lemmatheorem \aliascntresetthelemma \newaliascntassumptiontheorem \aliascntresettheassumption \newaliascntproblemtheorem \aliascntresettheproblem \newaliascntclaimtheorem \aliascntresettheclaim \newaliascntquestiontheorem \aliascntresetthequestion \newaliascntcorollarytheorem \aliascntresetthecorollary \newaliascntconstructiontheorem \aliascntresettheconstruction \newaliascntfacttheorem \aliascntresetthefact \newaliascntpropositiontheorem \aliascntresettheproposition \newaliascntconjecturetheorem \aliascntresettheconjecture \newaliascntdefinitiontheorem \aliascntresetthedefinition \newaliascntremarktheorem \aliascntresettheremark \newaliascntprototheorem \aliascntresettheproto \newaliascntalgotheorem \aliascntresetthealgo \newaliascntexprtheorem \aliascntresettheexpr

A Theoretical Analysis of Fine-tuning with Linear Teachers

Abstract

Fine-tuning is a common practice in deep learning, achieving excellent generalization results on downstream tasks using relatively little training data. Although widely used in practice, it is lacking strong theoretical understanding. Here we analyze the sample complexity of this scheme for regression with linear teachers in several architectures. Intuitively, the success of fine-tuning depends on the similarity between the source tasks and the target task, however measuring this similarity is non trivial. We show that generalization is related to a measure that considers the relation between the source task, target task and covariance structure of the target data. In the setting of linear regression, we show that under realistic settings a substantial sample complexity reduction is plausible when the above measure is low. For deep linear regression, we present a novel result regarding the inductive bias of gradient-based training when the network is initialized with pretrained weights. Using this result we show that the similarity measure for this setting is also affected by the depth of the network. We further present results on shallow ReLU models, and analyze the dependence of sample complexity on source and target tasks in this setting.

1 Introduction

In recent years fine-tuning has emerged as an effective approach to learning tasks with relatively little labeled data. In this setting, a model is first trained on a source task where much data is available (e.g., masked language modeling for BERT), and then it is further tuned using gradient descent methods on labeled data of a target task [1, 2, 3, 4]. Furthermore, it has been observed that fine-tuning can outperform the strategy of fixing the representation learned on the source task, mainly in natural language processing [1, 5]. Despite its empirical success, fine-tuning is poorly understood from a theoretical perspective. One apparent conundrum is that fine-tuned models can be much larger than the number of target training points, resulting in a heavily overparameterized model that is prone to overfitting and poor generalization. Thus, the answer must lie in the fact that fine-tuning is performed with gradient descent and not an arbitrary algorithm that could potentially “ignore” the source task [6]. Here we set out to formalize this problem and understand the factors that determine whether fine-tuning will succeed. We note that this question can be viewed as part of the general quest to understand the implicit bias of gradient based methods [6, 7, 8, 9, 10, 11, 12, 13], but in the particular context of fine-tuning.

We begin by highlighting the obvious link between fine-tuning and initialization. Namely, the only difference between “standard” training of a target task and fine-tuning on it, is the initial value of the model weights before beginning the gradient updates. Our goal is to understand the interplay between the model parameters at initialization (namely the source task), the target distribution, and the accuracy of the fine-tuned model. A natural hypothesis is that the distance between the pretrained and fine-tuned model weights is what governs the success of fine-tuning. Indeed, some argue that this is both the key to bound the generalization error of a model and the implicit regularization of gradient-based methods [14, 15, 16, 17]. However, this approach has been discouraged both by empirical testing of the generalization bounds inspired by it [18] and by theoretical works showing this cannot be the inductive bias in deep neural networks [19]. Our results further establish the hypothesis that the success of fine-tuning is affected by other factors.

In this paper we focus on the case in which both source and target regression tasks are linear functions of the input. We start by considering one layer linear networks, and derive novel sample complexity results for fine-tuning. We then proceed to the more complex case of deep linear networks, and prove a novel result characterizing the fine-tuned model as a function of both the weights after pretraining and the depth of the network, and use it to derive corresponding generalization results.

Our results provide several surprising insights. First, we show that the covariance structure of the target data has a significant effect on the success of fine-tuning. In particular, sample complexity is affected by the degree of alignment between the source-target weight difference and the eigenvectors of the target covariance. Second, we find a strong connection between the depth of the network and the results of the fine-tuning process, since deeper networks will serve to cancel the effect of scale differences between source and target tasks. Our results are corroborated by empirical evaluations.

We conclude with results on ReLU networks, providing the first sample complexity result for fine-tuning. For the case of linear teachers, this asserts a simple connection between the source and target models and the test error of fine-tuning.

Taken together, our results demonstrate that fine-tuning is affected not only by some notion of distance between the source and target tasks, but also by the target covariance and the architecture of the model. These results can potentially lead to improved accuracy in this setting via appropriate design of the tasks used for pretraining and the choice of the model architecture.

2 Related work

Empirical work [20] has shown that two instances of models initialized from pre-trained weights are more similar in features space than those initialized randomly. Other works [21, 22, 23] have shown that fine-tuned models generalize well when the representation used by the target task is similar to the one used by the source tasks.

In linear regression, [24] showed that gradient descent finds the solution with minimal distance to the initial weights. More recently, attention has turned towards the phenomenon of “benign overfitting” [25, 26] in high dimensional linear regression, where despite fitting noise in training data, population risk may be low. Theoretical analysis of this setting [25] studied how it is affected by the data covariance structure. Benign overfitting was also recently analyzed in the context of ridge-regression [27] and online stochastic gradient descent [28]. Our work continues this line of work on high dimensional regression, but differs from the above papers as we start from a source task, then train on a fixed training set from a target task and consider the global optimum of the this training loss (unlike online SGD). Furthermore, we go beyond the linear regression framework, and obtain surprising characteristics of fine-tuning in deep linear networks.

For linear regression with deep linear models, [29] have recently shown an implicit bias for a two-layer network with deterministic initialization, and [30] have shown an implicit bias for a network with arbitrary depth and near-zero random initialization. Our work generalizes the inductive bias found by [29] to a network of arbitrary depth, and analyses the generalization error of such networks for infinite depth. For linear regression with shallow linear networks [31] have shown a generalization bound that depends only on the norm of the target task, which we use in Section 6.

3 Preliminaries and settings

Notations

Let be the norm for vectors and the spectral norm for matrices. For a vector we denote . For a matrix and some , we define to be the matrix containing the first columns of . Similarly, we let denote the matrix containing the columns from to in .

Let be a distribution over . Let be the covariance matrix of and let be its eigenvalue decomposition such that . We define the projection matrices:

projecting onto the span of the top eigenvectors of , onto the span of the bottom eigenvectors of , respectively. We will refer to the former as the “top- span” of , and to the latter as the “bottom- span” of .

Let be the row matrix of samples drawn from , and denote the empirical covariance matrix by . Define to be the projection matrix into the row space of , and to be the projection matrix into its orthogonal complement, i.e.:

Consider a set of parameters , and let denote the set of parameters at time . We denote the output of a model whose weights are on a vector by . In the different sections of this work we will overload with different architectures.

We consider the problem of fine-tuning based transfer learning in regression tasks with linear teachers. Let be the ground-truth parameters of the target task, i.e. the linear teacher which we wish to learn, and be the target labels of , s.t. .

We define to be the empirical MSE loss on and define as the population loss:

We separate the training procedure into two parts. In the first “pretraining” part, we train a model on pretraining samples labeled by a linear teacher (i.e., ), resulting in the set of model weights . In the second part, which we call fine-tuning, we initialize a model with the pretrained weights and learn the target task by optimizing .

