Polynomial Time Algorithms to Find an Approximate Competitive Equilibrium for Chores

Abstract

Competitive equilibrium with equal income (CEEI) is considered one of the best mechanisms to allocate a set of items among agents fairly and efficiently. In this paper, we study the computation of CEEI when items are chores that are disliked (negatively valued) by agents, under 1-homogeneous and concave utility functions which includes linear functions as a subcase. It is well-known that, even with linear utilities, the set of CEEI may be non-convex and disconnected, and the problem is PPAD-hard in the more general exchange model. In contrast to these negative results, we design FPTAS: A polynomial-time algorithm to compute -approximate CEEI where the running-time depends polynomially on .

Our algorithm relies on the recent characterization due to Bogomolnaia et al. (2017) of the CEEI set as exactly the KKT points of a non-convex minimization problem that have all coordinates non-zero. Due to this non-zero constraint, naïve gradient-based methods fail to find the desired local minima as they are attracted towards zero. We develop an exterior-point method that alternates between guessing non-zero KKT points and maximizing the objective along supporting hyperplanes at these points. We show that this procedure must converge quickly to an approximate KKT point which then can be mapped to an approximate CEEI; this exterior point method may be of independent interest.

When utility functions are linear, we give explicit procedures for finding the exact iterates, and as a result show that a stronger form of approximate CEEI can be found in polynomial time. Finally, we note that our algorithm extends to the setting of un-equal incomes (CE), and to mixed manna with linear utilities where each agent may like (positively value) some items and dislike (negatively value) others.

1 Introduction

Allocating a set of items among agents in a non-wasteful (efficient) and agreeable (fair) manner is an age old problem extensively explored within economics, social choice, and computer science. An allocation based on competitive equilibria (CE) has emerged as one of the best mechanisms for this problem due its remarkable fairness and efficiency guarantees [AD54, Var74, BMSY17]. The existence and computation of competitive equilibria has seen much work when all the items are goods, i.e. liked (positively valued) by agents. However, when items are chores, i.e. disliked (negatively valued) by agents, the problem is relatively less explored even though it is as relevant in every day life; for example dividing teaching load among faculty, job shifts among workers, and daily household chores among tenants.

In this paper, we study the problem of computing competitive equilibria with equal income (CEEI) [Var74, BMSY17] for chore division, where a set of divisible chores has to be allocated among a set of agents. Agents receive payments for doing chores, and are required to earn a minimum amount, and under equal income, these amounts are the same.333The earning requirement of an agent can also be thought of as her importance/weight compared to others, and thereby under equal income all agents have the same weight. A competitive equilibrium (CE) for chores consists of a payment per-unit for each chore, and an allocation of chores to agents such that every agent gets her optimal bundle, i.e., the disutility-minimizing bundle subject to fulfilling her earning requirement. Typically, agent preferences are represented by a monotone and concave utility function [AD54, BMSY17], that is negative and decreasing in case of chores. Equivalently, we consider disutility functions, namely for agent , that is monotone increasing and convex. We assume disutility functions to be 1-homogeneous as otherwise the problem is known to be intractable [CT09, CGMM20]. We note that 1-homogeneous functions form a rich class that includes the well-studied linear and CES functions as special cases.

The computational complexity of CE is well-understood when items are goods, e.g., [DPSV08, CDDT09, CPY17, VY11, CDG+17, Rub18] (see Section 2 for a detailed discussion): for 1-homogeneous utilities, the famous Eisenberg-Gale [EG59] convex programming formulation and its dual are known to give equilibrium allocation and prices respectively. As a consequence the set of CE is convex, and the ellipsoid and/or interior point methods would find an approximate CE in polynomial-time, assuming utility functions are well-behaved. When utility functions are further restricted to be linear, there are many (strongly) polynomial time combinatorial algorithms known [DPSV08, Orl10], even for the more general exchange model where agents want to exchange items they own to optimize their utilities [DM15, DGM16, GV19].

Although goods and chores problems seem similar, results for chores are surprisingly contrasting: Even in the restricted case of linear disutilities, the set of CEEI can be non-convex and disconnected [BMSY17, BMSY19], and in the exchange model computing a CE is PPAD-hard [CGMM20]. No polynomial time algorithms are known to find CEEI with chores, except for when number of agents or number of chores is a constant [BS19, GM20].444These algorithms are based on enumeration from a cleverly designed set of candidates. Similar approaches are known for goods manna when the number of items or agents is a constant [DK08, GMSV15], while the general case is PPAD-hard even to approximate [CT09, Rub18] We note that the combinatorial approaches known for the goods case [DPSV08, Orl10, Vég12] seem to fail due to disconnectedness of the CEEI set (see Remark 1 for further explanation). In light of these results, computing exact CEEI may turn out to be hard even with linear disutilities, but what about an approximate CEEI?

We resolve the above question by designing an FPTAS for the more general class of 1-homogeneous disutilities. Specifically, we design an algorithm to find -approximate CEEI in time polynomial in and bit-size of the input instance parameters. We remark that many of the above bottlenecks exist even when we focus on approximate CEEI. In particular, the set of approximate CEEI can be non-convex and disconnected. And the fundamental bottleneck in generalizing the combinatorial algorithm explained in Remark 1 still persists. Despite these challenges, we are able to design an FPTAS to find an approximate CEEI, and extend it to more general valuations than linear which includes CES valuation functions.

Our algorithm crucially builds on the characterization of Bogomolnaia et al. [BMSY17], which states that the set of CEEI is exactly the strictly positive local-minima (KKT points) of a non-convex formulation, namely minimize the product of disutilities (equivalently ) over the space of feasible disutility vectors. The set of feasible disutility vectors may not be convex, but they can be made convex by allowing overallocation. Unfortunately, standard interior-point methods for finding local optimum, such as gradient descent, will fail at ensuring the strict positivity constraint, since the gradient of the objective is attracted towards the minimum disutility coordinate. This difficulty is not alleviated by barrier function methods either. A possible fix is to introduce additional constraints to avoid zeros, but then we loose the CEEI characterization.

The above issues would not arise if we maximize instead of minimizing it. Motivated from this observation, we design an exterior-point method that tries to maximize the objective outside of the feasible region, starting from an outside point that is below the lower-hull. However, we are faced with two crucial difficulties: now the outside region is truly non-convex, and we must ensure that we do find a desired local minimum from the inside.

Our exterior-point method handles the above issues by repeatedly guessing candidate solutions, and checking if they are local minima for the problem inside the feasible region by verifying if the gradient is parallel to some supporting hyperplane. If not, it goes on to try another such candidate, while ensuring it is always increasing along the objective function. Thus, the objective acts as a potential function, and we can bound convergence rates by the size of objective improvement at each step. This method may be of independent interest. We terminate search when the supporting hyperplane direction is approximately equal to the gradient, in a multiplicative sense, and argue that such an approximate KKT point suffices to guarantee an approximate CEEI.

The crucial step in each iteration of this procedure is to find the nearest feasible point in the disutility space, which allows us to find a boundary point along with a supporting hyperplane at it. When disutility functions are linear, we argue that both distance minimization and supporting hyperplane computation can be solved exactly, leading to a stronger form of approximate CEEI.

For the case of general 1-homogeneous and convex disutility functions, the nearest feasible point must be found by interior point methods. We assume black-box access to the disutility functions’ value and partial derivatives. This approximate nearest-point computation introduces errors in the local optimum and the supporting hyperplane both, that are tricky to handle. We show how to handle these extra errors by modifying the algorithm, and argue that a slight weakening of approximately competitive equilibria can still be guaranteed. As expected, these guarantees, including successful application of the interior point method, rely on the disutility functions being “well-behaved”, and the running time of the algorithm depends logarithmically on continuity parameters of the disutility functions, namely, the Lipschitz constants for lower-bounding and upper-bounding the partial derivatives.

