On the discrete-time simulation of the rough Heston model

Abstract

We study Euler-type discrete-time schemes for the rough Heston model, which can be described by a stochastic Volterra equation (with non-Lipschtiz coefficient functions), or by an equivalent integrated variance formulation. Using weak convergence techniques, we prove that the limits of the discrete-time schemes are solution to some modified Volterra equations. Such modified equations are then proved to share the same unique solution as the initial equations, which implies the convergence of the discrete-time schemes. Numerical examples are also provided in order to evaluate different options’ prices under the rough Heston model.

Key words: Rough Heston model, stochastic Volterra equations, Euler scheme, Monte-Carlo method.

MSC2020 subject classification: 60H20, 45D05, 91G60.

1 Introduction

The modelling of rough volatilities is an important subject in mathematical finance, especially since the paper [22] which brought statistical evidence of such behaviour in the financial markets (see also the pioneering works [14, 10, 21, 15] in this direction). Rough volatility models have the advantage to better exhibit the roughness of the volatility time series, to reproduce the shape and the dynamic of the implied volatility surface, etc. Many of the rough volatility models consist in replacing the Brownian motions in the classical models by fractional Brownian motions, which leads to some SDEs or more general stochastic system driven by fractional Brownian motions, see e.g. [14, 15, 12, 6, 22, 11] among many others. Another important way to model the rough volatility process is to use a stochastic Volterra equation, such as the rough Heston model introduced by El Euch and Rosenbaum [17]:

| (1) |

where are two correlated Brownian motions with some correlation constant , and is the kernel function with some Hurst parameter . Above, is the risky asset price process under the risk neutral probability, and represents the volatility process. Further, by considering the integrated processes:

the rough Heston model (1) is shown to be equivalent (see e.g. Abi Jaber [1]) to the following system

| (2) |

where are two continuous martingales with quadratic variation and quadratic covariation . Based on the above formulations in (1) and (2), the super-rough Heston model [16] and the hyper-rough Heston model [1, 30] have also been developed recently.

In the rough volatility literature, an important topic is to find a good approximation method (e.g. in order to evaluate option prices), whenever a closed formula is not available. For different models, some approximation and asymptotic methods have been introduced and studied, see e.g. [10, 21, 18, 26, 25, 3, 20, 27, 19], etc. In the meantime, for affine models such as (1) and (2), one can in fact obtain the marginal distributions of or at any time , by computing their characteristic function via Riccati-type systems, see e.g. [9, 1, 4, 17]. This allows in particular to compute efficiently the European call/put options prices under the affine rough volatility models. Nevertheless, as the path distribution of the process or is still unknown, one cannot compute prices of path-dependent options this way. In this case, a natural and simple solution would be the Monte-Carlo method based on a discrete-time scheme.

The main objective of the paper is to study the Euler-type discrete-time scheme for the rough Heston model in both formulations (1) and (2), and to provide a convergence result. We will stay in a more general rough Heston setting, i.e. the kernel function is not necessarily of the form . Throughout the paper, we would like to call (1) the rough Heston model in the stochastic Volterra equation formulation, and (2) the rough Heston model in the integrated variance formulation (or simply integrated-rough Heston model).

Notice that Equation (1) satisfied by is a standard stochastic Volterra equation (but with non-Lipschitz coefficient). For stochastic Volterra equations with Lipschitz coefficient equations, the discrete-time schemes such as Euler scheme and/or Milstein scheme have been studied in [36, 35, 8, 33], where (sharp) strong convergence rates have been obtained. Nevertheless, because of the square root term , the coefficient function in (1) is non-Lipschitz. Hence the techniques and results in the aforementioned papers cannot be applied to obtain a convergence result.

We will apply weak convergence techniques to provide a convergence proof of the discrete-time scheme for both Equations (1) and (2). The idea is very classical in the literature on SDEs, see e.g. [31, 28]. First, one shows that the sequence of discrete time numerical solutions is tight, then that any limit of the sequence is solution to the continuous-time equation. Next, it is enough to show that the limit continuous-time equation has a unique weak solution, so that the numerical solution converges weakly to the unique solution of the limit equation. In the context of the rough Heston model, such weak convergence techniques have already been used in [1, 5, 4], in particular to show the existence of weak solutions of the related equations.

