Stochastic Relaxed Inertial Forward-Backward-Forward splitting for Monotone Inclusions in Hilbert spaces

Abstract

We consider monotone inclusions defined on a Hilbert space where the operator is given by the sum of a maximal monotone operator and a single-valued monotone, Lipschitz continuous, and expectation-valued operator . We draw motivation from the seminal work by Attouch and Cabot [1, 2] on relaxed inertial methods for monotone inclusions and present a stochastic extension of the relaxed inertial forward-backward-forward (RISFBF) method. Facilitated by an online variance reduction strategy via a mini-batch approach, we show that (RISFBF) produces a sequence that weakly converges to the solution set. Moreover, it is possible to estimate the rate at which the discrete velocity of the stochastic process vanishes. Under strong monotonicity, we demonstrate strong convergence, and give a detailed assessment of the iteration and oracle complexity of the scheme. When the mini-batch is raised at a geometric (polynomial) rate, the rate statement can be strengthened to a linear (suitable polynomial) rate while the oracle complexity of computing an -solution improves to . Importantly, the latter claim allows for possibly biased oracles, a key theoretical advancement allowing for far broader applicability. By defining a restricted gap function based on the Fitzpatrick function, we prove that the expected gap of an averaged sequence diminishes at a sublinear rate of while the oracle complexity of computing a suitably defined -solution is where . Numerical results on two-stage games and an overlapping group Lasso problem illustrate the advantages of our method compared to stochastic forward-backward-forward (SFBF) and SA schemes.

1 Introduction

1.1 Problem formulation and motivation

A wide range of problems in areas such as optimization, variational inequalities, game theory, signal processing, or traffic theory, can be reduced to solving inclusions involving set-valued operators in a Hilbert space , i.e. to find a point such that , where is a set-valued operator. In many problems such inclusion problems display specific structure revealing that the operator can be additively decomposed. This leads us to the main problem we consider in this paper.

Problem 1.

Let be a real separable Hilbert space with inner product and associated norm . Let and be maximally monotone operators, such that is -Lipschitz continuous. The problem is to

| (MI) |

We assume that Problem 1 is well-posed:

Assumption 1.

.

We are interested in the case where (MI) is solved by an iterative algorithm based on a stochastic oracle (SO) representation of the operator . Specifically, when solving the problem, the algorithm calls to the SO. At each call, the SO receives as input a search point generated by the algorithm on the basis of past information so far, and returns the output , where is a random variable defined on some given probability space , taking values in a measurable set with law . In most parts of this paper, and the vast majority of contributions on stochastic variational problems in general, it is assumed that the output of the SO is unbiased,

| (1.1) |

Such stochastic inclusion problems arise in numerous problems of fundamental importance in mathematical optimization and equilibrium problems, either directly or through an appropriate reformulation. An excellent survey on the existing techniques for solving problem (MI) can be found in [9] (in general Hilbert spaces) and [29] (in the finite-dimensional case).

1.2 Motivating examples

In what follows, we provide some motivating examples.

Example 1.1 (Stochastic Convex Optimization).

Let be separable Hilbert spaces. A large class of stochastic optimization problems, with wide range of applications in signal processing, machine learning and control, is given by

| (1.2) |

where is a convex differentiable function with a Lipschitz continuous gradient , represented as . and are proper, convex lower semi-continuous functions, and is a bounded linear operator. Problem (1.2) gains particular relevance in machine learning, where usually is a convex data fidelity term (e.g. a population risk functional), and and embody penalty or regularization terms; see e.g. total variation [74], hierarchical variable selection [46, 88], and graph regularization [83, 84]. Applications in control and engineering are given in [5, 53]. We refer to (1.2) as the primal problem. Using Fenchel-Rockafellar duality [9, ch.19], the dual problem of (1.2) is given by

| (1.3) |

where is the Fenchel conjugate of and represents the infimal convolution of the functions and . Combining the primal problem (1.2) with its dual (1.3), we obtain the saddle-point problem

| (1.4) |

Following classical Karush-Kuhn-Tucker theory [69], the primal-dual optimality conditions associated with (1.4) are concisely represented by the following monotone inclusion: Find such that

| (1.5) |

We may compactly summarize these conditions in terms of the zero-finding problem (MI) using the operators and , defined as

Note that the operator is the sum of a maximally monotone and a skew-symmetric operator. Hence, in general, it is not cocoercive111An operator is cocoercive if there exists such that .. Conditions on the data guaranteeing Assumption 1 are stated in [21].

Since is represented as an expected value, we need to appeal to simulation based methods to evaluate its gradient. Also, significant computational speedups can be made if we are able to sample the skew-symmetric linear operator in an efficient way. Hence, we assume that there exists a SO that can provide unbiased estimator to the gradient operators and . More specifically, given the current position , the oracle will output the random estimators such that

This oracle feedback generates the random operator , which allows us to approach the saddle-point problem (1.4) via simulation-based techniques.

Example 1.2 (Stochastic variational inequality problems).

There are a multitude of examples of monotone inclusion problems (MI) where the single-valued map is not the gradient of a convex function. An important model class where this is the case is the stochastic variational inequality (SVI) problem. Due to their huge number of applications, SVI’s received enormous interest over the last several years from various communities [48, 75, 80, 58]. This problem emerges when is represented as an expected value as in (1.1) and for some proper lower semi-continuous function . In this case, the resulting structured monotone inclusion problem can be equivalently stated as

| (1.6) |

An important and frequently studied special case of (1.6) arises if is the indicator function of a given closed and convex subset . In this cases the set-valued operator becomes the normal cone map

| (1.7) |

This formulation includes many fundamental problems including fixed point problems, Nash equilibrium problems and complementarity problems [29]. Consequently, the equilibrium condition (1.6) reduces to

1.3 Contributions

Despite the advances in stochastic optimization and variational inequalities, the algorithmic treatment of general monotone inclusion problems under stochastic uncertainty is a largely unexplored field. This is rather surprising given the vast amount of applications of maximally monotone inclusions in control and engineering, encompassing distributed computation of generalized Nash equilibria [17, 86, 31], traffic systems [34, 35, 43], and PDE-constrained optimization [10]. The first major aim of this manuscript is to introduce and investigate a relaxed inertial stochastic forward-backward-forward (RISFBF) method, building on an operator splitting scheme originally due to Paul Tseng [85]. RISFBF produces three sequences , defined as

| (RISFBF) |

The data involved in this scheme are explained as follows:

-

•

and are random estimators of obtained by consulting the SO at search points and , respectively;

-

•

is a sequence of non-negative numbers regulating the memory, or inertia of the method;

-

•

is a positive sequence of step-sizes;

-

•

is a non-negative relaxation sequence.

If and the above scheme reduces to the stochastic forward-backward-forward method developed in [15, 24], with important applications in Gaussian communication networks [80] and dynamic user equilibrium problems [82]. However, even more connections to existing methods can be made.

Stochastic Extragradient. If , we obtain the inertial extragradient method

If , this reduces to a generalized extragradient method

recently introduced in [27].

Proximal Point Method. If , the method reduces to the well-known deterministic proximal point algorithm [2], overlaid by inertial and relaxation effects. The scheme reads explicitly as

The list of our contributions reads as follows:

-

(i)

Wide Applicability. A key argument in favor of Tseng’s operator splitting method is that it is provably convergent when solving structured monotone inclusions of the type (MI), without imposing cocoercivity of the single-valued part . This is a remarkable advantage relative to the perhaps more familiar and direct forward-backward splitting methods (aka projected (stochastic) gradient descent in the potential case). In particular, our scheme is applicable to the primal-dual splitting described in Example 1.1.

-

(ii)

Asymptotic guarantees. We show that under suitable assumptions on the relaxation sequence , the non-decreasing inertial sequence , and step-length sequence , the generated stochastic process weakly almost surely converges to a random variable with values in . Assuming demiregularity of the operators yields strong convergence in the real (possibly infinite-dimensional) Hilbert space.

-

(iii)

Non-asymptotic linear rate under strong monotonicity of . When is strongly monotone, strong convergence of the last iterate is shown and the sequence admits a non-asymptotic linear rate of convergence without a conditional unbiasedness of the SO. In particular, we show that the iteration and oracle complexity of computing an -solution is no worse than and , respectively.

-

(iv)

Non-asymptotic sublinear rate under monotonicity of . When is monotone, by leveraging the Fitzpatrick function [30, 77, 9] associated with the structured operator , we propose a restricted gap function. We then prove that the expected gap of an averaged sequence diminishes at the rate of . This allows us to derive an upper bound on the iteration complexity, and an upper bound (for on the oracle complexity for computing an -solution.

The above listed contributions shed new light on a set of urgent open questions, which we summarize below:

-

(i)

Absence of rigorous asymptotics. So far no aymptotic convergence guarantees have been available when considering relaxed inertial FBF schemes when is maximally monotone and is a single-valued monotone expectation-valued map.

-

(ii)

Unavailability of rate statements. We are not aware of any known non-asymptotic rate guarantees for algorithms solving (MI) under stochastic uncertainty. A key barrier in monotone and stochastic regimes in developing such statements has been in the availability of a residual function. Some recent progress in the special stochastic variational inequality case has been made by [45, 44, 15], but the general Hilbert-space setting involving set-valued operators seems to be largely unexplored (we will say more in Section 1.4).

-

(iii)

Bias requirements. A standard assumption in stochastic optimization is that the SO generates signals which are unbiased estimators of the deterministic operator . Of course, the requirement that the noise process is unbiased may often fail to hold in practice. In the present Hilbert space setting this is in some sense even expected to be the rule rather than the exception, since most operators are derived from complicated dynamical systems or the optimization method is applied to discretized formulations of the original problem. See the recent work [37, 38] for an interesting illustration in the context of PDE-constrained optimization. Some of our results go beyond the standard unbiasedness assumption.

