Alternative Microfoundations for Strategic Classification

Abstract

When reasoning about strategic behavior in a machine learning context it is tempting to combine standard microfoundations of rational agents with the statistical decision theory underlying classification. In this work, we argue that a direct combination of these standard ingredients leads to brittle solution concepts of limited descriptive and prescriptive value. First, we show that rational agents with perfect information produce discontinuities in the aggregate response to a decision rule that we often do not observe empirically. Second, when any positive fraction of agents is not perfectly strategic, desirable stable points—where the classifier is optimal for the data it entails—cease to exist. Third, optimal decision rules under standard microfoundations maximize a measure of negative externality known as social burden within a broad class of possible assumptions about agent behavior.

Recognizing these limitations we explore alternatives to standard microfoundations for binary classification. We start by describing a set of desiderata that help navigate the space of possible assumptions about how agents respond to a decision rule. In particular, we analyze a natural constraint on feature manipulations, and discuss properties that are sufficient to guarantee the robust existence of stable points. Building on these insights, we then propose the noisy response model. Inspired by smoothed analysis and empirical observations, noisy response incorporates imperfection in the agent responses, which we show mitigates the limitations of standard microfoundations. Our model retains analytical tractability, leads to more robust insights about stable points, and imposes a lower social burden at optimality.111A shorter version of this manuscript was accepted for publication at ICML 2021.

1 Introduction

Consequential decisions compel individuals to react in response to the specifics of the decision rule. This individual-level response in aggregate can disrupt both statistical patterns and social facts that motivated the decision rule, leading to unforeseen consequences. A similar conundrum in the context of macroeconomic policy making fueled the microfoundations program following the influential critique of macroeconomics by Lucas in the 1970s [Lucas Jr, 1976]. Microfoundations refers to a vast theoretical project that aims to ground theories of aggregate outcomes and population forecasts in microeconomic assumptions about individual behavior. Oversimplifying a broad endeavor, the hope was that if economic policy were microfounded, it would anticipate more accurately the response that the policy induces.

Predominant in neoclassical economic theory is the assumption of an agent that exhaustively maximizes a utility function on the basis of perfectly accurate information. This modeling assumption about agent behavior underwrites many celebrated results on markets, mechanisms, and games. Although called into question by behavioral economics and related fields (e.g. see [Camerer et al., 2004]), the assumption remains central to economic theory and has become standard in computer science, as well.

When reasoning about incentives and strategic behavior in the context of classification tasks, it is tempting to combine the predominant modeling assumptions from microeconomic theory with the statistical decision theory underlying classification. In the resulting model, agents have perfect information about the decision rule and compute best-response feature changes according to their utility function with the goal of achieving a more favorable classification outcome. We refer to this agent model as standard microfoundations. Building on the assumption that agents follow standard microfoundations, the decision-maker then chooses the decision rule that maximizes their own objective in anticipation of the resulting agent response. This is the conceptual route taken in the area of strategic classification, but similar observations may apply more broadly to the intersection of economics and learning.

1.1 Our work

We argue that standard microfoundations are a poor basis for studying strategic behavior in binary classification problems. We make this point through three observations that illustrate the limited descriptive power of the standard model and the problematic solution concepts it implies. In response, we explore the space of alternative agent models for strategic classification, and we identify desirable properties that when satisfied by microfoundations lead to more realistic and robust insights. Guided by these desiderata, we propose noisy response as a promising alternative to the standard model.

A) Limitations of standard microfoundations

In strategic classification, agents respond strategically to the deployment of a binary decision rule specified by classifier weights . The decision-maker assumes that agents follow standard microfoundations: that is, agents have full information about and change their features so as to maximize their utility function. The utility function captures the benefit of a positive classification outcome, as well as the cost of feature change. Consequently, an agent only invests in changing their features if the cost of feature change does not exceed the benefit of positive classification.

Our first observation concerns the aggregate response—the distribution over feature, label pairs induced by a classifier . We show that in the standard model, the aggregate response necessarily exhibits discontinuities that we often do not observe in empirical settings. The problem persists even if we assume an approximate best response or allow for heterogeneous cost functions.

Our second observation reveals that, apart from lacking descriptive power, the standard model also leads to brittle conclusions about the solution concept of performative stability. Performative stability [Perdomo et al., 2020] refers to decision rules that are optimal on the particular distribution they entail. Stable points thus represent fixed points of retraining methods, which repeatedly update the classifier weights to be optimal on the data distribution induced by the previous classifier. We show that the existence of performatively stable classifiers breaks down whenever a positive fraction of randomly chosen agents in the population are non-strategic. This brittleness of the existence of fixed points suggests that the standard model does not constitute a reliable basis for investigating dynamics of retraining algorithms.

Our last observation concerns the solution concept of performative optimality. Performative optimality [Perdomo et al., 2020] refers to a decision rule that exhibits the highest accuracy on the distribution it induces. The global nature of this solution concept means that finding performatively optimal points requires the decision-maker to anticipate strategic feedback effects. We prove that relying on standard microfoundations to model strategic behavior leads to extreme decision rules that maximize a measure of negative externality called social burden within a broad class of alternative models. Social burden, proposed in recent work, quantifies the expected cost that positive instances of a classification problem have to incur in order to be accepted. Thus, standard microfoundations produce optimal solutions that are unfavorable for the population being classified.

B) Alternative microfoundations

Recognizing the limitations of standard microfoundations, we systematically explore alternatives to the standard model. We investigate alternative assumptions on agent responses, encompassing general agent behavior that need not be fully informed, strategic, or utility maximizing. We formalize microfoundations as a randomized mapping that assigns each agent to a response type . The response type is associated with a response function specifying how agents of type change their features in response to each decision rule .

Letting be the base distribution over features and labels prior to any strategic adaptation, the aggregate response to a classifier is given by the distribution over induced feature, label pairs for a random draw and . In this sense, the mapping microfounds the distributions induced by decision rules, endowing the distributions with structure that allows the decision-maker to deduce the aggregate response from a model of individual behavior.

To guide our search for more appropriate microfoundations for binary classification, we introduce a collection of properties that are desirable for a model of agent responses to satisfy. The first condition, that we call aggregate smoothness, rules out the discontinuities arising from standard microfoundations. Conceptually, it requires that varying the classifier weights slightly must change the aggregate response smoothly. We find that this property alone is sufficient to guarantee the robust existence of stable points under mixtures with non-strategic agents.

The second condition, that we call the expenditure constraint, helps ensure that the model encodes realistic agent-level responses . At a high level, it requires that each agent does not spend more on changing their features than the utility of a positive outcome. This natural constraint gives rise to a large set of potential models. For any such model that satisfies an additional weak assumption, the social burden of the optimal classifier is no larger than the social burden of the optimal classifier deduced from the standard model. Moreover, the optimal points are determined by local behavior. This frees the decision-maker from fully understanding the aggregate response and makes the task of finding an approximately optimal classifier more tractable.

C) Noisy response—an alternative model

Using the properties described above as a compass to navigate the large space of alternative models, we identify noisy response as a compelling model of microfoundations. In this model, each agent best responds with respect to , where is an independent sample from a zero mean noise distribution. This model is inspired by smoothed analysis [Spielman and Teng, 2009] and encodes imperfection in the population’s response to a decision rule by perturbing the manipulation targets of individual agents.

We show that noisy response satisfies a number of desirable properties that make it a promising model of microfoundations for classification in strategic settings, both for theoretical analyses and from a practical standpoint. First, noisy response satisfies aggregate smoothness, and thus leads to the robust existence of stable points. Moreover, the model satisfies the expenditure constraint, and thus encodes natural agent-level responses which can be used to reason about metrics such as social burden. When used to anticipate strategic feedback effects and compute optimal points, noisy response leads to strictly less pessimistic acceptance thresholds than those computed under standard microfoundations, given the same constraints on manipulation expenditure. In fact, we show via simulations that a larger variance of the noise in the manipulation target leads to a more conservative optimal threshold, and for , we approximate the extreme case of standard microfoundations. Finally, from a practical perspective, we demonstrate that the distribution map for noisy response can be estimated by gathering information about individuals to learn the parameter and the cost function . This has the desirable consequence that the decision-maker can compute performatively optimal points without ever deploying a classifier.