Optimization is done by either gradient descent (GD) or gradient flow (GF). Let be some weight vector or weight matrix in . The dynamics for gradient descent optimization with some learning rate are , and the dynamics for gradient flow are . Next we state several assumptions about our setup.

Assumption \theassumption.

is non-singular. i.e. the rows of are linearly-independent.

This assumption holds with high probability for, e.g., a continuous distribution with support over a non-zero measure set. This assumption is only used for simplicity, as the high probability can be incorporated into the analysis.

Assumption \theassumption (Perfect pretraining).

The pretraining optimization process learns the linear teacher perfectly, e.g. for linear regression we assume that , for .

Notice that for linear and deep linear models, perfect pretraining can be achieved when . Our results can be easily extended to the case where the equality holds approximately and with high probability, but for simplicity we assume equality.

Assumption \theassumption (Zero train loss).

The fine-tuning converges, i.e.

4 Analyzing fine-tuning in linear regression

In this section we analyze fine-tuning for the case of linear teachers for linear regression when using gradient descent for optimization. We define and overload . In what follows we denote the parameter learned in the fine-tuning process by .

4.1 Results

The following known results (e.g., [24, 25, 10]) show the inductive bias of gradient descent with non-zero initialization in under-determined linear regression and the corresponding population loss.

Theorem 4.1.

Theorem 4.1 provides two interesting observations: the first is that consists of two parts, one which is the projection of the initial weights into the null space of , and the other which is the projection of into the span of . The second observation is that the population risk depends solely on the difference that is projected to the null space of the data. For completeness, the proof of Theorem 4.1 is given in the supplementary.

Theorem 4.1 depends on the data matrix (via ). However, to better understand the properties of fine-tuning, a high probability bound on that does not depend on is desirable. We provide such a bound, highlighting the dependence of the population risk on the source and target tasks, and the target covariance .

Theorem 4.2.

Assume the conditions of Theorem 4.1 hold, and assume that the rows of are i.i.d. subgaussian centered random vectors. Then, there exists a constant , such that, for all , and for all such that , with probability at least over , the population risk is bounded by:

| (3) |

where and .

In the proof, we address the randomness of in (2), by decomposing into its top- span and bottom- span components, and then applying the Davis-Kahan sin() theorem [33] to bound the norm of the projection of the former to the null space of the data. The full proof is given in the supp.

The bound in Theorem 4.2 has two key components. The first is the function that captures how well the covariance is estimated, and shows the dependence of the bound on the number of train samples used (as it depends on ). The second relates to the two matrix norms of with respect to different parts of the covariance . Notice that the term relating to the top-k span decreases like , while the term relating to bottom-k span decreases like .

This theorem highlights the conditions under which fine-tuning is expected to perform well. For small enough s.t. , the bound mainly depends on . In this case, the bound will be low if and are close in the span of the top eigenvectors of the target distribution. On the other hand, for large enough s.t. , the bound mainly depends on . Thus, the bound will be low if and are close in the span of the bottom eigenvectors of the target distribution.

We conclude with a remark regarding the integer appearing in the bound, in the case where . While finding the exact that minimizes the bound is not straightforward, the trade-off in selecting it suggests taking the largest which holds . This will “cover” more of without greatly increasing the left part of (3).

4.2 Experiments

In Figure 1 we empirically verify the conclusions from the bound in (3). We set and design the target covariance s.t. the first eigenvalues are significantly larger than the rest (1.5 vs. 0.3). We then consider two settings for . In the first, which we call “Top Eigen Align”, we select and such that . In the second which we call “Bottom Eigen Align” we set . In both settings we use the same norm , to show that the bound is not affected by this norm.

As discussed above, our bound suggests better generalization performance of “Bottom Eigen Align” for large and better performance of “Top Eigen Align” for small . Indeed, we see that while for very few samples “Top Eigen Align” has a lower population loss than “Bottom Eigen Align”, the population loss of ”Bottom Eigen Align” drops significantly as grows, and drops to zero well before .

We next evaluate the bound on fine-tuning tasks taken from the MNIST dataset [34], and compare it to alternative bounds. Specifically, since we do not expect bounds to be numerically accurate, we calculate the correlation between the actual risk in the experiment and the risk predicted by the bounds. The task we consider (both source and target) is binary classification, which we model as regression to outputs . We generate source-target task pairs (e.g., source task is label vs label and target tasks is label vs label ). For each such pair we perform source training followed by fine-tuning to target. We then record both the 0-1 error on an independent test set and the value predicted by the bounds. This way we obtain pairs of points (i.e., actual error vs bound), and calculate the for these pairs, indicating the level to which the bound agrees with the actual error. In addition to our bound in (3), we consider the following: the norm of source-target difference and a bound adapted from [25] to the case of fine-tuning.111The adaptation is straightforward: since the population loss for non-random initialization depends on instead of , we can replace the ground-truth expression in Theorem 4 from [25] with . The results in Table 1 show that there is a strong correlation between our bound and the actual error, and the correlation is weaker for the other bounds.

| Number of Samples | 10 | 15 | 20 | 25 | 30 |

|---|---|---|---|---|---|

| 0.69 0.03 | 0.68 0.04 | 0.66 0.04 | 0.64 0.03 | 0.62 0.02 | |

| Bound from [25] | 0.73 0.03 | 0.75 0.03 | 0.74 0.03 | 0.71 0.02 | 0.67 0.02 |

| Ours for | 0.86 0.02 | 0.89 0.02 | 0.84 0.02 | 0.75 0.01 | 0.69 0.02 |

5 Analyzing fine-tuning in deep linear networks

In this section we focus on the setting of overparameterized deep linear networks. Although the resulting function is linear in its inputs, like in the previous section, we shall see that the effect of fine-tuning is markedly different. Previous works (e.g. [35, 36]) have shown that linear networks exhibit many interesting properties which make them a good study case towards more complex non-linear networks.

We consider networks with layers, given by the following matrices: s.t. , , and for . We also define:

such that . From Section 3, we have that .

We recall the condition of perfect balancedness (or 0-balancedness) [32]:

Definition \thedefinition.

The weights of a depth deep linear network at time are called 0-balanced if:

| (4) |

Our analysis requires the initial random initialization (prior to pretraining) to be 0-balanced, which can be achieved with a near zero random initialization, as discussed in [32]. We provide three results on the effect of fine-tuning in this setting. The first result shows the inductive bias of fine-tuning a depth deep linear network (Theorem 5.1), which holds for arbitrary and generalizes known results for (Theorem 4.1) and [29]. The second result analyzes the population risk of such a predictor when for certain settings (Theorem 5.2 and Theorem 5.3). The third result shows why fixing the first layer (or any set of layers containing the first layer) after pretraining can harm fine-tuning (Theorem 5.4).

The next theorem characterizes the model learned by fine-tuning in the above setting (it can thus be viewed as the deep-linear version of the result in Theorem 4.1):

Theorem 5.1.

To prove this, we focus on , and notice that the gradients are in the span of , and hence and its norm remain static during the GF optimization ([30]). We then analyze the norm of the fine-tuned model by using the 0-balancedness property of the weights and the min-norm solution to the equivalent linear regression problem, and achieve (5). (6) is achieved by calculating the limit w.r.t. . The proof of Theorem 5.1 is given in the supplementary.

