Optimal Transport for Model Calibration

Abstract.

We provide a survey of recent results on model calibration by Optimal Transport. We present the general framework and then discuss the calibration of local, and local-stochastic, volatility models to European options, the joint VIX/SPX calibration problem as well as calibration to some path-dependent options. We explain the numerical algorithms and present examples both on synthetic and market data.

1. Introduction

In recent years, optimal transport theory has attracted the attention of many researchers. The problem was first formulated by Monge [20] in the context of civil engineering and was later given a rigorous mathematical treatment by Kantorovich [19] through the introduction of linear programming (for which he was awarded the Nobel Prize in economics in 1970). Brenier [4] in 1991 then revisited the subject (having in mind applications to the famous Euler equations of fluid dynamics), and later on, in 2000, Benamou and Brenier [3] introduced a time-continuous formulation of the problem, which gave rise to a massive amount of applications and mathematical results, see [23, 24] for an account of these results. Two recent Fields medallists (Villani 2010 and Figalli 2018) are world specialists of optimal transport, which says a lot about the importance that the topic has taken nowadays.

Recently, the theory of optimal transport has been adapted to solve problems in robust hedging and pricing both in discrete and in continuous-time models, see [2, 17, 21, 7], when it was discovered that pricing bounds on path-dependent derivatives with fixed European options could be formulated as a martingale optimal transport problem. Martingale optimal transport then became a subject of study in itself. The theory has been further used to calibrate the non-parametric discrete-time model proposed by Guyon [14] (see [15] for an extended version) to solve the so-called VIX/SPX calibration problem. The Schrödinger bridge problem, which is highly related to optimal transport, has been recently applied by Henry-Labodère [16] to introduce a new class of stochastic volatility models. These models can be calibrated by modifying only the drift while keeping the volatility of volatility unchanged.

In this paper, we give a synthetic overview of recent results on the continuous-time optimal transport for model calibration, obtained in [10, 11, 12, 13]. The results allow for exact calibration in the spirit of the celebrated Dupire’s formula, albeit without requiring the the knowledge of prices for a continuum of European options. We review the calibration of

-

-

local volatility models to European options [13],

-

-

local-stochastic volatility models to European options [12],

-

-

the joint VIX/SPX calibration problem [11],

-

-

path-dependent models to path-dependent options (e.g., Asian, barrier and lookback options) [10].

In particular, to the best of our knowledge, the last result was the first rigorous calibration framework including non-European options.

2. The semimartingale optimal transport problem

2.1. Probabilistic formulation

The problem of optimal transport by semimartingales was studied by Tan and Touzi [21]. Later in [12], motivated by financial applications, the authors extended this problem by replacing the terminal distribution constraint with a finite number of discrete constraints.

Let be the set of continuous paths, be the canonical process and be the canonical filtration generated by . Let be the collection of all probability measures on , under which is an -semimartingale such that

where is a -Brownian motion, and are -adapted processes. In particular, we say that is characterised by . Let be a subset of probability measures characterised by that are -integrable on , i.e.,

where is the Euclidean norm.

corresponds to the set of feasible market dynamics. Throughout, for simplicity, we will take the interest rates and the dividend yield to be zero111In applications with market data we then work out the forward prices.. To consider the subset of calibrated models, we fix and a finite number of constraints: market prices corresponding to options with payoffs and maturities . We assume that the longest maturity coincides with the time horizon, . We are then interested in:

We may have further restrictions on the pricing measures, e.g., some assets may have to be martingales. This, as well as other desirable properties, e.g., proximity to a reference model, are encoded through a cost function , where denotes the set of symmetric matrices of order . is taken convex in . Finding a suitable calibrated market model corresponds to solving

| (1) |

where and, in particular, a finite value indicates that a perfectly calibrated model was found.

2.2. PDE formulation

If in the above problem the state variables are matched to the constraints then the mimicking properties of diffusions, see [5], allow us to restrict the optimisations to local diffusions, i.e., to which are functions of time and the state variables . Therefore, the problem in (1) can be studied via PDE methods. Following the Benamou–Brenier formulation of the classical optimal transport from [3], we introduce the following formulation:

Formulation 1 (PDE formulation).

Solve

where the infimum is taken among all satisfying (in the distributional sense)

2.3. Dual formulation

In the PDE formulation, the objective function is convex and all constraints are linear in . Applying the classical tools of convex analysis222The proof of duality mainly relies on the Fenchel–Rockafellar theorem. We refer the reader to [12] for the full proof., we introduce a dual formulation:

Formulation 2 (Dual formulation).

If the optimal has been found, one can obtain the optimal of the PDE formulation by solving the supremum of in (2).

The dual formulation can be solved by gradient descent methods, and each component of the gradient vector can be calculated by solving a linear PDE. Given a , denote by the associated solution to (2). Let be the maximisers in the definition (2) of with . Define , then . Since depends on , by taking functional derivatives of (2) with respect to , we can formulate the gradients as

| (3) |

where solves

| (6) |

Since where is characterised by , the gradient that can be interpreted as the difference between the option prices given by the current optimisation iteration (or simply model prices) and the market option prices. The optimum is reached when the gradient is zero, in other words, the market option prices are attained exactly.

Remark 2.1.

Remark 2.2.

