Joint parametric specification checking of conditional mean and volatility in time series models with martingale difference innovations

Abstract

Using cumulative residual processes, we propose joint goodness-of-fit tests for conditional means and variances functions in the context of nonlinear time series with martingale difference innovations. The main challenge comes from the fact the cumulative residual process no longer admits, under the null hypothesis, a distribution-free limit. To obtain a practical solution one either transforms the process in order to achieve a distribution-free limit or approximates the non-distribution free limit using a numerical or a re-sampling technique. Here the three solutions will be considered. It is shown that the proposed tests have nontrivial power against a class of root-n local alternatives, and are suitable when the conditioning information set is infinite-dimensional, which allows including models like autoregressive conditional heteroscedastic stochastic models with dependent innovations. The approach presented assumes only certain conditions on the first- and second-order conditional moments, without imposing any autoregression model. The test procedures introduced are compared with each other and with other competitors in terms of their power using a simulation study and a real data application. These simulations have shown that the statistical powers of tests based on re-sampling or numerical approximation of the original statistics are in general slightly better than those based on a martingale transformation of the original process.

Key words: Autoregression, conditional mean, conditional variance, cumulative residual process, heteroscedasticity, martingale transform, re-sampling, interest rate, martingale differences, nonlinear times series, parametric specification.

Subject Classifications: 62F10, 62F05, 62J02, 62M10, 60J15.

1 Introduction

A great deal of the data in econometrics, engineering and natural sciences occurs in the form of time series, where the data are naturally dependent and the volatility is, in general, function of the past. One then expects better forecast results if additional information allowing the conditional variance to depend upon the past realizations is supposed. One of the earliest development in this area is the work of Engle, (1982) who introduced the so-called autoregressive conditional heteroscedastic (ARCH) model, which has been extended in a number of directions. The most important of these is the extension designed to include moving-average parts, namely the generalized ARCH (GARCH) model introduced by Bollerslev, (1986). These models are often used to parameterize conditional heteroscedasticity that appears in many financial time-series such as exchange rates and stock return. In applications, GARCH models have been specified for data at different frequencies assuming that the rescaled innovations are independent and identically distributed (i.i.d.). Drost and Nijman, (1993) pointed out that, the common assumption in applications that rescaled innovations are independent is disputable, since it depends upon the available data frequency. They classified GARCH models into three categories: Strong GARCH requires that rescaled innovations are independent, semi-strong GARCH assumes that rescaled innovations are martingale difference sequences, the weak form, where the martingale difference sequence assumption is relaxed. The weak-GARCH representation has been used previously, for instance, by Gonçalves and White, (2004), were the authors showed, through simulations, the effects of misspecification when the true model is a GARCH with an innovation term that follows an AR(1) process. Kristensen and Rahbek, (2005) also noted the relevance of this model. Dahl and Iglesias, (2007) provided an empirical application showing that this process has empirical relevance.

Diagnostic tests are integral part of any modelling exercise. Several time series models are given by specifying conditional mean and conditional variance functions. Testing the correct specification of these quantities is of major importance in the model validation. A great deal of tests proposed in the literature focuses on testing either the mean function or the volatility function for time series, but usually not both. Escanciano, (2008, 2010) discussed joint tests for parametric form of the mean and volatility functions. He also argued that if the mean is misspecified, tests of volatility functions are usually misleading.

This paper derives joint goodness-of-fit tests for the conditional means and variances functions for strictly stationary ergodic time series with martingale difference innovations , where is the -field generated by the observations obtained up to time , without imposing any type of autoregressive model. The martingale hypothesis is very important in economics theory, for instance, dynamic equilibrium approaches to macroeconomics have imposed martingale restrictions on numerous time series of interest (see, e.g., Durlauf, (1991) for more discussions on the martingale hypothesis arising in other contexts of economic theory). The assumption of martingale difference innovations considered here is more general than the standard assumption of i.i.d innovations as it allows some dependence structure in the innovations. The framework we are considering here is suitable for cases in which the conditioning set is infinite-dimensional and may be used for models that do not necessary satisfy Markov property, particularly, semi-parametric models, where the conditional mean and the conditional variance of given have parametric forms. This includes most processes usually used for modeling financial time series with dependent innovations, such as GARCH, ARMA-GARCH, exponential and threshold autoregressive processes with GARCH errors.

Goodness-of-fit tests for parametric and semiparametric hypotheses of the regression function have been considered in the literature, with emphasis on i.i.d innovations, see for instance Stute, (1997) who presented non-parametric full-model checks for regression based on the limiting law of the residual marked process, see also González-Manteiga and Crujeiras, (2013) for a survey on the topic. Escanciano et al., (2018) discussed a general methodology for constructing nonparametric/semiparametric asymptotically distribution-free tests about regression models for possibly dependent data. Similar study investigated the autoregressive function in time series models, see, e.g., Diebolt, (1990), McKeague and Zhang, (1994), Laïb, (1999), Koul and Stute, (1999). In the context of time series with martingale difference innovations, Stute et al., (2006) provided non-parametric tests based on residual cusums for testing the autoregressive function in higher-order time-series models, and Escanciano and Mayoral, (2010) proposed data-driven smooth asymptotically distribution-free tests based on the principal components of certain marked empirical processes for testing the martingale difference hypothesis of a possibly non-linear time series.

Testing hypotheses about the conditional variance function of regression models are investigated by many authors in the literature.

Wang and Zhou, (2005) considered a nonparametric diagnostic test for checking the constancy of the conditional variance function, in a nonparametric regression model, where the co-variables are fixed design points, without assuming a known parametric form for the conditional mean function. Dette et al., (2007) proposed a test procedure

for testing the parametric form of the conditional variance in the common nonparametric regression model.

Koul and Song, (2010) discusses the problem of fitting a parametric model to the conditional variance function in a class of heteroscedastic regression models. Their test is

based on the supremum of the Khmaladze type martingale transformation of a certain partial sum process of calibrated squared residuals.

The proposed statistical test is shown to be consistent against a large class of fixed

alternatives and to have nontrivial asymptotic power against a class of nonparametric local alternatives.

Recently, Pardo-Fernández et al., (2015) have proposed several nonparametric statistical tests for checking whether the conditional variances are equal in location-scale regression models. Their

procedure is based on the comparison of the error distributions under the null hypothesis of equality of variances functions.

Polonik and Yao, (2008) propose two tests for testing multivariate volatility functions using minimum volume sets and inverse regression. Their tests are based on cumulative sums coupled with either minimum volume sets or inverse regression ideas.

Tests of conditional variance functions in time series context were also previously considered in the literature. In particular, Auestad and Tjøstheim, (1990), focused on kernel estimate of the one step lagged conditional mean and variance functions for the purpose of identifying common linear models such as threshold and exponential autoregressive. Diebolt, (1990) established the consistency of regressogram type estimators of the conditional mean and conditional variance functions. He deduced nonparametric goodness-of-fit tests for known form of these functions. Chen and An, (1997) proposed a Kolmogorov-Smirnov type statistic to test the homoscedasticity hypothesis, when the observations are assumed to be strongly mixing. Their test uses only a subsample which induces a loss of information and power. Ngatchou-Wandji, (2002) presented a procedure, based on marked empirical process, for testing the goodness-of-fit of the conditional variance function of a Markov model of order one.

For time series with martingale difference innovations Laïb and Chebana, (2011) considered a class of nonlinear semi-parametric models and established the local asymptotic normality for cumulative residual process. They also derived an efficient simultaneous test for testing the conditional mean and the conditional variance functions. Laïb and Louani, (2002) provided a test of conditional homoscedasticity hypothesis of the one-step forecast error in the context of first-order AR-ARCH model. Their works was extended by Laïb, (2003) for the context of time series with martingale difference innovations. The author established the asymptotic of the cumulative residual process and developed a test for homoscedasticity when the innovations are independent of the past of . Chen et al., (2015) developed two tests for parametric volatility function of a diffusion model, with i.i.d. innovations, based on Khamaladze’s martingale transformation. Their tests use the structural properties of the diffusion process and do not require the estimation or the specification of the drift function. Escanciano, (2008) proposed a class of joint and marginal spectral diagnostic tests for parametric conditional means and variances of time series models. The proposed tests are not distribution-free and the author introduced a bootstrap procedure that should be used to implement these tests. Escanciano, (2010) constructed asymptotic distribution-free joint specification tests, that can be applied in many financial and economic time series including GARCH and ARMA-GARCH models. These tests are based on carefully weighted residual empirical process. The weights are chosen in a way to insure that the weighted empirical process of residuals admits a distribution free limit. It is shown that the proposed tests generalize those of Wooldridge, (1990). Note however that, the performance of the constructed tests strongly depend on the choice of the weights.

