Policy Gradient Methods for Distortion Risk Measures

Abstract

We propose policy gradient algorithms which learn risk-sensitive policies in a reinforcement learning (RL) framework. Our proposed algorithms maximize the distortion risk measure (DRM) of the cumulative reward in an episodic Markov decision process in on-policy and off-policy RL settings, respectively. We derive a variant of the policy gradient theorem that caters to the DRM objective, and integrate it with a likelihood ratio-based gradient estimation scheme. We derive non-asymptotic bounds that establish the convergence of our proposed algorithms to an approximate stationary point of the DRM objective.

keywords:

Distortion risk measure, risk-sensitive RL, non-asymptotic analysis, policy gradient.AND ,

1 Introduction

In a classical reinforcement learning (RL) problem, the objective is to learn a policy that maximizes the mean of the cumulative rewards. But, in many practical applications, we may learn unsatisfactory policies if we only consider the mean. Instead of focusing only on the mean, it is important to consider other aspects of a cumulative reward distribution, viz., variance, shape, and tail probabilities. In literature, a statistical measure, called a risk measure is used to quantify these aspects.

While several risk measures are studied in the literature, there is no consensus on an ideal risk measure. Coherent risk measures are a popular class of risk measures that satisfy desirable properties from a risk aversion viewpoint. In particular, a risk measure is said to be coherent if it is translation invariant, sub-additive, positive homogeneous, and monotonic [1]. Value-at-Risk (VaR) is a popular risk measure that lacks coherence as it is not sub-additive. Conditional Value-at-Risk (CVaR) [20] is a conditional expectation of outcomes not exceeding VaR, and is a coherent risk measure. However, as suggested in [28], CVaR is not preferable since it treats all outcomes below VaR equally, and ignores those beyond VaR. Cumulative prospect theory (CPT) [25] is a popular risk measure in human-centered decision making problems. However, CPT is a non-coherent risk measure. Instead of giving equal focus to all the outcomes, or treating only a fraction of the outcomes using a tail-based risk measure such as CVaR, it is preferable to consider all outcomes with the right emphasis, while retaining coherency. We describe such a risk measure next.