However, for the analysis of the discrete-time numerical solution, it is not straightforward to apply their techniques and results. First, they usually consider sequences of continuous-time processes and which are solutions of equations with smoother coefficients, where generalized Grönwall lemma applies under conditions on the kernel . For the discrete-time numerical solution, because of discretization of the kernel function , it is not trivial to formulate explicit conditions on to have the discrete-time generalized Grönwall lemma. We therefore need to develop different techniques to estimate the (uniform) moment estimates to obtain the tightness of discrete-time solutions. Next, their approximating processes are already positive (resp. non-decreasing), so that the limit process (resp. ) is automatically positive (resp. non-decreasing). In the discrete-time setting, the numerical solution may not always be positive, we hence need to take its positive part before taking the square root, i.e. . As for the numerical solution , we need to replace by to make it non-decreasing, so that it can be the quadratic variation of some martingales. Consequently, it turns out that the limit of the numerical solutions is solution to some modified equations. We will then need to show that the limit process is positive and is non-decreasing, and the modified equation shares the same unique weak solution as the initial equations. For this, we will adapt the ideas from [2] to our context. This allows us to obtain weak convergence results of the discrete-time numerical solutions. Finally, we also provide some numerical simulation examples to evaluate (path-dependent) options’ prices in the rough Heston model.

The rest of the paper is organised as follows. In Section 2, we state the two equivalent formulations of the rough Heston model with more details, and present the corresponding discrete-time schemes as well as the convergence results. In Section 3, we provide some numerical examples in order to evaluate the option prices in the rough Heston model. Proofs of the main (weak) convergence results in Theorems 2.2 and 2.3 are provided in Section 4.

2 Discrete-time simulation of the rough Heston model

We will first restate the two equivalent formulations (1) and (2) of the rough Heston model with more precise definitions. Based on the two formulations, we introduce the corresponding Euler-type schemes, which are defined on a discrete grid. Let us consider a sequence of discrete-time grid on , with for each . For each , we define for , , and .

To provide the convergence results, we will make some assumptions on the kernel function used in the model. For a (measurable) kernel function , let us recall that the resolvent of the first kind of is a finite measure on such that

| (3) |

Notice that we are in a one-dimensional context, so that the above definition is much simpler than the general one (see [24]).

Assumption 2.1.

The function is nonnegative, not identically , non-increasing and continuous. Its resolvent of the first kind is nonnegative and such that is non-increasing for all . Moreover, there exist constants and such that, for all , and , , one has

| (4) |

and

| (5) |

Remark 2.1.

Let with Hurst constant and some constant . Then (4) and (5) can be checked by direct computation, while the resolvent of is for some , and thus satisfies Assumption 2.1.

Let , where and for some constants , and . One can check by direct computation that satisfies (4) and (5). Moreover, the resolvent of is explicitely given in [4, Table 1] and satisfies Assumption 2.1.

More generally, if is a completely monotone function (as defined in [24, Section 5.2]) and is not identically , then by [24, Theorem 5.5.4] it admits a resolvent of the first kind which is nonnegative and is such that is non-increasing for all . So if also verifies (4) and (5), it will satisfy Assumption 2.1. This is for instance the case of and above, as well as for instance . In addition, any linear combination and multiplication of completely monotone function is still a completely monotone function. Hence Assumption 2.1 covers a wide range of kernels.

2.1 The rough Heston model in two equivalent formulations

Let be a constant, , , , and be all strictly positive constants. The first formulation of the rough Heston model is given by

| (6) |

where are two independent Brownian motions. Namely, represents the risky asset price under the risk-neutral probability, is the volatility at time . We give immediately a precise definition of weak solution to (6).

Definition 2.2.

Remark 2.3.

The process is called the volatility process. Let us consider the integrated variance process given by

As observed in [1], one can reformulate (6) into an equivalent system on . Namely, by applying the stochastic Fubini theorem (see e.g. [34, p.175]), the processes satisfy the following stochastic Volterra equation

| (7) | ||||

where are two orthogonal continuous martingales with quadratic variation , and initial condition . We will call it the integrated variance formulation (or simply integrated-rough Heston model). Following [1], let us introduce the definition of weak solution of Equation (7).

Definition 2.4.

Remark 2.5.

Remark 2.6.

Let us define , then it is clear that one has

and

2.2 The discrete-time schemes and their convergence

Recall that is a sequence of discrete-time grids on , with for each . Let us denote , with and , for , . We will simulate of (6) and of (7) on the discrete-time grid . More precisely, in view of Remark 2.6, we would like to simulate the process in place of in (6), and to simulate in place of in (7). As observed in the Black-Scholes model, the simulation of permits to avoid the time discretization of the process in the dynamics of , and one can expect a better performance for its simulation.

Let us first give the Euler-type scheme for (6). Notice that the process is -valued in the continuous-time setting, but it could become negative in a discrete-time simulation. For this reason, we use in the square root term to define the discrete-time scheme. For the discrete grid , let us write as for simplicity, and denote by the corresponding numerical solution, which is given as follows: , , and

| (8) |

For the process defined on the discrete-time grid , one can use linear interpolation to obtain a continuous time process (with continuous paths), which is still denoted by . We can provide a weak convergence result of the numerical solution.

Theorem 2.2.

