Capital Requirements and Claims Recovery:

A New Perspective on Solvency Regulation

Abstract

Protection of creditors is a key objective of financial regulation. Where the protection needs are high, i.e., in banking and insurance, regulatory solvency requirements are an instrument to prevent that creditors incur losses on their claims. The current regulatory requirements based on Value at Risk and Average Value at Risk limit the probability of default of financial institutions, but they fail to control the size of recovery on creditors’ claims in the case of default. We resolve this failure by developing a novel risk measure, Recovery Value at Risk. Our conceptual approach can flexibly be extended and allows the construction of general recovery risk measures for various risk management purposes. By design, these risk measures control recovery on creditors’ claims and integrate the protection needs of creditors into the incentive structure of the management.

We provide detailed case studies and applications: We analyze how recovery risk measures react to the joint distributions of assets and liabilities on firms’ balance sheets and compare the corresponding capital requirements with the current regulatory benchmarks based on Value at Risk and Average Value at Risk. We discuss how to calibrate recovery risk measures to historic regulatory standards. Finally, we show that recovery risk measures can be applied to performance-based management of business divisions of firms and that they allow for a tractable characterization of optimal tradeoffs between risk and return in the context of investment management.

Keywords: Risk Measures, Capital Requirements, Solvency Regulation, Recovery on Liabilities.

1 Introduction

Banks and insurance companies are subject to a variety of regulatory constraints. A key objective of financial regulation is the appropriate protection of creditors, e.g., depositors, policyholders, and other counterparties. Corporate governance, reporting, and transparency are cornerstones of regulatory schemes, but equally important is capital regulation. Financial companies are required to respect solvency capital requirements that define a minimum for their current net asset value. Firms that fail to meet these requirements are subject to supervisory interventions.

The computation of solvency capital requirements is often based on some pre-specified notion of acceptable default risk. Banks and insurance companies must hold enough capital to meet their obligations in a sufficient number of future economic scenarios. Regulators typically focus on quantities such as the change of net asset value over a specific time horizon — for example, one year — and require that a suitable risk measure applied to such quantities is below the current level of available capital. The risk measure implicitly defines a notion of acceptable default risk. Different risk measures are applied in practice.

The standard example are solvency capital requirements defined in terms of Value at Risk. In this case, a company is adequately capitalized if its default probability is lower than a given threshold. The upcoming regulatory framework for the internationally active insurance groups uses a Value at Risk at the level . In Europe, insurance companies and groups are subject to the same requirement under the Solvency II regime. Value at Risk has been strongly criticized due to its tail blindness and its lack of convexity – not encouraging diversification.

An alternative to Value at Risk is the coherent risk measure Average Value at Risk, also called Conditional or Tail Value at Risk or Expected Shortfall. The market risk standards in Basel III, the international regulatory framework for banks, and the Swiss Solvency Test, the Swiss regulatory framework for insurance companies, are both based on Average Value at Risk with levels and , respectively. In this case, a company or portfolio is deemed adequately capitalized, if it generates profits on average conditional on its tail distribution below the chosen level. Average Value at Risk is sensitive to the tail, and, being convex, it does not penalize diversification. It is also a tractable ingredient to optimization problems in the context of asset-liability-management and provides an instrument for decentralized risk management, e.g., limit systems within firms.

Despite all its merits, Average Value at Risk fails — just as Value at Risk — at one central task: It cannot control recovery in the case of default, i.e., the probabilities that creditors recover prespecified fractions of claims! This goal is, of course, important from a regulatory point of view. Recovering, say, 80% instead of 0% in the case of default makes a big difference to creditors such as depositors or policyholders. This failure is apparent when we consider Value at Risk. By design, the corresponding solvency tests only limit the probability of insolvency and are incapable of imposing any stricter bound on the loss given default.

But the same failure is shared by Average Value at Risk. In spite of being sensitive to tail losses, Average Value at Risk still leaves too many degrees of freedom to control recovery. This is because the loss given default is captured by way of an average loss, which is too gross to exert a fine control on the recovery probability. An additional key deficiency is that all monetary risk measures in current solvency regulation focus on a residual quantity, i.e., the difference between assets and liabilities, that is owned by shareholders. This quantity is insufficient to adequately capture what will happen in the case of default.

The goal of this paper is to address the question:

How should solvency tests be designed that control

the recovery on creditors’ claims in the case of default?

Our contributions are the following:

-

I.

We demonstrate that classical monetary risk measures such as Value at Risk and Average Value at Risk are unable to control recovery on creditors’ claims in the case of default. In fact, we argue that, to capture this important aspect of tail risk, one has to abandon solvency tests based on the net asset value only and consider more articulated solvency tests based on both the net asset value and the firm’s liabilities.

-

II.

A novel risk measure, Recovery Value at Risk, is developed in the paper that can successfully resolve the failure of the standard risk measures employed in solvency regulation. We demonstrate that Recovery Value at Risk can serve as the basis of solvency tests. It admits an operational interpretation as a capital requirement rule. This new risk measure can be applied to both external and internal risk management and helps to quantify how far standard regulatory risk measures are from controlling liability recovery risk.

-

III.

Our conceptual approach is flexible and leads to the construction of general recovery risk measures that include Recovery Average Value at Risk. This allows to integrate the ability to control the recovery on creditors’ claims with other desirable properties such as convexity or subadditivity. Convexity facilitates applications to optimization problems such as portfolio choice under risk constraints. Subadditivity provides incentives for the diversification of positions and enables limit systems within firms for decentralized risk management.

-

IV.

In order to better understand the behavior of recovery risk measures we illustrate how they react to changes of the joint distribution of the assets and the liabilities on the firm’s balance sheet. We focus on two characteristics – marginal distributions and stochastic dependence – and compare risk measurements to the classical solvency benchmarks, i.e., Value at Risk and Average Value at Risk.

-

V.

We discuss a possible strategy to calibrate recovery risk measures consistently with existing regulatory standards, following a common methodology chosen by regulators in the context of classical risk measures.

-

VI.

We demonstrate how recovery risk measures can be applied to performance-based management of business divisions of firms. We define and investigate the appropriate notion of RoRaC-compatibility.

-

VII.

Optimal tradeoffs between risk and return, as originally suggested by Harry Markowitz in the special case of the variance, may also be characterized for recovery risk measures. We show how efficient frontiers can be computed in this case.

The paper is structured as follows. Section 2 reviews solvency regulation based on Value at Risk and Average Value at Risk and reveals its failure to control recovery. Section 3 describes how to resolve this problem and develops the novel risk measure Recovery Value at Risk. Section 4 introduces a notion of general recovery risk measures that include the convex Recovery Average Value at Risk. Section 5 complements the conceptual innovations of this paper with detailed case studies and applications. These provide insights on how risk measures react to the shape of distributions and stochastic dependence. We also discuss calibration issues that arise when solvency regimes are modified. In order to show the wide spectrum of applicability of recovery risk measures in practice, we discuss risk allocation in the context of decentralized risk and performance management of firms and portfolio optimization under risk constraints. Proofs and further technical supplements are collected in the appendix.

Literature

Solvency capital requirements impose constraints on the operations of businesses such as bank and insurance companies. Their purpose is to protect creditors from excessive downside risk. Capital requirements are an integral part of broader regulatory frameworks that allow companies to freely operate within pre-specified legal boundaries. Historically, regulatory deliberations like Basel I and Solvency I formulated simple rules. However, these could be exploited by regulatory arbitrage, see, e.g., \citeasnounBaselI, \citeasnounSolvencyIb, \citeasnounSolvencyIa, and \citeasnounJones. Regulatory frameworks have been modified multiple times during the past decades, but – as we will demonstrate in this paper – serious problems remain.

A key issue is how to define the required solvency capital in an appropriate manner. Basel II, Solvency II, and the upcoming international Insurance Capital Standard compute solvency capital on the basis of Value at Risk, while Basel III and the Swiss Solvency Test use Average Value at Risk. The risk measure Value at Risk has been criticized in the context of solvency regulation since the 1990s, in particular due to its tail blindness and lack of convexity. Alternatives are provided by the axiomatic theory of risk measures — initiated in a seminal paper by \citeasnounADEH99 — that systematically analyzes properties of risk measures, implications, and examples. The notion of coherent risk measure is introduced in \citeasnounADEH99 and is generalized to the class of convex risk measures in \citeasnounfrittelli2002 and \citeasnounFS02. Key developments are discussed in the monograph \citeasnounFS and the surveys \citeasnounFSW09 and \citeasnounFW15. The coherence of Average Value at Risk is first established in \citeasnounacerbi2002coherence. We refer to \citeasnounwang2020axiomatic for a recent axiomatic characterization of Average Value at Risk.

