Inference and forecasting for continuous-time integer-valued trawl processes

Abstract

This paper develops likelihood-based methods for estimation, inference, model selection, and forecasting of continuous-time integer-valued trawl processes. The full likelihood of integer-valued trawl processes is, in general, highly intractable, motivating the use of composite likelihood methods, where we consider the pairwise likelihood in lieu of the full likelihood. Maximizing the pairwise likelihood of the data yields an estimator of the parameter vector of the model, and we prove consistency and, in the short memory case, asymptotic normality of this estimator. When the underlying trawl process has long memory, the asymptotic behaviour of the estimator is more involved; we present some partial results for this case. The pairwise approach further allows us to develop probabilistic forecasting methods, which can be used to construct the predictive distribution of integer-valued time series. In a simulation study, we document the good finite sample performance of the likelihood-based estimator and the associated model selection procedure. Lastly, the methods are illustrated in an application to modelling and forecasting financial bid-ask spread data, where we find that it is beneficial to carefully model both the marginal distribution and the autocorrelation structure of the data.

Keywords: Count data; Lévy basis; pairwise likelihood; estimation; model selection; forecasting.

JEL Codes: C13; C51; C52; C53; C58.

1 Introduction

In this paper, we develop likelihood-based methods for estimation, inference, model selection, and forecasting of continuous-time integer-valued trawl (IVT) processes. IVT processes, introduced in Barndorff-Nielsen et al. (2014), are a flexible class of integer-valued, serially correlated, stationary, and infinitely divisible continuous-time stochastic processes. In general, however, IVT processes are not Markovian, which implies that the structure of the full likelihood of an IVT process is highly intractable (Shephard & Yang, 2016). This is the impetus of the present paper, where we propose to use composite likelihood (CL, Lindsay, 1988) methods for estimation and inference. Specifically, we propose to estimate the parameters of an IVT model by maximizing the pairwise likelihood of the data. CL methods in general, and the pairwise likelihood approach in particular, have been successfully used in many applications, such as statistical genetics (Larribe & Fearnhead, 2011), geostatistics (Hjort & Omre, 1994), and finance (Engle et al., 2020). See Varin et al. (2011) for an excellent overview of CL methods. Although the theory behind CL estimation is quite well understood in the case of iid observations (e.g. Cox & Reid, 2004; Varin & Vidoni, 2005), the time series case, which is what we consider here, generally requires separate treatment (Varin et al., 2011, p. 11). For instance, Davis & Yau (2011) develops the theory of CL estimators in the setting of linear Gaussian time series models, while Chen et al. (2016) and Ng et al. (2011) consider CL methods for a hidden Markov model and a time series model with a latent autoregressive process, respectively. Also, Sørensen (2019) develops a two-step CL estimation method for parameter-driven count time series models with covariates. Our paper adds to the literature on CL methods for time series models by deriving the theoretical properties (consistency, asymptotic normality) of a pairwise CL estimator applied to IVT models.

A central feature of IVT processes is that they allow for specifying the correlation structure of the model separately from the marginal distribution of the model, making them flexible and well-suited for modelling count- or integer-valued data. In particular, the marginal distribution of an IVT process can be any integer-valued infinitely divisible distribution, while the correlation structure can be specified independently using a so-called trawl function. This setup allows for both short- and long-memory of the IVT process. So far, IVT processes have been applied to financial data (Barndorff-Nielsen et al., 2014; Shephard & Yang, 2017; Veraart, 2019) and real-valued trawl processes to the modelling of extreme events in environmental time series (Noven et al., 2018). IVT processes are, under weak conditions, stationary and ergodic, which motivated Barndorff-Nielsen et al. (2014) to suggest a method-of-moments-based estimator for the parameters of the IVT model. This method-of-moments-based estimator has been used in most applied work using IVT processes (e.g. Barndorff-Nielsen et al., 2014; Shephard & Yang, 2017; Veraart, 2019). Exceptions are Shephard & Yang (2016) and Noven et al. (2018). In Noven et al. (2018), a pairwise likelihood was used for a hierarchical model involving a latent (Gamma-distributed) trawl process and the corresponding asymptotic theory was derived in Courgeau & Veraart (2021). However, the asymptotic theory for inference for integer-valued trawl processes which are observed directly is not covered by these earlier papers. In Shephard & Yang (2016), the authors derive a prediction decomposition of the likelihood function of a particularly simple IVT process, the so-called Poisson-Exponential IVT process, allowing them to conduct likelihood-based estimation and inference. Although the likelihood estimation method developed in Shephard & Yang (2016) theoretically applies to more general IVT processes, the computational burden quickly becomes overwhelming in these scenarios, making estimation by classical maximum likelihood methods infeasible in practice.

The contributions of this paper can be summarized as follows. First, we derive the theoretical mixing properties of IVT processes. Using these, we prove consistency and, in the short memory case, asymptotic normality of the maximum composite likelihood (MCL) estimator of the parameter vector of an IVT model. We discuss the long memory case and, based on a result about the asymptotic behaviour of partial sums of IVT processes, conjecture that the MCL estimator has an -stable limit with infinite variance in this case. For the purpose of conducting feasible inference and model selection, we propose two alternative estimators of the asymptotic variance of the MCL estimator in the short memory case: a kernel-based estimator, inspired by the heteroskedastic and autocorrelation consistent (HAC) estimator of Newey & West (1987), and a simulation-based estimator. Second, we use the same principle of considering the pairwise likelihood in lieu of the full likelihood, to derive the predictive distribution of an IVT model, conditional on the current value of the process; this allows us to use the IVT framework for forecasting integer-valued data. In a simulation study, we compare the MCL estimator to the standard method-of-moments-based estimator suggested in Barndorff-Nielsen et al. (2014) and find that the MCL estimator provides substantial improvements in most cases. Indeed, in a realistic simulation setup, we find that the MCL estimator can improve on the method-of-moments-based estimator by more than , in terms of finite sample root median squared error. Since the asymptotic theory for (G)MM estimation of trawl processes has not been worked out elsewhere, we also derive the asymptotic theory for GMM estimation and present the results for comparison purposes in the Supplementary Material, see Section S12.

We apply the methods developed in the paper to a time series of the bid-ask spread of a financial asset. The time series behaviour of the bid-ask spread has been extensively studied in the literature on the theory of the microstructure of financial markets (e.g. Huang & Stoll, 1997; Bollen et al., 2004). The model selection procedure developed in the paper indicates that a model with Negative Binomial marginal distribution and slowly decaying autocorrelations most adequately describe the data. These findings are in line with those of Groß-KlußMann & Hautsch (2013), who also found strong persistence in bid-ask spread time series. Then, in a pseudo-out-of-sample forecast exercise, we find that it is important to carefully model both the marginal distribution and the autocorrelation structure to get accurate forecasts of the future bid-ask spread. These findings highlight the strength of modelling using a framework where the choice of marginal distribution can be made independently of the choice of autocorrelation structure.

The rest of the paper is structured as follows. Section 2 outlines the mathematical setup of IVT processes, while Section 3 contains details on the estimation and model selection procedures. Section 4 presents the theory behind our proposed forecasting approach. Section 5 summarises the results from our simulation study, investigating the finite sample properties of the estimation and model selection procedures. Section 6 illustrates the use of the new methodology in an empirical application to financial bid-ask spread data. Section 7 concludes. The proofs of the main mathematical results are given in an Appendix. Practical details on the implementation of the asymptotic theory and additional derivations are given in the Supplementary Material, which also contains further simulation results and extensive details on various calculations used in the implementation of the methods. A software package for the implementation of simulation, estimation, inference, model selection, and forecasting of IVT processes is freely available in the MATLAB programming language.111The software package can be found at https://github.com/mbennedsen/Likelihood-based-IVT.

2 Integer-valued trawl processes

Let denote a probability space, supporting a Poisson random measure , defined on , with mean (intensity) measure . Throughout denotes the Lebesgue measure and is a Lévy measure. A Lévy basis is a homogeneous and independently scattered random measure on , defined as

| (2.1) |

See, e.g., Rajput & Rosinski (1989) and Barndorff-Nielsen (2011) for further details on Lévy bases. Since we are only interested in integer-valued Lévy bases, we will work under the following assumption.

Assumption 2.1.

The Lévy basis is given by (2.1) with Lévy measure , concentrated on the integers (), such that .

The Lévy basis is an infinitely divisible random measure with cumulant (log-characteristic) function

An important random variable associated with the Lévy basis is the so-called Lévy seed, , which we define as the random variable satisfying with .

Remark 2.1.

Because the distribution of a Lévy process is entirely determined by its distribution at a particular time point, we can specify a Lévy process from a Lévy seed , by requiring that .

Using the Lévy seed, we can rewrite the cumulant function of the Lévy basis as , or, for a Borel set

| (2.2) |

From (2.2) we have that , , where denotes the th cumulant of the random variable , when it exists.222Recall that the cumulants of the random variable are defined implicitly through the power series expansion of the cumulant function of , i.e., . In particular , and . The relationship (2.2) implies that the distribution of the random variable is entirely specified by the Lévy seed and the Lebesgue measure of the set . In Section 2.1 below, we illustrate how this can be used to construct trawl processes with a given marginal distribution.

The Lévy basis acts on sets in . We restrict attention to trawl sets of the form

| (2.3) |

where is a trawl function, determining the shape of the trawl set . Section 2.2 contains several parametric examples for the trawl function . We will impose the following assumption.

Assumption 2.2.

The trawl set is given by (2.3), where the trawl function is continuous and monotonically increasing such that .

Intuitively, is obtained from the set by “dragging” it along in time. Note in particular that for all . Finally, define the IVT process as the Lévy basis evaluated over the trawl set:

| (2.4) |

2.1 Modelling the marginal distribution

For an IVT process as defined in (2.4), we have , where is a Lévy process with . Hence we observe that the marginal distribution of the IVT process is entirely decided by the Lebesgue measure of the trawl set and the Lévy seed of the underlying Lévy basis . Indeed, by specifying a distribution for , we can build IVT processes with the corresponding marginal distribution. The following two examples illustrate how to do this; additional details can be found in the Supplementary Material.

Example 2.1 (Poissonian Lévy seed).

Let , i.e. is distributed as a Poisson random variable with intensity . It follows from standard properties of the Poisson distribution that . In other words, for all , , .

Example 2.2 (Negative Binomial Lévy seed).

Let , i.e. is distributed as a Negative Binomial random variable with parameters and . It follows from standard properties of the Negative Binomial distribution that . In other words, for all , , , where for is the -function.

2.2 Modelling the correlation structure

Recall that the shape of the trawl set is determined by the trawl function , see Equation (2.3). A particularly tractable and flexible class of parametrically specified trawl functions are the so-called superposition trawls (Barndorff-Nielsen et al., 2014; Shephard & Yang, 2017). They are defined as , for , where is a probability measure on This construction essentially randomizes the decay parameter in an otherwise exponential function.