1.4 Related research

Understanding the role of inertial and relaxation effects in numerical schemes is a line of research which received enormous interest over the last two decades. Below, we try to give a brief overview about related algorithms.

Inertial, Relaxation, and Proximal schemes.

In the context of convex optimization, Polyak [67] introduced the Heavy-ball method. This is a two-step method for minimizing a smooth convex function . The algorithm reads as

| (HB) |

The difference from the gradient method is that the base point of the gradient descent step is taken to be the extrapolated point , instead of . This small difference has the surprising consequence that (HB) attains optimal complexity guarantees for strongly convex functions with Lipschitz continuous gradients. Hence, (HB) resembles an optimal method [64]. The acceleration effects can be explained by writing the process entirely in terms of a single updating equation as

Choosing and for a small parameter, we arrive at

This can be seen as a discrete-time approximation of the second-order dynamical system

[68] introduced this dynamical system in an optimization context. Since then, it has received significant attention in the potential, as well as in the non-potential case (see e.g [3, 13, 4] for an appetizer). As pointed out in [81], if , the above system reduces to a continuous version of Nesterov’s fast gradient method [63]. Recently, [36] defined a stochastic version of the Heavy-ball method.

Motivated by the development of such fast methods for convex optimization, Attouch and Cabot [1] studied a relaxed-inertial forward-backward algorithm, reading as

| (RIFB) |

If , this reduces to a relaxed inertial proximal point method analyzed by Attouch and Cabot [2]. If , an inertial forward-backward splitting method is recovered, first studied by Lorenz and Pock [56].

Convergence guarantees for the forward-backward splitting rely on the cocoercivity (inverse strong monotonicity) of the single-valued operator . Example 1.1, in which is given by a monotone plus a skew-symmetric linear operator, illustrates an important instance for which this assumption is not satisfied (see [16] for further examples). A general-purpose operator splitting framework, relaxing the cocoercivity property, is the forward-backward-forward (FBF) method due to Tseng [85]. Inertial [12] and relaxed-inertial [14] versions of FBF have been developed. An all-encompassing numerical scheme can be compactly described as

| (RIFBF) |

Weak and strong convergence under appropriate conditions on the involved operators and parameter sequences are established in [14], but no rate statements are given.

Related work on stochastic approximation. Efforts in extending stochastic approximation methods to variational inequality problems have considered standard projection schemes [48] for Lipschitz and strongly monotone operators. Extragradient and (more generally) mirror-prox algorithms [61, 50] can contend with merely monotone operators, while iterative smoothing [87] schemes can cope with with the lack of Lipschitz continuity. It is worth noting that extragradient schemes have recently assumed relevance in the training of generative adversarial networks (GANS) [40, 59]. Rate analysis for stochastic extragradient (SEG) have led to optimal rates for Lipschitz and monotone operators [50], as well as extensions to non-Lipschitzian [87] and pseudomonotone settings [45, 51]. To alleviate the computational complexity single-projection schemes, such as the stochastic forward-backward-forward (SFBF) method [15, 24], as well as subgradient-extragradient and projected reflected algorithms [25] have been studied as well.

SFBF has been shown to be nearly optimal in terms of iteration and oracle complexity, displaying significant empirical improvements compared to SEG. While the role of inertia in optimization is well documented, in stochastic splitting problems, the only contribution we are aware of is the work by Rosasco et al. [72]. In that paper asymptotic guarantees for an inertial stochastic forward-backward (SFB) algorithm are presented under the hypothesis that the operators and are maximally monotone and the single-valued operator is cocoercive.

Variance reduction approaches. Variance-reduction schemes address the deterioration in convergence rate and the resulting poorer practical behavior via two commonly adopted avenues:

- (i)

- (ii)

In terms of run-time, improvements in iteration complexities achieved by mini-batch approaches are significant; e.g. in strongly monotone regimes, the iteration complexity improves from to [24, 25]. Beyond run-time advantages, such avenues provide asymptotic and rate guarantees under possibly weaker assumptions on the problem as well as the oracle; in particular, mini-batch schemes allow for possibly biased oracles and state-dependency of the noise [25]. Concerns about the sampling burdens are, in our opinion, often overstated since such schemes are meant to provide -solutions; e.g. if and the obtained rate is , then the batch-size where , implying that the batch-sizes are , a relatively modest requirement, given the advances in computing.

Outline. The remainder of the paper is organized in five sections. After dispensing with the preliminaries in Section 2, we present the (RISFBF) scheme in Section 3. Asymptotic and rate statements are developed in Section 4 and preliminary numerics are presented in Section 5. We conclude with some brief remarks in Section 6.

2 Preliminaries

2.1 Notation

Throughout, is a real separable Hilbert space with scalar product , norm , and Borel -algebra . The symbols and denote strong and weak convergence, respectively. denotes the identity operator on . Stochastic uncertainty is modeled on a complete probability space , endowed with a filtration . By means of the Kolmogorov extension theorem, we assume that is large enough so that all random variables we work with are defined on this space. A -valued random variable is a measurable function . We denote by the set of sequences of real-valued random variables such that, for every , is -measurable. For , we set

We denote the set of summable non-negative sequences by . We now collect some concepts from monotone operator theory. For more details, we refer the reader to [9]. Let be a set-valued operator. Its domain and graph are defined as respectively. Recall that an operator is monotone if

| (2.1) |

The set of zeros of , denoted by , defined as . The inverse of is . The resolvent of is If is maximally monotone, then is a single-valued map. We also need the classical notion of demiregularity of an operator.

Definition 2.1.

An operator is demiregular at if for every sequence and every , we have

The notion of demiregularity captures various properties typically used to establish strong convergence of dynamical systems. [5] exhibit a large class of possibly set-valued operators which are demiregular. In particular, demiregularity holds if is uniformly or strongly monotone, or when is the subdifferential of a uniformly convex lower semi-continuous function .

3 Algorithm

Let be a complete probability space. Our aim is to solve the monotone inclusion problem (MI) under the following assumption:

Assumption 2.

Consider Problem 1. The set-valued operator is maximally monotone with an efficiently computable resolvent. The single-valued operator is maximally monotone and -Lipschitz continuous ( with full domain .

For numerical tractability, we make a finite-dimensional noise assumption, common to stochastic optimization problems in (possibly infinite-dimensional) Hilbert spaces [42].222Our analysis does not rely on this assumption. It is made here only for concreteness and because it is the most prevalent one in applications.

Assumption 3 (Finite-dimensional Noise).

All randomness can be described via a finite dimensional random variable , where is a measurable set with Borel sigma algebra . The law of the random variable is denoted by , i.e. for all .

To access new information about the values of the operator , we adopt a stochastic approximation (SA) approach where samples are accessed iteratively and online: At each iteration, we assume to have access to a stochastic oracle (SO) which generates some estimate on the value of the deterministic operator when the current position is . This information is obtained by drawing an iid sample form the law . These fresh samples are then used in the numerical algorithm after an initial extrapolation step delivering the point , for some extrapolation coefficient . Departing from , we call the SO to retrieve the mini-batch estimator with sample rate :

| (3.1) |

is the data sample employed by the SO to return the estimator . Subsequently we perform a forward-backward update with step size :

| (3.2) |

In the final updates, a second independent call of the SO is made, using the data set , yielding the estimator

| (3.3) |

and the new state

| (3.4) |

This iterative procedure generates a stochastic process , defining the relaxed inertial stochastic forward-backward-forward (RISFBF) scheme. A pseudocode is given as Algorithm 1 below.

Note that RISFBF is still conceptual since we have not explained how the sequences and should be chosen. We will make this precise in our complexity analysis, starting in Section 4.

3.1 Equivalent form of RISFBF

We can collect the sequential updates of RISFBF as the fixed-point iteration

| (3.6) |

where is the time-varying map given by

Formulating the algorithm in this specific way establishes the connection between RISFBF and the Heavy-ball system. Indeed, combining the iterations in (3.6) in one, we get a second-order difference equations, closely resembling the structure present in (HB):

Also, it reveals the Markovian nature of the process ; It is clear from the formulation (3.6) that is Markov with respect to the sigma-algebra .

3.2 Assumptions on the stochastic oracle

In order to tame the stochastic uncertainty in RISFBF, we need to impose some assumptions on the distributional properties of the random fields and . One crucial statistic we need to control is the SO variance. Define the oracle error at a point as

| (3.7) |

Assumption 4 (Oracle Noise).

We say that the SO

-

(i)

is conditionally unbiased if for all ;

-

(ii)

enjoys a uniform variance bound: for some and all .

Define

The introduction of these two processes allows us to decompose the random estimator into a mean component and a residual, so that

If Assumption 4(i) holds true then . Hence, under conditional unbiasedness, the processes and are martingale difference sequences, where the filtrations are defined as , and iteratively, for ,

Observe that for all . The uniform variance bound, Assumption 4(ii), ensures that the processes have finite second moment.

Remark 3.1.

For deriving the stochastic estimates in the analysis to come, it is important to emphasize that is -measurable for all , and is -measurable.

The mini-batch sampling technology implies an online variance reduction effect, summarized in the next Lemma, whose simple proof we omit.

Lemma 3.1 (Variance of the SO).

Suppose Assumption 4 holds. Then for ,

| (3.8) |

We see that larger sampling rates lead to more precise point estimates of the single-valued operator. This comes at the cost of more evaluations of the stochastic operator. Hence, any mini-batch approach faces a trade-off between the oracle complexity and the iteration complexity. We want to use mini-batch estimators to achieve an online variance reduction scheme, motivating the next assumption.

