Estimation of high-dimensional change-points under a group sparsity structure

Abstract

Change-points are a routine feature of ‘big data’ observed in the form of high-dimensional data streams. In many such data streams, the component series possess group structures and it is natural to assume that changes only occur in a small number of all groups. We propose a new change point procedure, called groupInspect, that exploits the group sparsity structure to estimate a projection direction so as to aggregate information across the component series to successfully estimate the change-point in the mean structure of the series. We prove that the estimated projection direction is minimax optimal, up to logarithmic factors, when all group sizes are of comparable order. Moreover, our theory provide strong guarantees on the rate of convergence of the change-point location estimator. Numerical studies demonstrates the competitive performance of groupInspect in a wide range of settings and a real data example confirms the practical usefulness of our procedure.

1 Introduction

Modern applications routinely generate time-ordered high-dimensional datasets, where many covariates are simultaneously measured over time. Examples include wearable technologies recording the health state of individuals from multi-sensor feedbacks (Hanlon and Anderson, 2009), internet traffic data collected by tens of thousands of routers (Peng, Leckie and Ramamohanarao, 2004) and functional Magnetic Resonance Imaging (fMRI) scans that record the time evolution of blood oxygen level dependent (BOLD) chemical contrast in different areas of the brain (Aston and Kirch, 2012). The explosion in number of such high-dimensional data streams calls for methodological advances for their analysis.

Change-point analysis is an essential statistical technique used in identifying abrupt changes in a time series. Time points at which such abrupt change occurs are called ‘change-points’. Through estimating the location of change-points, we can divide the time series into shorter segments that can be analysed using methods designed for stationary time series. Moreover, in many applications, the estimated change-points indicate specific events that are themselves of great interest. In the examples mentioned in the previous paragraph, they can be used to raise alarms about abnormal health events, detect distributed denial of service attacks on the network and pinpoint the onset of certain brain activities.

Classical change-point analysis focuses on univariate time series. The current state-of-art methods including Killick, Fearnhead and Eckley (2012); Frick, Munk and Sieling (2014); Fryzlewicz (2014). However, classical univariate change-point methods are often inadequate for high-dimensional datasets that are routinely encountered in modern applications. When applied componentwise, they are often sub-optimal as signals can spread over many components. As a result, several new methodologies have been proposed to test and estimate change-points in the high-dimensional settings. These include methods that apply a simple or aggregation of test statistics across different components (Horváth and Hušková, 2012; Jirak, 2015), and more complex methods such as a scan-statistics based approach by Enikeeva and Harchaoui (2019), the Sparsified Binary Segmentation algorithm by Cho and Fryzlewicz (2015), the double CUSUM algorithm of Cho (2016) and a projection-based approach by Wang and Samworth (2018).

To get around the issue of the curse of dimensionality, existing high-dimensional change-point methods often assume that the signal of change possesses some form of sparsity. For example, in the high-dimensional mean change setting studied in Jirak (2015); Cho and Fryzlewicz (2015); Wang and Samworth (2018); Enikeeva and Harchaoui (2019), it is assumed that the difference in mean before and after a change-point is nonzero only in a small subset of coordinates. While the sparsity assumption greatly reduces the complexity of the original high-dimensional problem, it often does not capture the the full extent of the structure in the vector of change available in real data applications. For instance, in many applications, the coordinates of the high-dimensional vectors are naturally clustered into groups and coordinates within the same group tend to change together. At each change-point, only a small number of groups will undergo a change. Such a group sparsity change-point structure is useful in modelling many practical applications. Examples include financial data stream where changes are often grouped by industry sectors and a small number of sectors may experience virtually simultaneous market shocks. Also, in functional magnetic resonance imaging data, voxels belonging to the same brain functional regions tend to change simultaneously over time. Similar group sparsity assumptions have been made in other statistical problems including Yuan and Lin (2006); Wang and Leng (2008); Simon et al. (2020).

