[figure]capposition=top \floatsetup[table]capposition=top

Difference-in-Differences with a Continuous Treatment††thanks: We thank the participants of many seminars, workshops, and conferences for their comments. We are grateful to Xiaohong Chen for numerous discussions about implementing the data-driven sieve estimator used in this paper, Amy Finkelstein for sharing her data with us, Carol Caetano, Greg Caetano, Stefan Hoderlein, Jo Mullins, Jon Roth, and Abbie Wozniak for their comments, and Honey Batra for valuable research assistance. The views expressed here are those of the authors and do not necessarily represent those of the Federal Reserve Bank of Minneapolis or the Federal Reserve System.

This paper analyzes difference-in-differences setups with a continuous treatment. We show that treatment effect on the treated-type parameters can be identified under a generalized parallel trends assumption that is similar to the binary treatment setup. However, interpreting differences in these parameters across different values of the treatment can be particularly challenging due to selection bias that is not ruled out by the parallel trends assumption. We discuss alternative, typically stronger, assumptions that alleviate these challenges. We also provide a variety of treatment effect decomposition results, highlighting that parameters associated with popular linear two-way fixed-effect (TWFE) specifications can be hard to interpret, even when there are only two time periods. We introduce alternative estimation procedures that do not suffer from these TWFE drawbacks, and show in an application that they can lead to different conclusions.

JEL Codes: C14, C21, C23

Keywords: Difference-in-Differences, Continuous Treatment, Multi-Valued Discrete Treatment, Parallel Trends, Two-way fixed effects, Multiple Periods, Variation in Treatment Timing, Treatment Effect Heterogeneity

1 Introduction

The canonical difference-in-differences (DiD) research design compares outcomes between treated and untreated groups (difference one), before and after treatment started (difference two). But in many DiD applications, the treatment does not simply “turn on”, it has a “dose” or operates with varying intensity. Pollution dissipates across space, affecting locations near its source more severely than faraway locations. Localities spend different amounts on public goods and services, or set different minimum wages. Students choose how long to stay in school.

Continuous treatments can offer advantages over binary ones.111We generally use “continuous” treatments also to mean multi-valued ordered discrete treatments, but make the distinction explicit for certain results. Variation in intensity makes it possible to evaluate treatments that all units receive. A clear “dose-response” relationship between outcomes and treatment intensity can bolster the case for a causal interpretation or test a theoretical prediction.222In his 1965 presidential address to the Royal Society of Medicine, Sir Austin Bradford Hill, a pioneer in the study of smoking and cancer, included among his criteria for inferring causality from observational data, “a biological gradient, or dose-response curve” and argued that “we should look most carefully for such evidence” ([34]). Finally, we may care more about the effect of changes in treatment intensity, such as increased funding, pollution abatement, or expanded eligibility, than about the effect of the existence of a treatment that already exists.

Despite how conceptually useful and practically common continuous DiD designs are, currently available econometric results provide little guidance on applying and interpreting them, except in some specific cases. In this paper, we introduce a set of tools that are suitable for DiD setups with variation in treatment dosage. In particular, we (a) discuss how one can identify a variety of treatment effect parameters by exploiting parallel-trends-type assumptions, (b) show that two-way fixed-effects (TWFE) estimators typically fail to have appealing causal interpretations, even when weights are non-negative, and (c) propose nonparametric estimators for clearly defined causal parameters that have attractive statistical properties, such as fast uniform convergence rates and narrow confidence bands. Our results cover DiD setups with varying treatment intensity or differential exposure to treatment but do not cover fuzzy designs.

We start by discussing causal parameters in a two-period DiD design in which units move from no treatment to a non-zero dose—we first focus on simple setups with two time periods to foster intuition and simplify exposition but later present extensions to more complex staggered designs with continuous treatments. We call the difference between a unit’s potential outcome under dose and its untreated potential outcome a level treatment effect. We call the difference in a unit’s potential outcome with a marginal increase in the dose a causal response [8]. When treatment is binary, these two notions of treatment effects coincide, but they do not under a continuous treatment. Importantly, level treatment effects and causal responses can have meaningfully different interpretations, and we establish that they require different identifying assumptions as well. Comparisons between treated and untreated units identify average (level) treatment effect parameters under a parallel trends assumption on untreated potential outcomes, similar to binary DiD designs. Comparisons between adjacent dose groups, however, do not identify average causal response parameters under the “standard” parallel trends assumption. We discuss an alternative but typically stronger assumption, which we call strong parallel trends, that says that the path of outcomes for lower-dose units must reflect how higher-dose units’ outcomes would have changed had they instead experienced the lower dose. Thus, strong parallel trends restricts treatment effect heterogeneity and justifies comparing dose groups. Absent this type of condition, comparisons across dose groups include causal responses but are “contaminated” by an additional term involving possibly different treatment effects of the same dose for different dose groups—we refer to this additional term as selection bias.333In applications where units choose their amount of the treatment, it is natural to refer to this term as selection bias. In other applications where the dose measures a unit’s amount of exposure to some treatment, a different term such as “heterogeneity bias” could be more appropriate. For simplicity, throughout the paper, we simply refer to this term as selection bias.

We next use the identification results to evaluate the most common way that practitioners estimate continuous DiD designs, which is to run a TWFE regression that includes time fixed effects (), unit fixed effects (), and the interaction of a dummy for the post-treatment period () with a variable that measures unit ’s dose or treatment intensity, :

| (1.1) |

This TWFE specification is clearly motivated by DiD setups with two periods and two treatment groups, though many prominent textbooks recommend using it in more general setups (e.g., [16], [9], and [50]). There are several ways to interpret , each corresponding to a different type of causal parameter. We decompose it in terms of level effects, scaled level effects, causal responses, and scaled high-versus-low () effects. Each decomposition is a weighted integral of dose-specific causal parameters, and none provide a clear causal and policy-relevant interpretation of , at least not when treatment effects are allowed to vary across doses and/or groups.

For instance, we show that can be expressed as a weighted integral of average level treatment effect parameters but where the weights integrate to zero, indicating that should not be interpreted as an average (level) treatment effect. Interestingly, however, TWFE puts negative weights on the below-average dose units and positive weights on above-average dose units, and, thus, after re-scaling by a weighted average of the difference between doses for high- and low-dose units, is equivalent to a weighted binary DiD using higher-dose units as the “treated” group and lower-dose units as the “comparison” group, with weights proportional to a unit’s absolute distance from the mean dose. Our next decomposition, based on average level treatment effect parameters scaled by their dose, also displays negative weights, though their weights integrate up to one and not zero.

In contrast, a TWFE decomposition in terms of average causal response parameters has weights that integrate up to one and are non-negative, but also includes a selection bias term stemming from effect heterogeneity across doses. The strong parallel trends assumption eliminates this selection bias. The weights on causal responses at different doses, however, differ from the distribution of the dose, which creates a further challenge to interpreting in the presence of treatment effect heterogeneity, even if strong parallel trends holds. This is particularly important when the magnitude of the causal effects is of interest, but also has a strong bite in setups with nonlinear average level treatment effects, as average causal responses may have different signs across the dosage distribution. We reach a similar conclusion when decomposing using the scaled average effects as building blocks.

