Nonlinear Approaches to Intergenerational Income Mobility allowing for Measurement Error††thanks: We thank Yonghong An, Gary Chamberlain, Hao Dong, Jerry Hausman, Weige Huang, Chengye Jia, Josh Kinsler, Dan Millimet, Ariel Pakes, Xun Tang, Emmanuel Tsyawo, and seminar participants at the Harvard/MIT Econometrics Workshop, Monash University, National Tsinghua University, Rice University, Southern Methodist University, UC Irvine, UC Riverside, University of Southern California, University of Surrey, and at the 2018 Triangle Econometrics Conference, the 2019 Tsinghua Econometrics Conference, and the 2019 North American Summer Meetings of the Econometric Society for helpful comments.

Abstract

This paper considers nonlinear measures of intergenerational income mobility such as (i) the effect of parents’ permanent income on the entire distribution of child’s permanent income, (ii) transition matrices, and (iii) rank-rank correlations when observed annual incomes are treated as measured-with-error versions of permanent incomes. We develop a new approach to identifying joint distributions in the presence of “two-sided” measurement error, and, hence, identify essentially all parameters of interest in the intergenerational income mobility literature. Using recent data from the 1997 National Longitudinal Study of Youth, we find that accounting for measurement error notably reduces various estimates of intergenerational mobility.

JEL Codes: J62, C21

Keywords: Intergenerational Income Mobility, Measurement Error, Quantile Regression, Continuous Treatment Effects, Poverty, Inequality

1 Introduction

Economists studying intergenerational income mobility have been interested in the effect of parents’ permanent income on child’s permanent income. A key empirical challenge in this literature is that, instead of observing permanent incomes, researchers typically observe annual income (or some other shorter-term measure of income). The modern literature on intergenerational income mobility (e.g., [81]) considers annual income as an error-ridden measure of permanent income;111As is common in the intergenerational mobility literature, our main concern related to measurement error comes from annual income not being equal to permanent income rather than annual income itself being misreported (see, for example, [9, 71, 8] on issues related to annual income being misreported). has developed and used techniques to deal with measured-with-error versions of permanent incomes; and has demonstrated that accounting for measurement error leads to significant quantitative differences in estimates of intergenerational mobility.222This branch of the literature has focused on estimating Intergenerational Elasticities (IGEs) which are the coefficient on the log of parents’ income in a regression of the log of child’s income on the log of parents’ income. See, for example, [82, 60, 40], among others.

Much recent work on intergenerational income mobility has also considered nonlinear measures of intergenerational mobility. To give some prominent examples, transition matrices provide a way to see how likely children are to move to different parts of the income distribution conditional on what part of the income distribution their parents are in. Work on transition matrices includes [48, 5, 7, 74, 63]. Researchers have also been interested in (functionals of) the entire distribution of child’s income as a function of parents’ income ([73, 14]); these sorts of parameters are related to the literature on continuous treatment effects and include things like the fraction of children whose income is below the poverty line as a function of parents’ income. The correlation of the ranks of parents’ income and child’s income has also received considerable recent attention in the intergenerational mobility literature ([23, 25, 21, 22]). Another nonlinear measure of intergenerational income mobility is the probability that a child’s income is greater than their parents’ income ([5]).333Another related branch of the literature focuses on allowing Intergenerational Elasticities to be nonlinear; see, for example, [4, 12, 6, 64, 65, 54, 13, 2, 53].

What each of the above parameters has in common is that they depend on the joint distribution of the outcome (child’s income) and the treatment (parents’ income) possibly conditional on covariates. In this paper, we consider nonlinear measures of intergenerational income mobility while allowing for measurement error in both child’s income and parents’ income. In terms of methods, this boils down to identifying joint distributions in the presence of measurement error in either variable. The main case that we consider in the paper is the one where a researcher has access to a single measurement of parents’ income and child’s income. In this case, we impose two main conditions. First, we impose “classical” measurement error conditions; in particular, we impose that measurement error for child’s income and parents’ income is additively separable from their true permanent incomes, that the measurement errors are independent of true permanent incomes and covariates, and that the measurement errors are independent of each other.444In the intergenerational mobility literature, the assumption of classical measurement error is typically considered more plausible for some ages of children and parents (typically mid-career ages). We discuss how to adjust our arguments to the case of “life-cycle” measurement error (as in [40]) rather than classical measurement error; see Remark 1 and Appendix C for more details. The second main assumption that we make is on reduced forms for the outcome and the treatment conditional on other covariates. In particular, we assume that both the outcome and the treatment are generated by a quantile regression (QR) model that is linear in parameters across all quantiles. Besides these two main conditions, we do not require an instrument, repeated measurements, or distributional assumptions about the measurement errors for identification.555One common strategy, both for linear and nonlinear measures of intergenerational mobility, is to average repeated measures of annual income into a single measure of permanent income. Generally, in nonlinear models, these sorts of approaches would require consistent estimation of permanent income, which due to the incidental parameters problem, would require the number of time periods to grow to infinity (see, e.g., [51, 33]). For these sorts of arguments to work, it seems likely that a researcher would already have access to an individual’s entire annual earnings history. In this case, there is no measurement error issue at all as one can simply compute permanent income. Even in the context of linear models, averaging a few years of earnings may be of limited use in accounting for measurement error especially when transitory income shocks can be persistent ([60]).

The first step of our identification argument builds on recent work on quantile regression with measurement error in the outcome. [42] show that the structure imposed by the QR model is enough to identify the QR parameters as well as the distribution of the measurement error in the case with classical measurement error for the outcome variable. Hence, the conditional quantiles and conditional distributions of the outcome and treatment are identified. However, identifying these marginal distributions is not enough to identify the nonlinear measures of intergenerational income mobility that we are interested in. In particular, these nonlinear measures depend on the joint distribution of the outcome and the treatment. From Sklar’s Theorem, a well-known result in the literature on copulas, we know that joint distributions can be written as the copula (which captures the dependence between two random variables) of the outcome and the treatment. We show that, under the conditions above, the copula is also identified. This means that the joint distribution is identified and, hence, any nonlinear measure of intergenerational income mobility is also identified.

Besides our contributions to the literature on intergenerational income mobility, the methods that we develop in this paper are more generally applicable to cases where a researcher is interested in the effect of a continuous treatment on some outcome in the case where both are possibly measured with error. We show that, under the assumption of selection on observables, our approach can be used to identify dose-response functions which are the main object of interest in the literature on continuous treatment effects (e.g., [45, 36, 38]). Even without invoking the assumption of selection on observables, our approach can be used to study counterfactual distributions (e.g., [30, 59, 62, 18, 14]), and distributional policy effects (e.g., [75]) in the presence of measurement error in both the outcome and the treatment. More generally, because our approach recovers the joint distribution of the outcome and treatment, the method we propose may be useful for recovering any parameter that depends on this joint distribution when the outcome and treatment are both continuously distributed and possibly measured with error (possible examples include trade flows, expenditures, budget shares, income, wealth, GDP, charitable contributions, among many others).

For estimation, we propose a three-step approach to estimating the joint distribution of the outcome and the treatment conditional on covariates and then recovering parameters of interest from the joint distribution. In the first step, we estimate the quantile regression parameters and then convert these into estimates of the reduced form distributions of the outcome/treatment conditional on covariates. Our estimation approach here is new. We implement an EM-type algorithm that iterates back and forth between making draws of the measurement error (conditional on values of the parameters) and estimating new values of the parameters. Once the reduced form QR parameters have been estimated, we estimate the copula parameters using a simulated maximum likelihood approach that plugs in the first step estimators. To simplify estimation, we assume that the copula is known up to a finite number of parameters (in particular, we consider copulas from an Archimedean family or the Gaussian copula). This step provides an estimate of the joint distribution. Finally, we can manipulate the estimated joint distribution into any parameters of interest.

We apply our approach to study intergenerational income mobility using recent data from the 1997 cohort of the National Longitudinal Survey of Youth (NLSY97). This is a rich dataset where we observe much information about families and can link child’s income with their parents’ income. We employ the 1997 wave of the NLSY97 to obtain the information about parents’ income and the 2015 wave of the NLSY to obtain the child’s income. However, there are some notable challenges. First, we only observe parents’ income in a single year. Second, although, in principle, we observe child’s income in every period where they participate in the survey, children are still relatively young, and, in light of much work in the intergenerational mobility literature, it seems most appropriate to only use their income in more recent waves. Our main results indicate that (i) adjusting for measurement error and (ii) using our copula-based approach relative to quantile regression of child’s income directly on parents’ income and covariates are both important. Accounting for measurement error in child’s and parents’ income tends to reduce various estimates of intergenerational mobility resulting in estimates that are more similar to those in the literature where multiple observations of income are available relative to estimates coming directly from the observed data that do not account for measurement error.

