Whiteout: when do fixed- knockoffs fail?

Abstract

A core strength of knockoff methods is their virtually limitless customizability, allowing an analyst to exploit machine learning algorithms and domain knowledge without threatening the method’s robust finite-sample false discovery rate control guarantee. While several previous works have investigated regimes where specific implementations of knockoffs are provably powerful, general negative results are more difficult to obtain for such a flexible method. In this work we recast the fixed- knockoff filter for the Gaussian linear model as a conditional post-selection inference method. It adds user-generated Gaussian noise to the ordinary least squares estimator to obtain a “whitened” estimator with uncorrelated entries, and performs inference using as the test statistic for . We prove equivalence between our whitening formulation and the more standard formulation involving negative control predictor variables, showing how the fixed- knockoffs framework can be used for multiple testing on any problem with (asymptotically) multivariate Gaussian parameter estimates. Relying on this perspective, we obtain the first negative results that universally upper-bound the power of all fixed- knockoff methods, without regard to choices made by the analyst. Our results show roughly that, if the leading eigenvalues of are large with dense leading eigenvectors, then there is no way to whiten without irreparably erasing nearly all of the signal, rendering too uninformative for accurate inference. We give conditions under which the true positive rate (TPR) for any fixed- knockoff method must converge to zero even while the TPR of Bonferroni-corrected multiple testing tends to one, and we explore several examples illustrating this phenomenon.

1 Introduction

1.1 The knockoff filter in the Gaussian linear model

Knockoff methods are a flexible class of multiple testing procedures that operate by introducing a “negative control” or “knockoff” for each predictor variable in a supervised learning problem and then testing a learning algorithm’s ability to distinguish each real predictor from its knockoff. The original method, the fixed- knockoff filter (Barber and Candès,, 2015), is a multiple testing method for the Gaussian linear model where we observe design matrix and response

The parameters and are unknown, and the goal is to test the hypothesis against the two-sided alternative, for . Following Barber and Candès, (2015), we assume throughout that has full column rank with .

For testing individually, the usual two-sided -test is uniformly most powerful unbiased. That test rejects for extreme values of the -statistic , where and and are respectively the OLS estimator

and the residual variance . Taken together, these two estimators are a complete sufficient statistic for the model. Let denote the -value for the two-sided -test on .

For multiple testing, a classical approach would reject when is sufficiently small, after making an appropriate correction for the multiplicity of tests. If is the number of rejections and is the number of true null hypotheses rejected (false discoveries), Benjamini and Hochberg, (1995) define the false discovery proportion as , and the false discovery rate (FDR) as its expectation. While the Benjamini–Hochberg (BH) procedure of Benjamini and Hochberg, (1995) is not known to control the FDR in this problem unless the columns of are orthogonal, recent methods can directly adjust BH for the multivariate dependence, guaranteeing FDR control while performing similarly to BH (Fithian and Lei,, 2020). The FDR criterion relaxes the more conservative family-wise error rate , the probability of making any false rejections, which we could control using the conservative Bonferroni correction that rejects when .111A more accurate FWER correction would apply the closure of the max- test: if is the maximal set for which is below its quantile under , then we can reject for ; see Marcus et al., (1976) and Hothorn et al., (2008) for more details.

The knockoff filter of Barber and Candès, (2015) takes a radically different approach, bypassing the -test -values entirely. The method begins by augmenting the design matrix with a second matrix of negative control or knockoff variables, constructed to satisfy

for some diagonal matrix , where denotes the positive semidefinite ordering. As we will discuss, a larger value of preserves more signal for the inference on , but in general it is not possible to maximize all simultaneously so tradeoffs must be made between variables.

Knockoffs then calculates so-called -statistics satisfying two properties:

- 1. Sufficiency

-

depends on and only through and , and

- 2. Antisymmetry

-

Swapping any variable with its knockoff would flip the sign of and leave every other fixed. That is, if exchanges the th and th columns of an input matrix, then

The absolute values determine a data-adaptive hypothesis ordering, with larger values assigned higher priority. Sufficiency and antisymmetry, along with the Gaussian modeling assumptions, ensure two key distributional properties: first, that are conditionally independent given ; and second, that if then given , unless .

After calculating -statistics, the knockoff filter applies an ordered multiple testing method called Selective SeqStep (Barber and Candès,, 2015) treating each as a “binary -value” for . To control FDR at level , the knockoff+222Barber and Candès, (2015) also propose a version without the “” in the numerator, which controls a relaxed FDR criterion. All results in this paper pertain to the knockoff+ method, but they also apply with very minor modifications to the more liberal version. method rejects all hypotheses for which exceeds the adaptive threshold :

The fixed- knockoff filter is a highly versatile method that offers its users a multitude of choices in selecting both the knockoff matrix and the -statistics. Spector and Janson, (2020) show the importance of choosing well and discuss ramifications on the procedure’s power, and various other works detail myriad ways to tailor the -statistics using machine learning methods that exploit structural assumptions or other prior beliefs about the coefficients (see e.g., Dai and Barber,, 2016; Katsevich and Sabatti,, 2019; Chen et al.,, 2020; Dai et al.,, 2021). The method’s customizability poses a major challenge if we hope to bound its power uniformly over the analyst’s entire choice set, since well-informed analysts have ample opportunities to stack the deck in their own favor.

In light of this tremendous flexibility, it may come as a surprise to discover regimes where no knockoffs method — not even one designed with full knowledge of the true regression coefficients — can achieve nontrivial power, even while Bonferroni-corrected inference achieves near-perfect power. To begin to explain how knockoffs can go wrong, Section 1.2 formally recasts the knockoff filter as a conditional post-selection inference method built around a randomized estimator , where is user-generated Gaussian noise in the style of Tian and Taylor, (2018). Our interpretation builds on a conditioning argument in Barber and Candès, (2019) and an observation in Sarkar and Tang, (2021) that knockoffs constructs two independent estimators for .

1.2 Knockoffs as conditional inference on a whitened estimator

We now give an alternative but equivalent account of the knockoff filter without -statistics, without sufficiency and antisymmetry properties, and even without knockoff variables. We view the method instead as a conditional post-selection inference procedure, where the key step is to construct a whitened estimator with diagonal covariance. If is any diagonal matrix with , let

| (1) |

is noise generated by the user, independently of . We will see in Section 3 that even when is unknown, can be “carved” out of as long as , where .

The independence of the coordinates of is bought at the price of higher variance, since . However, this price can be recouped by an exploratory analysis using the statistic

| (2) |

carries the information lost by whitening since , and it is independent of since

Thus, is effectively “split” into two independent Gaussian vectors, and , each holding part of the information about . In terms of and , the fixed- knockoff filter can be equivalently defined as follows:

- Stage 1 (whitening).

- Stage 2 (exploratory analysis).

-

Let the analyst observe and and use them to order the hypotheses for Selective SeqStep as , where indexes the first hypothesis in order and the last. In addition, select a one-sided alternative for each . Let if the right-tailed alternative is selected, and for the left-tailed alternative.

- Stage 3 (confirmatory analysis).

-

Using Selective SeqStep, test the hypotheses in order using as a conditional test statistic for . The signs are conditionally independent given and , with

(3)

Let denote the -value for the conditional test of against a right- or left-tailed alternative according to . Because under , and is stochastically increasing in , we have when , and when .

Using these -values, the Selective SeqStep method rejects if and , where

The conditional -values are independent given and , satisfying Selective SeqStep’s requirements, so the method described above controls the FDR, both conditionally and marginally. In Section 2.1 we formally state and prove equivalence between this formulation and the usual formulation of knockoffs, building on a conditioning argument in the Supplement of Barber and Candès, (2019).

The exploratory analysis is defined vaguely because the analyst can use and however they like, provided they have not yet observed anything else about (while the sufficiency property of Barber and Candès, (2015) also restricts how the analyst may use the design matrix , we will see in Section 2.1 that no such rule is needed). It is in this unrestricted stage that knockoffs can freely exploit prior information and structural assumptions. Indeed, the analyst can even use an informal process that iterates between trying out several models, visualizing the (observable) data, consulting their intuitions or their colleagues, and so on.

When the exploratory stage goes well, the ordering is highly informative, effectively reducing the multiplicity in Stage 3 by focusing inferential power on the first few hypotheses. In many problems, a good exploratory analysis can more than compensate for the randomization and binarization of the confirmatory test statistics , helping knockoffs to outperform less flexible methods like BH.

