Effect of Labour Income on the Optimal Bankruptcy Problem

Abstract: In this paper we deal with the optimal bankruptcy problem for an agent who can optimally allocate her consumption rate, the amount of capital invested in the risky asset as well as her leisure time. In our framework, the agent is endowed by an initial debt, and she is required to repay her debt continuously. Declaring bankruptcy, the debt repayment is exempted at the cost of a wealth shrinkage. We implement the duality method to solve the problem analytically and conduct a sensitivity analysis to the cost and benefit parameters of bankruptcy. Introducing the flexible leisure/working rate, and therefore the labour income, into the bankruptcy model, we investigate its effect on the optimal strategies.

Keywords: Power Utility Optimization, Bankruptcy Stopping Time, Consumption-Portfolio-Leisure Controls, Legendre-Fenchel Transform, Variational Inequalities

1 Introduction

In this paper, we study an optimal stopping time problem, in which an agent decides her consumption-portfolio-leisure strategy as well as the optimal bankruptcy time. Her utility is described by a power utility function concerning the consumption and leisure rates. Moreover, the leisure rate should be upper bounded by a positive constant (). Relating to the leisure rate, the agent earns the labour income with a fixed wage rate. The sum of labour and leisure rates is assumed to be constant . As the complement, the labour rate is lower bounded by a positive constant for the consideration of retaining the employment state. By determining the continuous and stopping regions of the corresponding stopping time problem, we prove that the optimal bankruptcy time is the first hitting time of the wealth process downward to a critical wealth boundary.

The idea is directly inspired by Jeanblanc et al. (2004), in which a stochastic control model is constructed to quantify the benefit of filing consumer bankruptcy in the perspective of complete debt erasure. Their research is a response to the sharp growth in bankruptcy cases between 1978 and 2003 due to the promulgation of the 1978 Bankruptcy Reform Act in American. The Act introduced two kinds of consumer bankruptcy mechanisms, which are reflected in its Chapter 7 and Chapter 13 separately: debtors following Chapter 7 to file bankruptcy are granted the debt exemption, but must undertake the liquidation of non-exempt assets. Alternatively, the mechanism in Chapter 13 adopts the reorganization procedure instead of the liquidation. Debtors are permitted to retain assets, but the debt is required to be reorganized and paid continuously from future revenues. The statistical data shows that filing bankruptcy under Chapter 7 predominates in all consumer bankruptcy cases (1,156,274 out of 1,625,208 cases in 2003, accounting for 72%).111Administrative Office of the U.S Courts, Table F-2— Bankruptcy Filings (December 31, 2003) [Online]. Available: https://www.uscourts.gov/statistics/table/f-2/bankruptcy-filings/2003/12/31 Following Jeanblanc et al. (2004), an affine loss function, , is established to serve the fixed and variable costs of filing bankruptcy, which corresponds to the mathematical description for the bankruptcy mechanism under Chapter 7. Here is the wealth level at the moment of bankruptcy , and represents the fixed cost of bankruptcy. Therefore, the bankruptcy option reduces the wealth from to , with a drop in wealth equal to . The loss of the proportion of the remaining wealth after the bankruptcy liquidation is related, for example, to taxes costs.

Compared to Jeanblanc et al. (2004), we make an extension in two aspects: firstly, a new control variable, the leisure rate, is inserted for a more realistic consideration; accordingly, the agent earns the labour income. For the introduction of the leisure as a control variable into the optimal stopping time problem, the reader can refer to (Choi et al., 2008; Farhi and Panageas, 2007), where authors studied the optimal retirement -from labour- model regarding the consumption-portfolio-leisure strategy. Different from these two researches, we consider the stopping time concerning the bankruptcy issue rather than the retirement: while the optimal retirement is the first hitting time of the wealth process to an upper critical wealth boundary (Barucci and Marazzina, 2012; Choi et al., 2008; Farhi and Panageas, 2007), the optimal bankruptcy is related to a lower boundary. This extension permits us to study the impact of the disutility from full work on the bankruptcy option. Secondly, in order to deal with a utility from consumption and leisure rate, we implement a different method from Jeanblanc et al. (2004), where the utility of the agent only depends on her consumption, solving the optimal problem with the duality method instead of the dynamic programming method, to deduce the solution analytically, as in (Barucci and Marazzina, 2012; Choi et al., 2008). We would like to stress that in this work we deal with the duality method applied to intertemporal consumption, for terminal utility problem the reader can refer, for example, to (Barucci et al., 2021; Colaneri et al., 2021; Nicolosi et al., 2018). The duality method throughout this paper can be summarized into four steps. We first tackle the post-stopping time problem to deduce a closed form of the corresponding value function. Then we apply the Legendre-Fenchel transform to the utility function and the value function of post-bankruptcy time problem obtained in the first step. Afterwards, we construct the duality between the optimal control problem with the individual’s shadow prices problem, by the aid of the liquidity and budget constraints and the dual transforms acquired before. Finally, we cast the dual shadow price problem as a free boundary problem, which leads to a system of variational inequalities and enables us to solve it analytically. The methodology discussed here refers to (He and Pages, 1993; Karatzas and Wang, 2000): in Karatzas and Wang (2000) authors applied the duality method to solve a discretionary stopping time problem explicitly, while in He and Pages (1993) authors used the duality approach to link the individual’s shadow price problem with the optimal control problem and investigated the impact of the liquidity constraint on the optimization.

Other related literatures are Karatzas et al. (1997), where authors studied the general optimal control problem involving the consumption and investment, and offered the solution in a closed-form, Sethi et al. (1995), where a general continuous-time consumption and portfolio decision problem with a recoverable bankruptcy option is considered, and Bellalah et al. (2019) where authirs address the role of labour earnings in optimal asset allocation.

In the numerical results part, we first of all conduct the sensitivity analysis with respect to the key bankruptcy parameters , and . The fixed toll and can be treated as the fixed and flexible bankruptcy costs; the debt is the continuous-time debt repayment. As already said, the optimal bankruptcy corresponds to the first hitting time of the wealth process of a downward boundary, the bankruptcy wealth threshold. This threshold, as a function of the debt repayment , is an increasing and convex curve. The rationale of this result is the following: a heavier debt repayment, in fact, implies that the benefit of bankruptcy becomes more attractive, therefore inducing the agent to take a higher threshold to make the bankruptcy requirement more accessible such that she can enjoy the debt exemption easily. Furthermore, the convexity of the mapping can be explained by the fact that this motivation is diminishing as the debt repayment decreases. Similar results hold true if we consider the bankruptcy threshold as a function of , i.e., the proportion of wealth after the bankruptcy liquidation: a lower value of indicates a higher flexible cost (a higher value of ) and pushes the agent to set a lower wealth level to avoid suffering the bankruptcy. Our numerical results also show the non-monotonic relationship between the bankruptcy wealth threshold and itself; this is due to the role of , which is not only the fixed cost of bankruptcy, but, according to the model in Jeanblanc et al. (2004), in order to make the problem feasible, it also has an important role as liquidity constraint in the pre-bankruptcy period. Moreover, comparing the optimal control policies between the model with and without the bankruptcy option, we find that this additional option offers the agent a better circumstance such that the optimal consumption-portfolio-leisure policies dominate the ones without it before the bankruptcy. Whereas, after declaring bankruptcy, the agent suffers the wealth shrinkage and prefers to invest less in the risky asset for the needs of obtaining utility from consumption and leisure. In addition, we also study the impact of introducing the leisure rate as a second control variable, such that the influence of labour income can be disclosed. The numerical result indicates that the optimal consumption and portfolio policies with the flexible leisure option always prevail over the corresponding policies of the model with a full leisure rate, and therefore without labour income.

The paper is organized as follows. Section 2 formulates the corresponding optimization problem, and provides the financial market setting. Section 3 offers the value function of post-bankruptcy problem and its Legendre-Fenchel transform. In Section 4, we construct the duality between the optimal control problem with the individual’s shadow price, and obtain a free boundary problem which endows us the closed-form optimal solutions. Section 5 presents the numerical tests to this model and the sensitivity analysis of the bankruptcy wealth threshold to main parameters. Finally, Section 6 concludes. Most of the proofs and computations are reported in the online appendix.