The IVT process with a superposition trawl function is stationary. Hence, we get the autocorrelation function (Barndorff-Nielsen et al., 2014)

| (2.5) |

Example 2.3 (Exponential trawl function).

For the case where the measure has an atom at i.e. where is the Dirac delta function at we get for . Consequently, , for .

Example 2.4 (Inverse Gaussian trawl function).

Letting be given by the inverse Gaussian distribution , where is the modified Bessel function of the third kind and with both not zero simultaneously. It can be shown that the resulting trawl function is given by , for , and hence that the correlation function of the IVT process with inverse Gaussian trawl function becomes , for . The details on these calculations can be found in the Supplementary Material.

Example 2.5 (Gamma trawl function).

Let have the density, , where and We can show that , , which implies the correlation function . Note that in this case for and for , from which we see that an IVT process with a Gamma trawl function enjoys the long memory property, in the sense of a non-integrable autocorrelation function, when The details on these calculations can be found in the Supplementary Material.

2.3 Modelling IVT processes

Using the above methods, we can build flexible continuous-time integer-valued processes with a marginal distribution determined by the underlying Lévy basis, and independently specified correlation structure determined by the trawl function. In our main examples given above, we considered a Lévy basis with Poisson or Negative Binomial marginals, and various trawl functions, namely the Exponential trawl function, the IG trawl function, and the Gamma trawl function. Other specifications for the underlying Lévy basis and trawl function than those given here could of course be considered. In practice, these choices should be guided by the properties of the data being modelled.

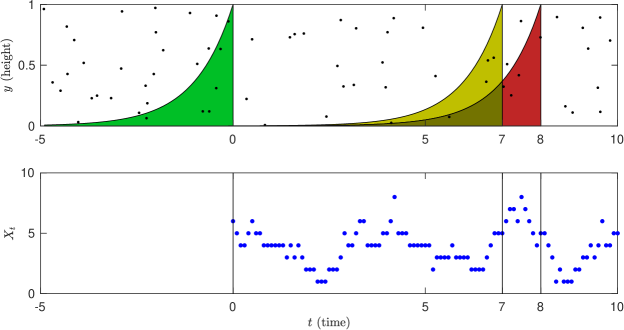

The simplest IVT process we can construct in this way is the Poisson-Exponential IVT process, i.e., the case where and , , see Examples 2.1 and 2.3. This special case results in a Markovian process, which is not in general true of IVT processes (Barndorff-Nielsen et al., 2014). In fact, the model is similar to the popular Poissonian INAR(1) model, introduced in McKenzie (1985) and Al-Osh & Alzaid (1987). An illustration of the exponential trawl set, dragged through time, together with a simulation of the resulting Poisson-Exponential IVT trawl process , is seen in Figure 1. The parameters used are and . At each time point , the value of (bottom plot) is the number of points inside the trawl set (top plot).

3 Estimation of integer-valued trawl processes

Barndorff-Nielsen et al. (2014) showed that the parameter vector of an IVT process can be consistently estimated using a generalized method of moments (GMM) procedure. In Section 3.1, we propose a likelihood-based approach instead. Both estimation procedures rely on the fact that the IVT process is stationary and mixing. The mixing property of IVT processes is obtained from results given in Fuchs & Stelzer (2013), see Barndorff-Nielsen et al. (2014, p. 699). Although mixing, in general, is sufficient for the consistency of the estimators, the central limit theorem for the likelihood-based estimator (Theorem 3.3 below) relies on the stronger mixing concept of -mixing, where the size (or rate) of mixing can also be established. Let us recall the definition of -mixing for a stationary process. Let and, for , , and define the numbers , for . The process is -mixing if as . It is -mixing of size if , as , for some .

We obtain the following important property for IVT processes.

Theorem 3.1.

Remark 3.1.

Remark 3.2.

As an alternative to the proof of Theorem 3.1 provided in Appendix A, we could first show that trawl processes are -weakly dependent, which we do in the Supplementary Material, see Section S12. Then, as pointed out in Curato & Stelzer (2019, p. 324) and shown in the discrete-time case in Doukhan et al. (2012), for integer-valued trawl processes, the fact that they are -weakly dependent, implies that they are strongly mixing with the coefficient as stated in Theorem 3.1.

3.1 Estimation by composite likelihoods

Due to the non-Markovianity of the IVT process, we face computational difficulties when attempting to estimate the model by maximizing the full likelihood, hence we propose to use the CL method instead. The main idea behind the CL approach is to consider a, possibly misspecified, likelihood function which captures the salient features of the data at hand; here this means capturing the features of the Lévy basis, controlling the marginal distribution, and those of the trawl function, controlling the dependence structure. We focus on pairwise CLs.

3.1.1 Pairwise composite likelihood

Suppose we have observations of the IVT process on an equidistant grid of size , for some . Define the following likelihood function using pairs of observations periods apart,

| (3.1) |

where is the joint probability mass function (PMF) of the observations and , parametrized by the vector . From (3.1), we construct the composite likelihood function

| (3.2) |

where denotes the number of pairwise likelihoods to include in the calculation of the composite likelihood function.

The maximum composite likelihood (MCL) estimator of is defined as

| (3.3) |

where is the parameter space and is the log composite likelihood function. To apply this estimator in practice, we need to be able to calculate the PMFs . Section S5 in the Supplementary Material contains a discussion on how to do this in the general integer-valued case. In the count-valued case, takes a particularly simple form which is convenient in implementations. Indeed, letting denote the probability of the event given parameters , we have the following.

Proposition 3.1.

The probabilities in (3.4) can be expressed as a function of the parameters of the Lévy seed and the trawl function. Indeed, for a Borel set we have , where is a Lévy process with , and being the Lévy seed associated to , see Remark 2.1. Also, , and . Plugging these into (3.4) we obtain the pairwise likelihoods, , and thus the CL function, , as a function of .

Example 3.1 (Poisson-Exponential IVT process).

3.1.2 Asymptotic theory

Because we are only considering dependencies across pairs of observations and not their dependence with the remaining observations, the pairwise composite likelihood function (3.2) can be viewed as a misspecified likelihood. Nonetheless, since the individual PMFs in (3.2) are proper bivariate PMFs, the composite score function provides unbiased estimating equations and, under certain regularity assumptions, the usual asymptotic results will apply (Cox & Reid, 2004). However, as pointed out in Varin et al. (2011), formally proving the results in the time series case requires more rigorous treatment. The following two theorems provide the details on the asymptotic theory in the setup of this paper. We will work under the following identification assumption.

Assumption 3.1.

For all , it holds that

| (3.5) |

for some .

First, we have a Law of Large Numbers.

Theorem 3.2.

Remark 3.3.

As is often the case, the identification condition in Assumption 3.1 can be difficult to check in practice. For the IVT processes considered in this paper and presented in the examples above, our numerical experiments indicate that requiring , where denotes the dimension of the parameters controlling the trawl function , results in being identified. A similar requirement was suggested in Davis & Yau (2011).

We also impose a standard assumption on the parameter space.

Assumption 3.2.

The set is compact such that the true parameter vector, , lies in the interior of .

It turns out that the asymptotic behaviour of the MCL estimator differs in the short- and long-memory cases. The former is captured by the following assumption.

Assumption 3.3 (Short memory).

The autocorrelation function of the IVT process satisfies .

Remark 3.4.

Under this assumption, the mixing property of IVT processes, presented in Theorem 3.1, implies that we can invoke a Central Limit Theorem for triangular arrays of mixing processes (Davidson, 1994, Corollary 24.7) to get the following result.

Theorem 3.3.

Theorem 3.3 implies that feasible inference can be conducted using an estimate of the inverse of the Godambe information matrix , where is the MCL estimate from (3.3). Note that while the straight-forward estimator is consistent for due to the stationarity and ergodicity of the IVT process, is more difficult to obtain, since the obvious candidate vanishes at , a fact also remarked in Varin & Vidoni (2005). While it is possible to estimate using a Newey-West-type kernel estimator (Newey & West, 1987), we obtained more precise results using a simulation-based approach to estimating . The details of both approaches are provided in the Supplementary Material, Section S4.333It is also possible to approximate the standard error of using a standard parametric bootstrap approach. However, as we discuss in Section S4.2 of the Supplementary Material, this solution is more computationally expensive than the two alternative approaches suggested here.

3.1.3 Asymptotic theory in the long memory case

While the consistency result in Theorem 3.2 applies for all IVT processes satisfying Assumptions 2.1–2.2 and 3.1, Assumption 3.3, required in the central limit result in Theorem 3.3, excludes IVT processes with long memory, e.g. those with autocorrelation function adhering to for . As mentioned in Remark 3.1, this is for instance the case for the Gamma trawl function (Example 2.5) with .

Although a long memory CLT as such eludes us, we can say some things about the asymptotic behaviour of the MCL estimator in the long memory case. For instance, the convergence rate is likely slower than , as the following result suggests.

Theorem 3.4.

Let the conditions from Theorem 3.2 hold and assume that the autocorrelation function of the IVT process satisfies for some , where is a function which is slowly varying at infinity, i.e. for all it holds that . Then,

-

(i)

For all , , as .

-

(ii)

Let be the dimension of and denote by and the th component of the vectors and , respectively. Then, for , we have that for all , , as .

Theorem 3.4(i) implies that the convergence rate of cannot be slower than for . Further, Theorem 3.4(ii) implies that if the convergence rate is faster than it must necessarily be the case that the limiting random variable has an infinite variance. We conjecture that for a matrix , where is an -stable random vector. Note that, for it is the case , meaning that the conjectured convergence rate is faster than , but slower that . Our reason for the conjecture has its roots in Theorem 3.5 below. First, we introduce a technical assumption on the trawl function , ensuring that we are in the long memory case.

Assumption 3.4 (Long memory).

Assume that and

-

1.

, , where is a function that is slowly varying at infinity.

-

2.

, , where is a function that is slowly varying at infinity.

Theorem 3.5.

Suppose and that the parameters of the trawl function are known. Let the conditions from Theorem 3.2 hold, along with Assumptions 3.2 and 3.4. Then,

where is given as in Theorem 3.3, is an -stable random variable with characteristic function

| (3.6) |

and where is given by

with denoting the de-meaned partial sum of the sequence , where and .

Remark 3.7.

The asymptotic behaviour of the remainder term in Theorem 3.5 is decided by a quite general function of the pairs and one can show that similar issues arise in the more general case where is integer-valued and the parameters in the trawl function are estimated. The asymptotic behaviour of such general functions of the data could possibly be studied using mixing conditions for partial sums with -stable limits (e.g. Jakubowski, 1993) or by deriving Breuer-Major-like theorems (Breuer & Major, 1983; Nourdin et al., 2011) valid for IVT processes using Malliavin calculus for Poissonian spaces, see Basse-O’Connor et al. (2020) for a related approach. We believe that especially this latter route could be fruitful, but leave it for future work.

The proof of Theorem 3.5 relies on a result about the partial sums of the IVT process , which might be of independent interest. We, therefore, state it here.

Theorem 3.6.

Remark 3.8.