In this paper we develop a joint test for parametric form specification of the conditional mean and variance functions when innovations satisfy the martingale difference hypothesis and are allowed to depend on the past -field. The main challenge comes from the fact the marked cumulative residual process no longer admits a distribution-free limit. To obtain a practical solution one either transforms the process in order to achieve a distribution-free limit or approximates the non-distribution free limit using numerical or re-sampling techniques. Here, three solutions, based on Khmaladze transform of cumulative residual process, a multiplier bootstrap re-sampling procedure, and a numerical approximation of the limiting distribution, are considered and their finite sample performance is compared with Escanciano, (2010)’s procedure.

Though Khmaladze transform of the cumulative residual process was considered in previous works, such as Chen et al., (2015) or Stute et al., (1998), the setting addressed here is more general and does not assume any explicit data-generating model or independence of innovations. It may be applied for several non-linear time series models with martingale innovations. The second added value of this paper is that it compares numerically the three classical procedures used for constructing joint tests based on the cumulative residual process. The numerical study particularly revealed that the Khmaladze transform is slightly less performant than re-sampling and numerical approximation techniques.

The rest of the paper is organize as follows: Section 2 defines the problem and states some preliminaries results. Section 3 defines and establishes the asymptotic behavior of the martingale transformation applied to the cumulative residual process. Section 4 introduces the marginals as well as the joint parametric specification Cramér von-Mises-type tests statistics for the conditional mean and conditional variance functions. Subsection 4.1 presents the martingale transform based test statistics. A numerical approximation procedure for the asymptotic distribution of the test statistics based on the original process is given in Subsection 4.2. A re-sampling algorithm for test statistics based on the original cumulative residual process is also detailed in Subsection 4.3. A comparison between these statistical procedures, via simulations, is outlined in Section 5 and an application to real data is given in Section 6. A conclusion summarizing our findings is given in Section 7. All proofs are provided in the Appendix.

2 Assumptions and Main results

Let be a strictly stationary ergodic defined on the probability space . The random variables ’s are real-valued with common continuous distribution function . For each we let denote the past information at time . We let denotes -field generated by . The purpose is to verify if the conditional mean almost surely (a.s.) and the conditional variance a.s. of given satisfy, respectively, the following relations a.s. and a.s., where and are -measurable known parametric functions that depend on a finite dimensional vector of parameters for , and assumed to be finite with probability one. More precisely, we are interested in examining hypotheses stating that

| (2.1) | |||||

We assume throughout this manuscript that for the true value of , denoted belongs to the interior of some compact subset . We also assume that the sequence of innovations is a sequence of martingale differences with respect to , that is is -measurable and This condition combined with the fact that the set of information has an infinite dimensional will allow to consider non markovian processes such as the ARMA-GARCH process and all others. In practice the set is not observable and may be estimated, see Remark 2.2 and Escanciano, (2010) for more discussion.

To test the specification of the conditional mean function we will use and to test for the conditional variance function we will use . Following Escanciano, 2007a , Escanciano, (2008), Koul and Stute, (1999), Laïb, (2003) and Ngatchou-Wandji, (2002) we introduce the following cumulative empirical residuals processes

where is the indicator function of the set , is consistent estimators of . Note that, under , for . To test specification of the conditional mean and variance jointly, we introduce the bivariate processes and defined by and , where the script stands for the transpose of the matrix . Note that letting one sees that

and

Remark 2.1.

Remark 2.2.

As pointed in Escanciano, (2010), the past information is not completely observable and needs to be estimated by . Such estimation usually involves replacing the unknown initial state by some quantity . One must insure that replacing by does not affect the asymptotic behaviour of the process . One easily verifies that if for ,

then the asymptotic behaviour of is not altered when is replaced by . We will assume that such condition holds and will use in the definition of throughout the manuscript. The discussion in Escanciano, (2010) shows that this condition holds true for ARMA-GARCH models in particular.

The limiting laws of and are given in Koul and Stute, (1999) and Escanciano, 2007a . The limiting behavior of is given in Laïb, (2003), who also obtained the limit law of in the special case with . The next section studies the asymptotic for the bivariate process .

2.1 Limiting law of the process under the null hypothesis

The following notations are used in the rest of the paper. denotes the Euclidian norm of the vector and for any matrix , is the associated matrix norm for the matrix . For any bounded function , let and for any , set and .

The asymptotic results are stated under the following assumptions:

Assumption A1: For each ,

-

1.

.

-

2.

for any real .

-

3.

is non-decreasing continuous function of .

-

4.

with such that .

Assumption A2: Under , the estimators of is such that

where is an -valued measurable function satisfying a.s. and

exists and is positive definite.

Assumption A3:

For let denote the gradient of with respect to the components of evaluated at a fixed point . Assume that and

where and are positive functions satisfying and goes to zero as .

Note that Assumption (A1) is an adaptation of conditions (A–D) of Theorem 1 of Escanciano, 2007b to the context of stationary and ergodic sequence. As argued in Escanciano, 2007b these are among the weakest conditions to ensure the weak convergence of marked empirical processes. Assumption (A2) and (A3) are commonly used to ensure the convergence of and to validate the expansion of the process . These assumptions hold for most commonly used models and estimation procedures, see, for example Koul and Stute, (1999); Escanciano, 2007a ; Escanciano, (2010) for discussion and details.

From now on let denotes the space of càdlàg functions and for define

| (2.4) |

where and are given in Assumption (A1) and for

| (2.5) |

Let denotes the Gaussian process with covariance function defined above. The following result summarizes the weak convergence of the processes and .

Theorem 2.3.

If Assumption (A1) holds then, under , converges weakly to If Assumptions (A1)-(A3) hold true, then, under , converges weakly to where is a centered Gaussian process given by

| (2.6) |

where is a multivariate normal with mean zero and covariance and the function with

and

The covariance function of is given by

| (2.7) |

where with

Remark 2.4.

The limiting covariance function is in general complicated, therefore classical statistics based on the process do not admit distribution-free limits. To overcome this, one usually uses one of the following approaches. The first approach consists in transforming the process in a such way to achieve a distribution-free limit and then using the transformed process to define test statistics. While the second approach uses to construct test statistics and then adopts either a numerical approximation or a re-sampling technique to estimate the non-distribution free limit. Both approaches will be discussed and compared in the rest of this manuscript. The transformation is discussed in Section 3 while the numerical and re-sampling approximations are outlined in Section 4.

2.2 Limiting law of the process under local alternatives

In this section we establish the limiting behavior of the process under local alternatives defined as follows.

where and are some non-zero functions indicating the direction of departure from the null hypothesis. We assume that for .

The following assumption is needed to establish the limiting behavior under .

Assumption (L1) Under , the estimator satisfies

where is a random/nonrandom vector and is as in Assumption (A2).

The following Theorem shows that our tests are able to detect local alternatives of the type described by .

Theorem 2.5.

Under , if Assumptions A1, A3 and L1 hold, the process converges weakly to where .

3 Khmaladze transform of the process

This section presents a martingale transformation of the Khmaladze type that will be applied to the process in order to achieve a distribution-free limit for classical test statistics. It worth mentioning that the Khmaladze transformation will ensure that the limit of the transformed process is Brownian motion.

To define such transformation, assume the functions , for , can be written as

| (3.1) |

where . Let the matrix for be defined as . Assume that there exists such is non-singular. Note that it follows from the definition of that is non-negative definite for all implying that is invertible for all whenever is invertible.

Following the concept in Khmaladze, (1988), for any function consider the linear transformations for given by

| (3.2) |

for all . The Khmaladze transform of the cumulative residual process considered here is an application of the transformation and to the processes and . It is formally defined by

| (3.3) |

Easy manipulations show that for

| (3.4) |

Observe also that cannot be used in practice to build test statistics since it depends on several unknown quantities, namely, and . Replacing and by their consistent estimates and respectively, one obtains an empirical version of defined as follows

where .

The Following assumptions are needed to ensure the convergence of .

Assumption K1: Assume there exists such that is invertible for .

Assumption K2: Assume that , , , , and are all finite.

Assumption K3: Assume that converges to zero in probability,

and that converges to zero in probability.

Assumption K4: For each and for each ,

-

1.

.

-

2.

, for any .

-

3.

is non-decreasing continuous function of .

-

4.

with such that .

The next result establishes the weak convergence of .

Theorem 3.1.

If assumptions A1–A4 and K1–K4 are satisfied then for

where is the -th component in the process defined in Theorem 2.3.

Remark 3.2.

Note that the process has marginal and where and are Brownian motions. In general and are not independent. The distribution of will only be distribution free if and are independent. This defeats the purpose of the martingale transformation in general. Though the above results clearly show that the transformation provides a distribution-free limit for testing the mean or the variance function separately. The transformation is only useful for joint testing of conditional mean and variance functions only in the case of independent components of the bivariate process . This was the case in the work of Chen et al., (2015). In general, the components and will be independent if which translates to a condition on the third moment of . In particular, if a.s. then the components and are independent. This holds true for all time series models that assume that the errors are i.i.d provided that we add a condition stating that the error is symmetric or just has zero third conditional moment.

Remark 3.3.

