Financial network games

University of Essex, UK)

Abstract

We study financial systems from a game-theoretic standpoint. A financial system is represented by a network, where nodes correspond to firms, and directed labeled edges correspond to debt contracts between them. The existence of cycles in the network indicates that a payment of a firm to one of its lenders might result to some incoming payment. So, if a firm cannot fully repay its debt, then the exact (partial) payments it makes to each of its creditors can affect the cash inflow back to itself. We naturally assume that the firms are interested in their financial well-being (utility) which is aligned with the amount of incoming payments they receive from the network. This defines a game among the firms, that can be seen as utility-maximizing agents who can strategize over their payments.

We are the first to study financial network games that arise under a natural set of payment strategies called priority-proportional payments. We investigate the existence and (in)efficiency of equilibrium strategies, under different assumptions on how the firms’ utility is defined, on the types of debt contracts allowed between the firms, and on the presence of other financial features that commonly arise in practice. Surprisingly, even if all firms’ strategies are fixed, the existence of a unique payment profile is not guaranteed. So, we also investigate the existence and computation of valid payment profiles for fixed payment strategies.

1 Introduction

A financial system comprises a set of institutions, such as banks and firms, that engage in financial transactions. The interconnections showing the liabilities (financial obligations or debts) among the firms are represented by a network and can be highly complex. Hence, the wealth and financial well-being of a firm depends on the entire network and not just on the well-being of its immediate borrowers/debtors. For example, a possible bankruptcy of a firm and the corresponding damage to its immediate lenders/creditors resulting from the firm’s failure to repay (known as credit risk), can be propagated through the financial network by causing the creditors’ (and other firms’, in sequence) inability to repay their debts, thus having a global effect.

In this work, we examine the global effect of payment decisions of individual firms. We assume that each firm has a fixed amount of external assets (not affected by the network) which are measured in the same currency as the liabilities. A firm’s total assets comprise its external assets and its incoming payments, and can be used for (outgoing) payments to its creditors. A firm’s payment decision, for example, can specify the priority to be given to each of its debts or creditors. An authority (such as the government or the court) is assumed to monitor the decisions of the firms in order to guarantee that they comply with general regulatory principles, such as the absolute priority and the limited liability ones (see, e.g., [8]). According to these principles, a firm can leave a liability unpaid only if its assets are not enough to fully repay its liabilities. In particular, the absolute priority principle requires that all creditors must be paid off before a firm’s stakeholders can split assets, and the limited liability principle implies that a firm that does not have enough assets to pay its liabilities in full, has to spend all its remaining assets to pay its creditors. Surprisingly, not all decisions of the firms lead to valid solutions (or payment profiles)111An example of such a network appears in [20] and assumes the presence of default costs and Credit Default Swaps (definitions appear in Section 2)., or there can be ambiguity in the overall solution despite the individual fixed payment decisions of the firms222Consider, for example, four firms A, B, C, and D, with zero external assets each, and the following liabilities: A owes coins to B and another coins to C; B owes coins to A and another coins to D. Assume that the payment strategy of firm A is to prioritize payments towards B over C, and that the payment strategy of firm B is to prioritize payments towards A over D (firms C and D are not strategic since they do not have multiple creditors—or any for that matter). Then there exist infinitely many valid solutions that are consistent with this strategy profile: Indeed, A paying B the amount of coins and B paying A the same amount ( coins), is a valid solution for any positive value . [8]. This gives rise to the clearing problem aiming to determine the final payment profile of the network for fixed individual payment decisions. Such payments are called clearing payments and are compatible with the given individual payment decisions. Computing clearing payments is a necessary step before performing a game-theoretic analysis.

We investigate the consequences of individual firm decisions in clearing from a game-theoretic standpoint [15]. Following the recent work of Bertschinger et al. [4], we diverge from the common assumption of proportionality in payments, that dictates that a firm pays its creditors proportionally to their respective liabilities. We assume that firms strategize about their payments by appropriately deciding the priority of their payment actions, consistently with a predefined payment scheme (and the current regulation); the chosen priorities may have an effect on the incoming payments of a given firm. We consider a natural payment scheme that allows allocations of creditors to priority-classes independently of the available assets. We refer to this payment scheme as priority-proportional scheme, and the corresponding strategies as priority-proportional strategies.

Our paper is the first to perform a game-theoretic analysis of priority-proportional payments in financial networks. Payments with priorities are simple to express as well as quite common and very well-motivated in the financial world. Indeed, bankruptcy codes allow for assigning priorities to the payout to different creditors, in case an entity is not able to repay all its obligations. Such a distribution of payments can be part of a reorganization plan ordered by the court [3]. Priority classes in bankruptcy law have also been considered in [10, 12], among others. Moving beyond regulated financial contexts, similar behavior is common in everyday transactions between individuals with pairwise debt relations. This is the first time that the impact of priority-proportional payments is assessed in a strategic setting, as are other elements of our analysis, even though such payments have been considered in the past (most recently by Papp and Wattenhofer [16]). Our work demonstrates that, despite their simplicity, priority-proportional strategies exhibit certain desired properties with respect e.g., to equilibria existence and quality. They are also not very restrictive, which can lead to unattractive instances. Our work can be seen as an attempt to examine whether such priority-based payment plans are indeed stable equilibria; this can be useful from a mechanism design perspective.

