Rate-Optimal Robust Estimation of High-Dimensional Vector Autoregressive Models

Abstract

High-dimensional time series data appear in many scientific areas in the current data-rich environment. Analysis of such data poses new challenges to data analysts because of not only the complicated dynamic dependence between the series, but also the existence of aberrant observations, such as missing values, contaminated observations, and heavy-tailed distributions. For high-dimensional vector autoregressive (VAR) models, we introduce a unified estimation procedure that is robust to model misspecification, heavy-tailed noise contamination, and conditional heteroscedasticity. The proposed methodology enjoys both statistical optimality and computational efficiency, and can handle many popular high-dimensional models, such as sparse, reduced-rank, banded, and network-structured VAR models. With proper regularization and data truncation, the estimation convergence rates are shown to be almost optimal in the minimax sense under a bounded -th moment condition. When , the rates of convergence match those obtained under the sub-Gaussian assumption. Consistency of the proposed estimators is also established for some , with minimax optimal convergence rates associated with . The efficacy of the proposed estimation methods is demonstrated by simulation and a U.S. macroeconomic example.

Keywords: Autocovariance, high-dimensional time series, minimax optimal, robust statistics, truncation

1 Introduction

1.1 High-dimensional vector autoregression

Vector autoregressive (VAR) models are arguably the most commonly used multivariate time series models in practice; see, e.g., Lütkepohl, (2005), Tsay, (2013), and the references therein. Applications of the model can be found in a wide range of fields, such as economics and finance (Wu and Xia,, 2016), time-course functional genomics (Michailidis and d’Alché Buc,, 2013), and neuroimaging (Gorrostieta et al.,, 2012). Consider a -dimensional zero-mean VAR model of order , i.e., VAR() model,

| (1) |

where is the observed time series, is the lag- coefficient matrix, and is a serially uncorrelated white noise innovation. We assume that all solutions of the determinant equation are outside the unit circle, where is referred to as the AR matrix polynomial in . In modern applications, the dimension is often large. However, since the number of coefficient parameters is and those coefficients are often highly correlated, an unrestricted VAR() model is likely to encounter the difficulty of over-parameterization and, hence, cannot provide reliable estimates nor accurate forecasts without further restrictions.

Estimation consistency of high-dimensional VAR models is achievable under some structural assumptions, provided that certain regularity conditions are satisfied. For example, if the coefficient matrices have an unobserved low-dimensional structure, such as sparsity or low-rankness, the structure-inducing regularization methods, including Lasso (Basu and Michailidis,, 2015), Dantzig selector (Han et al.,, 2015), and nuclear norm penalty (Negahban and Wainwright,, 2011), give consistent estimates under the Gaussian assumption of the time series. Recently, Zheng and Raskutti, (2019), Zheng and Cheng, (2021), and Wang et al., 2021b developed novel technical tools to relax the distributional assumption from Gaussian to sub-Gaussian.

However, in real applications, time series data often contain aberrant observations, which can occur in many ways, such as missing values, measurement error contamination, and heavy-tailed distribution. Those aberrant observations, if overlooked, can lead to biased estimates, erroneous inference, and sub-optimal forecasts. The situation can easily be further exacerbated when the dimension is large. It is, therefore, important to study robust estimation of high-dimensional VAR models. In addition, the true data generating process is unlikely to follow a VAR model. Model uncertainty, including using a high-dimensional VAR() model as an approximation to the true model, also deserves a careful investigation.

Recently there have been emerging interests in studying high-dimensional VAR models with non-i.i.d. and/or non-sub-Gaussian innovations. For example, Wu and Wu, (2016) studied theoretical properties of Lasso and constrained minimization estimators for a VAR model with weakly correlated and heavy-tailed . Wong et al., (2020) investigated the estimation and prediction performance of Lasso for the sub-Weibull time series data under a -mixing condition. Both theoretical and numerical results in the literature show that the performance of standard regularized estimators deteriorates substantially when the data have heavy tails. For robust estimation of high-dimensional heavy-tailed time series data, Qiu et al., (2015) developed a quantile-based Dantzig selector for the class of elliptical VAR processes. Han et al., (2020) proposed a robust estimation method for high-dimensional sparse generalized linear models with temporal dependent covariates. However, the existing literature on robust estimation for time series data focuses on sparse models. To the best of our knowledge, there is no unified solution to address the robust estimation problem for a large class of high-dimensional VAR models.

Our proposed robust estimation procedure is built on two key ingredients: the constrained Yule–Walker estimator and the robust autocovariance matrix estimator. The first ingredient, the constrained Yule–Walker estimator, provides a general and flexible estimation framework for two classes of high-dimensional models, namely the approximately low-dimensional VAR models and linear-restricted VAR models. The second ingredient, the robust autocovariance matrix estimator, is easy to implement by truncating the time series data. However, based on the specific model structure, we need to adapt the data truncation methods. With a large class of distributions having bounded second or higher-order moments, the proposed estimators are shown to be consistent under high-dimensional scaling. To be specific, we summarize the main contributions of this paper as follows:

-

(i)

For various high-dimensional VAR models, the paper provides a simple and general estimation procedure robust to model misspecification, heavy-tailed noise contamination, and conditional heteroskedasticity. Our proposal can handle many popular high-dimensional VAR models, such as sparse, reduced-rank, banded, and network VAR models. An efficient and scalable alternating direction method of multipliers (ADMM) algorithm is developed.

-

(ii)

The proposed methodology enjoys statistical optimality in the minimax sense. Our theoretical framework deals with heavy-tailed distributions with bounded -th moments for any . It results in a phase transition on the rates of convergence: for , the estimator achieves the same convergence rates as those obtained under the Gaussian or sub-Gaussian distribution, while consistency is also established with a slower rate for . By establishing the matching minimax lower bounds, we show that the proposed estimators for high-dimensional VAR models and autocovariance matrices are rate-optimal.

1.2 Related literature

This work is related to a huge body of literature on the robust estimation of high-dimensional regression and covariance matrices. The early developments in robust statistics were pioneered by Huber, (1964) and Hampel, (1971, 1974); see also the overview by Hampel, (2001) and the references therein. For time series data, robust estimation methods were developed for univariate and multivariate ARMA models (Martin,, 1981; Muler et al.,, 2009; Muler,, 2013). For high-dimensional i.i.d. data, inspired by Catoni, (2012), the non-asymptotic deviation analysis for heavy-tailed variables and robust -estimators for high-dimensional regression were proposed by Fan et al., (2017), Loh, (2017), Sun et al., (2020), Wang et al., (2020), and many others. These recent robust estimation methods and their theoretical results were further extended to high-dimensional covariance and precision matrix estimation problems, such as Avella-Medina et al., (2018), Minsker, (2018), and Zhang, (2021). Another research line of robust regression is the least absolute deviation loss, and more generally, quantile loss, which have been studied extensively; see, e.g., Wang et al., (2007), Belloni and Chernozhukov, (2011), and Wang et al., (2012). Recently, Fan et al., (2021) and Ke et al., (2019) independently proposed truncated variants of the sample covariance, which are easy to implement and motivate us to develop the robust estimators of high-dimensional autocovariance matrices.

The upper and lower bound development for high-dimensional estimation problems under heavy-tailed distributions is another emerging and important research topic. Under heavy-tailed distributions, the phase transition phenomenon in the rate of convergence was previously discovered by Bubeck et al., (2013), Avella-Medina et al., (2018), Sun et al., (2020), Tan et al., (2022), and others. For the lower bound development, the phase transition phenomenon was first established by Devroye et al., (2016) for univariate mean estimation problem, and was extended to the fixed and high-dimensional linear regression problems in Sun et al., (2020). Compared with the existing literature, our minimax lower bound results are established under a much more complicated setting. First, all existing lower bound results are developed for i.i.d. data, but we allow weak serial dependency and establish the minimax lower bounds under strong mixing conditions. Second, for the lower bounds of the linear regression problem in Sun et al., (2020), a finite moment condition is imposed on the random error terms while the covariates are assumed to be light-tailed. Without any assumption on data generating process, we consider the finite moment condition on the observed time series data that serve as both predictors and responses in the autoregressive models, which is fundamentally different from the conventional linear regression problem.

1.3 Notation and outline

We start with some notations used in the paper. Let denote a generic positive constant, which is independent of the dimension and sample size. For any two real-valued sequences and , if there exists a such that for all . In addition, we write if and . For any two real numbers and , let denote their minimum. Throughout the paper, we use bold lowercase letters to denote vectors. For any vector , denote its norm as for , its maximum norm as , and its norm as . We use bold uppercase letters to denote matrices. For any matrix , where is the -th column of , denote its norm as , for any , and its th largest singular value as , for all . For a given matrix , we let , , and denote its Frobenius norm, operator norm, and nuclear norm, respectively, where , , and . For any two matrices and , their Kronecker product is . For any subspace and any matrix , denote by and the orthogonal complement of and the projection of onto , respectively.

The rest of the paper is organized as follows. Section 2 studies constrained Yule–Walker estimators for two classes of VAR models: VAR with approximately low-dimensional structure and VAR with linear restrictions. Section 3 develops robust autocovariance estimators tailored for various low-dimensional structures. Minimax lower bounds for both high-dimensional VAR estimation and autocovariance matrix estimation are investigated in Section 4. Computational algorithms and implementation details are discussed in Section 5. Section 6 presents some simulation results, and Section 7 shows an empirical application of U.S. macroeconomic data. All technical proofs and detailed algorithms are relegated to the Appendices. The codes and data can be found at https://github.com/diwangstat/RobustAR.