Monetary risk measures are based on the notion of acceptability. While preferences rank distributions, random variables, or processes, acceptance sets divide this universe into acceptable objects and those that are not acceptable. Monetary risk measures are numerical representations of acceptance sets and parallel in this respect utility functionals that represent preferences. Within the theory of choice, risk measures provide a model of guard rails for the actions of financial firms. At the same time, they possess an operational interpretation as capital requirement rules, measuring the distance from acceptability in terms of cash or, more generally, eligible assets. We refer to \citeasnounFS for a broad discussion on these aspects and to \citeasnounfilipovic2008optimal, \citeasnounadk2009, \citeasnounfarkas2014beyond, \citeasnounFRW17, and \citeasnounBFFM19 for specific applications to capital adequacy, hedging, risk sharing, and systemic risk. Our paper follows the same approach, i.e., taking the notion of acceptability as the starting point when formalizing recovery-based solvency tests. A different approach is pursued by the literature on acceptability indices that mainly focus on performance measurement, see \citeasnounaumann2008economic, \citeasnouncherny2009, \citeasnounfoster2009operational, \citeasnounbrown2012aspirational, \citeasnoundrapeau2013risk, \citeasnoungianin2013acceptability, \citeasnounbielecki2014dynamic.555Parametric families of Value at Risk were previously studied in this literature. But acceptability indices are applied to fixed univariate positions (modelling net asset values). In our case, a parametric family of Value at Risk or different risk measures are applied to bivariate positions (modelling net asset values jointly with liabilities). As a consequence, the formal construction of acceptability and their financial interpretation differs substantially from our approach. A related concept is also the notion of Loss Value at Risk introduced by \citeasnounbignozzi2020risk.

Monetary risk measures have natural applications to risk allocation and portfolio optimization problems. Risk allocation in the context of decentralized risk and performance management of firms has been widely investigated, e.g., in \citeasnountasche1999risk, \citeasnounkalkbrener2005axiomatic, \citeasnountasche2007capital, \citeasnoundhaene2012optimal, \citeasnounbauer2013capital, \citeasnounbauer2016marginal, \citeasnounembrechts2018quantile, \citeasnounweber_solvency2017, \citeasnounHaKnWe20, and \citeasnounbauer2020. Portfolio optimization under risk constraints with a characterization of efficient frontiers goes back to the classical approach in \citeasnounMarkowitz52. In the context of Average Value at Risk, the solution to this problem was developed in \citeasnounRU00 and \citeasnounRU02. The methodology relies on a representation of Average Value at Risk that is closely related to optimized certainty equivalents, which are discussed in \citeasnounBT87 and \citeasnounBT07. Applications to robust portfolio management are studied, e.g., in \citeasnounZhuFu09. We complement this previous work by discussing how efficient frontiers can be characterized for risk constraints in terms of recovery-based risk measures.

To the best of our knowledge, this paper is the first to introduce and study solvency capital requirements that are designed to control the recovery on creditors’ claims. The literature on recovery rates has historically focused on explaining the determinants of recovery rates in specific settings, e.g., for corporate and government bonds or bank loans. We refer to \citeasnounduffie1999modeling, \citeasnounaltman2005link, and \citeasnounguo2009modeling for a presentation of different models for recovery rates and to \citeasnounkhieu2012determinants, \citeasnounjankowitsch2014determinants, and \citeasnounivashina2016ownership for some recent empirical investigations.

2 Solvency Regulation and Claims Recovery

The protection of creditors is a key goal of capital regulation. To achieve this goal, financial institutions are required to hold a certain amount of capital as a buffer against future losses. The regulatory capital is chosen such that it ensures an acceptable level of safety against the risk of default. The standard rules used in practice to compute solvency capital requirements are based on risk measures such as Value at Risk or Average Value at Risk. We demonstrate that these rules are insufficient to provide a satisfactory control on the recovery on creditors’ claims and suggest an alternative approach that achieves this goal.

2.1 Risk-Sensitive Solvency Regimes

Most existing regulatory frameworks share a “balance sheet approach” to determine capital requirements. The random evolution of assets and liabilities of a financial institution is captured at time horizons specified by regulators, typically one year.666A balance sheet approach requires an internal model of the stochastic evolution of the balance sheet of the financial firm or insurance company that is subject to capital regulation. Many firms do not have sufficient capacities and expertise to implement and analyze such models. For this reason, in practice, simplifications are admissible which may substantially deviate from the original objectives of the regulator. Examples are the standard approach in the Insurance Capital Standard or the standard formula in Solvency II. The following table displays a stylized balance sheet of a company at a generic time :

| Assets | Liabilities |

|---|---|

The quantity represents the net asset value of the firm and can be either positive or negative depending on whether the asset value is larger than the liability value or not. In the typical setting of a one-year horizon we have two reference dates, which are denoted by (today) and (end of the year). The quantities at time are known whereas the quantities at time are random variables on a given probability space . In a risk-sensitive solvency framework, a company is deemed adequately capitalized if its available capital is larger than a suitable solvency capital requirement that reflects the inherent risk in the evolution of the balance sheet. This is typically captured by applying a suitable risk measure to the net asset value variation .777In practice, solvency capital requirements may only refer to “unexpected” losses. In this case, is replaced by the expected value of (the suitably discounted) . In this respect, the European regulatory framework for insurance companies Solvency II is contradictory in itself. We refer to \citeasnounHaKnWe20 for a detailed discussion. The corresponding solvency test is formally defined by:888For simplicity, we assume in this paper that interest rates over the one-year horizon are approximately zero. For adjustments on the definition of the solvency tests if interest rates are not zero see \citeasnounchristiansen2014.

| (1) |

If is a monetary risk measure such as Value at Risk or Average Value at Risk, condition (1) can be equivalently expressed in terms of the future net asset value only as

| (2) |

The standard risk measures are Value at Risk () and Average Value at Risk () at some pre-specified level :

where is some random variable.999Throughout the paper we apply the following sign convention: Positive values of represents a profit or a positive balance, negative values of represent a loss or a negative balance. In particular, the risk measure corresponds to a quantile of the underlying probability distribution.

In insurance regulation, at level is used in the Insurance Capital Standard and in Solvency II while at level is adopted in the Swiss Solvency Test. In banking regulation, with level has recently become the reference risk measure in Basel III, where it replaces at level . In a setting, the solvency test (2) can equivalently be reformulated as

| (3) |

This shows that a company is adequately capitalized under if it is able to maintain its default probability below a certain level. Similarly, in an setting, we can equivalently rewrite the solvency test (2) as101010The second equivalence holds provided the cumulative distribution function of is, e.g., continuous.

| (4) |

Hence, a company is adequately capitalized under if on the lower tail beyond the -quantile it is solvent on average. In this case, we automatically have . In other words, if we fix the same probability level , capital adequacy under is more conservative than capital adequacy under .

It is often stressed that — in contrast to — is a tail-sensitive risk measure and, hence, captures tail risk in a more comprehensive way. In fact, is completely blind to the tail of the reference loss distribution beyond a certain quantile level. While this is correct, one should bear in mind that captures tail risk in a specific way, namely via expected losses in the tail, thereby leaving many degrees of freedom to the behavior of the tail distribution.

2.2 Claims Recovery Under and

The point of departure of our contribution is to highlight that risk measures such as and fail to provide a direct control on a fundamental aspect of tail risk, namely the recovery on creditors’ claims. The basic problem is that both risk measures are functions of the net asset value only. The net asset value summarizes the financial resources of the equity holders without any reference to leverage, i.e., without imposing any direct constraints on the liabilities . However, controlling the recovery on claims requires to deal explicitly with .

This failure is documented by the next proposition. To motivate it, observe that, for given , the solvency test based on as described in (3) guarantees that the probability of solvency is at least . The same is true for the solvency test based on at the same level because dominates . The question we ask is if and how the probability of recovering at least a fraction of claims can be made higher than the probability of solvency. For V@R and AV@R the answer is negative: The lower bound is sharp for any target fraction of claims payments. In other words, both and impose the same weak lower bound on recovery probabilities, and this bound cannot be improved upon, even if the target recovery fraction is arbitrarily small.