Related Work on Measurement Error in Nonlinear Models

Our work builds on an extensive literature in econometrics on measurement error. Early work focused on addressing measurement error in linear models. For example, it is well-known that under the classical measurement error assumptions a mismeasured right-hand side variable in a linear model leads to attenuation bias, while the mismeasured left-hand side variable does not lead to inconsistency of the parameter estimates under the same assumption in the linear framework. Important early work on obtaining the distribution of a variable of interest in the presence of measurement error includes [32, 29]. These papers relied on parametric assumptions about the distribution of the measurement error; [58] relax the distributional assumption on the measurement error when there are repeated measurements available.

Noticeable advances on measurement error problems have also been made in nonlinear frameworks, particularly for the case of the right-hand side (RHS) mismeasured variable. To give some examples, [46] and [56] propose a minimum distance estimator and a simulated version of that, respectively, in estimating structural nonlinear models allowing for measurement error. [57] proposes consistent semiparametric estimators of general nonlinear models with right-hand side measurement error using replicate measurements. [43] study nonlinear regression models with the right-hand side measurement error in the case of a polynomial specification and propose to address measurement error using either multiple measurements or instrumental variables. [44] investigate a general nonlinear model with mismeasured regressors using multiple measurements. [77] extends the results from [43] from the polynomial specification to general nonlinear models with mismeasured regressors using two measurements. [78] exploits instrumental variables to identify nonparametric models with the RHS measurement error problem using Fourier transforms of the conditional means of the observed variables.

Dealing with the left-hand side (LHS) measurement error in a nonlinear context has received much less attention. This is unfortunate since what we know about the linear setting with either the RHS or LHS measurement error does not generally carry over to nonlinear models. [41] and [26] represent some exceptions and study two widely used nonlinear models with the LHS mismeasured variable — probit and tobit, respectively. Additionally, [1] consider a general linear index model but focus primarily on duration and hazard models and demonstrate that a semiparametric monotone rank estimator due to [16] produces consistent estimates of the model parameters when the effect of the mismeasurement on average preserves the ordering of the mismeasured LHS variable with respect to that of its true unobserved version.

Furthermore, even less consideration has been given to nonlinear models with both the RHS and LHS measurement error. Rare exceptions include [55] that studies parametric Engel curves with measurement error on both sides of the equation and [27] that extends [78] to allow for both the RHS and LHS measurement error in nonparametric models.

Within the measurement error literature, the current paper is most closely related to work on quantile regression with measurement error. The econometric literature for estimating quantile regressions with the RHS measurement error includes [79, 85, 20, 34]. Our approach, however, is more closely related to quantile regression with LHS measurement error. [42] show that the parameters of a linear quantile regression model are identified when there is measurement error in the outcome variable without imposing distributional assumptions on the measurement error or requiring instruments or repeated observations. Our approach builds on this one as we use their identification arguments in our first step to show that the reduced forms for the outcome and the treatment are identified. On the other hand, our estimators of the conditional quantiles are different from those proposed in [42]; we propose an EM-type algorithm while their estimators are based on maximum likelihood.

Finally, there are a few related papers that examine measurement error in the context of nonlinear approaches to understanding intergenerational mobility. [63] consider transition matrices particularly in the case where individuals can be misclassified into the wrong cell. [70, 52] study rank-rank correlations (i.e., Spearman’s Rho), which is a commonly encountered parameter in the intergenerational mobility literature, in the presence of measurement error. [70] consider measurement error in the ranks of child’s income and parents’ income rather than in the levels of income (they also note that, by construction, measurement error in the ranks must be non-classical). The approach in [52] builds on the small variance approximations of [19] to recover rank-rank correlations when there is measurement error in the levels of child’s and parents’ income. [2] study a nonparametric version of the IGE in the presence of non-classical measurement error (particularly, life-cycle measurement error).

Organization of the paper

The paper is organized as follows. In Section 2, we discuss parameters of interest that include parameters that depend on the distribution of child’s income conditional on parents’ income as well as parameters that depend on the copula of child’s income and parents’ income. Section 3 considers identification of these parameters of interest allowing for measurement error. In Section 4, we propose a three-step estimation procedure to estimate the parameters of interest. Our application on intergenerational income mobility using our approach is in Section 5. Final remarks are contained in Section 6. In the Appendix, we provide all proofs, Monte Carlo simulations, and some additional empirical results and technical details.

2 Parameters of Interest

Notation

Let denote the outcome of interest and denote a continuous treatment variable. We allow both and to be mismeasured. Also let denote a vector of covariates that are correctly measured.

All of the parameters that we consider are features of the joint distribution . Later, our identification arguments will center on identifying this joint distribution. For now, notice that, in the absence of measurement error, this joint distribution is directly identified by the sampling process. In the presence of measurement error, identifying this distribution is non-trivial. We take this issue up in Section 3 below, but for now we consider a wide variety of parameters in the intergenerational income mobility literature and in the continuous treatment effect literature that are features of this joint distribution and can therefore be obtained if this joint distribution is identified.

We divide the parameters in this section into two categories that we call: Conditional Distribution-type parameters and Copula-type parameters. The first category includes parameters from the treatment effects literature (e.g., quantile treatment effects and dose response functions) as well as counterfactual distributions and distributional policy effects. These types of parameters are of general interest in the case where a researcher is interested in the effect of a continuous treatment on features of the distribution of some outcome. These sorts of parameters are also of interest in the particular case of intergenerational mobility. One parameter in this category is the fraction of children whose income is below the poverty line as a function of parents’ income; we also can consider this parameter after adjusting for differences in the distribution of characteristics (e.g., race and education) across different values of parents’ income. Another parameter in this class is quantiles of child’s income conditional on parents’ income and other background characteristics (or after adjusting for differences in other background characteristics).

The copula-type parameters that we consider include transition matrices, measures of upward mobility (i.e., the probability that child’s income is greater than their parents’ income), and rank-rank correlations. Each of these are nonlinear measures of intergenerational income mobility and have received considerable interest in recent work on intergenerational mobility (though not much attention has been paid to measurement error for these types of parameters).

2.1 Conditional Distribution-type Parameters

The parameters that we consider in this section come from the distribution of conditional on and which is given by

| (1) |

and which will be identified when the joint distribution of conditional on is identified. In our application on intergenerational income mobility, this conditional distribution is the distribution of child’s income conditional on parents’ income and on other characteristics. One parameter of particular interest is given by setting equal to the poverty line, varying (parents’ income), and fixing characteristics . This gives the fraction of children with income below the poverty line as a function of parents’ income and holding other characteristics fixed. Another parameter of interest is the quantiles of conditional on and . The quantiles are given by

| (2) |

for . These sort of conditional quantiles are what would be recovered, in the absence of measurement error, using quantile regression. Quantile regression has been used in the context of intergenerational mobility in [31], [39], and [11].

In many applications, it makes sense to integrate out the covariates from the above conditional distributions. Manipulations of the distribution of covariates (while fixing the conditional distribution ) are called counterfactual distributions. There are multiple possibilities here, but the most common one is

| (3) |

which adjusts the distribution of covariates at every value of to be given by the overall population distribution of covariates.

Our framework is also closely related to the literature on continuous treatment effects (see, for example, [45, 35, 36, 38]). Like that literature, we consider the case with one particular continuous “treatment” variable whose effect on the outcome is of primary interest, but with other covariates that need to be controlled for. Let denote an individual’s “potential” outcome if they experience treatment ; note that this is well-defined regardless of what treatment level a particular individual actually experiences, but (in the absence of measurement error) only is observed. Next we show that our parameters of interest correspond to the parameters of interest in the continuous treatment effect literature under the commonly invoked assumption of selection on observables.

Assumption S (Selection on Observables).

For all ,

Assumption S says that, after conditioning on covariates , the amount of the treatment is as good as randomly assigned. This is a strong assumption; it seems unlikely that it would hold in the context of intergenerational mobility. That being said, Assumption S is the leading assumption in the continuous treatment effects literature (as well as being a leading assumption in the binary treatment effects literature), and a similar assumption has been made in each of the continuous treatment effect papers cited above. Under Assumption S, it is straightforward to show that

which implies that the distribution of potential outcomes is the same as the distribution in Equation 1. Thus, the expression in Equation 1 is likely to be of interest whether or not one is willing to invoke Assumption S. In particular, Assumption S only serves to give terms like those in Equation 1 a causal interpretation as in the next example.

Example 1 (Dose Response Functions and Distributional Treatment Effects).