Recall that are required to be bounded continuous functions due to technical reasons. In practice, many options do not have bounded payoffs (e.g., call options). This can be fixed by either converting them into options with bounded payoffs via arbitrage arguments (e.g., put options via put-call parity), or by truncating the domain at some extremely large value. Options that do not have continuous payoffs (e.g., digital options, barrier options, etc.) can be approximated by uniformly continuous functions.

2.4. Numerical method

A numerical method for solving the dual formulation was proposed in [12]. The method can be described as follows:

-

(i)

set an initial , e.g., ,

-

(ii)

obtain by solving the backward HJB equation and obtain by solving the supremum of in (2),

- (iii)

-

(iv)

update by a gradient descent algorithm,

-

(v)

repeat step (ii)-(iv) until the all components of gradients are close to zero.

In [12] and [11], the HJB equation (2) was solved by the standard implicit finite difference method with the so-called policy iteration technique to handle the nonlinearity, and the linear pricing PDEs (6) were solved by an alternating direction implicit finite difference method that is faster than the standard implicit method. For the gradient descent algorithm, the L-BFGS algorithm was employed and showed good convergence in both works.

It should be mentioned that the dual formulation and the numerical method were also studied in [1] much earlier in the context of uncertain volatility calibration via entropy minimisation, although the connection to optimal transport and the proof the duality result was not established at that time.

3. Applications in model calibration

From now on, we will refer to the proposed calibration method simply as OT framework.

3.1. Local volatility calibration

The application of optimal transport to calibrate the local volatility model of Dupire [8] was explored in [13]. In [13], as an extension of the seminal work of [3], an augmented Lagrangian method was developed to solve the PDE formulation. In this section, we resolve the local volatility calibration problem by the OT framework.

Let be the logarithm of the underlying stock price at time . We are interested in finding a probability measure with characteristics where is some adapted process. In other words, we want to be a -semimartingale in the form of

| (7) |

To ensure that solves the above SDE, we consider a cost function of the form

| (10) |

where is some reference volatility level, are constants greater than 1, and are constants chosen so that the function reaches its minimum at with .

Given a vector of (discounted) European option payoff functions , a vector of maturities and a vector of European option prices , we want to further restrict so that are satisfied. Let be the logarithm of the current stock price, then the local volatility calibration problem can be reformulated as solving

| (11) |

where

Following the OT framework, we introduce the dual formulation of (11):

| (12) |

where is a solution to the HJB equation (in the viscosity sense)

| (13) |

with the terminal condition .

Numerical example

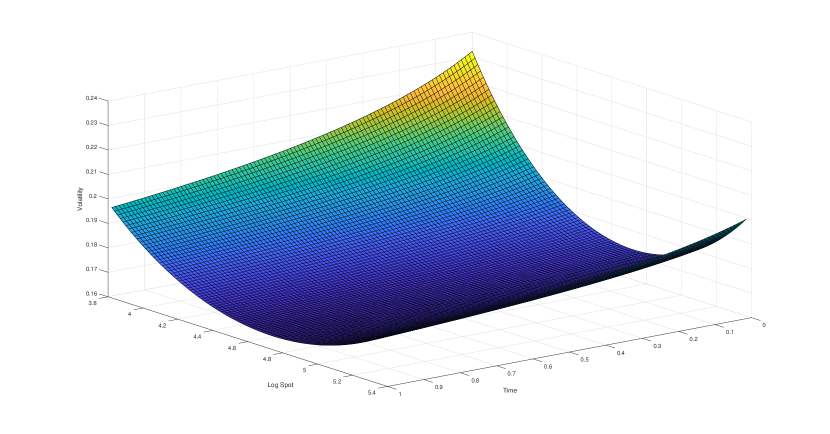

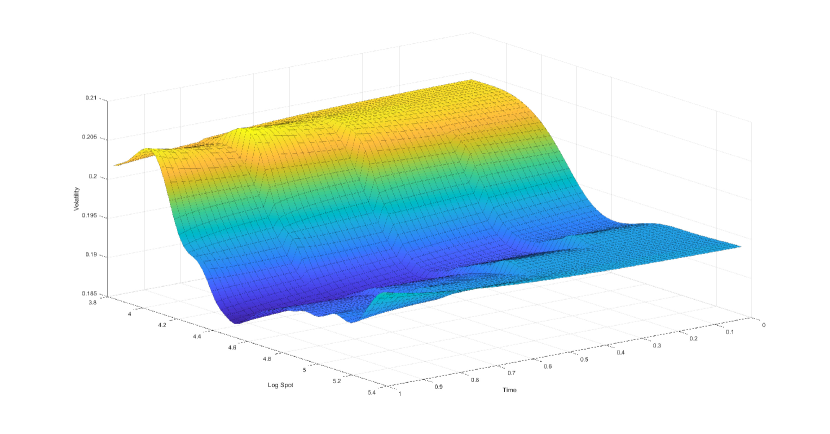

We give here an example in which a local volatility model is calibrated to the prices of 5 European put options at 5 different strikes and maturity . The option prices are generated by another local volatility model with the volatility given in Figure 1. The value of in (10) is set to 0.2.