Proposition 1.

We denote by a set of positive random variables on some nonatomic probability space . We assume that contains all positive discrete random variables. For all and we have

Proof.

See Section A.1. ∎

The preceding proposition shows that, from the perspective of controlling the probability of claims recovery (beyond the probability of solvency), there is little difference between and . This lack of control is not desirable for a financial regulator, as companies that seek to boost the payoff to shareholders are not prevented from taking on excessive risk thereby significantly reducing recovery payments to creditors in the case of their own default. This is illustrated by the following stylized but insightful example.

Example 2.

We consider a scenario space consisting of two states, (the good state) and (the bad state). The probability of the bad state is with close to zero, say or . A financial company sells a contract to a customer that results in the following liability schedule for the company:

The company can manage its assets by engaging in a stylized financial contract with zero initial cost transferring dollars from the good state to the bad state. More specifically, we assume that the company can choose one of the following asset profiles at time 1:

Hedging its liabilities completely would require the company to choose . However, since the contract transforms dollars in the high probability scenario into dollars in the low probability scenario, this is not attractive from the point of view of the company. Indeed, for any , the company’s net asset value is given by

Due to limited liability, the corresponding shareholder value is

Hence, the choice is optimal from the perspective of shareholders. We show that this choice is possible under capital requirements based on and . In fact, the company is adequately capitalized under and at level regardless of the size of . Indeed,

At the same time, this choice is detrimental for the creditors because it leads to no recovery on the expected claims payment. Indeed, in the default state , the creditor’s recovery on their claims is equal to and may take any value between 0 and 1, depending on the level of . For the optimal choice from the perspective of shareholders, namely , the recovery fraction in state is minimal, in fact zero.

The example shows that pursuing the interests of shareholders might trigger investment decisions with adverse effects on creditors. A solvency framework based on and fails to disincentivize firms from taking investment decisions that increase shareholders’ value at the price of jeopardizing their ability to cover liabilities. In the next section we show how to mitigate this deficiency of current regulatory frameworks.

3 Recovery Value at Risk

In this section we introduce a solvency test that controls the loss given default by imposing suitable bounds on the recovery on creditors’ claims. The test is based on a new risk measure called Recovery Value at Risk. The main difference with respect to standard risk measures like and is that Recovery Value at Risk is not a function of the net asset value only but also of the liabilities . As shown in the previous section, this extension is necessary if we want to explicitly control the recovery on claims. Throughout the section we continue to use the balance sheet notation introduced in Section 2.

3.1 Introducing

Creditors receive at least a recovery fraction on their claims payments if111111For simplicity, we neglect bankruptcy costs (administrative expenses, legal fees, etc.) which can substantially impair the size of recovery. Regulators may improve the efficiency of bankruptcy procedures and thereby decrease their costs, e.g., by requiring last wills of financial institutions.

| (5) |

In this event, assets may not be sufficient to meet all obligations, but they cover at least a fraction of liabilities. We control recovery by imposing lower bounds on the recovery probabilities

for all recovery fractions .121212We can rewrite the event of recovering a fraction of in different ways: where the last equality holds only if . In this sense, our approach can also be interpreted in terms of target probabilities for future leverage ratios. Focusing on the modified net asset value instead of is more aligned with current regulation and has the mathematical advantage to avoid divisions by zero. For this purpose, we introduce the following risk measure.

Definition 3.

We denote by the vector space of all random variables on some probability space . Let be an increasing function. The Recovery Value at Risk

with level function is defined by

| (6) |

If the random variables and in Definition 3 are interpreted, respectively, as the net asset value and liabilities in a company’s balance sheet,131313To allow for different applications, we mathematically define recovery risk measures over generic pairs without any restriction on the sign of and and without any specific assumptions about their relationship and interpretation. In the relevant applications, we have or and . the risk measure can be used to formulate a solvency test of the form (1). As shown in Remark 20, the condition

| (7) |

is equivalent to requiring that the recovery probabilities satisfy

| (8) |

for all recovery fractions . This guarantees the desired control on the loss given default. In particular, the solvency test (7) can be seen as a refinement of the standard solvency test (3) based on where the probability bound is replaced by a bound that depends on the target recovery fraction through the function . The assumption that is increasing captures the basic requirement that smaller recovery fractions on liabilities should be guaranteed at higher probability levels.

Remark 4.

The recovery-adjusted solvency test (7) can easily be combined with a standard solvency test based on at level . Indeed, setting , it follows that

| (9) |

showing that recovery-based capital requirements are more stringent than the standard ones. The standard test can be reproduced by setting for all recovery fractions , in which case the inequality in (9) becomes an equality. It is worth highlighting that the level may also be strictly larger than a regulatory level . In this case, the inequality in (9) may be reversed. The recovery-based risk measure can be viewed as a flexible generalization of that reacts to the entire loss tail as specified by the recovery function . As explained in Remark 21, the solvency test (7) also controls the conditional recovery probabilities given default. Contrary to and , the risk measure depends on the joint distribution of the tuple . In particular, the marginal distributions of and are not a sufficient statistic for but knowledge of the dependence structure, as captured, e.g., by the copula of the pair, is additionally required.141414The evaluation of is technically not more complicated than the computation of standard solvency capital requirements, since it only requires the computation of a supremum of distribution-based risk measures, namely ’s. In practical situations, knowledge of the precise joint distribution between assets and liabilities is challenging. We refer to Section 5 for a detailed numerical illustration. The problem is akin to risk estimation in the presence of aggregate positions where a model for the joint distribution is also needed. The structure of recovery risk measures opens up a variety of interesting technical questions related to dependence modelling that, however, go beyond the scope of the current work. The rich and growing literature on the topic is a good starting point to address such questions, see, e.g., \citeasnounembrechts2013model, \citeasnounbernard2014risk, \citeasnounbernard2017risk, \citeasnouncai2018asymptotic.

3.2 Choosing the Recovery Function

The choice of the recovery function is a critical step in our model and should reflect the risk profile of the (external or internal) regulators. In this section we describe a class of parametric recovery functions151515We describe a methodology to calibrate to an existing regulatory framework in Section 5. This mirrors a common strategy chosen by regulators when adapting a new solvency setting to replace a pre-existing one. Another possibility to choose is to elicit it from the risk profile of risk managers or customers, e.g., by way of a questionnaire targeting recovery distributions. This would raise a number of interesting questions for future research that are, however, beyond the scope of the paper. that provides an ideal compromise between flexibility and tractability and can be successfully tailored to different applications as demonstrated in Section 5.

We consider step-wise recovery functions of the form

| (10) |

with and . The parameters correspond to critical target recovery fractions while the parameters define bounds on the corresponding recovery probabilities for every . As shown in the next proposition, the induced by such recovery functions can be expressed as a maximum of finitely many ’s.

Proposition 5.

Let be defined as in (10). Then, for all with

Proof.

See Section A.3. ∎

The preceding proposition shows that, under a recovery function of the form (10), the recovery-based solvency test (7) takes the particularly simple form:

| (11) |

In this case, a company is adequately capitalized under if, for every , assets are sufficient to cover a fraction of liabilities with a probability of at least . The largest recovery probability with target recovery fraction caps the default probability and could correspond to the level of in a classical solvency test. This shows that a solvency test of the form (11) can easily be harmonized with the solvency tests currently used in solvency regulation.

3.3 Basic Properties of

We ask which basic properties of are inherited by its recovery counterpart . For a comprehensive survey on scalar monetary risk measures we refer to \citeasnounFS. A monetary risk measure is a function that satisfies the following two properties:

-

•

Cash invariance: for all and ;

-

•

Monotonicity: for all with -almost surely.

The cash invariance property formalizes that adding cash to a capital position reduces risk by exactly the same amount and implies that risk is measured on a monetary scale. In particular, cash invariance allows to rewrite the risk measure as a capital requirement rule:

i.e., the quantity can be interpreted as the minimal amount of cash that needs to be injected into the position in order to pass the solvency test in (2). If the position already fulfills this solvency condition, then corresponds to the maximal amount of capital that can be extracted from the balance sheet without compromising capital adequacy. Monotonicity reflects that larger capital positions correspond to lower risk and to lower capital requirements. In addition to its defining properties, a monetary risk measure may possess the following properties:

-

•

Convexity: for all and ;

-

•

Subadditivity: for all ;

-

•

Positive homogeneity: for all and .