Our game-theoretic analysis considers two different definitions of utility motivated by the financial literature, namely total assets, computed as the sum of external assets and incoming payments, or equity, respectively. Traditionally, the financial health of a firm has been measured by its equity, which is equal to the amount of remaining assets after payments (total assets minus liabilities) if this is positive, and otherwise. This means that all firms that have more debt than assets have equity , so equities fail to capture the potentially different available assets these firms might have. Total assets can be seen as a refinement of the equities: indeed, for any financially healthy firm (that can repay all its debt) its total assets equal its equity plus its liabilities (a fixed term), while for other firms, total assets allow them to distinguish among different states that are indistinguishable in terms of equity. Note that, since by the absolute priority principle a firm is obliged by law to fully repay all its creditors if it has enough assets, it is only the payment decisions of firms whose debt is more than their assets that can have an effect on the network. For this reason, computing the firms’ utility as their total assets is a suitable approach in a game-theoretic context. Overall, both definitions are aligned with the individual financial wealth and welfare of a firm, so maximizing the utility is a firm’s natural individual objective.

Our model is based on the seminal and widely adopted work of Eisenberg and Noe [8] who provide a basic financial network model, i.e., proportional payments, non-negative external assets, and debt-only liabilities. In addition to considering a different payment scheme, we enhance the basic model by also considering financial features commonly arising in practice, such as default costs [17], Credit Default Swap (CDS) contracts [20], and negative external assets [7] (definitions appear in Section 2). We analyze the efficiency of the states arising from various clearing payments of financial networks, with a focus on ones consistent with equilibrium strategies. Note that even though, as stated above, both utility definitions are aligned with the individual financial wealth and welfare of a firm, it turns out that these notions of individual utility are not always aligned with the welfare of the whole financial system.

Overall, we aim to quantify the extent to which strategic behavior of the firms affects the welfare of the society, by analyzing the financial network games that are defined by a particular utility function, and possibly allow the presence of other financial instruments. In particular, we consider financial network games under priority-proportional strategies, defined for different utility functions, such as total assets or equities, and which potentially allow CDS contracts, default costs, or negative external assets. We derive structural results that have to do with the existence, the computation, and the properties of clearing payments for fixed payment decisions in a non-strategic setting, and/or the existence and quality of equilibrium strategies. In particular, in Section 3 we prove the existence of maximal clearing payments under priority-proportional strategies, even in the presence of default costs, and provide an algorithm that computes them efficiently. We are then able to prove existence of equilibria when the utility is defined as the equity, but show that equilibria are not guaranteed to exist when the utility is captured by the total assets. We then turn our attention to the efficiency of equilibria and provide an almost complete picture of the price of anarchy [13] and the price of stability [21, 2]. Our results for total assets appear in Section 4, while the case of equities is treated in Section 5.

Related work

Financial networks and their related properties have been analyzed in various works that follow the standard (non-strategic) model developed by Eisenberg and Noe [8]. They introduce a financial network model allowing debt-only contracts among firms with non-negative external assets that make proportional payments. Among other results, they prove that there always exist maximum and minimum clearing payments and identify sufficient conditions so that uniqueness is guaranteed; they also present an efficient iterative algorithm that computes them.

Following the model of Eisenberg and Noe [8], a series of papers extend and enrich the model by adding default costs [17], cross-ownership [9, 22], liabilities with various maturities [1, 14] and CDS contracts [16, 20]. In [17], Rogers and Veraart prove the existence of maximal clearing payments in the presence of default costs and provide an algorithm that computes them. Schuldenzucker et al. [20] also consider CDS contracts and show that, in general, there can be zero or many clearing payments. Furthermore, they provide sufficient conditions for the existence of unique clearing payments. Demange [7] proposes a model that allows for firms to be indebted to entities outside the network, and captures this by allowing negative external assets.

The strategic aspects of financial networks have been considered very recently. Most relevant to our setting is the paper by Bertschinger et al. [4] who also study the inefficiency of equilibria in financial networks. They follow the standard model of [8] and focus mainly on two payment schemes, namely coin-ranking and edge-ranking strategies, while also considering the total assets (as opposed to equity) as a measure of the individual utility of each firm. Apart from defining the graph-theoretic version of the clearing problem, they present a large range of results on the existence and quality of equilibria. Our work extends this line of research by considering a different payment scheme (which extends edge-ranking strategies by allowing ties in the ranking) and the possibility of additional common financial features (default costs, CDS contracts, and negative external assets). In a similar spirit, Papp and Wattenhofer [16] consider the impact of individual firm actions, such as removing an incoming debt, donating extra funds to another firm, or investing more external assets, when CDS contracts are also allowed. They mostly focus on the case where firms have predefined priorities over their creditors and they remark that even by redefining such priorities, a firm cannot affect its equity.

Schuldenzucker and Seuken [18] consider the problem of portfolio compression, where a set of liabilities forming a directed cycle in the financial network may be simultaneously removed, if all participating firms approve it. They consider questions related to the firms’ incentives to participate in such a compression, while Schuldenzucker et al. [19] show that finding clearing payments when CDS contracts are allowed is PPAD-complete. Additional strategic considerations, albeit less related to our setting, are the focus of Allouch and Jalloul [1] who consider liabilities with two different maturity dates and study how firms may strategically deposit some amount from their first-period endowment in order to increase their assets in the second period, while Csóka and Herings [6] consider liability games and study how to distribute the assets of a firm in default, among its creditors and the firm itself.

2 Preliminaries

In the following, we denote by the set of integers . The critical notions of this section and their graphical representation are presented in an example (Figure 1), at the end of this Section.

Financial networks.

Consider a set of firms, where each firm initially has some external assets corresponding to income received from entities outside the financial system; note that may also be negative.