The treatment effects mentioned above depend on particular values of the covariates . Often, researchers would like to report a summary measure that integrates out the covariates. For a continuous treatment, researchers often report these dose response functions.666Dose response functions are closely related to unconditional quantile treatment effects that are commonly reported in the case with a binary treatment. For example, in the case of intergenerational income mobility, having an income at a high conditional quantile (e.g., conditional on parents’ education) indicates that a child has a relatively high income conditional on their parents’ income and their parents’ education. If child’s income tends to be increasing in parents’ education, then it could be the case that a child of highly educated parents might be in a low conditional quantile but a middle or upper unconditional quantile. Unconditional quantiles correspond to being in the lower or upper part of the overall income distribution ([37] and [72] contain good discussions of the difference between conditional and unconditional quantiles). In particular, under Assumption S, the distributional dose response function is given by

| (4) |

Interestingly, this is exactly the same transformation of the conditional distribution as for the counterfactual distribution in Equation 3. Moreover, under Assumption S, an unconditional distributional treatment effect of moving from treatment level to treatment level is given by

One can analogously define unconditional quantile treatment effects by the change in particular quantiles when moving from one treatment level to another. Under Assumption S, each of these treatment effect parameters has a causal interpretation.

2.2 Copula-type Parameters

The next set of parameters that we consider depends on the copula of the outcome and the treatment. The copula is the joint distribution of the ranks of random variables. That is, . Sklar’s Theorem, which is one of the most well-known results in the literature on copulas, says that joint distributions can be written as the copula of the marginal distributions where the copula contains the information about the dependence between the two random variables.777[50, 66] are leading references on copulas.

Parameters that depend on the copula of child’s income and parents’ income are common in the intergenerational mobility literature. Intuitively, one reason why these types of parameters are useful is that they only depend on child and parent ranks in the income distribution and will not be contaminated with information related to how income distributions change across generations ([23, 24, 70]). Main examples include transition matrices, upward mobility parameters, and rank-rank correlations. We consider each of these in turn next.

Transition Matrices

Transition matrices are one of the main tools to study intergenerational mobility ([48, 5, 7, 74, 63]). However, not much attention has been paid to transition matrices allowing for measurement error (see [63] for an exception though the arguments are substantially different from ours). Particular cells in transition matrices are given by

where and all take values from 0 to 1 (in a typical case, these are chosen so that cells in the transition matrix have cutoffs at the quartiles of the income distribution for children and parents). Notice that transition matrices can be written in terms of the copula of child’s income and parents’ income. In particular,

| (5) |

where the first equality follows from re-expressing the conditional probability as an unconditional probability and the second equality follows by rewriting the copula in the numerator and because the ranks are uniformly distributed in the denominator.

Upward Mobility

Another parameter of interest in the intergenerational mobility literature is the probability that child’s income rank is greater than their parents’ income rank. Following [5], we define this as a function of parents’ income rank,

The leading case here is when (other values of allow for one to consider the probability of child’s income rank exceeding parents’ income rank by ). In this case, is the fraction of children who have a higher rank in the income distribution than their parents’ rank in the income distribution conditional on their parents’ rank falling in a particular range. Notice that can be written in terms of the copula of parents’ income and child’s income. That is,

where the first equality holds by writing the conditional distribution as the joint distribution divided by the marginal distribution (and because the ranks of parents’ income are uniformly distributed) and the second equality holds because the numerator depends on the joint distribution of the ranks of child’s income and parents’ income (i.e., the copula).

Rank-Rank Correlations

Finally, we consider rank-rank correlations which have received much attention in the intergenerational mobility literature ([23, 25, 21, 22]). These are the correlation between the rank of child’s income and the rank of parents’ income. The primary advantage of the rank-rank correlation over the more traditional intergenerational elasticity is that the rank-rank correlation does not depend on (changes in) the marginal distributions of income over time; this is a desirable feature of an intergenerational mobility measure. In the terms of the literature on copulas and dependence measures, rank-rank correlations are called Spearman’s Rho. The rank-rank correlation is given by

which, like the other parameters in this sections, depends solely on the copula of child’s income and parents’ income.

3 Identification

The previous section suggests that one could obtain all the parameters of interest from the joint distribution of and conditional on . In our setting, this is challenging because and are mismeasured. In particular, we make the following assumptions

Assumption 1 (Measurement Error).

(i)

(ii)

(iii)

Assumption 1 is a “classical” measurement error assumption. Assumption 1(i) says that the researcher observes and which are mismeasured versions of and . Assumption 1(ii) says that the measurement error is independent of , , and . In other words, the joint distribution of the measurement errors does not depend on the true value of child’s permanent income, the true value of parents’ permanent income, and observed covariates. This type of assumption is very common both in the literature on nonlinear models with measurement error (e.g., Assumption 1(i) and (ii) are the same as the assumptions in [42] applied to both the outcome conditional on covariates and the treatment conditional on covariates; similar assumptions are also made in [58, 34], among many others) as well as in the literature on intergenerational mobility that allows for measurement error (e.g., the main case considered in [52] involves classical measurement error though they discuss how their arguments can continue to apply under certain violations of classical measurement error).

Assumption 1(iii) says that and are mutually independent; that is, the measurement error in child’s permanent income is independent of measurement error in parents’ permanent income. This sort of assumption will hold as long as shocks to parents’ income are independent of shocks to child’s income which seems plausible because parents’ income and child’s income are typically observed many years apart from one another. Related assumptions that measurement error for child’s income and parents’ income are uncorrelated are common in the literature (see, for example, Assumption 2 and related discussion in [2]); instead of uncorrelatedness, we require full independence due to focusing on parameters that depend on the entire joint distribution of child’s and parents’ income.

Remark 1.

A leading alternative setup for measurement error in the intergenerational mobility literature is life-cycle measurement error (see [49, 40] as well as [84, 7, 69, 2] for additional related discussion). Here, a typical setup would impose that

where and denote particular ages where child’s income and parents’ income could be observed. This modification to Assumption 1 allows for things like income at younger ages to be systematically lower than permanent income and for the distribution of the measurement error to change at different ages. This sort of model is also consistent with the common finding that estimates of intergenerational mobility tend to be higher when child’s income is observed when they are relatively young. We discuss how to adapt our arguments to the case of life-cycle measurement error in detail in Appendix C. One of the conditions that is often invoked in the life-cycle measurement error literature is that there exist known ages, typically thought to be starting in the early thirties and perhaps lasting until the late forties ([40, 69]), when and . Thus, even in the presence of life-cycle measurement error, one simple way to get back to the case with classical measurement error is to only use observations from prime age children and parents.888This strategy might not always be available, but, especially for applications like ours that use NLSY data where there is little variation in child’s age, this approach may be reasonable.

Remark 2.

Another way to relax the classical measurement error assumption would be to allow for the independence conditions in Assumption 1(ii) and Assumption 1(iii) to hold conditional on (instead of the measurement error also being independent from ). In that case, our arguments exploiting quantile regression do not go through, but it seems likely that one could identify the joint distribution of conditional on covariates building on existing arguments on recovering distributions of mismeasured variables with repeated measurements. In general, many approaches exist for identifying these distributions even in the presence of complicated forms of non-classical measurement error (see [47] for a recent review). In applications where repeated observations are available, it would seem possible to substitute these types of approaches for quantile regression in the first step of our identification arguments. See Remarks 3 and 4 for additional discussion on the pros and cons of using quantile regression in the first step.

3.1 Identifying Parameters of Interest

Recall that all the parameters of our interest will be identified if the joint distribution of and conditional on is identified. Besides the assumptions on measurement error above, the main additional condition that we require is that the quantiles of the outcome conditional on the covariates and the quantiles of the treatment conditional on the covariates are linear in parameters across all quantiles.

Next, we state a series of results for identifying this joint distribution. As a first step, recall that by Sklar’s Theorem ([80]), joint distributions can be written as the copula of their marginals, i.e.,

| (6) |

where is the copula of and conditional on which captures the dependence between the ranks of and conditional on . Equation 6 is helpful because it splits the identification challenge into two parts: (i) identifying the marginal distributions and (ii) identifying the copula. This section provides two propositions showing that (i) the distributions of the outcome/treatment conditional on covariates are identified; and (ii) the conditional copula in Equation 6 is identified. Taken together, these results show that the joint distribution is identified and, therefore, that all of our parameters of interest are also identified.

Before stating these results, we make the following additional assumption.

Assumption 2 (Quantile Regression).

(i) with .

(ii) with .

Assumption 2 imposes a quantile regression type of model for and in terms of . Assumption 2 implies that and arise from models that are both monotonically increasing in a scalar unobservable as well as being known up to the parameters and , respectively. [42] show that QR parameters are identified in exactly this sort of setup. Here, identifying and also implies that the distributions of the outcome/treatment conditional on covariates are also identified. The next proposition states this result. Some additional more technical conditions required for identification of the reduced form distributions are listed in Assumption A1 in the appendix.