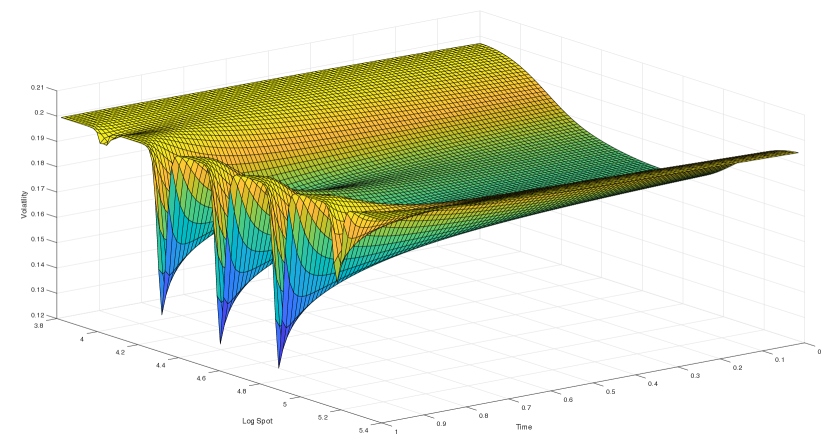

Figure 2 shows the calibrated local volatility surface and the model implied volatility skew. The humps between strikes in the volatility skew are caused by the spikes in the volatility surface. These spikes were also observed in [1].

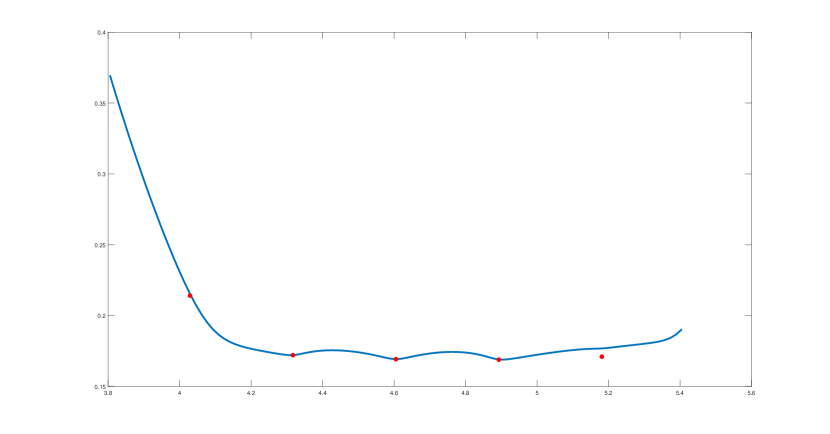

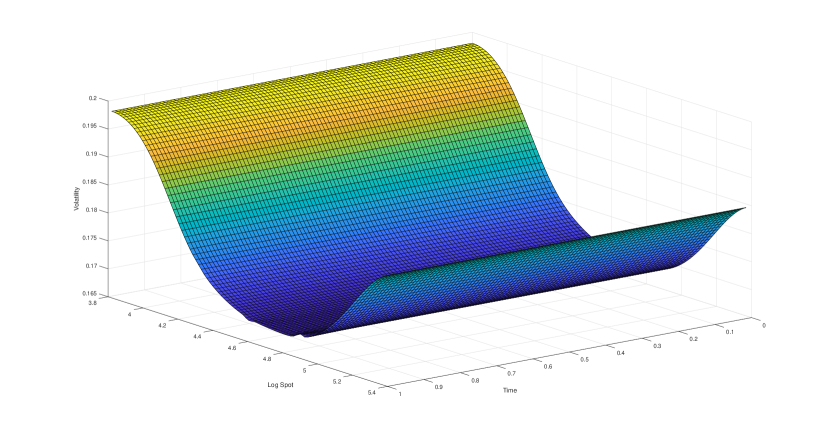

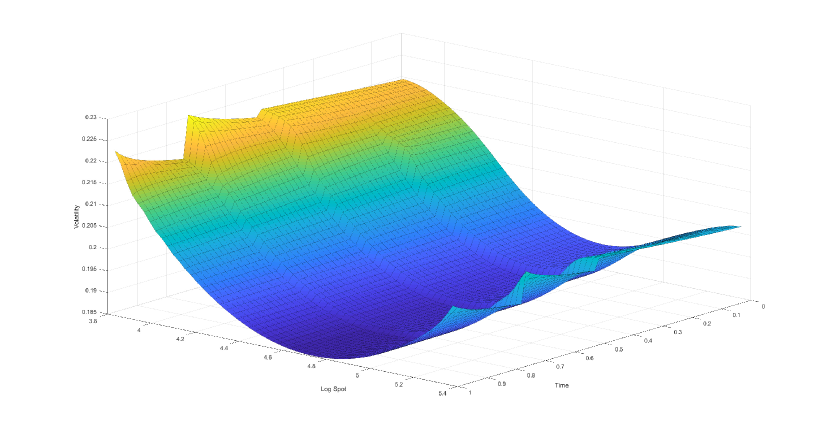

To smooth the volatility surface and hence the volatility skew, we suggest a reference iteration method. We start smoothing the spiky volatility surface by a simple moving average method. Next, we set the smoothed surface as the reference value and recalibrate the model by solving the dual formulation (12). After iterating the above steps 8 times, we obtain a local volatility model that has a smooth volatility skew and is also fully calibrated to the given option prices. The results are shown in Figure 3.

3.2. Local Stochastic Volatility Calibration

The Local-stochastic volatility (LSV) model was first introduced in [18]. It incorporates a nonparametric local factor (also called leverage) into a classical stochastic volatility model. Thus, while keeping consistent dynamics, the LSV model can match all observed market option prices, as long as one restricts to European products. In this section, we apply the OT framework to solve the LSV model calibration problem, as done in [12].