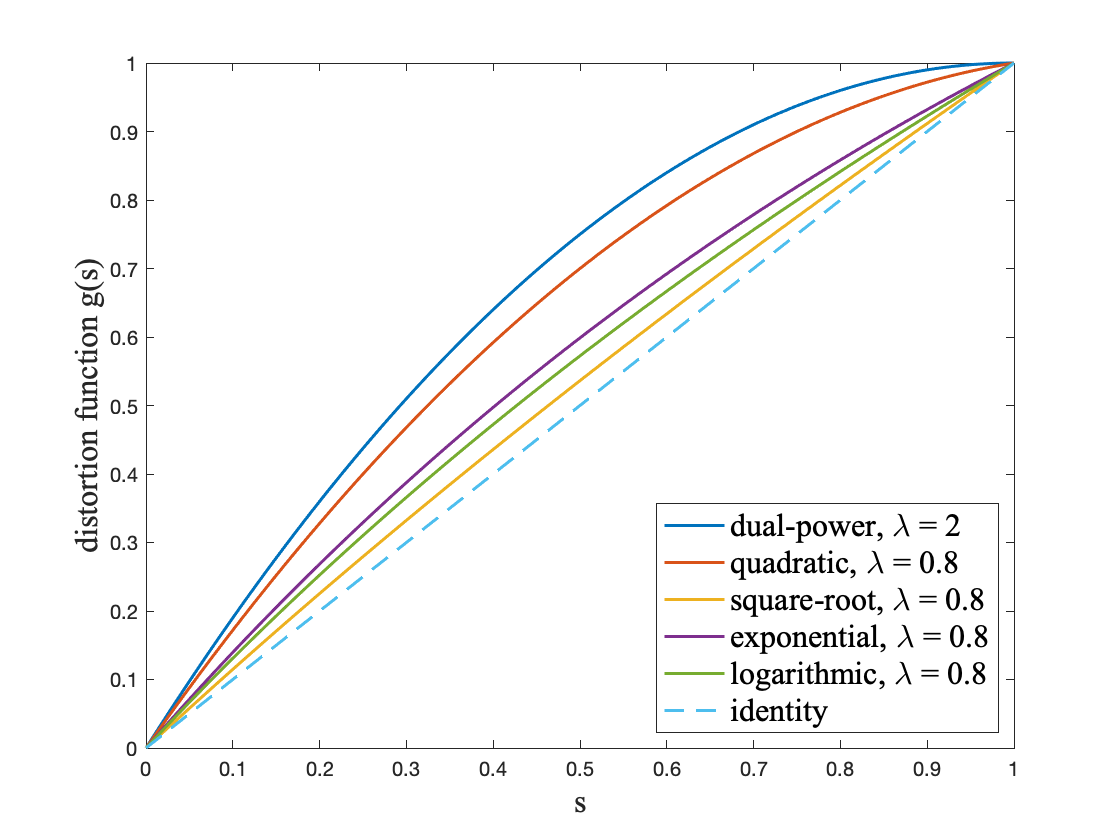

A family of risk measures called distortion risk measures (DRM) [7, 27] is widely used for optimization in finance and insurance. A DRM uses a distortion function to distort the original distribution, and calculate the mean of the rewards with respect to the distorted distribution. A distortion function allows one to vary the emphasis on each possible reward value. The choice of the distortion function governs the risk measure. A DRM with an identity distortion function is simply the mean of the rewards, while a concave distortion function ensures that the DRM is coherent [29]. As an aside, the spectral risk functions are equivalent to distortion functions [10]. The popular risk measures like VaR and CVaR can be expressed as a DRM using appropriate distortion functions. But, the distortion function is discontinuous for VaR, and though continuous, it is not differentiable at every point for CVaR. As shown in [28], smoothness is a desirable property for a distortion function. In this paper, we focus on smooth distortion functions. Examples include the dual-power function, quadratic function, square-root function, exponential function, and logarithmic function (for additional examples, refer to [12, 27]).

Risk-sensitive RL has been studied widely in the literature, with focus on specific risk measures like expected exponential utility [4], variance related measures [17], CVaR [16, 6], and CPT [18]. In this paper, instead of deriving algorithms that cater to specific risk measures, we consider the whole family of DRMs with smooth distortion functions. The risk-neutral RL approach gives equal importance to all the events, and hence an occasional high/low reward event gets equal priority as all other events. But using DRMs, we can give more emphasis to frequent events, while accounting for infrequent high severity events. As there is no universally accepted ideal risk measure, we may choose a risk measure which best fits our particular problem by picking an appropriate distortion function.

In this paper, we consider a risk-sensitive RL problem, in which an optimal policy is learned by maximizing the DRM of cumulative rewards in an episodic Markov decision process (MDP). We consider this problem in on-policy as well as off-policy settings, and employ the policy gradient solution approach. The basis for a policy gradient algorithm is the expression for the gradient of the performance objective. In the risk-neutral case, such an expression is derived using the likelihood ratio (LR) method [22]. We derive a DRM analogue to the policy gradient theorem. In the case of DRM, policy gradient estimation is challenging since DRM of a given policy cannot be estimated using a sample mean. We formulate an LR-based estimation using the empirical distribution function (EDF) to approximate DRM, leading to a biased estimate of the DRM policy gradient. In contrast, policy gradient estimation is considerably simpler in a risk-neutral setting as the task is to estimate the mean cumulative reward, and using a sample mean leads to an unbiased gradient estimate.

We characterize the mean squared error (MSE) in DRM policy gradient estimates. In particular, we establish that the MSE is of order , where is the batch size (or the number of episodes). Using the DRM policy gradient expression, we propose two policy gradient algorithms which cater to on-policy and off-policy RL settings, respectively. To the best of our knowledge, we are first to derive a policy gradient theorem under a DRM objective, and devise/analyze policy gradient algorithms to optimize DRM in a RL context.

We provide bounds on the bias and variance of the DRM policy gradient estimates. Using these bounds, we establish that our algorithms converge to an approximate stationary point of the DRM objective at a rate of . Here denotes the total number of iterations of the DRM policy gradient algorithm. Our algorithms require episodes per iteration for both on-policy and off-policy RL settings.

