Robust Clearing Price Mechanisms for Reserve Price Optimization

Abstract

Setting an effective reserve price for strategic bidders in repeated auctions is a central question in online advertising. In this paper, we investigate how to set an anonymous reserve price in repeated auctions based on historical bids in a way that balances revenue and incentives to misreport. We propose two simple and computationally efficient methods to set reserve prices based on the notion of a clearing price and make them robust to bidder misreports. The first approach adds random noise to the reserve price, drawing on techniques from differential privacy. The second method applies a smoothing technique by adding noise to the training bids used to compute the reserve price. We provide theoretical guarantees on the trade-offs between the revenue performance and bid-shading incentives of these two mechanisms. Finally, we empirically evaluate our mechanisms on synthetic data to validate our theoretical findings.

1 Introduction

A fundamental problem in auction design is the question of setting a reserve price to optimize revenue. In a data-rich environment like online advertising, it becomes possible to learn an effective reserve pricing policy by drawing on past bidding data (Paes Leme et al., 2016). Under simplifying assumptions such as i.i.d. bidders and a monotone hazard rate, the form of the optimal reserve price in a single-item auction has been well understood since the seminal work of (Myerson, 1981). Reserve prices are still a revenue-optimal mechanism when these assumptions are relaxed, but they become challenging to implement both in theory (Morgenstern and Roughgarden, 2015) and in practice due to the nonconvexity of the optimization problem (Medina and Mohri, 2014).

Nonetheless, in practice simple pricing strategies such as using some fixed quantile of historical bid distributions have been found to work well (Ostrovsky and Schwarz, 2011), even if they are not technically optimal. In this paper, we consider a generalization of quantile-based reserve pricing recently proposed by (Shen et al., 2019), whereby a market-clearing price fit to historical bid data is used as a reserve price going forward. Much previous work uses personalized reserve prices, where each bidder sees a different price; this is largely motivated by the fact that when bidders values are not i.i.d. the optimal auction uses personalized reserves (Myerson, 1981). The current standard in online display advertising, however, is to use an anonymous reserve price common to all bidders. Shen et al. (2019) show that fitting a clearing price to historical bids, using an appropriate convex loss function, leads to an effective anonymous reserve price with a favorable trade-off between revenue and match rate, compared to nonconvex surrogate losses that aim to directly optimize revenue (Medina and Mohri, 2014).

However, a key concern with this approach (and with learning approaches more generally), is that bidders may be motivated to misreport if this leads to a more favorable reserve price in the future. That is, an auction such as a second price auction with fixed reserve, which is truthful in a single shot, may no longer be truthful in a repeated setting with dynamically updated reserve prices. Advanced bidders may take advantage of this fact (Nedelec et al., 2019). In this work, we therefore ask to what extent a reserve pricing policy such as clearing prices can be made robust to bidder manipulations: bidders may still be able to effect future reserves, but the effect may be muted enough to make misreports hardly worthwhile. To add a measure of robustness to the mechanism, we consider two simple schemes, one based on techniques used in differential privacy (McSherry and Talwar, 2007) and the other based on smoothing techniques.

Our Contributions. We propose two robust clearing price (RCP) mechanisms: a differentially private RCP mechanism (DC-RCP) and a smoothing RCP mechanism (sRCP). We provide analytical characterizations of their performance to confirm that they can both effectively balance revenue and incentives.

For the DP-RCP mechanism, we first give a revenue guarantee in Theorem 3.2 relating the performance of the noisy reserve to the original clearing price. To obtain a nuanced characterization of the incentives of DP-RCP, we consider an incentive compatibility metric recently proposed by (Deng et al., 2020). This metric is tailored to quantifying the incentives towards uniform bid shading, a common strategy in online advertising where bids are simply values scaled down by a fixed constant factor. In Theorem 3.3 we provide an exact characterization of the IC metric of DP-RCP and find that it is directly related to the quantile chosen for pricing in the single bidder setting.

DP-RCP requires random drawn noise for each auction, which may cause it to be problematic to use in practice. To handle this issue, we propose a smoothing RCP (sRCP) mechanism, where we add noise to the training bids to compute the reserve price. We characterize the revenue guarantee (Theorem 4.2) and IC-metric (Theorem 4.3) for the sRCP mechanism, in terms of the magnitude of the noise. Theoretically, we show sRCP achieves better revenue guarantee ( revenue loss) than DP-RCP ( revenue loss), in terms of the magnitude of the noise in Theorem 4.2.