Consider probability measures under which are two-dimensional -semimartingales. Let be the logarithm of the underlying price and let be a mean-reverting stochastic factor. We are particularly interested in the following LSV model

| (14) |

where is some adapted process, and are constant parameters and are assumed given. The above model dynamics can be captured by probability measures characterised by such that

The model we consider here is slightly different from the standard LSV model from the literature. In the standard LSV model, the correlation between and is a constant and , where is known as the leverage function. Our simple modification allows that if a function is convex in , then it is convex in , which makes it easier to define a suitable cost function. Note that if , the correlation is simply and reduces to a Heston model. If we define a cost function to penalise away from , and we obtain by calibrating a Heston model to the market prices, then will be close to and hence the correlation will be close to . Moreover, if is independent of , then is indeed a local volatility model, and can be exactly calibrated to the option prices generated by any arbitrage-free implied volatility surface. Our goal is to calibrate with given so that is fully calibrated to the observable market European option prices.

In the spirit of (10), let us first define a convex function

where are constants greater than 1, and are constants chosen so that the function reaches its minimum at with . To ensure that has the dynamics (14), we define the cost function

where the convex set

In the function , we set to keep so that remains positive semidefinite for all . We set to regularise (or ) by penalising deviations of from a standard Heston model.

Given a vector of (discounted) European option payoff functions 444Note that are functions of . For example, if is the payoff function of an European call option, ., a vector of maturities and a vector of European option prices , we want to further restrict so that are satisfied. Assume that is given. Its first element is the logarithm of the current stock price, which is observed from the market, and its second element is the initial value of the instantaneous variance, which is a parameter but can be obtained by calibrating a Heston model. Then the LSV model calibration problem can be reformulated as solving

| (15) |

where

Applying the arguments developed in Section 2, we can derive a dual formulation of (15):

where is a solution to the following HJB equation (in the viscosity sense):

with the terminal condition .