Extensions. Finally, we argue how our algorithm easily extends to the setting of un-equal income (CE) when max to min income/weight ratios is polynomially bounded. Another natural extension we consider is to mixed manna, where each agent may like some items and dislike others. Again, using the characterization of [BMSY17], every instance can be put into one of the three categories, namely positive, negative, and null. We argue that the instance in the positive category can be solved using the Eisenberg-Gale convex program [EG59], and those in null have a trivial solution. For instances in the negative category, we discuss how our algorithm can be extended with simple modifications.

Linear Disutilities with Infinities. We note that, [CGMM20] that shows PPAD-hardness for the linear exchange model allows an agent to have infinite disutility for some chores indicating they do not have skills to do the chore in a reasonable amount of time. Our algorithm extends to this model as well, since their sufficiency conditions to ensure existence of equilibrium dictates that every component of the bipartite graph between agents and chores with finite disutility edges should be a complete bipartite graph. They show that even CEEI may not exist without this condition, and checking if it exists is NP-hard. Under this condition, it suffices to find CEEI for each of the connected component separately where there are no agent-chore pairs with infinite disutility.

In order to convey the main ideas cleanly we mainly focus on CEEI with chores in what follows, and discuss the extensions to CE and mixed manna at the end of the paper.

1.1 Model and Our Results

In the chore division problem, a set of divisible chores is to be allocated to a set of agents . It is without loss of generality to assume that exactly one unit of each chore needs to be allocated. Agent ’s preferences (over chores) is represented by a non-negative, non-decreasing, and convex disutility function .555Typically, agents’ preferences for chores are represented by non-positive, non-increasing, and concave utility functions since agents dislike chores [BMSY17]. By taking the negation of these utility functions we get non-negative, non-decreasing, convex disutility functions that agents want to minimize. We denote by the fraction of item that is allocated to agent , and we denote . We assume that ’s are 1-homogeneous, i.e.

| (1) |

If is linear, then it is represented by where is the disutility of agent per unit of chore .666If for some pair then chore can be freely allocated to agent , and can be removed. Infinite disutilities can be handled as discussed in the introduction. Equivalently, we write where . We also use to denote the disutility vector .

Competitive equilibrium with equal income (CEEI)

At a CE with chores, payments are linear, and the -th chore pays per unit of the chore assigned. Let denote the vector of payments, and then the payment to agent is . Each agent seeks to minimize their disutility subject to being paid at least 1 unit. We note that, under equal income, the exact value being paid is immaterial so long as all agents get paid the same amount. Prices and allocation are said to be at CEEI if all the chores are fully allocated when every agent consumes her least-disliked bundle with payment at least 1, i.e., an optimal bundle. Formally [Var74, BMSY17]

-

(equal payments) for all agents and we have , and

-

(optimal bundle) for all , we have for all s.t. , and

-

(feasible allocation) for all , we have .

It is known that the set of CEEI may be nonconvex, or even disconnected [BMSY17]. In light of this fact, and the PPAD-hardness of CE in the linear-exchange model [CGMM20], we turn our attention to approximately competitive equilibria. We formalize the notion of -CEEI as follows:

Definition 1.

Prices and allocation are termed a -CEEI for an , if and only if

-

(1)

for all agents and , we have , and

-

(2)

for all , we have and for all such that , and

-

(3)

for all , we have .

It is well known that CEEI satisfy well-sought-after fairness and efficiency notions of envy-freeness and Pareto-optimality respectively. An allocation is said to be envy-free (EF) if every agent prefers their own bundle over that of any other agent. And it is said to be Pareto-optimal (PO) if no other allocation Pareto-dominates it, i.e., there is no feasible allocation such that for all , and for some agent , . In Appendix B we show that an -CEEI allocation approximately guarantees these properties.

Our main contribution in this paper is an FPTAS – a polynomial time algorithm to find an -CEEI where the running time depends polynomially on ; proved formally in Section 5. Informally, lets say that function is -well-behaved if it satisfies Assumption 16 regarding it’s derivatives.

Theorem.

Given black-box access to 1-homogeneous and convex disutilities that are -well-behaved, and also to their partial derivatives, Algorithm 2, finds an -CEEI in time polynomial in , , , and .

We note that our result holds under a weaker assumption than of Assumption 16; discussed briefly in Remark 42. For linear disutilities, we show the following stronger guarantee in Section 4.

Theorem.

Given an instance with linear disutility functions represented by , and an , a stronger -CEEI can be computed in time where no error is incurred in the last two conditions, i.e., that satisfies (1), , and .

More importantly, our algorithm is an exterior point method that builds on tools from continuous optimization to find an approximate KKT point, which may be of independent interest. Next we give an overview of this method and it’s analysis.

1.2 Overview of the Algorithm and Analysis

Our algorithm builds on the following characterization of CEEI due to Bogomolnaia et al. [BMSY17]: Analogous to the convex program of Eisenberg and Gale [EG59], the CEEI in the case of bads are characterized as local minima to the product of disutilities. However, this optimization program is over disutility space, rather than allocation space.

Formally, we let denote the set of feasible allocations, namely

| (2a) | |||

| The disutility space will be the set of all disutility profiles which can be attained over , or | |||

| (2b) | |||

In all that follows, we will distinguish between disutilities as functions and as variables by the upper- and lower-case symbols respectively. When disutility functions are linear, is a polytope. However, for more general convex disutility functions, may not be a convex set. We will remedy this by working instead with the extended feasible region , the Minkowski sum, which we show is convex (Claim 3). This is the set of all disutility profiles which are at least as bad as some feasible profile, i.e., disutility profiles attainable at over-allocations of the chores.

The characterization of Bogomolnaia et al. [BMSY17] states that any disutility profile which is a local minimum (KKT point) to the following non-convex minimization program is the disutility profile of some CEEI, and the prices and allocation of this CEEI can be found by understanding in allocation-space.

Note that minimizing over the set is equivalent to minimizing over the extended set . And the KKT points to this program are equivalent to the KKT points for the minimization of the logarithm of objective, . Hence the above program can equivalently stated as,

| (3) |

Primary difficulty.

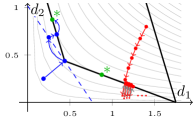

The open constraints are both fundamental to the above characterization, and the source of the main difficulty of the problem. Any disutility profile with a zero coordinate are trivial optima to these minimization problems, but are economically meaningless since no fairness or efficiency properties can be guaranteed. Furthermore, any naïve interior-point attempt at finding local minima are attracted by these constraints: the gradient of the objective at is inversely proportional to componentwise, since . This has the effect of accelerating gradient descent towards the constraint for the smallest value. See Figure 1 (red) for an illustration. This effect is robust to barrier methods at the boundaries, and thus gradient-following methods are not helpful in this task. The same problem afflicts attempts at strengthening the constraint to for some small , as the dual variables for these constraint break the CEEI characterization. We circumvent this issue by designing an iterative exterior-point method that always increases the log-sum .

Remark 1.

A natural question is if the combinatorial methods known for computing CE in linear Fisher (exchange) model with goods, e.g., [DPSV08, Orl10], extend to chores with linear disutilities? Unfortunately, they do not. In particular, the non-convexity and disconnectedness of the CEEI set is a primary difficulty in extending any algorithm from the goods setting to the chores setting. For example, these methods rely on the fact that CE allocation and prices changes continuously with the the (money) endowments of the agents [MV07], which is not true with chores. A chore division instance may have multiple disconnected equilibria some of which may disappear as we change these parameters, and as a result the said methods may get stuck. This fundamental bottleneck persists even if we restrict ourselves to approximate-CEEI.

In the rest of this section, we will outline our approach first for linear disutility functions, and then afterwards in the general case. In the linear setting, many sub-routines can be solved exactly. Thus, it requires less technical detail to present, and serves as a good intuition for the more involved general case that we address later.