2 Problem Formulation

2.1 Financial Market

We first formulate the considered financial market over the infinite-time horizon. Based on the mutual fund theorem from Karatzas et al. (1997), we consider only one risky asset which dynamics follows the Geometric Brownian Motion with constant drift and diffusion coefficients. The agent faces two investment opportunities: the investment in the money market, which endows her a fixed and positive interest rate , and the risky asset, which dynamically evolves according to the stochastic differential equation (SDE)

| (2.1) |

Here, denotes a standard Brownian motion on the filtered probability space , is the augmented natural filtration on this Brownian motion, and represents the initial stock price, which is assumed to be a positive constant. Since the drift and diffusion terms and are positive constants, there exists a unique solution to the SDE , .

Then referring to Karatzas and Shreve (1998b), we introduce the state-price density process as , with , , the discount process and an exponential martingale, respectively defined as

Moreover, stands for the market price of risk, that is, the Sharpe-Ratio. Since the exponential martingale is, in fact, a -martingale, and both the number of risky assets and the dimension of the driving Brownian motions are equal to one, the financial market defined with the above setting, , is standard and complete, based on the result from (Karatzas and Shreve, 1998b, Section 1.7, Definition 7.3). Additionally, we can define an equivalent martingale measure through , . Then based on the Girsanov Theorem, we can get a standard Brownian motion under the measure as

| (2.2) |

2.2 The Optimization Problem

The agent optimally chooses the consumption rate, the amount of money allocated in the risky asset and the leisure rate, which are denoted as , and , treated as the three control variables in the optimization. The sum of the labour and leisure rate is constant and equals . Therefore, the working rate at time is that enables the agent to earn a wage of , where represents the constant wage rate. Obviously, the condition must be imposed for the positive labour income consideration. Furthermore, a realistic constraint is introduced into the model, that is, the working rate should be lower bounded by a positive constant for the sake of retaining the employment state.

Following Jeanblanc et al. (2004), an affine loss function is introduced for accommodating fixed and variable costs of filing bankruptcy. Let denote the bankruptcy time, the agent is obliged to repay continuously a positive fixed debt until the stopping time , whereas this debt obligation is exempted after declaring bankruptcy, but with the fixed cost and the variable cost , where the proportional coefficient takes the value in . In more detail, the agent needs to pay a fixed toll once for all at the time , and the proportion of the remaining wealth, which is related to the social cost, time cost and taxes cost of declaring bankruptcy. Therefore, the agent is able to keep the amount of wealth for the consumption and investment after bankruptcy. For the purpose of making sure that the agent is capable of affording the bankruptcy, the wealth level is required to cover the cost before the stopping time , that is, , , where is a small non-negative constant to guarantee that there is still a few amounts of wealth left even after the liquidation. The bankruptcy mechanism described above entails the wealth process to satisfy the following SDE

Furthermore, we assume that the agent’s preference is described by a power utility function of consumption and leisure rate

| (2.3) |

Setting makes the mixed second partial derivative negative,

which clarifies that consumption and leisure are substitute goods. The following lemma introduces the Legendre-Fenchel transform of the function , which will help us to reduce the number of control variables up to a single one. Referring to (Choi et al., 2008, Section 2.2), the Legendre-Fenchel transform of the utility function is defined as

| (2.4) |

and it is given in the following lemma.

Lemma 2.1.

The Legendre-Fenchel transform of the utility function is

with

Furthermore, the consumption-leisure policy reaching the supremum in (2.4) is

Proof.

See Appendix A.1. ∎

In this framework, the primal optimization problem, which is denoted as , is expressed as

| () |

stands for the admissible control set and follows the definition below.

Remark 2.1.

The above framework is consistent with an infinitely lived agent or an agent which death is modelled as the first jump time of an independent Poisson process. In the first case, is the subjective discount rate. In the second case, we have , where is the subjective discount rate and is the intensity of the Poisson process. In fact, if is the time in which the death occurs, we have

due to the independence of the Poisson process.

Definition 2.1.

Given the initial wealth , is defined as the set of all admissible policies satisfying:

-

•

is an -stopping time,

-

•

is an -progressively measurable and non-negative process such that , a.s., ,

-

•

is an -progressively measurable process such that , a.s., ,

-

•

is an -progressively measurable and non-negative process such that , ,

-

•

for , and for a.s.,

-

•

with .

Moreover, we assume , since represents the market value of the debt repayment reduced by the maximum amount to borrow against the future income in the pre-bankruptcy period: the agent is therefore unable to allocate the investment and consumption when the wealth level stays below it.

The subsequent proposition provides the corresponding budget constraint.

Proposition 2.1.

Given any initial wealth , any strategy , the budget constraint is given by

| (2.5) |

Proof.

See Appendix A.2. ∎

Completing the construction of the primal optimization problem, we are going to solve it explicitly in the following sections. The gain function of the primal optimization problem can be rewritten as the expectation of two separated terms representing the pre- and post-bankruptcy part,

where we define in the post-bankruptcy framework, i.e., no debt repayment. We perform the backward approach, hence, begin with the post-bankruptcy part by means of the dynamic programming principle.

3 Post-Bankruptcy Problem

We first tackle the post-bankruptcy problem, assuming without loss of generalization , which is the optimization over an infinite time horizon through controlling the investment amount, consumption and leisure rate. Since the debt repayment is removed from the wealth process after the bankruptcy, the corresponding dynamics becomes

Afterwards, based on the gain function defined at the end of the previous section, we can express the value function of the post-bankruptcy part as follows,

| () |

The admissible control set is compatible with Definition 2.1, only removing the condition about the stopping time and changing the liquidity condition from “ for , and for a.s.” to “ for a.s.”. Additionally, for any given initial endowment and admissible consumption-portfolio-leisure strategy , the following propositions provide us the budget and liquidity constraint to the post-bankruptcy problem.

Proposition 3.1.

The infinite horizon budget constraint of the post-bankruptcy problem is

Proof.

Similarly as in Appendix A.2, we can prove that . Then the above budget constraint can be obtained by taking the limit as . ∎

Proposition 3.2.

The infinite horizon liquidity constraint of the post-bankruptcy problem is

Proof.

The result directly comes from (Karatzas and Shreve, 1998b, Section 3.9, Theorem 9.4), more precisely, the non-negative property of and . ∎

Then, we implement the methodology presented in (Karatzas and Wang, 2000; He and Pages, 1993) to establish a duality between the optimal control problem and the individual’s shadow price problem through the Lagrange method. We make the following derivation of , introducing a non-increasing process and a Lagrange multiplier ,

By the Fubini’s Theorem, see e.g. (Björk, 2009, Appendix A, Theorem A.48), we have

and the inequality concerning can be rewritten as

the last inequality is derived from the budget constraint, the liquidity constraint and the non-increasing property of . Referring to (He and Pages, 1993, Section 4), we can define the corresponding individual’s shadow price problem as below,

| () |

where represents the set of non-negative, non-increasing and progressively measurable processes. Then, we put forward a theorem to construct the duality between the optimal consumption-portfolio-leisure problem and the individual’s shadow price problem .

Theorem 3.1.

(Duality Theorem) Suppose is the optimal solution (the arg inf) to the dual shadow price problem , then the optimal consumption-leisure strategy to the primal problem satisfies , and we have the following relation

Here is the parameter which gives the infimum in the above equation.

Proof.

See Appendix B.1. ∎

It can be known from the above duality theorem that the optimal solution of the post-bankruptcy problem is transformed into finding the optimal . In order to solve the problem explicitly, we follow the approach in Davis and Norman (1990) and first provide the subsequent assumption.

Assumption 3.1.

The non-increasing process is absolutely continuous with respect to t. Hence, there exists a process such that .

