Cardinality-constrained structured data-fitting problems

Abstract

A memory-efficient framework is described for the cardinality-constrained structured data-fitting problem. Dual-based atom-identification rules are proposed that reveal the structure of the optimal primal solution from near-optimal dual solutions. These rules allow for a simple and computationally cheap algorithm for translating any feasible dual solution to a primal solution that satisfies the cardinality constraint. Rigorous guarantees are provided for obtaining a near-optimal primal solution given any dual-based method that generates dual iterates converging to an optimal dual solution. Numerical experiments on real-world datasets support confirm the analysis and demonstrate the efficiency of the proposed approach.

keywords:

convex analysis, sparse optimization, low-rank optimization, primal-retrieval1 Introduction

Consider the problem of fitting a model to data by building up model parameters as the superposition of a limited set atomic elements taken from a given dictionary. Versions of this cardinality-constrained problem appear in a number of statistical-learning applications in machine learning [46, 53, 38, 4], data mining, and signal processing [11]. In these applications, common atomic dictionaries include the set of one-hot vectors or matrices (i.e., vectors and matrices that contain only a single element) and rank-1 unit matrices. The elements of the given dictionary encode a notion of parsimony in the definition of the model parameters.

The cardinality-constrained formulation that we consider aims to

| (P) |

where is an -smooth and convex function, is a linear operator with , is the observation vector, and is the atomic dictionary. The cardinality function

| (1) |

measures the complexity of with respect to the atomic set . The loss term measures the quality of the fit. When is the set of signed canonical unit vectors, the function simply counts the number of nonzero elements in . Typically , which indicates that we seek a feasible model parameter that has an efficient representation in terms of atoms from the set .

For the application areas that we target, the two characteristics of this feasibility problem that pose the biggest challenge to efficient implementation are the combinatorial nature of the cardinality constraint, and the high-dimensionality of the parameter space. To address the combinatorial challenge, we follow van den Berg and Friedlander [47, 48] and Chandrasekaran et al. [15], and use the convex gauge function

| (2) |

as a tractable proxy for the cardinality function (1); see section 3. In tandem with the convexity of the loss function, this function allows us to formulate three alternative relaxed convex optimization problems that, under certain conditions, have approximate solutions satisfying the feasibility problem; see problems (P1), (P2), and (P3) in section 4.

The high-dimensionality of the parameter space, however, may imply that it’s inefficient—and maybe even practically impossible—to solve these convex relaxations because it’s infeasible to store directly the approximations to a feasible solution . Instead, we wish to develop methods that leverage the efficient representation that feasible solutions have in terms of the atoms in the dictionary . For example, consider the case in which the dictionary is the set of symmetric rank-one matrices, and is the trace linear operator that maps these matrices into -vectors. Any method that iterates directly on the parameters requires storage for the iterates and the data. An alternative is the widely-used conditional gradient method [22], which requires storage after iterations [31], but also often requires a substantial number of iterations to converge. Instead of storing directly, we apply a dual method to one of the convex relaxations (P1), (P2), and (P3) (defined below); these dual methods typically require only storage, and still allow us to collect information on which atoms in participate in the construction of a feasible . One of the aims of this paper is to describe how to collect and use this information.

1.1 Approach

We propose a unified algorithm-agnostic strategy that uses any sequence of improving dual solutions to one of the convex relaxations. This dual sequence identifies an essential subset of atoms in needed to construct an -infeasible solution that satisfies the conditions

for any positive tolerance . These atomic-identification rules, described in section 5, derive from the polar-alignment property and apply to arbitrary dictionaries [19]. These atom-identification rules generalize earlier approaches described by El Ghaoui [25] and Hare and Lewis [27]. Once an essential subset of atoms is identified, an -feasible solution can be computed by optimizing over all positive linear combinations of this subset. This relatively small -variable problem can often be solved efficiently.

We prove that when the atomic dictionary is polyhedral, we can set to zero and still identify in polynomial time a set of feasible atoms; see Corollary 9. When the atomic dictionary is spectrahedral, we prove that an -feasible set of atoms can be identified also in polynomial time; see Corollary 15.

We demonstrate via numerical experiments on real-world datasets that this approach is effective in practice.

There are three important elements in our primal-retrieval algorithm. The first element is an atom-identifier function that maps , where is any feasible dual variable, to a cone generated by atoms that are essential. These atoms have the property that

The explicit definition of the essential cone depends on the particular atomic set . In section 6, we make it explicit for atomic sets that are polyhedral (section 6.1) and spectral (section 6.2).

The second element is an arbitrary function (such as an appropriate first-order iterative method) that generates dual iterates converging to the optimal dual variable of any of the dual problem (Di). It’s this oracle that generates the dual estiamtes subsequently used by .

The third algorithmic component is the reduced convex optimization problem

| (PR) |

which at each iteration constructs a primal estimate using the atoms identified through the dual estimate . The detailed algorithm is shown in Algorithm 1. Note that our primal-retrieval strategy doesn’t aim to recover the optimal solutions to (P1), (P2) or (P3). These problems serve as a guidance for our atom-identification rule. The final output of Algorithm 1 maybe different from the optimal solutions to (P1), (P2), or (P3).

2 Related work

Many recent approaches for atomic-sparse optimization problems are based on algorithms [20, 17]. These methods, however, still need to retrieve at some point a primal solution , which may require a prohibitive amount of memory for its storage. A widely used heuristic applies the truncated singular value decomposition to obtain low-rank solutions, but this heuristic is unreliable in minimizing the model misfit [19, Algorithm 6.4]. Memory-efficient atomic-sparse optimization thus requires efficient and reliable methods to retrieve an atomic-sparse primal solution.