Firms have payment obligations, i.e., liabilities, among themselves. These are in the form of a simple debt contract or of a Credit Default Swap. A debt contract creates a liability of firm (the debtor) to firm (the creditor); we assume that and . Note that both and may hold. Firms with sufficient funds to pay their obligations in full are called solvent firms, while ones that cannot are in default. The recovery rate, , of a firm that is in default, is defined as the fraction of its total liabilities that it can fulfill. A Credit Default Swap (CDS) is a conditional liability of of the debtor to the creditor , subject to the default of , called the reference entity. Overall, the total liability of firm to firm is Let be the total liabilities of firm and set .

Let denote the payment from to ; we assume that . These payments define a payment matrix with . Then, represents the total outgoing payments of firm , while is the payment vector; this should not be confused with the breakdown of individual payments of firm that is denoted by . A firm in default may need to liquidate its external assets or make payments to entities outside the financial system (e.g., to pay wages). This is modeled using default costs defined by values . A firm in default can only use an fraction of its external assets (when this is positive) and a fraction of its incoming payments. The absolute priority and limited liability regulatory principles, discussed in the introduction, imply that a solvent firm must repay all its obligations to all its creditors, while a firm in default must repay as much of its debt as possible, taking default costs also into account. Summarizing, it must hold that and, furthermore, , where

| (1) |

Payments that satisfy these constraints are called clearing payments333Clearing payments are not necessarily unique.. We define the notion of proper clearing payments, which are clearing payments that satisfy that all the money circulating in the financial network have originated from some firm with positive external assets. In the following, we only consider proper clearing payments.

Financial network games.

These games arise naturally when we view the firms as strategic agents. We denote the strategy of firm by ; this dictates how allocates its existing funds, for any possible value these might have. Similarly, we can define the strategy profile .

Given clearing payments , we define firm ’s utility using either of the following two notions. The total assets (see also [4, 5]) are

while the equity (see also [16]) is

Proportional payments have been frequently studied in the financial literature (e.g., in [7, 8, 17]). Given clearing payments (see Equation (1)), each must also satisfy Note that, when constrained to use proportional payments, there is no strategic decision making involved.

We focus on priority-proportional payments, where a firm’s strategy is independent of its total assets and consists of a complete ordering of its creditors allowing for ties. Creditors of higher priority must be fully repayed before any payments are made towards creditors of lower priority, while creditors of equal priority are treated as in proportional payments. For example, a firm having firms and as creditors may select strategy that has firms in the top priority class, followed by and, finally, with in the lowest priority class.

Let denote the total liability of firm to firms in its -th priority class. We use parameters to imply that firm is in the -th priority class of firm and denote by the relative liability of towards in the corresponding priority class, i.e., if , and if . For given priority-proportional strategies for all firms, the clearing payments (see Equation (1)) must also satisfy

| (2) |

That is, the payment of to a creditor in priority class occurs only after all payments to creditors of higher priority have been guaranteed. Then, payments to creditors in are made proportionally to their claims in that priority class. Finally, we also have .

We will now define the notion of Nash equilibrium in a financial network game. First, let us stress that a strategy profile has consistent clearing payments which are not necessarily unique. It is standard practice (see, e.g. [8, 17]) to focus attention to maximal clearing payments (such payments point-wise maximize all corresponding payments) to avoid this ambiguity. So, we say that a strategy profile is a Nash equilibrium if no firm can increase her utility by deviating to another payment strategy. We only consider pure Nash equilibria and clarify that the utility of a firm for a given strategy profile is computed based on the assumption that the maximal clearing payments will be realized every time. In Section 3, we show how we can compute such payments efficiently. Extending strategy deviations to coalitions and joint deviations, we are interested in strong equilibria where no coalition can cooperatively deviate so that all coalition members obtain strictly greater utility.

Social welfare:

Given clearing payments , the social welfare is the sum of the firm utilities; the particular utility notion (total assets or equities) will be clear from the context. The optimal social welfare is denoted by . Let be the set of clearing payments consistent with (pure) Nash equilibrium strategy profiles. The price of anarchy (PoA) of a particular instance is defined as the worst-case ratio of the optimal social welfare over the social welfare achieved at any equilibrium at the instance, In contrast, the price of stability (PoS) of a given instance of a game measures how far the highest social welfare that can be achieved at equilibrium is from the optimal social welfare, i.e., The Price of Anarchy (Price of Stability, respectively) of a game is the maximum PoA (PoS, respectively) of any instance of the given game.

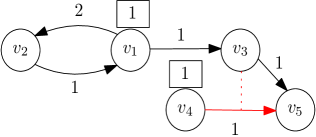

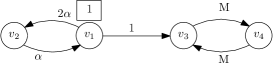

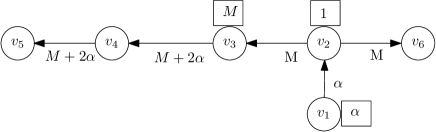

Example 1.

We represent a financial network by a graph as follows. Nodes correspond to firms and black edges correspond to debt-liabilities; a directed edge from node to node with label implies that firm owes firm an amount of money equal to . Nodes are also labeled, their label appears in a rectangle and denotes their external assets; we omit these labels for firms with external assets equal to . A pair of red edges (one solid and one dotted) represents a CDS contract: a solid directed edge from node to node with label and a dotted undirected edge connecting this edge with a third node implies that firm owes an amount of money equal to .