For all , there exists a constant such that

We now consider the discrete-time simulation problem of Equation (7). Notice that the process in the continuous-time setting is a non-decreasing process, which is the quadratic variation process of the martingales and . In discrete-time simulation, would not be non-decreasing, and for this reason, we will consider its running maximum to define the quadratic variation process. For each discrete time grid , let us define as follows: , , and

| (9) |

where , and is a sequence of i.i.d. random variables with standard Gaussian distribution .

Similarly, one can interpolate the process from the discrete-time grid to obtain a continuous time process (with continuous paths) .

Theorem 2.3.

For each , there exists a constant such that

Remark 2.7.

By the weak convergence of to , one has the convergence for any bounded continuous payoff function on . Moreover, since for any , it follows that converges to under the -Wasserstein distance, for any . Consequently, one has the convergence for any continuous function with polynomial growth.

Unfortunately, we do not have a uniform moment estimation on for all . For the process in (6), the moment explosion of has been studied in [23]. This is possible since one can find a Volterra type equation to compute the characteristic function of the marginal distribution of . It is nevertheless not clear how to elaborate the same technique on the discrete time Euler scheme solution . We would like to leave this for future research.

Our technique does not allow us to obtain a strong convergence rate. At the same time, as the processes and are not semimartingales, it is not clear how to adapt the error analysis techniques for classical Heston models, such as in [13, 7], to this rough Heston model context. Moreover, for Equations (1) and (2), because of the singular kernels and square-root-type coefficients, the strong existence and uniqueness of the solution is still an open question. It is therefore not surprising that a strong convergence rate is left as an open question.

3 Numerical examples

In this section, we provide some numerical examples to evaluate option prices in the rough Heston model with interest rate , by using the Monte-Carlo method based on the schemes (8) and (9). Namely, for an option with payoff function , one aims to estimate its price given by

We use the uniform discrete-time grid with , for Schemes (8) and (9). We use i.i.d. copies of simulations or to estimate the option price by the mean value :

Notice that from the simulations , one can use to compute . We also compute the empirical standard deviation of the simulations, which (divided by ) can serve as the statistical error, i.e.

We then use the following interval as confidence interval of the estimation:

For the rough Heston model, we choose the following parameters: , , , , , , and the kernel function with . We will use different discretization parameters in our simulations. For each example, we set the number of i.i.d. copies , and display the mean value, the statistical error as well as the computational time in the tables.

Notice also that in (9), one can compute explicitly instead of approximating it by . This will be taken into account in our simulation.

3.1 Pricing options on the risky asset

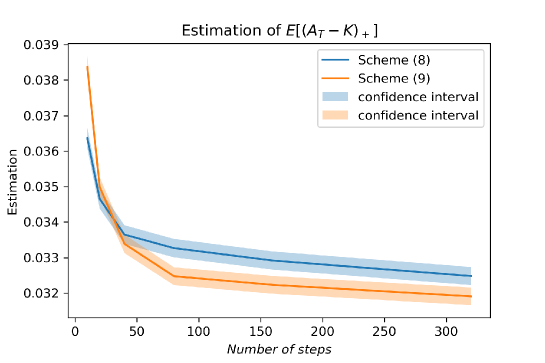

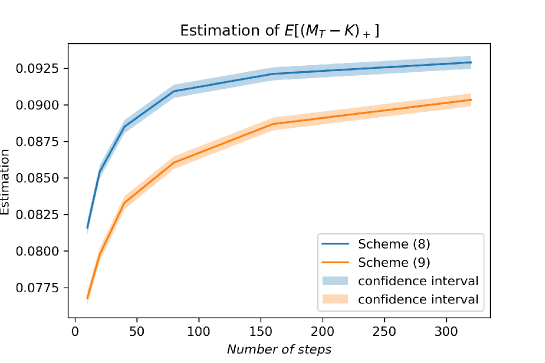

Let us first consider the European Call options, Asian options and Lookback options with the following payoff:

where , and . For the Monte-Carlo method, we simply replace by in the payoff function to compute the estimations, where , .

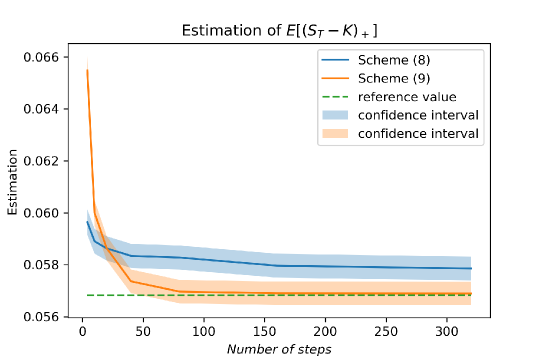

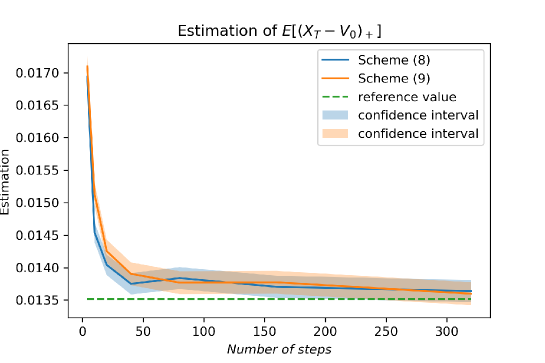

For the European call option, one can compute a reference value for . Indeed, as described in [17], one can compute the characteristic function of by solving a fractional Riccati equation, and then use the inverse Fourier transform method to compute . With the above parameters of the rough Heston model, we obtain as reference value for the European call option.