We validate our theoretical findings by simulating the two RCP mechanisms over synthetic bid data generated from lognormal distributions. We consider Laplace noise to make the mechanisms robust. We find that the two RCP mechanisms have different tradeoff between revenue and IC-metric for different settings, e.g., whether to choose a conservative quantile to compute clearing price in the single-bidder case. For a suitably chosen parameter (i.e., , defined in Eq. (3), which is used to control how aggressive the clearing price is, by generalizing the choice of quantile) for computing clearing price, sRCP achieves a better tradeoff between expected revenue and IC-metric than DP-RCP.

Related Work. There is a rich and growing literature on learning algorithms for pricing in auctions. With respect to this paper, related work can be categorized along two dimensions: batch vs. online access to data, and whether bidders are myopic in their bidding. Our work considers batch learning of anonymous reserve prices under non-myopic bidders.

In the batch setting, starting with the work of (Cole and Roughgarden, 2014), several works have studied the theoretical design of approximately optimal mechanisms based on historical samples of bidder values (Balcan et al., 2019; Devanur et al., 2016; Morgenstern and Roughgarden, 2015), with a focus on the complexity of the problem. A parallel line of research in machine learning develops learning algorithms for reserve prices based on historical batch samples of bids or values. (Medina and Mohri, 2014; Paes Leme et al., 2016) show how to learn reserve prices in lazy second price auctions, while (Duetting et al., 2019) learn optimal multi-item auctions using deep learning, subject to incentive compatibility constraints. Most closely related to our work, (Shen et al., 2019) propose a reserve pricing policy based on learning the clearing price from historical bids. In (Deng et al., 2021) the authors examine the tradeoffs between revenue and incentives for different reserve pricing policies, just as we do in this work; whereas we consider smoothing techniques on a specific reserve pricing policy, their approach is to use mixtures of policies. A loosely related work by (Maillé, 2007) analyzed the equilibrium of clearing price in second price auctions.

All of these works assume that bidders are myopic: they can strategize within individual auctions, but do not consider the impact of their bids on future auctions. Robustness to non-myopic has recently been studied in (Kanoria and Nazerzadeh, 2014; Epasto et al., 2018). A common idea is to limit the influence of any particular bidder either by assuming a large number of bidders, or imposing a cost associated with manipulation. There has also been a lot of interest in the online version of the pricing problem (Caillaud and Mezzetti, 2004; Amin et al., 2013, 2014; Mao et al., 2018), but those ideas are not directly applicable to the batch-learning setting. Robust learning is also relevant in the online model and several papers develop policies that limit a non-myopic agent’s incentive to misreport (Golrezaei et al., 2019; Deng et al., 2019; Liu et al., 2018; Drutsa, 2018, 2020).

Our work applies ideas from a recent literature on metrics to quantify incentive compatibility. The most standard metric in this respect has been a bidder’s regret from truthful bidding (i.e., the maximum foregone utility), which has been used as a design constraint in auctions where exact incentive compatibility was not possible or desirable (Parkes et al., 2001). Computing regret as an informative metric in its own right is studied in (Feng et al., 2019; Colini-Baldeschi et al., 2020). Due to its analytical tractability, we pay particular attention to the incentive metric introduced by (Deng et al., 2020) when analyzing the robustness of our mechanism.

2 Preliminaries

We consider a setting with a set of bidders, denoted , participating in repeated auctions with a single seller. The repeated auctions sell a single item at each round. The items arrive in an online manner and they must be sold once they arrive. For ease of exposition, we assume there is exactly one item per round.

At each round , each bidder ’s private valuation is drawn independently from a distribution over . Upon the arrival of the -th item, each bidder observes her private valuation and submits a bid to the seller. After receiving the bids from all bidders at each round , the seller runs an auction to decide how to allocate and charge for the item. Throughout this paper, we assume that is a closed interval, and without loss of generality rescale it to .

In this paper, we consider a widely adopted auction format: the second price auction with anonymous reserve price. The seller allocates the item to the unique bidder who bids higher than the highest bid from all the other bidders , and the reserve price at round . (We assume that the bids are all distinct, which holds generically.) This winning bidder is charged . In this paper, we focus on setting an anonymous reserve price, i.e., the reserve prices for all bidders are the same.