Given these drawbacks, we propose nonparametric DiD estimators that build on our identification results and recover interpretable causal parameters. When the treatment is discrete, this is as simple as running a linear regression with multiple treatment indicators, which is similar to staggered DiD setups [15]. When the treatment is continuous, we propose a modest adaption of [20] that allows us to estimate the average level treatment effects and the average causal responses as functions of the dose. These tools are motivated by clearly defined parallel trends assumptions, do not rely on strong functional form assumptions, are easy to implement, and are fully data-driven. It follows from [20] that our DiD estimators for continuous treatment converge at the fastest possible (i.e., minimax) rate in sup-norm, and our uniform confidence bands are asymptotically narrower (more precise) than those based on undersmoothing, and yet have correct asymptotic coverage and contract at, or within a factor of, the minimax rate. We also show how to construct causal summary measures of our average treatment effect functions that bypass the TWFE weighting problems by using the dose density as weights. Our results suggest that one can easily summarize average level treatment effects among treated units by comparing the average change in outcomes for all treated units to the average change in outcomes for untreated units [49]. This can be estimated by running a binary DiD with a “treatment dummy” equal to one for any units with positive doses. Summarizing average causal responses using dose density weights involves estimating an average derivative, which is simple to compute using “flexible” linear regressions. We also discuss how to construct event-study results using these summary measures, which can then be used to assess the plausibility of the parallel trends assumptions.

To show how TWFE regressions perform in practice and to illustrate the benefits of our proposed estimators, we revisit [1]’s \citeyearacemoglu-finkelstein-2008 study of a 1983 Medicare reform that eliminated labor subsidies for hospitals. The original paper uses a TWFE estimator to compare the change in capital-labor ratios between hospitals whose input prices were more or less affected by the end of the subsidy. It concludes that price regulations favoring capital significantly increase capital use. The distinction between level treatment effect parameters and causal responses is important in this example: a positive level treatment effect shows that the policy as a whole increased the use of capital, while causal responses describe which subsidy levels generated the largest responses. We find that the reform raised capital-labor ratios by about 18 percent, which is 50 percent larger than the comparable TWFE estimate because of the weighting issues highlighted by our decompositions. We also estimate variable average causal response () parameters that are quite large at low subsidy levels—implying elasticities of substitution greater than 2—yet slightly negative for most positive doses. These negative estimates cast doubt on the strong parallel trends assumption, the simple two-factor model of hospital production, or both. Our results support [1]’s \citeyearacemoglu-finkelstein-2008 conclusion that the 1983 Medicare reform led hospitals to favor capital over labor, but suggests caution in a policy interpretation about which subsidy levels have the largest effects or an economic interpretation in terms of production function parameters.

Related Literature: This paper contributes to the fast-growing literature on modern DiD methods; see, e.g., [44], [28], and [14] for overviews. Most of this work focuses on binary treatment setups, with a few exceptions. [25] focuses on fuzzy designs, where a researcher is interested in individual-level effects of a binary treatment that has been aggregated across units into a continuous “treatment rate.” In contrast, we study “sharp” designs where the treatment exposure is itself continuous or multi-valued discrete at the unit-level. The supplemental appendix of [26] considers the case with ordered multi-valued treatments and presents a decomposition of TWFE regressions using a scaled treatment effect measure as the “building block.” Our decomposition differs from theirs in that we allow for continuous treatments and also consider different building blocks. See also [24] for Changes-in-Changes-types of procedures with a continuous treatment in the spirit of [11].

In work subsequent to ours, [27] consider a DiD setup with continuous treatments with potentially non-staggered (but static) treatments. Their paper and ours tackle related but different and complementary problems. For instance, their target parameters differ from ours, as they consider (distance-weighted) averages of what we refer to as average effects. Unlike our , these parameters average effects of discrete rather than marginal changes of treatments. Furthermore, our estimation procedures greatly differ from theirs, as we consider both functional parameters (dose-response and curves) and causal summary measures. On the other hand, they consider instrumental variable extensions, which we do not.

Our TWFE decompositions are related to a number of recent results on the limitations of TWFE linear regressions in the presence of treatment effect heterogeneity. For example, that some of our TWFE decompositions include negative weights is related to the negative weights that can arise for TWFE estimators with binary treatments (see, e.g., [32], [26], [48], and [13]). We add to this literature by highlighting that the same TWFE regression coefficient can have different interpretations depending on the “building blocks”, and that new “bias” terms may appear, depending on the type of parallel trends assumption being used. Although our results show that negative weights can show up even in the two-period cases, which is not the case in the papers above, a perhaps more important lesson from our decompositions is that even when all weights are non-negative, TWFE can still provide an unappealing causal summary parameter with heterogeneous treatment effects. We also note that, as a by-product of our decomposition results, if one replaces our DiD setting with one with cross-sectional data and a randomly assigned dose, all four of our decomposition results would continue to go through (e.g., just take the pre-treatment outcome to be zero almost surely), highlighting that linear specifications may not be very attractive with continuous treatments, even when the dose is fully randomized. These results seem to be new to the literature.

To construct our new DiD estimators and conduct asymptotically valid (data-driven) inferences, we build on [20]; see also [21, 22]. More specifically, we adapt [20]’s nonparametric IV data-driven sup-norm adaptive estimation and inference procedures to our context. Doing so allows us to estimate the average level treatment effect and the average causal response curves in a single shot, at least under strong parallel trends. We also show how one can build on these estimators to get easy-to-interpret summary treatment effect measures. This feature of our paper connects to the literature on the efficient estimation of average derivatives, examples of which include [40], [3], [19] and references therein.

Our results are also related to other branches of causal inference and econometrics. For instance, [31] connect Bartik instruments to DiD designs under an independence assumption. We complement this analysis by studying identification in a similar setup under different kinds of parallel trends assumptions. Our cautionary results about interpreting comparisons of s at different doses echo related points on comparing “local” treatment effect parameters to each other. Some examples include [42, 6, 38] in the context of local average treatment effects; [18] and [17] in the context of regression discontinuity designs with multiple cutoffs; or [29] in the context of difference-in-differences with two treatments. Our results highlighting limitations of linear regressions to approximate treatment effects are related to [10], [46, 47], [12], and [30]. In particular, our decomposition results about the importance of the building block parameters are related to [46], which also discusses related points in binary cross-sectional designs based on unconfoundedness. Finally, we note that our causal response decomposition builds on [51, Proposition 2 ], which expresses the slope coefficient in a regression of an outcome on a continuous variable as a weighted average of underlying local slopes. Besides differences related to causal interpretations and panel data, we extend those results to allow for a mass of untreated units.

2 Motivating Continuous DiD from an Empirical Perspective

To fix ideas and provide intuition for our theoretical results, we revisit [1]’s \citeyearacemoglu-finkelstein-2008 (AF) study of how price regulations affect firms’ input choices. When Medicare began in 1965, hospitals received reimbursements from the federal government for a share of their labor and capital expenditures proportional to the fraction of total patient days accounted for by Medicare recipients (). Hospital thus faced input prices equal to for labor and for capital, where and are the labor and capital subsidy rates and and are market wages and rental rates. In 1983, Medicare moved to the Prospective Payment System (PPS), which replaced the labor subsidy with a small payment per episode/diagnosis. This set but left the capital subsidy unchanged. Therefore, the price of labor for a given hospital rose from to , skewing relative factor prices.

The statutory relationship between a hospital’s Medicare volume, , and the change in its price of labor, , motivates AF’s use of a continuous DiD design comparing changes in capital/labor ratios before and after 1983 between hospitals with different pre-PPS Medicare inpatient shares.444AF use data reported by hospitals each year to the American Hospital Association from 1980 to 1986 [4]. They proxy for the capital/labor ratio using the depreciation share of total operating expenses, which averages about 4.5 percent in their period. AF’s description, estimation, and interpretation of this empirical strategy touch on some of the most common ways of justifying and implementing continuous DiD designs.

One motivation for this design is practical: variation in a dose (or exposure) permits the evaluation of treatments for which binary DiD is either infeasible or undesirable. In AF’s case, about 15 percent of hospitals were “untreated” by the change in Medicare’s subsidy policy because they served non-Medicare-eligible populations, like children or psychiatric patients, so they may not constitute a valid comparison group. AF therefore describe , which is the hospital’s Medicare volume in 1983, as an “attractive source of variation” in the price of labor both because it varies substantially—the mean of among treated hospitals is 0.45, and the standard deviation is 0.15—and because hospitals with may be more comparable to each other than treated hospitals are to untreated hospitals.

