact that . Moreover, it follows from (B.20) and (B.21) that and have bounded derivatives:

| (B.36) | ||||

| (B.37) |

By definition of , and (B.30), it follows that and as well as and . Together with (B.34) and (B.35), this implies that is an upper solution of the ODE (B.29) on and is essentially a lower solution of the ODE – note that is not defined but can be interpreted as .999Indeed, one can show that . For this reason, we have to modify to get a proper lower solution and it will be useful to also modify to get some sharper estimates. (These refined upper and lower solutions are compared to and in Figure B.1 below.)

To this end, we first establish some estimates on the derivatives of and with respect to . Fix and let . Then by (B.20) and (B.21),101010Note that since is increasing, .

| (B.38) | ||||

| (B.39) |

Together with the fact that and , this gives

| (B.40) | ||||

| (B.41) |

We proceed to construct a solution that lies strictly between and . To this end, for (to be chosen sufficiently small later on) define the functions by

| (B.42) | ||||

| (B.43) |

Then for all with . Moreover, for each , and . Together with (B.36)–(B.37) and (B.40)–(B.41), this gives

| (B.44) | ||||

| (B.45) |

Now, if we choose such that the right-hand side of (B.44) is nonpositive and such that the right-hand side of (B.45) is nonnegative, then we automatically have so that and Proposition C.4 in turn shows that there exists a solution to the ODE (3.8) on with . In particular, we also have the additional Property (a). For normally distributed primitives, Figure B.1 illustrates how the refined upper and lower solutions , improve the bounds that can be gleaned from , .

Moreover, Property (b) follows from (B.29) and (B.40)–(B.41) via

Finally, we establish uniqueness of a solution to (3.8) that satisfies (B.31). It follows from (B.23) that for ,

| (B.46) | ||||

| (B.47) |

Seeking a contradiction, suppose there are two solutions to (3.8) that satisfy (B.31). By local uniqueness (the right-hand side of (3.8) is local Lipschitz-continuous whenever it is well defined), it follows that and are ordered everywhere. Hence, we may assume without loss of generality that , where the last inequality follows from (B.31). Set . Using the growth conditions of and in (B.23) and (B.24), we aim to show that then for sufficiently small, which yields a contradiction. Using that is decreasing in by (B.38) and is increasing in by (B.39), it follows from (B.47) and (B.30) (recalling that ) that for, ,

Using (B.46) and Grönwall’s lemma, we obtain

We arrive at the contradiction for sufficiently small, if we can show that

| (B.48) |

To this end, note that by the fact that by (B.37), de l’Hôpital, (B.36) and (B.37),

Moreover, by (B.24) and the fact that , we obtain

Combining these two limits gives (B.48) and thereby completes the proof. ∎

Remark B.6.

The upper and lower solutions constructed in the proof of Theorem 3.8] can be used to solve the ODE 3.8 numerically as follows:

- (a)

- (b)

-

(c)

Starting from these upper and lower bounds at some negative and positive values and , solve the 3.8 on and with a standard ODE solver for uniformly Lipschitz ODEs. This in turn leads to upper and lower bounds for the exact solution, as depicted in Figure 3.2. Already for moderate values of , , these upper and lower solutions converge very quickly. They therefore provide extremely accurate bounds for the exact solution and, in particular, its value at and that are crucial for the application of the Verification Theorem 3.11.

Finally, we prove the Verification Theorem 3.11, which ensures that solution to the ODE (3.8) indeed identifies a Nash equilibrium.

Proof of Theorem 3.11.

We prove the result under the weaker Assumptions B.2, B.4, B.5 and 3.10. The idea of the proof is to show by a direct argument that given the candidate price schedule for dealers , any deviation for dealer from the candidate is suboptimal, i.e., . To this end, we write for a suitable function and establish the pointwise optimality

Given the bid-ask spread at zero, this is rather delicate. A similar sufficient optimality condition also appears in (Back and Baruch, 2013, Equation (10)), but is only verified in a number of concrete examples, e.g. normally-distributed client types.

Let be an admissible price schedule for dealers and set

| (B.49) |

Since and by the proof of Theorem 3.8, and from (2.4) satisfy and . Hence, is automatically compatible with by Theorem 2.8. Set and

Now setting and , the same calculations as in (B.15) give

| (B.50) |

where are given by

| (B.51) | ||||

| (B.52) |

To establish optimality of , it suffices to establish pointwise optimality, that is,

| (B.53) | ||||

| (B.54) |

We only establish (B.53); (B.54) follows by a similar argument.

We first derive some preliminary estimates on derivatives of the function . To this end, define the functions by111111In view of the proof of Theorem 3.8, this is a slight abuse of notation. But this is justified as coincides with from Theorem 3.8 for , and the same is true for and .