Closely related results about partial sums of trawl processes have previously been put forth in Doukhan et al. (2019) and Pakkanen et al. (2021) in the context of a discrete-time trawl process under a standard asymptotic scheme () and in the context of a continuous-time trawl process under an infill asymptotic sampling scheme (), respectively. In this paper, we consider observations of the continuous-time trawl process sampled on an equidistant -grid, , where is fixed, and let . In this sense, our setup is closer to the one in Doukhan et al. (2019). Indeed, it can be shown that the law of is equal to the law of , where is an appropriately specified discrete-time trawl process in the sense of Doukhan et al. (2019). Although this highlights a close connection between the long memory results of Doukhan et al. (2019) and those presented in this section, the underlying assumptions in the two approaches are different. Firstly, the assumptions on the marginal distribution made in Doukhan et al. (2019) are different from ours. In particular, while Doukhan et al. (2019) are not restricting the marginal distribution of the process to be infinitely divisible, they do impose a restrictions on the size of the jumps of the Lévy basis, see Equation (3.36) in Doukhan et al. (2019). Secondly, our assumptions on the correlation structure of the process are slightly different than the assumptions made in Doukhan et al. (2019). In particular, besides polynomial decay, we also allow for a slowly varying function to enter the correlation structure, compare Assumption 3.4 with Equation (2.12) in Doukhan et al. (2019). For these reasons, although our setting is closely related to that in Doukhan et al. (2019), we cannot use their results directly. We can, however, follow similar lines of arguments as done in Doukhan et al. (2019), and this is what we do in the proof of Theorem 3.6, given in the Appendix.

3.2 Information criteria for model selection

Takeuchi’s Information Criterion (Takeuchi, 1976) is an information criterion, which can be used for model selection in the case of misspecified likelihoods. Varin & Vidoni (2005) adapted the ideas of Takeuchi to the composite likelihood framework and provided arguments for using the composite likelihood information criterion (CLAIC)

as a basis for model selection, where is the trace of the matrix . Specifically, Varin & Vidoni (2005) suggest picking the model that maximizes .

Analogous to the usual Bayesian/Schwarz Information Criterion (BIC, Schwarz, 1978), we also suggest the alternative composite likelihood information criterion (Gao & Song, 2010)

where is the number of observations of the data series . Note that the various models we consider are generally non-nested, whereas most research on model selection using the composite likelihood approach has considered nested model (Ng & Joe, 2014). An analysis of the properties of and in the non-nested case in the spirit of, e.g., Vuong (1989) would be very valuable but is beyond the scope of the present article.

4 Forecasting integer-valued trawl processes

Let be the sigma-algebra generated by the history of the IVT process up until time and let be a forecast horizon. We are interested in the predictive distribution of the IVT process, i.e. the distribution of . However, since the IVT process is in general non-Markovian, the distribution of is highly intractable. This problem is similar to the one encountered when considering the likelihood of observations of , cf. Section 3.1. For this reason, we propose to approximate the distribution of by , i.e. instead of conditioning on the full information set, we only condition on the most recent observation. Thus, our proposed solution to the forecasting problem is akin to the proposed solution to the problem of the intractability of the full likelihood. That is, instead of considering the full distribution of , we use the conditional “pairwise” distribution implied by .

To fix ideas, let and , and consider the random variables and . The goal is to find the conditional distribution of given . Note that and are independent random variables. Further, since is independent of with a known distribution, we only need to determine the distribution of given . The following lemma characterises the conditional distribution of .

Lemma 4.1.

Let and , then

Example 4.1.

In the case when , we get the Binomial distribution:

which implies that

Example 4.2.

In the case when , we get the Dirichlet-multinomial distribution:

where and . For , the corresponding probability mass function is given by

where is the binomial coefficient. This implies that, as before,

Using Lemma 4.1, we can derive the distribution of , which can be used for probabilistic forecasting. The details for non-negative-valued Lévy bases are given in the following proposition.

Proposition 4.1.

The following corollaries give the specific details for our two main specifications for the marginal distribution of , studied in Examples 4.1 and 4.2 above.

Corollary 4.1.

If , then

Corollary 4.2.

If , then

If the parameters of an IVT process with Poisson or Negative Binomial marginal distribution are known, we can use Corollary 4.1 or 4.2, and the calculations for the Lebesgue measures of the trawl sets given in Section 2.2, for computing the predictive PMFs and thus for forecasting. When the true parameter values are unknown, they can be estimated using the MCL estimator suggested above, and plugged into the formulas to arrive at estimates of the predictive PMFs.

5 Monte Carlo simulation experiments

Using simulations, we examine the finite sample properties of the composite likelihood-based estimation procedure and of the model selection procedure. Details are available in the Supplementary Material, see Section S6. Here we summarise our main findings.

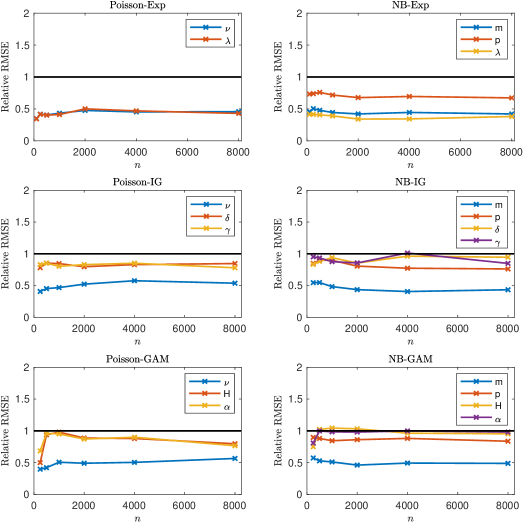

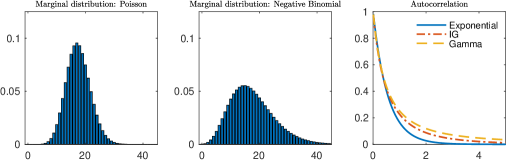

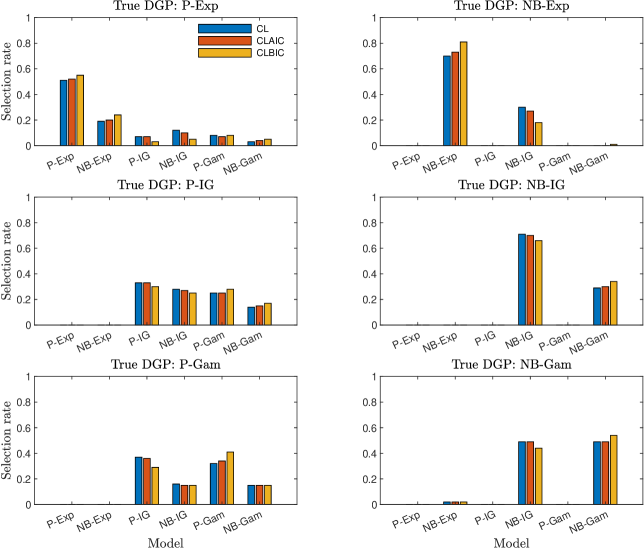

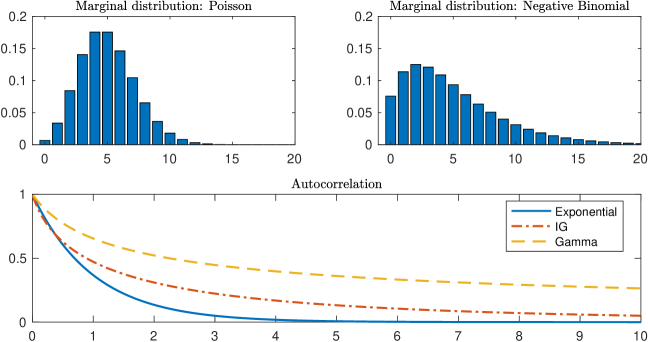

We consider six data-generating processes (DGPs): the Poisson-Exponential (P-Exp), the Poisson-Inverse Gaussian (P-IG), the Poisson-Gamma (P-Gamma), the Negative Binomial-Exponential (NB-Exp), the Negative Binomial-Inverse Gaussian (NB-IG), and the Negative Binomial-Gamma (NB-Gamma) IVT models. The parameter choices used in the simulation study, see Table S1 in the Supplementary Material, are motivated by the estimates of our empirical study.

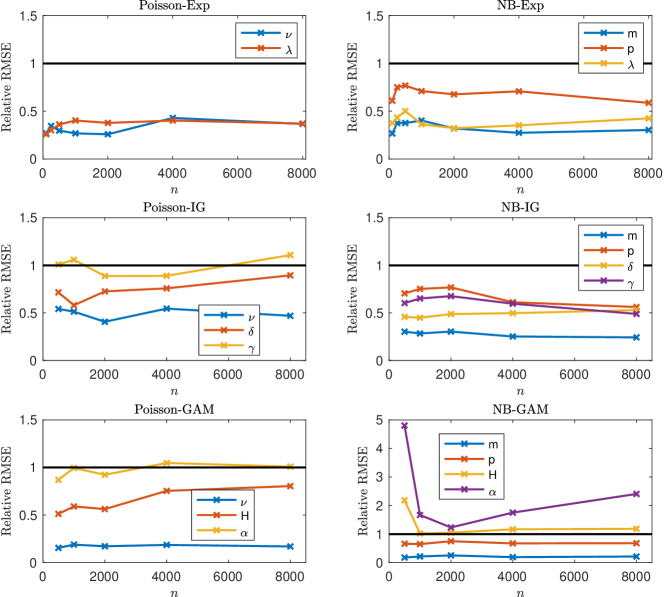

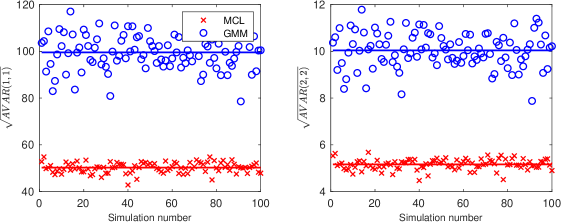

We compare the finite sample properties of the MCL estimator with the GMM estimator, which has been used in the existing literature. Figure 2 plots the root median squared error (RMSE) of the MCL estimator of a given parameter divided by the RMSE of the GMM estimator of the same parameter for the six DGPs. Thus, numbers smaller than one indicate that the MCL estimator has a lower RMSE than the GMM estimator and vice versa for numbers larger than one. We see that for most parameters in most of the DGPs, the MCL estimator outperforms the GMM estimator substantially; indeed, in many cases, the RMSE of the MCL estimator is around that of the GMM estimator. The exception seems to be the trawl parameters, i.e. the parameters controlling the autocorrelation structure, in the case of the Gamma and IG trawls, where the GMM estimator occasionally performs on par with the MCL estimator. However, in most cases, it appears that the MCL estimator is able to provide large improvements over the GMM estimator.