2.1 Multi-stage Model for Reserve Pricing

In this paper we consider a multi-stage model for strategic bidders. It follows a canonical setup: the seller learns an anonymous reserve price from the bidders’ historical bids and applies it in the future. More specifically:

-

•

In stage 1, the seller sets the reserve to 0.

-

•

For each stage , the seller computes a reserve from the bidders’ bids in stage . The seller sets the reserve to all the auctions in stage .

We assume that each stage consists of sufficiently many auctions (queries) to faithfully estimate bid distributions. Throughout this paper, we further assume that for each bidder , for all . This stationarity assumption of valuation widely holds for large markets in practice.

2.2 Incentive Compatibility Metric

In this paper, we adopt the dynamic incentive compatibility (dynamic-IC) metric proposed in (Deng et al., 2020) to measure the incentive compatibility of the mechanism in the multi-stage model. A mechanism is dynamic-IC if for any stage , reporting the true value at stage is an optimal strategy for the bidder regardless of her own value and others’ bids, given the bidder always bid truthfully in the future (Deng et al., 2020).

It is without loss of generality to assume there are only two stages as shown in (Deng et al., 2021).111To elaborate on this, in our multi-stage model, when measuring dynamic-IC for stage , only stage is relevant since the bids at stage only affect the reserve price at stage ; and the reserve prices for all future stages are the same provided that the buyer always reports truthfully from stage onwards, under the dynamic-IC definition. Therefore, it is without loss of generality to focus on two-stage model. It is well-known that the second price auction is incentive compatible (IC); i.e., reporting truthfully (bid is equal to value) is always a bidder’s optimal bidding strategy, regardless of the others’ bids and her private value. However, this no longer the case in the two-stage model, because the bidder may benefit from misreporting in stage 1 to induce the seller to set a lower reserve price in stage 2. In stage 2, given the reserve price, each bidder will report truthfully because of the truthfulness of the second price auction with fixed reserve.

In the two-stage model, we assume each bidder has a private (unknown to others and the seller) weakly increasing bidding strategy , which maps values to bids in stage 1. We denote by and the distribution of valuation profile and the valuation profile of the bidders other than , respectively. Specifically, the bidding strategy is the identity function if bidder reports truthfully. With a slight abuse of notation we write and . Let be the identity bidding strategies of the bidders other than . Denote and be the largest and the second largest value among valuation profile . Let and be the cumulative distribution function (CDF) of and , respectively. Let , as well as and are the corresponding probability density function (PDF) and CDF.

Formally, the reserve price set in stage 2 is a function of the distribution of the bids which are induced by the bidding function, so we write the reserve as . We next define the expected utility for each bidder in both stages. In stage 1, let be the expected utility of bidder in stage 1 when she adopts bidding strategy and the other bidders report truthfully, i.e.

| (1) |

In stage 2, the optimal bidding strategy is to bid truthfully, given the reserve price computed from the bids in stage 1. Therefore, we define as the expected utility of bidder in stage 2, when her bidding strategy is and the other bidders report truthfully in stage 1:

| (2) |

Given the above notations, we define the incentive compatibility metric (IC-metric) in the following,

Definition 2.1 (IC-metric).

The IC-metric for bidder locally at true value is

where represents the expected utility of bidder in stage 2 when her bidding strategy is (resp. ), and is allocation of bidder under truthful bidding in stage 1.

To understand the intuition behind this metric, note that the second term in is essentially the derivative of second-stage utility with respect to a uniform bid shading factor ; i.e., it captures the marginal future utility gain from shading away from the true value . Typically, bid shading is beneficial (because it lowers future reserves), in which case the second term in is negative and the metric drops below 1. If truthful bidding (i.e., no shading) is optimal, then the second term is 0 and the metric takes on the reference value 1. Comparing to Regret, the IC-metric turns out to be much more analytically tractable because it is a local metric that focuses specifically on bid-shading deviations.