Proposition 1.

Under Assumptions 1 and 2 and Assumption A1 in the appendix, and are uniquely identified for .

With the quantiles identified, one can obtain the marginals simply by inverting the quantiles. The next part of our identification argument shows that the copula of and conditional on covariates, , is identified.

Proposition 2.

Under Assumptions 1 and 2, Assumption A1 in the appendix, and under the assumption that the characteristic functions of and are non-vanishing, is identified.

Together, Propositions 1 and 2 imply that the joint distribution is identified — Proposition 1 implies that the marginals are identified (because the conditional quantiles can be inverted) and Proposition 2 implies that the conditional copula is identified. These results also imply that all of our parameters of interest — both the Conditional Distribution-type parameters and the Copula-type parameters — are identified.

Remark 3.

The quantile regression structure imposed in Assumption 2 is crucial for being able to identify the conditional distributions of the outcome and the treatment without requiring repeated measurements of the outcome and treatment. It does not require the parameters and to have a structural/causal interpretation, but it does require that both models of the conditional quantiles are correctly specified. There is an interesting connection between this requirement and very early work on identifying the distribution of a variable of interest in the presence of measurement error (e.g., [15]); this literature often invoked parametric assumptions on the measurement error (e.g., that the measurement error follows a normal distribution) which enabled recovering the distribution of the random variable of interest without extra requirements such as repeated measurements. Instead of making a parametric assumption about the measurement error, Assumption 2 amounts to a flexible parametric assumption on the variable of interest while leaving the distribution of the measurement error unrestricted up to some regularity conditions.

Remark 4.

Assumption 2 is relatively less important for showing the result in Proposition 2; for example, given that the conditional distributions of the outcome and treatment are identified and that the distributions of the measurement errors in the outcome and treatment equation are identified, Proposition 2 does not otherwise rely on Assumption 2. This suggests that our arguments in the second step are likely to go through under alternative first step assumptions. In particular, in applications where a researcher has access to repeated measurements of the outcome and treatment, it might be attractive to impose less structure than is provided by the quantile regression setup in Assumption 2.

Remark 5.

A leading alternative to our approach would be to use quantile regression of the outcome conditional on the treatment and covariates. We are unaware of work that allows for measurement error in both the outcome and the treatment in a quantile regression setup. Conditional on handling measurement error, this setup would deliver the Conditional Distribution-type parameters that we consider; however, it would not immediately deliver the Copula-type parameters that we consider.

4 Estimation

This section considers estimating the parameters of interest from the previous section using our approach. We make some simplifying assumptions next that make estimation simpler; in general, we have tried to strike a balance between generality and being able to implement our model in a practical way in realistic applications though noting that one could proceed in a less restrictive way here at the cost of making estimation more difficult to implement. In Appendix D, we assess the performance of our estimation strategy using Monte Carlo simulations.

Assumption 3 (Random Sampling).

are iid draws from the joint distribution .

Assumption 4 (Distribution of Measurement Error).

and

Assumption 5 (Copula).

is the same across all values of , and

Assumption 6 (Splines).

Let denote a (fixed) number of knots and consider the sequence of equally spaced , . For any ,

where and ; i.e., is the closest smaller value of for which has been estimated and is the closest larger value of for which has been estimated.

Assumption 3 says that we have access to a sample of iid draws of , , and . Assumption 4 says that the distribution of the measurement errors and is known up to a finite number of parameters. In practice, we will assume that and are both mixtures of normal distributions. This is similar to what [42] do in their application, and mixtures of normals are likely to have good approximating properties for continuously distributed measurement error. The first part of Assumption 5 says that the conditional copula does not vary across different values of the covariates (note that this does not imply that it is equal to the unconditional copula). This sort of condition is very commonly invoked in the literature on conditional copulas (see, for example, the discussion in [28]). The second part of Assumption 5 says that the conditional copula of and is known up to a finite dimensional number of parameters. In principle, the conditional copula could be nonparametrically estimated (Proposition 2 implies that it is identified though it does not provide a directly estimable expression). While possible, proceeding this way is likely to be quite complicated in practice (see, for example, [58, 57, 83, 34]). Instead, we proceed by considering the case where is specified parametrically. Assumption 6 allows us to recover the process from estimating a finite number of , i.e., estimate them over a finite grid of and interpolate the process from the particular set of that we estimate (see [85] and [3] for similar assumptions in related contexts).

4.1 Step 1: Estimating Conditional Quantiles

The first step is to estimate and . In this section, we outline the estimation procedure for and note that the arguments for are identical.

First, notice that, if were observed, then we could estimate the QR parameters by quantile regression of on . Next, let which is the derivative of the check function . If were observed, the first order condition for estimating the QR parameters is given by

This is an infeasible moment condition because (and ) is unobserved. However, notice that it can be re-written as

| (7) |

Further, notice that from Bayes’ Theorem,

and that

which hold by Assumption 1(i)999To see the first part, notice that which holds by Assumption 1(ii) and then the result follows immediately. and Assumption 1(ii). Moreover, given , the conditional density of can be recovered as with (see, for example, [76]). Equation 7 thus suggests a two-step estimation procedure. In the first step, make draws from ; in the second step, run QR using the observed , , and the simulated measurement error. In practice, we use the following estimation scheme, iterating back and forth between making draws of the measurement error and estimating the parameters using QR and maximum likelihood.

Algorithm 1.

Initialize:

1. Set the counter . Set initial values of the parameters . In the application, we set equal to the estimates of the QR parameters ignoring measurement error. We also set the measurement error to be a mixture of normals with means given by equally spaced points from to normalized to have mean 0. Set a tolerance level .

Iterate:

2. Set . For , make draws from . In practice, we use a Metropolis-Hastings algorithm for this step.

3. Use the pseudo-observations from Step 2 above, estimate using quantile regression of as the outcomes and as the covariates. Estimate using the same observations; in practice, we use an internal EM-algorithm for this step — this is a standard (and relatively computationally cheap) approach for estimating mixtures of normals models (see, for example, [61]).

4. If , return , else continue iterating.

4.2 Step 2: Estimating the copula parameter

Under Assumption 5, the copula is known up to a finite number of parameters. In this section, we propose to estimate the copula parameters by simulated maximum likelihood.

Building up to an estimation routine based on maximum likelihood, first notice that the observed distribution of mismeasured variables and are given by

| (8) |

where the second equality holds by Assumption 1, and the third holds (after some manipulation) by Proposition 2 and Assumption 5. Note that Proposition 1 implies that , , , and are identified; they are each known up to a finite number of parameters by Assumptions 4, 5 and 6. What remains is estimating the copula parameters.

Section 4.2 suggests estimating the copula parameters by maximum likelihood, and it implies

where is the copula pdf and the expectation is over the measurement error variables and . And the copula parameter can be obtained by maximizing the log likelihood function. Let

where and are draws from for . Then, we estimate the copula parameter by

4.3 Step 3: Estimating Parameters of Interest

First, we focus on estimating the Conditional Distribution-type parameters such as and . [10] study the relationship between copulas and quantile regression in the bivariate case (see also [17]). The bivariate case is the relevant case for the setup in the current paper as the results for quantile regression and a bivariate copula go through in our case with everything holding conditional on . The results of [10, p. 726 ] imply that

| (9) |

where which provides an alternative expression for (here we also use Assumption 5 which says that the conditional copula does not vary with ). Under the conditions that is invertible in its first argument, the quantiles can be directly obtained by

| (10) |

where is the inverse of with respect to its first argument.

Example 2 (Archimedean Family of Copulas).

Example 3.

The Clayton copula is a particular Archimedean family with where we restrict ; the generator function is given by , and one can show that

and

The Clayton copula has the nice property that it has a one to one correspondence with Kendall’s Tau.

Example 4 (Gaussian Copula).

The Gaussian copula is given by where is the cdf of a standard normal random variable and is the cdf of a pair of random variables that are jointly normally distributed with mean 0, variance 1, and correlation coefficient . Then,

and

See [10] for more discussion of particular parametric families of copulas and quantile regression.

Next, we consider estimating our Copula-type parameters. One thing to notice is that the copula that we estimated was the conditional copula, but the copula parameters that we focus on are functionals of the unconditional copula. However, our estimation procedure produces draws for each individual at each simulation iteration.101010To be precise, given the estimates of the conditional copula, for a particular observation , we can make draws of where is the estimated conditional copula. Then, we can set and where and come from the first step quantile regression estimates. These are draws from the joint distribution of and can be used directly to estimate the Copula-type parameters. For example, to estimate particular cells in the transition matrix, one can simply plug in to Equation 5; i.e.,

where is the estimated unconditional copula that comes from the simulation draws.

