Deep Learning for Two-Sided Matching

Abstract

We initiate the study of deep learning for the automated design of two-sided matching mechanisms. What is of most interest is to use machine learning to understand the possibility of new tradeoffs between strategy-proofness and stability. These properties cannot be achieved simultaneously, but the efficient frontier is not understood. We introduce novel differentiable surrogates for quantifying ordinal strategy-proofness and stability and use them to train differentiable matching mechanisms that map discrete preferences to valid randomized matchings. We demonstrate that the efficient frontier characterized by these learned mechanisms is substantially better than that achievable through a convex combination of baselines of deferred acceptance (stable and strategy-proof for only one side of the market), top trading cycles (strategy-proof for one side, but not stable), and randomized serial dictatorship (strategy-proof for both sides, but not stable). This gives a new target for economic theory and opens up new possibilities for machine learning pipelines in matching market design.

1 Introduction

Two-sided matching markets, classically used for settings such as high-school matching, medical residents matching, and law clerk matching, and more recently used in online platforms such as Uber, Lyft, Airbnb, and dating apps, play a significant role in today’s world. As a result, there is a significant interest in designing better mechanisms for two-sided matching.

The seminal work of Gale and Shapley (1962) introduces a simple mechanism for stable, one-to-one matching in two-sided markets—deferred-acceptance (DA)—which has been applied in many settings, including doctor-hospital matching (Roth and Peranson, 1999), school choice (Abdulkadiroğlu and Sönmez, 2003; Pathak and Sönmez, 2008; Abdulkadiroğlu et al., 2009), and cadet-matching (Sönmez and Switzer, 2013; Sönmez, 2013). The DA mechanism is stable, i.e., no pair of participants prefer each other to their match (or to being unmatched, if they are unmatched in the outcome). However, the DA mechanism is not strategy-proof (SP), and a participant can sometimes misreport their preferences to obtain a better outcome (although it is SP for participants on one side of the market). Although widely used, this failure of SP for the DA mechanism presents a challenge for two main reasons. First, it can lead to unfairness, where better-informed participants can gain an advantage in knowing which misreport strategies can be helpful. Second, strategic behavior can lead to lower quality, unintended outcomes, and outcomes that are unstable with respect to true preferences.

In general, it is well-known that there must necessarily be a tradeoff between stability and strategy-proofness: it is provably impossible for a mechanism to achieve both stability and strategy-proofness (Dubins and Freedman, 1981; Roth, 1982). A second example of a matching mechanism is random serial dictatorship (RSD) (Abdulkadiroglu and Sönmez, 1998), which is typically adopted for one-sided assignment problems rather than two-sided matching. When adapted to two-sided matching, RSD is SP but not stable. In fact, a participant may even prefer to remain unmatched than participate in the outcome of the matching. A third example of a matching mechanism is the top trading cycles (TTC) mechanism (Shapley and Scarf, 1974), also typically adopted for one-sided assignment problems rather than problems of two-sided matching. In application to two-sided matching, TTC is neither SP nor stable (although it is SP for participants on one side of the market).

There have been various research efforts to circumvent this impossibility result. Some relax the definition of strategyproofness (Mennle and Seuken, 2021) while others characterize the constraints under which stability and strategyproofness are achieved simultaneously (Kamada and Kojima, 2018; Hatfield et al., 2021; Hatfield and Milgrom, 2005). The tradeoff between these desiderata remains poorly understood beyond the existing point solutions of DA, RSD, and TTC. However, we argue that real-world scenarios demand a more nuanced approach that considers both properties. The case of the Boston school choice mechanism highlights the negative consequences of lacking strategy-proofness, resulting in unfair manipulations by specific parents (Abdulkadiroglu et al., 2006). At the same time, the importance of stability in matching markets is well understood (Roth, 1991).

Recognizing this, and inspired by the success of deep learning in the study of revenue-optimal auction design (Duetting et al., 2019; Curry et al., 2020; Shen et al., 2019; Rahme et al., 2020), we initiate the study of deep learning for the design of two-sided matching mechanisms We ask whether deep learning frameworks can enable a systematic study of this tradeoff. By answering this question affirmatively, we open up the possibility of using machine learning pipelines to open up new opportunities for economic theory—seeking theoretical characterizations of mechanisms that can strike a new balance between strategyproofness and stability.

We use a neural network to represent the rules of a matching mechanism, mapping preference reports to a distribution over feasible matchings, and show how we can use an unsupervised learning pipeline to characterize the efficient frontier for the design tradeoff between stability and SP. The main methodological challenge in applying neural networks to two-sided matching comes from handling the ordinal preference inputs (the corresponding inputs are cardinal in auction design) and identifying suitable, differentiable surrogates for approximate strategy-proofness and approximate stability.

We work with randomized matching mechanisms, for which the strongest SP concept is ordinal strategy-proofness. This aligns incentives with truthful reporting, whatever an agent’s utility function (i.e., for any cardinal preferences consistent with an agent’s ordinal preferences). Ordinal SP is equivalent to the property of first-order stochastic dominance (FOSD) (Erdil, 2014), which suitably defines the property that an agent has a better chance of getting their top, top-two, top-three, and so forth choices when they report truthfully. As a surrogate for SP, we quantify during training the degree to which FOSD is violated. For this, we adopt an adversarial learning approach, augmenting the training data with defeating misreports that reveal the violation of FOSD. We also define a suitable surrogate to quantify the degree to which stability is violated. This surrogate aligns with the notion of ex ante stability—the strongest stability concept for randomized matching.

We train neural network representations of matching mechanisms by adopting stochastic gradient descent (SGD) for loss functions that are defined on different convex combinations of the two surrogate quantities, and construct the efficient frontier for stability and strategy-proofness for different market settings. A further challenge with ordinal preference inputs as opposed to cardinal inputs arises because ordinal preferences are discrete. In the present work, we simply enumerate the possible misreports of an agent as a step when evaluating the derivative of error for a particular training example. In contrast, the use of deep-learning approaches for the design of revenue-optimal auctions works with a continuous space of agent valuations and gradient-ascent in this adversarial step of identifying useful misreports (Duetting et al., 2019). As discussed at the end of the paper, the challenge that this presents in scaling to large numbers of agents can be resolved by assuming a suitable structure on preference orderings in the domain, or on the language that is made available to agents in reporting their preferences to the mechanisms.