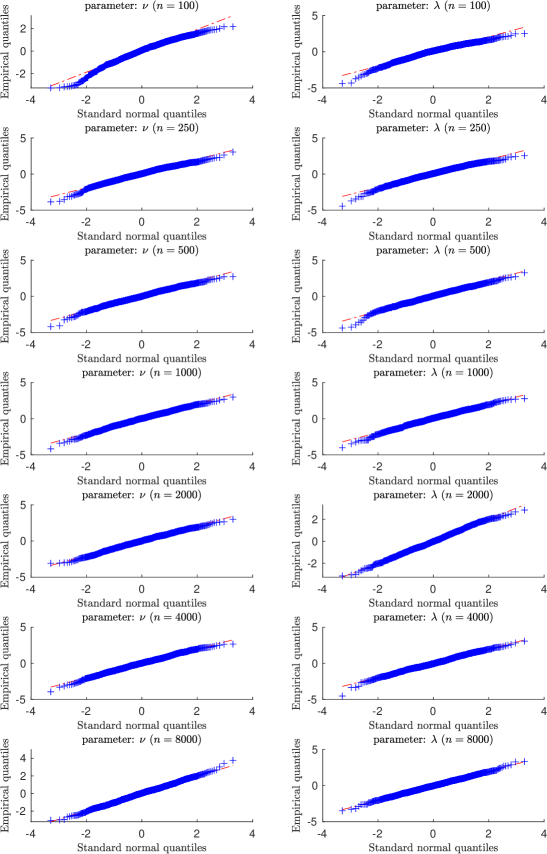

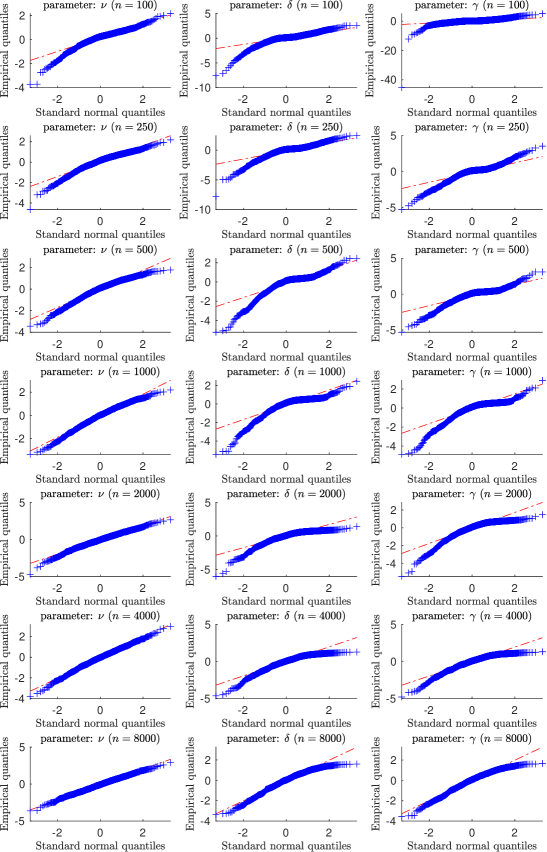

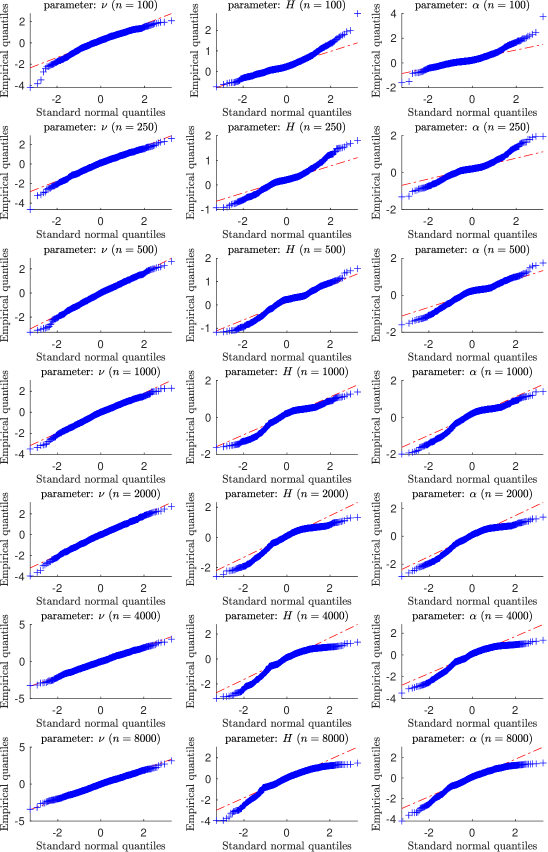

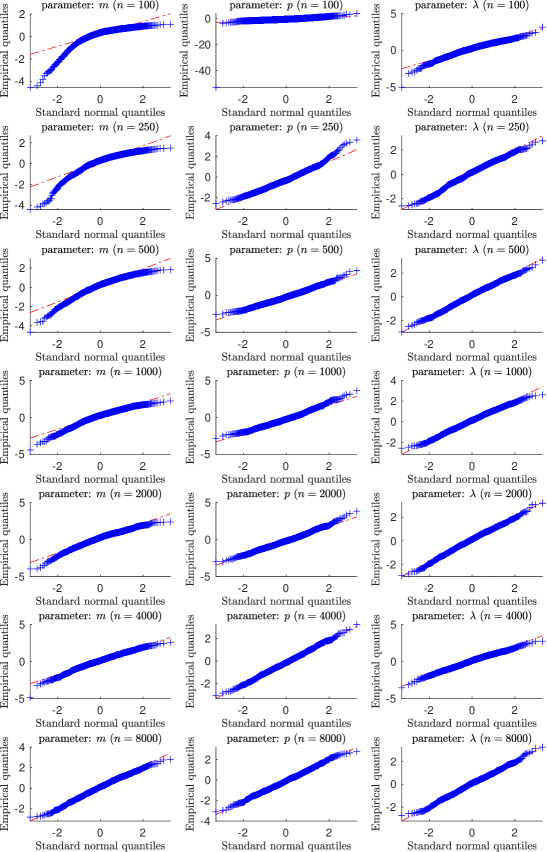

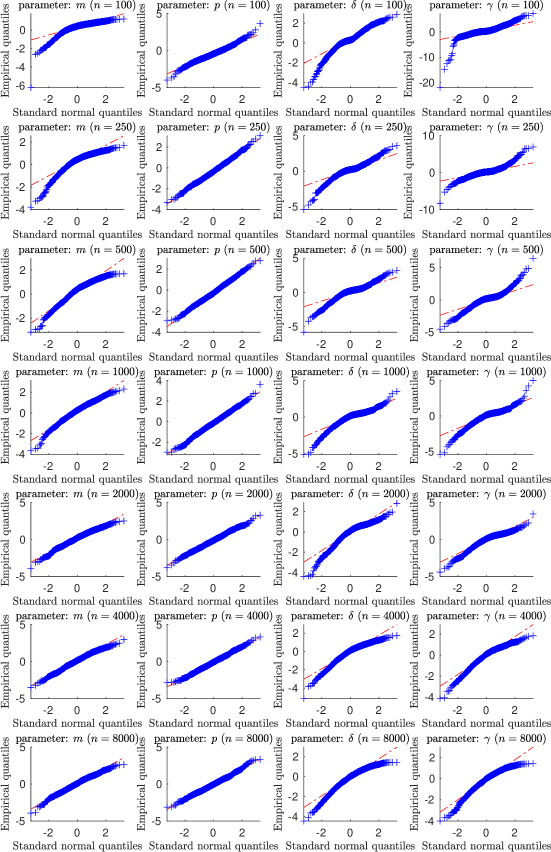

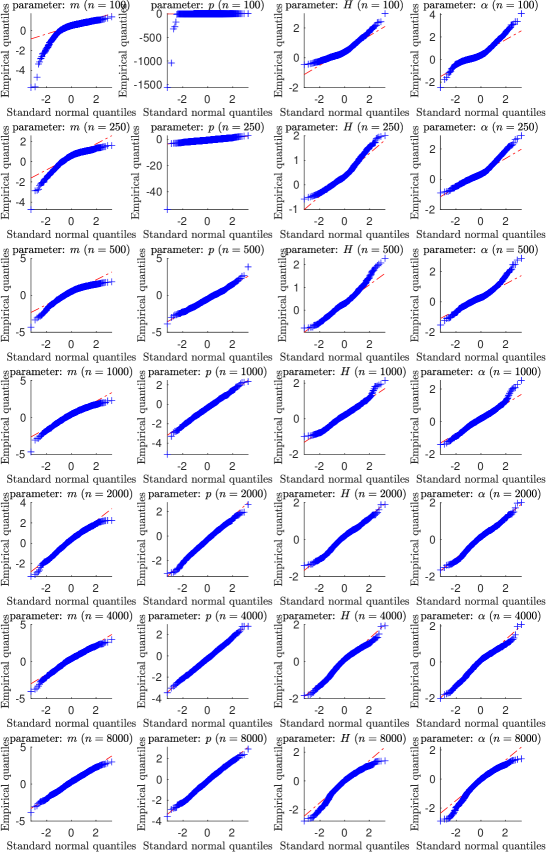

In the Supplementary Material (Section S6.3), we also examine how close the finite sample distribution of the MCL estimator is to the true (Gaussian) asymptotic limit, as presented in Theorem 3.3. We find that the Gaussian approximation is very good for the case of the parameters governing the marginal distribution, as well as for the parameter for the case of IVTs with exponential trawl functions. When there are two parameters in the trawl function ( and in the case of the IG trawl and and in the case of the Gamma trawl), however, the Gaussian distribution can be a poor approximation to the finite sample distribution of the MCL estimator in case of the trawl parameters. This indicates that for constructing confidence intervals or testing hypotheses on these parameters, it might be useful to consider bootstrap approaches instead of relying on the Gaussian distribution.

6 Application to financial bid-ask spread data

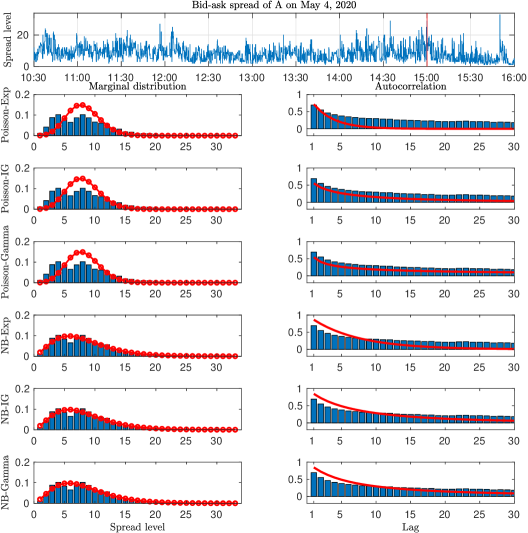

In this section, we apply the IVT modelling framework to the bid-ask spread of equity prices. The bid-ask spread has been extensively studied in the market microstructure literature, see, e.g., Huang & Stoll (1997) and Bollen et al. (2004). An application similar to the one studied in this section was considered in Barndorff-Nielsen et al. (2014). To illustrate the use of the methods proposed in this paper, we study the time series of the bid-ask spread, measured in U.S. dollar cents, of the Agilent Technologies Inc. stock (ticker: A) on a single day, May , . We cleaned the data and sampled the data in 5s intervals, leading to observations, see Section S7 in the Supplementary Material for details.

