126ct \forLoop126ct

Hida-Matérn Kernel

Abstract

We present the class of Hida-Matérn kernels, a canonical family of covariance functions that densely represents the entire space of stationary Gauss-Markov processes. It extends upon the Matérn kernels with flexible oscillatory components. Any stationary kernel, including the widely used squared-exponential and spectral mixture kernels, are either directly within this class or are appropriate asymptotic limits, demonstrating the generality of this class. Taking advantage of its Markovian nature, we show how to analytically represent a Hida-Matérn process as a state-space model using only the kernel and its derivatives. In turn this allows us to perform Gaussian process inference more efficiently and side step the usual computational burdens. We further improve the numerical stability and reduce computational complexity by exploiting the structural properties of the state-space representation.

Keywords: Hida-Matern Kernel, Stationary Gaussian Process, Kernel Methods

1 Introduction

The Gaussian process (GP) framework provides principled means to make inferences on functions (Rasmussen and Williams, 2005). Endowed with a calibrated measure of uncertainty, GPs fit well within the Bayesian machine learning paradigm and can be embedded as a part of a broad class of models (Karaletsos and Bui, 2020; Kuss and Rasmussen, 2005; Ng et al., 2018). However, in practice the computational burden of using GPs typically limits their applicability to moderately sized datasets. Scalable frameworks such as inducing point methods, specially structured kernels, streaming approaches, state-space formulation of GPs and so on seek to remedy this weakness by reducing the computational complexity of GP inferences (Bui et al., 2017; Titsias, 2009; Wilson and Nickisch, 2015; Hartikainen and Sarkka, 2010). Earlier literature on GPs in the 1950s and 60s was largely focused on their theoretical properties. We discovered that many of these findings have practical implications for developing more scalable inference frameworks. Building on pioneering works by Takeyuki Hida and others, we introduce the class of Hida-Matérn kernels, which form a basis for translation invariant kernels and readily admit a state-space representation through which exact inference can be made in linear time.

A specific GP is characterized by its covariance function, or kernel; if its analytical form is given, its inspection reveals properties such as stationarity, periodicity, and differentiability. However, beyond the second order statistical structure of the process, the kernel alone fails to rigorously quantify aspects such as Markovianity, sample path properties, and uniqueness of representation. Building on P. Levy’s constructive formulation of GPs, or as it was called, a canonical representation (Lévy, 1956, 1951), T. Hida was able to broadly generalize characteristics of GPs (Hida, 1960; Hida and Hitsuda, 1993).

While in a practical sense many of these theoretical properties may be of little consequence, fully understanding the Markov properties of GPs can help alleviate the computational burden commonly associated with them. For example, the GP with Matérn kernel (a.k.a. Ornstein-Uhlenbeck process) is well known to admit fast inference schemes thanks to its Markov property (Stein, 1999). As we will see in Section 4, there exist other ways of defining a generalized GP Markov property, which in turn, provide a clear avenue to formulating them in terms of a state-space model (SSM). The SSM representation can then be used so that exact GP inference can be had in linear time given ordered data.

More than this though, we will show that the class of GPs with admissible state-space representations turns out to be very broad. In fact, all stationary, real-valued, and finitely differentiable GPs, which we will refer to as Hida-Matérn GPs (H-M GPs), have canonical representations that must be linear combinations of basis functions initially derived by T. Hida in Hida (1960). The derived covariance functions, or Hida-Matérn kernels, corresponding to these basis thus span the space of all such kernels governing H-M GPs. Moreover, translation-invariant covariance functions that govern GPs not in this class can be approximated arbitrarily well by linear combinations of Hida-Matérn kernels (Thm. 2).

Although state-space formulations of GPs have been examined extensively in recent literature, their formulation involves parametrizing a stochastic differential equation (SDE) whose stationary covariance matches that of the GP in question (Solin et al., 2018; Corenflos et al., 2021; Solin and Särkkä, 2014; Solin, 2016). In contrast, our approach only requires determining all derivatives of the covariance function. Furthermore, owing to Markov properties that will be discussed, the SSM formulation of any H-M GP is trivial to construct (Sec. 4.3).

To facilitate thinking beyond the second order structure of GPs, we re-introduce the importance of defining GP Markov properties through simple, yet enlightening examples (Sec. 2). We then introduce the family of Hida-Matérn kernels, present their universality with respect to convergence in the space of translation-invariant kernels, how their Markovianity leads to simple SSM representations, and then how said representations open the door for computationally feasible GP inference (Sec. 3). We show that certain linear SDEs with stable dynamics admit a solution that lies within the Hida-Matérn family, which consequently implies that the matrix exponential of such dynamics matrices has a closed form solution (Sec. 4). Finally, we show examples of approximating arbitrary kernels through linear combinations of Hida-Matérn kernels (Sec. 7.1), demonstrate how low-order Hida-Matérn kernels extrapolate well on the Mauna Loa CO2 data set, and illustrate the scalability of our approach in speed comparisons against state of the art methods (Sec. 10).

2 Background: Canonical representation of stationary Gaussian processes

2.1 Two senses of Markovian GP

Let be a GP indexed over time, that is, for any finite time indices , the joint distribution of is normal (Rasmussen and Williams, 2005). The covariance function, , and the mean function, , of a GP fully specifies its probabilistic structure. An alternative constructive formulation of GPs by P. Levy led to the development of a canonical representation for GPs as stochastic integrals with respect to a Brownian motion, from which new Markov properties were formulated.

2.1.1 Markov in the restricted sense

In the following, we consider univariate centered stationary GPs which are fully characterized by a translation invariant covariance kernel where . One of the simplest examples of a Markovian GP is the Ornstein-Uhlenbeck (OU) process, with kernel (Stein, 1999). As we will see, it is how one defines a Markov property for GPs that allows for greater insight into their behavior. In this case, the OU process possesses the simplest Markov property in that, , where 111rigorously, is the filtration of the process up until time . represents all information known about the process up to time . The fact the OU process is Markov is easily identified by writing down its corresponding SDE and associated solution:

| (1) | ||||

| (2) |

where is the Wiener process (Brownian motion) (Hida and Hitsuda, 1993; Oksendal, 1992; Särkkä and Solin, 2019). Note that the solution, which is a Gaussian process, depends only on the most recent known value and not on the farther history (Jazwinski, 2007). Now, it is easy to determine that the conditional distribution, ,

| (3) |

In this pedagogical example, we can view the kernel not only as a covariance function, but also as the operator which propagates the process forward in time. That said, the OU process has undesirable limitations – it is mean square differentiable nowhere, thus its sample functions are very rough (Jazwinski, 2007; Stein, 1999; Lévy, 1956). This leads us to P. Levy’s definition of -ple Markov in the restricted sense, extending the Markov property to GPs of higher order differentiability (Lévy, 1951; Hida and Hitsuda, 1993).

Definition 1 (-ple Markov in the restricted sense).

A GP, , is called -ple Markov in the restricted sense if it is exactly times differentiable in mean square and

| (4) |

where denotes the mean square derivative of .

This definition has immediate consequences in reasoning about finitely differentiable GPs which we will show through a motivating example. First, note that a GP and all of its mean square derivatives are jointly Gaussian (Jazwinski, 2007; Särkkä, 2011) and define so that for a stationary GP, the covariance functions of the corresponding mean square derivative GP are

| (5) |

Now, consider a GP, , with the Matérn kernel (see Table 1) parameterized by unit variance and length-scale, (Rasmussen and Williams, 2005). Since is once differentiable, this GP has only one mean square derivative, , so that , making it a -ple Markov GP in the restricted sense. By the joint Gaussianity, the conditional density is

| (6) |

where and . Note how linear combinations of and fully describe how the process, , evolves over time.

We can generalize this to arbitrary N-ple Markov GPs in the restricted sense and their mean square derivatives to understand how they evolve together over time. Define a vector representation , which, like the OU process earlier, is not differentiable (because of non-differentiable ). The vector process is a -ple GP. Now, can be determined so that

| (7) | ||||

| (8) |

where . While Eq. (7) could be used to recursively determine the trajectory of , Eq. (6) could not; retaining the most recent information about the process in conjunction with its mean square derivatives is key to inferring its future behavior.

2.1.2 Markov in the Hida sense

Consider a GP, , where and are both GPs with differently parameterized Matérn kernels. Then, is only once differentiable, however, it is not a -ple GP in the restricted sense because Def. 1 is not satisfied. With Levy’s definition being insufficient, we introduce T. Hida’s more general description of a GP Markov property, which we refer to as -ple Markov (in the Hida sense).