Our main experimental results demonstrate that this novel use of deep learning can strike a much better trade-off between stability and SP than that achieved by a convex combination of the DA, TTC, and RSD mechanisms. Taken as a whole, these results suggest that deep learning pipelines can be used to identify new opportunities for matching theory. For example, we identify mechanisms that are provably almost as stable as DA and yet considerably more strategy-proof. We also identify mechanisms that are provably almost as strategy-proof as RSD and yet considerably more stable. These discoveries raise opportunities for future work in economic theory, in regard to understanding the structure of these two-sided matching mechanisms as well as characterizing the preference distributions for which this is possible.

2 Related work.

Dubins and Freedman (1981) and Roth (1982) show the impossibility of achieving both stability and SP in two-sided matching. Alcalde and Barberà (1994) also show the impossibility of individually rational, Pareto efficient, and SP allocation rules, and this work has been extended to randomized matching (Alva and Manjunath, 2020). RSD is SP but may not be stable or even individually rational (IR) (Abdulkadiroglu and Sönmez, 1998). We will see that the top trading cycles (TTC) mechanism (Shapley and Scarf, 1974), when applied in a two-sided context, is only SP for one side, and is neither stable nor IR. The DA mechanism (Gale and Shapley, 1962) is stable but not SP; see also (Roth et al., 1993), who study the polytope of stable matchings. The stable improvement cycles mechanism (Erdil and Ergin, 2008) achieves as much efficiency as possible on top of stability but fails to be SP even for one side of the market. Finally, a series of results show that DA becomes SP for both sides of the market in large-market limit contexts (Immorlica and Mahdian, 2015; Kojima and Pathak, 2009; Lee, 2016).

Aziz and Klaus (2019) discuss different stability and no envy concepts. We focus on ex ante stability (Kesten and Ünver, 2015), also discussed by (Roth et al., 1993) as strong stability. Mennle and Seuken (2021) discuss different notions of approximate strategy-proofness in the context of matching and allocation problems. In this work, we focus on ordinal SP and its analog of FOSD (Erdil, 2014). This is a strong and widely used SP concept in the presence of ordinal preferences. There are a lot of other desiderata, such as efficiency, that are also incompatible with strategyproofness. Mennle and Seuken (2017) study this trade-off through hybrid mechanisms which are convex combinations of a mechanism with good incentive properties with another which is efficient. In the context of social choice, other work studies the trade-off between approximate SP and desiderata, such as plurality and veto voting (Mennle and Seuken, 2016).

Conitzer and Sandholm (2002, 2004) introduced the automated mechanism design (AMD) approach that framed problems as a linear program. However, this approach faces severe scalability issues as the formulation scales exponentially in the number of agents and items (Guo and Conitzer, 2010). Overcoming this limitation, more recent work seeks to use deep neural networks to address problems of economic design (Duetting et al., 2019; Feng et al., 2018; Golowich et al., 2018; Curry et al., 2020; Shen et al., 2019; Rahme et al., 2020; Duan et al., 2022; Ivanov et al., 2022), but not until now to matching problems. As discussed in the introduction, two-sided matching brings about new challenges, most notably in regard to working with discrete, ordinal preferences and adopting the right surrogate loss functions for approximate SP and approximate stability. Other work has made use of support vector machines to search for stable mechanisms, but without considering strategy-proofness (Narasimhan et al., 2016). A different line of research is also considering stable matching together with bandits problems, where agent preferences are unknown a priori (Das and Kamenica, 2005; Liu et al., 2020; Dai and Jordan, 2021; Liu et al., 2022; Basu et al., 2021; Sankararaman et al., 2021; Jagadeesan et al., 2021; Cen and Shah, 2022; Min et al., 2022).

There have also been other recent efforts that leverage deep learning for matching (in the context of online bipartite matching (Alomrani et al., 2022)) and other related combinatorial optimization problems (Bengio et al., 2021). Most of these papers adopt a reinforcement learning based approach to compute their solutions. Our approach, on the other hand, is not sequential but rather end-to-end differentiable, and our parameter weights are updated through a single backward pass. Additionally, the focus of our work is on matching markets and mechanism design, and is concerned with capturing core economic concepts within a machine learning framework and balancing the trade-offs between stability and strategy-proofness.

3 Preliminaries

Let denote a set of workers and denote a set of firms. A feasible matching, , is a set of (worker, firm) pairs, with each worker and firm participating in at most one match. Let denote the set of all matchings. If , then matches to , and we write and . If a worker or firm remains unmatched, we say it is matched to . We also write (resp. ). Each worker has a strict preference order, , over the set . Each firm has a strict preference order, , over the set . Worker (firm ) prefers remaining unmatched to being matched with a firm (worker) ranked below (the agents ranked below are said to be unacceptable). If worker prefers firm to , then we write , similarly for a firm’s preferences. Let denote the set of all preference profiles, with denoting a preference profile comprising of the preference order of the workers and then the firms.

A pair forms a blocking pair for matching if and prefer each other to their partners in (or in the case that one or both are unmatched). A matching is stable if and only if there are no blocking pairs. A matching is individually rational (IR) if and only if it is not blocked by any individual; i.e., no agent finds its match unacceptable and prefers .111Stability precludes empty matchings. For example, if a matching leaves a worker and a firm unmatched, where finds acceptable, and finds acceptable, then is a blocking pair to .

3.1 Randomized matchings.

We work with randomized matching mechanisms, , that map preference profiles, , to distributions on matchings, denoted (the probability simplex on matchings). Let denote the marginal probability, , with which worker is matched with firm , for each and . We require for all , and for all . For notational simplicity, we write for the marginal probability of matching worker (or ) and firm (or ).

Theorem 1 (Birkhoff von-Neumann).

Given any randomized matching , there exists a distribution on matchings, , with marginal probabilities equal to .

The following definition is standard (Budish et al., 2013), and generalizes stability to randomized matchings.

Definition 2 (Ex ante justified envy).