Although the expression in (5) is not a closed form expression for (because appears on the RHS), taking to infinity (6) does result in a closed form expression and demonstrates the effect of increasing model depth. As in (1), we see that the end-to-end equivalent has two components: one which is parallel to the data and one which is orthogonal to it. However, while in (1) the orthogonal component has the original norm of the orthogonal projection of , the expression in (6) offers a re-scaling of the norm of this component by some ratio that also depends on . Presenting this phenomenon for the infinity depth limit might look impractical, but the empirical results given in this section show that the effect of depth is apparent even for models of relatively small depth.

5.1 When Does Depth Help Fine-Tuning?

In this subsection we wish to understand the effect of depth on the population risk of the fine-tuned model. For simplicity we focus on the limit in (6), and denote .

Since the linear network is a linear function of , we can derive an expression for the population risk of the network, similar to (2):

| (7) |

However, since depends on the random matrix , without further assumptions this expression by itself is not enough to understand the behaviour of . Theorem 5.2 and Theorem 5.3 analyze cases for which a bound on (7) can be achieved, showing that it depends on , i.e. the product of the norm of and the difference of the normalized and , compared to (2) which depends on the difference between the un-normalized vectors. This observation further highlights the fact that the distance between source and target vectors is not a good predictor of fine-tuning accuracy for some architectures, as fine-tuning can still succeed even if the source and target are very far as long as they are aligned.

We formalize this in the following result, where is identical to in direction, but not in norm.

Theorem 5.2.

Assume that the conditions of Theorem 5.1 hold, and that . Namely:

then for the risk of the end-to-end solution is

while for the solution , the risk is:

| (8) |

This setting highlights our conclusion on the role of alignment in deep linear models: if the tasks are aligned, the deep linear predictor achieves zero generalization even with a single sample, while the population risk of the predictor still depends on .

Another example for this behaviour can be seen when is i.i.d Gaussian (i.e., ).

Theorem 5.3.

Assume that the conditions of Theorem 5.1 hold, and let . Suppose , then there exists a constant such that for any with probability at least the population risk for the end-to-end predictor is bounded as follows:

| (9) |

for . For the linear regression solution this risk is bounded by

| (10) |

The above result is a direct analysis of (7) when by using Lemma 5.3.2 from [37] to analyze the effects of . Comparing (9) and (10), we see that while (10) depends on the distance between the two un-normalized tasks, (9) depends on the norm of the target task and the alignment of the tasks, but not at all on the norm of the source task. The proofs of Theorem 5.2 and Theorem 5.3 are given in the supp.

5.2 Deep linear fine-tuning with fixing the first layer(s)

A common trick when performing fine-tuning is to fix, or “freeze” (i.e. not train), the first layers of a model during the optimization on the target task. This method reduces the risk of over-fitting these layers to the small training set.222This over-fitting is sometimes referred to as “catastrophic forgetting” of the source task. The next theorem shows that for deep linear networks this method degenerates the training process.

Theorem 5.4.

Assume the setting of Theorem 5.1. Then, if we freeze the first layer (or any number of first layers) during fine-tuning, the fine-tuned model will be given by , for some constant .

The key idea in the proof is to show that the product of the first layers is equal to up to a scaling factor, which is a result of [30]. The result implies that after fine-tuning the model is still equal to the source task, independently of the target task. Thus, fine-tuning essentially fails completely, and its error cannot be reduced with additional target data.

This result is achieved under the assumption of -balancedness prior to pretraining, which happens e.g. when initializing the weights with an infinitesimally small variance, as this property leads to the degeneracy of the output of the frozen k-layers. Though the proof of Theorem 5.4 depends on this -balancedness property of the network, the experiments shown in Figure 3 were conducted with a small initialization scale, that is not guaranteed to result in -balancedness, but rather in -approximate balancedness [32] when is small. These experiments show empirically that the phenomenon of learning failure is observed even when . Intuitively, this is because the effective rank of the weight matrices is close to one, and thus learning the second layer is an ill-conditioned problem, which leads to slower convergence and can prevent the model from fine-tuning on the target data with a constant gradient step.

A possible workaround to this failure of learning would be to initialize the weights prior to pretraining with a larger scale of initialization (e.g. with Xavier [38]), thus increasing the rank of each layer and preventing degeneracy. Pre-training with multiple source tasks (as suggested in e.g. [22]) may also help the fine-tuning optimization.

5.3 Experiments

We next describe experiments that support the results in this section. Theorem 5.2 predicts that deeper nets will successfully learn a case where source and target vectors are aligned, but with different norms. This is demonstrated in Figure 2(a) where source and target tasks are related via , where is a standard Gaussian vector whose norm is approximately . It can be seen that when , there is no difference between models of different depth. However, as increases, adding depth has a positive effect on fine-tuning accuracy. Theorem 5.3 predicts that the test loss for a deep linear model would depend only on the alignment of and (i.e. and on the , but not on . This is demonstrated in Figure 2(b) where source and target task are initialized s.t. . In each experiment, either or , where is the “Scaling Factor”, and the other has norm of 1. It can be seen that increasing the norm of the target vector harms generalization much more than increasing the norm of the source vector, as the theorem predicts, even for a relatively shallow model.

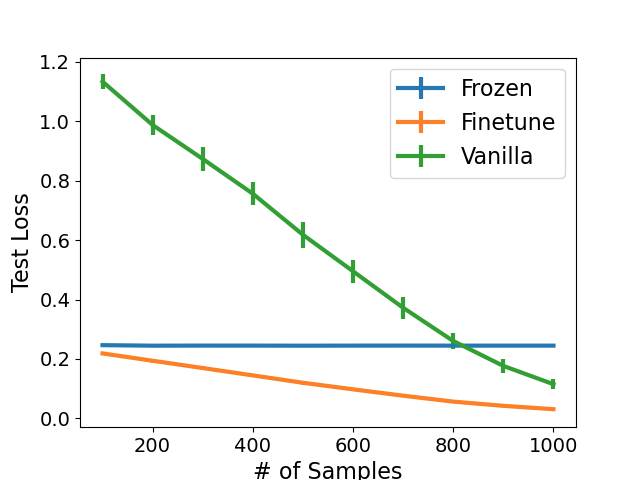

Theorem 5.4 states that fixing the first layer in deep linear nets can result in failure to fine-tune. We illustrate this empirically in Figure 3, where we compare three two-layer linear models on the same target task: 1) A “Frozen” model that fixes the first layer after pretraining. 2) A “Vanilla” model that trains the network from scratch on the target, ignoring the source pre-training. 3) A “Finetune” model that first trains on source and fine-tunes to target. As predicted by theory, the ”frozen” model’s performance is poor, and fine-tuning has better sample complexity.

6 Analyzing fine-tuning in shallow ReLU networks

Analyzing optimization and generalization in non-linear networks is challenging. However, analysis in the Neural Tangent Kernel (NTK) regime is sometimes simpler [39, 31]. Thus, here we take a first step towards understanding fine-tuning in non-linear networks by analyzing this problem in the NTK regime. Specifically, we consider the setting of a two-layer ReLU network with neurons in the hidden layer. Hence, we consider and where is the ReLU function, , the rows of , are vectors in the first layer, and is the vector of weights in the second layer. We initialize uniformly and fix it during optimization as in [39]. Before pretraining, the first layer parameters are initialized from a standard Gaussian with variance . We also assume that for all samples from . We let be the vector of predictions of on the data .

For the next theorem we do not assume linear teachers, and instead assume an arbitrary labeling function such that , for the pretraining data and labels, respectively. We also assume that for some arbitrary function . For simplicity, we assume for . We consider a setting where the pretraining phase is done using a two-layer network in the NTK regime, under the assumptions of Theorem 4.1 from [31] with respect to the variables , , and sufficiently many iterations.333See the supp for a bound on the number of iterations. Next, in the fine-tuning phase, we train a network initialized with the weights given by the pretraining phase. We use the same value of for the fine-tuning phase. We rely on the analysis given in [39, 31] and achieve an upper bound on the population risk of the fine-tuned model:

Theorem 6.1.

