On choosing optimal response transformations for dimension reduction

Abstract

It has previously been shown that response transformations can be very effective in improving dimension reduction outcomes for a continuous response. The choice of transformation used can make a big difference in the visualization of the response versus the dimension reduced regressors. In this article, we provide an automated approach for choosing parameters of transformation functions to seek optimal results. A criterion based on an influence measure between dimension reduction spaces is utilized for choosing the optimal parameter value of the transformation. Since influence measures can be time-consuming for large data sets, two efficient criteria are also provided. Given that a different transformation may be suitable for each direction required to form the subspace, we also employ an iterative approach to choosing optimal parameter values. Several simulation studies and a real data example highlight the effectiveness of the proposed methods.

Keywords principal Hessian directions, ordinary least squares, effective dimension reduction directions, sufficient summary plots, iterative dimension reduction.

1 Introduction

With advances in technology and decreases in data storage costs, we continue to collect more and more data. It is therefore becoming increasingly important to adapt existing methods to large data sets to visualise data sets that contain many attribute variables. Dimension reduction methods have proven to be a popular tool for the visualisation and modeling of multivariate data in a lower-dimensional framework.

In the setting of a random univariate continuous response variable, , and a random -dimensional predictor variable , Li, (1991) considered the dimension reduction model (DRM)

| (1) |

where is the unknown link function, are linearly independent -dimensional column vectors and is the error term independent of . It should be noted that a more general form of the DRM exists if we assume that is independent of given expressed as (see, e.g. Cook,, 1998b). However, we find the DRM in (1) convenient when discussing transformations of a continuous predictor.

The set, is referred to as the effective dimension reduction (e.d.r ) space and elements of the e.d.r space are e.d.r directions. For identifiability, we assume that is the Central Dimension Reduction subspace (CDRS, e.g. Cook,, 1998b), defined as the intersection of all dimension reduction subspaces.

In this setting, the aim of dimension reduction methods is to find a basis for . Since cannot be uniquely identified given that the link function is unknown, any set of directions such that span is sufficient. When , dimension reduction is achieved without loss of information when is replaced by .

Many dimension reduction methods exist, however there is no consensus as to which method is best. Performance depends on the unknown link function , the sample size and many other factors. For some models, some methods can only find a partial basis for or return very poor estimates of the basis, often due to the form of . In some such cases transformations of the response have proven to be effective (e.g. Li,, 1992; Garnham & Prendergast,, 2013). The fact that transformations can greatly improve dimension reduction outcomes motivates us to consider an automated approach to choosing parameters of transformation functions that produce optimal results.

Our automated approach is implemented on two existing dimension reduction methods, which will be introduced in Section 2. In Section 3, we introduce the response transformations and the criteria used to choose the optimal parameter value of the transformation. Simulated comparisons and a real-world example are considered in Section 4 and 5. Finally, concluding remarks are provided in Section 6 and further research discussed.

2 Dimension reduction and Influence measures

Since the introduction of Sliced Inverse Regression (SIR, Li,, 1991), which is capable of finding a basis for under some conditions, many other methods have followed. In this article, we focus on Ordinary Least Squares (OLS, Brillinger,, 1977, 1983) and Principal Hessian Directions Analysis (PHD, Li,, 1992), both of which are methods that can be used for dimension reduction that can benefit from response transformations.

Dimension reduction methods seek information regarding the form of the link function from (1) by reducing dimensionality to allow for a visual inspection using a Sufficient Summary Plot (SSP, Cook,, 1998b). The SSP is achieved by plotting against the reduced regressors . In the sample setting, let a sample of observations be denoted by . Then, an Estimated SSP (ESSP) is a plot of the ’s against the ’s, , ’s, where are the estimated e.d.r directions. So far we have not discussed how we can choose . This will be done when we discuss PHD shortly.

2.1 Ordinary Least Squares

OLS is commonly used in the multiple linear regression setting where is the population slope vector, is the covariance between and , and the variance-covariance matrix of . However, Brillinger, (1977, 1983) showed that OLS can be used as a dimension reduction method when , is additive and is Gaussian for the model in (1). Then, can be identified up to a multiplicative scalar, meaning that , for some as long as . Li & Duan, (1989) generalised this result without the need for a Gaussian or an additive error, only requiring the Linear Design Condition (LDC) to hold:

Condition 1 (LDC).

For any , is linear in .

The LDC holds when follows an elliptically symmetric distribution although this is not the only assumption under which it holds. When is large, Hall & Li, (1993) showed that the LDC will often approximately hold. Note here that even though OLS can be used for , it can only provide one informative direction and therefore a partial basis for .

Further, Li & Duan, (1989) showed that other linear regression methods with different convex criterion functions can also identify e.d.r. directions. Such methods include robust linear regression methods such as -estimators.

OLS can perform well with a wide variety of models. However, there are some cases where it can fail. One example is when the underlying relationship between and is symmetric about the mean of , in which case and no direction is found. Other examples that result in , or close to , are much less apparent. For example, Garnham & Prendergast, (2013) and Garnham, (2014) provide other examples where OLS fails, and also highlight the benefits of transforming the response.

2.2 Principal Hessian Directions

Li, (1992) used Stein’s Lemma (Lemma 4; Stein,, 1981) and the Hessian matrix to introduce principal Hessian direction (PHD) for identifying e.d.r directions. Assuming that , where and are the mean and variance-covariance matrix of respectively, then the average Hessian matrix of is given by,

| (2) |

where , where is the mean of . Then, the eigenvectors that correspond to nonzero eigenvalues of are elements of . The PHD estimation process is as follows:

- Step 1.

-

Standardise the ’s, so that where and are the sample mean and covariance of the ’s respectively.

- Step 2.

-

Calculate the estimate to the average Hessian matrix on the -scale as

where is the sample mean of the ’s.

- Step 3.

-

Carry out an eigen-decomposition of and let denote the eigenvectors associated with the ordered absolute eigenvalues

- Step 4.

-

Return as the estimated basis for .

In the above we have assumed that is known, however this is unlikely to be the case in practice. Under the normality assumption of and assuming the average Hessian matrix is of rank , Li, (1992) shows that

| (3) |

where the degrees of freedom is . Hence, this could be used iteratively to decide on a choice of . This will be discussed more later when we discuss the use of test statistics to guide transformation choices. For other methods on estimating see, for example, Cook, (1998a) and Ferré, (1998).

PHD is not guaranteed to find all directions (in which case the rank of the average Hessian matrix is less than ) and usually performs well in finding directions that have a non-linear association with the response. E.g, as an extreme example, the average Hessian matrix for the multiple linear regression model is equal to , so that only by chance can an eigenvector be informative. Cook, (1998b) referred to this phenomenon as elusive linear trends.

Li also pointed out that adding or subtracting a linear function of the predictor from does not change the Hessian matrix, and therefore proposed a variation of PHD where the response is replaced by the OLS residual. In some cases this residual-based PHD can be more successful, on average, in finding directions it is not expected to find (e.g., the elusive linear trends, Cook,, 1998b; Prendergast & Smith,, 2010). In this paper we focus on the -based PHD since the transformations we consider help to uncover these directions. However, the residuals could similarly be transformed and so the work that follows can be directly applied when residuals are used instead.