2 Constrained Yule–Walker Estimation

2.1 Yule–Walker equation

Consider a general mean-zero and covariance stationary process , where . In many applications, it is common to model the time series data and predict their future values using a linear VAR model. The VAR() model in (1) can be rewritten as

| (2) |

where is the predictor vector and is the combined parameter matrix. Throughout this paper, we consider that the lag order is fixed. Given the stationarity of , the parameter matrix of interest is defined as the minimizer of the risk function

| (3) |

For any integer , denote the lag- autocovariance matrix of by . By simple algebra,

| (4) |

which implies that or if is invertible, where and

| (5) |

This relationship between the parameter matrix and autocovariance matrices is well known as the multivariate Yule–Walker equation for VAR() models (Lütkepohl,, 2005; Tsay,, 2013). When the data generating mechanism of is not the VAR() process, the Yule–Walker equation still holds if VAR is used as a running model.

The existence of aberrant observations, such as missing values or data contaminated by measurement errors, is ubiquitous in high-dimensional macroeconomic, environmental, and genetic data, among many other applications. In a VAR process, when some of the variables are removed as they cannot be observed or measured, the rest of the available variables generally would not follow any finite-order VAR model (Lütkepohl,, 2005). In addition, if the true signal of the time series follows a VAR process and the observed time series is a contaminated version of the true signal plus a measurement error, no longer follows a VAR process. Hence, the VAR model assumption commonly used in real applications is questionable, but the Yule–Walker equation which holds without any data generating mechanism assumption can be utilized to construct estimation methodology for the general covariance stationary time series.

In addition to the sub-Gaussian innovation assumption, another key limitation in the existing literature is the i.i.d. assumption for the innovation series . The conditional heteroskedasticity is often observed in financial time series, and violation of the homogeneous error assumption can affect the performance of standard estimation methods. Another major advantage of our moment-based methodology is that the i.i.d. assumption for can be relaxed to a serially uncorrelated, but weakly stationary condition. Specifically, our theoretical analysis allows some serial dependence in , dependence between and , and conditional heteroskedasticity in . Note that this setting of innovations includes many important conditional heteroskedasticity models, such as GARCH models (Engle,, 1982; Bollerslev,, 1986) and double AR models (Ling,, 2004; Zhu et al.,, 2018).

Based on the Yule–Walker equation, we propose a constrained minimization estimation approach, named the constrained Yule–Walker estimation, for two classes of high-dimensional VAR() models. In Section 2.2, we consider the VAR() model, where in (3) can be approximated by a matrix with some latent low-dimensional structure. In Section 2.3, we consider the VAR() model whose coefficients are subject to some linear restrictions. These two classes of models are shown to encompass many commonly-used high-dimensional VAR models in practice.

2.2 Approximately low-dimensional VAR

We first consider the situations where the dimension is relatively large compared to the sample size and the parameter matrix of interest in (3) can be well approximated by a matrix with certain types of low-dimensional structure. The approximately low-dimensional structure, such as weak sparsity and approximate low-rankness, is general and natural in high-dimensional time series modeling.

Based on the Yule–Walker equation, we consider a general class of constrained estimation:

| (6) |

where is a matrix norm as the regularization function, is its dual norm as the constraint function, is the constraint parameter, and and are robust autocovariance estimators to be specified later in Section 3. When is sufficiently small, the constraint function guarantees that the sample version of the Yule–Walker equation holds roughly, and the regularizer induces the low-dimensional structure and improves the estimation efficiency.

Following the framework for high-dimensional analysis in Negahban et al., (2012), we consider a decomposable regularizer . For a generic low-dimensional structure, define , where is referred to as the model subspace to represent the specific model constraints; for instance, it can be the subspace of low-rank matrices (see Example 1). The orthogonal complement of , denoted by , is the associated perturbation subspace to capture the deviation from the model subspace and is adopted to measure the error of approximation to the low-dimensional structure. We assume that the true value can be decomposed into its projections onto and , i.e., .

We call a regularizer decomposable with respect to a pair of subspaces , if for any and ,

| (7) |

Many of the commonly-used convex regularizers, such as the nuclear norm for low-rankness, are shown to be decomposable; see Negahban et al., (2012) for more details of decomposable regularizers. To measure the magnitude of the low-dimensional structure, define by the associated constant such that for any . In our theoretical analysis, we consider another auxiliary matrix norm such that satisfy that and for any symmetric matrix and any compatible matrix . The following example illustrates the suitable choice of , , and for a reduced-rank VAR model.

Example 1 (Reduced-rank VAR).

The reduced-rank VAR model is an important approach to modeling high-dimensional time series by imposing a low-rank structure on ; see also Velu and Reinsel, (2013), Basu et al., (2019), and Wang et al., 2021a . To induce low-rankness, we use the nuclear norm as the regularizer and the operator norm as the constraint function; that is, and . By the submultiplicative property of the operator norm, . For the approximately low-rank matrix , denote by and the subspace spanned by its leading left and right singular vectors, respectively. Define the model subspace

| (8) |

and the perturbation space

| (9) |

For the general mean-zero and covariance stationary process , if we model the data by a VAR() model in (1) and apply the constrained Yule–Walker estimator in (6) with robust autocovariance estimators and , we have the following upper bounds for the estimation error between the estimated matrix and the true value defined in (3).

Proposition 1.

For the constrained Yule–Walker estimator in (6), suppose that , , and . Then, for ,

| (10) |

This proposition presents the deterministic estimation error bounds in , , and , given that the estimators and satisfy some regularity conditions. The estimation error bounds are related to and , and these terms could be bounded or diverge slowly as the dimension increases; see more discussions for each specific model in Section 3. When the true parameter matrix admits a low-dimensional approximation rather than an exact structure, is strictly positive, and the second terms in the second and third upper bounds are related to the approximation error. In this case, the upper bounds in this proposition hold uniformly for a class of low-dimensional structures with respect to , and the class of upper bounds can be minimized by balancing the estimation error on and the approximation error on .

Moreover, in some cases, it is of interest to consider the approximate low dimensionality in a more structured manner. In particular, based on the multi-response nature, the VAR model in (2) can be split into sub-models:

| (11) |

where is the -th row of , for . For these sub-models, as each is a -dimensional vector, we may consider some low-dimensional structures, such as sparsity, on . Then, we consider the constrained estimation framework for each :

| (12) |

where is a vector norm, is its dual norm, and is the -th row of . For simplicity, we consider the same constraint parameter for all sub-problems. In this framework, these sub-problems can be handled in parallel and thus can be solved efficiently.

In an analogous fashion, we consider a pair of subspaces of , , for each , where and for any and , for all . In addition, define by the constant such that for any . Moreover, for theoretical analysis, we consider the auxiliary matrix norms and satisfying that and for any compatible matrix and vector . The following example shows that the regularization can be applied to the sparse VAR model.

Example 2 (Sparse VAR).

The sparse VAR model assumes that each is strictly or weakly sparse, so that each response variable is only related to a subset of lagged values . Though the overall sparsity in has been considered in many existing literature, such as Basu and Michailidis, (2015) and Kock and Callot, (2015), the sparsity structure in rows seems more natural in the time series context. For example, in the diagonal VAR(1) model, the total degree of sparsity grows with , while the sparsity level in each row remains fixed. To induce sparsity in each row, as in Han et al., (2015), we consider , , , and . For the weakly sparse , , denote by any index set corresponding to those coefficients significantly distant from zero in . For each , define the model subspace associated with the chosen index set as

| (13) |

and the perturbation subspace

| (14) |

For the general mean-zero and covariance stationary process , if we separate the VAR() model to sub-problems in (11) and apply the separated constrained Yule–Walker estimator in (12) with robust autocovariance estimators and , we have the following upper bounds for the estimation error between and the true value .

Proposition 2.

2.3 Linear-restricted VAR

In modern high-dimensional time series modeling, domain knowledge and prior information are commonly available in addition to the time series data. In many such cases, prior information can be formulated as linear restrictions on the parameter matrix, and in this subsection, we apply the constrained Yule–Walker estimation approach to the high-dimensional VAR models with linear restrictions.

As discussed in Tsay, (2013), a general linear parameter restriction can be expressed as , where is a prespecified constraint matrix, is a known constant vector, and is the unknown parameter vector. Note that the linear constraint representation is not unique; that is, for any nonsingular matrix , . Thus, we require that is a tall orthonormal matrix, i.e., . Otherwise, we can apply singular value decomposition or QR decomposition to .

For simplicity, we consider the case where . In this case, we can rewrite the VAR() model in (2) to

| (16) |

Similarly to the discussions in Section 2.1, for the general stationary time series which may not strictly follow a linear-restricted VAR process, the parameter of interest is defined as

| (17) |

It implies the linear-restricted version of the Yule–Walker equation

| (18) |

provided that is invertible.

Let and . For and , suppose that we have robust estimators and . Then, we consider the constrained Yule–Walker estimator

| (19) |

where is the constraint parameter and the norm provides both element-wise regularization on and element-wise constraint on the sample version of Yule–Walker equation. Decompose the restriction matrix , where each is a matrix. Let and then the estimator of is .

