Bayesian iterative screening in ultra-high dimensional settings

Abstract

Variable selection in ultra-high dimensional linear regression is often preceded by a screening step to significantly reduce the dimension. Here a Bayesian variable screening method (BITS) is developed. BITS can successfully integrate prior knowledge, if any, on effect sizes, and the number of true variables. BITS iteratively includes potential variables with the highest posterior probability accounting for the already selected variables. It is implemented by a fast Cholesky update algorithm and is shown to have the screening consistency property. BITS is built based on a model with Gaussian errors, yet, the screening consistency is proved to hold under more general tail conditions. The notion of posterior screening consistency allows the resulting model to provide a good starting point for further Bayesian variable selection methods. A new screening consistent stopping rule based on posterior probability is developed. Simulation studies and real data examples are used to demonstrate scalability and fine screening performance.

Key words: Forward regression; Large small ; Screening consistency; Spike and slab; Sure independent screening; Variable selection.

1 Introduction

These days, in diverse disciplines, data sets with hundreds of thousands of variables are commonly arising although only a very few of these variables are believed to be relevant for the response. Thus variable selection in linear regression has been a major topic of research over the last two decades in both frequentist and Bayesian statistics. A common approach to variable selection as well as coefficient estimation is by penalizing a loss function. These shrinkage methods include, but are not limited to, the ridge regression (Hoerl and Kennard, 1970), the popular Lasso (Tibshirani, 1996), the bridge regression (Huang et al., 2008), the SCAD (Fan and Li, 2001), the elastic net (Zou and Hastie, 2005), the Dantzig selector (Candes and Tao, 2007) and the adaptive Lasso (Zou, 2006).

The Lasso estimate can be interpreted as the mode of a posterior density when independent Laplace priors are assumed on the regression coefficients (Tibshirani, 1996). Using a scale mixture of normal distributions representation for the Laplace distribution, a hierarchical Bayesian Lasso model can be formulated (Park and Casella, 2008). Several such Bayes and empirical Bayes penalized regression methods have been developed in the literature. See, for example, Li and Lin (2010), Kyung et al. (2010), Xu and Ghosh (2015) and Roy and Chakraborty (2017). Another approach to Bayesian variable selection is using auxiliary indicator variables (1 indicating presence and 0 indicating absence of the corresponding covariate in the model) to obtain a ‘spike and slab’ prior on the regression coefficients (see e.g. Mitchell and Beauchamp, 1988; George and McCulloch, 1993; Yuan and Lin, 2005; Ishwaran and Rao, 2005; Liang et al., 2008; Johnson and Rossell, 2012; Ročková and George, 2014; Narisetty and He, 2014; Roy et al., 2018; Shin et al., 2018; Li et al., 2020). Here the ‘spike’ corresponds to the probability mass concentrated at zero or around zero for the variables vulnerable to deletion and the ‘slab’ specifies prior uncertainty for coefficients of other variables. We will discuss one such model in details in Section 2.1. Analysis using such models determines (selects) the most promising variables by summarizing the posterior density of the indicator variables and/or the regression coefficients.

In the ultra-high dimensional settings where the number of variables () is much larger than the sample size (), previously mentioned variable selection methods may not work and the computational cost for large-scale optimization or Markov chain Monte Carlo (MCMC) exploration (in the Bayesian methods) becomes too high to afford. This is why, in practice, a computationally inexpensive screening is performed before conducting a refined model selection analysis. Motivated by these, Fan and Lv (2008) proposed the sure independence screening (SIS) method where marginal Pearson correlations between the response and the variables are used to screen out unimportant variables, and thus rapidly reduce the dimension to a manageable size. The SIS method has been extended to generalized linear models (Fan and Song, 2010) and additive models (Fan et al., 2011) among others. Various other correlation measures as for example general correlation (Hall and Miller, 2009), distance correlation (Li et al., 2012b), rank correlation (Li et al., 2012a), tilted correlation (Cho and Fryzlewicz, 2012; Lin and Pang, 2014) and quantile partial correlation (Ma et al., 2017) have also been proposed to rank and screen variables. Chang et al. (2013) discussed a marginal likelihood ratio test, Mai and Zou (2013) used Kolmogorov-Smirnov statistic, Xu and Chen (2014) suggested maximum likelihood estimate to remove unimportant variables, respectively. He et al. (2013) discussed a nonparametric screening method, Zhou et al. (2019) used a divergence based screening method and Mukhopadhyay and Dunson (2020) proposed the randomized independence screening. Wang (2009) studied the popular forward regression (FR) method (see also Hao and Zhang, 2014) and Wang and Leng (2016) proposed the high dimensional ordinary least squares projection (HOLP) for screening variables in ultra-high dimensional settings. However, currently, there is no available screening method that allows incorporating prior information on the variables. In this paper we develop a Bayesian screening method.

In order to develop a Bayesian screening method, we consider a hierarchical model with zero inflated mixture priors which are special cases of the spike and slab priors. As mentioned earlier, variants of these hierarchical models have previously been used for variable selection and MCMC algorithms are generally used to approximate posterior probabilities. It is known that MCMC chains suffer from slow mixing in high dimensional variable selection models and consequently due to increasing (per iteration) computational cost it may be unfeasible to obtain enough samples to accurately estimate the posterior probabilities. On the other hand, the sequential screening method proposed here called Bayesian iterative screening (BITS) does not involve any MCMC sampling. Under the hierarchical model considered here, the marginal posterior density of the latent indicator vector is analytically available up to a normalizing constant. BITS uses this density to iteratively include variables that have maximum posterior inclusion probability conditional on the already selected variables. The computation of the posterior probabilities is done by a one-step delayed Cholesky update. Wang and Leng (2016) mention that there are two important aspects of a successful screening method: computational efficiency and screening consistency property under flexible conditions. Even though BITS allows incorporation of prior information, it is computationally competitive with the frequentist screening methods like HOLP. The hierarchical model on which BITS is based assumes Gaussian errors. But we show that BITS has screening consistency even under the more general -exponential tail condition on the errors. Also, we do not assume that the marginal correlations for the important variables are bounded away from zero—an assumption that is often violated in practice but used for showing screening consistency of SIS. Finally, we introduce the notion of posterior screening consistency and discuss its usefulness in Bayesian high dimensional data analysis.

BITS although is similar in spirit with the popular, classical variable screening method, namely forward regression (FR) (Wang, 2009) there are important differences between the two. By introducing the notion of ridge partial correlations, we show that unlike FR, BITS takes into account ridge partial variances to include potential variables. Also, by varying the ridge penalty, BITS can include groups of correlated important variables whereas FR selects only a candidate from each group which is not desirable for a screening method. For deciding the screened model size Wang (2009) considers the extended BIC (EBIC) criterion developed by Chen and Chen (2008). In addition to the use of EBIC and the liberal choice of having a model as large as the sample size, we construct a new stopping rule based on the posterior probability (PP). Furthermore, we prove that the PP stopping rule is screening consistent again under the general -exponential tail condition on the errors. Through examples we demonstrate how the PP criterion can lead to informative screening by specifying suitable prior hyperparameter values.

The rest of the paper is organized as follows. We describe the hierarchical model and BITS in Section 2. We establish screening consistency properties of BITS in Section 2.3 as well as discuss the notion of posterior screening consistency. In Section 2.4 we emphasize the contrast between the proposed method and FR. In Section 2.5 we describe different possible stopping rules for BITS and establish screening consistency of the proposed PP stopping rule. Section 3 lays out the fast statistical computation algorithm for BITS. Extensive simulation studies are used to study the effect of the hyperparameters on the properties of BITS (Section 4.2) and to highlight the competitiveness of BITS with several other screening methods (Section 4.3). A real data set from a genomewide association studies with more than half a million markers is analyzed in Section 5. Some concluding remarks are given in Section 6. Several theoretical results and proofs of the theorems are given in the Appendix. A supplement document containing the proofs of some of the theoretical results and some additional simulation results is provided with sections referenced here with the prefix ‘S’. The methodology proposed here is implemented as a function named bits in an accompanying R package bravo (Li et al., 2021).

2 A Bayesian iterative screening method

2.1 A hierarchical Gaussian regression model

Let the vector denote the vector of responses and the matrix denote the matrix of covariate values with vector of partial regression coefficients The Bayesian variable selection model we consider here assumes latent indicator vector such that is included in the linear regression model if and only if and that the conditional distribution of given and is a multivariate Gaussian distribution given by

| (1) |

where is the sub-matrix of that consists of columns of corresponding to model is the vector that contains the regression coefficients for model and is the model size. However, the original covariates may have unbalanced scales and we reparameterize the above model using a scaled covariate matrix. That is, we let where is the vector column means of and is the diagonal matrix whose th diagonal entry is the standard deviation of Also let and Similarly, is the sub-matrix of corresponding to model . We then assume the Bayesian Gaussian hierarchical model

| (2a) | ||||

| (2b) | ||||

| (2c) | ||||

| (2d) | ||||

In this hierarchical setup a popular non-informative prior is set for in (2b) and a conjugate independent normal prior is used on given in (2c) with controlling the precision of the prior independently from the scales of measurements. Note that under this prior, if a covariate is not included in the model, the prior on the corresponding regression coefficient degenerates at zero. In (2d) an independent Bernoulli prior is set for , where reflects the prior inclusion probability of each predictor. We assume and are known non-random functions of and .