Figure 1 depicts a financial network with five firms having external assets and . There exist four debt contracts, i.e., firm owes and two coins and one coin, respectively; owes one coin, and owes one coin. There is also a CDS contract between , , and , with nominal liability , with being the debtor, the creditor, and the reference entity. will only need to pay if is in default; the amount owed would be equal to .

In this network, only can strategize about its payments, hence we focus just on ’s strategy:

-

•

Let select the priority-proportional strategy . Then, the payment vector would be with . Note that this is valid since and . The total assets of the firms are , , , and , and the social welfare is .

-

•

If ’s strategy is , the only consistent payment vector would be with . Then, , , , and , resulting in .

-

•

If decides to pay proportionally, that is , the payment vector would be with ; note that . Then, , , , and , resulting in .

Comparing the total assets under the different strategies discussed above, would select either strategy or , returning the maximum possible total assets (i.e., ). Therefore, any strategy profile where either or is a Nash equilibrium.

3 Existence and computation of clearing payments

This section contains our results relating to the existence and the properties of (proper) clearing payments in priority-proportional games. We begin by arguing that, given a strategy profile, clearing payments always exist even in presence of default costs. Furthermore, in case there are multiple clearing payments, there exist maximal payments, i.e., ones that point-wise maximize all corresponding payments, and we provide a polynomial-time algorithm that computes them. Note that this result is in a non-strategic context, but it is necessary in order to perform our game-theoretic analysis as it allows us to argue about well-defined deviations by considering clearing payments consistently among different strategy profiles.

Lemma 1.

In priority-proportional games with default costs, there always exist maximal clearing payments under a given strategy profile.

Proof.

The proof follows by Tarski’s fixed-point theorem, along similar lines to [8, 17]. We first focus on the case of not necessarily proper payments. Indeed, the set of payments form a complete lattice. Any payment is lower-bounded by and upper-bounded by and for any two clearing payments and such that ( is pointwise at least as big as ) it holds that , where is defined in (1). Therefore, has a greatest fixed-point and a least fixed-point.

We now claim that the existence of maximal clearing payments implies the existence of maximal proper clearing ones. Indeed, consider some maximal clearing payments and the resulting proper payments obtained by when ignoring all payments that do not originate from some firm with positive external assets. We note that are clearing payments since the payments that are deleted, in the first place only reached firms whose outgoing payments are decreased to zero as well. Clearly, if are not maximal proper clearing payments, then there exist proper clearing payments with for some firms . If we obtain a contradiction to the maximality of , otherwise if , then cannot be proper. ∎

We now show how such maximal clearing payments can be computed. Given a strategy profile in a priority-proportional game, Algorithm 1 below, that extends related algorithms in [8, 17], computes the maximal (proper) clearing payments in polynomial time. In particular, and since the strategy profile is fixed, we will argue about the payment vector consisting of the total outgoing payments for each firm; the detailed payments then follow by the strategy profile.

Lemma 2.

The payment vectors computed in each round of Algorithm 1 are pointwise non-increasing, i.e., for any round .

Proof.

We prove the lemma by induction. The base of our induction is . It holds that if , so it suffices to compute and show that for .

We wish to find the solution to the following system of equations

| (3) | |||||

We compute using a recursive method and starting from . We define , , recursively by

Now for , we have

where the first inequality holds because , and the second inequality holds by our assumption that . Hence, sequence is decreasing. Since the solution to Equation (3) is non-negative, can be computed as , which completes the base of our induction.

Now assume that for some . We will prove that . Similarly to before, if , so it suffices to compute and show that for .

The desired is the solution to the following system of equations

| (6) |

We compute recursively starting with . We define , , recursively by

| (7) |

For , we have

where we note that our assumption implies that . Now we can split the set into and . For we have . For we have

which implies that the sequence is decreasing. Since the solution to Equation (6) is non-negative, can be computed as , which completes our claim that for any round . ∎

We now present the main result of this section.

Theorem 3.

Algorithm 1 computes the maximal clearing payments under priority-proportional strategies in polynomial time.

Proof.

The algorithm proceeds in rounds. In each round , tentative vectors of payments, , and effective equities, , are computed. At the beginning of round , all firms are marked as tentatively solvent, which we denote by ; is used to denote the firms in default after the -th round of the algorithm. The algorithm works so that once a firm is in default in some round, then it remains in default until the termination of the algorithm. Indeed, by Lemma 2 the vectors of payments are non-increasing between rounds and the strategies are fixed. Algorithm Proper is called when , which requires at most rounds; clearly, each round requires polynomial time. The running time of Proper is also polynomial. Indeed, note that each firm can enter set Marked at most once and will leave Marked to join set Checked after each other firm is examined at most once.

Regarding the correctness of the Algorithm, we start by proving by induction that the payment vector provided as input to Algorithm 2 is at least equal (pointwise) to the maximal clearing vector . As a base of our induction, it is easy to see that . Now assume that for some ; we will prove that . We denote by the firms in default under the maximal clearing vector , i.e., . Our inductive hypothesis implies . Hence, for firms , we have . For we refer to the proof of Lemma 2 above and consider Equation (7) again while starting the recursive solution with . For , we observe

Recursion (7) then implies that for all and hence .