The whitening interpretation underscores not only the versatility of the fixed- knockoff filter, but also its broad applicability. Other than defining , the above method is defined without reference to any design matrix and would be equally applicable if we simply observed directly. In Section 3 we push this interpretation further and consider how to apply the whitening method in generic statistical models with asymptotically Gaussian estimators of parameters, a ubiquitous problem encompassing generalized least squares, generalized linear models, quantile regression, and many other settings.

1.3 Which problems are hard for knockoffs?

Having seen that the fixed- knockoff filter is an appealing and generally applicable method, it is natural to ask when we can expect it to outperform competitors like BH or Bonferroni. While this is a complicated question for a method as flexible as knockoffs, the whitening interpretation helps to identify an important vulnerability of the method: when the eigenstructure of is unfavorable, the price of whitening can be very steep, dooming the confirmatory analysis before the exploratory analysis even begins. One such example is the well-studied and seemingly innocuous multiple comparisons to control (MCC) problem (Dunnett,, 1955).

Example 1 (Multiple comparisons to control).

Assume that we observe a continuous response on units under each of treatments, along with units under a control condition, and estimate an additive treatment effect. Let denote the th response under treatment , with representing the control condition. We can pose this problem as a linear model by writing for the control group, and

for the th treatment group, so that is the differential effect of treatment relative to control. If we compose a vector and model the errors as Gaussian with a common variance , we obtain a standard linear regression problem with intercept and can perform multiple testing on the hypotheses , for .

In the MCC problem, the OLS estimator of for is

so that for distinct . If we normalize the design matrix appropriately, then is an equicorrelated matrix with diagonal entries equal to 1 and off-diagonal entries equal to . Its first eigenvalue is , with eigenvector As we will see in Section 2.3, the eigenstructure of makes it impossible to find without making most of the values enormous. Specifically, the th smallest diagonal entry of any valid matrix can be no smaller than .

Let denote the number of nonzero coefficients. As our measure of power, we use the true positive rate (TPR), defined as the expectation of the true positive proportion , the fraction of non-nulls discovered. TPP and TPR are meaningless if , so we assume in all power calculations.

In Section 2.4 we will show that in an MCC problem where the non-null proportion tends to a nonzero constant, no knockoff method can achieve a nontrivial TPR as unless the nonzero coefficients grow roughly as ; by contrast, the Bonferroni method has when the nonzero coefficients grow at the rate . If all of the nonzero coefficients have size then, applying Theorem 2, the expected number of rejections of any fixed- knockoffs method at level is no larger than

| (4) |

If and , and the coefficients are all at the Bonferroni threshold , the upper bound evaluates to . This is a finite-sample result that applies even for a knockoff method designed by an analyst with full knowledge of the coefficient vector at every stage of the procedure, who can favor the non-null variables both by adding less noise to them and by ensuring they are always ordered first. We also show in Section 2.4 how to improve the bounds by simulation; in this example we can improve the bound from to . Reducing from to only helps a little, increasing the simulation bound to . Asymptotically, unless shrinks at the rate , any knockoffs method will be have for signals of size .

By contrast, in a linear regression whose design matrix has positively equicorrelated columns, the situation is completely different. In that case, is negatively equicorrelated, so its leading eigenvalue is small and all of the values can be . Likewise, if the design matrix is i.i.d. Gaussian with , then for large we expect the largest eigenvalue of to be no larger than roughly , per the Marchenko–Pastur distribution. Finally, if is very large but is heavily concentrated on only a few variables, knockoffs may still perform well on the other variables. Section 2.3 gives explicit and efficiently computable lower bounds for all order statistics of as a function of a general matrix .

The MCC setting is a prototypical example of a hard problem for knockoffs. More generally, if has large leading eigenvalues with dense eigenvectors then we must have for most of the variables, rendering the test statistic nearly uninformative about even when the coefficient is very large. In short, we cannot whiten the estimator without burying the signal under a blizzard of noise.

1.4 Related work

Several prior works foreshadow the whitening interpretation of Section 1.2. Most notably, an argument in the Supplement of Barber and Candès, (2019) conditions on and to prove the knockoff filter controls the directional FDR, a more stringent version of FDR where the analyst must draw a conclusion about whenever they reject . An analogous argument to theirs shows that the whitening method, viewed as a conditional post-selection inference procedure, controls the directional FDR as well. If we define the data-dependent one-sided null hypothesis , then are independent and valid conditional -values for given and . As a result, if we conclude whenever is rejected then we will control the directional FDR, both conditionally and marginally.

Sarkar and Tang, (2021) also exploit the independence of and with a view toward developing new methodology. When is invertible, they view and as two independent unbiased estimators of , very similar to our data splitting interpretation. From this starting point they derive hybrid multiple testing procedures blending fixed- knockoffs with the BH method.

As a conditional post-selection inference method that uses a randomized data set for exploration, knockoffs is related to two other lines of work. In the statistics literature, the data carving method of Fithian et al., (2014) improves on the Lee et al., (2016) post-selection inference method by performing a selection algorithm such as the lasso (Tibshirani,, 1996) only on a subset of the data points, effectively randomizing the selection. Tian and Taylor, (2018) proposed explicitly randomizing the selection algorithm by adding Gaussian or other noise to the sufficient statistics used by the selection algorithm. Their work was inspired by a parallel literature on adaptive data analysis wherein randomized algorithms are used to answer many statistical queries about a database, one after the other, without allowing the analyst to “overfit” (Dwork et al., 2015b, ; Dwork et al., 2015a, ). More recently Zrnic and Jordan, (2020) adapted a related approach based on algorithmic stability, also using randomization to preserve data for post-selection inference in a selected linear regression model.

Prior work on the knockoff filter’s power has focused on positive results for specific implementations of the method. When studying the TPP-FDP tradeoff on the Lasso path, it is frequently assumed that a constant fraction of non-zero coefficients are sampled from a fixed distribution (Bayati and Montanari,, 2011; Su et al.,, 2017). In addition, it is often assumed that for some positive constant . Under this intermediate-dimensional regime, the theory of approximate message passing (AMP) (Bayati and Montanari,, 2011) may be used to derive the asymptotic power of knockoff. Weinstein et al., (2017) derives the asymptotic TPP-FDP tradeoff for a knockoff-inspired procedure that is only valid for i.i.d. covariates, while Weinstein et al., (2020) and Wang and Janson, (2020) quantify the asymptotic power of knockoffs with the lasso coefficient difference test statistic. Liu and Rigollet, (2019) studied the power of knockoffs under correlated design in the low dimensional setting, and showed that the knockoff filter has full asymptotic power when the precision matrix has vanishing diagonal entries. Going beyond the aforementioned linear sparsity assumptions, Fan et al., (2020) studied the power of an oracle knockoff filter where the covariance structure of the variables is known. They assumed that the coefficients are fixed and relatively large, and showed under certain regularity conditions that the oracle knockoff filter is consistent. Ke et al., (2020) analyzed the phase diagram of the SDP knockoff, but their results are restricted to block-equicorrelated correlation structure with block size .

Recently, Spector and Janson, (2020) showed that the equicorrelated and SDP knockoff methods can be asymptotically powerless for equicorrelated Gaussian design matrices with correlation , and propose a new method for generating knockoff variables, called minimum variance-based reconstructability (MVR) knockoffs, to resolve the issue. They showed that the TPR of the MVR knockoff converges to 1 under regularity conditions. The failure mode identified by Spector and Janson, (2020) is very different from the one we discuss here, which cannot be fixed within the knockoffs framework as currently defined. Section 5.2 discusses their results in light of the whitening interpretation.

To the best of our knowledge, our results give the first universal upper bounds on what any feasible fixed- knockoff method can achieve. We prove finite-sample bounds on the maximum number of rejections that any knockoffs method can make, as a function of the design matrix and . Our bounds reveal that in some contexts the best achievable knockoff method markedly underperforms the Bonferroni method, but in other contexts off-the-shelf knockoff implementations outperform all other known methods. Understanding the fundamental limitations of the fixed- knockoff framework is a first step toward developing generalizations that ameliorate its flaws while retaining its many strengths.