It follows from (B.20), (3.9) and (3.10) that

| (B.55) | ||||

| (B.56) | ||||

| (B.57) |

Also note that

| (B.58) |

The above implies that

| (B.59) |

Indeed, the equality in (B.59) follows from the fact that . For the inequality in (B.59), recall that by Theorem 3.8. We distinguish two cases: First, if , (B.56) and positivity of on give

Next, if , there is with . Then by positivity of on , , and for the inequality follows as in the first case.

The importance of becomes clear when we note that the ODE (3.8) can be written as

| (B.60) |

and by the definition of in (B.51),

| (B.61) | ||||

| (B.62) |

After these preparations fix and set and . We shall distinguish the two cases and . For the latter, we have to consider the subcases , and . This is due due to the fact that price schedules are discontinuous at zero.

Case 1. Let . Then . By (B.55) and (B.56), we obtain for

Combining this with the ODE (B.60) for , we obtain

We conclude that

Case 2(a). Let . Then , and a similar argument as in Case 1 gives

and hence

| (B.63) |

Proof of Remark 3.12.

Using the notation of Example 3.2, define by

Set and . We proceed to show that under condition (3.11),

| and | (B.65) | ||||||

| and | (B.66) |

We only establish the first parts of (B.65) and (B.66). The proof for the second parts are analogous. Set . Then the scaling properties and the symmetry of the normal distribution imply that the first parts of (B.65) and (B.66) are equivalent to

| (B.67) | ||||

| (B.68) |

Since and on , (B.67) is automatically satisfied, and since is increasing on , (B.68) is equivalent to

| (B.69) |

To establish (B.69), note that the second part of (3.11) together with the fact that by the first part of (3.11) and the definition of yield

Hence, by the definition of . Next, using that by definition of and using that gives

and we have (B.69). Next, define the function by

| (B.70) |

Then is continuously differentiable and nondecreasing by (B.65). Moreover, it satisfies the ODE

| (B.71) |

We only establish (B.71) on . To this end, fix and set . Using the definition of , the identity , the formula and the identity , we obtain

Finally, since is nondecreasing and satisfies the ODE (B.71), it follows that

Hence, on , is an upper solution to the ODE (B.71), and on , it is a lower solution. Thus, on , we can replace the upper solution in the proof of Theorem 3.8 by the smaller and whence tighter upper solution and conclude that on . In particular, we have . A similar argument on gives on and . Together with (B.66), this establishes (3.9)–(3.10). ∎

Appendix C Auxiliary Calculus Results

For lack of easy references, this appendix collects a number of calculus results that are used in the proofs.

Lemma C.1.

Let and . Suppose that each has an open neighbourhood such that, for all ,

| (C.1) |

Then is increasing on .

Proof.

Seeking a contradiction, suppose there are with and . Set and . Let be an open neighbourhood of such that (C.1) is satisfied. By the definition of , there is with such that . Hence . It follows from (C.1) that . Let be such that (C.1) is satisfied for . Then by definition of , there is such that . This yields the desired contradiction and therefore shows is indeed increasing as asserted. ∎

Lemma C.2.

Let be absolutely continuous functions. Suppose that for some nonnegative Borel function and for some locally integrable Borel function . Moreover, suppose there exists a nonnegative and nondecreasing function with such that . Then

Proof.

We may assume without loss of generality that is nondecreasing. Indeed, otherwise write , where and , and use linearity of the integral.

Fix . Integration by parts gives

Moreover, by the assumptions on it follows that

By the assumption on , we may conclude that . Now the claim follows from monotone convergence. ∎

Lemma C.3.

Let and be continuously differentiable. Then:

-

(a)

is increasing if and only if and is nowhere dense.

-

(b)

For each compact set and any continuously differentiable function that is supported on , there is such that is increasing for all .

Proof.

(a) Note that the set is open and is closed in as is continuous. “”: If is increasing it is in particular nondecreasing and hence . Seeking a contradiction, suppose that is not nowhere dense. Then there is an nonempty open set . Then there is such that . It follows from the fundamental theorem of calculus that , and we arrive at a contradiction.

“”: As , it follows that is nondecreasing. Seeking a contradiction, suppose there is such that . As is nondecreasing, this implies that is constant on and hence , whence fails to be nowhere dense and we arrive at a contradiction.

(b) Fix a compact set and any continuously differentiable function that is supported on . Set and . By compactness of , continuity of and and the fact that , it follows that and . Set . Then if ,

It follows that and . Hence is strictly increasing by part (a). ∎

Proposition C.4.

Let or . Let be differentiable functions with and set . Finally let be a continuous function such that the partial derivative is also continuous (up to the boundary). Then the differential equation

| (C.2) |

has global solution on that satisfies if either and

| (C.3) |

or and

| (C.4) |

We call a lower and an upper solution to (C.2)

Appendix D Log-Concave Distributions

In this appendix, we list some well-known and not so well-known facts about log-concave distributions; see An (1998) and Saumard and Wellner (2014) for general overviews on log-concave distributions.

First, we recall some basic properties of log-concave distributions on the real line.

Proposition D.1.