Assumption 5 (Batch Size).

The batch size sequence is non-decreasing and satisfies .

4 Analysis

This section is organized into three subsections. The first subsection derives asymptotic convergence guarantees, while the second and third subsections provides linear and sublinear rate statements in strongly monotone and monotone regimes, respectively.

4.1 Asymptotic Convergence

Given , we define the residual function for the monotone inclusion (MI) as

| (4.1) |

Clearly, for every , . Hence, is a merit function for the monotone inclusion problem. To put this merit function into context, let us consider the special case where is the subdifferential of a lower semi-continuous convex function , i.e. . In this case, the resolvent reduces to the well-known proximal-operator

In the potential case, where for some smooth convex function , the residual function is thus seen to be a constant multiple of the norm of the so-called gradient mapping , which is a standard merit function in convex [62] and stochastic [26, 52] optimization. We use this function to quantify the per-iteration progress of RISFBF. The main result of this subsection is the following.

Theorem 4.1 (Asymptotic Convergence).

Let be fixed parameters. Suppose that Assumption 1-5 holds true. Let be a non-decreasing sequence such that . Let be a converging sequence in such that . If for all , then

-

(i)

in ;

-

(ii)

the stochastic process generated by algorithm RISFBF weakly converges to a -valued limiting random variable ;

-

(iii)

-a.s.

We prove this Theorem via a sequence of technical Lemmas. Our proof strategy for Theorem 4.1 follows [15], where a stochastic quasi-Fejér principle is established, including the residual function. We start with a basic relation.

Lemma 4.2.

For all , we have

| (4.2) |

Proof.

By definition,

where the last inequality uses the non-expansivity property of the resolvent operator. Rearranging terms gives the claimed result.

Next, for a given pair , we define the stochastic processes , and as

| (4.3) | |||

| (4.4) | |||

| (4.5) |

Key to our analysis is the following energy bound on the evolution of the anchor sequence .

Lemma 4.3 (Fundamental Recursion).

Let be the stochastic process generated by RISFBF with , , and . For all and , we have

Proof.

To simplify the notation, let us call and . We also introduce the intermediate update . For all , it holds true that

Since

Introducing the process from eq. (4.5), the aforementioned set of inequalities reduces to

Hence,

But , implying that

Pick , so that . Then, the monotonicity of yields the estimate

This is equivalent to

| or | (4.6) |

This implies that

Hence, we obtain the following,

Rearranging terms, we arrive at the following bound on :

| (4.7) | ||||

Next, we observe that may be bounded as follows.

| (4.8) |

We may then derive a bound on the expression in (4.8),

| (4.9) | |||

| (4.10) |

By invoking (4.2), we arrive at the estimate

Furthermore,

which implies that

| (4.11) |

Multiplying both sides by , a positive scalar since , we obtain

| (4.12) |

Rearranging terms, and noting that , the above estimate becomes

| (4.13) |

Substituting this bound into the first majorization of the anchor process , we see

Observe that

| (4.14) |

and Lemma A.1 gives

| (4.15) |

By hypothesis, are defined such that . Then, using both of these relations in the last estimate for , we arrive at

Using the respective definitions of the stochastic increments in (4.3) and (4.4), we arrive at

| (4.16) |

Recall that is -measurable. By the law of iterated expectations, we therefore see

for all . Observe that if we choose , meaning that , then is a martingale difference sequence. Furthermore, for all ,

| (4.17) |

where .

To prove the a.s. convergence of the stochastic process , we rely on the following preparations. Motivated by the analysis of deterministic inertial schemes, we are interested in a regime under which is non-decreasing.

For a fixed reference point , define the anchor sequences , and the energy sequence In terms of these sequences, we can rearrange the fundamental recursion from Lemma 4.3 to obtain

For a given pair , define

| (4.18) |

Then, in terms of the sequence

| (4.19) |

and using the monotonicity of , guaranteeing that , we get

Defining

we arrive at

| (4.20) |

Our aim is to use as a suitable energy function for RISFBF. For that to work, we need to identify a specific parameter sequence pair so that and , taking the following design criteria into account:

-

1.

for all ;

-

2.

is non-decreasing with

(4.21)

Incorporating these two restrictions on the inertia parameter , we are left with the following constraints:

| (4.22) |

To identify a constellation of parameters satisfying these two conditions, define

| (4.23) |

Then,

which gives

| (4.24) |

Solving this condition for reveals that Using the design condition , we need to choose the relaxation parameter so that . This suggests to use the relaxation sequence . It remains to verify that with this choice we can guarantee This can be deduced as follows: Recalling (4.23), we get

In particular, we note that if , then

We consider two cases:

Case 1: . In this case

Case 2: . In this case

Thus, is decreasing in , where .

Using these relations, we see that (4.20) reduces to

| (4.25) |

where . This is the basis for our proof of Theorem 4.1.

Proof of Theorem 4.1.

We start with (i). Consider (4.25), with the special choice , so that . Taking conditional expectations on both sides of this inequality, we arrive at

where . By design of the relaxation sequence , we see that

Since , and , we conclude that the sequence is bounded. Consequently, thanks to Assumption 5, the sequence is in . We next claim that . To verify this, note that

where the first and second inequality uses and , the third inequality makes use of the Young inequality: . Finally, the fourth inequality uses the triangle inequality . Lemma A.2 readily yields the existence of an a.s. finite limiting random variable such that , -a.s., and . Since , we get . Hence,

-a.s. We conclude that , -a.s..

To prove (ii) observe that, since and , it follows

Consequently, , -a.s., and is almost surely bounded. Hence, for each , there exists a bounded random variable such that

Iterating this relation, using the fact that , we easily derive

Hence, is a.s. bounded, which implies that is bounded -a.s. We next claim that converges to a -valued random variable -a.s. Indeed, take such that is bounded. Suppose there exists , and subsequences and such that and . Then, , a contradiction. It follows that and, in turn, . Thus, for each , -a.s.

Since we assume that is separable, [22, Prop 2.3(iii)] guarantees that there exists a set with , and, for every and every , the sequence converges.

We next show that all weak limit points of are contained in . Let such that is bounded. Thanks to [9, Lemma 2.45], we can find a weakly convergent subsequence with limit , i.e. for all we have . This implies

showing that . Along this weakly converging subsequence, define

Clearly, , so that . By definition

Since and are maximally monotone, their graphs are sequentially closed in the weak-strong topology [9, Prop. 20.33(ii)]. Therefore, by the strong convergence of the sequence , we deduce weak convergence of the sequence . Therefore . Hence, , showing that . Invoking [22, Prop 2.3(iv)], we conclude that converges weakly -a.s to an -valued random variable.

We now establish (iii). Let , so that (4.25) yields the recursion

By Assumption 5, and the definition of all sequences involved, we see that . Hence, a telescopian argument gives

Hence, for all , rearranging the above reveals

Letting , we conclude . Classically, this implies -a.s. By a simple majorization argument, we deduce that -a.s.

Remark 4.1.

The above result gives some indication of the balance between the inertial effect and the relaxation effect. Our analysis revealed that the maximal value of the relaxation parameter is . This is closely aligned with the maximal relaxation value exhibited in Remark 2.13 of [2]. Specifically, the function . This function is decreasing in . For this choice of parameters, one observes that for we get and for it is observed .

As an immediate corollary of Theorem 4.1, we obtain a convergence result when all parameter sequences are constant.

Corollary 4.4 (Asymptotic convergence under constant inertia and relaxation).

Let the same Assumptions as in Theorem 4.1 hold. Consider Algorithm RISFBF with the constant parameter sequences and . Then converges weakly -a.s. to a limiting random variable with values in .

In fact, the a.s. convergence with a larger is allowed as shown in the following corollary.

Corollary 4.5 (Asymptotic convergence under larger steplength).

Let the same Assumptions as in Theorem 4.1 hold. Consider Algorithm RISFBF with the constant parameter sequences and , where . Then converges weakly -a.s. to a limiting random variable with values in .

Proof.

Another corollary of Theorem 4.1 is a strong convergence result, assuming that is demiregular (cf. Definition 2.1).

Corollary 4.6 (Strong Convergence under demiregularity).

Let the same Assumptions as in Theorem 4.1 hold. If is demiregular, then converges strongly -a.s. to a -valued random variable.

Proof.

Set , and . We know from the proof of Theorem 4.1 that and . If is demiregular then . Since we know , we conclude . Since and have the same limit points, it follows .

4.2 Linear Convergence

In this section, we derive a linear convergence rate and prove strong convergence of the last iterate in the case where the single-valued operator is strongly monotone. Various linear convergence results in the context of stochastic approximation algorithms for solving fixed-point problems are reported in [23] in the context of the random sweeping processes. In a general structured monotone inclusion setting [73] derive rate statements for cocoercive mean operators in the context of forward-backward splitting methods. More recently, Cui and Shanbhag [24] provide linear and sublinear rates of convergence for a variance-reduced inexact proximal-point scheme for both strongly monotone and monotone inclusion problems. However, to the best of our knowledge, our results are the first published for a stochastic operator splitting algorithm, featuring relaxation and inertial effects. Notably, this result does not require imposing Assumption 4(i) (i.e. the noise process be conditionally unbiased.) Instead our derivations hold true under a weaker notion of an asymptotically unbiased SO.

Assumption 6 (Asymptotically unbiased SO).

There exists a constant such that

| (4.26) |

for all .