Defining a new process , the value function of Problem can be rewritten as , where is the state variable, and follows the dynamics

| (3.1) |

Then we introduce a new function as

| (3.2) |

which implies that . The Bellman equation associated to is

| (3.3) |

with the operator . The above Bellman equation makes the optimum possess the following characterizations:

Moreover, the Bellman Equation (3.3) can be transformed into

which corresponds to the variational inequalities: find a function and a free-boundary , satisfying

| (3.4) |

for any , with the smooth fit conditions , . In line with (Choi et al., 2008, Appendix A), we assume that takes the time-independent form for solving the above variational inequalities explicitly. The solution is computed in Appendix B.2 in a semi-analytical framework, i.e., as the solution of a non-linear system of equations. Once the function is computed, and therefore is known, we can recover from Theorem 3.1.

4 Primal Optimization Problem

Once we solved the post-bankruptcy problem, we first of all have to deal with the jump in the wealth at bankruptcy time. We introduce a subset of the primal optimization problem’s admissible control set, , inside which any policy maximises the gain function of the post-bankruptcy problem. That is to say, for any , the following holds,

Here is the wealth at time given an initial wealth and assuming the policies for consumption, allocation in the risky asset and leisure rate, respectively. Then, from the dynamic programming principle, the whole optimization problem is converted into

denoting the value function at the moment of bankruptcy as

Therefore, it can be observed that the relationship between and the post-bankruptcy value function is

Simple computations give us the Legendre-Fenchel transform of , that is,

| (4.1) |

After obtaining the optimal solution for the post-bankruptcy problem, we now reduce the primal optimization problem by fixing the stopping time. Defining a set of admissible controls corresponding to a fixed stopping time as

and a utility maximization problem as

| () |

the problem can be transformed into an optimal stopping time problem, . Then, we put forward the liquidity constraint for the optimal bankruptcy problem.

Proposition 4.1.

The liquidity constraint of the considered problem is

| (4.2) |

Proof.

See Appendix C.1. ∎

Following the same technique as in the post-bankruptcy problem, considering the budget and liquidity constraints (2.5) and (4.2), we introduce a real number , the Lagrange multiplier, and a non-increasing continuous process . We obtain

As in (He and Pages, 1993, Section 4), the individual’s shadow price problem inspired by the above inequality is defined as below,

| () |

Hereafter, we provide a theorem to construct the duality between the individual’s shadow price problem and the optimal consumption-portfolio-leisure problem .

Theorem 4.1.

(Duality Theorem) Suppose is the optimal solution (the arg inf) to Problem , then, and coincide with the optimal solution to Problem , and we have the following relationship

Here is the parameter which gives the infimum in the above equation.

Proof.

See Appendix C.2. ∎

Furthermore, the duality theorem makes the value function of Problem conforms to the following derivation,

Let us introduce a new function . As in (Karatzas and Wang, 2000, Section 8, Theorem 8.5), the value function satisfies under the condition that exists and is differentiable for any . Hence, the objective optimization problem contains two steps:

The first step involves an optimal stopping time problem, and the second refers to obtain the optimum achieving the infimum part. We begin with the first optimization problem related to the individual’s shadow price. Before this, following the method of Davis and Norman (1990), an assumption is imposed on the process .

Assumption 4.1.

The non-increasing process is absolutely continuous with respect to t. Hence, there is a non-negative process such that .

Introducing a new process , the value function of the dual problem is rewritten as

We consider a new generalized optimization problem

it can be observed that , which indicates the solution of is resorted to solve the above generalized problem. We start with the infimum part through defining

the dynamic programming principle gives us the subsequent Bellman equation

with introducing the operator . The following characterizations hold for the optimum (the arg min):

-

•

: then we get that there exists a boundary such that

(4.3) -

•

: in this case, is reduced to a pure optimal stopping time problem,

(4.4)

We first focus on the optimal stopping time problem (4.4) and present a lemma to determine its continuous and stopping regions. But before this, one relationship should be noticed. With the optimum , the function can be rewritten as

Fixing the time with , can be treated as a single variable function of , that is,

From this equation, and Equation (4.1) and (4.3), we obtain ; considering the convex property of , we directly obtain the relationship

| (4.5) |

Lemma 4.1.

Assuming

| (4.6) |

there exists such that the continuous region of the optimal stopping problem (4.4) with the state variable is , and the stopping region is . is the boundary that separates and .

Proof.

See Appendix C.3 ∎

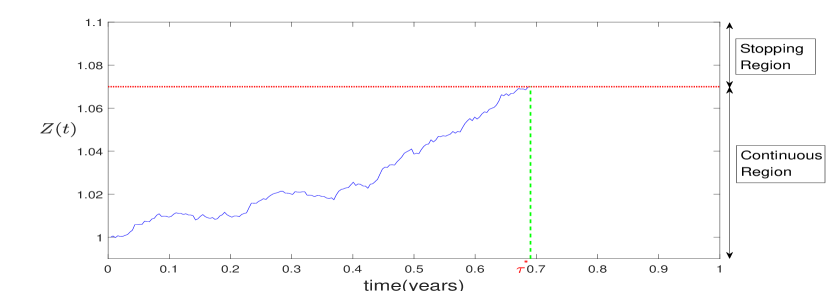

After obtaining the continuous region , we can treat the stopping time of bankruptcy as the first hitting time of process to the boundary from the inner region of . Figure 4.1 describes the relationship between the optimal stopping time and the continuous and stopping regions.

The optimal bankruptcy time is the moment when process first touches the boundary, which is represented with the red dotted line, from within the continuous region. Hence, the stopping time satisfies and will be proved to be finite with probability one under a sufficient constraint with the following lemma. Besides, it should be clear that , corresponding to the bankruptcy threshold, is an upper barrier for the process , and therefore a lower barrier of the wealth process, as we will show in Remark 4.1.

Lemma 4.2.

Under the assumption

| (4.7) |

we have , with two stopping times, and .

Proof.

See Appendix C.4. ∎

Subsequently, combining Condition (4.3) and the optimal stopping time problem (4.4), we get the free boundary problem which characterizes the function , considering two different cases:

(1) Variational Inequalities assuming : Find the free boundaries (Bankruptcy), (-wealth level), and a function satisfying

| (4.8) |

for any , with the smooth fit conditions

Furthermore, in the period up to the stopping time , which corresponds to the interval , we need to consider that whether the constraint is trigged or not, which is related to the boundary introduced in Lemma 2.1. Hence, the problem of the pre-bankruptcy part is divided into two cases, and . Then combining with the two cases of the post-bankruptcy part, we have the following framework of partition for the primal optimization problem .

-

•

:

-

•

:

(2) Variational Inequalities assuming : Find the free boundaries (Bankruptcy), (-wealth level), and a function satisfying

| (4.9) |

for any , with the smooth fit conditions and .

Same as before, we provide a diagram to show the possible situations under this prerequisite.

As in the post-bankruptcy problem, we assume that adopts a time-independent form, , then the solution is obtained, see Appendix C.5. We would like to stress that only one of the seven cases admits a solution.

After acquiring the closed form of , (Karatzas and Wang, 2000, Section 8, Theorem 8.5) indicates that

keeps true for a unique under the differentiable property of . Then the wealth threshold of bankruptcy, namely , can be calculated from the relationship . Therefore, given any initial wealth , we get the optimal Lagrange multiplier through solving the equation, . Furthermore, since the optimum is the initial value of process (3.1), , the optimal wealth process follows . The optimal bankruptcy time satisfies . Moreover, recalling Lemma 2.1, the optimal consumption and leisure strategies are

and the optimal portfolio strategy is , which can be obtained from (He and Pages, 1993, Section 5, Theorem 3).

Remark 4.1.

In Figure 4.1, we plot the relationship between the optimal bankruptcy time and the continuous and stopping regions with respect to , showing that the optimal bankruptcy time is the first time the process touch the upper barrier . The same plot can be done with respect to : the convex property of , see (Karatzas and Shreve, 1998b, Section 3.4, Lemma 4.3), indicates that is a decreasing function of , therefore, in this case the optimal bankruptcy time is the first time the process touch a lower barrier .