The numerical results are reported in Figures 1, 2 and 3 (see also respectively Tables 1, 2 and 3 for the data). We can observe the convergence of both schemes as increases. For European call option and Asian option, it seems that the scheme (9) based on integrated variance formulation (7) has a better performance. But for the lookback option, the scheme (8) based on the stochastic Volterra equation (6) seems to perform better.

3.2 Pricing options on the variance process

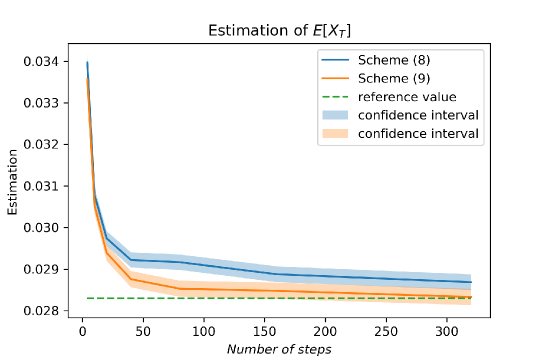

We next consider the options on the variance process , including the variance option with payoff , and the call option on the variance with payoff . Under the Rough Heston model with interest rate , the price of the options are given respectively by and . For both options, one can compute the reference value by deterministic methods.

Indeed, for the variance swap option, one can deduce from the dynamic

that

which is a linear Volterra ODE. With the above parameters of the rough Heston model, one obtains as the reference value for the variance swap option price .

For the call option on the variance, one can use the results in [1] to compute the characteristic function of by solving the corresponding Riccati ODE, and then use the inverse Fourier transform method to compute the value of . With the above parameters of the rough Heston model, we obtain as reference value for .

The discrete-time scheme in (9) allows simulating directly the value of . Nevertheless, the discrete-time scheme in (8) provides simulations of , we then set for the Monte-Carlo estimation.

The numerical results are reported in Figures 4 and 5 (see respectively Tables 4 and 5 for the data). We can observe the convergence of both scheme as the number of time steps increases. At the same time, for the example on variance swap, the performance of Scheme (9) based on the integrated variance formulation seems slightly better.

4 Proofs of Theorems 2.2 and 2.3

Recall that, throughout the paper, Assumption 2.1 holds true.

4.1 Tightness of solutions to Scheme (8)

Let us first rewrite the system (6) and the corresponding discrete-time scheme (8) in two-dimensional equations.

Let be the weak solution of (6), recall that , for all . We denote

and define functions , and by

Notice that is -valued, then it is easy to check that satisfies

| (10) |

Next, for , and , we define the following new coefficients:

| (11) |

Let be the numerical solution to Scheme (8). Then we can write as solution to the stochastic integral equation

| (12) |

We next define the infinitesimal generators and as follows: for all and and , let

| (13) |

It is easy to check that for some constant depending on , one has

| (14) |

We next provide a technical lemma.

Lemma 4.1.

Let be a sequence of non-negative functions on such that . Assume that for some constants and , one has

| (15) | ||||

Then

Proof.

Let be a fixed integer, and denote . Let us define the nondecreasing function . We can then apply (15) for and to obtain that

with some positive constants , satisfying that, for each , and ,

Without loss of generality, we can assume that , so that

Moreover, in view of (4)-(5), one can choose a fixed big enough so that . Then

and, noticing that , it follows that

Notice that the r.h.s. of the above inequality is independent of , which is enough to conclude the proof. ∎

Proposition 4.2.

For each , there exist a constant such that for all and ,

| (16) | ||||

| (17) | ||||

| (18) |

Proof.

(i) First, one has by Equation (12) that, for all ,

| (19) |

Then using the Burkholder-Davis-Gundy inequality, there is a constant depending only on such that

Applying Hölder’s inequality and using the linear growth of and , there is a positive constant (independent of ), such that

Applying now Minkowski’s integral inequality yields

| (20) |

It follows that there is a positive constant (independent of ) such that

Let , one can then apply Lemma 4.1 to obtain that

As a consequence of Proposition 4.2, we immediately obtain the following tightness result.

Corollary 4.3.

The sequence is tight in .