This definition is rather mild and is imposed in many simulation-based optimization schemes in finite dimensions. Amongst the more important ones is the simultaneous perturbation stochastic approximation (SPSA) method pioneered by Spall [78, 79]. In this scheme, it is required that the gradient estimator satisfies an asymptotic unbiasedness requirement; in particular, the bias in the gradient estimator needs to diminish at a suitable rate to ensure asymptotic convergence. In fact, this setting has been investigated in detail in the context of stochastic Nash games [28]. Further examples for stochastic approximation schemes in a Hilbert-space setting obeying Assumption 6 are [7, 8] and [38]. We now discuss an example that further clarifies the requirements on the estimator.

Example 4.1.

Let be a collection of independent random -valued vector fields of the form such that

where and such that is an -valued sequence satisfying in an a.s. sense. These statistics can be obtained as

Setting , we see that condition (4.26) holds. A similar estimate holds for the random noise .

Assumption 7.

is -strongly monotone (), i.e.

| (4.27) |

Combined with Assumption 1, strong monotonicity implies that for some .

Remark 4.2.

In the context of a structured operator , the assumption that the single-valued part is strongly monotone can be done without loss of generality. Indeed, if instead is assumed to be -strongly monotone, then is maximally monotone and Lipschitz continuous while may be seen to be -strongly monotone operator.

Our first result establishes a “perturbed linear convergence” rate on the anchor sequence , similar to the one derived in [23, Corollary 3.2] in the context of randomized fixed point iterations.

Theorem 4.7 (Perturbed linear convergence).

Consider RISFBF with . Suppose Assumptions 1-3, Assumption 6 and Assumption 7 hold. Let denotes the unique solution of (MI). Suppose , where , , . Define . Let be a non-decreasing sequence such that , and define for every . Set

| (4.28) | |||

where , . Then the following hold:

-

(i)

.

-

(ii)

For all

(4.29) In particular, this implies a perturbed linear rate of the sequence as

(4.30) -

(iii)

.

Proof.

Our point of departure for the analysis under the stronger Assumption 7 is eq. (4.6), which becomes

Repeating the analysis of the previous section with reference point and , the unique solution of (MI), yields the bound

The triangle inequality gives

By Young’s inequality, we have for all ,

| (4.31) |

Observe that this estimate is crucial in weakening the requirement of conditional unbiasedness. Choose to get

Assume that . Then,

where . Moreover, choosing , we see

Using these bounds, we readily deduce for , that

| (4.32) |

Proceeding as in the derivation of eq. (4.1), one sees first that

and therefore,

| (4.33) |

Define . Using the equality (4.8),

with stochastic error term . From here, it follows that

| (4.34) |

Since , and , we claim that for . Indeed,333To wit, the function is attains a global minumum at , which gives the global lower bound . Furthermore, the function attains a global maximum at , with corresponding value .

In particular, this implies for all . We then have

| (4.35) |

Next, we show that , for defined in (4.28). This can be seen from the next string of inequalities:

In this derivation we have used the Young inequality and the specific choice .

By recalling (4.34) and invoking (4.35), we are left with the stochastic recursion

| (4.36) |

where and Since for every , we have that for every . Furthermore, , so that . Taking conditional expectations on both sides on (4.36), we get

using the notation . Applying the operator and using the tower property of conditional expectations, this gives

Proceeding inductively, we see that

This establishes eq. (4.29). To validate eq. (4.30), recall that we assume , so that . Furthermore, , so that

We now show that . Simple algebra, combined with Assumption 6, gives

| (4.37) |

Hence, since is bounded, Assumption 5 gives a.s. Using again the tower property, we see , where for every . Consequently, the discrete convolution is summable. Therefore and . Clearly, this implies and consequently the subsequently stated two implication follow as well:

Remark 4.3.

It is worth remarking that the above proof does not rely on unbiasedness of the random estimators. The reason why we can lift this rather typical assumption lies in our application Young’s inequality in the estimate (4.31). The only assumption needed is a summable oracle variance as formulated in Assumption 6 to get the above result working.

Remark 4.4.

The above result illustrates again nicely the well-known trade-off between relaxation and inertial effects (cf. Remark 4.1). Indeed, up to constant factors, the coupling between inertia and relaxation is expressed by the function . Basic calculus reveals that this function is decreasing for increasing. In the extreme case when , it is necessary to let , and vice versa. When then the limiting value of our specific relaxation policy is . In practical applications, it is advisable to choose small in order to make large. The value must be calibrated in a disciplined way in order to allow for a sufficiently large step size . This requires some knowledge of the condition number of the problem . As a heuristic argument, a good strategy, anticipating that should be close to , is to set . This means .

We obtain a full linear rate of convergence when a more aggressive sample rate is employed in the SO. We achieve such global linear rates, together with tuneable iteration and oracle complexity estimates in two settings: First, we consider an aggressive simulation strategy, where the sample size grows over time geometrically. Such a sampling frequency can be quite demanding in some applications. As an alternative, we then move on and consider a more modest simulation strategy under which only polynomial growth of the batch size is required. Whatever simulation strategy is adopted, key to the assessment of the iteration and oracle complexity is to bound the stopping time

| (4.38) |

In order to understand the definition of this stopping time, recall that RISFBF computes the last iterate by extrapolating between the current base point and the correction step involving , which requires iid realizations from the law . In total, when executing the algorithm until the terminal time , where therefore need to simulate random variables. We now estimate the integer under a geometric sampling strategy.

Proposition 4.8 (Non-asymptotic linear convergence under geometric sampling).

Suppose the conditions of Theorem 4.7 hold. Let and choose the sampling rate . Let , and define

| (4.39) | ||||

| (4.40) |

Then, whenever , we see that

and whenever ,

In particular, the stochastic process converges strongly and -a.s. to the unique solution at a linear rate.

Proof.

Departing from (4.36), ignoring the positive term from the right-hand side, and taking expectations on both sides leads to

| (4.41) |

where the equality follows from being deterministic. The sequence is further upper bounded by the following considerations: First, the relaxation sequence is bounded by ; Second, the sample rate is bounded by . Using these facts, eq. (4.37) yields

| (4.42) |

where . Iterating the recursion above, one readily sees that

| (4.43) |

Consequently, by recalling that and , the bound (4.42) allows us to derive the recursion

| (4.44) |

We consider three cases.

(i) : Defining , we obtain from (4.44)

Proposition 4.9 (Oracle and Iteration Complexity under geometric sampling).

Proof.

First, let us recall that the total oracle complexity of the method is assessed by

If define . Then, , and hence . We now compute

This gives the oracle complexity bound

If , we can replicate this calculation, after setting . After so many iterations, we can be ensured that , with an oracle complexity

To the best of our knowledge, the provided non-asymptotic linear convergence guarantee appears to be amongst the first in relaxed and inertial splitting algorithms. In particular, by leveraging the increasing nature of mini-batches, this result no longer requires the unbiasedness assumption on the SO, a crucial benefit of the proposed scheme.

There may be settings where geometric growth of is challenging to adopt. To this end, we provide a result where the sampling rate is polynomial rather than geometric. A polynomial sampling rate arises if for some parameters . Such a regime has been adopted in related mini-batch approaches [54, 55]. This allows for modulating the growth rate by changing the exponent in the sampling rate. We begin by providing a supporting result. We make the specific choice for all , and , leaving essentially the exponent as a free parameter in the design of the stochastic oracle.

Proposition 4.10 (Polynomial rate of convergence under polynomially increasing ).

Suppose the conditions of Theorem 4.7 hold. Choose the sampling rate where . Then, for any ,

| (4.46) |

Proof.

From the relation (4.43), we obtain

A standard bound based on the integral criterion for series with non-negative summands gives

The upper bounding integral can be evaluated using integration-by-parts, as follows:

Note that when . Therefore, we can attain a simpler bound from the above by

Consequently,

Furthermore,

Note that . Hence,

Plugging this into the opening string of inequalities shows

Since and , we finally arrive at the desired expression (4.46).

Proposition 4.11 (Oracle and Iteration complexity under polynomial sampling).

Proof.

We first note that for all . Hence, the bound established in Proposition 4.10 yields

Consider the function for . Then, straightforward calculus shows that is unimodal on , with unique maximum and associated value . Hence, for all , we have , and consequently, for all . This allows us to conclude

where

| (4.47) |

Then, for any , we are ensured that . Since , we conclude that . The corresponding oracle complexity is bounded as follows:

Remark 4.5.

It may be observed that if the or , there is a worsening of the rate and complexity statements from their counterparts when the sampling rate is geometric; in particular, the iteration complexity worsens from to while the oracle complexity degenerates from the optimal level of to . But this deterioration comes with the advantage that the sampling rate is far slower and this may be of signficant consequence in some applications.

4.3 Rates in terms of merit functions

In this subsection we estimate the iteration and oracle complexity of RISFBF with the help of a suitably defined gap function. Generally, a gap function associated with the monotone inclusion problem (MI) is a function such that (i) is sign restricted on ; and (ii) if and only if . The Fitzpatrick function [30, 77, 11, 9] is a useful tool to construct gap functions associated with a set-valued operator . It is defined as the extended-valued function given by

| (4.48) |

This function allows us to recover the operator , by means of the following result (cf. [9, Prop. 20.58]): If is maximally monotone, then for all , with equality if and only if . In particular, . In fact, it can be shown that the Fitzpatrick function is minimal in the family of convex functions such that for all , with equality if [11].

Our gap function for the structured monotone operator is derived from its Fitzpatrick function by setting for . This reads explicitly as

| (4.49) |

It immediately follows from the definition that for all . It is also clear, that is convex and lower semi-continuous and if and only if . Let us give some concrete formulae for the gap function.

Example 4.2 (Variational Inequalities).

Example 4.3 (Convex Optimization).