5 Numerical Analysis

We now implement the sensitivity analysis with respect to the input parameters. As baseline parameters, we consider the ones listed in Table 5.1. These inputs satisfy conditions (2.3), (4.6) and (4.7).

| 0.6 | 3 | 0.05 | 0.1 | 0.2 | 0.3 | 0.3 | 1.5 | 0.96 | 0.0001 | 0.9 | 1 | 0.8 | 6.6 |

The parameters , , , and are directly taken from Jeanblanc et al. (2004). Whereas the fixed bankruptcy toll and the debt repayment amount in their study are and , we set and such that the ratios of and in our and their research keep consistent. The same consideration is also applied for the setting of the initial wealth . As discussed in Section 4, seven cases should be considered simultaneously and only one must be verified: in fact with these parameters, only Case 2, “”, admits a solution. With the above input parameters, we derive the output parameters: , , , , the set of wealth thresholds , the optimal Lagrange multiplier and the value function . The results are listed in Table 5.2 and 5.3. The , i.e., the value of the function at its zero, in Tables 5.2 represents the maximum error generating from using the function of MATLAB to solve the non-linear equations (C.6), (C.7) and (C.8): as expected, the value is close to zero, i.e., the algorithm correctly solve the system of equations.

| 5.3104 | 2.6126 | 0.3280 | 0.1591 | -2.7741 | 0.3110 | 3.6973e-11 |

| -wealth level | minimum wealth level for | bankruptcy wealth level |

| 0.9601 | 6.3164 | 10.0651 |

We first of all want to stress that in this case the optimal bankruptcy time is 0, since the initial wealth, 6.6, is lower than the optimal bankruptcy barrier , i.e., the starting wealth is inside the stopping region.

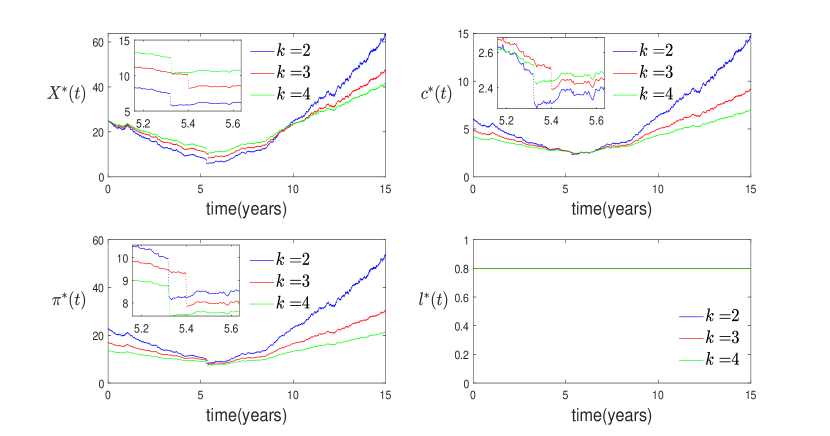

Sensitivity of optimal solutions with respect to the risk aversion coefficient :

In this part, we use the Monte Carlo method to simulate the single path of optimal wealth process and consumption-portfolio-leisure strategy by taking different values of for discovering the sensitivity of optimal solutions to the risk aversion coefficient. Parameters are the ones in Table 5.1, with the exception of the initial wealth which is set to 25 instead of 6.6 for observing the bankruptcy mechanism. The agent with a higher value of prefers to have a higher wealth threshold for declaring bankruptcy ( for , for and for ). This is reasonable, as shown in Figure 5.1: the more risk-averse agent tends to smooth the consumption and leisure, and invest less in the risky asset such that maintaining a relatively higher wealth level. Moreover, from the optimal trajectories of leisure, it can be observed that the relatively low fixed and flexible bankruptcy costs, and , and the high bankruptcy wealth thresholds enable the agent to enjoy the maximum leisure rate even after suffering the wealth shrinkage caused by declaring bankruptcy. Therefore, the leisure processes corresponding to different values are fully identical. Finally, in Figure 5.1 we zoom close to the bankruptcy time, to show the discontinuity of the optimal strategies.

Sensitivity of the optimal bankruptcy threshold with respect to the market risk premium jointly with the risk aversion coefficient:

The parameter , which is the Sharpe-Ratio, measures the market risk premium. For the purpose of discovering the relationship between and , we keep , constant and change the value of from 0.035 to 0.2, with an interval of 0.0075, which leads the value of to change from 0.1 to 1.2. Figure 5.2 shows that, with a lower risk premium, that is, a smaller value of , the agent prefers to set a higher wealth threshold to more easily get rid of the debt thanks to the bankruptcy. Contrarily, a better market performance entails the agent a stronger ability to bear the debt repayment; hence, she sets a lower wealth threshold to avoid suffering the bankruptcy costs. Furthermore, there is a positive relationship between the optimal wealth threshold of bankruptcy and the risk aversion level , which is already clarified through Figure 5.1.

Sensitivity of the optimal bankruptcy threshold with respect to the debt repayment, the fixed and flexible bankruptcy cost:

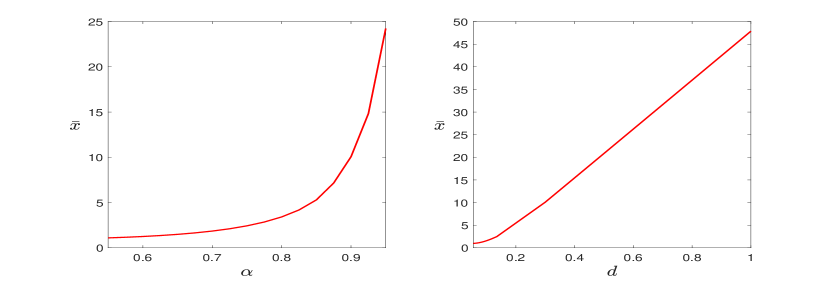

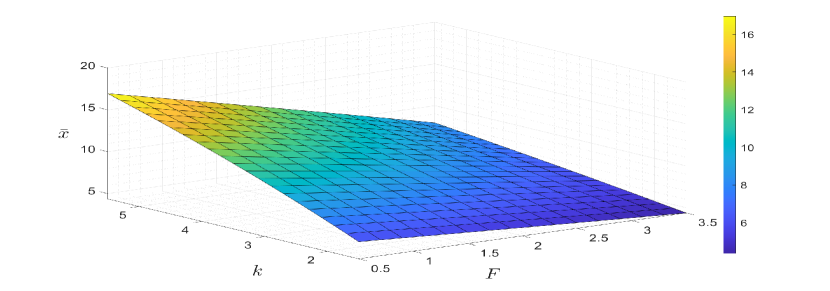

The wealth process suffers a shrinkage through an affine function declaring bankruptcy, and the debt repayment is exempted. Hence, and can be treated as the fixed and flexible cost of bankruptcy, and is the benefit of bankruptcy. In order to discover the influence of the bankruptcy option, we provide Figures 5.3-5.4 to illustrate the sensitivity of optimal wealth threshold of bankruptcy with respect to the coefficients , and .

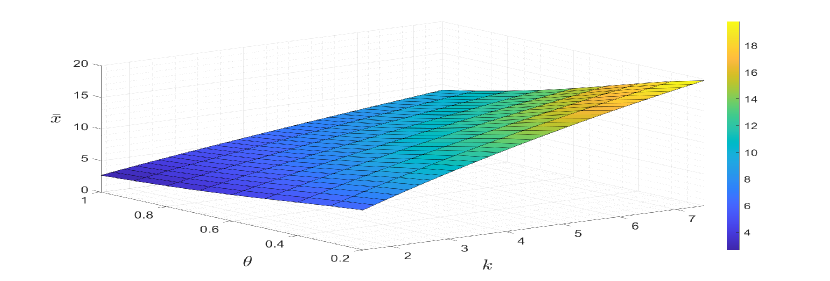

First considering the sensitivity of bankruptcy wealth threshold to the flexible cost coefficient, we can observe that is an increasing function of . The rationale is the following: since represents the proportion of wealth held after bankruptcy, a lower value of indicates a higher cost such that the agent prefers to set a lower wealth threshold to avoid suffering the wealth shrinkage from bankruptcy. As for the relationship between and , it can be observed the same increasing and convex curve. When the debt repayment is higher, which implies that the benefit of bankruptcy is more attractive, the agent tends to take a higher threshold such that the wealth process satisfies the bankruptcy requirement more easily to enjoy the debt exemption. However, this incentive becomes weaker as the debt repayment decreases, which leads to the convexity of the considering mapping. Finally, in Figure 5.4 we provide a three-dimensional image to explain the sensitivity of bankruptcy wealth threshold to the parameter jointly with .