1.2 Related work

Existing work on strategic classification in machine learning has mostly followed standard microfoundations for modeling agent behavior in response to a decision rule, e.g., [Dalvi et al., 2004; Brückner and Scheffer, 2011; Hardt et al., 2016a; Khajehnejad et al., 2019; Tsirtsis and Gomez Rodriguez, 2020] to name a few. This includes works that focus on minimizing Stackelberg regret [Dong et al., 2018; Chen et al., 2020], quantify the price of transparency [Akyol et al., 2016], and investigate the benefits of randomization in the decision rule [Braverman and Garg, 2020]. Investigations on externalities such as social cost [Milli et al., 2019; Hu et al., 2019] and whether classifiers incentivize improvement as opposed to gaming [Kleinberg and Raghavan, 2019; Miller et al., 2020; Shavit et al., 2020; Haghtalab et al., 2020] have also mostly built on the standard assumption of best-responding agents with perfect information. Recent work by Levanon and Rosenfeld [2021] studied practical implications of the optimization problem resulting from standard microfoundations and how to make it more amenable to practical optimization methods.

A handful of works have suggested potential limitations of the standard strategic classification framework. Brückner et al. [2012] recognized that the standard model leads to very conservative Stackelberg solutions, and proposed resorting to Nash equilibria as an alternative solution concept. We instead take a different route and advocate for altogether rethinking standard microfoundations that lead to these conservative acceptance thresholds. Concurrent and independent work by Ghalme et al. [2021] and Bechavod et al. [2021] relaxed the perfect information assumption in the standard model and studied strategic classification when the classifier is not fully revealed to the agents. In this work, we argue that agents often do not perfectly respond to the classifier even when the decision rule is fully transparent. Therefore, we propose incorporating imperfection into the model of microfoundations in order to anticipate natural deviations from the standard assumptions.

Related work in economics also investigates strategic responses to decision rules. This line of work, initiated by Spence [1973], has shown that information about individuals can become muddled as a result of heterogeneous gaming behavior [Frankel and Kartik, 2019], investigated the role of commitment power of the decision-maker [Frankel and Kartik, 2020], considered the impact of an intermediary who aggregates the agents’ multi-dimensional features [Ball, 2020], and considered the performance of different training approaches in strategic environments [Hennessy and Goodhart, 2020]. A notable work by Björkegren et al. [2020] investigates strategic behavior through a field experiment in the micro-lending domain, with a focus on evaluating approaches for designing strategy-robust classifiers. An important distinction is that these works tend to study regression, while we focus on classification. These settings appear to be qualitatively different in the context of strategic feedback effects (e.g. see note in [Hennessy and Goodhart, 2020]).

Our work is conceptually related to recent work in economics that has recognized mismatches between the predictions of standard models and empirical realities, for example in macroeconomic policy [Stiglitz, 2018; Kaplan and Violante, 2018; Coibion et al., 2018] and in mechanism design [Li, 2017]. These works, and many others, have explored incorporating richer behavioral and informational assumptions into typical models used in economic settings. Although our work also explores alternatives to standard microfoundations, we focus on algorithmic decision-making, where the limitations of the standard model had not been previously identified. We believe that our approach of navigating the entire space of potential models using a collection of properties could be of broader interest when developing alternative microfoundations.

1.3 Setup and basic notation

Let denote the feature space, and let be the space of binary outcomes. Each agent is associated to a feature vector and a binary outcome which represents their true label. A feature, label pair need not uniquely describe an agent, and many agents may be associated to the same pair . The base distribution is a joint distribution over describing the population prior to any strategic adaption. Throughout the paper we assume that is continuous and has zero mass on the boundary of . We focus on binary classification where each classifier is parameterized by , and the decision-maker selects classifier weights from which is a compact, convex set. We assume that for every , the set is closed, and the decision boundary is measure . We adopt the notion of a distribution map from [Perdomo et al., 2020] to describe the distribution over induced by strategic adaptation of agents drawn from the base distribution in response to the classifier .

2 Limitations of standard microfoundations

In the strategic classification literature, the typical agent model is a rational agent with perfect information. At the core of this model lies the assumption that agents have perfect knowledge of the classifier and maximize their utility given the classifier weights. The utility consists of two terms: a reward for obtaining a positive classification and a cost of manipulating features. The reward is denoted and the manipulation cost is represented by a function where reflects how much agents need to expend to change their features from to . A valid cost function satisfies a natural monotonicity requirement as stated in Assumption 1. Given a feature vector and a classifier , agents solve the following utility maximization problem:

| (1) |

Assumption 1.

A cost function is valid, if it is continuous in both arguments, it holds that for , and increases with distance in the sense that and for every that lies on the line segment connecting the two points .222We model a non-zero cost for all modifications to features, regardless of whether they result in positive classification or not. Generalizing beyond standard microfoundations, this accounts for how agents may erroneously expend effort on changing their features in an incorrect direction, as empirically demonstrated by Björkegren et al. [2020].

We will refer to this response model as standard microfoundations.

2.1 Discontinuities in the aggregate response

A striking property of distributions induced by standard microfoundations in response to a binary classifier is that they are necessarily either trivial or discontinuous. The underlying cause is that agents behaving according to standard microfoundations either change their features exactly up to the decision boundary, or they do not change their features at all.

Proposition 1.

Given a base distribution , let be the distribution induced by a classifier . Then, if is continuous and , there does not exist a valid cost function such that is an aggregate of agents following standard microfoundations.

In addition to the discontinuities implied by Proposition 1, the aggregate response induced by standard microfoundations faces additional degeneracies. Namely, a similar argument shows that any non-trivial distribution arising from the standard model must have a region of zero density below the decision boundary.

These properties are unnatural in a number of practical applications, as we discuss in the following examples.

Example 1 (Lending decisions and credit scores).

Consider banking lending decisions and the corresponding distribution over FICO credit scores. If lending decisions are based on FICO scores, then under standard microfoundations, the distribution over credit scores should exhibit a discontinuity at the threshold. However, this is not what we observe empirically. In particular, previous work [Hardt et al., 2016b] studied a FICO dataset from 2003, where credit scores range from 300 to 850, and a cutoff of 620 was commonly used for prime-rate loans. The observed distribution over credit scores appears continuous and is supported across the full range of scores.333In practice, lending decisions might be based on additional features beyond credit scores, and different lenders might use different cutoffs. In any case, this example demonstrates that the observed aggregate response cannot be captured by agents behaving according to standard microfoundations in response to a decision rule that is a threshold function of the credit score.

Example 2 (Yelp online ratings and rounding thresholds).

Restaurant ratings on Yelp are rounded to the nearest half star, and the star rating of a restaurant can significantly influence restaurant customer flows. In this setting, strategic adaptation arises from restaurants leaving fake reviews. Under standard microfoundations, the distribution of restaurant ratings would exhibit discontinuities at the rounding thresholds. However, previous work [Anderson and Magruder, 2012] examined the distribution of restaurant ratings, and showed that there is no significant discontinuity in the density of the restaurants at the rounding thresholds (see Figure 4 in their work).

Example 3 (High school exit exams and score cutoffs).