Our Bayesian screening method hinges on the fact that given it is possible to integrate out other variable analytically. Indeed, integrating out we derive the following marginal distribution of given ,

| (3) | |||||

where, is a constant depending only on the sample size , , and . The hierarchical Gaussian regression model (2) and its variants have been used extensively and exclusively for variable selection. In particular, several works have established strong model selection consistency results (Narisetty and He, 2014) under the ultra-high dimensional setup that is considered here. In practice, however, these methods are mostly used after reducing the number of covariates using frequentist screening methods that are not driven by the same Bayesian hierarchical model. In the next section we describe the first ever Bayesian screening method based on the hierarchical model (2).

2.2 The BITS algorithm

We now describe our proposed screening method. This method uses the posterior density of , which is available up to a normalizing constant. Indeed, if is assumed fixed, then

| (4) |

that is,

| (5) |

Let be the th dimensional canonical basis vector, that is, the th element of is one, and all other elements are zero. In the first step, we select the variable such that

| (6) |

Thus we select the unit vector with highest posterior probability. In the next step, we select the variable with

Note that for ,

| (7) |

So, and are maximized at the same . Thus, in the second step, we choose the variable which has maximum posterior inclusion probability given that (the variable selected in the first step) is included in the model. An efficient computational method for calculating using a fast Cholesky update is given in Section 3. One problem with marginal correlation based screening methods like SIS (Fan and Lv, 2008) is that unimportant variables that are correlated with important variables may get selected. This is not likely to happen in our proposed screening procedure as the only variables that have high (conditional) posterior inclusion probability after taking into account the selected variables survive the screening. Let be the vector at the th step. Below we describe the st iteration of the BITS. Iteration of the screening algorithm:

Given , let

| (8) |

Set .

Using the same argument as (7), the st variable has the highest posterior probability of being included given that have already been included in the model. BITS although is not guaranteed to produce the posterior mode, or any other standard summary measures of the posterior distribution , in the next section we show that it enjoys screening consistency.

Remark 1.

Since,

with , the first step of the BITS algorithm, given in (6), selects the variable with largest marginal correlation as in Fan and Lv’s (2008) SIS algorithm.

2.3 Screening consistency of BITS

Ideally, as the sample size increases we would like all the important variables to be included in after a reasonable number of steps. The notion of frequentist screening consistency (Fan and Lv, 2008; Wang, 2009) states that if for some subset then should converge to as under some regularity conditions. In order to state the assumptions and the results more rigorously, we use the following notations. Abusing notation, we interchangeably use a model either as a -dimensional binary vector or as a set of indices of non-zero entries of the binary vector. For models and denotes the complement of the model , and denote the union (intersection) of and . For we say if and if . For two real sequences and , means for some constant ; (or ) means ; (or ) means . Also for any matrix , let and denote its minimum and maximum eigenvalues, respectively, and let be its minimum nonzero eigenvalue. Again, abusing notations, for two real numbers and , and denote max and min respectively. Finally, let

2.3.1 Orthogonal design with Gaussian errors

We first explore the notion of frequentist screening consistency in the simple case where and the design matrix is orthogonal, i.e., The following theorem shows that under a Gaussianity assumption and some mild conditions on the effects sizes, BITS include all and only the important variables in the first steps.

Theorem 1.

Suppose where for some and Then for any as

Such a strong conclusion holds for the orthogonal design because the variables are uncorrelated and hence the marginal correlations are asymptotically ordered by the magnitudes of the regression coefficients (Fan and Lv, 2008). Furthermore, the orthogonality restricts to be at most . Thus, it is unrealistic to expect the same conclusion to hold in general situations. In particular, note that the first variable included is the one with the highest absolute marginal correlation with the response (Remark 1). There are ample examples of realistic designs (Fan and Lv, 2008; Wang et al., 2021) where an unimportant variable has the highest absolute marginal correlation with the response.

2.3.2 Screening consistency in more general cases

Although BITS is developed under the Gaussianity assumption on for computational tractability, we would like to establish screening consistency even under more general tail conditions. As we shall see, the tail behavior of the error distribution plays a crucial role in proving screening consistency. To that end, we consider the family of distributions with -exponential tail condition (Wang and Leng, 2016) given below.

Definition 1 (-exponential tail condition).

A zero-mean distribution is said to have -exponential tail, if there exists a function such that for any , with , and we have where

This tail condition is assumed by Wang and Leng (2016) in establishing screening consistency of their HOLP screening method. In particular, as shown in Vershynin (2012), for standard normal distribution, when is sub-Gaussian for some constant depending on and when is sub-exponential distribution for some constant depending on Finally, when only first moments of are finite,

We assume the following set of conditions:

-

C1

where is the true model, , which has -exponential tail with unit variance.

-

C2

and where is the largest eigenvalue of .

-

C3

There exist and such that ,

where and is the smallest nonzero eigenvalue of with

Although our assumption on is related only to the tail behavior of the error distribution, it is evident that under sub-Gaussian or sub-exponential tailed , BITS is screening consistent in the ultra-high dimensional setting. For example, suppose , for some and Also, suppose for some constant . When is sub-Gaussian, simple calculations show that a sufficient condition for (C1)–(C3) is that if and if If is subexponential, a sufficient condition is if and if which is slightly more stringent than the sub-Gaussian case. We now present the screening consistency result.

Theorem 2.

Under conditions (C1)–(C3), there exists such that for all sufficiently large

where

Note that, the limit of is bounded above by almost everywhere which is bounded by C2. Thus it is easy to see from C3 that That is, with overwhelmingly large probability, the true model is included in at most many steps. However, when higher order moments of exist, further lower bounds to can be obtained as described in the following corollary.

Corollary 1.

Suppose conditions (C1)–(C3) holds. If further, then with Var, and a constant for all sufficiently large

2.3.3 Posterior screening consistency

The screening consistency considered in Sections 2.3.1 and 2.3.2 are in the frequentist sense and therefore are not guaranteed to be fidelitous to the posterior inference. In this section we discuss the concept of posterior screening consistency (see also Song and Liang, 2015, Theorem 3). We start with the following definition.

Definition 2.

A sequence of models with is said to be posterior screening consistent if

| (9) |

in probability as where is the set of all sub-models of containing

In other words, with probability tending to 1, the posterior mass of is entirely supported on models which are sub-models of Considering that there are originally possible models, this can be a great reduction in the search space for models with high posterior probabilities. Typically Bayesian variable selection algorithms search for the posterior mode and other high-posterior probability models. Many competitive algorithms are available to search for the best model including, but surely not limited to, the stochastic shotgun algorithm (Hans et al., 2007), simplified stochastic shotgun algorithm (Shin et al., 2018), shotgun with embedded screening (Li et al., 2020), Gibbs sampling (Narisetty and He, 2014) and Metropolis-Hastings algorithm (Zhou and Guan, 2019). Since the size () of the model space grows exponentially with the number of variables, due to computational cost and convergence issues of these iterative algorithms, when dealing with high dimensional data sets, generally a screening step is performed before applying a Bayesian variable selection algorithm. For example, Narisetty and He (2014), in their real data example, use SIS to reduce the number of variables from 22,575 to 400 before applying their variable selection algorithm. One important aspect of posterior screening consistency is that the best model (in terms of posterior probability) for variable selection can be searched among a much smaller number of models instead of among the humongous number () of all possible models. Thus a posterior screening consistent model can serve as an excellent starting point for implementing further Bayesian variable selection methods.

In the above we have described important practical consequences of using posterior screening consistent algorithms. We now discuss conditions guaranteeing such consistency. In the context of ultra-high dimensional Bayesian variable selection, under different hierarchical model setups, recently several articles have established strong (posterior) selection consistency, that is, in probability as (see e.g. Narisetty and He, 2014; Yang et al., 2016; Shin et al., 2018; Li et al., 2020). Thus under strong selection consistency, posterior probability of the true model goes to one as . We have the following lemma.

Lemma 1.

If a sequence of models is screening consistent and strong selection consistency holds then is posterior screening consistent.

Proof.

For given , denoting the events and by and respectively, we have Then the proof follows since and as . ∎

2.4 Contrast with the forward regression method

BITS although is similar in spirit of the forward selection, the step-wise regression method, there are significant differences between BITS and the FR method of Wang (2009). Firstly, under the conditions of Wang (2009), BITS is screening consistent:

Lemma 2.

Under the conditions of Wang (2009), that is, with for some finite constant , for some finite constant , and , , then C3 holds with .

A proof of Lemma 2 is given in Section S1.1 of the supplement. We indeed prove that the lemma holds under a weaker condition of In order to show the contrasts between BITS and FR, we introduce the notion of ridge partial correlations.

Definition 3.

For any and , the ridge partial correlation between and given with ridge penalty is given by

where

is the ridge (sample) partial variance of given ,

and

Remark 3.

When and is exactly the (sample) partial correlation between and after eliminating the effects of , and the ridge partial sample variances ’s are exactly the (sample) partial variances of ’s given .

In fact, BITS can be reformulated using these ridge sample partial correlations and ridge sample partial variances. To that end, we first show how the log-marginal posterior probability increments depend on the ridge partial correlations and partial variances.