Note that the conditions imposed on the estimate are similar to those used in Bai, (2003) and Bai and Ng, (2001). Note also that the converges to zero in probability can be weakened to converges to zero in probability. But for simplicity, the proof is presented with the stronger assumption. The second condition on , in Assumption (K3), is usually verified using the structure of the estimator and the nature of the process , for details see the discussion in Bai, (2003).

4 Test statistics

Test statistics for the hypothesis are obtained by considering continuous functional of the process or of its Khmaladze transform . That is, given a continuous functional a test statistic can be obtained using or . The continuous mapping theorem provides the asymptotic behavior of and . The most commonly used functional, in practice, are of the Cramér-von-Mises or Kolmogorov-Smirnov type. For simplicity, the rest of this paper only focuses on Cramér-von-Mises type statistics, but the approaches discussed apply to any continuous functional. To be specific, the following marginal Cramér-von-Mises test statistics

for , will be used here. Clearly, the statistics given in (4) converge in distribution to which is equivalent to .

The statistic can be used to test the conditional mean function and the statistic can be used to test the conditional variance function. To conduct a joint test of mean and variance functions one must combine and . To combine both statistics, Chen et al., (2015) used and . Such combinations were adequate since in his case both statistics had the same limiting distribution. In our context, this is not true in general, hence to combine these test statistics we will need a more general approach such as the ones discussed in Ghoudi et al., (2001) and Genest and Rémillard, (2004). To be specific, define , and , where and denotes the P-value of the statistics . According to Fisher, (1950, pp. 99-101), when and are independent converges to Chi-square distribution with degrees of freedom and provides the optimal way of combining and . It will be seen, in the simulation and application sections, that and are easier to compute and have similar power to .

4.1 Martingale transform based test statistics

Next, we repeat a similar approach using the transformed process yielding

| (4.2) |

where

| (4.3) |

and . Observe that Theorem 3.1 and the continuous mapping Theorem imply that, under the null hypothesis, converges in distribution to , where is a standard Brownian motion. According to Shorack and Wellner, (1986) (page 748), for with , the limiting critical values for 90%, 95% and 99% are 1.2, 1.657 and 2.8 respectively.

Since and admit the same limiting distribution, there is no need for the normalization by and in the definition of the combined statistics. Therefore, the combined statistics using the transformed process are defined as follows: , and .

The statistics , and will only be distribution-free if and are independent. As argued earlier, this is the case if the covariance term or more precisely if a.s.

As mentioned above, the statistics given in (4) converge weakly towards . Since the process has a complicated covariance, which depends on the unknown distribution and some unknown parameters, the p-values of the test statistic need to be approximated using either numerical techniques or re-sampling algorithms. A numerical approximation of the limiting distribution, using the approach introduced by Deheuvels and Martynov, (1996), is outlined in Subsection 4.2 and a re-sampling algorithm based on multipliers bootstrap is described in Subsection 4.3.

4.2 Numerical approximation of the asymptotic distribution of the test statistics

To approximate the limiting distribution of the statistics and we follow the numerical integration procedure given by Deheuvels and Martynov, (1996). We will only outline how the procedure applies to since the application to is similar and much simpler. The main idea consists in using numerical integration to approximate by the quadratic form , where are the quadrature nodes, are the quadrature coefficients and is the number of quadrature points. Because is a Gaussian process, is a quadratic form of normal random variables. Imhof’s characteristic function inversion procedure (Imhof, (1961)) is used to compute the distribution function of . When applying the procedure to or , will be a quadratic form with normal random variables. Note that in the computation of the characteristic function the covariance operator is replaced by its empirical estimate obtained by replacing , , and by their consistent estimators , , and , where is a symmetric two by two matrix whose diagonal entries are for and whose off diagonal entry is given by

and where

and We also used, in the simulation and application sections, the simplest quadratures, namely and .

For the statistics is computed after obtaining the p-values of statistics and . The p-value of are obtained form the Chi-square distribution which is only valid when and are independent. The independence argument also allows for easy computation of the p-values of the statistics . If the independence argument is not valid, then the computation for both and are more complex and requires the numerical approximation of the joint distribution of and .

4.3 Multipliers bootstrap for the test statistics

Another approach to approximate the limiting distributions of and consists in using a re-sampling algorithm. To define such algorithm, let be a positive integer denoting the number of bootstrap samples. For , let be a sequence of independent identically distributed random variables with mean zero and variance one independent of the sigma field generated by the ’s. The multipliers bootstrap technique applied to the empirical process , is defined as follows

| (4.4) |

Observe that the process defined in (4.4) depends on unknown quantities, namely, and . A plug-in estimator of is obtained by replacing and by their consistent estimators and yielding

| (4.5) |

The following extra assumptions are needed to establish the weak convergence of .

Assumption M1: Assume that there exists such that for all satisfying one has where is a positive function satisfying .

Assumption M2: Assume that there exists such that for all satisfying one has where and are positive functions satisfying and .

Assumption M3: Assume that .

The next result summarizes the asymptotic behavior of the bootstrapped process .

Theorem 4.1.

Suppose that assumptions A1–A4 and M1–M3 hold true, then for , converge weakly to independent copies of .

Note that the bootstrapped version of the statistic for is given by

where

where and .

Let for . To obtain a bootstrapped version of and one uses and respectively.

To apply the multipliers bootstrap procedure to approximate the p-value of any of the Cramér-von Mises statistics ,, or one proceeds according to the following algorithm. The algorithm is explained in the context of but works in the same manner for any of the statistics mentioned above.

-

•

Estimate by and compute the test statistic .

-

•

For

-

–

Generate as sequence of i.i.d normal random variables.

-

–

Compute the bootstrapped Cramér-von Mises statistics for .

-

–

-

•

Estimate the -value, of by .

The statistics where for are the estimated -values given by the above procedure. The -value of the statistics are obtained using the Chi-square distribution with degrees of freedom.

Remark 4.2.

Note that is estimated only once and the matrix is only computed once which make the multipliers Bootstrap extremely fast to implement. This is much faster than the classical parametric bootstrap which requires re-estimating the parameters for each bootstrap iteration. Moreover, Theorem 4.1 and the continuous mapping Theorem imply that converges in law to independent copies of .

5 Finite sample performance

This section presents several simulation experiments carried out to assess the power of the proposed test statistics. The first experiment, described in Subsection 5.1, is designed to assess the fit of an ARCH(1) model. The second experiment, outlined in Subsection 5.2, assess the power of our test statistics for detecting departure from GARCH(1,1) model. The third experiment given in Subsection 5.3 studies the behavior of the test when fitting and AR(1)-GARCH(1,1) model. The fourth experiment, presented in Subsection 5.4 outlines the finding of applying our test procedures to the case of stochastic differential equation models. Two sub-experiments are considered, in the first we test if the model has a linear drift and a constant diffusion while in the second we test if the model has linear drift and a diffusion proportional of square root of series.

5.1 Testing ARCH(1) model

The purpose of the simulation experiment considered here is to test whether the data is generated from pure ARCH(1) model or not. That is we wish to test

| (5.1) | |||||

The data is generated according to one of the following models, where are independent and identically distributed random variables and

-

()

-

()

-

()

-

()

-

()

A pure ARCH(1) model is fitted to the data. Then tests described in Section 4 are applied using the corresponding to maximum likelihood estimator of the ARCH parameters and . We generated series of length following models –. The results given in Table 1 summarize a Monte-Carlo simulation study with 2000 replications of tests with significance levels. Note that corresponds to the null hypothesis and as shown in the table, the test maintains its level quite well. Tests based on Khamaladze transform are in general a bit less powerful than those based on the original process. Table 1 also shows that and have no detection power in this context. This is expected since there is no change in the mean function for all the alternative considered here. The power of the combined statistics and (or and ) are similar in general. The powers obtained using the multipliers procedure and those derived from numerical approximation are very close. This shows that both techniques provide very good estimation of p-values of these test statistics.