Proof.

Then we identify the equation satisfied by the limit of , by considering an appropriate martingale problem.

Lemma 4.4.

Let be a compact subset of under the uniform norm, then

Proof.

Let be a compact subset of . Recall from the Arzelà-Ascoli Theorem that the following properties hold:

Since and are uniformly continuous on , one can find, for any , an integer such that

This concludes the proof. ∎

The next lemma is a convergence result for the operator defined in (13), which is in line with Lemmas 3.5 and 3.6 of [5].

Lemma 4.5.

Let in , then for any , the following uniform convergence holds:

Proof.

Let us consider the following decomposition:

We will detail the convergence of , as the convergence of follows by a simpler argument. We get

Since converges uniformly, it lies in a compact of . Hence by Lemma 4.4, converges to uniformly in . Then with the boundedness of , this yields the convergence . The convergence of to is a direct consequence of the Lipschitz continuity of , the boundedness of and the uniform convergence of towards . The boundedness of , continuity of and uniform convergence of then give, by an application of the dominated convergence theorem, the convergence of to . ∎

Now we define a martingale problem, which adapts the one from [5, Def. 3.1] to our framework without jumps. It extends the usual definition of a martingale problem to take into account the non-Markovian property because of the kernel . As in the classical setting, there is equivalence between being a weak solution of an SDE and being a solution to the associated martingale problem. More discussions are provided in Remark 4.8. We denote by the space of twice continuously differentiable functions which are compactly supported.

Definition 4.6.

A solution of the (local) martingale problem for , where is the operator given by Equation (13), is a pair of -valued processes defined on a filtered probability space, such that is predictable, is a continuous semimartingale, the process

is a local martingale for every , and one has the equality

| (21) |

Proposition 4.7.

Any weak limit of is a solution of the local martingale problem for .

Proof.

Let be a filtered probability space where is defined and be a weak limit of . Fix and . For any , define

Then is an -stopping time, and we have

The Itô formula implies that the following process

is a uniformly bounded martingale. Thus, for any and , we have

| (22) |

Then, by Skorokhod’s representation Theorem, we may assume that all and are defined on a common probability space , that in almost surely, and that each pair has the same law under as it did under .

By Lemma 4.5, one has

almost surely for any . Define

We conclude that almost surely for . Since is bounded uniformly in , we may use the dominated convergence theorem to pass to the limit in (22) to get

| (23) |

Thus is a martingale with respect to the filtration given by

Since is a stopping time for this filtration and the constant in the definition of was arbitrary, the process

is a local martingale.

Remark 4.8.

Our definition of martingale problem in Definition 4.6 differs slightly from [5, Def. 3.1]. More precisely, our condition (21) is on the process , but Condition (3.3) of [5] is on the process . Nevertheless, as soon as has continuous paths, the two conditions are in fact equivalent, so that the two definitions are equivalent. The formulation based on has the advantage to obtain the tightness more easily than that of , but still we are able to obtain the tightness of in our context.

4.2 Tightness of solutions to Scheme (9)

Let us first rewrite the discrete scheme (9) as an integrated-rough Volterra equation in a continuous-time form: , and

| (25) |

where , and are independent standard Brownian motions. In view of the above definition, and are continuous martingales with quadratic variation

which means that for any ,

| (26) |

Recall the following BDG inequality: for some constant , one has

| (27) |

Lemma 4.9.

Assume and in . Then the following uniform convergence holds:

Proof.

One has

The term converges to 0 uniformly since uniformly and by the fact that .

As for the second term, it follows from the boundedness of that

∎

Since the processes and may differ, we now introduce the auxiliary process

We will eventually show that and converge to the same limit, which is .

Proposition 4.10.

For all , there exists a constant such that for all and ,

Proof.

Recall that is non-increasing, so that

Then by the equation on in (25), together with Cauchy-Schwarz and Hölder’s inequality, one has for some positive constants and (independent of ) that

Using the inequality , one obtains that for some constant (independent of ),

Since and , it follows by Grönwall’s lemma that, for some constant independent of ,

First, we observe that and . Hence it suffices to prove that

| (28) |

From the Cauchy-Schwarz inequality and (4)-(5) we get that

Thus taking the supremum on and the expectation, and applying again the Hölder inequality (), one gets

Hence using (27) and point , we deduce from the previous inequality that (28) holds.

Corollary 4.11.

By passing to a subsequence, one has for some stochastic processes in , where and are two martingales in with quadratic variation and covariation .

Proof.

In view of Proposition 4.10 and Theorem 2.4.11 of [31], the sequences of processes , , , and are tight in . Up to passing to a subsequence (without loss of generality, we do not rename the processes), one has for some processes in .

For any , the mapping

is continuous. So by the continuous mapping theorem and the convergence in law of to , there is

Moreover the convergence in law of to implies that

Thus the finite dimensional distributions of and are identical, and since the class of finite dimensional distributional sets is a separating class in , we obtain .