Let be the bid-ask spread level at time , the time series of which is displayed in the top panel of Figure 3. Since the minimum spread level in the data is one tick (one dollar cent), we work on this time series minus one, i.e on . We can now apply our model selection method. We first inspect the empirical autocorrelation of the data (shown in the right panels of Figure 3) which shows evidence of a very persistent process; we, therefore, set to a moderately large value to accurately capture the dependence structure of the data. Here, we choose but the results are robust to other choices.

| Model: | Poisson-Exponential | Poisson-IG | Poisson-Gamma | NB-Exponential | NB-IG | NB-Gamma |

|---|---|---|---|---|---|---|

Composite likelihood and information criteria values for fitting the A bid-ask spread data on May 4, 2020, shown in the top plot of Figure 3, calculated using six different models as given in the top row of the table using . The maximum value for a given criteria (i.e. row-wise) is given in bold. The parameter estimates corresponding to the fits are given in Table 2.

| DGP | ||||||||

|---|---|---|---|---|---|---|---|---|

| P-Exp | ||||||||

| P-IG | ||||||||

| P-Gamma | ||||||||

| NB-Exp | ||||||||

| NB-IG | ||||||||

| NB-Gamma | ||||||||

Parameter estimates (standard errors in parentheses) from the six different DGPs when applied to the bid-ask spread data of A on May 4, 2020 using the MCL estimator with . The standard errors have been obtained using the simulation-based approach to estimating the asymptotic covariance matrix of the MCL estimator, see Section S4 in the Supplementary Material. Since our asymptotic theory does not cover the long memory case, no standard deviations are reported for the P-Gamma model. See Figure 3 for the resulting fits of the models to the empirical distribution and autocorrelation.

Using this setting, we calculated the maximized composite likelihood value, CL, and the two information criteria, and , obtained for these data using the six models considered in Section 5. The results are shown in Table 1. The table shows that the NB-Gamma model is the preferred model on all three criteria, while the second-best model is the NB-IG model.

To further examine the fit of the various models, the bottom six rows of Figure 3 contain the empirical autocorrelation (left; blue bars) and the empirical marginal distribution of the spread level (right; blue bars). Each respective row also shows the fit of one of the six models considered in Table 1; the parameter estimates corresponding to the models are given in Table 2. The fit of the models shown in the bottom six panels of Figure 3 and the selection criteria of Table 1 indicate that the models based on the Negative Binomial distribution are preferred to the models based on the Poisson distribution. We conclude that, for this data series, the Poisson distribution is unable to accurately describe the marginal distribution of the spread level sampled every seconds. That the Gamma and IG trawl functions are preferred to the Exponential trawl function indicates that the Exponential autocorrelation function is not flexible enough to capture the correlation structure of the data. By both visual inspection of the autocorrelations in Figure 3 and the selection criteria of Table 1, we conclude that the NB-Gamma model is the preferred model for these data. As shown in Table 2, this model has (s.e. ), implying that the model possesses a slowly decaying autocorrelation structure, albeit not the long memory property.

6.1 Forecasting the spread level

This section illustrates the use of IVT models for forecasting, as outlined in Section 4. The aim is to forecast the future spread level of the A stock on May , i.e. the data studied above and plotted in the top panel of Figure 3. We set aside the first observations as an “in-sample period” for initial estimation of the parameters of the models, see the vertical red line in the top panel of Figure 3 for the placement of this split. We then forecast the spread level from seconds until seconds into the future, using the approach presented in Section 4. That is, we forecast given the current value . After this, we update the in-sample data set with one additional observation so that this sample now contains observations. Then we again forecast the next observations, , given . We repeat this procedure until the end of the sample, which yields out-of-sample forecasts for each forecast horizon. To ease the computational burden, we only re-estimate the model every periods (i.e. every minutes).

To evaluate the forecasts, we consider four different loss metrics. The first two, the mean absolute error (MAE) and the mean squared error (MSE), are often used in econometric forecasting studies of real-valued data (e.g. Elliott & Timmermann, 2016). For a forecast horizon , define the mean absolute forecast error,

where is the -step ahead forecast of , constructed using the information available up to observation . That is, is the point forecast of coming from a particular IVT model, such as the conditional mean, median, or mode. In what follows, we set equal to the estimated conditional mean, i.e. we set , where is a large (cut-off) number and is the estimated predictive density of the IVT model.444Letting be the conditional mode, instead of the conditional mean, produces results similar to those reported here. These results are reported in the Supplementary Material, Section S7.2. Here, we set but the results are very robust to other choices. Define also the mean squared forecast error

We consider two additional loss metrics, designed to directly evaluate the accuracy of the estimated predictive PMF , which is arguably more relevant to the problem at hand than MAE and MSE. The first is the logarithmic score (Elliott & Timmermann, 2016, p. 30),

where is the realized outcome. The second is the ranked probability score (RPS; Epstein, 1969),

where is the estimated cumulative distribution function of coming from a given model and is the indicator function of the event .

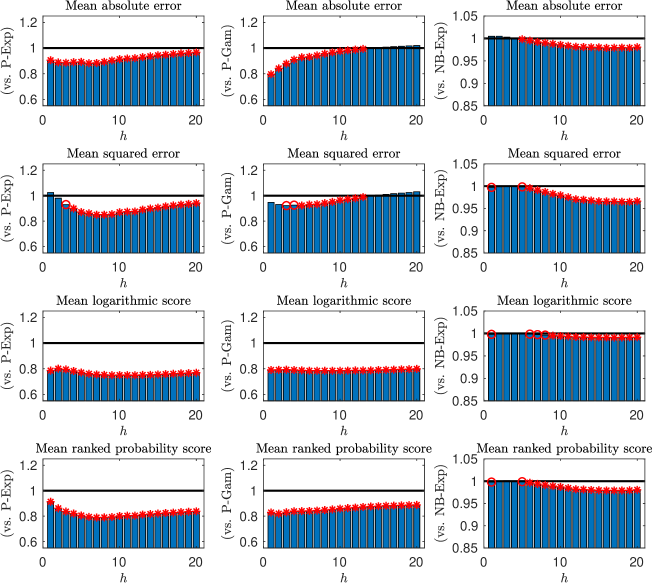

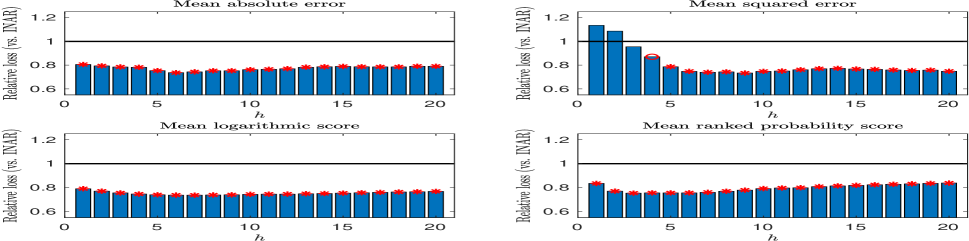

Figure 4 shows the four different forecast loss metrics for the preferred NB-Gamma IVT model as a ratio of the forecasting loss of a given benchmark model in the out-of-sample forecasting exercise described above. The numbers plotted in the figure are , where “” denotes one of the four loss metrics given above and denotes the forecasting horizon. Thus, numbers less than one favour the NB-Gamma model compared to the benchmark model and vice versa for numbers greater than one. Initially, we choose the Poisson-Exponential IVT process as the benchmark model (Figure 4, first column); as remarked above, this process is identical to the Poissonian INAR(1) model, which is often used for forecasting count-valued data (e.g. Freeland & McCabe, 2004; McCabe & Martin, 2005; Silva et al., 2009). It is evident from the figure that losses from the NB-Gamma model are smaller than those from the Poisson-Exponential model for practically all forecast horizons and loss metrics. In the case of the two most relevant loss functions for evaluating the predictive distribution, the logS and RPS, the reduction in losses are substantial for all forecast horizon, on the order of .

To assess whether these loss differences are also statistically significant, we perform the Diebold-Mariano test of superior predictive ability (Diebold and Mariano, 1995). The null hypothesis of the statistical test is that the two models have equal predictive power, while the alternative hypothesis is that the NB-Gamma model provides superior forecasts compared to the benchmark model. In Figure 4, a circle (asterisk) denotes rejection of the Diebold-Mariano test at a () level. The test rejects the null hypothesis of equal predictive ability for almost all forecast horizons and loss metrics at a level.

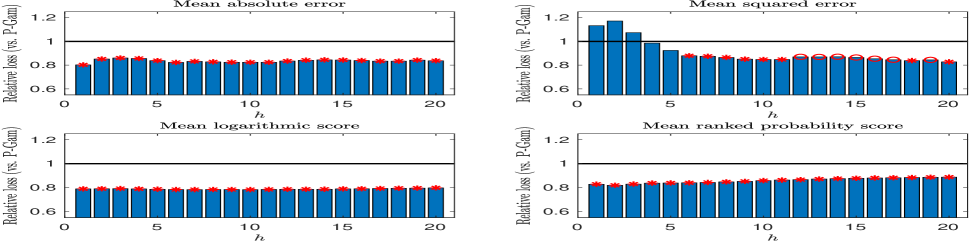

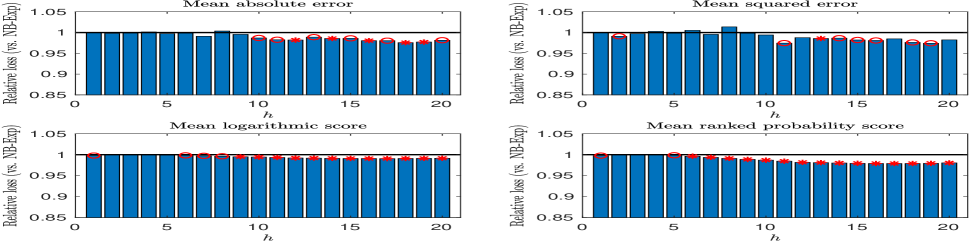

To investigate whether the increased forecast performance of the NB-Gamma model comes from having a more flexible marginal distribution than the Poisson-Exponential benchmark model (Negative Binomial vs. Poisson marginals) or from having a more flexible correlation structure (polynomial decay vs. exponential decay) or both, we compare the forecasts from NB-Gamma model to those coming from a Poisson-Gamma model and from an NB-Exp model. These results are given in the second and third columns of Figure 4, respectively. From the second column, we see that the NB-Gamma model outperforms the Poisson-Gamma model considerably, especially for the shorter forecast horizons, indicating that it is important to use a model with Negative Binomial marginals when forecasting these data. From the third column of the figure, we see that for the shorter forecast horizons, the NB-Exp model performs on par with the NB-Gamma model, but for the longer forecast horizons, the NB-Gamma model is superior. Hence, when forecasting, it also appears to be important to specify a model with an accurate autocorrelation structure, especially for longer forecasting horizons.