| Transformation technique | Multipliers procedure | Numerical approximation | ||||||||||||||

| n | DGP | |||||||||||||||

| 3.7 | 4.2 | 3.9 | 4.0 | 4.0 | 4.3 | 3.6 | 3.7 | 3.8 | 4.0 | 4.7 | 3.3 | 3.6 | 3.8 | 3.8 | ||

| 4.5 | 20.8 | 15.0 | 14.5 | 15.1 | 5.3 | 21.2 | 12.0 | 10.8 | 14.0 | 5.5 | 18.4 | 11.6 | 10.2 | 13.3 | ||

| 100 | 4.3 | 20.9 | 14.9 | 14.9 | 14.8 | 4.8 | 15.2 | 9.5 | 7.9 | 11.8 | 5.2 | 14.2 | 9.0 | 7.6 | 11.3 | |

| 3.8 | 43.4 | 30.7 | 32.9 | 29.4 | 5.2 | 61.0 | 42.2 | 44.7 | 44.5 | 5.3 | 60.4 | 42.6 | 44.5 | 43.1 | ||

| 3.1 | 47.4 | 35.1 | 35.9 | 34.3 | 3.6 | 43.5 | 24.8 | 24.1 | 32.5 | 3.9 | 42.6 | 24.5 | 24.0 | 31.0 | ||

| 3.9 | 5.5 | 4.6 | 5.0 | 4.7 | 4.4 | 5.0 | 4.5 | 4.5 | 4.8 | 4.4 | 4.6 | 4.3 | 4.7 | 4.4 | ||

| 3.7 | 45.3 | 35.9 | 37.0 | 35.1 | 4.7 | 57.7 | 44.3 | 44.5 | 45.3 | 4.9 | 57.8 | 44.3 | 45.1 | 44.3 | ||

| 300 | 3.8 | 40.2 | 31.7 | 31.6 | 30.5 | 4.6 | 38.0 | 23.8 | 22.2 | 29.3 | 4.1 | 37.9 | 23.6 | 21.2 | 27.6 | |

| 3.5 | 63.1 | 54.6 | 56.4 | 53.9 | 4.3 | 92.1 | 88.9 | 89.8 | 87.0 | 4.2 | 92.2 | 89.3 | 90.0 | 86.9 | ||

| 3.6 | 68.0 | 59.2 | 60.4 | 58.4 | 4.3 | 76.0 | 64.6 | 64.7 | 66.9 | 4.4 | 75.9 | 64.7 | 64.9 | 66.7 | ||

5.2 Testing GARCH(1,1) model

This section presents the result of a simulation study in which we assess the power of the tests, discussed in this manuscript, in detecting departure from a GARCH(1,1) model. That is we wish to test is the mean and variance functions are those of a GARCH(1,1) or not. We use the same settings as in Experiment 2 of Escanciano, (2010). More precisely, we generated the data from an AR(1)-GARCH(1,1) model with autoregressive coefficient varying from to . We fitted a GARCH(1,1) and recorded the percentage of rejection. As in all simulation reported in this manuscript we used Monte-Carlo simulation iterations. For this experiment we used a sample size an in Escanciano, (2010). The results are reported in Table 2. Note that corresponds to the null hypothesis in this case. Table 2 shows that the level is respected quite well in general. It also shows that the type of alternative considered here is mainly detected by the contribution of component or to the combined statistics. This makes all combined statistics quite power in detecting such alternatives. The component and have no power against this type of alternatives. This is expected since these components were designed to detect change in the variance function. In this context statistics based on the transformed process seem to be a bit more powerful than those based on the original process. Comparing our results to Figure 1 of Escanciano, (2010), we notice that the power of the tests presented here is slightly better.

| Transformation technique | Multipliers procedure | Numerical approximation | ||||||||||||||

| n | ||||||||||||||||

| -0.9 | 100 | 1.3 | 100 | 100 | 100 | 99.4 | 2.5 | 96.2 | 96.2 | 99.1 | 99.4 | 1.9 | 95.9 | 96.0 | 99.2 | |

| -0.7 | 100 | 3.0 | 100 | 100 | 100 | 98.7 | 1.5 | 96.4 | 96.9 | 97.7 | 98.7 | 1.2 | 96.2 | 96.7 | 97.8 | |

| -0.5 | 98.9 | 2.9 | 97.8 | 97.9 | 97.7 | 93.4 | 2.4 | 85.3 | 87.5 | 86.9 | 93.3 | 2.1 | 84.4 | 87.0 | 86.5 | |

| -0.3 | 76.3 | 2.9 | 63.8 | 66.0 | 62.3 | 59.6 | 3.1 | 43.9 | 45.6 | 46.3 | 59.7 | 2.4 | 42.5 | 45.1 | 45.2 | |

| 100 | 0.0 | 6.3 | 2.9 | 4.4 | 4.2 | 4.1 | 3.6 | 4.1 | 3.4 | 3.4 | 4.1 | 3.5 | 4.0 | 2.9 | 3.2 | 3.8 |

| 0.3 | 68.1 | 2.1 | 54.2 | 57.9 | 52.4 | 42.4 | 2.2 | 26.8 | 31.2 | 26.7 | 42.4 | 1.5 | 25.4 | 30.1 | 24.7 | |

| 0.5 | 99.0 | 2.5 | 96.8 | 97.3 | 96.3 | 80.7 | 1.4 | 67.7 | 72.4 | 65.6 | 81.4 | 1.5 | 67.4 | 72.0 | 65.3 | |

| 0.7 | 100 | 1.5 | 100 | 100 | 100 | 87.9 | 0.5 | 79.8 | 83.9 | 77.8 | 87.9 | 0.4 | 79.8 | 83.6 | 77.5 | |

| 0.9 | 100 | 1.0 | 100 | 100 | 100 | 80.6 | 0.3 | 62.1 | 69.6 | 69.8 | 80.9 | 0.2 | 62.0 | 68.5 | 69.9 | |

| -0.9 | 100 | 2.9 | 100 | 100 | 100 | 100 | 4.1 | 99.8 | 99.8 | 99.9 | 100 | 3.9 | 99.8 | 99.8 | 99.9 | |

| -0.7 | 100 | 4.7 | 100 | 100 | 100 | 100 | 3.8 | 99.9 | 100 | 100 | 100 | 3.1 | 100 | 100 | 100 | |

| -0.5 | 100 | 4.9 | 100 | 100 | 100 | 99.7 | 3.1 | 99.3 | 99.5 | 99.5 | 99.7 | 3.0 | 99.3 | 99.5 | 99.5 | |

| -0.3 | 99.3 | 4.6 | 98.4 | 98.6 | 98.2 | 95.6 | 3.1 | 91.5 | 92.9 | 90.9 | 95.8 | 2.7 | 91.8 | 92.9 | 91.0 | |

| 300 | 0.0 | 4.8 | 4.1 | 4.7 | 4.4 | 4.5 | 4.4 | 4.4 | 4.2 | 4.6 | 4.5 | 4.4 | 4.3 | 4.0 | 4.2 | 4.2 |

| 0.3 | 99.2 | 3.1 | 97.8 | 98.5 | 97.5 | 94.3 | 2.5 | 88.8 | 92.1 | 88.3 | 94.5 | 2.6 | 89.3 | 91.5 | 88.4 | |

| 0.5 | 100 | 2.9 | 100 | 100 | 100 | 99.6 | 2.2 | 99.3 | 99.5 | 99.4 | 99.6 | 2.0 | 99.3 | 99.5 | 99.4 | |

| 0.7 | 100 | 2.0 | 100 | 100 | 100 | 99.7 | 1.3 | 99.5 | 99.6 | 99.5 | 99.7 | 0.8 | 99.4 | 99.5 | 99.5 | |

| 0.9 | 100 | 0.5 | 100 | 100 | 100 | 96.6 | 0.3 | 90.7 | 94.1 | 93.1 | 96.6 | 0.2 | 90.6 | 93.6 | 92.9 | |

5.3 Testing AR(1)-GARCH(1,1) model

In this section we present the result of a study testing the null hypothesis that the mean and variance functions are those of an AR(1)-GARCH(1,1) model. The same five alternatives considered in Experiment 3 of Escanciano, (2010) are used. To be specific the data is generated according to one of these alternatives, and AR(1)-GARCH(1,1) model is fitted to the data. The test statistics proposed in this manuscript are applied and the percentage of rejection, in a replicates Monte-Carlo simulation, is reported in Table 3. The alternative considered are defined as follows:

- A0:

-

The null hypothesis AR(1)-GARCH(1,1) model: where with and i.i.d Normal random variables with mean zero and variance one.

- A1:

-

ARMA(1,1)-GARCH(1,1) model: and is as in model A0.

- A2:

-

TAR model: if and if with is as in model A0.

- A3:

-

EGARCH(1,1) model: where and is as in model A0.

- A4:

-

Bilinear model: where is as in model A0.