We have now proved that the input to Algorithm 2 is at least equal (pointwise) to the desired maximal clearing vector . However, by Lemma 2 we also know that for all . It holds by design that the input of Algorithm 2 is a clearing vector, so is the only possible such input. By the arguments in the proof of Lemma 1, Algorithm 2 with input the maximal clearing payments computes the maximal proper clearing payments, and the claim follows. ∎

4 Maximizing the total assets

We now turn our attention to financial network games under priority-proportional strategies when the utility is defined as the total assets. We note that in this case, the maximal clearing payments, computed in Section 3 are weakly preferred by all firms among all clearing payments of the given strategy profile; indeed, the utility is computed as the sum between a fixed term (external assets) and the incoming payments which are by definition maximized. So, in case of various clearing payments, it is reasonable to limit our attention to the (unique) maximal clearing payments computed in Section 3.

We begin with a negative result regarding the existence of Nash equilibria.

Theorem 4.

Nash equilibria are not guaranteed to exist when firms aim to maximize their total assets.

Sketch of Proof.

Consider the financial network depicted in Figure 2 where is an arbitrarily large integer. Only firms , , have more than one available strategies and, hence, it suffices to argue about them. The instance is inspired by an equivalent result in [4] regarding edge-ranking strategies, however the instance used in the proof of that result admits an equilibrium under priority-proportional strategies.

Observe that since is large, whenever (respectively, ) has (respectively, ) in its top priority class, either alone or together with , then the payment towards is at most , where , i.e., a very small payment. Furthermore, and can never fully repay their liabilities to any of their creditors; this implies that any (non-proportional) strategy that has a single creditor in the topmost priority class will never allow for payments to the second creditor.

If none of and has as their single topmost priority creditor, then, by the remark above about payments towards , at least one of them has an incentive to deviate and set as their top priority creditor. Indeed, each of , has utility at most , and at least one of them would receive utility at least by deviating. Furthermore, it cannot be that both and have as their single top priority creditor, as at least one of them is in the top priority class of . This firm, then, wishes to deviate and follow a proportional strategy so as to receive also the payment from its other debtor.

It remains to consider the case where one of , , let it be , has as the single top priority creditor and the remaining firm, let it be , either has a proportional strategy or has as its single top priority creditor. In this setting, if follows a proportional strategy, wishes to deviate and select as its single top priority creditor. Otherwise, if has as its top priority creditor, then deviates and sets as its top creditor. Finally, if has as its single top priority creditor, then deviates to a proportional strategy.

We now aim to quantify the social welfare loss in Nash equilibria when each firm aims to maximize its total assets. While the focus is on financial network games under priority-proportional payments, we warm-up by considering the well-studied case of proportional payments, where we show that these may lead to outcomes where the social welfare can be far from optimal.

Theorem 5.

Proportional payments can lead to arbitrarily bad social welfare loss with respect to total assets. In acyclic financial networks, the social welfare loss is at most a factor of and this is almost tight.

Proof.

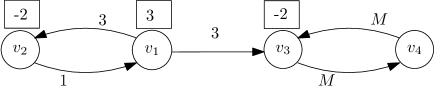

Consider the financial network between firms , , and that is shown in Figure 3, where is arbitrarily large.

Observe that paying proportionally leads to clearing payments . Hence, the total assets are , , and , and, therefore, . However, if firm chooses to pay firm , the resulting clearing payments would be with total assets , , and , that sum up to . Since and can be very large, we conclude that the social welfare achieved by proportional payments can be arbitrarily smaller than the optimal social welfare.

For the case of acyclic financial networks, let and denote the total external assets of non-leaf and leaf nodes, respectively; note that a leaf node has no creditors in the network. Clearly, since there are no default costs, a non-leaf firm with external assets and total liabilities will generate additional revenue of at least through payments to its neighboring firms. Hence, for any clearing payments we have that . In the optimal clearing payments, each non-leaf firm with external assets may generate additional revenue of at most , since the network is acyclic, and, therefore, we have that , i.e., the social welfare loss is at most a factor of as the ratio is maximized when, for each we have .

To see that this social welfare loss factor is almost tight, consider an acyclic financial network where firm with external asset has two creditors, and , with and , where is an arbitrarily large integer. Firm is, then, the first firm along a path from to , where for is a creditor of and all liabilities equal . Under proportional payments, we obtain that and for any , where is the entry, thus . In the optimal clearing payments, firm fully repays its liability towards and this payment propagates along the path from to resulting to , leading to a social welfare loss factor of , where goes to zero as tends to infinity. ∎

We remark that, given clearing payments with proportional payments, a firm may wish to deviate.

Remark 1.

Proportional payments may not form a Nash equilibrium when firms aim to maximize their total assets.

Proof.

We now turn our attention to priority-proportional strategies. To avoid text repetitions, we omit referring to priority-proportional games in our statements. We start with a positive result on the quality of equilibria when allowing for default costs in the (extreme) case .

Theorem 6.

The price of stability is if default costs apply and firms aim to maximize their total assets.

Proof.

Consider the equilibrium resulting to the optimal social welfare. Clearly, each solvent firm pays all its liabilities to its creditors and, hence, its strategy is irrelevant. Furthermore, each firm that is in default cannot make any payments towards its creditors, due to the default costs, therefore its strategy is irrelevant as well. Since no firm can increase its total assets, any strategy profile that leads to optimal social welfare is a Nash equilibrium and the theorem follows. ∎

In the more general case, however, the price of stability may be unbounded, as the following result suggests. Recall that the setting without default costs corresponds to .

Theorem 7.

The price of stability is unbounded if default costs or apply when firms aim to maximize their total assets.

Proof.