New York high school exit exams have important stakes for students, teachers, and schools, based on whether students meet designated score cutoffs. Interestingly, test score distributions did exhibit discontinuities prior to reforms on teacher grading procedures in 2012 [Dee et al., 2019]. These discontinuities resulted from teachers deliberately adjusting student scores to be just above the cutoff during grading. This example demonstrates that sharp discontinuities can arise when there is perfect information about the decision rule and perfect control over manipulations. However, following grading reforms that largely eliminated the possibility for strategic manipulation by teachers, these discontinuities disappeared and test score distributions appeared continuous [Dee et al., 2019]. Similar to observations in Examples 1-2, strategic adaptation by students cannot be described by standard microfoundations.

It is important to note that the degeneracies in the aggregate response induced by standard microfoundations arise from the fact that classification decisions are discrete and based on a hard decision. Agents who are not classified positively receive no reward: it does not matter how close to the decision boundary the agent is. This discontinuity in the utility is specific to classification and does not arise in regression problems that are predominantly studied in the economics literature. However, in machine learning and statistical decision theory, binary classification is ubiquitous, and degeneracies that we have identified pertain to general settings where the decisions are binary.

The reader might imagine that common variations and generalizations of standard microfoundations can mitigate these issues. Unfortunately, the two variations of standard microfoundations that are typically considered—heterogeneous cost functions [Hu et al., 2019], and approximate best response [Miller et al., 2020]—result in similar degeneracies. Heterogeneity in the cost (or utility) function can only change whether or not an agent decides to change their features, but it does not change their target of manipulation. If agents approximately best-respond, and thus move to features that approximately maximize their utility, the model no longer leads to point masses at the decision boundary, but agents will never undershoot the decision boundary. This means that any nontrivial aggregate distribution must have a region of zero density below the decision boundary to comply with standard microfoundations and any of these variants.

In fact, agent behavior that is not consistent with standard microfoundations or variants has been observed in field experiments. In particular, agents both overshoot and undershoot the decision boundary as well as generally exhibit noisy responses, even if the classifier is fully transparent.

Example 4 (Field Experiment [Björkegren et al., 2020]).

The authors developed an app that mimicked aspects of “digital credit” applications, and deployed it in Kenya in order to empirically investigate strategic behavior. Participants were rewarded if the app guessed that they were a high-income earner. When the participants were given access to the coefficients of the decision rule, they tended to change their features in the right direction, but a high variance in their responses was observed—see Table 5 in their work. The noise in the response was even more pronounced when participants were only given opaque access to the decision rule. In this case, agents often did not even change their features in the right direction.

2.2 Brittleness under natural model misspecifications

We describe two scenarios where the behavior of standard microfoundations is undesirable under natural model misspecifications. In particular, the existence of stable solutions crucially relies on all agents being perfectly strategic, and the optimal solutions associated with the standard model cause extreme negative externalities within a broad class of alternative approaches to model agent behavior.

A) Stability as a fragile solution concept

Performatively stable solutions are guaranteed to exist under standard microfoundations (see Milli et al. [2019]). Our first result demonstrates that this no longer holds if any positive fraction of randomly chosen individuals are non-strategic.

Recall that performative stability [Perdomo et al., 2020] requires that a classifier is optimal on the data distribution that it induces: that is, that is a global optimum of the following optimization problem:

| (2) |

Since we focus on the 0-1 loss in this work, the objective in (2) need not be convex, and it is natural to consider a local relaxation of performative stability. We say is locally stable if is a local minimum or a stationary point of (2). Note that any performatively stable solution is locally stable.

Performative stability defines the fixed points of repeated risk minimization—the retraining method where the decision-maker repeatedly updates the classifier to a global optimum on the data distribution induced by the previous classifier. Thus, there is no incentive for the decision-maker to deviate from a stable model based on the observed data. Similarly, when the objective in (2) is differentiable, locally stable points correspond to fixed points of repeated gradient descent [Perdomo et al., 2020]. Another interesting property of performatively stable points is that they closely relate to the concept of a pure strategy (local) Nash equilibrium in a simultaneous game between the strategic agents who respond to the classifier and the decision-maker who responds to the observed distribution .444More precisely, when agents follow standard microfoundations, any pure strategy local Nash equilibrium is locally stable.

To showcase that the existence of locally stable classifiers under standard microfoundations crucially relies on all agents following the modeling assumptions, we focus on the following simple 1-dimensional setting.

Setup 1 (1-dimensional).

Let and consider a threshold functions with . Let be the conditional probability over of the true label being given features . Suppose that is strictly increasing in and there is an such that .

Proposition 2.

Consider Setup 1. Suppose that a fraction of agents drawn from do not ever change their features, and a fraction of agents drawn independently from follow standard microfoundations with a valid cost function . Then, we have the following properties:

-

a)

For , locally stable points exist.

-

b)

For , locally stable points do not exist.

-

c)

Let denote the smallest locally stable point when all agents follow standard microfoundations, and let denote the optimal classifier for the base distribution .

For , repeated risk minimization will oscillate between and a threshold .The threshold is decreasing in , approaching as and as .

Proof Sketch.

For , it is easy to see that is the unique locally stable point, and for , the claim follows from an argument similar to Lemma 3.2 in [Milli et al., 2019]. For , the core observation is that for any the distribution contains no strategic agents in the interval for some . Furthermore, for any the misclassification rate on non-strategic agents could be improved by reducing the threshold to . Thus, it is not hard to see that or any , the threshold achieves smaller loss than , and thus cannot be stable. We formalize this argument and the case for in Appendix B.2. ∎

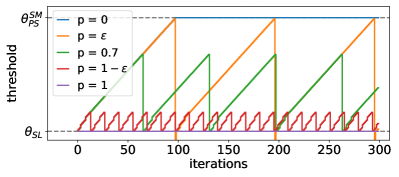

Proposition 2 implies that not only does the existence of locally stable points break down if a positive fraction of randomly chosen agents are non-strategic, but also repeated risk minimization oscillates between two extreme points. To illustrate this, we have implemented a simple instantiation of Setup 1, and we visualize the trajectories of repeated risk minimization for different values of in Figure 1(a). The main insight is that repeated risk minimization starts oscillating substantially even when is very close to (only an fraction of agents are not following standard microfoundations), even though this method converges when . This sensitivity of the trajectory to natural deviations from the modeling assumptions suggests that standard microfoundations do not constitute a reliable model to study algorithm dynamics.

Remark.

Unlike repeated risk minimization, repeated gradient descent is not well-defined for standard microfoundations. Because of the induced discontinuities, the optimization objective in (2) for Setup 1 with is not differentiable in the classifier weights. Thus, standard microfoundations do not serve as a useful basis to study repeated gradient descent.

B) Maximal negative externalities at optimality

Our next result describes a natural scenario where performatively optimal classifiers computed under standard microfoundations lead to the highest negative externalities within a broad class of alternative models for agent responses.

Recall that a performatively optimal solution corresponds to the best classifier for the decision-maker from a global perspective, but it is not necessarily stable under retraining. Formally, a classifier is performatively optimal [Perdomo et al., 2020] if it minimizes the performative risk:

| (3) |

Performative optimality is closely related to the concept of a Stackelberg equilibrium in a leader-follower game, where the decision-maker plays first and the agents respond.

The key challenge of computing performative optima is that optimizing (3) requires the decision-maker to anticipate the population’s response to any classifier . A natural approach to model this response is to build on microfoundations and deduce properties of the distribution map from individual agent behavior. Different models for agent behavior can lead to solutions with qualitatively different properties.

While the decision-maker is unlikely to have a fully specified model for agent behavior at hand, we outline a few natural criteria that agent responses could reasonably satisfy. To formalize these criteria, we again focus on the 1-dimensional setting.

Property 1 (Expenditure monotonicity).

For every feature vector , any agent with true features must have manipulated features in response to each classifier that satisfy:

-

a)

for every .

-

b)

.