A randomized matching causes ex ante justified envy if:

(1) some worker prefers over some fractionally matched firm (including ) and firm prefers over some fractionally matched worker (including ) (“ has envy towards " and “ has envy towards "), or

(2) some worker finds a fractionally matched unacceptable, i.e. and , or some firm finds a fractionally matched unacceptable, i.e. and .

A randomized matching is ex ante stable if and only if it does not cause any ex ante justified envy. Ex ante stability reduces to the standard concept of stability for deterministic matching. Part (1) of the definition includes non-wastefulness: for any worker , we should have if there exists some firm for which and and for for any firm , we need if there exists some worker for which and . Part (2) of the definition captures IR: for any worker , we should have for all for which , and for any firm , we need for all for which .

To define strategy-proofness, say that is a -utility for worker when if and only if , for all . We similarly define a -utility for a firm . The following concept of ordinal SP is standard (Erdil, 2014), and generalizes SP to randomized matchings.

Definition 3 (Ordinal strategy-proofness).

A randomized matching mechanism satisfies ordinal SP if and only if, for all agents , for any preference profile , and any -utility for agent , and for all reports , we have

| (1) |

By this definition, no worker or firm can improve their expected utility (for any utility function consistent with their preference order) by misreporting their preference order. For a deterministic mechanism, ordinal SP reduces to standard SP. Erdil (2014) shows that first-order stochastic dominance is equivalent to ordinal SP.

Definition 4 (First Order Stochastic Dominance).

A randomized matching mechanism satisfies first order stochastic dominance (FOSD) if and only if, for worker , and each such that , and all reports of others , we have (and similarly for the roles of workers and firms transposed),

| (2) |

FOSD states that, whether looking at its most preferred firm, its two most preferred firms, or so forth, worker achieves a higher probability of matching on that set of firms for its true report than for any misreport. We make use of a quantification of the violation of this condition to provide a surrogate for the failure of SP during learning.

Theorem 5 ((Erdil, 2014)).

A two-sided matching mechanism is ordinal SP if and only if it satisfies FOSD.

3.2 Deferred Acceptance, RSD, and TTC.

We consider three benchmark mechanisms: the stable but not SP deferred-acceptance (DA) mechanism, the SP but not stable randomized serial dictatorship (RSD) mechanism, and the Top Trading Cycles (TTC) mechanism, which is neither SP nor stable. The DA and TTC mechanisms are ordinal SP for the proposing side of the market but not for agents on both sides of the market.

Definition 6 (Deferred-acceptance (DA)).

In worker-proposing deferred-acceptance (firm-proposing is defined analogously), each worker maintains a list of acceptable firms () for which it has not had a proposal rejected (“remaining firms"). Repeat until all proposals are accepted:

-

•

: proposes to its best acceptable, remaining firm.

-

•

: tentatively accepts its best proposal (if any), and rejects the rest.

-

•

: If is rejected by firm , it updates its list of acceptable firms to remove .

Theorem 7 (see (Roth and Sotomayor, 1990)).

DA is stable but not Ordinal SP.

Definition 8 (Randomized serial dictatorship (RSD)).

In the two-sided version of RSD, we first sample a priority order, , on the set , uniformly at random, such that is a permutation on in decreasing order of priority. For the one-sided version, we sample a priority order on either or .

Proceed as follows:

-

•

Initialize matching to the empty matching.

-

•

In round :

-

–

If is not yet matched in , then add to the match between and its most preferred unmatched agent, or if all remaining agents are unacceptable to .

-

–

Theorem 9.

RSD satisfies FOSD—and thus is ordinal SP by Theorem 5—but is not stable.

Proof.

We defer the proof to appendix A ∎

Definition 10 (Top Trading Cycles (TTC)).

In worker-proposing TTC (firm-proposing is defined analogously), each agent (worker or firm) maintains a list of acceptable firms. Repeat until all agents are matched:

-

•

Form a directed graph with each unmatched agent pointing to their most preferred option. The agents can point at themselves if there are no acceptable options available. Every worker that is a part of a cycle is matched to a firm it points to ( or itself, if the worker is pointing at itself). The unmatched agents remove from their lists every matched agent from this round.

Theorem 11.

TTC is neither strategy-proof nor stable for both sides.

Remark 12.

TTC, like RSD, is usually used in one-sided assignment problems, where it is SP, and where the notion of stability which is an important consideration in two-sided matching, is not a concern.

4 Two-Sided Matching as a Learning Problem

In this section, we develop the use of deep learning for the design of two-sided matching mechanisms.

4.1 Neural Network Architecture

We use a neural network to represent a matching mechanism. Let denote the mechanism, for parameters . The input is a preference profile, and the output defines a distribution on matchings. We use a feed-forward neural network with fully connected hidden layers, units in each layer, leaky ReLU activations, and a fully connected output layer.222Leaky ReLU is a variation of ReLU that addresses the issue of dead neurons by allowing a small positive gradient for negative input values, thereby preventing gradients from getting stuck at . See Figure 1.

To represent an agent’s preference order in the input, we adopt a utility for each agent on the other side of the market that has a constant offset in utility across successive agents in the preference order. This is purely a representation choice and does not imply that we use this particular utility to study SP (on the contrary, we work with a FOSD-based quantification of the degree of approximation to ordinal SP). In particular, let and represent the preference order of a worker and firm, respectively. We define and , and to further illustrate this representation:

-

•

For a preference order with , we represent this at the input as .

-

•

For a preference order with , we represent this as .

-

•

For a preference order with , we represent this as .

Formally, we have:

| (3) | ||||

| (4) |

where is the indicator function for event .

Taken together, the input is vector of numbers.

The output of the network is a vector , with and for every every and . This defines the marginal probabilities in a randomized matching for this input profile. The network first outputs two sets of scores and . We apply the softplus function (denoted by ) element-wise to these scores, where . To ensure IR, we first construct a Boolean mask variable , which is zero only when the match is unacceptable to one or both the worker and firm, i.e., when or . We set for and for . We multiply the scores and element-wise with the corresponding Boolean mask variable to compute and .