Reconsider the general non-smooth convex optimization problem in Example 1.1, with primal objective function . Let us introduce the convex-concave function

Define

| (4.50) |

It is easy to check that , and equality holds only for a primal-dual pair (saddle-point) . Hence, is a gap function for the monotone inclusion derived from the Karush-Kuhn-Tucker conditions (1.5). In fact, the function (4.50) is a standard merit function for saddle-point problems (see e.g. [19]). To relate this gap function to the Fitzpatrick function, we exploit the maximally monotone operators and introduced Example 1.1. In terms of these mappings, first observe that for we have

Since is convex differentiable, the classical gradient inequality reads as . Using this estimate in the previous display shows

For , we again employ convexity to get

Hence,

Therefore, we see

Hence,

It is clear from the definition that a convex gap function can be extended-valued and its domain is contingent on the boundedness properties of . In the setting where is bounded for all , the gap function is clearly globally defined. However, the case where is unbounded has to be handled with more care. There are potentially two approaches to cope with such a situation: One would be to introduce a perturbation-based termination criterion as defined in [60], and recently used in [20] to solve a class of structured stochastic variational inequality problems. The other solution strategy is based on the notion of restricted merit functions, first introduced in [65], and later on adopted in [57]. We follow the latter strategy.

Let denote an arbitrary reference point and a suitable constant. Define the closed set , and the restricted gap function

| (4.51) |

Clearly, . The following result explains in a precise way the meaning of the restricted gap function. It extends the variational case in [65, Lemma 1] and [57, Lemma 3] to the general monotone inclusion case.

Lemma 4.12.

Let be nonempty closed and convex. The function is well-defined and convex on . For any we have . Moreover, if is a solution to (MI), then . Moreover, if for some such that , then .

Proof.

The convexity and non-negativity for of the restricted function is clear. Since for all , we see

To show the converse implication, suppose for some with . Without loss of generality we can choose in this particular way, since we may choose the radius of the ball as large as desired. It follows that for all . Hence, is a Minty solution to the Generalized Variational inequality with maximally monotone operator . Since is upper semi-continuous and monotone, Minty solutions coincide with Stampacchia solutions, implying that there exists such that for all (see e.g. [18]). Consider now the gap program

This program is solved at , which is a point for which . Hence, the constraint can be removed, and we conclude for all . By monotonicity of , it follows

Hence, and we conclude .

We start with the first preliminary result.

Lemma 4.13.

Consider the sequence generated by RISFBF with the initial condition . Suppose for every . Moreover, suppose is a non-decreasing sequence such that , for every . Define

| (4.52) |

and for , we define as in (4.4). Then, for all , we have

| (4.53) |

Proof.

For , we know from eq. (4.6)

where the last inequality uses the monotonicity of . We first derive a recursion which is similar to the fundamental recursion in Lemma 4.3. Invoking (4.8) and (4.9), we get

| (4.54) |

Multiplying both sides of (4.11) and noting that , we obtain the following inequality

Inserting the above inequality to (4.54) and using the same fashion in deriving (4.16), we arrive at

| (4.55) |

Invoking the monotonicity of and rearranging (4.55), it follows that

We define as

and similarly with (4.19), we can show is non-increasing by choosing and . Thus, . Together with , the last inequality gives

Recall that . Hence, after setting , rearranging the expression given in the previous display shows that

Summing over , we obtain

where we notice in the last inequality.

Next, we derive a rate statement in terms of the gap function, using the averaged sequence

| (4.56) |

Theorem 4.14 (Rate and oracle complexity under monotonicity of ).

The proof of this Theorem builds on an idea which is frequently used in the analysis of stochastic approximation algorithms, and can at least be traced back to the robust stochastic approximation approach of [61]. In order to bound the expectation of the gap function, we construct an auxiliary process which allows us to majorize the gap via a quantity which is independent of the reference points. Once this is achieved, a simple variance bound completes the result.

Proof of Theorem 4.14.

We define an auxiliary process such that

| (4.57) |

Then,

so that

Introducing the iterate , the above implies

As , this implies via a telescopian sum argument

| (4.58) |

Using Lemma 4.13 and setting , for any it holds true that

Define , divide both sides by and using our definition of an ergodic average (4.56), this gives

Using the bound established in eq. (4.58), it follows

Choosing and introducing , we see that the above can be bounded by a random quantity which is independent of :

Taking the supremum over pairs such that and , it follows

| (4.59) |

In order to proceed, we bound the first moment of the process in the same way as in (4.17), in order to get

Next, we take expectations on both sides of inequality (4.59), and use the bound (3.8), and This yields

Since , we know that . Similarly, since for all , it follows . Using this upper and lower bound on the relaxation sequence, we also see that , so that

where . Hence, defining the deterministic stopping time , we see .

(ii). Suppose , for . Then the oracle complexity to compute an such that is bounded as

Remark 4.6.

In the prior result, we employ a sampling rate where . This achieves the optimal rate of convergence. In contrast, the authors in [45] employ a sampling rate, loosely given by where or . We observe that when and , the mini-batch size grows faster than our proposed while it is comparable in the other case.

5 Applications

In this section, we compare the proposed scheme with its SA counterparts on a class of monotone two-stage stochastic variational inequality problems (Sec. 5.1) and a supervised learning problem (Sec. 5.2) and discuss the resulting performance.

5.1 Two-stage stochastic variational inequality problems

In this section, we describe some preliminary computational results obtained from the (RISFBF) method when applied to a class of two-stage stochastic variational inequality problems, recently introduced by Rockafellar and Wets [70].

Consider an imperfectly competitive market with firms playing a two-stage game. In the first stage, the firms decide upon their capacity level , anticipating the expected revenues to be obtained in the second stage in which they compete by choosing quantities à la Cournot. The second-stage market is characterized by uncertainty as the per-unit cost is realized on the spot and cannot be anticipated. To compute an equilibrium in this game, we assume that each player is able to take stochastic recourse by determining production levels , contingent on random convex costs and capacity levels . In order to bring this into the terminology for our problem, let use define the feasible set for capacity decisions of firm as . The joint profile of capacity decisions is denoted by an -tuple . The capacity choice of player is then determined as a solution to the parametrized problem (Play)

| (Play) |

where is a -smooth and convex cost function and denotes the inverse-demand function defined as , . The function denotes the optimal cost function of firm in scenario , assuming a value when the capacity level is chosen. The recourse function denotes the expectation of the optimal value of the player ’s second stage problem and is defined as

| (Rec) | ||||

A Nash equilibrium of this game is given by a tuple where for each . A simple computation shows that , and hence it is nonsmooth. In order to obtain a smoothed variant, we introduce , defined as

This is the value function of a quadratric program, requiring the maximization of an -strongly concave function. Hence, is single-valued and is -Lipschitz and -strongly monotone [71, Prop. 12.60] for all . The latter is explicitly given by

Employing this smoothing strategy in our two-stage noncooperative game yields the individual decision problem

| (Play) |

The necessary and sufficient equilibrium conditions of this -smoothed game can be compactly represented by the inclusion problem (SGEϵ)

| (SGEϵ) |

and , , and are single-valued maps given by

We note that the interchange between the expectation and the gradient operator can be invoked based on smoothness requirements (cf. [76, Th. 7.47]). The problem (SGEϵ) aligns perfectly with the structured inclusion (MI), in which is a maximal monotone map and is an expectation-valued maximally monotone map. In addition, we can quantify the Lipschitz constant of as ,where , and . Here, is the identity matrix, and 1 is the vector consisting only of ones.

Problem parameters for 2-stage SVI. Our numerics are based on specifying , , and . We consider four problem settings of ranging from (See Table 1). For each setting, the problem parameters are defined as follows.

-

(i)

Specification of . The cost parameters where and .

-

(ii)

Specification of , , and . Since when , . Let be defined as and . It follows that and .

-

(iii)

Specification of . The cost function is defined as where and Further, and is a diagonal matrix with nonnegative elements.

Algorithm specifications.

We compare (RISFBF) with a standard stochastic approximation (SA) scheme and a stochastic forward-backward-forward (SFBF) scheme. Solution quality is compared by estimating the residual function . All of the schemes were implemented in MATLAB on a PC with 16GB RAM and 6-Core Intel Core i7 processor

(2.6GHz).

(i) (SA): Stochastic approximation scheme. The (SA) scheme utilizes update (SA).

| (SA) |

where and . The operator means the orthogonal projection onto the set . Note that is randomly generated in .

(ii) (SFBF): Variance-reduced stochastic modified forward-backward scheme.

| (SFBF) |

where , . We choose a constant . We assume

for merely monotone problems and for

strongly monotone problems.

(iii) (RISFBF): Relaxed inertial stochastic forward-backward-forward scheme. We choose a constant steplength . In merely monotone settings, we utilize an increasing sequence , where , the relaxation parameter sequence defined as , and . In strongly monotone regimes, we choose a constant inertial parameter , a constant relaxation parameter , and .