Property 1 describes agents that a) do not expend more on gaming than their utility from a positive outcome, and b) do not have their outcome worsened if the threshold is lowered. However, agents complying with Property 1 do not necessarily behave according to standard microfoundations. For example, Property 1 is satisfied by non-strategic agents who do not ever change their features and by the imperfect agents that we describe in Section 4.

We now show that within the broad class of microfoundations that exhibit Property 1, the standard model leads to an extreme acceptance threshold. For the formal statement, see Appendix B.3.

Proposition 3 (Informal).

A problematic implication of Proposition 3 is that standard microfoundations also maximize the negative externality called social burden [Milli et al., 2019]:

Social burden quantifies the average cost that a positively labeled agent has to expend in order to be positively classified by . While previous work introduced and studied social burden within standard microfoundations, and showed that Nash equilibria lead to smaller social burden than Stackelberg equilibria, we instead use social burden as a metric to study implications of different modeling assumptions on agent behavior. In particular, the following corollary demonstrates that standard microfoundations lead to worst possible social burden across all microfoundations that satisfy Property 1.

Corollary 4.

Under the same assumptions as Proposition 3, for every distribution map , it holds that

where is the distribution map induced by standard microfoundations.

This result has implications for the natural situation where standard microfoundations do not exactly describe agent behavior. In particular, relative to the performative optimal point of the true agent responses, the solutions computed using standard microfoundations would not only experience suboptimal performative risk but also would cause unnecessarily high social burden. This makes it hard for the decision-maker to justify the use of standard microfoundations as a representative model for agent behavior. Implicit in our argument is the following moral stance: given a set of criteria for what defines a plausible model for microfoundations, the decision-maker should not select the one that maximizes negative externalities.

3 Alternative microfoundations

We now depart from the classical approach and systematically search for models that are more appropriate for binary classification. We define the space of all possible alternative microfoundations and collect a set of useful properties that we show are desirable for microfoundations to satisfy.

3.1 Defining the space of alternatives

The principle behind microfoundations for strategic classification is to equip the distribution map with structure by viewing the distribution induced by a decision rule as an aggregate of the responses of individual agents. We consider agent responses in full generality by introducing a family of response types that represents the space of all possible ways that agents can perceive and react to the classifier . The response type fully determines agent behavior through the agent response function . In particular, an agent with true features and response type changes their features to when the classifier is deployed.

Remark.

Using the language of agent response functions, non-strategic agents correspond to a response type such that for all , and standard microfoundations correspond to a response type where is given by (1) for all . Note that a population of agents could be heterogeneous and exhibit a mixture of different types, or even be described by a continuum of response types.

We formalize microfoundations through a mapping from agents to response types. We denote the set of possible mappings by the collection that consists of all555These mappings are subject to mild measurability constraints that we describe in detail in Appendix A.2. possible randomized functions . For example, standard microfoundations correspond to the mapping such that for all , and a population of non-strategic agents corresponds to the mapping such that for all . While these two homogeneous populations can be captured by deterministic mappings, randomization is necessary to capture heterogeneity in agent responses across agents with the same original features. For example, randomness allows us to capture a mixed population of agents where some agents behave according to standard microfoundations and other agents are non-strategic.

Conceptually, the mapping sets up the rules of agent behavior. One aspect that distinguishes our framework from typical approaches to microfoundations in the economics literature is that it directly specifies agent responses, rather than specifying an underlying behavioral mechanism. An advantage of this approach is that responses can be observed, whereas the behavioral mechanism is harder to infer.

Importantly, the mapping coupled with the base distribution provides all the necessary information to specify the population’s response to a classifier . In particular, for each , the aggregate response is the distribution over where and . We use the notation to denote the aggregate response map induced by . By defining the distribution map, the mapping thus provides sufficient information to reason about the performative risk; in addition, it also provides sufficiently fine-grained information about individuals to reason about metrics such as social burden.

Naturally, with such a flexible model, any distribution map can be microfounded, albeit with complex response types, as long as feature manipulations do not change the fraction of positively labeled agents in the population. We refer to Appendix C.1 for an explicit construction of .

Proposition 5.

Let be a non-atomic distribution. Let be any distribution map that preserves the marginal distribution over of . Then, there exists a mapping such that is equal to .

This result primarily serves as an existence result to show that our general framework for microfoundations can capture continuous distributions that are observed empirically (e.g. Examples 1-3). In the following subsections, we focus on narrowing down the space of candidate models and describe two properties that we believe microfoundations should satisfy.

3.2 Aggregate smoothness

The first property pertains to the induced distribution and its interactions with the function class. This aggregate-level property rules out unnatural discontinuities in the distribution map. We call this property aggregate smoothness, and formalize it in terms of the decoupled performative risk [Perdomo et al., 2020].

Property 2 (Aggregate smoothness).

Define the decoupled performative risk induced by to be . For a given base distribution , a mapping satisfies aggregate smoothness if the derivative of the decoupled performative risk with respect to exists and is continuous in and across all of .

Intuitively, the existence of the partial derivative of with respect to guarantees that each distribution is sufficiently continuous (and cannot have a point mass at the decision boundary), and assuming continuity of the derivative we guarantee that changes continuously in . This connection between aggregate smoothness and continuity of the distribution map can be made explicit in the case of 1-dimensional features:

Proposition 6.

Suppose that , and let be a function class of threshold functions. Then, if the distribution map has the following properties, the mapping satisfies aggregate smoothness w.r.t. :

-

1.

For each , the probability density of exists everywhere and is continuous in .

-

2.

For each , the probability density is continuous in .

We believe that these two continuity properties are natural and likely to capture practical settings, given the empirical evidence in Examples 1-4. A consequence of aggregate smoothness is that it is sufficient to guarantee the existence of locally stable points.

Theorem 7.

Given a base distribution and function class , for any mapping that satisfies aggregate smoothness, there exists a locally stable point.

In fact, this result implies that stable points exist under deviations from the model, as long as aggregate smoothness is preserved. Our next result shows that under weak assumptions on the base distribution this is the case for any mixture with non-strategic agents. For ease of notation, we formalize such a mixture through the operator , where for , we let be equal to with probability and equal to otherwise.

Proposition 8.

Suppose that the non-performative risk is continuously differentiable for all . Then, for any , aggregate smoothness of a mapping is preserved under the operator .

Proposition 8, together with Theorem 7, implies the robust existence of locally stable points under mixtures with non-strategic agents, for any microfoundations model that satisfies aggregate smoothness.

Conceptually, our investigations in this section have been inspired by the line of work on performative prediction [Perdomo et al., 2020; Mendler-Dünner et al., 2020] that demonstrated that regularity assumptions on the aggregate response alone can be sufficient to guarantee the existence of stable points for smooth, strongly convex loss functions. However, our results differ from these previous analyses of performative stability in that we instead focus on the 0-1 loss. In Appendix E, we provide an example to show why the Lipschitzness assumptions on the distribution map used in prior work are not sufficient to guarantee the existence of stable points in a binary classification setting.

3.3 Constraint on manipulation expenditure

While aggregate smoothness focused on the population-level properties of the induced distribution, a model for microfoundations must also be descriptive of realistic agent-level responses in order to yield useful qualitative insights about metrics such as social burden or accuracy on subgroups. A minimal assumption on agent responses is that an agent never expends more on manipulation than the utility of a positive outcome.

Property 3 (Expenditure constraint).

Given a function class and a cost function , a mapping is expenditure-constrained if for every and every .

This constraint is implicitly encoded in standard microfoundations and many of its variants. We have previously encountered the expenditure constraint in Section 2.2, where we showed that if is a valid cost function, then this property, together with a basic monotonicity requirement on agent’s feature manipulations, defines a set of microfoundations models among which the standard model achieves extreme social burden at optimality. In Section 4 we will describe on one particular model for microfoundations within this set which results in a strictly lower social burden than the standard model.

Reducing the complexity of estimating the distribution map.

Apart from defining a natural class of feasible microfoundations models, an additional advantage of Property 3 is that it naturally constrains each agent’s range of manipulations. This can significantly reduce the complexity of estimating the distribution map for a decision-maker who wants to compute a strategy robust classifier offline.

Assume the decision-maker follows a two-stage estimation procedure to estimate a performatively optimal point, similar to [Miller et al., 2021]. First, they compute an estimate of the true mapping and infer from the base distribution . Second, they assume the model reflects the true decision dynamics and approximate optimal points as follows:

| (4) |

Using a naive bound (see Lemma 24) it is not difficult to see that it suffices to compute an estimate of , such that to guarantee that . However, achieving this level of accuracy fundamentally requires a full specification of the response types for every agent in the population.

The expenditure constraint helps to make this task more tractable, in that the decision-maker only needs to estimate responses for a small fraction of the agents to achieve the same bound on the suboptimality of the obtained performative risk. To formalize this, let’s assume the decision-maker can define a set that contains the performatively optimal classifier . Then, given the implied restriction in the search space in (4), the expenditure constraint enables us to restrict the set of covariates that are relevant for the optimization problem to

| (5) |

The salient part captures all agents who are sufficiently close to the decision boundary for some so they are able to cross it without expending more than units of cost.

The subset can be entirely specified by the cost function and can be much smaller than . To see this, consider the following example setting.

Example 5 (Informal).

Example 5 demonstrates the salient part consists of agents who are sufficiently close to the supervised learning threshold, where closeness is measured by the cost function. We formalize this example in Appendix F.1.

We now describe the implications of constraining to the salient part for a 1-dimensional setting where and is a threshold function.666Proposition 9 directly extends to posterior threshold functions [Milli et al., 2019]. Let us define an agent response oracle that given and , outputs a draw from the response distribution where . We show with few calls to the oracle, the decision-maker can build an sufficiently precise estimate of .

Proposition 9.

Let , let be the function class of threshold functions. Suppose that satisfies the expenditure constraint, the distribution map is 1-Lipschitz with respect to TV distance777That is, for any , we have that ., and . We further assume that an agent’s type does not depend on their label, i.e., for all . Then, with calls to the agent response oracle, where , the decision-maker can create an estimate so that:

with probability for any .888We note that the decision-maker will only search over in (4) when computing . In particular, they compute rather than .

The number of necessary calls to the response function oracle for estimating decays with . Without any assumption on agent responses we have and . However, when the decision-maker is able to constrain to a small part of the input space by relying on the expenditure constraint, domain knowledge, or stronger assumptions on agent behavior, and thus the number of oracle calls can be reduced significantly.

The concept of a salient part bears resemblance to the approaches by Zhang and Conitzer [2021]; Zhang et al. [2021], which directly specify the set of feature changes that an agent may make, rather than implicitly specifying agent actions through a cost function. While these models assume that agents best-respond, our key finding is that constraining agent behavior alone can lessen the empirical burden on the decision-maker.

4 Microfoundations based on imperfect agents

Using the properties established in the previous section as a guide, we propose an alternate model for microfoundations that naturally allows agents to undershoot or overshoot the decision boundary, while complying with aggregate smoothness and expenditure monotonicity. Furthermore, we show that this model, called noisy response, leads to strictly smaller social burden than the standard model while retaining analytical tractablility.

4.1 Noisy response

Noisy response captures the idea of an imperfect agent who does not perfectly best-respond to the classifier weights. This imperfection can arise from many different sources—including interpretability issues, imperfect control over actions, or opaque access to the classifier. Inspired by smoothed analysis [Spielman and Teng, 2009], we do not directly specify the source of imperfection but instead capture imperfection in an agnostic manner, by adding small random perturbations to the classifier weights targeted by the agents. Since smoothed analysis has been successful in explaining convergence properties of algorithms in practical (instead of worst case) situations, we similarly hope to better capture empirically observed strategic phenomena.

We define the relevant set of types so that each type is associated with a noise vector . An agent of type perceives as and responds to the classifier as follows:

| (6) |

where denotes a valid cost function, denotes the utility of a positive outcome, and is a compact, convex set containing .999We assume that is defined on all of , and for all and all that are on the boundary of . For each , we model the distribution over noise across all agents with feature, label pair as a multivariate Gaussian. To formalize this, we define a randomized mapping as follows. For each , the random variable is defined so that if , then is distributed as . This model results in the perceived values of across all agents with a given feature, label pair following a Gaussian distribution centered at . The noise level reflects the degree of imperfection in the population.

Conceptually, our model of noisy response bears similarities to models of incomplete information [Harsanyi, 1968] that are standard in game theory (but that have not been traditionally considered in the strategic classification literature). However, a crucial difference is that we advocate for modeling agents actions as imperfect even if the classifier is fully transparent, because we believe that imperfection can also arise from other sources. This is supported by the empirical study of Björkegren et al. [2020] discussed in Example 4 where agents act imperfectly even when the classifier weights are revealed.

We want to emphasize that we instantiate imperfection by adding noise to the manipulation targets, instead of directly adding noise to the responses. While both approaches would mitigate the discontinuities in the aggregate distribution, the approach of adding noise directly to the responses results in a less natural model for agent behavior that violates the expenditure constraint.

4.2 Aggregate-level properties of noisy response

Intuitively, the noise in the manipulation target of noisy response smooths out the discontinuities of standard microfoundations, eliminating the point mass at the decision boundary and region of zero density below the decision boundary. We show this explicitly in a 1-dimensional setting.

Proposition 10.

Let be a function class of threshold functions, and suppose also that . For any , the distribution map satisfies the continuity properties in Proposition 6, and thus the mapping satisfies aggregate smoothness.

Remark.

This result implies that noisy response inherits the robust existence of stable points under mixtures with non-strategic agents from Theorem 7. Furthermore, we illustrate in Figure 1(b) how noisy response mitigates the large oscillations of repeated retraining that we observed for standard microfoundations. We observe that in the case of , noisy response results in a lower stable point than standard microfoundations.

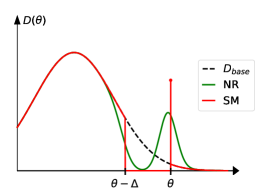

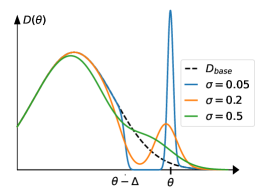

To visualize the aggregate-level properties of noisy response and contrast them with standard microfoundations we depict the respective density functions for a 1-dimensional setting with a Gaussian base distribution in Figure 2(a). The distribution can be bimodal, since agents closer to the threshold are more likely to change their features. The shape of the response distribution changes with as illustrated in Figure 2(b). As , the aggregate response of a population of noisy response agents approaches that of standard microfoundations. This means that noisy response maintains continuity while also being able to approximate the aggregate response of standard microfoundations to arbitrary accuracy. Finally, we note that the distribution map of noisy response changes continuously with , as visualized in Figure 2(c). In fact, the distribution map induced by noisy response is Lipschitz in total-variation distance, where the Lipschitz constant grows with .

Lemma 11.

Given , the distribution map is continuous in TV distance and supported on all of . Moreover, the distribution map is Lipschitz in TV distance. That is, for any , we have that .

This result highlights a favorable property of noisy response compared to standard microfoundations, in that the performative risk changes smoothly with changes in the classifier weights.

Remark (Implications beyond 0-1 loss).

Lemma 11 implies that noisy response induces a distribution map that is Lipschitz in Wasserstein distance for any cost function, where the Lipschitz constant depends on the diameter of the set . For smooth and strongly convex loss functions, this readily implies convergence of repeated retraining [Perdomo et al., 2020; Mendler-Dünner et al., 2020].

4.3 Trade-off between imperfection and social burden

Apart from satisfying desirable aggregate-level properties, noisy response also satisfies the expenditure monotonicity requirement in Property 1 (see Proposition 23 for a proof). By Corollary 4, this implies that in Setup 1 the social burden of the optimal classifier computed under noisy response is no larger than that of standard microfoundations. That is, . In certain cases, we can obtain a stronger result and show that the social burden of noisy response is strictly lower than that of standard microfoundations.

Corollary 12.

Consider Setup 1. Let be the mapping associated with standard microfoundations, let , and let the cost function be of the form . Suppose that , where is defined so that . Then, it holds that:

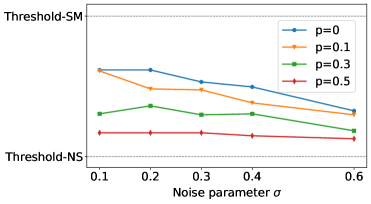

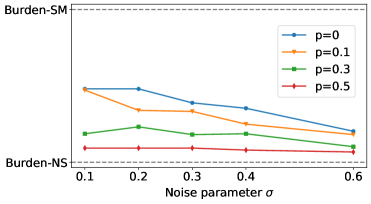

In fact, the social burden for fuzzy perception can be well below the social burden of standard microfoundations. To demonstrate this we visualize the threshold and social burden across a variety of different values of the noise parameter and the fraction of non-strategic agents in Figure 3. The dashed lines indicate the respective reference values for standard microfoundations (SM) and for a population of non-strategic agents (NS). We observe that the threshold as well as the social burden decrease with the fraction of non-strategic agents in the population. Furthermore, if every agent follows noisy response (), the threshold and the social burden are decreasing with (and hence the degree of imperfection in agents response). Overall, the acceptance threshold and the social burden of optimal classifiers derived under our new microfoundations is significantly lower than for standard microfoundations.

4.4 Approximating the distribution map for noisy response

Microfoundations are useful in practice to model and anticipate how the population responds to a deployed classifier. This tool is particularly powerful if the decision-maker can estimate agent behavior without needing to expose the population to potentially inaccurate and harmful classifiers to explore and learn about agents responses.

An appealing aspect of assuming a parameterized model of the agent responses is that the complex task of learning agent behavior is reduced to a parameter estimation problem. For noisy response, the aggregate response is parameterized by the variance of the target noise. In practice such parameters of individual responses can often be estimated via individual experiments, i.e., by gathering information about individuals without ever deploying a classifier. For example, the decision-maker can randomly sample agents in the population, ask survey questions to learn about their perceptions of the deployed classifier, and infer the variance from these samples. We refer to [Björkegren et al., 2020] for an actual field experiment that shows an example procedure for how to similarly obtain a reasonable estimate of the cost function . We now show that an error in parameter estimation can then be translated into an error in the aggregate response.

Lemma 13.

Given a population of agents following noisy response with parameter , and an estimate of , it holds that where is the dimension of the feature space.

Combining Lemma 13 with a bound on the performative risk, we obtain the following robustness guarantee of the performative risk to estimation errors in the noise parameter .

Corollary 14.

Let the population be the aggregate of agents following noisy response with parameter , and let be an estimate of the perception parameter . Then the suboptimality of the estimated performative risk of on the true population represented by is bounded by:

Hence, if the true distribution map is sufficiently close to some parameterization of noisy response, estimating the noise parameter provides a robust procedure to infer an estimate of performative optima in practice.

Overall, noisy response offers a more descriptive and prescriptive model of agent behavior compared to standard microfoundations, and still maintains analytical tractability. While we have focused on Gaussian noise in the perception function throughout this work, the outlined benefits of noisy response also apply to other parameterized noise distributions, as long as they are sufficiently smooth and continuous on all of . Hence, depending on the application, the decision-maker might prefer to pick a different noise model that can better capture the expected particularities of agents imperfections. The inference procedure via individual experimentation can then be adapted to obtain performative risk estimates that depend on the parameters of the noise distribution.

5 Discussion

To anticipate the strategic behavior of a population in response to a classifier, the decision-maker needs to understand and model the distribution shifts induced by decision rules. Traditional approaches for modeling these distribution shifts are either purely individual-level or purely population-level: strategic classification typically builds on standard microfoundations as a specification of individual-level behavior to deduce aggregate-level responses, whereas performative prediction directly works with a population-level characterization of distribution shifts.

In this work, we provided a fresh perspective on microfoundations for strategic classification that is inspired by performative prediction. While microfoundations can provide valuable structure to distribution shifts, we illustrated that the standard model for agent responses can lead to degenerate behavior in aggregate. These unanticipated degeneracies motivated us to consider population-level properties, rather than only individual-level properties, when searching through the space of alternative models for agent responses. This approach helped us identify noisy response as a promising candidate model for reasoning about strategic behavior in response to a binary decision rule.

While we have focused on strategic classification in this work, we believe that striving for a synergy between individual-level and aggregate-level considerations of agent behavior can more broadly lead to interesting insights about algorithmic decision-making in a social context.

Acknowledgments

We would like to thank Jacob Steinhardt and Tijana Zrnic for feedback on this manuscript. MJ acknowledges support from the Paul and Daisy Soros Fellowship. CMD acknowledges support from the Swiss National Science Foundation Postdoc.Mobility fellowship program. MH acknowledges support from NSF Award 1750555.

References

- Akyol et al. [2016] Emrah Akyol, Cedric Langbort, and Tamer Basar. Price of transparency in strategic machine learning. Arxiv:1610.08210, 2016.

- Anderson and Magruder [2012] Michael Anderson and Jeremy Magruder. Learning from the crowd: Regression discontinuity estimates of the effects of an online review database. The Economic Journal, 122(563):957–989, 2012.

- Ball [2020] Ian Ball. Scoring strategic agents. ArXiv:1909.01888, 2020.

- Bechavod et al. [2021] Yahav Bechavod, Chara Podimata, Zhiwei Steven Wu, and Juba Ziani. Information discrepancy in strategic learning. Arxiv:2103.01028, 2021.

- Björkegren et al. [2020] Daniel Björkegren, Joshua E. Blumenstock, and Samsun Knight. Manipulation-proof machine learning. Arxiv:2004.03865, 2020.

- Braverman and Garg [2020] Mark Braverman and Sumegha Garg. The role of randomness and noise in strategic classification. In Proc. st FORC 2020, volume 156 of Leibniz International Proceedings in Informatics (LIPIcs), pages 9:1–9:20, 2020.

- Brown et al. [2020] Gavin Brown, Shlomi Hod, and Iden Kalemaj. Performative prediction in a stateful world. Arxiv:2011.03885, 2020.

- Brückner and Scheffer [2011] Michael Brückner and Tobias Scheffer. Stackelberg games for adversarial prediction problems. In Proc. th ACM KDD, page 547–555, 2011.

- Brückner et al. [2012] Michael Brückner, Christian Kanzow, and Tobias Scheffer. Static prediction games for adversarial learning problems. JMLR, 13(1):2617–2654, September 2012.

- Camerer et al. [2004] Colin F. Camerer, George Loewenstein, and Matthew Rabin. Advances in Behavioral Economics. Princeton University Press, 2004.

- Chen et al. [2020] Yiling Chen, Yang Liu, and Chara Podimata. Learning strategy-aware linear classifiers. In Proc. rd NeurIPS, volume 33, pages 15265–15276, 2020.

- Coibion et al. [2018] Olivier Coibion, Yuriy Gorodnichenko, and Rupal Kamdar. The formation of expectations, inflation, and the phillips curve. Journal of Economic Literature, 56(4):1447–1491, 2018.

- Dalvi et al. [2004] Nilesh N. Dalvi, Pedro M. Domingos, Mausam, Sumit K. Sanghai, and Deepak Verma. Adversarial classification. In Proc. th KDD, page 99–108, 2004.

- Dee et al. [2019] Thomas S. Dee, Will Dobbie, Brian A. Jacob, and Jonah Rockoff. The Causes and Consequences of Test Score Manipulation: Evidence from the New York Regents Examinations. American Economic Journal: Applied Economics, 11(3):382–423, July 2019.

- Devroye et al. [2018] Luc Devroye, Abbas Mehrabian, and Tommy Reddad. The total variation distance between high-dimensional Gaussians. October 2018.

- Dong et al. [2018] Jinshuo Dong, Aaron Roth, Zachary Schutzman, Bo Waggoner, and Zhiwei Steven Wu. Strategic classification from revealed preferences. In Proc. EC, page 55–70, 2018.

- Frankel and Kartik [2019] Alex Frankel and Navin Kartik. Muddled Information. Journal of Political Economy, 127(4):1739–1776, 2019.

- Frankel and Kartik [2020] Alex Frankel and Navin Kartik. Improving Information via Manipulable Data. Working Paper, 2020.

- Gatzouras [2002] Dimitris Gatzouras. On images of borel measures under borel mappings. Proceedings of the American Mathematical Society, 130(9):2687–2699, 2002.

- Ghalme et al. [2021] Ganesh Ghalme, Vineet Nair, Itay Eilat, Inbal Talgam-Cohen, and Nir Rosenfeld. Strategic classification in the dark. Arxiv:2102.11592, 2021.

- Haghtalab et al. [2020] Nika Haghtalab, Nicole Immorlica, Brendan Lucier, and Jack Z. Wang. Maximizing welfare with incentive-aware evaluation mechanisms. In Proc. th IJCAI, pages 160–166, 2020.

- Hardt et al. [2016a] Moritz Hardt, Nimrod Megiddo, Christos H. Papadimitriou, and Mary Wootters. Strategic classification. In Proc. th ITCS, page 111–122. ACM, 2016a.

- Hardt et al. [2016b] Moritz Hardt, Eric Price, and Nati Srebro. Equality of opportunity in supervised learning. In Proc. th NeurIPS, pages 3315–3323, 2016b.

- Harsanyi [1968] John C. Harsanyi. Games with incomplete information played by "bayesian" players, i-iii. part ii. bayesian equilibrium points. Management Science, 14(5):320–334, 1968.

- Hennessy and Goodhart [2020] Christopher Hennessy and Charles Goodhart. Goodhart’s law and machine learning. SSRN, 2020.

- Hu et al. [2019] Lily Hu, Nicole Immorlica, and Jennifer Wortman Vaughan. The disparate effects of strategic manipulation. In Proc. FAccT, page 259–268, 2019.

- Kaplan and Violante [2018] Greg Kaplan and Giovanni L. Violante. Microeconomic Heterogeneity and Macroeconomic Shocks. Journal of Economic Perspectives, 32(3):167–194, 2018.

- Khajehnejad et al. [2019] Moein Khajehnejad, Behzad Tabibian, Bernhard Schölkopf, Adish Singla, and Manuel Gomez-Rodriguez. Optimal decision making under strategic behavior. Arxiv:1905.09239, 2019.

- Kleinberg and Raghavan [2019] Jon Kleinberg and Manish Raghavan. How do classifiers induce agents to invest effort strategically? In Proc. EC, page 825–844, 2019.

- Levanon and Rosenfeld [2021] Sagi Levanon and Nir Rosenfeld. Strategic classification made practical. Arxiv:2103.01826, 2021.

- Li [2017] Shengwu Li. Obviously strategy-proof mechanisms. American Economic Review, 107(11):3257–3287, 2017.

- Lucas Jr [1976] Robert E Lucas Jr. Econometric policy evaluation: A critique. In Carnegie-Rochester conference series on public policy, volume 1, pages 19–46. North-Holland, 1976.

- Mendler-Dünner et al. [2020] Celestine Mendler-Dünner, Juan Perdomo, Tijana Zrnic, and Moritz Hardt. Stochastic optimization for performative prediction. Proc. rd NeurIPS, 33:4929–4939, 2020.

- Miller et al. [2020] John Miller, Smitha Milli, and Moritz Hardt. Strategic classification is causal modeling in disguise. In Proc. th ICML, volume 119, pages 6917–6926, 2020.

- Miller et al. [2021] John Miller, Juan C. Perdomo, and Tijana Zrnic. Outside the echo chamber: Optimizing the performative risk. Arxiv:2102.08570, 2021.

- Milli et al. [2019] Smitha Milli, John Miller, Anca D. Dragan, and Moritz Hardt. The social cost of strategic classification. In Proc. FAccT, page 230–239, 2019.

- Perdomo et al. [2020] Juan C. Perdomo, Tijana Zrnic, Celestine Mendler-Dünner, and Moritz Hardt. Performative prediction. In Proc. th ICML, volume 119, pages 7599–7609, 2020.

- Shavit et al. [2020] Yonadav Shavit, Benjamin L. Edelman, and Brian Axelrod. Causal strategic linear regression. In Proc. th ICML, volume 119, pages 8676–8686, 2020.

- Spence [1973] Michael Spence. Job market signaling. The Quarterly Journal of Economics, 87(3):355–374, 1973.

- Spielman and Teng [2009] Daniel A. Spielman and Shang-Hua Teng. Smoothed analysis: An attempt to explain the behavior of algorithms in practice. Commun. ACM, 52(10):76–84, October 2009.

- Stiglitz [2018] Joseph E Stiglitz. Where modern macroeconomics went wrong. Oxford Review of Economic Policy, 34(1-2):70–106, 01 2018.

- Tsirtsis and Gomez Rodriguez [2020] Stratis Tsirtsis and Manuel Gomez Rodriguez. Decisions, counterfactual explanations and strategic behavior. Proc. rd NeurIPS, 33:16749–16760, 2020.

- Zhang and Conitzer [2021] Hanrui Zhang and Vincent Conitzer. Incentive-aware PAC learning. Proc. th AAAI, 2021.

- Zhang et al. [2021] Hanrui Zhang, Yu Chen, and Vincent Conitzer. Automated mechanism design for classification with partial verification. Proc. th AAAI, 2021.

Appendix

For all of the proofs in the Appendix, we assume WLOG that the utility of a positive outcomes is equal to .

Appendix A Additional discussion of assumptions

A.1 Cost function

Let us discuss some context and implications of Assumption 1 defining a valid cost function. Unlike prior work [Milli et al., 2019, Miller et al., 2020, Braverman and Garg, 2020], we model a nonzero cost for all modifications to features, regardless of whether these modifications are in the right direction. In the spirit of generalizing beyond standard microfoundations, this accounts for how agents may erroneously expend effort on changing their features in an incorrect direction, as empirically demonstrated in Example 4. We further note that the definition of a valid cost function does not require symmetry in the arguments, which differentiates it from a metric.

A.2 Measurability requirements for alternative microfoundations

We now describe the measurability requirements that we need in order to define and work with maps . If we ignore measurability requirements for a moment, then notice that each map can be associated with a distribution given by . Defining measurability requirements on gives an implicit specification of requirements on . First, we define the probability space: Consider the sample space . We can define a sigma algebra over by viewing as the set of functions , and using that . The probability measure can then be given by .

Since contains a very small fraction of the sample space , we can work with a much smaller probability space in this context. This probability space is defined as follows: the sample space is (i.e. a subset of in the sigma-algebra), and the sigma-algebra is intersections of every set in with . The probability measure given by can be defined over this smaller probability space.

The distribution map can thus be viewed as random variables over this probability space. In particular, is the distribution of the random variable . In order for this random variable to be well-defined, we place the following measurability assumption.

Assumption 2 (Measurability requirement on ).

We require that for each the function given by is measurable.

A.3 Assumption on gaming behavior

In Section 3.3 we make the assumption that agent cannot have differing types solely on the basis of their true label. In other words, the map cannot take into account the true label.