For each , we have , for all . For each , we have , for all . We normalize along the rows and along the columns to obtain normalized scores, and respectively. The match probability , for worker and firm , is computed as the minimum of the normalized scores: . We have whenever , ensuring that every matching in the support of the distribution will be IR. Based on our construction, the allocation matrix is weakly doubly stochastic, with rows and columns summing to at most 1. Budish et al. (2013) show that any weakly doubly stochastic matrix can be decomposed to a convex combination of 0-1, weakly doubly stochastic matrices.

4.2 Formulation as a Learning Problem

We formulate a loss function that is defined on training data of preference profiles, . Each preference profile sampled i.i.d. from a distribution on profiles. We allow for correlated preferences; i.e., workers may tend to agree that one of the firms is preferable to one of the other firms, and similarly for firms. The loss function captures a tradeoff between stability and ordinal SP. Recall that denotes the randomized matching. We write and to denote the probability of worker and firm being unmatched, respectively.

Stability Violation. For worker and firm , we define the stability violation at profile as

| (5) |

This captures the first kind of ex ante justified envy in Definition 2. We can omit the second kind of ex ante justified envy because the learned mechanisms satisfy IR through the use of the Boolean mask matrix (and thus, there are no violations of the second kind).

The average stability violation (or just stability violation) of mechanism on profile is We define the expected stability violation, . We also write to denote the average stability violation on the training data.

Theorem 13.

A randomized matching mechanism is ex ante stable up to zero-measure events if and only if .

Proof.

We defer the proof to appendix C ∎

Ordinal SP violation. We turn now to quantifying the degree of approximation to ordinal SP. Let . For a valuation profile, , and a mechanism , let . The regret to worker (firm ) is defined as:

| (6) |

The average regret on profile is:

| (7) |

The expected regret is . We can also write to denote the average regret on training data.

Theorem 14.

The regret to a worker (firm) for a given preference profile is the maximum amount by which the worker (firm) can increase their expected normalized utility through a misreport, fixing the reports of others.

Proof.

Consider some worker . Without loss of generality, let . Any normalized -utility function, , consistent with ordering given by satisfies . Let be the set of all such consistent utility functions.

Consider some misreport . We have . The increase in utility for worker when the utility function is is given by . The maximum amount by which worker can increase their expected normalized utility through misreport is given by the objective: .

Since always guarantees IR, we have:

| (8) |

. Thus, we can simplify our search space by only considering where .

Define . This objective can thus be rewritten as:

| max | (9) | |||

| such that | (10) |

Changing the order of summation, we have the following optimization problem:

| (11) | ||||

| (12) |

This objective is of the form and it’s solution is given by the . Thus, the solution to the above maximization problem is given by . But this is the same as . Computing the maximum possible increase over all such misreports gives us . This quantity is exactly . The proof follows similarly for any firm . ∎

Theorem 15.

A randomized mechanism, , is ordinal SP up to zero-measure events if and only if .

4.3 Training Procedure

For a mechanism parameterized as , the training problem that we formulate is,

| (13) |

where controls the tradeoff between approximate stability and approximate SP. We use SGD to solve (13). The gradient of the degree of violation of stability with respect to network parameters is straightforward to calculate. The gradient of regret is complicated by the nested maximization in the definition of regret. In order to compute the gradient, we first solve the inner maximization by checking possible misreports. Let denote the defeating preference report for agent (a worker or firm) at preference profile that maximizes . Given this, we obtain the derivative of regret for agent with respect to the network parameters, fixing the misreport to the defeating valuation and adopting truthful reports for the others.

For the case of TTC and RSD, we also need to quantify the IR violation (this is necessarily zero for the other mechanisms). We define the IR violation at profile as:

| (14) | ||||

For the case of RSD, we also include the average IR violation on test data when reporting the stability violation.

5 Experimental Results

We report the results on a test set of 204,800 preference profiles, and use the Adam optimizer to train our models for 50,000 mini-batch iterations, with mini-batches of 1024 profiles. We use the PyTorch deep learning library, and all experiments are run on a cluster of NVIDIA GPU cores.

We study the following market settings:

-

•

For uncorrelated preferences, for each worker or firm, we sample uniformly at random from all preference orders, and then, with probability 0.2 (truncation probability), we choose at random a position at which to truncate this agent’s preference order.

-

•

For correlated preferences, we sample a preference profile as in the uncorrelated case. We also sample a common preference order on firms and a common preference order on workers. For each agent, with probability, , we replace its preference order with the common preference order for its side of the market.

Specifically, we consider matching problems with workers and firms with uncorrelated preference and varying probability of correlation .

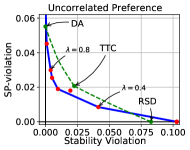

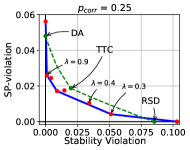

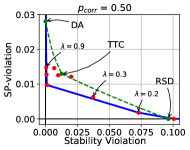

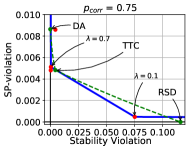

We compare the performance of our mechanisms, varying parameter between and , with the best of worker- and firm- proposing DA and TTC (as determined by average SP violation over the test data) and RSD333We only plot the performance of one-sided RSD as it achieves lower stability violation the two-sided version. We also compare against convex combinations of DA, TTC, and RSD. We plot the resulting frontier on stability violation () and SP violation () in Figure 2. As explained above, because TTC and RSD mechanisms do not guarantee IR, we include the IR violations in the reported stability violation (none of the other mechanisms fail IR).

At , we learn a mechanism that has very low regret () but poor stability. This performance is similar to that of RSD. For large values of , we learn a mechanism that approximates DA. For intermediate values, we find solutions that dominate the convex combination of DA, TTC, and RSD and find novel and interesting tradeoffs between SP and stability. Notably, for lower levels of correlations we see substantially better SP than DA along with very little loss in stability. Given the importance of stability in practice, this is a very intriguing discovery. For higher levels of correlations, we see substantially better stability than RSD along with very little loss in SP. It is also interesting to see that TTC itself has intermediate properties, between those of DA and RSD. Comparing the scale of the y-axes, we can also see that increasing correlation tends to reduce the opportunity for strategic behavior across both the DA and the learned mechanisms.