1.2.1 Linear Disutilities: Relating Approximate KKT to Approximate CEEI

The main insights of our result are that (1) approximate KKT points allow for approximately competitive equilibria to be constructed, and (2) approximate KKT points can be found, despite the difficulty described above about ensuring strict positivity constraints. We begin here by formally defining the approximate KKT conditions.

Recall, KKT points are local optima where the cone of normal vectors of the tight constraints contains the function’s gradient. Equivalently, there exists a supporting hyperplane at the local optimum whose normal vector is parallel to the function’s gradient. Formally, is a KKT point for the problem if there exists a normal vector such that: is a supporting hyperplane for , and there exists some such that , i.e. for all .

Since our procedure is iterative, it will converge in the limit to a KKT point, but only approximately after finitely many iterations. We show that after a polynomial number of iterations, it finds an approximate KKT point, defined below, with inverse-polynomial error.

Definition 2 (-Approximate KKT).

For , we say a point along with the normal direction is a -KKT point for problem (3) if

-

(1)

, (2) for all , and (3) .

Informally, each entry of is a -approximation of , the gradient of , and is normal to a supporting hyperplane for at . Furthermore, we say is a -KKT point if there exists a vector such that satisfy the above conditions.

Recall, when disutilities are linear, is a linear polytope and is therefore convex. Hence, the above definition need not be defined over , but we introduce it as it will be necessary later.

We outline here the first insight of our result, that approximate local minima give approximate equilibria. In the original analysis of the Eisenberg-Gale program [EG59] for goods, and more notably in the proof of [BMSY17] for chores, the relationship between competitive equilibria and local maxima hinges on the gradient being inversely proportional to the marginal (dis)utility-per-dollar incurred. Intuitively, the KKT conditions enforce that the payment to each agent (in the chores setting) is perfectly balanced by their disutility incurred, and their payment is equal to that of any other player. It can be shown that if some player is paid more, then the KKT conditions are violated. Thus, we can conclude condition (1) of Definition 1, with . Condition (2) is argued using the fact that an agent is only allocated her minimum disutility-per-dollar chores, and (3) is true by definition since the allocation lies in .

To extend this argument to the approximate setting, it suffices to observe that when multiplicative error is introduced in the gradient direction, then this argument suffers only multiplicatively. A -sized error bound in the gradient direction allows for some player to be paid less than the unit, and another more, which allows us to show that -KKT points satisfy condition (1) of Definition 1 with . As above, condition (2) is argued similarly with the same , and condition (3) holds with , again by feasibility. Formally, by extending the argument of Bogomolnaia et al. [BMSY17], we show the following.

Theorem.

Let be a -KKT point for the problem of minimizing subject to , and . Let be any allocation that realizes , i.e. for all . Then there exists payments such that form a stronger -CEEI, where no error is incurred in the last two conditions, i.e., satisfies (1), , and .

Furthermore, when disutilities are linear, the allocation and payments can be computed exactly in polynomial time from the disutility profile and normal vector .

This theorem is proven in Section 4.1, Theorem 4, and the first part of it does not require that the disutilities be linear. However, as we will see below, -KKT points can only be guaranteed when disutilities are linear, and the definitions will need to be modified for the general case. The allocation and prices can be efficiently computed when disutilities are linear because they are the solutions to linear feasibility problems. With this theorem in hand, it remains therefore to compute -KKT points, discussed next.

1.2.2 Linear Disutilities: Exterior Point Methods for Approximate KKT Points.

Here we discuss our approach to find approximate-KKT point in polynomial time; formal details are presented in Section 4.2. As discussed above, it is tempting to hope that interior-point methods will find local minima efficiently, but they will not work in this setting. Instead, we will rely on the geometry of the feasible space and objective function to allow us to repeatedly make guesses at KKT points, all the while increasing along the objective , which we treat as a potential function. This potential will ensure that if we do not find approximate KKT points, then we make significant progress, dependent on the degree of precision needed. By bounding the values that the potential can take, this will suffice to show that the procedure is an FPTAS. Refer to Figure 1 (blue) for a pictorial representation of the algorithm.

Our “guesses” at KKT points are made by starting with an exterior, infeasible point , and finding the nearest feasible point to it. Formally, is the solution to . Using the fact that it is the nearest point to in the sense, we show that is normal to a supporting hyperplane for at (Lemma 8). Notice that, so long as componentwise, then this all still holds when replacing with . Furthermore, this will ensure that we are increasing along the potential .

It remains to find the start of the next iterate, while ensuring that we are increasing in the direction. Note that we have that the hyperplane is supporting for , and therefore none of the points on this hyperplane are in the interior of . Thus, we can choose our next starting point to be the -maximizing point on this hyperplane. Since is also feasible, this will ensure that we are increasing in the direction, and that we are starting from a new exterior, infeasible point. This -maximizer on the hyperplane can be found efficiently, since we have a closed form for it: the maximizer on the hyperplane will be the point at which is proportional to , and we show that it is exactly a rescaling of (Claim 11).

Thus, the algorithm is iterative, and each round proceeds as follows:

-

0.

is the infeasible point “lying below” starting the round. is any infeasible point.

-

1.

Set to be the nearest feasible point to , i.e. the solution to .

-

2.

Set , rescaled so that .

-

3.

Define to be , the maximizer of subject to .

-

4.

Stop if is “close enough” to , otherwise repeat.

We initialize the procedure at any infeasible point “lying below” the feasible region. When disutilities are linear, this can be found by noticing that we can lower-bound the disutilities over the feasible region, and picking an allocation which assigns half of the lower bound to each agent (Claim 9). The normalization in Step 2 ensures that if is approximately parallel to the gradient , then it is also of the right magnitude. The notion of “close enough” in Step 4 is multiplicative, as it measures increase in the potential function .

The Potential Function, and Convergence Rates.

As discussed above, we wish to use as a potential function to measure the progress of the algorithm. For each iteration , we will have (Claim 11). This first inequality is due to the observation that the nearest feasible point to Pareto dominates it, and is monotone increasing in each coordinate. The second inequality is by construction, as we show that maximizes on a hyperplane that contains .

It remains then to argue that progress along is rapid, relative to its range. We noted above that the stopping condition in Step 4 is multiplicative. Formally, we stop when the norm of the logarithmic difference, i.e. is at most . When this log-distance is more than , we show that the objective increases by at least (Lemma 12).

Conversely, when this log-distance is upper-bounded by , we will show that form a -KKT point (Lemma 10). Thus, since it is reasonable to bound over the feasible region, we will be able to bound the maximum number of iterations as a polynomial in , , and . This allows us to argue that an approximate equilibrium may be found in polynomially many iterations.

Implementing Iterations in Polynomial Time.

We have argued above that an approximate KKT point, and therefore an approximate equilibrium, can be found in polynomially many iterates of the exterior point method. However, it remains to show that each step can be solved efficiently.

With the exception of Step 1 above, the rest of the algorithm is arithmetic, which can be easily performed. The minimization problem in Step 1 may pose a problem in general, if we expect an exact minimum. This is the source of the extra care needed in the general case. However, in the case of linear disutilities, we show that the minimization problem is actually a quadratic program with a semidefinite bi-linear form over space (Lemma 14), and methods for finding exact solutions to such programs have long been known [KTK80].