7 Conclusion

This paper has developed likelihood-based methods for the estimation, inference, model selection, and forecasting of IVT processes. We proved the consistency and asymptotic normality of the MCL estimator and provided the details on how to conduct feasible inference and model selection. We also developed a pairwise approach to approximating the conditional predictive PMF of the IVT process, which can be used for forecasting integer-valued data. All these methods are implemented in a freely available software package written in the MATLAB programming language.

In a simulation exercise, we demonstrated the good properties of the MCL estimator compared to the often-used method-of-moments-based estimator. Indeed, the reduction in root median squared error of the MCL estimator was in many cases more than compared to the corresponding GMM estimator.

In an empirical application to financial bid-ask spread data, we illustrated the model selection procedure and found that the Negative Binomial-Gamma IVT model provided the best fit for the data. Using the forecast tools developed in the paper, we saw that this model outperformed the simpler Poisson-Exponential IVT model considerably, resulting in a reduction in forecast loss on the order of for most forecast horizons. We demonstrated that most of the superior forecasting performance came from accurate modelling of the marginal distribution of the data; however, we also found that it was beneficial to carefully model the autocorrelation structure, especially for longer forecasting horizons. These findings highlight the strengths of the IVT modelling framework, where the marginal distribution and autocorrelation structure can be modelled independently in a flexible fashion.

References

- (1)

- Abramowitz & Stegun (1972) Abramowitz, M. & Stegun, I. A. (1972), Handbook of mathematical functions with formulas, graphs, and mathematical tables, Vol. 55, 10th edn, United States Department of Commerce.

- Al-Osh & Alzaid (1987) Al-Osh, M. A. & Alzaid, A. A. (1987), ‘First-order integer-valued autoregressive (INAR(1)) process’, Journal of Time Series Analysis 8(3), 261–275.

- Andrieu et al. (2010) Andrieu, C., Doucet, A. & Holenstein, R. (2010), ‘Particle Markov chain Monte Carlo methods’, Journal of the Royal Statistical Society: Series B 72, 269–342.

- Barndorff-Nielsen (2011) Barndorff-Nielsen, O. E. (2011), ‘Stationary infinitely divisible processes’, Brazilian Journal of Probability and Statistics 25(3), 294 – 322.

- Barndorff-Nielsen et al. (2009) Barndorff-Nielsen, O. E., Hansen, P. R., Lunde, A. & Shephard, N. (2009), ‘Realized kernels in practice: trades and quotes’, The Econometrics Journal 12(3), C1–C32.

- Barndorff-Nielsen et al. (2014) Barndorff-Nielsen, O. E., Lunde, A., Shephard, N. & Veraart, A. (2014), ‘Integer-valued trawl processes: A class of stationary infinitely divisible processes’, Scandinavian Journal of Statistics 41, 693–724.

- Barndorff-Nielsen et al. (2012) Barndorff-Nielsen, O. E., Pollard, D. G. & Shephard, N. (2012), ‘Integer-valued Lévy processes and low latency financial econometrics’, Quantitative Finance 12, 587–605.

- Basse-O’Connor et al. (2020) Basse-O’Connor, A., Podolskij, M. & Thäle, C. (2020), ‘A Berry–Esseén theorem for partial sums of functionals of heavy-tailed moving averages’, Electronic Journal of Probability 25, 1–31.

- Bingham et al. (1989) Bingham, N. H., Goldie, C. M. & Teugels, J. L. (1989), Regular Variation, Cambridge University Press.

- Bollen et al. (2004) Bollen, N. P. B., Smith, T. & Whaley, R. E. (2004), ‘Modeling the bid/ask spread: measuring the inventory-holding premium’, Journal of Financial Economics 72(1), 97–141.

- Breuer & Major (1983) Breuer, P. & Major, P. (1983), ‘Central limit theorems for non-linear functionals of Gaussian fields’, Journal of Multivariate Analysis 13(3), 425–441.

- Chen et al. (2016) Chen, J., Huang, Y. & Wang, P. (2016), ‘Composite likelihood under hidden Markov model’, Statistica Sinica 26(1), 1569–1586.

- Courgeau & Veraart (2021) Courgeau, V. & Veraart, A. (2021), Asymptotic theory for the inference of the latent trawl model for extreme values. Available at SSRN: https://ssrn.com/abstract=3527739 or http://dx.doi.org/10.2139/ssrn.3527739.

- Cox & Reid (2004) Cox, D. R. & Reid, N. (2004), ‘A note on pseudolikelihood constructed from marginal densities’, Biometrika 91(3), 729–737.

-

Curato & Stelzer (2019)

Curato, I. V. & Stelzer, R. (2019), ‘Weak dependence and GMM estimation of supOU and mixed moving average

processes’, Electronic Journal of Statistics 13(1), 310 – 360.

https://doi.org/10.1214/18-EJS1523 -

Curato et al. (2022)

Curato, I. V., Stelzer, R. & Ströh, B. (2022), ‘Central limit theorems for stationary random fields

under weak dependence with application to ambit and mixed moving average

fields’, The Annals of Applied Probability 32(3), 1814 – 1861.

https://doi.org/10.1214/21-AAP1722 - Davidson (1994) Davidson, J. (1994), Stochastic Limit Theory: Introduction for Econometricians, Advanced Texts in Econometrics, Oxford University Press.

- Davis & Yau (2011) Davis, R. A. & Yau, C. Y. (2011), ‘Comments on pairwise likelihood in time series models’, Statistica Sinica 21(1), 255–277.

-

Dedecker & Rio (2000)

Dedecker, J. & Rio, E. (2000), ‘On

the functional central limit theorem for stationary processes’, Annales

de l’Institut Henri Poincare (B) Probability and Statistics 36(1), 1–34.

https://www.sciencedirect.com/science/article/pii/S0246020300001114 - Diebold & Mariano (1995) Diebold, F. X. & Mariano, R. S. (1995), ‘Comparing predictive accuracy’, Journal of Business & Economic Statistics 13(3), 253–263.

-

Doukhan et al. (2012)

Doukhan, P., Fokianos, K. & Li, X. (2012), ‘On weak dependence conditions: The case of discrete

valued processes’, Statistics & Probability Letters 82(11), 1941–1948.

https://www.sciencedirect.com/science/article/pii/S0167715212002544 - Doukhan et al. (2019) Doukhan, P., Jakubowski, A., Lopes, S. R. C. & Surgailis, D. (2019), ‘Discrete-time trawl processes’, Stochastic Processes and their Applications 129(4), 1326–1348.

- Elliott & Timmermann (2016) Elliott, G. & Timmermann, A. (2016), Economic Forecasting, Princeton University Press.

- Engle et al. (2020) Engle, R. F., Pakel, C., Sheppard, K. & Shephard, N. (2020), ‘Fitting vast dimensional time-varying covariance models’, Journal of Business and Economic Statistics .

- Epstein (1969) Epstein, E. S. (1969), ‘A scoring system for probability forecasts of ranked categories’, Journal of Applied Meteorology and Climatology 8(6), 985–987.

- Flury & Shephard (2011) Flury, T. & Shephard, N. (2011), ‘Bayesian inference based only on simulated likelihood: particle filter analysis of dynamic economic models’, Econometric Theory (27), 933–956.

- Freeland & McCabe (2004) Freeland, R. K. & McCabe, B. P. M. (2004), ‘Forecasting discrete valued low count time series’, International Journal of Forecasting 20(3), 427–434.

- Fuchs & Stelzer (2013) Fuchs, F. & Stelzer, R. (2013), ‘Mixing conditions for multivariate infinitely divisible processes with an application to mixed moving averages and the supOU stochastic volatility model’, ESAIM: Probability and Statistics 17, 455–471.

- Gao & Song (2010) Gao, X. & Song, P. X. K. (2010), ‘Composite likelihood Bayesian information criteria for model selection in high-dimensional data’, Journal of the American Statistical Association 105(492), 1531–1540.

- Godambe (1960) Godambe, V. P. (1960), ‘An optimum property of regular maximum likelihood equation’, Ann. Math. Stat. 31, 1208–1211.

- Gradshteyn & Ryzhik (2007) Gradshteyn, I. S. & Ryzhik, I. M. (2007), Table of integrals, series, and products, seventh edn, Academic Press, Amsterdam.

- Groß-KlußMann & Hautsch (2013) Groß-KlußMann, A. & Hautsch, N. (2013), ‘Predicting bid–ask spreads using long-memory autoregressive conditional Poisson models’, Journal of Forecasting 32(8), 724–742.

- Hjort & Omre (1994) Hjort, N. L. & Omre, H. (1994), ‘Topics in spatial statistics (with discussion, comments and rejoinder)’, Scandinavian Journal of Statistics 21, 289–357.

- Huang & Stoll (1997) Huang, R. D. & Stoll, H. R. (1997), ‘The components of the bid-ask spread: A general approach’, The Review of Financial Studies 10(4), 995–1034.

- Ibragimov & Linnik (1971) Ibragimov, I. A. & Linnik, Y. V. (1971), Independent and Stationary Sequences of Random Variables, Wolters-Noordhoff.

- Jakubowski (1993) Jakubowski, A. (1993), ‘Minimal conditions in p-stable limit theorems’, Stochastic Processes and their Applications 44, 291–327.

- Larribe & Fearnhead (2011) Larribe, F. & Fearnhead, P. (2011), ‘On composite likelihoods in statistical genetics’, Statistica Sinica 21(1), 43–69.

- Lerman & Manski (1981) Lerman, S. & Manski, C. (1981), On the use of simulated frequencies to approximate choice probabilities, in S. Lerman & C. Manski, eds, ‘Structural analysis of discrete data with econometric applications’, MIT Press, pp. 305–319.

- Lindsay (1988) Lindsay, B. (1988), ‘Composite likelihood methods’, Contemporary Mathematics 80, 220–239.

-

Mátyás (1999)

Mátyás, L., ed. (1999), Generalized method of moments estimation, Cambridge University Press,

Cambridge.

https://doi.org/10.1017/CBO9780511625848 - McCabe & Martin (2005) McCabe, B. & Martin, G. (2005), ‘Bayesian predictions of low count time series’, International Journal of Forecasting 21(2), 315–330.

- McKenzie (1985) McKenzie, E. (1985), ‘Some simple models for discrete variate time series’, Journal of the American Water Resources Association 21(4), 645–650.

- Newey & McFadden (1994) Newey, W. K. & McFadden, D. (1994), Chapter 36: Large sample estimation and hypothesis testing, Vol. 4 of Handbook of Econometrics, Elsevier, pp. 2111 – 2245.

- Newey & West (1987) Newey, W. K. & West, K. D. (1987), ‘a simple positive semi-definite heteroskedasticity and autocorrelation consistent covariance matrix’, Econometrica 55(3), 703–708.