Related work. In [26], the authors develop a general framework for optimization of any smooth risk measure which satisfy certain predefined conditions. It employs a zeroth-order optimization technique, specifically the smooth functional (SF) based estimator for estimating the gradient. In [24], the authors consider a policy gradient algorithm for an abstract coherent risk measure. They derive a policy gradient theorem using the dual representation of a coherent risk measure. Next, using the EDF of the cumulative reward distribution, they propose an estimate of the policy gradient, and this estimation scheme requires solving a convex optimization problem. Finally, they establish asymptotic consistency of their proposed gradient estimate. In [18], the authors consider a CPT-based objective in an RL setting. They employ a simultaneous perturbation stochastic approximation (SPSA) method for policy gradient estimation, and provide asymptotic convergence guarantees for their algorithm. In [19], the authors survey policy gradient algorithms for optimizing different risk measures in a constrained as well as an unconstrained RL setting. In a non-RL context, the authors in [9] study the sensitivity of DRM using an estimator that is based on the generalized likelihood ratio method, and establish a central limit theorem for their gradient estimator.

In comparison to the aforementioned works, we would like to note the following aspects:

(i) For a smooth risk measure, which satisfy certain predefined conditions, [26] employs an SF-based gradient estimation scheme. Since our algorithms focus solely on optimizing DRMs, we have derived an equivalent of the policy gradient theorem specifically tailored for DRMs. Furthermore, we have devised a LR-based approach for estimating DRM gradients.

While [26] illustrates DRM optimization as an instance within a broader framework, the required number of episodes for achieving convergence varies. The SF-based gradient estimation method employs two trajectories, which might not be practical for all applications, especially those in on-policy RL settings. Conversely, the policy gradient theorem we introduce enables a single trajectory algorithm. Furthermore, our approach illustrates better sample complexity, implying that LR-based methods require fewer episodes to achieve convergence compared to SF-based methods. Our algorithms require episodes per iteration for both on-policy and off-policy RL scenarios. In contrast, the algorithms proposed in [26] necessitate episodes per iteration for on-policy RL and episodes per iteration for off-policy RL.

(ii) For an abstract coherent risk measure, [24] uses gradient estimation scheme which requires solving a convex optimization sub-problem, whereas our algorithms can directly estimate the gradient from the samples without solving any optimization sub-problem. Thus our gradient estimation schemes are computationally inexpensive compared to the one in [24].

(iii) Using the DRM gradient estimate, we analyze policy gradient algorithms, and provide a convergence rate result of order . But, the convergence guarantees in [24] are asymptotic in nature.

(iv) In [18], the guarantees for a policy gradient algorithm based on SPSA are asymptotic in nature, and is for CPT in an on-policy RL setting. CPT is also based on a distortion function, but the distortion function underlying CPT is neither concave nor convex, and hence, it is non-coherent.

(v) In [19], the authors derive a non-asymptotic bound of for an abstract smooth risk measure. They use abstract gradient oracles which satisfies certain bias-variance conditions. In contrast, we provide concrete gradient estimation schemes in RL settings, and our bounds feature an improved rate of .

The rest of the paper is organized as follows: Section 2 describes the DRM-sensitive episodic MDP. Section 3 introduces our proposed gradient estimation methods and corresponding algorithms. Section 4 introduces the non-asymptotic bounds for our algorithms, while Section 5 offers detailed proofs of convergence. Section 6 presents empirical results from our proposed algorithms. Finally, Section 7 provides the concluding remarks.

2 Problem formulation

2.1 Distortion risk measure (DRM)

Let denote the cumulative distribution function (CDF) of a r.v. . The DRM of is defined using the Choquet integral of w.r.t. a distortion function as follows:

The distortion function is non-decreasing, with and . Some examples of the distortion functions are given in Table 1, and their plots in Figure 1. A distortion function applies varying importance to different segments of the distribution. If we use the identity function as a distortion function, the original distribution remains unaltered. Consequently, the DRM becomes equivalent to the expected value, as demonstrated below.

| Dual-power function | , |

|---|---|

| Quadratic function | , |

| Exponential function | , |

| Square-root function | , |

| Logarithmic function | , |

The DRMs are well studied from an ‘attitude towards risk’ perspective, and we refer the reader to [8, 2] for details. In this paper, we focus on ‘risk-sensitive decision making under uncertainty’, with DRM as the chosen risk measure. We incorporate DRMs into a risk-sensitive RL framework, and the following section describes our problem formulation.

2.2 DRM-sensitive MDP

We consider an MDP with a state space and an action space . We assume that and are finite spaces. Let be the scalar reward function, and be the transition probability function. The actions are selected using parameterized stochastic policies . We consider episodic problems, where each episode starts at a fixed state , and terminates at a special absorbing state . We denote by and , the state and action at time respectively. We assume that the policies are proper, i.e., they satisfy the following assumption:

(A1).