In this work, we provide a new high-dimensional change-point methodology that exploits the group sparsity structure of the changes. More precisely, given pre-specified grouping information of all the coordinates, our algorithm, named groupInspect (standing for group-based informative sparse projection estimator of change-points), will first estimate a vector of projection that is closely aligned with the true vector of change at each change-point. It will then project the high-dimensional data series along this estimated direction and apply a univariate change-point method on the projected series to identify the location of the change. The above procedure can be combined with a wild binary-segmentation algorithm (Fryzlewicz, 2014) to recursively identify multiple change-points. We show that, in a single change-point setting, the projection direction estimator employed in groupInspect has a minimax optimal dependence, up to logarithmic factors, on both the sparsity parameter and the group-sparsity parameter, representing respectively the number of nonzero elements and the number of nonzero groups in the vector of change. Furthermore, groupInspect achieves a rate of convergence for the estimated location of a single change-point, where denotes the norm of the vector of change, which up to logarithmic factors is minimax optimal.

The outline of the paper is as follows. In Section 2, we describe the formal setup of our problem. The groupInspect methodology is then introduced in Section 3, with its theoretical performance guarantees provided in Section 4. We illustrate the empirical performance of groupInspect via simulatinos and a real-data example in Section 5. Proofs of all theoretical results are deferred to Section 6, and ancillary results and their proofs are given in Section 7.

1.1 Notation

For any positive integer , we write . For a vector , we define , and for any positive integer , and let . For a matrix , we write for its nuclear norm and write for its Frobenius norm.

For any , we write for the -dimensional vector obtained by extracting coordinates of in . For a matrix , and , we write for the submatrix obtained by extracting rows and columns of indexed by and respectively. When , we abbreviate by . When is a single element set, we slightly abuse notation and write instead of .

Given two sequences and such that for all , we write (or equivalently ) if for some universal constant .

2 Problem description

Let be independent random vectors with distribution:

| (1) |

which we can combine into a single data matrix . We assume that the sequence of mean vectors undergoes changes at times for , in the sense that

| (2) |

where we use the convention that and . We assume that consecutive change-points are sufficiently separated in the sense that

Suppose further that each of the coordinates belong to (at least) one of groups. Specifically, let denotes the set of indices associated with the th group for , we have that

| (3) |

We assume that coordinates in the same group will tend to change together. We will consider both the case of overlapping and non-overlapping groups. In the latter scenario, each coordinate belongs to a unique group and forms a partition of .

Our goal is to estimate the locations of change from the data matrix and the pre-specified grouping information . Motivated by Wang and Samworth (2018), the best way to aggregate the component series so as to maximise the signal-to-noise ratio around the th change-point is to project the data along a direction close to the vector of change . Let be the unit vector parallel to :

which we will call the oracle direction for the th change-point. We measure the quality of any estimated projection direction with the Davis–Kahan sin loss (Davis and Kahan, 1970)

and measure the quality of the subsequent location estimator by .

The difficulty of the estimation task depends on both the noise level and the vector of change . More precisely, we assume that the change is localised in a small number of the groups as defined in (3). Define such that , we assume that

| (4) |

3 Methodology

3.1 Single change-point estimation

Initially, we will consider estimation of a single change-point, where . This can be extended to estimate multiple change-points in conjunction with top-down approaches such as wild binary segmentation, which we will discuss in Section 3.2.

We define the CUSUM transformation by

| (5) |

and compute the CUSUM matrix . As discussed in Section 2, our general strategy is to use the matrix to estimate a projection direction that is well-aligned with the direction of change, and then project the data along this direction to estimate the change-point location from the univariated projected series. More precisely, we would like to solve for

| (6) |

where, . However, the above optimisation problem is non-convex due to the group-sparsity constraint. Consequently, we perform the following convex relaxation of the above problem. We first note that the set of optimisers of (6) is equal to the set of leading left singular vectors of

We relax the above matrix-variate optimisation problem by dropping the combinatorial rank constraint, and replacing the nuclear norm constraint set by the larger Frobenius norm set of . The constraint that has at most groups of non-zero rows can be written as an constraint on the vector of Frobenius norms of such submatrices, i.e. . Motivated by the group lasso penalty (Yuan and Lin, 2006), we replace this group sparsity constraint with a group norm penalty, where the group norm for a matrix is defined as

where is the sum of column norms of the submatrix and . Overall, we obtain the following optimisation problem:

| (7) |

where is a regularization parameter.

If the groups are non-overlapping, in the sense that for all , then we see from Proposition 5 that (7) has a closed form solution

| (8) |

where .

For overlapping groups, (7) can be optimised using Frank–Wolfe algorithm (Frank and Wolfe, 1956), as described in Algorithm 1. We first compute the gradient of the objective function which is the step 4 in Algorithm 1. We then project the back onto .