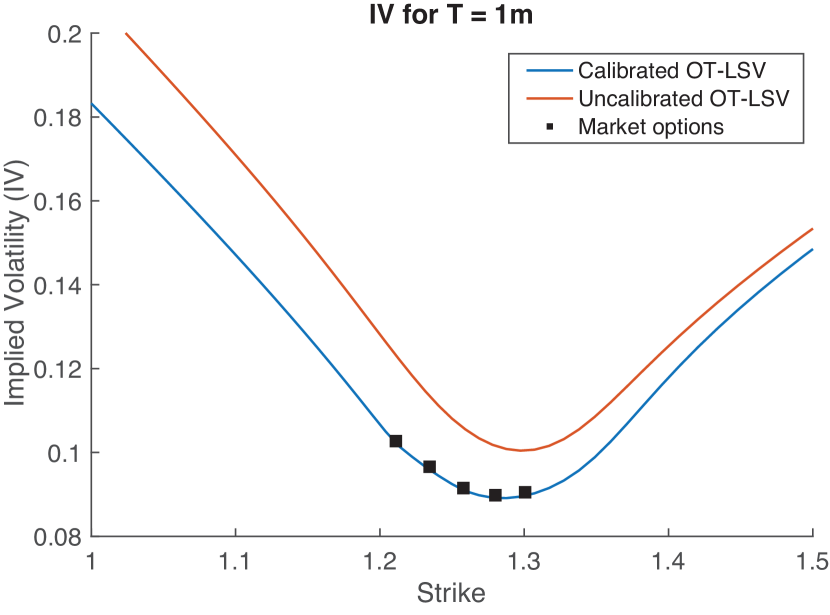

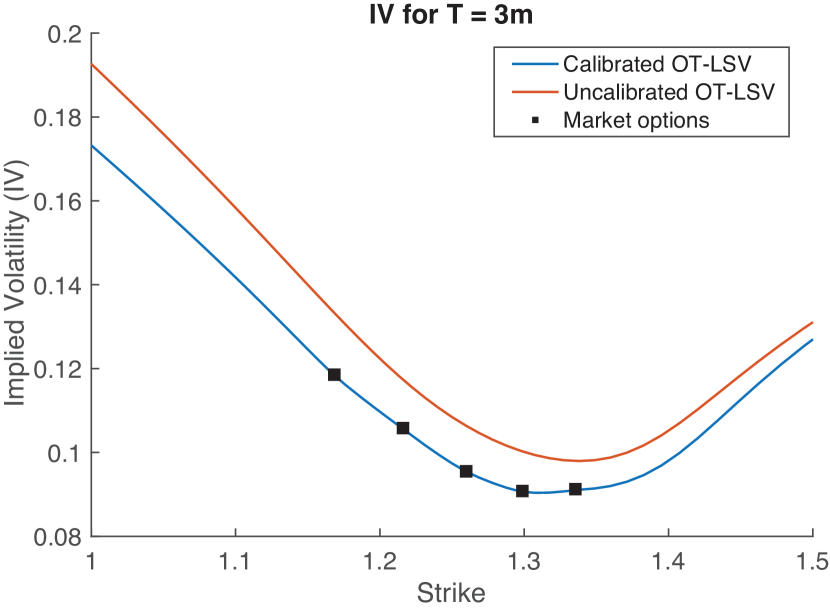

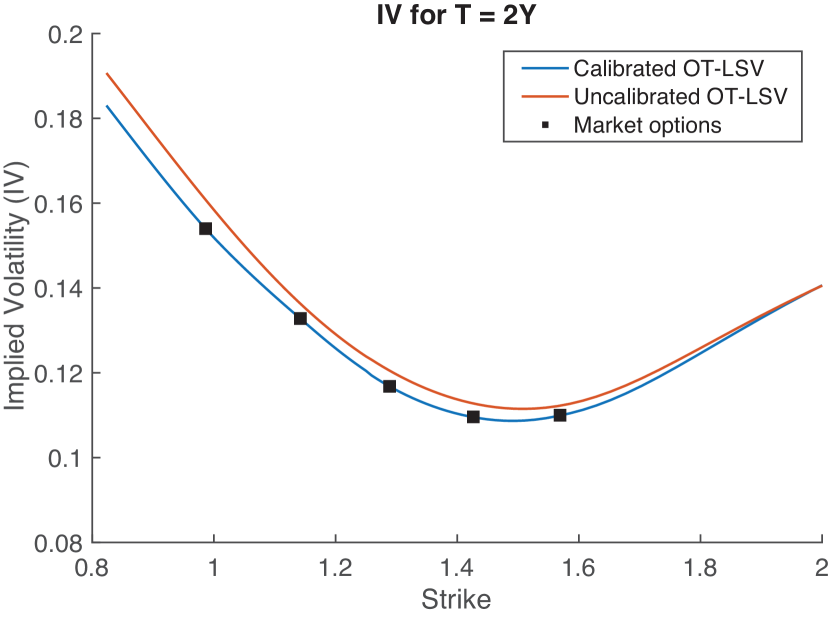

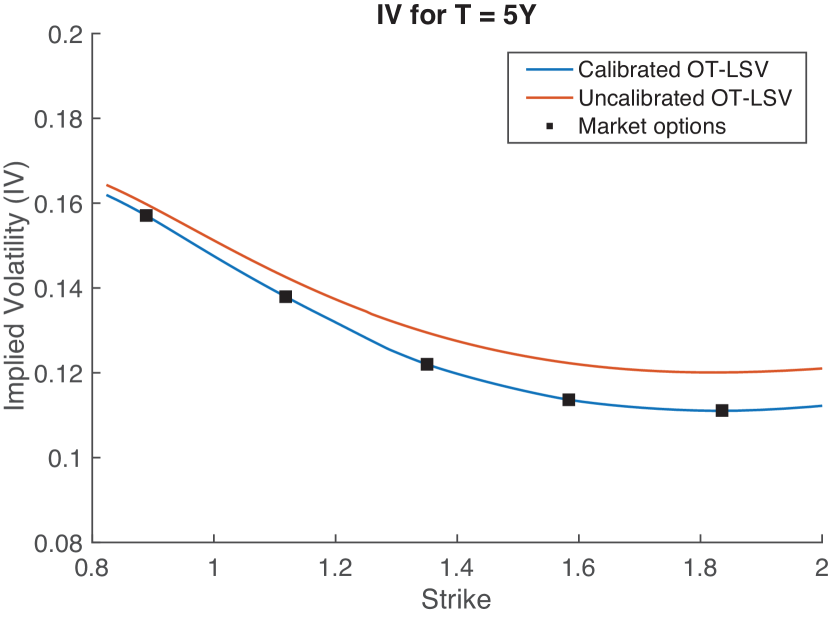

Numerical example

In the numerical example provided in [12], the process in (14), also called the OT-LSV model, was calibrated to the FX options market data provided in [22]. The data contains 10 maturities ranging from 1 month to 5 years. At each maturity, there are 5 European options at different strikes. The parameters are which are obtained by (roughly) calibrating a standard Heston model to the market option prices. Since , the Feller condition is strongly violated in this case. The initial position .

Figures 4 and 5 compare the implied volatility skews of both the calibrated and uncalibrated OT-LSV model. The results show that the OT-LSV model can be accurately calibrated to both short-maturity and long-maturity market option prices. Unlike the local volatility example in Section 3.1, the volatility skews are very smooth even without iterating the reference values.

3.3. VIX/SPX joint calibration

Since it was first reported in [9], the joint calibration on SPX and VIX has been known to be a challenging problem. More specifically, we want to build a stochastic volatility model that could be jointly calibrated to the options and futures of SPX and VIX. We refer the reader to [14] for a comprehensive discussion of the literature and a martingale optimal transport approach with a discrete-time model. In this paper, we introduce the work of [11] in which the OT framework was applied to solve the joint calibration problem.

Consider probability measures under which are two-dimensional -semimartingales. We want to be the logarithm of the SPX price that takes the form of

| (16) |

For such , we then use (or when emphasising the dependence on ) to represent a half of the expectation of the forward quadratic variation of on observed at time , that is

| (17) |

Note that the the second term on the right-hand side of (17) is a martingale. It follows that the modelling setting we just described is captured by probability measures characterised by such that

| (18) |

where and and with the additional property that -a.s.

In order to restrict the probability measures to those characterised by of the form (18), we can define a cost function that penalises characteristics that are not in the following convex set:

where is the set of positive semidefinite matrices of order two. Define the convex cost function as follows:

| (21) |

where is a matrix of some reference values for . Note that may depend on as well.