Finally, we note that although each step in our algorithm generates polynomial sized rational numbers wrt it’s parameters, one needs to be careful about how their bit-sizes grow. This can be taken care of by rounding down the to a nearest rational vector with polynomial bit-size at the end of each iteration. Note that this step will ensure that lies below and we also argue why the bound on the iterations still hold: Since at every iteration of our algorithm, the value of each can be lower bounded using the value of the potential at and the upper bound on the maximum disutility values in ,777Note that we start with a where each agent has a non-negligible disutility, and at any point in time, the disutilities of the agents in are upper-bounded (as the disutility vector lies below ), implying that there cannot be a significant increase in the disutility of any agent throughout the algorithm. Also, since the sum of logs of the disutilities is increasing throughout the algorithm, we can conclude that there cannot be a significant decrease in the disutility of any agent throughout the algorithm, implying that the disutilities in are also lower bounded. such a rounding is possible without hitting the boundary, and while ensuring at least increase in the potential . However, to convey the main important technical ideas, in Section 4 we focus on bounding number of arithmetic operations. And we note that the analysis of Section 5 for the general case is robust to such a rounding.

Putting all the above together, we get an FPTAS to compute stronger approximate CEEI where the last two conditions of -CEEI are satisfied with (Theorem 15).

1.2.3 General 1-Homogeneous Disutilities

In general, the disutility functions are 1-homogeneous and convex, and are given as a value oracle black-box, along with a value oracle for their partial derivatives. In this section we outline the new issues that arise in extending our algorithm, and their resolutions; see Section 5 for formal details.

At a high-level the issues are as follows: First, to find the nearest points we need to employ interior point methods which returns approximate solutions, and in turn we incur error in the hyperplane as well as the gradient. Secondly, in order to use the interior point method, we will have to work in the allocation space and can not work with the disutility space directly. This causes problems as convex constraints in disutility space need not be convex in allocation space. We elaborate these two issues and also highlight how we overcome them. Finally, we give an overview of the entire algorithm by putting everything together.

Finding Approximate Nearest Point.

Recall, we have defined . The natural program to find the nearest point in to a point below (or equivalently outside ) requires finding a that minimizes , where . Unfortunately the objective function is not necessarily convex888The natural sufficient condition for composition of two convex functions to be convex is if the outer function is monotone in the variables. We do not have this with our current objective function.. One way to ensure it’s convexity is to put additional constraints of the form for all . But again, since the disutility functions are convex, these constraints create non-convex feasible region.

We come up with an alternative formulation for finding the approximate nearest point which is convex. The crucial observation is the fact that given any point outside there exists no point , such that Pareto-dominates(coordinate-wise larger or equal) , i.e., does not belong in the negative orthant centered at . Therefore, a point can Pareto-dominate any point if and only if . We now show how to use this fact to come up with a convex program to find the nearest point in . Our goal is to find a vector of smallest magnitude and a point such that the point Pareto-dominates : Note that this is only possible when . Since is minimum, is the nearest point in to . Formally,

It is easy to verify that the above program minimizes a convex function over a convex domain. The above convex program returns point such that is the nearest point in to . Unfortunately, this program cannot be solved exactly in polynomial time and therefore we need to argue about how to extract an approximate-CEEI given an approximate nearest neighbour.

Approximate Supporting Hyperplane and -KKT Points.

In polynomial time, we can only find an approximate nearest neighbour of a point in . Therefore, our supporting hyperplanes will also be approximate, and therefore we need to redefine the approximate KKT points that we can compute. Let be the nearest point in to . Then, is normal to a supporting hyperplane of at , i.e., is a supporting hyperplane of at . Since we have access only to an approximate nearest neighbour of , say , we wish to have as an approximate supporting hyperplane, i.e. for all for a sufficiently small .

With this, we introduce the notion of -KKT points.

Definition 3 (-Approximate KKT).

We say , i.e., a point along with the normal direction and a pre-image is a -KKT point with , , and , for the minimization problem on if

-

1.

for all and , and for all ,

-

2.

and for all , and

-

3.

and .

Informally, all chores are almost fully allocated, each entry of is a -approximation of , the gradient of , and is a -approximately-supporting hyperplane for .

In Section 5.1, we show that a -KKT point with where , and can be mapped to a -CEEI. The proof emulates the proof in [BMSY17], and consequently matches the proof in the linear case.

However, some subtle problems arise when generalizing the algorithm from the linear case to determine a -KKT point. Firstly, the convergence of the entire algorithm relies crucially on the fact that the potential never decreases at any point. For this, we require that we have Pareto-dominate . We can ensure this by first computing an arbitrary approximate nearest point and then increase the consumption of certain chores in to get such that Pareto-dominates . Since we know that Pareto-dominates , and is small, the increase in consumption of the chores will also be small (Observations 23 and 24).

Secondly, the hyperplane can be a good approximation of the hyperplane (or equivalently is inverse-exponentially small) only if is significantly larger than . Therefore, if at any point in our algorithm, we have for a sufficiently large , where , then we stop and return a pre-image of (note that as the disutility functions are -homogeneous, this can be done by appropriately scaling the consumption of chores for each agent).

Finally, and most importantly, we need to ensure that the approximate supporting hyperplanes do not introduce point with excessive over-allocation. Let and represent the hyperplanes and respectively after appropriate scaling, i.e., for . Since we are dealing with approximate supporting hyperplane999 for all , where ., the point maximizing , say on , maybe contained in the strict interior of . Also note that in this case, the nearest point in to is itself, and therefore the distance between and its approximate nearest point in is significantly smaller than and our algorithm will return the point , the normal to the hyperplane and its pre-image, say in the very next iteration. Now note that while conditions (2) and (3) in Definition 3 are satisfied, condition (1) may not be satisfied. In particular, there could be chores that are significantly over-allocated! At first this may seem to be counter-intuitive as the hyperplane is a good approximation of the exact supporting hyperplane , and, the point that maximizes on lies outside and as a result no chores are over allocated in a pre-image of . However, we show that the disutility profiles of the point maximizing on the hyperplane and the point maximizing on the hyperplane can be very far apart even if is small101010In fact will be small as is significantly small.. This is primarily due to the fact that and , and even though for all , and can be very far apart. We circumvent this issue by showing that if there are some chores that are significantly over-allocated in , then we can find an allocation from by reducing consumption of the over-allocated chores and re-allocating some of the not-over-allocated chores such that and , which is a contradiction to the fact that is an approximate supporting hyperplane to . This is where the bulk of the error analysis is required (summarized in Lemmas 28 and 34).

We now outline the entire procedure.

Putting it Together.

Similar to the case with linear disutilities, the algorithm is iterative. In each iteration ,

-

0.

is the infeasible point “lying below” at the start of round . is any infeasible point.

-

1.

Find such that is an -approximate nearest feasible point to in , s.t. for all and then round up to the nearest rational point with polynomial bit size.

-

2.

If , then return where is a pre-image of obtained by rescaling appropriately, i.e., for all .

-

3.

Set , rescaled so that .

-

4.

Define to be , the maximizer of subject to .

-

5.

Return if is “close enough” to , otherwise repeat.

The algorithm has polynomially many iterations, since similar to the case when agents have linear disutilities, if it does not terminate in iteration , then the potential increases by at least . And is upper bounded. By arguing that every iteration can be done in polynomial time in Section 5.3, we get an FPTAS in Theorem 41.

1.3 Organization

We give a brief road map of the rest of the paper. In what follows, we first discuss some related work on CE in Section 2 and state some fundamental results from [BMSY17] that we use crucially for our algorithm design in Section 3 . Thereafter, we present the FPTAS when agents have linear disutilities in Section 4 so that the reader gets a good idea of the meta-level algorithm. Finally, in Section 5 we discuss the FPTAS when agents have general 1-homogeneous disutilities. In section 6, we discuss the extensions of our results to the setting when the items to be divided contain both goods and bads (mixed manna) with linear valuations, and when agents have unequal income needs (CE in Fisher model).