.

The cumulative discounted reward is defined by

| (1) |

where , , , and is the random length of an episode. Notice that , a.s. From (A1), we infer that . This fact in conjunction with implies the following bound:

| (2) |

The DRM is defined by

| (3) |

where is the CDF of , and , or any problem specific tight upper bound for .

Our goal is to find a which maximizes , i.e.,

| (4) |

3 DRM policy gradient algorithms

An iterative gradient-based algorithm can solve (4) using the following update iteration:

| (5) |

where is set arbitrarily, and is the step-size. Here denotes the gradient w.r.t. .

But, in a typical RL setting, we do not have direct measurements of the gradient . To overcome this difficulty, we derive a variant of the policy gradient theorem that caters to the DRM objective, and integrate it with an LR-based gradient estimation scheme. In the following sections, we describe our policy gradient algorithms in on-policy and off-policy RL settings, respectively.

3.1 DRM policy gradient

In this section, we present a DRM analogue to the policy gradient theorem under the following assumptions:

(A2).

, where is the -dimensional Euclidean norm.

(A3).

.

The assumptions (A2)-(A3) ensure the boundedness of the DRM policy gradient. An assumption like (A2) is common to the analysis of policy gradient algorithms (cf. [30, 15]). A few examples of distortion functions, which satisfy (A3) are given in Table 1.

For deriving a policy gradient theorem variant with DRM as the objective, we first express the CDF , and its gradient as expectations w.r.t the episodes from the policy . Starting with

| (6) |

we obtain an expression for in the lemma below, and the proof is available in Section 5.

Lemma 1.

,

| (7) |

We now state the DRM policy gradient theorem below. The reader is referred to Section 5 for a proof.

Theorem 1.

We make the following additional assumptions to ensure the smoothness of the DRM .

(A4).

, where is the operator norm.

(A5).

, .

An assumption like (A4) is common in literature for the non-asymptotic analysis of the policy gradient algorithms (cf. [30, 21]). A few examples of distortion functions, which satisfy (A5) are given in Table 1. Since is bounded by definition, we can see that any that satisfies (A5) will satisfy (A3). Smoothness assumptions align with (A3) and (A5) can be observed in the literature when optimizing risk measures. For instance, in [24], the assumption regarding the risk envelope ensures the smoothness of the constraints. Additionally, in [18], the authors assume that the CPT weight functions exhibit continuity, Lipschitz continuity, or local Lipschitz continuity, and that the utility functions are continuous and strictly increasing, or that the first moments are bounded.

The following result establishes that the DRM is smooth in the parameter . The reader is referred to Section 5 for a proof.

3.2 DRM optimization

In the following sections, we describe gradient algorithms that use (8) to derive DRM gradient estimates.

3.2.1 On-policy DRM optimization

We generate episodes using the policy , and estimate and using sample averages. We denote by the cumulative reward, and the length of the episode . Also, we denote by and the action and state at time in episode , respectively. Let denote the EDF of , and is defined by

| (9) |

We form the estimate of as follows:

| (10) |

Using the estimates from (9) and (10), we estimate the gradient in (8) as follows:

| (11) |

Using order statistics of samples , we can compute the integral in (11) as given in the lemma below. The reader is referred to Appendix A for a proof.

Lemma 3.

| (12) |

In the above, is the smallest order statistic from the samples , and

, with denoting the length, and and the state and action at time of the episode corresponding to . Here is the right derivative of the distortion function at .

The gradient estimator in (11) is biased since . However, the bias can be controlled by increasing the number of episodes . A bound for the MSE of this estimator is given below. The reader is referred to Section 5 for a proof.

Lemma 4.

We solve (4) using the following update iteration:

| (13) |

Algorithm 1 presents the pseudocode of DRM-OnP-LR.

3.2.2 Off-policy DRM optimization

In an off-policy RL setting, we optimize the DRM of from the episodes generated by a behavior policy , using the importance sampling (IS) ratio. We require the behavior policy to be proper, i.e.,

(A6).

.

We also assume that the target policy is absolutely continuous w.r.t. the behavior policy , i.e.,

(A7).

.