Li, (1992) provided an example of where a transformation can greatly benefit the PHD results. Also, Lue, (2001) showed that PHD is adversely affected by large values and that by trimming them improvements can be found. Hence, transformations that reduce the magnitude of observations relative to others may then also be helpful.

2.3 Iterative dimension reduction

Similarly as noted for PHD above, many dimension reduction methods can find only a partial basis for for some types of models. Shaker & Prendergast, (2011) introduced an iterative application of dimension reduction methods for estimating the full basis of . They proposed the use of different dimension reduction methods for each iteration to collectively form a basis of . They considered combinations of methods that naturally complement each other, e.g. PHD and OLS (as detailed above), SAVE and SIR (methods based on slicing) etc. In the iterative approach, the e.d.r direction obtained by the first method is removed from the dimension reduction matrix derived for the following method. This is done by pre- and post-multiplying the matrix with , where is the projection matrix onto and is the first e.d.r direction recovered (see, Proposition 3.1, Shaker & Prendergast,, 2011). This ensures that only new information regarding is obtained in the second iteration since the second direction will be an element of , where is the complement of .

When using OLS first followed by PHD (where we write PHDOLS since PHD is carried out conditional on a direction for OLS having already been found), this equates to carrying out an eigen-decomposition on

| (4) |

where is the normalised (i.e. ) OLS slope vector for the regression of the ’s on the ’s. In terms of the OLS slope, , for the regression of the ’s on the ’s, . Hence, the direction resulting from the decomposition of the above matrix will be orthogonal to that already found by OLS, and a new direction (or directions) can be added to estimate the basis for by re-standardising with respect to (as in Step 4 of the PHD algorithm).

2.4 Influence measures for dimension reduction

The Influence Function (IF; Hampel,, 1974) is commonly used for assessing the robustness properties of an estimator and these have been derived and studied in the context of dimension reduction (e.g. Prendergast,, 2005; Prendergast & Smith,, 2010). We are specifically interested in influence in the sample setting, where we wish to detect observations whose removal from the sample causes a big change in estimation. The aforementioned theoretical works regarding the IF have lead to the introduction of suitable sample versions for dimension reduction.

There are some challenges that need to be overcome when thinking of influence in the context of dimension reduction. We are interested in estimators of e.d.r directions that collectively estimate the dimension reduction subspace. Two subspaces that are equal in span contain exactly the same information for dimension reduction, and this has lead to several influence functions focusing on spans of directions (e.g., for principal component analysis, Bénasséni,, 1990). On the other hand, two subspaces can be different in span, yet produce almost identical ESSPs in our setting of dimension reduction. For example, suppose that the target e.d.r direction is and that we also have another candidate . These two directions are orthogonal to one another, yet the ESSPs (plots of the ’s versus the dimension reduced ’s using either of the directions) would be similar if the first two predictor variables were highly correlated. The amount of information lost if we replaced by depends on the underlying covariance structure of the predictors. Hence we need influence measures that can detect changes in the dimension reduced predictor space.

Let denote the predictor matrix whose th row is and let be the estimated OLS slope vector. Then Prendergast, (2008) considered the influence measure

| (5) |

where is the estimated OLS slope without the th observation and cor denotes the squared correlation between the two arguments.

In the case of , the average squared canonical correlation between the dimension reduced predictors based on estimation with and without the th observation are considered instead. Hence, Prendergast & Smith, (2010) provided a general form of the influence measure to be used with any and applicable to many dimension reduction methods, including OLS, and specifically used this measure to study robustness of PHD. The relative sample influence version of this measures is,

| (6) |

where is the average of the squared canonical correlations between and (where and is the matrix of the ’s (for ) estimated without the th observation).

Therefore, a large is obtained when there is a big difference between the e.d.r spaces, which means that the th observation has a comparatively large effect on estimation of the e.d.r space.

3 Optimal transformations for dimension reduction

We begin this section with a motivating example before introducing the methods and transformations.

3.1 A motivating example

Li, (1992) used the absolute value transformation to show how simple transformations can improve PHD estimation. In this article, one of the transformations we consider is a one-parameter mean-centered absolute value transformation. At the model level and for , this is defined as , where . In the sample setting we can apply this to each where we use the sample mean of the ’s, , as an estimate to .

Note that is just the mean-centered response and so the transformation makes no difference to estimation of the e.d.r space. is the absolute value of the mean-centered response and an provides a linear combination of the two.

PHD is excellent at detecting curvature (see, e.g. Li,, 1992; Cook,, 1998a) or similarly, non-linearity, and by mean centering the response we can be more hopeful of introducing some additional non-linearity when linear relationships are present. For example, when all the response values are positive, the absolute value transformation will not change anything. However, by mean centering first thereby shifting the response, then these negative values will be folded back to the positive domain creating non-linearity.

Consider the model,

| (7) |

where , is the ten-dimensional e.d.r direction to be estimated and independent of . As discussed in Section 2.2 we expect PHD to fail at finding an informative e.d.r direction estimate since the Hessian matrix is equal to .

We simulated observations, denoted from the model in (7) and applied PHD on the ’s with different values of set to . This produced 11 estimates of the e.d.r direction.

0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1 29.264 31.468 36.265 45.725 62.898 91.630 137.438 192.406 244.913 291.968 Cor2 0.884 0.862 0.830 0.778 0.697 0.578 0.436 0.309 0.219 0.160

The squared correlation between each and are shown in Table 1. Further, the average of the sample influence measure given in (6) associated with each estimate is shown. The optimal parameter value is the one that results in the largest squared correlation, in this case choice , which results in the absolute value of the mean-centered response. However, we can only calculate this because, unlike in practice, we know the true e.d.r direction for comparison.

The choice of resulting in the largest correlation also resulted in the lowest mean influence, . Unlike the correlation, we can compute this sample influence in practice and therefore use this to choose the best . On average, the estimate of the e.d.r. direction, when is chosen, is the least sensitive to the removal of an observation. The squared correlation decreases as increases towards one and conversely, the mean sample influence increases. The worst estimate occurs when which still corresponds to a linear model.

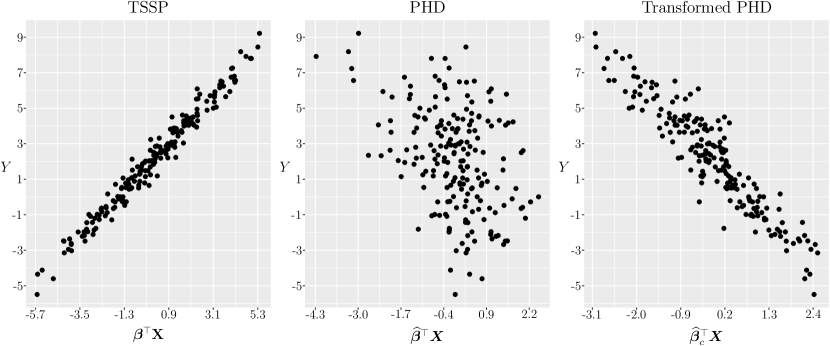

Compared to the true SSP (TSSP; left plot in Figure 1), the ESSP using PHD (middle plot) with no transformation shows that PHD failed to find an informative e.d.r direction for the model in (7). However, the PHD estimate using the ’s provides a very good ESSP (right plot) that depicts the linear relationship between and . Note here, that even though the ESSP shows a mirrored reflection of the TSSP, this simply means that PHD is estimating an e.d.r direction in the direction of .

