Unifying Revealed Preference and Revealed Rational Inattention

Abstract.

This paper unifies two key results from economic theory, namely, revealed rational inattention (CD15, ) and classical revealed preference (AF67, ; FO09, ). Revealed rational inattention tests for rationality of information acquisition for Bayesian decision makers. On the other hand, classical revealed preference tests for utility maximization under known budget constraints. Our first result is an equivalence result - we unify revealed rational inattention (CD15, ) and revealed preference (AF67, ; FO09, ; BC15, ) through an equivalence map over decision parameters and partial order for payoff monotonicity over the decision space in both setups. Second, we exploit the unification result computationally to extend robustness measures for goodness-of-fit of revealed preference tests in the literature to revealed rational inattention. This extension facilitates quantifying how well a Bayesian decision maker’s actions satisfy rational inattention. Finally, we illustrate the significance of the unification result on a real-world YouTube dataset comprising thumbnail, title and user engagement metadata from approximately 140,000 videos. We compute the Bayesian analog of robustness measures from revealed preference literature on YouTube metadata features extracted from a deep auto-encoder, i.e., a deep neural network that learns low-dimensional features of the metadata. The computed robustness values show that YouTube user engagement fits the rational inattention model remarkably well. All our numerical experiments are completely reproducible.

1. Introduction

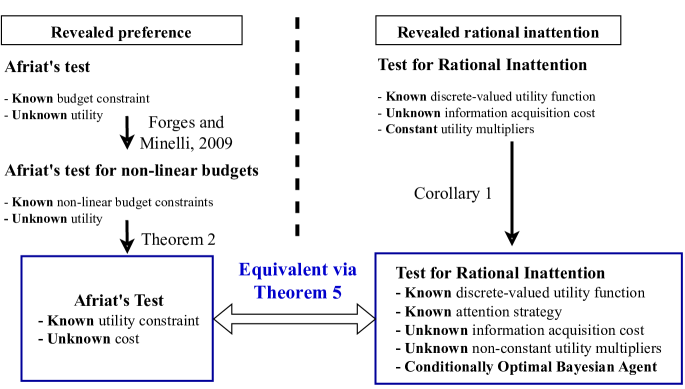

Afriat’s theorem (SM38, ; HO50, ; AF67, ; VR82, ) in revealed preference theory gives necessary and sufficient conditions for a finite sequence of linear budget constraints and consumption bundles to be rationalized by a monotone concave utility function. (FO09, ) generalized Afriat’s theorem to general (non-linear) budget sets and provided feasibility conditions for utility maximization under monotone budget constraints. More recently, in a Bayesian context in information economics, authors in (CD15, ) address costly information acquisition and give necessary and sufficient conditions for a finite sequence of utility functions and action selection policies to be consistent with expected utility maximization with an information acquisition cost. In this paper, we refer to testing for costly information acquisition in (CD15, ) as “revealed rational inattention”.

Revealed preference and revealed rational inattention, respectively, test for economics based rationality (optimal decision making under resource constraints) in a non-Bayesian and Bayesian sense, respectively. So it is intuitively plausible that there exists a one-to-one correspondence between the two results. Our key finding is that the NIAC (No Improving Attention Cycles) condition of (CD15, , Theorem 1) in revealed rational inattention is a special case of the General Axiom of Revealed Preference (GARP) (VR82, ) used widely in revealed preference.111Specifically, the NIAC condition (CD15, ) is equivalent (under an appropriate variable map) to the feasibility of Afriat inequalities (AF67, ) for GARP with the additional constraint that the feasible Lagrange multipliers are constant across all problem instances. On a related note, in Sec. 3, we also discuss the equivalence between the NIAC condition (20) and the cyclical monotonicity condition for testing quasi-linear utility maximization (BR07, ). To the best of our knowledge, this result is new222(CD15, ) allude to the cyclical monotonicity condition of (RO15, ) in the discussion of the NIAC condition. This provided us with additional motivation to investigate the connection between revealed preference and revealed rational inattention. Also, (CH17-nonseparable, ) generalize the setup in (CD15, ) and consequently propose a GARP-type condition for testing rational inattention. In Sec. 4, we argue how our unification result differs from that of (CH17-nonseparable, )., and stated formally in Theorem 1. To prove this result, we first develop a revealed preference to test for cost minimization subject to utility constraints, and then extend the test to probability vectors in the unit simplex equipped with the Blackwell partial order (BW53, ).

Theorem 1 states that GARP for non-linear budgets is a generalization of the NIAC condition (CD15, ). Indeed, GARP is an acyclic condition due to unconstrained Lagrange multipliers (marginal utility values) and is a less restrictive condition compared to the the cyclical monotonicity structure of NIAC (20). To complete the connection between NIAC and GARP, we generalize the revealed rational inattention result of (CD15, ) to test for expected utility maximization subject to a bound on the information acquisition cost (the result Lagrange multipliers need not be a constant across decision problems unlike (CD15, )). The NIAC generalizes to a condition we term ‘GARRI’ (Generalized Axiom of Revealed Rational Inattention), and show GARRI is equivalent to GARP under the variable map of Theorem 1.

Since we will unify revealed preference and revealed rational inattention, the reader might wonder: how to abstract Bayes rule into the revealed preference formulation? It is here that the usage of Blackwell partial order is critical. In the Bayesian framework, the decision maker computes the posterior belief of the state of nature via Bayes rule using a private measurement unknown to the analyst, and then takes an action observed by the analyst. From the analyst’s perspective, the decision maker chooses analyst-observable probabilistic information structures that map the state to a distribution over actions. The observed information structures are termed as action selection policies in this paper, that link the decision maker’s prior belief to its posterior belief given a chosen action. As a result, the action selection policy also determines the decision maker’s expected utility. We will show that the consumption bundle in the revealed preference test translates to the action selection strategy (which is a probability distribution) in the revealed rational inattention test. In revealed preference, an element-wise higher consumption good yields a larger utility for the decision maker. Thus, the utility function is a monotonically increasing function of the consumption bundle with respect to the natural (element-wise) partial order on the Euclidean space (space of consumption bundles). In complete analogy, for the Bayesian case, a more accurate action selection policy (in the Blackwell sense) results in a higher expected utility of the Bayesian decision maker. Equivalently, the expected utility in the Bayesian setup is monotone in the action selection policy with respect to the Blackwell order.333For revealed rational inattention, it suffices to ensure weak monotonicity of the expected utility with respect to attention strategies. One well-known partial order that satisfies this condition is the Blackwell (BW53, ) order. This analogy is crucial for the main unification result of this paper, Theorem 1 and is schematically shown in Fig. 1. We formally discuss the Blackwell order and the monotonicity of expected utility wrt the Blackwell order in Lemma 3. To convey the key ideas early on in the paper, we present below an information version of our unification result, Theorem 1 below:

Theorem 0 (Unification Result (Informal)).

(S1.) The NIAC condition (CD15, ) for revealed rational inattention is a special case of GARP (FO09, ) under the Blackwell partial order (BW53, ) and an appropriate variable map.

(S2.) The minimum modification needed in the decision model of (CD15, ) so that a GARP-type condition is necessary and sufficient for revealed rational inattention is the addition of a multiplier that scales the decision maker’s expected utility. We term the rational inattention analog of the GARP condition as ‘GARRI’ (26), defined formally in Corollary 4.

Several reasons motivate our paper. Revealed preference and revealed rational inattention are developed largely independently in the literature; an exception being works like (Var83, ) that use revealed preference ideas to identify maximization of the mean (not Bayesian) utility. However, unlike (CD15, ), the expected utility maximization problem assumes the probability distribution over states of nature as an exogenous variable. With our unification result, the results in these two areas can enrich each other. In Sec. 5, we extend the concept of robustness measures for goodness-of-fit in revealed preference literature to revealed rational inattention. We also illustrate the rational inattention analog of robustness measures to show rationally inattentive user engagement behavior in a massive YouTube dataset.444The term ‘user engagement’ is used widely in the literature (KH17, ; user-eng-twitter, ; user-eng-orkut, ) to describe user interaction on online multimedia platforms. Apart from applications in economics, revealed preference methods have also been applied in areas like machine learning, specifically for inverse reinforcement learning (NG00, ; LOP09, ; DIM11, ; HKP20, ; PK23, ), adversarial signal processing (PKB22, ) and interpretable machine learning (PK21, ).

Related Work

Extending the revealed preference test of (AF67, ) to more general partially ordered sets of consumption bundles dates back to (RI66, ), and more recently, to (NIS17, ) where the consumption bundles are partially ordered via first-order stochastic dominance. (FR16, ; FR21, ) generalize the revealed preference test to the partial order over probability distributions (mixed strategies). Unlike the problem setting in this paper, the decision maker in (FR21, ) does not update its belief via Bayes rule. The subtle distinction between (FR21, ) and our work is that the decision maker’s choice in this paper lies in the Cartesian product of probability simplices and thus requires a different partial order. (CR20, ) consider a generalized decision model (compared to (CD15, )) for the Bayesian agent, and give necessary and sufficient conditions for Bayesian rationality, namely, NIAS and GACI (Generalized Axiom of Costly Information) that generalize Theorem 1 in (CD15, ). In this paper, we focus primarily on the result of (CD15, ) and its connection to revealed preference. In spite of a unification flavor in the result of (CR20, ) where GACI and GARP are discussed in a similar vein, the variable map in the unification result of this paper is distinct from that used by (CR20, ) to formulate GACI. Finally, (FRE22, ) unify multiple approaches in revealed preference theory under an algebraic axiom of revealed preference. Our result builds on (FRE22, ) in that we connect revealed preference to revealed rational inattention (CM15, ; CD15, ) where the consumer’s response takes the form of attention strategies and action selection policies, and the aim is to test for costly information acquisition. Also, we discuss relevant works that bridge revealed preference and revealed rational inattention in Sec. 4 in more detail.

Terminology

We use the terms ‘costly information acquisition’, ‘rationally inattentive utility maximization’, ‘rational inattention’ and ‘Bayesian rationality’ interchangeably in the paper. We also use the terms ‘decision maker’ and ‘agent’ interchangeably.

Outline of Results

Revealed preference background:

In Sec. 2, we introduce the key results of revealed preference and revealed rational inattention. We also propose: (i) the test , an extension of the classical revealed preference test to identify the existence of a rationalizing cost subject to utility constraints on the decision maker, and (ii) the test, , a modification of the revealed rational inattention that introduces one extra degree of freedom in the objective function of the Bayesian decision maker.

Unification result - Relating GARP and NIAC:

Theorem 1 in Sec. 3 is our key unification result that says that is equivalent to when the Bayesian decision maker is assumed to be conditionally optimal - it chooses the action that maximizes its expected utility conditioned on its posterior belief. Our second result, Corollary 4, introduced the minimal set of assumptions that facilitates testing for rational inattention via a GARP-type inequality, we term this inequality as GARRI (Generalized Axiom of Revealed Rational Inattention).

Discussion of related works:

Sec. 4 discusses existing works in the literature that bridge the methodologies of revealed preference and revealed rational inattention, and also highlights the differences between existing unification results and the key results of Sec. 3.

Extending robustness measures in revealed preference to revealed rational inattention:

Building on the unification results in Sec. 3, Sec. 5 introduces robustness measures for revealed rational inattention that measure how far a dataset is from being consistent with rationally inattentive behavior. We introduce Bayesian analogs of well-studied robustness measures in the literature, for example, the Afriat’s efficiency index (AFT72-efficiency, ), the Houtman-Maks index (HTM85-consistency, ) and the minimal perturbation test (VAR85-measurement, ). To the best of our knowledge, robustness measures for revealed rational inattention have not been explored in the literature.

Robustness analysis of revealed rational inattention on a real-world YouTube dataset:

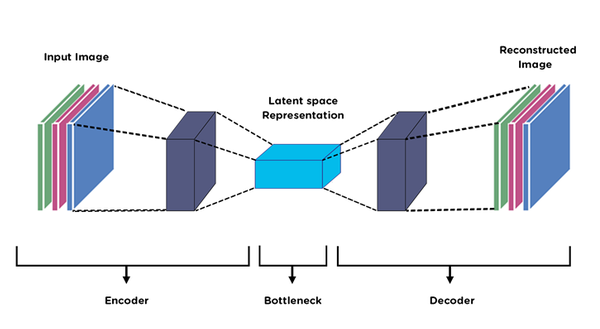

Finally, in Sec. 6, we perform a revealed rational inattention test on a real-world YouTube dataset comprising meta-data from approximately videos. The metadata in the YouTube dataset comprises the video thumbnail, title, viewcount, number of comments, and number of likes and dislikes on each video, recorded after 20 days of posting the video. The numerical experiments on the YouTube dataset extend our recent works (HKP20, ; PK23, ) in the following aspects: (i) we present a novel deep auto-encoder and natural language processing (NLP)-based feature extraction procedure for YouTube metadata (video thumbnail and title), (ii) we use the equivalence results developed in the paper to conduct a systematic robustness analysis of YouTube metadata by computing robustness measures adapted from revealed preference theory, and (iii) we test for a generalized rational inattention model compared to that proposed by (CD15, ). Testing YouTube metadata for a generalized model of rational inattention is useful because YouTube user engagement literature (YT-diff-1, ; YT-diff-2, ; YT-diff-3, ) shows that different groups of YouTube users have different attention spans. In the rational inattention context, different attention spans translates to different marginal costs of information acquisition. The forward optimization model of (CD15, ) is restrictive in that the decision maker has the same marginal cost in all decision problems (video categories in the YouTube context). The generalized model proposed in Corollary 4 allows for non-constant attention spans in different decision problems. In the context of the YouTube dataset for our numerical experiments, we use the terms ‘user engagement’ and ‘commenting behavior’ interchangeably.

Our numerical results show that

YouTube metadata features output pass the revealed rational inattention test by a large margin, where the goodness-of-fit to the rational inattention model is measured by computing the robustness metrics defined in Sec. 5. All our numerical results are completely reproducible and can be accessed from the GitHub repository https://github.com/KunalP117/YouTube-Commenting-Analysis.

2. Background

To set the stage for our unification result that relates revealed preference and revealed rational inattention, we start with a review of the key results of (FO09, ) (revealed preference for non-linear budgets) and (CD15, ) (revealed rational inattention).

2.1. Revealed preference (non-linear budget)

Theorem 1 ((FO09, )).

Consider a decision maker that, at time , chooses a consumption bundle subject to a non-linear budget constraint . Assume that is continuous, monotone and known to the external analyst, the set of feasible bundles is compact, and the budget constraint is active at , that is, . Then, the following statements are equivalent:

-

1.

There exists a monotone, continuous utility function that rationalizes the data set :

(1) -

2.

The data set satisfies GARP:

(2) where the relation (‘revealed preferred to’) means there exists indices such that .

- 3.

Theorem 1 says that a sequence of budget constraints and consumption bundles are rationalized by a utility function if and only if a set of linear inequalities (3) has a feasible solution. The GARP condition (2) is equivalent (due to (VR82, )) to the cyclical consistency condition proposed in (AF67, ). For completeness, we remark that constraining in the feasibility test (3) to be a constant for all , and assuming a linear budget in Theorem 1 is equivalent to testing for quasi-linear utility maximization (BR07, ), that is, the cyclical monotonicity condition of (BR07, , Theorem 2.2) holds. Indeed, cyclical monotonicity for quasi-linear utility maximization is a stronger condition than GARP.

2.2. Modifying the revealed preference test: Observed utility, unobserved budget constraint

Our key aim in this paper is to establish a correspondence between revealed preference and revealed rational inattention. However, both results differ in what the analyst knows about the decision maker’s decisions. Revealed rational inattention assumes the analyst knows the decision maker’s utility function and tests for the existence of a rationalizing information acquisition cost. Hence, to establish the correspondence, we need to modify Theorem 1 to the case where the analyst knows the decision maker’s utility function and tests for the existence of a rationalizing cost.555In classical revealed preference, the decision maker maximizes its utility (unknown to the analyst) subject to an upper bound on their budget (known to the analyst). Assumption 1 modifies the classical setup to the case where the decision maker minimizes a cost (unknown to the analyst) subject to a lower bound on their utility (known to the analyst). Under mild conditions on the decision maker’s cost and utility, both optimization problems are equivalent. However, for notational convenience, we pose the decision problem in such a way that the revealed preference estimand is the decision maker’s objective function. We formalize this departure from the problem setting in Theorem 1 in Assumption 1 below.

Assumption 1.

Consider the decision maker and analyst described in Theorem 1.

(A1.1) The analyst’s aim is to test if the decision maker chooses its consumption bundles optimally by solving the following optimization problem:

| (5) |

In (5), the decision maker minimizes the cost of choosing bundle subject to a lower bound on the utility.

(A1.2) The utility constraint in (5) is active, that is, for all .

(A1.3) The analyst knows the dataset defined as:

| (6) |

(A1.4) The analyst’s aim is to identify if there exists a cost that rationalizes the analyst’s dataset (6), that is, the observed responses solve the optimization problem (5).

In (5), we refer to in (5) as the ‘cost’ of purchasing consumption bundle , in comparison to a budget constraint in classical revealed preference where the utility function is unknown. The optimization problem in (6) is a cost minimization problem subject to a lower bound on the utility. A related model is studied in (VAR84-costminimization, ) where the decision maker at time minimizes a cost function but is constrained to choose its response from a specified compact set. In (VAR84-costminimization, ), analogous to WARP, the Weak Axiom of Cost Minimization (WACM) is proposed as a necessary and sufficient condition that rationalizes the dataset. In this paper, we focus on relating GARP from revealed preference theory to revealed rational inattention results. Hence, in Theorem 2 below, our necessary and sufficient condition for rationalizability is expressed in terms of the GARP condition (7) even though it is straightforward to express (7) in the style of (VAR84-costminimization, , Theorem 1). We are now ready to state Theorem 2. In complete analogy to Theorem 1, Theorem 2 below states necessary and sufficient conditions for utility maximization when the analyst knows the decision maker’s utility constraints (5).

Theorem 2 (Revealed Preference (Unknown Cost, Known Utility Constraints)).

Consider a decision maker that, at time , chooses a consumption bundle subject to a utility constraint . Suppose Assumption 1 holds and the set of feasible bundles is compact for all . Then, the following statements are equivalent:

-

1)

There exists a monotone, continuous cost that rationalizes the dataset , that is, (5) holds.

- 2)

- 3)

Theorem 2 above yields necessary and sufficient conditions for utility maximization behavior when the decision maker’s utility function is observed by the analyst; its budget (cost) is unobserved and must be reconstructed by the analyst by testing for feasibility of a set of Afriat-type inequalities (8) for rationalizability. The proof of Theorem 2 is in the appendix. At first sight, (5) in Theorem 2 appears to be a dual statement to the optimization problem (1) in Theorem 1. However, the proof does not use duality. Also, in comparison to the reconstruction procedure (4) that yields a point-wise minimum of piece-wise monotone functions, notice the reconstructed cost in (9) is a point-wise maximum of piece-wise monotone functions. Indeed, if is differentiable for all , then the cost also rationalizes the decision maker’s actions. This result follows from (FO09, , Proposition 2). Notice how in comparison to a piece-wise linear, concave utility reconstruction in Afriat’s theorem for linear budget constraints, we now have a piece-wise linear convex cost that rationalizes the decision maker’s actions if is differentiable.

Recall that our key objective is to establish a correspondence between revealed preference and revealed rational inattention (CD15, ). In revealed rational inattention, the analyst knows the agent’s utility and tests for the existence of a rationalizing information acquisition cost. In Sec. 3, we will show that the setup in (CD15, ) is a Bayesian analog of Theorem 2 and relate the reconstructed cost in (9) to the information acquisition cost. The key takeaway of Theorem 2 is that we have a revealed preference test for unobserved costs in terms of GARP. Authors in (CH17-nonseparable, ) have generalized the forward optimization problem in revealed rational inattention (CD15, ) so that the inverse learner uses a Bayesian analog of GARP instead of NIAC to test for rational inattention. However, as will be discussed in Theorem 1, the variable map for relating NIAC and GARP in this paper is distinct from (CH17-nonseparable, ); we rely on the auxiliary revealed preference result of Theorem 2 to establish the one-to-one correspondence.

2.3. Revealed Rational Inattention

Having introduced revealed preference results for non-linear budgets, we now turn our attention to the Bayesian utility maximization setup of (CD15, ). Since our aim is to relate Theorem 2 to revealed rational inattention, we review the key revealed rational inattention result of (CD15, ).

Before we state the key result, we describe the decision model of the Bayesian agent. Suppose the decision maker acts in a sequence of decision problems , where the decision problem parametrizes the decision maker’s utility. The decision maker in (CD15, ) is a Bayesian agent - it has a prior probability distribution over a finite set of states . In every decision problem , the agent chooses an information structure that maps every state to a probability distribution over a finite set of subjective signals ; the kernel is termed as the agent’s attention strategy in decision problem :

| (10) |

where denotes the space of probability distributions over the set . The agent then observes a realized signal (random variable) (and not the ground truth ) and updates its belief (posterior) of the unobserved state using Bayes rule:

| (11) |

After computing the belief , the agent then chooses an action from a finite set of actions according the conditional action policy:

| (12) |

The agent’s attention strategy and conditional action policy induce the action selection policy and is defined as the probability of choosing action if the true state is :

| (13) |

where is defined in (11) and conditional action selection policy is the probability the agent chooses action given belief in decision problem . In the revealed rational inattention problem, we assume the analyst knows the dataset:

| (14) |

In (14), is the prior probability distribution over the state space and is the agent’s action selection policy defined in (13). The variable is the agent’s discrete-valued utility in decision problem that depends on the state and action :

| (15) |

The analyst’s aim in revealed rational inattention is to test if the Bayesian agent acts optimally and maximizes its expected utility maximization less a non-negative information cost that depends only the attention strategy . The forward optimization problem is termed as ‘rationally inattentive utility maximization’ in the literature:

| Rationally Inattentive Utility Maximization: | ||||

| (16) | ||||

| (17) | ||||

| (18) |

In (16), denotes the agent’s belief computed using Bayes rule in (11) after observing signal . In (17), denotes the space of probability distributions over a set . Eq. 16 ensures that the agent maximizes its conditional expected utility given any posterior probability distribution computed using (11). Assuming (16) is true, (17) ensures that agent’s chosen attention strategy maximizes its objective function, namely, expected utility (17) minus an information acquisition cost. The analyst’s aim is to test for the existence of an information cost (18) that rationalizes the dataset (14), that is, the unobserved agent variables satisfy the optimality conditions (16), (17), which makes the revealed rational inattention result of (CD15, ) stated below remarkable.

Theorem 3 (Revealed rational inattention (CD15, )).

Consider a Bayesian agent that faces decision problems, where decision problem is parameterized by a finite set of states , signals , actions and utility (15). Suppose an analyst knows the dataset (14) that comprises the agent’s action selection policies and its utility functions in the decision problems. Then, the following statements are equivalent:

1) There exists a monotone information acquisition cost

that rationalizes the dataset . That is, the agent’s unobserved attention strategy (10) and conditional action policy (12) solve the nested optimization problem (16), (17) for all decision problems .

2) The dataset satisfies the ‘No-Improving-Action-Switches’ (NIAS) and the ‘No-Improving-Action-Cycles’ (NIAC) conditions:

| (19) | |||

| (20) | |||

| (21) |

The variable in (21) is the Bayesian agent’s surrogate expected utility. In (20), the variable is the marginal distribution of the action , the variable is the posterior belief of the state when action is realized.

3) The dataset satisfies the data-matching condition:

| (22) |

Theorem 3 is well-known in the information economics literature (CD15, ); see (CD15, , Sec. 10.2) and (PK23, , Appendix C.2.2) for the proof. The ‘No-Improving-Action-Switches’ (NIAS) (19) and ‘No-Improving-Action-Cycles’ (NIAC) (20) conditions in Theorem 3 are necessary and sufficient for the existence of an information acquisition cost that rationalizes the dataset , that is, conditions (a) (16) and (b) (17) hold. The first term in the LHS in (20) is the expected utility of the agent in decision problem . The second term in the LHS is the agent’s surrogate expected utility , surrogate since the expectation is in terms of the action selection policy of the agent, and not its attention strategy. It is straightforward to show that the attention strategy Blackwell dominates the action selection policy. We make the notion of Blackwell dominance precise in Lemma 3 below. Due to Blackwell dominance and Lemma 3, we further have the following inequality:

| (23) |

where equality holds when . A second observation that is crucial for the unification result of Theorem 1 below is that if and only if NIAS holds. Proving this relation is straightforward and omitted for brevity. Intuitively, the term is a surrogate for the agent’s expected utility since the inverse learner does not know the agent’s attention strategies. While necessity for optimality is straightforwardly determined, the sufficiency proof assumes to be a one-to-one map; the surrogate expected utility matches the true expected utility, that is, .

Abstractly, the NIAS condition is true if and only if condition (a) (16) is true, and the NIAC condition is true if and only if condition (b) (17) is true. Finally, the data-matching condition (22) ensures that the dataset is indeed generated from a Bayesian decision maker that makes an action based on its realized posterior belief.

Discussion of Theorem 3.

-

(1)

Classical revealed rational inattention (CD15, ) assumes that there exists a single utility function , and the Bayesian agent’s action choice in decision problem is restricted to a subset . This restriction can be equivalently modeled as the decision maker having a utility function in decision problem without any restriction on the choice of actions.666The problem setting in (CD15, ) is equivalent to setting if and otherwise, where is the agent’s fixed utility over decision problems.

-

(2)

Abstractly, Theorem 3 says that the analyst can test for rationally inattentive utility maximization (16), (17) even if the analyst only has access to a stochastically garbled 777Indeed, . Hence, the matrix with elements can be viewed as a noisy channel that takes as input the attention strategy and outputs the action selection policy . version of the attention strategy, namely, the action selection policy. We discuss this concept of stochastic garbling in more detail later in the paper in the context of Blackwell (BW53, ) partial order on the space of probability distributions.

2.4. Revealed rational inattention and observability of Bayesian agent’s decisions by the analyst

In revealed preference (Theorem 2), the analyst observes the agent decisions accurately. In revealed rational inattention (Theorem 3), the analyst observes a noisy version of the Bayesian agent’s decisions. A key yet unusual takeaway of revealed rational inattention is that the analyst can test for rational inattention by treating the noisy measurement of the agent decision as the true decision. We justify this claim below.

In the rational inattention model (16), (17), the decision maker, in decision problem , chooses its attention strategy and conditional action policy . The quantities of interest to the Bayesian decision maker, namely, the information acquisition cost and expected utility only depend on and , in addition to the prior that is assumed known to the analyst. Hence, it is intuitive to expect that test for optimal Bayesian decision-making is possible only if the chosen attention strategies and conditional action policies are known to the analyst performing revealed rational inattention.

However, unlike revealed preference, the analyst only observes the action selection policy that is a noisy (less informative) version of the attention strategy . Theorem 3 indicates that the knowledge of the action selection policies suffices for testing Bayesian rationality. In the context of our equivalence result stated in Theorem 1 below, testing if rational inattention (16), (17) holds is equivalent to testing if rational inattention (16), (17) holds when the attention strategy is replaced by the action selection policy . Hence, for the purpose of our equivalence result, we can treat the effective Bayesian decision maker’s ‘response’ as simply its action selection policy in decision problem . Let us briefly elaborate on the above claims:

-

•

If the agent is Bayes rational (16), (17), then the optimality conditions (16), (17) also hold when the attention strategy is replaced with the action selection policy, a noisy version of the attention strategy. Indeed, the proof of necessity of NIAS and NIAC for rational inattention shows that replacing the attention strategy in (16), (17) with the action selection policy, and testing for a weaker version of (17) to ensure optimality over a finite number of strategies yields the NIAS and NIAC inequalities. The key component in the necessity of the NIAS and NIAC conditions for rational inattention is Blackwell dominance discussed in Lemma 3; at a deeper level, NIAS and NIAC is necessary for (16) and (17) to hold since the attention strategy ‘Blackwell dominates’ the action selection policy.

-

•

The sufficiency proof of NIAS and NIAC for rational inattention assumes a one-to-one map from the observation to the action . Since the attention strategy is not observed, the analyst can assume that the observed action selection policy is the same as the unobserved attention strategy without loss of generality. Afriat (AF67, ) computes a set-valued utility function that rationalizes the finite dataset (6). In complete analogy, (CD15, ) exploit a result from quadratic assignment problems (KM57, ) to construct a set-valued rational inattention cost that is non-zero at the observed finitely many action selection policies (or equivalently, the attention strategies) in the environments, and elsewhere. Since the reconstruction of the rational inattention cost only occurs in the sufficiency part of the proof, it thus suffices to replace the attention strategy with the action selection policy and simply check for Bayesian rationality of the chosen action selection policies. For clarity, we also express the reconstructed information acquisition cost as a function of the action selection policy in the generalization of the revealed rational inattention test of (CD15, ) stated in Corollary 4 below and implicitly assume a one-to-one map from the observations to the actions.

To summarize, in this section we justify how an analyst can test for Bayesian rationality (16), (17) by assuming the observed action selection policy is the same as the unobserved attention strategy. The key idea is that since the attention strategy is not observed, the analyst can, without loss of generality, assume a one-to-one mapping from the observation to the action . As a result, in the equivalence result below, we will show that the Bayesian decision maker’s equivalent response is the action selection policy, and not the unobserved attention strategy and conditional action policy. Also, in Corollary 4 (a generalization of Theorem 3), the reconstructed information acquisition cost from the revealed rational inattention test is expressed in terms of the action selection policy; it is assumed that the action selection policy is the same as the unobserved attention strategy.

3. Main Result. Unification of Revealed preference and Revealed rational inattention

We present our first key result in this section that unifies revealed preference and revealed rational inattention. Our unification result is Theorem 1 below. Informally, the key takeaway of Theorem 1 is as follows:

The NIAC condition of (CD15, ) is a special case of GARP (7) if NIAS holds. If NIAC (20) holds, then the GARP condition (7) for utility maximization is true under an equivalent variable map. If NIAS holds, and the Afriat-type feasibility inequalities (8) are feasible with the Lagrange multipliers set to under the variable map, then the NIAC condition is true.

Let us now formalize the above takeaways in Theorem 1 below.

Theorem 1 (Unification of revealed preference and revealed rational inattention).

Consider the revealed rational inattention result of Theorem 3 and the revealed preference result of Theorem 2. Recall that the analyst uses dataset (14) to test for rational inattention (16), (17) in Theorem 3, and uses dataset (6) to test for utility maximization (5). Also, suppose the NIAS condition (19) holds for the dataset . Then:

- (1)

-

(2)

The following modification of rationally inattentive utility maximization (16), (17) generalizes NIAC in the revealed rational inattention test of Theorem 3 to a GARP-type condition:

Modified Rationally Inattentive Utility Maximization (16) and the following modification of (17) holds:(24) (25) where is defined in (18), and in (24) is a utility multiplier. We formalize the GARP-type generalization of NIAC in Corollary 4 below. Also, the setup in (24) is the “minimum” modification needed wrt the forward decision model in (CD15, ) specified by conditions (16), (17) that allows checking for optimality of the chosen attention strategy via a GARP-type condition.

We prove Theorem 1 in Appendix B and briefly discuss the intuition behind the proof below. A key aspect of the unification result (statement (1)) in Theorem 1 is that the equivalent variables in the Bayesian decision setup comprise only the variables observed by the external analyst. For example, although the analyst knows the Bayesian decision maker chooses the attention strategy and the action selection policy (12), the equivalent response under the variable map is only the observed action selection policy that depends on and . We justify this unusual claim in Sec. 2.4.

The key idea behind relating NIAC (20) and GARP (7) is to first express the NIAC condition for revealed rational inattention test in Theorem 3 as a feasibility inequality (51) (see Appendix B.1 for the proof), and then compare the feasibility inequality to the Afriat-type inequality (8) for the modified revealed preference test in Theorem 1. Under the variable map outlined in statement (1) in Theorem 1 above, we observe in the proof that the inequality (51) is the same as (8) with the Lagrange multipliers in (8) set to 1. As a result, we show that NIAC is a special case of GARP, when NIAS is true, under the variable map of Theorem 1.

3.1. Discussion of Theorem 1

Theorem 1 presents three key results on the unification of revealed preference and revealed rational inattention discussed in more detail below:

-

(1)

Assuming NIAS holds for the unification result. Recall from Theorem 3 that the first term in the summation in the LHS of the NIAS feasibility condition is the expected utility under the joint distribution . The variable map in statement (1) of Theorem 1 requires that the surrogate expected utility be equal to the expected utility that holds only if NIAS is true. In words, the revealed rational inattention test of Theorem 3 checks (a) if the decision maker chooses the optimal action given its posterior belief from a realized observation, and (b) if the decision maker’s expected utility from the chosen attention strategy less the information acquisition cost exceeds that for any other attention strategy chosen in the remaining decision problems. Assuming NIAS is true ensures the decision’s expected utility is the maximum possible utility for the decision maker, where the maximum is taken over all conditional action policies . Put differently, assuming NIAS to be true only requires the analyst to check NIAC for testing rational inattention, and hence, enables a one-to-one comparison with revealed preference.

-

(2)

Treating the action selection policy as the effective response for the Bayesian agent. The variable map in statement (1) in Theorem 1 states the the equivalent response in the Bayesian setup is the action selection policy, a noisy version of the unobserved attention strategy chosen by the agent. Although unusual, it suffices for the analyst to treat the action selection policy to be the same as the attention strategy for testing Bayesian rationality; we discuss this in more detail in Sec. 2.4.

-

(3)

Relating NIAC and GARP via a variable map. Statement (1) in Theorem 1 establishes a one-to-one correspondence between revealed preference and revealed rational inattention and relates both approaches via a variable map. The key takeaway is that NIAC is a special case of GARP, when NIAS is true. We see from the variable map in Theorem 1 that in the Bayesian decision framework, the “effective” utility function from revealed preference is the surrogate expected utility (21) that encodes both the prior pmf and utility , and depends on the observed action selection policy. The cost in revealed preference translates to the information acquisition cost in revealed rational inattention.

Statement (2) introduces a generalization of the forward optimization model considered in (CD15, ) for which the NIAC condition generalizes to a GARP-type condition. We formalize the revealed rational inattention test for the generalized model in Corollary 4 below. The generalization of NIAC, namely, GARRI defined in (26) in Corollary 4 is equivalent to a Bayesian analog of GARP, thus completely unifying revealed rational inattention and revealed preference. -

(4)

Generalizing the rational inattention model of (CD15, ). The key distinction between the generalized model (24) and the classical rational inattention model considered in (CD15, ) specified by (16) and (17) is the free variable . Analogous to Theorem 1 where the Lagrange multipliers (3) can be interpreted as the marginal utility of the decision maker, in (24) can be interpreted as the marginal cost in the constrained cost minimization problem (25). Eq. 17 is equivalent to (24) with set to a constant. As a result, the revealed rational inattention test of Theorem 3 yields the cyclic NIAC condition for checking Bayesian rationality (17). However, the generalized model of (24) has as a free variable and must be estimated by the external analyst in addition to testing for the existence of an information acquisition cost. The revealed rational inattention test for the generalized model yields the acyclic GARRI condition defined in (26) in Corollary 4 below, and is equivalent to GARP under the above variable map.

-

(5)

Change of partial order from revealed preference to revealed rational inattention. In the variable mapping of Theorem 1, the “response” in the Bayesian setup lies in the unit simplex of probability mass functions. More precisely, the response belongs to the space , where is the unit simplex of pmfs over the set of signals . Clearly, with respect to the natural element-wise partial order of Euclidean spaces, the expected utility and information acquisition cost are not monotonically increasing in . Hence, the unification result of Theorem 1 involves equipping the space of attention strategies with a different partial order, namely, the Blackwell partial order (BW53, ) for probability measures discussed in more detail below.

3.2. Change of partial order from revealed preference to revealed rational inattention

The change of partial order from the natural element-wise partial ordering of positive vectors in the Euclidean space for revealed preference to the Blackwell (BW53, ) partial ordering of attention strategies is a key component in establishing the one-to-one correspondence in Theorem 1 above. Let us discuss the Blackwell order in detail.

Definition 0 (Blackwell order (BW53, )).

Consider two attention strategies , where and denote the finite set of states and private signals, respectively, in the rationally inattentive utility maximization framework of Theorem 3. Then, Blackwell dominates (denoted as ) if there exists a row-stochastic matrix such that .

The Blackwell order introduces the notion of monotonicity in the space of attention strategies (probability distributions). The Blackwell order is a partial order, since there exist attention strategy pairs that cannot be ordered via the Blackwell relation (Definition 2). Intuitively, attention strategy Blackwell dominates if is a noisy (garbled) version of . In classical revealed preference results, the decision maker’s response belongs to the Euclidean space. The standard assumption (and key to establishing revealed preferences results) is to impose a monotonicity condition on the decision maker’s budget constraint with respect to the element-wise partial ordering for the Euclidean space. The Blackwell partial order can be viewed as a Bayesian analog of the element-wise ordering for rational inattention. Recall from the equivalence result of Theorem 1 that a constraint on the expected utility is the rational inattention analog of the decision maker’s budget constraint in revealed preference. For the reader’s clarity, we show below the expected utility is monotone with respect to the Blackwell partial order.888That a convex functional in monotone with respect to the Blackwell partial order is well-known in the literature, and stated in the main text for completeness. In future work, we will investigate more general partial orders such as interval dominance and integral precision dominance and how they affect revealed rational inattention results.

Lemma 0.

Consider the rationally inattentive utility maximization setup in Theorem 2. Suppose NIAS holds, that is, the decision maker chooses the optimal action given its posterior belief. Also, suppose the space of attention strategies (probability simplices) are equipped with the Blackwell partial order (Definition 2). Then, the decision maker’s expected utility (21) is monotonically increasing and convex in the attention strategy.

The proof of Lemma 3 is in Appendix C. Lemma 3 facilitates the one-to-one correspondence between the revealed preference results of Theorem 2 (element-wise partial order over consumption vectors) and the revealed rational inattention result of Corollary 4 (Blackwell partial order over attention strategies).

Remark. Lemma 3 states the expected utility is monotone is the Bayesian decision maker’s ‘response’, namely, the action selection policy under the Blackwell order. However, it is straightforward to show any convex functional is monotone wrt the Blackwell order. Indeed, the expected utility (21) is convex in the action selection strategy.

To summarize, in revealed preference, the cost of consumption is monotone with respect to the natural element-wise partial order on the Euclidean space. The reconstructed utility function (AF67, ) is a monotone function of the consumption cost, and hence, is also monotone with respect to the natural element-wise partial order. In complete analogy, in revealed rational inattention, the expected utility is monotone with respect to the Blackwell order on the space of attention strategies. Corollary 4 below presents an Afriat-type reconstruction of a valid information acquisition cost. The reconstructed information acquisition cost is a monotone function of the expected utility, and hence, is also monotone with respect to the Blackwell order.

3.3. Generalizing Revealed Rational Inattention to Variable Attention Spans

Having stated our equivalence result in Theorem 1 and Lemma 3 above, we now state our second theoretical result, Corollary 4. Recall from statement (1) in Theorem 1 that NIAC is a special case of GARP. Corollary 4 generalizes the revealed rational inattention result of (CD15, , Th. 1) to a decision model with added degrees of freedom to accommodate variable attention spans of the Bayesian decision maker in different decision problems, or equivalent, different marginal costs of information acquisition in the rational inattention setup of (17). The key idea is to introduce minimum additional degrees of freedom in the rationally inattentive utility maximization model of (CD15, ) so that the rationalizability condition for the inverse task generalizes from NIAC to a GARP-type condition. We term the rational inattention analog of GARP as GARRI, defined in (26) below.

Motivation to generalize the rational inattention model of (CD15, )

Generalizing the revealed rational inattention test of (CD15, ) is useful because empirical studies (YT-diff-1, ; YT-diff-2, ; YT-diff-3, ) on online user engagement data show that online multimedia users have different attention spans in different decision problems. In the rational inattention context, different attention spans translate to different marginal costs of information acquisition. The forward optimization model of (CD15, ) is restrictive in that the decision maker has the same marginal cost in all decision problems (video categories in the YouTube context). In comparison, the generalized revealed rational inattention test proposed in Corollary 4 below allows for non-constant attention spans of the decision maker in different decision problems. Also, cognitive psychology literature (diff-lambda-supp-1, ; diff-lambda-supp-2, ; diff-lambda-supp-3, ) suggests the human attention span (hence, the information acquisition cost) is task-dependent (decision problem-dependent), in contrast to the rational inattention model of (CD15, ) where the expected utility and information acquisition cost are weighed equally for decision making. The above works serve as motivation to generalize the rational inattention model of (CD15, ) to test for non-constant values for the margin cost of information acquisition in datasets aggregated from human decisions.

Corollary 0.

Consider the Bayesian decision maker in Theorem 3. Suppose the analyst knows the dataset (14) and tests for generalized rationally inattentive utility maximization, namely, conditions (16) and (24). In (24), the positive utility multiplier is unknown to the analyst. Then, the following statements are equivalent:

1) There exists a monotone (wrt Blackwell order (Lemma 3)) information acquisition cost

that rationalizes the dataset . That is, the dataset satisfies the data-matching condition (22), and the agent’s unobserved attention strategy (10) and conditional action policy (12) solve the nested optimization problem (16) and (24) for all decision problems .

2) The dataset satisfies the data-matching condition (22), NIAS (19) and the Generalized Axiom of Revealed Rational Inattention (GARRI) defined below. GARRI (26) is equivalent to GARP (7) under the variable map of statement (1) in Theorem 1.

| (26) | GARRI: |

where the relation means there exists indices s.t. , . The surrogate expected utility in (26) is defined in (21).

3) The dataset satisfies the data-matching condition (22) and NIAS (19). Also, there exist positive scalars such that the following inequalities hold for all pairs of decision variables :

| (27) |

where is the marginal distribution of the agent’s action in decision problem , is the posterior distribution of the agent’s state in decision problem .

4) If NIAS and GARRI hold, the following reconstructed information acquisition cost rationalizes the dataset :

| (28) |

where the positive scalars are feasible solutions of (27), and is the decision maker’s surrogate expected utility defined in (21).

The Afriat-type (AF67, ) reconstructed cost in (28) is a point-wise maximum of monotone convex functions, monotone with respect to the Blackwell order on the space of action selection policies.

The reconstructed cost also satisfies the axiomatic properties of weak monotonicity and mixture feasibility as postulated in (CD15, , Theorem 2).

Equivalence between GARRI and GARP. Corollary 4 assumes the same problem setting as that of Theorem 3. The only difference in the problem setting between Theorem 3 and Corollary 4 is the additional scalar multiplier in (24). The key takeaway is that the NIAC condition for checking optimality of attention strategies across decision problems is replaced by the generalized axiom of revealed rational inattention (GARRI) (26). Indeed, NIAC is a special case of GARRI since (17) is a special case of (24) with for all . In fact, the addition of the non-constant multiplier is the minimum modification needed in the decision model of (CD15, ) for checking the optimality of the chosen attention strategies via the cyclical consistency of condition of GARP, instead of the more restrictive cyclical monotonicity condition of NIAC.

Afriat-type reconstruction of information acquisition cost. Corollary 4 builds on (CD15, ) and reconstructs an Afriat-type monotone convex cost of information acquisition (28) that rationalizes the dataset (14). Afriat’s (AF67, ) utility reconstruction involves ‘stitching’ a piece-wise linear, concave utility function that rationalizes the agent’s actions and is expressed in terms of the utility value earned by the agent at every time step and the budget constraints. In complete analogy, the piece-wise convex monotone cost (28) rationalizes the dataset (14) and is expressed in terms of the information acquisition cost incurred by the agent in every decision problem and the surrogate expected utility functional . Recall from Sec. 2.4 that the analyst performing revealed rational inattention can treat the observed action selection policy as the unobserved attention strategy chosen by the Bayesian agent. Hence, the reconstructed cost of information acquisition is a function of the observed variable, namely, the action selection policy. The reconstructed utility function in (AF67, ) is locally non-satiated, monotone and concave, and rationalizes the observed price and consumption bundles. In complete analogy, the reconstructed cost (28) is weakly monotonic (in information (Blackwell partial order (BW53, ))), mixture feasible (convex) and normalized, and rationalizes the observed utility functions and action selection strategies in (14).

Remark. The authors of (CD15, ) generalize their results to posterior separable costs of information acquisition in (CDL19rationalinattention, ). Specifically, (CDL19rationalinattention, , Theorem 2) provides a constructive procedure for recovering a posterior separable cost that satisfies the rationalizability axioms for optimality in decision making under posterior cost constraints. Apart from the Afriat-style of cost construction, the construction style in (CDL19rationalinattention, , Theorem 2) differs from that in Theorem 1 in one key aspect. Our reconstruction procedure assumes the inverse learner only has access to a finite set of agent utility functions from finitely many environments, that is, the completeness axiom in (CDL19rationalinattention, , Axiom A4) is not assumed.

4. Related Works

There are several works in the economics literature that generalize classical results of revealed preference and revealed rational inattention. In this section, we compare GARRI (26), the Bayesian analog of GARP, in Corollary 4 with related existing works.

GARRI and GAPP. (DEB18-GAPP, ) test for the existence a preference relation over prices set by the buyer, instead of a preference relation over consumption bundles. The key testable axiom is Generalized Axiom of Price Preference (GAPP). Corollary 4 proposes a GARP-type condition, GARRI that generalizes NIAC. In complete analogy, GARP is a generalization of the GAPP condition of (DEB18-GAPP, ). A key point is that GAPP generalizes (and is not equivalent to) the test for quasi-linear utility maximization, even though the above relations might suggest drawing this conclusion. We discuss the relation between GARI and revealed preference test for quasi-linear utility maximization below.

GARRI, NIAC and Strong law of demand. We now relate revealed rational inattention (Corollary 4) and revealed preference for quasi-linear utility maximization (BR07, ). Theorem 2.2 in (BR07, ) proposes testable conditions for quasilinear utility maximization and term this rationalization as strong law of demand. Test for quasilinear utility maximization checks for the existence of a utility function such that the following condition holds for :

| (29) |

The objective function of (29) is a non-Bayesian analog of the decision framework of (CD15, ), with the response replaced with , utility replaced with , and cost replaced with the information acquisition cost . Under the variable map of Theorem 1, the cyclical monotonicity condition of (BR07, , Definition 3), a special case of GARP (7), is equivalent to NIAC (20), a special case of GARRI (26). Testing for quasilinear utility maximization (BR07, , Theorem 2.2) is equivalent to checking for the feasibility of Afriat’s inequalities with constant Lagrange multipliers. In complete analogy, testing for the classical rational inattention setup of (CD15, ) is equivalent to checking for the feasibility of (27) with the Lagrange multipliers set to a constant.

GARRI and GACI.

(CH17-nonseparable, ; REH20-rational, ) generalize (CD15, ) to the case where the decision maker maximizes a non-separable objective function. The key axiom that generalizes NIAC to the non-separable case is the Generalized Axiom of Costly Information (GACI) (CH17-nonseparable, , Condition 1), that possesses the cyclical monotonicity structure of GARP. However, on careful examination, we observed that the variable map from the Bayesian to non-Bayesian decision framework in (CH17-nonseparable, ) is distinct from the one proposed in Theorem 1 in spite of the GARP flavor in both GACI and our proposed generalization of NIAC, namely, GARRI (26) in Corollary 4. (CH17-nonseparable, ) relate the revealed attention strategy to the price of a good, and the

expected utility functional to the response of the decision maker in revealed preference. However, in our equivalence result, the expected utility functional is analogous to the utility constraint (5), and attention strategy is analogous to the decision maker’s response in the modified revealed preference setup in Sec. 2.2. The difference in the variable map between GARRI and (CH17-nonseparable, ) to GARP can be attributed to Theorem 2 that yields a GARP-type condition for testing if the decision maker minimizes an unobserved cost subject to a lower bound on its utility. We remark that the decision model of (CH17-nonseparable, ) accommodates both models of (CD15, ) and Corollary 4 as special cases. However, the addition of the scalar multiplier in (24) is the minimum modification required in the decision framework of (CD15, ) for the dataset to be rationalized by a GARP-type condition.

5. Extending Robustness Measures in Revealed Preference to Revealed Rational Inattention

We now exploit the equivalence result of Theorem 1 and the generalized revealed rational inattention result of Corollary 4 to construct robustness measures for the revealed rational inattention test. The key idea is to compute the minimum perturbation needed for a dataset to pass the revealed rational inattention test, namely, the feasibility of NIAS and GARRI conditions in Corollary 4. There are several works in the revealed preference literature that characterize how far a sequence of budget constraints and consumption bundles is from satisfying GARP (2). To the best of our knowledge, there is no formal approach in the literature to measure how well a dataset (14) fits the rational inattention model.

Abstractly, the key idea behind the robustness measures in revealed preference is to minimally perturb the observed dataset so that GARP holds. A few notable robustness measures include:

1. The ‘Afriat Efficiency Index (AEI)’ (AFT72-efficiency, ) that yields the minimum relaxation (expenditure wastage) needed in the budget constraints to rationalize the data.

2. The chi-squared ‘Minimal Perturbation Test (MPT)’ (VAR85-measurement, ) where the analyst assumes an additive measurement error in the observed response, and performs a chi-squared test on the minimum -deviation from the observed responses such that the perturbed responses rationalize the dataset.

3. The ‘Money Pump Index (MPI)’ (ECH11-moneypump, ) that yield the maximum profit a seller can make from a dataset violating GARP.

4. The ‘Minimum Cost Index (MCI)’ (DEA16-mincost, ) that yields the lowest normalized cost of breaking all revealed preference cycles from a dataset.

5. The ‘Houtman-Maks Index (HMI)’ (HTM85-consistency, ) that, for a specified rationalizability tolerance, outputs the largest subset that satisfies GARP.

In this section, we exploit the equivalence result of Theorem 1 and extend the robustness measures described above to revealed rational inattention. For brevity, we only discuss the rational inattention analogs of robustness measures 1-3 above, namely, the Afriat Efficiency Index (AEI), Minimal Perturbation test (MPT) and the Money Pump Index (MPI). However, we emphasize that any robustness measure from the revealed preference literature can be extended to the revealed rational inattention test via the unification result of Theorem 1.

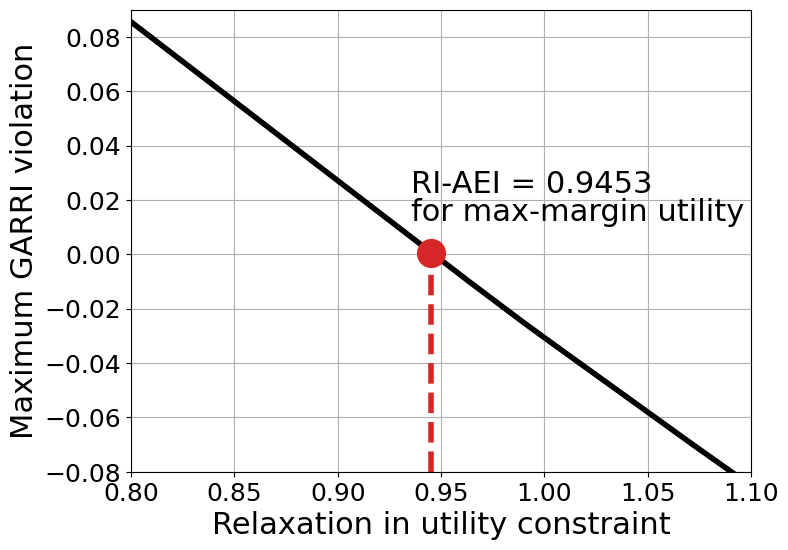

5.1. Afriat Efficiency Index for Rational Inattention (RI-AEI)

In the classical revealed preference setup with linear budget constraints, the Afriat Efficiency Index (AEI) (AFT72-efficiency, ) is a uniform lower bound on the scalar multiplier so that GARP holds for a dataset The variables and denote the price vector and consumption bundle at time , the consumer’s budget constraint is given by . AEI is defined as:

| (30) |

where GARP() is a generalization of GARP defined as:

| (31) |

In (31) above, is the indicator function. In words, the constraint in (31) says that, for a relaxation level , if is e-affordable at time , then it must be that must not be e-affordable at time . Clearly, setting in (31) yields the classical GARP condition (2) for linear budget constraints. The parameter can be viewed as a relaxation of the GARP condition. Hence, AEI measures the minimum relaxation in budget constraints needed for the dataset to satisfy utility maximization behavior.

It is straightforward to show that, for a fixed value of , checking if GARP() (31) holds is equivalent to checking for the feasibility of the following set of linear inequalities:

| (32) |

Hence, AEI for the dataset can be computed as:

| (33) |

If the dataset satisfies Afriat’s inequalities for utility maximization behavior, then AEI when computed via (33).999Indeed, GARP() is equivalent to the square matrix satisfying GARP. Using the relation between the elements of the square GARP matrix to the Afriat inequalities (FOS04, , Th. 2), the constraint in (33) results as an equivalent formulation for GARP(). We now extend AEI to the revealed rational inattention setup of Corollary 4 by invoking the equivalence result of Theorem 1. For clarity, we term AEI for the revealed rational inattention case as Rationally Inattentive-AEI (RI-AEI).

Definition 0 (Rationally Inattentive Afriat Efficiency Index (RI-AEI)).

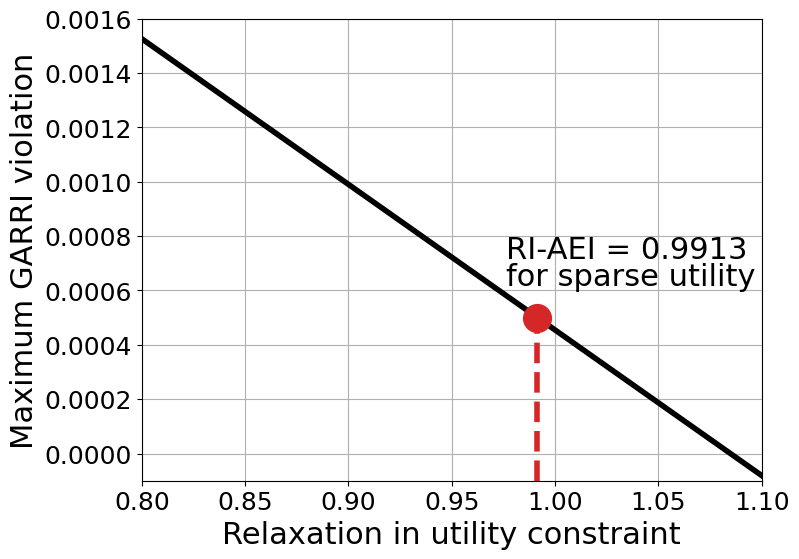

Consider an external analyst with the stochastic choice dataset (14). The rationally inattentive Afriat efficiency index (RI-AEI) is the minimum relaxation in expected utility constraints (25) required for the dataset to be consistent with rationally inattentive utility maximization behavior. RI-AEI is defined as:

| (34) |

If satisfies the feasibility inequality in (LABEL:eqn:RI-AEI) above, then the dataset is consistent with rationally inattentive utility maximization. If not, then the minimum value of for which (LABEL:eqn:RI-AEI) has a feasible solution is bounded from below by , in contrast to AEI (30), where the minimum perturbation needed for a dataset to satisfy GARP is less than unity. This difference arises due to the decision maker’s constraint in the rationally inattentive case. Recall from (1) that for the non-Bayesian decision model in revealed preference, the decision maker faces an upper bound on its budget, whereas in the rational inattention setup of Corollary 4, the decision maker faces a lower bound on the expected utility (25).

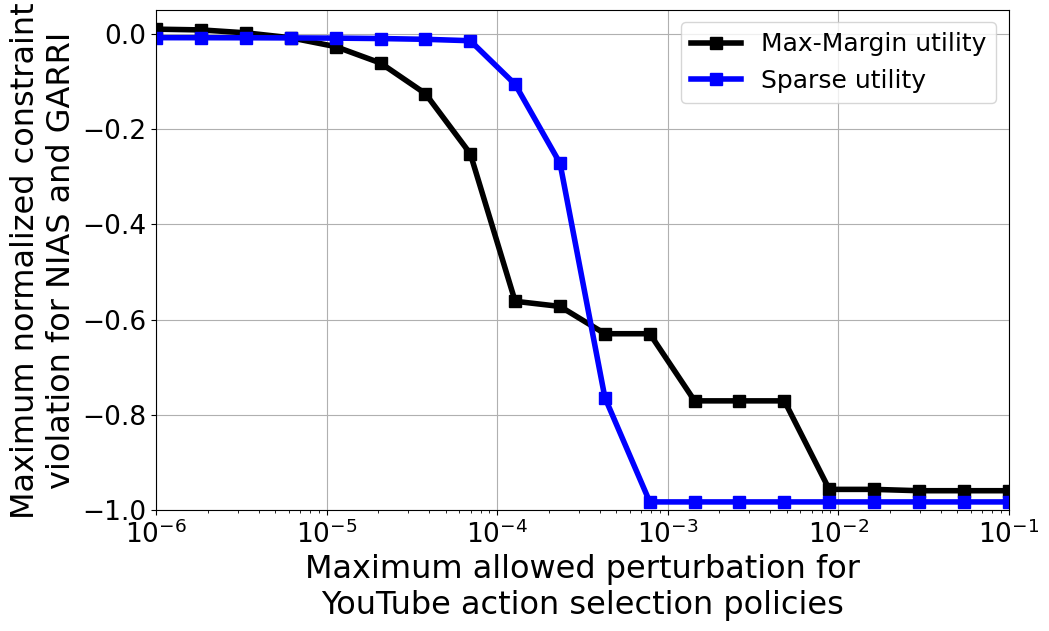

5.2. Minimum Perturbation Test for Rational Inattention (RI-MPT)

The minimum perturbation test (MPT) introduced in (VAR85-measurement, ) assumes the decision maker’s chosen consumption bundles are measured in noise, and computes the minimum perturbation needed in the consumption bundles for the dataset to be consistent with utility maximization behavior.

Suppose the analyst has a noisy dataset , where is a noisy version of the true response unobserved by the analyst, and the measurement error is an i.i.d. random variable with pdf . Assume, WLOG, that the decision maker’s budget constraint at time is given by .

Let us now introduce the null and alternate hypotheses and :

: The true (noiseless) dataset satisfies GARP (2), : The true dataset does NOT satisfy GARP (2).

The analyst then performs MPT on the noisy dataset , namely, computes a test statistic defined below and performs a hypothesis test to reject or accept the null hypothesis :

| (35) |

where is a parameter that bounds the detector’s Type-I error probability . The rationale behind (35) is that if holds, then is a lower bound on the measurement error . This observation further implies (see (KH17, ; PKB22-jrnl, ) for details) that the Type-I error probability of the hypothesis test is upper bounded by , where is the cdf of the noise pdf .

We now extend MPT (35) to the rationally inattentive utility maximization setup of (CD15, ) by exploiting the equivalence result of Theorem 1. Suppose the analyst has a noisy dataset , where is a noisy version of the true action selection policy .101010Noise in probability mass functions may arise due to multiple factors such as misspecification error, or computing the action selection policy empirically from a finite number of samples; see (PK23, ) for a finite sample analysis of the revealed preference test. For clarity, we term MPT for the revealed rational inattention case as Rationally Inattentive-MPT (RI-MPT).

Definition 0 (Rationally Inattentive Minimum Perturbation Test (RI-MPT)).

Consider an external analyst with the stochastic choice dataset (14). The rationally inattentive minimum perturbation test (RI-MPT) is the minimum perturbation in the observed action selection policies required for the dataset to be consistent with rationally inattentive utility maximization behavior. The RI-MPT is defined as:

| (36) |

In (36) above, is the marginal action probability, and is the posterior state distribution given action selection policy .

RI-MPT defined in (36) above is a hypothesis test that considers the minimum perturbation needed in the action selection policies for the feasibility of NIAS and GARRI conditions as the sufficient statistic for the test. In complete analogy to (35), the variable in (36) controls the Type-I error probability of detecting Bayesian rationality, that is, NIAS and GARRI conditions hold for the noise-less dataset (14).

5.3. Money Pump Index for Rational Inattention (RI-MPI)

The money pump index (MPI) introduced in (ECH11-moneypump, ) quantifies the severity of violations of GARP. If the decision maker’s choices are observed in noise, the computed value of MPI can be used to test if the decision maker is rational or not. In this section, we consider the case where the decision maker’s responses are measured accurately. MPI is defined for a sequence of tuples of prices and consumption bundles that violate GARP. Consider the classical revealed preference setup in Theorem 1 with linear budget constraints . Suppose the sequence violates GARP (). Then MPI for the violating sequence is defined as:

| (37) |

If GARP fails for the sequence , it is straightforward to show that MPI in (37). Intuitively, MPI measures the profit a malicious arbitrager can make by buying the consumption bundles in the GARP-violating sequence at a lower price, and selling the same bundles to the non-rational decision maker at a higher price.

We now extend MPI (37) to the rationally inattentive utility maximization setup of (CD15, ) by exploiting the unification result of Theorem 1. We term MPI for the revealed rational inattention case as Rationally Inattentive-MPI (RI-MPI).

Definition 0 (Rationally Inattentive Money Pump Index (RI-MPI)).

Consider an external analyst with the stochastic choice dataset (14). The rationally inattentive money pump index RI-MPI is defined as:

| (38) |

where and defined below is the net expected utility a malicious arbitrager can gain by exploiting the fact that the Bayesian decision maker’s choices fail the GARRI (26) condition:

| (39) |

In (39), is the expected utility functional defined in (18).

In (ECH11-moneypump, ), the money pump index is defined for a sequence of indices for which GARP fails. In complete analogy, (38) in Definition 3 computes the maximum ‘profit’ a malicious arbitrager can make over all possible sequences of decision problems combinations, normalized by the sum of expected utilities of the Bayesian decision maker in the decision problems. The extent of irrationality of the Bayesian maker that facilitates arbitrage is captured by the variable in (38) and discussed below in more detail.

Let us briefly discuss the intuition behind RI-MPI (38). Without loss of generality, suppose GARRI fails for indices (sequence of length 2), which implies the following set of inequalities hold:

| (40) |

The term measures the excess expected utility a malicious arbitrager can gain by ‘buying’ choices when presented with utilities in decision problems , respectively, and selling choices to the Bayesian decision maker in decision problems , respectively.

Summary. In this section, we extended three robustness measures from revealed preference to the revealed rational inattention result of Corollary 4. Specifically, we extended the Afriat Efficiency Index (AEI) (AFT72-efficiency, ), Varian’s (VAR85-measurement, ) Minimum Perturbation Test (MPT) and the Money Pump Index (MPI) (ECH11-moneypump, ) to the Bayesian case. We now illustrate the Bayesian analogs of AEI, MPT and MPI on a real-world YouTube metadata comprising user engagement from approximately 140,000 videos. We characterize, using the robustness measures for rational inattention defined above, the goodness-of-fit to the YouTube dataset to the rationally inattentive utility maximization model.

6. Example. Testing YouTube metadata for rational inattention

The first part of the paper thus far comprised theoretical results on unification of tests for revealed preference and revealed rational inattention, and extension of measures for goodness-of-fit in revealed preference to revealed rational inattention. The second part of the paper, namely, this section, focuses on computational aspects of the results presented in the first part. In this section, we illustrate the robustness metrics introduced in Sec. 5, namely, RI-AEI, RI-MPT and RI-MPI on a real-world YouTube dataset.111111Although our past works (HKP20, ; PK23, ) use the same dataset for numerical experiments, the dataset pre-processing steps and experimental results in this paper are new.

For our numerical experiment on a real world dataset, we consider a YouTube dataset comprising approximately 140,000 videos across 25,000 channels spanning 18 video categories and over 9 millions users from April 2007 to May 2015. The diversity of videos in YouTube is immense; YouTube users engage differently with YouTube videos in different video categories (YT-commenting, ). There are several works in the literature (PK23, ; HKP20, ; YT-content, ) that perform YouTube metadata analysis using tools from microeconomics and machine learning. However, to the best of our knowledge, a principled approach to characterizing the goodness-of-fit of YouTube user engagement to revealed rational inattention tests have not been addressed in the literature. A revealed rational inattention-based analysis is especially suitable for the YouTube dataset since the dataset does not comprise the visual cues (private signals) perceived by the online user from the video webpage before choosing to engage on the YouTube platform. In complete analogy, the analyst performing revealed rational inattention has no knowledge of the decision maker’s private signals,and yet, due to Blackwell dominance, can reconstruct feasible utility functions and information acquisition costs that rationalize the decision maker’s actions.

Our aim in the second part of the paper is to analyze groups of YouTube users in different video categories and test using revealed rational inattention if YouTube user engagement is consistent with rationally inattentive utility maximization. The authors in (YT-cognition, ; YT-cognition-2, ; YT-cognition-3, ) analyze how YouTube video content affects user behavior, emotion and cognitive engagement. Our aim in this paper is to study YouTube user engagement from an information economics perspective - characterize YouTube user engagement in different video categories with different utility functions, but the same cost of information acquisition. Formally, our aim is to:

(1) Transform the Youtube video metadata in a form amenable to the rationally inattentive utility maximization framework of (16) and (24) in order to perform revealed rational inattention analysis.

(2) Identify if YouTube user engagement is rationally inattentive (checking the feasibility of NIAS and GARRI conditions of Corollary 4), and if so, construct the YouTube users’ utility functions in different video categories, and their cost of information acquisition. In the YouTube context, the utility function is the online social reward a typical YouTube user earns by engaging with a particular YouTube video. The information acquisition cost abstracts the cognitive perception cost expended by the online user on the YouTube video.

(3) Compute the goodness-of-fit of YouTube user engagement to the revealed rational inattention test of Corollary 4 by computing the robustness metrics in Sec. 5. The goodness-of-fit for rational inattention quantifies the maximum perturbation needed in the YouTube dataset so that the revealed rational inattention test of Corollary 4 fails. Goodness-of-fit tests for rational inattention are novel and are facilitated primarily due to the unification result of Theorem 1, and, to the best of our knowledge, have not been previously explored in the literature.

6.1. Context. YouTube user engagement and rational inattention

YouTube is a social multimedia platform where human users interact with video content on YouTube channels by posting comments and rating videos. Empirical studies ((KH17, ; HG17, ; ABCH15, ; AK17, )) show that the comments and ratings from users are influenced by the thumbnail, title, category, and perceived popularity of each video. Models for human decision making in the context of online multimedia platforms have been studied extensively in the literature. Two widely-used classes of models that motivate us to understand YouTube user engagement from the lens of rational inattention are ‘parallel constraint satisfaction models’ and ‘evidence accumulation models’.

Parallel constraint satisfaction models ((GCK08, ; MC89, )) assume that information is screened sequentially to highlight salient alternatives and final choice is made when the decision maker reaches sufficient internal coherence.

Evidence accumulation models ((KRA10, ; RC04, )) model consumers’ attention by drift-diffusion models that accumulate evidence based on whether they are fixating their gaze on either the product or its price. The decision is taken when any of the alternatives’ evidence threshold level is achieved.

Both classes of models described above have one aspect in common - the decision maker makes a final choice after sequentially accumulating information, and naturally fits our rational inattention framework. In particular, we refer the reader to (CD15, , Sec. 5.1), (PK23, ) where sequential information accumulation frameworks are expressed as a one-shot decision framework (17). The key idea is to map the sequence of realized observations to a single meta-observation, where is a stopping time. The main takeaway is that NIAS and NIAC are still necessary and sufficient for rational inattention in a sequential information accumulation framework. Hence, we are justified in performing the revealed rational inattention test on YouTube metadata.

In terms of YouTube webpage parameters, we hypothesize the YouTube user is a Bayesian agent that sequentially consumes webpage cues such as thumbnail and title and incurs a cost of attention, followed by engaging on the YouTube platform and gaining a social utility (YT-social-utility, ). Our revealed rational inattention aim is to embed YouTube user engagement in the rational inattention framework, and construct utility functions identify using the YouTube dataset, if online users engage ‘optimally’ on the YouTube multimedia platform in a rationally inattentive utility maximization sense.

6.2. YouTube Dataset and Model Parameters

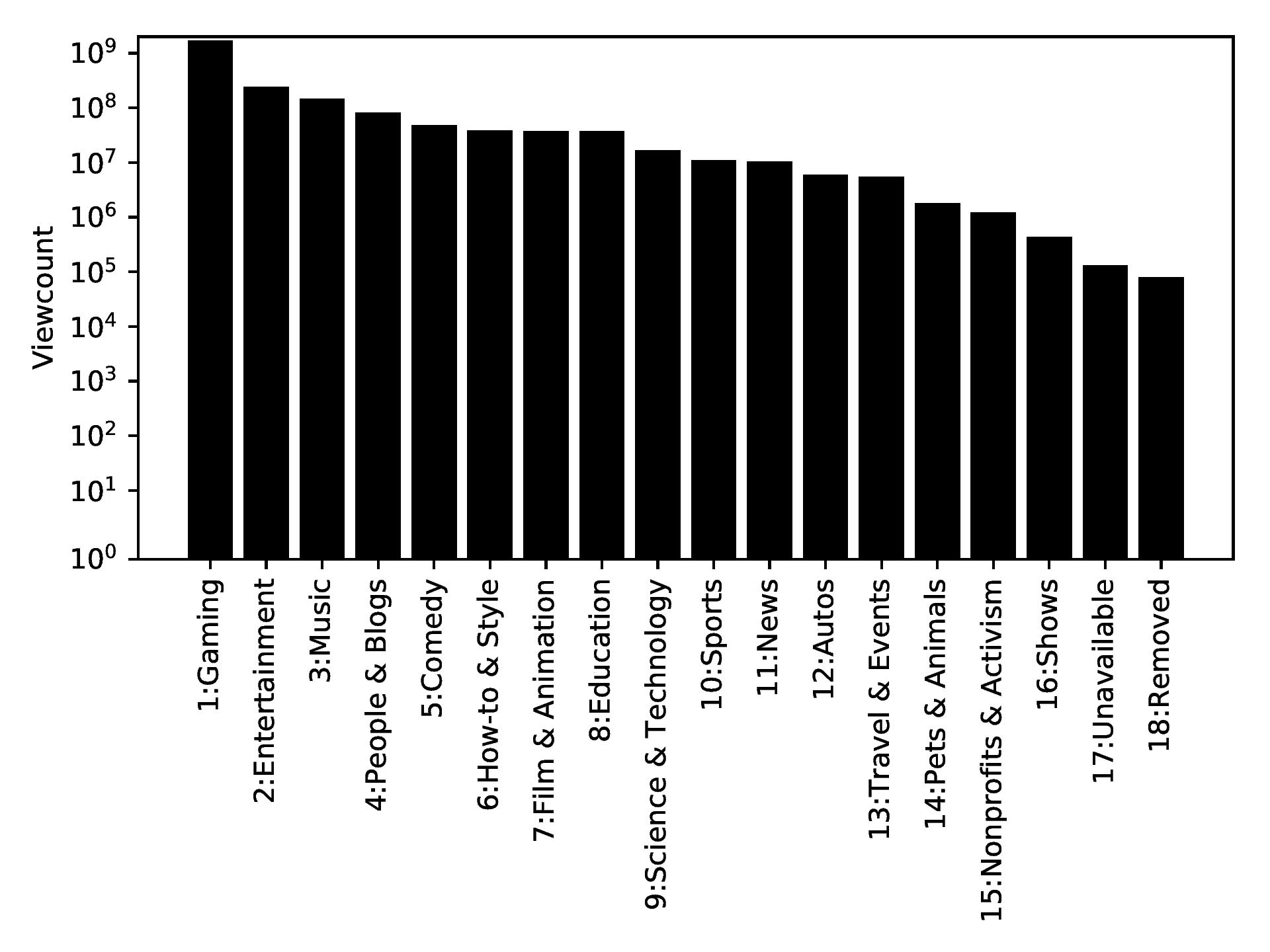

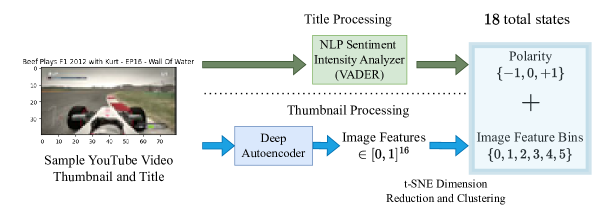

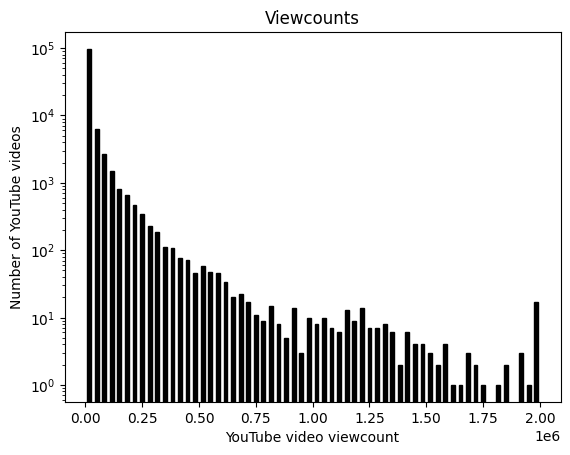

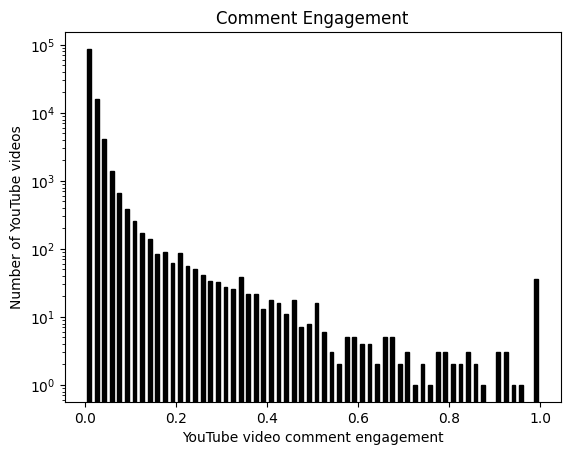

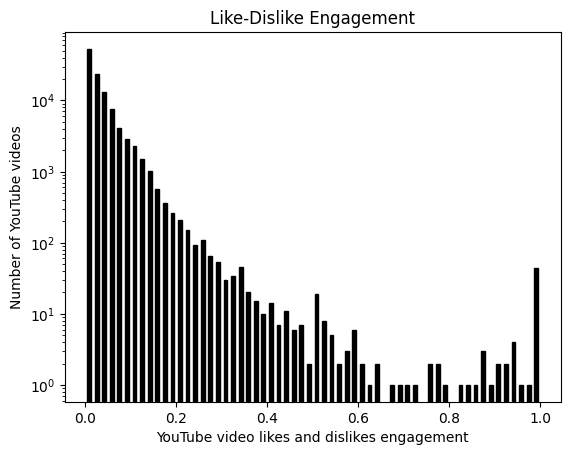

Categories in YouTube (e.g. News, Gaming, Music etc.) are numbered from (See Fig. 3 for the full listing). Recall from the rationally inattentive utility maximization setup of (16) and (24) that the decision maker observes the ground truth (state ) in noise (private measurement ), and then takes an action . In our numerical experiments on the YouTube dataset, we assume the user’s state depends on the YouTube video’s thumbnail (image) and title (text), since the thumbnail and title influence whether or not a user clicks on the video thumbnail and interacts with the video (through comments and likes/dislikes). The user’s private measurement are the perceived visual cues abstracted away in the dataset. Finally, we assume the user’s action depends on (i) video viewcount (did the user watch the video or not), (ii) total comments on the video (user inclination to comment on a video), (iii) number of likes and dislikes on the video (user inclination to like/dislike a video) and (iv) difference in the number of likes and dislikes (indicates user engagement polarity). We formalize this abstraction of YouTube metadata to rational inattention framework’s variables below.

The video categories have mean numbers of users ranging from to for high viewcount (greater than ) videos and to for low viewcount videos (less than ). Figure 3 lists each video category along with the total number of views. Note that the video categories “Unavailable” or “Removed” are videos flagged by YouTube as being suspected of violating YouTube’s video policies.