2 Related Work

Competitive equilibrium (CE) has been a fundamental concept in several economic models since the time of Léon Walras [Wal74] in the 19th century. In this paper, we primarily focus on CEEI, which is a special case of CE in Fisher markets, which again is a special case of CE in exchange markets (also referred to as Arrow-Debreu markets). The existence of CE under some mild assumption was proved in the exchange setting by Arrow and Debreu [AD54] and independently by Mackenzie [McK54, McK59]. However, the proofs of existence used fixed point theorems and were non-constructive. In the last few decades, there has been substantial contribution from the computer science community in coming up with constructive algorithms to determine a CE. As mentioned in the introduction, there has been a long line of convex programs, interior point and combinatorial polynomial time algorithms for determining CE with goods in both Fisher and the exchange setting [CDG+17, DGV16, NP83, DPSV08, Orl10, Vég12, DM15, DGM16, GV19, CCD13]. There are also hardness results known when agents have more general utility functions [CPY17, CDDT09, CT09, Rub18]. The existence and computational complexity of CE and its relaxations have been studied in discrete settings (with indivisible objects) as well [FGL16].

The study of CE with chores/ bads has not received similar extensive investigation. One plausible reason could be that this does not capture a natural market and such a setting is interesting only from a fair division perspective. Nevertheless, the CE with bads exhibits far less structure than the CE with goods as explained in the introduction. There are polynomial time enumerative algorithms known only when there are constant number of agents or chores [BS19, GM20]. Quite recently, [CGMM21] gave an LCP formulation for determining CEEI with mixed manna (goods and bads) when the utility functions are separable piecewise-linear and concave (SPLC) which includes linear.

3 Preliminaries

Recall the chore division problem formalized in Section 1.1 above: We seek to divide divisible chores among agents with convex, 1-homogeneous disutility functions , through the mechanism of competitive equilibrium with equal income (CEEI). In this section we state a characterization of CEEI and certain properties of the disutility space that are crucial for our results.

In the case of dividing goods, the seminal work of Eisenberg and Gale [EG59] shows that any allocation that maximizes the Nash welfare — or equivalently the geometric mean of the utilities — is at a CEEI. Since the Nash welfare maximization is a convex program, an approximate CEEI can be determined by an ellipsoid algorithm. Unfortunately, in the case of dividing bads, the set of equilibria could be non-convex and therefore one cannot hope for convex program formulation that captures equilibria [BMSY17]. However, a recent result by Bogomolnaia et al. [BMSY17] show a similar, but non-convex formulation for an exact CEEI (Definition 1, with ) with chores. In particular, [BMSY17] show that the conditions of an exact CE hold if and only if the disutility profile is a critical point for the Nash welfare on the boundary of the feasible region. Formally:

Theorem 2 ([BMSY17]).

Let and be the feasible space of allocations and disutility profiles as defined in (2). For some , denote the Nash social welfare as . Then can be achieved by a CEEI if and only if the following conditions all hold: a) , b) , and c) satisfies the KKT conditions for the problem of minimizing on . Equivalently, is on the lower-boundary of , but not on the boundary of , and the gradient is parallel to some supporting hyperplane normal for at the point .

Note that when dis-utilities are linear functions, is a linear polytope, though it need not have an efficient representation. When dis-utilities are general, 1-homogeneous, convex functions, the set need not be convex. However, we next show that is convex, and we will therefore use it as our feasible region in the analysis; see Appendix A for the proof.

Claim 3.

is convex, when the disutility functions are convex.

4 Polynomial-Time Algorithm for -CEEI under Linear Disutilities

In this section we present an algorithm to find an -CEEI in time polynomial in and the size of the input instance, when agents have linear disutility functions. Recall that, the linear function of agent is represented by , or equivalently where .

Our algorithm will ensure a stronger notion of approximation where all the chores are exactly allocated, i.e., condition in Definition 1 is satisfied exactly. For this, the algorithm finds a -KKT point as defined in Definition 2. Let us first discuss how such a KKT point gives a stronger approximate CEEI in the next section, thereby extending Theorem 2.

4.1 Approximate KKT Suffices to get Approximate CEEI

We begin with some notation: as we often use element-wise inverse of a vector, for any two -dimensional vectors and , we denote

Recall that we are interested in finding local minima for the logarithm of the Nash social welfare

| (4) |

Observe that . From Definition 2, recall the -KKT point, , for minimizing on : point on the boundary of , such that it has as a supporting hyperplane for , where approximates coordinate-wise, i.e., .

We emulate here the proof of Bogomolnaia et al. [BMSY17] to show that approximate KKT points give approximate CEEI.

As stated in the overview, we wish to show the following.

Theorem 4.

Let be a -KKT point for the problem of minimizing subject to , and . Let be any allocation that realizes , i.e. for all . Then there exists payments such that form a stronger -CEEI, where no error is incurred in the last two conditions, i.e., satisfies (1), , and .

Furthermore, when disutilities are linear, the allocation and payments can be computed exactly in polynomial time from the disutility profile and normal vector .

Proof.

Let , then it suffices to show that -KKT gives -CEEI since for . Recall we have defined , and sets and are as in (2), namely, the set of feasible allocations and the set of feasible disutility profiles, in general.

Defining and Computing the Allocation and Prices.

Let be the disutility profile of the approximate KKT point. Since and the entries of are positive, then , by minimality. Now, consider any allocation in , such that .

For the second part of the statement of the theorem, we must show that can be computed, as this will be the allocation of the approximate CEEI. In fact, it suffices to find an allocation vector which simultaneously satisfies the non-negativity constraints of , and the linear equality constraints of along with . This can be solved by linear programming techniques in polynomial time.

We wish now to compute the prices at the allocation, for which we will need separating hyperplanes. To this end, define the set . As the disutility functions are convex and continuous, we can conclude that the set is closed, convex, and non-empty for all , since . When disutilities are linear, is in fact a closed half-space, since

Now, because for all , we can conclude that the does not intersect for any . Denote . The set must be only tangent to , since the ’s are continuous, but . See Figure 2 for an illustration. Thus, there exists a half-space which separates the two sets, i.e. , and . Also, note that we must have . Note that when disutilities are linear, we have , and as the hyperplane separating and is .

Finally, we can define the prices at the allocation. Let , and let . See Figure 2 for an illustration of the supporting hyperplanes in and in .

It remains then to show that the allocation and the price vector satisfy the conditions in Definition 1 where the last two are satisfied without any error, since we have argued already that they can be computed efficiently.

Satisfying Condition (1) in Definition 1.

We want to show that for all agents and , we have . But first we make some simple but crucial observations about the price vector .

Claim 5.

We have .

Proof.

for all by definition. Also, since , we can claim that . Observe that is obtained by assigning each chore fully to the agent that has the smallest value for it. Therefore, we have that (by the definition of ). ∎

Now, consider the half-space . We first observe that this half-space is entirely contained in .

Claim 6.

We have .

Proof.

Consider any point . We have . Since for all , we have that , implying that , i.e., . Therefore . ∎

Finally, note that every point is also contained in .

Claim 7.

Consider any . Then .

Proof.

Consider any . We have

Therefore . ∎

Now, we are ready to show that . Assume otherwise and say we have . Then we could replace the allocation as follows: Construct by setting , and . Since , we have . Also note that

since the payment subtracted from agent is equal to the payment added to agent and so .

By Claim 6, we have that . Recall that is a separating half-space between and , i.e., and , implying that for every point we have . Since , we have . However,

| (as ) | ||||

which is a contradiction. The first inequality is due to the definition of -approximate KKT, which dictates that for all .

Satisfying Condition (2) in Definition 1 Exactly (i.e., Condition ).

We want to show that for all , we have for all such that . Let us assume that there exists a such that and . We define a new allocation . First note that as . Therefore . By Claim 6, we have that . Recall that is a separating half-space between and , i.e., and , implying that for every point we have . Since , we have . However, since and (by the definition of approximate KKT point), we have that , which is a contradiction.

Satisfying Condition (3) in Definition 1 Exactly (i.e., Condition ).

Since , we have that for all . ∎

This concludes the proof that an approximate-CEEI can be determined from approximate-KKT points in polynomial time. In the next subsection, we outline a polynomial time algorithm that determines an approximate-KKT point.