Fix a failure probability . We assume that Section 3 holds. Suppose , . Consider any loss function that is -Lipschitz in the first argument such that . Then with probability at least ,444Over the random initialization of the pretraining network. the two-layer neural network fine-tuned by GD for iterations has population loss:

| (11) |

for .

The above result shows that the true risk of the fine-tuned model is related to the distance of learned outputs from the outputs after pretraining . The proof of Theorem 6.1 is given in the supp.

As in previous NTK regime analyses, this result holds when the weights of the fine-tuned model do not “move” too far away from the weights at random initialization. Thus, the proof approach is to bound the distance between the Gram matrix and the infinite-width gram matrix with a decreasing function in . The main challenge is that the weights are not initialized i.i.d as described above. To address this we provide a careful analysis of the dynamics and show that is close to at random initialization, even when considering the pretraining phase, which in turn is close to .

We next apply our results to the case of linear source and target tasks. We thus assume that are linear functions with parameters . For simplicity of exposition we assume exactly (Assumption 3). Before bounding the risk of fine-tuning we bound the RHS of (11) in the linear case:

Corollary \thecorollary.

Suppose that , , and assume Assumption 3 holds. Then,

This is a direct corollary of Theorem 6.1 from [31] on defined above. Theorem 6.1 and Section 6 result in the a bound on the risk of the fine-tuned model:

Corollary \thecorollary.

Under the conditions of Theorem 6.1 and Section 6, it holds that

We note that fine-tuning is improved as the distance between source and target decreases. In our analysis of linear networks (Theorem 4.2 and Theorem 5.3) we obtained a more fine-grained result depending on the covariance structure. We conjecture that the non-linear case will have similar results, which will likely involve the covariance structure in the NTK feature space.

7 Discussion

This paper gives a fine-grained analysis of the process of fine-tuning with linear teachers in several different architectures. It offers insights into the inductive bias of gradient-descent and the implied relation between the source task, the target task and the target covariance that is needed for this process to succeed. We believe our conclusions pave a way towards understanding why some pretrained models work better than others and what biases are transferred from those models during fine-tuning.

A limitation of our work is the simplicity of the models analyzed, and it would certainly be interesting to extend these. Our setting deals only with linear teachers, and assumes the label noise to be zero. Furthermore, we only show upper bounds on the population risk, and not matching lower bounds. For deep linear networks we assume a certain initialization which is less standard than normalized initializers such as Xavier. For non-linear models, we analyze the simple model of a shallow ReLU network, and only in the NTK regime.

An interesting direction to explore is formulating a bound similar to Theorem 4.2 for regression in the RKHS space given by the NTK, where the covariance is now over the RKHS space and thus more challenging to analyze. Another interesting setting is classification with exponential losses. Since the classifier learned by GD in this case has diverging norm, it is not clear how fine-tuning is beneficial, although in practice it often is. We leave these questions for future work.

Acknowledgments and Disclosure of Funding

This work has been supported by the Israeli Science Foundation research grant 1186/18 and the Yandex Initiative for Machine Learning. AB is supported by the Google Doctoral Fellowship in Machine Learning.

References

- [1] Jacob Devlin, Ming-Wei Chang, Kenton Lee, and Kristina Toutanova. Bert: Pre-training of deep bidirectional transformers for language understanding. In Proceedings of the 2019 Conference of the North American Chapter of the Association for Computational Linguistics: Human Language Technologies, Volume 1 (Long and Short Papers), pages 4171–4186, 2019.

- [2] Kenton Lee, Ming-Wei Chang, and Kristina Toutanova. Latent retrieval for weakly supervised open domain question answering. In Proceedings of the 57th Annual Meeting of the Association for Computational Linguistics, pages 6086–6096, 2019.

- [3] Mor Geva, Ankit Gupta, and Jonathan Berant. Injecting numerical reasoning skills into language models. In Proceedings of the 58th Annual Meeting of the Association for Computational Linguistics, pages 946–958, 2020.

- [4] Suchin Gururangan, Ana Marasović, Swabha Swayamdipta, Kyle Lo, Iz Beltagy, Doug Downey, and Noah A Smith. Don’t stop pretraining: Adapt language models to domains and tasks. In Proceedings of the 58th Annual Meeting of the Association for Computational Linguistics, pages 8342–8360, 2020.

- [5] Matthew E Peters, Sebastian Ruder, and Noah A Smith. To tune or not to tune? adapting pretrained representations to diverse tasks. In Proceedings of the 4th Workshop on Representation Learning for NLP (RepL4NLP-2019), pages 7–14, 2019.

- [6] Chiyuan Zhang, Samy Bengio, Moritz Hardt, Benjamin Recht, and Oriol Vinyals. Understanding deep learning requires rethinking generalization. In 5th International Conference on Learning Representations, ICLR 2017, Toulon, France, April 24-26, 2017, Conference Track Proceedings. OpenReview.net, 2017.

- [7] Kaifeng Lyu and Jian Li. Gradient descent maximizes the margin of homogeneous neural networks. In International Conference on Learning Representations, 2019.

- [8] Blake Woodworth, Suriya Gunasekar, Jason D Lee, Edward Moroshko, Pedro Savarese, Itay Golan, Daniel Soudry, and Nathan Srebro. Kernel and rich regimes in overparametrized models. In Conference on Learning Theory, pages 3635–3673. PMLR, 2020.

- [9] Lenaic Chizat and Francis Bach. Implicit bias of gradient descent for wide two-layer neural networks trained with the logistic loss. In Conference on Learning Theory, pages 1305–1338. PMLR, 2020.

- [10] Jingfeng Wu, Difan Zou, Vladimir Braverman, and Quanquan Gu. Direction matters: On the implicit bias of stochastic gradient descent with moderate learning rate. In International Conference on Learning Representations, 2021.

- [11] Edward Moroshko, Blake E Woodworth, Suriya Gunasekar, Jason D Lee, Nati Srebro, and Daniel Soudry. Implicit bias in deep linear classification: Initialization scale vs training accuracy. Advances in Neural Information Processing Systems, 33, 2020.

- [12] Sanjeev Arora, Nadav Cohen, Wei Hu, and Yuping Luo. Implicit regularization in deep matrix factorization. Advances in Neural Information Processing Systems, 32, 2019.

- [13] Roei Sarussi, Alon Brutzkus, and Amir Globerson. Towards understanding learning in neural networks with linear teachers. In International Conference on Machine Learning, 2021.

- [14] Vaishnavh Nagarajan and J Zico Kolter. Generalization in deep networks: The role of distance from initialization. arXiv preprint arXiv:1901.01672, 2019.

- [15] Mingchen Li, Mahdi Soltanolkotabi, and Samet Oymak. Gradient descent with early stopping is provably robust to label noise for overparameterized neural networks. In International Conference on Artificial Intelligence and Statistics, pages 4313–4324. PMLR, 2020.

- [16] Behnam Neyshabur, Zhiyuan Li, Srinadh Bhojanapalli, Yann LeCun, and Nathan Srebro. Towards understanding the role of over-parametrization in generalization of neural networks. In International Conference on Learning Representations (ICLR), 2019.

- [17] Gintare Karolina Dziugaite and Daniel M Roy. Computing nonvacuous generalization bounds for deep (stochastic) neural networks with many more parameters than training data. arXiv preprint arXiv:1703.11008, 2017.