-

•

Normalization: .

The first two properties characterize the behavior of the risk measure with respect to aggregation and require that diversification is not penalized. The third property specifies that risk measurements scale with the size of positions.

The next proposition records elementary properties of . In particular, is a standard monetary risk measure if the second argument is fixed.

Proposition 6.

The risk measure has the following properties:

-

(a)

Cash invariance in the first component: For all and

-

(b)

Monotonicity: For all with and -almost surely161616Note that monotonicity does not mean that increasing leverage would lead to a decrease in risk. While it is true that an increase in the value of liabilities might be accompanied by a decrease in risk, this is only possible if the value of assets increase in parallel. However, if assets are held constant, then an increase in the value of liabilities will always cause an increase in risk. In this respect, monotonicity does not differ from the standard monotonicity property of classical monetary risk measures.

-

(c)

Positive homogeneity: For all and

-

(d)

Star-shapedness171717We refer to the recent preprint \citeasnouncastagnoli2021star for a study of star-shaped risk measures. in the first component: For all with and

-

(e)

Normalization: For every with we have .

-

(f)

Finiteness: For all with we have under any of the following conditions: , , or is bounded from below.

Proof.

See Section A.4. ∎

The previous proposition shows that is a standard monetary risk measure in its first component and can conveniently be expressed as a capital requirement:

where the second equality is a consequence of Remark 20. This leads to the following useful operational interpretation of :

-

•

If , the company fails to pass the recovery-based solvency test (7) and is the minimal amount of cash that needs to be added to its assets in order to become adequately capitalized.

-

•

If , the company is adequately capitalized according to the recovery-based solvency test (7) and is the maximal amount of cash that may be extracted from the asset side without compromising capital adequacy.

Remark 7.

From an operational perspective the interpretation of monetary risk measures as capital requirement rules relies on the cash invariance property. is cash invariant in the first but not in the second argument. If one intends to modify the liabilities, e.g. by transferring them to another institution, instead of the assets on the balance sheet, an alternative definition of is appropriate, namely (“L” stands for “liabilities”)

| (12) |

In this case, the correct way to express the solvency test (7) is

| (13) |

which is still equivalent to condition (8). Note that is cash invariant (in the appropriate sense) with respect to its second argument, i.e., for all and

This leads to the following operational interpretation:

-

•

If , the company fails the solvency test (13) and is the minimal nominal amount of liabilities that needs to be removed from the balance sheet in order to pass the test, e.g., by transferring these liabilities to suitable equity holders outside the firm.

-

•

If , the company is adequately capitalized. The company may at most create an additional amount of liabilities, e.g., via additional debt, and immediately distribute the same amount of cash to its shareholders.

Observe that assets and liabilities are used in the definition of instead of the net asset value and liabilities in order to obtain a simple cash-invariant recovery risk measure with a transparent operational interpretation.181818Combining and leads to the question of how to combine asset and liability management for capital adequacy purposes, which, however, goes beyond the scope of this paper. The literature on set-valued risk measures may help to address this question.

4 General Recovery Risk Measures

The risk measure allows to control the loss given default by prescribing suitable bounds on the probability that part of the creditors’ claims can be recovered. If one replaces with other monetary risk measures, e.g. convex risk measures, one obtains recovery risk measures of a different type. In particular, by choosing appropriate monetary risk measures as the basic ingredients, it is possible to construct convex recovery risk measures. This may be desirable from the perspective of decentralized risk management or optimal risk sharing and capital allocation. In this section we describe the general structure of recovery risk measures and give special attention to recovery risk measures based on . We continue to use the balance sheet notation introduced in Section 2.

4.1 Introducing Recovery Risk Measures

To motivate the general definition of a recovery risk measure, we observe that may be expressed in terms of a decreasing family of monetary risk measures indexed by recovery fractions . Indeed, for a given level function , the collection of monetary risk measures given by

defines the associated by setting

By construction, smaller recovery fractions are guaranteed with higher probability, which is captured by being increasing. As a consequence, the family of maps , , is decreasing in the sense that whenever . A smaller recovery fraction corresponds to a more conservative risk measure. This motivates the general definition of a recovery risk measure.

Definition 8.

Let be the set of random variables on some probability space . We denote by a vector space that contains the constants. For every consider a map and assume that whenever . The recovery risk measure

is defined by

| (14) |

In line with our discussion on , if the random variables and in Definition 8 are respectively interpreted as the net asset value and liabilities in a company’s balance sheet, the recovery risk measure can be employed to formulate a solvency test of the form (1). Indeed, similarly to what we have shown in Remark 20, we have

| (15) |

The specific interpretation of this recovery-based solvency test will, of course, depend on the choice of the monetary risk measures used to build .

The next result collects some basic properties of recovery risk measures. In particular, we analyze how a recovery risk measure inherits the key properties of its underlying building blocks. If the risk measures ’s are convex, the recovery risk measure admits a dual representation, which is recorded in Section A.6 in the appendix. This type of duality results plays an important role in applications such as optimization problems involving risk measures.

Proposition 9.

A recovery risk measure has the following properties:

-

(a)

Cash invariance in the first component: If is cash invariant for every , then for all and

-

(b)

Monotonicity: If is monotone for every , then for all such that and -almost surely

-

(c)

Convexity: If is convex for every , then for all and

-

(d)

Subadditivity: If is subadditive for every , then for all

-

(e)

Positive homogeneity: If is positively homogeneous for every , then for all and

-

(f)

Star-shapedness in the first component: If is monotone and positively homogeneous for every , then for all with and

-

(g)

Normalization: If is monotone and for every , then for every with .

-

(h)

Finiteness: If is monotone for every , then for every with and for every with we have .

Proof.

See Section A.5. ∎

4.2 Recovery Average Value at Risk

The recovery risk measure shares one major deficiency with the classical , namely the lack of convexity. Unlike convex risk measures, and its recovery counterpart may thus penalize diversification, i.e., the capital requirement of a diversified position might be higher than the maximum of the capital requirements of the individual non-diversified positions. In addition, the lack of convexity complicates the solution of portfolio optimization problems with constraints on the downside risk and prevents the construction of limit systems within companies that facilitate decentralized risk management. A useful alternative is the following recovery-based version of .

Definition 10.

We denote by the vector space of integrable random variables on some probability space . Let be an increasing function. The Recovery Average Value at Risk

with level function is defined by

| (16) |

In line with our discussion on general recovery risk measures, if the random variables and in Definition 10 are interpreted, respectively, as the net asset value and liabilities in a company’s balance sheet, the recovery risk measure can be used to formulate the solvency test (15):

| (17) |

This means that a company will be adequately capitalized according to with level function if for all recovery fractions the modified net asset value is positive on average on the lower tail beyond the -quantile. Since dominates at the same level, domination is inherited by their recovery-based versions, i.e., for all

This implies, in particular, that the solvency test (17) is stricter than (7) and the recovery probabilities are still controlled as described in Remark 20. In the next example we show that is the maximum of finitely many AV@R’s if the recovery function is piecewise constant. This parallels the representation of recorded in Proposition 5.

Proposition 11.

Let be defined as in (10). Then, for all with

Proof.

See Section A.7. ∎

As an application of Proposition 9, we record some basic properties of in the next result. We refer to Section A.9 in the appendix for a proof of a dual representation of in line with the general dual representation recorded in Section A.6. As mentioned above, this type of duality results plays an important role in applications such as optimization problems involving risk measures.

Proposition 12.

The risk measure is cash invariant in its first component, monotone, convex, subadditive, positively homogeneous, star shaped in its first component, and normalized. Moreover, for all with under any of the following conditions: , , or is bounded from below.

Proof.

See Section A.8. ∎

Remark 13.

The subadditivity of makes it suitable to serve as a basis for limit systems that enable decentralized risk management within firms. We consider a bank or an insurance company that consists of subentities. For each date their assets, liabilities, and net asset value are denoted by , , and , . The consolidated figures are denoted by

The firm may enforce entity-based risk constraints of the form

where are given risk limits. If the limits are chosen to satisfy , then

by subadditivity. This shows that imposing risk constraints at the level of subentities allows to fulfill the “global” solvency test (17). A closely related issue is performance measurement and adaptive management of the balance sheets of firms, as often seen in practice. This is discussed for general recovery risk measures in Section 5.4.