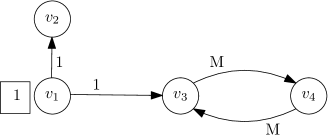

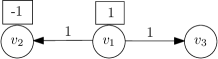

We begin with the case where and consider the financial network shown in Figure 4(a) where is arbitrarily large. Firm is the only firm that can strategize about its payments. Its strategy set comprises , , and , which result in utility , , and , respectively; note that, unless selects strategy , is also in default as is arbitrarily large. For sufficiently large , we observe that any Nash equilibrium must have choosing strategy , leading to clearing payments , and with . Now, when chooses strategy , we obtain clearing payments , and with . The claim follows since .

Now, let us assume that and and consider the financial network shown in Figure 4(b).

Again, firm is the only firm that can strategize about its payments. ’s total assets when choosing strategies , , and are , , and , respectively; note that when chooses strategy , firm is also in default as it receives a payment of which is strictly less than for any . Hence, in any Nash equilibrium chooses strategy , resulting in clearing payments with social welfare . The optimal social welfare, however, is achieved when chooses strategy , resulting in clearing payments , and with . ∎

We now show that the price of stability may also be unbounded in the absence of default costs, if negative external assets are allowed.

Theorem 8.

The price of stability is unbounded if negative external assets are allowed and firms aim to maximize their total assets.

Proof.

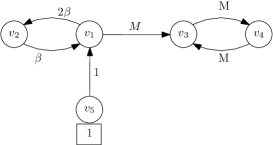

Consider the financial network shown in Figure 5.

Only firm can strategize about its payments. Clearly, ’s total assets equal , unless pays its debt (even partially). This is only possible when chooses strategy and prioritizes the payment of (note ’s negative external assets will “absorb” any payment that is at most ). Therefore, the resulting Nash equilibrium leads to the clearing payments , and with social welfare . However, when chooses strategy we obtain the clearing payments , and with social welfare . Hence, since we obtain the theorem. ∎

The proof of Theorem 8 in fact holds for any type of strategies as always prefers to pay in full its liability to . This includes the case of a very general payment strategy scheme, namely coin-ranking strategies [4] that are known to have price of stability with non-negative external assets.

Next, we show that the price of anarchy can be unbounded even in the absence of default costs, CDS contracts, and negative externals. Bertschinger et al. [4] have shown a similar result for coin-ranking strategies, albeit for a network that has no external assets; our result extends to the case of coin-ranking strategies and strengthens the result of [4] to capture the case of proper clearing payments.

Theorem 9.

The price of anarchy is unbounded when firms aim to maximize their total assets.

Proof.

Consider the financial network between firms , , that is shown in Figure 6, where is arbitrarily large.

Clearly, firm is the only firm that can strategize about its payments, and observe that regardless of ’s strategy. Hence, any strategy profile in this game is a Nash equilibrium. Consider the clearing payments that are obtained when ’s strategy is and note that . If, however, selects strategy , we end up with the clearing payment , and and we obtain . Hence, which can become arbitrarily large. ∎

5 Maximizing the equity

In this section we consider the case of equities. Similarly, the social welfare is defined as the sum of equities. We present interesting properties of clearing payments and observe that Nash equilibria always exist in such games, contrary to the case of total assets.

5.1 Existence and properties of equilibria

We warm up with a known statement in absence of default costs; the short proof is included here for completeness. In particular, each firm obtains the same equity under all clearing payments, so it does not have a preference; this provides additional justification to our assumption to limit our attention to maximal clearing payments computed in Section 3, in case of various clearing payments.

Lemma 10 ([11]).

Each firm obtains the same equity under different clearing payments, given a strategy profile. That is, given the firms’ strategies, for any two different (not necessarily maximal) clearing payments and , it holds for each firm .

Proof.

Let be the maximal clearing payments and let be any other clearing payments. The corresponding equities for each firm are

| (8) |

and

| (9) |

respectively. The rightmost equalities above hold, since each firm either pays all its liabilities, if it is solvent, or uses all its external and internal assets to pay part of its liabilities, if it is in default.

Lemma 10 also indicates that, for any given strategy profile, any firm is always either solvent or in default in all resulting clearing payments. We exploit this property to obtain the following result; this extends a result by Papp and Wattenhofer (Theorem 7 in [16]) which holds for the maximal clearing payments.

Theorem 11.

Even with CDS contracts, any strategy profile is a Nash equilibrium, when firms aim to maximize their equity. This holds even if the clearing payments that are realized are not maximal.

Proof.

Assume otherwise that there exists a strategy profile which is not a Nash equilibrium. Let be a firm that wishes to deviate and be its strategy. Clearly, if is solvent it can repay all its liabilities in full and, hence, the payment priorities are irrelevant. So, let us assume that is in default. If, by deviating, remains in default, then its equity remains . Therefore, assume that deviates to another strategy where it is solvent. In that case, however, could fully repay its liabilities regardless of the payment priorities and, therefore, it can still repay its liabilities when playing ; a contradiction. ∎

Note that Lemma 10 no longer holds once default costs are introduced; see e.g., Example 3.3 in [17] where both firms, each having a singleton strategy set, may be in default or solvent depending on the clearing payments. The next result extends Theorem 7 in [16] to the setting with default costs, and guarantees the existence of Nash equilibria (and actually strong ones) when firms wish to maximize their equity.

Theorem 12.

Even with default costs and negative external assets, any strategy profile is a strong equilibrium when firms aim to maximize their equity.

Proof.