- [18] Yiding Jiang, Behnam Neyshabur, Hossein Mobahi, Dilip Krishnan, and Samy Bengio. Fantastic generalization measures and where to find them. arXiv preprint arXiv:1912.02178, 2019.

- [19] Noam Razin and Nadav Cohen. Implicit regularization in deep learning may not be explainable by norms. In Advances in Neural Information Processing Systems (NeurIPS), 2020.

- [20] Behnam Neyshabur, Hanie Sedghi, and Chiyuan Zhang. What is being transferred in transfer learning? arXiv preprint arXiv:2008.11687, 2020.

- [21] Kurtland Chua, Qi Lei, and Jason D Lee. How fine-tuning allows for effective meta-learning. arXiv preprint arXiv:2105.02221, 2021.

- [22] Simon Shaolei Du, Wei Hu, Sham M. Kakade, Jason D. Lee, and Qi Lei. Few-shot learning via learning the representation, provably. In International Conference on Learning Representations, 2021.

- [23] Daniel McNamara and Maria-Florina Balcan. Risk bounds for transferring representations with and without fine-tuning. In International Conference on Machine Learning, pages 2373–2381. PMLR, 2017.

- [24] Suriya Gunasekar, Jason Lee, Daniel Soudry, and Nathan Srebro. Characterizing implicit bias in terms of optimization geometry. In International Conference on Machine Learning, pages 1832–1841. PMLR, 2018.

- [25] Peter L Bartlett, Philip M Long, Gábor Lugosi, and Alexander Tsigler. Benign overfitting in linear regression. Proceedings of the National Academy of Sciences, 117(48):30063–30070, 2020.

- [26] Trevor Hastie, Andrea Montanari, Saharon Rosset, and Ryan J Tibshirani. Surprises in high-dimensional ridgeless least squares interpolation. arXiv preprint arXiv:1903.08560, 2019.

- [27] Alexander Tsigler and Peter L Bartlett. Benign overfitting in ridge regression. arXiv preprint arXiv:2009.14286, 2020.

- [28] Difan Zou, Jingfeng Wu, Vladimir Braverman, Quanquan Gu, and Sham M Kakade. Benign overfitting of constant-stepsize sgd for linear regression. arXiv preprint arXiv:2103.12692, 2021.

- [29] Shahar Azulay, Edward Moroshko, Mor Shpigel Nacson, Blake Woodworth, Nathan Srebro, Amir Globerson, and Daniel Soudry. On the implicit bias of initialization shape: Beyond infinitesimal mirror descent. arXiv preprint arXiv:2102.09769, 2021.

- [30] Chulhee Yun, Shankar Krishnan, and Hossein Mobahi. A unifying view on implicit bias in training linear neural networks. In International Conference on Learning Representations, 2020.

- [31] Sanjeev Arora, Simon Du, Wei Hu, Zhiyuan Li, and Ruosong Wang. Fine-grained analysis of optimization and generalization for overparameterized two-layer neural networks. In International Conference on Machine Learning, pages 322–332. PMLR, 2019.

- [32] Sanjeev Arora, Nadav Cohen, Noah Golowich, and Wei Hu. A convergence analysis of gradient descent for deep linear neural networks. In International Conference on Learning Representations, 2018.

- [33] Chandler Davis and William Morton Kahan. The rotation of eigenvectors by a perturbation. iii. SIAM Journal on Numerical Analysis, 7(1):1–46, 1970.

- [34] Yann LeCun and Corinna Cortes. MNIST handwritten digit database. 2010.

- [35] Sanjeev Arora, Nadav Cohen, and Elad Hazan. On the optimization of deep networks: Implicit acceleration by overparameterization. In International Conference on Machine Learning, pages 244–253. PMLR, 2018.

- [36] Ziwei Ji and Matus Telgarsky. Gradient descent aligns the layers of deep linear networks. In 7th International Conference on Learning Representations, ICLR 2019, 2019.

- [37] Roman Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- [38] Xavier Glorot and Yoshua Bengio. Understanding the difficulty of training deep feedforward neural networks. In Yee Whye Teh and Mike Titterington, editors, Proceedings of the Thirteenth International Conference on Artificial Intelligence and Statistics, volume 9 of Proceedings of Machine Learning Research, pages 249–256, Chia Laguna Resort, Sardinia, Italy, 13–15 May 2010. PMLR.

- [39] Simon S Du, Xiyu Zhai, Barnabas Poczos, and Aarti Singh. Gradient descent provably optimizes over-parameterized neural networks. In International Conference on Learning Representations, 2018.

- [40] Adam Paszke, Sam Gross, Francisco Massa, Adam Lerer, James Bradbury, Gregory Chanan, Trevor Killeen, Zeming Lin, Natalia Gimelshein, Luca Antiga, Alban Desmaison, Andreas Kopf, Edward Yang, Zachary DeVito, Martin Raison, Alykhan Tejani, Sasank Chilamkurthy, Benoit Steiner, Lu Fang, Junjie Bai, and Soumith Chintala. Pytorch: An imperative style, high-performance deep learning library. In H. Wallach, H. Larochelle, A. Beygelzimer, F. d'Alché-Buc, E. Fox, and R. Garnett, editors, Advances in Neural Information Processing Systems 32, pages 8024–8035. Curran Associates, Inc., 2019.

- [41] Charles R. Harris, K. Jarrod Millman, Stéfan J. van der Walt, Ralf Gommers, Pauli Virtanen, David Cournapeau, Eric Wieser, Julian Taylor, Sebastian Berg, Nathaniel J. Smith, Robert Kern, Matti Picus, Stephan Hoyer, Marten H. van Kerkwijk, Matthew Brett, Allan Haldane, Jaime Fernández del Río, Mark Wiebe, Pearu Peterson, Pierre Gérard-Marchant, Kevin Sheppard, Tyler Reddy, Warren Weckesser, Hameer Abbasi, Christoph Gohlke, and Travis E. Oliphant. Array programming with NumPy. Nature, 585(7825):357–362, September 2020.

- [42] Pauli Virtanen, Ralf Gommers, Travis E. Oliphant, Matt Haberland, Tyler Reddy, David Cournapeau, Evgeni Burovski, Pearu Peterson, Warren Weckesser, Jonathan Bright, Stéfan J. van der Walt, Matthew Brett, Joshua Wilson, K. Jarrod Millman, Nikolay Mayorov, Andrew R. J. Nelson, Eric Jones, Robert Kern, Eric Larson, C J Carey, İlhan Polat, Yu Feng, Eric W. Moore, Jake VanderPlas, Denis Laxalde, Josef Perktold, Robert Cimrman, Ian Henriksen, E. A. Quintero, Charles R. Harris, Anne M. Archibald, Antônio H. Ribeiro, Fabian Pedregosa, Paul van Mulbregt, and SciPy 1.0 Contributors. SciPy 1.0: Fundamental Algorithms for Scientific Computing in Python. Nature Methods, 17:261–272, 2020.

- [43] John D. Hunter. Matplotlib: A 2d graphics environment. Computing in Science Engineering, 9(3):90–95, 2007.

- [44] Vladimir Koltchinskii and Karim Lounici. Concentration inequalities and moment bounds for sample covariance operators. Bernoulli, 23(1):110–133, 2017.

- [45] jlewk (https://mathoverflow.net/users/141760/jlewk). Difference between identity and a random projection. MathOverflow. URL:https://mathoverflow.net/q/393720 (version: 2021-05-25).

- [46] Keyulu Xu, Mozhi Zhang, Jingling Li, Simon S Du, Ken-ichi Kawarabayashi, and Stefanie Jegelka. How neural networks extrapolate: From feedforward to graph neural networks. arXiv preprint arXiv:2009.11848, 2020.