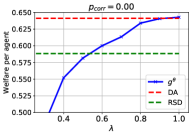

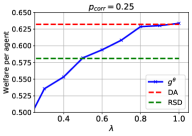

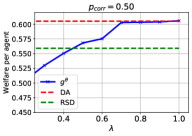

Figure 3 shows the expected welfare for the learned mechanisms, measured here for the equi-spaced utility function (the function used in the input representation). We define the welfare of a mechanism (for the equi-spaced utility function) on a profile as:

| (15) |

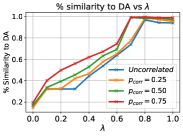

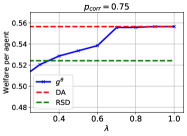

We compare against the maximum of the expected welfare achieved by the worker- and firm- proposing DA and TTC mechanisms, as well as that from RSD. As we increase , and the learned mechanisms come closer to DA, the welfare of the learned mechanisms improves. It is notable that for choices of in the range 0.8 and higher, i.e., the choices of that provide interesting opportunities for improving SP relative to DA, we also see good welfare. We also see that TTC, and especially RSD have comparably lower welfare. It bears emphasis that when a mechanism is not fully SP, as is the case for all mechanisms except RSD, this is an idealized view of welfare since it assumes truthful reports. In fact, we should expect welfare to be reduced through strategic misreports and the substantially improved SP properties of the learned mechanisms relative to DA (Figure 2) would be expected to further work in favor of improving the welfare in the learned mechanisms relative to DA.444In fact, the same is true for the stability of a non-SP mechanism such as DA, but it has become standard to assume truthful reports to DA in considering the stability properties of DA. Lastly, we observe that for small values of the learned mechanisms have relatively low welfare compared to RSD. This is interesting and suggests that achieving IR together with SP (recall that RSD is not IR!) is very challenging in two-sided markets. In interpreting the rules of the learned mechanisms, and considering the importance of DA, we can also compare their functional similarity with DA. For this, let -DA and -DA denote the worker- and firm-proposing DA, respectively. For a given preference profile, we compute the similarity of the learned rule with DA as

| (16) |

This calculates the agreement between the two mechanisms, normalized by the size of the DA matching, and taking the best of -DA or -DA. Let denote the average similarity score on test data. As we increase , i.e., penalize stability violations more, we see in Figure 3 that the learned matchings get increasingly close to the DA matchings, as we might expect. We also quantify the degree of randomness of the learned mechanisms, by computing the normalized entropy per agent, taking the expectation over all preference profiles. For a given profile , we compute normalized entropy per agent as (this is 0 for a deterministic mechanism):

| (17) | ||||

Figure 3 shows how the entropy changes with . As we increase and the mechanisms come closer to DA, the allocations of the learned mechanisms also becomes less stochastic.

6 Discussion

The methodology and results in this paper give a first but crucial step towards using machine learning to understanding the structure of mechanisms that achieve nearly the same stability as DA while surpassing DA in terms of strategy-proofness. This is an interesting observation, given the practical and theoretical importance of the DA mechanism. Our experimental results also suggest that achieving IR together with SP (recall that RSD is not IR) is challenging in two-sided markets, and this is reflected in the lower welfare achieved by our learning mechanisms in the part of the frontier that emphasizes SP. The experimental results also show that for larger weights assigned to the importance of stability, the learned mechanisms recover the DA mechanism, whereas when more emphasis is given to the importance of strategy-proofness, the learned mechanisms are more randomized. There are other interesting questions waiting to be addressed. For instance, can we use this kind of framework to understand other tradeoffs, such as tradeoffs between strategy-proofness and efficiency?

As discussed in the introduction, a challenge in scaling to larger problems is the need to find defeating misreports, as exhaustively enumerating all misreports for an agent becomes intractable as the number of agents on the other side of the market increases (and thus the preference domain increases). A simple remedy is to restrict the language available to agents in making preference reports; e.g., it is commonplace to only allow for “top- preferences" to be reported. Another remedy is to work in domains where there exists some structure on the preference domain, so that not all possible preference orders exist; e.g., single-peaked preferences are an especially stark example (Black, 1948). It will also be interesting to study complementary approaches that relax the discrete set of preference orderings to a continuous convex hull such as the Birkhoff polytope. Confining these preference orderings to the Birkhoff polytope can be accomplished using differentiable operations, such as the sinkhorn operator (Adams and Zemel, 2011). Such continuous relaxation allows misreports to be identified through gradient ascent rather than sampling (and would be similar to working with continuous valuations when learning revenue-optimal auctions (Duetting et al., 2019)). Despite this limitation, our current approach scales much further than other, existing methods for automated design, which are not well suited for this problem. For instance, methods that use linear programs or integer programs do not scale well because of the number of variables555 output variables required to make explicit the input and output structure of the functional that must be optimized over.

A second challenge is that we have not been able to find a suitable, publicly available dataset to test our approach. As a fallback, we have endeavored to capture some real-world structures by varying the correlation between agent preferences and the truncation probabilities of preferences. Using such stylized, probabilistic models and simulations for validating approaches is a well-established and prevalent practice, consistently utilized when investigating two-sided matching markets (Chen and Sönmez, 2006; Echenique and Yariv, 2013; Das and Kamenica, 2005; Liu et al., 2020; Dai and Jordan, 2021). For instance, Chen and Sönmez (Chen and Sönmez, 2006) design an environment for school choice where they consider six different schools with six seats each and where the students’ preferences are simulated to depend on proximity, quality, and a random factor. Echenique an Yariv (Echenique and Yariv, 2013) use a simulation study with eight participants on each side of the market, with the payoff matrix designed such that there are one, two, or three stable matches. Further, recent papers on bandit models for stable matching model agent preferences through synthetic datasets (Das and Kamenica, 2005; Liu et al., 2020; Dai and Jordan, 2021).