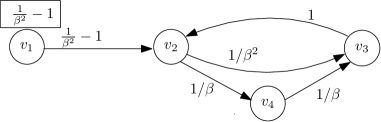

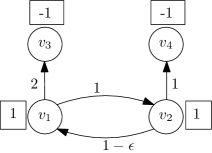

We begin by transforming an instance with negative external assets into another instance without negative external assets, albeit with a slightly restricted strategy space for each firm. In particular, we add an auxiliary firm and define liabilities and assets as follows. For any pair of firms , which does not include , we set . For each firm with , we set and set liability , while for any other firm we set and . Furthermore, we restrict the strategy space of each firm in so that their topmost priority class includes only firm . An example of this process is shown in Figure 7.

Given a strategy profile for instance , we create the corresponding strategy profile for instance by having firm as the single topmost priority creditor and, then, append the initial strategy profile. It holds that, for any given strategy profile, the maximal clearing payments for instance corresponds to maximal clearing payments in for the new strategy profile; this can be easily proved by contradiction. We can now proceed with the proof by assuming non-negative external assets, without loss of generality.

Consider maximal clearing payments and the associated strategy profile . Let us assume that there is a coalition of firms where each member of the coalition can strictly increase its equity after a joint deviation. In particular, let , for change its strategy from to . Clearly, each must have a strictly positive equity in the resulting new maximal clearing payments , since its equity was before. But then, each should remain solvent under strategy as well, and therefore ’s actual payment priorities are irrelevant, for . Note that should also be maximal clearing payments under the initial strategy profile; a contradiction to the maximality of . ∎

5.2 (In)efficiency of equilibria

We start by noting that Lemma 10 together with Theorem 11 imply the following, which we note holds for any payment scheme.

Corollary 13.

The price of anarchy in financial network games with CDS contracts is when firms aim to maximize their equity.

The above positive result, however, no longer holds when default costs or negative external assets exist. For these cases we derive the following results.

Theorem 14.

The price of anarchy with default costs when firms aim to maximize their equity, is

-

(i)

when ,

-

(ii)

unbounded when: i) , ii) and , or iii) and ,

-

(iii)

at least , if and for any .

Proof.

We begin with the case . We claim that all strategy profiles correspond to the same clearing payments hence admit the same social welfare. It suffices to observe that neither the strategy of a solvent firm, nor the strategy of a firm in default, affect the set of firms in default and consequently the clearing payments. Consider two strategy profiles and . A firm that is solvent under , will be solvent and continue to make payments under any strategy (given the strategies of everyone else), i.e., will be solvent at the clearing payments consistent with strategy vector , derived by if firm alone changes her strategy from to . On the other hand, a firm that is in default under , will similarly remain in default under and continue to make payments since , thus not affecting the set of firms in default. The claim follows by considering the individual deviations from to of all firms sequentially and observing that the set of firms in default and, hence, the clearing payments are unaffected at each step.

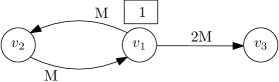

Regarding the case , consider the financial network in Figure 8. Clearly, only firm can strategize and observe that it is always in default irrespective of its strategy. When selects strategy , we obtain the clearing payments , and . Notice that , and are in default and we have .

When, however, selects strategy , we obtain the clearing payments , and . Now, and are in default and we have . Since , the claim follows.

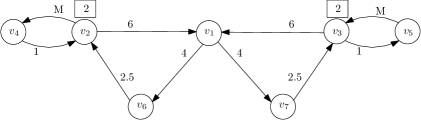

Regarding the case and , consider the financial network in Figure 9 and note that is always in default irrespective of its strategy. If selects strategy , then ends up having equity . However, strategy is also an equilibrium strategy for , but it results in each firm having equity .

Regarding the remaining case, i.e., and , consider again the financial network in Figure 9. As before, is always in default. If selects strategy , then ends up having equity . However, is also an equilibrium strategy for , but it results in equity for , equity for and equity for the remaining firms. The theorem follows by straightforward calculations. ∎

We complement this result with a tight upper bound for the case .

Theorem 15.

The price of anarchy with default costs when firms aim to maximize their equity is at most . This holds even if the clearing payments that are realized are not maximal.

Proof.

Consider any clearing payments and let and be the set of solvent and in default firms under . Recall that for any firm , we have . For any firm , it holds that , as . Similarly, for any , we have , since . By summing over all firms, we get

Clearly, the social welfare is maximized when , i.e., , while it is minimized when includes all firms, i.e., ; this completes the proof. ∎

Extending the setting to allow for negative external assets again may lead to unbounded social welfare loss.

Theorem 16.

The price of anarchy is unbounded when negative external assets are allowed and firms aim to maximize their equity.

Proof.

Consider the financial network in Figure 10. Clearly, only can strategize but, irrespective of its strategy, is always in default and ; hence, any strategy profile is a Nash equilibrium. When selects strategy we obtain the clearing payments . However, when selects strategy we obtain the clearing payments with . Since , the claim follows.

∎

Still, in the presence of default costs or negative external assets, Theorem 12 leads to the next positive result.

Corollary 17.

The strong price of stability is even with default costs and negative external assets, when firms aim to maximize their equity.

If we relax the stability notion and consider the price of stability in super-strong equilibria, where a coalition of firms deviates if at least one strictly improves its utility and no firm suffers a decrease in utility, then we obtain a negative result.

Theorem 18.

The price of stability in super-strong equilibria is unbounded when negative external assets are allowed and firms aim to maximize their equity.

Proof.