- A5:

-

Nonlinear Moving average model: where is as in model A0.

| Transformation technique | Multipliers procedure | Numerical approximation | ||||||||||||||

| n | DGP | |||||||||||||||

| A0 | 4.6 | 3.9 | 4.6 | 4.5 | 4.9 | 2.6 | 5.4 | 4.4 | 5.3 | 4.5 | 2.3 | 5.3 | 4.5 | 5.1 | 4.2 | |

| A1 | 3.6 | 4.1 | 3.4 | 3.8 | 3.6 | 1.4 | 4.3 | 3.2 | 3.5 | 2.9 | 1.3 | 3.8 | 2.9 | 3.4 | 2.8 | |

| A2 | 100 | 5.8 | 99.8 | 99.9 | 99.8 | 77.8 | 31.9 | 61.6 | 47.2 | 78.8 | 77.7 | 31.9 | 63.1 | 47.3 | 78.4 | |

| 300 | A3 | 6.2 | 6.0 | 7.1 | 6.8 | 7.1 | 55.5 | 51.6 | 71.8 | 64.9 | 78.1 | 55.5 | 52.0 | 71.7 | 64.9 | 76.9 |

| A4 | 68.3 | 5.3 | 59.0 | 60.3 | 57.7 | 13.6 | 27.6 | 30.5 | 27.2 | 32.2 | 13.0 | 27.4 | 31.1 | 27.3 | 31.7 | |

| A5 | 100 | 15.4 | 100 | 100 | 100 | 91.3 | 18.1 | 87.2 | 87.4 | 89.0 | 91.4 | 18.2 | 87.7 | 86.7 | 89.4 | |

| A0 | 6.2 | 3.4 | 4.8 | 4.7 | 4.7 | 3.5 | 4.4 | 3.8 | 4.1 | 3.9 | 3.2 | 4.7 | 3.9 | 4.5 | 3.8 | |

| A1 | 4.0 | 4.9 | 3.7 | 3.8 | 3.6 | 2.2 | 5.0 | 4.2 | 4.5 | 3.3 | 2.2 | 4.7 | 3.8 | 4.4 | 3.1 | |

| A2 | 100 | 11.2 | 100 | 100 | 100 | 98.2 | 63.7 | 96.0 | 91.0 | 98.4 | 98.1 | 63.6 | 96.1 | 91.0 | 98.4 | |

| 600 | A3 | 4.8 | 13.7 | 10.8 | 11.2 | 10.6 | 80.1 | 69.6 | 92.6 | 90.5 | 94.6 | 80.7 | 70.0 | 92.6 | 90.4 | 94.8 |

| A4 | 88.4 | 6.4 | 84.0 | 84.4 | 83.3 | 30.7 | 41.7 | 51.6 | 44.0 | 56.6 | 29.5 | 41.1 | 50.8 | 43.3 | 55.9 | |

| A5 | 100 | 40.9 | 100 | 100 | 100 | 97.6 | 50.2 | 97.5 | 97.2 | 97.9 | 97.6 | 51.0 | 97.5 | 97.3 | 97.8 | |

Comparing with Table 2 in Escanciano, (2010), one notice that combined tests introduced in this manuscript are more powerful than the tests considered in Escanciano, (2010). The only exception being the case of alternative A1: ARMA(1,1)-GARCH(1,1) where our tests were not able to detect such alternative while those in Escanciano, (2010) had reasonable power. We also notice that tests based on the transformed process are bit more powerful in the case of alternatives A2, A4 and A5. On the other hand these tests fall way behind in the case A3. This seems to concord with the observations from the first simulation experiment where tests based on the transformed process were a bit more powerful in detecting a change in the mean function. In fact, for the three alternatives A2, A4 and A5 there is a change in the conditional mean function. While in the case of alternative A3, the conditional mean function is still that of an AR(1) while the change occurred in the conditional variance function.

5.4 Testing stochastic differential equation models

In this part, we are interested in testing whether the data fits a specified stochastic differential equation (SDE) model. In finance continuous time models are widely used to study the dynamic of some financial products such as asset prices, interest rate and bonds. Continuous-time modelling in finance was introduced by Bachelier, (1900) on the theory of speculation and really started with Merton, (1970) seminal work. Since then several models were developed which can be formulated by the following general SDE

| (5.2) |

where is a standard Brownian motion. The drift and the diffusion are known functions. Several well-known models in financial econometrics, including Black and Scholes, (1973), Vasicek, (1977), Cox et al., (1980), Chan et al., (1992) and Ait-Sahalia, (1996), among others, can be written under the form (5.2) with a specific form of drift and diffusion functions. Below the list of SDE models considered here.

-

N1:

Vasicek:

-

N2:

Hyperbolic:

-

N3:

CIR:

-

N4:

CKLS1:

-

N5:

CKLS2:

-

N6:

Aït-Sahalia:

In practice, the diffusion process is observed at instants , where is generally small, but fixed as increases. For instance the series could be observed hourly, daily, weekly or monthly. Therefore, we may model these discretely observed measurements using time series models. In fact, despite the fact that (5.2) is written in a continuous-time form, one often uses the following Euler discretization scheme to get

| (5.3) |

as an approximation that facilitates computational and theoretical derivation. The accuracy of such Euler discretisation is studied in Jacod and Protter, (1998). The purpose of this simulation study is to generate processes satisfying the SDEs described by models N1–N6 above, then use the procedures described in Section 4 to test whether the data fits a specific type of SDE models. Two types of null hypotheses will be considered. In the first sub-experiment we test if the data fits a Vasicek type SDE model, namely we test if is of the form for some parameters and that for some parameter . Note that only model N1 belongs to this class of models. In the second sub-experiment the null hypothesis considered is a CIR model where is of the form and of the form . For this second sub-experiment, N3 belongs to the null hypothesis.

We suppose the process is observed over the time interval and corresponds to the number of instants where the process is observed. The sampling mesh in such case is . In order to assess the sensitivity of our test to the sampling frequency from the underlying process, we consider and and , corresponding to a total sampling instants and respectively. Such framework supposes that collecting more observations means shortening the time interval between successive existing observations, not lengthening the time period over which data are recorded.

The data is generated according to one of SDE models listed above. The parameters are estimated, after discretization, using the maximum pseudo-likelihood method (see Aït-Sahalia, (2002)). Table 4 and 5 report the percentage of rejection of the two null hypotheses considered. The results are obtained using Monte-Carlo replications for different values of sampling mesh .

For the first sub-experiment, Table 4 shows that the tests are quite powerful in detecting change in the diffusion term. Alternatives N3–N6 are rejected with high probability even for . The three combined statistics are more or less similar in term of their detection power. As expected the statistics or do no detect change in the diffusion term. All statistics fail to detect the alternative N2 even for large sample sizes.

For the second sub-experiment, reported in Table 5, tests based on the original process and using either the multipliers procedure or the numerical approximation do respect their levels more appropriately than those based on the transformed process. The three combined statistics have the power to detect all alternatives considered here with N5 and N6 being easier to detect. This could be explained by the large change in the diffusion functions between N5 or N6 and the null hypothesis in this case N3.

| Transformation technique | Multipliers procedure | Numerical approximation | ||||||||||||||

| n | DGP | |||||||||||||||

| N1 | 6.1 | 4.1 | 4.7 | 4.6 | 5.1 | 6.1 | 4.1 | 3.8 | 4.1 | 4.7 | 5.2 | 3.7 | 3.5 | 3.6 | 4 | |

| N2 | 5.1 | 5.9 | 5.2 | 4.9 | 5.3 | 6.6 | 4.2 | 4.2 | 4.4 | 5.9 | 5.8 | 4.1 | 4.3 | 4.1 | 4.5 | |

| 100 | N3 | 2.4 | 95 | 84.8 | 87.8 | 82.5 | 4.9 | 98.4 | 98.3 | 98.4 | 94.1 | 4.9 | 98.6 | 98.3 | 98.6 | 93.3 |

| N4 | 6.1 | 84.4 | 73.1 | 76.1 | 70.9 | 4 | 90.7 | 90 | 90.7 | 79.4 | 3.7 | 90.8 | 90.2 | 90.8 | 77.3 | |

| N5 | 9.2 | 92.4 | 82.8 | 82.9 | 81.9 | 4.9 | 91.5 | 90.6 | 91.5 | 80.7 | 5.1 | 92.3 | 91.5 | 92.2 | 79.9 | |

| N6 | 11.3 | 88.9 | 80.3 | 79.3 | 78.6 | 10.2 | 91.1 | 89.4 | 91.1 | 77.9 | 9.3 | 91.3 | 90 | 91.3 | 75.9 | |

| N1 | 5.2 | 5.5 | 5.4 | 5.2 | 5.2 | 6.9 | 4.7 | 4.5 | 5.2 | 5.4 | 7.6 | 4.6 | 4 | 4.8 | 4.7 | |

| N2 | 5.9 | 6.1 | 4.9 | 5.6 | 4.8 | 6.5 | 3.9 | 3.8 | 3.9 | 5.4 | 6.3 | 3.9 | 4.1 | 4 | 4.7 | |

| 200 | N3 | 4.1 | 100 | 99.8 | 99.9 | 99.5 | 5.6 | 100 | 100 | 100 | 99.6 | 5.7 | 100 | 100 | 100 | 99.7 |

| N4 | 7.5 | 96.5 | 94.7 | 94.4 | 94.1 | 4.1 | 98.2 | 98.2 | 98.2 | 96.1 | 3.9 | 98.2 | 98.1 | 98.2 | 95.8 | |

| N5 | 10.7 | 99.5 | 97.8 | 98.7 | 97.4 | 5.1 | 98.9 | 98.7 | 98.9 | 95.9 | 4.8 | 98.7 | 98.6 | 98.7 | 96.8 | |

| N6 | 11.4 | 99.4 | 98.3 | 98.7 | 97.8 | 6 | 99.6 | 99.6 | 99.6 | 97 | 6.3 | 99.6 | 99.5 | 99.6 | 97.3 | |

| N1 | 4.9 | 5.5 | 5.3 | 5.4 | 6.4 | 8.2 | 4.8 | 5.6 | 5.1 | 7.7 | 8.3 | 4.3 | 5.5 | 4.7 | 6.3 | |

| N2 | 5.1 | 6.4 | 5.6 | 5.7 | 5.8 | 7.1 | 4.3 | 4.6 | 4.4 | 5.3 | 6.8 | 4.4 | 4.6 | 4.5 | 4.7 | |

| 500 | N3 | 4.1 | 100 | 100 | 100 | 100 | 5.5 | 100 | 100 | 100 | 100 | 5.2 | 100 | 100 | 100 | 100 |

| N4 | 8.6 | 100 | 100 | 100 | 100 | 6.4 | 100 | 100 | 100 | 100 | 6 | 100 | 100 | 100 | 100 | |

| N5 | 11.8 | 100 | 100 | 100 | 100 | 4.4 | 100 | 99.8 | 99.9 | 99.9 | 4.4 | 100 | 99.8 | 99.8 | 99.9 | |

| N6 | 13.7 | 100 | 100 | 100 | 100 | 7.6 | 100 | 100 | 100 | 99.9 | 7.8 | 100 | 100 | 100 | 99.9 | |

| Transformation technique | Multipliers procedure | Numerical approximation | ||||||||||||||