Lemma 3.

For the model (2), for any and

Consequently, under the independent prior, having chosen model the BITS method chooses the candidate index that maximizes over This is clearly different from the forward screening method of Wang (2009) where it only maximizes the absolute partial correlations In particular, BITS also takes into consideration the (sample) partial variances of each given the already included variables. Thus, between two candidates which have the same partial correlations with the response given already included variables, the one with smaller conditional variance is preferred. However, if the partial correlations with the response are different then because of the presence of the the multiplier the effect of the conditional variance is practically insignificant. Furthermore, by shrinking the effects using the ridge penalty, BITS can include groups of important variables that are highly correlated among themselves in contrast to FR which would only select a candidate variable from the group. Finally, note that during screening it could be useful to be liberal and include more than variables. This however, is not possible by FR because all models of size bigger than have zero residual sum of squares. BITS, on the other hand, allows to have a screened model of size bigger than In different simulation examples in section 4.3, we demonstrate that BITS performs much better than FR.

2.5 Stopping criteria

Note that BITS provide a sequence of predictor indices A practical question is when to stop the algorithm. Theorem 2 suggests that the first indices contain the true model with overwhelming probability. However, there is nothing to stop us from being liberal and include the first indices

The aforementioned rule is not affected by the prior inclusion probability We now propose a new stopping rule, called the posterior probability (PP) criterion that depends on . As we expect the important variables to be included early, the BITS algorithm is expected to provide a sequence of nested models with increasing posterior probabilities until all the important variables are included. Thus we may stop BITS when the first drop occurs in these posterior probabilities, that is, we stop at iteration

Since , the PP criterion never selects more than variables. Under the orthogonal design described in Section 2.3.1, we saw that with probability tending to one, BITS include all and only the important variables in the first steps. In addition, we will now prove that the PP criterion stops right after steps.

Theorem 3.

If the conditions for Theorem 1 hold and in addition, that and that there exists such that for some . Then as

However, in general, as we have seen in Section 2.3, BITS may include unimportant variables before it includes all the important variables. Thus it is unrealistic to require that the conclusions of the previous theorem holds in the more general case. However, the following theorem guarantees that is screening consistent.

Theorem 4.

Under conditions (C1)–(C3), there exists a positive constant such that for all sufficiently large

where

Later in Section 4.2 we discuss how with proper choices of the hyperparameters, the PP rule can provide an informative screening method using BITS. Alternatively, Wang (2009) and Wang and Leng (2016) also promote the use of EBIC (Chen and Chen, 2008). Under this stopping rule, the screening is stopped at the smallest EBIC, that is, at where for , and is the ordinary least squares residual sum of squares from regression of on the first screened variables. Evidently, due to its ultra-high dimensional penalty, EBIC is expected to be very conservative and yield small screened models. Compared to the PP rule, the EBIC rule is computationally expensive as it requires a model of size . On the other hand, a similar variant of the PP criterion can be to choose the model according to the largest drop in the posterior probability among the first steps, that is, the model size is

2.6 BITS for other priors

A popular alternative to the independent normal prior in (2c) is the Zellner’s -prior (Zellner, 1986) for indexed by a hyperparameter under the assumption that all submatrices of are non-singular. That is, we also consider the hierarchical model (2) where the prior in (2c) is replaced with whence the marginal density becomes

It is evident that the Zellner’s -prior provides the same screening path as FR because for fixed the posterior density under Zellner’s prior is a monotonic decreasing function of the regression sum of squares Also, the Zellner’s -prior does not allow to have screened models of size more than

Similarly, BITS can easily accommodate beta-binomial prior distribution on where is the beta function, and Since the beta-binomial prior also depend on only via it does not have any effect on the screening path of BITS for a given

Recently, Kojima and Komaki (2016) have proposed a class of discrete determinantal point process priors on the model space that discourages simultaneous selection of collinear predictors. The founding member of this class of priors is given by where controls the prior expectation of the model size. A value of promotes larger models, while promotes smaller models. Although Kojima and Komaki (2016) have studied the prior when it can be also used when In particular, puts zero prior probability on all models of size greater than Notice that this prior is not a function of and hence will have an effect on the BITS screening path.

3 Fast statistical computation

In this section we describe how BITS is implemented in practice. One major challenge in BITS is the computation of posterior probabilities of models for all in the st iteration. We show how these can be computed in minimal computational complexity using a one-step delayed Cholesky updates.

Before delving into the algorithm, let us define the notation and as the element-wise multiplication and division between two vectors. Also when adding or subtracting a scalar to or from each entry of a vector we use the traditional ‘’ and ‘’ operators. We also denote by the vector which can be simply computed as without having to store Also for greater numerical stability, we scale the vector so that although the algorithm is described without this assumption.

In the first iteration, and thus Let denote the Cholesky factor of Also let and let

denote up to an additive constant. Under the PP stopping rule, we stop if the right side being up to the same additive constant.

Next, we also add the second index before going into a loop. To that end, let

and where the square root is computed element-wise. Let Then,

Set and compute up to an additive constant as

Under the PP stopping rule, we stop if

For until stopping we

-

–

Compute where

The order of the columns is important because the Cholesky factor is computed according the screening path. -

–

The Cholesky factor of up to an ordering of the columns, is given by

-

–

Update

-

–

Set

-

–

Update and set

-

–

Update

-

–

Set where

-

–

Compute up to an additive constant as

As before, under the PP stopping criterion, we stop at the th iteration and return if

Overall, the computational complexity in the th iteration is Assuming the worse case scenario when the number of iterations is the total computational cost is If is sparse, then this reduces to where is the number of non-zero entries in This is same as the computational complexity of HOLP as it computes where computing incurs a cost of and computing incurs a cost of Also the computational complexity of robust rank correlation screening (Li et al., 2012a) is In contrast, the computational complexities of iterated sure independence screening (Fan and Lv, 2008) and tilting procedures (Cho and Fryzlewicz, 2012; Lin and Pang, 2014) are much higher. Furthermore, the memory requirement of BITS, in addition to storing the original matrix is mainly for storing the Cholesky factors s. This is same as the memory requirement of HOLP even if the matrix is not explicitly stored. The complexity of the FR method as implemented in the github repository ‘screening’111https://github.com/wwrechard/screening by Wang and Leng (2016) in the th iteration is although a faster implementation of FR can be achieved by the delayed Cholesky update proposed here.

4 Simulation studies

In this section we provide results from extensive simulation studies with high dimensional examples to study performance of the BITS algorithm. In section 4.2 we present results showing how hyperparameters values affect the screening properties. This, in turn, shows how informative screening can be performed by appropriately choosing these values. In section 4.3, we compare BITS with some other popular screening methods in the context of a variety of simulation settings described in Section 4.1. In particular, we compare BITS with SIS (Fan and Lv, 2008), forward regression (Wang, 2009) and HOLP (Wang and Leng, 2016). We also compare different stopping rules for BITS.

4.1 Simulation settings

We consider our numerical study in the context of seven simulation models described below. For these examples E.1–E.7, the rows of are generated from multivariate normal distributions with mean zero and different covariance structures, that is, rows of ’s are iid with mentioned in the example. Three values of theoretical are assumed ().

-

E.1

Independent predictors We set for and for .

-

E.2

Compound symmetry In this example, The value of is set to be equal to . The values of ’s are same as in example E.1.

-

E.3

Autoregressive correlation The auto regression, correlation structure among covariates is appropriate when there is an ordering (say, based on time) in covariates, and variables further apart are less correlated. We use the AR(1) structure where the th entry of is We set . The values of ’s are same as in example E.1.

- E.4

-

E.5

Group structure This special correlation structure arises when variables are grouped together in the sense that the variables from the same group are highly correlated. This example is similar to example 4 of Zou and Hastie (2005) where 15 true variables are assigned to 3 groups. We generate the predictors as , , where , and ’s and ’s are independent for and for . The regression coefficients are set as for and otherwise.

-

E.6

Extreme correlation We modify Wang’s (2009) challenging Example 4 to make it more complex. Let for all , and for . Simulate , and . Set and for . The marginal correlation between the response and any unimportant variable is ( times) larger in magnitude than the same between the response and the true predictors.

-

E.7

Sparse factor models This example is a sparse version of E.4. Let denotes the th entry of . In this example, for each fixed if and otherwise. Also, Finally, for and 0 for

For each simulation setup considered here, a total of 100 replications were performed and the estimates were averaged over the replications. Let be the model chosen in the th replication for . The coverage probability is calculated by CP = . This measures whether all important variables are discovered by the screening method or not. We also calculate the true positive rate (TPR) defined as In order to compare the posterior probability based stopping rules for BITS, we also calculate the median model size based on the 100 repetitions.