- Ng & Joe (2014) Ng, C. T. & Joe, H. (2014), ‘Model comparison with composite likelihood information criteria’, Bernoulli 20(4), 1738–1764.

- Ng et al. (2011) Ng, C. T., Joe, H., Karlis, D. & Liu, J. (2011), ‘Composite likelihood for time series models with a latent autoregressive process’, Statistica Sinica 21(1), 279–305.

- Nourdin et al. (2011) Nourdin, I., Peccati, G. & Podolskij, M. (2011), ‘Quantitative Breuer–Major theorems’, Stochastic Processes and their Applications 121(4), 793–812.

- Noven et al. (2018) Noven, R., Veraart, A. E. D. & Gandy, A. (2018), ‘A latent trawl process model for extreme values’, Journal of Energy Markets 11(3), 1–24.

- Pakkanen et al. (2021) Pakkanen, M. S., Passeggeri, R., Sauri, O. & Veraart, A. E. D. (2021), Limit theorems for trawl processes. Forthcoming in Electronic Journal of Probability.

- Rajput & Rosinski (1989) Rajput, B. S. & Rosinski, J. (1989), ‘Spectral representations of infinitely divisible processes’, Probability Theory and Related Fields 82(3), 451–487.

- Schwarz (1978) Schwarz, G. (1978), ‘Estimating the dimension of a model’, The Annals of Statistics 6(2), 461–464.

- Shephard & Yang (2016) Shephard, N. & Yang, J. J. (2016), Likelihood inference for exponential-trawl processes, in M. Podolskij, R. Stelzer, S. Thorbjørnsen & A. E. D. Veraart, eds, ‘The Fascination of Probability, Statistics and their Applications: In Honour of Ole E. Barndorff-Nielsen’, Springer International Publishing, pp. 251–281.

- Shephard & Yang (2017) Shephard, N. & Yang, J. J. (2017), ‘Continuous time analysis of fleeting discrete price moves’, Journal of the American Statistical Association 112(519), 1090–1106.

- Silva et al. (2009) Silva, N., Pereira, I. & Silva, M. E. (2009), ‘Forecasting in INAR(1) model’, Revstat - Statistical Journal 7(1), 119–134.

-

Sørensen (2019)

Sørensen, H. (2019), ‘Independence,

successive and conditional likelihood for time series of counts’, Journal of Statistical Planning and Inference 200, 20–31.

https://www.sciencedirect.com/science/article/pii/S0378375818302556 - Takeuchi (1976) Takeuchi, K. (1976), ‘Distribution of informational statistics and a criterion of model fitting’, Suri Kagaku [Mathematical Sciences] (in Japanese) 153, 12–18.

- Varin et al. (2011) Varin, C., Reid, N. & Firth, D. (2011), ‘An overview of composite likelihood methods’, Statistica Sinica 21(1), 5–42.

- Varin & Vidoni (2005) Varin, C. & Vidoni, P. (2005), ‘A note on composite likelihood inference and model selection’, Biometrika 92(3), 519–528.

- Veraart (2019) Veraart, A. E. (2019), ‘Modeling, simulation and inference for multivariate time series of counts using trawl processes’, Journal of Multivariate Analysis 169, 110–129.

- Vuong (1989) Vuong, Q. H. (1989), ‘Likelihood ratio tests for model selection and non-nested hypotheses’, Econometrica 57(2), 307–333.

- Wooldridge (1994) Wooldridge, J. M. (1994), Chapter 45: Estimation and inference for dependent processes, Vol. 4 of Handbook of Econometrics, Elsevier, pp. 2639 – 2738.

Appendix A Mathematical proofs

We first give an alternative representation of the Lévy basis , underlying the IVT process X. From the construction of the IVT process in Section 2 in the main article, it is clear that the distribution of is representable as a compound Poisson distribution. That is, for a Borel set , we can write

| (A.1) |

where are iid integer-valued random variables with probability mass function , i.e. , where is the Lévy measure given in the construction of the IVT process in Equation. Likewise, is a Poisson random measure, given by

with an underlying intensity . The random variables are independent of the random measure . Intuitively, we have decomposed the event that the sum of the points in the set equals (i.e. ) into the intersection of the two events that there are individual points in (i.e. ) and the “sizes” of these points add up to (i.e. ). With this construction, we have

| (A.2) |

We will use this alternative representation of in our proofs below.

Proof of Theorem 3.1.

Let and define as the Poisson random variable, which counts the number of ‘events’ in the set . From (A.2), we know that there exists a constant such that

and, therefore,

| (A.3) |

as .

Let and be such that , and write, using the law of total probability,

where

We seek to bound these expressions. For , we use the fact that on the event the two events and are independent. For both and , we will use that the probability of the complementary event is “small enough”, cf. Equation (A.3). For the first of the terms, we get, using conditional independence of and and (A.3),

and, using the Bayes formula and then the law of total probability,

We conclude that

For the second term above, we get

where

Now, by (A.3),

Also,

Using Bayes formula, we can write

so that, from (A.3),

We conclude that

Taking it all together, we have that

implying, since and were arbitrary, that (taking supremums)

which implies that .

To finish the proof, we show that we also have . Letting and defining the events and , the results and the arguments in the proof of Lemma A.1 imply that

Since, clearly, and , we conclude that .

∎

Proof of Proposition 3.1.

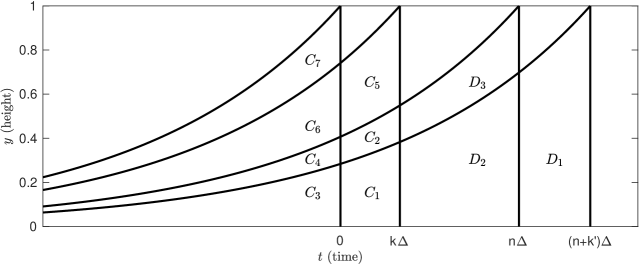

When for we have for . Further, since the maximal amount of events in is bounded by the number of events in and (no negative values in the trawl sets), we also have for . This, together with the discussion of the decomposition of trawl sets in Section 3.1.1 (cf. Figure S1 in the Supplementary Material), and the law of total probability implies that

as we wanted to show. ∎

Proof of Theorem 3.2.

Due to the stationarity and ergodicity of the IVT processes considered in this paper, the normalized log-composite likelihood function will converge in probability to its population counterpart, i.e.

as . By the identifiability condition (3.5), and the fact that the pairwise likelihoods are indeed proper (bivariate) likelihoods, the information inequality implies that is uniquely maximized at (Lemma 2.2 in Newey & McFadden 1994, p. 2124). The result now follows from Theorem 4.1 and Theorem 4.3 in Wooldridge (1994). ∎

Proof of Theorem 3.3.

Let

denote the score function and consider the estimating equation related to the MCL estimator , namely . Using this equation, we Taylor expand around the true parameter vector to get

where lies on the line segment between and and is shorthand for . Rearranging this equation and multiplying through by , we get

Stationarity and ergodicity, along with consistency of due to Theorem 3.2, implies that as . To prove the result, we thus need to show that as . By the mixing properties of the IVT process , given in Theorem 3.1, it is enough to show that and as (e.g. Davidson 1994, Corollary 24.7, p. 387).555Note that the crucial condition (c’) of Corollary 24.7 in Davidson (1994) relies on the IVT process being mixing of size for some . This rules out the long memory processes, as shown in Theorem 3.1.

To show this, we consider, for simplicity, the case where is a scalar. The vector case is similar, but with slightly more involved notation. First note that, clearly,

Also

Due to stationarity, the first sum is as . To prove the proposition, we, therefore, investigate the second sum. With slight abuse of notation, let be denoted by . For , define also the joint probability mass functions

and

Now, using that

we have, for all ,

where the last equality follows because e.g.,

Now, Lemma A.1 below shows that

from which we conclude, using Equation (2.5), i.e. , and the condition on imposed in the theorem, that the second sum in the expression for is as well. Indeed, taking it all together, we have that, as ,

where the series converges. This finalizes the proof.

∎

Lemma A.1.

Fix , let be an IVT process, let be the joint PMF of , and let be the joint PMF of . That is

and

Define the function

The following holds:

where is a function, given in Equation (A.7) below, that depends on the Lévy basis and trawl function of . (In Remark A.1 below, we give the function in the special case where the Lévy basis is Poissonian and the trawl function is the Gamma trawl.)

Proof of Lemma A.1.

Letting , we can write

To prove the lemma, we, therefore, study the asymptotic behaviour of as .

Recall first the decomposition of the trawl sets into three disjoint sets which led to Proposition 3.1, see Figure S1. In a similar manner, we can decompose the four trawl sets associated to , , , and , into disjoint sets as illustrated in Figure 5 below. For ease of notation, we ignore the dependence on , , and for a moment and write

where the sets are disjoint. We will use below that for , , , , , , and , cf. Figure 5.

Using this decomposition and the law of total probability, we may write

and

Taking these together, we get

Note that, for the first term in the parenthesis, the following holds

which allows us to write

Define the set . The above calculations imply that

| (A.4) |

where

and

We can think of as the part of where , while is the remainder.

We study first the behavior of as . Considering the first two factors of this term, the continuity of the probability measure implies that

The third term in , i.e.

will, by the same logic as above, converge to zero as . In fact, by decomposition of the trawl sets of in the same manner as above, we get that

In the first part of Lemma A.2 below, we show that there exists a constant , such that

as . Similarly, in the second part of Lemma A.2, we show that there exists a non-negative function concentrated on the integers, such that, for ,

as , while

as . This shows that for quadruplets where for some and for the remaining (i.e. quadruplets of the form , , or ), we have

as . Conversely, for quadruplets where for at least two distinct , we have

as .

Define the numbers , , which are such that since , cf. Figure 5 below. Taking the above together, we may, after a little algebra, conclude that, as ,

| (A.5) | ||||

Turning now to , similar calculations yield that, as ,

| (A.6) |

Finally, recalling Equation (A.4), we can conclude that

| (A.7) |

where for are given above in Equations (A.5)–(A.6). (See the following Remark A.1 for how the expression for simplifies slightly in the case of an IVT process with Poisson Lévy basis and Gamma trawl function.)

∎

Remark A.1.

Note that in the case of a Poisson Lévy basis (Example 2.1 in the main article), we have , , and for . Further, in the case of being a Gamma trawl function (Example 2.5), it is straightforward to show that and . For this specification, the limit in the proof of Lemma A.1 simplifies somewhat. Indeed, in this case, Equation (A.7) yields

Lemma A.2.

In the setting of the proof of Lemma A.1, we have the following two-part result.

(First part) There exists a constant , such that

as .

(Second part) There exists a non-negative function , concentrated on the integers, such that, for ,

as , while

as .

Proof of Lemma A.2.

The proof of the lemma relies on the alternative representation of the Lévy basis given at the start of the Appendix, see Equation (A.1).

(Proof of second part) Note that since , we have . Using this in the setup of Lemma A.1, we get, from Equations (A.1) and (A.2),

as , while for ,

as . This proves the second part of the lemma.