1.5 Outline of results

Section 2 derives both finite-sample and asymptotic bounds on the power of knockoffs as a function of the matrix and the coefficient vector . Our argument proceeds in several steps. First, Theorem 1 in Section 2.1 proves a strong form of equivalence between the usual formulation of fixed- knockoffs as presented in Section 1.1 and the whitening formulation presented in Section 1.2, establishing that every implementation of the former is also an implementation of the latter. Thus, it suffices to bound the whitening method’s power.

The main challenge in proving universal negative results is dealing with the analyst’s ability to customize two stages of the procedure: in Stage 1, the analyst can choose any diagonal matrix , and in Stage 2, the analyst can use any exploratory method to order the hypotheses and select the alternative directions. We address these two choices in sequence: in Section 2.2, we show that an oracle analyst can optimize the exploration stage by sorting the variables in order of the log-odds , and derive bounds on the expected number of rejections in terms of the number of values exceeding the critical threshold . In Section 2.3 we obtain lower bounds on the order statistics of .

Theorem 2 in Section 2.4 combines these two lines of argument to bound the expected number of rejections in terms of and . For the case where is sparse (), Theorem 2 is very optimistic since the analyst can “cheat” by giving up on the null indices while constructing . Theorem 3 in Section 2.5 obtains a stronger bound for the more realistic setting where the analyst must choose without knowing which hypotheses are non-null. Corollary 2 applies Theorems 2–3 to prove, roughly, that if and is dense then all knockoff methods have even in a regime where the Bonferroni correction enjoys .

Since it is infeasible for a real analyst to achieve the same power as the oracle methods we describe, the bounds should not be taken as power estimates for real knockoff methods; instead, they reflect fundamental limits on the performance of the cleverest possible analyst, no matter how much domain wisdom or methodological wizardry they can bring to bear on the problem.

We emphasize that our results do not spell doom for knockoffs in all or even most settings; they hardly could, because there are indeed settings where knockoff methods outperform not only Bonferroni but also more powerful competitors like BH. Rather, they are a first step toward characterizing the regimes where each method is preferred and, we hope, toward developing methods that achieve near-optimal performance across all regimes. In particular, the regimes we identify can largely be recognized from the structure of , which is known before the responses are observed. As a result, we can simply use a different method when the structure of is unfavorable.

Section 3 delves deeper into the whitening method. Section 3.1 shows how we can implement it when we only observe an unbiased multivariate Gaussian estimator with no accompanying design matrix, and Theorem 4 in Section 3.2 shows we can do the same with an asymptotically normal estimator along with a consistent covariance matrix estimator, though the result is limited to the classical asymptotic regime. Section 3.3 applies Theorem 4 to analyze a nonparametric bootstrap example using stock market return data. Section 4 shows empirical comparisons between knockoffs and competing methods in several regimes of interest, and Section 5 concludes.

2 Bounding the power of fixed- knockoffs

2.1 Equivalence of the two formulations

Next we will show that the two formulations of knockoffs in Sections 1.1 and 1.2, which we will respectively call the standard method and the whitening method, are essentially equivalent. In the standard method, an implementation of the knockoff filter is fully defined by a valid knockoff matrix and a recipe for computing -statistics satisfying the sufficiency and antisymmetry properties. In the whitening method, an implementation is fully defined by a diagonal matrix along with a recipe for computing a hypothesis ordering and values from and . We will show that the implementations of each method are essentially in one-to-one correspondence with each other, using a coupling between and .

To begin our analysis, assume that is a valid knockoff matrix with , which can be constructed for any (Barber and Candès,, 2015), and assume all . Set , so .

Following a conditioning argument in Barber and Candès, (2019), if we add and subtract from we obtain a useful -variate Gaussian statistic whose mean and variance follow from :

| (5) |

It is suggestive that by rescaling the second component in (5) we obtain , which is the desired distribution for . Pursuing this ansatz, set

| (6) |

Because is ancillary and is complete sufficient in the submodel where is known, it follows by Basu’s Theorem that is independent of . As a result we have and

Next we relate the whitening method’s exploratory stage to a slight relaxation of the sufficiency and antisymmetry properties.

Proposition 1.

For define

| (7) |

If satisfies the sufficiency and antisymmetry properties, then depends on only through the unordered pairs . In terms of the coupling defined by (6), if satisfies the sufficiency and antisymmetry properties then depends on only through and .

The first claim of Proposition 1 is proven in the supplement of Barber and Candès, (2019) but we provide a full proof here for expository purposes.

Proof.

By the antisymmetry property we have

so for all including .

By the sufficiency property, only depends on through , so the same is true of . But we have just seen that is invariant to swapping with , which amounts to swapping with without changing . In other words, depends on only through the unordered pairs , for .

For the coupling in (6), we have and . Hence, observing and is the same as observing and , which is the same as observing the unordered pairs. ∎

We will say that satisfies the unordered pair property if depends on only through for . This condition relaxes the sufficiency and antisymmetry properties because it allows for to have unrestricted dependence on and . With these relationships established, we are now prepared to prove formal equivalence.

Theorem 1.

Assume that and let be a knockoff matrix with . Let and define as in (6). Then

-

(a)

For any implementation of the whitening method, we can construct -statistics satisfying the unordered pair property so that the two methods give identical rejection sets.

-

(b)

For any -statistics satisfying the unordered pair property such that are almost surely positive with no ties, we can construct an implementation of the whitening method so that the two methods give identical rejection sets.

Proof.

For (a), take , for . Recalling that , we have , so depends on only through and , satisfying the unordered pair property.

For (b), because the method depends on only through the ordering of its coordinates, we can assume without loss of generality that is a permutation of . Take to be the index of the th largest value, so that , and set , which is a function of and . Then we again have .

To see why the two methods return the same rejection sets when , note first that . As a result

For other values of , , where is the integer ceiling of . Therefore, and the rejection sets are the same.

∎

Because the whitening method controls FDR, Theorem 1 implies that the unordered pair property is a sufficient condition for the standard knockoff filter to control FDR as well, relaxing the sufficiency and antisymmetry properties. The requirement in (b) that all be positive and distinct is not really necessary; we could break ties or generate “signs” at random, or generalize the whitening method so that is only calculated for a subset of corresponding to the indices where is positive and decreases. We ignore these generalizations for the sake of brevity because they can only reduce the number of rejections.

As Theorem 1 shows, any implementation of the standard method is achievable with the whitening method. It follows that any uniform bound on TPR for all implementations of the whitening method is also a uniform bound for all implementations of the standard method.

2.2 The oracle analyst and the knockoff* procedure

Throughout the rest of Section 2, we consider the perspective of an oracle analyst with full knowledge of . To bound the power of this analyst we work backwards from the end of the procedure. In this section we discuss how the oracle analyst can make optimal decisions in the exploratory analysis of Stage 2, and in Sections 2.3–2.4 we apply our analysis to understand the ramifications for choosing .

The analyst’s task in Stage 2 is to choose alternative directions and a hypothesis ordering , after observing and . To choose , recall that only if . As a result, an analyst who knows will always set , unless in which case makes no difference and can be chosen arbitrarily. Then the best possible ordering of variables is in decreasing order of the conditional log-odds:

| (8) |

Because is continuous, the values for nonzero are almost surely positive and distinct, whereas if then too. Define the knockoff* procedure to be any method that sets if and arbitrarily otherwise, and returns an ordering with

The relative ordering of the null hypotheses is also arbitrary. We show next that the knockoff* procedure maximizes the TPR among all implementations using the same .

Proposition 2.

Conditional on and , both the TPP and the expected total number of rejections for the knockoff* procedure are stochastically larger than they are any other implementation with the same . Consequently, the knockoff* procedure maximizes both the TPR and the expected number of rejections.

While there is some ambiguity in defining the knockoff* procedure concerning the alternative direction and relative ordering for the null indices, the statement of Proposition 2 applies to any version of it, implying in particular that any two versions of knockoff* have the same TPR. The proof, given in Section 6, uses the following useful formula for the number of rejections as a function of . Because we must have ,

| (9) |

Next, we develop tools for bounding the power of the knockoff* procedure. If we write the order statistics of as , then we can obtain upper bounds on the TPR of any knockoff procedure by bounding the knockoff* procedure which has for all .

Roughly speaking, for knockoffs to make rejections, we must see at least times as often as near the beginning of the list, so the largest values must exceed ; Proposition 3 gives a simple result relating these quantities. For , define the random walk

and let .