As in Wang (2009) and Wang and Leng (2016) we let the error and vary to achieve different values of theoretical (). As in Wang and Leng (2016), we use either for low, for moderate or for high signal to noise ratio. We consider and .

| Method | Correlation Structure | |||||||||||||

| IID | Compound | Group | AR | Factor | ExtrmCor | SparseFactor | ||||||||

| TPR | CP | TPR | CP | TPR | CP | TPR | CP | TPR | CP | TPR | CP | TPR | CP | |

| BITS1 | ||||||||||||||

| 100 | 100 | 60.4 | 2 | 100 | 100 | 100 | 100 | 57.6 | 4 | 100 | 100 | 78.1 | 5 | |

| PP | 100 | 100 | 36.2 | 0 | 100 | 100 | 99.9 | 99 | 7.6 | 0 | 100 | 100 | 53.2 | 0 |

| (45.74) | (49.37) | (48.46) | (46.73) | (14.04) | (12.03) | (56.38) | ||||||||

| EBIC | 100 | 100 | 14.0 | 0 | 33.3 | 0 | 64.4 | 1 | 0 | 0 | 97 | 97 | 14 | 0 |

| (9.00) | (5.01) | (3.00) | (5.80) | (2.37) | (10.98) | (3.50) | ||||||||

| BITS2 | ||||||||||||||

| 100 | 100 | 50.9 | 0 | 100 | 100 | 100 | 100 | 57.4 | 5 | 100 | 100 | 79.1 | 10 | |

| PP | 100 | 100 | 28.1 | 0 | 99.9 | 99 | 98.7 | 91 | 21.8 | 2 | 100 | 100 | 49.0 | 0 |

| (68.74) | (85.31) | (80.80) | (77.68) | (34.88) | (33.69) | (86.96) | ||||||||

| EBIC | 100 | 100 | 14.3 | 0 | 33.3 | 0 | 65.1 | 1 | 0.3 | 0 | 100 | 100 | 14.2 | 0 |

| (9.00) | (5.00) | (3.00) | (5.81) | (2.35) | (10.68) | (3.55) | ||||||||

| BITS3 | ||||||||||||||

| 100 | 100 | 22.7 | 0 | 100 | 100 | 97.7 | 81 | 16.0 | 1 | 100 | 100 | 75.9 | 4 | |

| PP | 100 | 100 | 21.7 | 0 | 35.4 | 0 | 90 | 45 | 1.3 | 0 | 100 | 100 | 16.7 | 0 |

| (172.99) | (155.34) | (132.30) | (175.96) | (3.81) | (179.14) | (156.60) | ||||||||

| EBIC | 100 | 100 | 14.0 | 0 | 33.3 | 0 | 64.2 | 0 | 0.3 | 0 | 100 | 100 | 14.5 | 0 |

| (9.00) | (5.00) | (3.01) | (5.79) | (2.29) | (10.27) | (3.63) | ||||||||

| BITS(ALL) | ||||||||||||||

| 100 | 100 | 65.2 | 3 | 100 | 100 | 100 | 100 | 63.2 | 10 | 100 | 100 | 81 | 13 | |

| (1353.45) | (1289.17) | (1355.48) | (1352.44) | (1209.98) | (1156.41) | (1340.00) | ||||||||

| PP | 100 | 100 | 40.2 | 0 | 100 | 100 | 99.9 | 99 | 23.4 | 2 | 100 | 100 | 56.2 | 0 |

| (254.90) | (256.95) | (231.60) | (265.01) | (44.79) | (198.01) | (264.00) | ||||||||

| HOLP | ||||||||||||||

| 100 | 100 | 67.0 | 3 | 100 | 100 | 100 | 100 | 48.6 | 3 | 100 | 100 | 71.5 | 5 | |

| EBIC | 97.9 | 81 | 18.7 | 0 | 71.8 | 0 | 91.6 | 51 | 5 | 0 | 99.8 | 98 | 22.4 | 0 |

| (9.05) | (5.07) | (6.46) | (8.24) | (4.43) | (9.01) | (5.59) | ||||||||

| FR | ||||||||||||||

| 100 | 100 | 23.4 | 0 | 36.1 | 0 | 89.6 | 44 | 17.1 | 1 | 100 | 100 | 18.6 | 0 | |