Consider the financial network as shown in Figure 11, where is a small constant. Observe that is always in default since even its maximal possible total asset is still less than its total liabilities , which means in any scenario. If ’s strategy is other than , then is always in default no matter what strategies it chooses, that is . Thus, any strategy profile where does not prioritize the payment of is a Nash equilibrium with . However, if and form a coalition, then the only superstrong equilibrium occurs when and prioritize the payment of each other, resulting in the clearing payments with . Furthermore, when follows the strategy and follows strategy , we obtain the clearing payments with . Since , we obtain that the superstrong price of stability is at least and the theorem follows since can be arbitrarily small. ∎

6 Conclusions and discussion

We have studied strategic payment games in financial networks with priority-proportional payments and we have presented an almost full picture both with respect to structural properties of clearing payments as well as the quality of Nash equilibria.

Our work reveals several interesting open questions. In particular, an interesting restriction on the strategy space is to always prioritize strategies that could lead to incoming payments, i.e., when each firm always ranks higher a payment that might create a cash flow through a directed cycle (in the liabilities graph) back to , than a payment that does not. While some of our negative results would still hold, e.g., Theorem 4, others, such as Theorem 7, crucially rely on the reverse ranking. Furthermore, one could consider addressing computational complexity questions like deciding whether a Nash equilibrium exists or computing a Nash equilibrium when it is guaranteed to exist, when firms aim to maximize their total assets.

References

- [1] Allouch, N., Jalloul, M.: Strategic default in financial networks. Tech. rep., Queen Mary University of London (2018)

- [2] Anshelevich, E., Dasgupta, A., Kleinberg, J., Tardos, E., Wexler, T., Roughgarden, T.: The price of stability for network design with fair cost allocation. SIAM Journal on Computing 38(4), 1602–1623 (2008)

- [3] Ayer, E.J.D., Bernstein, M.L., Friedland, J.: Priorities. Issues and Information for the Insolvency Professional Journal 11 (2004), https://www.kirkland.com/siteFiles/kirkexp/publications/2392/Document1/Friedland_Priorities.pdf

- [4] Bertschinger, N., Hoefer, M., Schmand, D.: Strategic payments in financial networks. In: Proceedings of the 11th Innovations in Theoretical Computer Science Conference (ITCS). pp. 46:1–46:16 (2020)

- [5] Csóka, P., Jean-Jacques Herings, P.: Decentralized clearing in financial networks. Management Science 64, 4471–4965 (2018)

- [6] Csóka, P., Jean-Jacques Herings, P.: Liability games. Games and Economic Behavior 116, 260–268 (2019)

- [7] Demange, G.: Contagion in financial networks: A threat index. Management Science 64(2), 955–970 (2018)

- [8] Eisenberg, L., Noe, T.H.: Systemic risk in financial systems. Management Science 47(2), 236–249 (2001)

- [9] Elliott, M., Golub, B., Jackson, M.O.: Financial networks and contagion. American Economic Review 104(10), 3115–53 (2014)

- [10] Elsinger, H.: Financial Networks, Cross Holdings, and Limited Liability (156) (May 2009), https://ideas.repec.org/p/onb/oenbwp/156.html

- [11] Groote Schaarsberg, M., Reijnierse, H., Borm, P.: On solving mutual liability problems. Mathematical Methods of Operations Research 87, 383–409 (2018)

- [12] Kaminski, M.M.: Hydraulic rationing. Mathematical Social Sciences 40(2), 131–155 (2000). https://doi.org/https://doi.org/10.1016/S0165-4896(99)00045-1, https://www.sciencedirect.com/science/article/pii/S0165489699000451

- [13] Koutsoupias, E., Papadimitriou, C.: Worst-case equilibria. Comput. Sci. Rev. 3(2), 65–69 (2009)

- [14] Kusnetsov, M., Veraart, L.A.M.: Interbank clearing in financial networks with multiple maturities. SIAM Journal on Financial Mathematics 10(1), 37–67 (2019)

- [15] Nisan, N., Roughgarden, T., Tardos, E., Vazirani, V.E.: Algorithmic Game Theory. Cambridge University Press (2007). https://doi.org/10.1017/CBO9780511800481

- [16] Papp, P., Wattenhofer, R.: Network-aware strategies in financial systems. In: Proceedings of the 47th International Colloquium on Automata, Languages, and Programming (ICALP). pp. 90:1–90:15 (2020)

- [17] Rogers, L.C., Veraart, L.A.M.: Failure and rescue in an interbank network. Management Science 59(4), 882–898 (2013)

- [18] Schuldenzucker, S., Seuken, S.: Portfolio compression in financial networks: Incentives and systemic risk. In: Proceedings of the 21st ACM Conference on Economics and Computation (EC). p. 79 (2020)

- [19] Schuldenzucker, S., Seuken, S., Battiston, S.: Finding clearing payments in financial networks with credit default swaps is PPAD-complete. In: Proceedings of the 8th Innovations in Theoretical Computer Science Conference (ITCS). pp. 32:1–32:20 (2017)

- [20] Schuldenzucker, S., Seuken, S., Battiston, S.: Default ambiguity: Credit default swaps create new systemic risks in financial networks. Management Science 66(5), 1981–1998 (2020)

- [21] Schulz, A.S., Stier-Moses, N.: On the performance of user equilibria in traffic networks. In: Proceedings of the Fourteenth Annual ACM-SIAM Symposium on Discrete Algorithms (SODA). pp. 86–87 (2003)

- [22] Vitali, S., Glattfelder, J.B., Battiston, S.: The network of global corporate control. PloS one 6(10), e25995 (2011)

Appendix A Proof of Theorem 4 (cont’d)

| 0, 3, 3 | |||