Definition 2 (-ple Markov in the Hida sense (Hida and Hitsuda, 1993)).

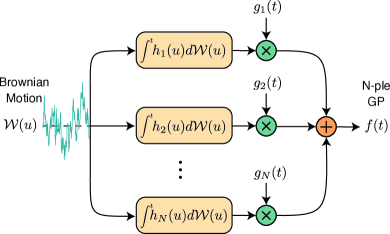

A GP, , is called an -ple Markov GP if it admits the following filtered white noise representation:

| (9) | ||||

| (10) |

is called the “canonical kernel” of the process in the literature, however, it should not be confused with a positive-semi-definite (covariance) kernel. For clarity’s sake, we will henceforth refer to as the canonical filter of the process. Substitution of Eq. (10) into Eq. (9) shows is constructed as a linear combination of additive random processes by writing,

Hence, the process would be described as -ple Markov in the Hida sense. We see then that if a process is -ple Markov (in the Hida sense) it may not be -ple Markov in the restricted sense as Def. 2 does not require differentiability of the process. Both of these definitions will be the groundwork for constructing appropriate state-space models that can be used for GP inference.

2.2 The complete canonical basis

A remarkable fact is that the canonical filter of any stationary -ple Markov GP lies in the span of a known set of basis functions. The form of those basis functions as derived in Hida and Hitsuda (1993) is given in the following theorem.

Theorem 1 (Canonical Kernels (Hida and Hitsuda, 1993, p. 102)).

If is a stationary -ple Markov GP, then its canonical filter, , can be represented by a linear combination of the basis

| (11) |

where with , , , and .

As an example, take , , , and , then . By plugging this canonical filter into the equation above, we find that the stationary covariance of this process equals the Matérn kernel with unit length-scale and variance. This invites the obvious question: what are the equivalent set of basis functions that span the space of admissible covariance functions over stationary, finitely differentiable GPs?

3 The Hida-Matérn Kernel

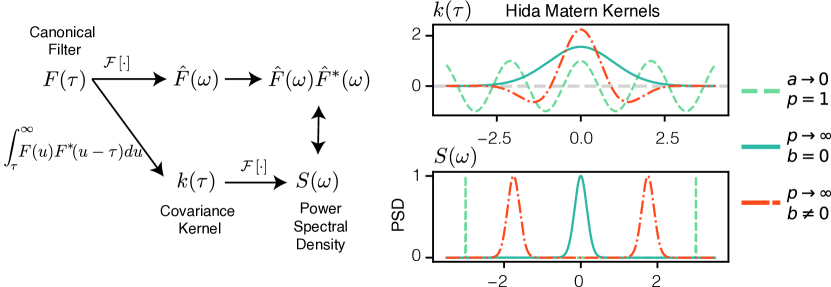

Leveraging the basis over canonical filters describing stationary and Markovian GPs, we can determine a corresponding basis over admissible covariance functions. Let be a GP with canonical filter given by a single basis as described in Thm. 1, i.e. , then has power spectral density (PSD), , given by where is the Fourier transform of . In the case that is complex, then would not be the PSD of a real-valued GP as it would not be purely real and symmetric.

Keeping this in mind, we can determine a basis over real-valued covariance functions by isolating the real and symmetric parts of , giving us . Then, by invoking Bochner’s theorem we can arrive at through taking the inverse Fourier transform of (Rasmussen and Williams, 2005). The result is stated below and the full derivation is in Appendix A.

Proposition 1.

The real-valued covariance function, and PSD corresponding to a canonical basis, , with , are

| (12) | ||||

| (13) |

where is the general Matérn covariance kernel of order and length-scale . Although simple, these kernels, which we call Hida-Matérn kernels, span the space of stationary and finitely differentiable GP covariance functions. Similar to a standard Matérn kernel the parameter controls the differentiability/smoothness, is the inverse length-scale, and controls the center of the PSD. To conceptualize the Markov property better take , and , then a GP with covariance function will be -ple Markov in the Hida sense; however, when , then this covariance function coincides exactly with the Matérn kernels and such a GP would be -ple Markov in the restricted sense. The functional form of (12) has appeared in the literature before and we discuss this in Section 8.

There may be some confusion in the previous statement with regards to being an -ple GP when but -ple when that an example may help clarify. Take to be a GP with canonical filter and , . Clearly, is conjugate to and individually each would be the canonical filter of a -ple GP. If we had that then both filters are identical and is simply making a -ple GP in the restricted sense however, summing them when results in a GP that is -ple in the Hida sense.

We can gain more expressive power from the Hida-Matérn kernel by considering their linear combinations. Though many strictly concern themselves with linear combinations such that the coefficients are always positive, it can be somewhat restrictive. As long as the coefficients are chosen such that the resulting kernel is positive semidefinite, then negative coefficients are permitted (Posa, 2021). Thus, the following theorem gives us good faith that we can achieve a respectable approximation of kernels that produce GPs infinitely differentiable in mean square using only a finite linear combination of Hida-Matérn kernels parameterized by the same value of but varying inverse length-scales, , and frequency parameters, .

Theorem 2 (Mixture of stationary Hida-Matérn kernels are dense.).

For any fixed , Hida-Matérn kernels are dense in the space of square integrable functions, hence they are dense with respect to convergence.

While those GPs that are infinitely differentiable in mean square have kernels that can not be approximated exactly with a finite linear combination of Hida-Matérn kernels, those that are finitely differentiable can. GPs with covariance functions such as the squared exponential, spectral mixture, and cosine kernel fall into the class of infinitely differentiable GPs and in some literature are referred to as “completely deterministic”.

Remark 1.

Certain kernels such as the squared exponential do not fall within the class of GPs which may be represented by finite dimensional SDEs as they have a countably infinite number of derivatives and are analytic. Such GPs are regarded as “completely deterministic” (Lévy, 1956)—meaning if observed for an infitessimal amount of time their future behavior is in theory completely known (Stein, 1999).

3.1 The family of Hida-Matérn GPs – Hida-Matérn Mixture (MHM) kernels

With the Hida-Matérn kernel defined, we can now consider the family formed by their linear combinations. We define a mixture of Hida-Matérn (MHM) kernels as,

| (14) | ||||

| (15) | ||||

| (16) |

where specifies the mixands smoothness, their respective weights, and the order of the Markov property in the Hida sense. Note how based on the value of each , if , then the process can be anywhere from -ple Markov to -ple Markov in the Hida sense. Since Hida-Matérn kernels with fixed form a universal class, the Hida-Matérn mixture kernels do as well.

4 Hida-Matérn State Space Representations

The intuition regarding Markov GPs that we developed earlier will help now in constructing a state-space representation of GPs that can be described by the Hida-Matérn class of kernels (Jazwinski, 2007). Though the state-space representation of GPs has been used successfully in the literature (see Sec. 8), construction of an appropriate SSM usually begins by correctly parameterizing a linear SDE whose solution has a stationary distribution coinciding with the GP of interest (Hartikainen and Sarkka, 2010; Solin et al., 2018; Solin, 2016). In contrast, the construction we present leverages the -ple Markov property and allows for a state-space representation that only depends on the kernel and its derivatives. To start, consider GPs that are -ple Markov in the restricted sense, which for now, limits our scope to Hida-Matérn kernels of order with (or Matérn kernels of order for ). In the course of doing so, we will gradually expand upon this construction to handle the full family of Hida-Matérn kernels.

4.1 SSMs for -ple GPs in the restricted sense

Let be an times differentiable, and stationary GP with kernel , then is an -ple Markov GP. By consolidating and its mean square derivatives into the vector process

| (17) |

we have that is a -ple Markov GP in the restricted sense so that . Recognizing is a multioutput GP described by the kernel , with , we can write the conditional distribution explicitly:

| (18) | ||||

| (19) | ||||

| (20) |

where with (Álvarez and Lawrence, 2011). It is easy to see now that the conditional density in Eq. (18) can be rewritten as a difference equation so that is equivalently described by,

| (21) | ||||

| (22) |

The main object of interest is easily extracted from by letting so that . Thus, we can reason about the behavior of through linear combinations of its past mean square derivatives or equivalently . Much like our motivating examples earlier, alone characterizes how the process propagates forward through time. In order to motivate the practical utility of this construction we proceed by considering standard GP regression.