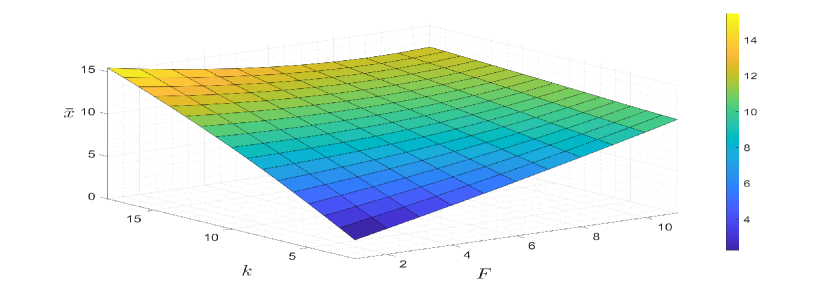

Since the value of adjusted according to Jeanblanc et al. (2004) is relatively low, the liquidity constraint triggered by is easy to be covered by the labour income. Thus, the role of is more related to the fixed cost of bankruptcy such that a higher value of will make the agent set a lower wealth threshold to avoid suffering the bankruptcy, which results in a monotonic decreasing relationship between and . However, is not only the cost of bankruptcy, but also can be regarded as the liquidity constraint to limit the agent’s investment behaviour. In order to reflect the phenomenon that the role of is the trade-off between the liquidity constraint boundary of the pre-bankruptcy period and the fixed cost of bankruptcy, we conduct the same three-dimensional image with different input parameters, particularly, we follow the baseline of inputs in Table 5.1 and only change the values of , , , and to satisfy Condition (4.6) also for larger values of . From Figure 5.5, we find that the relationship between and is not monotonous. When the risk aversion level is low, a positive relationship between and the bankruptcy threshold of wealth is observed. This is because a larger value, which is treated as the collateral recalling that before bankruptcy, will reduce the agent’s available capital and limit her investment behaviour. Therefore, the agent will set a higher bankruptcy wealth threshold to get rid of the limitation of the liquidity constraint. Whereas for the agent with deep risk aversion, liquidity constraints are less restrictive, and the parameter plays more as the role of the bankruptcy cost.

Influence of the bankruptcy option:

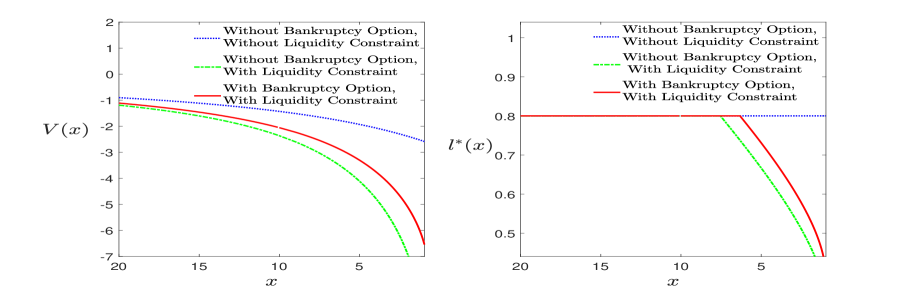

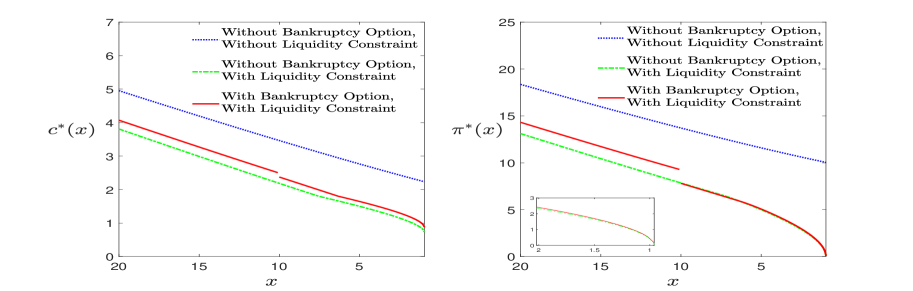

To study the influence of introducing the bankruptcy option, we also solve a pure optimal control problem without optimal stopping, see Appendix D. In Figure 5.6, we take the inputs baseline in Table 5.1 and show the optimal controls (as a function of the initial wealth) for the case with and without bankruptcy option models to reveal its influence. In the second case, we consider both the case with a liquidity constraint and without liquidity constraint.

From Figure 5.6, five phenomena should be noticed by comparing the two curves with liquidity constraint. First, due to the additional bankruptcy option, the value function is always greater than the value function without such an option at any given initial wealth level. Second, before the occurring of optimal stopping time, the additional option offers the agent a better circumstance, and the optimal consumption-portfolio-leisure policies always dominates the corresponding policies without bankruptcy option model. Third, in order to meet the needs of obtaining utility from consumption and leisure, the agent with the bankruptcy option and a low initial wealth immediately file bankruptcy, facing a shrinkage of wealth, which causes a downward jump in consumption and allocation in the risky asset. Fourth, when a liquidity constraint is considered, the optimal leisure rate decreases for low values of the initial wealth , since the agent needs to spend more time working to get a larger wage, therefore not exploiting the full leisure, to face debt and liquidity constraint. Finally, the amount of money allocated in the risky asset is 0 as the wealth level drops to the liquidity constraint boundary (). This is to avoid that the wealth process violates the liquidity constraint due to the risky asset’s fluctuation. However, the optimal consumption always keeps positive even as the wealth approaches the liquidity boundary since the agent continues to obtain the labour income. Additionally, we can observe that the optimal solutions without the liquidity constraint always dominates the solutions with this extra constraint.

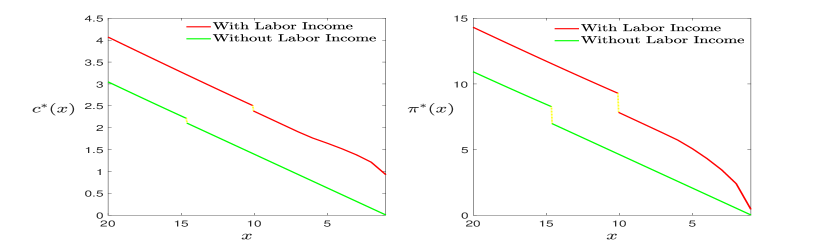

Influence of the labour income:

In order to investigate the influence of introducing the leisure rate as an additional control variable and thus the labour income, we first of all compare the results with the optimal bankruptcy model in Jeanblanc et al. (2004), therefore with full leisure and no labour income, to conduct the numerical analysis to discover the sensitivity with respect to the presence of leisure rate and labour income.

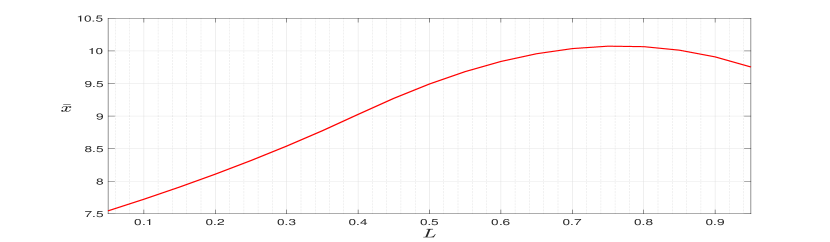

Figure 5.7 shows that there exists a downward jumps of optimal control strategies for both full and selectable leisure models due to the shrinkage of wealth at the moment of declaring bankruptcy. Moreover, it can be observed that the optimal consumption and portfolio policies of the optimization problem introducing the leisure as a control variable always keep dominating the corresponding policies of the model with full leisure rate since the agent can earn the additional income from labour. Meanwhile, comparing the wealth levels corresponding to the downward jumps, we can observe that the agent with the full leisure rate tends to have a higher bankruptcy wealth threshold such that more wealth can be taken into the post-bankruptcy period to support the further consumption ( for the “with labour income case”, for the “without labour income -full leisure- case”). Secondly, in Figure 5.8 we discover the sensitivity of bankruptcy wealth threshold with respect to different values of within the optimization model considering leisure selection.