This motivating example shows that the application of a one-parameter response transformation, along with a criterion for choosing the optimal parameter value of the transformation, can provide great improvements in the estimation of the e.d.r direction.

3.2 A method for optimal parameter selection

As shown by the motivating example, using a variation of the absolute transformation considered by Li, (1992), can greatly improve the estimation of the PHD method. Other works have also further emphasised the benefits of response transformations; for an example of transformations for PHD refer to Li, (1992), and to Garnham & Prendergast, (2013) for a discussion of transformations for OLS. Garnham, (2014) provides an extended discussion of transformations for both PHD and OLS.

Finding a single direction

Similar to the motivating example of Section 3.1 using an absolute value transformation and a criterion of minimal mean influence, we consider a general framework for any transformation and criteria.

Let denote a transformation function with parameter value . For the single index model with , the algorithm for selecting the optimal parameter value is straightforward:

- Step 1:

-

Transform the ’s using for chosen values of .

- Step 2:

-

Perform dimension reduction on the transformed responses and , and obtain for each in Step 1.

- Step 3:

-

Select the optimal based on a chosen criterion (e.g. based on minimal mean influence) and denote that as .

- Step 4:

-

Return as the estimated e.d.r. direction.

Finding multiple directions

The above method can also be used for , where instead of returning only the first e.d.r direction, we return the first two or more estimates. However, our initial explorations highlighted that improvements could be obtained using transformations to find directions, instead of a single transformation of the response (i.e. a single choice of the parameter ). Additionally, a single transformation may only find a partial basis for . Therefore, for , we adopt the iterative approach from Shaker & Prendergast, (2011) to perform iterations of the above method where either the same or different dimension reduction methods can be used for each iteration. Furthermore, the same or different response transformations can be implemented in each iteration.

Below we assume that PHD is the method to be used to obtain a second direction, although suitable variations of this are possible. As an example, the iterative approach with algorithm continues as follows:

- Step 5:

-

Calculate the for chosen values of , where (and the choices of ) can be the same or different to that used for the first iteration.

- Step 6:

-

Let be the e.d.r direction estimated in the first iteration. Then,

- Step 6.1:

- Step 6.2:

-

Obtain for each value of where is the eigenvector that corresponds to the largest non-zero eigenvalue of .

- Step 7:

-

Using a chosen criteria, determine the optimal transformation parameter value denoted .

- Step 8:

-

Return as the estimated second e.d.r direction.

Remark 1.

For to be a projection matrix, we need to ensure that it is idempotent, or in this case, ensure that . If OLS is used first, then (see Eqn. 4). If PHD is used first, then where is the eigenvector corresponding to the largest eigenvalue in Step 3 of the PHD algorithm (where, in our approach, and were produced using the appropriate optimally transformed responses).

Note that this algorithm searches for each direction in turn. A more exhaustive search can also be implemented: for example, for each possible pair of where these are values for the transformation parameters, compute every pair of estimated e.d.r. directions using the iterative dimension reduction approach and choosing the pair based on a criterion. However, this is very time-consuming, especially in the high-dimensional setting and our explorations did not reveal any substantial improvements.

Finally, we limited the approaches above to or . These choices of allow for visualisation of the response versus the dimension reduced predictors using scatterplots. However, it is possible that , in which case Steps 5 to 7 can be repeated but where is used to remove all previous components. More on this can be found in Shaker & Prendergast, (2011).

3.3 Response Transformations

Response transformations do not affect Condition 1, required for OLS, or the normality condition of the predictors for PHD. Hence, the following transformations, and others, can be used for the improvement of the e.d.r direction estimates of the OLS and PHD methods. When defining the transformations we do so with respect to the random response and note that in practice these are applied to the observed responses, ’s, and where appropriate the sample mean of the ’s, , is used as an estimate to .

Box-Cox transformation

OLS was conceptualized in the setting of linear models, and it was not until later that it was realised it could also be used in dimension reduction for many more models (e.g. Li & Duan,, 1989). However, seeking to linearize the response has been shown to benefit OLS estimation in many cases, and we can be hopeful that such transformations are of benefit in the dimension reduction framework. To this end we consider the Box-Cox transformation (Box & Cox,, 1964) given as:

| (8) |

Note that we have limited the parameter since we found that the best choice was usually in this range. It should also be pointed out that this transformation does not help to improve performance when the problem of symmetric dependency occurs. For example, if is symmetric about the mean of , such as when where , then the OLS vector is equal to . The BC transformation will not fix this problem, although other transformations are possible in this situation (Prendergast & Garnham,, 2016).

Mean-centered absolute transformation

For convenience we restate the transformation used in our motivating example (Section 3.1):

| (9) |

Mean-centered absolute Box-Cox transformation

Recalling that PHD does not like linear trends, we combine elements of the above two transformations to first introduce some possible element of linearity, before applying the absolute mean-centered transformation to benefit PHD. This is given as:

| (10) |

For convenience in what follows, we use the following to identify methods using the above transformations.

- BC-OLS:

-

OLS using the Box-Cox transformation.

- -PHD:

-

PHD using the mean-centered absolute transformation ().

- -PHD:

-

PHD using the mean-centered Box-Cox transformation .

- -PHDBC-OLS:

-

PHD for the second e.d.r. direction using transformation , conditional on the first direction found by BC-OLS.

- -PHD -PHD:

-

PHD for the second e.d.r. direction using transformation , conditional on the first direction found by PHD using transformation .

3.4 Criteria for choosing the optimal parameter value

We now introduce three criteria that can be used to choose the optimal parameter value of a transformation.

Minimum influence criterion

In Section 2.4 we presented the generalised sample influence measures derived by Prendergast & Smith, (2010) for dimension reduction with many methods including OLS and PHD and for any . Then in Section 3.1 we chose the optimal parameter for the mean-centered absolute transformation using the mean influence across all observations. The first criterion uses this influence measure to determine the optimal parameter value of a transformation.

Let us consider BC-OLS. In this case, we let denote the set of transformation parameter values to be used and Step 3 of the algorithm for the single-index model () becomes:

- Step 3:

-

Let denote the average of the influence values in (6) where the OLS slope vectors are estimated using the BC transformed ’s with parameter value . Then the optimal parameter value is

Step 3 is the same for the -PHD and -PHD methods.

This also extends to the iterative methods (for ) where Step 7 is performed in the same way. Note that we only have to consider influence associated with the new direction found at this step. This is because the first direction is fixed, so that the first squared canonical correlation from (6) will be trivially equal to one since the first direction appears identically in both and . We also provide the following comment on the use of the influence measures.