The calibration instruments we consider are SPX European options, VIX options and VIX futures. The market prices of these products can be imposed as constraints on . Let be a vector of number of SPX option (discounted) payoff functions. For example, if the -th option is a put option with a strike , then the payoff function is given by . Let be the market SPX option prices and be the vector of their maturities. The prices can be imposed on by restricting to probability measures that satisfy

Let . The annualised realised variance of the SPX price over a time grid is defined to be

where is an annualisation factor. For example, if corresponds to the daily observation dates, then , and the realised variance is expressed in basis points per annum. As , the realised variance can be approximated by the quadratic variation of , given by

The VIX index at is defined using a synthetic log-payoff option. In our setting, it can be equivalently re-written as the square root of the expected realised variance over the next 30 days (i.e., days), that is

Consider VIX options and futures both with maturity . Let be the market VIX futures price and let be the market VIX option prices. Let be a vector of number of VIX option payoff functions. Similarly to , if the -th VIX option is a put option with a strike , then the payoff function is given by . Let be given by . Then, we want to further restrict to those under which also satisfies the following constraints:

Finally, to ensure that , one additional constraint is imposed on the model. Let be a function such that if and only if . Here, we choose and add constraint . This constraint can be interpreted as a contract that has a payoff at time , and its price is always null. We will call it the singular contract.

We assume that is known, and the initial marginal of is a Dirac measure on . The value of is the logarithm of the current SPX price. In practice, can be inferred if the market prices of SPX call and put options maturing at are available over a continuous spectrum of strikes:

where is the -forward price of the SPX index (e.g., see [6]). If is not observable from the market, we can treat it as a parameter.

Now, to group all constraints together, we define

Then the joint calibration problem can be reformulated as solving

| (22) |

where

Applying the arguments developed in Section 2, we can derive a dual formulation of (22):

where is a solution to the following HJB equation (in the viscosity sense):

with the terminal condition .