4.2 Algorithm, and Convergence Guarantees

We show that approximate-KKT points can be found in polynomial time. We begin with an overview of the procedure, and later show how the steps are implemented. The idea is to perform an exterior-point procedure outside of the feasible region, which produces a sequence of guesses for approximate KKT points, while increasing along the objective. Due to the nature of the objective function, we alternate between finding supporting hyperplanes, and finding -maximizing points on these hyperplanes, until we find a point whose gradient is approximately in line with the supporting hyperplane.

To be precise, our algorithm starts from a point very close to . Note that this point lies below . Then, we find the nearest point in to . We will address how to find this nearest point, and explain how to robustly handle approximation errors in finding this nearest point. In doing so, it will be helpful to find nearest points in the convex region , but keeping in mind that the true optimum lies in : to see this, note that has to lie on the lower envelope of , and since it is the closest point in to , it follows that is normal to a supporting hyperplane of at . Furthermore, we show that Pareto-dominates , thereby implying that the Nash welfare at is larger than the Nash welfare at .

Let be the supporting hyperplane of at , where . Let be a point on this hyperplane with maximum Nash welfare. Observe that at , we should have proportional to , i.e., , implying that . Since is a supporting hyperplane of at (a point on the lower envelope of ), we have that also lies below the lower envelop of . We prove that if the distance between and is small, then is our approximate KKT-point, otherwise we have a new point below , which has significantly higher Nash welfare than . We run the exact same steps from . We argue that such a procedure should eventually give us an approximate KKT point as there is significant increase in Nash welfare with every iteration of the algorithm whenever no approximate KKT point is found. The full description of the algorithm is given in Algorithm 1.

In what follows, define . Notice that if , then for all , since for all . We will find a point which is a -approximate KKT point following Algorithm 1.

Correctness.

We begin by proving here that the algorithm truly returns an approximate KKT point and we will later show that it will terminate in polynomially many iterations, each iteration can be implemented in polynomial time. To this end, we will need the following technical results, about the steps of the algorithm.

Lemma 8.

Regardless of the geometry of , so long as is convex, we have that for each iteration of Algorithm 1:

-

1.

The hyperplane defined as is supporting for , at .

-

2.

If has strictly positive entries and does not lie in , then , , and have strictly positive entries, and .

We show these results in Appendix A, as the proofs are mostly technical. Informally, these hold due to the geometry of the feasible region, and ensure that each iterate is well-defined, and economically meaningful. To complete the proof of correctness, we show that we can efficiently find a starting point which is strictly positive in every entry, and is infeasible. Thus, Lemma 8 will inductively show that every point is positive and well-defined.

Claim 9.

The point where is a strictly positive infeasible disutility profile.

Proof.

Since for all and , any feasible dis-utility profile must assign disutility at least to some agent. Therefore, it is impossible for every agent to have disutility at a feasible point. ∎

We now show that in the stopping condition, Algorithm 1 returns an approximate KKT point. Intuitively, this holds because the function in the stopping condition is designed to correctly captures the multiplicative error needed in the definition of approximate KKT.

Lemma 10.

Algorithm 1 returns a -KKT point for minimizing on .

Proof.

In the rest of this section, we will argue that the number of iterations must be polynomial, and that each iteration can be solved in polynomial time, which will allow us to conclude the correctness and efficiency of the algorithm.

Polynomially Many Iterations.

We show that in polynomially many iterations the algorithm finds an approximate KKT point. In particular, we show that (a) the log-NSW is always increasing throughout Algorithm 1, and (b) it increases additively by every time . Bounding the range of over the course of the iteration will then give our desired bound.

Proof.

By Lemma 8, , coordinate-wise. Thus, since is monotone increasing in each coordinate direction, .

We prove that Step 6 is an improvement by showing that is the maximizing point on the hyperplane , and therefore .

Since is a concave function, it is maximized on this hyperplane when is proportional to , i.e. when for some , for all . Since we need , it suffices to set . Thus, is the -maximizing point on the supporting hyperplane which contains , and so this move is an -improvement. ∎

Using the above claims, next we show that increases significantly in each iteration of our algorithm.

Lemma 12.

Proof.

Since by Claim 11, it suffices to show that if , then is large. Let , and note that , and furthermore, . Let , and notice that

Note that , where we take the quotient componentwise as is defined at the start of Section 4.1. With , this gives . Therefore, we know that . We also get

Define:

At , we have that and . By comparing derivatives for the other values of , we can show that for all . Thus,

Now, since we have , there must be some such that . If , then . Conversely, if , we being by noting that for , we have for reasons similar to the above. Thus, we get

We must have , since the argument can’t be negative, so we have , or . Noting that for all , we can then conclude

as desired. ∎

Finally, to bound the number of iterations Algorithm 1 would take we need to bound the log-NSW value at the starting point, namely , where , as in Claim 9. We show the following.

Lemma 13.

Proof.

If we can bound the range of the log-NSW objective, then the proof follows using Lemmas 10 and 12. Let be such that for every agent , at every feasible . Note that .

Then we have that for any feasible , . Since each round of the above algorithm that doesn’t terminate increases the log-NSW by at least , then the total number of rounds possible is at most

which gives the desired bound. ∎

Now that we have shown there are polynomially many iterations in our algorithm, it suffices to show that each iteration can be implemented in polynomial time to establish that Algorithm 1 is indeed polynomial time.

Implementing Each Iteration in Polynomial Time.

To show that each iteration can be implemented in polynomial time, it suffices to show that the nearest neighbour search (step 3 in Algoritm 1) can be implemented in polynomial time.

Lemma 14.

Each iteration of Algorithm 1 can be computed exactly in time polynomial in , , and the description complexity of the ’s.

Proof.

Let as defined previously. Recall that disutility functions are linear, with .

Let be the block-diagonal matrix such that . To find the nearest-feasible disutility profiles, we will find the allocation which minimizes the following convex quadratic program:

It was shown by Khachiyan et al. [KTK80] that this program can be solved exactly, with running time polynomial in the description complexity of the system. Thus, so long as and have rational entries with polynomial description complexity (polynomial-sized numerators and denominators), the problem can be solved exactly in polynomial time, and the solution will have small description complexity.

The matrix consists of the ’s and our running time is assumed to depend on their description complexity. ∎

Final Result.

We now have all the ingredients to conclude that an approximate CEEI (Definition 1) can be computed in polynomial time. Lemma 13 bounds the number of iterations as a polynomial in , , and the description complexity of the instance, Claim 9 shows how to find a good starting point, Lemma 14 shows that each iteration can be computed in polynomial time, with the same arguments, and Theorem 4 shows how to compute a -CEEI in polynomial time given the output of Algorithm 1. Thus, we conclude that Algorithm 1 is an FPTAS for finding -CEEI.

5 1-Homogeneous Disutilities: Computing -CEEI in Polynomial-Time

In this section, we show how to extend the results of the previous section when agents’ disutility functions are general 1-homogeneous and convex. Access to the disutility functions are through value oracle. For ease of notation, throughout this section, we refer to the coordinate of a disutility vector as (or equivalently ). Similarly, given an allocation , we refer to agent ’s bundle as (or equivalently )and the amount of chore allocated to agent as (or equivalently ). We first discuss the two main roadblocks in generalizing the approach in Section 4. The convex program for finding the nearest neighbour is not necessarily convex when agents have general -homogeneous and convex disutilities. We design an alternative formulation that returns the nearest feasible point, and is convex. However, the domain of the new convex program is not defined by a set of linear inequalities and as such one can only find approximate nearest neighbours, e.g., via interior point methods [Bub14]. In turn, the supporting hyperplanes in Algorithm 1 are now approximate supporting hyperplanes. To allow this extra error, we extend the notion of approximate KKT to that given in Definition 3, namely

-

1.

for all , and , and for all ,

-

2.

and for all , and

-

3.

for each , we have .