2.3 Reserve Pricing via Clearing Prices

There are many different approaches to setting reserve prices in second price auctions, most commonly focusing on personalized reserves because these are revenue-optimal when bidders are not identical (Myerson, 1981). A simple strategy for reserves considered in the literature is to use quantiles of historical bid distributions (e.g., setting the reserve price to the 25th quantile) (Ostrovsky and Schwarz, 2011). In this paper, we focus on a reserve pricing strategy recently introduced by Shen et al. (2019) which generalizes using bid quantiles for individual bidders to an anonymous reserve price for all bidders. They propose to compute and apply the clearing price of historical bid profiles as an anonymous reserve, obtained by optimizing the clearing loss function

| (3) |

averaged over all historical bid profiles, where . The parameter here controls the trade-off between match rate (probability that the item is sold) and revenue.

We consider using the clearing price to set the reserve price in stage 2 based on the bids from bidders in stage 1. Given the bidding strategies of bidders, the optimal clearing price is obtained as

| (4) |

The clearing loss is convex and can be easily optimized using standard machine learning libraries, e.g. stochastic gradient descent. Given a reserve price (clearing price) obtained by minimizing the clearing loss, we denote by the expected revenue in stage 2 when bidders bid truthfully.

Definition 2.2 (Expected Revenue).

The expected revenue in stage 2 is defined as,

where and are the largest and the second largest value among valuation profile .

In our analysis, we focus on the revenue performance in stage 2 of the model, as this is the stage in which reserves are set.

3 A Differentially Private Approach

In this section, we propose a simple differentially private (DP) approach to set a reserve price, which can be used to control the revenue and incentive compatibility in the two-stage model. All the proofs are deferred to Appendix B.

In the robust clearing price mechanism below, the seller collects historical bid profiles from stage 1 and computes the clearing price to minimize the empirical clearing loss (5), given a parameter . In stage 2, for each auction, the seller adds a random noise i.i.d. sampled from a (CDF) distribution on the clearing price , to set the reserve price. This mechanism, which we call the Differentially Private Robust Clearing Price (DP-RCP) Mechanism, is summarized in Algorithm 1.

| (5) |

Suppose each bid profile in stage 1 follows a distribution . Since we assume each stage contains a sufficiently large number of auctions, from (5) can be regarded as the optimal expected clearing price, associated with the distribution of bids and . Given this observation, the reserve price for bidders with bidding strategies adopted in stage 1, given a noise and parameter , can be defined as:

| (6) |

Similarly to Shen et al. (2019), we first characterize in the following.

Proposition 3.1.

Suppose , for bidders such that each bidder ’s value is drawn from and uses strictly increasing bidding strategy, the optimal clearing price is the solution to the following equation 222Since is weakly increasing, we denote .,

We next characterize the expected revenue in stage 2, achieved by the DP-RCP mechanism. The following theorem shows that with high probability, the revenue loss caused by the noise in the DP-RCP mechanism will be bounded by , with high probability. The randomness in the result comes from the random noise .

Theorem 3.2 (Revenue Guarantee).

Given , noise , and are both -Lipschitz. For any strictly increasing bidding strategies in the DP-RCP mechanism, we have

| (7) |

holds with probability at least , where is the optimal expected clearing price defined in Eq. (4)

We next characterize the IC-metric of each bidder in the following.

Theorem 3.3 (IC-metric).

For bidders and any noise distribution , the IC-metric of the DP-RCP mechanism satisfies,

where and , where .

Here captures the local sensitivity of the clearing price to linear bid shading. We characterize in the following.

| (8) |

Remark. For the single bidder setting, , which is the th quantile of the value. For i.i.d bidders, i.e., for all , we have . This naturally generalizes the single-bidder case. As grows large, the sensitivity goes to 0 as long as the bid distribution is bounded. This is intuitive, as a bidder’s misreporting should have a negligible effect when there is a large number of competitors.

To implement the DP-RCP mechanism, we need to randomly draw a noise to add to the reserve for each auction, which may be undesirable in practice. To address this difficulty, we next introduce another approach which applies noise to historical bids used to fit the clearing price (one single time), rather than to the output of each auction.