Another common justification for continuous DiD designs is that a “dose-response” relationship between exposure and outcomes can support a causal interpretation or test a theoretical prediction. [37, p. 158 ], for example, argues that “differences in the intensity of the treatment across different groups allow one to examine if the changes in outcomes differ across treatment levels in the expected direction.”555[34] makes this point in the context of smoking and cancer: “The fact that the death rate from cancer of the lung rises linearly with the number of cigarettes smoked daily, adds a very great deal to the simpler evidence that cigarette smokers have a higher death rate than non-smokers.” He also notes that more deaths among light rather than heavy smokers would weaken the causal claim unless one could “envisage some much more complex relationship to satisfy the cause-and-effect hypothesis.” AF lay out a simple theoretical framework in which the move to PPS should (i) raise capital/labor ratios and (ii) do so more strongly for hospitals with higher pre-PPS values of . They view their continuous DiD design as a way to estimate a causal effect of PPS as a whole and test the theoretical predictions of their model.

Finally, researchers often advocate for continuous DiD designs because they can be used to estimate average causal effects of small changes in the dose. In many economic models, price and income elasticities determine optimal policies like tax rates, tax bases, subsidies, and regulations [33], but these are continuous concepts that can be estimated accurately only with continuous variation. We discuss how AF’s theoretical framework implies, under some assumptions, that DiD estimates provide information about hospitals’ elasticity of substitution between capital and labor, although AF do not argue for this kind of “marginal” interpretation.

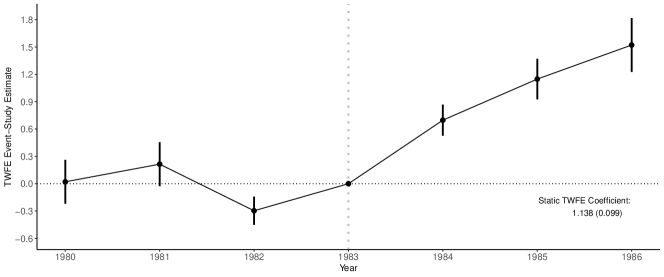

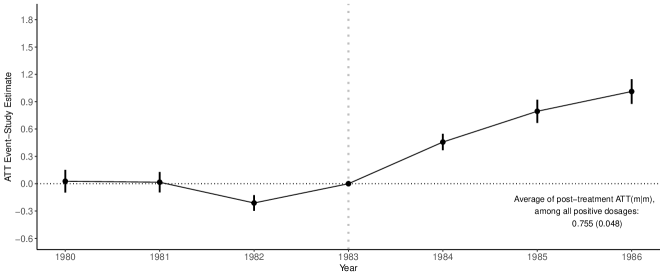

Notes: The figure plots TWFE event-study coefficients and their 95% confidence intervals from regressions with hospital fixed effects, year fixed effects, and the 1983 Medicare inpatient share () interacted with either a dummy for years after 1983 or the year dummies. The outcome variable is the depreciation share of total operating expenses, a measure of hospitals’ capital/labor ratio. The data cover the years 1980-1986 and come from the American Hospital Association’s annual survey [4]. We dropped 860 hospitals (out of 6741) that have missing data for the outcome. We also report the static TWFE coefficient and standard errors associated with (1.1). All standard errors are clustered at the hospital level.

In terms of estimation, AF use the standard tool for continuous DiD designs: a TWFE regression with hospital and year fixed effects. They follow textbook advice. [50, p. 132 ] observes that a two-period DiD regression estimator “can be easily modified to allow for continuous, or at least non-binary, ‘treatments.”’ [9, p. 234 ] emphasize “a second advantage of regression DD is that it facilitates the study of policies other than those that can be described by a dummy.” They also follow common practice and describe their identifying assumption as an extension of the parallel trends assumption from binary designs: “Without the introduction of PPS, hospitals with different ’s would not have experienced differential changes in their outcomes in the post-PPS period” (emphasis added).

Figure 1 reproduces AF’s DiD event-study coefficients for each calendar year, relative to 1983, and the estimate of from an equation like (1.1).666The results in Figure 1 are not numerically identical to AF’s because we drop 860 hospitals (out of 6,741) with missing outcomes for some years. AF interpret these results as indicative that after 1983, capital/labor ratios rose more strongly for hospitals with higher values of , without a substantial differential change in input mix before PPS. Our impression is that event-study results like those in Figure 1 would usually be interpreted as strong causal evidence because there are (relatively) small pre-trend estimates, large differences in outcomes between higher- and lower-dose units after treatment, and tight confidence intervals. What is missing from most continuous DiD analyses, however, is a specific statement about what causal parameters researchers would like to estimate, the assumptions under which they are identified, and a formal justification for a particular estimator. Our goal is to shed light on these three issues.

3 Baseline Case: A New Treatment with Two Periods

We illustrate our main points in a setup with two periods of panel data, and . In the second period, some units receive a treatment “dose,” denoted by , and others remain untreated. Extensions to multiple periods and staggered setups are discussed in Section 5. We denote the support of by . can be (absolutely) continuous or can be multi-valued discrete, but to simplify the exposition, we refer to it as “continuous.” We define potential outcomes for unit in period as . This is the outcome that unit would experience in period under dose . In each time period , the observed outcome for unit is . We assume that all expectations are finite and well-defined. Henceforth, we omit the unit index to make the notation less cluttered and define .

3.1 Parameters of Interest with a Continuous Treatment

The potential outcomes notation reflects that treatment can take many values, and so each unit can experience many types of causal effects. The level treatment effect of dose in time period for a given unit is defined as its potential outcome when minus its untreated potential outcome: . Level treatment effects measure the treatment effect at time from switching treatment dosage from to . This is a straightforward extension of a binary “treatment effect” to a continuous “treatment effect function” or “dose-response function.”

But zero-treatment is not the only relevant counterfactual. We define a unit’s causal response at as , the derivative of the potential outcome with respect to dose (when the treatment is continuous), 777This is a slight abuse of notation as we do not require to be differentiable (or even continuous), but rather we mean here the effect of a marginal change in the dose on a unit’s outcome: . or as the difference in potential outcomes between adjacent doses, (when the treatment is discrete). Causal responses measure the treatment effect at time of a “marginal” increment of dose . These two types of treatment effects—the level of or its slope, —define unit-level causal parameters in continuous designs, and connect to results in the instrumental variables (IV) literature on multi-valued discrete or continuous endogenous variables ([8], [7]).

We focus on “building block” parameters that are averages of these two kinds of causal effects in the post-treatment period, . Average level treatment effects (which we refer to as average treatment effects) extend definitions from the binary case:

where is the average effect of dose compared to zero dosage in the post treatment period , on units that actually experienced dose . When , this is the among units that received dose . is the average difference between potential outcomes under dose relative to untreated potential outcomes across all units, not just those that experienced dose , in time period .

Average causal response parameters for absolutely continuous treatments are defined as

equals the derivative of the average potential outcome for units that received dose evaluated at . This is equivalent to the derivative of with respect to , evaluated at . For discrete treatments, average causal responses are defined in a similar way but with slightly different notation to accommodate discreteness of :

equals the difference in mean potential outcomes between dose level and the next lowest dose in period . We follow the literature, particularly [8], by not defining as being scaled by the difference between and though, up to definitions of parameters, that does not affect the results below.