Similarly, upward mobility parameters can be estimated by

where and are simulated draws of child’s income and parents’ income and and are corresponding estimators of their unconditional distributions. This amounts to simply counting the number of children whose income exceeds their parents’ income conditional on parents’ income being in a certain range using the simulated data. Finally, rank-rank correlations can be computed by calculating Spearman’s Rho using the simulated data (i.e., ranking the simulated outcome and treatment and computing the correlation of these ranks).

Inference

In principle, the asymptotic theory for our estimator should be fairly straightforward. Under the additional conditions in this section, particularly Assumptions 3, 4, 5 and 6, our estimation procedure is essentially a parametric three-step simulation based estimator. Standard results on stochastic EM algorithms (see, for example, [68, 67, 3]) can be used to show that the resulting functionals are asymptotically normal and converge at the parametric rate. The resulting asymptotic distributions will be complicated though. In particular, due to estimating the quantiles in the first step, part of the asymptotic variance will involve conditional densities in the denominator. These will be challenging to estimate as they require smoothing and choosing tuning parameters. Similarly, the part of the variance coming from estimating the copula will depend on derivatives of the copula pdf which are likely to be complicated as well. Instead of pursuing this route, we instead use the empirical bootstrap to approximate the limiting distribution of our estimators.

5 Intergenerational Income Mobility allowing for Measurement Error

In this section, we use the methods developed in the previous sections to estimate a variety of nonlinear measures of intergenerational mobility allowing for measurement error in both parents’ income and child’s income and assess how much allowing for measurement error affects the resulting estimates.

Data

The data that we use come from the 1997 National Longitudinal Survey of Youth (NLSY97). The NLSY97 represents the 1997 cohort of the National Longitudinal Survey that contains detailed panel data on individuals who were 12-16 at the start of 1997. It is a very useful resource for studying recent intergenerational income mobility. Following much work on intergenerational income mobility, we focus on a subset of the data involving fathers and sons. We use son’s total labor income in 2014 (which is self-reported in the 2015 survey wave) as the outcome variable. In 2014, survey respondents are between 29 and 33 years old. We use father’s total labor income in 1996 (in 2014 dollars) as the treatment variable.

The main advantages of using the NLSY97 relative to other datasets such as the Panel Study of Income Dynamics (PSID) are (i) the NLSY97 sample sizes tend to be larger and there are more individuals who are of a similar age, and (ii) the NLSY97 tends to have more individual level covariates that can be included in our analysis. There are two main disadvantages, however. The first is that since we are looking at very recent intergenerational income mobility, we do not observe permanent incomes; we only observe several years of income and at relatively young ages for sons. In practice, we only use income reported for the year 2014 and discard information about income in other years. The second disadvantage is that we only observe father’s income in a single year as well — the first year of the survey. Therefore, the techniques that we have developed in the current paper to deal with measurement error with only a single observation of parents’ income and child’s income seem necessary in this case.

[caption=Summary Statistics,label=tab:ss,pos=!tbp,]lllll\tnote[]Notes: The table provides summary statistics by father’s income quartiles.

Sources: NLSY97, as described in text.\FL Q1 Q2 Q3 Q4 \MLSon’s Income46.1750.8259.1866.34\NN(1.99)(2.09)(2.46)(3.07)\NNFather’s Income19.4643.2064.22112.28\NN(0.57)(0.34)(0.38)(3.35)\NN% White0.530.670.740.84\NN(0.03)(0.03)(0.03)(0.02)\NN% Black0.140.130.130.06\NN(0.02)(0.02)(0.02)(0.02)\NN% Hispanic0.320.190.120.09\NN(0.03)(0.02)(0.02)(0.02)\NNSon Age 199714.1514.1614.2714.27\NN(0.08)(0.09)(0.09)(0.10)\NNFather Age 199740.6140.9141.9742.79\NN(0.43)(0.35)(0.32)(0.33)\NNFather Education 11.3813.0313.9215.32\NN(0.20)(0.15)(0.14)(0.18)\LL

Besides the income variables for fathers and sons, we also observe race, ethnicity, ages of both fathers and sons, and the father’s education (in years). We drop observations that are missing values for any of these. This results in a dataset with 1,096 observations. Summary statistics for our dataset are available in LABEL:tab:ss. Each column provides average values of each variable by quartile of father’s income. Like almost all work on intergenerational mobility, we see that son’s income is increasing in father’s income and that sons from low income families tend to have higher incomes than their fathers while sons from high income families tend to have lower incomes than their fathers. However, the estimated intergenerational elasticity (IGE) is only 0.054 in our data. This is broadly similar to early studies of intergenerational income mobility that ignored measurement error in income variables. The estimated value of the IGE using our data is small though relative to more recent IGE estimates that account for measurement error in income in a linear regression framework. The relatively low IGE estimate based on our sample is likely related to (i) the relatively young ages at which we observe son’s income, and (ii) that we only observe a single year of income for fathers and sons rather than their actual permanent income. Both of these issues often lead to lower estimates of the IGE. In terms of other covariates, the percentage of sons that are white, father’s age, and father’s education are all increasing in father’s income. The percentage of sons that are black and the percentage of sons that are Hispanic are both decreasing in father’s income. The son’s age in 1997 does not appear to be correlated with father’s income.

Implementation Details

In this section, the only covariates that we include are son’s age and father’s age; this sort of specification is common in the intergenerational mobility literature. In Appendix E, we provide additional results that condition on more covariates. For our first step quantile regression estimates (that allow for measurement error), we estimate over equally spaced values of from 0.02 to 0.98. We specify the measurement error for both son’s income and father’s income as a mixture of two normal distributions. Given an estimate of , for each observation we make 100 measurement error draws that come from the last 100 draws from a Metropolis-Hastings algorithm after 200 burn-in draws. Finally, we set the tolerance level to be equal to where is the number of regressors and is the number of mixture components for the measurement error (here and which includes an intercept). For estimating the conditional copula in the second step of our estimation procedure, we specify that the conditional copula is a Clayton copula and estimate its parameter. In Appendix E, we provide analogous results to the ones in this section that use a Gaussian copula instead. To estimate the copula parameter, we use 250 simulated measurement error draws in our simulated maximum likelihood procedure. We report standard errors and confidence intervals below that come from using the empirical bootstrap with 100 iterations.

Copula-Type Parameters

To start with, we consider copula-type parameters: rank-rank correlations, transition matrices, and upward mobility measures. Although our estimation approach involves estimating quantile regressions conditional on covariates (and accounting for measurement error), the copula-type parameters that we consider are unconditional and, therefore, can be directly compared to rank-rank correlations, transition matrices, or upward mobility measures computed directly from the observed data. We report both of these types of results in this section which gives a straightforward way to compare our estimates that allow for measurement error to estimates that ignore measurement error.

We start with rank-rank correlations. Using the raw data (and ignoring measurement error), we estimate the rank-rank correlation is equal to 0.208 (s.e.=0.029). By contrast, our estimates of the rank-rank correlation that allows for measurement error is 0.357 (s.e.=0.092). The difference between these estimates is large — our estimates that adjust for measurement error suggest substantially less intergenerational mobility (due to the rank-rank correlations being higher) than is implied by the estimates that use the observed data directly.

| Father’s Income Quartile | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | ||

| 4 | 0.121 | 0.220 | 0.293 | 0.366 | |

| (0.032) | (0.013) | (0.012) | (0.034) | ||

| 3 | 0.162 | 0.253 | 0.286 | 0.299 | |

| (0.026) | (0.004) | (0.013) | (0.012) | ||

| 2 | 0.245 | 0.279 | 0.256 | 0.220 | |

| (0.007) | (0.018) | (0.003) | (0.014) | ||

| 1 | 0.471 | 0.248 | 0.166 | 0.115 | |

| Son’s Income Quartile | (0.063) | (0.008) | (0.026) | (0.031) | |

| Father’s Income Quartile | |||||

|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | ||

| 4 | 0.161 | 0.234 | 0.255 | 0.376 | |

| (0.020) | (0.023) | (0.027) | (0.030) | ||

| 3 | 0.197 | 0.215 | 0.303 | 0.266 | |

| (0.024) | (0.031) | (0.029) | (0.027) | ||

| 2 | 0.328 | 0.230 | 0.314 | 0.175 | |

| (0.028) | (0.037) | (0.038) | (0.026) | ||

| 1 | 0.303 | 0.277 | 0.175 | 0.190 | |

| Son’s Income Quartile | (0.024) | (0.027) | (0.027) | (0.028) | |

Notes: The table provides estimates of transition matrices either allowing for measurement error using the techniques developed in the paper (Panel (a)) or coming directly from the observed data (Panel (b)). The columns are organized by quartiles of father’s income; i.e., columns labeled “1” use data from fathers whose income is in the first quartile. Similarly, rows are organized by quartiles of son’s income. Standard errors are computed using the bootstrap.