Code

Appendix A Proofs for linear regression

This appendix includes proofs for Section 4. It starts by analyzing the solution achieved by applying gradient descent on a linear regression problem with non-zero initialization, and shows its exact population risk. Then, this risk is bounded from above by using concentration bounds to bound various aspects of the difference between the true target covariance and the estimated target covariance.

Recall the assumptions:

Assumption 3.1 (Main Text).

is non-singular. i.e. the rows of are linearly-independent.

Assumption 3.2 (Main Text).

The pretraining optimization process learns the linear teacher perfectly, e.g. for linear regression we assume that , for .

Assumption 3.3 (Main Text).

The fine-tuning converges, i.e.

A.1 Proof of Theorem 4.1

As mentioned in the main text, both parts of the theorem have been proven before [24, 25, 10]. The proof is provided for completeness, and can be skipped.

Lemma \thelemma.

Assume 3.3, and that there exists some vector s.t. (i.e. the data is generated via a linear teacher), then the solution achieved by using GD with initialization in order to minimize:

| (12) |

is

| (13) |

Proof.

First, observe that the gradient step for this problem is

Hence, all of the steps are in the span of , and GD converges to a solution of the form:

for some . The vector must also achieve a loss of zero in Equation 12 (because we know that achieves a loss of zero, and GD minimizes this objective). Therefore:

with (1) due to 3.1.

Replacing with , and by using the definitions of and from Section 3, it follows that

We can now prove the theorem.

Proof of Theorem 4.1 (Main Text).

The proof for Eq.1 in the main text is straightforward by using Section A.1 with and .

As for Eq.2 in the main text, by Section A.1 it follows that

Since it follows that

thus concluding the proof.

A.2 Proof of Theorem 4.2: Upper bound of the population risk for linear regression

Recall the Davis-Kahan theorem:

Theorem A.1 ([33]).

Let and be symmetric matrices with and orthogonal. If the eigenvalues of are contained in an interval , and the eigenvalues of are excluded from the interval for some , then

| (14) |

for any unitarily invariant norm .

The following theorem is a concentration bound on the difference between the true and estimated covariance matrices: :

Theorem A.2 (Theorem 9 from [44]).

Let be i.i.d. weakly square integrable centered random vectors in with covariance operator If is subgaussian and pregaussian, then there exists a constant such that, for all with probability at least

where

The following lemma uses Theorem A.1 to upper bound the dot product between the bottom eigenvectors of the estimated covariance and the top eigenvectors of the target covariance:

Lemma \thelemma.

For all such that it holds that:

Proof.

In order to use Theorem A.1 with to bound , one must show that the conditions of Theorem A.1 are met. Let , , , , , and . Notice that is a rank- matrix, and so is the estimated covariance , hence it bottom eigenvalues are zero. Thus, all of the eigenvalues of equal zero. Also, recall that the eigenvalues of are in descending order. Thus, all of the eigenvalues of are in the interval and all of the eigenvalues of (which equal 0) are excluded from the interval . Hence the conditions of Theorem A.1 are met and for :

with (1) due to Cauchy-Schwartz inequality, (2) due to , being orthonormal matrices, which concludes the proof.

We can now prove the theorem.

Proof of Theorem 4.2 (Main Text).

Let be the singular value decomposition of such that are unitary matrices and let be the -th column of .

First, notice that can be also written as :

Where (1),(3),(4) are due to , being unitary, and (2) is due to .

From Eq.2 in the main text it follows that:

Then:

| (15) |

where the last inequality is due to the Cauchy-Schwartz inequality.

The next step in the proof is to bound . We start by bounding by decomposing to its top- span component and bottom- span component. First notice that since , , we can write :

| (16) |

Where the last inequality is due to Cauchy Schwartz for matrix-vector. The last step in the proof is to bound by using Section A.2 , and bound by 1 as follows:

due to and being orthonormal matrices and because spectral norm is sub-multiplicative.

To conclude the proof we apply Theorem A.2 from [44] to provide a high probability bound for , as was done in [25].

Appendix B Proofs for deep linear networks

In this section we analyze the solution achieved by applying gradient flow optimization to fine-tuning a deep linear regression task (i.e. a regression task using a deep linear network as the regression model).

Our results show that the population risk of a fine-tuned deep linear model depends not only on the source and target tasks and the target covariance, as was shown in the previous section, but also on the depth of the model. We show that as the depth of the model goes to infinity, its population risk depends on the difference between the directions of the source and target task (i.e. the difference between their normalized vectors), instead on the difference between the un-normalized task vectors.

In Section B.2 this is shown by analysing two settings where this effect is most pronounced: one where we make an assumption on the target task (but not on the target covariance), and one where we make an assumption on the target covariance (but not on the target task).

We conclude in Section B.3 by showing that fine-tuning only some of the layers can lead to failure to learn.

We begin by recalling some definitions. An -layer linear fully-connected network is defined as

where for (we use ) and . Thus, the linear network is equivalent to a linear function with weights .

The weights of a deep linear network are called 0-balanced (or perfectly balanced) at time if:

| (17) |

B.1 Proof of Theorem 5.2: The inductive bias of deep linear network fine-tuning

For this section, let , and denote the top left singular vector, top right singular vector and top singular value of the weights , respectively. Define as the end of pretraining.

Before proving the theorem, we state several useful lemmas.

Lemma \thelemma.

Assume that at time the weights are 0-balanced. Then ,

| (18) |

and:

| (19) |

Proof for Section B.1.

This proof is a similar to the proof of Theorem 1 in [35]. Focusing on balancedness implies that:

Hence, is (at most) rank-1 and so is . By iterating from to , it follows that is rank-1 for .

Consider the SVD of the weights at time . Since all weights are rank-1, they can be decomposed such that

Plugging this into (17) it follows that

Thus proving (18) and showing that the top singular values of all the layers in time are equal to each other.555maybe add in footnote that because the two matrices have the same SVD, their spectra are equal.

We now consider the norm of the end to end solution at time , :

Since all of the top singular values at time equal each other, and by construction, the result follows.

The following Lemma is also used in the analysis:

Lemma \thelemma (Theorem 1 from [35]).

Suppose a deep linear network is optimized using GF, starting from a 0-balanced initialization, i.e. initialization in which weights are 0-balanced. Then the weights stay balanced throughout optimization.

We are now ready to prove the theorem.

Proof of Theorem 5.2.

First consider the pretraining of the model under 3.2. Assume that before the pretraining, the model weights are perfectly balanced. From Section B.1 it follows that after pretraining on the source task, i.e. at , the weights of the model are still balanced. From Section B.1, this means they are also rank-1. From 3.2:

and since this implies:

| (20) |

Section B.1 gives us that:

Hence:

and

| (21) |

Hence:

| (22) |

We next analyze the fine-tuning dynamics. Section B.1 ensures that if the pretrained model has 0-balanced weights, then the weights will remain 0-balanced during finetune. This implies that Section B.1 holds for all .

Observe the gradient flow dynamics of the layers during fine-tuning:

where is the residual vector satisfying .

From Section B.1:

Using (18) and (19) it follows that :

For ,

| (23) |

Where the last equality is due to (18). Hence is always a rank-1 matrix whose columns are in the row space of . This implies that the decomposition into two orthogonal components and so that and yields that it follows that

Hence, does not change for all . Using (22) it follows:

| (24) | ||||

| (25) |

The next lemma states that does not change during optimization if .

Lemma \thelemma.