Proposition 3.

Conditional on , the number of rejections for any knockoff procedure at FDR level is stochastically smaller than for , .

Proof.

Conditioning on and , define , and . Then for the knockoff* procedure,

The number of knockoff* rejections is , where is the largest index with

Next, define auxiliary random variables and construct the random walk whose first increments are . Then , so we have almost surely . ∎

In particular, Proposition 3 implies that in any asymptotic regime where , the number of knockoff rejections is for any FDR level .

While Proposition 3 can help build our intuition about the role of the log-odds threshold , it is not a strong enough result to control the power of an oracle analyst, who can always take and force for a single promising variable . The next result generalizes Proposition 3, showing that knockoff* can expect no more than rejections when there are fewer than large log-odds.

Proposition 4.

Fix a significance level and margin . Conditional on , the expected number of rejections for any knockoff procedure at FDR significance level is upper bounded by , where and are constants that depend only on and . In particular, if and if

then for any knockoff procedure at any FDR significance level.

We defer the proof of this proposition to Section 6, where we also give explicit formulae for the constants and . For example, when and , we have and . These constants are not optimal and better bounds can be obtained for specific values by simulating the random walk with and .

Whereas Proposition 4 bounds what is possible after whitening and observing and , the next section analyzes when it is impossible to carry out the whitening step without dramatic information loss that prevents the values from being large enough. We will show that this loss is determined by the eigen-decomposition of , and characterize how large the signal must be to overcome this information loss and achieve nontrivial TPR, and illustrate our analysis with examples.

2.3 Lower bounds for : how much noise must we add?

Because the power of any knockoff procedure can be upper bounded by the knockoff* procedure from the previous section, understanding the best attainable power of knockoffs is a matter of investigating the joint distribution of the values, which are independent of with distribution

| (10) |

The distribution of depends on the ratio of two quantities: the signal-to-noise ratio (SNR) , and the diagonal entry . Since is stochastically increasing in , so is . As a result, the marginal power of the knockoff* procedure is strictly increasing in each . We will be primarily interested in the standardized case where ; in that case , so knockoffs will (potentially) have power when the squared SNR is large compared to the whitening noise.

Although most knockoff methods seek roughly to balance the whitening noise across the coordinates, if we want to bound the power of the best possible knockoff method we must consider the possibility that the analyst will favor some variables over others. For example, it is always possible to drive a single , but only at the cost of driving for all with , since we must have

Thus, while it is always possible to make any one small, it is sometimes impossible to make them all small at the same time. In this section we derive explicit lower bounds for the order statistics of as functions of , uniformly over all diagonal matrices . Let be the leading eigenvalue of , with eigenvector . For any subset , we must have , for the corresponding matrix blocks. As a result,

Therefore

and we have

| (11) |

To interpret equation (11), suppose that the entries of the unit vector are all at least as large as , for some . Then for any block , we must have . Taking to be the set with the smallest entries, it follows that the th smallest diagonal entry of is at least . Extending this argument yields explicit lower bounds for order statistics of , in terms of .

Proposition 5.

Let be the eigenvalues of , with corresponding eigenvectors , and let be the order statistics of , and let be the order statistics of the diagonal entries of . Then for all , we can lower bound

| (12) |

Proof.

Note that in the argument for the lower bound (11), we can just as well replace with for any . If is the index set for the smallest diagonal entries of , then

Maximizing the lower bound over gives the result. ∎

By construction, we have , and also for all . Continuing the example from above, we will have .

In the MCC case with and , we have exactly for all . These bounds are nearly tight: for any size- subset , the leading eigenvalue of is

Then for any , we can set

but if we take we must have for every . In other words, we can “rescue” our favorite variables from having , as long as we are willing to give up completely on the other .

2.4 Uniform bounds on the power of fixed- knockoffs

Theorem 2 combines Propositions 4 and 5 to obtain a finite-sample upper bound on the power of any fixed- knockoff procedure. We first give one more technical lemma:

Lemma 1.

Suppose that for , where , for some integer and . Then the expected number of values with is bounded by .

Whereas Proposition 4 controls the number of rejections in terms of the number of large values, Lemma 1 controls the number of large values we can get by chance from values falling below . We are now ready to prove our main result.

Theorem 2.

Let be the order statistics of and let be defined as in (12). For any target FDR level , let be the smallest integer such that

| (13) |

Then the expected number of rejections for any knockoff procedure at FDR level is upper bounded by , where and depend only on .

To sketch the proof, in expectation there are at most indices for which : with large , more with small , and more by chance; then applying Proposition 4 gives the final result. As discussed in the proof of Theorem 2, if we replace with in (13) then we eliminate the portion with large , so improves to , giving correspondingly smaller bounds. Table 1 shows the bounds at several levels of interest.

| Bound if | |||

|---|---|---|---|

| Bound if |

The dimension does not appear in the inequality (13), unless it plays a role in determining . For MCC, , so the number of rejections as grows no faster than the square of the SNR. If we set the signal strength at the Bonferroni threshold , then solving (13) gives , which we can plug directly into the bounds in the second row of Table 1. As a consequence, the TPR of any knockoffs method will tend to 0 if . By contrast, if converges to a nonzero constant, then we must have to achieve nontrivial TPR in the limit.

More generally, to apply Theorem 2 for a given covariance matrix at any signal strength, we can calculate the sequence using the formula (12), and plug the smallest satisfying (13) into Table 1.

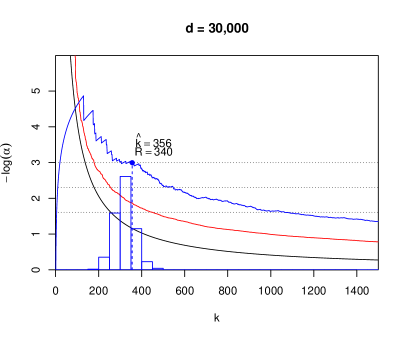

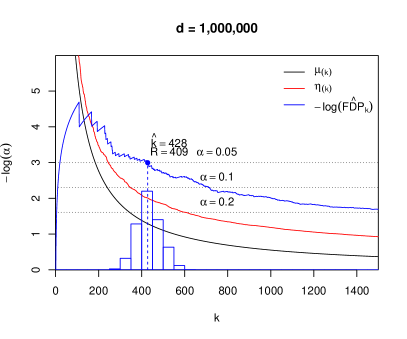

We can visualize the logic of Theorem 2 and obtain improved bounds for specific examples by simulation. If all nonzero values are set to a common value , then the th largest is no larger than . To simulate the knockoff* procedure, we sample the values according to (10), sort them in descending order, and then simulate the resulting process. Figure 1 illustrates two examples, with and , and with set at the Bonferroni threshold . We also set to simulate under the most optimistic conditions.333Alternatively we could choose a value for and set for , but it makes little difference if . We simulate the case and show along with a single realization of the and processes. In addition we plot a histogram showing the distribution of the number of rejections for .

|

|

Continuing the example from the previous section where , suppose that all nonzero coefficients take the same value . In that case, Theorem 2 implies that no knockoffs method can make more than rejections. If then no knockoffs method can make more than rejections, so knockoffs must have if . Thus, if converges to a nonzero constant, then for knockoffs whenever . Thus, knockoffs can underperform Bonferroni even in settings where the first eigenvalue asymptotically accounts for a vanishingly small fraction of the total variance. By contrast, if , then Theorem 2 does not necessarily suggest we will have a problem. As we will discuss in the next section, Theorem 2 gives especially optimistic predictions when because the oracle analyst is too powerful.

2.5 Stronger results with random non-null indices

While the bounds from Theorem 2 are nontrivial, they are still highly optimistic, since they allow the analyst to optimize not only the exploratory stage (equivalent to choosing perfect -statistics), but also the choice of (equivalent to the choice of knockoff matrix ), with full knowledge of the coefficients. In particular, suppose that the true coefficient vector is sparse with and . Then the analyst loses nothing by sending for all , effectively reducing the multiplicity of the problem to by giving up on the null variables before the method has even begun. Whereas we might find it plausible that the exploratory stage is highly efficient, especially when the signals are very strong and the -statistics are designed well, it is much less plausible that the analyst can discard all of the null variables even before observing any data. In any case, such a strategy is contrary to the spirit of knockoff methods that are actually in use, which seek to balance the (or ) values, spreading power across all variables.