We now aim at proving that . In view of the convergence of to , it suffices to prove that .

As an immediate consequence of Corollary 4.11, we get that up to taking a subsequence, the following convergence holds:

We next prove that the limit processes satisfy

| (29) |

Proof.

Let be a filtered probability space in which is defined. Corollary 4.11 gives the existence of a subsequence such that converges, and without loss of generality we simply consider that , for some in and a martingale with quadratic variation in a filtered probability space . By the Skorokhod representation theorem, one can assume that (but the filtrations and are different a priori) such that almost surely in . From Lemma 4.9, one has

uniformly in , almost surely. Therefore, solves (29). ∎

4.3 Equivalence and uniqueness of weak solutions

We will adapt the ideas in the proof of [2, Theorem A.1], in order to prove that the process in a (weak) solution of (24) is non-negative, and that the process in a (weak) solution of (29) is non-decreasing. Consequently, Equation (24) shares the same unique weak solution as (6), and Equation (29) shares the same unique weak solution as (7).

Recall that the resolvent of the first kind of the kernel function is defined in (3), together with the definition of the convolution:

Let us fix for , and denote .

Proposition 4.13.

(i) Let be a (weak) solution to the following equation

| (30) |

where . Then is non-negative on .

(ii) Let be a (weak) solution to the following equation

| (31) |

where , is a continuous martingale with quadratic variation and . Then is non-decreasing on .

Proof.

(i) Define the stopping time . Assume that the set is nonempty, then for every fixed , there exists such that

| (32) |

Denote

It follows that

where

By (3.7) of [4], one has for any stopping time ,

Then one has

Recall also from [2, Lemma B.2] that for any such that is right-continuous and of bounded variation, one has

Then for and the resolvent of the first kind of , is right-continuous and of bounded variation (see [2, Remark B.3.]). Thus one has

Notice that , for , and is non-negative and non-decreasing (see [2, Remark B.3.]). It follows that

Further, notice that for all ,

since and are non-negative. Then

Finally, since , for all , it follows that

and hence , which is a contradiction to the fact that in (32). Therefore, . Since is arbitrary, it follows that for any , a.s.

(ii) For equation (31), denote , where is a continuous martingale with quadratic variation . We follow the proof of [1, Lemma 2.1] and apply the stochastic Fubini theorem (see e.g. [34, p.175]) to obtain that

Then is absolutely continuous in so that both and are well defined, and

with and for some Brownian motion . Let us define , then satisfies

Notice that implies that , then we can apply the same arguments as in (i) to deduce that for any . Since , this proves that all solutions to equation (31) are non-decreasing over [0,T]. ∎

4.4 Proofs of Theorems 2.2 and 2.3

Appendix A Tables of simulation results

| Mean Value | Stat. Error | Comp. Time | Mean Value | Stat. Error | Comp. Time | |

| Ref. | 0.056832 | - | - | - | - | - |

| n=4 | 0.059642 | 0.000245 | 7.856192 | 0.065483 | 0.000279 | 7.050599 |

| n=10 | 0.058905 | 0.000238 | 17.419916 | 0.059996 | 0.000244 | 16.307883 |

| n=20 | 0.058630 | 0.000234 | 35.061742 | 0.058635 | 0.000234 | 31.698260 |

| n=40 | 0.058344 | 0.000232 | 70.921679 | 0.057363 | 0.000228 | 60.035371 |

| n=80 | 0.058280 | 0.000232 | 129.678460 | 0.056967 | 0.000225 | 123.884151 |

| n=160 | 0.057965 | 0.000230 | 266.368216 | 0.056905 | 0.000225 | 247.920679 |

| n=320 | 0.057858 | 0.000229 | 582.703205 | 0.056897 | 0.000225 | 482.391579 |

| Mean Value | Stat. Error | Comp. Time | Mean Value | Stat.Error | Comp. Time | |

| Ref. | - | - | - | - | - | - |

| n=10 | 0.036363 | 0.000145 | 18.126627 | 0.038373 | 0.000155 | 16.334577 |

| n=20 | 0.034653 | 0.000136 | 34.257258 | 0.034992 | 0.000138 | 31.231823 |

| n=40 | 0.033647 | 0.000132 | 68.872156 | 0.033387 | 0.000130 | 61.623905 |

| n=80 | 0.033266 | 0.000130 | 144.862723 | 0.032474 | 0.000126 | 121.671897 |

| n=160 | 0.032915 | 0.000128 | 292.438511 | 0.032230 | 0.000125 | 239.012198 |

| n=320 | 0.032479 | 0.000127 | 563.534848 | 0.031907 | 0.000124 | 450.094275 |

| Mean Value | Stat. Error | Comp. Time | Mean Value | Stat. Error | Comp. Time | |