The linear-restricted model encompasses several important recent developments in high-dimensional vector autoregression.

Example 3 (Banded VAR).

The banded VAR(1) proposed by Guo et al., (2016) has the following banded coefficient structure:

| (20) |

where is called the bandwidth parameter. The banded structure is a special sparse structure, so we can formulate it to a linear constraint , where each column of is a coordinate vector corresponding to one nonzero index in .

Example 4 (Network VAR).

Zhu et al., (2017) proposed the network VAR model for the network time series data , which has an observable network structure with the adjacency matrix . The network VAR model assumes the form

| (21) |

In other words, it is a VAR(1) model with , and the associated coefficient vector can be written as , where , and . In this parameterization, is an orthonormal matrix.

For a general zero-mean and covariance stationary time series , if we model the data by the linear-restricted VAR() model in (16) and apply the linear-restricted Yule–Walker estimator in (19) with the robust estimators and , we have the upper bounds for the estimation error between the estimated parameter vector and the true vector defined in (17).

Proposition 3.

For the constrained Yule–Walker estimator in (19), suppose that , , and . Then,

| (22) |

This proposition presents the norm estimation error bounds of the low-dimensional parameter , which is a new result for the linear-restricted VAR models. Similarly to Proposition 1, the upper bound is proportional to that could be related to the dimension , depending on the specific linear restrictions. The upper bound directly implies that , and some sharper bounds may be obtained based on the the special structure of . More concrete results and discussions are provided in Section 3.3.

Remark 1.

For the upper bound result in Proposition 3, the terms and may vary or even diverge with the dimension . Indeed, the term for the network VAR model in Example 3 naturally diverges at a rate . The explicit rate of depends on the specific linear restriction structure and further assumptions. More discussions about these terms are given in Section 3.3 for some specific models.

The deterministic upper bounds in Propositions 1-3 imply that the performance of parameter estimation of the constrained Yule–Walker estimators hinges on the accuracy of autocovariance matrix estimation. It suffices to find reliable robust autocovariance estimators, which will be introduced in the next section.

3 Robust Autocovariance Estimation

3.1 Element truncation estimator

Fan et al., (2021) and Ke et al., (2019) proposed a simple robust estimation approach via appropriate truncation on data and showed that the truncated covariance estimator can achieve the optimal rate as that under the sub-Gaussian distribution for independent samples. We first apply the truncation method to estimate the elements of autocovariance matrices.

We consider the element-wise truncated data , where , for , and is the truncation parameter. Based on this truncation scheme, can be estimated by , for any integer . The corresponding autocovariance estimators are

| (23) |

and

| (24) |

where , for . The element-wise truncation can control the deviation of or and the truncation parameter allows us to balance the tradeoff between the truncation bias and robustness.

Note that no data generating mechanism assumption is imposed, and we adopt the -mixing condition to quantify the serial dependency. For any stochastic process , the lag- -mixing dependence coefficient is defined as , where

| (25) |

the supremum being taken over all events and , and is the sigma field generated by the process. To derive the theoretical guarantees of the autocovariance estimation, we have the following assumptions.

Assumption 1.

The process is weakly stationary and -mixing with the mixing coefficients , where is a sequence possibly depending on such that for some constant .

Assumption 2.

For , , for some .

Assumption 1 states the weak stationarity and geometrically decayed -mixing, rather than assuming that the true data generating process (DGP) of is a VAR() process. If truly follows a VAR() model in (1), Assumption 1 holds by the stationarity and geometric ergodicity of the VAR process; see Proposition 2 in Liebscher, (2005). Assumption 2 relaxes the commonly-used sub-Gaussian condition in the existing literature to the bounded -th moment condition, where may diverge to infinity with the dimension . For the strong mixing time series, we denote as the effective sample size representing the number of effectively independent samples from observations. Note that is of almost the same rate as since for any .

This proposition presents the bounds for the element-wise truncation autocovariance estimators and . If the truncation parameter is chosen appropriately and the moment bound is fixed, the convergence rate of autocovariance matrix estimation in the norm is . When , the data has a bounded fourth moment and the convergence rates of the autocovariance matrices scale as . When , the convergence rates have a smooth phase transition phenomenon, decreasing from to .

Remark 2.

For robust covariance estimators based on data truncation or shrinkage, the existing theoretical analysis in Fan et al., (2021) and Ke et al., (2019) focused on the data with a bounded fourth moment. Our results in Proposition 4 relax the fourth moment condition to the -th moment condition and can effectively handle a much larger class of distributions. In addition, Avella-Medina et al., (2018) proposed rank-based and adaptive Huber regression methods for robust covariance estimation and obtained a similar phase transition in the upper bound with respect to .

For the weakly sparse VAR model in Example 2, and can be used as robust autocovariance estimators in the constrained Yule–Walker estimation in (12) with and . The resulting estimator for the -th row of is denoted as and the sparse estimator is .

Define an -“ball” with radius as . Note that when , is the set of all -by- matrices whose rows are at most -sparse. For , requires that the absolute values of entries in decay sufficiently fast, which is more general than the exact sparsity assumption. Given the weak sparsity in the rows of , it is natural to assume that is bounded.

We are ready to present the theoretical properties of .

Theorem 1 (Sparse VAR upper bounds).

This theorem presents non-asymptotic estimation upper bounds in various matrix norms under the weakly sparse structure. If both and are fixed, the , , and upper bounds scale as , , and , respectively. If the data have a bounded fourth moment with , the first two rates of convergence match those of Gaussian sparse VAR in Han et al., (2015). When the true model has a strict sparsity structure with and sparsity level , based on the bound, the sample size requirement is . That is, if the sparsity level in each row of is finite, the dimension is allowed to be exponentially large compared to . If the data do not have a bounded fourth moment but only a bounded -th moment for some , the proposed estimator is still consistent but the rate of convergence in the norm decreases from to .

Remark 3.

The boundedness of is widely assumed in the existing literature of the Dantzig selector for sparse VAR models; see, for example, Han et al., (2015) and Wu and Wu, (2016). Indeed, if follows a VAR(1) process in (1), the covariance of has an explicit form , where is the covariance matrix of , and can be verified to be independent of given that and satisfy certain structures. For example, if both and are block diagonal with a fixed block size, is also block diagonal and its norm is independent of . If has a banded structure as in Example 3, shrinks to zero exponentially as increases to infinity, and hence the boundedness of can be expected.

Remark 4.

The robust estimation of sparse linear regression has been investigated in Fan et al., (2017), Sun et al., (2020), and Fan et al., (2021), among many others. We highlight some main differences between conventional linear regression and vector autoregression in terms of robust estimation. First, for linear regression models, the heavy-tailed distribution condition is considered on the random errors; that is, the response is conditionally heavy-tailed given the predictors. In our analysis, as no data generating mechanism assumption is imposed, the heavy-tailed distributional assumption, i.e. the moment condition in Assumption 2, is directly considered on the observed data . Second, when the design matrix of the linear regression model satisfies some regulatory conditions, the -th moment condition is considered for the random errors in Sun et al., (2020). However, for the VAR models, as both predictor and response are simultaneously heavy-tailed, a more stringent -th moment condition has to be imposed in our theoretical analysis. Though the distributional assumptions are different in these two problems, the similar phase transition phenomenon can be obtained for two regimes and .

3.2 Vector truncation estimator

In this subsection, we propose and study an autcovariance estimator that is robust in the operator norm. Intuitively, in order to achieve the operator norm robustness, we need to control the spectrum of and . Note that and . Therefore, we propose the truncation method to the whole vector in the norm. To construct robust estimators for and of a VAR() model, we consider the vector-truncated responses and predictors and , for , where two truncation parameters and are adopted as and are of different dimension when . For the case with , we can use a single parameter by setting . Based on the vector truncation of the data, the corresponding truncation autocovariance estimators are defined as

| (30) |

Remark 5.

Fan et al., (2021) proposed a robust covariance estimator based on the vector-wise truncation in the norm and investigated its theoretical properties under the finite fourth moment condition. However, as we are interested in the relaxed setting with the finite -th moment, the truncation in the norm is not appropriate in our setting. Ke et al., (2019) proposed the spectrum-wise truncation for robust estimation of covariance matrix, and our method shares the same idea.

For the vector-wise truncation estimator, we adopt the -mixing condition to quantify the serial dependency. Specifically, for any stochastic process , the lag- -mixing dependence coefficient is defined as , where

| (31) |

the supremum being taken over all pairs of partitions and such that and . To study the theoretical properties of the vector-wise truncation estimators, we need the following assumptions.

Assumption 3.

The process is weakly stationary and -mixing with the mixing coefficients , where is a sequence possibly depending on such that for some constant .

Assumption 4.

For any such that and some , .

Note that the -mixing condition in Assumption 3 is slightly stronger than the -mixing condition in Assumption 1 for the element-wise truncation estimators. Here we adopt the -mixing condition in order to apply the Bernstein-type inequality for -mixing random matrices developed by Banna et al., (2016). For the VAR process with independent and identically distributed , the absolute regularity with geometrically decayed -mixing coefficients is equivalent to the geometric ergodicity (Liebscher,, 2005). The bounded -th moment condition in Assumption 4 is also slightly stronger than the bounded -th moment condition in Assumption 2. Here is only for the technical purpose and can be arbitrarily small.