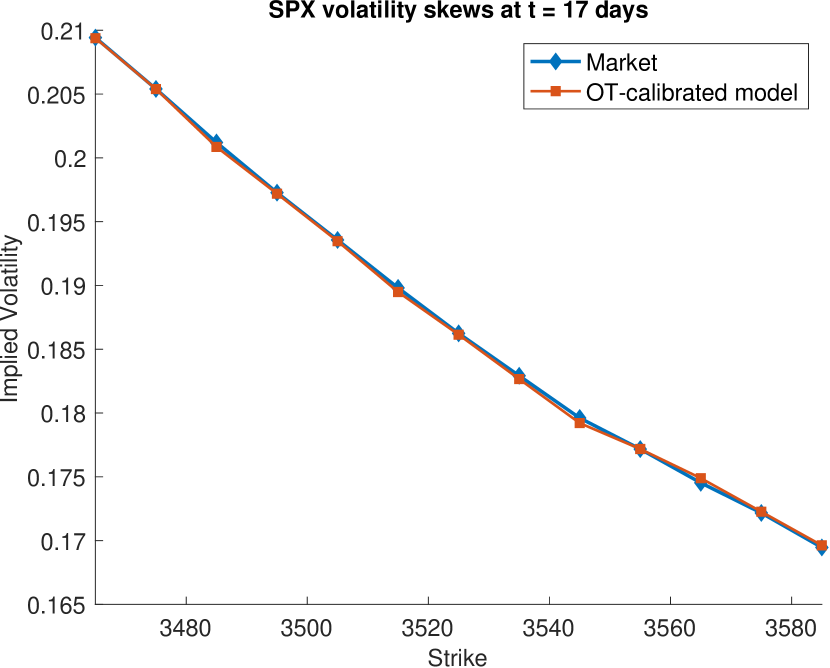

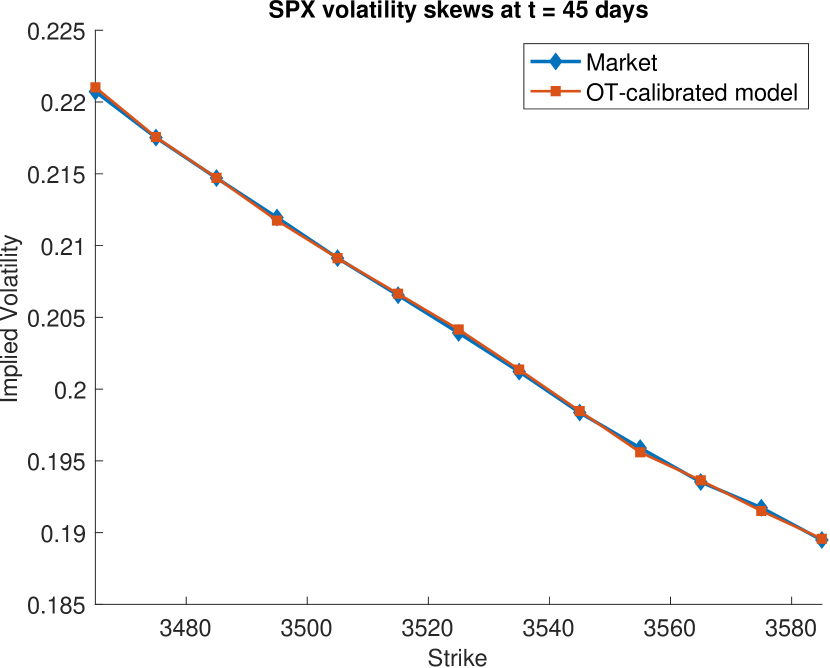

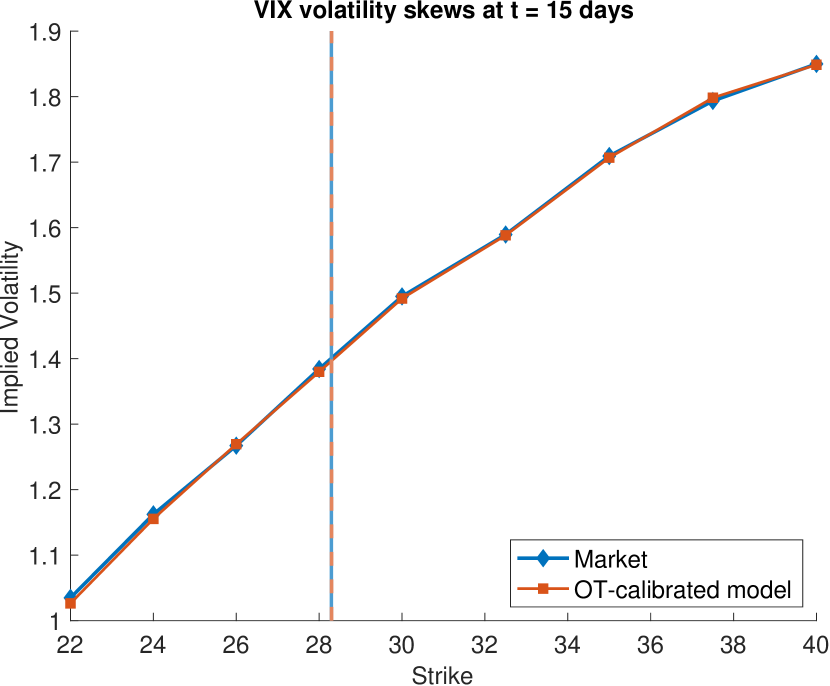

Numerical example

In [11], the process , also called the OT-calibrated model, was calibrated to market data as of September 1st, 2020. The data consists of monthly SPX options maturing at 17 days and 45 days and monthly VIX futures and options maturing at 15 days. We also add the singular contract as a calibrating instrument (i.e., ) to ensure that the additional property , -a.s. is satisfied.

Define and . The in (21) was set to

| (25) |

where . The in (25) was derived by reformulating a standard Heston model in terms of and defined in (16) and (17). The parameters have the usual interpretations as in the Heston model and are obtained by (roughly) calibrating a Heston model to the SPX option prices. The initial position is . In addition, a reference iteration method was used for smoothing the volatility surfaces and skews, which is similar to iterating in the local volatility example presented in Section 3.1. We refer the reader to [11] for more details.

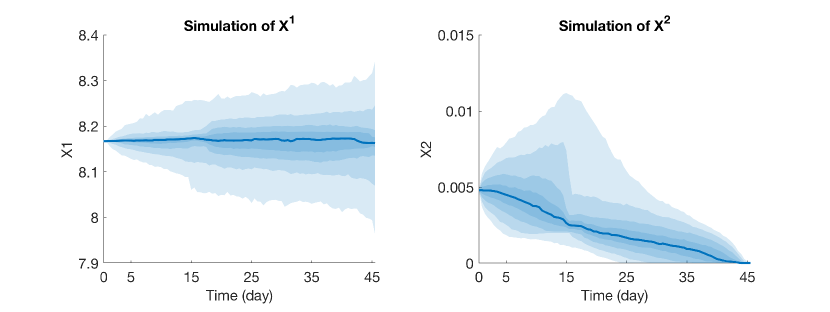

Figure 6 shows the model volatility skews of the OT-calibrated model. The simulation of is given in Figure 7. The results show that the model accurately attains the market prices while keeping the property , -a.s. satisfied.

3.4. Path-dependent volatility calibration

The result of [10] can be applied to the calibration of volatility models to path-dependent options. In [10], a path-dependent model, which has the same form of (7), was first calibrated to European options and then to path-dependent options. The theoretical developments are out of the scope of this paper, so we only highlight the results here.

Consider probability measures , with sufficient regularity, under which takes the form of (7). We also consider the same cost function defined in Section 10, which is (10). If we only consider European options as the calibrating instruments, the path-dependent model recovers a local volatility model, and the calibration problem is equivalent to the one introduced in Section 3.1. When calibrating to path-dependent options, instead of solving the HJB equations (13), one needs to solve a class of path-dependent PDEs (PPDE) which is numerically difficult to solve. By identifying the relevant path-dependent state variables, the infinite dimensional PPDE reduces to a finite dimensional PDE which depends on the spot price as well as the additional path-dependent state variable and can be solved via conventional numerical methods. Here are some examples of relevant state variables:

-

•

European options: the spot price ;

-

•

Asian options: the spot price and the running average ;

-

•

Continuous barrier options: the spot price and the indicator variable for lower barriers or for upper barriers;

-

•

Lookback options: the spot price and either the running minimum or running maximum .