| Ref. | - | - | - | - | - | - |

| n=10 | 0.081591 | 0.000234 | 18.394217 | 0.076769 | 0.000238 | 17.260538 |

| n=20 | 0.085409 | 0.000228 | 33.485885 | 0.079742 | 0.000226 | 33.581574 |

| n=40 | 0.088502 | 0.000226 | 66.453965 | 0.083297 | 0.000222 | 64.918632 |

| n=80 | 0.090927 | 0.000225 | 130.933455 | 0.086043 | 0.000219 | 124.431435 |

| n=160 | 0.092118 | 0.000223 | 290.638306 | 0.088685 | 0.000219 | 246.881069 |

| n=320 | 0.092904 | 0.000222 | 558.946791 | 0.090338 | 0.000219 | 492.821703 |

| Mean Value | Stat. Error | Comp. Time | Mean Value | Stat. Error | Comp. Time | |

| Ref. | 0.028295 | - | - | - | - | - |

| n=4 | 0.033967 | 0.000080 | 8.389909 | 0.033565 | 0.000090 | 8.291969 |

| n=10 | 0.030781 | 0.000085 | 17.706663 | 0.030522 | 0.000098 | 17.645600 |

| n=20 | 0.029736 | 0.000088 | 33.061506 | 0.029387 | 0.000098 | 31.253372 |

| n=40 | 0.029218 | 0.000091 | 69.696746 | 0.028756 | 0.000098 | 59.500006 |

| n=80 | 0.029165 | 0.000093 | 132.443006 | 0.028527 | 0.000097 | 123.055661 |

| n=160 | 0.028875 | 0.000095 | 267.132785 | 0.028477 | 0.000098 | 248.295026 |

| n=320 | 0.028685 | 0.000094 | 575.724998 | 0.028328 | 0.000098 | 486.069715 |

| Mean Value | Stat. Error | Comp. Time | Mean Value | Stat. Error | Comp. Time | |

| Ref. | 0.013517 | - | - | - | - | - |

| n=4 | 0.016940 | 0.000074 | 8.425556 | 0.017096 | 0.000081 | 7.537352 |

| n=10 | 0.014542 | 0.000076 | 18.414490 | 0.015131 | 0.000088 | 15.891882 |

| n=20 | 0.014043 | 0.000079 | 36.577253 | 0.014254 | 0.000088 | 30.900766 |

| n=40 | 0.013752 | 0.000082 | 70.948186 | 0.013905 | 0.000088 | 59.677628 |

| n=80 | 0.013841 | 0.000084 | 144.526883 | 0.013770 | 0.000088 | 118.789620 |

| n=160 | 0.013705 | 0.000085 | 273.132594 | 0.013775 | 0.000088 | 230.445799 |

| n=320 | 0.013641 | 0.000085 | 585.570704 | 0.013600 | 0.000088 | 471.164119 |

References

- Abi Jaber [2021] E. Abi Jaber. Weak existence and uniqueness for affine stochastic volterra equations with L1-kernels. Bernoulli, 27(3):1583–1615, 2021.

- Abi Jaber and El Euch [2019a] E. Abi Jaber and O. El Euch. Markovian structure of the Volterra Heston model. Statist. Probab. Lett., 149:63–72, 2019a.

- Abi Jaber and El Euch [2019b] E. Abi Jaber and O. El Euch. Multifactor approximation of rough volatility models. SIAM J. Financial Math., 10(2):309–349, 2019b.

- Abi Jaber et al. [2019] E. Abi Jaber, M. Larsson, and S. Pulido. Affine Volterra processes. Ann. Appl. Probab., 29(5):3155–3200, 2019.

- Abi Jaber et al. [2021] E. Abi Jaber, C. Cuchiero, M. Larsson, and S. Pulido. A weak solution theory for stochastic Volterra equations of convolution type. Ann. Appl. Probab., 31(6):2924–2952, 2021.

- Akahori et al. [2017] J. Akahori, X. Song, and T.-H. Wang. Probability density of lognormal fractional SABR model. Preprint arXiv:1702.08081, 2017.

- Alfonsi [2015] A. Alfonsi. Affine diffusions and related processes: simulation, theory and applications, volume 6 of Bocconi & Springer Series. Springer, Cham; Bocconi University Press, Milan, 2015.

- Alfonsi and Kebaier [2021] A. Alfonsi and A. Kebaier. Approximation of Stochastic Volterra Equations with kernels of completely monotone type. Preprint arXiv:2102.13505, 2021.

- Alòs and Yang [2014] E. Alòs and Y. Yang. A closed-form option pricing approximation formula for a fractional Heston model. Preprint, 2014.

- Alos et al. [2007] E. Alos, J. A. León, and J. Vives. On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Finance and Stochastics, 11(4):571–589, 2007.