This proposition presents the operator norm bounds for the vector truncation autocovariance estimators and . Similarly to the element truncation estimator in Section 3.1, we define . If the moment bound is fixed, the operator norm convergence rates of both autocovariance matrix estimators scale as . When the time series data has a bounded fourth moment, that is , our results are almost the same as those of covariance matrix estimators for i.i.d. data in Ke et al., (2019) and Fan et al., (2021). Smooth transition on the operator norm convergence rate is observed when the fourth moment condition is relaxed to the -th moment condition.

Based on the rates of the vector truncation autocovariance matrices, we derive the estimation rate of the nuclear norm constrained Yule–Walker estimator for the weakly low-rank VAR model. Define an -“ball” for the singular values with radius as . When the singular values of are weakly sparse, it is natural to assume that , the sum of singular values of , is bounded. Denote by the reduced-rank constrained Yule–Walker estimator with the regularizer , the constraint function , the constraint parameter , and the vector truncation autocovariance estimators in (30) with truncation parameters and .

Theorem 2 (Reduced-rank VAR upper bounds).

This theorem presents the non-asymptotic estimation upper bounds in the operator norm, nuclear norm, and Frobenius norm, respectively. If is fixed, the convergence rates of in the operator norm and Frobenius norm scale as and . Specifically, when , that is the time series have a bounded fourth moment, the Frobenius norm convergence rate of the robust estimator is nearly the same as those obtained by the standard nuclear norm penalized estimators for Gaussian VAR model in Negahban and Wainwright, (2011) and Basu et al., (2019). When the time series only has a bounded -th moment for some , the estimation error rates decrease from to . Note that though the estimation convergence rates decrease, if is fixed, the sample size requirement for estimation consistency remains unchanged when the moment condition is relaxed.

Remark 6.

The boundedness of is equivalent to that the smallest eigenvalue of is bounded away from zero. If follows a stationary VAR model in (1), this condition can be guaranteed if the smallest eigenvalue of is bounded away from zero, where is the covariance matrix of .

3.3 Linear-restricted truncation estimator

For the linear-restricted VAR model in (16), the linear transformations of autocovariance matrices are defined as

| (36) |

Motivated by the element and vector-wise truncation in the previous subsections, in order to robustly estimate each element of , we apply the truncation to , where each is the -th column of . When each is highly sparse, e.g., is an coordinate vector for the banded VAR in Example 3, the vector is also highly sparse. In this case,let be the non-zero index set of , and and be the sub-vectors. It is obvious to check that and , for .

Therefore, we consider the vector-wise truncation and , and the elements of and can be estimated by the linear-restricted truncated data

| (37) |

for .

Remark 7.

For the special matrix whose columns are coordinate vectors corresponding to the non-zero entries in , the linear-restricted estimators with are equivalent to the linear transformations of element truncation estimators, namely and .

For the linear-restricted models, we consider the following moment conditions.

Assumption 5.

For , and .

The moment conditions in Assumption 5 can be viewed as an extension of the element-wise moment condition in Assumption 2. In addition, due to the normalization of the matrix , the moment bounds and are allowed to vary with the dimension . More discussions on the moment bounds are presented below for each specific linear-restricted model. For the linear-restricted model in (16) with , the general results of the autocovariance estimators are given as follows.

This proposition presents the estimation upper bounds for and in the norm. Following this proposition, we first consider the banded VAR model with the bandwidth in Example 3, denote by and the linear-restricted constrained Yule–Walker estimators with robust autocovariance estimators and . Note that as each is a coordinate vector, both and are 1-dimensional, and the Assumption 5 reduces to the element-wise moment bound in Assumption 2. The following estimation upper bounds can be derived.

Theorem 3 (Banded VAR upper bounds).

When and are fixed, the upper bounds in this theorem imply that asymptotically the rates of convergence in the operator norm and Frobenius norm scale as and , respectively. In other words, the sample size requirement in the operator norm is . When , our results are comparable and consistent with those in Guo et al., (2016) up to a logarithm factor. However, in Guo et al., (2016), they imposed the i.i.d. condition and sub-exponential tail condition for when . Hence, under high-dimensional scaling, both the operator norm and Frobenius norm convergence rates of the robust constrained Yule–Walker estimator for heavy-tailed data with a bounded fourth moment are almost the same as those of the standard ordinary least squares under the sub-exponential tail condition. In sum, the convergence rates obtained under the sub-exponential distribution can be achieved by the robust estimator under a much relaxed fourth moment condition, and we also establish the estimation consistency and the rates of convergence under the -th moment condition.

Remark 8.

The stationarity of the VAR(1) model requires that the largest eigenvalue of in terms of absolute value is strictly smaller than one, and hence the absolute value of is expected to be bounded. As and the columns of are all coordinate vectors, is bounded by , and the boundedness of has been discussed in Remark 3.

Next, we consider another case of the linear-restricted VAR models, the network VAR model in Example 4. In this model, is a -by-2 matrix with and being the restrictions associated with the nodal effect and network effect, respectively. Accordingly, . As needs to be normalized fro identification purpose, we assume that the unscaled parameters, and are constants independent of . In addition, we assume that each node in the network is only connected to a fixed number of nodes, so the network adjacency matrix satisfies .

According to the linear restriction matrix of the network VAR model, it can be verified that , , and . Hence, if which is independent of , then, . For the network VAR model, denote by the constrained Yule–Walker estimator with the constraint parameter and the autocovariance estimators and . The estimation upper bounds of the network VAR model can be derived as follows.

Theorem 4 (Network VAR upper bounds).

The upper bounds in this theorem are new for the network VAR model under the non-asymptotic scheme. Due to the normalization for the linear restriction matrix , both the true value and estimated value will diverge at a rate of as the dimension increases to infinity. Hence, the rate of convergence for the normalized coefficients scales as , independent of the dimension , and our result with is comparable to that obtained under the sub-Gaussian condition in Zheng and Cheng, (2021). The convergence rates under a bounded -th moment condition are established under a phase transition pattern.

4 Minimax Lower Bounds

In this section, we investigate theoretical properties on the lower bounds of estimation tasks for heavy-tailed high-dimensional time series data, including estimation of the high-dimensional VAR models and the autocovariance matrices. The lower bound analysis shows that the rates of convergence obtained in Section 3 are optimal in the minimax sense: there exists a distributional setting for the time series process for which the upper bounds obtained cannot be improved without further distributional assumptions.

4.1 Lower bounds of VAR estimation

Similarly to the upper bound analysis, no assumption on the data generating mechanism is imposed on the time series data in the lower bound analysis. We consider the VAR() model and denote the distribution of as . By the Yule–Walker equation, the true value of the VAR model coefficient matrix is defined as , where and .

The first case we consider is the sparse VAR model, where all row vectors of are strictly sparse. For any , and , let denote the class of all joint distributions for the -mixing stochastic process with the element-wise moment condition, such that they satisfy and for any integer and lag order . The moment parameter is imposed on the element of , which is consistent with Assumption 2.

For belonging to the sparse set defined in Section 3.1 and the process following the distribution , we have the minimax lower bound for the VAR estimation.

Theorem 5 (Sparse VAR lower bound).

For any , and , suppose that and the joint distribution of belongs to . Then, for any estimator which depends on the observations from to ,

| (44) |

The minimax lower bound in this theorem matches the upper bound in Theorem 1 with up to a logarithm factor that is negligible compared with . Hence, for the strictly sparse VAR model, the constrained Yule–Walker estimator introduced in Section 3.1 is nearly rate-optimal when the regularization parameter and truncation parameter are properly chosen. In addition, the effective sample size in the lower bound is , where the factor can be referred to as the price paid for the serial dependency in the data.

Moreover, it is clear that the banded VAR model with the bandwidth is a special case of the strictly sparse VAR model with the sparsity level . When is fixed, Theorem 5 directly implies that the minimax lower bound of the banded VAR model is of rate in the operator norm, matching the upper bound of the banded VAR in Theorem 3.

The second case considered is the reduced-rank VAR model where is of low rank. For any , and , let denote the class of all joint distributions for the -mixing stochastic process with the vector-wise moment condition, such that and for any integer and lag order . The moment condition defined on the whole vector is similar to Assumption 3 for the reduced-rank VAR model, but the technical term is omitted in the lower bound analysis.

For belonging to the low-rank set defined in Section 3.2 and the process following the distribution , the lower bound in terms of Frobenius norm is derived.

Theorem 6 (Reduced-rank VAR lower bound).

For any , and , suppose that , , and the joint distribution of belongs to . Then, for any estimator which depends on the observations from to ,

| (45) |

This theorem presents the minimax lower bound of the reduced-rank VAR model with the exact low-rankness in terms of Frobenius norm, which matches the upper bound in Theorem 2 up to a logarithm factor.

Remark 9.

The minimax lower bounds in Theorems 5 and 6 are developed for the VAR models with an exact low-dimensional structure, such as the strict row-wise sparsity and exact low-rankness. The lower bounds for the high-dimensional regression and covariance estimation with the weakly sparse coefficients have been investigated by Raskutti et al., (2011), Cai and Zhou, (2012), and others under the ball constraints. However, the theoretical techniques in their proofs rely heavily on the Gaussian distributional assumption, and hence cannot be applied to the heavy-tailed setting. The minimax lower bounds for the VAR estimation under the weak sparsity and approximate low-rankness are left for future research.