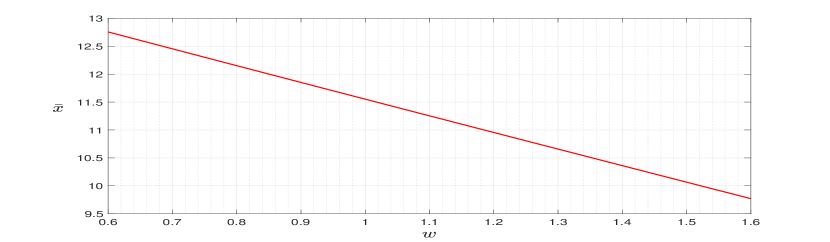

Figure 5.8 shows that the bankruptcy wealth threshold is not a monotonic function of ; the relationship between these two variables works in a complex way and can be analysed briefly into two separated pieces: one piece is with a relatively low value of , and another is with higher value. Since represents the upper boundary of the leisure variable , represents the minimum mandatory working rate. In the first part, the low enough value of obliges the agent to allocate most of the time on work, thereby gaining enough labour income to afford the debt repayment. Hence, she prefers to set a smaller wealth threshold for bankruptcy to avoid encountering the wealth shrinkage. However, for the second part, the restriction on the optimal leisure choice caused by becomes weaker as its value increases, the agent gains the utility from taking more leisure, which leads to a decreasing labour income, a decreasing consumption since leisure and consumption are substitute, and a corresponding lower bankruptcy wealth threshold. Finally, we conduct the sensitivity analysis to the wage rate and present the result in Figure 5.9, in which an inverse relationship occurs between and . Because the economic situation of the agent becomes worse with a lower wage rate , she tends to set a higher critical wealth level such that more wealth is retained for supporting the post-bankruptcy life.

6 Conclusion

In this work the optimal consumption-portfolio-leisure and bankruptcy problem concerning a power utility function has been solved semi-analytically. By the Legendre-Fenchel transform, we have established the duality between the optimization problem with the individual’s shadow price problem, which results in a system of variational inequalities then enables us to obtain the closed-form solutions. The optimal wealth and control strategies are represented as functions of wealth’s dual process, . Then we have proved that the optimal policy for the agent is to file bankruptcy at the first hitting time of the optimal wealth process to a critical wealth level, which is the boundary separating the continuous and stopping regions of the corresponding stopping time model. We have also conducted the sensitivity analysis of this wealth threshold to critical parameters. The bankruptcy wealth threshold is the increasing function of both , which can be treated as the benefit of declaring bankruptcy, and , with representing the flexible cost of bankruptcy. Whereas, the non-monotonic relationship between the bankruptcy wealth threshold and is because performs a trade-off between the liquidity constraint boundary in the pre-bankruptcy period and the fixed cost of bankruptcy. Regarding the effect of labour income, we show that the bankruptcy wealth threshold is a concave function of the upper bound of the leisure rate, , that is, it first increases and then decreases: a high value for permits the agent to have large utility from leisure, while a low value of “forces” the agent to get a large wage, even if low utility from leisure. Moreover, the bankruptcy wealth threshold is strictly decreasing for the wage rate since a worse economic situation requires more wealth to support the post-bankruptcy period.

References

- Barucci and Marazzina (2012) Emilio Barucci and Daniele Marazzina. Optimal investment, stochastic labor income and retirement. Applied Mathematics and Computation, 218(9):5588–5604, 2012.

- Barucci et al. (2021) Emilio Barucci, Daniele Marazzina, and Elisa Mastrogiacomo. Optimal investment strategies with a minimum performance constraint. Annals of Operations Research, 299:215–239, 2021.

- Bellalah et al. (2019) Mondher Bellalah, Yaosheng Xu, and Detao Zhang. Intertemporal optimal portfolio choice based on labor income within shadow costs of incomplete information and short sales. Annals of Operations Research, 281(1):397–422, 2019.

- Björk (2009) Tomas Björk. Arbitrage theory in continuous time. Oxford university press, 2009.

- Choi et al. (2008) Kyoung Jin Choi, Gyoocheol Shim, and Yong Hyun Shin. Optimal portfolio, consumption-leisure and retirement choice problem with ces utility. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 18(3):445–472, 2008.

- Colaneri et al. (2021) Katia Colaneri, Stefano Herzel, and Marco Nicolosi. The value of knowing the market price of risk. Annals of Operations Research, 299(1):101–131, 2021.

- Davis and Norman (1990) Mark HA Davis and Andrew R Norman. Portfolio selection with transaction costs. Mathematics of operations research, 15(4):676–713, 1990.

- Dellacherie and Meyer (1982) Claude Dellacherie and Paul-André Meyer. Probabilities and Potential B, Theory of Martingales, volume 72 of North–Holland Mathematics Studies. Amsterdam: North–Holland Publishing, 1982.

- Farhi and Panageas (2007) Emmanuel Farhi and Stavros Panageas. Saving and investing for early retirement: A theoretical analysis. Journal of Financial Economics, 83(1):87–121, 2007.

- He and Pages (1993) Hua He and Henri F Pages. Labor income, borrowing constraints, and equilibrium asset prices. Economic Theory, 3(4):663–696, 1993.

- Jeanblanc et al. (2004) Monique Jeanblanc, Peter Lakner, and Ashay Kadam. Optimal bankruptcy time and consumption/investment policies on an infinite horizon with a continuous debt repayment until bankruptcy. Mathematics of Operations Research, 29(3):649–671, 2004.

- Karatzas and Shreve (1998a) Ioannis Karatzas and Steven E Shreve. Brownian Motion and Stochastic Calculus. Second Edition. Springer-Verlag, 1998a.

- Karatzas and Shreve (1998b) Ioannis Karatzas and Steven E Shreve. Methods of mathematical finance, volume 39. Springer, 1998b.

- Karatzas and Wang (2000) Ioannis Karatzas and Hui Wang. Utility maximization with discretionary stopping. SIAM Journal on Control and Optimization, 39(1):306–329, 2000.

- Karatzas et al. (1997) Ioannis Karatzas, John P Lehoczky, Suresh P Sethi, and Steven E Shreve. Explicit solution of a general consumption/investment problem. In Optimal Consumption and Investment with Bankruptcy, pages 21–56. Springer, 1997.

- Nicolosi et al. (2018) Marco Nicolosi, Flavio Angelini, and Stefano Herzel. Portfolio management with benchmark related incentives under mean reverting processes. Annals of Operations Research, 266(1):373–394, 2018.

- Oksendal (2013) Bernt Oksendal. Stochastic differential equations: an introduction with applications. Springer Science & Business Media, 2013.

- Sethi et al. (1995) Suresh P Sethi, Michael I Taksar, and Ernst L Presman. Explicit solution of a general consumption/portfolio problem with subsistence consumption and bankruptcy. Journal of Economic Dynamics and Control, 5(19):1297–1298, 1995.