4.2 GP Regression with finite SSMs

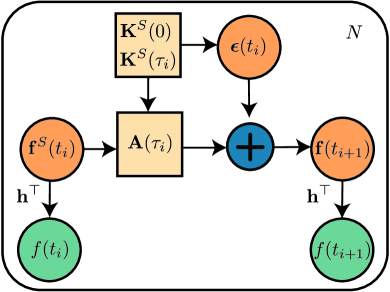

In a GP regression setting with noisy observations, , and stationary GP that is times differentiable, the standard generative model, as in Rasmussen and Williams (2005), can be recast as a linear Gaussian SSM using Eq. (21) so that,

| (23) | ||||

| (24) |

with , , and . Since the aforementioned SSM is stable it admits a stationary covariance (Anderson and Moore, 1979).

Ensuring the process begins in the stationary state amounts to specifying . For SSMs, determining involves finding the solution of the continuous/discrete Lyapunov equation, however here (see Appendix C). In this form, the usual Kalman filtering and smoothing algorithms can be used to recover the posterior in time, where is the number of data points.

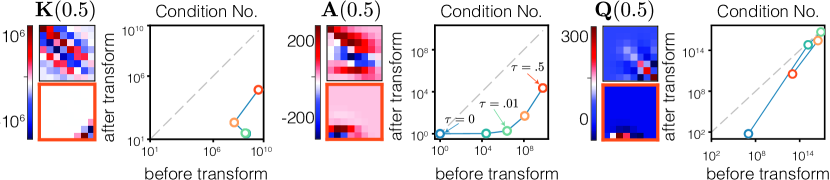

While the Kalman filtering algorithm is computationally efficient, ensuring that it is numerically stable can often be difficult. As a result, ill numerical conditioning will be exacerbated by the fact that elements of are increasing in magnitude towards the bottom right, which we illustrate in Fig. 5. Approaches such as balancing or Nordsieck coordinate transformations, often used to combat this problem, formulate a surrogate SSM that can be used for equivalent inference (Osborne, 1966; Nordsieck, 1962; Corenflos et al., 2021; Krämer and Hennig, 2020). Similar in spirit to those approaches, we propose a correlation transform, taking advantage of the SSMs formulation in terms of covariances. Concretely, consider a linear transformation of the original process, where

so that . An alternative SSM is formed by substituting for and rewriting the observation equation as . Whereas would be ill conditioned and thus cause problems when taking its inverse, will have a significantly lower condition number, and we can expect the better numerical conditioning to provide more accurate inference. After inference pertaining to is made, properties of interest related to are easily recovered.

4.3 SSMs for general -ple GPs

Having introduced how an SSM for a GP with Hida-Matérn kernel of order when can be constructed, we are now in a position to consider the general case. In order to make this jump, first observe that when , a GP, , with kernel , will be a -ple process in the Hida sense but not the restricted sense. We can see this most readily by breaking the cosine term into a sum of two complex exponentials so that,

| (25) | ||||

| (26) |

which shows is times differentiable, but the sum of complex conjugate Hida-Matérn kernels of order . However, it is apparent that the representation given by Eq. (25) is redundant due to the complex conjugacy. Hence, we can consider a complex GP, , with kernel , so that an equivalent description of is given by the SSM,

| (27) | ||||

| (28) | ||||

| (29) |

where

| (30) | ||||

| (31) |

and similar to earlier, , and . This shows that we can reason about these particular -ple Markov GPs, in the Hida sense, with an -dimensional state-space model by exploiting the complex-conjugate symmetries present. Sans the necessity of having to work with complex numbers, this formulation lends itself to GP regression exactly as described in Section 4.2.

4.4 SSMs for Hida-Matérn mixtures

Now that we have explored how to formulate the SSM describing a GP whose covariance function is an elementary Hida-Matérn kernel, it is a trivial extension to consider the SSM formulation for the Hida-Matérn mixture kernel, .

| (32) |

so that , and . Thus, we can engineer arbitrarily complex kernels as linear combinations of Hida-Matérn kernels, yet work with them in the same manner by constructing an SSM with . For clarity sake later on if is a GP with covariance function that is a mixture of Hida-Matérn kernels we will say that is an MHM (mixture of Hida-Matérn kernels) GP denoted .

5 Hida-Matérn GPs and SDEs driven by Brownian motion

It is well known that the solution of a linear SDE driven by Brownian motion is a Gauss-Markov process (Jazwinski, 2007; Särkkä and Solin, 2019; Oksendal, 1992). In conjunction with our earlier discussion about Markovinity of univariate GPs, this observation raises the question, how does the state-space representation of a Hida-Matérn GP relate to the solution of an SDE with the same stationary covariance. Delving into this question, we restrict ourselves to SDEs that can be written symbolically as

| (33) |

where is a differential operator of order . This formal representation can be transformed into an equivalent SDE much like in the works of (Hartikainen and Sarkka, 2010; Corenflos et al., 2021; Solin and Särkkä, 2014) so that

| (34) |

with and a one dimensional Brownian motion. Taking to be a Hida-Matérn GP then we can consider its solution in terms of the preceding SDE and equivalent state-space representation so that we may develop stronger intuitions. Writing the two representations side-by-side, for reasons that will become clear, we have

where is the state transition matrix of the system and (Jazwinski, 2007). Our first insight is that in order for both equations to be consistent and must be equivalent so that is the same under either representation. This tells us that we can find closed form solutions to the matrix exponential in terms of the derivatives of the Hida-Matérn kernel.

Moving forward it will be helpful to note that if is a GP with kernel then its SDE representation will have a dynamics matrix with one eigenvalue of multiplicity . So, just to keep all of the ideas clear we have that a Hida-Matérn GP with kernel will be times differentiable in mean square, have a dimensional state-space representation, and its dynamics will have one eigenvalue of multiplicity .

Now, consider an arbitrary vector valued GP, , described by the SDE

| (35) |

with , and the dynamics such that has one eigenvalue of multiplicity . If is a Hida-Matérn GP with kernel then it in conjunction with its derivative processes satisfy a linear SDE . In this case, , like , has one eigenvalue of multiplicity , and .

The hyperparameters of can be adjusted so that and have the same eigenvalue of multiplicity in which case they can be decomposed into their Jordan forms with and . We can form a surrogate process, , such that , where is chosen so that . Now, satisfies the SDE

| (36) | ||||

| (37) | ||||

| (38) | ||||

| (39) |

which is equivalent to the SDE for the Hida-Matérn GP if . So far, this illustrates that -dimensional SDEs with dynamics of multiplicity can be transformed by a change of coordinates to an SDE for a Hida-Matérn GP and its derivative processes when .

However, it is possible that has several eigenvalues of different multiplicity in which case we may wonder how to determine if that SDE can also be transformed into one that aligns with a Hida-Matérn GP. To fix the idea, take as described in Eq. (35) and to have the Jordan decomposition with . We can construct a GP whose covariance function is a sum of Hida-Matérn kernels parameterized so that its dynamics can be decomposed into Jordan blocks with the same multiplicity and eigenvalues as . Again, if with selected so that then an appropriate coordinate change of will produce an SDE that describes a Hida-Matérn GP. This gives us a necessary condition on a linear change of coordinates that transforms an arbitrary SDE into one with the interpretation that the vector process represents a Hida-Matérn GP and its derivative processes given by the following Lemma.

Lemma 1.

If given a linear and finite-dimensional SDE, written as

| (40) |

where , a one dimensional Brownian motion process and dynamics , with Jordan decomposition , , then a coordinate change, , mapping to an SDE representing a Hida-Matérn GP and its derivative processes exists if where . Here, is taken so that the SDE for a Hida-Matérn GP with mixands has dynamics matrix .

In other words, a linear SDE with dynamics matrix having Jordan blocks may be equivalent to a linear transformation of the SSM formulation of a Hida-Matérn GP with mixands. Our second insight concerns the derivatives of a Hida-Matérn covariance kernel. When is a Hida-Matérn GP with kernel we have the relation that for some whose eigenvalues lay in the left half plane. By properties of the matrix exponential , but we can use the fact that is a matrix of derivatives to understand what the form of is by inspection.