- Araneda [2020] A. A. Araneda. The fractional and mixed-fractional CEV model. J. Comput. Appl. Math., 363:106–123, 2020.

- Bayer et al. [2016] C. Bayer, P. Friz, and J. Gatheral. Pricing under rough volatility. Quant. Finance, 16(6):887–904, 2016.

- Berkaoui et al. [2008] A. Berkaoui, M. Bossy, and A. Diop. Euler scheme for sdes with non-lipschitz diffusion coefficient: strong convergence. ESAIM: Probability and Statistics, 12:1–11, 2008.

- Comte and Renault [1998] F. Comte and E. Renault. Long memory in continuous-time stochastic volatility models. Math. Finance, 8(4):291–323, 1998.

- Comte et al. [2012] F. Comte, L. Coutin, and E. Renault. Affine fractional stochastic volatility models. Ann. Finance, 8(2-3):337–378, 2012.

- Dandapani et al. [2021] A. Dandapani, P. Jusselin, and M. Rosenbaum. From quadratic Hawkes processes to super-Heston rough volatility models with Zumbach effect. Quant. Finance, pages 1–13, 2021.

- El Euch and Rosenbaum [2019] O. El Euch and M. Rosenbaum. The characteristic function of rough Heston models. Math. Finance, 29(1):3–38, 2019.

- Forde and Zhang [2017] M. Forde and H. Zhang. Asymptotics for rough stochastic volatility models. SIAM J. Financial Math., 8(1):114–145, 2017.

- Forde et al. [2021] M. Forde, S. Gerhold, and B. Smith. Small-time, large-time, and asymptotics for the rough Heston model. Math. Finance, 31(1):203–241, 2021.

- Friz et al. [2021] P. K. Friz, P. Gassiat, and P. Pigato. Short-dated smile under rough volatility: asymptotics and numerics. Quant. Finance, pages 1–18, 2021.

- Fukasawa [2011] M. Fukasawa. Asymptotic analysis for stochastic volatility: martingale expansion. Finance and Stochastics, 15(4):635–654, 2011.

- Gatheral et al. [2018] J. Gatheral, T. Jaisson, and M. Rosenbaum. Volatility is rough. Quant. Finance, 18(6):933–949, 2018.

- Gerhold et al. [2019] S. Gerhold, C. Gerstenecker, and A. Pinter. Moment explosions in the rough Heston model. Decisions in Economics and Finance, 42(2):575–608, 2019.

- Gripenberg et al. [1990] G. Gripenberg, S.-O. Londen, and O. Staffans. Volterra integral and functional equations, volume 34 of Encyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, 1990.

- Guennoun et al. [2018] H. Guennoun, A. Jacquier, P. Roome, and F. Shi. Asymptotic behavior of the fractional Heston model. SIAM J. Financial Math., 9(3):1017–1045, 2018.

- Horvath et al. [2017] B. Horvath, A. J. Jacquier, and A. Muguruza. Functional central limit theorems for rough volatility. Available at SSRN 3078743, 2017.

- Horvath et al. [2020] B. Horvath, A. Jacquier, and P. Tankov. Volatility options in rough volatility models. SIAM J. Financial Math., 11(2):437–469, 2020.

- Jacod and Shiryaev [2003] J. Jacod and A. N. Shiryaev. Limit theorems for stochastic processes, volume 288 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, second edition, 2003.

- Jakubowski et al. [1989] A. Jakubowski, J. Mémin, and G. Pagès. Convergence en loi des suites d’intégrales stochastiques sur l’espace de Skorokhod. Probab. Theory Related Fields, 81(1):111–137, 1989.

- Jusselin and Rosenbaum [2020] P. Jusselin and M. Rosenbaum. No-arbitrage implies power-law market impact and rough volatility. Math. Finance, 30(4):1309–1336, 2020.

- Karatzas and Shreve [1991] I. Karatzas and S. E. Shreve. Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- Kurtz and Protter [1991] T. G. Kurtz and P. Protter. Weak limit theorems for stochastic integrals and stochastic differential equations. Ann. Probab., 19(3):1035–1070, 1991.

- Li et al. [2021] M. Li, C. Huang, and Y. Hu. Numerical methods for stochastic Volterra integral equations with weakly singular kernels. IMA Journal of Numerical Analysis, 2021.

- Revuz and Yor [1999] D. Revuz and M. Yor. Continuous martingales and Brownian motion, volume 293 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, third edition, 1999.

- Richard et al. [2021] A. Richard, X. Tan, and F. Yang. Discrete-time simulation of stochastic Volterra equations. Stochastic Process. Appl., 141:109–138, 2021.

- Zhang [2008] X. Zhang. Euler schemes and large deviations for stochastic Volterra equations with singular kernels. J. Differential Equations, 244(9):2226–2250, 2008.