A disadvantage of using the minimum influence criterion is that many leave-one-out computations are required. The influence can be computed quicker for OLS even for large data sets compared to the PHD which involves an eigen-decomposition each time an observation is removed. If we are doing this for choices of the transformation parameter, then total eigen-decompositions are required (for each direction to be found). Prendergast & Smith, (2010) provide an empirical influence measure that quickly approximates in (6). However, the approximation is poor when the method performs poorly and so is unreliable in this setting where some transformations may result in poor estimates. This means that the empirical influence measure cannot be used for its efficiency and that the ’s should be used. Therefore, we also introduce two time-efficient criteria that do not require leave-one-out computations.

Furthermore, Garnham, (2014) derived the theoretical influence diagnostic for the OLS e.d.r space following a response transformation and provided an efficient empirical version that can be used in practice to approximate the OLS ’s under the response transformation setting. This measure can also be used in our approach to chose the optimal parameter value of the transformation.

Maximum eigenvalue ratio criterion

We take advantage of the nature of the eigenvalues of the average Hessian matrix to provide a time-efficient criterion for choosing the optimal parameter value of a transformation. We determine the optimal parameter value by identifying the maximum eigenvalue ratio. Consider, for example, the transformation and let denote the PHD eigenvalues based on estimation with the ’s. Then, the ratio of the sum of the eigenvalues associated with the e.d.r. direction estimators, to the sum of all the eigenvalues, for a given parameter value is,

where the ’s are the eigenvalues estimated from the PHD using the ’s with a particular value of . Larger ratios indicate the e.d.r. directions that are more prominent in the eigen-decomposition of the Hessian matrix. Then the optimal parameter value is,

While this approach could be used to simultaneously estimate more than one e.d.r. direction (e.g. choose to find a single transformation that results in the largest two eigenvalues relative to the sum of all eigenvalues), recall that we found different transformations were needed to improve estimation of individual directions. Hence, in our algorithms we choose either to find a single direction, or to iteratively seek more than one direction.

Maximum evidence criterion

Another efficient way to seek the optimal parameter value is to choose the parameter that maximizes a test statistic used as evidence against . First, we consider a standard test for determining when using PHD. Tested sequentially over , the hypotheses are defined to be

where the number of e.d.r. directions to form the basis is the first for which is not rejected. From Theorem 4.2 of Li, (1992), a test statistic for a fixed where denotes the sample variance of the ’s is

| (11) |

Hence, to start and for the transformation as an example, let (i.e. so that ) denote the test statistic above but where PHD estimation has been carried out with the ’s. Then

so that we choose the transformation that maximises the evidence in favour of there being at least one e.d.r. direction. The most prominent PHD direction can then be used either as the only direction for a model or as the next direction in the iterative dimension reduction.

4 Simulations

In this section we present simulated examples that demonstrate the performance of the proposed methods in estimating the e.d.r direction(s) of the OLS and PHD methods.

For assessing the performance of the dimension reduction methods used in this section, we provide tables of the average squared correlations, in the case of , and average squared canonical correlations, in the case of , between the true and estimated dimension reduced regressors. In addition, we provide the boxplots of the squared correlations or the squared canonical correlations, for and respectively, for all of the methods compared in each example. For each model we perform 1000 simulated runs for each combination of the different and values chosen. For all examples, we simulate and independent of .

4.1 Single-index models

For dimension reduction with , we consider the following models,

Model 1 with .

Model 2 with .

For Model 4.1, we perform simulated runs for each combination of and and and . We compared the performance of all the methods for focusing on the OLS and BC-OLS methods. For each run of Model 4.1, the BC-OLS method was performed with parameter values from to in increments of and the minimum influence criterion was used to choose the optimal parameter value.

| n | p | OLS | BC-OLS |

| 50 | 5 | 0.864 ( 0.093 ) | 0.987 ( 0.010 ) |

| 10 | 0.734 ( 0.113 ) | 0.971 ( 0.016 ) | |

| 20 | 0.569 ( 0.116 ) | 0.939 ( 0.026 ) | |

| 200 | 5 | 0.926 ( 0.060 ) | 0.997 ( 0.002 ) |

| 10 | 0.848 ( 0.086 ) | 0.993 ( 0.003 ) | |

| 20 | 0.732 ( 0.108 ) | 0.986 ( 0.005 ) | |

| 500 | 5 | 0.953 ( 0.044 ) | 0.999 ( 0.001 ) |

| 10 | 0.904 ( 0.062 ) | 0.997 ( 0.001 ) | |

| 20 | 0.819 ( 0.091 ) | 0.994 ( 0.002 ) | |

| 1000 | 5 | 0.969 ( 0.032 ) | 0.999 ( 0.000 ) |

| 10 | 0.935 ( 0.051 ) | 0.999 ( 0.001 ) | |

| 20 | 0.869 ( 0.078 ) | 0.997 ( 0.001 ) |

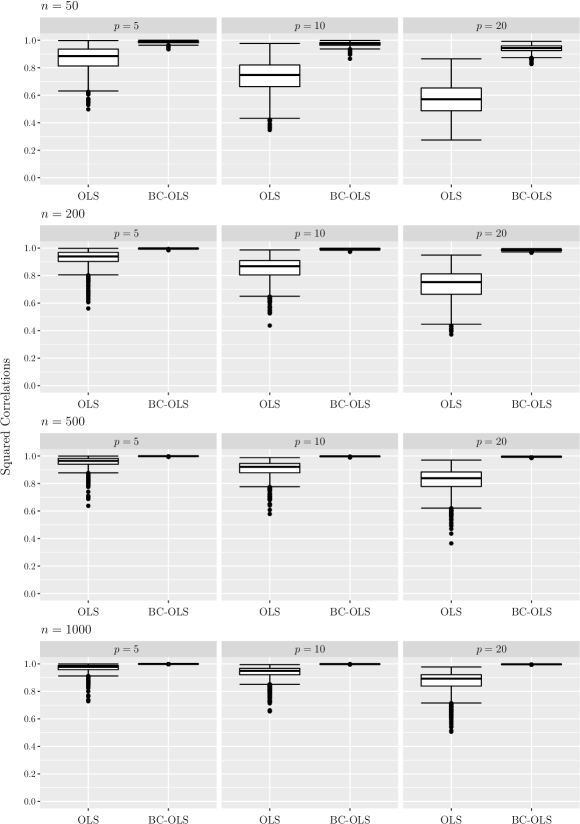

For OLS, we observe that the average squared correlations in Table 2 decrease when dimensionality increases. However, as sample size increases the performance of OLS also improves, on average. This indicates that OLS performance declines under the high-dimensional, low sample-size setting and generally can be more sensitive when is large.

For BC-OLS, the average squared correlations in Table 2 show that the method performs extremely well for this model across all choices of and . Furthermore, changes in the average squared correlations, as dimensionality increases, are much smaller than the OLS method, indicating that BC-OLS is less sensitive to large values of . The standard deviations also show that there is very small estimator variability in the results of BC-OLS which highlights consistently good estimates of the direction.