The cumulative discounted reward is defined by

| (14) |

where , , , and is the random length of an episode. As before, (A6) implies and the following bound:

| (15) |

The importance sampling ratio is defined by

| (16) |

From (A2) and (A7), we obtain and , . This fact in conjunction with (15) implies the following bound for :

| (17) |

We express the CDF , and its gradient as expectations w.r.t. the episodes from the policy . Starting with

| (18) |

we obtain the following analogue of Lemma 1 for the off-policy case. The reader is referred to Appendix B for a proof.

Lemma 5.

,

| (19) |

We generate episodes using the policy to estimate and using sample averages. We denote by the cumulative reward, the IS ratio.

We form the estimate of as follows:

| (20) | |||

| (21) |

The importance sampling ratio in (21) can set a value above . Since we are estimating a CDF, we restrict to one in .

As in the on-policy case, the integral in (23) can be computed using order statistics of the samples , as given in the lemma below. The reader is referred to Appendix A for a proof.

Lemma 6.

| (24) |

In the above, is the smallest order statistic from the samples , and is the importance sampling ratio corresponding to . Also, , with denoting the length, and and are the state and action at time of the episode corresponding to .

As in the on-policy case, the estimator in (23) is biased, but can be controlled by increasing the number of episodes . A bound on the MSE of our estimator is given below. The reader is referred to Section B for a proof.

Lemma 7.

4 Main results

Our non-asymptotic analysis establishes a bound on the number of iterations of our algorithms to find an -stationary point of the DRM, which is defined below.

Definition 1.

(-stationary point) Let be the output of an algorithm. Then, is called an -stationary point of problem (4), if .

In an RL setting, the DRM objective need not be convex. Hence, we establish the convergence of our proposed algorithms to an -stationary point. Such an approach is common in the risk-neutral setting as well, cf. [15, 21].

We derive convergence rate of our algorithms for a random iterate , that is chosen uniformly at random from the policy parameters . We provide a convergence rate for the algorithm DRM-OnP-LR and DRM-OffP-LR below. The proofs are available in Section 5 and Appendix B, respectively.

Theorem 2.

(DRM-OnP-LR) Assume (A1)-(A5). Let be the policy parameters generated by DRM-OnP-LR using (13), and let be chosen uniformly at random from this set. Then,

| (26) |

In the above, , , and is as in Lemma 2. The constants , and are as defined in (A2)-(A5), while is an upper bound on the episode length from (2).

We specialize the bound in (2) to a particular choice of step-size , and batch size in the corollary below.

Corollary 1.

Set , and . Then, under the conditions of Theorem 2, we have

Theorem 3.

(DRM-OffP-LR) Assume (A1)-(A7). Let be the policy parameters generated by DRM-OffP-LR using (25), and let be chosen uniformly at random from this set. Then,

| (27) |

where , , , , and are as defined in Theorem 2. The constant is an upper bound on the importance sampling ratio from (17), and is an upper bound on the episode length from (15).

We specialize the bound in (3) to a particular choice of step-size , and batch size in the corollary below.

Corollary 2.

Set , and . Then, under the conditions of Theorem 3, we have

5 Convergence proofs

Proof.

(Lemma 1) Let denote the set of all sample episodes. For any episode , we denote by , its length, and and , the state and action at time respectively. For any , let the cumulative discounted reward be

Also, let

| (28) |

From (28), we obtain

| (29) |

Now,

| (30) | |||

In the above, follows by an application of the dominated convergence theorem to interchange the differentiation and the expectation operation. The aforementioned application is allowed since (i) is finite and the underlying measure is bounded, as we consider an MDP where the state and actions spaces are finite, and the policies are proper, (ii) is bounded from (A2). The step follows, since for a given episode , the cumulative reward does not depend on , and follows from (29).∎

The following lemma establishes an upper bound on the norm of the gradient and the Hessian of the CDF .

Lemma 8.

,

Proof.

Proof.

(Theorem 1) Notice that,

In the above, follows by an application of the dominated convergence theorem to interchange the differentiation and the integral operation. The aforementioned application is allowed since

(i) is finite for any ; (ii) from (A3), and is bounded from Lemma 8. The bounds on and imply

.

∎

Proof.

In the lemma below, we establish an upper bound on the variance of the DRM gradient estimate as defined in (11). Subsequently, we use this result to prove Lemma 4, and Theorem 2.

Lemma 9.

Proof.

Proof.

(Lemma 4)

From the fact that

, a.s.,

we observe that is a set of partial sums of bounded mean zero r.v.s, and hence they are martingales.