Effect of Labour Income on the Optimal Bankruptcy Problem - Online Appendix

Guodong Ding1, Daniele Marazzina1,2

1 Department of Mathematics, Politecnico di Milano

I-20133, Milano, Italy

2 Corresponding Author. E-mail: daniele.marazzina@polimi.it

Appendix A Appendix of Section 2

A.1 Proof of Lemma 2.1

In order to get rid of the constraint , we begin with the maximization of with . From the first-order derivative conditions with respect to and , we obtain the following equations

| (A.1) |

The above system entails the optimal consumption and leisure policies as

guarantees the positive values of and . Besides, with treating and as functions of , we get

Then the remaining constraint of the Legendre-Fenchel transform of Equation (2.4) is . Since

the optimal leisure plan also satisfies the constraint under the condition . Conversely, this constraint comes into force to make the optimal leisure to be for the interval . Thereafter, we can summarize as follows,

| (A.2) |

The first equation in (A.1) implies the relationship between the optimal consumption and leisure, . Taking Equation (A.2) into this relationship, we obtain

Finally, we can deduce the Legendre-Fenchel transform directly by substituting and into Equation (2.4).

A.2 Proof of Proposition 2.1

Referring to (Karatzas and Shreve, 1998b, Section 3.3, Remark 3.3), we first apply the Itô’s formula to , ,

in which is the Brownian motion under the measure mentioned in Equation (2.2). Taking the integral on both sides of the above equation from 0 to , we obtain

The left-hand side can be rewritten as

the condition from the definition of admissible control set ensures that the left-hand side is bounded below by the constant , so the Itô integral on the right-hand side is proved to be a -supermartingale by means of Fatou’s Lemma. Then, taking the expectation on both sides under the measure, we have

which endows us with the desired budget constraint through converting the measure to ,

Appendix B Appendix of Section 3

B.1 Proof of Theorem 3.1

Before proving Theorem 3.1, we insert a lemma which helps us to prove the theorem.

Lemma B.1.

For any given initial wealth , and any given and progressively measurable consumption and leisure processes, , , satisfying , with standing for the set of -stopping times, there exists a portfolio process making

holds almost surely.

Proof.

Referring to (He and Pages, 1993, Appendix, Lemma 1), we first define a new process

From the properties of processes , and , it is directly observed that , which implies that is uniformly integrable. Then, as in (Dellacherie and Meyer, 1982, Appendix I), there exists a Snell envelope of denoted as . It is a super-martingale under the measure and satisfies

By the Doob-Meyer Decomposition Theorem from (Karatzas and Shreve, 1998a, Section 1.4, Theorem 4.10), the super-martingale can be represented as

where is a uniformly integrable martingale under the measure with the initial value , is a strictly increasing process with the initial value . According to the Martingale Representation Theorem from (Björk, 2009, Section 11.1, Theorem 11.2), can be expressed as

with an -adapted process satisfying a.s.. Let us define a new process

Based on the fact that , we can conclude that is a non-negative process with the initial wealth . We express this process with the martingale as

As for the dynamics of wealth process

we implement the Itô’s formula to to get

If we take the portfolio strategy as , the wealth process is rewritten as , which shows that , a.s.. The non-negativity of claims , a.s., ∎

Then we move to the proof of Duality Theorem 3.1. Following (He and Pages, 1993, Section 4, Theorem 1), the proof mainly contains two aspects: the first part is to show the admissibility of and , and the second part is to claim that they are the optimal consumption-leisure strategy to Problem .

(1) We begin with verifying that any consumption-leisure strategy satisfying is admissible. Taking any stopping time from , which is the set of -stopping times, we can define a process

where a positive constant. It is evident that is a non-negative, non-increasing, and progressively measurable process, that is, . Let us define a function

Since is the optimal solution of Problem , and , we get

The above inequalities give us and

The decreasing property of endows us with . Applying the Fatou’s lemma, we have

Because of , we get

.

Since can be any -stopping time in the set , there exists a portfolio strategy that makes the corresponding wealth process satisfying , based on the result from Lemma B.1.

(2) In this part, we claim that and are the optimal consumption and leisure to Problem under the liquidity constraint. Taking an arbitrary consumption strategy , the proof of Lemma B.1 guarantees that there exists a process satisfying

| (B.1) |

Since a.s., we obtain the following inequality with any process ,

where is any time satisfying . Because is bounded variation, we can integrate by parts and get

Taking the expectation under the measure on both sides and replacing Equation (B.1), we obtain

then, by Lebesgue’s Monotone Convergence Theorem, we have

The above inequality keeps true for any admissible control strategy , , and any non-negative, non-increasing process ; furthermore, we will show that the inequality changes into equality with the given , and . We define a new process

where is a small enough constant. Following the same argument as in the first part of the proof, we have and

Applying the Fatou’s lemma, we obtain separately

which give us . Subsequently, we define a new optimization problem named as

| () |

We denote the optimal consumption solution of the above problem is . From the Lagrange method, we know that , where is the Lagrange multiplier. The constraint of problem takes equality when . Then, the condition implies that and are the optimal control policies of Problem . Moreover, since the maximum utility of primal problem is upper bounded by the maximum utility of , we can conclude that and are also the optimal consumption and leisure solutions of Problem .

B.2 Solutions of Variational Inequalities (3.4)

The solution is computed considering two cases: and .

Case 1. :

Condition in (3.4) results in a differential equation,

| (B.2) |

which has the solution

For avoiding the explosion of term when goes to 0, we set . Then four parameters are left to be determined, which are , , and . To accomplish this task, we use the smooth conditions at and to construct a four-equation system:

-

•

condition at

-

•

condition at

-

•

condition at

-

•

condition at

Case 2. :

The same argument with the previous case, we first handle Condition in (3.4). Recalling Lemma 2.1, the corresponding interval restricts the function only takes the form , which is identical with the piece of in Case 1. Hence, the differential equation from has the same solution, only changing the parameters’ notations from to , and to , that is,

We set the coefficient for the reason that the term goes to as approaches 0, which violates the boundedness assumption of . Subsequently, using the smooth condition at , a two-equation system is established to determine the exact values of and :

-

•

condition at

-

•

condition at

Appendix C Appendix of Section 4

C.1 Proof of Proposition 4.1

Let us first introduce a process , . Following (Karatzas and Shreve, 1998b, Section 3.9, Theorem 9.4), we firstly claim that is a -martingale. Let and be the consumption and leisure processes such that

For any fixed stopping time , we define . Then we have . (Karatzas and Shreve, 1998b, Section 3.3, Theorem 3.5) implies that there exists a portfolio process satisfying . Moreover, since

the process is a -martingale. Combined with the constraint , , we have

then,

C.2 Proof of Theorem 4.1

The proof here is consistent with Appendix B.1, but some modification is needed due to the stop-time embedding. We first introduce a lemma, which will be used in the proof of the duality theorem.

Lemma C.1.

For any given initial wealth , any -stopping time with , any -measurable random variable with under the measure, and any given progressively measurable consumption and leisure processes , , satisfying , where stands for the set of -stopping times before the fixed stopping time , and , there exists a portfolio process making , , and hold almost surely.

Proof.

Following the similar argument with (He and Pages, 1993, Appendix, Lemma 1), we first define a new process

From the properties of processes , and , it can be observed that , which implies is uniformly integrable. Therefore, there exists a Snell envelope of denoted as . It is a super-martingale under the measure and satisfies

By the Doob-Meyer Decomposition Theorem from (Karatzas and Shreve, 1998a, Section 1.4, Theorem 4.10), the super-martingale can be decomposed into

where is a uniformly integrable martingale under the measure with the initial value , is a strictly increasing process with the initial value . According to the Martingale Representation Theorem from (Björk, 2009, Section 11.1, Theorem 11.2), can be expressed as

with an -adapted process satisfying a.s.. Let us define a new process

It can be verified that

using the condition , and the martingale property of . Further, because of , we can prove that , by constructing a contradiction. Let us assume that attains the supremum within the expression of , i.e., , and introduce a stopping time as . Since , we have , which is contradictory to the definition of . Then, based on the fact that , we can conclude that , a.s.. Additionally, the process is re-expressed in terms of the martingale as

| (C.1) |

As for the wealth process

by implementing the Itô’s formula to and adopting the portfolio strategy as

it is rewritten as . Taking the integral from to , and then the conditional expectation w.r.t. on both sides of the above equation, we obtain

Since , we have , a.s.. Finally, through comparing the process of with Equation (C.1),

is observed. The non-negativity of claims , a.s., . ∎

With the aid of the above lemma, we can complete the statement and proof of Duality Theorem 4.1.