After solving the optimization problem, we can obtain the estimated projection direction by computing the leading left singular vector of . Then, we project the data along to obtain a univariate series for which existing one-dimensional change-point estimation methods apply. Specifically, we perform the CUSUM transformation over the projected data series, and locate the change-point by the maximum absolute value of the CUSUM vector. The full procedure is described in Algorithm 2.

3.2 Multiple change-point estimation

When the data matrix possess multiple change-points, we may combine Algorithm 2 with a top-down approach, such as the wild binary segmentation (Fryzlewicz, 2014), to recursively identify all the change-points. Specifically, we start by drawing a large number of random intervals and apply Algorithm 2 to the data matrix restricted to each of these time intervals to obtain candidate change-point locations. We then aggregate candidate change-point locations to choose the one with the maximum projected CUSUM statistics. If the value of the CUSUM statistic at the best candidate location is above a threshold , we will admit this candidate location as a change-point and repeat the above process on the data submatrix to the left and right of this change-point. The pseudocode for the full procedure is given in Algorithm 3.

4 Theoretical guarantees

In this section, we provide theoretical guarantees to the performance of the groupInspect algorithm. As we have noted in Section 2, a key to the successful change-point estimation in the current problem is a good estimator of the oracle projection direction .

The following theorem controls the sine angle risk of the estimated projection direction in Step 3 of Algorithm 2. We define to be the set of data distributions satisfying (1), (2), (3) and (4). For any , we write where is the difference between post-change and pre-change means.

Theorem 1.

For a given grouping , let and suppose further that there exists a universal constant , such that . Let be a data matrix, let be the vector of change and let be as in Step 3 of Algorithm 2 with input , and . Then there exists , depending only on , such that

| (9) |

We remark that the condition is to control the extent of overlapping between different groups. Specifically, it requires that each coordinate can belong to at most groups. In the special case when all groups are disjoint, which is often true in practical applications, then it suffices to take .

We note that, when , with high probability, the sine angle loss in (9) has an upper bound that is proportional to , similar to what has been previously observed in Wang and Samworth (2018, Proposition 1). However, Theorem 1 reveals an interesting interaction between the sparsity and the group sparsity when all groups are of comparable size. Specifically, for and assuming that , then we can simplify (9) to obtain that

In other words, the risk upper bound undergoes a phase transition as the number of coordinates per group increases above a level. Similar phase transitions have been previously observed in the context of high-dimensional linear model where the regression coefficients satisfy a group sparsity assumption (see, e.g. Cai et al., 2019, Theorem 3).

We now turn our attention to a minimax lower bound of the estimation risk of the oracle projection direction. Theorem 2 below shows that the phase transition observed in Theorem 1 is not due to the specific proof techniques employed but rather an intrinsic feature of the problem.

Theorem 2.

Suppose , and a grouping satisfy that for all , , and , where are order statistics of . Then for some universal constant , we have

where the infimum is taken over the set of all measurable functions of the data .

The condition that is to ensure that the upper bound on the -sparsity is not too loose in the sense that is not too much larger than the cardinality of the union of the largest groups. If we assume that , and , then the lower bound in Theorem 2 matches the upper bound of Theorem 1 up to universal constants, when all groups are non-overlapping.

After obtaining guarantees on the quality of the projection direction estimator, we now provide theoretical guarantees of the overall change-point procedure. We note that the projection direction estimator is dependent on the CUSUM panel . While this dependence is observed to be very weak in practice, it creates difficulties in analysing the projected CUSUM series in Step 4 of Algorithm 2. As such, for theoretical convenience, we will instead analyse a sample-splitting version of the algorithm. Specifically, we split the data into and , consisting of odd and even time points respectively, as described in Algorithm 4. We use to estimate the projected direction and then project along this direction to locate the change-point. Theorem 3 below provides a performance guarantee for the estimated location of the change-point of this sample-splitting version of our procedure.

Theorem 3.

Given data matrix , let be the output from the Algorithm 4 with input and . There exist universal constants , such that, if is even, is even, and

then,

5 Numerical studies

In this section, we provide some simulation results to demonstrate the empirical performance of the groupInspect method. In all our numerical studies, unless otherwise specified, we will assume that data are generated according to (1), (2), (3) and (4), with . In all simulations, we do not assume that is known, or even equal across rows. Instead, we estimate the variance in each row using the mean absolute deviation of successive differences of the observations. We then standardise the data by the estimated row standard deviation. The groupInspect procedure is then applied to the standardised data with .