Notes: The figure plots (the average effect of experiencing each dose among units that actually experienced dose ). We highlight causal parameters for two doses, and . and are average treatment effect on the treated parameters and refer to the height of the curve. and are average causal response parameters and refer to the slope of the curve. We show them for a continuous dose, when the is a tangent line, and for a discrete dose when is a line connecting two discrete points on .

Figure 2 illustrates these parameters graphically. The concave line plots an average treatment effect function against the dose for units actually treated with dose , . If we consider dose levels and , there are two possible parameters. The first, , the level of group ’s average treatment effect function at , is an average treatment effect that is “local” to units that experienced dose . The second, , is also “local” to the group, but refers to the effect they would experience at dose even though they did not actually receive that dose. The continuous-dose parameters are the slopes of tangent lines to the function, and the discrete-dose parameters are the slopes of lines connecting two points on the function. As with s, our definitions encompass causal responses to doses other than the one a group actually receives (i.e., ).

A proper interpretation of continuous DiD results hinges on which type of parameter one wants, and can identify and estimate. For instance, even if all parameters are large and positive, some parameters could be zero or negative. A researcher misinterpreting a large estimate as an , in this case, would mistakenly conclude that a policy to raise every unit’s dose would have large effects. A researcher confusing a small for an would mistakenly conclude that an entire policy was ineffective, even though it actually just has small effects at the margin.

The above-mentioned causal parameters are functional parameters because they are allowed to vary arbitrarily across dose groups and across (counterfactual) doses . This contrasts with from (1.1), which is a single number. In practice, we expect researchers to also typically want to aggregate these functional parameters into lower-dimensional objects that are easier to report and may be more precisely estimated. We focus on aggregating the functional parameters discussed above by averaging them using the distribution of the dose among all treated units. We denote these summary parameters by

These provide natural ways to summarize the underlying parameters; moreover, all four of these parameters provide “best” approximations in the sense of minimizing the mean squared distance between the summary parameter and the functional parameters. Also, note that and are average derivative-type parameters, and average derivatives have been widely studied in econometrics, see, e.g., [40], [3], [19], and references therein.

3.2 Identification with a Continuous Treatment

This section discusses the identification of average treatment effect and average causal response parameters. Toward this end, we make the following assumptions.

Assumption 1 (Random Sampling).

The observed data consist of , which is independent and identically distributed.

Assumption 2 (Continuous or Multi-Valued Discrete Treatment).

In period , no unit is treated, while in period , the treatment dosage has support and is either continuous or multi-valued discrete. More precisely, one of the following is true:

-

(a)

, where with , for some . In addition, , is a Lebesgue density which satisfies for some positive constant and all , and is continuously differentiable on .

-

(b)

where where , for some . In addition, for all .

Assumption 3 (No-Anticipation and Observed Outcomes).

For all units, and all ,

Assumption 1 says that we observe two periods of panel data. Assumption 2 formalizes that a mass of units do not participate in the treatment in either period (we discuss the case with no untreated units in more detail at the end of this section), and the rest receive a continuous (2a) or discrete (2b) treatment. Assumption 2a allows for the smallest value of the treatment to be strictly larger than zero, which is common in applications. Assumption 3 says that units do not anticipate future treatments, so we observe untreated potential outcomes for all units in the first period. In the second period, we observe the potential outcome corresponding to the actual dose that unit experienced.

3.2.1 Identification under parallel trends

Identification of average level treatment effects follows closely from the DiD setup with binary treatments. In particular, our results rely on an extension of the binary parallel trends assumption.

Assumption 4 (Parallel Trends).

For all ,

Assumption 4 says that the average evolution of outcomes that units with any dose would have experienced without treatment is the same as the evolution of outcomes that units in the untreated group actually experienced. Binary DiD designs also rely on assumptions like this. To simplify the exposition below, we often simply refer to Assumption 4 as parallel trends (PT). The following result shows that under Assumption 4, is identified; all proofs are in Appendix B.

Theorem 3.1.

The identification results for in Theorem 3.1 hold by essentially the same arguments used for binary treatments. Because Assumption 4 ensures that is the same as the evolution of outcomes that treated units would have experienced without the treatment, equals the difference between the change in outcomes for the dose group and the untreated group. As a direct consequence, by averaging all the s over the distribution of non-zero dosages, we have that the summary parameter is identified by simply comparing units with a positive dose to untreated units. On the other hand, parallel trends, as defined in Assumption 4, is not strong enough to guarantee the identification of ; this issue is also present in binary setups.

The identification of average causal response parameters differs from the identification of parameters because it requires comparisons between dose groups. Our central identification result is that causal response parameters are not identified under Assumption 4, because comparisons between different dose groups are biased when treatment effects (of the same dose) vary across dose groups, even when the average evolution of untreated potential outcomes is the same.

Theorem 3.2.

Under Assumptions 1, 2, 3 and 4, causal response parameters are not identified. Specifically,

-

(a)

Under Assumption 2(a), for ,

- (b)

Theorem 3.2 says that under parallel trends, comparisons of outcome paths between higher- and lower-dose groups mix together (i) causal responses and (ii) a “selection bias” type of term that comes from differences in average treatment effects of the same dose for different dose groups. Intuitively, even if untreated potential outcomes evolve in the same way, observed paths of outcomes differ between dose groups for two reasons. One is the causal response itself, which comes from differences in doses ( versus ) causing differences in outcomes. The other is a selection bias type of contamination, which comes from differences across dose groups in the average level effect of the particular dose —parallel trends does not rule out that different dose groups could experience different treatment effects of the same dose.

Notes: The figure shows that comparing adjacent estimates equals an parameter (the slope of the higher-dose group’s function) and selection bias (the difference between the two groups’ functions at the lower dose).

Figure 3 illustrates this result for an example with two groups and two doses: and . The slope of the line that connects the points and is steeper than the average causal response of interest, , because it jumps from one function to the other. This is captured by the selection bias term, a version of selection-on-gains that equals the difference in treatment effects at the lower dose: . It breaks the causal interpretation because observed outcomes for lower-dose units are not a valid counterfactual for what higher-dose units would have experienced at a lower dose. The selection bias is not identified as we do not observe for units that experienced dose . Such a result precludes a causal interpretation of differences across doses, at least when one is not willing to further strengthen parallel trends as defined in Assumption 4.

3.2.2 Identification under strong parallel trends

The fact that average causal responses are not identified under a traditional parallel trends assumption suggests that learning about this type of parameter with continuous DiD designs requires new assumptions as well. This section discusses an alternative, typically stronger assumption that allows for the identification of (and ) parameters, which we refer to as strong parallel trends (SPT).

Assumption 5 (Strong Parallel Trends).

For all ,

Under Assumption 3, the right-hand side of the equation in Assumption 5 is the (observed) average evolution of outcomes for dose group . Assumption 5 says that the average evolution of outcomes for the entire population if all experienced dose (the left-hand side of the previous equation) is equal to the path of outcomes that dose group actually experienced. Assumption 5 notably differs from Assumption 4 because it involves potential outcomes under different doses, , rather than only untreated potential outcomes, .

An alternative way to think about Assumption 5 is as an assumption that restricts treatment effect heterogeneity.888There are some instances of versions of strong parallel trends implicitly being discussed in empirical work. [23, p. 1636 ]’s cross-region study of marginal propensities to consume (MPC) notes the possibility of finding a zero even when the MPC¿0 in all areas: “if low wealth areas have high MPCs and high wealth areas have low MPCs, an increase in the stock market could induce the same change in spending in both low and high wealth areas.” Similarly, [45, p. 25 ] discuss a version of strong parallel trends in the context of estimating the elasticity of taxable income for two groups facing different positive tax changes: “if the control group faces a tax change, difference-in-differences estimates will be consistent only if the elasticities are the same for the two groups.” In Theorem C.1 in Appendix C, we show that if one maintains Assumption 4, Assumption 5 is equivalent to assuming that for all doses. While this condition does not impose full treatment effect homogeneity, it does rule out selection-on-gains into a particular dose group and ensures the observed outcome changes for every dose group reflect what would have happened to all other groups had they received that dose. This condition can also be viewed as a structural assumption in the sense that it effectively allows one to extrapolate treatment effects of dose among dose group to treatment effects of dose for the entire population.