In the previous section, with linear disutilities we have and in the above definition, and this was crucially used to map approximate KKT to stronger approximate CEEI. We show in Section 5.1 that the claim follows even with .

For all of these to work, the disutility functions have to be well-behaved. To this end, we make the following assumptions about the rate of growth of the disutility functions.

Assumption 16.

We assume that the disutility functions have Lipschitz-style lower- and upper-bounds. Formally, for some constant , we assume that for all and for all , we have ; furthermore, for all , and all , we assume .

The running time of our algorithm will be polynomial in . However, we believe that we can also handle cases with a weaker lower-Lipschitz condition: for all , for . Towards the end of this section, we briefly mention what changes would be required to Algorithm 2 to make it work with the weaker assumption. For simplicity, we stick to Assumption 16 for the rest of this section.

Analogously to the linear case, we begin by showing in Section 5.1 that approximate KKT points will constructively yield approximate CEEI, and show in Section 5.2 a refinement of Algorithm 1 to find these approximate KKT points in the general setting. Finally, in Section 5.3, we bound the number of iterations of this new algorithm, and show how to compute each iteration efficiently.

5.1 -KKT Gives Approximate CEEI.

In this Subsection, we show the following strengthening of Theorem 4.

Theorem 17.

Let be a -KKT point for the problem of minimizing subject to , and . Then there exists payments such that form a -CEEI, as in Definition 1, where .

The whole of this subsection constitutes the proof of the above theorem. Let be a -KKT point, as in Definition 3. Since for all , let be any point in such that is a supporting hyperplane for . Since and for all , we have , or equivalently, .

From here on, our proof emulates the proof of Theorem 4, and consequently the proof of Bogomolnaia et al. [BMSY17]. Recall that we have defined

the pre-image of under . As before, let . is non-empty, closed and convex for all as the disutilities are convex, and is feasible. Since for all , we have for all . Thus, is tangent to at the point and . Therefore, there exists a supporting hyperplane of at , separating from . We define the vector such that . Define and . As before, we have .

Satisfying Condition (1) in Definition 1.

We want to show that for all agents and , we have . Note that for sufficiently close to 1, and sufficiently small, . We begin with the following observations.

Claim 18.

We have .

Proof.

Since is a supporting hyperplane of at , we have . Observe that this minimum is obtained by assigning each chore fully to the agent that has the smallest value for it. Therefore, we have that

Claim 19.

.

Proof.

Consider any point . We have . Since for all and ,

as desired. ∎

Claim 20.

, and , the boundary.

Proof.

Consider any . Note that this is the original feasible region with equality. We have

The first equality holds since we assume in , and the second holds by Claim 18. If instead , then the first equality becomes an inequality, concluding the proof. ∎

With these three claims, we can show the first condition for CEEI. Assume for a contradiction that for some , . Then we could replace the allocation as follows: Construct by setting , and . Since , we have . Also note that

since the payment subtracted from agent is equal to the payment added to agent and so .

By Claim 19, we have that . Recall that is a separating half-space between and , i.e., and , implying that for every point we have . Since , we have . However,

Now, we have for , and therefore

for sufficiently close to 0 and sufficiently close to 1. This implies that we have , which is a contradiction.

Satisfying Condition (2) in Definition 1.

We want to show that for all , we have for all such that . Let us assume that there exists a such that and . We define a new allocation . First note that as . Therefore . By Claim 19, we have that . Recall that is a separating half-space between and , i.e. and . Therefore . However,

This implies that , which is a contradiction.

Satisfying Condition (3) in Definition 1.

By definition of -KKT point, we have for all , and and also for all .

5.2 Exterior-Point Methods for -KKT Points

We introduce here a refinement of Algorithm 1 which allows us to handle the extra errors, and finds -KKT points in polynomial time. The algorithm takes as input three error terms, , , and , and we will later see how to set these to attain polynomial running time. We encourage the reader to go through Subsection 1.2.3 to get an overview of the entire algorithm and the challenges it handles compared to the setting where all agents have linear disutilities.

Recall that , as above, and note that . Our new algorithm is as follows.

Returns the point such that and and where such that is the nearest point to in . Also every coordinate of and is an integral multiple of for some . The details of this algorithm will be presented in Section 5.3.

We begin by showing that the above algorithm will correctly return a -KKT point for the appropriate values of , which will be chosen later. For now, the reader should think of the ’s as being related as follows: . In particular, we have and .

The proof of correctness for Algorithm 2 will be significantly more involved than that of Algorithm 1. Notably, the error in the computation of the nearest point on line 3 will introduce many sources of additive error, which will need to be handled along with Assumption 16 above, to ensure that we can recover multiplicative error guarantees.

We will need to argue that an approximate equilibrium can be found whether the algorithm returns in either of Steps 7 or 12. The latter was the stopping condition for the original Algorithm 1, and its proof will be simpler.

Let be the true nearest point to in and let be such that .

5.2.1 Stopping on Line 12 of Algorithm 2

We first show that the vectors are indeed normals to approximately supporting hyperplanes.

Before proving this results, we first need some technical claims.

Proof.

Note that since the algorithm has constructed the vector , in iteration , we have . Otherwise, by the choice of ’s, the algorithm would have terminated since would have been too close to . Therefore, we have and our algorithm will terminate before step 9. Therefore, lies outside , i.e., below the lower envelop of . By Lemma 8, . This implies that has a pre-image under . As a result, we can bound . Note that by Assumption 16, we have for all . Therefore, we have . ∎

Proof.

By construction, after step 3, we have for all and and for all . Then in step 4, we increase all by and thus we have . Since our disutility functions have lower-bounded partial derivatives, we have for each , the disutility of agent increases by at least and thus we have for all . We complete the proof by showing that for all . To this end, first observe that if , then and the claim holds trivially. If , then by the same argument in Lemma 8, we can prove for all . ∎

We also show that and are in the neighbourhood of and respectively.

Proof.

We can now prove the lemma.

Proof of Lemma 21..

With the bound of Lemma 21, we can now show that if the algorithm stops on Step 12, i.e. if is too close to , then we have an approximate KKT point.

Proof.

We first show that for each , we have . Since our algorithm returns this point in step 12, we have . This implies that for each , we have . Also, by Lemma 21, we have for all and .

It remains to show that for all , and . We have that after step 4 of Algorithm 2, for all . This is because by construction, after step 3 of Algorithm 2, . Furthermore after step 4, is increased by an additive factor of and thus it becomes larger than . Since and , we have , further implying that as well.

5.2.2 Stopping on Line 7 of Algorithm 2

We have shown that if Algorithm 2 stops in step 12, then we have an approximate KKT point. It remains to show that this holds if we stop in step 7. We start by addressing a small subtlety. The normal vector is only well defined from . Therefore, we need to show that Algorithm 2 never returns at Line 7 at (the first iteration). This follows from the fact that the distance between and any point in . To see this, note that for any disutility vector , there is one agent who gets at least fraction of some chore and as a result his disutility will be at least (by Assumption 16). However, the disutility of any agent in is at most (by Assumption 16 and Algorithm 3). Therefore . We now focus on the main proof.

Note that this stopping condition is an additive error, and we will need to be more careful. The bulk of the proof will lie in showing that the allocation is neither an over-allocation nor an under-allocation of any of the chores. The remaining conditions will be relatively straightforward, as they are a consequence of Lemma 21 on the previous iteration.

Lemma 26.

Proof.

We have that (i) lies on the hyperplane where , by construction, and (ii) is a -approximate supporting hyperplane of , by Lemma 21). Therefore, to show that is a -approximate KKT point with no bound, it suffices to show that for all and .