4.2 Lower bounds of autocovariance estimation

For any process following distribution , let , and a by-product of our lower bound analysis is the minimax lower bounds for the autocovariance estimation. First, we develop the minimax lower bounds in the norm for estimating the autocovariance matrices and .

Proposition 7.

For any , and , suppose that the joint distribution of belongs to . Then, for any covariance estimator which depends on the observations from to ,

| (46) |

The minimax lower bound matches the upper bounds in Proposition 4 up to a logarithmic factor , indicating the nearly minimax optimality of the proposed shrinkage estimator with chosen properly. Compared with the upper and lower bounds of the covariance matrix estimation for the i.i.d. data in Avella-Medina et al., (2018) and Devroye et al., (2016), our minimax lower bound involves a factor , which is due to the weak serial dependency under the geometrically decayed -mixing condition. It is also noteworthy that the factor can also be found in the upper bound analysis in Zhang, (2021) under the functional dependence measures (Wu,, 2005).

In addition, this minimax lower bound can easily be extended to the linear transformations of autocovariance matrices and , where consists of coordinate vector columns. In other words, Proposition 7 implies that the upper bounds in Proposition 6 are rate-optimal up to a logarithm factor.

Moreover, the minimax lower bound in the operator norm is also established.

Proposition 8.

For any , and , suppose that , , and the joint distribution of belongs to . Then, for any covariance estimator which depends on the observations from to ,

| (47) |

This lower bound matches the upper bound in Proposition 5 up to a logarithm factor , indicating that the vector-wise truncated estimators introduced in Section 3.2 are nearly rate-optimal when is chosen properly.

Remark 10.

To the best of our knowledge, for covariance or autocovaraince estimation problems, the minimax lower bound in Proposition 8 is the first operator norm lower bound result with the phase transition phenomenon. This lower bound is sharper than that in Fan et al., (2021) by constructing a special multivariate discrete distribution with the -th moment condition; see Appendix B for details.

5 Algorithm and Implementation

5.1 Linearized ADMM algorithm

The constrained Yule–Walker estimators in (6), (12) and (19) are convex optimization problems as each of them consists of a convex objective function and a convex constraint function. For the constrained problem in (6), define the constraint set and the optimization problem can be rewritten as

| (48) |

The augmented Lagrangian form is given as

| (49) |

subject to , where is the Lagrangian multiplier and is the regularization parameter. The augmented Lagrangian form can be solved by the alternating direction method of multipliers (Boyd et al.,, 2011, ADMM) with the iterative updates of :

| (50) |

The efficiency of the ADMM algorithm depends largely on the complexity of the resulting subproblems. Note that -update in the ADMM algorithm is a regularized least squares problem of , which might not have an explicit solution and can be computationally expensive.

To alleviate the computational burden in -update, we use an inexact proximal method to minimize

| (51) |

where is another prespecified parameter. As in Wang and Yuan, (2012), can be viewed as a linearized approximation of .

For the separated constrained Yule–Walker estimation in (12), the linearized ADMM algorithm can be developed in similar fashion. For the norm and nuclear norm regularized estimators, in -update and the proximal variant of -update, the soft-thresholding operator and truncation operator can be applied to the elements and singular values, respectively. The proposed ADMM algorithm can be illustrated as a particular application of the inexact Bregman ADMM algorithm (Wang and Banerjee,, 2014). To guarantee the global convergence, needs to be greater than the largest eigenvalue of .

In summary, the ADMM algorithm has explicit updates and can be solved efficiently. The details of the linearized ADMM algorithm for sparse and reduced-rank VAR models are presented in Appendix C.

5.2 Linear and semidefinite programmings

Some specific cases of the constrained Yule–Walker estimator in (6) can be formulated as linear programmings (LP) or semidefinite programs (SDP), and can thus be efficiently solved by any of the standard LP or SDP solvers.

As discussed in Example 2, for sparse VAR models, a separated constrained minimization framework in (12) is proposed with and . Following the lead of Dantzig selector (Candès and Tao,, 2007), each of the sub-problems can be recast to an LP:

| (52) |

where the optimization variables are and . As discussed in Candès and Tao, (2007), there is a large class of efficient algorithms for solving such problems.

Similarly, the constrained Yule–Walker estimator in (6), with and , can be used to estimate the reduced-rank VAR models. As introduced by Candès and Plan, (2011), the nuclear norm minimization problem can be recast to a SDP with a linear matrix inequality constraint:

| (53) |

with optimization variables , , and . Interior point methods or first-order methods, such as splitting cone solver, can be applied to efficiently solve large-scale SDP.

For linear-restricted VAR models, the optimization problem of the constrained Yule–Walker estimator in (19) can also be formulated as a LP:

| (54) |

with optimization variables and , and can be solved by standard LP solvers.

As the data truncation and robust autocovariance estimator calculation are computationally cheap, the operation time of ADMM, LP and SDP algorithms mainly depends on the dimension and AR order . As shown in the simulation experiments in Section 6, the proposed ADMM algorithm is much more efficient than the LP and SDP solvers, especially when is large.

5.3 Tuning parameter selection

For the constrained Yule–Walker estimators, both the robustification parameter(s) (or and ) and constraint parameter need to adapt properly to the dimension , sample size and moment condition bound to achieve optimal trade-off between the truncation bias and tail robustness. However, based on the conditions and convergence rates in Section 3, the optimal value of both parameters rely on some unknown parameters and . In the literature on robust estimation of i.i.d. data, cross-validation is an intuitive data-driven method to select robustification and regularization parameters. To accommodate the intrinsically ordered nature of time series data, we use a rolling forecasting validation, one of the standard approaches to tuning parameter selection for time series data.

To simultaneously select robustification and constraint parameters, a two-dimensional or multidimensional grid of tuning parameters is constructed. The search of the constraint parameter starts from a predetermined and decreases in log-linear increments. For the robustification parameter , grid search on the data-driven interval is suggested, where and are empirical quantiles of the data. For instance, to tune for the element truncation estimators, we may set and to be the median and maximum of , for all and , respectively. If at least one of and is very large, we may calculate the quantiles of some randomly sampled .

For the dataset with time series observations from to , we determine a validation period whose length is supposed to be slightly smaller than . Given the constraint and robustification parameters , at any time point , we use all the historical data to calculate the constrained Yule–Walker estimates and the corresponding one-step-ahead forecast . The performance evaluation is based on the mean squared forecast error (MSFE)

| (55) |

and the tuning parameters are selected by minimizing the over the grid points.