Barrier options

Here, we give an example of barrier options (see [10] for more examples). Formally speaking, a barrier is a closed subset whose complement is a connected region containing . The payoff of a barrier product expiring at time is a function of and the indicator variable , checking whether the path of the underlying has hit the barrier. When calibrating to a collection of barrier products with a single fixed barrier, the required state variables are and . Then the function can be effectively split into two functions, and , corresponding to the cases and , respectively. The dual formulation of the calibration problem is solving

where is the solution to the split PDE

where is the convex conjugate of defined in (10) with respect to the last two variables. Similarly, the optimal volatility will be switching between two local volatilities and , conditional to whether the underlying has hit or not. The PDE for will be used to compute the volatility function prior to the stock hitting the barrier, while the PDE for will be used to compute the volatility function after the barrier has been hit.

Numerical example

As an example, let us consider barrier products with respect to a continuous lower barrier where is a constant. In particular, we will be calibrating to all down-and-in and down-and-out puts with strikes at all the grid points and four different maturities. The left half of Figure 8 shows the calibrated volatility function (before hitting the barrier) and the right half shows (after hitting the barrier). Even though is only defined for , for the purpose of visualisation, we set for . For comparison, the volatility calibrated to only European options with the same strikes and maturities is shown in Figure 9.

References

- [1] Marco Avellaneda, Craig Friedman, Richard Holmes, and Dominick Samperi. Calibrating volatility surfaces via relative-entropy minimization. Appl. Math. Finance, 4(1):37–64, 1997.

- [2] Mathias Beiglböck, Pierre Henry-Labordère, and Friedrich Penkner. Model-independent bounds for option prices—a mass transport approach. Finance and Stochastics, 17(3):477–501, 2013.

- [3] Jean-David Benamou and Yann Brenier. A computational fluid mechanics solution to the Monge–Kantorovich mass transfer problem. Numerische Mathematik, 84(3):375–393, 2000.

- [4] Y. Brenier. Polar factorization and monotone rearrangement of vector-valued functions. Comm. Pure Appl. Math., 44(4):375–417, 1991.

- [5] Gerard Brunick and Steven Shreve. Mimicking an Itô process by a solution of a stochastic differential equation. Annals of Applied Probability, 23(4):1584–1628, 2013.

- [6] Peter Carr and Dileep Madan. Towards a theory of volatility trading. In Robert Jarrow, editor, Volatility, pages 417–27. Risk Publications, 1998.

- [7] Stefano De Marco and Pierre Henry-Labordère. Linking vanillas and VIX options: a constrained martingale optimal transport problem. SIAM Journal on Financial Mathematics, 6(1):1171–1194, 2015.

- [8] Bruno Dupire. Pricing with a smile. Risk Magazine, pages 18–20, 1994.

- [9] Jim Gatheral. Consistent modeling of SPX and VIX options. In Bachelier congress, volume 37, pages 39–51, 2008.

- [10] Ivan Guo and Grégoire Loeper. Path dependent optimal transport and model calibration on exotic derivatives. The Annals of Applied Probability, 31(3):1232–1263, 2021.

- [11] Ivan Guo, Grégoire Loeper, Jan Oblój, and Shiyi Wang. Joint modelling and calibration of SPX and VIX by optimal transport. Available at SSRN 3568998, 2020.

- [12] Ivan Guo, Grégoire Loeper, and Shiyi Wang. Calibration of local-stochastic volatility models by optimal transport. arXiv preprint arXiv:1906.06478, 2019.

- [13] Ivan Guo, Grégoire Loeper, and Shiyi Wang. Local volatility calibration by optimal transport. In 2017 MATRIX annals, volume 2 of MATRIX Book Series, pages 51–64. Springer, Cham, 2019.

- [14] Julien Guyon. The joint S&P 500/VIX smile calibration puzzle solved. Risk, April, 2020.

- [15] Julien Guyon. Dispersion-constrained martingale schrödinger problems and the exact joint S&P 500/VIX smile calibration puzzle. Available at SSRN 3853237, 2021.

- [16] Pierre Henry-Labordère. From (martingale) schrodinger bridges to a new class of Stochastic Volatility Models. arXiv preprint arXiv:1904.04554, 2019.

- [17] Pierre Henry-Labordère and Nizar Touzi. A stochastic control approach to no-arbitrage bounds given marginals, with an application to lookback options. The Annals of Applied Probability, 24(1):312–336, February 2014.

- [18] Mark Jex, Robert Henderson, and David Wang. Pricing exotics under the smile. Risk Magazine, pages 72–75, 1999.

- [19] L. V. Kantorovich. On a problem of Monge (in Russian). Uspekhi Matematicheskikh Nauk, 3:255–226, 1948.

- [20] Gaspard Monge. Mémoire sur la théorie des déblais et des remblais. Histoire de l’Académie Royale des Sciences de Paris, 1781.

- [21] Xiaolu Tan and Nizar Touzi. Optimal transportation under controlled stochastic dynamics. The Annals of Probability, 41(5):3201–3240, 2013.

- [22] Yu Tian, Zili Zhu, Geoffrey Lee, Fima Klebaner, and Kais Hamza. Calibrating and pricing with a stochastic-local volatility model. Journal of Derivatives, 22(3):21, 2015.

- [23] C. Villani. Topics in optimal transportation, volume 58 of Graduate Studies in Mathematics. American Mathematical Society, Providence, RI, 2003.

- [24] C. Villani. Optimal transport: old and new, volume 338 of Grundlehren der Mathematischen Wissenschaften. Springer-Verlag, Berlin, RI, 2009.