The boxplots of the squared correlations for the OLS and BC-OLS methods in Figure 2 support the findings of Table 2. Even though OLS can perform well, especially for small , the BC-OLS method provides obvious improvements for Model 4.1, for each combination of the and choices. Furthermore, the greater variability of the OLS correlations is clearly shown indicating that consistently good estimates are not achieved when compared to the BC-OLS method.

In Table 3 we report the frequency by which a specific value of was chosen as optimal, by the minimum influence criterion for the BC-OLS method, across the 1000 simulated runs from Model 4.1 and for each combination of and values. There is decreased variability of the optimal parameter values chosen for versus the other choices of and also a shift towards a value between 0 to as increases. Hence, something very close to the log transformation is typically chosen as optimal.

50 200 500 1000 5 10 20 5 10 20 5 10 20 5 10 20 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1 0 0 9 4 4 13 2 1 46 31 15 177 151 127 393 393 371 154 112 124 597 590 636 775 801 848 595 602 625 0.0 531 571 536 357 377 349 47 48 25 3 1 0 0.1 271 286 305 0 2 0 0 0 0 0 0 0 0.2 29 29 34 0 0 0 0 0 0 0 0 0 0.3 2 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

For Model 4.1, we performed 1000 simulated runs for each combination of the different choices of and 1000 and and 20. We compared the results of the default against the proposed methods for , focusing on the comparison between the PHD, PHD with transformation (-PHD) and with transformation (-PHD).

Both -PHD and -PHD provided substantial improvements and similar results, on average. Therefore, for simplicity we only report and discuss the results of -PHD and note that there was a little more variability when using the transformation. Note that in each run of the -PHD method, the transformation is performed with parameter values from to in increments of 0.1. Throughout, we will denote the -PHD method applied with each of the aforementioned criteria by -PHDρ (minimum influence), -PHDΛ (maximum eigenvalue ratio) and -PHD (maximum evidence), respectively.

| PHD | -PHDρ | -PHDΛ | -PHD | ||

| 100 | 5 | 0.174 ( 0.215 ) | 0.850 ( 0.250 ) | 0.769 ( 0.317 ) | 0.865 ( 0.208 ) |

| 10 | 0.070 ( 0.101 ) | 0.649 ( 0.350 ) | 0.575 ( 0.370 ) | 0.637 ( 0.334 ) | |

| 20 | 0.031 ( 0.049 ) | 0.235 ( 0.305 ) | 0.150 ( 0.234 ) | 0.215 ( 0.289 ) | |

| 500 | 5 | 0.167 ( 0.223 ) | 0.985 ( 0.013 ) | 0.979 ( 0.055 ) | 0.984 ( 0.013 ) |

| 10 | 0.068 ( 0.098 ) | 0.963 ( 0.022 ) | 0.962 ( 0.023 ) | 0.963 ( 0.023 ) | |

| 20 | 0.029 ( 0.044 ) | 0.920 ( 0.050 ) | 0.917 ( 0.059 ) | 0.912 ( 0.078 ) | |

| 1000 | 5 | 0.174 ( 0.222 ) | 0.992 ( 0.006 ) | 0.992 ( 0.007 ) | 0.992 ( 0.006 ) |

| 10 | 0.069 ( 0.107 ) | 0.983 ( 0.010 ) | 0.982 ( 0.010 ) | 0.983 ( 0.010 ) | |

| 20 | 0.024 ( 0.036 ) | 0.962 ( 0.017 ) | 0.962 ( 0.017 ) | 0.962 ( 0.018 ) |

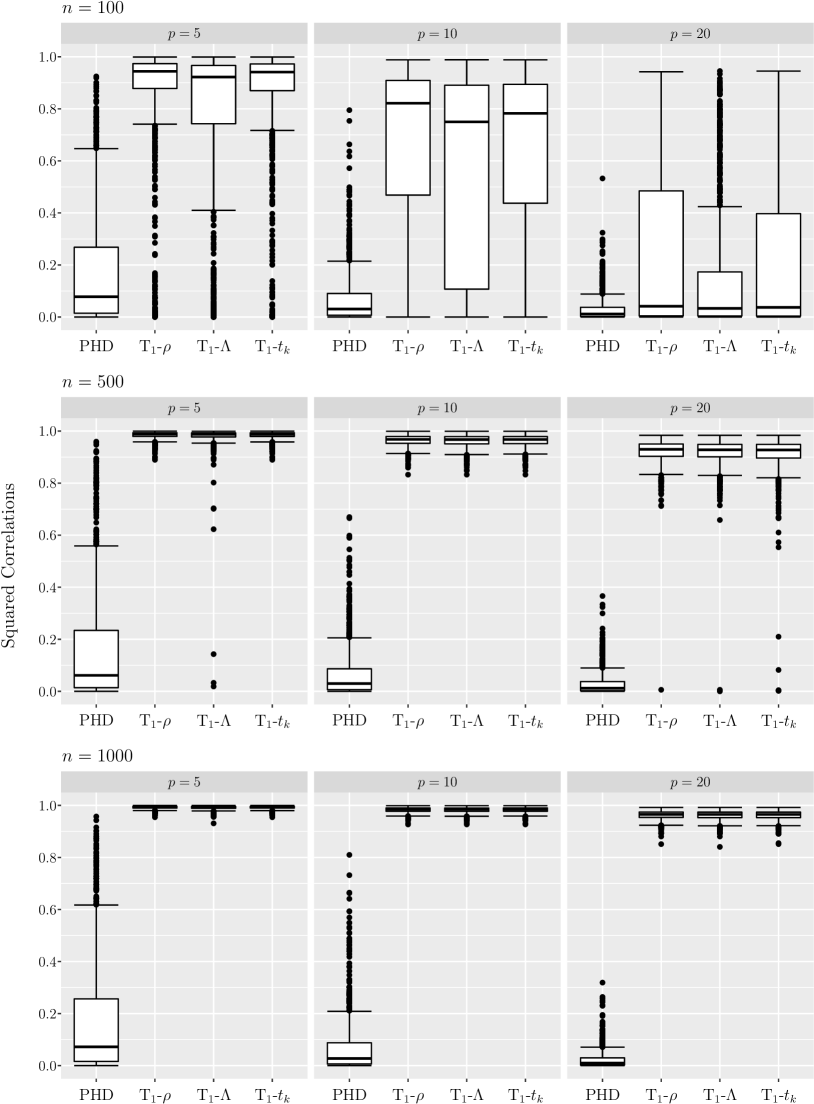

The average squared correlations in Table 4 show that PHD performs poorly for Model 4.1, whereas the -PHD methods perform extremely well with similar results provided by the different criteria. Generally, PHD does not perform well when the sample-size is small and in higher dimensions. This is true, to a smaller extent, for the -PHD methods, which even though they provide good improvements when , they show a greater variability in estimation. For the larger sample sizes of and , large improvements are achieved whereas PHD continues to fail. Furthermore, both the maximum eigenvalue ratio () and the maximum evidence () criteria provide results very close to those of the minimum influence criterion for this model.

The boxplots of the PHD, -PHDρ, -PHDΛ and -PHD squared correlations in Figure 3 support the above interpretations, clearly showing the variability and reduced performance of the -PHD method in the high-dimensional low sample-size setting. They also highlight the big improvements using the response transformation in the estimation of the dimension reduced regressors when compared to PHD.