4 A Smoothing Approach

In this section, we introduce a smoothing approach to set a deterministic reserve price to make it robust to bidder misreports. In this method, we add a random noise to each bid and compute the clearing price based on the smoothed bids (in stage 1), as shown in Algorithm 2. We call this mechanism Smoothing Robust Clearing Price (sRCP) Mechanism.

| (9) |

Similarly to the DP approach, suppose each bid profile in stage 1 follows a distribution , (in Eq. 9) can be represented as the optimal expected smoothed clearing price, associated with distribution of bids , distribution of noise and . Therefore, the reserve price for bidders adopting bidding strategies in stage 1, computed by this sRCP mechanism, can be defined as:

| (10) |

We can characterize in sRCP in the following.

Proposition 4.1.

Given , the reserve price computed by sRCP mechanism for bidders is if . Otherwise, it is the solution of price to .

The proof of the above Proposition is deferred to Appendix C. By monotonicity of , it is straightforward to verify the uniqueness of the . Theorem 4.2 characterizes the revenue guarantee for the sRCP mechanism.

Theorem 4.2 (Revenue Guarantee).

Let function be the inverse of function . Suppose , noise , and are -Lipschitz, is -Lipschitz, and . For any strictly increasing bidding strategies in the sRCP mechanism, we have

for any , where is the optimal (non-robust) clearing price defined in Eq. (4).

Proof.

We first rewrite the expected revenue as, . See Appendix A for the detailed derivative of the above representation of the expected revenue. Then, by the Lipschitz assumption of and , we can bound

| (11) |

Next, we will show how to bound . To facilitate the proof, we provide another characterization of (see Lemma A.2 in Appendix A), such that .

We observe for any when . Therefore, by the non-negativity and monotonicity of , we have

Thus, . On the other hand, since for any , we have,

This implies . By the characterization of in Proposition 3.1 and the definition of function , . Given the lower and upper bounds of , we can bound,

Setting , we have by the fact that . Combining Eq. (11), we complete the proof. ∎

The above theorem shows that sRCP has better revenue guarantee compared with DP-RCP in terms of with additional assumption for function, i.e., revenue loss in sRCP v.s. revenue loss in DP-RCP. This advantage is also verified through our simulations, and we also observe that it depends on the choice of . Astute readers may note that depends on number of bidders , but it is decreasing with in general. Therefore, the revenue advantage achieved by sRCP mechanism is even stronger with a large number of bidders.

We characterize the IC-metric (see Definition 2.1) in the following theorem, the proof is deferred to Appendix C.

Theorem 4.3 (IC-metric).

Let . For bidders and any noise distribution , the IC-metric of the robust clearing price mechanism by smoothing approach satisfies,

where when for any .

Remark. is the probability that is between and . Indeed, is similar to in Theorem 3.3 and . depends on implicitly: when , sRCP is dynamic-IC since for each bidder ; when , is just half of the under and sRCP is more dynamic-IC.

5 Experiments

In this section, we run simulations over synthetic data to validate our theoretical findings. By varying the magnitude of the noise and parameter in the clearing loss, we obtain the tradeoff between revenue and IC-metric in the DP-RCP and sRCP mechanisms.

5.1 Set-up

For our simulations we assume the bids of each bidder follow a truncated log-normal distribution: truncated by .333We truncate the bids to make them bounded to be consistent with our theory. Indeed, we observe the similar results without the truncation. The lognormal is commonly used to model bid and value distributions in practice (Thompson and Leyton-Brown, 2013). We randomly generate 5,000 sample bids profiles for each stage. To compute the IC-metric, we set the perturbation magnitude to . The revenue is normalized by the expected total value in stage 2 assuming there is no reserve price and all bidders report truthfully. We only focus on Laplace noise distribution. All experiments are repeated 10 times and we present 95% confidence intervals in all plots.

5.2 Expected Revenue and IC-metric

Due to space limitations, we only report the tradeoff between revenue and IC-metric for the single bidder setting and the two bidders setting.