In closing, we see exciting work ahead in advancing the design of matching mechanisms that strike the right balance between stability, strategyproofness, and other considerations that are critical to real-world applications. As an example, it will be interesting to extend the learning framework to encompass desiderata such as capacity limitations or fairness considerations. Also relevant is to explore additional kinds of neural network architectures, such as attention mechanisms (Vaswani et al., 2017) or architectures that incorporate permutation equivariance (Rahme et al., 2020; Duan et al., 2022), with the advantage that they can significantly reduce the search space.

Acknowledgements

The source code for all experiments along with the instructions to run it is available from Github at https://github.com/saisrivatsan/deep-matching/. This work is supported in part through an AWS Machine Learning Research Award.

References

- Abdulkadiroglu and Sönmez [1998] A. Abdulkadiroglu and T. Sönmez. Random serial dictatorship and the core from random endowments in house allocation problems. Econometrica, 66(3):689–702, 1998.

- Abdulkadiroglu et al. [2006] A. Abdulkadiroglu, P. Pathak, A. E. Roth, and T. Sonmez. Changing the Boston School Choice Mechanism. NBER Working Papers 11965, National Bureau of Economic Research, Inc, Jan. 2006. URL https://ideas.repec.org/p/nbr/nberwo/11965.html.

- Abdulkadiroğlu and Sönmez [2003] A. Abdulkadiroğlu and T. Sönmez. School choice: A mechanism design approach. American Economic Review, 93:729–747, 2003.

- Abdulkadiroğlu et al. [2009] A. Abdulkadiroğlu, P. A. Pathak, and A. E. Roth. Strategyproofness versus efficiency in matching with indifferences: Redesigning the NYC high school match. American Economic Review, 99:1954–1978, 2009.

- Adams and Zemel [2011] R. P. Adams and R. S. Zemel. Ranking via sinkhorn propagation. arXiv preprint arXiv:1106.1925, 2011.

- Alcalde and Barberà [1994] J. Alcalde and S. Barberà. Top dominance and the possibility of strategy-proof stable solutions to matching problems. Economic Theory, 4(3):417–435, 1994.

- Alomrani et al. [2022] M. A. Alomrani, R. Moravej, and E. B. Khalil. Deep policies for online bipartite matching: A reinforcement learning approach. Transactions on Machine Learning Research, 2022. ISSN 2835-8856. URL https://openreview.net/forum?id=mbwm7NdkpO.

- Alva and Manjunath [2020] S. Alva and V. Manjunath. The impossibility of strategy-proof, Pareto efficient, and individually rational rules for fractional matching. Games and Economic Behavior, 119:15–29, 2020.

- Aziz and Klaus [2019] H. Aziz and B. Klaus. Random matching under priorities: stability and no envy concepts. Social Choice and Welfare, 53(2):213–259, 2019. ISSN 01761714, 1432217X. URL http://www.jstor.org/stable/45212389.

- Basu et al. [2021] S. Basu, K. A. Sankararaman, and A. Sankararaman. Beyond regret for decentralized bandits in matching markets. In M. Meila and T. Zhang, editors, Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pages 705–715. PMLR, 18–24 Jul 2021. URL https://proceedings.mlr.press/v139/basu21a.html.

- Bengio et al. [2021] Y. Bengio, A. Lodi, and A. Prouvost. Machine learning for combinatorial optimization: A methodological tour d’horizon. European Journal of Operational Research, 290(2):405–421, 2021. ISSN 0377-2217. doi: https://doi.org/10.1016/j.ejor.2020.07.063. URL https://www.sciencedirect.com/science/article/pii/S0377221720306895.

- Black [1948] D. Black. On the Rationale of Group Decision-making. Journal of Political Economy, 56(1):23–34, 1948. ISSN 0022-3808. doi: 10.2307/1825026. URL http://www.jstor.org/stable/1825026.

- Budish et al. [2013] E. Budish, Y.-K. Che, F. Kojima, and P. Milgrom. Designing random allocation mechanisms: Theory and applications. American Economic Review, 103(2):585–623, April 2013. doi: 10.1257/aer.103.2.585. URL https://www.aeaweb.org/articles?id=10.1257/aer.103.2.585.

- Cen and Shah [2022] S. H. Cen and D. Shah. Regret, stability and fairness in matching markets with bandit learners. In G. Camps-Valls, F. J. R. Ruiz, and I. Valera, editors, Proceedings of The 25th International Conference on Artificial Intelligence and Statistics, volume 151 of Proceedings of Machine Learning Research, pages 8938–8968. PMLR, 28–30 Mar 2022. URL https://proceedings.mlr.press/v151/cen22a.html.

- Chen and Sönmez [2006] Y. Chen and T. Sönmez. School choice: an experimental study. Journal of Economic Theory, 127(1):202–231, 2006. ISSN 0022-0531. doi: https://doi.org/10.1016/j.jet.2004.10.006. URL https://www.sciencedirect.com/science/article/pii/S0022053104002418.

- Conitzer and Sandholm [2002] V. Conitzer and T. Sandholm. Complexity of mechanism design. In Proceedings of the 18th Conference on Uncertainty in Artificial Intelligence, pages 103–110, 2002.

- Conitzer and Sandholm [2004] V. Conitzer and T. Sandholm. Self-interested automated mechanism design and implications for optimal combinatorial auctions. In Proceedings of the 5th ACM Conference on Electronic Commerce, pages 132–141, 2004.

- Curry et al. [2020] M. J. Curry, P. Chiang, T. Goldstein, and J. P. Dickerson. Certifying strategyproof auction networks. CoRR, abs/2006.08742, 2020. URL https://arxiv.org/abs/2006.08742.

- Dai and Jordan [2021] X. Dai and M. Jordan. Learning in multi-stage decentralized matching markets. Advances in Neural Information Processing Systems, 34:12798–12809, 2021.

- Das and Kamenica [2005] S. Das and E. Kamenica. Two-sided bandits and the dating market. In IJCAI, volume 5, page 19. Citeseer, 2005.

- Duan et al. [2022] Z. Duan, J. Tang, Y. Yin, Z. Feng, X. Yan, M. Zaheer, and X. Deng. A context-integrated transformer-based neural network for auction design. In K. Chaudhuri, S. Jegelka, L. Song, C. Szepesvari, G. Niu, and S. Sabato, editors, Proceedings of the 39th International Conference on Machine Learning, volume 162 of Proceedings of Machine Learning Research, pages 5609–5626. PMLR, 17–23 Jul 2022. URL https://proceedings.mlr.press/v162/duan22a.html.