Table 6 shows the counts of the optimal parameter values chosen from the different criteria ( and ) across 1000 simulated runs from Model 4.1 for the different values of and for the -PHD method. The counts show greater variability when which is expected due to PHD’s sensitivity to small sample-sizes. However, as increases the frequencies are concentrated mainly in two choices. The optimal parameter value chosen most often by all three criteria for Model 4.1 is , which means that the optimal transformation will probably be, .

100 500 1000 5 5 10 20 0.0 631 485 655 555 420 550 289 176 426 814 597 917 866 691 843 945 788 728 914 629 977 950 743 961 960 846 875 0.1 225 137 220 196 155 198 159 71 142 185 213 83 134 263 155 54 201 226 86 225 23 50 235 39 40 154 124 0.2 50 116 70 37 110 99 114 80 109 1 119 0 0 45 2 1 8 40 0 109 0 0 22 0 0 0 1 0.3 18 59 28 28 56 37 52 187 74 0 52 0 0 1 0 0 1 2 0 30 0 0 0 0 0 0 0 0.4 9 40 7 31 48 25 50 244 47 0 11 0 0 0 0 0 1 1 0 6 0 0 0 0 0 0 0 0.5 17 25 3 24 57 12 27 129 17 0 2 0 0 0 0 0 1 3 0 1 0 0 0 0 0 0 0 0.6 11 26 1 20 30 10 26 31 18 0 1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0.7 6 20 1 19 20 5 38 7 13 0 3 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0.8 6 14 15 12 11 1 48 1 6 0 2 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0.9 3 18 0 15 8 3 47 1 4 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1.0 24 60 0 63 85 60 150 73 144 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

| -PHDρ | -PHDΛ | -PHD | |

| 1.6143 | 0.0250 | 0.0790 | |

| 26.7699 | 0.0300 | 0.0610 | |

| 102.6824 | 0.0200 | 0.1375 |

Finally, Table 6 clearly shows that the time taken to perform the -PHD method with the minimum influence criterion () increases rapidly when the sample size increases. Increases in dimensionality would result in further increased times. However, the -PHD method with the maximum eigenvalue () and maximum evidence () criteria is performed very quickly with very small changes across the different sample sizes. We see that the and criteria are very efficient and capable of providing an improved e.d.r direction estimate. These calculations were performed using an AMD Ryzen 7 2700X Eight-Core Processor 3.70 GHz processor with 32.0 GB RAM using RStudio Version 1.3.1056 with R version 4.0.2.

4.2 Multiple-index models

Li, (1992) considered the following model to demonstrate how simple response transformations can aid PHD in improving estimation of the e.d.r directions. Here, we will use the same model to compare the estimation of the e.d.r predictors of PHD with and without the proposed iterative response transformations approach. An error term of the appropriate size has been added to the original model to form a more realistic example. So, for dimension reduction with , the first model we consider is,

Model 3 where , .

For Model 4.2 we performed 1000 simulated runs of the PHD, -PHD -PHD and -PHD -PHD methods, for each combination of and 1000 and and 20. We focus on the results given by the default PHD and compare them with the -PHD -PHD method which showed the best improvements. For brevity, we will denote the iterative -PHD method with each of the criteria, as -PHD, -PHD and -PHD, respectively.

n p PHD -PHD -PHD -PHD 200 5 0.633 ( 0.325 ) 0.910 ( 0.143 ) 0.846 ( 0.179 ) 0.917 ( 0.115 ) 10 0.490 ( 0.285 ) 0.805 ( 0.163 ) 0.648 ( 0.249 ) 0.763 ( 0.199 ) 20 0.356 ( 0.228 ) 0.593 ( 0.223 ) 0.414 ( 0.238 ) 0.523 ( 0.242 ) 500 5 0.646 ( 0.316 ) 0.961 ( 0.057 ) 0.895 ( 0.122 ) 0.968 ( 0.036 ) 10 0.511 ( 0.295 ) 0.910 ( 0.079 ) 0.761 ( 0.200 ) 0.909 ( 0.078 ) 20 0.398 ( 0.245 ) 0.813 ( 0.113 ) 0.527 ( 0.262 ) 0.755 ( 0.177 ) 1000 5 0.656 ( 0.318 ) 0.976 ( 0.040 ) 0.919 ( 0.105 ) 0.984 ( 0.017 ) 10 0.534 ( 0.283 ) 0.950 ( 0.051 ) 0.808 ( 0.181 ) 0.955 ( 0.037 ) 20 0.429 ( 0.250 ) 0.892 ( 0.082 ) 0.621 ( 0.260 ) 0.884 ( 0.091 )

Table 7 shows the average of the squared canonical correlations for each of the aforementioned methods, across 1000 simulated runs from Model 4.2, for each combination of the and values chosen. The corresponding standard deviations are given in parentheses. The results indicate that the default PHD performs poorly and with greater variability, as seen by the standard deviations, compared to the three variations of the iterative -PHD method which provide significant improvements. Furthermore, the maximum evidence () criterion performs slightly better and with less variability than the maximum eigenvalue ratio () criterion, and provides similar results to those of the minimum influence () criterion.

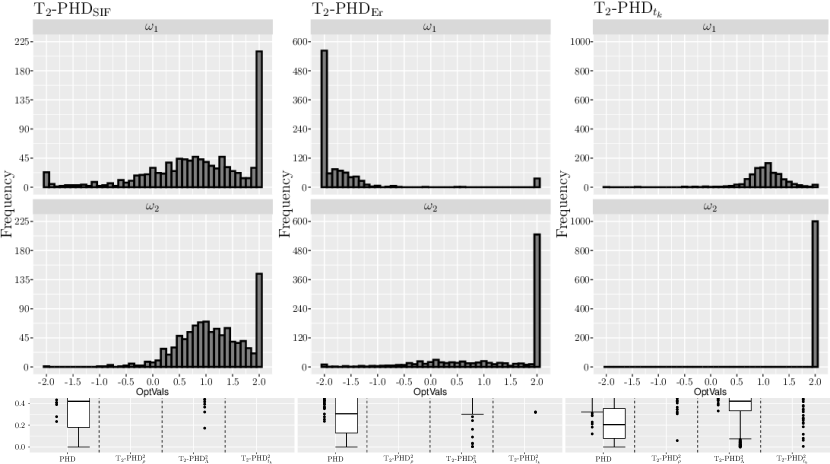

In Figure 4, we present the boxplots of the squared canonical correlations of each of the methods, across 1000 simulated runs for each choice of and , to show the performance of the methods in greater detail. The boxplots show that PHD can estimate only a partial basis well, when dimensionality is low, but performance deteriorates for both directions as the dimension increases.

On the other hand, all three variants of the iterative -PHD method show improved estimates for both directions. The results decline as the dimension increases but improve further when sample size increases. As mentioned earlier, the and criteria were proposed as alternatives to the criterion for time efficiency and can provide different results for the same model. Here, the criterion is similar to the criterion whereas the shows smaller, and in some cases insufficient, improvements in estimation, for Model 4.2.