Dual approaches for nuclear-norm or trace-norm regularized problems are attractive because they enjoy optimal storage, which means that they have space complexity instead of [17]. For example, the bundle method for solving the Lagrangian dual formulation of semi-definite programming [28], and the gauge dual formulation of general atomic sparse optimization problem [20], exhibit promising results in practice.

A related line of research uses memory-efficient primal-based algorithms based on hard-thresholding. Some examples include gradient hard-thresholding [54], periodical hard-thresholding [1], and many proximal-gradient or ADMM-based hard-thresholding algorithms [37, 35, 30]. These approaches are primal-based and tangential to to our purposes. We do not include them in our discussion.

The theoretical analysis of our primal-retrieval approach is related to optimal atom identification [10, 27, 26], and especially to recently developed safe-screening rules for various kind of sparse optimization problems [25, 51, 36, 50, 43, 9, 52, 40, 55, 34, 5, 6]. One of our main results, given by Theorem 5, generalizes the gap safe-screening rule developed by Ndiaye et al. [39] to general atomic-sparse problems and to more general problem formulations. Some of the techniques used in our analysis are related to the facial reduction strategy from Krislock and Wolcowicz [33].

3 Preliminaries

We introduce in this section the main tools of convex analysis used to understand atomic sparsity.

The gauge function (2) is always convex, nonnegative, and positively homogeneous. This function is finite only at points contained within the cone

generated from the elements of the set . The gauge is not necessarily a norm because it may not be symmetric (unless is centrosymmetric), may vanish at points other than the origin, and may not be finite valued (unless contains the origin in the interior of its convex hull). Throughout, we make the blanket assumption that the dictionary is compact, and that the origin is contained in its convex hull. The assumption on the origin ensures that the gauge function is continuous. The compactness assumption isn’t strictly necessary for many of our conclusions, but does considerably simplify the analysis. The set may be nonconvex, which is the case, for example, if it consists of a discrete set of two or more items.

The definition of the gauge function makes explicit this function’s role as a convex penalty for atomic sparsity. The atomic support of a vector to be the collection of atoms that contribute positively to the conic decomposition implied by the value [19, Definition 2.1].

Definition 1 (Atomic support).

A subset of atoms is a support set for with respect to if every atom satisfies

For example, the support set for the atomic set of 1-hot unit vectors coincides with the nonzero elements of with the corresponding sign. The support function to the set is given by . Because is compact, every direction generates a supporting hyperplane to the convex hull of . The atoms contained in that supporting hyperplane are said the be exposed by . The following definition also includes the notion of atoms that are approximately exposed.

Definition 2 (Exposed and -exposed atoms).

The exposed atoms and -exposed atoms, respectively, of a set in the direction are defined by the sets

where is the support function with respect to .

When , the -exposed atoms coincide with the exposed atoms.

We list in Table 1 commonly used atomic sets, their corresponding gauge and support functions, and atomic supports.

| Atomic sparsity | ||||

|---|---|---|---|---|

| non-negative | ||||

| element-wise | ||||

| low rank | singular vectors of | |||

| PSD & low rank | eigenvectors of |

4 Atomic-sparse optimization

We introduce in this section convex relaxations to the structured data-fitting problem (P). In particular, we consider the following three related gauge-regularized optimization problems:

| (P1) | |||

| (P2) | |||

| (P3) |

It’s well known that under mild conditions, these three formulations are equivalent for appropriate choices of the positive parameters , and [23]. Practitioners often prefer one of these formulations depending on their application. For example, tasks related to machine learning, including feature selection and recommender systems, typically feature one of the first two formulations [46, 53, 38]. On the other hand, applications in signal processing and related fields, such as as compressed sensing and phase retrieval, often use the third formulation [47, 11].

Our primal-retrieval strategy relies on the hypothesis that the atomic-sparse optimization problems (P1), (P2) and (P3) are reasonable convex relaxations to the structured data-fitting problem (P), in the sense that the corresponding optimal solutions are feasible for (P). We formalize this in the following assumption.

Assumption 3.

Let denote an optimal solution to (Pi), . Then is feasible for (P), i.e.,

As described in section 1, the Fenchel-Rockafellar duals for these problems have typically smaller space complexity. These dual problems can be formulated as

| (D1) | |||

| (D2) | |||

| (D3) |

where is the convex conjugate function of , and is the adjoint operator of , which satisfies for all and . The derivation of these dual problems can be found in appendix A.

5 Atom identification

We demonstrate in this section how an optimal dual solution can be used to identify essential atoms that participate in the primal solutions. In order to develop atomic-identification rules that apply to arbitrary atomic sets —even those that are uncountably infinite—we require generalized notions of active constraint sets. In linear programming, for example, the simplex multipliers give information about the optimal primal support. By analogy, our atomic-identification rules give information about the essential atoms that participate in the support of the primal optimal solutions. In addition, we extend the identification rules to approximate the essential atoms from approximate dual solutions.

We build on the following result, due to Fan et al. [19, Proposition 4.5 and Theorem 5.1].

Theorem 4 (Atom identification).

Let and be optimal primal-dual solutions for problems (Pi) and (Di), with . Then

| (3) |

The following theorem generalizes this result to show similar atomic support identification properties that also apply to approximate dual solutions. In particular, given a feasible dual variable close to , the support of is contained in the set of -exposed atoms that includes .

Theorem 5 (Generalized atom identification).

Let and be feasible primal and dual vectors, respectively for problems (Pi) and (Di), with . Then

| (4) |

where each is defined for problem by

-

a)

,

-

b)

,

-

c)

,

where and are positive lower and upper bounds, respectively, for , and is the induced atomic operator norm.

Theorem 5 asserts that the underlying atomic support of is contained in the set of the -exposed atoms of . Moreover, when (and, for problem (D3), the bounds and ), each , and thus (4) implies that we have a tighter containment for the optimal atomic support. The proofs for parts (a) and (b) of Theorem 5 depend on the strong convexity of , which is implied by the Lipschitz smoothness of [29, Theorem 4.2.1]. This convenient property, however, is not available for part (c) because the dual objective of (D3) is the perspective map of , which is not strongly convex [2]. We resolve this technical difficulty by instead imposing the additional assumption that bounds are available on the dual optimal variable . Appendix C describes how to obtain these bounds during the course of the level-set method developed by Aravkin et al. [3].

The gap safe-screening rule developed by Ndiaye et al. [40] is a special case of Theorem 5 that applies only to (P1) for the particular case in which is the one-norm. We also note that Theorem 5 states a tighter bound on that relies on the optimal primal value rather than the primal value at an arbitrary primal-feasible point.

6 Primal retrieval

Theorem 5 serves mainly as a technical tool for error bound analysis, in particular because it’s impractical to compute or approximate . However, the inclusions (3) and (4), respectively, of Theorem 4 and 5 motivate us to define an atom-identifier function that depends on the dual variable and satisfies the inclusions

The next two sections demonstrate how to construct such a function for polyhedral and spectral atomic sets, which are two important examples that appear frequently in practice. With this function we can thus implement the primal-recovery problem required by Step 5 of Algorithm 1. Moreover, we show how to use the error bounds of Theorem 5 to analyze the atomic-identification properties of the resulting algorithm.

6.1 Primal-retrieval for polyhedral atomic sets

We formalize in this section a definition for the function for the case in which is a finite set of vectors, which implies that the convex hull is polyhedral. Given a feasible dual vector , consider the top- atoms in with respect to the inner product with the vector :

| (5) |

Note that there may be many sets of atoms that satisfy this property. We then construct the cone of essential atoms as the convex conic hull generated from this set of top- atoms:

Thus, the primal-retrieval computation in step 5 of Algorithm 1 is given by

where

| (6) |

is the -vector of coefficients obtained by minimizing the reduced objective over a -dimensional polyhedron defined by the top-k atoms.

Example 6 (Sparse vector recovery).

We consider the problem of recovering a sparse vector from noisy observations , where is a given measurement matrix and is standard Gaussian noise. For some expected noise level , the sparse recovery problem can be thus be expressed as

which corresponds to (P) with and with the atomic set

| (7) |

where each is the th canonical unit vector. The basis pursuit denoising (BPDN) approach approximates this problem by replacing the cardinality constraint with an optimization problem that minimizes the 1-norm of the solution:

| (8) |

see Chen et al. [16]. This convex relaxation corresponds to problem (P3).

There are many dual methods that generate iterates converging to the optimal dual solution to (8), including the level-set method coupled with the dual conditional-gradient suboracle, as described by [3, 19]. The resulting primal-retrieval strategy for Step 5 of Algorithm 1 can thus be implemented by executing the following steps:

-

1.

(Top- atoms) Find the top indices of the vector with largest absolute value and gather their corresponding signs for . The top- atoms are thus ; see (5).

-

2.

(Retrieve coefficients) Solve the reduced problem (6), where in this case,

This is a nonnegative least-squares problem for which many standard algorithms are available. For example, an accelerated projected gradient descent method requires iterations when has full column rank.

-

3.

(Termination) Step 6 of the Algorithm 1 is implemented simply by verifying that . (As verified by Corollary 9, we may take in this polyhedral case.) Thus, we can terminate the algorithm and return the primal variable

which is the superposition of the top- atoms. Otherwise, the algorithm proceeds to the next iteration.

We describe numerical experiments for the sparse vector recovery problem in section 7.1.

6.1.1 Iteration complexity

In order to guarantee the quality of the recovered solution, we rely on a notion of degeneracy introduced by Nutini et al. [41].

Definition 7.

Let and , respectively, be optimal primal and dual solutions for problems (Pi) and (Di), where is polyhedral. Let be a positive scalar. The problem pair ((Pi), (Di)) is -nondegenerate if for any , either or .

The next proposition guarantees a finite-time atom identification property when the atomic set is polyhedral.

Proposition 8 (Finite-time atom-identification).

For each problem , let be a sequence that converges to an optimal dual solution . If the atomic set is polyhedral and the problem pair ((Pi), (Di)) is -nondegenerate, then there exists such that

It follows that Algorithm 1 will terminate in iterations regardless of the tolerance .

Proposition 8 ensures that the atom-identification property described by Theorem 5 is guaranteed to discard superfluous atoms in a finite number of iterations as long as we have available an iterative solver that generates dual iterates converging to a solution. Thus, Algorithm 1 is guaranteed to generate a feasible solution to (P). The following corollary characterizes a bound on in terms of the convergence rate of the dual method.

Corollary 9.

For each problem , suppose the dual oracle generates iterates converging to optimal variable with rate

for some . If the atomic set is polyhedral and the problem pair ((Pi), (Di)) is -nondegenerate, then Algorithm 1 with terminates in iterations.

6.1.2 Centrosymmetry and unconstrained primal recovery

Further computational savings are possible when the atomic set is centrosymmetric, i.e.,

| (9) |

Centrosymmetry is a common property, and perhaps the prototypical example is the set of signed canonical unit vectors given by the set (7). Whenever centrosymmetry holds, . This motivates us to replace the function with the function

where is the collection of top- atoms defined by 5. Thus, the primal-retrieval optimization problem (6) reduces to the unconstrained version

The following corollary simply asserts that the complexity results described in section 6.1.1 continue to hold for centrosymmetric atomic sets when using the essential span function.

Corollary 10 (Atom identification under centrosymmetry).

If the atomic set is centrosymmetric and polyhedral, then Proposition 8 and Corollary 9 hold with replaced by .

6.2 Primal-retrieval for spectral atomic sets

We formalize in this section a definition for the function for the case in which is a collection of rank-1 matrices, either asymmetric or symmetric, respectively:

| (10) | ||||

| (11) |

We mainly focus on the former atomic set of asymmetric matrices because all of our theoretical results easily specialize to the symmetric case. Note that this atomic set is centrosymmetric (cf. 9), and as we’ll see below, the recovery problem is unconstrained. Later in section 6.2.2 we’ll describe the recovery problem for the atomic set of symmetric matrices, which is in fact a non-centrosymmetric set.

For this section only, we work with the linear operator , and replace the vector of observations with the -by- matrix . In this context, the dual variables for one of the corresponding dual problems is a matrix of the same dimension.

Fix a feasible dual variable and define the singular value decomposition (SVD) for its product with the adjoint of by

| (12) |

where is the diagonal matrix consisting of top- singular values of , the matrices and contain the corresponding left and right singular vectors, and the matrices , , and contain the remaining singular vectors and values. Then the reduced atomic set by and can be expressed as

We construct the cone of essential atoms as the convex cone generated from the reduced atomic set , i.e.,

| (13) |

Thus, the primal-retrieval computation in Step 5 of Algorithm 1 is then given by

| (14) |

where

| (15) |

is a matrix obtained by solving the reduced problem (PR), which is defined over the cone generated by the essential atoms identified through the top- singular triples of , desribed by (13).

Example 11 (Low-rank matrix completion).

The low-rank matrix completion (LRMC) problem aims to recover a low-rank matrix from partial observations, which arises in many real applications such as recommender systems [44] and in a convex formulation of the phase retrieval problem [14]. The LRMC problem can be expressed as

| (16) |

where is the set of observations over the index set . Problem (16) corresponds to (P) with the objective , the atomic set given by (10), and the linear operator defined by the mask

Fazel [21] popularized the convex relaxation of (16) that minimizes the sum of singular values of :

| (17) |

This problem corresponds to formulation (P3). As with Example 6, there are many dual methods that can generate dual feasible iterates converging to the dual solution of (17), such as a dual bundle method [20]. The resulting primal-retrieval strategy for Step 5 of Algorithm 1 can be implemented by executing the following steps:

-

1.

(Top- atoms) Compute the leading singular vectors of the matrix , given by and as defined by the SVD 12.

-

2.

(Retrieve coefficients) Solve the reduced problem (15), where in this case,

This least squares problem can be solved to within -accuracy in iterations, for example, with the FISTA algorithm [7]. Typically, , and so we expect that this reduced problem is significantly cheaper to solve than the original problem (17).

-

3.

(Termination) Step 6 of Algorithm 1 terminates when the value of the reduced objective satisifes the condition , where is some pre-defined tolerance. In that case, the algorithm returns with the primal estimate constructed from the left and right singular vectors:

We describe numerical experiments for the low-rank matrix completion problem in section 7.2.

6.2.1 Iteration complexity

In the polyhedral case, we were able to assert through Proposition 8 that the optimal primal variable’s atomic support could be identified in finite time. As we show here, however, finite-time identification is not possible for the spectral case. The following counterexample shows that the partial SVD of , which we used in (12), is not able to give us a safe cover of the essential atoms in even when this set is a singleton and arbitrarily close to a dual solution .

Example 12 (Limitation of Partial SVD).

Consider the problem

| (18) |

where

for some fixed . The dual problem is

| (19) |

The solutions for the dual pair (18) and (19) are

In this pair of problems, the linear operator is simply the identity map, and the cone of essential atoms described by (13) depends only on the dual variable . Let and , respectively, be the first columns of and . Evidently, the support of coincides with the essential atoms of , and moreover, the support is a unique singleton. In other words,

We construct the following dual feasible solution

Because is diagonal, its left and right singular vectors and are given by . Note also that the top singular vector lies in the span of the basis vectors and that constitute the top and bottom singular vectors of . Therefore, any top- SVD of , with , cannot be used to recover exactly a primal solution . Moreover, for any , which in effect implies that it’s impossible to recover exactly the true solution even with an arbitrarily accurate dual approximation .

This last example motivates our study of the quality with which a partial SVD of a given feasible dual solution can be used to approximate the support . The next result measures the difference between and using one-sided Hausdorff distance.

Proposition 13 (Error in truncated SVD).

Oustry [42, Theorem 2.11] developed a related result based on the two-sided Hausdorff distance. Directly applying Oustry’s result to our context results in a bound on the order , which is looser than the bound shown in Proposition 13 because .

Finally, we show the error bound for primary recovery.

Proposition 14.

Assume that and . Let and , respectively, be primal optimal and dual feasible for one of the primal-dual pairs (Pi) and (Di), for . Let be the singular values satisfying , where we assume . Let denote the cone generated according to equation (13). Let be the solution recovered via (14). Then

where each is defined in Theorem 5.

Proposition 14 characterizes the error bound for our primal-retrieval strategy when is spectral. Our next corollary shows that Algorithm 1 can terminate in polynomial time with any tolerance .

Corollary 15.

For one of the problems (Di), , suppose that a dual oracle generates iterates converging to optimal variable with convergence rate

for some . If the atomic set is spectral then Algorithm 1 with will terminate in iterations.

6.2.2 Non-centrosymmetry and constrained primal recovery

We now consider the case in which the atomic set given by (11), which is not centrosymmetric. As we show below, the corresponding primal recovery problem is constrained.

Fix a feasible dual variable and define the eigenvalue decomposition for its product with the adjoint of by

where and the diagonal matrix , respectively, contain the top- eigenvectors and eigenvalues of , and and the diagonal matrix , respectively, contain the remaining eigenvectors and eigenvalues. Then the reduced atomic set by can be expressed as

The convex cone of essential atoms generated from the reduced atomic set is given by

The recovery problem (15) then becomes constrained, i.e.,

7 Numerical experiments

We conduct several numerical experiments on both synthetic and real-world datasets to empirically verify the effectiveness of our proposed primal-retrieval strategy. In section 7.1, we describe experiments on the basis pursuit denoising problem (Example 6), which shows the performance of our strategy on polyhedral atomic set. In section 7.2, we apply our primal-retrieval technique to the low-rank matrix completion problem (Example 11) and test the effectiveness of our proposed method on the spectral atomic set. In section 7.3, we describe experiments on a image preprocessing problem, where the atomic set is the sum of a polyhedral atomic set and a spectral atomic set. This shows that our strategy can be applied to more complicated cases. For all experiments, we implement the level-set method proposed by Aravkin et al. [3] where we only store the dual variable . We implement the level-set method and our primal-retrieval strategy in the Julia language [8] and our code is publicly available at https://github.com/MPF-Optimization-Laboratory/AtomicOpt.jl. All the experiments are carried out on a Linux server with 8 CPUs and 64 GB memory.

7.1 Basis pursuit denoise

The experiments in this section include a selection of five relevant basis pursuit problems from the Sparco collection [49] of test problems. The chosen problems are all real-valued and suited to one-norm regularization. Each problem in the collection includes a linear operator and a right-hand-side vector . Table 2 summarizes the selected problems. We compare the results with SPGL1 [47]. In all problems, we set . The results are shown in Table 3 where nMat denotes the total number of matrix-vector products with or . As we can observe from Table 3, the level-set algorithm equipped with our primal-retrieval technique can obtain an -feasible solution within a small number of iterations, which is consistent with the finite-time identification property described by Proposition 8. We also observe that level-set method coupled with the primal-retrieval strategy can converge faster than SPGL1 with its default stopping criterion. This suggests that our primal-retrieval technique is both a memory-efficient method for obtaining approximal primal solutions with provable error bounds, and is also a practical technique that allow the optimization algorithm to stop early.

| Problem | ID | ||||

|---|---|---|---|---|---|

| blocksig | 2 | 1024 | 1024 | 7.9e+1 | wavelet |

| cosspike | 3 | 1024 | 2048 | 1.0e+2 | DCT |

| gcosspike | 5 | 300 | 2048 | 8.1e+1 | Gaussian ensemble + DCT |

| sgnspike | 7 | 600 | 2560 | 2.2e+0 | Gaussian ensemble |

| spiketrn | 903 | 1024 | 1024 | 5.7e+1 | 1D convolution |

| Problem | nnz(x) | nMat(SPGL1) | nMat(level-set+PR) |

|---|---|---|---|

| blocksig | 71 | 22 | 5 |

| cosspike | 113 | 77 | 71 |

| gcosspike | 113 | 434 | 141 |

| sgnspike | 20 | 44 | 21 |

| spiketrn | 35 | 4761 | 1888 |

7.2 Low-rank matrix completion

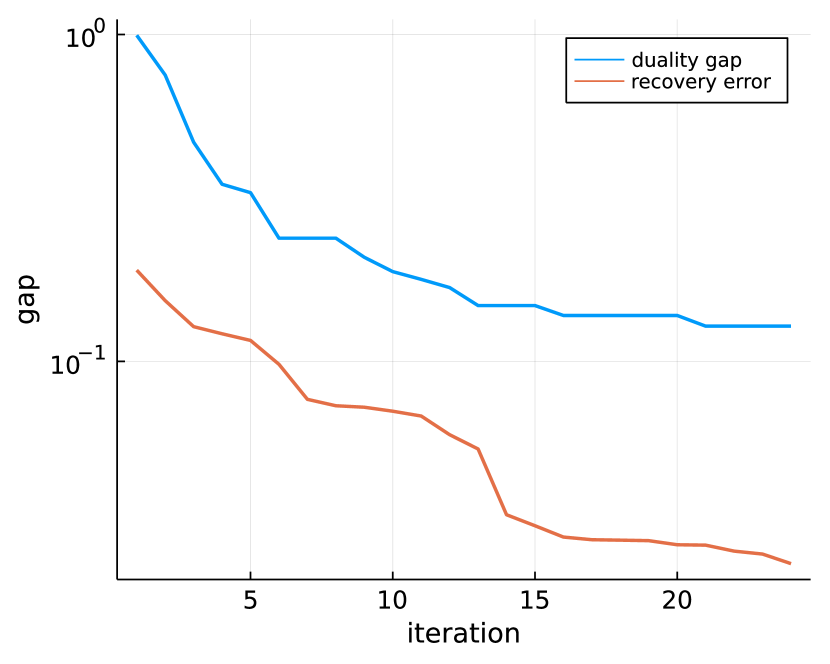

For this atomic set, we conduct an experiment similar to that carried out by Candés and Plan [13]. We retrieved from the website of National Centers for Environmental Information111https://www.ncei.noaa.gov a 6798-by-366 matrix whose entries are daily average temperatures at 6798 different weather stations throughout the world in year 2020. The temperature matrix is approximately low rank in the sense that , where is the matrix created by truncating the SVD after the top 5 singular values.

To test the performance of our matrix completion algorithm, we subsampled 50% of and then recovered an estimate . The solution gives a relative error of . The result is shown in Figure 1(a). As we can see from Figure 1(a), the recovery error exhibits a positive correlation with the duality gap, both the duality gap and the recovery gap decrease as the number of iteration increase. The observation in this experiment is consistent with our theory (Proposition 14).

7.3 Robust principal component analysis

In this section, we show that our primal-retrieval strategy can be applied to more complicated atomic sets besides polyhedral and spectral. We conduct the the similar experiment as in [12]. Face recognition algorithms are sensitive to shadows on faces, and therefore it’s necessary to remove illumination variations and shadows on the face images. We obtained face images from the Yale B face database [24]. We show the original faces in Figure 1(b), where each face image was of size with 64 different lighting conditions. The images were then reshaped into a matrix . Because of the similarity between faces and the sparse structure of the shadow, the matrix can be approximately decomposed into two components, i.e.,

where is a low-rank matrix corresponding to the clean faces and is sparse matrix corresponding to the shadows. Based on the work by Fan et al. [18], we know that such decomposition can be obtained via solving the following convex optimization problem:

| (20) |

By [19, Proposition 7.3], we know that (20) is equivalent to

with and where , and . The recovered low-rank component is shown in Figure 1(c). As we can see from the figure, most of the shadow are successfully removed. This experiment suggests that our primal-retrieval technique can potentially be used for more complex atomic set and allow the underlying the dual-algorithm to produce satisfactory result within a reasonable number of iterations.

8 Conclusion

In this work, we proposed a simple primal-retrieval strategy for atomic-sparse optimization. We demonstrate both theoretically and empirically that our proposed strategy can obtain good solutions to the cardinality-constrained problem given a dual-based algorithm converging to the optimum dual solution.

Further research opportunities remain, particularly for designing meaningful primal-retrieval strategies for non-polyhedral and non-spectral atomic sets. The primal-retrieval technique developed in this work is algorithm-agnostic, and it is an open questionn if it’s possible to develop more efficient primal-retrieval approaches tailored to specific optimization algorithms, such as the conditional-gradient method.

Références

- [1] Zeyuan Allen-Zhu, Elad Hazan, Wei Hu, and Yuanzhi Li. Linear convergence of a frank-wolfe type algorithm over trace-norm balls. In Proceedings of NeurIPS, pages 6191–6200, 2017.

- [2] A. Y. Aravkin, J. V. Burke, D. Drusvyatskiy, M. P. Friedlander, and K. MacPhee. Foundations of gauge and perspective duality. SIAM J. Optim., 28(3):2406–2434, 2018.

- [3] A. Y. Aravkin, J. V. Burke, D. Drusvyatskiy, M. P. Friedlander, and S. Roy. Level-set methods for convex optimization. Math. Program., Ser. B, 174(1-2):359–390, December 2018.

- [4] Andreas Argyriou, Theodoros Evgeniou, and Massimiliano Pontil. Convex multi-task feature learning. Machine Learning, 73, 2008.

- [5] Alper AtamtÅ«rk and Andrés Gómez. Safe screening rules for -regression. In Proceedings of ICML, 2020.

- [6] Runxue Bao, Bin Gu, and Heng Huang. Fast oscar and owl with safe screening rules. In Proceedings of ICML, 2020.

- [7] Amir Beck and Marc Teboulle. A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal on Imaging Sciences, 2(1):183–202, 2009.

- [8] Jeff Bezanson, Alan Edelman, Stefan Karpinski, and Viral B Shah. Julia: A fresh approach to numerical computing. SIAM review, 59(1):65–98, 2017.

- [9] Antoine Bonnefoy, Valentin Emiya, Liva Ralaivola, and Rémi Gribonval. Dynamic screening: Accelerating first-order algorithms for the lasso and group-lasso. IEEE Trans. Sig. Proc., 63(19):5121–5132, 2015.

- [10] J. V. Burke and J. J. More. On the identification of active constraints. SIAM J. Numer. Anal., 25(2):1197–1211, 1988.

- [11] Emmanuel J. Candès, Yonina C. Eldar, Thomas Strohmer, and Vladislav Voroninski. Phase retrieval via matrix completion. SIAM J. Imag. Sci., 6(1):199–225, 2013.

- [12] Emmanuel J Candès, Xiaodong Li, Yi Ma, and John Wright. Robust principal component analysis? J. Assoc. Comput. Mach., 58(3):11, 2011.

- [13] Emmanuel J Candes and Yaniv Plan. Matrix completion with noise. Proceedings of the IEEE, 98(6):925–936, 2010.

- [14] Emmanuel J Candès, Thomas Strohmer, and Vladislav Voroninski. Phaselift: Exact and stable signal recovery from magnitude measurements via convex programming. Comm. Pure Appl. Math., 66(8):1241–1274, 2013.

- [15] Venkat Chandrasekaran, Benjamin Recht, PabloA. Parrilo, and Alan S. Willsky. The convex geometry of linear inverse problems. Found. Comput. Math., 12(6):805–849, 2012.

- [16] S. S. Chen, D. L. Donoho, and M. A. Saunders. Atomic decomposition by basis pursuit. SIAM J. Sci. Comput., 20(1):33–61, 1998.

- [17] Lijun Ding, Alp Yurtsever, Volkan Cevher, Joel A. Tropp, and Madeleine Udell. An optimal-storage approach to semidefinite programming using approximate complementarity. SIAM J. Optim., 31(4):2695–2725, 2021.

- [18] Z. Fan, H. Jeong, B. Joshi, and M. P. Friedlander. Polar deconvolution of mixed signal. https://arxiv.org/abs/2010.10508.

- [19] Zhenan Fan, Halyun Jeong, Yifan Sun, and Michael P. Friedlander. Atomic decomposition via polar alignment: The geometry of structured optimization. Foundations and Trends in Optimization, 3(4):280–366, 2020.

- [20] Zhenan Fan, Yifan Sun, and Michael P Friedlander. Bundle methods for dual atomic pursuit. In Asilomar Conference on Signals, Systems, and Computers (ACSSC 2019), pages 264–270. IEEE, 2019.

- [21] M Fazel and J Goodman. Approximations for partially coherent optical imaging systems. Technical Report, 1998.

- [22] Marguerite Frank and Philip Wolfe. An algorithm for quadratic programming. Naval Research Logistics (NRL), 3(1-2):95–110, 1956.

- [23] M. P. Friedlander and P. Tseng. Exact regularization of convex programs. Technical Report TR-2006-26, Department of Computer Science, University of British Columbia, Vancouver, BC, Canada, November 2006. To appear in SIAM J. Optim.

- [24] Athinodoros S. Georghiades, Peter N. Belhumeur, and David J. Kriegman. From few to many: Illumination cone models for face recognition under variable lighting and pose. IEEE transactions on pattern analysis and machine intelligence, 23(6):643–660, 2001.

- [25] Laurent El Ghaoui, Vivian Viallon, and Tarek Rabbani. Safe feature elimination in sparse supervised learning. J. Pacific Optim., 8(4):667–698, 2012.

- [26] W. L. Hare. Identifying active manifolds in regularization problems. In Fixed-Point Algorithms for Inverse Problems in Science and Engineering, pages 261–271. Springer, 2011.

- [27] WL Hare and Adrian S Lewis. Identifying active constraints via partial smoothness and prox-regularity. J. Convex Anal., 11(2):251–266, 2004.

- [28] Christoph Helmberg and Franz Rendl. A spectral bundle method for semidefinite programming. SIAM J. Optim., 10(3):673–696, 2000.

- [29] J.-B. Hiriart-Urruty and C. Lemaréchal. Fundamentals of Convex Analysis. Springer, New York, NY, 2001.

- [30] Cho-Jui Hsieh and Peder A Olsen. Nuclear norm minimization via active subspace selection. In Proceedings of ICML, 2014.

- [31] Martin Jaggi. Revisiting frank-wolfe: Projection-free sparse convex optimization. In Inter. Conf. Mach. Learning (ICML 2013), pages 427–435, 2013.

- [32] Sham Kakade, Shai Shalev-Shwartz, and Ambuj Tewari. On the duality of strong convexity and strong smoothness: Learning applications and matrix regularization. Unpublished Manuscript, https://home.ttic.edu/~shai/papers/KakadeShalevTewari09.pdf, 2(1), 2009.

- [33] Nathan Krislock and Henry Wolkowicz. Explicit sensor network localization using semidefinite representations and facial reductions. SIAM J. Optim., 20(5):2679–2708, 2010.

- [34] Zhaobin Kuang, Sinong Geng, and David Page. A screening rule for -regularized ising model estimation. Advances in neural information processing systems (NIPS 2017), 30:720, 2017.

- [35] Zhouchen Lin, M. Chen, L. q. Wu, and Yi Ma. Linearized alternating direction method with adaptive penalty for low rank representation. In Proceedings of NeurIPS, 2011.

- [36] Jun Liu, Zheng Zhao, Jie Wang, and Jieping Ye. Safe screening with variational inequalities and its application to lasso. In International Conference on Machine Learning, pages 289–297. PMLR, 2014.

- [37] Rahul Mazumder, Trevor Hastie, and Robert Tibshirani. Spectral regularization algorithms for learning large incomplete matrices. Journal of machine learning research, 11(Aug):2287–2322, 2010.

- [38] Nicolai Meinshausen and Peter B uhlmann. High dimensional graphs and variable selection with the lasso. The Annals of Statistics, 34, 09 2006.

- [39] Eugene Ndiaye, Olivier Fercoq, Alexandre Gramfort, and Joseph Salmon. Gap safe screening rules for sparse-group lasso. In Advances in Neural Information Processing Systems (NIPS 2016), pages 388–396, 2016.

- [40] Eugène Ndiaye, Olivier Fercoq, Alexandre Gramfort, and Joseph Salmon. Gap safe screening rules for sparsity enforcing penalties. J. Mach. Learn. Res., 18:128:1–128:33, 2017.

- [41] Julie Nutini, Mark Schmidt, and Warren Hare. “active-set complexity" of proximal gradient: How long does it take to find the sparsity pattern? Optimization Letters, 13(4):645–655, 2019.

- [42] François Oustry. A second-order bundle method to minimize the maximum eigenvalue function. Math. Program., 89(1):1–33, 2000.

- [43] Anant Raj, Jakob Olbrich, Bernd Gärtner, Bernhard Schölkopf, and Martin Jaggi. Screening rules for convex problems. ArXiv, abs/1609.07478, 2015.

- [44] Jasson DM Rennie and Nathan Srebro. Fast maximum margin matrix factorization for collaborative prediction. In Proceedings of the 22nd International Conference on Machine Learning, pages 713–719, 2005.

- [45] R. T. Rockafellar. Convex Analysis. Princeton University Press, Princeton, 1970.

- [46] Robert Tibshirani. Regression shrinkage and selection via the lasso. J. Royal Stat. Soc. Ser. B, pages 267–288, 1996.

- [47] E. van den Berg and M. P. Friedlander. Probing the Pareto frontier for basis pursuit solutions. SIAM J. Sci. Comput., 31(2):890–912, 2008.

- [48] E. van den Berg and M. P. Friedlander. Sparse optimization with least-squares constraints. SIAM J. Optim., 21(4):1201–1229, 2011.

- [49] E. van den Berg, M. P. Friedlander, G. Hennenfent, F. J. Herrmann, R. Saab, and O. Yilmaz. Algorithm 890: Sparco: A testing framework for sparse reconstruction. ACM Trans. Math. Softw., 35(4), 2008.

- [50] Jie Wang, Jiayu Zhou, Jun Liu, Peter Wonka, and Jieping Ye. A safe screening rule for sparse logistic regression. In Advances in Neural Information Processing Systems (NIPS 2014), pages 1053–1061, 2014.

- [51] Jie Wang, Jiayu Zhou, Peter Wonka, and Jieping Ye. Lasso screening rules via dual polytope projection. In Advances in Neural Information Processing Systems (NIPS 2013), pages 1070–1078. Citeseer, 2013.

- [52] Zhen James Xiang, Yun Wang, and Peter J. Ramadge. Screening tests for lasso problems. IEEE Trans. Pattern Anal. Mach. Intell., 39(5):1008–1027, 2017.

- [53] M. Yuan and Y. Lin. Model selection and estimation in regression with grouped variables. J. Royal Stat. Soc. B., 68, 2006.

- [54] Xiao-Tong Yuan, Ping Li, and Tong Zhang. Gradient hard thresholding pursuit. J. Mach. Learn. Res., 18:166:1–166:43, 2017.

- [55] Weizhong Zhang, Bin Hong, Wei Liu, Jieping Ye, Deng Cai, Xiaofei He, and Jie Wang. Scaling up sparse support vector machines by simultaneous feature and sample reduction. In Proceedings of ICML, 2017.

Appendix

Annexe A Derivation of duals

We derive the dual problems (D1), (D2) and (D3) using the Fenchel–Rockafellar duality framework. We use the following result.

Theorem 16 ([45, Corollary 31.2.1]).

Let and be two closed proper convex functions and let be a linear operator from to , then

If there exist in the interior of such that in the interior of , then strong duality holds, namely both infima are attained.

We also need a result that describes the relationship between gauge, support, and indicator functions.

Proposition 17 ([19, Proposition 3.2]).

Let be a closed convex set that contains the origin. Then

For problem (P1), let

By the properties of conjugate functions and Proposition 17, we obtain

Then by Theorem 16, we can get the dual problem for (P1) as

For (P2),

By the properties of conjugate functions and Proposition 17, we obtain

Then by Theorem 16, it follows that the dual problem for (P2) is

For (P3),

By the properties of conjugate functions and Proposition 17, we can get that

Then by [29, Example E.2.5.3], we know that the support function of the sublevel set is

Finally, by Theorem 16, we can get the dual problem for (P3) as

Annexe B Proof of Theorem 5

The proof of this Theorem relies on the following duality property between smoothness and strong convexity.

Lemma 18 ([32, Theorem 6]).

If is -smooth, then is -strongly convex.

Proof of Theorem 5.

- a)

-

b)

Let denote the optimal dual variable for D2. First, we show that can be bounded by the duality gap. Let . By Lemma 18, is -strongly convex, and it follows that is also -strongly convex. By the definition of strongly convex,

By optimality, . Reordering the inequality to deduce that

Next, we show that . For any ,

where the last inequality follows from the definition of in Theorem 5.

-

c)

Let denote the optimal dual variables for D3. First, we show that can be bounded by the duality gap. Let

By Lemma 18, is -strongly convex, and it’s not hard to check that is -strongly convex. By the definition of strongly convex,

By optimality,

Reorder the inequality to deduce that

Since is unknown to us, we will then get an upper bound for . Fix , let . By the property of perspective function, we know that is convex. Then it follows that

Therefore,

Finally, we show that . For any ,

∎

Annexe C Upper and lower bound for

First, we consider (D3). Let , then (D3) can be equivalently expressed as

Fix , then (D3) can be expressed as

| (21) |

Now compare (21) with (D1) to conclude that they are equivalent when . It thus follows that (P3) is equivalent to

Next, consider using the level-set method [3] with bisection to solve (P3). There exists such that (P3) is equivalent to

With the level-set method, we are able to get and such that and is the optimum for

for . Then there exits and such that and is optimal for

for .

Finally, by [19, Theorem 5.1] we can conclude that

Therefore, we can get upper and lower bounds for via level-set method with bisection. Moreover, by strong duality and convergence of the bisection method, the gap between and will converge to zero.

Annexe D Proof of Proposition 8

Démonstration.

First, we show that for any such that , the condition

holds. By Assumption 3 and the definition of -nondegeneracy, we know that

| (22) |

For any , we have

On the other hand, for any , we have

Therefore,

Notice that contains only the atoms that corresponds to the largest . Therefore .

By the assumption . For , we know there exist such that for all . Therefore and we complete the proof. ∎

Annexe E Proof for Proposition 13

Démonstration.

First, we derive a monotonicity property of . By the definition of , it follows that

| (23) |

For any , we know that by Theorem 5. Then by 23, we have

For any ,

where the second equality holds since by the definition of . Define and , where are the top- singular vectors of . Let , and , then

| (24) |

Now we consider the subproblem in (24):

| (Psub) | ||||

| subject to |

If and is a solution of the problem (Psub), then it’s easy to verify that

| and |

is also a valid solution. Therefore there must exist solution such that , that is only and and are greater or equal than 0. This allow us to further reduce the problem to

| subject to | |||

It’s easy to verify that when , the above problem attains solution at

When , the solution is simply . Therefore the optimal value of (Psub) is , plug this into 24 and we finish the proof. ∎

Annexe F Proof of Proposition 14

We describe the following lemma before proceeding to the proof of Proposition 14.

Lemma 19 (Hausdorff error bound).

Given , there exists such that

| (25) |

Démonstration.

Let . By the definition of the one-sided Hausdorff distance , for any , there exist a corresponding such that

Let , then it’s straighforward to verify that and

where (i) follows from the orthonormal decomposition and when our atomic set is the set of rank-one matrices. ∎

Proof of Proposition 14.

By Lemma 19, we know that there exist satisfies 25. Then by the -smoothness of ,

| (26) |

By the smoothness and convexity of , we further have

Note we assume and , the above reduces to . Combining with 26, we obtain

where the last inequality is by Lemma 19. Combining the above with Proposition 13 leads to the desired result. ∎