5.1 Theory validation

We first show that the practical performance of the groupInspect procedure is well captured by the theoretical results in Theorems 1 and 2. There are two related measures of the signal sparsity in our problem, which are the total number of coordinates of change and the total number of groups with a change . We conduct two sets of simulation experiments fixing one of these sparsity measures and varying the other. Specifically, for , and , we split the coordinates into disjoint groups of coordinates per group, where is allowed to vary over all divisors of . In the first set of experiments, we fix so that varies with , whereas in the second set of experiments, we fix so that varies with . The vector of change is constructed so that the magnitude of change is equal across all coordinates of change. We will use the theoretical choice of tuning parameter for both sets of experiments here. Figure 1 shows how the loss, averaged over Monte Carlo repetitions, varies with , for different choices of and in both settings.

In the left panel of Figure 1, where the number of signal coordinates is fixed, we see that the average loss decreases as increases. Furthermore, at a log-log scale, and for relatively large signal sizes of , we see the loss curves follow an initial linear decreasing trend as increases before plateauing eventually. This is in agreement with the two terms contributing to the loss described in Theorem 1. Specifically, for small , we expect the second term of (9) to dominate and the loss decreases at a rate approximately proportional to initially. For large , we expect the first term of (9) to dominate and the loss will have minimal dependence on . In the right panel of Figure 1, where the number of signal groups is fixed, the average loss increases with , as expected from our theory. It appears that for studied here, the first term of (9) is dominant and the average loss increases linearly at the log-log scale with respect to .

We further remark that in both panels of Figure 1, the average loss for large shows equally spaced separation for the signal size in the dyadic grid . This is in good agreement with the dependence of expected loss given in Theorem 1. Finally, we note that the ambient dimension has minimal effect on the loss curves, for all signal strengths studied here. Again, this is predicted by our theory as the dimension enters the mean loss in (9) only through the expression in the second term.

5.2 Practical choice of tuning parameter

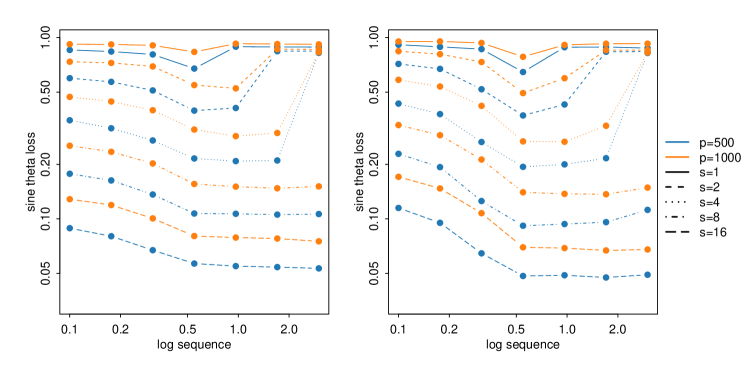

The theoretical choice of turns out to be conservative in practical use. In this subsection, we will perform numerical simulations to suggest a suitable practical tuning parameter choice. We fix , , , . The signal size is varied in and is chosen from . All groups are set to have equal size. For the choice of tuning parameters, we first form a logarithmic sequence of values between and with length and then times each value with the theoretically suggested value of to form the sequence of the tuning parameter. For each setting of the signal size, we will run algorithm with all the values and record the sine angle loss.

We plot loss against in Figure 2. The -axis is the log sequence. In most cases, the loss is minimized when tuning parameter value is half of the theoretical value. However, when the minimum loss is achieved by other values of , this lambda value can still achieve the loss which is close to optimal value. Therefore, we suggest that using in practical is less conservative.

5.3 Comparison between different methods

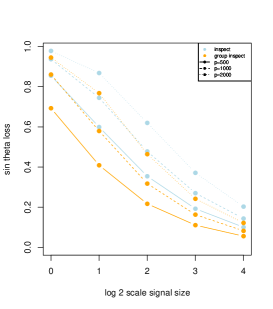

Now, we would like to compare our method with other existing change-point estimation procedures. As groupInspect is a two-stage procedure that first estimates a projection direction before localising the change-point on the projected series, we will investigate its performance both in terms of its accuracy in estimating the projection direction and the quality of the final change-point location estimator. For the former, we compare the estimated projection direction from groupInspect with that from the inspect algorithm. We measure the accuracy in terms of the sine angle loss introduced in Section 2. We use the recommended values for tuning parameters in both methods, i.e., in inspect as in Wang and Samworth (2018) and for groupInspect as suggested in Section 5.2.