First, note that taking the element wise derivative of , for now not worrying about its last row, is equivalent to shifting its rows up by one position. Hence, must be a companion form matrix that essentially takes the element wise derivative of so that

| (41) | ||||

| (42) |

What this reveals is that derivatives of of order up to are linear combinations of its first derivatives. Since computing requires computing the derivatives of this offers another avenue for reducing computation as we only need to calculate the first . Let’s work through a motivating example to make some of the ideas concrete. Say we take the Matérn 3/2 kernel with unit variance and length-scale so that . Then, we have that

| (43) |

Standard calculations yield

| (44) | ||||

| (45) |

By the derivative property of the fundamental matrix solution, , we can calculate the SDEs dynamics since . Plugging in reveals the dynamics

| (46) | ||||

| (47) | ||||

| (48) |

which shows that is in companion form. That fact will hold no matter the dimensionality of the SDE through recognizing that

| (49) |

which implies that higher order derivatives will be linear combinations of their lower order counterparts due to the companion form structure of . As a sanity check, one can consult the works Solin (2016); Hartikainen and Sarkka (2010) to see that the same dynamics were found albeit through a much more algebraically demanding procedure.

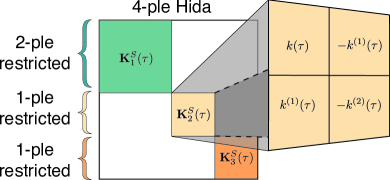

5.1 Multi-output Hida-Matérn kernels

In our discussion of SDEs we were more focused on the latent evolution of and its derivatives, however, vector processes defined that way are valid multioutput GPs. We will now consider those vector valued processes as a means to define a new class of multioutput GPs.

To consider multi-output GPs take a MHM GP, , and ignore the observation equation so that we are only concerned with . As we said, has an equivalent SDE formulation, with associated dynamics matrix having a particular Jordan block structure. Taking , we have a new GP of the same dimension, and its SSM formulation becomes immediate as so that

| (50) |

Now, we have that is a multi-output MHM (MO-MHM) GP, i.e. . Taking this one step farther, the observations can be modified so that rather than projecting the latent process onto one dimension via , we project it to via . The augmented SSM becomes

| (51) | ||||

| (52) |

Whereas before, we had latents that represented the process and its mean square derivatives, the latents, , are their linear combinations as mapped by . We note that these linear transformations do not alter the Markov property of the process, they simply transform it to a different coordinate system. From the discussion earlier, it is also clear that the dynamics matrix of the SDE describing has the same Jordan block structure as that of since the coordinate change only results in a new SSM whose dynamics are similar to those of (where similar should be taken to mean the two are related through a similarity transform).

6 Numerical and Algorithmic Properties

In Section 4.2 we noted that the structure of can lead to technical difficulties which make naive state-space inference infeasible. The proposed correlation transform amends the ill numerical conditioning that manifests itself in a naive implementation and makes it possible to work with higher order Hida-Matérn kernels. There are additional precautions we may take that guarantee higher numerical stability as well as reductions in computational complexity.

6.1 Special structure of

As the building blocks of are covariances between the process and its mean square derivatives, one may suspect that has some special structure that can be exploited. In fact, many of the properties exhibits are similar to those of matrices explored in Strang and MacNamara (2014).

For any multioutput covariance matrix formed from a single Hida-Matérn kernel we have that the off diagonal, up to appropriate sign flips, will only consist of the derivative of the kernel evaluated at . Hence, the multioutput covariance kernel is composed of only unique elements, leading to memory requirements that scale linearly with the order of the kernel used. This is especially useful when we consider that if we were working with observations not spaced uniformly then , whose elements may require evaluation of complex equations, would need to be recomputed every time step.

Let’s now consider the inversion of . If the correlation transform is properly used, then this inverse should not be a source of much trouble. However, when , the multioutput covariance kernel will be identically 0 at all indices such that is odd. To see this, note that the PSD of the Hida-Matérn kernel is real and symmetric, and that exactly coincides with the moment of , which is 0 for odd. Recognizing this, elementary row and column operations can be used to transform the covariance matrix into the block matrix

| (53) |

with and being elementary row/column operations. The inverse of the altered matrix is then easily taken block by block. Subsequent application of the inverse row and column operations return the desired inverse. When we do not have this sparsity present as we have chosen to work with the reduced, yet equivalent, SSM. Understanding its structure can still help us to achieve improved numerical stability by enforcing properties we expect that numerical noise may break. For example, if then should be purely imaginary at indices such that is odd. Hence, its inverse should retain this structure and if numerical noise causes these entries to become real, then they are easily masked.

6.2 Kalman updates

In performing Kalman filtering over time-steps, the updated covariance, at time-step , is not guaranteed to retain the positive semidefinite structure of a proper covariance matrix. Often, the Joseph form of the covariance update or square root filtering can be used to ensure that positive semidefiniteness is not lost (Anderson and Moore, 1979). However, since is sparsely populated (i.e. a kernel which is the sum of Hida-Matérn kernels will have nonzero values), the equations for the updated mean and covariance, and , can be simplified for additional computational savings and superior numerical stability.

Input

Kalman Filtering

In Algorithm 1, which outlines the Kalman filtering/RTS smoothing algorithm to return the marginal posterior means and covariances in a GP regression setting, we can see the succint updates for and . The updated posterior mean, , is a sum of the predicted mean, , and the indexed columns of the predicted covariance, . Similarily, the updated covariance is a rank update of predicted covariance, where is the number of Hida-Matérn mixands.

7 Relation to Other Kernels

Previously we noted that many frequently used kernels either reside in the Hida-Matérn family or can be approximated appropriately. Take as an example the squared exponential kernel, it is well known that the standard Matérn family of kernels with smoothness parameter approaches a squared exponential as . Remembering this, it is clear that the Spectral Mixture family of kernels is an asymptotic limit of a Hida-Matérn mixture as the smoothness parameter (Wilson and Adams, 2013).

The cosine kernel, , is also not directly within the Hida-Matérn family, but it is approached in the limit for . As another example, take the periodic kernel defined as , which can be expanded using its Taylor series representation (Solin and Särkkä, 2014)

| (54) | ||||

| (55) | ||||

| (56) | ||||

| (57) | ||||

| (58) |

Which illustrates how a kernel such as the periodic covariance can be decomposed such that it can be approximated by a Hida-Matérn mixture.

| kernel | |

|---|---|

| Squared Exp. | |

| Rational Quadr. | |

| Gabor. | |

| Sinc |

| kernel | |

|---|---|

| Matérn | |

| Matérn | |

| Spectral Mix. |

Now consider the LEG family of kernels introduced in Loper et al. (2021). Take to be the solution of a linear SDE driven by Brownian motion. Linear transformation of and addition of Gaussian noise gives an observed process so that

| (69) | ||||

| (70) | ||||

| (71) |

In which case it is said that where . The equivalence to a MO-MHM kernel is immediate from the discussion earlier on SDEs; the number of mixands determined by the Jordan block structure of , with their hyperparameters determined by the eigenvalues of .

To make the equivalence more concrete, decompose into where is a Jordan block matrix. Say that has blocks, each of size , . Then, a GP, , with Hida-Matérn mixture kernel containing mixands, the th having order , has an SSM formulation equivalent to the solution of a linear SDE with dynamics matrix such that . Taking , the SSM formulation of the vector process will then be the solution of the SDE as defined in Eq. (69). Further, setting and taking the covariance of to be shows GPs defined either way are equivalent.

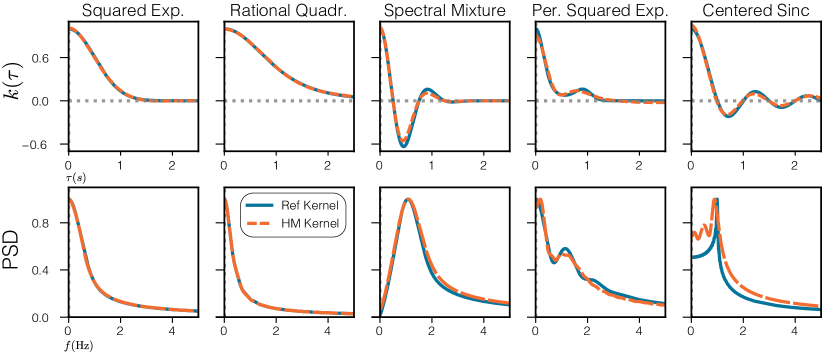

7.1 Approximating arbitrary kernels

Imagine a scenario where a kernel, , has been designed, its hyperparameters chosen, and we wish to make GP inference under this kernel. If the data set is small, exact GP inference can be used, however, scalability quickly becomes a concern and only approximate methods are viable. When the kernel of interest can be approximated well by linear combinations of Hida-Matérn kernels, then the SSM formulation presented is an appealing avenue.