We can force the oracle analyst into a more “honest” allocation of values by assuming the indices in are drawn uniformly at random from only after has been chosen. As before, we still assume is revealed to the analyst before the exploratory stage. Theorem 3 gives a directly analogous result to Theorem 2, with a similar proof.

Theorem 3.

Let be the order statistics of , and assume is a random permutation of the order statistics, independent of . Let be the non-null proportion, and define as in (12). For any target FDR level , let be the smallest integer for which

| (14) |

where is the integer floor. Then the expected number of rejections for any knockoff procedure at FDR level is upper bounded by , where and are the same constants as in Theorem 2.

We can tighten the bounds if we replace with in (13), just as with Theorem 2, so the bounds in both rows of Table 1 apply. Likewise, we can simulate better bounds just as we did in Theorem 2, with the modification that after calculating , we randomly zero out of the values. Algorithm 1 fully specifies a Monte Carlo estimate for the highest achievable TPR when the analyst only knows the order statistics when choosing .

By placing this mild limitation on the analyst’s otherwise-total omniscience, we dramatically strengthen the result from Theorem 2 in sparse problems. To illustrate, consider the bound from Table 1, the version of the bound as applied to . If we were applying Theorem 2, then to get , we would only need small values. By contrast, applying Theorem 3 we would need small values, since we can expect all but a fraction of them to be wasted on null indices. Pragmatically, even is not enough because the bounds in Table 1 are not optimal; to achieve we realistically need most of the values to be small.

Corollary 1 formalizes the sense in which Theorem 3 and Algorithm 1 both upper-bound the best achievable knockoff method. Let denote any valid implementation of fixed- knockoffs at FDR level , mapping its inputs to a randomized rejection set. Then we have

Corollary 1.

We finish by applying Theorems 2–3 to prove a simple corollary classifying asymptotic regimes where knockoffs underperform Bonferroni. Whereas other works commonly assume a specific limiting distribution for the covariance matrix (e.g. Liu and Rigollet,, 2019; Weinstein et al.,, 2017), we only impose a less stringent condition quantifying how “dense” the first eigenvector is. For , define the distribution function of the entries of , scaled by :

We have been analyzing the case where for some . For the next results, we will assume only that . If , the following corollary gives relatively weak conditions for when the best possible knockoff procedure must have for signals above the Bonferroni threshold.

Corollary 2.

Consider a sequence of problems with for which

-

(i)

has a distribution limit with no point mass at 0, i.e. .

-

(ii)

For some , for a subset of indices, and for the rest.

-

(iii)

Either and is uniformly random, or and is arbitrary.

Then

-

1.

The Bonferroni procedure at any level has , and

-

2.

If then any knockoff method at any level has .

Whereas negative results in prior works have focused on specific implementations of knockoffs under restrictive assumptions about the limiting distribution of the covariance matrix, typically under a polynomial sparsity regime ( for ), Corollary 2 holds uniformly over all possible design choices made by the analyst, makes only mild limiting assumptions about the leading eigenvalue and eigenvector of , and holds whenever .

3 Knockoffs for multivariate normal estimators

3.1 Implementing the whitening method

As we observed in Section 1.2, the whitening method can be defined without reference to any design matrix . If is any estimator of a -variate parameter with distribution and is known, or known up to a scalar multiplier, the whitening method can be applied directly. Theorem 4 in Section 3.2 shows that if is only asymptotically Gaussian with a consistent estimator , then the whitening method can also be applied directly using as a plug-in estimator, and the FDR will be controlled asymptotically (though we note that the result is limited to classical fixed-dimensional asymptotics).

By shifting our focus to the estimator , the whitening interpretation suggests easier solutions to closely related regression problems that do not easily lend themselves to introducing knockoff predictor variables. For example, if represents the population-risk-minimizing coefficients in a logistic regression, quantile regression, or robust regression with Huber loss, we can rely on well-established asymptotic normality results instead of trying to invent a novel framework for generating knockoff predictors in each new example.

Because of the one-to-one correspondence between methods in each formulation, we can even deploy state-of-the-art knockoff implementations, such as those in the knockoff package (Patterson and Sesia,, 2017), by constructing a pseudo-design matrix and pseudo-response using and .

Recalling that , and that is the counterpart of , a short calculation verifies that

so the distribution of the rejection set using and as inputs to any off-the-shelf knockoffs package is the same as it would be if the problem had been posed as a linear regression to begin with.

The whitening interpretation also suggests simpler methods like estimating and , and therefore also , by regularized likelihood or Bayesian methods using the known Gaussian likelihood for and . Because are missing, the log-likelihood is not necessarily concave, but the expectation-maximization (EM) algorithm can be used to impute the missing values. We defer these ideas to future work.

While the coupling in Section 2.1 gives a recipe for generating as a function of and , we can alternatively generate the noise directly using the residual variance . We can even relax the usual dimension requirement that , and require only that where . In that case let be any fixed matrix with , and set

| (15) |

or if . Here and are auxiliary random variables generated independently of the data and each other. Then is independent of because is, and Proposition 6 shows it has the desired distribution.

Proposition 6.

Define and as in (15). Then , and .

Proof.

If and then is immediate. If , independently generate and . Then it is a standard fact that the ratio is independent of . As a result,

Similarly, is independent of . As a result,

and setting gives the desired result. ∎

If we want the software package to generate the knockoff matrix for us, we can also do this as long as . Then we can generate

| (16) |

where is defined as in Proposition 6; then and as desired.

If , then part of is not used up in generating :

It is easily shown that and are mutually independent, so allowing the analyst to use in Stage 2 has no effect on the conditional inference in Stage 3.

The analogous quantity in the standard implementation is the residual variance from the augmented regression of on . Because is independent of , the unordered pair property could be immediately relaxed to a requirement that be a function of the unordered pairs and without affecting the FDR control proof. We note Chen et al., (2020) also suggested the possibility of using this quantity. One use for could be as an input to generalized cross-validation (Golub et al.,, 1979), and another could be as an aid in estimating and , as suggested above.

3.2 Knockoffs for an asymptotically normal estimator

In this section we give simple sufficient conditions under which the whitening method can be applied to any asymptotically normal estimator of a -variate parameter , along with a consistent covariance estimator . We consider a classical local asymptotic regime in which , for a local parameter and a quantity that we can think of as a sample size, and assume444There is nothing special about being -consistent; for example if we had we could just as well define the local parameter and repeat the argument in this section.

If we define , we have . It will be more convenient to work in terms of rather than ; note that the null and directional alternative hypotheses are the same if we define them in terms of or . For most implementations of knockoffs, there is a preprocessing step effectively standardizing either or to have unit diagonal entries, in which case applying the method to or would yield identical results.

We assume the analyst carries out knockoffs on according the usual whitening method, but plugging in for . Let denote the analyst’s choice of diagonal matrix based on . To generate the whitening noise, the analyst sets , where and independently of the data.

Once the noise has been generated, the method proceeds exactly as described in Section 1.2. That is, for

the analyst chooses alternative directions and an ordering based on and then carries out Selective SeqStep on the binary -values.

To impose some regularity on the exploratory analysis, we consider knockoff methods for which the exploratory stage can be defined in terms of non-negative random variables , along with

| (17) |

where flips the sign of its th argument and leaves the others fixed. The -statistics given in (17) are then used the same way the -statistics are used in the standard formulation of knockoffs: the variables are ordered by with , so . It is easy to see that is a function of and alone, so any statistic defines a valid implementation of the whitening method. This way of defining knockoffs is inspired by the “ signed max” statistic, which we can recover by setting

where is some regularized estimator of with penalty parameter , possibly in an augmented linear regression model for the response against the design matrix as defined above.

Let denote the -level rejection set for the knockoff method defined by and , as it would be applied to with whitening noise ; we will typically suppress the randomization variable . We say is a continuous knockoffs procedure if and are continuous functions of their arguments. In the fixed asymptotic regime under mild conditions, the rejection set converges to its distribution under exact Gaussian sampling, as we show next.

Theorem 4.

Assume that we carry out a continuous knockoffs procedure on the asymptotically normal estimator

where is nonsingular. Let

and assume that has Lebesgue measure zero. Then we have for any ,

where and independently. In particular, the FDR and TPR of converge to their values under exact normal sampling.