6 Simulation Study

6.1 VAR estimation

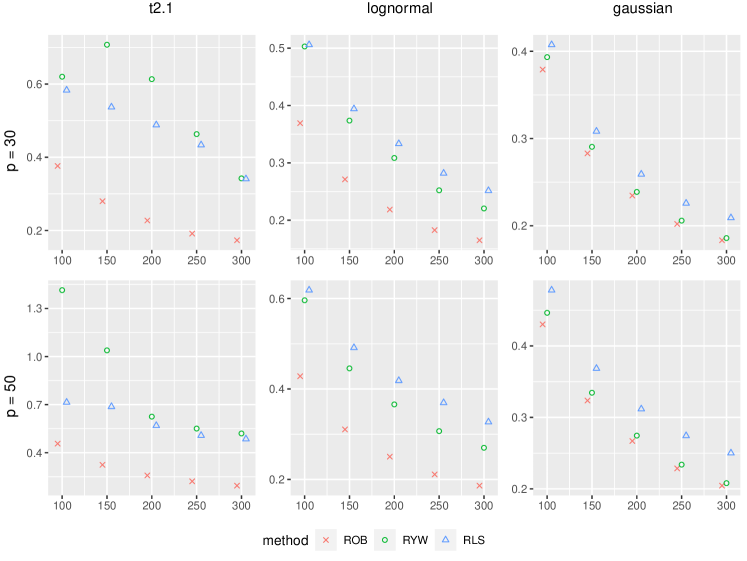

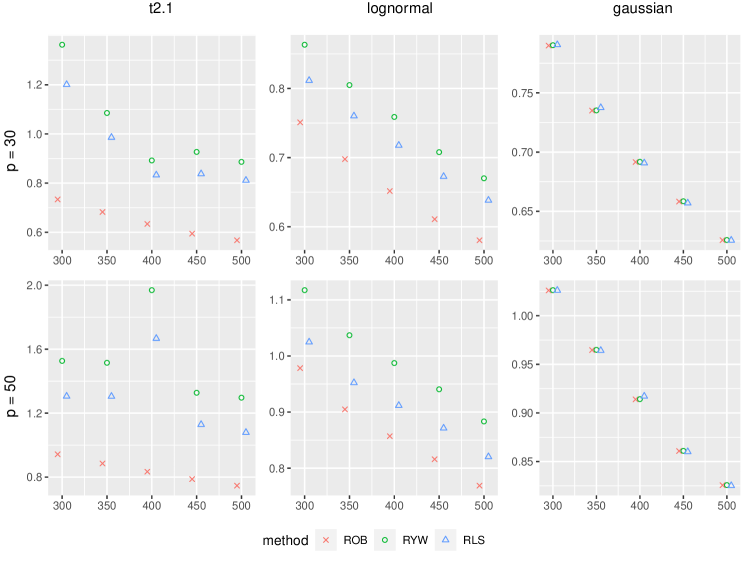

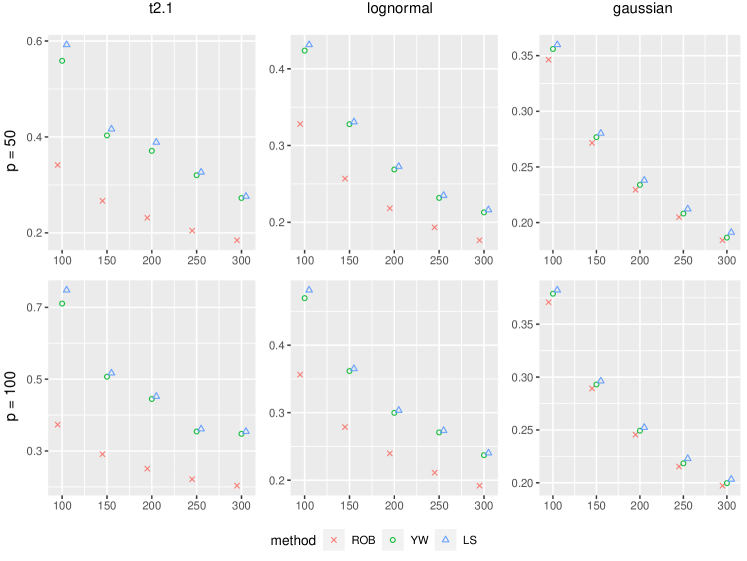

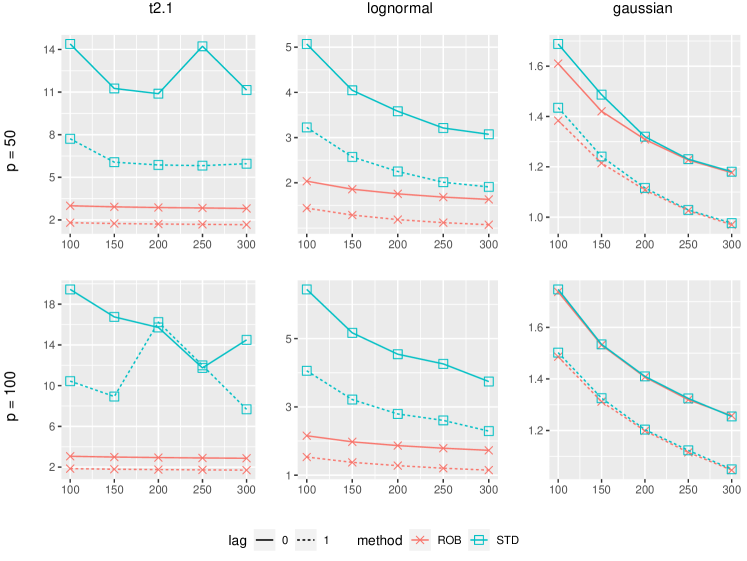

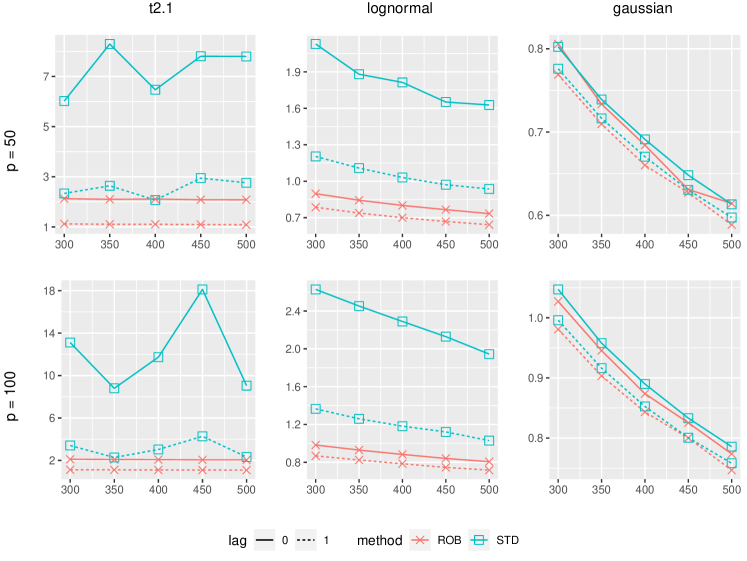

In this subsection, we compare the performance of the robust procedure and two standard estimation procedures for sparse, reduced-rank, and banded VAR models in finite samples. For each model, we consider three innovation settings: standardized -distributed innovations, standardized log-normal innovations, and standard Gaussian innovations. They represent heavy-tailed symmetric distributions with finite second moments, heavy-tailed asymmetric distributions with finite fourth moments, and light-tailed symmetric distribution, respectively. The data are drawn from the VAR(1) process with the following structures of .

DGP-1: Sparse VAR with specified as if , if , if , and otherwise. We consider and .

DGP-2: Reduced-rank VAR with having a low-rank singular value decomposition . Specifically, we consider a fixed , and generate random orthonormal and from the first two leading singular vectors of a random -by- Gaussian matrix. We consider and .

DGP-3: Banded VAR with a banded having bandwidth . Specifically, if ; if ; if ; if ; and for all . We consider and .

We first specify the robust estimation procedure, denoted as ROB, for these three DGPs. For DGP-1, as discussed in Example 2, we apply the split estimation method in (12) with , , and the element-wise truncation autocovariance estimators and specified in Section 3.1. For DGP-2, as discussed in Example 1, we apply the estimation method in (6) with , , and the vector-wise truncation autocovariance estimators and specified in Section 3.2. For DGP-3, as discussed in Example 3, we apply the estimation method in (19) with the element-wise truncation autocovariance estimators and in Section 3.3. The tuning parameters and are selected simultaneously by the MSFE in Section 5.3.

Alternatively, if the possibility of heavy-tailed distribution is ignored, we consider the sample autocovariance estimators

| (56) |

and plug them in the Yule–Walker estimators. We denote this estimation procedure as the regular Yule–Walker (RYW) method. In the high-dimensional VAR literature, another popular estimation procedure is the regularized least squares (RLS) method. For DGP-1 and 2, we apply the regularized method

| (57) |

with and , respectively. For DGP-3, we consider the least squares (LS) estimator

| (58) |

To evaluate the estimation performance and to confirm the theoretical results in Theorems 1-3, for , we calculate the norm for sparse VAR models, the Frobenius norm for reduced-rank VAR models, and the operator norm and norm for banded VAR models. For the three DGPs, the estimation errors are calculated by averaging 500 replications for each setting and presented in Figures 1, 2 and 3, respectively.

For the three types of VAR models considered, we can observe from Figures 1-3 that the proposed robust estimation method yields much small statistical errors than both standard estimation methods under the heavy-tailed innovations, i.e. the standardized distributed innovation and log-normal innovation. In particular, under the innovation setting, the estimation performance of both standard estimation methods is not stable. Under the setting of Gaussian innovation, the proposed robust estimator produces almost the same or even slightly smaller estimation errors than the standard methods, indicating that it does not hurt to use the robust procedure under the light-tailed innovation setting. In sum, the simulation results generally confirm the theoretical convergence rates and demonstrate the robustness of the proposed estimators against heavy-tailed distributions.

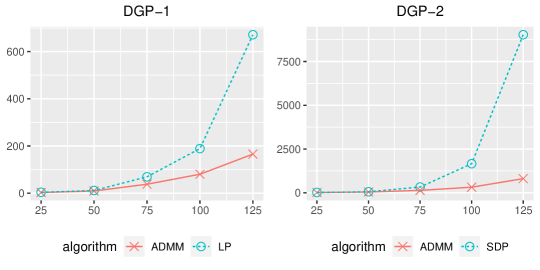

We also compare the performance of two computational algorithms discussed in Section 5, using the simulated data with a fixed and varying dimension from the Gaussian settings of DGP-1 and 2, respectively. We obtain almost identical estimates from the two algorithms under the same choices of and . Regarding computational time, we record the averaged time consumed over 100 replications for each algorithm. Figure 4 demonstrates that the ADMM is much more efficient than the LP and SDP solvers, especially when the dimension is large.

6.2 Autocovariance matrix estimation

We also conduct a simulation experiment to compare the truncation-based autocovariance matrix estimator with the standard sample autocovariance estimator. Two data generating processes, DGP-1 and DGP-2 in Subsection 6.1, are employed. Similarly to the previous experiment, we also consider three innovation settings for each DGP. The element and vector truncation estimators are considered for these two processes. Based on 1000 replications, the average estimation errors of autocovariance matrices in terms of and operator norms are presented in Figures 5 and 6 for the two processes, respectively.

For these two DGPs, the truncation-based autocovariance matrix estimators yield much smaller estimation errors than the sample autocovariance estimator under the heavy-tailed innovation settings. Similarly to the previous experiment, under the innovation setting, the performance of the sample autocovariance estimator is not stable, but the smoothly decreasing pattern of the proposed robust estimator can be observed. Under the Gaussian innovation setting, the performance of both estimators are nearly the same. The numerical results in this experiment confirm the rates of convergence in Propositions 4 and 5 and verify the robustness of the proposed autocovariance estimators.