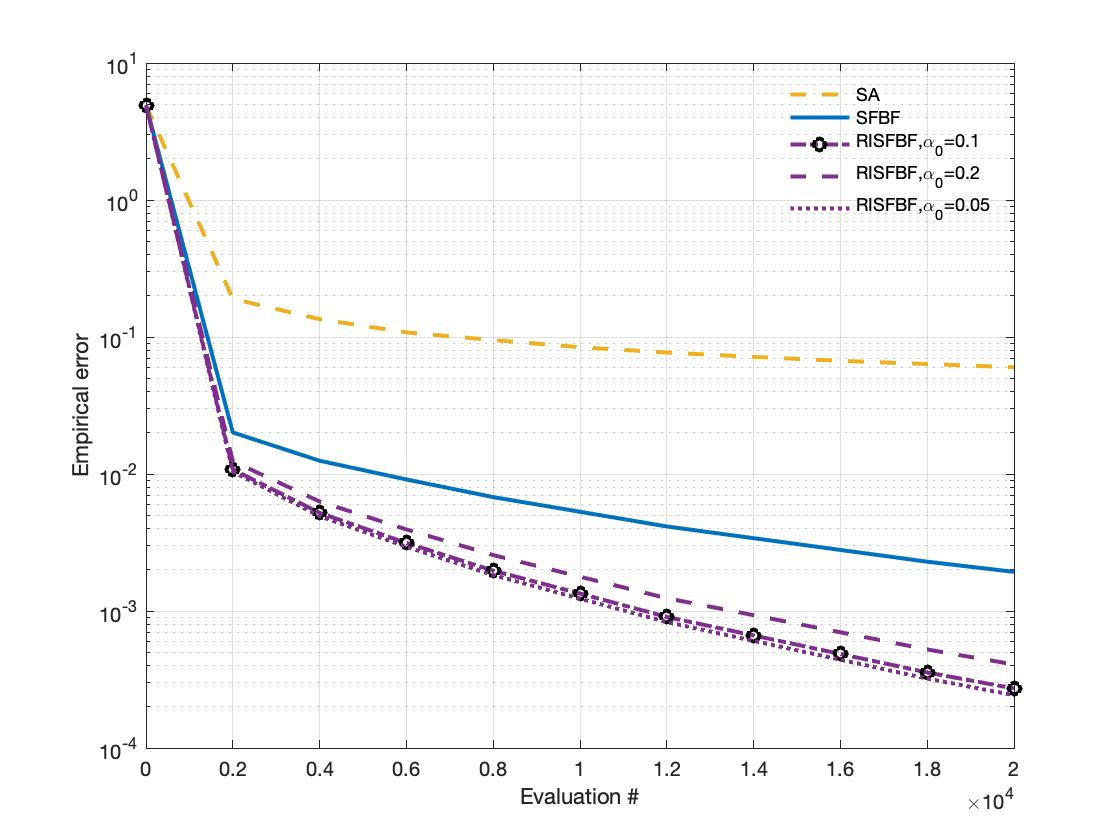

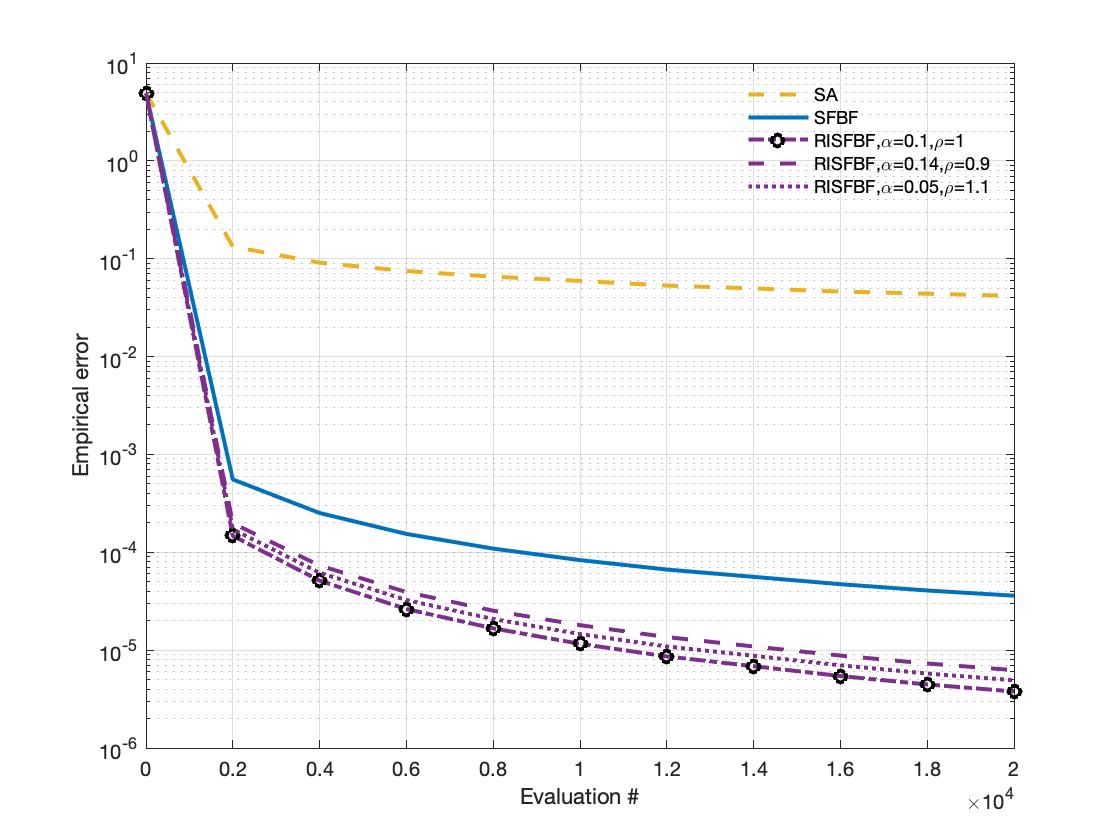

In Fig. 1, we compare the three schemes under maximal monotonicity and strong monotonicity, respectively and examine their senstivities to inertial and relaxation parameters. Both sets of plots are based on selecting .

| merely monotone, 20000 evaluations | |||||||||

| RISFBF | SFBF | SA | |||||||

| error | time | CI | error | time | CI | error | time | CI | |

| 1e1 | 2.2e-4 | 2.7 | [2.0e-4,2.5e-4] | 1.6e-3 | 2.6 | [1.3e-3,1.8e-3] | 5.3e-2 | 2.7 | [5.0e-2,5.7e-2] |

| 1e2 | 2.7e-4 | 2.7 | [2.5e-4,3.0e-4] | 1.9e-3 | 2.6 | [1.6e-3,2.1e-3] | 6.1e-2 | 2.7 | [5.8e-2,6.4e-2] |

| 1e3 | 6.9e-4 | 2.7 | [6.7e-3,7.1e-4] | 2.2e-3 | 2.6 | [2.0e-3,2.5e-3] | 7.6e-2 | 2.5 | [7.3e-2,7.9e-2] |

| 1e4 | 2.7e-3 | 2.7 | [2.5e-3,3.0e-3] | 5.9e-3 | 2.6 | [5.4e-3,6.2e-3] | 9.4e-2 | 2.6 | [9.0e-1,9.7e-1] |

| strongly monotone, 20000 evaluations | |||||||||

| RISFBF | SFBF | SA | |||||||

| error | time | CI | error | time | CI | error | time | CI | |

| 1e1 | 1.5e-6 | 2.6 | [1.3e-6,1.7e-6] | 1.5e-5 | 2.6 | [1.2e-5,1.7e-5] | 2.9e-2 | 2.5 | [2.7e-2,3.1e-2] |

| 1e2 | 3.7e-6 | 2.6 | [3.5e-6,3.9e-6] | 3.6e-5 | 2.5 | [3.3e-5,3.9e-5] | 4.1e-2 | 2.5 | [3.8e-2,4.4e-2] |

| 1e3 | 4.5e-6 | 2.6 | [4.3e-6,4.7e-6] | 5.6e-5 | 2.5 | [4.2e-6,4.7e-6] | 5.5e-2 | 2.4 | [5.2e-2,5.7e-2] |

| 1e4 | 1.4e-5 | 2.6 | [1.1e-5,1.7e-5] | 7.4e-5 | 2.5 | [7.1e-5,7.7e-5] | 6.0e-2 | 2.5 | [5.7e-2,6.3e-2] |

(a) First, from Table 1, one may conclude that on this class of problems, (RISFBF) and (SFBF) significantly outperform (SA) schemes,

which is less surprising given that both schemes employ an increasing

mini-batch sizes, leading to performance akin to that seen in deterministic

schemes. We should note that when is somewhat more complicated, the difference in run-times between SA schemes and mini-batch variants becomes for more pronounced; in this instance, the set is relatively simple to project onto and there is little difference in run-time across the three schemes.

(b) Second, we observe that while both (SFBF) and (RISFBF) schemes can

contend with poorly conditioned problems, as seen by noting that as

grows, their performance does not degenerate significantly in terms of empirical error; However, in both

monotone and strongly monotone regimes, (RISFBF) provide consistently better solutions in terms of empirical error over (SFBF). Figure 1 displays the range of

trajectories obtained for differing relaxation and inertial parameters and in

the instances considered, (RISFBF) shows consistent benefits over (SFBF).

(c) Third, since such schemes display geometric rates of convergence for strongly monotone inclusion problems, this improvement is reflected in terms of the empirical errors for strongly monotone vs monotone regimes.

5.2 Supervised learning with group variable selection

Our second numerical example considers the following population risk formulation of a composite absolute penalty (CAP) problem arising in supervised statistical learning [88]

| (CAP) |

where the feasible set is a Euclidean ball with , denotes the random variable consisting of a set of predictors and output . The parameter vector is the sparse linear hypothesis to be learned. The sparsity structure of is represented by group . When the groups in do not overlap, is referred to as the group lasso penalty [33, 46]. When the groups in form a partition of the set of predictors, then is a norm afflicted by singularities when some components are equal to zero. For any , is a sparse vector constructed by components of whose indices are in g, i.e., with few non-zero components in . Here, we assume that each group consists of elements. Introduce the linear operator , given by . Let us also define

where denotes the indicator function with respect to the set . Then (CAP) becomes

This is clearly seen to be a special instance of the convex programming problem (1.2). Specifically, we let with the standard Euclidean norm, and with the product norm

Since

the Fenchel-dual takes the form (1.3). Accordingly, a primal-dual pair for (CAP) is a root of the monotone inclusion (MI) with

involving variables.

Problem parameters for (CAP): We simulated data with , covered by 10 groups of 10 variables with 2 variables of overlap between two successive groups: . We assume the nonzeros of lie in the union of groups 4 and 5 and sampled from i.i.d. Gaussian variables. The operator is estimated by the mini-batch estimator using iid copies of the random input-output pair . Specifically, we draw each coordinate of the random vector from the standard Gaussian distribution and generate , for . In the concrete experiment reported here, the error variance is taken as . In all instances, the regularization parameter is chosen as . The accuracy of feature extraction of algorithm output is evaluated by the relative error to the ground truth, defined as

Algorithm specifications. We compare (RISFBF) with stochastic extragradient (SEG) and stochastic forward-backward-forward (SFBF) schemes and specify their algorithm parameters. Again, all the schemes are run on MATLAB 2018b on a PC with 16GB RAM and 6-Core Intel Core i7 processor (2.68GHz).

(i) (SEG): Variance-reduced stochastic extragradient scheme. Set . The (SEG) scheme [45] utilizes update (SEG).

| (SEG) |

where , . In this scheme, is chosen to be ( is the Lipschitz constant of ). We assume .

(ii) (SFBF): Variance-reduced stochastic modified forward-backward scheme. We employ the algorithm paramters employed in (i). Specifically, we

choose a constant and .

(iii) (RISFBF): Relaxed inertial stochastic forward-backward-forward scheme. Here, we employ a constant steplength , an increasing sequence , where , a relaxation parameter sequence , and assume .

| Iteration | RISFBF | SFBF | SEG | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Rel. error | CPU | Rel. error | CPU | Rel. error | CPU | ||||

| 400 | 5.4e-1 | 0.1 | 34.6 | 0.1 | 34.7 | 0.1 | |||

| 800 | 8.1e-3 | 0.5 | 1.1e-1 | 0.5 | 1.5e-1 | 0.5 | |||

| 1200 | 6.0e-3 | 1.1 | 2.4e-2 | 1.1 | 2.4e-2 | 1.1 | |||

| 1600 | 5.2e-3 | 2.0 | 2.0e-2 | 2.0 | 1.9e-2 | 2.0 | |||

| 2000 | 4.6e-3 | 3.1 | 1.6e-2 | 3.1 | 1.5e-2 | 3.1 |

-

•

The relative error and CPU time in the table is the average results of 20 runs

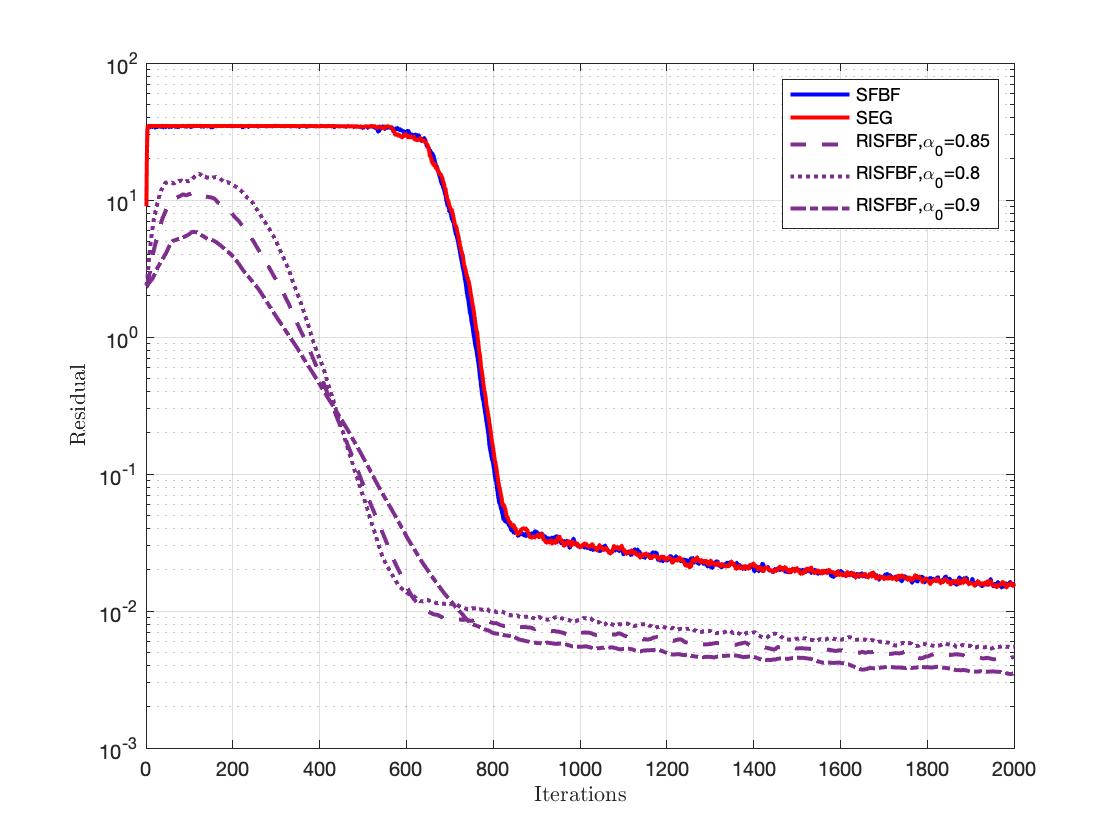

Insights. We compare the performance of the schemes in Table 2 and observe that (RISFBF) outperforms its competitors others in extracting the underlying feature of the datasets. In Fig. 2, trajectories for (RISFBF), (SFBF) and (SEG) are presented where a consistent benefit of employing (RISFBF) can be seen for a range of choices of .

6 Conclusion

In a general structured monotone inclusion setting in Hilbert spaces, we introduce a relaxed inertial stochastic algorithm based on Tseng’s forward-backward-forward splitting method. Motivated by the gaps in convergence claims and rate statements in both deterministic and stochastic regimes, we develop a variance-reduced framework and make the following contributions: (i) Asymptotic convergence guarantees are provided under both increasing and constant mini-batch sizes, the latter requiring somewhat stronger assumptions on ; (ii) When is monotone, rate statements provided in terms of a restricted gap function, inspired by the Fitzpatrick function for inclusions, show that the expected gap of an averaged sequence diminishes at the rate of and oracle complexity of computing an -solution is where ; (iii) When is strongly monotone, a non-asymptotic linear rate statement can be proven with an oracle complexity of of computing an -solution. In addition, a perturbed linear rate is also developed. It is worth emphasizing that the rate statements in the strongly monotone regime accommodate the possibility of a biased SO. Unfortunately, the growth rates in batch-size may be onerous in some situations, motivating the analysis of a polynomial growth rate in sample-size which is easily modulated. This leads to an associated polynomial rate of convergence.

Various open questions arise from our analysis. First, we exclusively focused on a variance reduction technique based on increasing mini-batches. From the point of view of computations and oracle complexity, this approach can become quite costly. Exploiting different variance reduction techniques, taking perhaps special structure of the single-valued operator into account (as in [66]), has the potential of improving the computational complexity of our proposed method. At the same time, this will complicate the analysis of the variance of the stochastic estimators considerably and consequently, we leave this as an important question for future research.

Second, our analysis needs knowledge about the Lipschitz constant . While in deterministic regimes, line search techniques have obviated such a need, such avenues are far more challenging to adopt in stochastic regimes. Efforts to address this in variational regimes have centered around leveraging empirical process theory [44]. This remains a goal of future research. Another avenue emerges in applications where we can gain a reasonably good estimate about this quantity via some pre-processing of the data (see e.g. Section 6 in [39]). Developing such an adaptive framework robust to noise is an important topic for future research.

Acknowledgments

The authors thank Radu I. Bot̨ and Robert E. Csetnek for valuable discussions on this topic. Special thanks to Patrick Johnstone for helping us to clarify the discussion in Section 4.2.

Appendix A Technical Facts

Lemma A.1.

For and scalars with , it holds that

| (A.1) |

We recall the Minkowski inequality: For and ,

| (A.2) |

In the convergence analysis, we use the Robbins-Siegmund Lemma [68, Lemma 11, pg. 50].

Lemma A.2 (Robbins-Siegmund).

Let be a discrete stochastic basis. Let and be such that for all ,

Then converges a.s. to a random variable , and .

The next technical lemma will be needed in deriving a linear convergence result.

Lemma A.3.

Let and . Then, if , it holds true that for all .

Proof.

We want to find a positive constant such that for all . Choosing larger than this, gives a valid value. Rearranging, this is equivalent to for all , or, which is still equivalent to Define the extended-valued function by if , and if . Then, for all , simple calculus show and . Hence, is a convex function with a unique minimum and a corresponding function value . Hence, for , we see that , and thus for all .

References

- Attouch and Cabot [2019] Hedy Attouch and Alexandre Cabot. Convergence of a relaxed inertial forward–backward algorithm for structured monotone inclusions. Applied Mathematics & Optimization, 80(3):547–598, 2019. doi: 10.1007/s00245-019-09584-z. URL https://doi.org/10.1007/s00245-019-09584-z.

- Attouch and Cabot [2020] Hedy Attouch and Alexandre Cabot. Convergence of a relaxed inertial proximal algorithm for maximally monotone operators. Mathematical Programming, 184(1):243–287, 2020. doi: 10.1007/s10107-019-01412-0. URL https://doi.org/10.1007/s10107-019-01412-0.

- Attouch and Maingé [2011] Hedy Attouch and Paul-Emile Maingé. Asymptotic behavior of second-order dissipative evolution equations combining potential with non-potential effects. ESAIM: Control, Optimisation and Calculus of Variations, 17(3):836–857, 2011.

- Attouch and Peypouquet [2019] Hedy Attouch and Juan Peypouquet. Convergence of inertial dynamics and proximal algorithms governed by maximally monotone operators. Mathematical Programming, 174(1):391–432, 2019. ISSN 1436-4646. doi: 10.1007/s10107-018-1252-x. URL https://doi.org/10.1007/s10107-018-1252-x.

- Attouch et al. [2010] Hédy Attouch, Luis M. Briceno-Arias, and Patrick L. Combettes. A parallel splitting method for coupled monotone inclusions. SIAM Journal on Control and Optimization, 48(5):3246–3270, 2021/03/28 2010. doi: 10.1137/090754297. URL https://doi.org/10.1137/090754297.

- Auslender et al. [1974] A. Auslender, M. Gourgand, and A. Guillet. Resolution numerique d’inegalites variationnelles. In Lecture Notes in Economics and Mathematical Systems (Mathematical Economics), 1974.

- Barty et al. [2007] Kengy Barty, Jean-Sébastien Roy, and Cyrille Strugarek. Hilbert-valued perturbed subgradient algorithms. Mathematics of Operations Research, 32(3):551–562, 2020/11/23 2007. doi: 10.1287/moor.1070.0253. URL https://doi.org/10.1287/moor.1070.0253.

- Barty et al. [2009] Kengy Barty, Jean-Sébastien Roy, and Cyrille Strugarek. A stochastic gradient type algorithm for closed-loop problems. Mathematical Programming, 119(1):51–78, 2009. doi: 10.1007/s10107-007-0201-x. URL https://doi.org/10.1007/s10107-007-0201-x.

- Bauschke and Combettes [2016] Heinz H. Bauschke and Patrick L. Combettes. Convex Analysis and Monotone Operator Theory in Hilbert Spaces. Springer - CMS Books in Mathematics, 2016.

- Börgens and Kanzow [2021] Eike Börgens and Christian Kanzow. Admm-type methods for generalized nash equilibrium problems in hilbert spaces. SIAM J. Optim., pages 377–403, January 2021. ISSN 1052-6234. doi: 10.1137/19M1284336. URL https://doi.org/10.1137/19M1284336.

- Borwein and Dutta [2016] Jonathan M Borwein and Joydeep Dutta. Maximal monotone inclusions and fitzpatrick functions. Journal of Optimization Theory and Applications, 171(3):757–784, 2016.

- Bot and Csetnek [2016] Radu Ioan Bot and Erno Robert Csetnek. An inertial forward-backward-forward primal-dual splitting algorithm for solving monotone inclusion problems. Numerical Algorithms, 71(3):519–540, 2016. doi: 10.1007/s11075-015-0007-5. URL https://doi.org/10.1007/s11075-015-0007-5.

- Boţ and Csetnek [2016] Radu Ioan Boţ and ErnöRobert Csetnek. Second order forward-backward dynamical systems for monotone inclusion problems. SIAM Journal on Control and Optimization, 54(3):1423–1443, 2021/06/24 2016. doi: 10.1137/15M1012657. URL https://doi.org/10.1137/15M1012657.

- Bot et al. [2020] Radu Ioan Bot, Michael Sedlmayer, and Phan Tu Vuong. A relaxed inertial forward-backward-forward algorithm for solving monotone inclusions with application to gans. arXiv preprint arXiv:2003.07886, 2020.

- Boţ et al. [2021] Radu Ioan Boţ, Panayotis Mertikopoulos, Mathias Staudigl, and Phan Tu Vuong. Minibatch forward-backward-forward methods for solving stochastic variational inequalities. Stochastic Systems, 2021. doi: 10.1287/stsy.2019.0064. URL https://doi.org/10.1287/stsy.2019.0064.

- Briceño-Arias and Combettes [2011] Luis M. Briceño-Arias and Patrick L. Combettes. A monotone+skew splitting model for composite monotone inclusions in duality. SIAM Journal on Optimization, 21(4):1230–1250, 2011. doi: 10.1137/10081602X. URL https://doi.org/10.1137/10081602X.

- Briceno-Arias and Combettes [2013] Luis M Briceno-Arias and Patrick L Combettes. Monotone operator methods for Nash equilibria in non-potential games, pages 143–159. Springer, 2013.

- Burachik and Millán [2020] Regina S. Burachik and R. Díaz Millán. A projection algorithm for non-monotone variational inequalities. Set-Valued and Variational Analysis, 28(1):149–166, 2020. doi: 10.1007/s11228-019-00517-0. URL https://doi.org/10.1007/s11228-019-00517-0.

- Chen et al. [2014] Yunmei Chen, Guanghui Lan, and Yuyuan Ouyang. Optimal primal-dual methods for a class of saddle point problems. SIAM Journal on Optimization, 24(4):1779–1814, 2021/04/27 2014. doi: 10.1137/130919362. URL https://doi.org/10.1137/130919362.

- Chen et al. [2017] Yunmei Chen, Guanghui Lan, and Yuyuan Ouyang. Accelerated schemes for a class of variational inequalities. Mathematical Programming, 2017. doi: 10.1007/s10107-017-1161-4. URL https://doi.org/10.1007/s10107-017-1161-4.

- Combettes and Pesquet [2012] Patrick L Combettes and Jean-Christophe Pesquet. Primal-dual splitting algorithm for solving inclusions with mixtures of composite, lipschitzian, and parallel-sum type monotone operators. Set-Valued and variational analysis, 20(2):307–330, 2012.

- Combettes and Pesquet [2015] Patrick L. Combettes and Jean-Christophe Pesquet. Stochastic quasi-fejér block-coordinate fixed point iterations with random sweeping. SIAM Journal on Optimization, 25(2):1221–1248, 2020/07/11 2015. doi: 10.1137/140971233. URL https://doi.org/10.1137/140971233.

- Combettes and Pesquet [2019] Patrick L. Combettes and Jean-Christophe Pesquet. Stochastic quasi-fejér block-coordinate fixed point iterations with random sweeping ii: mean-square and linear convergence. Mathematical Programming, 174(1):433–451, 2019. doi: 10.1007/s10107-018-1296-y. URL https://doi.org/10.1007/s10107-018-1296-y.

- Cui and Shanbhag [2021a] Shisheng Cui and Uday V Shanbhag. On the computation of equilibria in monotone and potential stochastic hierarchical game. arXiv preprint arXiv:2104.07860, 2021a.

- Cui and Shanbhag [2021b] Shisheng Cui and Uday V Shanbhag. On the analysis of variance-reduced and randomized projection variants of single projection schemes for monotone stochastic variational inequality problems. Set-Valued and Variational Analysis (to appear), 2021b.

- Davis and Drusvyatskiy [2019] Damek Davis and Dmitriy Drusvyatskiy. Stochastic model-based minimization of weakly convex functions. SIAM Journal on Optimization, 29(1):207–239, 2019.

- Diakonikolas et al. [2021] Jelena Diakonikolas, Constantinos Daskalakis, and Michael Jordan. Efficient methods for structured nonconvex-nonconcave min-max optimization. International Conference on Artificial Intelligence and Statistics, pages 2746–2754, 2021.

- Duvocelle et al. [2018] Benoit Duvocelle, Panayotis Mertikopoulos, Mathias Staudigl, and Dries Vermeulen. Learning in time-varying games. arXiv preprint arXiv:1809.03066, 2018.

- Facchinei and Pang [2003] Francisco Facchinei and Jong-shi Pang. Finite-Dimensional Variational Inequalities and Complementarity Problems - Volume I and Volume II. Springer Series in Operations Research, 2003.

- Fitzpatrick [1988] Simon Fitzpatrick. Representing monotone operators by convex functions. In Workshop/Miniconference on Functional Analysis and Optimization, pages 59–65. Centre for Mathematics and its Applications, Mathematical Sciences Institute …, 1988.

- Franci et al. [2020] B. Franci, M. Staudigl, and S. Grammatico. Distributed forward-backward (half) forward algorithms for generalized nash equilibrium seeking. In 2020 European Control Conference (ECC), pages 1274–1279, 2020. doi: 10.23919/ECC51009.2020.9143676.

- Friedlander and Schmidt [2012] M. P. Friedlander and M. Schmidt. Hybrid deterministic-stochastic methods for data fitting. SIAM J. Scientific Computing, 34(3):A1380–A1405, 2012.

- Friedman et al. [2001] Jerome Friedman, Trevor Hastie, and Robert Tibshirani. The elements of statistical learning, volume 1. Springer series in statistics Springer, Berlin, 2001.

- Friesz et al. [1993] Terry L. Friesz, David Bernstein, Tony E. Smith, Roger L. Tobin, and B. W. Wie. Variational inequality formulation of the dynamic network user equilibrium. Operations Research, 41(1):179–191, 1993.

- Fukushima [1996] Masao Fukushima. The primal douglas-rachford splitting algorithm for a class of monotone mappings with application to the traffic equilibrium problem. Mathematical Programming, 72(1):1–15, 1996. ISSN 1436-4646. doi: 10.1007/BF02592328. URL https://doi.org/10.1007/BF02592328.

- Gadat et al. [2018] Sébastien Gadat, Fabien Panloup, and Sofiane Saadane. Stochastic heavy ball. Electronic Journal of Statistics, 12(1):461 – 529, 2018. doi: 10.1214/18-EJS1395. URL https://doi.org/10.1214/18-EJS1395.

- Geiersbach and Pflug [2019] Caroline Geiersbach and Georg Ch. Pflug. Projected stochastic gradients for convex constrained problems in hilbert spaces. SIAM Journal on Optimization, 29(3):2079–2099, 2020/11/23 2019. doi: 10.1137/18M1200208. URL https://doi.org/10.1137/18M1200208.