As an immediate application of Theorem 4, we see that continuous knockoff methods can be applied to any asymptotically normal maximum likelihood estimator.

Example 2 (Maximum likelihood estimation).

Suppose we observe a sample from a parametric family , where is a density with respect to a common dominating measure . Define the maximum likelihood estimator (MLE)

Assume further that is sufficiently regular so that for in the interior of ,

where is the Fisher information at . If is nonsingular and continuous at , and is continuous, then by Theorem 4, asymptotically controls the FDR at level .

One interesting special case of Example 2 is the logistic regression model where we observe predictors and binary response , and model for some . Then, just as in linear regression, we have a design matrix and response . If we think of knockoffs in terms of the standard formulation, we might be tempted to try generalizing it by adding some matrix of predictor variables and fitting a logistic regression on the augmented matrix . But it is unclear how to design such a matrix a priori, since the MLE solves the weighted least squares problem

In particular, it is the predictor variables’ weighted correlations with each other that determine the asymptotic distribution of , not the unweighted correlations as in linear regression. But to design a knockoff predictor whose weighted correlations with are the same as those of the real predictor , we would need to know , which determines the weights, ahead of time.

By contrast, if we view the MLE for linear regression as an asymptotically Gaussian random vector, we can simply treat it just as we would the OLS estimator for a linear regression, and treat the variance estimator as a consistent plug-in estimator for the asymptotic variance.

We caution, however, that asymptotic normal approximations can be unreliable in high-dimensional settings, particularly when . See e.g. El Karoui et al., (2013) and Donoho and Montanari, (2016) regarding the limitations of asymptotic normal approximation in high-dimensional M-estimation; El Karoui and Purdom, (2018) also cast doubt on the accuracy of the bootstrap in high dimensions. In particular Sur and Candès, (2019) showed that logistic regression is unreliable in high dimensions even with five to ten observations per predictor variable. As a result, we recommend applying this method only in settings where so the multivariate Gaussian approximation is reliable; determining the full range of application beyond the classical setting is outside the scope of this work.

3.3 Example: Analysis of stock market data

We now use an example from stock market data to illustrate the implementation of fixed-X knockoff when the test statistics are asymptotically multivariate Gaussian. Our goal is to test whether the daily returns of a given stock are predictable based on the one-day-lagged returns of the overall market, as measured by the Standard and Poors (S&P) 500 index. We use S&P 500 data from February 2013 to February 2018555Source: https://www.kaggle.com/camnugent/sandp500, totalling 1259 trading days, and restrict our analysis to the stocks that belonged to the S&P 500 over the entire period considered. For each stock, we test whether its excess returns relative to the market are correlated with the one-day-lagged market returns.

For , let denote the price of stock on day , and let denote the level of the S&P 500 index on day . Then for , the return for stock on day is

Our parameter of interest for stock is the Spearman (rank) correlation of its excess return, relative to the market, with the one-day-lagged market return:

and denotes the Spearman correlation. Roughly speaking, if then stock is a “good bet” today if the market performed well yesterday and a “bad bet” otherwise, and if the reverse is true. Because economic theory suggests stock returns should be unpredictable, we expect most of the true correlations to be close to 0. We will test against the two-sided alternative for .

We define the problem in terms of excess returns instead of “raw” returns for two reasons: First, predictability of excess returns is more easily translated into a trading strategy, since an investor could hedge their bets against the market, giving another reason for most to be small. Second, the pairwise correlation between stock returns for any two stocks is usually positive, since good or bad news about the economy at large tends to move all stocks in the same direction. As a result, the leading eigenvalue and eigenvector of mimics the leading eigenvalue and eigenvector for MCC, giving knockoffs no chance to perform well. The common market factor is so strong, accounting for almost half the total variance, that it is doubtful whether FDR is even the right error rate to control (Efron,, 2007; Schwartzman and Lin,, 2011; Kluger and Owen,, 2021). By contrast, the excess returns do not exhibit the same sort of positive correlation because we have removed it by subtracting off the market index return.

To test the hypotheses, we calculate the sample Spearman correlations , and use the bootstrap to obtain a nonparametric estimator for the covariance matrix ; which has similar structure to . Because the autocorrelations of are small, we use the i.i.d. bootstrap, but we obtain similar rejection sets if we use the block bootstrap for block length 15 or 50 (blocks of three or ten weeks respectively). The bootstrap resampling is repeated 10,000 times. By inspecting the normal Q-Q plot of the sample Spearman correlation across bootstrapped samples, we find that the asymptotic Gaussian approximation fits the bootstrap distribution reasonably well even in the tails where rejections occur, at least marginally for each stock. We use the formulation in the previous section to implement the fixed- knockoff treating as an asymptotically Gaussian estimator of . We use the lasso signed-max method with SDP knockoffs.

The leading eigenvalue of the bootstrap correlation matrix is 53, accounting for about 11% of the total variance, and the entries of the leading eigenvector are dense but roughly symmetrically distributed around zero, ranging from to . Thus, the eigenstructure does not rule out a well-designed implementation of knockoffs performing well but it may nonetheless be worrisome.

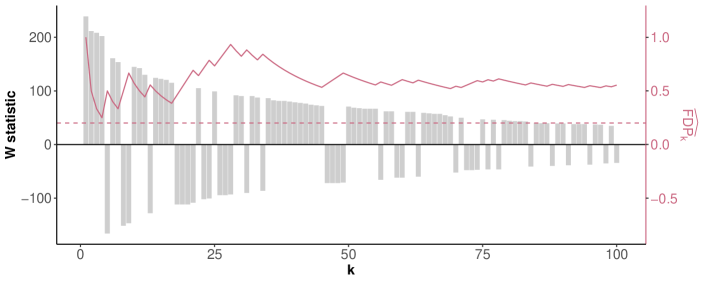

Given the estimated correlation matrix, we use the procedure in Section 4.2 to implement the fixed-X knockoff. Since this requires generating additional Gaussian noise, we repeat the procedure 30 times to obtain more stable rejection sets, and report hypotheses that are rejected for at least 50% of times. This stability selection criteria is similar to that proposed in (Ren et al.,, 2020). We found that at FDR level , knockoff obtains no rejections for 26 out of 30 trials. The other 4 times, there are 7 rejections on average, and the stocks BA, BRK.B, MDLZ and UAA are always rejected. As such, no stocks meet the stability selection threshold. By contrast, both the BH and the Bonferroni correction makes a number of rejections, with the BH making 11. The stocks rejected by the BH and the Bonferroni correction are summarized in Table 2.

Figure 2 shows the -statistics and along with from a representative trial. We find that there are many negative statistics in the front of the list, indicating that knockoff will not have many rejections even if the significance level is reasonably relaxed. We see in Section 5.3 that we could have anticipated this underperformance by inspecting the values.

| Method | Rejections at (stock tickers) | Additional rejections at |

|---|---|---|

| BH | 7 (AVGO, BA, BRK.B, JEC, MOS, SWKS, UAA) | 4 (FISV, KORS, V, WAT) |

| Bonferroni | 3 (BRK.B, JEC, MOS) | 0 |

| Fixed- knockoff | 0 | 0 |

|

4 Numerical results

4.1 Fixed knockoff for Gaussian linear model

In this section, we simulate under the Gaussian linear model to compare scenarios where the TPR of the best achievable knockoff method is close to zero against similar scenarios where knockoff methods perform well. For the design matrix , we generate random matrices whose rows are generated i.i.d from . We consider the following two regimes:

-

(a)

Positively equi-correlated OLS estimator is an equicorrelation matrix with correlation , i.e. , and ;

-

(b)

Positively equi-correlated covariates is an equicorrelation matrix with correlation .

In regime (a), the columns of are negatively correlated and the OLS test statistics are positive correlated, and we expect that any knockoff methods will have trivial power. In regime (b), the columns of are positively correlated and the OLS test statistics are negatively correlated.

We choose and . For each , we fix one realization of the random matrix, and then normalize its columns to obtain the design matrix . Next, we generate the response as follows. First, to define , we choose coefficients uniformly at random and let for each of the selected coefficients. We then generate , where are i.i.d standard normal errors. The above data generating procedure is repeated 600 times for each .