Under this scenario, the question becomes how can the parameters of a Hida-Matérn mixture, , be estimated so that it closely matches . A practical, yet simple manner of estimating these hyperparameters is to minimize the squared loss between the reference kernel and the Hida-Matérn mixture with respect to the mixtures hyperparameters. This results in the following optimization problem,

| (72) |

where contains all hyperparameters of the Hida-Matérn mixture to optimize. Through Parseval’s Theorem, we can see that the objective in Eq. (72) not only minimizes the squared distance between the mixture and target kernels but also the squared distance of their PSDs (Oppenheim and Schafer, 2014).

In Fig. 6 are plotted Hida-Matérn mixtures containing four mixands fit to various stationary kernels. Though some of the reference kernels would have been approximated better through a single Hida-Matérn kernel (take for example the Spectral Mixture kernel) the kernel functions and their PSDs, visually, are matched well.

8 Historical Remarks

In passing we have discussed the canonical representation of GPs. Historically, many different representations and constructions of GPs have been used to understand their properties. One of the most famous examples is the Kahrunen-Loeve expansion (KL) in which a stationary GP is decomposed as an infinite sum of randomly weighted basis functions. Prior to Kahrunen and Loeve’s work however, a similar representation was explored in the work of Kosambi but was not quite fully fleshed out (Kosambi, 1943).

The representations we have mainly focused on are those that express GPs in terms of integral and differential operators. Typically cited as one of the first works exploring this avenue is that of Doob, where he considers stationary and finitely differentiable GPs who can be formally described by a differential equation

| (73) |

which should only be read symbolically as the derivative of Brownian motion does not exist (Doob, 1944). Subsequently, P. Lévy being concerned with uniqueness of GP constructions developed what he called a canonical representation. This representation allowed for specification of a stronger Markov property than that of Doob by dropping the restriction on stationarity of the process (Lévy, 1956; Hida, 1960; Hida and Hitsuda, 1993).

Tangentially related, and almost in parallel to Levy’s development of a canonical GP representation was Woodbury’s exploration of the connection between GP covariance functions and the Green’s function of a suitably defined adjoint equation (Dolph and Woodbury, 1952). Approaching the problem similarily, T. Hida was able to determine an appropriate set of basis over GP covariance functions that are stationary and finitely differentiable (Hida, 1960).

Following Hida’s work, relationships between L-splines and realizations of sample functions from GPs defined by an appropriate SDE were made concrete in Wahba (1978). Viewing L-splines as realizations of GP sample functions, Weinert formulated L-spline fitting as making inference pertaining to an equivalent SSM formulation subsequently allowing for inference in time (Weinert and Sidhu, 1978; Weinert et al., 1980). Shortly after, Ansley considered the same SSM representation of a scalar GP although with a novel smoothing algorithm and further theoretical insights (Kohn and Ansley, 1987).

More recently, in the context of machine learning, Hartikainen and Sarkka (2010) consider SDEs that have solutions whose stationary covariance coincides with the GP of interest. Further work considered GPs’ infinitely differentiable in mean square whose power spectral density is an analytic function; use of Pade approximations facilitated forming approximate SSMs for the purpose of posterior inference (Karvonen and Sarkka, 2016). Building more on these concepts later works were able to determine an SDE parameterization for periodic covariances, leverage the SSM representation in conjuction with approximate inference for fast inference in non-conjugate models, and used infinite horizon updates of the Kalman filter and Rauch-Tung-Striebel (RTS) smoother to ameliorate computation time in models with higher dimensional latent spaces (Solin and Särkkä, 2014; Chang et al., 2020; Solin et al., 2018). In Samo and Roberts (2015a) generalized spectral mixture kernels were explored which include the functional form identical to the Hida-Matérn kernel, under the name Spectral Matérn kernel. However, they did not touch upon the criticial implication that the Hida-Matérn kernel forms a complete basis over finitely differentiable and stationary GPs. In addition, the authors extended upon that work in Samo and Roberts (2015b) where they explore consequences of the GP Markov property, but only in the restricted sense. Only exploring the Markov property in the restricted sense leaves open questions about how the Markov property can be explained or reasoned about once GPs are added together or more pathological cases where differentiability of the GP arise.

9 SSMs for GPs with Multivariate Input

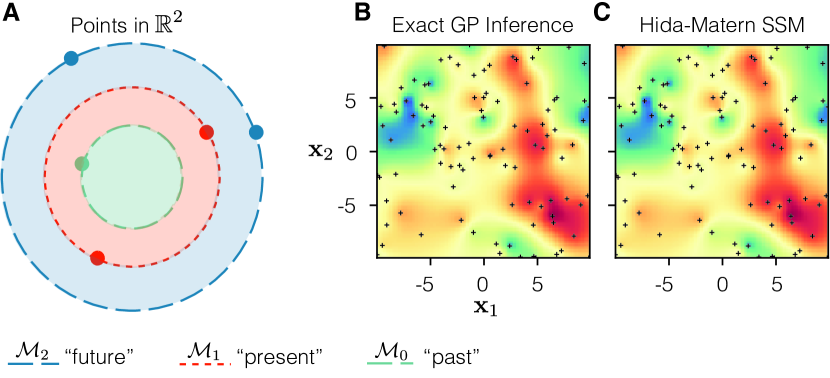

Thus far we have explored the SSM representation for GPs where the index variable is a scalar. In this setting defining an ordering over the index variable that defines a Markov property is simple and intuitive; at time if then is the future of the process while if then is the past. When we consider with it is not immediately obvious how to similarily define an appropriate Markov property for elements of .

In Pitt (1971), explored was the notion of a GP Markov property where the index variable is not a scalar. Let , be dimensional manifolds in dimensional euclidian space such that if and then . Note that with concentric manifolds defined as such that we must have . Intuitively then, we can see how notions of ‘past’ and ‘future’ might be defined by viewing observations laying along any of as the past with respect to .

Hence, if we have points laying in dimensional space it is easy to define concentric series of manifolds with so that for a simple Gaussian Markov process . To lay down some notation, define a differential operator , taken to mean , with and each such that .

Let’s play the same game as we did in the univariate case and see how we can take advantage of Pitt’s Markov property to achieve fast inference when the index variable is no longer scalar. Going back to our favorite Matérn , its multivariate analogue is which has three partial derivatives, , , and . Once these partial derivatives are calculated we can then form the multioutput covariance .

| (74) |

from which we have that where . If we extract from via just as in the scalar input case, then all we have discussed so far carries over quite easily; for example, we could form the standard generative model and easily perform GP regression in the case we have observations that can be modeled as where is Gaussian noise.

In Fig. 7 we can see the result of performing posterior inference over with the two dimensional input Matérn with exact GP inference as well as the SSM formulation. Inspecting the posterior mean, we can see that the posterior under the SSM formulation is faithful to the posterior under exact GP inference. One downside to performing spatial inference in this manner is that observations will need to be sorted according to the norm of their location; however, even with sorting and making use of Kalman filtering/smoothing the computational cost is still minute compared to naive GP inference.

It is worthwhile noting for historical purposes that there are works outside of Pitt’s that consider a Markov property for Gaussian random fields with multidimensional support. Preceding Pitt’s work is that of McKean (1963) who like Levy explores the characterization of a Markovian property for processes with an odd dimensional index variable, albeit taking a different approach. It is Pitt’s work that builds on McKean’s by succesfully characterizing the Markov property of random fields with a support of arbitrary dimension. Mentions of these works as well as others exploring a Markov property for processes with multidimensional index are briefly summarized in the text of Adler (2010, Appendix). Hida in pursuit of a general theory for representation of white noise processes also considered those defined over a multivariate domain, the curious reader can consult the text Hida and Si (2004) for a fully fleshed out presentation similar to that of his theory of canonical representations of univariate GPs. Also worth mentioning is the paper, Lee (1990), that goes more in depth with regards to functional forms of covariance kernels over manifold domains.