7 Real Data Example

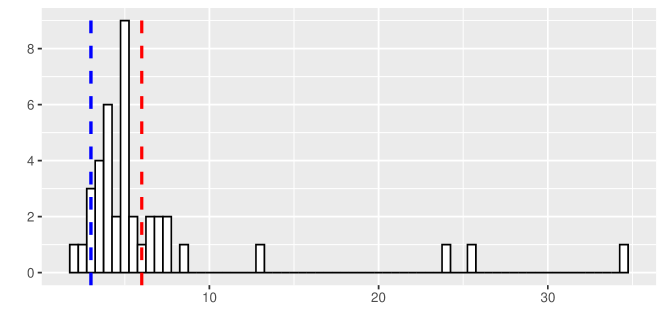

In this section, we apply the proposed robust estimation procedure to a real data set consisting of 40 quarterly macroeconomic variables of the United States from the third quarter of 1959 to fourth quarter of 2007, with 194 observations for each variable. Following Stock and Watson, (2009), all variables are seasonally adjusted except for financial variables, transformed by differencing or log differencing to be stationary, and standardized to zero mean and unit standard deviation. These macroeconomic variables capture many aspects of the U.S. economy, including GDP, National Association of Purchasing Manager indices, industrial production, pricing, employment, credit and interest rate. Both factor model and VAR model have been applied to these series in empirical econometric analyses for structural analysis and forecasting; see Stock and Watson, (2009), Koop, (2013) and Wang et al., 2021a . The kurtosis of the standardized variables are plotted in Figure 7, with the blue and red dashed lines indicating the kurtosis of normal distribution and distribution, respectively. Among 40 variables, 36 and 11 variables have larger kurtosis than standard normal distribution and distribution, providing some evidence of the existence of heavy-tailed distributions in this macroeconomic dataset.

Following Koop, (2013), we apply a VAR(4) model to these macroeconomic time series. If no structural assumption is imposed on the parameter matrix, we can directly use the ordinary least squares estimator by minimizing the least squares loss function, namely

| (59) |

where . If the low-rank structure on is considered and the rank is pre-specified, the rank-constrained least squares estimator is formulated as

| (60) |

As shown in Section 6, if the low-rank structure is not directly imposed, we can use the nuclear norm regularized least squares (NN-RLS), nuclear norm regularized Yule–Walker (NN-RYW), and the proposed nuclear norm robust (NN-ROB) methods. For the sparse VAR model, the regularized least squares (L1-RLS), regularized Yule–Walker (L1-RYW), and robust (L1-ROB) methods can be applied as discussed in Section 6.

The performance of these eight methods are compared via out-of-sample forecasting errors. From the first quarter of 1993 () to the fourth quarter 2007 (), we fit the VAR model by different methods utilizing all the historical data available until time and obtain the one-step-head forecast . Then, we calculate the rolling forecasting errors in the and norms, respectively, and summarized the their means and medians in Table 1.

| Model | Full | Sparse | Reduced-rank | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Method | OLS | L1-RLS | L1-RYW | L1-ROB | RRR | NN-RLS | NN-RYW | NN-ROB | |

| mean of | 22.63 | 5.64 | 5.82 | 4.17 | 19.67 | 8.82 | 8.91 | 6.52 | |

| median of | 14.57 | 5.21 | 5.20 | 3.81 | 9.62 | 5.39 | 5.34 | 3.97 | |

| mean of | 9.29 | 2.16 | 2.42 | 1.66 | 6.42 | 3.44 | 3.27 | 2.49 | |

| median of | 6.42 | 1.96 | 2.01 | 1.43 | 3.06 | 2.16 | 2.09 | 1.80 | |

As shown in Table 1, the OLS estimator produces the largest out-of-sample prediction errors as the full VAR(4) model is highly over-parameterized, while low-dimensional and sparse structure can alleviate the problem of overfitting and significantly improve the forecasting performance. Both L1-ROB and NN-ROB estimators have smaller out-of-sample forecasting errors than their standard counterparts, indicating the necessity of robust estimation for large-scale time series data and the satisfactory performance of the proposed methodology. The L1-ROB estimator performs best among all estimators as it produces a parsimonious sparse parameter matrix and prevents overfitting effectively.

References

- Avella-Medina et al., (2018) Avella-Medina, M., Battey, H. S., Fan, J., and Li, Q. (2018). Robust estimation of high-dimensional covariance and precision matrices. Biometrika, 105:271–284.

- Banna et al., (2016) Banna, M., Merlevède, F., and Youssef, P. (2016). Bernstein-type inequality for a class of dependent random matrices. Random Matrices: Theory and Applications, 5:1650006.

- Basu et al., (2019) Basu, S., Li, X., and Michailidis, G. (2019). Low rank and structured modeling of high-dimensional vector autoregressions. IEEE Transactions on Signal Processing, 67:1207–1222.

- Basu and Michailidis, (2015) Basu, S. and Michailidis, G. (2015). Regularized estimation in sparse high-dimensional time series modevls. Annals of Statistics, 43:1535–1567.

- Belloni and Chernozhukov, (2011) Belloni, A. and Chernozhukov, V. (2011). -penalized quantile regression in high-dimensional sparse models. Annals of Statistics, 39:82–130.

- Bollerslev, (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31:307–327.

- Boyd et al., (2011) Boyd, S., Parikh, N., Chu, E., Peleato, B., and Eckstein, J. (2011). Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine learning, 3:1–122.

- Bubeck et al., (2013) Bubeck, S., Cesa-Bianchi, N., and Lugosi, G. (2013). Bandits with heavy tail. IEEE Transactions on Information Theory, 59:7711–7717.

- Cai et al., (2011) Cai, T., Liu, W., and Luo, X. (2011). A constrained minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association, 106:594–607.

- Cai and Zhou, (2012) Cai, T. T. and Zhou, H. H. (2012). Optimal rates of convergence for sparse covariance matrix estimation. Annals of Statistics, 40:2389–2420.

- Candès and Tao, (2007) Candès, E. and Tao, T. (2007). The dantzig selector: Statistical estimation when p is much larger than n. Annals of Statistics, 35:2313–2351.

- Candès and Plan, (2011) Candès, E. J. and Plan, Y. (2011). Tight oracle inequalities for low-rank matrix recovery from a minimal number of noisy random measurements. IEEE Transactions on Information Theory, 57:2342–2359.

- Catoni, (2012) Catoni, O. (2012). Challenging the empirical mean and empirical variance: a deviation study. Annales de l’IHP Probabilités et Statistiques, 48:1148–1185.

- Devroye et al., (2016) Devroye, L., Lerasle, M., Lugosi, G., and Oliveira, R. I. (2016). Sub-gaussian mean estimators. Annals of Statistics, 44:2695–2725.

- Doukhan, (1994) Doukhan, P. (1994). Mixing. In Mixing, pages 15–23. Springer.

- Engle, (1982) Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica, 50:987–1007.

- Fan et al., (2017) Fan, J., Li, Q., and Wang, Y. (2017). Estimation of high dimensional mean regression in the absence of symmetry and light tail assumptions. Journal of the Royal Statistical Society: Series B, 79:247–265.

- Fan et al., (2021) Fan, J., Wang, W., and Zhu, Z. (2021). A shrinkage principle for heavy-tailed data: High-dimensional robust low-rank matrix recovery. Annals of Statistics, 49:1239–1266.

- Fan and Yao, (2008) Fan, J. and Yao, Q. (2008). Nonlinear time series: nonparametric and parametric methods. Springer Science & Business Media.

- Gorrostieta et al., (2012) Gorrostieta, C., Ombao, H., Bédard, P., and Sanes, J. N. (2012). Investigating brain connectivity using mixed effects vector autoregressive models. NeuroImage, 59:3347–3355.

- Guo et al., (2016) Guo, S., Wang, Y., and Yao, Q. (2016). High-dimensional and banded vector autoregressions. Biometrika, 103:889–903.

- Hampel, (1971) Hampel, F. R. (1971). A general qualitative definition of robustness. The Annals of Mathematical Statistics, 42:1887–1896.

- Hampel, (1974) Hampel, F. R. (1974). The influence curve and its role in robust estimation. Journal of the American Statistical Association, 69:383–393.

- Hampel, (2001) Hampel, F. R. (2001). Robust statistics: A brief introduction and overview. In Research report/Seminar für Statistik, Eidgenössische Technische Hochschule (ETH), volume 94. Seminar für Statistik, Eidgenössische Technische Hochschule.

- Han et al., (2015) Han, F., Lu, H., and Liu, H. (2015). A direct estimation of high dimensional stationary vector autoregressions. Journal of Machine Learning Research, 16:3115–3150.

- Han et al., (2020) Han, Y., Tsay, R. S., and Wu, W. B. (2020). Robust estimation of high dimensional generalized linear models for temporal dependent data. Technical report.

- Huber, (1964) Huber, P. J. (1964). Robust estimation of a location parameter. The Annals of Mathematical Statistics, 35:73–101.

- Ke et al., (2019) Ke, Y., Minsker, S., Ren, Z., Sun, Q., and Zhou, W.-X. (2019). User-friendly covariance estimation for heavy-tailed distributions. Statistical Science, 34:454–471.

- Kock and Callot, (2015) Kock, A. B. and Callot, L. (2015). Oracle inequalities for high dimensional vector autoregressions. Journal of Econometrics, 186:325–344.