Sources: NLSY97, as described in text.

The results on transition matrices are presented in Table 1. First, ignoring measurement error (as in Panel (b)), the estimated transition matrix indicates a large degree of intergenerational income mobility. While sons generally are somewhat more likely to stay in the same income quartile as their father was in, large movements in the income distribution do not appear to be uncommon. For example, for a son whose father was in the lowest quartile of the income distribution, we estimate the probability that the son is in the lowest quartile of the income distribution is 30% but that the probability that the son moves to the top quartile of the income distribution is 16%. Similarly, for fathers in the top quartile of the income distribution, we estimate that the probability their son is in the top quartile of the income distribution to be 38% and that the probability that their son is in the bottom quartile of the income distribution to be 19%. Allowing for measurement error (as in Panel (a)) indicates substantially less intergenerational mobility. For example, for fathers in the lowest quartile of the income distribution, we estimate that 47% of their sons stay in the lowest quartile of the income distribution and only 12% move to the top quartile of the income distribution. For fathers in the top quartile of the income distribution, we estimate that 37% of their sons stay in the top quartile while only 12% move to the bottom quartile.

Finally, we present upward mobility estimates. These are estimates of the fraction of sons whose rank in the income distribution exceeds the rank of their fathers. We present these results by quartile of father’s income as well as separately by whether we use our approach that allows for measurement error or just use the observed data directly. Compared to using the observed data directly, the upward mobility estimates allowing for measurement error are lower when the father is in the first quartile of the income distribution and higher when the father is in the second, third, or fourth quartile of the income distribution. As for the other parameters in this section, these results suggest that allowing for measurement error reduces estimates of intergenerational income mobility.

[pos=!tbp,caption=Upward Mobility,label=tab:um]lllll\tnote[]Notes: The table provides estimates of upward mobility allowing for measurement error using the techniques developed in the paper (top panel) or coming directly from the observed data (bottom panel). The columns are organized by quartiles of father’s income; i.e., columns labeled “1” use data from fathers whose income is in the first quartile. Standard errors are computed using the bootstrap.

Sources: NLSY97, as described in text.\FL Father’s Income Quartile \NN 1 2 3 4 \MLMeasurement Error\NN \NN \MLObserved\NN \NN \LL

Conditional Distribution-Type Results

The next set of results that we present correspond to the Conditional Distribution-type parameters. Because Assumption S seems unlikely to hold in the case of intergenerational mobility, we focus on reporting conditional quantiles and conditional distributions as in Equations 1 and 2. In this section, we primarily compare estimates using our approach that allows for measurement error to estimates of conditional distribution-type parameters that ignore measurement error and come directly from quantile regression estimates of son’s income on father’s income, son’s age, and father’s age.

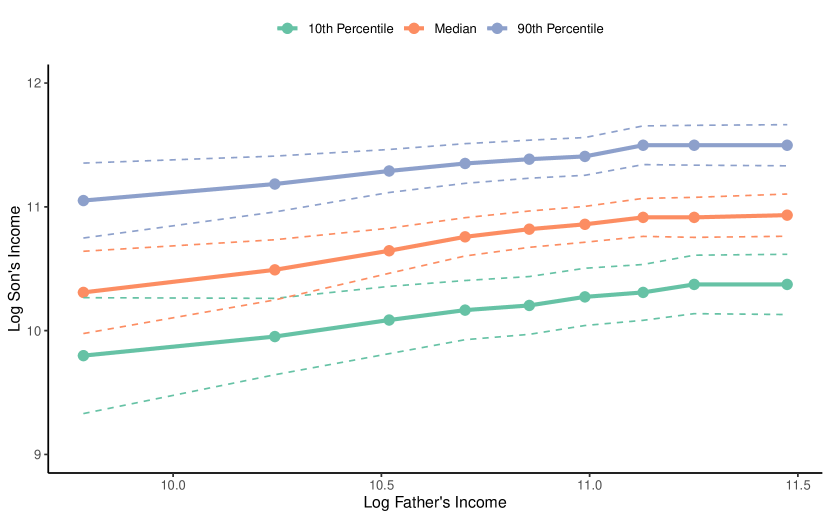

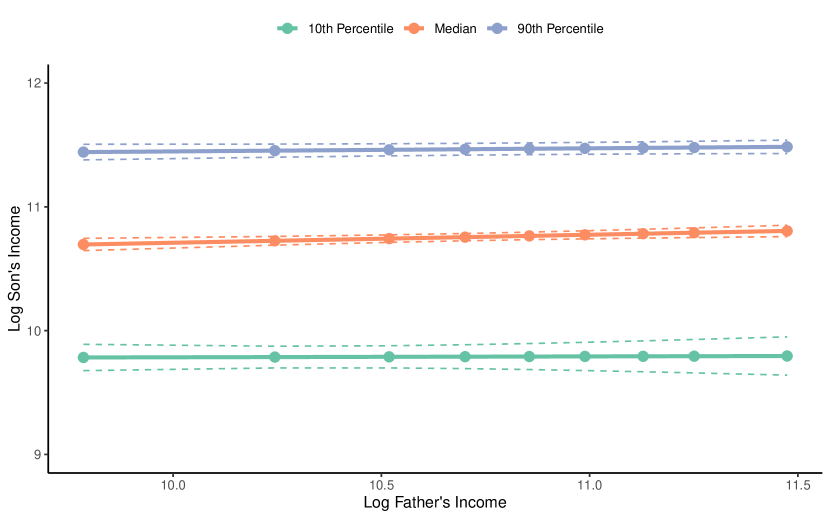

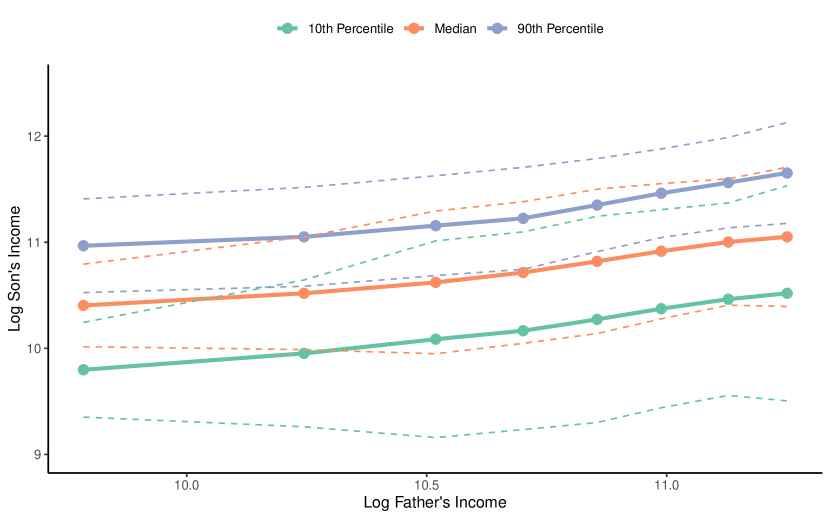

Notes: The figure provides estimates of quantiles of son’s income as a function of father’s income and conditional on son’s age and father’s age being equal to their averages in the sample. The estimates in Panel (a) come from the approach suggested in the current paper that allows for measurement error. The estimates in Panel (b) ignore measurement error and come from quantile regression of observed son’s income on observed father’s income and covariates. The three lines in each panel are estimates of the 10th percentile, median, and 90th percentile of son’s income which are estimated at the 10th, 20th, …, and 90th percentiles of father’s income. Standard errors are computed using the bootstrap.

Figure 1 contains estimates of conditional quantiles (the 10th percentile, median, and 90th percentile) of son’s income as a function of father’s income where son’s age and father’s age (both in 1997) are set at their average values in our sample (14 and 42, respectively). Estimates of these conditional quantiles are reported at the 10th, 20th, …, and 90th percentiles of father’s income. These are unequally spaced values of father’s income, but they range from about $18,000 to just over $96,000. Panel (a) contains estimates using our approach that allows for measurement error and Panel (b) contains estimates coming from quantile regression of son’s income on father’s income and covariates ignoring measurement error.