(Proof of first part) As for the first part, use Equations (A.1) and (A.2) to write

as , where we in the last line Taylor expanded the exponential function. This proves the first part of the lemma.

∎

Proof of Theorem 3.4.

With similar calculations to those used in the proof of Theorem 3.3, we can write

We again have that as . As in the proof of Theorem 3.3, we can write

where is . Further, Lemma A.1 implies that

as . Equation (2.5) along with the condition on imposed in the theorem thus yields

as . Using this, we get that, for all ,

| (A.8) |

as . Finally, we recall the so-called Potter bounds for slowly varying functions: Since is a slowly varying function, for all it holds that (Bingham et al. 1989, Theorem 1.5.6(ii))

as . Combining the Potter bounds with (A.8) yields the required results. ∎

Proof of Theorem 3.5.

Set, for simplicity, . From the proof of Theorem 3.3, it is clear that the asymptotic behaviour of is governed by the asymptotic behaviour of the score function

| (A.9) |

Let be a Borel set. Since , we have

Hence,

Using this, along with Proposition 3.1, it is straightforward to show that

| (A.10) |

where

| (A.11) |

and

| (A.12) |

Define , . Recall that from which we deduce that

Using the above and Equations (A.10)–(A.11) in Equation (A.9), we get

Using arguments similar to those in the proof of Theorem 3.3, the result now follows from Theorem 3.6.

∎

Before we provide the proof of Theorem 3.6, we will need the following two lemmas. For two sequences , we will write “” if tends to a non-zero constant as .

Lemma A.3.

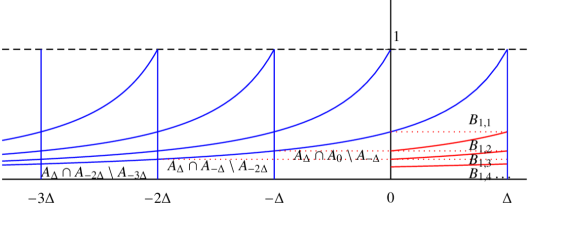

Let Assumption 3.4 hold and define the sets

| (A.13) |

for and . Then, for all ,

where . In particular,

and

Proof of Lemma A.3.

Fix and . Using the mean value theorem twice, we may write,

where and , which proves the first part of the lemma. Note that and will in general depend on and , but we will suppress this for ease of notation. The latter parts of the lemma now follow from Assumption 3.4. ∎

Lemma A.4.

Proof of Lemma A.4.

Proof of Theorem 3.6.

Suppose for simplicity that for some . The general case follows along similar lines to the proof in the Poisson case, using the compound Poisson representation of the IVT process as presented above.

We follow the strategy of the proof outlined in Theorem 2 of Doukhan et al. (2019), adapted to our purposes. First, define the sequence of random variables

where the sum converges almost surely by Kolmogorov’s three-series theorem. Note that

and, hence, applying a time shift of leads to

We observe that we can write as a sum of independent variables,

where are disjoint sets, given as in Equation (A.14). The construction of , and the decomposition into independent variables, are illustrated in Figure 6. Note furthermore that, by construction, the sequence is iid. Let denote the de-meaned partial sums of a process, e.g. . Here we use the short-hand notation that . Our aim is to show that

-

(i)

, as , where is a slowly varying function.

-

(ii)

, as .

Indeed, the result of the present theorem follows from (i) and (ii). To see this, note that (i) implies that (Ibragimov & Linnik 1971, Theorem 2.6.7)

where is an -stable random variable with characteristic function as given in Equation (3.6). Secondly, (ii) now implies that

which is what we wanted to show.

We proceed to prove (i). First, let be given by

where is the indicator of the set . Note that . Second, define . Let be a slowly varying function. As in Doukhan et al. (2019), we prove that (a) and (b) as , which allows us to deduce (i), i.e. as .

To prove (a), define the random variables

where, as before,

| (A.15) |

The intuition is that takes the value if there is an observation in but not in , while takes the value if there is an observation in and precisely one observation in . Note that . Define, analogously to above , which is with the two largest “points” removed.666It can be shown that if , then we can set , i.e., in this case, we only need to remove the largest point from for the proof to go through. We prove that (a’) and (b’) and as , which allows us to deduce (a), i.e. as . As noted in Doukhan et al. (2019), to prove (a’), we only need to prove for , where . Let therefore . We get, using Lemma A.4 and the fact that ,

as .

To prove (b’), note that, by Lemma A.4,

as , by Lemma A.4. To show that as , we show that is bounded in . Let . Using Minkowski’s inequality, the independence of and , and Lemmas A.3 and A.4, we get

where we used, repeatedly, that .

To prove (b), we show that is bounded in . We utilize the assumption that , which implies that for all Borel sets . This allows us to write

and

We deduce that

Using this and then Minkowski’s inequality, we may write

by Lemma A.3.

We now prove (ii). Let . Note first that

and

see Figure 6 for an illustration of these results. Now, following again Doukhan et al. (2019), we can use this to write

where

and

Let . By Karamata’s Theorem, Assumption 3.4, and properties of slowly varying functions, we have

as . Note that since , then , proving that . Similarly, using Lemma A.4,

as . This concludes the proof. ∎

Proof of Lemma 4.1.

Using Bayes’ theorem and the unconditional independence of and , we have for and :

∎

Proof of Proposition 4.1.

Using the conditional law of total probability we obtain the following convolution formula

∎

Supplemental Materials: Inference and forecasting for continuous-time integer-valued trawl processes

Appendix S1 Introduction

This document is structured as follows.

-

•

Section S2 presents a decomposition of trawl processes.

-

•

Section S3 provides the details of a method of moment-based estimation of integer-valued trawl processes so far used in the literature.

-

•

Section S4 describes how the composite likelihood estimator and the corresponding asymptotic covariance matrices can be computed in practice.

-

•

Section S5 presents an expression for the pairwise likelihood for integer-valued processes (not restricted to count data) and discusses a simulation unbiased estimator for the composite likelihood.

-

•

Section S6 contains additional details for the simulation study: Subsection S6.1 describes the simulation setup for the simulation study reported in the main article. Subsections S6.2 and S6.4 present the finite sample results of the MCL estimator and of the model selection procedure, respectively. Section S6.5 repeats the simulation study using different parameter choices.

- •

- •

-

•

Section S10 contains details on how to calculate the gradients for the log-composite likelihood functions implied by most of the parametric IVT processes. These calculations are straightforward to make (although somewhat tedious) and can rather easily be made for other IVT specifications than those considered here. The gradients can be used in the numerical optimization of the composite likelihood functions and are also crucial for implementing the asymptotic theory presented in the main paper. In particular, to estimate the asymptotic variance matrix , it is necessary to evaluate the gradient at .

-

•

Section S11 contains some additional technical calculations.

- •

-

•

Lastly, Section S13 contains brief details on the software packages accompanying the main paper. In particular, we supply software for simulation, estimation (including inference), model selection, and forecasting of IVT processes.

Appendix S2 Trawl process decomposition

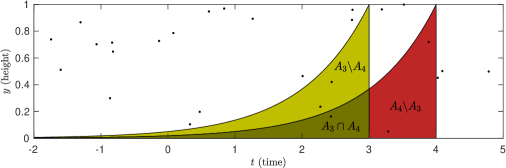

When deriving theoretical results for trawl processes, we typically decompose trawl sets at different time points into a partition of disjoint sets. We note that, given a trawl function it holds that

| (S2.1) |

It is also useful to note that for ,

| (S2.2) |

and

| (S2.3) |

Thus, given a trawl function , it is straightforward to calculate , and for all .

Also, we can write, for ,

where the three random variables are independent since the corresponding sets are disjoint. In Figure S1, we illustrate such a decomposition for .

Appendix S3 Method-of-moments-based estimation of IVT processes

For a parametric IVT model, let the parameter vector of the model be given by , where contains the parameters governing the trawl function and contains the parameters governing the marginal distribution of the IVT process, as specified by the underlying Lévy seed . For instance, in the case of the Poisson-Exponential IVT process considered above, cf. Figure 1, we would have and . This section discusses how and can be estimated in a two-step procedure using a method-of-moments procedure. It is this procedure that has been used so far in most applied work on IVT processes. Note that we develop the asymptotic theory for the full (one-step) GMM estimation of in Section S12 below.

Because the correlation structure of an IVT process is decoupled from its marginal distribution, the theoretical autocorrelation function of the process will not depend on , and we can thus estimate in the first step, using the empirical autocorrelations of the data. To be precise, let be the parametric autocorrelation function as implied by the trawl function , see Equation (2.5), and let be the estimate of the empirical autocorrelation of the data at lag . The GMM estimator of is

| (S3.1) |

where denotes the number of lags to include in the estimation and is the parameter space of the trawl parameters in .777In the case of the IVT process with an exponential trawl function , , we use a closed-form estimator of the parameter using only the autocorrelation function calculated at the first lag, that is , where is the equidistant time between observations.

For the estimation of the parameters governing the marginal distribution of the IVT process, recall that the th cumulant of is given by

where is the th cumulant of the Lévy seed . Using the estimates from the first step, we can estimate the Lebesgue measure of the trawl set as

| (S3.2) |

where denotes the estimate of the trawl function implied by the estimated trawl parameters . The parameters governing the marginal distribution, , can now be estimated as follows. Let be the number of elements in and denote by the estimate of the Lebesgue measure obtained from (S3.2). Estimates of the cumulants, , can be obtained straightforwardly by calculating the empirical cumulants of the data. Let be a set of distinct natural numbers (e.g., the numbers from to ). Now

defines equations in the unknowns . GMM estimates of the elements in , , can be obtained by solving these equations. Finally, set , which is the method-of-moments-based estimator of .

Appendix S4 Practical details on feasible inference using the MCL estimator

As shown in Theorem 3.3 of Section 3.1.2, the asymptotic variance of the maximum composite likelihood estimator, is given by the inverse Godambe information matrix,

As mentioned, the matrices and can be consistently estimated by

where

and is the number of autocorrelation terms to take into account in the HAC estimator. The Hessian, , is straightforwardly estimated by the above expression. Indeed, a numerical approximation of this matrix is often directly available as output from the software maximizing the composite likelihood function. We have found that while this estimator is quite precise, the HAC estimator can be rather imprecise. In practice, we therefore recommend estimating using simulation-based approach; the details are given in the following S4.1.

S4.1 Simulation-based approach to estimating the asymptotic covariance matrix

To obtain a simulation-based estimator of , let denote a positive integer (e.g. ) and suppose that is the maximum composite likelihood estimate of from (3.3) when applied to the original data. To estimate , do as follows:

-

1.

For , simulate observations of a trawl process with underlying parameters .

-

2.

For , use the simulated data to calculate . The gradient can either be calculated numerically or analytically.888The Supplementary Material contains analytical expressions for the gradients implied by the various parametric specifications considered in this paper. Note that the bootstrap data is used to calculate the gradient, but the parameter vector is the original estimator obtained from the initial (real) data set.

-

3.