| EBIC | 100 | 100 | 14.0 | 0 | 33.3 | 0 | 64.1 | 0 | 0.3 | 0 | 100 | 100 | 14.5 | 0 |

| (9.00) | (5.00) | (3.01) | (5.78) | (2.28) | (10.27) | (3.63) | ||||||||

| SIS | 100 | 100 | 50.2 | 0 | 100 | 100 | 100 | 100 | 5.6 | 0 | 0 | 0 | 71.9 | 0 |

4.2 Effects of hyperparameters

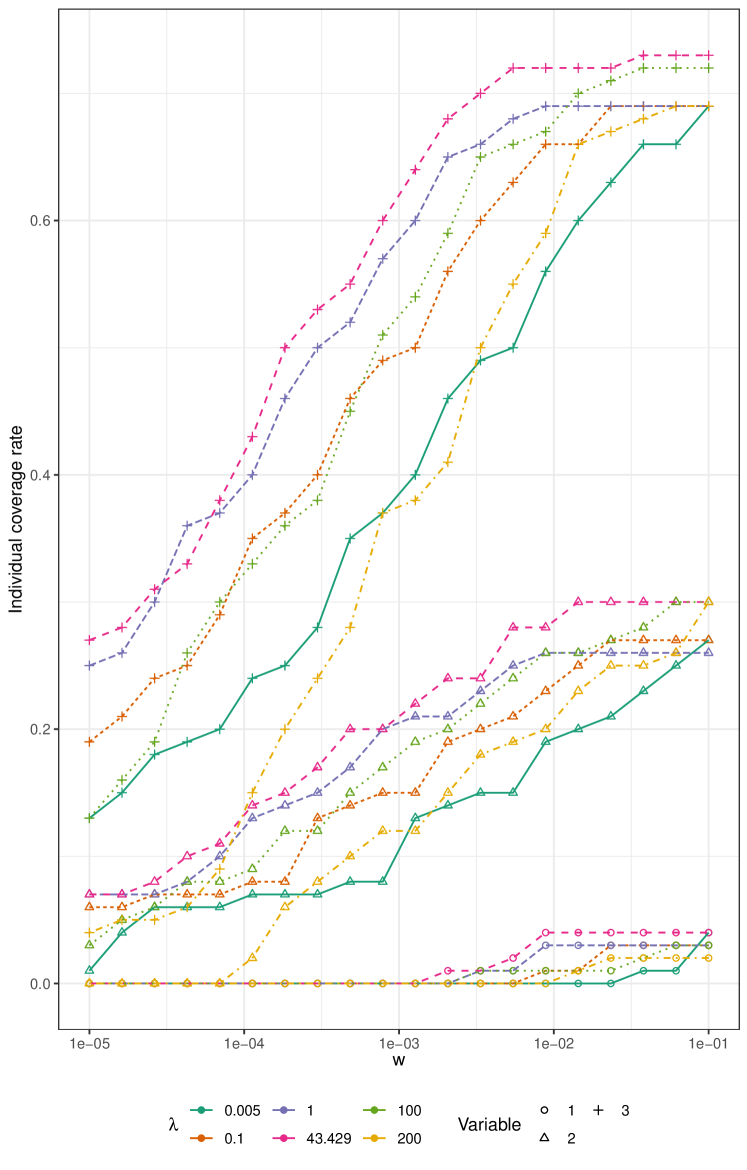

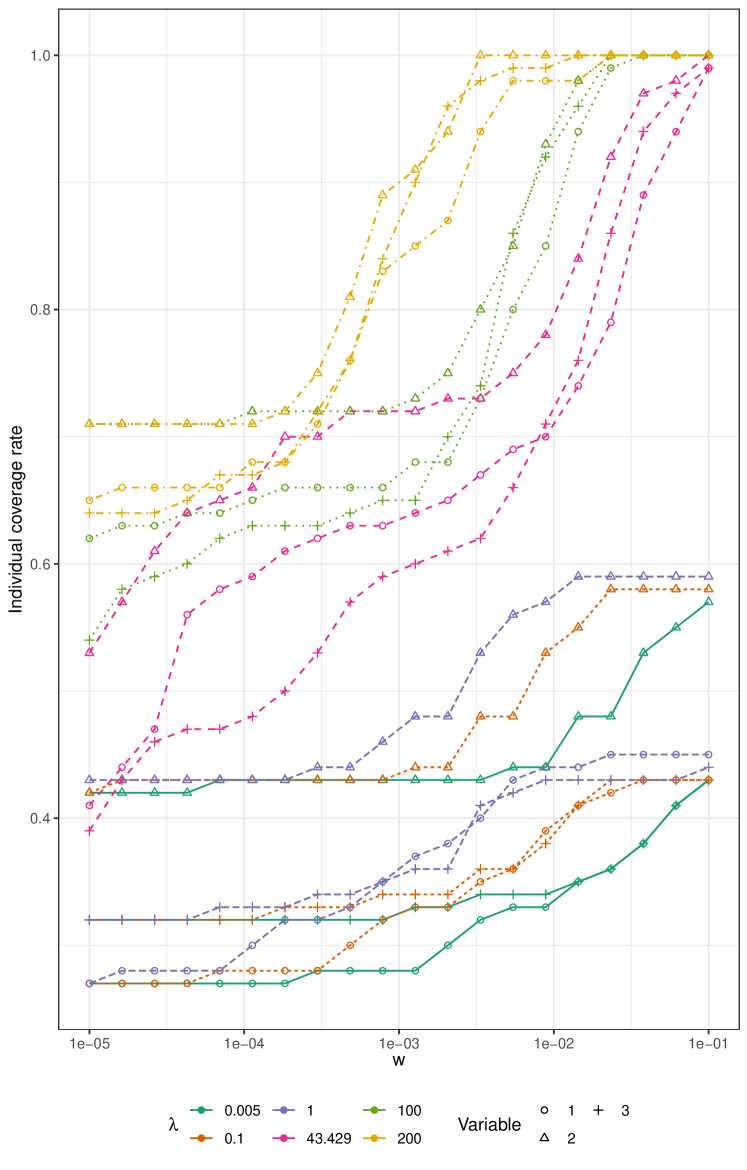

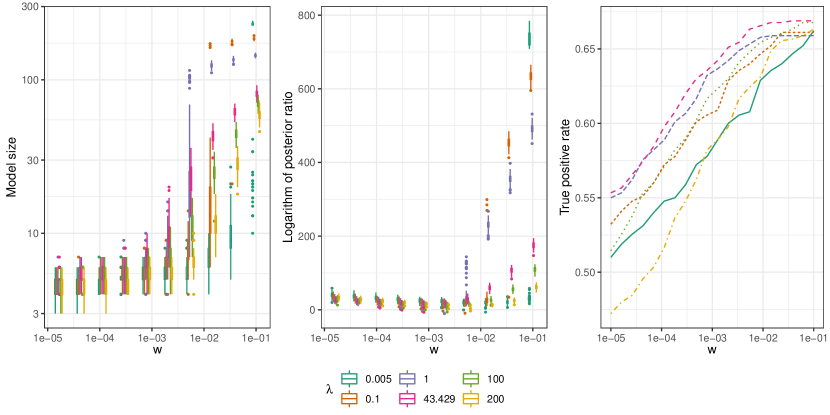

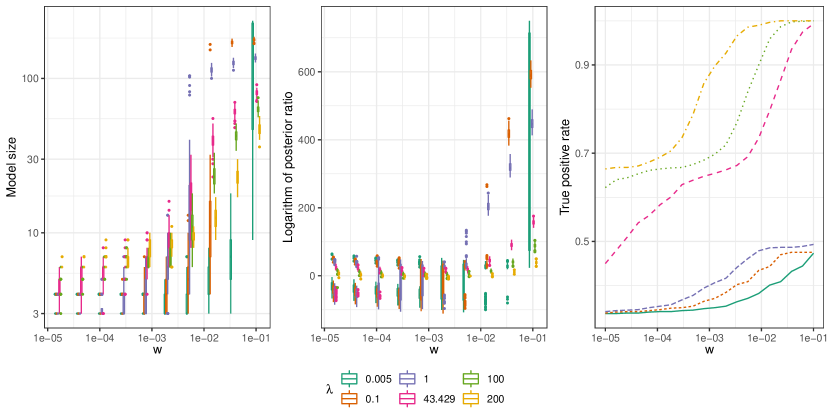

In order to study the effects of and on the screening performance under the PP stopping rule, we choose two scenarios: the iid setup (Section E.1) and the group structure (Section E.5) both with theoretical However, the nonzero -values for the iid setup were taken to be an increasing sequence We use 10 values of between and equally spaced on the log-scale and where the first three numbers are negligible compared to and correspond to low shrinkage and the last three numbers correspond to high shrinkage. We focus on the PP stopping rule because it is the only stopping rule that is impacted by In Figures 1 and 2 we summarize the model sizes and TPRs in addition to the logarithm of the ratio of the posterior probabilities of the screened model to the true model.

Several features stand out from these simulation studies. First, when the important predictors are highly correlated, larger values of (higher shrinkage) yield better screening accuracy in terms of TPR. In contrast, in the Independent setting, the smaller values of (lower shrinkage) yield better TPR. In either case, the model size, as well as TPR and the variability in the model size increase with however, even a 10% prior inclusion probability yields models with reasonable size. Second, we see an interaction between and as a ‘sprouting effect’ on the model size. In particular, although the model sizes are smaller for low shrinkage than the same for high shrinkage when is small, the situation reverses as increases. Third, logarithm of the posterior probability ratios increase slowly with when the shrinkage is high, while they increase rapidly with when the shrinkage is low. Finally, from the coverage proportions of the first three variables given in Section S3 of the supplement, we observe that the regression coefficients of smaller magnitudes tend to be over penalized and the corresponding variables are excluded when is large and is small but these are eventually included as increases.

These results suggest that a large is very helpful when the important predictors are correlated and a small is preferred otherwise. Also, a reasonably large helps in obtaining good screening accuracy without producing unreasonably large screened models. Thus prior knowledge on the nature of dependence among the predictors could be incorporated through and Even if no such prior knowledge is available, these simulation studies suggest uniting the models from BITS with different values should have a good screening accuracy.

4.3 Comparison against other screening methods

In this section, we summarize the simulation results. We consider three distinct values of , namely (BITS1), (BITS2) and (BITS3). We consider three screening model sizes obtained by the stopping rules mentioned in Section 2.5, that is, (denoted by ), the EBIC and the PP stopping rule with In addition, we also consider a union based rule denoted by BITS(ALL) which consists of the union of the models obtained in BITS1, BITS2 and BITS3 using a screening size of or the PP rule. For SIS, we simply look at the top variables. In Table 1 we present the results for theoretical . Additional simulation results are given in Section S2 of the supplementary document.

In general, BITS perform better when the first variables are included than when the PP rule is used. The PP criterion also results in a much smaller screened model size suggesting that it is very conservative. Also, BITS with higher shrinkage typically performs better in terms of TPR particularly when the variables are highly correlated among themselves. The EBIC based stopping rule is even more conservative than the PP and results in very low screening accuracy. Finally, BITS(ALL) with union of three size models performs the best among all the BITS methods in terms of screening accuracy. Although, it results also in significantly large screened model size it is encouragingly smaller than , suggesting that quite a few variables are common among the models from BITS1, BITS2 and BITS3.

BITS(ALL) also beats other methods in terms of TPR, albeit being more liberal in terms of the model size. In particular, because FR does not shrink the coefficient estimates it ends up picking a single candidate from each group in the group structure setting, thus having a TPR only about 3/9. For the same reason, FR also performs poorly in the compound symmetry and the two factor covariance settings. Thus, despite having some philosophical similarities with FR, BITS has a superior performance. In general, performance of HOLP closely follows BITS(ALL).

5 Real data example

We compare the screening methods using a real data set from (Cook et al., 2012) on a genomewide association study for maize starch, protein and oil contents. The original field trial at Clayton, NC in 2006 consisted of more than 5,000 inbred lines and check varieties primarily coming from a diverse panel consisting of 282 founding lines. The response from the field trials are typically spatially correlated, thus we use a random row-column adjustment to obtain the adjusted phenotypes of the varieties. However, marker information of only of these varieties are available from the panzea project (https://www.panzea.org/) which provides information on 546,034 single nucleotide polymorphisms (SNP) markers after removing duplicates and SNPs with minor allele frequency less than 5%. We use the starch content as our phenotype for conducting the association study. Because the inbred varieties are bi-allelic, we store the marker information in a sparse format by coding the minor alleles by one and major alleles by zero.

In this study, we do a cross-validation by randomly splitting the whole data set with training set of size and testing set of size 751. We run BITS with PP stopping rule with fixed at but with three distinct values of : (BITS1), (BITS2) and (BITS3). We also consider the union of these models. We compare these methods with HOLP and FR. The EBIC stopping criterion is also applied to all these methods for comparison. We repeat the process 100 times. In order to be able to use least squares estimates of the regression coefficients, we do not use screened model size same as However, HOLP and FR result in very small screened models (Figure 3) under EBIC based stopping rule. Indeed, out of 100 repetitions, 44 times HOLP with EBIC results in a null model and the numbers for HOLP (EBIC) in Figure 3 are based on the remaining 56 repetitions. In order to keep the comparison fair, we also use HOLP and FR with same model size as the union of models from the BITS1, BITS2 and BITS3. For each of the three BITS methods, we use both the ordinary least squares estimates of the regression coefficients (denoted by LM) and the ridge estimates with the associated because they are the posterior mode of the regression coefficient given the screened model.