In the remainder of this section, we show that Assumption 5 is useful for recovering “global” average causal effect parameters, which are straightforward to compare to each other, and, hence, sidestep the selection bias issues discussed above. Before doing that, it is worth mentioning that we are not proposing Assumption 5 as an assumption that empirical researchers should readily adopt; in fact, in many applications, Assumption 5 may be a strong or implausible assumption. Rather, our aim is to clarify that many natural target parameters in DiD applications with a continuous treatment require stronger assumptions than parallel trends as defined in Assumption 4.

Theorem 3.3.

Assume that Assumptions 1, 2, 3 and 5 hold.

-

(a)

For , it follows that

-

(b)

When Assumption 2(a) holds (i.e., treatment is continuous), it follows that, for ,

- (c)

For part (a) of Theorem 3.3, recall that and differ when there is selection into dose group on the basis of treatment effects. Strong parallel trends rules out that kind of selection, which means that comparing average outcome changes of dose group to the untreated group identifies . For parts (b) and (c), the same implication of strong parallel trends ensures that lower-dose groups are valid counterfactuals for higher-dose groups.

Strong parallel trends only changes the interpretation of the estimand, not its form. One important implication is that conventional pre-tests for differential changes across groups before treatment cannot distinguish between Assumption 4 and Assumption 5. Because only untreated potential outcomes are observed before treatment, these periods cannot test the additional content of an assumption like SPT that necessarily involves treated potential outcomes.999There are caveats to this argument, particularly in cases where the researcher targets an aggregated parameter such as . See the discussion in Section 5.4 for more details.

Finally, the identification results in Theorem 3.3 immediately imply that averages of the and building blocks are identified as well. The following corollary states these results.

Corollary 3.1.

Assume that Assumptions 1, 2, 3 and 5 hold.

-

(a)

For , it follows that

-

(b)

When Assumption 2(a) holds (i.e., treatment is continuous), it follows that, for ,

-

(c)

When Assumption 2(b) holds (i.e., treatment is multi-valued), it follows that, for ,

These results highlight how identification in continuous DiD designs is fundamentally a question about dose-specific building block parameters and the underlying parallel trends assumption, not the aggregation choices that lead to particular summary parameters.

Remark 3.1 (No untreated units).

Researchers often use continuous designs when all units in their sample receive some amount of the treatment having in mind comparing units that are “more treated” to units that are “less treated”. Without untreated units, it is infeasible to compare dose group to an untreated group, and, hence, it is infeasible to directly recover or . However, a natural alternative is to compare dose group to dose group (the lowest possible amount of the treatment). In LABEL:app:no-untreated-units in the Supplementary Appendix, we show that, under parallel trends, when there are no untreated units,

This shows that this comparison is related to underlying causal effect parameters under parallel trends; however, recall from Theorem 3.2 that the expression on the right-hand side mixes together the average causal response of moving from to with selection bias. Under strong parallel trends, we have instead that

which does not include selection bias terms. This discussion highlights that (unlike a setting with a binary treatment) continuous variation in the dose can be used to learn about causal effects even if there is no untreated comparison group, but interpreting these results as causal effects of the treatments requires strengthening Assumption 4.

Remark 3.2 (Comparison between different parallel trends assumptions).

A researcher may be interested in comparing what is and what is not identified under different parallel trends assumptions, how these parallel trends assumptions restrict treatment effect heterogeneity, and how they compare to each other. In Appendix C, we pursue this exercise and provide a Portmanteau-type theorem that allows us to better understand the “bite” of each assumption. Among other things, we show that, in general, Assumption 4 and Assumption 5 are non-nested, though Assumption 5 will probably be stronger in most applications. We also introduce an aggregated parallel trends assumption that is useful for directly targeting , and an alternative strong parallel trends assumption that implies both Assumption 4 and Assumption 5 but further restricts treatment effect heterogeneity. See Theorem C.1 for additional details.

3.3 What Parameter Does TWFE Estimate?

In practice, empirical researchers using a continuous DiD design typically estimate a single summary parameter using a TWFE regression like Equation 1.1. This section links the TWFE estimand to our identification results for dose-specific parameters, describes the assumptions necessary to give TWFE some causal interpretation, and discusses what that interpretation is. We focus on continuous treatments and defer the discussion of multi-valued discrete treatments to LABEL:app:twfe-multivalued-treatment in the Supplementary Appendix.

Our impression is that empirical researchers typically interpret in three main (and related) ways, implicitly relying on different building blocks. First, is often directly interpreted as a causal response parameter; that is, how much the outcome causally increases on average when the treatment increases by one unit. This is the causal version of how regression coefficients are often taught to be interpreted in introductory econometrics classes. Second, it is common to pick a representative value for , to report , and interpret this quantity as . This is the main interpretation provided in [1]: “Given that the average hospital has a 38 percent Medicare share prior to PPS, this estimate [i.e., of , here equal to 1.129] suggests that in its first 3 years, the introduction of PPS was associated with an increase in the depreciation share of about 0.42 ( 1.129 0.38) for the average hospital.” Rearranging this expression shows that under this interpretation , which relates to a scaled level effect. Third, it is common to take two different representative values of the dose, and —a common choice is the 25th percentiles and 75th percentiles of the dose—and interpret as the average causal response of moving from dose to dose scaled by the distance between and ; this is a scaled effect. We aim to assess whether such types of interpretations are justified and under which conditions.

| Decomposition | Weights | Weights | ||||

|---|---|---|---|---|---|---|

| Causal response | ||||||

| Levels | ||||||

| Scaled levels | ||||||

| Scaled | ||||||

Notes: The table provides the formulas for the weights used in the decompositions of provided in this section.

The next proposition presents our decompositions of under parallel trends (Assumption 4) and under strong parallel trends (Assumption 5). The decompositions differ on the basis of the underlying building block parameters: causal response parameters ( and ), level treatment effect parameters ( and ), scaled level effects ( and ), or scaled effects ( and ). These building blocks are connected with the dose-parameters discussed in Section 3.2 and how empirical researchers interpret .101010The decompositions in the main text integrate over all possible doses. In LABEL:app:additional-twfe-decomposition-results in the Supplementary Appendix, we additionally consider scaled level and scaled decompositions for particular, fixed values of the dose. There we show that, even under strong parallel trends, can be (possibly much) different from these parameters when there is treatment effect heterogeneity due to (i) different weighting schemes (similar to the differences that we point out in this section) and (ii) being dependent on causal responses at other doses. The weights attached to each of these decompositions are presented in Table 1.

Theorem 3.4.

Under Assumptions 1, 2(a), 3, and 4, can be decomposed in the following ways:

-

(a)

Causal Response Decomposition:

where the weights are always positive and integrate to 1.

-

(b)

Levels Decomposition:

where for , and .

-

(c)

Scaled Levels Decomposition:

where for , and .

-

(d)

Scaled Decomposition

where the weights and are always positive and integrate to 1.

If one imposes Assumption 5 instead of Assumption 4, then the selection bias terms from Part (a) and Part (d) become zero, and the remainder of the decompositions remain true, except one needs to replace with in Part (a), with in Parts (b), (c) and (d), and with in Part (d).