We start by discussing the estimates that ignore measurement error in Panel (b). By construction, the quantile regression estimates in Panel (b) are linear. Ignoring measurement error, the slope of the quantile regression estimates are very flat indicating little effect of father’s income on son’s income. For interpreting the results, we mainly discuss results conditional on father’s income being in the 10th percentile (which is roughly equal to the poverty line) and in the 90th percentile. Using quantile regression and ignoring measurement error, the 10th percentile of son’s income conditional on having father’s income at the 10th percentile (and conditional on having average values for father’s age and son’s age) is estimated to be $17,700, the median is estimated to be $44,200, and the 90th percentile is estimated to be $93,200. For sons whose father is in the 90th percentile of the income distribution, the distribution of their income is very similar — we estimate that the 10th percentile (conditional on having average values for father’s age and son’s age) is $17,900, the median is $49,300, and the 90th percentile is $97,200.111111For , from our quantile regression estimates of the log of son’s income on the log of father’s income and father’s and son’s age, the estimated effect of father’s income is small (ranging from 0.005 to 0.067) but positive across all values of . The estimated effect is only statistically significant for . This immediately translates to the small estimated effects of father’s income in Panel (b) of Figure 1.

Moving to results that allow for measurement error (these are in Panel (a) of Figure 1), there are notable differences. The slopes of the estimates are steeper which indicates a stronger relationship between father’s and son’s income. For sons whose father’s income is in the 10th percentile, allowing for measurement error substantially reduces the median and 90th percentile of their income distribution — the median is now estimated to be $30,000 and the 90th percentile to be $63,000. The other major difference is in the lower part of the income distribution for sons whose fathers had high incomes. There, we estimate that the 10th percentile of income is $32,000 and the median income is $56,000 — these are both notably higher than our earlier quantile regression estimates that ignored measurement error.

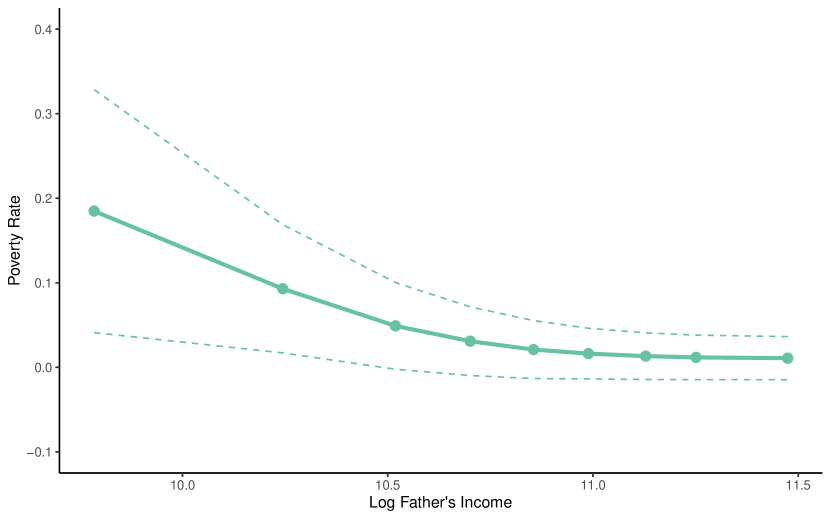

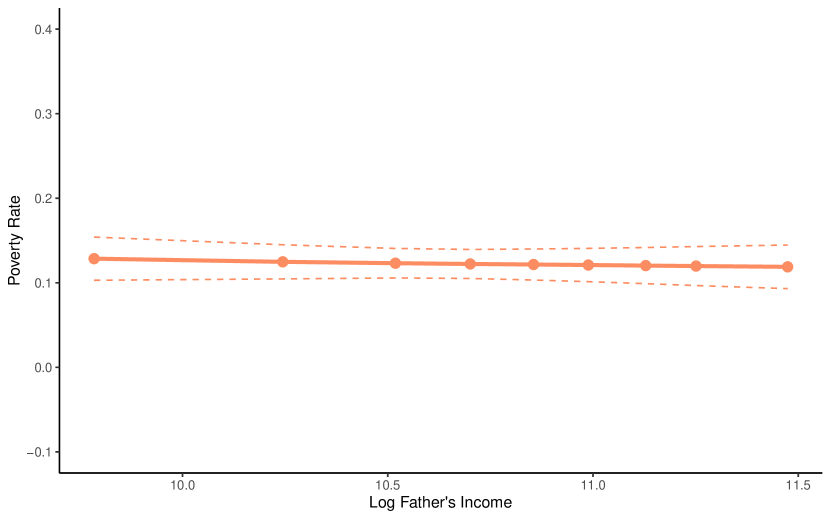

Notes: The figure provides estimates of son’s poverty rate as a function of father’s income and conditional on son’s age and father’s age being equal to their averages in the sample. The estimates in Panel (a) come from the approach suggested in the current paper that allows for measurement error. The estimates in Panel (b) ignore measurement error and come from inverting quantile regressions of observed son’s income on observed father’s income and covariates. The poverty line is set at (the logarithm of) $20,000. Standard errors are computed using the bootstrap.

Next, we consider estimates of the fraction of sons whose income is below the poverty line (which we set at $20,000) as a function of father’s income and conditional on father’s and son’s ages being set at their average in our sample. Using quantile regression (and ignoring measurement error), we estimate that 12.8% of sons whose father’s income is in the 10th percentile have income that is below the poverty line. For sons whose father’s income was in the 90th percentile, we estimate that 11.9% have income that is below the poverty line. Allowing for measurement error again has a large effect and indicates substantially less intergenerational income mobility. For sons whose father’s income is in the 10th percentile, we estimate that 18.5% have income below the poverty line, but for sons whose father’s income is in the 90th percentile, we estimate that only 1.1% have income below the poverty line.

6 Conclusion

In this paper, we developed a new method to obtain the joint distribution of an outcome and a continuous treatment conditional on covariates when the outcome and the treatment are potentially measured with error. Our main innovation and departure from the existing literature was to model both the outcome and the treatment as a function of the covariates; that is, changing the problem from measurement error on the left and right to two cases of measurement error on the left. Then, we showed that the copula of the outcome and treatment was identified in this setup which, in turn, implies that a large number of parameters of interest (particularly in the intergenerational mobility and continuous treatment effects literature) are identified.

We applied our approach to study intergenerational income mobility. We use this as a leading example for our approach because researchers studying intergenerational income mobility only have noisy measurements of an individual’s permanent income. In addition, we used recent data from the NLSY where only one observation of child’s and parents’ income was available which means that many existing approaches to accounting for measurement error are not applicable. We found that accounting for measurement error led to substantially lower estimates of a variety of measures of intergenerational mobility relative to implementing common alternative approaches while ignoring measurement error.

References

- [1] Jason Abrevaya and Jerry Hausman “Semiparametric estimation with mismeasured dependent variables: An application to duration models for unemployment spells” In Annales D’Economie et de Statistique 55/56, 1999, pp. 243–275

- [2] Yonghong An, Le Wang and Ruli Xiao “A nonparametric nonclassical measurement error approach to estimating intergenerational mobility elasticities” In Journal of Business & Economic Statistics Taylor & Francis, 2020, pp. 1–17

- [3] Manuel Arellano and Stéphane Bonhomme “Nonlinear panel data estimation via quantile regressions” In The Econometrics Journal 19.3 Wiley Online Library, 2016

- [4] J.R. Behrman and P. Taubman “The intergenerational correlation between children’s adult earnings and their parents income: Results from the Michigan Panel Survey of Income Dynamics” In Review of Income and Wealth 36.2, 1990, pp. 115–127

- [5] Debopam Bhattacharya and Bhashkar Mazumder “A nonparametric analysis of black–white differences in intergenerational income mobility in the United States” In Quantitative Economics 2.3 Wiley Online Library, 2011, pp. 335–379

- [6] Anders Björklund, Jesper Roine and Daniel Waldenström “Intergenerational top income mobility in Sweden: Capitalist dynasties in the land of equal opportunity?” In Journal of Public Economics 96.5 Elsevier, 2012, pp. 474–484

- [7] Sandra E Black and Paul Devereux “Recent developments in intergenerational mobility” In Handbook of Labor Economics 4 Amsterdam: North-Holland, 2011, pp. 1487–1541

- [8] John Bound, Charles Brown and Nancy Mathiowetz “Measurement error in survey data” In Handbook of Econometrics 5 Elsevier, 2001, pp. 3705–3843

- [9] John Bound and Alan B Krueger “The extent of measurement error in longitudinal earnings data: Do two wrongs make a right?” In Journal of Labor Economics 9.1 University of Chicago Press, 1991, pp. 1–24

- [10] Eric Bouyé and Mark Salmon “Dynamic copula quantile regressions and tail area dynamic dependence in Forex markets” In The European Journal of Finance 15.7-8 Taylor & Francis, 2009, pp. 721–750

- [11] Espen Bratberg, Oivind Anti Nilsen and Kiell Vaage “Trends in intergenerational mobility across offspring’s earnings distrbution in Norway” In Industrial Relations 46.1, 2007, pp. 112–129