Using Azuma-Hoeffding’s inequality, we obtain ,

| (38) |

Using (32) from Lemma 8, we observe that

is a set of partial sums of bounded mean zero r.v.s, and hence they are martingales. Using vector version of Azuma-Hoeffding inequality from Theorem 1.8-1.9 in [11], for any , we have

| (39) |

From (37), for any , we have

| (40) |

where the last two inequalities follow from (34) and (38). From (A3), for any , we have

| (41) |

where the last inequality follows from (39).

6 Simulation Results

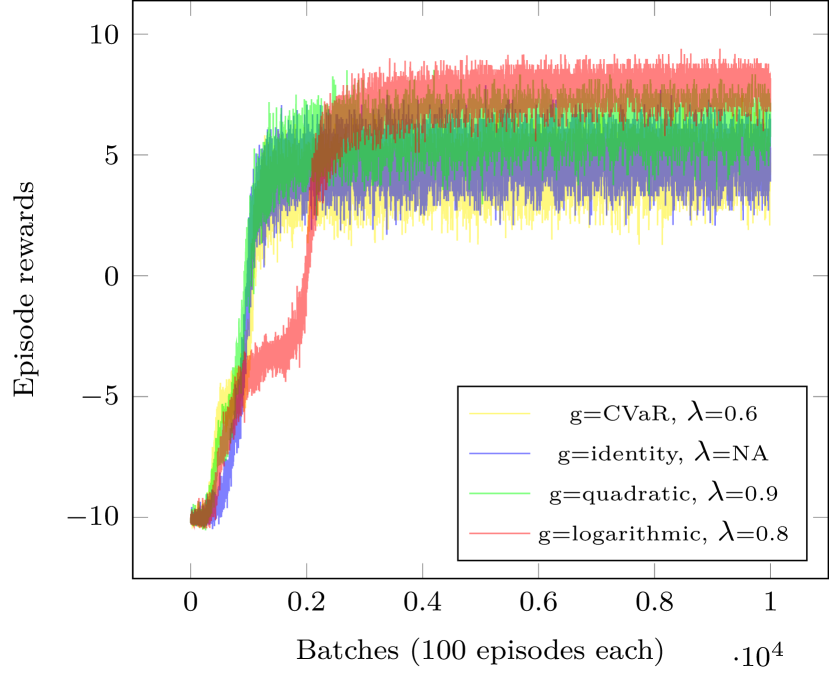

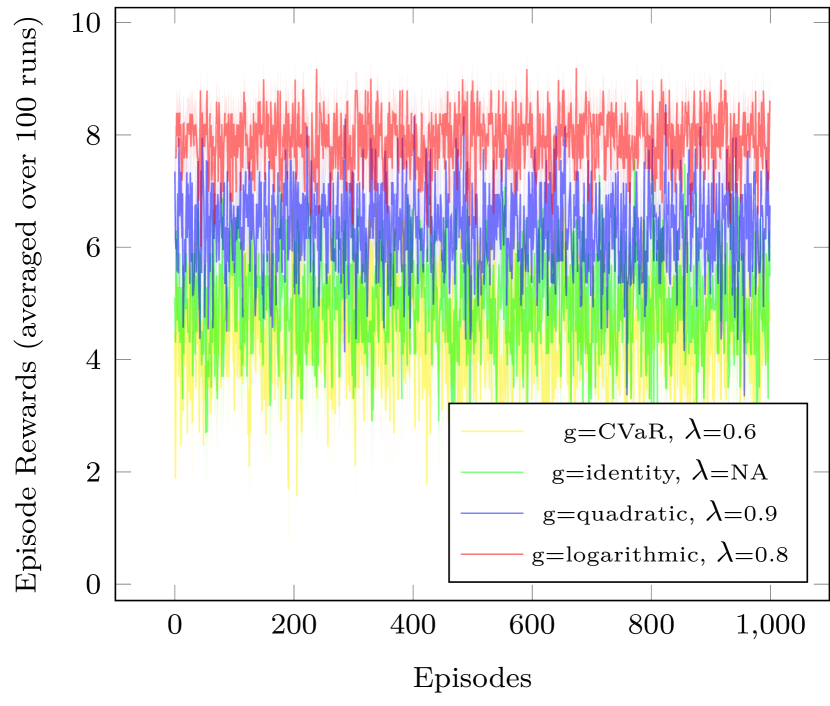

We conducted experiments on a control problem known as Frozen Lake, sourced from the OpenAI Gym toolkit [5]. We customized the environment, depicted in Figure 2. The state space comprises a grid, while the action space consists of . Each action corresponds to movement in the specified direction. When selecting an action, there is a probability that the agent moves in the intended direction, and a probability for each of the adjacent directions. Episodes terminate after steps, if the agent falls into hole H, or upon reaching the goal G. The rewards are assigned as follows: for reaching the goal G, for falling into hole H, and for stepping on a frozen state F.