Heuristically, the proof of Theorem 3.4 builds on the fact that equals the univariate slope coefficient from a regression of on an intercept and : . The covariance between outcome changes and the dose can be written in several different ways, each involving one type of comparison of paths of outcomes across different dose groups analyzed in Section 3.2. Upon imposing parallel trends (Assumption 4) or strong parallel trends (Assumption 5), we can map these comparisons of means to causal estimands, allowing us to write these decompositions in terms of different causal building blocks. The weights show how TWFE then aggregates dose-specific estimands. The same TWFE coefficient can, therefore, have different interpretations that depend on which building block parameter one has in mind. Unfortunately, Theorem 3.4 highlights that, in general, does not have a clear causal interpretation: the weights are hard to interpret and can be negative, and/or selection-bias terms contaminate the interpretation of as causal parameters. Despite the overall negative message, each decomposition provides interesting insights.

Theorem 3.4(a) shows that when causal responses are taken as the building blocks of the analysis, under Assumption 4, is equal to a weighted average (the weights are all positive and integrate to 1) of and the same selection bias derived in Theorem 3.2.111111Part (a) also includes a term that shows how TWFE handles a discrete jump from 0 to the minimum treated dose, . Paths of outcomes are not observed for doses below , but the scaled for dose group , , is averaged into . The sign of this selection bias depends on how treatment effects vary across dose groups at a given dose. If units in higher dose groups would have had larger positive treatment effects at every dose, for example, then will be larger than the weighted average of the ’s that appear in Theorem 3.4(a). Figure 3 illustrates this case for two groups. Invoking strong parallel trends eliminates the selection bias term.

The discussion above has important implications but does not come from TWFE itself. The weights, however, do inherit their form from ordinary least squares. Even under strong parallel trends, the particular interpretation of in terms of s hinges on the aggregation embodied in the weights . Because is positive and integrates to 1, is weakly causal under Assumption 5.121212We borrow the term weakly causal from [12], who define it to mean that some summary parameter is a weighted average of underlying causal parameters where the weights are all non-negative. They argue that this is a bare minimum requirement for a summary parameter to have a causal interpretation. However, it does not estimate a natural target parameter like because the TWFE weights do not generally equal the dose distribution among treated, . Differentiating shows that the weights are hump-shaped and centered around , so causal responses around the average dose affect the most (likewise, under parallel trends, selection bias around the average dose matters the most). Therefore, when varies across , TWFE’s weighting scheme can generate a misleading summary parameter except for special dose distributions.131313Another difference between the weighting scheme of and is that the weights underlying depend on the entire distribution of the dose while the weights underlying only depend on the distribution of the dose among treated units. This means that is (undesirably) sensitive to the size of the untreated group—this is in contrast to DiD with a binary treatment. For example, in our application, if we drop the untreated group (dropping the untreated group does not change the underlying average causal responses), our estimate of shrinks by 78%. This large difference in estimates is fully explained by how dropping the untreated group changes the weighting scheme inherited by . In contrast, our estimate of is invariant to removing the untreated group. Instead of letting the estimation method implicitly summarize the s, we recommend that researchers choose these aggregation schemes explicitly. In our view, a natural and econometrically-guided way to aggregate the ’s into a summary parameter is given by , which is identified (as indicated in Corollary 3.1) and can also be easily estimated.

Under linearity of realized outcomes, i.e, , because the weights integrate to one, . However, linearity alone does not imply that one necessarily recovers average causal responses. To see this, recall that , which is the sum of a causal response and a selection bias term. A leading example of linearity with selection bias would be when , where is the causal response and is selection bias—under linearity, we would recover the sum of these two terms. In other words, in terms of ACRs, linearity gets rid of interpretation issues inherited from the weighting scheme but does not get rid of selection bias. Strong parallel trends, on the other hand, avoids selection bias, suggesting that SPT and linearity would restore a causal interpretation of in terms of ACRs.

Part (b) expresses as a weighted integral of under parallel trends with weights that integrate to zero rather than one. Therefore, some weights are negative, and more significantly, puts the same amount of negative weight on s for doses below as it does positive weight on s for doses above .141414Unlike the other building block parameters considered in this section, even under versions of treatment effect homogeneity embedded in functional form restrictions, , in general, will not recover or . One way to view this result is that TWFE uses above-average dose units as an “effective treated group” and below-average dose units as an “effective comparison group” that potentially includes some treated units. While the cumulative positive weights and negative weights are equal to each other, they do not generally integrate to one within these groups, which means that does not equal the difference between a weighted average of outcome paths for the effective treated group relative to the effective comparison group. In LABEL:app:additional-twfe-decomposition-results in the Supplementary Appendix, however, we derive a corollary of the result in Part (b), which shows that we can re-write as the following weighted Wald-estimand:

| (3.1) |

The numerator of Equation (3.1) shows that compares weighted average outcome changes above and below with weights proportional to how far a unit’s dose is from .151515The exact expressions for the weights are and . These are true weights in the sense that they additionally satisfy . See LABEL:app:additional-twfe-decomposition-results in the Supplementary Appendix for more details. The denominator scales this comparison by the same weighted difference in . This representation highlights major limitations of using to summarize the average level-effect of a continuous treatment. First, while the numerator is (roughly) a weighted level-effect, the denominator shows that additionally depends on a measure of the average distance between the effective treated and comparison group.161616To give an example of why this scaling term is undesirable in the context of summarizing level effects, suppose that a researcher re-scales the dose by some constant, such as multiplying it by 100. This will not change the numerator in Equation 3.1, nor will it change the effective treated and comparison groups, nor will it change summary level effect parameters such as ; however, it will change through its effect on the denominator in Equation 3.1. At a higher level, all the other decompositions of considered in this section (which all have weights that integrate to one) involve building blocks that reflect different notions of slopes (rather than level effects). The expression in Equation 3.1 also relates to a binarized version of a slope effect. Second, the effective comparison group can include treated units. Third, uses “distance” weights ’s to aggregate across dosages. In contrast, does not suffer from any of these issues. In applications where the researcher is targeting level-effect parameters, we recommend favoring vis-a-vis .

Parts (c) and (d) of Theorem 3.4 provide interpretations of taking scaled paths of outcomes as building blocks. For part (c), (under parallel trends) and (under strong parallel trends) are “per-dosage” causal parameters. This part shows that the TWFE estimand includes negative weights under the same conditions as in part (b), though the weights integrate to one. Negative weights also appear in the TWFE estimand with a binary staggered treatment [32, 26, 13], and Theorem 3.4(c) shows that, with a continuous treatment, this drawback can arise even with two-periods (i.e., no staggering).171717As in the binary staggered case, a larger untreated group reduces the influence of negative weights. In fact, here, if there are enough untreated observations to make , then the weights are all positive. The weights themselves equal weights times the dose, which creates two key differences. First, they integrate to one. Second, they weigh the building block parameters for the highest and lowest doses even more heavily than in part (a). We note that, in the case of a discrete dose, this result is similar to the one in Theorem S3 of the Supplementary Appendix of [26]. Therefore, using “average slopes” as the underlying parameter of interest eliminates neither TWFE’s potential for negative weights nor its non-intuitive weighting scheme. For part (d), when is interpreted in terms of all possible comparisons of changes of outcomes for higher dose groups relative to lower dose groups, the weights are all positive and integrate to 1, but, under parallel trends, these comparisons all mix together causal effects of the higher treatment with selection bias terms. Although strong parallel trends removes the selection bias, the weights attached to the causal parameters are still hard to interpret.

To conclude this section, it is worth pointing out the pattern that emerges from the decomposition results presented in this section. When the building block parameters are mainly level-effect parameters, as in parts (b) and (c), is not affected by selection bias, but includes negative weights. On the other hand, when the building block parameters involve comparisons across different doses, as in parts (a) and (d), has positive weights but it includes selection bias terms under parallel trends alone.