We fix , and vary in . We consider settings with both non-overlapping groups and overlapping groups. For the non-overlapping setting, we have groups of equal size , whereas for the overlapping setting, we have groups of size each, where neighbouring groups overlap in exactly coordinates. Both methods have access to exactly the same data sets and the performance is averaged over 100 Monte Carlo repetitions.

Figure 3 shows the comparison of the average sine angle loss between groupInspect and inspect over all signal sizes on a logarithmic scale, in both the non-overlapping and overlapping settings. In both cases, groupInspect outperforms the inspect algorithm. From the left panel, we can see that the estimation accuracy of the projection direction using groupInspect is substantially better even when the signal is small.

We now turn our attention to the overall change-point localisation accuracy of the groupInspect procedure. To this end, we compare the mean absolute deviation of various high-dimensional change-point procedures over 100 Monte Carlo repetitions using the same data sets. In addition to inspect, we also compare against the aggregation procedures of Horváth and Hušková (2012), the aggregation procedure of Jirak (2015) and the double CUSUM procedure of Cho (2016). We set , , . The simulation results are presented in Table 1. For simplicity, we have only shown the results for 10 equal-sized non-overlapping groups here, but qualitatively similar results were obtained in other settings as well. We see that groupInspect is very competitive over a wide range of dimensions and signal-to-noise ratio settings, though the benefit of using the group sparsity structure via groupInspect is most apparent in low signal-to-noise ratio settings where the change-point estimation problem is more difficult.

|

|

| groupInspect | inspect | -aggregate | -aggregate | double cusum | ||

|---|---|---|---|---|---|---|

5.4 Multiple change-points simulation

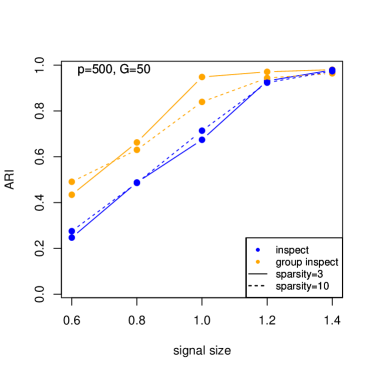

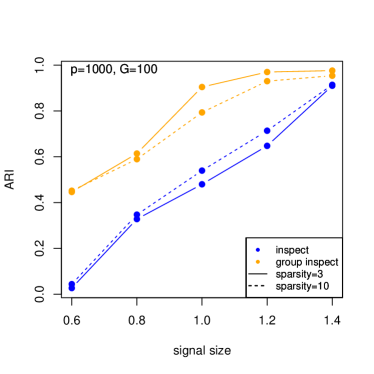

The numerical studies so far have focused mainly on the single change-point estimation problem. In this subsection, we investigate the empirical performance of groupInspect in multiple change-point estimation tasks. We will compare its performance as implemented in Algorithm 3 to that of the inspect algorithms for estimating multiple change-points under different settings. We choose , , , . Each data series contains three true change-points located at , and with the norm of the change equal to , and respectively. We vary in . For simplicity, we further assume that the same coordinates undergo change in all three change-points and that all groups have 10 elements. We use the tuning parameter choice suggested in Section 5.2 for the groupInspect method and that suggested in Wang and Samworth (2018) for the inspect algorithm. For the thresholding parameter of the wild binary segmentation recursion used in both groupInspect and inspect, we choose via Monte Carlo simulation. More precisely, we randomly generate 1000 data sets from the null model with no change-points and take the maximum absolute CUSUM statistics from Algorithm 3 and Wang and Samworth (2018, Algorithm 4) as and respectively. We compare the performance of two algorithms using the Adjusted Rand index (ARI) of the estimated segmentation against the truth (Rand, 1971; Hubert and Arabie, 1985).