Referring to (He and Pages, 1993, Section 4, Theorem 1), the proof procedure is divided into two aspects: the first part is focused on the admissibility of and , and the second part is revolved around claiming that and are the optimal consumption-leisure strategy to the primal optimization problem.

(1) We begin verifying that any consumption-leisure strategy satisfying

is admissible. Taking any stopping time from , we can define a process , where is a positive constant. It is evident that is a non-negative, non-increasing and progressively measurable process, that is, . Let us define a function

Considering is the optimal solution of problem and the fact , we obtain

The above inequalities give us , combining with , , we have

The decreasing property of endows us with . Applying the Fatou’s lemma, we have

Because of , we get

| (C.2) |

Following the same technique, if defining , we can obtain that

| (C.3) |

We now follow the same argument as before, introducing a new process , here is no longer required to be positive, but a sufficiently small real number. Defining a function

we have , and

Given the conditions

the Fatou’s lemma entails the following relations respectively:

which lead to

| (C.4) |

Subtracting Equation (C.4) from (C.2), we get

which is equivalent to

, for any stopping time . Additionally, subtracting Equation (C.4) from (C.3), we obtain

,

which implies that a.s.. Since can be any -stopping time in the set , there exists a portfolio strategy that makes the corresponding wealth process satisfying , , according to Lemma C.1.

(2) Then we turn to claim that and are the optimal consumption and leisure to the problem . Taking an arbitrary control strategy , the proof of Lemma C.1 guarantees that there exists a process satisfying

| (C.5) |

Since a.s., , we obtain the following inequality with any process ,

Since is of bounded variation, we can implement the integration by parts and get

Taking the expectation under the measure on both sides and replacing Equation (C.5), we obtain

The above inequality keeps true for any admissible control strategy and any non-negative, non-increasing process . Furthermore, we will show that the inequality changes into equality with the given , and . We first define a new process

where is a small enough constant. Following the same argument in the first part proof, we have , and

Applying the Fatou’s lemma, we obtain separately

which give us

Moreover, we define a new optimization problem named as

| () |

subject to

We denote the optimal solutions of the above problem as and .The Lagrange method endows us

where is the Lagrange multiplier. The constraint of Problem takes equality when . Then, the condition implies that and are the optimal control policies of the problem . Moreover, since the maximum utility of primal problem is upper bounded by the maximum utility of , we can conclude that and are also the optimal consumption and leisure solution to the problem

C.3 Proof of Lemma 4.1

Referring to (Oksendal, 2013, Section 10.3, Example 10.3.1), the notations here almost coincide with the ones there. Let us first introduce two new functions:

Defining an operator , the continuous region of the corresponding optimal stopping time problem is expressed as

Since

defining a new function , the continuous region can be rewritten as Because takes the piecewise form of

we can rewrite as

the last equality comes from Condition (B.2) on the interval . From Condition (4.5), it can be observed that the function only takes the form

on the considering interval . We first extend the domain of to the whole positive real line, and discover the existence and uniqueness of its zero , then discuss the magnitude between and . The decreasing property of leads to ; hence, a necessary condition to ensure that there is at least one zero point is put forward as Afterwards, for the sake of determining the curvature of , we take the second-order derivative and obtain

therefore we focus on the sign of function . Since is strictly decreasing and convex on and adopts the piecewise form, we discover the sign of on three different intervals: , and .

-

•

On : from , and , we get

-

•

On : the function is rewritten as

The first term inside the square bracket has the following inequality relationship

as for the second term, we have

Then we can determine the sign of as

-

•

On : The conditions , and endows us

Hence, we can summarize that , which means the function is strictly concave for . Additionally, combining with the subsequent facts

we can conclude that there exists a unique such that . Moreover, solutions of the primal optimization problem are discussed in two different cases, and .

C.4 Proof of Lemma 4.2

Referring to (Jeanblanc et al., 2004, Appendix, A.2), we make use of the scale function to calculate the probability of the stopping time. Related to the diffusion process of , the scale function is

where , are the drift and diffusion coefficients of and is an arbitrary constant located in . Then we obtain

with . It follows that in order to prove that the above probability is one instead of depending on the initial value , it suffices to show that . Since

a sufficient condition to make is , which is equal to Moreover, following the same argument, it can be easily proven that with the condition (4.7), which also gives us .

C.5 Solutions of Variational Inequalities (4.8) and (4.9)

Case 1. :

The differential equation generated from Condition in the system (4.8) takes the solution as

Since , the term will suffer the explosion as goes to 0. Therefore, we set the coefficient to meet the boundedness assumption of . Forward, the smooth fit condition leads to the subsequent two-equation system to resolve the parameters and .

-

•

condition at

(C.6) -

•

condition at

(C.7)

Besides, the condition generates the following equation

which endows us the value of .

Case 2. :

The Condition from (4.8) leads to the following differential equation

since the condition remains unchanged, the above equation keeps the same compared with the previous sections, hence, takes the identical solution as

Furthermore, because the condition also coincides with Case 1, we have the same smooth fit condition , which results in the identical values of parameters and . The difference from the previous case occurs at the boundary . Because of , the function adopts a different form at the point ; furthermore, and in the system (4.8) produces a different equation, that is,

| (C.8) |

to acquire the value of .

Case 3. :

Under the same condition with the previous cases, the differential equation generating from of (4.8) follows the identical solution,

Then the smooth fit condition enables us to determine the values of parameters and with the following two-equation system:

-

•

condition at

-

•

condition at

Besides, from Condition and of (4.8), we have the smooth fit condition . Combining with the prerequisite , we have the subsequent equation,

which gives us the exact value of parameter .

Case 4. :

Same with the previous cases, Condition of (4.8) forces the function to take the solution as

Then, considering the smooth fit condition , a two-equation system is established to resolve the parameters and :

-

•

condition at

-

•

condition at

Combining the condition with the prerequisite , we get the following equation

which enables us to obtain the exact value of .

Case 5. :

We begin with Condition of (4.8), which leads to the subsequent differential equation on the interval ,

Since , Lemma 2.1 shows that the function takes two different forms on the corresponding interval with as the separating threshold. Hence, the solution of the above differential equation inherits this piecewise property and has the following resolution,

To meet the boundedness assumption of , we set to avoid the explosion of term as goes to 0. Then, the same argument with the previous cases, we need to construct a four-equation system, which resorts to the smooth conditions at the point and , to determine the boundary , and the coefficient of function , i.e., , , :

-

•

condition at

-

•

condition at

-

•

condition at

-

•

condition at

Meanwhile, considering the prerequisite and the smooth fit condition , we have

which gives us the value of .

Case 6. :

The Condition of (4.9) endows us a partial differential equation with the solution

Due to the same considerations as before, we set to meet the boundedness of . Then, with the smooth fit conditions at and , we can construct a four-equation system to determine the values of parameters , , and :

-

•

condition at

-

•

condition at

-

•

condition at

-

•

condition at

Case 7. :

The prerequisite makes the function of the form . Then Condition in (4.9) has the solution

We set for avoiding the explosion of the term when goes to 0. Then a two-equation system is created to solve the value of parameters and explicitly:

-

•

condition at

-

•

condition at

Appendix D No Optimal Bankruptcy Problem

To study the influence of introducing the bankruptcy option, we also solve a pure optimal control problem without optimal stopping, which is defined subsequently as

The subscript indicates that the considering variables and functions are concerned with the no bankruptcy option model. Moreover, the admissible control set is almost consistent with the definition of except the liquidity condition. adopts “, a.s., ” instead of “, a.s., ”. Then we provide the budget and liquidity constraints as:

Following the same argument with the post-bankruptcy part, we can solve the optimal control problem with two different cases:

-

•

Case 1. : the optimal consumption-portfolio-leisure strategy is

and the optimal wealth process is

-

•

Case 2. : the optimal consumption-portfolio-leisure strategy defined on the interval is

and the optimal wealth process is