For each design matrix , we generate the knockoff matrix using the MVR-knockoff (Spector and Janson,, 2020) and SDP-knockoff algorithms (Barber and Candès,, 2015). For each instance of , we first consider the knockoff* procedure introduced in Section 2.2, which is the best achievable knockoff method once the knockoffs have been constructed, but is infeasible since it can only be carried out with knowledge of the true coefficients . We also consider a practically feasible knockoff method which uses the maximum lasso penalty level as test statistic.

In addition, we include the T3-knockoff* “procedure” from Section 2.5, a simulation-based bound of any knockoff method under the assumptions of Theorem 3, where the analyst is not allowed to know the nonzero indices of at the time of determining the knockoff matrix (or equivalently, determining ). is still revealed to the analyst immediately after the knockoffs are generated so the analyst can carry out the knockoff* method. T3-knockoff* is defined in Algorithm 1 and uniformly upper bounds the power achievable by SDP-knockoffs or MVR-knockoffs in any setting where is random with an exchangeable distribution over the indices, so it is more optimistic than SDP-knockoff* or MVR-knockoff*.

Finally, we consider the BH procedure and the Bonferroni test on OLS -values for baseline comparison. Note that the BH procedure is not theoretically guaranteed to control the FDR at the desired level unless the columns of are orthogonal.

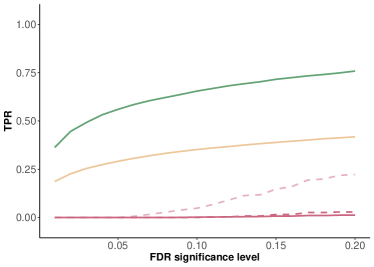

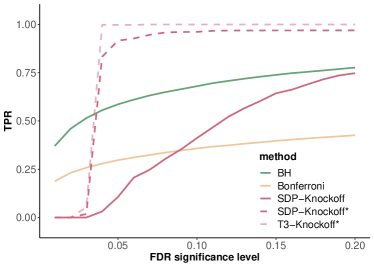

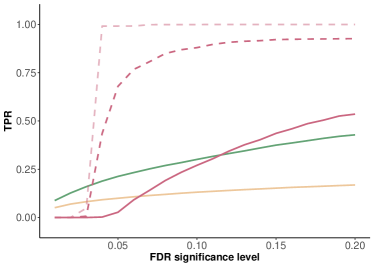

We obtain the SDP-knockoff matrix using the knockoff package (Patterson and Sesia,, 2017), and the MVR-knockoff using the knockpy package (Spector and Janson,, 2020). For both knockoff matrices, we then compute the the maximum lasso penalty level statistics with the knockoff package. Overall, the performance of knockoff shows a stark contrast under these two regimes, while the performance of BH and Bonferroni appear to be much more stable. Figure 3 shows the power of the BH, the Bonferroni and the SDP-knockoff tests. For reference, we also include the case where the design matrix is i.i.d. Gaussian. We find that the SDP-knockoff outperforms the BH method when the covariates are independent. However, we see that when the OLS test statistics are positively correlated, the TPRs of the oracle knockoff methods are close to zero. Table 3 shows the FDR and TPR of all methods for targeted FDR level and . We find that the TPR of SDP-knockoff* is smaller than 0.02 when controlling the FDR at 0.2.

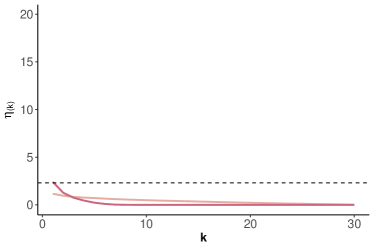

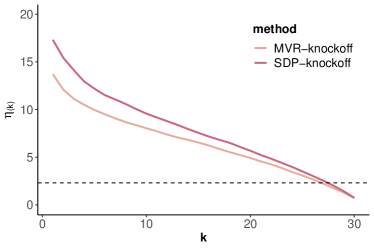

We can understand the performance of knockoffs in each case by plotting the sorted log-odds values , as we do in Figure 4. While the knockoff* method can achieve the sorting pictued in Figure 4, feasible knockoff methods cannot achieve a perfect ordering because is unknown. Recall that when the covariance matrix of the test statistics has factor model structure, the whitening step of knockoff destroys virtually all the information, and the log-odds of observing small -values in the inference cannot rise above . This is again confirmed by Figure 4, which shows the average of the largest log-odds across different trials. The rest of the log-odds are zero since the corresponding coefficient is zero. In particular, we find that most of the log-odds are smaller than with . Thus by Proposition 4, the number of rejections of any knockoffs method must be small.

4.2 Knockoff for multivariate Gaussian statistics

In Section 1.2, we reinterpreted the knockoff method and generalized the fixed-X knockoff procedure to multivariate normal test statistics. Here we use simulations to investigate the performance of different methods for testing the means of multivariate normal, and hint at the possible use cases and limitations of knockoffs for such problems.

We generate dimensional multivariate Gaussian vectors . The mean vector is generated in the same way as the linear coefficient in the previous simulation, except that the non-zero means are set to 3.5. We consider two types of covariance matrices:

-

(a)

has factor model structure. In particular, we let

(18) where are drawn independently from the uniform sphere.

-

(b)

has factor model structure, i.e.

(19)

In particular, we choose and . We normalize the covariance matrix such that has unit diagonal entries. After normalization, the largest eigenvalue of is approximately 19 and 75 for and 100, respectively (the sum of all eigenvalue is ). For each setup, we consider one fixed realization of the random matrix . In each trial of our simulation, we first generate the mean vector and then the multivariate normal vector .

For each matrix , we repeat the above data generating procedure times. Again, we consider both the SDP knockoff and the equi-correlated knockoff to create the diagonal matrix that satisfies . For each diagonal matrix , we first implement the oracular ordering and the associated knockoff* procedure defined in Section 2.2. For each observed , we generate a pseudo-design matrix and pseudo-response as in (16).

Table 4 shows the FDR and TPR of different methods for . As expected, we found that the power of even the best achieveable knockoff method is less than that of Bonferroni when the covariance matrix has a factor model structure with reasonably large leading eigenvalue. This suggests that the knockoff-type approaches suffer from severe power loss when applied to general test statistics with factor model structure. However, when the precision matrix has a factor model structure, it may be possible to use the knockoff framework procedure to design a test with superior TPR than baseline methods such as the BH. We leave this for future research.

|

|

| (a) Positively equi-correlated OLS estimator | (b) Positively equi-correlated covariates |

|

| Reference: i.i.d Gaussian covariates with non-null . |

|

|

| (a) Positively equi-correlated OLS estimator | (b) Positively equi-correlated covariates |

| SDP-knockoff | MVR-knockoff | Other methods | |||||

|---|---|---|---|---|---|---|---|

| Knockoff* | Maximum penalty level | Knockoff* | Maximum penalty level | BH | Bonferroni | ||

| FDR | 0.00 | 0.00 | 0.00 | 0.00 | 0.09 | 0.01 | |

| TPR | 0.00 | 0.00 | 0.00 | 0.00 | 0.65 | 0.35 | |

| FDR | 0.00 | 0.01 | 0.00 | 0.00 | 0.18 | 0.02 | |

| TPR | 0.03 | 0.00 | 0.02 | 0.01 | 0.76 | 0.42 | |

| SDP-knockoff | MVR-knockoff | Other methods | |||||

|---|---|---|---|---|---|---|---|

| Knockoff* | Maximum penalty level | Knockoff* | Maximum penalty level | BH | Bonferroni | ||

| FDR | 0.06 | 0.07 | 0.05 | 0.06 | 0.10 | 0.01 | |

| TPR | 0.96 | 0.44 | 0.95 | 0.44 | 0.68 | 0.36 | |

| FDR | 0.16 | 0.17 | 0.15 | 0.16 | 0.19 | 0.01 | |

| TPR | 0.97 | 0.77 | 0.96 | 0.74 | 0.78 | 0.43 | |

| SDP-knockoff | MVR-knockoff | Other methods | |||||

|---|---|---|---|---|---|---|---|

| Knockoff* | Maximum penalty level | Knockoff* | Maximum penalty level | BH | Bonferroni | ||

| FDR | 0.00 | 0.04 | 0.03 | 0.05 | 0.19 | 0.01 | |

| TPR | 0.54 | 0.18 | 0.70 | 0.36 | 0.77 | 0.42 | |

| FDR | 0.00 | 0.02 | 0.00 | 0.00 | 0.18 | 0.01 | |

| TPR | 0.21 | 0.05 | 0.23 | 0.07 | 0.77 | 0.41 | |

| SDP-knockoff | MVR-knockoff | Other methods | |||||

|---|---|---|---|---|---|---|---|

| Knockoff* | Maximum penalty level | Knockoff* | Maximum penalty level | BH | Bonferroni | ||