As we have emphasized in this section, often, parametric linearity restrictions can “assume away” issues related to the weighting scheme inherited from the TWFE regression, though it does not fix the issues related to selection bias. In the next section, we show that one can propose alternative estimators to TWFE that also “fix” the weighting scheme but do not require the hard-to-justify linearity assumption. On the other hand, issues related to selection bias are still relevant and cannot be fixed through alternative estimation strategies.

Remark 3.3 (Decomposition with no untreated units).

It is straightforward to extend the TWFE decompositions discussed above to settings with no untreated units. For the causal response decomposition (part (a)), the exact same result applies with the exception that the second term involving is equal to 0. Similarly, for the scaled decomposition (part (d)), nothing changes except that the second term involving is equal to 0. For the levels decomposition and the scaled levels decomposition (parts (b) and (c)), with no untreated units, (or ) is not identified; instead, along the lines mentioned in Remark 3.1, instead of using the untreated comparison group, we can instead compare to the path of outcomes of the “least treated”. Thus, the same decompositions continue to apply except for that should be replaced by . This immediately means that these decompositions (in addition to negative weights) become complicated by issues related to selection bias.

4 DiD estimators that can highlight or summarize heterogeneity

So far, we have discussed two types of average causal effects with continuous DiD designs (average level effects and average causal responses), described different assumptions to identify them (parallel trends and strong parallel trends), and shown that, as a summary of these effects, a TWFE coefficient suffers from at least one of three problems: negative weights, selection bias, or non-intuitive weighting schemes. In this section, we discuss how one can bypass the limitations of TWFE by proposing data-driven estimation procedures that target well-defined causal parameters without relying on parametric functional form restrictions.

4.1 Nonparametric estimation of average causal functions

We start with the estimation of the dose-specific functions, , and under Assumption 4 or Assumption 5. When the treatment is multi-valued discrete, accommodating dose heterogeneity is simple and can be done by comparison of means, which can be operationalized via regressions. More explicitly, it suffices to regress outcome changes on a saturated set of dose indicators with untreated units as the omitted category:

| (4.1) |

Under parallel trends, the OLS coefficients are estimators of , and under SPT, each is a consistent (nonparametric) estimator for the , and is a consistent (nonparametric) estimator for ; see also [49].

When dose groups are small, or when the dose is absolutely continuous, (4.1) becomes less desirable, especially when one is unwilling to impose rigid functional form assumptions. In such cases, one needs to seek alternative nonparametric estimation strategies. To grasp the intuition behind the nonparametric methods we propose below, consider the case where a researcher entertains regression specifications of the type

| (4.2) |

where is a -dimensional vector of flexible (known) transformations of the dose (which includes an intercept), is a vector of finite dimensional (unknown) parameters, and is an idiosyncratic error term. These transformations could be as simple as a polynomial or B-spline in . One could then use OLS estimates of the coefficients to form estimators for , , or and conduct inference using the (functional) delta method.

The multiple choices involved in implementing this approach represent the main practical challenge that our nonparametric estimators help overcome. To estimate equation (4.2), one must pick the class of transformations (, basis functions) and the number of terms . This is difficult to justify without external information on functional forms, especially . Poor tuning parameter choices can lead to estimators that converge “too slowly”, and confidence bands that do not have the correct (asymptotic) coverage. Including too many terms risks overfitting and imprecise estimates, while including too few terms risks failing to capture heterogeneity well enough to eliminate bias; TWFE is an extreme example of this. On the other hand, “good” choices of tuning parameters usually require additional knowledge of model structure, such as the smoothness of , which, in practice, is ex-ante unknown. It is thus desirable to have a data-driven estimation method that adapts to these unknown model regularities, yields estimators and confidence bands with solid statistical guarantees and, at the same time, is easy to implement. Fortunately, such a class of nonparametric estimators has been recently proposed by [20] in a nonparametric IV context, and we show how one can modestly adapt their procedure to our context. As a consequence, our proposed DiD estimators of , , and parameters inherit attractive statistical properties from [20]. For instance, our data-adaptive DiD estimators converge at the fastest possible (i.e., minimax) rate in sup-norm, and our data-driven uniform confidence bands have correct asymptotic coverage and contract at, or within a factor of, the minimax rate.

We discuss our data-adaptive estimator under SPT (Assumption 5) so that it estimates the and curves. If one imposes Assumption 4 instead, then the same estimator yields the curve, but as Theorem 3.2 shows, its derivatives do not have a clear causal interpretation. We recommend this procedure when the number of cross-section units is large. If that is not the case, one may prefer a parametric specification with fixed.

Next, let us discuss how we implement our data-adaptive DiD estimator, which follows closely from [20]. The first step is to pick a family of basis functions . We restrict our attention to dyadic cubic B-splines as they are easy to compute and are able to achieve minimax sup-norm rates; see discussion in [20].

The next step is to pick our data-driven choice of sieve dimension, , related to how many transformations of we will include in our regression. Let be the set of possible sieve dimensions for our cubic B-splines. For a given sieve dimension , our proposed nonparametric estimator for and are given by

| (4.3) |

where ,

| (4.4) |

and denote the Moore-Penrose inverse of a generic matrix A, and for a generic variable ,

Note that is simply the OLS estimated coefficient of the regression of the “transformed outcome” onto the -dimensional B-spline , in the sub-sample of units that have positive treatment dosage.

In order to discuss how to pick appropriately, we need to add more notation. Let be the smallest sieve dimension in exceeding , and (so unless is bigger than 10 billion). Let be iid standard normal draws independent of the data . In addition, let

with

and . Finally, for a given and , let

be an estimator of the (asymptotic) variance of the contrast , and consider the bootstrap process

Our data-driven choice of the sieve dimension leverages the Lepskii-type selection of [20] (henceforth, CCK) and can be computed as follows.

Algorithm 1 (Computation of data-driven choice of sieve-dimension based on CCK.).

-

1.

Compute the data-drive index set of sieve dimensions

(4.5) where

(4.6) -

2.

Let . For each independent draw of , compute

(4.7) Let denote the quantile of the sup-t statistic (4.7) across a large number of independent draws of , say, 1,000.

-

3.

The data-driven choice of the sieve dimension is

(4.8)

The intuition behind Algorithm 1 is that it selects the most parsimonious specification across all considered ones, provided that the estimated curves are not “statistically different” from each other. If increasing leads to a statistically different estimate of , then it is “worth it” to increase the dimension. Heuristically, this is how Algorithm 1 trades off “bias” and “variance”.

It is worth stressing that Algorithm 1 is an adaptation of Procedure 1 of CCK, with small changes to adapt it to our DiD context. For instance, we consider a “transformed outcome” as the regressand of the sieve-based regression, whereas CCK consider an “observed” outcome as the regressand. We also focus on a specific sub-population, those with positive treatment. These modifications are important in our DiD context, as we allow for the causal effect of on to be discontinuous when the dose changes from to (the minimum positive dose). However, we note that these adaptions of the CCK procedure are modest and do not affect the asymptotic properties of the proposed estimators, as is -estimable and can be treated as known when establishing the asymptotic properties of the procedure.

Given Algorithm 1, our data-driven estimators for the and are therefore given by

| (4.9) |

Before we establish that and attain the minimax rate for estimating both and , we define the parameter space for . Let denote the Holder ball of smoothness and radius M. For given constants and , let and . For each , we let denote the distribution of where each observation is generated by iid draws of from a distribution of satisfying Assumptions 1, 2(a), 3, 5, Assumption 6 listed in Appendix A, and setting .

Theorem 4.1.

Let Assumptions 1, 2(a), 3, 5, and Assumption 6 listed in Appendix A hold. Then,

-

(a)

There exists a universal constant for which

-

(b)

For , there exists a universal constant for which

Importantly, the convergence rates in parts (a) and (b) are the minimax rates for estimating and , , under sup-norm loss.