10 Experiments

10.1 Mauna Loa Carbon Dioxide

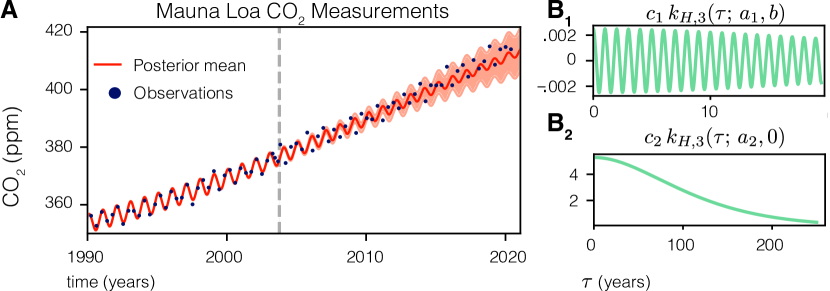

Here, we examine the predictive capabilities and expressivity of the Hida-Matérn family by applying it to the popular Mauna Lua dataset (Rasmussen and Williams, 2005). The long upward trend present in this data as well as the yearly periodic component mean that an appropriate linear combination of Hida-Matérn kernels will need to be constructed. To demonstrate that a low order SSM is sufficient for this dataset we construct a simple kernel that is the sum of two order Hida-Matérns, i.e.

with , , , and , , i.e. one kernel which is decaying periodic with a short lengthscale to capture the yearly periodic trend and another which is not periodic with a long lengthscale to capture the linear trend. This setup is similar to those commonly used in the literature, where the first additive kernel would usually be a Matérn/Squared Exponential multiplying the periodic covariance function (Rasmussen and Williams, 2005; Corenflos et al., 2021; Solin and Särkkä, 2014).

The GP is fit using the data from 1974-2004, and predictions are made for the time window from 2004-2020 as shown in Fig. 8. From the fit, we can see that the sum of these two low order Hida-Matérn kernels form a covariance function such that the resulting GP inference can make predictions that capture both the seasonal and linear trends in the data.

10.2 Scalability of SSM representation

From a practical standpoint, one of the most useful implications that arises from the -ple GP Markov characterization is the ability to quickly formulate a corresponding state-space model amenable for inference. As a result, it is trivial to form appropriate state-space models that can be used to recover exact GP inference over large datasets where naive GP regression would be impractical due to the cubic scaling of the computational complexity.

We now consider a toy dataset containing 50,000 observations, with uniform spacing of 0.05, that are generated according to a prior GP whose covariance function is the sum of two spectral mixture kernels, i.e., (Wilson and Adams, 2013)

| (75) | ||||

| (76) |

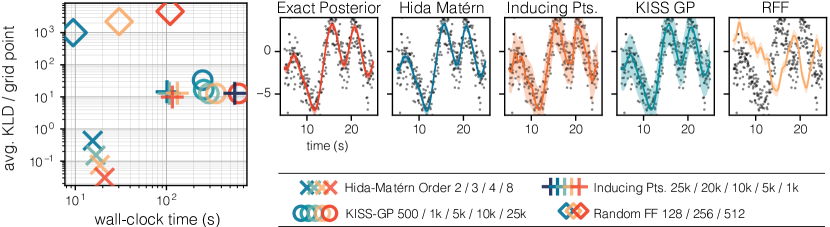

where the hyperparameters are , , , and , , . For comparison, we consider SVGPR, KISSGP, as well as random Fourier features (Titsias, 2009; Wilson and Nickisch, 2015; Rahimi and Recht, 2007). Experiments for SVGPR and KISSGP are ran using GPyTorch with all hyperparameter optimization done before computing the wall-clock time of the calculation for the posterior distribution over the grid (Gardner et al., 2018). To subserviate any numerical difficulties that would arise from calculating the KLD between the posterior under each method and exact GP inference we instead consider the average KLD per grid point, or average marginalized KLD.

As the data points are distributed on a uniform grid we expect that inference using the SSM and Hida-Matérn kernels should be the fastest as only need be computed once. Indeed, this is the case and it also has the lowest marginal KLD to the true posterior even though there is a model mismatch (as the Spectral Mixture is only an asymptote of the Hida-Matérn family).

11 Conclusion

We showed how viewing GPs through the lens of their Markov property has both theoretical and practical consequences. We reintroduced results from Hida that all finitely differentiable stationary GPs are Markovian and their kernel must admit a decomposition in terms of linear combinations of the derived Hida-Matérn kernels. As a consequence, Hida-Matérn GPs can be simply rewritten as a linear Gaussian state-space model. The SSM representations enabled us to make exact GP inference in linear time for any 1-dimensional stationary GP whose kernel is in the Hida-Matérn family. As a by product of the admitted SSM representation, we also fleshed out connections to SDEs whose solutions are GPs, showing that the fundamental matrix solution of those systems has a closed form representation. Finally, we showed many commonplace kernels either reside directly within the Hida-Matérn family or can be seen as appropriate asymptotic limits. The Hida-Matérn kernel provides a unifying framework that bridges linear models used in the statistical signal processing literature and the nonlinear kernel methods in the machine learning literature.

References

- Adler (2010) Robert J Adler. The Geometry of Random Fields. Society for Industrial and Applied Mathematics, January 2010. doi: 10.1137/1.9780898718980. URL https://doi.org/10.1137/1.9780898718980.

- Anderson and Moore (1979) Brian D. O Anderson and John B Moore. Optimal Filtering. Prentice-Hall, Englewood Cliffs, N.J., 1979. ISBN 978-0-13-638122-8.

- Bateman (1954) Harry Bateman. Tables of Integral Transforms Volume 1. Bateman Manuscript Project. McGraw-Hill, 1st edition, 1954. URL https://books.google.com/books?id=HfZQAAAAMAAJ.

- Bui et al. (2017) Thang D Bui, Cuong Nguyen, and Richard E Turner. Streaming sparse gaussian process approximations. In I. Guyon, U. V. Luxburg, S. Bengio, H. Wallach, R. Fergus, S. Vishwanathan, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 30. Curran Associates, Inc., 2017. URL https://proceedings.neurips.cc/paper/2017/file/f31b20466ae89669f9741e047487eb37-Paper.pdf.

- Chang et al. (2020) Paul E. Chang, William J. Wilkinson, Mohammad Emtiyaz Khan, and Arno Solin. Fast variational learning in state-space gaussian process models. CoRR, abs/2007.04731, 2020. URL https://arxiv.org/abs/2007.04731.

- Corenflos et al. (2021) Adrien Corenflos, Zheng Zhao, and Simo Särkkä. Temporal Gaussian Process Regression in Logarithmic Time. arXiv:2102.09964 [cs, stat], May 2021.

- Dolph and Woodbury (1952) C. L. Dolph and M. A. Woodbury. On the relation between green’s functions and covariances of certain stochastic processes and its application to unbiased linear prediction. Transactions of the American Mathematical Society, 72(3):519–519, March 1952. doi: 10.1090/s0002-9947-1952-0050215-4. URL https://doi.org/10.1090/s0002-9947-1952-0050215-4.

- Doob (1944) J. L. Doob. The elementary gaussian processes. The Annals of Mathematical Statistics, 15(3):229–282, September 1944. doi: 10.1214/aoms/1177731234. URL https://doi.org/10.1214/aoms/1177731234.

- Gardner et al. (2018) Jacob Gardner, Geoff Pleiss, Kilian Q Weinberger, David Bindel, and Andrew G Wilson. Gpytorch: Blackbox matrix-matrix gaussian process inference with gpu acceleration. In S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018. URL https://proceedings.neurips.cc/paper/2018/file/27e8e17134dd7083b050476733207ea1-Paper.pdf.

- Hartikainen and Sarkka (2010) Jouni Hartikainen and Simo Sarkka. Kalman filtering and smoothing solutions to temporal Gaussian process regression models. In 2010 IEEE International Workshop on Machine Learning for Signal Processing, pages 379–384. IEEE, 2010. ISBN 978-1-4244-7875-0. doi: 10.1109/MLSP.2010.5589113. URL http://ieeexplore.ieee.org/document/5589113/.

- Hida (1960) Takeyuki Hida. Canonical representations of Gaussian processes and their applications. Memoirs of the College of Science, University of Kyoto. Series A: Mathematics, 33(1):109 – 155, 1960. doi: 10.1215/kjm/1250776062. URL https://doi.org/10.1215/kjm/1250776062.

- Hida and Hitsuda (1993) Takeyuki Hida and Masuyuki Hitsuda. Gaussian Processes. American Mathematical Society, 1993.