| n | DGP | |||||||||||||||

| N1 | 4.8 | 50.1 | 38.9 | 39.6 | 38.9 | 4.4 | 30.9 | 27.1 | 30.5 | 23.2 | 3.6 | 31.4 | 26 | 29.7 | 20.7 | |

| N2 | 4.9 | 63.3 | 53.9 | 53.5 | 52.9 | 4.3 | 42.2 | 37.5 | 41.3 | 30.4 | 4 | 42.3 | 36 | 40.4 | 28.9 | |

| 100 | N3 | 4.1 | 10.2 | 7.3 | 8.2 | 6.4 | 4.5 | 3.9 | 3.8 | 4.2 | 4.9 | 4 | 4.9 | 3.8 | 4.5 | 4.4 |

| N4 | 5.4 | 10.5 | 9.4 | 7 | 10.1 | 3.8 | 24.6 | 19.2 | 23.6 | 16.5 | 3.3 | 25.5 | 19.2 | 23.8 | 16.3 | |

| N5 | 10.6 | 54 | 40.7 | 35.7 | 41.7 | 5.8 | 70.1 | 65.9 | 69.7 | 52.2 | 5.3 | 71.9 | 66.1 | 70.7 | 51.7 | |

| N6 | 10.2 | 51.1 | 42.9 | 37.5 | 44 | 7.6 | 53.8 | 50.5 | 53.7 | 39.5 | 6.4 | 55.2 | 50 | 55 | 37.6 | |

| N1 | 5.4 | 71.2 | 62.2 | 63.6 | 61 | 5.5 | 55.7 | 50.8 | 52.7 | 45.1 | 4.7 | 54.9 | 49.6 | 52.1 | 44.4 | |

| N2 | 4.9 | 85.5 | 79.9 | 80.6 | 79.1 | 5.8 | 77.6 | 70.9 | 75.8 | 64.3 | 5.2 | 76.1 | 70 | 74.7 | 63.9 | |

| 200 | N3 | 5.9 | 9.8 | 8.5 | 9.6 | 8.2 | 5.3 | 4.7 | 4.5 | 4.5 | 5.3 | 5.7 | 4.6 | 4.4 | 4.1 | 4.5 |

| N4 | 6.3 | 24.1 | 19.3 | 17.5 | 19.7 | 3.9 | 51.4 | 46.6 | 49.6 | 39.7 | 4.2 | 50.4 | 45.5 | 49.1 | 38.5 | |

| N5 | 11.7 | 88.2 | 79.2 | 77.5 | 79.0 | 5.1 | 95.4 | 95.1 | 95.3 | 89.0 | 4.6 | 95.4 | 95.1 | 95.4 | 88.3 | |

| N6 | 12.2 | 84.3 | 75.7 | 73.3 | 74.8 | 7.1 | 87.7 | 87.0 | 87.7 | 76.9 | 6.8 | 88.1 | 86.8 | 88.1 | 77.6 | |

| N1 | 7.6 | 94.3 | 91.6 | 91.8 | 90.9 | 6.7 | 88.4 | 85.2 | 87 | 84.2 | 6.9 | 89.1 | 85.6 | 86.9 | 83.5 | |

| N2 | 7.1 | 98.4 | 97.1 | 96.8 | 97.3 | 4.6 | 96.3 | 94.7 | 96 | 93 | 4.4 | 96.5 | 94.5 | 96 | 92.2 | |

| 500 | N3 | 4.8 | 9.3 | 7.8 | 8 | 7.6 | 4.6 | 4.3 | 3.9 | 4.3 | 3.9 | 4.5 | 3.8 | 3.4 | 3.8 | 4 |

| N4 | 7.5 | 64.8 | 56.3 | 54.5 | 55.9 | 4.3 | 82.1 | 81.3 | 81.9 | 75.9 | 4.3 | 82 | 81.5 | 81.6 | 75.7 | |

| N5 | 13.0 | 99.9 | 99.4 | 99.3 | 99.3 | 6.0 | 100.0 | 99.7 | 99.8 | 99.8 | 5.7 | 99.7 | 99.7 | 99.7 | 99.6 | |

| N6 | 14.9 | 99.7 | 99.7 | 99.4 | 99.6 | 9.2 | 99.8 | 99.7 | 99.8 | 99.5 | 8.7 | 99.8 | 99.7 | 99.8 | 99.5 | |

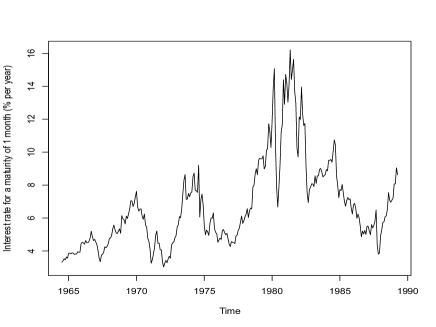

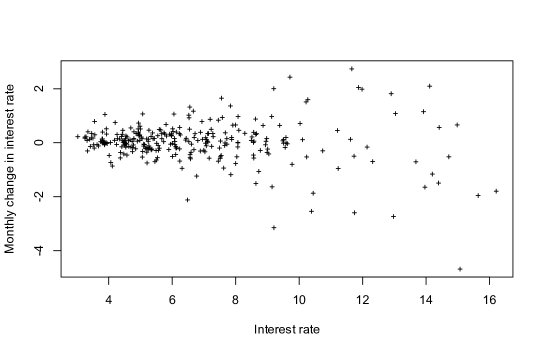

6 Application to interest rate data

This section presents as application the testing methodology to interest rate dynamics. Monthly values of interest rate for a maturity of 1 months (% per year) from July 1964 to April 1989 are considered. The monthly interest rate dynamic is displayed in Figure 1. Figure 2 is a scatter plot of monthly changes in interest rate against the previous month’s rate and it clearly shows an obvious heteroscedasticity, with the range of changes increasing significantly as the level of interest rates increases. An augmented Dickey-Fuller test of non stationarity of interest rate data is performed and the non stationarity hypothesis is rejected, with p-value equal to 0.01, for 1 to 12 months lagged series.

The aim here is to verify if the interest rate data described above fits a selected diffusion model. The following models will be considered as candidates

-

(D1)

Vasicek:

-

(D2)

Hyperbolic:

-

(D3)

Aït-Sahalia 1:

-

(D4)

CIR:

-

(D5)

CKLS 1:

-

(D6)

CKLS 2:

-

(D7)

Aït-Sahalia 2:

The procedure consists in fitting the interest rate data to each of the models outlined above and then apply the statistics described of Section 4 to see how good is the model fit. Table 6 reports the p-values resulting from applying the statistics discussed in Section 4 after fitting each of the models D1–D7 to the monthly interest rate data. As expected, all models with constant conditional volatility (D1-D3) are clearly rejected even when we considered different drift functions.

| Test | D1 | D2 | D3 | D4 | D5 | D6 | D7 | |

|---|---|---|---|---|---|---|---|---|

| 0.1432 | 0.1108 | 0.3589 | 0.1548 | 0.1574 | 0.1779 | 0.5179 | ||

| 0.0001 | 0.0001 | 0.0000 | 0.0018 | 0.0096 | 0.7873 | 0.7937 | ||

| Transformation technique | 0.0001 | 0.0002 | 0.0002 | 0.0028 | 0.0128 | 0.3911 | 0.7779 | |

| 0.0001 | 0.0002 | 0.0001 | 0.0036 | 0.0191 | 0.3241 | 0.7676 | ||

| 0.0001 | 0.0002 | 0.0002 | 0.0026 | 0.0113 | 0.4153 | 0.7765 | ||

| 0.2840 | 0.3080 | 0.5130 | 0.5370 | 0.6410 | 0.8170 | 0.9850 | ||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0020 | 0.6080 | 0.5920 | ||

| Multipliers procedure | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0020 | 0.7800 | 0.8350 | |

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0020 | 0.7060 | 0.6680 | ||

| 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0098 | 0.8443 | 0.8976 | ||

| 0.2566 | 0.2893 | 0.5424 | 0.5302 | 0.6522 | 0.8286 | 0.9868 | ||

| 0.0000 | 0.0001 | 0.0000 | 0.0001 | 0.0010 | 0.6077 | 0.6126 | ||

| Numerical approximation | 0.0000 | 0.0002 | 0.0000 | 0.0002 | 0.0019 | 0.7812 | 0.8343 | |

| 0.0000 | 0.0001 | 0.0000 | 0.0001 | 0.0010 | 0.7169 | 0.6908 | ||

| 0.0001 | 0.0003 | 0.0001 | 0.0008 | 0.0056 | 0.8490 | 0.9088 |

Models D4 and D5 are also rejected, implying that the rate in the diffusion function of the monthly interest rate is not or . On the other hand, all tests cannot reject the D6 and D7 implying that the diffusion of the interest rate is proportional to . This conclusion is in perfect concordance with existing findings in the literature (see for instance Aït-Sahalia, (1999)). In fact, the rate of was the recommended choice in Ait-Sahalia, (1996), among others, in a study of the same interest rate data.