- Dubins and Freedman [1981] L. E. Dubins and D. A. Freedman. Machiavelli and the Gale-Shapley algorithm. American Mathematical Monthly, 88:485–494, 1981.

- Duetting et al. [2019] P. Duetting, Z. Feng, H. Narasimhan, D. C. Parkes, and S. S. Ravindranath. Optimal auctions through deep learning. In Proceedings of the 36th International Conference on Machine Learning, ICML, pages 1706–1715, 2019.

- Echenique and Yariv [2013] F. Echenique and L. Yariv. An Experimental Study of Decentralized Matching. Working Papers 2013-3, Princeton University. Economics Department., Nov. 2013. URL https://ideas.repec.org/p/pri/econom/2013-3.html.

- Erdil [2014] A. Erdil. Strategy-proof stochastic assignment. Journal of Economic Theory, 151:146 – 162, 2014. ISSN 0022-0531.

- Erdil and Ergin [2008] A. Erdil and H. Ergin. What’s the matter with tie-breaking? Improving efficiency in school choice. American Economic Review, 98(3):669–89, 2008.

- Feng et al. [2018] Z. Feng, H. Narasimhan, and D. C. Parkes. Deep learning for revenue-optimal auctions with budgets. In Proceedings of the 17th Conference on Autonomous Agents and Multi-Agent Systems, pages 354–362, 2018.

- Gale and Shapley [1962] D. Gale and L. S. Shapley. College admissions and the stability of marriage. The American Mathematical Monthly, 69(1):9–15, 1962.

- Golowich et al. [2018] N. Golowich, H. Narasimhan, and D. C. Parkes. Deep learning for multi-facility location mechanism design. In Proceedings of the 27th International Joint Conference on Artificial Intelligence, pages 261–267, 2018.

- Guo and Conitzer [2010] M. Guo and V. Conitzer. Computationally feasible automated mechanism design: General approach and case studies. In Proceedings of the 24th AAAI Conference on Artificial Intelligence, 2010.

- Hatfield and Milgrom [2005] J. W. Hatfield and P. R. Milgrom. Matching with contracts. American Economic Review, 95(4):913–935, September 2005. doi: 10.1257/0002828054825466. URL https://www.aeaweb.org/articles?id=10.1257/0002828054825466.

- Hatfield et al. [2021] J. W. Hatfield, S. D. Kominers, and A. Westkamp. Stability, Strategy-Proofness, and Cumulative Offer Mechanisms [Stability and Incentives for College Admissions with Budget Constraints]. Review of Economic Studies, 88(3):1457–1502, 2021. URL https://ideas.repec.org/a/oup/restud/v88y2021i3p1457-1502..html.

- Immorlica and Mahdian [2015] N. Immorlica and M. Mahdian. Incentives in large random two-sided markets. ACM Transactions on Economics and Computation, 3:#14, 2015.

- Ivanov et al. [2022] D. Ivanov, I. Safiulin, I. Filippov, and K. Balabaeva. Optimal-er auctions through attention. In A. H. Oh, A. Agarwal, D. Belgrave, and K. Cho, editors, Advances in Neural Information Processing Systems, 2022. URL https://openreview.net/forum?id=Xa1T165JEhB.

- Jagadeesan et al. [2021] M. Jagadeesan, A. Wei, Y. Wang, M. Jordan, and J. Steinhardt. Learning equilibria in matching markets from bandit feedback. In A. Beygelzimer, Y. Dauphin, P. Liang, and J. W. Vaughan, editors, Advances in Neural Information Processing Systems, 2021. URL https://openreview.net/forum?id=TgDTMyA9Nk.

- Kamada and Kojima [2018] Y. Kamada and F. Kojima. Stability and strategy-proofness for matching with constraints: A necessary and sufficient condition. Theoretical Economics, 13(2):761–793, 2018.

- Kesten and Ünver [2015] O. Kesten and M. U. Ünver. A theory of school-choice lotteries. Theoretical Economics, 10(2):543–595, 2015.

- Kojima and Pathak [2009] F. Kojima and P. A. Pathak. Incentives and stability in large two-sided matching markets. American Economic Review, 99:608–627, 2009.

- Lee [2016] S. Lee. Incentive compatibility of large centralized matching markets. The Review of Economic Studies, 84(1):444–463, 2016.

- Liu et al. [2020] L. T. Liu, H. Mania, and M. Jordan. Competing bandits in matching markets. In S. Chiappa and R. Calandra, editors, Proceedings of the Twenty Third International Conference on Artificial Intelligence and Statistics, volume 108 of Proceedings of Machine Learning Research, pages 1618–1628. PMLR, 26–28 Aug 2020. URL https://proceedings.mlr.press/v108/liu20c.html.

- Liu et al. [2022] L. T. Liu, F. Ruan, H. Mania, and M. I. Jordan. Bandit learning in decentralized matching markets. J. Mach. Learn. Res., 22(1), jul 2022. ISSN 1532-4435.

- Mennle and Seuken [2016] T. Mennle and S. Seuken. The pareto frontier for random mechanisms. In Proceedings of the 2016 ACM Conference on Economics and Computation, EC ’16, page 769, New York, NY, USA, 2016. Association for Computing Machinery.

- Mennle and Seuken [2017] T. Mennle and S. Seuken. Hybrid mechanisms: Trading off strategyproofness and efficiency of random assignment mechanisms, 2017.

- Mennle and Seuken [2021] T. Mennle and S. Seuken. Partial strategyproofness: Relaxing strategyproofness for the random assignment problem. Journal of Economic Theory, 191:105–144, 2021.

- Min et al. [2022] Y. Min, T. Wang, R. Xu, Z. Wang, M. Jordan, and Z. Yang. Learn to match with no regret: Reinforcement learning in markov matching markets. In A. H. Oh, A. Agarwal, D. Belgrave, and K. Cho, editors, Advances in Neural Information Processing Systems, 2022. URL https://openreview.net/forum?id=R3JMyR4MvoU.