- Hida and Si (2004) Takeyuki Hida and Si Si. An Innovation Approach to Random Fields. WORLD SCIENTIFIC, July 2004. doi: 10.1142/5046. URL https://doi.org/10.1142/5046.

- Jazwinski (2007) Andrew H Jazwinski. Stochastic Processes and Filtering Theory. Courier Corporation, January 2007. ISBN 9780486462745. URL https://play.google.com/store/books/details?id=4AqL3vE2J-sC.

- Karaletsos and Bui (2020) Theofanis Karaletsos and Thang D Bui. Hierarchical gaussian process priors for bayesian neural network weights. In H. Larochelle, M. Ranzato, R. Hadsell, M. F. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 17141–17152. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper/2020/file/c70341de2c112a6b3496aec1f631dddd-Paper.pdf.

- Karvonen and Sarkka (2016) Toni Karvonen and Simo Sarkka. Approximate state-space gaussian processes via spectral transformation. In 2016 IEEE 26th International Workshop on Machine Learning for Signal Processing (MLSP). IEEE, September 2016. doi: 10.1109/mlsp.2016.7738812. URL https://doi.org/10.1109/mlsp.2016.7738812.

- Kohn and Ansley (1987) Robert Kohn and Craig F. Ansley. A new algorithm for spline smoothing based on smoothing a stochastic process. SIAM Journal on Scientific and Statistical Computing, 8(1):33–48, January 1987. doi: 10.1137/0908004. URL https://doi.org/10.1137/0908004.

- Kosambi (1943) D. D. Kosambi. Statistics in function space. In D.D. Kosambi, pages 115–123. Springer India, 1943. doi: 10.1007/978-81-322-3676-4˙15. URL https://doi.org/10.1007/978-81-322-3676-4_15.

- Krämer and Hennig (2020) Nicholas Krämer and Philipp Hennig. Stable implementation of probabilistic ode solvers, 2020.

- Kuss and Rasmussen (2005) Malte Kuss and Carl Edward Rasmussen. Assessing approximate inference for binary gaussian process classification. Journal of Machine Learning Research, 6(57):1679–1704, 2005. URL http://jmlr.org/papers/v6/kuss05a.html.

- Lee (1990) Ke-Seung Lee. White noise approach to gaussian random fields. Nagoya Mathematical Journal, 119:93–106, September 1990. doi: 10.1017/s0027763000003135. URL https://doi.org/10.1017/s0027763000003135.

- Loper et al. (2021) Jackson Loper, David Blei, John P. Cunningham, and Liam Paninski. Linear-time inference for gaussian processes on one dimension, 2021.

- Lévy (1951) Paul Lévy. Wiener’s Random Function, and Other Laplacian Random Functions. Proceedings of the Second Berkeley Symposium on Mathematical Statistics and Probability, pages 171–187, 1951. URL https://projecteuclid.org/ebooks/berkeley-symposium-on-mathematical-statistics-and-probability/Proceedings-of-the-Second-Berkeley-Symposium-on-Mathematical-Statistics-and/chapter/Wieners-Random-Function-and-Other-Laplacian-Random-Functions/bsmsp/1200500228.

- Lévy (1956) Paul Lévy. A special problem of brownian motion, and a general theory of gaussian random functions. In Jerzy Neyman, editor, Contributions to Probability Theory, pages 133–176. University of California Press, 1956. ISBN 978-0-520-35067-0. doi: 10.1525/9780520350670-013. URL https://www.degruyter.com/document/doi/10.1525/9780520350670-013/html.

- McKean (1963) H. P. McKean, jr. Brownian motion with a several-dimensional time. Theory of Probability & Its Applications, 8(4):335–354, 1963. doi: 10.1137/1108042. URL https://doi.org/10.1137/1108042.

- Ng et al. (2018) Yin Cheng Ng, Nicolò Colombo, and Ricardo Silva. Bayesian semi-supervised learning with graph gaussian processes. In S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018. URL https://proceedings.neurips.cc/paper/2018/file/1fc214004c9481e4c8073e85323bfd4b-Paper.pdf.

- Nordsieck (1962) Arnold Nordsieck. On Numerical Integration of Ordinary Differential Equations. Mathematics of Computation, 16(77):22–49, 1962. ISSN 0025-5718. doi: 10.2307/2003809.

- Oksendal (1992) Bernt Oksendal. Stochastic Differential Equations (3rd Ed.): An Introduction with Applications. Springer-Verlag, 1992. ISBN 3387533354.

- Oppenheim and Schafer (2014) Alan V. Oppenheim and Roland W. Schafer. Discrete-Time Signal Processing. Prentice Hall Signal Processing Series. Pearson, 3rd edition, 2014. ISBN 978-1-292-02572-8.

- Osborne (1966) M. R. Osborne. On Nordsieck’s method for the numerical solution of ordinary differential equations. BIT Numerical Mathematics, 6(1):51–57, 1966. ISSN 1572-9125. doi: 10.1007/BF01939549. URL https://doi.org/10.1007/BF01939549.

- Pitt (1971) Loren D Pitt. A Markov property for Gaussian processes with a multidimensional parameter. Arch. Rational Mech. Anal. Archive for Rational Mechanics and Analysis, 43(5):367–391, 1971. ISSN 0003-9527.

- Posa (2021) Donato Posa. Models for the difference of continuous covariance functions. Stochastic Environmental Research and Risk Assessment, 35(7):1369–1386, February 2021. doi: 10.1007/s00477-020-01947-1. URL https://doi.org/10.1007/s00477-020-01947-1.

- Proakis and Manolakis (2007) John G. Proakis and Dimitris G. Manolakis. Digital Signal Processing. Pearson Prentice Hall, 4th ed edition, 2007. ISBN 978-0-13-187374-2.

- Rahimi and Recht (2007) Ali Rahimi and Benjamin Recht. Random features for large-scale kernel machines. In Proceedings of the 20th International Conference on Neural Information Processing Systems, NIPS’07, pages 1177–1184, Red Hook, NY, USA, 2007. Curran Associates Inc. ISBN 9781605603520.

- Rasmussen and Williams (2005) Carl E Rasmussen and Christopher K I Williams. Gaussian Processes for Machine Learning. Adaptive Computation and Machine Learning. The MIT Press, November 2005. ISBN 9780262182539.

- Rudin (1991) Walter Rudin. Functional Analysis. McGraw-Hill, Inc, 1991. ISBN 978-0-07-054236-5 978-0-07-100944-7 978-7-111-13415-2 978-0-07-061988-3.

- Samo and Roberts (2015a) Yves-Laurent Kom Samo and Stephen Roberts. Generalized Spectral Kernels. 2015a. URL http://arxiv.org/abs/1506.02236.

- Samo and Roberts (2015b) Yves-Laurent Kom Samo and Stephen J. Roberts. p-markov gaussian processes for scalable and expressive online bayesian nonparametric time series forecasting, 2015b.

- Särkkä (2011) Simo Särkkä. Linear operators and stochastic partial differential equations in gaussian process regression. In Artificial Neural Networks and Machine Learning – ICANN 2011, pages 151–158. Springer Berlin Heidelberg, 2011. doi: 10.1007/978-3-642-21738-8“˙20. URL http://dx.doi.org/10.1007/978-3-642-21738-8_20.

- Solin (2016) A Solin. Stochastic Differential Equation Methods for Spatio-Temporal Gaussian Process Regression. PhD thesis, Aalto University, 2016.

- Solin and Särkkä (2014) Arno Solin and Simo Särkkä. Explicit Link Between Periodic Covariance Functions and State Space Models. In Samuel Kaski and Jukka Corander, editors, Proceedings of the Seventeenth International Conference on Artificial Intelligence and Statistics, volume 33 of Proceedings of Machine Learning Research, pages 904–912, Reykjavik, Iceland, 22–25 Apr 2014. PMLR. URL http://proceedings.mlr.press/v33/solin14.html.

- Solin et al. (2018) Arno Solin, James Hensman, and Richard E Turner. Infinite-horizon gaussian processes. In S. Bengio, H. Wallach, H. Larochelle, K. Grauman, N. Cesa-Bianchi, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc., 2018. URL https://proceedings.neurips.cc/paper/2018/file/b865367fc4c0845c0682bd466e6ebf4c-Paper.pdf.