| FDR | 0.18 | 0.20 | 0.18 | 0.19 | 0.19 | 0.02 | |

| TPR | 1.00 | 0.71 | 0.99 | 0.70 | 0.76 | 0.41 | |

| FDR | 0.18 | 0.15 | 0.19 | 0.17 | 0.19 | 0.02 | |

| TPR | 0.99 | 0.45 | 0.99 | 0.48 | 0.77 | 0.41 | |

5 Discussion

5.1 Knockoffs, randomized responses, and the selection-inference tradeoff

Viewing knockoffs as a conditional post-selection inference method sheds light on what Fithian et al., (2014) called the selection-inference tradeoff: that the more we condition on, the less data remains for confirmatory analysis. This tradeoff is most obviously apparent in the case of data splitting, where the analyst selects a model or hypotheses to test by means of some exploratory analysis using a fraction of the data points, and then carries out confirmatory inference using only the remaining fraction, i.e. inference conditions on the initial data set (this assumes the two data sets are independent; otherwise data splitting may be invalid). A similar phenomenon is present in other conditional post-selection inference problems, where whatever statistics of the data we observe in the selection (exploratory) stage are unavailable as inferential evidence in the conditional inference (confirmatory) stage.

Compared to most other conditional inference methods, knockoffs conditions on much more about the data, holding out only the randomized and binarized for confirmatory inference. What is more, because under , the binary conditional -values can never be smaller than . The reason knockoff methods are nevertheless able to compete with and sometimes outperform other state-of-the-art multiple testing methods is because the FDR is an aggregate error criterion: to control it, knockoffs need never be confident about rejecting any individual hypothesis, only about the fraction of nulls early in the list. As a result, no individual needs to be minuscule, so long as most of the highly prioritized ones are .

By giving up on making each powerful, knockoffs is able to use nearly all of the information in to supercharge the more flexible exploratory stage, betting on its ability to pack the front of the priority list with non-null hypotheses. This strategy of “betting on exploration” can pay off especially handsomely when Bayesian priors or structural assumptions like sparsity can be brought to bear during the exploration, which can use them in an unfettered way.

The whiteout phenomenon we describe here is an example of where that bet goes wrong, leaving too little information for inference. The fundamental problem is that the inference engine, Selective SeqStep requires independent binary -values, which can only be created by adding enough noise to make diagonal. If is “too far from diagonal” in the sense we describe, then this cannot be done without destroying the signal.

It may seem counterintuitive that adding more noise (larger ) means using up more data for selection and leaving less for inference. In most methods that use randomized data for exploration, such as Tian and Taylor, (2018), the opposite is true: adding more noise hides more information from the selection algorithm, preserving it for confirmatory inference. The difference is that, in knockoffs, the information “left over” after randomizing is also given to the analyst at exploration time, in the form of . Instead it is the randomized that is (partly) held out for inference.

We could equivalently define the whitening method in terms of Gaussian noise

viewed as a noisy version of , and viewed as the residual information. From this perspective, the “noise variance” is , so that more noise (smaller ) once again means holding out more information in the form of .

5.2 The whitening interpretation and Spector and Janson, (2020)

Our whitening interpretation sheds potentially interesting light on the phenomenon recently discovered by Spector and Janson, (2020) when is an equicorrelated covariance matrix with diagonal entries equal to and off-diagonal entries equal to . In this example the maximum eigenvalue of is , so there is no “whiteout” problem, but the authors find that both equicorrelated and SDP knockoffs struggle to make any rejections. To understand why, note that both methods would set , so and . As a result, in the exploratory analysis the analyst observes

Because only and are identifiable from the exploratory data set, the analyst has no way to make an educated guess about . This problem can be resolved by choosing , or , more judiciously, as Spector and Janson, (2020) show.

5.3 Power analysis in knockoffs

One takeaway message of Section 2 is the crucial role played by the threshold in knockoffs methods’ performance. If

| (20) |

then we are more likely than not to observe , since . In that case, even if we guess the alternative direction right we will still have

| (21) |

so variable will be a net drag on the FDP estimator’s struggle to remain below .

This observation can help us to do rudimentary power analysis at various stages of the procedure. For example, before we observe anything about the response vector , we can inspect the diagonal entries of the matrix and ask how large would have to be for us to have reasonable power to detect variable . Doing a little algebra on inequality (20), we arrive at

| (22) |

We can think of (22) as giving a critical threshold for the SNR of variable . For example, suppose , so . Then if (or equivalently ), should be larger than if we want to be above most of the time. Likewise, if (), then the critical SNR threshold is about 4 for .

Importantly, because this variable-by-variable power analysis can be done before we observe anything about , we can still change course if we don’t like the values we get — we could either choose a different knockoff matrix or abandon the knockoffs framework and use BH instead, without any threat to either method’s FDR control guarantees.

Whereas our theoretical results emphasize lower bounds on , for an analyst intending to use knockoffs the more interesting question is how large each actually is in the specific knockoff matrix they are about to use for their problem. Until more is understood about what regimes lead knockoffs to dominate BH or vice versa, we recommend that analysts at least inspect the values in light of these SNR thresholds as a diagnostic tool. If, say, only a few of the values are below , then the matrix may not be a suitable problem structure for knockoffs. In our stock market example, only two values are below and only are below , suggesting that only very strong signals have a good chance of generating rejections.

5.4 Concluding remarks

We emphasize once again that the results we derive for these asymptotic regimes do not imply that fixed- knockoffs are underpowered as a general rule. On the contrary, we believe our results are interesting precisely because the opposite is true: there are many problems where existing fixed- knockoff methods outperform all other known FDR-controlling methods. In particular, BH and knockoffs represent two completely different approaches to multiple testing in regression or with multivariate normal test statistics. To give practitioners appropriate guidance about which one to use, more work is needed to answer several crucial questions: When do knockoff methods outperform the BH procedure, and which implementations perform the best? How can practitioners recognize which is better for their context? Can hybrid methods such as those of Sarkar and Tang, (2021), or methods yet to be developed, balance the tradeoffs between the two approaches, preserving the strengths of the knockoffs framework without suffering its drawbacks? By identifying pitfalls for the knockoffs framework our results represent strides toward a more complete understanding of multiple testing in the linear model.

6 Proofs

6.1 Proof of Proposition 2

See 2

Proof.

If there is nothing to prove, so assume . Given , , and , the conditional -values are independent with

If we hold the ordering fixed, the rejection set is stochastically increasing in each of the above log-odds, so the TPP is always made stochastically larger by setting whenever . We can therefore restrict our attention to the case where the log-odds for each variable is .

Next, define the indicator . If , then swapping the two leaves fixed for all , but increases the conditional probability that given . Therefore, is stochastically largest when the log-odds are arranged in decreasing order. The same is true for the number of rejections .

Likewise, if then must be non-null, so conditional on the number of rejected non-null hypotheses is also made stochastically larger by arranging the log-odds in decreasing order. ∎

6.2 Proof of Proposition 4

For any and , we define

We will now prove the following proposition, which is stronger and more precise than Proposition 4.

Proposition 7.

Suppose that

where . Define

and

where

Then the expected number of rejections for any knockoff procedure at FDR significance level is upper bounded by .

Proof.

Consider the random walk

Then by (9), for any knockoff procedure, the number of rejections is upper bounded by , where

Consider another random walk

Note that

Since , we know that is stochastically smaller than , where . Therefore is stochastically smaller than Therefore

| (23) |

Define

Let , and then

| (24) | ||||

Therefore, combining Equations LABEL:eq:lasthittingtime and 23, we have

Recalling the definitions of and , we have

Therefore we have . Turning to the second term, by Lemma 4 we have

| (25) |

Note that we can bound the summation by (note that )

| (26) |

where

The first equality above is obtained by change of variable . Therefore,

Thus

and the proposition is proved. ∎

6.3 Proof of results in Sections 2.4–2.5

See 2

Proof.

Assume without loss of generality that , so we have for all that

If , then we have

Define

At most indices have , so the total number of indices with is at most . If , then we have

| (27) |