- Narasimhan et al. [2016] H. Narasimhan, S. Agarwal, and D. C. Parkes. Automated mechanism design without money via machine learning. In Proceedings of the 25th International Joint Conference on Artificial Intelligence, pages 433–439, 2016.

- Pathak and Sönmez [2008] P. A. Pathak and T. Sönmez. Leveling the playing field: Sincere and sophisticated players in the Boston mechanism. American Economic Review, 98(4):1636–1652, 2008.

- Rahme et al. [2020] J. Rahme, S. Jelassi, J. Bruna, and S. M. Weinberg. A permutation-equivariant neural network architecture for auction design. CoRR, abs/2003.01497, 2020. URL https://arxiv.org/abs/2003.01497.

- Roth [1982] A. E. Roth. The economics of matching: Stability and incentives. Mathematics of Operations Research, 7(4):617–628, 1982.

- Roth [1991] A. E. Roth. A natural experiment in the organization of entry-level labor markets: Regional markets for new physicians and surgeons in the united kingdom. The American Economic Review, 81(3):415–440, 1991. ISSN 00028282. URL http://www.jstor.org/stable/2006511.

- Roth and Peranson [1999] A. E. Roth and E. Peranson. The redesign of the matching market for american physicians: Some engineering aspects of economic design. American Economic Review, 89(4):748–780, September 1999.

- Roth and Sotomayor [1990] A. E. Roth and M. Sotomayor. Two-Sided Matching: A Study in Game-Theoretic Modeling and Analysis, volume 18 of Econometric Society Monographs. Cambridge University Press, 1990.

- Roth et al. [1993] A. E. Roth, U. G. Rothblum, and J. H. V. Vate. Stable matchings, optimal assignments, and linear programming. Mathematics of Operations Research, 18(4):803–828, 1993.

- Sankararaman et al. [2021] A. Sankararaman, S. Basu, and K. Abinav Sankararaman. Dominate or delete: Decentralized competing bandits in serial dictatorship. In A. Banerjee and K. Fukumizu, editors, Proceedings of The 24th International Conference on Artificial Intelligence and Statistics, volume 130 of Proceedings of Machine Learning Research, pages 1252–1260. PMLR, 13–15 Apr 2021. URL https://proceedings.mlr.press/v130/sankararaman21a.html.

- Shapley and Scarf [1974] L. Shapley and H. Scarf. On cores and indivisibility. Journal of Mathematical Economics, 1(1):23–37, 1974. ISSN 0304-4068. doi: https://doi.org/10.1016/0304-4068(74)90033-0. URL https://www.sciencedirect.com/science/article/pii/0304406874900330.

- Shen et al. [2019] W. Shen, P. Tang, and S. Zuo. Automated mechanism design via neural networks. In Proceedings of the 18th International Conference on Autonomous Agents and Multiagent Systems, 2019.

- Sönmez [2013] T. Sönmez. Bidding for army career specialties: Improving the ROTC branching mechanism. Journal of Political Economy, 121:186–219, 2013.

- Sönmez and Switzer [2013] T. Sönmez and T. B. Switzer. Matching with (branch-of-choice) contracts at United States Military Academy. Econometrica, 81:451–488, 2013.

- Vaswani et al. [2017] A. Vaswani, N. Shazeer, N. Parmar, J. Uszkoreit, L. Jones, A. N. Gomez, Ł. Kaiser, and I. Polosukhin. Attention is all you need. Advances in neural information processing systems, 30, 2017.

Appendix A RSD is ordinal SP but not Stable

We first show RSD satisfies FOSD and is thus ordinal SP. Consider agent in some position in the order. The agent’s report has no effect on the choices of preceding agents, whether workers or firms (including whether agent is selected by an agent on the other side). Reporting its true preference ensures, in the event that it remains unmatched by position , that it is matched with its most preferred agent of those remaining. For the one-sided version, the same argument holds for agents that are in the priority order. If an agent isn’t on the side that’s on the priority order, then that agent’s report has no effect at all.

In the following example, we show RSD mechanism is not stable.

Example 16.

Consider workers and firms with the following preference orders:

The matching found by worker-proposing DA is . This is a stable matching. If truncates and misreports its preference as , the matching found is . Firm is matched with a more preferred worker, and hence the mechanism is not strategy-proof. Now consider the matching under RSD. The marginal matching probabilities is given by:

and are the most preferred options for and respectively and they would prefer to be matched with each other always rather than being fractionally matched with each other. Here is a blocking pair and thus RSD is not stable.

Appendix B TTC is neither Stable nor Strategyproof

Example 17.

Consider workers and firms with the following preference orders:

If all agents report truthfully, is matched with . This violates IR as and thus the matching is not ex-ante stable. If misreports its preference as , then is matched with . Since is matched with a more preferred worker with , TTC is not strategyproof.

Appendix C Proof of Theorem 13

Proof.

Since then if and only if except on zero measure events. Moreover, implies for all , all . This is equivalent to no justified envy. For firm , this means , if and if . Then there is no justified envy for a firm . Analogously, there is no justified envy for worker . If is ex ante stable, it trivially implies by definition. ∎

Appendix D Proof of Theorem 15

Proof.

Since then if and only if except on zero measure events. Moreover, implies for any worker and for any firm . Thus, the maximum utility increase on misreporting is at most zero, and hence is ordinal SP. If is Ordinal-SP, it is also satisfies FOSD 5 and it is straightforward to show that . ∎

Appendix E Training Details and Hyperparameters

We use a neural network with hidden layers with hidden units each for all our settings. We use the leaky ReLU activation function at each of these layers. To train our neural network, we use the Adam Optimizer with decoupled weight delay regularization (implemented as AdamW optimizer in PyTorch) We set the learning rate to for uncorrelated preferences setting and when . The remaining hyperparameters of the optimizer are set to their default values. We sample a fresh minibatch of 1024 profiles and train our neural networks for a total of 50000 minibatch iterations. We reduce the learning rate by half once at iteration and once at iteration. We report our results on 204800 preference profiles. For our training, we use a single Tesla V-100 GPU. For each setting, the neural network takes 4.6 hours to train.