- Stein (1999) Michael L. Stein. Interpolation of Spatial Data. Springer Series in Statistics. Springer New York, 1999. ISBN 978-1-4612-7166-6 978-1-4612-1494-6. doi: 10.1007/978-1-4612-1494-6. URL http://link.springer.com/10.1007/978-1-4612-1494-6.

- Strang and MacNamara (2014) Gilbert Strang and Shev MacNamara. Functions of difference matrices are toeplitz plus hankel. SIAM Review, 56:525–546, 08 2014. doi: 10.1137/120897572.

- Särkkä and Solin (2019) Simo Särkkä and Arno Solin. Applied Stochastic Differential Equations. Cambridge University Press, 1 edition, 2019. ISBN 978-1-108-18673-5 978-1-316-51008-7 978-1-316-64946-6. doi: 10.1017/9781108186735. URL https://www.cambridge.org/core/product/identifier/9781108186735/type/book.

- Titsias (2009) Michalis Titsias. Variational learning of inducing variables in sparse gaussian processes. In David van Dyk and Max Welling, editors, Proceedings of the Twelfth International Conference on Artificial Intelligence and Statistics, volume 5 of Proceedings of Machine Learning Research, pages 567–574, Hilton Clearwater Beach Resort, Clearwater Beach, Florida USA, 16–18 Apr 2009. PMLR. URL http://proceedings.mlr.press/v5/titsias09a.html.

- Tobar (2019) Felipe Tobar. Band-limited gaussian processes: The sinc kernel. In H. Wallach, H. Larochelle, A. Beygelzimer, F. d’Alché Buc, E. Fox, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc., 2019. URL https://proceedings.neurips.cc/paper/2019/file/ccce2fab7336b8bc8362d115dec2d5a2-Paper.pdf.

- Wahba (1978) Grace Wahba. Improper priors, spline smoothing and the problem of guarding against model errors in regression. Journal of the Royal Statistical Society: Series B (Methodological), 40(3):364–372, July 1978. doi: 10.1111/j.2517-6161.1978.tb01050.x. URL https://doi.org/10.1111/j.2517-6161.1978.tb01050.x.

- Weinert and Sidhu (1978) H. Weinert and G. Sidhu. A stochastic framework for recursive computation of spline functions–part i: Interpolating splines. IEEE Transactions on Information Theory, 24(1):45–50, 1978. doi: 10.1109/TIT.1978.1055825.

- Weinert et al. (1980) H. L. Weinert, R. H. Byrd, and G. S. Sidhu. A stochastic framework for recursive computation of spline functions: Part II, smoothing splines. Journal of Optimization Theory and Applications, 30(2):255–268, February 1980. doi: 10.1007/bf00934498. URL https://doi.org/10.1007/bf00934498.

- Wilson and Adams (2013) A Wilson and R Adams. Gaussian process kernels for pattern discovery and extrapolation. International conference on machine, 2013. URL http://proceedings.mlr.press/v28/wilson13.html.

- Wilson and Nickisch (2015) Andrew Wilson and Hannes Nickisch. Kernel interpolation for scalable structured gaussian processes (KISS-GP). In Francis Bach and David Blei, editors, Proceedings of the 32nd International Conference on Machine Learning, volume 37 of Proceedings of Machine Learning Research, pages 1775–1784, Lille, France, 2015. PMLR. URL http://proceedings.mlr.press/v37/wilson15.html.

- Álvarez and Lawrence (2011) Mauricio A. Álvarez and Neil D. Lawrence. Computationally Efficient Convolved Multiple Output Gaussian Processes. Journal of Machine Learning Research, 12(41):1459–1500, 2011. URL http://jmlr.org/papers/v12/alvarez11a.html.

Appendix

A Derivation of the Hida-Matérn kernel starting from the basis of canonical filters

Let be a canonical filter of order , i.e.,

| (77) |

the covariance function, , of a process described with such a canonical filter is

where ∗ denotes complex conjugation. The PSD, , of is related to the fourier transform of so that we have where . For convenience we proceed by working with the Fourier cosine and Fourier sine transforms denoted by

so that (Oppenheim and Schafer, 2014). In general by working with this basis we are not guaranteed that the resulting power spectral density of the covariance function will be real and symmetric. To enforce this constraint the imaginary part of needs to be isolated. Through the Fourier sine and cosine transformations we have

| (78) | ||||

| (79) | ||||

| (80) |

Now, must be isolated. For analytic purposes, this will be more easily achieved by considering the following identity,

| (81) | ||||

With a canonical filter given in the form of Eq. (77) we have that it’s Fourier cosine and sine transforms respectively are given by Bateman (1954).

| (82) | ||||

| (83) |

Thus for the subtractive term in Eq. (81),

| (84) | ||||

| (85) |

and similarily for the additive term in Eq. (81)

| (86) |

Using these expansions Eq. (81) then becomes

which upon some simplification we obtain

| (87) | ||||

| (88) | ||||

| (89) | ||||

| (90) |

where partial fraction simplification was used in the last line (Proakis and Manolakis, 2007). Inspection shows that this PSD is very similar in terms of each summand to the PSD of the Matérn kernel. Substituting and the inverse Fourier transform is easily found.

B Mixture of stationary Hida-Matérn kernels are dense

Theorem (Mixture of stationary Hida-Matérn kernels are dense.).

For any fixed , Hida-Matérn kernels are dense in the space of square integrable functions, hence they are dense with respect to convergence.

Proof.

From Wiener’s Tauberian theorem, we have that if is square integrable then the span of the translations is dense in if and only if the real zeros of the Fourier transform of form a set of Lebesgue measure 0 (Rudin, 1991).

Take a Hida-Matérn kernel, fix and , then let and denote the PSD, or the Fourier transform of as . We can write, . By the frequency shifting property of the Fourier transform we have that .

Furthermore, since is symmetric about the origin, we have that . Recognizing that the second term results in the non-oscillatory Hida-Matérn kernel/Matérn kernel in the time domain now makes it clear that the Fourier transform of is strictly positive and so its real zeros have Lebesgue measure 0.

Now, using Wiener’s Tauberian theorem, we have that that the span of translations of is dense in . So, if we have some square integrable kernel with Fourier transform , then from Wiener’s Tauberian theorem we should be able to find a linear combination of Hida-Matérns such that

| (91) |

However, by now using Parseval’s theorem we also have that

| (92) |

which also means that the class of Hida-Matérn kernels are dense in the space of . ∎

Remark.

We note a similar way of proving pointwise convergence for any stationary, real valued, positive semidefinite kernel modulated by a cosine was used in Samo and Roberts (2015a).

C Stationary Covariance of an -ple Markov GP

Though the fact that the stationary covariance of the continuous time representation of a GP as in Eq. (21) being is intuitive, it is also true that the stationary covariance of the discretized model as presented for standard GP regression is – independent of the spacing of the observations.

Proposition 2.

For state space models as defined, the stationary marginal covariance of the process, , denoted is exactly .

Proof.

The stationary marginal covariance satisfies the discrete Lyapunov equation,

| (93) |

By substituting for and expanding we get that

| (94) |

which can be factored as

| (95) |

Letting gives us that upon whose substition we find

| (96) | ||||

| (97) |

Vectorizing Eq. 97 we now find that

| (98) |

which means that since a unique solution of must exist, then the only possibility is that since its premultiplier is of full rank and has no nullspace. This then means that

| (99) | ||||

| (100) | ||||

| (101) |

giving us the result

| (103) |

Remark 2.

We see that the stationary covariance is invariant to the choice of , as such we could have used the continuous or discrete lyapunov equations to solve for the stationary covariance. Indeed, plugging in this solution to the continuous time Lyapunov equation is consistent.

∎

D Numerically stable Kalman updates

Taking advantage of the sparsity of the observation extraction vector can also aid in reducing numerical noise by recognizing that its sparsity leads to low rank Kalman updates of the predicted covariance and simplified equations for the updates of the mean.

Kalman Equations Take and to be the mean and covariance prediction at with and to be the updated mean and covariance and . Then with and the Kalman recursions follow

In general we would not use the standard covariance update because numerically it will not guarantee is PSD. With that said, let be the set of indices where has non-zero elements and let’s first expand the equation for

Now take and and we get that

Making it obvious that it is sufficient to work with select columns and elements of and that the update is simply the sum of select scaled columns of .

Let’s do the same for the updated covariance,

Now, it is obvious that the updated covariance consists of subtracting a matrix from which is simply the sum of outer products of select columns of .