Suppose we run GF over a deep linear network starting from 0-balanced initialization. Also assume that at initialization is rank-1 and:

Then for all :

Proof.

Assume towards contradiction that there exists s.t. .

From being rank-1 (Section B.1), it follows that

And from the decomposition of to and , (24) and being rank-1 it follows that:

Hence:

From (23) we see that the orthogonal part of does not change during fine-tune:

hence:

| (26) |

Since , and because non-degenerate singular values always have unique left and right singular vectors (up to a sign), only if:

by contradiction to the assumption that , or if and , which contradicts (26).

In the case where , since , it follows that , which is similar to the case in [30], for which the solution is known to be . Also, from (25), this implies , and the expression for the end-to-end solution in Eq.5 in the main text holds.

The analysis continues for . By using Section B.1 and Section B.1 it follows that:

| (27) |

With (1) due to (24), (2) due to (25), (3) due to Section B.1 and (4) due to Section B.1. From the requirement of 3.3 that , it follows that:

| (28) |

Which is the only solution for this equation in the span of , and due to 3.1.

Eq.5 in the main text follows from (27) and (28):

| (29) |

To prove Eq.6 from the main text, consider the norm of .

At the limit we get:

Thus:

And it follows that at this limit:

| (30) |

From the same lines of proof as in Section A.1 it follows that

Corollary \thecorollary.

For the conditions in Theorem 5.2 in the main text,

B.2 Proofs of Theorems 5.3 and 5.4: How does depth affect the population risk?

Section B.1 above contains dependence on which is a random variable. We next provide high-probability risk bounds that can be derived from this result. The bounds are obtained under slightly different assumptions, either on the target task or on the target distribution, but both highlight the fact that fine-tuning in the case will depend on rather than the un-normalized .

Recall the definition of the fine-tuning solution as :

In the first setting we will assume that is a scaled version of , without any assumptions on . Theorem 5.3 from the main text demonstrates a gap between perfect fine-tuning for the case and non-zero fine-tuning error for .

Proof of Theorem 5.3 (Main Text).

First notice:

| (31) |

which from Eq.6 in the main text gives the solution

On the other hand, for the solution it follows from Eq.2 in the main text that

which is greater than zero for all .

In the second setting we assume that , without any assumptions on . Here it shows that while the population risk of the solution depends on , the population risk of the infinitely-deep linear solution depends on the normalized and , i.e. on the alignment of and and the norm of .

Theorem 5.4 (Main Text).

Assume that the conditions of Theorem 5.2 hold, and let . Suppose , then there exists a constant such that for an it holds that with probability at least the population risk for the end-to-end is bounded:

| (32) |

for . For the linear regression solution this risk is bounded by

Proof of Theorem 5.5 (Main Text).

We start by analyzing :

where (1) is due to from the definition of the distribution of . We then bound the RHS with:

We see that we can bound the expression on the left:

Let be the projection matrix onto the row space of , then from [45], is a projection onto a random -dimensional subspace uniformly distributed in the Grassmannian , and is a projection onto a random -dimensional subspace uniformly distributed in the Grassmannian .

According to Lemma 5.3.2 in [37], with probability at least

which bounds:

Again, by applying Lemma 5.3.2 from [37], with probability at least

Thus the following bound is obtained:

Define , which concludes the proof for the infinite depth case.

Now for the upper bound of the population risk of the solution . Look at Eq.2, and from being a random projection, it follows that with probability at least :

B.3 Proof of Theorem 5.5: The effect of fixing layers during fine-tuning

Proof.

Since we assume that the weights before pretraining are 0-balanced, it follows from Section B.1 and Section B.1 that all layers are rank-1. From 3.2 it follows that at the end of pretraining , and from (22) it follows that .

Consider the setting where the first layers are fixed. It follows that

Then from Section B.1 it follows that for and for any :

Let’s define

then for any constant it follows :

By setting we conclude the proof.

Appendix C Proofs for the shallow ReLU section

This section shows that fine-tuning from a shallow ReLU model pretrained on has sample complexity depending on , compared to training from a random initialization which depends on .

We would like to adapt the results from [31] to the case of fine-tuning in the NTK regime, where we can take better advantage of the fact that the bound in Theorem 4.1 in [31] fundamentally depends on , thus enabling us to bound the distance of each weight from by using instead of for our case, where is known.

The proof scheme is as follows:

-

1.

First we show that , thus ensuring we are indeed in the NTK regime for bounded from bellow as in Theorem 6.1 from the main text.

-

2.

Then, we can use an adaption of Theorem 4.1 from [31] to bound the distance of each weight .

-

3.

Since is fixed, we can use the Rademacher bound in Theorem 5.1 from [31] with instead of to obtain a bound that depends on instead of .

-

4.

For , we can use Corollary 6.2 from [31] with to obtain the generalization error using the Rademacher bound above.

C.1 Staying in the NTK regime

Start with the first item: showing that . This is done by bounding the distance each travels during both the pretraining and fine-tuning optimization, which is achievable by using Theorem 4.1 from [39] ”as is” for the pretraining part, and adapting it to the fine-tuning part.

Assumptions

For brevity, we assume for the pretraining data that for all . Also assume the following for all results:

Assumption \theassumption.

We assume that , i.e. the weights at , were i.i.d. initialized , for .

Also assume for :

Assumption \theassumption.

Define matrix with

We assume , and for being the NTK gram matrix of the pretraining data .

The assumption that is justified by combining 3.1 and Theorem 3.1 from [39]. The assumption that , which is actually the assumption for Theorem C.1, holds for most real-data data-sets and w.h.p for most real-life distributions, as discussed in [39].

Assumption \theassumption.

We assume that , and , .

We now restate a few results from [39] which are applied directly for the part of pretraining:

Theorem C.1 (Theorem 3.1 from [39]).

If for any , , then .

Theorem C.2 (Theorem 3.3 from [39] for pretraining).

Assume Section C.1, Section C.1 and Section C.1 hold, then with probability at least over the random initialization at time , we have:

Lemma \thelemma (Lemma C.1 from [31]).

Assume Section C.1, Section C.1 and Section C.1 hold, then there exists such that with probability at least over the random initialization at time we have

Plugging Theorem C.2 into Section C.1 we get:

Corollary \thecorollary.

Assume Section C.1, Section C.1 and Section C.1 hold, then there exists s.t. with probability at least over the random initialization at time we have

Lemma \thelemma (Lemma 3.2 from [39]).

If at are i.i.d. generated from , then with probability at least , the following holds. For any set of weight vectors that satisfy for any , for some small positive constants , then the matrix defined by

satisfies and .

We state the following lemmas that is used in the analysis:

Lemma \thelemma (Similar to Lemma C.2 from [31]).

Assume Section C.1 holds. For some we define:

| (33) |

then with probability at least on the initialization of we get:

and:

where the expectation is with respect to .

Proof.

Since has the same distribution as we have

Then we know . Due to Markov, with probability at least we have:

We now state our equivalent for Theorem 4.1 from [39] :

Theorem C.3 (Adaption of Theorem 4.1 from [39]).

Suppose Section C.1 and Section C.1 hold and for all , and for some constant . if we set the number of hidden nodes

and we set the step sizes , then with probability at least over the random initialization we have for

| (34) | |||

Proof of Theorem C.3.

We follow the exact proof as in [39], with the exception of using Section C.1 instead of Lemma 4.1, and Section C.1 instead of Lemma 3.2.

The lower bound for is derived from the requirement on the constant that bounds the distance of from the random initialization at . Notice that:

where the bound for the left expression on the R.H.S is given by with probability by Section C.1.