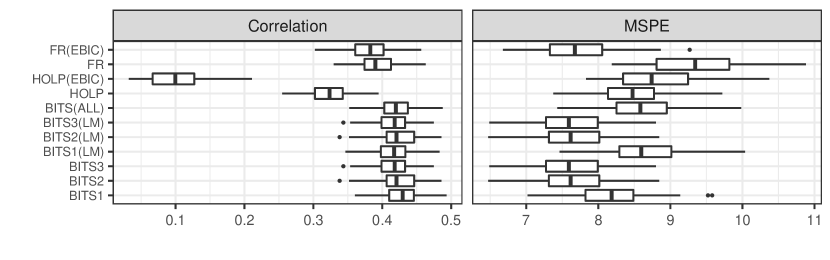

From the boxplots in Figure 3, it can be seen that models selected by BITS and FR with EBIC stopping rule yield very good prediction accuracies. In particular, BITS with lowest shrinkage (BITS3) yield more accurate predictions than other BITS methods on an average. The HOLP with EBIC stopping rule appears to be overtly conservative and also the method with lowest prediction accuracy. Surprisingly, the union of the BITS methods yields very good correlation (between observed and predicted) values, but somewhat larger mean squared prediction error (MSPE) values, perhaps because the MSPE is affected more by a few outlying values in the test set than the correlation coefficient is.

| Method | BITS1 | BITS2 | BITS3 | BITS(ALL) | HOLP(EBIC) | FR(EBIC) |

| Mean (SE) | 182.9 (16.3) | 46.5 (6.4) | 32.1 (5.6) | 213.2 (18.0) | 1.18 (0.47) | 8.96 (1.09) |

6 Discussion

In this paper, we propose a Bayesian iterative screening (BITS) method for screening variables in an ultra-high dimensional regression model that can accommodate prior information on the effect size and the model size. Despite being built on a Gaussian model assumption, BITS has been shown to be screening consistent even when the family is misspecified. In contrast to SIS, BITS does not require strong assumptions on marginal correlations. Compared to the frequentist iterative screening method FR, BITS naturally accommodates penalization on the effect size enhancing screening accuracy, particularly when important predictors are correlated among themselves. The proposed PP stopping rule, which is shown to be screening consistent, can provide informative screening by incorporating prior knowledge on the hyperparameters. BITS is implemented by a sophisticated algorithm that attains the same computational complexity as HOLP and allows fast statistical computations in ultra-high dimensional problems. Finally, BITS has been shown to have much better performance than several other competing methods by uniting results from different shrinkages. Thus, in practice, it could be useful to take union of models from BITS using various degrees of shrinkage. Then Bayesian or other variable selection algorithms may find it easier to discover useful models.

BITS can be extended to accommodate larger class of models, for example generalized linear regression models. In theory, the iterative algorithm (8) is quite general and does not require Gaussianity assumption. We may use Laplace approximations to achieve fast statistical computations in generalized linear models. Also, our future projects include developing Bayesian screening methods for non-linear, partial linear and functional linear models.

Supplemental materials

The supplemental materials contain proofs of some of the theoretical results stated in the paper and some additional simulation results.

Appendices

Appendix A Some useful notations and results

We use the following notations:

-

•

denotes the largest eigenvalue of for all

-

•

and denote the standard normal distribution and density function, respectively.

For any model with

-

•

and

-

•

-

•

=

-

•

which is equal to up to an additive constant that does not depend on

First we state some useful results whose proofs are given in Section S1 of the supplement. These results are used in the proofs of Theorems 2 and 4.

Lemma 4.

For any model with and any

Lemma 5.

For any model and lies between and where

Lemma 6.

Under conditions C2 and C3, there exists and such that for all sufficiently large

| (10) |

| (11) |

Lemma 7.

Suppose and then

Lemma 8.

Suppose and then with given in C3,

Corollary 2.

Suppose and . Let

Then

Appendix B Proofs of theorems

Proof of Theorem 1.

Under the orthogonal design,

which does not depend on Now, for each suppose denotes the event Then the theorem will be proved if as for which it is sufficient to show that as To that end, assume without loss that true and notice that for are iid standard normal because Thus for all and implies that and Thus, Consequently, since ’s are iid standard normal, we have,

| (12) | |||||

Because the first term on the right side of (12) is at most

| (13) |

because for all

Next, since for all sufficiently large , Thus, the second term on the right side of (12) is at most

| (14) |

where the third last inequality holds because , for

Proof of Theorem 2.

Let and denote the random inclusion times of the variables in in the models That is, and for

We note that,

| (15) | |||||

where denotes union of disjoint sets. We now analyze the th event Note that, implies that for each it must be that a variable outside of was selected in the st iteration, that is, for each such , and also that and

However, on the other hand, on we have using Lemma 5

| (17) |

because and

Thus applying (10) from (B) we get

| (18) |

Since for all sufficiently large the above is true for all we have from (15) that

| (19) |

Thus, for all sufficiently large using the union bound,

This proves the theorem. ∎

Proof of Theorem 3.

Assume without loss that the true First we shall show that As in the proof of Theorem 1 note that for any where ’s are i.i.d variables. Thus for any and is equivalent to,

| (20) | |||||

where But, and hence almost surely. Recall that as in Theorem 1, is assumed fixed here. Also, as

in probability. Hence, as where

for some constant . Next denote where ’s are defined in the proof of Theorem 1. Then as and for on .

Since we have for all large . Hence, from (20) note that for and we have, by symmetry of

| (21) | |||||

for sufficiently large Thus from (20) and (21) we have,

so that

Next, we show that To that end, suppose . Then the probability of stopping the iteration exactly at is Since for any where ’s are i.i.d variables, is equivalent to

| (22) | |||||

where is as defined before. We will now show that the left side is less than 2 with probability tending to 1 and the right side converges to in probability. This will complete the proof.

First, as we have

Then, note that under the orthogonal design, for any

and in probability, so that in probability. Consequently, as

in probability. This completes the proof.

∎

Proof of Theorem 4.

Let

Thus BITS is stopped prematurely by the posterior probability criterion without including all variables in iff happens for some However, note that

We first analyze To that end, note that when does not contain

Consequently, for we have

which is independent of In the second set inequality above we have used Lemma 7 and the third inequality is due to Corollary 2 and (11). Also, note that

by condition C3 for some for sufficiently large Hence, for sufficiently large

| (23) | |||||

where Note from the (19) that

| (24) |

Now let and Then, for all sufficiently large combining (23) and (24) we get,

∎

References

- Candes and Tao (2007) Candes, E. and Tao, T. (2007), “The Dantzig selector: Statistical estimation when p is much larger than n,” The Annals of Statistics, 35, 2313–2351.

- Chang et al. (2013) Chang, J., Tang, C. Y., and Wu, Y. (2013), “Marginal empirical likelihood and sure independence feature screening,” Annals of statistics, 41.

- Chen and Chen (2008) Chen, J. and Chen, Z. (2008), “Extended Bayesian information criteria for model selection with large model spaces,” Biometrika, 95, 759–771.

- Cho and Fryzlewicz (2012) Cho, H. and Fryzlewicz, P. (2012), “High dimensional variable selection via tilting,” Journal of the Royal Statistical Society, Series B, 74, 593–622.

- Cook et al. (2012) Cook, J. P., McMullen, M. D., Holland, J. B., Tian, F., Bradbury, P., Ross-Ibarra, J., Buckler, E. S., and Flint-Garcia, S. A. (2012), “Genetic architecture of maize kernel composition in the nested association mapping and inbred association panels,” Plant Physiology, 158, 824–834.

- Fan et al. (2011) Fan, J., Feng, Y., and Song, R. (2011), “Nonparametric independence screening in sparse ultra-high-dimensional additive models,” Journal of the American Statistical Association, 106, 544–557.

- Fan and Li (2001) Fan, J. and Li, R. (2001), “Variable selection via nonconcave penalized likelihood and its oracle property,” Journal of the American Statistical Association, 96, 1348–1360.

- Fan and Lv (2008) Fan, J. and Lv, J. (2008), “Sure independence screening for ultrahigh dimensional feature space,” Journal of Royal Statistical Society, Series B, 70, 849–911.

- Fan and Song (2010) Fan, J. and Song, R. (2010), “Sure independence screening in generalized linear models with NP-dimensionality,” The Annals of Statistics, 38, 3567–3604.

- George and McCulloch (1993) George, E. and McCulloch, R. E. (1993), “Variable selection via Gibbs sampling,” Journal of the American Statistical Association, 88, 881–889.

- Hall and Miller (2009) Hall, P. and Miller, H. (2009), “Using generalized correlation to effect variable selection in very high dimensional problems,” Journal of Computational and Graphical Statistics, 18, 533–550.

- Hans et al. (2007) Hans, C., Dobra, A., and West, M. (2007), “Shotgun stochastic search for “large p” regression,” Journal of the American Statistical Association, 102, 507–516.

- Hao and Zhang (2014) Hao, N. and Zhang, H. H. (2014), “Interaction screening for ultrahigh-dimensional data,” Journal of the American Statistical Association, 109, 1285–1301.

- He et al. (2013) He, X., Wang, L., and Hong, H. G. (2013), “Quantile-adaptive model-free variable screening for high-dimensional heterogeneous data,” The Annals of Statistics, 41, 342–369.

- Hoerl and Kennard (1970) Hoerl, A. E. and Kennard, R. W. (1970), “Ridge regression: Biased estimation for nonorthogonal problems,” Technometrics, 12, 55–67.

- Huang et al. (2008) Huang, J., Horowitz, J. L., and Ma, S. (2008), “Asymptotic properties of bridge estimators in sparse high-dimensional regression models,” The Annals of Statistics, 36, 587–613.

- Ishwaran and Rao (2005) Ishwaran, H. and Rao, J. S. (2005), “Spike and slab variable selection: frequentist and Bayesian strategies,” Annals of statistics, 730–773.

- Johnson and Rossell (2012) Johnson, V. E. and Rossell, D. (2012), “Bayesian model selection in high-dimensional settings,” Journal of the American Statistical Association, 107, 649–660.

- Kojima and Komaki (2016) Kojima, M. and Komaki, F. (2016), “Determinantal point process priors for Bayesian variable selection in linear regression,” Statistica Sinica, 26, 97–117.