Assumption 3.

For a map , we require that for all .

Assumption 3 means that agents with features who have true label versus true label have identical distributions over response types in aggregate. We need this assumption to reason about performatively optimal points, because a decision-maker has no access to the true labels beyond agents’ reported features when anticipating strategic behavior.

A.4 Compactness of

This assumption guarantees that the behavior of agents who follow standard microfoundations is well-defined.

Fact 1.

Suppose that is a valid cost function, and is compact. Then is attained on some and the behavior of rational agents with perfect information is well-defined.

Proof.

Let and . Suppose that . Then, by Assumption 1 the supremum is attained at . Now, suppose that . Then . By the fact that is a closed subset of a compact set (and thus compact), and is continuous, we know that is attained on some . ∎

Appendix B Proofs for Section 2

B.1 Proof of Proposition 1

In order to prove Proposition 1, we show that the gaming behavior of rational agents with perfect information can be characterized in the following way: Any rational agent with perfect information either will not change their features at all or will change their features exactly up to the decision boundary. We use the notation:

| (7) |

to denote how an agent with features who follows standard microfoundations will change their features in response to .

Lemma 15.

Suppose that is a valid cost function. Then for any the response (7) is either or is on the decision boundary of .

Proof of Proposition 15.

By Fact 1, we know that the quantity is well defined. It suffices to show that if , then is on the decision boundary of . If , then we know that . This means that and , where . Assume for sake of contradiction that is not on the decision boundary. Then since and , there must exist on the line segment between and such that is on boundary of , and thus the decision boundary of . Moreover, by Assumption 1, we know that . Since is closed, we see that . Thus, which is a contradiction. ∎

Proof of Proposition 1.

It suffices to show that is either equal to or is a discontinuous distribution. Let be the set of agents who change their features at , i.e.

If , then . Otherwise, suppose that . By Lemma 15, all of the agents in will game to somewhere on the decision boundary: that is, will be on the decision boundary for all . Thus, in , there will be at least a probability mass of agents at the decision boundary, which is measure . This means that is not a continuous distribution. ∎

B.2 Proof of Proposition 2

For convenience, we break down Proposition 2 into a series of propositions, roughly corresponding to part (a), part (b), and part (c), which we prove one-by-one.

First, let’s consider the case where . By the assumptions in Setup 1, we know that there exists a unique such that . We denote this value by (and it is in the interior of ). We claim that this is the unique locally stable point when .

Lemma 16.

Consider Setup 1 when fraction of agents are non-strategic. Then, (defined above) is the unique locally stable point.

Proof.

Since , the distribution map is given by . A locally stable point must be a local minimum or a stationary point of the following optimization problem:

Notice that the unique such is . ∎

We introduce some basic properties and notation for agents who behave according to standard microfoundations. By Lemma 15, we know if an agent games when the classifier is deployed, then they will game up to boundary, which in this case, is . We adopt similar notation to the proof of Proposition 1, and we denote the set of who game by101010Technically, the agents for whom are indifferent between not gaming and gaming to , but this is a measure set by the assumption that is continuous, and the assumption that is valid (Assumption 1):

For , we see that for , there will be a point mass at (from agents in ), the region will have zero probability density, and the rest of the distribution will remain identical to .

We first characterize the set of stable points at . This follows a very similar argument to Lemma 3.2 in [Milli et al., 2019], but since our assumptions as well as our requirements for stability are slightly weaker, the characterization result looks slightly different. (In particular, points above the Stackelberg equilibrium can be locally stable points.)

Lemma 17.

Consider Setup 1 when a fraction of agents are non-strategic. Then, there exists a locally stable point, and moreover, the set of locally stable points forms an interval , where is the unique value such that:

(Moreover, it holds that , and .)

Proof.

First, we show that cannot be a locally stable point. Assume for sake of contradiction that is a locally stable point. Notice that . Thus, is a local minimum or stationary point of . However, this is not possible because by the assumptions in Setup 1.

Now, we consider . In this case, as discussed above, has a point mass at . Roughly speaking, the only property that needs to be satisfied for in the interior of to be a local minimum of is that it needs to be suboptimal for the decision-maker to move just above the point mass (the decision-maker never benefits from moving to because there is a region of zero probability density underneath ). The loss induced from the point mass at by the classifier is . On the other hand, the loss induced from the point mass at by the classifier in the limit as is . A necessary and sufficient condition for to be locally stable is thus , which can be written as

| (8) |

It suffices to show that the set of points where (8) is satisfied is an interval of the form .

First, we show that the set of stable points forms an interval. It suffices to show that is continuous and strictly increasing in . By the assumption on (Assumption 1), we see that the endpoints of the interval are strictly increasing in . This, coupled with the fact that is strictly increasing in (assumed in Setup 1), implies that is continuous and strictly increasing as desired.

Furthermore, when , the condition in (8) is never satisfied, and thus all stable points satisfy , and hence .

We now prove that no locally stable points exist for .

Lemma 18.

Consider Setup 1 when a fraction of agents are non-strategic. Then, there are no locally stable points.

Proof.

When , we show that there are no locally stable points. Assume for sake of contradiction that is a locally stable point. Recall that for to be locally stable, must either be a stationary point or a local minimum of . We divide into three cases: (1) , (2) , (3) , and show that each results in a contradiction.

For the case (1), where , we see that . Thus, is a local minimum or stationary point of . However, this is not possible because by the assumptions in Setup 1. For the remaining two cases, we know that has a point mass at . This means that is not differentiable at , and so must be a local minimum.

For case (2), we see that consists a nonzero density of agents for whom , and for all agents , it holds that . The decision-maker thus wishes to move just to the other side of the point mass at . (This is possible because based on the fact that and the assumptions in Setup 1.) In particular,

which is a contradiction.

For case (3), notice that there exists such that and for all . The presence of non-strategic agents means that the decision-maker wishes to move to to achieve better performance on non-strategic agents. Since there are no strategic agents within , this can be done without affecting the classification of strategic agents. In particular,

which is a contradiction. ∎

Now, we analyze the oscillation behavior of repeated risk minimization when .

Lemma 19.

Consider Setup 1 when a fraction of agents are non-strategic. Repeated risk minimization will oscillate between and a threshold . The threshold is decreasing in , approaching as and approaching as .

Proof.

Using Lemma 16, we see that there is a unique performatively stable point for given by . We see that the smallest locally stable point for is given by as characterized in Lemma 17.

In the case of , the distribution map takes the form of a mixture with weight on and with weight on the distribution map of agents who behave according to standard microfoundations (which has a point mass at , zero density within , and the same as the original distribution elsewhere). The main step in our proof is an analysis of the global optima of

for each . For convenience, we let

We split into three cases: (a) , (b) , and (c) .

Case (a): .

We claim that .

First, we show that for . To see this, we note that the proof of Lemma 17 tells us that moving just above the point mass at will incur no better risk than at . Moreover, since for all , we see that for all , as desired.

Next, we show that for . This is because for , and so for all , as desired.

Next, we show that for , and . Because of the presence of non-strategic agents, a fraction of agents will be present in , and these agents do not change their features. Since for , we see that for all . Moreover, this argument actually shows that , as desired.

Case (b): .

We claim that .

First, we claim that for . This is because for , and so for all as desired.

Next, we claim that for . This is because for and so for all as desired.

Finally, we claim that for and . Since for , we see that for all . Moreover, this argument actually shows that , as desired.

Case (c): .

In this case, can sometimes out to technically be the empty set because of the discontinuities in the optimization problem. Let’s be slightly imprecise and introduce a classifier given by the threshold right above the point mass at (that is the classifier given by the limit ). (In practice, since repeated risk minimization necessarily has finite precision and discretizes the space , this corresponds to a classifier where is very small.) With the addition of this classifier, now is well-defined. We show that in some cases, and in some cases .