5 10 20 Criterion 72 6 836 2 0 0 34 1 822 16 1 0 26 1 927 77 53 0 22 2 122 9 0 0 12 0 122 9 2 0 4 0 54 59 10 0 46 12 12 26 0 0 19 5 11 18 0 0 7 4 1 61 20 0 56 17 1 74 0 0 30 8 6 38 4 0 16 8 0 55 18 0 87 60 1 89 0 0 87 19 1 67 11 0 38 8 0 55 42 0 107 91 1 88 9 0 106 87 0 83 23 0 112 61 0 38 77 0 108 164 0 93 119 0 175 209 2 69 183 0 207 213 0 24 176 0 110 209 0 73 655 0 144 252 0 70 530 0 169 264 0 14 309 0 75 172 0 89 200 0 125 185 0 50 204 0 167 224 0 7 155 0 317 267 27 457 17 1000 268 234 36 580 42 1000 254 217 18 610 140 1000

In Table 8, we present the counts of the optimal parameter values chosen by the -PHD, -PHD and -PHD methods, for and and 20. In each iteration, the -PHD method was performed for to in increments of 0.1. For brevity, we chose to group the parameter value choices in intervals, so that the counts represent the frequency by which parameter values within a particular interval were chosen as optimal across the 1000 simulated runs. The frequencies highlight the similarities between the and criteria on the choice of optimal parameter values, and the difficulty of the criterion in finding the optimal value for one of the e.d.r directions of Model 4.2. This is also evident from the boxplots of the -PHD method that show a poor performance in finding a good estimate for the second e.d.r direction.

The final model we consider is,

Model 4 where ,

For Model 4.2 we consider the results of the PHD, PHDOLS, -PHD -PHD, -PHD -PHD, -PHDBC-OLS and -PHDBC-OLS methods. Each method was performed for 1000 simulated runs from Model 4.2, for each combination of and 1000, and and 20. Here, we only report the results of the PHD, PHDOLS and -PHDBC-OLS methods where the later provided the biggest improvements compared to the other methods considered for this example. The PHDOLS method is considered to allow for the comparison between the iterative approach (Shaker & Prendergast,, 2011) and the iterative transformations approach (both of which allow for different dimension reduction methods to be used in each iteration).

PHD PHDOLS PHDρ BC-OLS PHDΛ BC-OLS PHD BC-OLS 200 5 0.510 ( 0.379 ) 0.647 ( 0.393 ) 0.882 ( 0.181 ) 0.786 ( 0.284 ) 0.863 ( 0.202 ) 10 0.345 ( 0.320 ) 0.561 ( 0.419 ) 0.781 ( 0.246 ) 0.658 ( 0.348 ) 0.750 ( 0.270 ) 20 0.246 ( 0.249 ) 0.501 ( 0.422 ) 0.668 ( 0.287 ) 0.541 ( 0.392 ) 0.639 ( 0.309 ) 500 5 0.512 ( 0.380 ) 0.657 ( 0.392 ) 0.939 ( 0.126 ) 0.842 ( 0.247 ) 0.925 ( 0.142 ) 10 0.360 ( 0.329 ) 0.570 ( 0.432 ) 0.873 ( 0.175 ) 0.724 ( 0.327 ) 0.845 ( 0.201 ) 20 0.275 ( 0.276 ) 0.522 ( 0.448 ) 0.795 ( 0.218 ) 0.611 ( 0.385 ) 0.760 ( 0.250 ) 1000 5 0.523 ( 0.379 ) 0.654 ( 0.396 ) 0.963 ( 0.093 ) 0.871 ( 0.221 ) 0.950 ( 0.115 ) 10 0.376 ( 0.340 ) 0.576 ( 0.434 ) 0.925 ( 0.129 ) 0.795 ( 0.292 ) 0.904 ( 0.151 ) 20 0.297 ( 0.292 ) 0.531 ( 0.456 ) 0.872 ( 0.157 ) 0.691 ( 0.359 ) 0.843 ( 0.187 )

The results in Table 9 indicate that PHDOLS is an improvement over the default PHD method which performs poorly for Model 4.2. However, PHDOLS still performs poorly, on average, and its performance is consistent across the different sample sizes and dimensions showing high estimator variability. The -PHDρ BC-OLS method has provided clear improvements over the PHD and PHDOLS methods where performance increases as sample sizes increases. Additionally, the results of the -PHD BC-OLS method are similar to those of the -PHDρ BC-OLS and show a better performance compared to the -PHDΛ BC-OLS with smaller standard deviations.

The boxplots of the canonical correlations for Model 4.2, in Figure LABEL:fig:SinCubeBox, show that PHDOLS can greatly improve one of the directions, when dimensionality is low, but completely fails to estimate the other direction. However, we obtain significant improvements by the -PHDρ BC-OLS and -PHD BC-OLS methods, where the estimator variability shown in Table 9 is mainly attributed to one of the directions of the model.

Finally, Table 10 shows the counts of the optimal values chosen by each iteration, for Model 4.2, across the simulated runs. The interpretation of this table is very similar to the previous example with the difference of the BC-OLS iteration which shows very consistent choices across the different values of . Note also that even though the and criteria choose different parameter values as optimal, the -PHD method still provides similar results to -PHDρ.

5 10 20 Criterion 0 17 160 0 0 16 302 0 0 17 471 0 0 8 103 0 0 8 115 0 0 2 144 0 0 5 129 0 0 5 96 0 0 3 80 0 2 9 126 0 0 9 76 0 0 8 37 0 5 31 77 0 2 18 58 0 0 15 36 0 67 79 59 0 47 74 35 0 17 38 25 0 242 175 47 0 264 201 25 0 248 195 15 0 314 263 27 0 369 288 32 0 427 304 13 0 205 178 21 1 202 181 12 0 213 221 4 0 165 235 251 999 116 200 249 1000 95 197 175 1000

5 Example

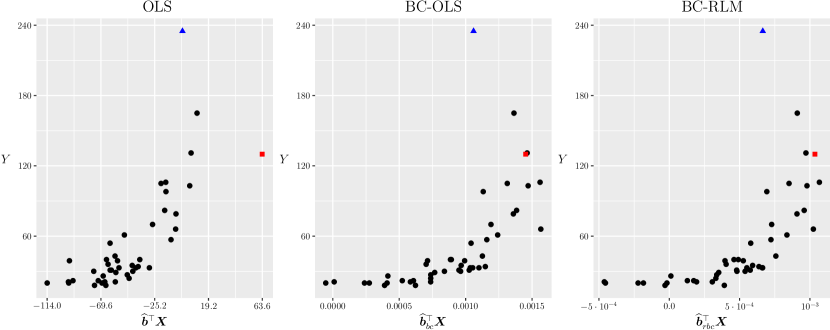

We consider the ‘bigmac’ dataset taken from Enz, (1991). The dataset contains the average values of 10 economic indicators in 1991 for 45 cities around the world. All prices are in US dollars, using currency conversion at the time of publication. We let the response be bigmac, which is the minimum labor required to buy a Big Mac and fries from MacDonalds in each city. Information of the 9 predictors are included in Table 11.