7 Conclusion

Though Khmaldze matringale transform is quite popular as it simplifies the asymptotic behavior, its finite sample behavior is in general far from being the best compared to re-sampling or numerical approximation of the original statistics. We also notice that even the level of tests based on Khmaladze transform was sensitive to the estimation of the function , defined in (3.1). In our case, the estimation function used a non-parametric estimate of the derivative of the function and we noticed that the level was sensitive to the bandwidth parameter utilized in the estimation. The level of the tests obtained by numerical approximation or re-sampling of the original statistics are stable and close to their target values. Tests, using the original cumulative residual process, are in general more powerful than the ones based on martingale transformation. Moreover, as mentioned earlier, p-values of the combined statistics based on the transformed process are only computable when the components and are independent. Whereas p-values for the multipliers procedure for both and are obtained in the same manner whether the components and are independent or not. For the approximation technique, the algorithm described in the manuscript provides the p-values of whether the components and are independent or not. For we used the independence of and to simplify our computation, but the process can be generalized to the dependent case by approximating the distribution of the maximum of two dependent quadratic forms of normal random variables. The computations involved in the approximation techniques are extremely fast. As mentioned in the paper, the computation involved in the multipliers bootstrap are quite fast since the parameters are estimated only once and that each bootstrap iteration just requires generating i.i.d normal mean zero and variance one random variables. The combined statistics , and have similar power behavior in general, but is much easier to compute and its p-values are easier to obtain. We, therefore, recommend practitioners to use tests based on the original process more often with a multipliers procedure or a numerical approximation technique. Among these statistics would be the easiest to implement. The tests introduced in this manuscript are in general a bit more powerful than those in Escanciano, (2010), but there are alternatives, like A1, where tests in Escanciano, (2010) clearly outperform those discussed here.

The procedures discussed here generalize to the case of multivariate time series where . The procedure based on the multipliers bootstrap would be the easiest to generalize. In fact, it will not require any modification it suffices to adjust the definition of the process and the functions and to the multivariate case. The generalization of the numerical approximation and that of the martingale transform would need more technical work.

Appendix A Proofs

We start by proving the next Lemma which is used repeatedly in the proofs. It establishes a uniform law of large number result needed to show that the convergence is uniform in for both theorems (3.1) and (4.1).

Lemma A.1.

If , is strictly stationary and ergodic series satisfying and if is strictly stationary and ergodic series then, we have

-

i)

converges to zero almost surely,

-

ii)

If and satisfy the conditions of Theorem 3.1 then

converges to zero almost surely for and for every satisfying invertible.

Proof.

The proof of i) and ii) are quite similar. Here only the proof of ii) is given. For i) one repeats the same steps. One also can see that i) is similar to 4.1 in Koul and Stute, (1999). Though ii) can be deduced from of ULLN of Andrews, (1992) if the set of ’s is compact. Since this is not the case here, a direct proof using a Glivenko-Cantelli type argument shall be given next. First recall that is invertible for all whenever is invertible and that one can easily verify that . One also sees that

since satisfies the condition of Theorem 3.1. The LLN for stationary ergodic sequence yields the almost sure convergence of ii) for every fixed . To prove that the convergence is uniform in one uses a Glivenko-Cantelli type argument applied using . Note that is a continuous increasing function and for all one has . Therefore for every there exist a finite partition such that . To ease presentation, let

and

Note that for any there exists such that . Clearly, Using its definition one sees that

One also easily verifies that . Therefore

The pointwise LLN and the fact that is finite implies that the first and last terms in the above inequality converge almost surely to zero. Since was arbitrary, one concludes that converges to zero almost surely. ∎

A.1 Proof of Theorem 2.3

The weak convergence of follows from Theorem 1 in Escanciano, 2007b . For , direct manipulations show that

where

and

Note that converges in probability to zero by Lemma A.1, the definition of and the fact that . By Assumption (A3), the term is bounded by which converges to zero in probability by the LLN and the fact that . Therefore, is asymptotically equivalent to . Calling on Assumption (A2), one verifies that is tight and converges to and that converge jointly to . Hence converges to . Straightforward computations show the covariance function of is precisely given by (2.7).∎

A.2 Proof of Theorem 2.5

The proof follows the same approach as that of Theorem 2.3. Precisely, one writes

where

and

converges uniformly to by Lemma A.1. Assumption (L1) and Lemma A.1, yield that converges to . From Assumption (A3), one concludes that the term is uniformly bounded by which goes to zero in probability since and by Assumption (L3), and .∎

A.3 Proof of Theorem 3.1

The proof of Theorem (3.1) is as follows. First, in Lemma A.2 we establish, for that is asymptotically equivalent to . Second, using the continuous mapping theorem, one concludes that converges to . Then the proof is completed by showing that is equal to which has the same law as .

Lemma A.2.

Under the assumptions of Theorem 3.1, converges to zero in probability for .

Proof.

To prove the Lemma, observe that

First, one establishes that is tight and that converges to zero in probability, where and . For the tightness of , set . Note that is a marked empirical process its tightness follows, from Escanciano, 2007b and Assumption (K4). Next, using the same decomposition as in the proof of Theorem 2.3, one sees that

The above with tightness of and assumptions (A3-A4, K4) imply the tightness of . For , the decomposition in the proof of Theorem 2.3, shows that

which converges to zero by assumptions and the LLN.

Next, it will be shown that converges to zero in probability. Observe that

The first term above is equal

which converges to almost surely zero by Lemma (A.1) and Assumption (K2).

The second term is bounded by which goes to zero in probability by assumptions.

As pointed earlier, for all one has non-negative definite implying that is invertible whenever is invertible and that . Using the above result for and classical algebraic manipulations one also easily see that .

To complete the proof of the Lemma A.2 note that

Direct computations show that

Hence

Using Lemma (4.1) in Koul and Stute, (1999) and the fact that is tight, one concludes that the first term in the above goes to zero in probability. Term 2 is bounded by where

and

Since is tight and , the proof is complete by noting that, using the assumptions and the above results, for converge to zero in probability.

The transformation is linear and continuous which implies that converges to since direct computations show that . Straightforward computations, similar to those in Stute et al., (1998), enable us to verify that has the same distribution as where is standard Brownian motion. ∎

A.4 Proof of Theorem 4.1

Theorem 4.1 will be shown by establishing parts and below

-

is asymptotically equivalent to

-

converge in Law to independent copies of

Proof of :

Straightforward computations show that

, where

and

The term converges to zero in probability by Lemma A.1, term converges in probability to zero uniformly for all following the same steps as for the term in the proof of Theorem 2.3. By Assumption (M1), which goes to zero in probability. One also sees that . Next, since by the multiplier central limit theorem, then the term converge uniformly to zero in probability.

since by Assumption (M3). Finally, by Assumption (M2),

Combining these results, yields which completes the proof of part .

Proof of :

One notices that the multiplier central limit theorem yields the weak convergence of . It just remain to show that the asymptotic covariance operator of the process is the same as that of the limiting process

where One has only to consider the terms with in the above sums, since for . Recalling that , one sees that the above covariance reduces to Straightforward computations show that

which is the same as the covariance of the process . ∎

References

- Ait-Sahalia, (1996) Ait-Sahalia, Y. (1996). Testing continuous-time models of the spot interest rate. The review of financial studies, 9(2):385–426.

- Aït-Sahalia, (1999) Aït-Sahalia, Y. (1999). Transition densities for interest rate and other nonlinear diffusions. The journal of finance, 54(4):1361–1395.

- Aït-Sahalia, (2002) Aït-Sahalia, Y. (2002). Maximum likelihood estimation of discretely sampled diffusions: a closed-form approximation approach. Econometrica, 70(1):223–262.

- Andrews, (1992) Andrews, D. W. (1992). Generic uniform convergence. Econometric theory, 8(2):241–257.