- Kyung et al. (2010) Kyung, M., Gill, J., Ghosh, M., and Casella, G. (2010), “Penalized Regression, Standard Errors, and Bayesian Lassos,” Bayesian Analysis, 5, 369–412.

- Li et al. (2020) Li, D., Dutta, S., and Roy, V. (2020), “Model Based Screening Embedded Bayesian Variable Selection for Ultra-high Dimensional Settings,” arXiv preprint arXiv:2006.07561.

- Li et al. (2021) — (2021), bravo: Bayesian Screening and Variable Selection, r package version 1.0.6.

- Li et al. (2012a) Li, G., Peng, H., Zhang, J., and Zhu, L. (2012a), “Robust rank correlation based screening,” The Annals of Statistics, 40, 1846–1877.

- Li and Lin (2010) Li, Q. and Lin, N. (2010), “The Bayesian Elastic Net,” Bayesian Analysis, 5, 151–170.

- Li et al. (2012b) Li, R., Zhong, W., and Zhu, L. (2012b), “Feature screening via distance correlation learning,” Journal of the American Statistical Association, 107, 1129–1139.

- Liang et al. (2008) Liang, F., Paulo, R., Molina, G., Clyde, M. A., and Berger, J. O. (2008), “Mixtures of priors for Bayesian variable selection,” Journal of the American Statistical Association, 103, 410–423.

- Lin and Pang (2014) Lin, B. and Pang, Z. (2014), “Tilted correlation screening learning in high-dimensional data analysis,” Journal of Computational and Graphical Statistics, 23, 478–496.

- Ma et al. (2017) Ma, S., Li, R., and Tsai, C.-L. (2017), “Variable screening via quantile partial correlation,” Journal of the American Statistical Association, 112, 650–663.

- Mai and Zou (2013) Mai, Q. and Zou, H. (2013), “The Kolmogorov filter for variable screening in high-dimensional binary classification,” Biometrika, 100, 229–234.

- Meinshausen and Bühlmann (2006) Meinshausen, N. and Bühlmann, P. (2006), “High-dimensional graphs and variable selection with the lasso,” The annals of statistics, 34, 1436–1462.

- Mitchell and Beauchamp (1988) Mitchell, T. J. and Beauchamp, J. J. (1988), “Bayesian variable selection in linear regression,” Journal of the American Statistical Association, 83, 1023–1032.

- Mukhopadhyay and Dunson (2020) Mukhopadhyay, M. and Dunson, D. B. (2020), “Targeted random projection for prediction from high-dimensional features,” Journal of the American Statistical Association, 115, 1998–2010.

- Narisetty and He (2014) Narisetty, N. N. and He, X. (2014), “Bayesian variable selection with shrinking and diffusing priors,” The Annals of Statistics, 42, 789–817.

- Park and Casella (2008) Park, T. and Casella, G. (2008), “The Bayesian Lasso,” Journal of the American Statistical Association, 103, 681–686.

- Ročková and George (2014) Ročková, V. and George, E. (2014), “EMVS: The EM approach to Bayesian variable selection,” Journal of the American Statistical Association, 109, 828–846.

- Roy and Chakraborty (2017) Roy, V. and Chakraborty, S. (2017), “Selection of tuning parameters, solution paths and standard errors for Bayesian lassos,” Bayesian Analysis, 12, 753–778.

- Roy et al. (2018) Roy, V., Tan, A., and Flegal, J. (2018), “Estimating standard errors for importance sampling estimators with multiple Markov chains,” Statistica Sinica, 28, 1079–1101.

- Shin et al. (2018) Shin, M., Bhattacharya, A., and Johnson, V. E. (2018), “Scalable Bayesian variable selection using nonlocal prior densities in ultrahigh-dimensional settings,” Statistica Sinica, 28, 1053–1078.

- Song and Liang (2015) Song, Q. and Liang, F. (2015), “A split-and-merge Bayesian variable selection approach for ultrahigh dimensional regression,” Journal of the Royal Statistical Society: Series B: Statistical Methodology, 947–972.

- Tibshirani (1996) Tibshirani, R. (1996), “Regression shrinkage and selection via the lasso,” Journal of the Royal Statistical Society, Series B, 58, 267–288.

- Vershynin (2012) Vershynin, R. (2012), “Introduction to the non-asymptotic analysis of random matrices,” in Compressed Sensing: Theory and Applications, eds. Eldar, Y. C. and Kutyniok, G., Cambridge University Press, p. 210–268.

- Wang (2009) Wang, H. (2009), “Forward regression for ultra-high dimensional variable screening,” Journal of the American Statistical Association, 104, 1512–1524.

- Wang et al. (2021) Wang, R., Dutta, S., and Roy, V. (2021), “A note on marginal correlation based screening,” Statistical Analysis and Data Mining: The ASA Data Science Journal, 14, 88–92.

- Wang and Leng (2016) Wang, X. and Leng, C. (2016), “High dimensional ordinary least squares projection for screening variables,” Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78, 589–611.

- Xu and Chen (2014) Xu, C. and Chen, J. (2014), “The sparse MLE for ultrahigh-dimensional feature screening,” Journal of the American Statistical Association, 109, 1257–1269.

- Xu and Ghosh (2015) Xu, X. and Ghosh, M. (2015), “Bayesian variable selection and estimation for group lasso,” Bayesian Analysis, 10, 909–936.

- Yang et al. (2016) Yang, Y., Wainwright, M. J., and Jordan, M. I. (2016), “On the computational complexity of high-dimensional Bayesian variable selection,” The Annals of Statistics, 44, 2497–2532.

- Yuan and Lin (2005) Yuan, M. and Lin, Y. (2005), “Efficient empirical Bayes variable selection and estimation in linear models,” Journal of the American Statistical Association, 100, 1215–1225.

- Zellner (1986) Zellner, A. (1986), “On assessing prior distributions and Bayesian regression analysis with g-prior distributions,” in Bayesian inference and decision techniques: Essays in Honor of Bruno de Finetti, eds. Goel, P. K. and Zellner, A., Elsevier Science, 233–243.

- Zhou and Guan (2019) Zhou, Q. and Guan, Y. (2019), “Fast model-fitting of Bayesian variable selection regression using the iterative complex factorization algorithm,” Bayesian Analysis, 14, 573.

- Zhou et al. (2019) Zhou, T., Zhu, L., Xu, C., and Li, R. (2019), “Model-Free Forward Screening Via Cumulative Divergence,” Journal of the American Statistical Association, 1–13.

- Zou (2006) Zou, H. (2006), “The adaptive lasso and its oracle properties,” Journal of the American Statistical Association, 101, 1418–1429.

- Zou and Hastie (2005) Zou, H. and Hastie, T. (2005), “Regularization and variable selection via the Elastic Net,” Journal of the Royal Statistical Society, Series B, 67, 301–320.

Supplement to

“Bayesian iterative screening in ultra-high dimensional settings”

Run Wang, Somak Dutta and Vivekananda Roy

Appendix S1 Proofs of lemmas and corollaries

S1.1 Proof of Lemma 2

Proof.

Since ,

Also, since and are fixed here, and ,

for some constant . Thus, if ,

Next, since , . Therefore,

| (S1) |

Note that (S1.1) because . ∎

S1.2 Proof of Lemma 3

Proof.

Note that Suppose denotes the upper triangular Cholesky factor of And let for Then arranging the columns of appropriately, we can assume that the Cholesky factor of is given by

where and Also note that,

Also,

Therefore,

which completes the proof. ∎

S1.3 Proof of Lemma 4

Proof.

Since

the proof follows from the fact that

where . ∎

S1.4 Proof of Lemma 5

Proof.

Note that,

because Since (equality holding iff and the result follows immediate. ∎

S1.5 Proof of Lemma 6

S1.6 Proof of Lemma 7

Proof.

Note that for any

In the above, the first inequality follows from the definition of and Lemma 5; the second inequality follows from the facts that for any model and that for Finally, the last inequality follows from the facts that for any and that for all of size at most we have

because the nonzero eigenvalues of and are the same. ∎

S1.7 Proof of Lemma 8

Proof.

Note that

for some vector where the first equality follows from the fact that for any the second inequality is the Cauch-Schwarz inequality, and the final inequality follows from the fact that the matrix has less than columns and that The proof follows because ∎

S1.8 Proof of Corollary 1

Proof.