It remains then to show that is not too far from 1 in any direction. Notice that our supporting hyperplane is approximately supporting the set . Thus, it is relatively straightforward to argue, as we do here, that under-allocations are unlikely, but any arbitrary over-allocation will need to be controlled. We begin by ruling out under-allocations.

Recall, if the algorithm stops on line 7, then it will have applied adjust-coordinates to the allocation. In what follows, let denote the value of before the application of adjust-coordinates, i.e. the value of on line 4, and let be the returned allocation. Formally .

Claim 27.

If we stop on line 7, then .

Proof.

Note that . As the disutility functions are -homogeneous, we have for each , . ∎

Proof.

We begin by showing that for all and , . Note that by Observation 23, we have for all . Therefore, for all , implying that no agent increases their consumption of any chore, i.e., for all and . Now, assume that there exist an and such that . Since the disutility functions have lower-bounded partial derivatives (Assumption 16), and agent does not increase consumption of any other chore from to , we have , or equivalently , contradicting the fact that . Therefore, .

Now, by Observation 23, we have that , implying that for all . Therefore, if we have , then we have for all . ∎

No chores are significantly over-allocated.

We now show for all , where and . The reason behind the exact choice of the upper bound will become explicit by the end of Claims 32 and 33. We start by making some observations on and . Recall, lies on the hyperplane , where

We start by showing that there is at least one coordinate where is not small, w.r.t .

Claim 29.

There exists an such that .

Proof.

In the -st iteration, Algorithm 2 did not return at step 7, and so . There must be some such that . By Observation 23, , and thus . Now,

| (by Observation 24) | ||||

Again, since the algorithm did not return at step 7 in the -st iteration, we have by Observation 21. This implies that .

Now note that . ∎

We now define a new allocation from such that and consequently . This would imply that . By Claim 27, this equals .

We will show in the following that if any chore is significantly over-allocated in , then which is a contradiction. Let us therefore assume that there is a which is over-allocated, i.e, . This implies that there is some such that . Furthermore, for all , we denote by , the excess amount of chore left undone in , i.e., .

As a corollary of Lemma 28, we can bound .

Claim 30.

For all , we have .

To define the allocation , we distinguish two cases. Recall that the agent has , by Claim 29. Furthermore, recall that we have chosen for our desired bound.

- Case 1.

-

For some item , . In this case, agent consumes a non-negligent amount of some chore w.r.t. the ’s. Define as follows:

This has the following effects: (i) we decrease ’s consumption of by units and increase ’s consumption of by units (so the total consumption of remains unchanged), then (ii) increase the consumption of every under-consumed chore for agent until their total consumption becomes 1 and finally (iii) decrease the ’s consumption of (the overallocated chore) by units.

- Case 2.

-

If instead, for all items , define as follows:

(i) We decrease ’s consumption of each chore to zero and increase ’s consumption of item by units (so the total consumption of each chore remains unchanged), then (ii) we increase the consumption of every under-consumed chore for agent until their total consumption becomes 1 and finally (iii) we decrease ’s consumption of (the overallocated chore) by units.

We first show that .

Claim 31.

We have .

Proof.

In both Case 1 and 2, we have increased agent ’s consumption of each the under-allocated chores () by , with the exception of and if applicable. Furthermore, the decrease in consumption of any chore for agent is matched by an increase for , before subtracting the term. Therefore, for all . Finally, the consumption of chore is decreased by , but since the total consumption of in is at least , the total consumption of in is at least . Thus and . ∎

We next argue that the disutility values of all agents have not increased.

Claim 32.

For all , we have .

Proof.

Note that we have only reduced the consumption of chores for all agents except . Therefore, the disutility values for all agents in decreases. It suffices to show that agent ’s disutility also decreases. We now argue that .

Let be defined to equal in Case 1, and in Case 2. In both cases, we are subtracting from and adding it to . We recall that 1-homogeneous and convex functions are sub-additive: . Therefore,

Now, in both cases, , and so by Assumption 16, , and . Finally, recall , and so we have

With these two claims, we can now show that despite , a contradiction.

Claim 33.

We have .

Proof.

Therefore, we have , but , which is a contradiction. This implies that no chores are significantly over-allocated. Thus, we have proven the following:

Lemma 34.

For all , we have , where and .

We now have everything we need to prove the following:

Theorem 35.

Algorithm 2 returns a -KKT point with , where , and .

5.3 Polynomially Bounding the Number and Running Time of Iterations

In this section, we show that in polynomially many iterations, Algorithm 2 finds the -KKT point of Lemma 35. The proof follows exactly the proof in the setting with linear disutilities (the proof of Lemma 12). One can argue that (a) the log-NSW is always increasing throughout Algorithm 1, and (b) it increases additively by every time . Therefore, the total number of iterations of the algorithm is bounded by .

Lemma 36.

After iterations, Algorithm 2 returns a -KKT point, where .

It remains therefore to show that each iteration can be efficiently computed. The main difficulty lies in finding the approximate nearest point , or rather , i.e. to explain the algorithm for nearest-point, from line 3 of Algorithm 2. The remaining steps of the algorithm and of the adjust-coordinates procedure are polynomial.

Recall that given a scalar and a point , the subroutine returns a point such that and , where is the nearest point in to and is a pre-image of . Also note that we have an additional requirement on the nearest point that each coordinate should be an integral multiple of . However, this can be implemented by rounding the nearest approximate point that we find in polynomial time without increasing and significantly (there will only be additive errors of ). Therefore, the main bottleneck is in finding the approximate nearest point. We focus mainly on this now.

We will implement this with the following convex program, which returns simultaneously and as its solution.

| (8) |

The objective function is clearly convex, and we show in Claim 44 in Appendix A that the constraints are convex as well.

We now prove that Program 8 is correct, i.e. its solution gives the nearest point in to .

Lemma 37.

Let be an exact solution to the convex program 8. Then and is a nearest point in to .

Proof.

Since satisfies the feasibility constraints, we have for all , and for all , implying that . Now, it remains to show that .

Let be the minimum value of the objective function in (8) achieved by any feasible solution. We wish to show that . First note that , since it is feasible to set and

Now, we show that . Note that if , then and thus will be trivially larger than . So we only focus on the case when . Suppose for a contradiction that and there exists a feasible such that . This implies that . Therefore, there exists a hyperplane that separates and the point . Since lies in , we have then by definition,

By the last constraint in program (8), each coordinate of is non-positive, and so for this inequality to hold, must have a strictly negative entry. However, since is unbounded in the positive directions, no hyperplane of the form can be supporting unless , a contradiction.

Therefore, at the optimum, . Since is a feasible point we have for all , implying that . Since is a closest point in to , and , we have , implying that is also a closest point in to . ∎

Let be the optimum solution to the program 8. We just need to find an approximate solution to the convex program such that , as this would give us the desired bounds in the allocation as well as the resulting disutility vector (follows from the Lipschitz condition of the disutility functions mentioned in Assumption 16). This can be determined in polynomial time by interior point algorithms. This brings us to the main lemma of this section.

Lemma 38.

Given a scalar and a point , the subroutine returns a point such that and , where is the nearest point in to and is a pre-image of , in time . Additionally, each coordinate of and is an integral multiple of .

Proof.

Many interior-point methods exist to solve this program, including the ellipsoid method, which can efficiently find a near-optimal point in time, given efficient separation oracles [Bub14]. The constraint region needs to be bounded for these methods to work, but we can use the correctness of Algorithm 2 (Theorem 35) to upper-bound the allocations, and Assumption 16 to bound the feasible values.

We can easily determine which constraint is violated in the program (8), but we need to return a hyperplane if the violated constraint is one of the constraints. We have assumed access to the partial derivatives of the ’s, and we therefore have access to the gradient of these constraints. A “good enough” candidate point at which to take the supporting hyperplane can be found by approximating the nearest feasible point using unconstrained optimization with barrier functions [Bub14], which gives separation oracles to implement a step of the ellipsoid method. ∎