We performed experiments utilizing our DRM-OnP-LR algorithm, employing various distortion functions, including CVaR and identity function (see Table 1 for the mathematical expressions defining distortion functions). Our algorithm DRM-OnP-LR was executed over iterations, with a batch size of and a stepsize of .

The reward plots depicted in Figure 2 indicate that the DRM with a logarithmic distortion function performs better than other distortion functions, notably outperforming both CVaR and the identity function. Due to the high stochasticity of the grid, there is a notable risk of falling into the hole H when the agent takes the shortest path toward the goal G. Our simulation experiments revealed that when utilizing the logarithmic distortion function, the agent consistently chooses a path that avoids the holes H, resulting in enhanced average rewards.

7 Conclusions and future work

We proposed DRM-based policy gradient algorithms for risk-sensitive RL control. We employed LR-based gradient estimation schemes in on-policy as well as off-policy RL settings, and provided non-asymptotic bounds that establish convergence to an approximate stationary point of the DRM.

As a future work, it would be interesting to study DRM optimization in a risk-sensitive RL setting with feature-based representations, and function approximation. In this setting, one could consider an actor-critic algorithm for DRM optimization, and study its non-asymptotic performance.

References

- [1] P. Artzner, F. Delbaen, J. Eber, and D. Heath. Coherent measures of risk. Mathematical Finance, 9(3):203–228, 1999.

- [2] A. Balbás, J. Garrido, and S. Mayoral. Properties of distortion risk measures. Methodology and Computing in Applied Probability, 11(3):385–399, 2009.

- [3] D. P. Bertsekas and J. N. Tsitsiklis. Neuro-Dynamic Programming. Athena Scientific, 1st edition, 1996.

- [4] V. S. Borkar. Q-learning for risk-sensitive control. Mathematics of Operations Research, 27:294–311, 2002.

- [5] Greg Brockman, Vicki Cheung, Ludwig Pettersson, Jonas Schneider, John Schulman, Jie Tang, and Wojciech Zaremba. Openai gym, 2016.

- [6] Y. Chow, M. Ghavamzadeh, L. Janson, and M. Pavone. Risk-constrained reinforcement learning with percentile risk criteria. J. Mach. Learn. Res., 18(1):6070–6120, 2017.

- [7] D. Denneberg. Distorted probabilities and insurance premiums. Methods of Operations Research, 63(3):3–5, 1990.

- [8] K. Dowd and D. Blake. After VaR: The theory, estimation, and insurance applications of quantile-based risk measures. The Journal of Risk and Insurance, 73(2):193–229, 2006.

- [9] P. Glynn, Y. Peng, M. Fu, and J. Hu. Computing sensitivities for distortion risk measures. INFORMS J. on Computing, pages 1–13, 2021.

- [10] H. Gzyl and S. Mayoral. On a relationship between distorted and spectral risk measures. Revista de Economía Financiera, 15:8–21, 2008.

- [11] T. Hayes. A large-deviation inequality for vector-valued martingales. Combinatorics, Probability and Computing, 2005.

- [12] B. Jones and R. Zitikis. Empirical estimation of risk measures and related quantities. North American Actuarial Journal, 7:44–54, 2003.

- [13] Joseph Kim. Bias correction for estimated distortion risk measure using the bootstrap. Insur.: Math. Econ., 47:198–205, 2010.

- [14] Yurii E. Nesterov. Introductory Lectures on Convex Optimization - A Basic Course, volume 87 of Applied Optimization. Springer, 2004.

- [15] M. Papini, D. Binaghi, G. Canonaco, M. Pirotta, and M. Restelli. Stochastic variance-reduced policy gradient. In ICML, pages 4026–4035, 2018.

- [16] L. A. Prashanth. Policy gradients for CVaR-constrained MDPs. In Algorithmic Learning Theory (ALT), pages 155–169, 2014.