From Figure 4, we see that the groupInspect algorithm generally performs much better than the inspect algorithm in the multiple change-point localisation tasks. The advantage of groupInspect is more pronounced when the signal is sparser and when the dimension of the data is higher.

|

|

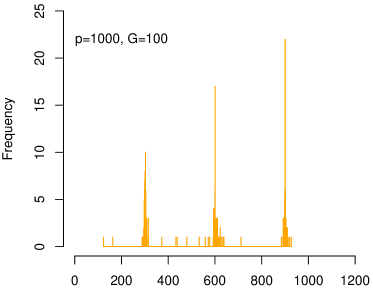

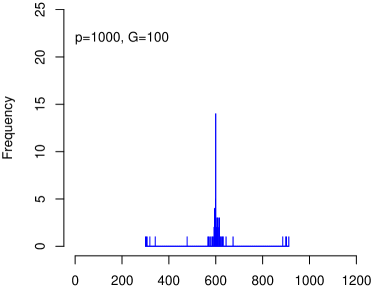

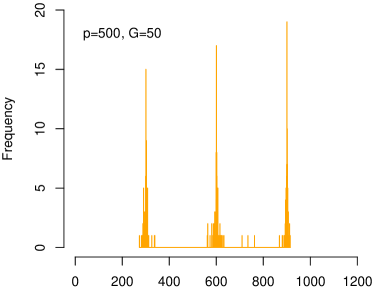

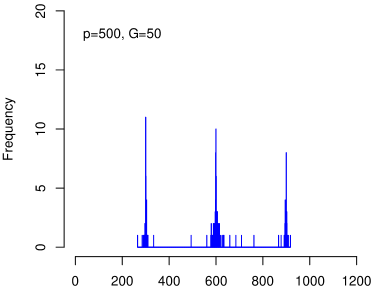

To further visualise the output of the two procedures, we plot the estimated change-point locations for one specific setting ( and ) of each of the two panels in Figure 4. The resulting histograms in Figure 5 shows that when , groupInspect was better at picking out all three change-points with higher accuracies. When , inspect was only able to pick out the change at in most of the trials, whereas groupInspect was still able to identify even the weakest change signal at in a substantial fraction of all trials.

|

|

|

|

5.5 Real data analysis

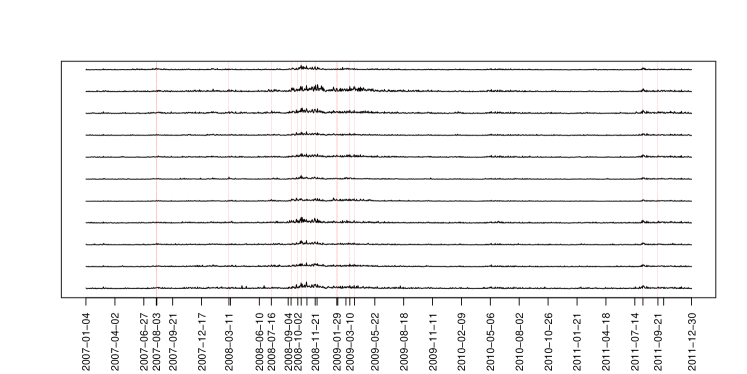

In this section, we apply groupInspect to a stock price data. The data consists of the logarithmic daily returns (computed from the adjusted closing prices) of S&P 500 stocks during the period 1 January 2007 to 31 December 2011. Since not all companies remained in the S&P 500 list and some companies have missing data at a few time points, we eventually selected 256 companies which have continuously traded throughout this this period to construct a multivariate time series of dimension and length . We then divide the companies into non-overlapping groups according to respective Global Industry Classification Standard sector memberships. We then rescale rows of the data matrix by their estimated standard deviation as in Section 5. We use the same procedure in Section 5.4 to choose thresholding parameter .

The groupInspect algorithm identifies the following change points , , , , , , , , , , , , , , , as illustrated in Figure 6. We see a large number of changes being identified in the period between September and October 2008, which corresponds to the period when the financial crisis reaches a climax, and when the stock market is most volatile.

6 Proofs of main results

In this section, we will give the proof of our results in section 4.

6.1 Proof of Theorem 1

6.2 Proof of Theorem 2

Proof.

We will use two different constructions to derive separate lower bounds of order and respectively. Without loss of generality, we may assume that .