- Auestad and Tjøstheim, (1990) Auestad, B. and Tjøstheim, D. (1990). Identification of nonlinear time series: First order characterization and order determination. Biometrika, 77(4):669–687.

- Bachelier, (1900) Bachelier, L. (1900). Théorie de la spéculation. In Annales scientifiques de l’École normale supérieure, volume 17, pages 21–86.

- Bai, (2003) Bai, J. (2003). Testing parametric conditional distributions of dynamic models. Review of Economics and Statistics, 85(3):531–549.

- Bai and Ng, (2001) Bai, J. and Ng, S. (2001). A consistent test for conditional symmetry in time series models. Journal of Econometrics, 103(1-2):225–258.

- Black and Scholes, (1973) Black, F. and Scholes, M. (1973). The pricing of options and corporate liabilities. Journal of political economy, 81(3):637–654.

- Bollerslev, (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. J. Econometrics, 31(3):307–327.

- Chan et al., (1992) Chan, K. C., Karolyi, G. A., Longstaff, F. A., and Sanders, A. B. (1992). An empirical comparison of alternative models of the short-term interest rate. The journal of finance, 47(3):1209–1227.

- Chen and An, (1997) Chen, M. and An, H. Z. (1997). A kolmogorov-smirnov type test for conditional heteroskedasticity in time series. Statistics & probability letters, 33(3):321–331.

- Chen et al., (2015) Chen, Q., Zheng, X., and Pan, Z. (2015). Asymptotically distribution-free tests for the volatility function of a diffusion. Journal of econometrics, 184(1):124–144.

- Cox et al., (1980) Cox, J. C., Ingersoll Jr, J. E., and Ross, S. A. (1980). An analysis of variable rate loan contracts. The Journal of Finance, 35(2):389–403.

- Dahl and Iglesias, (2007) Dahl, C. and Iglesias, E. ((2007). Asymptotic normality of the qmle of stationary and nonstationary garch with serially dependent innovations. Manuscript, pages 2–36.

- Deheuvels and Martynov, (1996) Deheuvels, P. and Martynov, G. V. (1996). Cramér-von mises-type tests with applications to tests of independence for multivariate extreme-value distributions. Communications in Statistics-Theory and Methods, 25(4):871–908.

- Dette et al., (2007) Dette, H., Neumeyer, N., and Keilegom, I. V. (2007). A new test for the parametric form of the variance function in non-parametric regression. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(5):903–917.

- Diebolt, (1990) Diebolt, J. (1990). Testing the functions defining a nonlinear autoregressive time series. Stochastic processes and their applications, 36(1):85–106.

- Drost and Nijman, (1993) Drost, F. C. and Nijman, T. E. (1993). Temporal aggregation of GARCH processes. Econometrica, 61(4):909–927.

- Durlauf, (1991) Durlauf, S. N. (1991). Spectral based testing of the martingale hypothesis. J. Econometrics, 50(3):355–376.

- Engle, (1982) Engle, R. F. (1982). Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica: Journal of the Econometric Society, pages 987–1007.

- (22) Escanciano, J. C. (2007a). Model checks using residual marked empirical processes. Statistica Sinica, 17(1):115–138.

- (23) Escanciano, J. C. (2007b). Weak convergence of non-stationary multivariate marked processes with applications to martingale testing. Journal of Multivariate Analysis, 98(7):1321–1336.

- Escanciano, (2008) Escanciano, J. C. (2008). Joint and marginal specification tests for conditional mean and variance models. Journal of Econometrics, 143(1):74–87.

- Escanciano, (2010) Escanciano, J. C. (2010). Asymptotic distribution-free diagnostic tests for heteroskedastic time series models. Econometric Theory, 26(3):744–773.

- Escanciano and Mayoral, (2010) Escanciano, J. C. and Mayoral, S. (2010). Data-driven smooth tests for the martingale difference hypothesis. Computational Statistics & Data Analysis, 54(8):1983–1998.

- Escanciano et al., (2018) Escanciano, J. C., Pardo-Fernández, J. C., and Van Keilegom, I. (2018). Asymptotic distribution-free tests for semiparametric regressions with dependent data. The Annals of Statistics, 46(3):1167–1196.

- Fisher, (1950) Fisher, R. A. (1950). Statistical Methods for Research Workers. Oliver and Boyd, London, 11h edition.

- Genest and Rémillard, (2004) Genest, C. and Rémillard, B. (2004). Tests of independence or randomness based on the empirical copula process. Test, 13:335–369.

- Ghoudi et al., (2001) Ghoudi, K., Kulperger, R. J., and Rémillard, B. (2001). A nonparametric test of serial independence for time series and residuals. J. Multivariate Anal., 79:191–218.

- Gonçalves and White, (2004) Gonçalves, S. and White, H. (2004). Maximum likelihood and the bootstrap for nonlinear dynamic models. J. Econometrics, 119(1):199–219.

- González-Manteiga and Crujeiras, (2013) González-Manteiga, W. and Crujeiras, R. M. (2013). An updated review of goodness-of-fit tests for regression models. Test, 22(3):361–411.

- Imhof, (1961) Imhof, J.-P. (1961). Computing the distribution of quadratic forms in normal variables. Biometrika, 48(3/4):419–426.

- Jacod and Protter, (1998) Jacod, J. and Protter, P. (1998). Asymptotic error distributions for the euler method for stochastic differential equations. The Annals of Probability, 26(1):267–307.

- Khmaladze, (1988) Khmaladze, E. (1988). An innovation approach to goodness-of-fit tests in . The Annals of Statistics, 16(4):1503–1516.

- Koul and Song, (2010) Koul, H. L. and Song, W. (2010). Conditional variance model checking. Journal of Statistical Planning and Inference, 140(4):1056–1072.

- Koul and Stute, (1999) Koul, H. L. and Stute, W. (1999). Nonparametric model checks for time series. The Annals of Statistics, 27(1):204–236.

- Kristensen and Rahbek, (2005) Kristensen, D. and Rahbek, A. (2005). Asymptotics of the QMLE for a class of models. Econometric Theory, 21(5):946–961.

- Laïb, (1999) Laïb, N. (1999). Nonparametric testing for correlation models with dependent data. Journal of Nonparametric Statistics, 12(1):53–82.

- Laïb, (2003) Laïb, N. (2003). Non-parametric testing of conditional variance functions in time series. Australian & New Zealand Journal of Statistics, 45(4):461–475.

- Laïb and Chebana, (2011) Laïb, N. and Chebana, F. (2011). A simultaneous test for conditional mean and conditional variance functions in time series models with martingale difference innovations. Statistical Methodology, 8(2):221–241.

- Laïb and Louani, (2002) Laïb, N. and Louani, D. (2002). On the conditional homoscedasticity test in autoregressive model with arch error. Communications in Statistics-Theory and Methods, 31(7):1179–1202.

- McKeague and Zhang, (1994) McKeague, I. W. and Zhang, M.-J. (1994). Identification of nonlinear time series from first order cumulative characteristics. The Annals of Statistics, pages 495–514.

- Merton, (1970) Merton, R. C. (1970). A dynamic general equilibrium model of the asset market and its application to the pricing of the capital structure of the firm. Sloan School of Management Working Paper, No. 497-70.

- Ngatchou-Wandji, (2002) Ngatchou-Wandji, J. (2002). Weak convergence of some marked empirical processes: Application to testing heteroscedasticity. Journal of Nonparametric Statistics, 14(3):325–339.

- Pardo-Fernández et al., (2015) Pardo-Fernández, J. C., Jiménez-Gamero, M. D., and El Ghouch, A. (2015). Tests for the equality of conditional variance functions in nonparametric regression. Electronic Journal of Statistics, 9(2):1826–1851.

- Polonik and Yao, (2008) Polonik, W. and Yao, Q. (2008). Testing for multivariate volatility functions using minimum volume sets and inverse regression. Journal of econometrics, 147(1):151–162.

- Shorack and Wellner, (1986) Shorack, G. and Wellner, J. (1986). Empirical processes with applications to statistics. 1986. John Wiley&Sons.

- Stute, (1997) Stute, W. (1997). Nonparametric model checks for regression. The Annals of Statistics, pages 613–641.

- Stute et al., (2006) Stute, W., Quindimil, M. P., Manteiga, W. G., and Koul, H. (2006). Model checks of higher order time series. Statistics & probability letters, 76(13):1385–1396.

- Stute et al., (1998) Stute, W., Thies, S., Zhu, L.-X., et al. (1998). Model checks for regression: an innovation process approach. The Annals of Statistics, 26(5):1916–1934.

- Vasicek, (1977) Vasicek, O. (1977). An equilibrium characterization of the term structure. Journal of financial economics, 5(2):177–188.

- Wang and Zhou, (2005) Wang, L. and Zhou, X.-H. (2005). A fully nonparametric diagnostic test for homogeneity of variances. Canadian Journal of Statistics, 33(4):545–558.

- Wooldridge, (1990) Wooldridge, J. M. (1990). A unified approach to robust, regression-based specification tests. Econometric Theory, 6(1):17–43.