- Koop, (2013) Koop, G. M. (2013). Forecasting with medium and large bayesian vars. Journal of Applied Econometrics, 28:177–203.

- Liebscher, (2005) Liebscher, E. (2005). Towards a unified approach for proving geometric ergodicity and mixing properties of nonlinear autoregressive processes. Journal of Time Series Analysis, 26:669–689.

- Ling, (2004) Ling, S. (2004). Estimation and testing stationarity for double-autoregressive models. Journal of the Royal Statistical Society: Series B, 66:63–78.

- Loh, (2017) Loh, P.-L. (2017). Statistical consistency and asymptotic normality for high-dimensional robust M-estimators. Annals of Statistics, 45:866–896.

- Lütkepohl, (2005) Lütkepohl, H. (2005). New introduction to multiple time series analysis. Springer Science & Business Media.

- Martin, (1981) Martin, R. D. (1981). Robust methods for time series. In Applied time series analysis II, pages 683–759. Elsevier.

- Massart, (2007) Massart, P. (2007). Concentration inequalities and model selection: Ecole d’Eté de Probabilités de Saint-Flour XXXIII-2003. Springer.

- Michailidis and d’Alché Buc, (2013) Michailidis, G. and d’Alché Buc, F. (2013). Autoregressive models for gene regulatory network inference: Sparsity, stability and causality issues. Mathematical Biosciences, 246:326–334.

- Minsker, (2018) Minsker, S. (2018). Sub-gaussian estimators of the mean of a random matrix with heavy-tailed entries. Annals of Statistics, 46:2871–2903.

- Muler, (2013) Muler, N. (2013). Robust estimation for vector autoregressive models. Computational Statistics & Data Analysis, 65:68–79.

- Muler et al., (2009) Muler, N., Pena, D., and Yohai, V. J. (2009). Robust estimation for arma models. Annals of Statistics, 37:816–840.

- Negahban and Wainwright, (2011) Negahban, S. and Wainwright, M. J. (2011). Estimation of (near) low-rank matrices with noise and high-dimensional scaling. Annals of Statistics, 39:1069–1097.

- Negahban et al., (2012) Negahban, S. N., Ravikumar, P., Wainwright, M. J., and Yu, B. (2012). A unified framework for high-dimensional analysis of M-estimators with decomposable regularizers. Statistical Science, 27:538–557.

- Qiu et al., (2015) Qiu, H., Xu, S., Han, F., Liu, H., and Caffo, B. (2015). Robust estimation of transition matrices in high dimensional heavy-tailed vector autoregressive processes. In International Conference on Machine Learning, pages 1843–1851. PMLR.

- Raskutti et al., (2011) Raskutti, G., Wainwright, M. J., and Yu, B. (2011). Minimax rates of estimation for high-dimensional linear regression over -balls. IEEE Transactions on Information Theory, 57:6976–6994.

- Stock and Watson, (2009) Stock, J. H. and Watson, M. (2009). Forecasting in dynamic factor models subject to structural instability. The Methodology and Practice of Econometrics. A Festschrift in Honour of David F. Hendry, 173:205.

- Sun et al., (2020) Sun, Q., Zhou, W.-X., and Fan, J. (2020). Adaptive huber regression. Journal of the American Statistical Association, 115:254–265.

- Tan et al., (2022) Tan, K. M., Sun, Q., and Witten, D. (2022). Sparse reduced rank huber regression in high dimensions. Journal of the American Statistical Association. To appear.

- Tsay, (2013) Tsay, R. S. (2013). Multivariate time series analysis: with R and financial applications. John Wiley & Sons.

- Velu and Reinsel, (2013) Velu, R. and Reinsel, G. C. (2013). Multivariate reduced-rank regression: theory and applications, volume 136. Springer Science & Business Media.

- Wainwright, (2019) Wainwright, M. J. (2019). High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge University Press.

- (51) Wang, D., Lian, H., Zheng, Y., and Li, G. (2021a). High-dimensional vector autoregressive time series modeling via tensor decomposition. Journal of the American Statistical Association. To appear.

- (52) Wang, D., Zheng, Y., and Li, G. (2021b). High-dimensional low-rank tensor autoregressive time series modeling. arXiv preprint arXiv:2101.04276.

- Wang and Banerjee, (2014) Wang, H. and Banerjee, A. (2014). Bregman alternating direction method of multipliers. Advances in Neural Information Processing Systems, 4:2816–2824.

- Wang et al., (2007) Wang, H., Li, G., and Jiang, G. (2007). Robust regression shrinkage and consistent variable selection through the LAD-Lasso. Journal of Business & Economic Statistics, 25:347–355.

- Wang et al., (2020) Wang, L., Peng, B., Bradic, J., Li, R., and Wu, Y. (2020). A tuning-free robust and efficient approach to high-dimensional regression. Journal of the American Statistical Association, 115:1700–1714.

- Wang et al., (2012) Wang, L., Wu, Y., and Li, R. (2012). Quantile regression for analyzing heterogeneity in ultra-high dimension. Journal of the American Statistical Association, 107:214–222.

- Wang and Yuan, (2012) Wang, X. and Yuan, X. (2012). The linearized alternating direction method of multipliers for dantzig selector. SIAM Journal on Scientific Computing, 34:A2792–A2811.

- Wong et al., (2020) Wong, K. C., Li, Z., and Tewari, A. (2020). Lasso guarantees for -mixing heavy-tailed time series. Annals of Statistics, 48:1124–1142.

- Wu and Xia, (2016) Wu, J. C. and Xia, F. D. (2016). Measuring the macroeconomic impact of monetary policy at the zero lower bound. Journal of Money, Credit and Banking, 48:253–291.

- Wu, (2005) Wu, W. B. (2005). Nonlinear system theory: Another look at dependence. Proceedings of the National Academy of Sciences, 102:14150–14154.

- Wu and Wu, (2016) Wu, W.-B. and Wu, Y. N. (2016). Performance bounds for parameter estimates of high-dimensional linear models with correlated errors. Electronic Journal of Statistics, 10:352–379.

- Zhang, (2021) Zhang, D. (2021). Robust estimation of the mean and covariance matrix for high dimensional time series. Statistica Sinica, 31:797–820.

- Zheng and Raskutti, (2019) Zheng, L. and Raskutti, G. (2019). Testing for high-dimensional network parameters in auto-regressive models. Electronic Journal of Statistics, 13:4977–5043.

- Zheng and Cheng, (2021) Zheng, Y. and Cheng, G. (2021). Finite-time analysis of vector autoregressive models under linear restrictions. Biometrika, 108:469–489.

- Zhu et al., (2018) Zhu, Q., Zheng, Y., and Li, G. (2018). Linear double autoregression. Journal of Econometrics, 207:162–174.

- Zhu et al., (2017) Zhu, X., Pan, R., Li, G., Liu, Y., and Wang, H. (2017). Network vector autoregression. Annals of Statistics, 45:1096–1123.

Supplementary material for

“Rate-Optimal Robust Estimation of High-Dimensional Vector Autoregressive Models”

Di Wang and Ruey S. Tsay

Booth School of Business, University of Chicago

This supplementary material provides all technical proofs of the theoretical results in the main paper, some auxiliary lemmas, and details of the linearized ADMM algorithm. Specifically, Appendices A and B present the proofs of upper and lower bound results, respectively, and some related auxiliary lemmas. Appendix C shows the ADMM algorithms for the regularized sparse VAR model and the nuclear norm regularized reduced-rank VAR model.

Appendix A Proofs of Upper Bound Results

We present the proofs of the deterministic upper bounds (Propositions 1–3) in Section A.1, the error bounds of the robust autocovariance estimators (Propositions 4–6) in Section A.2, and the error bounds of the robust VAR estimators (Theorems 1–4) in Section A.3, respectively. The auxiliary lemmas are relegated to Section A.4.

We start with some notation used in the Appendix. Denote by the -dimensional sphere with unit radius in the Euclidean norm. For any symmetric matrix , let and be its largest and smallest eigenvalues.

A.1 Proof of Propositions 1–3

Proof of Proposition 1.

The general idea of the proof follows from that of Dantzig selector (Candès and Tao,, 2007) and constrained minimization estimation (Cai et al.,, 2011; Han et al.,, 2015).

By the conditions in Proposition 1, and . Let be the estimation error. We first show that the true value is a feasible solution to the optimization problem in (6). Note that as is convex,

| (61) |

where the first inequality follows from the triangle inequality, and the second inequality follows from the properties of and .

Therefore, is feasible in the optimization equation, and hence . Then, by the triangle inequality, we have

| (62) |

By the definitions of model subspace and perturbation subspace, we can decompose . Since is feasible with respect to the constraint, we have

| (63) |

where the last equality follows from the decomposability of .

Moreover, we have

| (64) |

where the first inequality follows from the triangle inequality and the second inequality follows from the decomposibility of and the triangle inequality. Thus, together with (63), we have .

Hence, the upper bound in terms of can be found as

| (65) |

Finally, by the duality between and , the upper bound in the squared Frobenius norm can be derived as

| (66) |

∎

Proof of Proposition 2.

The proof of Proposition 2 generally follows that of Proposition 1. Note that we have and . Let . We first show that the true value is a feasible solution to the optimization sub-problem in (12). Note that

| (67) |

Therefore, is feasible in the optimization equation, and . Then, by triangle inequality, we have

| (68) |