For this data we compare the performance of the OLS and BC-OLS methods, for . PHD, -PHD and -PHD were also considered but did not provide informative results. A second direction from the iterative OTDR methods also provided no additional information about the relationship between the bigmac and the 9 economic indicators.

Keep in mind, that it has previously been shown that removing outliers from the estimation of the OLS slope vector can provide improved ESSP’s (Olive,, 2004). Also, Prendergast, (2008) showed that trimming influential observations from the estimation but including them in the visualisation can have great benefits. Inspired by these, we used the influence measure given in (6) and found two influential observations in the data. By examining their behaviour, when removed from the data, we determined the presence of an outlier and a highly influential observation in the ‘bigmac’ data. In the ESSP given by OLS in Figure 5, the outlier is the observation at the very top whereas the influential observation is the one at the far right of the plot, shown by a triangle and a square respectively.

| Name | Info |

| Bread | Minimum labor to buy 1 kg bread |

| BusFare | Lowest cost of 10k public transit |

| EngSal | Electrical engineer annual salary, 1000s |

| EngTax | Tax rate paid by engineers |

| Service | Annual cost of 19 services |

| TeachSal | Primary teacher salary, 1000s |

| TeachTax | Tax rate paid by primary teachers |

| VacDays | Average days vacation per year |

| WorkHrs | Average hours worked per year |

We also decided to perform the proposed method using robust linear regression to avoid removing any observations. We denote this as BC-RLM and used the lm function in R, which uses M-estimatos that are less sensitive to outliers (see, for example, Huber,, 1981). Furthermore, note that influential observations when considering might not be influential when considering the optimally transformed . The same can be true for outliers.

The ESSPs in Figure 5 indicate that the BC-OLS method shows a clearer relationship, similar to exponential growth, between and than the default OLS method. Finally, the ESSP given by BC-RLM shows an even sharper view of the relationship between and .

Note here that the BC-OLS and BC-RLM methods chose the same optimal parameter value, , for the transformation. The optimal response transformation that provides the improved e.d.r estimates, , , for the data is, .

6 Discussion and further work

In this article, we demonstrated how response transformations can greatly improve the estimation of the e.d.r directions in dimension reduction with OLS and PHD. We have provided an automated method that searches for the optimal transformation for a given model while using the influence measure (Prendergast & Smith,, 2010) as a criterion to find the optimal parameter value of the transformation. Alternative criteria for choosing the optimal transformation have also been provided for time-efficiency in practice, which were shown to be able to perform almost as good as the minimum influence criterion. An iterative approach of this method was also provided to further improve estimation for the second or more directions. Simulated comparisons and a real-world example highlighted the success of the methods proposed and showed that we can achieve improved visualizations of the relationship between the response and predictor variables.

This method can be extended further by considering more transformations and using them to improve other dimension reduction techniques which then allows for more iterative dimension reduction combination methods.

References

- Bénasséni, (1990) Bénasséni, J. 1990. Sensitivity coefficients for the subspaces spanned by principal components. Commun. Stat. - Theory Methods, 19, 2021–2034.

- Box & Cox, (1964) Box, G. E.P., & Cox, D. R. 1964. An analysis of transformations. J. R. Stat. Soc.: Series B (methodological), 26, 211–243.

- Brillinger, (1977) Brillinger, D. R. 1977. The identification of a particular nonlinear time series system. Biometrika, 64, 509–515.

- Brillinger, (1983) Brillinger, D. R. 1983. A genralized linear model with “Gaussian" regressor variables. A Festschrift for Eric L. Lehmann, Wadsworth Statist. /Probab. Ser. Belmont, CA: Wadsworth, 97–114.

- Cook, (1998a) Cook, R. D. 1998a. Principal hessian directions revisited. J. Am. Stat. Assoc., 93, 84–94.

- Cook, (1998b) Cook, R. D. 1998b. Regression graphics. Ideas for studying regressions through graphics. New York: John Wiley & Sons Inc.

- Enz, (1991) Enz, R. 1991. Prices and Earnings Around the Globe. Zurich: Union Bank of Switzerland.

- Ferré, (1998) Ferré, L. 1998. Determining the dimension in sliced inverse regression and related methods. J. Am. Stat. Assoc., 93, 132–140.

- Garnham, (2014) Garnham, A. L. 2014. Improving modern dimension reduction methods through transformations. Ph.D. thesis.

- Garnham & Prendergast, (2013) Garnham, A. L., & Prendergast, L. A. 2013. A note on least squares sensitivity in single-index model estimation and the benefits of response transformations. Electron. J. Stat., 7, 1983–2004.

- Hall & Li, (1993) Hall, P., & Li, K.-C. 1993. On almost linearity of low dimensional projections from high dimensional data. Ann. Stat., 21, 867–889.

- Hampel, (1974) Hampel, F. R. 1974. The influence curve and its role in robust estimation. J. Am. Stat. Assoc., 69, 383–393.

- Huber, (1981) Huber, P. J. 1981. Robust statistics. John Wiley & Sons, Hoboken, NJ.

- Li, (1991) Li, K.-C. 1991. Sliced inverse regression for dimension reduction. J. Am. Stat. Assoc., 86, 316–327.

- Li, (1992) Li, K.-C. 1992. On Principal Hessian Directions for Data Visualization and Dimension Reduction: Another Application of Stein’s Lemma. J. Am. Stat. Assoc., 87, 1025–1039.

- Li & Duan, (1989) Li, K.-C., & Duan, N. 1989. Regression analysis under link violation. Ann. Stat., 17, 1009–1052.

- Lue, (2001) Lue, H.-H. 2001. A study of sensitivity analysis on the method of principal Hessian directions. Comput. Stat., 16(1), 109–130.

- Olive, (2004) Olive, D. J. 2004. Visualizing 1d regression. Pages 221–233 of: Hubert, M., Pison G. Struyf A. Van Aelst S. (ed), Theory and applications of recent robust methods. Basel, Switzerland: Birkhäuser Basel.

- Prendergast, (2005) Prendergast, L. A. 2005. Influence functions for sliced inverse regression. Scand. J. Stat., 32, 385–404.

- Prendergast, (2008) Prendergast, L. A. 2008. Trimming influential observations for improved single-index model estimated sufficient summary plots. Comput. Stat. Data Anal., 52, 5319–5327.

- Prendergast & Smith, (2010) Prendergast, L. A., & Smith, J. A. 2010. Influence functions for dimension reduction methods: An example influence study of principal hessian direction analysis. Scand. J. Stat., 37, 588–611.

- Prendergast & Garnham, (2016) Prendergast, L.A., & Garnham, A. L. 2016. Response and predictor folding to counter symmetric dependency in dimension reduction. Aust. N. Z. J. Stat., 58, 515–532.

- Shaker & Prendergast, (2011) Shaker, A. J., & Prendergast, L. A. 2011. Iterative application of dimension reduction methods. Electron. J. Stat., 5, 1471–1494.

- Stein, (1981) Stein, C. M. 1981. Estimation of the mean of a multivariate normal distribution. Ann. Stat., 9, 1135–1151.