- [12] Bernt Bratsberg, Knut Røed, Oddbjørn Raaum, Robin Naylor, Markus Jantti, Tor Eriksson and Eva Osterbacka “Nonlinearities in intergenerational earnings mobility: Consequences for cross-country comparisons” In The Economic Journal 117.519 Oxford University Press Oxford, UK, 2007, pp. C72–C92

- [13] Brantly Callaway and Weige Huang “Local intergenerational elasticities” In Economics Bulletin 39.2 AccessEcon, 2019, pp. 919–928

- [14] Brantly Callaway and Weige Huang “Distributional effects of a continuous treatment with an application on intergenerational mobility” In Oxford Bulletin of Economics and Statistics 82.4 Wiley Online Library, 2020, pp. 808–842

- [15] Raymond J Carroll and Peter Hall “Optimal rates of convergence for deconvolving a density” In Journal of the American Statistical Association 83.404 Taylor & Francis, 1988, pp. 1184–1186

- [16] Christopher Cavanagh and Robert P. Sherman “Rank estimators for monotonic index models” In Journal of Econometrics 84.2, 1998, pp. 351–381

- [17] Xiaohong Chen and Yanqin Fan “Estimation of copula-based semiparametric time series models” In Journal of Econometrics 130.2 Elsevier, 2006, pp. 307–335

- [18] Victor Chernozhukov, Ivan Fernandez-Val and Blaise Melly “Inference on counterfactual distributions” In Econometrica 81.6 Wiley Online Library, 2013, pp. 2205–2268

- [19] Andrew Chesher “The effect of measurement error” In Biometrika 78.3 Oxford University Press, 1991, pp. 451–462

- [20] Andrew Chesher “Understanding the effect of measurement error on quantile regressions” In Journal of Econometrics 200.2 Elsevier, 2017, pp. 223–237

- [21] Raj Chetty and Nathaniel Hendren “The impacts of neighborhoods on intergenerational mobility I: Childhood exposure effects” In The Quarterly Journal of Economics 133.3 Oxford University Press, 2018, pp. 1107–1162

- [22] Raj Chetty, Nathaniel Hendren, Maggie R Jones and Sonya R Porter “Race and economic opportunity in the United States: An intergenerational perspective” In The Quarterly Journal of Economics 135.2 Oxford University Press, 2020, pp. 711–783

- [23] Raj Chetty, Nathaniel Hendren, Patrick Kline and Emmanuel Saez “Where is the land of opportunity? The geography of intergenerational mobility in the United States” In The Quarterly Journal of Economics 129.4 Oxford University Press, 2014, pp. 1553–1623

- [24] Raj Chetty, Nathaniel Hendren, Patrick Kline, Emmanuel Saez and Nicholas Turner “Is the United States still a land of opportunity? Recent trends in intergenerational mobility” In American Economic Review 104.5, 2014, pp. 141–47

- [25] William J Collins and Marianne H Wanamaker “Up from slavery? African American intergenerational economic mobility since 1880” Working Paper, 2017

- [26] S.R. Cosslett “Efficient semiparametric estimation of censored and truncated regressions via a smoothed self-consistency equation” In Econometrica 72.4, 2004, pp. 1277–1293

- [27] Michele De Nadai and Arthur Lewbel “Nonparametric errors in variables models with measurement errors on both sides of the equation” In Journal of Econometrics 191, 2016, pp. 19–32

- [28] Alexis Derumigny and Jean-David Fermanian “About tests of the “simplifying” assumption for conditional copulas” In Dependence Modeling 5.1 De Gruyter Open, 2017, pp. 154–197

- [29] Peter J Diggle and Peter Hall “A Fourier approach to nonparametric deconvolution of a density estimate” In Journal of the Royal statistical society: series B (Methodological) 55.2 Wiley Online Library, 1993, pp. 523–531

- [30] John DiNardo, Nicole M Fortin and Thomas Lemieux “Labor market institutions and the distribution of wages, 1973-1992: A semiparametric approach” In Econometrica 64.5, 1996, pp. 1001–1044

- [31] Eric R Eide and Mark H Showalter “Factors affecting the transmission of earnings across generations: A quantile regression approach” In Journal of Human Resources JSTOR, 1999, pp. 253–267

- [32] Jianqing Fan “On the optimal rates of convergence for nonparametric deconvolution problems” In The Annals of Statistics JSTOR, 1991, pp. 1257–1272

- [33] Iván Fernández-Val and Martin Weidner “Individual and time effects in nonlinear panel models with large N, T” In Journal of Econometrics 192.1 Elsevier, 2016, pp. 291–312

- [34] Sergio Firpo, Antonio F Galvao and Suyong Song “Measurement errors in quantile regression models” In Journal of Econometrics 198.1 Elsevier, 2017, pp. 146–164

- [35] Carlos A Flores “Estimation of dose-response functions and optimal doses with a continuous treatment” Working Paper, 2007

- [36] Carlos A Flores, Alfonso Flores-Lagunes, Arturo Gonzalez and Todd C Neumann “Estimating the effects of length of exposure to instruction in a training program: The case of Job Corps” In Review of Economics and Statistics 94.1 MIT Press, 2012, pp. 153–171

- [37] Markus Frolich and Blaise Melly “Unconditional quantile treatment effects under endogeneity” In Journal of Business & Economic Statistics 31.3 Taylor & Francis, 2013, pp. 346–357

- [38] Antonio F Galvao and Liang Wang “Uniformly semiparametric efficient estimation of treatment effects with a continuous treatment” In Journal of the American Statistical Association 110.512 Taylor & Francis, 2015, pp. 1528–1542

- [39] Nathan D Grawe “Reconsidering the use of nonlinearities in intergenerational earnings mobility as a test for credit constraints” In Journal of Human Resources 39.3 University of Wisconsin Press, 2004, pp. 813–827

- [40] Steven Haider and Gary Solon “Life-cycle variation in the association between current and lifetime earnings” In American Economic Review 96.4, 2006, pp. 1308–1320

- [41] Jerry Hausman, Jason Abrevaya and F.M. Scott-Morton “Misclassification of the dependent variable in a discrete-response setting” In Journal of Econometrics 87.2, 1998, pp. 239–269

- [42] Jerry Hausman, Haoyang Liu, Ye Luo and Christopher Palmer “Errors in the dependent variable of quantile regression models” In Econometrica 89.2 Wiley Online Library, 2021, pp. 849–873

- [43] Jerry A Hausman, Whitney K Newey, Hidehiko Ichimura and James L Powell “Identification and estimation of polynomial errors-in-variables models” In Journal of Econometrics 50.3 Elsevier, 1991, pp. 273–295

- [44] Jerry A Hausman, Whitney K Newey and James L Powell “Nonlinear errors in variables estimation of some Engel curves” In Journal of Econometrics 65.1 Elsevier, 1995, pp. 205–233

- [45] Keisuke Hirano and Guido W Imbens “The propensity score with continuous treatments” In Applied Bayesian Modeling and Causal Inference from Incomplete-Data Perspectives 226164 Chichester: Wiley & Sons, 2004, pp. 73–84

- [46] Cheng Hsiao “Consistent estimation for some nonlinear errors-in-variables models” In Journal of econometrics 41.1 Elsevier, 1989, pp. 159–185

- [47] Yingyao Hu “The econometrics of unobservables: Applications of measurement error models in empirical industrial organization and labor economics” In Journal of Econometrics 200.2 Elsevier, 2017, pp. 154–168

- [48] Markus Jantti, Bernt Bratsberg, Knut Roed, Oddbjorn Raaum, Robin Naylor, Eva Osterbacka, Anders Bjorklund and Tor Eriksson “American exceptionalism in a new light: A comparison of intergenerational earnings mobility in the Nordic countries, the United Kingdom and the United States” Working Paper, 2006

- [49] Stephen Jenkins “Snapshots versus movies: ‘Lifecycle biases’ and the estimation of intergenerational earnings inheritance” In European Economic Review 31.5 Elsevier, 1987, pp. 1149–1158

- [50] Harry Joe “Multivariate Models and Multivariate Dependence Concepts” CRC Press, 1997

- [51] Kengo Kato, Antonio F Galvao Jr and Gabriel V Montes-Rojas “Asymptotics for panel quantile regression models with individual effects” In Journal of Econometrics 170.1 Elsevier, 2012, pp. 76–91

- [52] Toru Kitagawa, Martin Nybom and Jan Stuhler “Measurement error and rank correlations” Working Paper, 2018

- [53] Andros Kourtellos, Christa Marr and Chih Ming Tan “Local intergenerational mobility” In European Economic Review 126 Elsevier, 2020, pp. 103460

- [54] Rasmus Landersø and James J Heckman “The Scandinavian fantasy: The sources of intergenerational mobility in Denmark and the U.S.” In The Scandinavian Journal of Economics 119.1 Wiley Online Library, 2017, pp. 178–230