- [17] L. A. Prashanth and M. Ghavamzadeh. Actor-critic algorithms for risk-sensitive mdps. In Adv. Neural Inf. Process. Syst., volume 26, pages 252–260, 2013.

- [18] L. A. Prashanth, C. Jie, M. Fu, S. Marcus, and C. Szepesvari. Cumulative prospect theory meets reinforcement learning: Prediction and control. In ICML, volume 48, pages 1406–1415, 2016.

- [19] L.A. Prashanth and M. Fu. Risk-sensitive reinforcement learning via policy gradient search. Foundations and Trends in Machine Learning, 15(5):537–693, 2022.

- [20] R. T. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. Journal of risk, 2:21–42, 2000.

- [21] Z. Shen, A. Ribeiro, H. Hassani, H. Qian, and C. Mi. Hessian aided policy gradient. In ICML, pages 5729–5738, 2019.

- [22] R. S. Sutton and A. G. Barto. Reinforcement Learning: An Introduction. The MIT Press, 2 edition, 2018.

- [23] Richard S Sutton, Hamid Maei, and Csaba Szepesvári. A convergent O(n) temporal-difference algorithm for off-policy learning with linear function approximation. In Adv. Neural Inf. Process. Syst., volume 21, pages 1609–1616, 2009.

- [24] A. Tamar, Y. Chow, M. Ghavamzadeh, and S. Mannor. Policy gradient for coherent risk measures. In Adv. Neural Inf. Process. Syst., pages 1468–1476, 2015.

- [25] A. Tversky and D. Kahneman. Advances in prospect theory: Cumulative representation of uncertainty. J. Risk Uncertain., 5:297–323, 1992.

- [26] N. Vijayan and L. A. Prashanth. A policy gradient approach for optimization of smooth risk measures. In UAI, volume 216, pages 2168–2178, 2023.

- [27] S. Wang. Premium calculation by transforming the layer premium density. ASTIN Bulletin, 26(1):71–92, 1996.

- [28] SS Wang. A risk measure that goes beyond coherence. In 12th AFIR International Colloquium, Mexico., 2002.

- [29] J. Wirch and M. Hardy. Distortion risk measures: Coherence and stochastic dominance. Insur. Math. Econ., 32:168–168, 2003.

- [30] K. Zhang, A. Koppel, H. Zhu, and T. Basar. Global convergence of policy gradient methods to (almost) locally optimal policies. SIAM J. Control. Optim., 58(6):3586–3612, 2020.

Appendix A Simplifying the estimate of the DRM gradient using order statistics

Proof.

(Lemma 3) Our proof follows the technique from [13]. Let is the smallest order statistic from the samples . We rewrite (9) as given below.

| (46) |

Let , where is the length, and and are the state and action at time of the episode corresponding to . We rewrite (10) as given below.

| (47) |

Now,

where is the right derivative of the distortion function at .∎

Proof.

Appendix B Analysis of DRM-offP-LR

Proof.

In the Lemma below, we establish an upper bound on the variance of the gradient estimate as defined in (23). Subsequently, we use this result to prove Lemma 7 and Theorem 3.

Lemma 10.

Proof.

Proof.

(Lemma 7) We use parallel arguments to the proof of Lemma 4. From (17), we obtain a.s., and we observe that is a set of partial sums of bounded mean zero r.v.s, and hence they are martingales. Using Azuma-Hoeffding’s inequality, we obtain ,

| (54) |

From (20) and (21), we observe that

. Hence, we obtain ,

| (55) |

Using similar arguments as in (38) along with (55), we obtain ,

| (56) |

From (A2), (15), and (17), we obtain ,

| (57) |

We observe that is a set of partial sums of bounded mean zero r.v.s from (57), and hence they are martingales. Using vector version of Azuma-Hoeffding inequality from Theorem 1.8-1.9 in [11], we obtain ,

| (58) |

Using similar arguments as in (39) along with (58), we obtain ,

| (59) |

Using similar arguments as in (40), along with (56), and (53), we obtain ,

| (60) |

Using similar arguments as in (5) along with (59), we obtain ,

| (61) |

The result follows by using similar arguments as in (42) along with (60) and (B).∎

Proof.

(Theorem 3) By using a completely parallel argument to the initial passage in the proof of Theorem 2 leading up to (45), we obtain

where the last inequality follows from Lemmas 7 and 10. Summing the above result from , we obtain

Since is chosen uniformly at random from the policy iterates , we obtain

∎