Let be a log-concave probability density function. Denote by and , its cumulative distribution function and survival function, respectively. Then:

-

(a)

both and are log-concave as well;

-

(b)

there exist and such that for all .

-

(c)

admits a right derivative everywhere and there exists such that on and on .

Proof.

Part (a) follows from (An, 1998, Lemma 3). Part (b) is a consequence of (An, 1998, Corollary 1(ii)) and the fact that is also log-concave. Existence of a right-derivative follows from the fact that admits a right derivative everywhere since it is concave. Finally, the existence of is implied by the fact that is (strongly) unimodal by (An, 1998, Proposition 1). ∎

Next, we show that convolutions preserve log-concavity and yield additional regularity.121212Note that both and need to be log-concave: (Biais et al., 2000, Proposition 16) is false; see Miravete (2002) for a counterexample.

Proposition D.2.

Let be log-concave probability density functions and let denote the right derivative of . Moreover, denote by the identity function.

-

(a)

The convolution is again a log-concave probability density function, and continuously differentiable with bounded derivative ;

-

(b)

The convolution is integrable and continuously differentiable with bounded derivative .

Proof.

The first part of (a) follows from (An, 1998, Proposition 4).

For the remainder of (a) and (b), fix as in Proposition D.1(c). The fundamental theorem of calculus yields

| (D.1) |

Since and are bounded Proposition D.1(b), the convolutions and are well-defined, continuous (by dominated convergence) and bounded. Now the result follows from the fundamental theorem of calculus and Fubini’s theorem. ∎

Finally, we derive a refined version of Efron’s theorem (Efron, 1965) on the conditional mean of a log-concave random variable given the sum of this random variable and another independent log-concave random variable.

Proposition D.3.

Let and be independent real-valued random variables with positive log-concave probability density functions and . Set . Then the conditional mean function

is continuously differentiable and satisfies .

Proof.

First, is continuously differentiable since

and both the numerator and denominator are continuously differentiable by Proposition D.2, with derivatives and respectively, where denotes the right derivative of .

To show that , fix . Then Fubini’s theorem gives

| (D.2) |

To complete the proof, it remains to show that the numerator in (D.2) is positive. Using symmetry and averaging over the first and second line for the third line, we obtain

| (D.3) |

By log-concavity of , the function (which is the right derivative of ) is nonincreasing. This implies that is nonpositive for and nonnegative for . Moreover, since is integrable, is not constant. As a consequence,

where for each sufficiently small, the inequality is strict if is sufficiently large (because is nonincreasing and not constant). Since is positive for each , it follows that (D.3) is positive. ∎

References

- An (1998) M. Y. An. Logconcavity versus logconvexity: a complete characterization. Journal of Economic Theory, 80(2):350–369, 1998.

- Attar et al. (2019) A. Attar, T. Mariotti, and F. Salanié. On competitive nonlinear pricing. Theoretical Economics, 14(1):297–343, 2019.

- Back and Baruch (2013) K. Back and S. Baruch. Strategic liquidity provision in limit order markets. Econometrica, 81(1):363–392, 2013.

- Bertsekas (1999) D. Bertsekas. Nonlinear programming. Athena Scientific, Belmont, MA, second edition, 1999.

- Biais et al. (2000) B. Biais, D. Martimort, and J.-C. Rochet. Competing mechanisms in a common value environment. Econometrica, 68(4):799–837, 2000.

- Biais et al. (2013) B. Biais, D. Martimort, and J.-C. Rochet. Corrigendum to “Competing mechanisms in a common value environment”. Econometrica, 81(1):393–406, 2013.

- Bielagk et al. (2019) J. Bielagk, U. Horst, and S. Moreno-Bromberg. Trading under market impact: Crossing networks interacting with dealer markets. Journal of Economic Dynamics and Control, 100:131–151, 2019.

- Cetin and Waelbroeck (2021) U. Cetin and H. Waelbroeck. An equilibrium analysis of price impact and order flow. Preprint, 2021.

- Efron (1965) B. Efron. Increasing properties of Polya frequency functions. Annals of Mathematical Statistics, 36(1):272–279, 1965.

- Glosten (1989) L. R. Glosten. Insider trading, liquidity, and the role of the monopolist specialist. Journal of Business, 62(2):211–235, 1989.

- Ho and Stoll (1981) T. Ho and H. R. Stoll. Optimal dealer pricing under transactions and return uncertainty. Journal of Financial Economics, 9(1):47–73, 1981.

- Miravete (2002) E. J. Miravete. Preserving log-concavity under convolution: Comment. Econometrica, 70(3):1253–1254, 2002.

- Saumard and Wellner (2014) A. Saumard and J. A. Wellner. Log-concavity and strong log-concavity: A review. Statistics Surveys, 8:45, 2014.

- Treynor (1971) J. Treynor. The only game in town. Financial Analysts Journal, 22:12–14, 1971.

- Walter (1998) W. Walter. Ordinary differential equations. Springer, New York, 1998.