The bound for the right expression on the R.H.S is given as a corollary of (34):

Hence we require . From this requirement we derive the lower bound for .

Using Section C.1 and Theorem C.3 we obtain a the following corollary:

Corollary \thecorollary.

Assume Section C.1, Section C.1 and Section C.1 hold, exists s.t. with probability at least over the random initialization at time we have

Restate Lemma C.2 and Lemma C.3 from [31]:

Lemma \thelemma (Adaption of Lemma C.2 from [31]).

Under the same setting as Theorem C.3, with probability at least over the random initialization, for all we have:

for .

Proof.

For the first and seconds equality we use the exact proof of Lemma C.2 from [31], replacing the value of with and respectively (by using Section C.1 and Section C.1 to bound the norm of the distance of each weight from initialization). The third equality also follows the same lines, with the difference being in:

The last pass is justified due to the bound on for all with probability from Theorem C.3. The wanted result is obtained, again, by plugging the R.H.S of Section C.1 instead of .

Lemma \thelemma (Lemma C.3 from [31]).

with probability at least , we have .

Using the results above, the wanted results of this section follows:

Corollary \thecorollary.

Under the same setting as Theorem C.3, with probability at least over the random initialization we have have

Proof.

This corollary is direct by bounding and using Section C.1 and Section C.1 to bound the R.H.S for the general case and for .

C.2 Bound the distance from initialization

Write the eigen-decomposition

where are orthonormal eigenvectors of and are corresponding eigenvalues. also define

Theorem C.4 (Adaption of Theorem 4.1 from [31]).

Assume Section C.1, and suppose . Then with probability at least over the random initialization before pretraining (), for all we have:

| (35) |

We first note the important difference between this result and the original theorem is in the treatment of , the predictions of the model at . While the original theorem shows that these predictions could be treated as negligible noise (for large enough ), we instead use them as part of the bound to the convergence of the training loss.

Proof.

The core of our proof is to show that when is sufficiently large, the sequence stays close to another sequence which has a linear update rule:

| (36) |

From (36) we have

which implies

Note that has eigen-decomposition

and that can be decomposed as

Then we have

which implies

| (37) |

To prove that the two sequences stay close, we follow the exact proof of Theorem 4.1 in Appendix C of [31]. We start by observing the difference between the predictions at two successive steps:

| (38) |

For each , divide the neurons into two parts: the neurons that can change their activation pattern of data-point during optimization and those which can’t. Since , a neuron cannot change its activation pattern with respect to if and for the value of in Section C.1. Define the indices of the neurons in this group (i.e. cannot change their activation pattern…) as as , and the indices of the complementary group as .

From Section C.1 we know that with probability , for

| (39) |

Following the same steps as in [31] and notice that (38) can be treated as:

| (40) |

where:

Next use (39) to bound :

Notice from Section C.1 that stays close to . Then it is possible to rewrite Equation 40 as

| (41) |

where . Using Section C.1 it follows that

C.3 Deriving a population risk bound

Before proving Theorem 6.1 from the main text, we start by stating and proving some Lemmas:

Lemma \thelemma.

Suppose and . Then with probability at least over the random initialization at , we have for all :

-

•

, and

-

•

.

Proof.

The bound on the movement of each is proven in Theorem C.3. The second bound is achieved by coupling the trajectory of with another simpler trajectory defined as:

| (44) | ||||

First we give a proof of as an illustration for the proof of Lemma C.3. Define . Then from (44) we have and , yielding . Plugging this back to (44) we get . Then taking a sum over we have

The desired result thus follows:

Now we bound the difference between the trajectories. Recall the update rule for :

| (45) |

Follow the same steps from Lemma 5.3 from [31], using the results from Theorem C.4 when needed to obtain the proof for this lemma. According to the proof of Theorem C.4 we can write

| (46) |

where

| (47) |

Plugging (46) into (45) and taking a sum over , we get:

| (48) |

The second and the third terms in (48) are considered perturbations, and we can upper bound their norms easily. For the second term, from Section C.1 we get:

| (49) |

For the third term we get:

| (50) |

Define . using (Section C.1) we have

| (51) | ||||

| (52) | ||||

| (53) | ||||

| (54) | ||||

| (55) | ||||

| (56) | ||||

| (57) |

Let the eigen-decomposition of be . Since is a polynomial of , it has the same set of eigenvectors as , and we have

It follows that

Plugging this into (51), we get

| (58) | ||||

| (59) |

Lemma \thelemma.

Given , with probability at least over the random initialization (, simultaneously for every , the following function class

has empirical Rademacher complexity bounded as:

Proof.

We need to upper bound

where .

Similar to the proof of Section C.1, we define events:

Since we only look at such that for all , if we must have . Thus we have:

It follows that:

Thus we can bound the Rademacher complexity as:

Next we bound and .

For , notice that

Now observe the following lemma:

Lemma \thelemma.

With probability , if then .

Proof.

From Section C.1 exists s.t. with probability , for all . From the triangle inequality:

Since , and with the same probability above:

thus

For , from Section C.3 we notice that

for being defined as in Section C.1. Since all neurons are independent at and from Section C.1 and Section C.1 we know . Then by Hoeffding’s inequality, with probability at least we have

Therefore, with probability at least , the Rademacher complexity is bounded as:

completing the proof of Lemma C.3. (Note that the high probability events used in the proof do not depend on the value of , so the above bound holds simultaneously for every .)

C.4 Proof of Theorem 6.1 (Main Text)

Proof of Theorem 6.1 (Main Text).

First of all, from 3.1 we have . The rest of the proof is conditioned on this happening. We follow exactly the same steps as in [31] with minor changes.

From Theorem C.3, Lemma C.3 and Lemma C.3, we know that for any sample , with probability at least over the random initialization, the followings hold simultaneously:

- (i)

-

(ii)

and , where and . Note that .

-

(iii)

Let (). Simultaneously for all , the function class has Rademacher complexity bounded as

Let be the smallest integer such that . Then we have and . From above we know , and

Next, from the theory of Rademacher complexity and a union bound over a finite set of different ’s, for any random initialization , with probability at least over the sample , we have

Finally, taking a union bound, we know that with probability at least over the sample and the random initialization , the followings are all satisfied (for some ):

These together can imply:

This completes the proof.

C.5 Linear teachers: Proof of corollary 6.3

We will start with stating the random initialization population risk bound for this case, which we will compare our result to:

Corollary \thecorollary (Population risk bound for random initialization from [31]).

Assume that the random initialized model with weights was trained according to Theorem 5.1 from [31] and that , then with probability

| (60) |

This corollary is a direct result of plugging into Corollary 6.2 from [31], and plugging the result into Theorem 5.1 from [31].

As discussed in Section 6.1, we will assume that . Since our model is non-linear, this assumption is not trivial, and requires some clarification. For infinite width, Lemma 1 from [46] tells us that can suffice to achieve this, if the samples are chosen according to some conditions. For the case of finite width , like is assumed in Theorem 6.1, no such equivalent exist. However, we can use Section C.5 for the pretraining, and achieve an bound on the pretraining population risk, for sufficiently large . Then, approximate relaxations can be derived when we assume the two functions are close (i.e. ).

We now restate our two corollaries from the main text:

Corollary 6.2 (Main Text).

Suppose that , , and assume Assumption 3.2 holds. Then,

This is a direct corollary of Theorem 6.1 from [31] on defined above.

Corollary 6.3 (Main Text).

Under the conditions of Theorem 6.1 and Corollary 6.2, it holds that

Comparing this to Section C.5 gives us the exact condition for when it is better to use fine-tuning instead of random initialization, which is

We will now provide a proof for this results: