Portfolio Allocation under Asymmetric Dependence in Asset Returns using Local Gaussian Correlations

Abstract

It is well known that there are asymmetric dependence structures between financial returns. In this paper we use a new nonparametric measure of local dependence, the local Gaussian correlation, to improve portfolio allocation. We extend the classical mean-variance framework, and show that the portfolio optimization is straightforward using our new approach, only relying on a tuning parameter (the bandwidth). The new method is shown to outperform the equally weighted (”1/N”) portfolio and the classical Markowitz portfolio for monthly asset returns data.

1 Introduction

In modern portfolio theory the aim is to allocate assets by maximizing the expected return of the porfolio while minimizing its risk, for instance measured by the standard deviation. Markowitz (1952) provides the foundation for this mean-variance (MV) approach, where the crucial assumption is that the asset returns follow a joint-Gaussian distribution, and hence that the dependence between these returns is fully described by the linear correlation coefficient. The idea is simple; low correlated assets are suitable for diversification, while highly correlated assets should be avoided.

However, as shown by numerous empirical studies, it is well documented that there are asymmetries in the distribution of financial returns. This is especially true when the market is going down, which often leads to stronger dependence between assets, known as asymmetric dependence structures, see e.g. (Silvapulle and Granger, 2001; Campbell et al., 2002; Okimoto, 2008; Ang and Chen, 2002; Hong et al., 2007; Chollete et al., 2009; Garcia and Tsafack, 2011). Other forms of asymmetries are also present; asymmetric volatility clustering, see e.g. Glosten et al. (1993) or skewness within the distribution of stock returns, see e.g. Patton (2004) or Aït-Sahalia and Brandt (2001). The asymmetric dependence implies that the classical mean-variance optimized portfolios are not efficient with respect to their effective risk profile. Thus the benefit of diversification will erode if the correlations are asymmetric. Several studies have sought to overcome this shortcoming by modeling the dependence structure by using copula theory, and employing it in the optimization of a portfolio. Among the first papers introducing such an idea, Patton (2004), examines whether the asymmetries are predictable and if portfolio decisions are improved by forecasting such asymmetries. He finds that for investors with no short-sales constraints, the knowledge of these asymmetries leads to economic gains. Hatherley and Alcock (2007) find that managing asymmetric dependence, using a Clayton copula against the multivariate Gaussian model, reduces downside exposure. Low et al. (2013) make use of the bivariate Clayton and the Clayton canonical vine copulas to address the asset allocation for loss-averse investors through the minimization of CVaR in portfolios of up to 12 constituents. Kakouris and Rustem (2014) employ a mixture of copulas to derive CVaR and the worst case CVaR used to optimize a convex portfolio of stock indices. Bekiros et al. (2015) use pair-vine copula models and minimum risk optimal portfolios applied to mining stock portfolios. Finally, Han et al. (2017) use a copula-GARCH and DCC copulas approach, and extend Kakouris and Rustem (2014) to dynamic portfolio optimization models.

However, these procedures are in most cases quite complicated, and there is no guarantee that portfolio allocations based on complex models will perform better (see e.g. DeMiguel et al. (2009) and Low et al. (2016), where they find that outperforming the naive portfolio remains an elusive task). A non-technical asset manager might be overwhelmed by such choices.

We propose a much simpler approach. Without making assumptions about the nature of the underlying probability model, we present an adjustment to the correlation matrix of the assets, that takes the current state of the market into account by using the local Gaussian correlation (LGC), which is a recently developed dependence measure capable of detecting non-linear and asymmetric dependence patterns, see Tjøstheim and Hufthammer (2013). In other words, if the market is going down and correlations increase as is often loosely stated as a fact, this effect, being a consequence of the nonlinearity/asymmetry of the dependence between assets, will be captured by the LGC. It will thus provide an updated correlation matrix to be used in the portfolio allocation problem. Our proposed procedure relates to other studies that use a dynamic model for the correlation matrix to improve the asset allocation, see e.g. Engle and Colacito (2006), Kalotychou et al. (2014) and Aslanidis and Casas (2013). But, our procedure differs, as the main goal of this paper is to extend the classical MV framework by using the theory of local Gaussian correlation.

The organisation of the paper is as follows. In section 2, we briefly review the local Gaussian correlation, while section 3 present the classical mean-variance portfolio approach and the extension using the local Gaussian correlation. In section 4 we analyse a data set consisting of several asset returns, and investigate the performance of portfolios constructed by our new approach and other methods. Finally, section 5 offers some conclusions and outlook.

2 Local Gaussian correlation

This paper relies on the recent developed dependence measure, the local Gaussian correlation (LGC), introduced by Tjøstheim and Hufthammer (2013). This is a local characterization of dependence in space, and this idea has also been extended to several different situations, as test of independence, see Berentsen and Tjøstheim (2014), Lacal and Tjøstheim (2017) and Lacal and Tjøstheim (2019), density and conditional density estimation, see Otneim and Tjøstheim (2017) and Otneim and Tjøstheim (2018), a local Gaussian partial correlation, Otneim and Tjøstheim (2021), and local Gaussian spectral estimation, see Jordanger and Tjøstheim (2020). Finally, the relationship between the local Gaussian correlation and different copulas has been studied in Berentsen et al. (2014). For completeness, we briefly present the local Gaussian correlation in a standard fashion, and we note that this section closely follows the presentation of the LGC in Tjøstheim et al. (2021).

Let represent the return on two risky assets with density . Next, a description of how can be approximated locally in a neighbourhood of each point by a Gaussian bivariate density, , where are running variables, is given. Let be the mean vector in the normal distribution having density , is the vector of standard deviations, and is the correlation coefficient in the normal distribution . The approximating density is then given as

| (2.1) |

Moving to another point gives another approximating normal distribution depending on a new set of parameters . One exception to this is the case where itself is Gaussian with parameters , in which case .

The population parameter vector, , are obtained by minimizing the local penalty function measuring the difference between and . It is defined by

| (2.2) |

where is a product kernel with bandwidths . As is seen in Hjort and Jones (1996, pp 1623-1624), the expression in (2.2) can be interpreted as a locally weighted Kullback-Leibler distance from to . Hence, the minimizer (also depending on ) should satisfy

| (2.3) |

In the first step we define the population value as the minimizer of (2.2), assuming that there is a unique solution to (2.3). The definition of and the assumption of uniqueness are essentially identical to those used in Hjort and Jones (1996) for more general parametric families of densities.

In the next step we let and consider the limiting value . This is in fact considered indirectly by Hjort and Jones (1996) and more directly in Tjøstheim and Hufthammer (2013), both using Taylor expansion arguments. In the following we assume that a limiting value independent of and exists.

In estimating and a neighborhood with a finite bandwidth has to be used, this is in analogy with nonparametric density estimation. The estimate is then obtained from maximizing a local likelihood. Given observations the local log likelihood is determined by

| (2.4) |

When , the last term has 1 as its limiting value, and the likelihood reduces to the ordinary global likelihood. This last term is essential, as it implies that is not allowed to stray far away from as . Indeed, using the notation

| (2.5) |

by the law of large numbers, or by the ergodic theorem in the time series case, assuming , we have almost surely

| (2.6) |

Setting the expression in the first line of (2.6) equal to zero yields the local maximum likelihood estimate () of the population value (and which satisfies (2.3)).

An asymptotic theory has been developed in Tjøstheim and Hufthammer (2013) for for the case that is fixed and for in the case that . The first case is much easier to treat than the second one. In fact for the first case the theory of Hjort and Jones (1996) can be taken over almost directly, although it is extended to the ergodic time series case in Tjøstheim and Hufthammer (2013). In the case that , this leads to a slow convergence rate of , which is the same convergence rate as for the the estimated dependence function treated in Jones (1996).

We have thus far concentrated on the bivariate case, in which we estimate a single local Gaussian correlation based on a bivariate sample. In principle, it is straightforward to extend to the case of more than two variables. Assume that we observe a multivariate sample , with dimension . We can then estimate the local correlation matrix , , , as well as the local means and local variances and by maximizing the local likelihood function (2.4). The precision of such estimates, however, deteriorates quickly as the dimension grows, due to the curse of dimensionality.