Remark 14.

As in Remark 7, we may construct a version of that is cash invariant with respect to its second component. This is given by

The operational interpretation is analogous to that of .

5 Applications

We complement the foundations on recovery risk measures with detailed case studies and applications. In Section 5.1 we demonstrate that recovery-based solvency requirements may help align the decisions of the management of firms with the interest of creditors in protecting their claims in the case of default. In Sections 5.2.1 and 5.2.2 we compare in case studies the standard risk measures adopted in solvency regulation — and — to the recovery risk measure . Such a comparison enables to identify and to quantify potential failures of the current regulatory standards by revealing those situations in which creditors are not appropriately protected from low recovery rates on their claims payments. In Section 5.3 we address the problem of calibrating the recovery function to pre-specified benchmarks, an issue that is relevant in the context of regulatory regime changes. In Section 5.4 we focus on performance-based management of business divisions of firms for recovery risk measures. Finally, in Section 5.5 we show that efficient combinations of risk and return can be characterized by a linear program if downside risk is quantified by .

5.1 Protecting the Interests of Creditors

In Example 2, we demonstrated that capital requirements based on and may fail to provide an adequate protection to creditors. We return to this example and show that and can successfully be employed to enforce guarantees on claims recovery. For detailed calculations we refer to Section A.10 in the appendix.

Example 15.

We consider the situation of Example 2, but with a different risk constraint in terms of . While solvency constraints in terms of or led to recovery , the recovery risk measure is able to guarantee a pre-specified recovery level.

We fix a recovery function in the class described in Section 3.2 with . For a probability level and a recovery level , we set

For every choice of we obtain from Proposition 5 that

A direct computation shows that

According to (7) the company is adequately capitalized if

A maximal shareholder value under the recovery-based solvency constraint is attained with when and with otherwise. The first case corresponds to successfully controlling recovery. Hence, the regulator may choose a suitable recovery function such that is more stringent than and the recovery fraction in the default state is equal to . This is in contrast to Example 2 with solvency constraints in terms of or that led to recovery when the management maximizes shareholder value.

Example 16.

We consider the same situation as in Example 15, but replace by with the same recovery function. We will demonstrate that the recovery risk measure is also able to guarantee a pre-specified recovery level.

To be more specific, it follows from Proposition 11 for every choice of that

A direct computation shows that

Hence, the company is adequately capitalized under (17) if

If and the management selects the individually optimal admissible level of , the recovery fraction in the default state is equal to as observed in Example 15. In this case, there is no difference between and .

Interestingly enough, contrary to , claims recovery can be controlled under even in the situation where . In this case, under the assumption that shareholder value is maximized, the fraction of claims recovered in the default state equals

This expression is strictly positive as soon as is strictly larger than the bound . (For example, taking always ensures a recovery equal to ). As claimed, solvency capital requirements based on are more effective in controlling claims recovery in comparison to those based on in Example 15

5.2 The Impact of the Distribution of the Balance Sheet

Standard solvency capital requirements based on and cannot control the probability of recovering certain pre-specified fractions of claims. Additional capital is required which needs to be computed on the basis of recovery risk measures such as and . In this section, we study the impact of a variation in the distribution of the underlying balance sheet figures on the size of necessary capital adjustments. Section 5.2.1 numerically illustrates this for standard parametric distributions. This allows to understand the influence of correlation between assets and liabilities and the tail size of liabilities. Section 5.2.2 presents a stylized example demonstrating that under standard solvency regimes sophisticated asset-liability-management may hide substantial tail risk. These situations correspond to high capital adjustments, if the required capital is instead computed by recovery risk measures.

Throughout the section, we consider a financial institution with assets , liabilities , and net asset value at dates . The changes of the net asset value over the considered time window or, equivalently, the corresponding cash flows are .

5.2.1 Parametric Distributions

In this section, we consider parametric distributions that model the evolution of the company’s assets and liabilities and show how the gap between standard capital requirements and those based on recovery risk measures is influenced by the dependence between assets and liabilities and by their marginal distributions, in particular the liability tail size. We refer to Section A.11 for further details and to Section B for several complementary plots.

Distribution of assets and liabilities.

We assume that possesses a lognormal distribution with log-mean and log-standard deviation . This specification for the asset distribution is standard in the finance literature and compatible, e.g., with the Black-Scholes setting. We fix and . Liabilities follow a mixture gamma distribution. More precisely, up to the quantile possesses a gamma distribution with shape parameter and rate parameter ; beyond the quantile is determined by a gamma distribution with shape parameter and rate parameter . This specification is encountered in many applications, including insurance, and allows a flexible control on the tail distribution (heavier tails correspond to higher levels of ). Setting and , we focus on the range .

Assets and liabilities are linked by a Gaussian copula. This choice allows to capture dependence by a single parameter, the correlation coefficient . Under positive dependence (), shocks increasing the value of liabilities are more frequently accompanied by increased asset values. In this case, the asset position may be considered a reasonable hedge of the liability position. We focus on the range .

Simulated distribution of assets and liabilities.

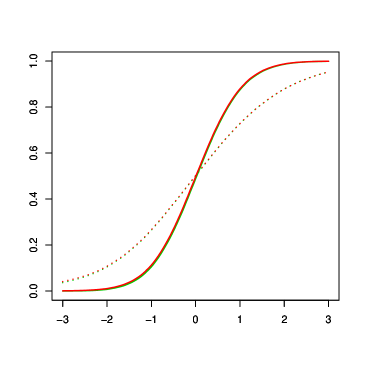

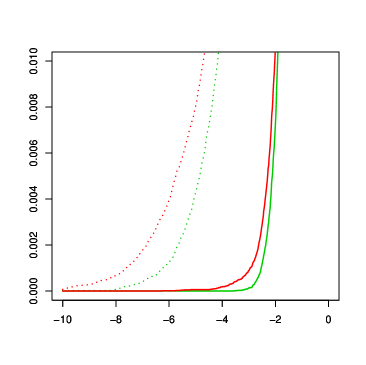

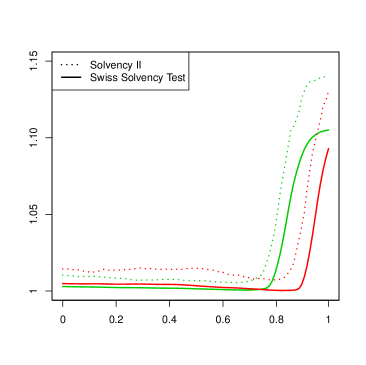

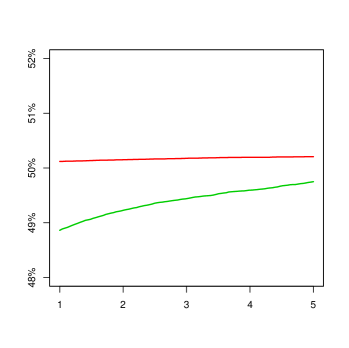

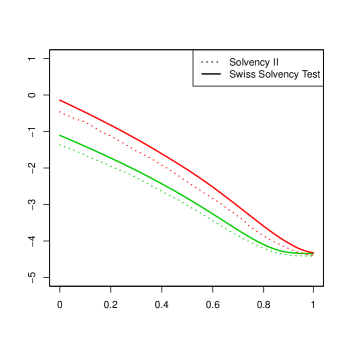

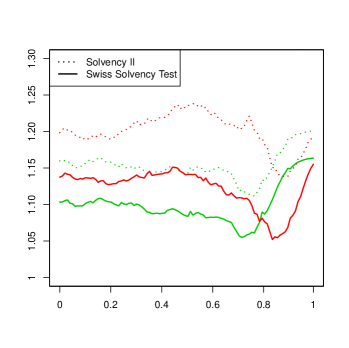

Our computations are implemented using the software R. We resort to standard Monte Carlo simulation based on quantile inversion (for the marginal distributions) and Cholesky decomposition (for the joint distribution); see, e.g., \citeasnounglasserman2013. The simulated cash flow distribution is displayed in Figure 1. The choice of is made to ensure a realistic probability of observing negative cash flows over the considered period of time, i.e., ; we target a value of about . This constraint is met in our case if, e.g., . As expected, increasing the correlation level between assets and liabilities leads to a more concentrated cash flow distribution. Increasing the size of the liability tail leads to a heavier cash flow tail. Probabilities of negative cash flows are decreasing functions of the correlation level and increasing functions of the liability tail size.191919This is illustrated in Figure 5 in the appendix. The first observation is due to the fact that the more positive the dependence, the more effective the assets as a hedge against liabilities and the lower the probability of negative cash flows.

Regulatory capital requirements.

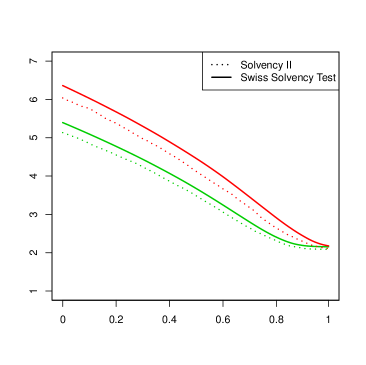

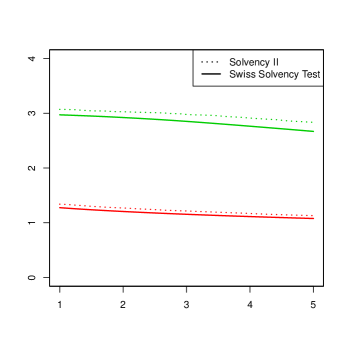

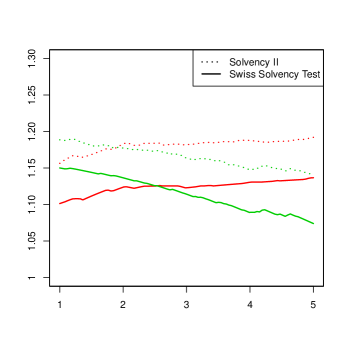

We focus on the two most prominent solvency regimes in insurance, Solvency II and the Swiss Solvency Test, with regulatory capital requirements

Figure 2 displays solvency capital requirements as functions of the correlation level between assets and liabilities and of the liability tail size. In line with our previous discussion, the level of regulatory capital is a decreasing function of correlation and an increasing function of tail size. The risk measure is always negative under our specifications, indicating that we are focusing on companies that are technically solvent with respect to the regulatory solvency tests under consideration. In addition, the solvency ratio lies in the interval , which is the relevant range in practice.202020This is illustrated in Figure 6 and Figure 7 in the appendix.

Recovery-based capital requirements.

For comparison, we consider recovery risk measures with a simple parametric recovery function belonging to the class described in Section 3.2 with . We fix a regulatory level and consider a piecewise constant recovery function

| (18) |

for suitable and . In line with the Solvency II standards we take . The solvency capital requirement induced by the corresponding is given by

the solvency test (7) is equivalent to

Besides controlling the default probability at the pre-specified regulatory level , the recovery risk measure additionally bounds the probability of covering less than a fraction of liabilities by a more stringent level .

Recovery adjustments.

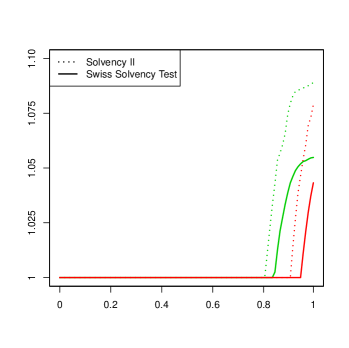

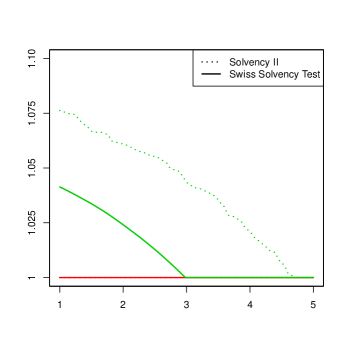

In order to capture the extent to which the regulatory solvency capital requirements fail to control the recovery on liabilities we define the recovery adjustment

| (19) |

This quantity is the maximum of 1 and the multiplicative factor by which regulatory requirements would have to be adjusted to guarantee the considered recovery levels. Recovery adjustments may also be conveniently expressed as a function of the regulatory level and the recovery rate as

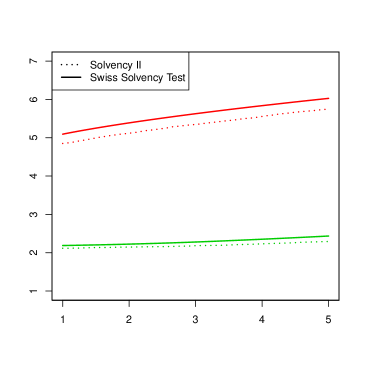

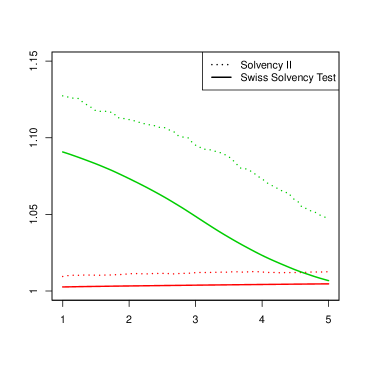

We consider the aggregate recovery adjustment212121We refer to Section B in the appendix for several plots of recovery adjustments for specific choices of and . These confirm the findings that are observed on an aggregate level.

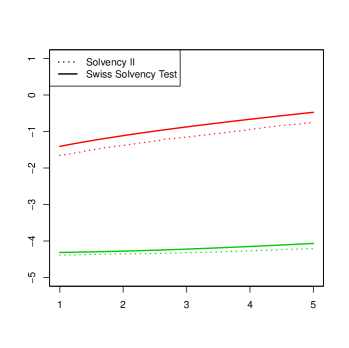

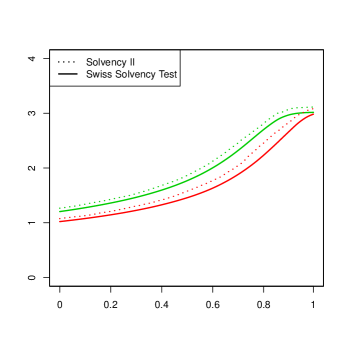

with and . Apart from a normalization constant, this quantity corresponds to the average recovery adjustment over the chosen range of the recovery parameters and . Figure 3 displays the aggregate recovery adjustment as a function of the correlation between assets and liabilities and of the size of the liability tail.

Observations.

The qualitative behavior of recovery adjustments can be described as follows:

-

(a)

Recovery adjustments are typically larger than , indicating that regulatory solvency requirements are too low to fulfill the target recovery-based solvency condition.

-

(b)

The size of the recovery adjustment depends on the recovery-based regulatory level and the recovery rate as expected: It is larger if is lower (a tighter constraint on the recovery probability) and if is higher (a larger portion of liabilities to recover). This relation holds across liability tail sizes and correlation levels but is more pronounced in the presence of lighter liability tails and higher correlations.

-

(c)

For sufficiently large correlation levels, recovery adjustments are increasing functions of the correlation level between assets and liabilities, suggesting that the failure of regulatory capital requirements to control the recovery on liabilities is more pronounced in the presence of large correlation levels. This relation holds across all liability tail sizes.

-

(d)

For sufficiently light tails, recovery adjustments are decreasing functions of the liability tail size, suggesting that the failure of regulatory capital requirements to control the recovery on liabilities is stronger in the presence of lighter liability tails. This relation holds across different correlation levels.

-

(e)

These observations hold for both regulatory frameworks under investigation. In comparison, recovery adjustments in the Swiss Solvency Test are lower than those induced in Solvency II under our distributional specifications.

Our observations demonstrate the importance of recovery risk measures from a risk management perspective. First, we observe that, under standard distributional assumptions, there may exist a considerable gap between the standard risk measures used in practice and our reference recovery risk measure. Second, this gap tends to be wider in the presence of lighter liability tails and higher levels of correlation between assets and liabilities. In situations when assets appear to better hedge liability claims, standard risk measures show lower ability to control recovery rates.

5.2.2 Sophisticated Asset-Liability-Management

In this section we consider a firm with a stylized balance sheet. Assets are deterministic, but the firm is capable of controlling the shape of the liability distribution in a sophisticated way. Our case study provides another perspective on the failure of standard solvency regulation to control recovery and highlights that this deficiency might be associated with large recovery adjustments. For detailed calculations we refer to Section A.12.

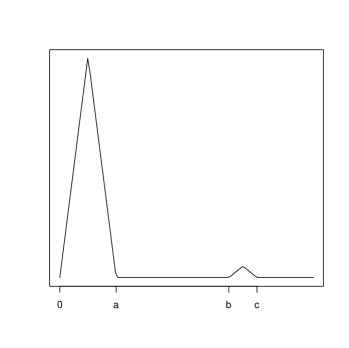

Distribution of assets and liabilities.

We assume that assets evolve in a deterministic way with being equal to a constant . The future value of liabilities follows a probability density function with two peaks as displayed in Figure 4. The probability of falling in the light tail peak is equal to and that of falling in the heavy tail peak is equal to .222222The explicit expression of the density function is provided in Section A.12 in the appendix.

Regulatory capital requirements.

In line with Solvency II and the Swiss Solvency Test, we focus on VaR at level and AVaR at level . The chosen regulatory risk measure is denoted by . The corresponding solvency capital requirements admit analytic solutions:

The capital requirements based on are blind to all liability payments beyond the first peak while capital requirements based on react to the entire distribution of liabilities.

Recovery-based capital requirements.

Fixing a regulatory level , consider a piecewise constant recovery function belonging to the class described in Section 3.2 with :

| (20) |

with , , and . The choice of is motivated by the standards implemented in Solvency II. The solvency capital requirement corresponding to is

and depends on the entire distribution of liabilities. This paralles , but tail risk is captured in a more sophisticated way: The recovery level determines the relative importance of the peaks of the liability distribution.

Recovery adjustments.

As in Section 5.2.1 we consider recovery adjustments as introduced in (19). We will answer the question how large the recovery adjustments may become, if a firm’s asset-liability-management is constrained by the following conditions:

| (1) | Solvent profile under | |

|---|---|---|

| (2) | Capital requirement under | |

| (3) | Solvent profile under | |

| (4) | Capital requirement under | |

| (5) | insufficient to control claims recovery | |

| (6) | Range of admissible regulatory solvency ratios |

More precisely, we focus on the optimization problem

| (21) |

under the constraints (1) to (6). The solvency ratios in (6) are in practice typically in the range between and .232323In general, we assume that .

It turns out that in many cases the highest admissible recovery adjustment coincides with , i.e., capital requirements under can be as large as times the capital requirements under or . This implies that the difference between the current capital requirements and their recovery-based versions in our asset-liability setting may be substantial. The next proposition states this in detail.

Proposition 17.

The optimal value of (21) is bounded from above by If , this upper bound is attained for every choice of . If , this upper bound is attained for special choices of , e.g., when and 242424For instance, if , then we can take .

Proof.

See Section A.13. ∎

The preceding result suggests that companies subject to capital requirements based on and may be far from guaranteeing acceptable recovery rates on their creditors’ claims. In the case, this is a consequence of tail blindness, which, in the absence of external controls, allows companies to accumulate tail risk without any regulatory cost. Also in the case this problem does not disappear because increased tail risk may often be compensated by a suitable shift in the asset distribution or in the body of the liability distribution. In our example, a more dispersed distribution beyond the quantile may leave the unchanged provided the distribution within the same quantile level shrinks.252525This phenomenon refers to the lack of surplus invariance and was studied in \citeasnounkoch2016unexpected.

5.3 Calibrating the Recovery Function

When regulatory solvency standards in practice are modified and improved, the old regulatory framework is often used as a benchmark for the new one. New and old requirements will, of course, differ for many distributions of assets and liabilities at the considered time horizon, and many companies might experience corresponding changes in solvency requirements. For this reason, a common approach in practice is to calibrate the new standards in such a way that they produce the same solvency requirement for a prototypical benchmark company. The rational behind this strategy is to ensure some form of continuity in the sense that benchmark firms are not too much affected over short time horizons. At the same time, regulatory standards are ideally modified in such a way that their new design is more efficient in achieving key regulatory goals in the long run. Choosing a benchmark balance sheet for calibration naturally remains a political decision.

In this section, we explain in the context of an example how recovery risk measures could be calibrated to existing regulatory standards. We begin by recalling the transition from Basel II to Basel III. Basel II was based on at level while the new Basel III has adopted at level . The choice of was justified a) by assuming in a benchmark model that changes in net asset value are normally distributed and b) by requiring262626We refer to \citeasnounPELVEwang for a general study on calibration of and .

The new regulatory level equates capital requirements of normally distributed positions for old and new standards. In the same spirit, we describe how to calibrate the recovery level function of . A challenge is that we deal with a function instead of a single parameter as well as with a pair of random variables, and , instead of just one random variable, . The aim is to equate, for a given level close to zero in the case that is normally distributed,

| (22) |

Definition of a benchmark. The choice of a benchmark is a political decision of the regulator. In our recovery-based setting, we consider a particularly simple choice. As discussed before, we assume that is normally distributed with mean and standard deviation . In addition, we suppose that is normally distributed with mean and standard deviation and is independent of . The latter assumption is not meant to capture realistic balance sheets, but is simply chosen for illustration as it leads to explicit calculations. By independence, for every the random variable is also normal with mean and standard deviation . We denote by the distribution function of a standard normal random variable. (Note that a positive random variable like cannot have a normal distribution. In practice, this can be taken into account by imposing the condition for a sufficiently small ).

Deriving the level function. We seek a function such that (22) holds. A sufficient requirement is that for every , or equivalently

Solving for gives

with . This function might be inconsistent with the requirements in Definition 3, namely with being increasing. A potential remedy to this problem could be to modify the choice of as follows. Since our solution for is differentiable with respect to , by taking derivatives, its increasing part can easily be characterized by

Here, we have used that because is assumed to be close to zero. Hence, is increasing on the interval where

If , the function is increasing on the whole interval . Otherwise, we compute

and redefine as follows:

Finally, if a piecewise-constant recovery function is sought, see Section 3.2, a suitable approximation of may be chosen. This provides a strategy to calibrate recovery risk measures to existing regulatory standards.

5.4 Performance Measurement

An important issue that is closely related to solvency capital requirements is performance measurement. We show that this task can be implemented on the basis of recovery risk measures. A popular metric in practice is the return on risk-adjusted capital (RoRaC). Consider a recovery risk measure that is subadditive and positively homogeneous as defined in Section 4.1. The associated RoRaC is defined by

This quantity measures the expected return per unit of economic capital expressed in terms of the risk measure . The goal of the firm is to improve its RoRaC. We assume that the company is composed of different subentities labelled . The central management may impose risk limits and adjust the size of different business units. A key question is which allocation of economic capital to business units and corresponding performance measurements provide appropriate information to improve the overall performance of the firm. We denote the net asset values and liabilities of the subentities at time by and for , respectively. Note that for

The subadditivity of implies

We seek an allocation of economic capital , , satisfying:

-

•

Full allocation: ;

-

•

Diversification: for all ;

-

•

RoRaC-compatibility: If for some we have

then there exists such that for every

The full allocation property requires that the entire solvency capital is allocated to the individual subentities. The diversification property specifies that no more capital is allocated to the individual subentities than their stand-alone solvency capital, taking beneficial diversification effects into account, which is feasible due to the subadditivity of . Finally, RoRaC-compatibility guarantees that performance measurement based on the chosen capital allocation provides the correct information to the management of the firm to improve the overall performance of the firm. To be more precise, if the performance of subentity — as captured by — is better than the overall RoRaC, the performance of the entire firm can be improved by growing subentity . An allocation fulfilling the above three properties is called a suitable allocation.

The existence of suitable allocations has been extensively studied in the literature, see, e.g., \citeasnountasche1999risk, \citeasnountasche2004allocating, \citeasnounkalkbrener2005axiomatic, \citeasnountasche2007capital, \citeasnoundhaene2012optimal, \citeasnounbauer2013capital, and the general review by \citeasnounbauer2020. It follows from the general results in these papers that the only suitable allocation in the above sense is the Euler allocation

for all . In the specific case of with a simple piecewise constant level function, the Euler allocation can explicitly be computed.

Proposition 18.

Proof.

See Section A.14. ∎

In summary, performance measurement inside firms can be based on recovery risk measures. Notions such as return on risk-adjusted capital (RoRaC) and RoRaC-compatible allocations may be extended to solvency regimes that control the size of recovery on creditors’ claims in the case of default.

5.5 Portfolio Optimization

Risk measures are an important instrument to limit downside risk in portfolio optimization problems. This idea is related to the classical Markowitz problem, originally studied by \citeasnounMarkowitz52, in which standard deviation quantifies the risk. Efficient frontiers characterize the best tradeoffs between return and risk. In this section, we show how recovery risk measures may successfully be applied to portfolio optimization in practice. Our results extend related contributions on the risk measure — discussed in \citeasnounRU00, \citeasnounRU02, and \citeasnounZhuFu09 — to the recovery risk measure .

Assets and liabilities. We consider assets whose (ask) prices at dates are described by and whose random one-period returns are denoted by so that

We assume that one-period returns have finite expectation. For every an investor invests a fraction of his or her total budget into asset so that . The total asset value at time is thus equal to

We set and . In addition, we suppose that the investor’s liabilities at time amount to a random fraction of the initial budget, i.e., the liabilities are equal to . We assume that liabilities have finite expectation.

Efficient frontier. We are interested in optimal combinations of return and downside risk – the efficient frontier – but with risk measured by instead of classical risk measures such as standard deviation or . This problem can equivalently be stated either as the maximization of return under a risk constraint or as the minimization of risk for a given expected return. We will consider the latter formulation.

Expected return. The expected future net asset value of the investor equals

implying that a target expected return can be achieved by requiring for some that

Downside risk and a minimax theorem. We are interested in computing and optimizing

We focus on the special case of piecewise-constant recovery functions introduced in Section 3.2. In this case, as shown in Proposition 11, is a maximum of finitely many terms involving , namely

For convenience, for every we define the auxiliary function by

which allows us to write

This follows from a representation of originally due to \citeasnounRU00 and \citeasnounRU02. Their results show that belongs to the family of divergence risk measures, which also correspond to optimized certainty equivalents, see \citeasnounBT87 and \citeasnounBT07. The following theorem facilitates the computation of an efficient frontier in the case of .

Theorem 19.

The following minimax equality holds:

Proof.

See Section A.15. ∎

Computing the efficient frontier. We now focus on the problem of determining the efficient frontier. This extends the methodology of \citeasnounRU00 and \citeasnounZhuFu09 to the case of . Characterizing the efficient frontier — consisting of pairs of returns and downside risk — is equivalent to minimizing the function in Theorem 19 additionally over where is a convex polyhedron. This problem can be conveniently reformulated as

The evaluation of involves the computation of an expectation. In typical applications in practice, these expectations are approximated via Monte Carlo simulations. This approach allows to reformulate the problem as a linear program, i.e., the minimization of a linear function on a convex polyhedron of the form

| s.t. | ||||

| over |

where are independent simulations of the pair . This problem is tractable on the basis of standard algorithmic implementations.

In this section, we showed how efficient frontiers can be computed that characterize the best tradeoffs between risk and return when risk is measured by recovery risk measures. This demonstrates that these risk measures can successfully be applied to portfolio optimization in practice.

6 Conclusion

Risk measures used in solvency regulation specify guard rails for financial firms such as banks or insurance companies. Within their legal boundaries firms can otherwise freely choose their actions, e.g., in order to maximize shareholder value. As a consequence, an axiomatic theory of risk measures for solvency regulation should carefully formulate and capture the goals of regulation, and determine and investigate suitable instruments to meet them. The issue of recovery on creditors’ claims has not yet been considered in sufficient detail, and the existing literature lacks solvency requirements that provide adequate protection of customers and counterparties in the case of default. In this paper, we propose the novel concept of recovery risk measures to resolve this issue. We analyze the properties of these risk measures and describe how to apply them in the context of solvency regulation, performance measurement, and portfolio optimization. Our findings suggest that recovery risk measures add value to the current risk management toolkit. They are tractable tools for both internal risk management and solvency regulation and can be employed to provide a more comprehensive picture on tail risk with a focus on safeguarding the interests of creditors and policyholders.

Various extensions of the suggested framework are possible. Our framework focuses on a static setting as common in solvency regulation where relevant time horizons are fixed. Dynamic or conditional solvency risk measures would be an interesting extension; see \citeasnounbc17 for a survey on previous research on this topic. Recovery risk measures are applied to single firms in this paper. From this perspective, another natural extension is the regulation of financial systems. As outlined in the literature, systemic risk measures should capture the local and global interaction of economic agents and operationalize the emerging risk at the level of the entire system; see, e.g., \citeasnounchen2013axiomatic, \citeasnounkromer2013systemic, \citeasnounFRW17, \citeasnounBFFM19. A related issue is a more comprehensive analysis of optimal investment under constraints in terms of recovery risk measures and equilibrium models of markets. Our approach to model firms’ balance sheets directly offers a natural and flexible starting point to address such problems.

Appendix A Proofs

A.1 Proof of Proposition 1

Proof.

Fix . By nonatomicity, for every we find an event such that . Set and and note that . Note also that both and belong to . A simple computation shows that

Moreover, we have . As a result,

This yields the desired statements. ∎

A.2 Remarks to Section 3.1

Remark 21.

The solvency test (7) also controls the conditional recovery probabilities given default. Indeed, assuming that , for all fractions we have

This implies the following equivalent formulation of the recovery-adjusted solvency test:

In particular, if the company’s unconditional default probability attains , then the lower bound on conditional recovery probabilities depends only on .

A.3 Proof of Proposition 5

Proof.

Fix and observe that is constant and equal to on the interval . Hence, we get

for every by positivity of and monotonicity of . As a result,

Similarly, observe that is constant and equal to on the interval . Hence, we get

for every by positivity of and monotonicity of . As a result,

The desired assertion is a direct consequence of the above identities. ∎

A.4 Proof of Proposition 6

Proof.

The statements from (a) to (d) follow directly from Proposition 9. To establish (e), take an arbitrary and note that both conditions and is bounded from below imply that . In particular, for some yields by monotonicity and cash invariance of . As a result, it suffices to show that implies . This is an immediate consequence of Proposition 9. ∎

A.5 Proof of Proposition 9

Proof.

(a) For every and the cash invariance of readily implies

(b) Since for every , the monotonicity of yields

(c) It follows from the convexity of that

(d) Similarly, we can use the subadditivity of to get

(e) Using the positive homogeneity of , we easily see that

(f) Observe that for every . This is because is positive. Then, it follows from the monotonicity and positive homogeneity of that

(g) It follows from monotonicity that for every . This is because is positive. Then, normalization yields

(h) Take such that and observe that for every . This is because is positive. Then, monotonicity implies

where we used that for every by assumption. ∎

A.6 General Dual Representation

The next proposition focuses on dual representations of recovery risk measures defined on standard spaces. We refer to \citeasnounFS for a broad discussion on dual representations. For every we denote by the set of probability measures over that are absolutely continuous with respect to and satisfy . Recall that a map satisfies the Fatou property if for every sequence and every we have

The Fatou property corresponds to a weak form of continuity, namely lower semicontinuity, with respect to dominated almost-sure convergence. A well-known result by \citeasnounJouini2006 shows that every distribution-based monetary risk measure defined on has the Fatou property. We refer to \citeasnoungao2018fatou for a general result beyond bounded random variables.

Proposition 22.

Let for some and assume that is a convex monetary risk measure with the Fatou property for every . Then, for all

where and for every we set

where .

Proof.

Set and fix . If , then it follows from Theorem 4.33 in \citeasnounFS that

for every , where

If , the same result follows from Corollary 7 in \citeasnounfrittelli2002 once we note that is lower semicontinuous with respect to the norm. To see this, take a sequence and such that in the norm. By Theorem 13.6 in \citeasnounaliprantis06, there exists a subsequence of , which we still denote by without loss of generality, such that -almost surely and . As a result of the Fatou property, we have

which implies the desired lower semicontinuity. Now, for every we obtain

This establishes the desired representation and concludes the proof. ∎

A.7 Proof of Proposition 11

Proof.

Fix and observe that is constant and equal to on the interval . Hence, we get

for every by positivity of and monotonicity of . As a result,

Similarly, observe that is constant and equal to on the interval . Hence, we get

for every by positivity of and monotonicity of . As a result,

The desired assertion is a direct consequence of the above identities. ∎

A.8 Proof of Proposition 12

Proof.