Since and , we have

| (S2) | |||||

By Berry-Esseen theorem,

where for all large as the conditions and are in force. Since Var , the proof follows as by the Chebyshev’s inequality we have

∎

S1.9 Proof of Corollary 2

Appendix S2 Further simulation results

In this section we present the comparison results for different simulation settings corresponding to and .

| Method | Correlation Structure | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Theoretical | ||||||||||||||

| IID | Compound | Group | AR | Factor | ExtrmCor | SparseFactor | ||||||||

| TPR | CP | TPR | CP | TPR | CP | TPR | CP | TPR | CP | TPR | CP | TPR | CP | |

| BITS1 | ||||||||||||||

| 99.9 | 99 | 24.2 | 0 | 100 | 100 | 100 | 100 | 28.8 | 1 | 99.9 | 99 | 72.8 | 4 | |

| PP | 99.9 | 99 | 8.3 | 0 | 100 | 100 | 96.8 | 73 | 2.2 | 0 | 99.3 | 94 | 43.3 | 0 |

| (60.26) | (48.67) | (62.27) | (60.33) | (9.72) | (11.38) | (65.05) | ||||||||

| EBIC | 94.7 | 71 | 3.6 | 0 | 33.3 | 0 | 44.3 | 0 | 0.1 | 0 | 0.2 | 0 | 11.5 | 0 |

| (8.52) | (3.39) | (3.00) | (3.99) | (1.88) | (1.02) | (2.88) | ||||||||

| BITS2 | ||||||||||||||

| 99.9 | 99 | 19.7 | 0 | 100 | 100 | 100 | 100 | 28.9 | 1 | 100 | 100 | 72.0 | 6 | |

| PP | 99.9 | 99 | 7.2 | 0 | 94.8 | 62 | 77 | 6 | 3.4 | 0 | 100 | 100 | 39.7 | 0 |

| (83.31) | (86.27) | (91.09) | (86.33) | (21.79) | (45.38) | (92.60) | ||||||||

| EBIC | 94.7 | 71 | 2.9 | 0 | 33.3 | 0 | 44.8 | 0 | 0.2 | 0 | 0.8 | 0 | 12.6 | 0 |

| (8.52) | (3.38) | (3.00) | (4.03) | (1.98) | (1.07) | (3.15) | ||||||||

| BITS3 | ||||||||||||||

| 99.8 | 98 | 6.0 | 0 | 100 | 100 | 84.8 | 18 | 4.8 | 0 | 73.4 | 59 | 69.0 | 5 | |

| PP | 99.8 | 98 | 5.1 | 0 | 33.7 | 0 | 59.4 | 0 | 0.4 | 0 | 52.9 | 40 | 14.6 | |

| (185.28) | (114.22) | (136.72) | (159.21) | (2.81) | (107.32) | (155.3) | ||||||||

| EBIC | 94.7 | 71 | 2.9 | 0 | 33.3 | 0 | 44.4 | 0 | 0.1 | 0 | 0.8 | 0 | 12.6 | 0 |

| (8.52) | (3.37) | (3.00) | (4.00) | (1.98) | (1.07) | (3.15) | ||||||||

| BITS(ALL) | ||||||||||||||

| 99.9 | 99 | 28.8 | 0 | 100 | 100 | 100 | 100 | 34.3 | 1 | 100 | 100 | 76.4 | 8 | |

| (1347.61) | (1289.91) | (1349.22) | (1348.93) | (1210.95) | (1149.66) | (1333.00) | ||||||||

| PP | 99.9 | 99 | 10.3 | 0 | 100 | 100 | 96.9 | 74 | 4.4 | 0 | 100 | 100 | 47.6 | 0 |

| (291.60) | (219.43) | (255.16) | (273.41) | (28.89) | (143.93) | (277.60) | ||||||||

| HOLP | ||||||||||||||

| 99.6 | 96 | 43.7 | 0 | 100 | 100 | 100 | 100 | 38.4 | 1 | 99.6 | 96 | 73.7 | 6 | |

| 99.2 | 93 | 29.4 | 0 | 100 | 100 | 100 | 100 | 24.2 | 0 | 99.2 | 93 | 68.9 | 3 | |

| EBIC | 76.4 | 12 | 3.7 | 0 | 68.1 | 0 | 48.3 | 0 | 0.6 | 0 | 91.9 | 59 | 12.6 | 0 |

| (7.01) | (3.72) | (6.13) | (4.35) | (1.80) | (8.30) | (2.03) | ||||||||

| FR | ||||||||||||||

| 99.8 | 98 | 5.9 | 0 | 36.1 | 0 | 59.6 | 0 | 6.8 | 0 | 84.7 | 73 | 16.6 0 | ||

| EBIC | 94.7 | 71 | 2.9 | 0 | 33.3 | 0 | 44.6 | 0 | 0.1 | 0 | 0.8 | 0 | 12.6 | 0 |

| (8.52) | (3.37) | (3.00) | (4.01) | (1.98) | (1.07) | (3.15) | ||||||||

| SIS | ||||||||||||||

| 99.8 | 98 | 43.8 | 0 | 100 | 100 | 100 | 100 | 9 | 0 | 99.6 | 96 | 74.1 | 8 | |

| 99.1 | 92 | 29.7 | 0 | 100 | 100 | 100 | 100 | 4.8 | 0 | 0 | 0 | 69.1 | 4 | |

| Theoretical | ||||||||||||||

| IID | Compound | Group | AR | Factor | ExtrmCor | SparseFactor | ||||||||

| TPR | CP | TPR | CP | TPR | CP | TPR | CP | TPR | CP | TPR | CP | TPR | CP | |

| BITS1 | ||||||||||||||

| 100 | 100 | 99.7 | 97 | 100 | 100 | 100 | 100 | 96.8 | 78 | 100 | 100 | 84.5 | 12 | |

| PP | 100 | 100 | 99.3 | 94 | 100 | 100 | 100 | 100 | 50.3 | 3 | 100 | 100 | 64.5 0 | |

| (15.79) | (41.33) | (17.72) | (16.93) | (23.58) | (12.98) | (32.34) | ||||||||

| EBIC | 100 | 100 | 94.8 | 60 | 49.0 | 0 | 100 | 100 | 3.8 | 3 | 100 | 100 | 18.6 | 0 |

| (9.00) | (9.03) | (4.41) | (9.01) | (4.03) | (11.22) | (4.66) | ||||||||

| BITS2 | ||||||||||||||

| 100 | 100 | 99.3 | 94 | 100 | 100 | 100 | 100 | 97.7 | 86 | 100 | 100 | 87.3 | 20 | |

| PP | 100 | 100 | 99.3 | 94 | 100 | 100 | 100 | 100 | 90.7 | 65 | 100 | 100 | 59.6 | 0 |

| (32.63) | (76.32) | (52.61) | (50.60) | (41.04) | (12.31) | (67.68) | ||||||||

| EBIC | 100 | 100 | 95 | 59 | 48.8 | 0 | 100 | 100 | 18.3 | 16 | 100 | 100 | 17.3 | 0 |

| (9.00) | (9.03) | (4.39) | (9.01) | (5.97) | (10.35) | (4.33) | ||||||||

| BITS3 | ||||||||||||||

| 100 | 100 | 99.1 | 92 | 100 | 100 | 100 | 100 | 83.9 | 62 | 100 | 100 | 85.2 | 11 | |

| PP | 100 | 100 | 99.1 | 92 | 66.9 | 100 | 100 | 100 | 23.9 | 12 | 100 | 100 | 21 | 0 |

| (163.04) | (193.94) | (153.49) | (162.17) | (10.93) | (164.06) | (144.50) | ||||||||

| EBIC | 100 | 100 | 94.9 | 59 | 49 | 0 | 100 | 100 | 22.4 | 17 | 100 | 100 | 17.5 | 0 |

| (9.00) | (9.03) | (4.42) | (9.01) | (6.68) | (10.12) | (4.39) | ||||||||

| BITS(ALL) | ||||||||||||||

| 100 | 100 | 99.7 | 97 | 100 | 100 | 100 | 100 | 98.4 | 89 | 100 | 100 | 88.6 | 23 | |

| (1360.51) | (1294.21) | (1363.04) | (1359.51) | (1214.20) | (1164.95) | (1346.00) | ||||||||

| PP | 100 | 100 | 99.3 | 94 | 100 | 100 | 100 | 100 | 91.2 | 66 | 100 | 100 | 67.2 | 0 |

| (186.94) | (274.42) | (199.41) | (200.89) | (60.45) | (167.88) | (212.50) | ||||||||

| HOLP | ||||||||||||||

| 100 | 100 | 99.8 | 98 | 100 | 100 | 100 | 100 | 97.0 | 75 | 100 | 100 | 78.6 | 7 | |

| 100 | 100 | 99.1 | 92 | 100 | 100 | 100 | 100 | 92.2 | 51 | 100 | 100 | 76.1 | 5 | |

| EBIC | 100 | 100 | 82.8 | 15 | 78.2 | 1 | 100 | 100 | 48.7 | 0 | 100 | 100 | 47.8 | 0 |

| (9.08) | (8.08) | (7.04) | (9.00) | (12.83) | (9.00) | (11.96) | ||||||||

| FR | ||||||||||||||

| 100 | 100 | 99.1 | 92 | 65.1 | 0 | 100 | 100 | 81.8 | 56 | 100 | 100 | 21.3 | 0 | |

| EBIC | 100 | 100 | 94.9 | 59 | 49 | 0 | 100 | 100 | 24.8 | 19 | 100 | 100 | 17.5 | 0 |

| (9.00) | (9.04) | (4.42) | (9.01) | (7.06) | (10.12) | (4.39) | ||||||||

| SIS | ||||||||||||||

| 100 | 100 | 89.3 | 33 | 100 | 100 | 100 | 100 | 9 | 0 | 100 | 100 | 78.6 | 8 | |

| 100 | 100 | 79.3 | 13 | 100 | 100 | 100 | 100 | 4.8 | 0 | 0 | 0 | 76.0 | 5 | |

Appendix S3 Additional plots from Section 4.2

This section contains plots of coverage probabilities for some true variables in the examples discussed in section 4.2.