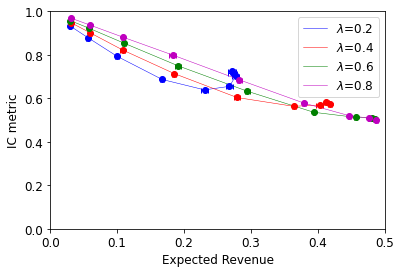

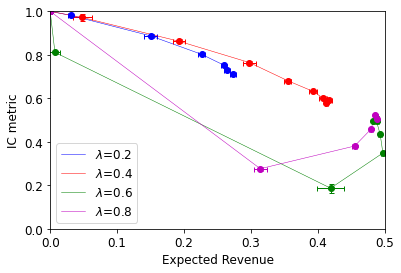

For the single bidder setting, we exhibit the tradeoff between the expected revenue and IC-metric in Figure 1(a) for the DP-RCP mechanism with different (as we observe that revenue is quite low when ) and (no noise corresponds to ). Based on this figure, the setting of (i.e., 20th quantile) in fact achieves the best tradeoff. When is small, e.g. , the clearing price is large and revenue achieved by the clearing price (with no noise) is small. In this case, adding a small noise (with large ) may decrease the IC-metric based on our characterization in Theorem 3.3, when is large. In addition, we test the tradeoff between the expected revenue and IC-metric for the sRCP mechanism for the single bidder setting and we visualize it in Figure 1(b). We find that (i.e., 60th quantile) achieves the best tradeoff between expected revenue and IC-metric, in the sense that at any desired level of expected revenue, can achieve the highest IC metric with an appropriately chosen noise level . Indeed, sRCP achieves better tradeoff than DP-RCP when , while DP-RCP performs better than sRCP when is larger. Based on the experiments, sRCP mechanism prefers more aggressive setting (higher quantile to set clearing price, or equivalently lower ) and DP-RCP mechanism benefits from more conservative (higher ) settings.

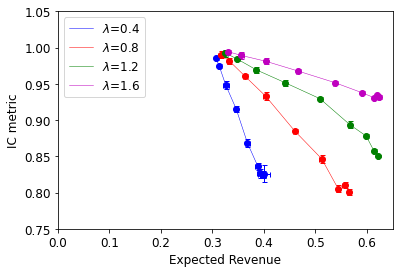

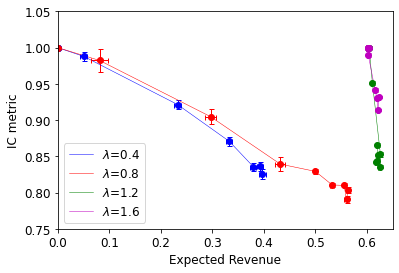

For the two bidders setting, we visualize the tradeoff between revenue and IC-metric of bidder 1 with different s and s for DP-RCP and sRCP in Figure 2(a) and Figure 2(b), respectively.444In this simulation, the two bidders are i.i.d. Therefore, we only report the IC-metric for bidder 1. As we observe, in the two bidders setting, with the existence of a competing bid, the IC-metric of bidder 1 is better than the IC-metric in the single bidder setting. The two RCP mechanisms both achieve better tradeoffs between revenue and IC-metric when is sufficiently large. For the DP-RCP mechanism, Figure 2(a) shows that achieves the best revenue-IC tradeoff among the set . Its tradeoff curve is remarkably better than the others, as it can achieve expected revenue close to the optimum with just an 0.05 decrease in the IC metric from 1.0 (the incentive compatible level). To reach this far, other settings see their IC metric dip below 0.9. For the sRCP mechanism, we observe achieves the best revenue-IC tradeoff, which is similar to the DP-RCP mechanism. Moreover, we find sRCP significantly outperforms than DP-RCP when .

6 Conclusion

This work proposed two robust clearing price mechanisms (DP-RCP and sRCP) to set anonymous reserve prices based on historical bid profiles. The mechanisms are both simple to implement: the first approach fits a clearing price to bid data (which involves optimizing a convex loss function) and the price is made robust to misreports by agents by adding noise to the mechanism output, while the second approach computes a clearing price based on smoothed bid data (adding noise to the training bids). For both mechanisms, we provided bounds on the revenue guarantee in terms of the noise level applied. We also provided exact characterizations of their IC-metric as defined in (Deng et al., 2020), which quantifies bidders’ incentives to uniformly shade their bids. Our empirical evaluation showed that sRCP outperforms than DP-RCP in terms of the revenue and IC metric tradeoff with appropriately chosen parameter .

References

- (1)

- Amin et al. (2013) Kareem Amin, Afshin Rostamizadeh, and Umar Syed. 2013. Learning prices for repeated auctions with strategic buyers. In Advances in Neural Information Processing Systems.

- Amin et al. (2014) Kareem Amin, Afshin Rostamizadeh, and Umar Syed. 2014. Repeated contextual auctions with strategic buyers. In Advances in Neural Information Processing Systems.

- Balcan et al. (2019) Maria-Florina Balcan, Tuomas Sandholm, and Ellen Vitercik. 2019. Estimating Approximate Incentive Compatibility. In Proceedings of the 2019 ACM Conference on Economics and Computation (EC ’19). ACM, New York, NY, USA.

- Caillaud and Mezzetti (2004) Bernard Caillaud and Claudio Mezzetti. 2004. Equilibrium reserve prices in sequential ascending auctions. Journal of Economic Theory 117, 1 (2004), 78 – 95.

- Cole and Roughgarden (2014) Richard Cole and Tim Roughgarden. 2014. The sample complexity of revenue maximization. In Proceedings of the forty-sixth annual ACM symposium on Theory of computing.

- Colini-Baldeschi et al. (2020) Riccardo Colini-Baldeschi, Stefano Leonardi, Okke Schrijvers, and Eric Sodomka. 2020. Envy, regret, and social welfare loss. In Proceedings of The Web Conference 2020.

- Deng et al. (2019) Yuan Deng, Sébastien Lahaie, and Vahab Mirrokni. 2019. A Robust Non-Clairvoyant Dynamic Mechanism for Contextual Auctions. In Advances in Neural Information Processing Systems.

- Deng et al. (2020) Yuan Deng, Sébastien Lahaie, Vahab Mirrokni, and Song Zuo. 2020. A Data-Driven Metric of Incentive Compatibility. In Proceedings of The Web Conference 2020.

- Deng et al. (2021) Yuan Deng, Sébastien Lahaie, Vahab Mirrokni, and Song Zuo. 2021. Revenue-Incentive Tradeoffs in Reserve Pricing. In Proceedings of the 38th International Conference on Machine Learning (ICML-21), to appear.

- Devanur et al. (2016) Nikhil R Devanur, Zhiyi Huang, and Christos-Alexandros Psomas. 2016. The sample complexity of auctions with side information. In Proceedings of the forty-eighth annual ACM symposium on Theory of Computing.

- Drutsa (2018) Alexey Drutsa. 2018. Weakly Consistent Optimal Pricing Algorithms in Repeated Posted-Price Auctions with Strategic Buyer. In International Conference on Machine Learning.

- Drutsa (2020) Alexey Drutsa. 2020. Reserve pricing in repeated second-price auctions with strategic bidders. In International Conference on Machine Learning.

- Duetting et al. (2019) Paul Duetting, Zhe Feng, Harikrishna Narasimhan, David Parkes, and Sai Srivatsa Ravindranath. 2019. Optimal Auctions through Deep Learning (Proceedings of Machine Learning Research).

- Epasto et al. (2018) Alessandro Epasto, Mohammad Mahdian, Vahab Mirrokni, and Song Zuo. 2018. Incentive-aware learning for large markets. In Proceedings of the 2018 World Wide Web Conference.

- Feng et al. (2019) Zhe Feng, Okke Schrijvers, and Eric Sodomka. 2019. Online Learning for Measuring Incentive Compatibility in Ad Auctions. In The World Wide Web Conference.

- Golrezaei et al. (2019) Negin Golrezaei, Adel Javanmard, and Vahab Mirrokni. 2019. Dynamic incentive-aware learning: Robust pricing in contextual auctions. In Advances in Neural Information Processing Systems.

- Kanoria and Nazerzadeh (2014) Yash Kanoria and Hamid Nazerzadeh. 2014. Dynamic Reserve Prices for Repeated Auctions: Learning from Bids. In Web and Internet Economics (WINE).

- Liu et al. (2018) Jinyan Liu, Zhiyi Huang, and Xiangning Wang. 2018. Learning optimal reserve price against non-myopic bidders. In Advances in Neural Information Processing Systems.

- Maillé (2007) Patrick Maillé. 2007. Market clearing price and equilibria of the progressive second price mechanism. RAIRO - Operations Research 41, 4 (2007).

- Mao et al. (2018) Jieming Mao, Renato Paes Leme, and Jon Schneider. 2018. Contextual Pricing for Lipschitz Buyers. (2018).

- McSherry and Talwar (2007) Frank McSherry and Kunal Talwar. 2007. Mechanism design via differential privacy. In 48th Annual IEEE Symposium on Foundations of Computer Science (FOCS’07). IEEE.

- Medina and Mohri (2014) Andres M Medina and Mehryar Mohri. 2014. Learning theory and algorithms for revenue optimization in second price auctions with reserve. In Proceedings of the 31st International Conference on Machine Learning (ICML-14).

- Morgenstern and Roughgarden (2015) Jamie H Morgenstern and Tim Roughgarden. 2015. On the pseudo-dimension of nearly optimal auctions. In Advances in Neural Information Processing Systems.

- Myerson (1981) Roger B Myerson. 1981. Optimal auction design. Mathematics of Operations Research 6, 1 (1981).

- Nedelec et al. (2019) Thomas Nedelec, Noureddine El Karoui, and Vianney Perchet. 2019. Learning to bid in revenue-maximizing auctions. In International Conference on Machine Learning.

- Ostrovsky and Schwarz (2011) Michael Ostrovsky and Michael Schwarz. 2011. Reserve prices in internet advertising auctions: A field experiment. In Proceedings of the 12th ACM conference on Electronic commerce.

- Paes Leme et al. (2016) Renato Paes Leme, Martin Pal, and Sergei Vassilvitskii. 2016. A field guide to personalized reserve prices. In Proceedings of the 25th international conference on world wide web.

- Parkes et al. (2001) David C. Parkes, Jayant Kalagnanam, and Marta Eso. 2001. Achieving Budget-balance with Vickrey-based Payment Schemes in Exchanges. In Proceedings of the 17th International Joint Conference on Artificial Intelligence (IJCAI’01). Morgan Kaufmann Publishers Inc., San Francisco, CA, USA.

- Shen et al. (2019) Weiran Shen, Sebastien Lahaie, and Renato Paes Leme. 2019. Learning to Clear the Market. In Proceedings of the 36th International Conference on Machine Learning.

- Thompson and Leyton-Brown (2013) David RM Thompson and Kevin Leyton-Brown. 2013. Revenue optimization in the generalized second-price auction. In Proceedings of the fourteenth ACM conference on Electronic commerce.

Robust Clearing Price Mechanisms for Reserve Price Optimization

Appendix

Appendix A Auxiliary Lemmas

A.1 Representation of the Expected Revenue

Lemma A.1.

The expected revenue in stage 2 can be represented as,

Proof.

∎

A.2 Another Characterization of Reserve Price in the sRCP Mechanism

Lemma A.2.

Given , the reserve price computed by sRCP mechanism for bidders is if . Otherwise, it is the solution of price to

where .

Proof.

Taking the gradient of above formula w.r.t. , we have

By integral by part, we have . Then if , the reserve price is equal to . Otherwise, setting the gradient to be zero, we complete the proof.

∎

Appendix B Missing Proofs from Section 3

B.1 Proof of Proposition 3.1

Proof.

Taking the derivative of w.r.t , we have

Setting the gradient to be zero and by the first order condition, we complete the proof. ∎

B.2 Proof of Theorem 3.2

Proof.

By Lemma A.1, the expected revenue in stage 2 is

By the Lipschitzness of and , we can bound the difference of the revenue under reserve prices and , as follows,

By the property of Laplace distribution, . Finally, we have

∎

B.3 Proof of Theorem 3.3

Proof.

We first rewrite the expected utility function in the following way,

For notation simplicity, we denote

By Leibniz integral rule, we compute the quantity as follows,

Therefore, we have

where the last equality above holds because

∎

B.4 Proof of Equation (8)

Proof.

Given the definition of and Proposition 3.1, we have . Taking gradient w.r.t of the both sides in the above equation, we have

Therefore, ∎

Appendix C Missing Proofs from Section 4

C.1 Proof of Proposition 4.1

Proof.

Taking the partial gradient of the above formula w.r.t , we have

If , the reserve price is equal to . Otherwise, setting the gradient to be zero, we complete the proof. ∎

C.2 Proof of Theorem 4.3

Proof.

Therefore, we have

where . Therefore, the IC-metric for bidder is

Then we can derive in the following way, by Proposition 4.1, when , we have

Taking derivative with respect to in the both sides, we have

Thus, we get

When , there exists a , . Thus .

When , the left derivative of at is 0, the right derivative of at is . Then .

Therefore, we complete the proof.

∎