Part (a) of Theorem 4.1 states that our estimator for the curve is uniformly consistent and that it attains the sup-norm minimax rate of convergence in an adaptive manner. Part (b) establishes the analogous results for our curve. As usual, the convergence rate for the derivative-type estimator () is slower than the level-type estimator (). These results follow from Theorem 4.1(a) and Corollary 4.1(a) of CCK, as we show in the proof of Theorem 4.1.

Next, we show how one can form data-driven uniform confidence bands (UCBs) for both and by adapting Procedure 2 of CCK to our DiD context. Toward this end, let and set . Define the bootstrap processes

where ,

Algorithm 2 (Computation of UCBs for and based on CCK.).

-

4.

For each independent draw of , compute

(4.10) Let and denote the quantile of the sup-t statistic and , respectively, across a large number of independent draws of , say, 1,000.

-

5.

The data-driven UCB for and , , are respectively given by

(4.11) (4.12)

Heuristically, Algorithm 2 is essentially describing that you can compute uniform confidence bands in a traditional way, except that we “inflate” critical values to account for potential “biases” that could be proportional to the “standard deviation”. The critical values also account for the model-selection uncertainty.

Importantly, the UCBs described in Algorithm 2 enjoy attractive statistical guarantees such as honesty and adaptivity. In practice, these mean that these UCBs are guaranteed to have asymptotically corrected coverage over a large (and generic) class of data-generating processes (honesty), and contract at the minimax sup-norm rate (adaptivity). These nice guarantees are established over a generic subclass of , as [35] shows that it is impossible to construct UCBs that are honest and adaptive over . This restriction, though, can be seen as a technical sidestep without major practical consequences, though; see Sections 4.3 and Appendix C.3 of CCK for a more detailed discussion.

We next describe the self-similar class of functions . As discussed in CCK, there exists a constant such that holds for all and all , with denoting the least squares projection of onto . For any small fixed and any , we define

and . Let and denote the UCBs from (4.11) and (4.12) replacing with a fixed .

The next theorem adapts Theorems 4.2 and 4.4 of CCK to our context.

Theorem 4.2.

Part (a) of Theorem 4.2 establishes that our proposed estimators are honest, i.e., they have the asymptotically correct coverage uniformly over generic classes of DGPs ( and ). Part (b) establishes that our uniform confidence bands are also adaptive, in the sense that they contract at, or within a logarithmic factor of, the minimax rate. These results are established by leveraging Theorem 4.2 and Theorem 4.4 of CCK.

4.2 Nonparametric estimation of summary measures of treatment effects

Researchers frequently want to report summary estimates either for interpretability or because a lower-dimensional parameter is an input into some model or post-estimation calculation. As we showed in Section 3, however, the predominant method for estimating such summary estimates, a TWFE regression coefficient, generally does not average across dose-specific parameters with intuitive weights. An estimate of average level treatment effects or average causal response functions, however, makes aggregation simple.

When there are untreated units, part (b) of Theorem 3.1 and part (a) of Corollary 3.1 suggest an extremely simple and familiar estimator of the average or over treatment dosages: the difference between the average change in outcomes among treated units minus the average outcome change for untreated units. This “binarized” DiD estimator can be obtained from the following simple linear regression specification:

| (4.13) |

where is a dummy variable for the dose being greater than zero, and are (unknown) finite-dimensional parameters, and and error term. It is straightforward to show that under Assumptions 1 to 4, . Thus, one can estimate and make (asymptotically valid) inferences about using (4.13), as long as some weak and standard regularity conditions are satisfied.181818This includes bounded second moments, and and being uniformly bounded away from zero. If one wishes to cluster the standard errors at a higher level than , there should also be sufficiently many treated () and untreated () clusters to justify the application of a Central Limit Theorem; see [44] for a discussion. If one imposes the SPT as in Assumption 5 instead of the PT as in Assumption 4, then it follows that . Note that this estimator applies in the same way to continuous and multi-valued discrete treatments.

Aggregated average causal response parameters can be constructed easily by weighting the estimated average causal functions across doses using the dose distribution itself. This solves the problem with TWFE’s weighting scheme. For multi-valued treatments, it is straightforward to aggregate these ’s based on the coefficients from (4.1) to form a plug-in estimator for the , using the identification formula in Corollary 3.1(c),191919When one imposes the PT Assumption 4 instead of the SPT Assumption 5, each is a consistent estimator for the . However, comparison across does not give an -type parameter, as indicated in Theorem 3.2. i.e.,

| (4.14) |

where . It follows from the delta method, our identification assumptions, and some weak regularity conditions that, as the sample size increases, converges to a normal distribution with mean zero and estimable asymptotic variance, implying that standard inference procedures can be reliably used when treatments are multi-valued discrete. One can follow a similar strategy when using the scaled as the “building blocks” of the aggregation.

A similar approach applies to estimating from a continuous dose. Our proposed estimator is simple to compute as it is based on the plug-in principle, i.e.,

with denoting the sample size with a positive dose.

Following [39] and [2], we can form a simple and practical estimator for the by “pretending” we follow a parametric model for the and functions and then using the delta-method. To provide an explicit formula, we introduce the following notation. For all observations with , let , and let , where

The next theorem establishes the large sample property of our proposed estimator.

5 Extensions

In this section, we briefly summarize several extensions of our main results that are further discussed in the Appendix and Supplementary Appendix.

5.1 Relaxing Strong Parallel Trends

Under traditional DiD assumptions, Assumption 4 led to the identification of local parameters that are difficult to compare across dosages. On the other hand, the strong parallel trends assumption led to parameters. These can be seen as extreme cases, and it is possible to trade off the strength of assumptions with the type of parameters that can be identified in different ways. The number of these intermediate possibilities is large, however. Here, we sketch what we consider to be three main ideas to relax strong parallel trends. LABEL:app:relaxing-strong-parallel-trends of the Supplementary Appendix provides substantially more detail.

First, in many cases, researchers may be willing to assume that they know the direction of the selection bias. For example, suppose that a researcher is willing to assume that, for all and any dose groups , , i.e., that higher dose groups would experience larger treatment effects at any value of the dose. In the Supplementary Appendix, we show that this type of assumption can lead to (possibly informative) bounds on causal effect parameters without requiring strong parallel trends. For example, it implies that, for all

which provides a bound on . See LABEL:prop:partial-identification in the Supplementary Appendix for more details.

A second possibility for relaxing strong parallel trends is to define a sub-region for which strong parallel trends holds. This would imply that one could identify parameters such as for (as well as its derivative)—this is a parameter that is more local than but less local than . These kinds of “local SPT” assumptions might be appealing in applications where there is substantial variation in the dose and the researcher is willing to assume that there is no selection bias among units that selected similar doses, but the researcher is unwilling to assume that there is no selection bias among units that select substantially different doses.202020A related intermediate assumption between Assumption 4 and Assumption 5 would be to directly assume that the selection bias term in Theorem 3.2 (i.e., is equal to 0. This would imply that is identified. This assumption is mechanically weaker than strong parallel trends though, to our knowledge, economic models that imply this condition (across all values of ) typically also imply strong parallel trends.

Finally, in some applications, strong parallel trends may be more plausible after conditioning on some observed covariates . Under a version of strong parallel trends conditional on covariates, one can show that the conditional average treatment effect, , is identified. Since this is an -type parameter, conditional on , one can compare across different values of the dose without inducing selection bias terms. This is an intermediate case, however, in that these are more local parameters than because they are local to the particular value of the covariates . See the discussion in LABEL:app:relaxing-strong-parallel-trends in the Supplementary Appendix for more details.

5.2 Multiple time periods and variation in treatment timing