For the first bound, let , , then in . By the Gilbert–Varshamov lemma as stated in Massart (2007, Lemma 4.10) (applied with and ), we can construct a set of -sparse vectors in , with cardinality at least , such that the pairwise Hamming distance between any pair of vectors in is at least . Let to be chosen later, we can define a set

We remark that for any pair of distinct , we have by construction that . We then define a map such that for any and , we have . Finally, let . We note that . Therefore, for distinct , we have

| (10) |

Now, for each , we can define a distribution , such that the pre-change mean is and the post-change mean is (we check that indeed satisfies the conditions of ). Then for any distinct , we have

| (11) |

By (10) and (11), we can apply Fano’s lemma (Yu, 1997, Lemma 3) to obtain that

By the condition in the theorem, we have . Moreover, the choice of

ensures that . Therefore,

| (12) |

For the second lower bound, let be the indices of the groups with largest cardinalities. By the given condition of the Theorem, we have that . Let , so . By Massart (2007, Lemma 4.7), we can construct a subset of of cardinality at least , such that any two points in the set are separated in Hamming distance by at least . Construct

Therefore, for distinct , we have ,then,

Following the same derivation as in (11), we have that

Again, we can use Fano’s lemma (Yu, 1997, Lemma 3) to obtain that

Now, choose . Since , we have , so that

| (13) |

The desired result follows by combining (12) with (6.2), and noting that . ∎

6.3 Proof of Theorem 3

Proof.

Recall the definition of and let . Define similarly and a random taking values in by and . Now, let and . We also write ,,,, and for the one-dimensional projected images. Note that by linearity, we have , and ,

Now, conditional on , the random variables are independent with

and the row vector undergoes a single change at with magnitude of change

Finally, let , so the first component of the output of the algorithm is . Consider the set

By Condition (3) and Theorem 1, we have that

| (14) |

Moreover, on the event , we have that . Set , we have by Proposition 9 that

| (15) |

Since and and are respectively maximized at and , we have on the event that

Hence, by Wang and Samworth (2018, Lemma 7 in the online supplement), on the event , we have that

Now we define the event

By Wang and Samworth (2018, Lemma 5), we have that

| (16) |

Following the proof of Theorem 1 of Wang and Samworth (2018), we have on that

From (3) for , we have on that

Finally, by (14), (15) and (16) we have that

as desired. ∎

7 Ancillary results

We collect in this section all ancillary propositions and lemmas used in the paper. For all results in this section, we assume that we are given a grouping of and the associated group norm . It is useful to define the following counterpart to the group norm. For any and a grouping of , we define

| (17) |

Lemma 4.

The norm is a dual to with respect to the inner product on .

Proof.

To prove the lemma, it suffices to show that for all . First, for any , let be the th column of . Define such that

Then, . Hence,

On the other hand, for any such that , we have for all and . Consequently, by the Cauchy–Schwarz inequality,

thus establishing the result. ∎

Proposition 5.

Let . For , , we have

where satisfies .

Proof.

Define functions and such that for , and and . By (17) and Lemma 4, we have that

By the minimax equality theorem (Fan, 1953, Theorem 1), we obtain that

Observe that . To find the optimiser , we consider the groups individually. For each group , and in the th column, if , then ; and if , then . Since the minimizer of is unique, we have that

as desired. ∎

Lemma 6.

For any , we have .

Proof.

By Cauchy–Schwarz inequality, we have that

as desired. ∎

Lemma 7.

Let and suppose further that there exists a universal constant , such that . Then, for any , we have .

Proof.

Define with . Then by applying the Cauchy–Schwarz inequality twice, we have

as desired. ∎

Proposition 8.

Let and suppose further that there exists a universal constant , such that . Let be a rank one matrix with for , and . Suppose satisfies for some , and let . Then, for any

we have

and

Proof.

Define . Since , from the basic inequality, we have

| (18) |

When , or equivalently, for all and , we have by Wang and Samworth (2018, Lemma 2) and (18) that

where we used Lemma 6 in the penultimate inequality and Lemma 7 in the final bound. This proves the first claim of the proposition, and the second claim follows from the first by the same argument as used in Wang and Samworth (2018, online supplement (18) and (19)). ∎

Proposition 9.

Let be an random matrix with independent entries and set . Let with . For any and , we have that

References

- Aston and Kirch (2012) Aston, J. A. D. and Kirch, C. (2012) Evaluating stationarity via change-point alternatives with applications to fMRI data. Ann. Appl. Stat., 6, 1906–1948.

- Cai et al. (2019) Cai, T. T., Zhang, A. and Zhou, Y. (2019) Sparse group lasso: Optimal sample complexity, convergence rate, and statistical inference. arXiv preprint, arxiv:1909.09851.

- Cho (2016) Cho, H. (2016) Change-point detection in panel data via double CUSUM statistic. Electron. J. Stat., 10, 2000-2038.

- Cho and Fryzlewicz (2015) Cho, H. and Fryzlewicz, P. (2015) Multiple-change-point detection for high dimensional time series via sparsified binary segmentation. J. R. Stat. Soc. Ser. B, 77, 475–507.

- Davis and Kahan (1970) Davis, C. and Kahan, W. M. (1970) The rotation of eigenvectors by a perturbation. III. SIAM J. Numer. Anal., 7, 1–46.

- Enikeeva and Harchaoui (2019) Enikeeva, F. and Harchaoui, Z. (2019) High-dimensional change-point detection under sparse alternatives. Ann. Statist., 47, 2051–2079.

- Fan (1953) Fan, K. (1953) Minimax theorems. Proc. Natl. Acad. Sci. USA, 39, 42–47.

- Frank and Wolfe (1956) Frank, M. and Wolfe, P. (1956) An algorithm for quadratic programming. Naval Res. Logist., 3, 95–-110.

- Frick, Munk and Sieling (2014) Frick, K., Munk, A. and Sieling, H. (2014) Multiscale change-point inference. J. Roy. Statist. Soc., Ser. B, 76, 495–580.

- Fryzlewicz (2014) Fryzlewicz, P. (2014) Wild binary segmentation for multiple change-point detection. Ann. Statist., 42, 2243–2281.

- Hanlon and Anderson (2009) Hanlon, M. and Anderson, R. (2009) Real-time gait event detection using wearable sensors. Gait & Posture, 30, 523–527.

- Horváth and Hušková (2012) Horváth, L. and Hušková, M. (2012) Change-point detection in panel data. J. Time Ser. Anal., 33, 631–648.

- Hubert and Arabie (1985) Hubert, L. and Arabie, P. (1985) Comparing partitions. J. Classification, 2, 193–-218.

- Jirak (2015) Jirak, M. (2015) Uniform change-point tests in high dimension. Ann. Statist., 43, 2451–2483.

- Killick, Fearnhead and Eckley (2012) Killick, R., Fearnhead, P. and Eckley, I. A. (2012) Optimal detection of change-points with a linear computational cost. J. Amer. Stat. Assoc., 107, 1590–1598.

- Laurent and Massart (2000) Laurent, B. and Massart, P. (2000) Adaptive estimation of a quadratic functional by model selection. Ann. Statist., 28, 1302–1338.

- Massart (2007) Massart, P. (2007) Concentration Inequalities and Model Selection, Springer, Berlin.

- Peng, Leckie and Ramamohanarao (2004) Peng, T., Leckie, C. and Ramamohanarao, K. (2004) Proactively detecting distributed denial ofservice attacks using source IP address monitoring. In Mitrou, N., Kontovasilis, K., Rouskas, G. N., Iliadis, I. and Merakos, L. eds, Networking 2004, pp. 771–782. Springer-Verlag, Berlin.

- Rand (1971) Rand, W. M. (1971) Objective criteria for the evaluation of clustering methods. J. Amer. Statist. Assoc., 66, 846–-850.

- Simon et al. (2020) Simon, N, Friedman, J, Hastie, T and Tibshirani, R (2013) A sparse-group lasso. J. Comput. Graph. Statist., 22, 231–245.

- Vershynin (2012) Vershynin, R. (2012) Introduction to the non-asymptotic analysis of random matrices. In Y. Eldar and G. Kutyniok (Eds.) Compressed Sensing, Theory and Applications. Cambridge University Press, Cambridge. 210–268.

- Wang and Leng (2008) Wang, H and Leng, C (2008) A note on adaptive group lasso. Comput. Statist. Data Anal. 52(12), 5277–5286.

- Wang and Samworth (2018) Wang, T and Samworth, R. J. (2018) High dimensional change-point estimation via sparse projection. J. Roy. Statist. Soc., Ser. B, 80, 57–83.

- Yu (1997) Yu, B. (1997) Assouad, Fano and Le Cam. In Pollard, D., Torgersen, E. and Yang G. L. (Eds.) Festschrift for Lucien Le Cam: Research Papers in Probability and Statistics, 423–435. Springer, New York.

- Yuan and Lin (2006) Yuan, M. and Lin, Y. (2006) Model selection and estimation in regression with grouped variables. J. Roy. Statist. Soc., Ser. B, 68, 49–67.