However, a simplifying technique that reduces the complexity of this estimation problem is to estimate each local correlation as a bivariate problem by only considering the corresponding pair of observation vectors , . Thus, we reduce the -variate problems of estimating the local parameters depending on all coordinates, to a series of bivariate problems of estimating pairwise local correlations depending on their respective pairs of coordinates. In this way, we obtain a simplification that is analogous to an additive approximation in nonparametric regression. This technique is applied in the empirical analysis that follows. For more details regarding this pairwise modeling approach, see Otneim and Tjøstheim (2017). In particular, they show that the convergence speed is improved to .

As already mentioned, the local estimates depend on the smoothing device - the bandwidth vector and a specific choice of the kernel function, . In the empirical analysis, we use the Gaussian kernel, and the bandwidth selector used is the plug-in selector suggested in Støve et al. (2014) — the global standard deviation of the observations times a constant equal to 1.1.

Finally, we note that the local Gaussian correlation has been used in several studies examining the dependence structure between asset returns, and in testing for financial contagion, see e.g. Støve and Tjøstheim (2014), Støve et al. (2014), Bampinas and Panagiotidis (2017) and Nguyen et al. (2020).

3 Portfolio allocation using local Gaussian correlation

Mean-variance based portfolio construction is a common approach for asset management. Introduced by Markowitz (1952), the measures of return and risk are the mean and variance of the portfolios’ returns, respectively. Portfolios are considered mean-variance efficient if they minimize the variance for a given mean return or maximize the return for a given level of variance.

In this section we adopt the general formulation for portfolio optimization, which consists of minimization of a risk measure given a target reward and operational constraints. We assume there are risky assets. The returns on the risky assets are denoted by , which are assumed to have expected values , and covariance matrix of the portfolio of asset returns at time . Further, let be the unknown vector of optimal portfolio weights at time .

The MV optimization problem is defined as follows; the weights of the chosen portfolio are given by a vector , invested in risky assets; and the investor selects to maximize the expected quadratic utility function at each time , that is

| (3.1) |

where is the investor’s utility, and represents the investor’s degree of risk aversion. Hence, for a range of different risk aversion levels, the MV optimization will produce corresponding optimal portfolios with a trade-of between expected volatility and expected return. However, throughout this section, for simplicity, the risk aversion coefficient will be fixed and equal to 1.

There are three different ways of formulating the MV optimization problem: minimize the risk subject to a lower bound on the expected return (which results in the Minimum Variance portfolio); maximize the expected return subject to an upper bound on the risk; optimize the corresponding ratio between risk and return subject to a given level of risk aversion. We assume that . This constraint states that all capital must be invested in the portfolio (full investment constraint), where the weights correspond to portions of the capital allocated to a given component. Another type of constraint is related to long only positions, which specify that we can only buy shares and therefore only have position-related weights in contrast to the case of short positions, in which the selling positions would be reflected as negative weights. In the empirical example that follows, both cases will be examined. Further, we do not include a risk-free asset in our treatment of the portfolio allocation problem, but this will not impact our main findings.

The optimization problem with additional non-negativity constraints cannot be solved by the method of Lagrange multipliers because of the inequality constraints; it must be represented as a quadratic programming problem. Furthermore, the theory is unable to account for the presence of higher moments beyond the mean and variance in both the portfolio returns distributions or investor preferences, such as skewness and kurtosis. See e.g. Francis and Kim (2013) or Yao and Fan (2015) for a more detailed treatment of modern portfolio theory.

The typical portfolio allocation problem that arises in practice is described below. In the empirical analysis, we use monthly return data, but of course, shorter or longer time horizons are possible. As data of returns become available in time, we follow the same approach as DeMiguel et al. (2009), Tu and Zhou (2011) and Low et al. (2016) where rolling sampling windows of historical returns are used to estimate the expected return vector and covariance matrix required as inputs into the Markowitz model. More specifically, the process is given as follows;

-

1.

At time , a rolling sampling window of trading months is selected.

-

2.

During each month at time , starting from , the return data for the previous months are used to estimate the one month ahead expected return vector and the covariance matrix by the standard empirical versions. As new information arrives at month , these estimates are updated. This process is repeated by incorporating the return for each month going forward and ignoring the earliest one, until the end of the sample.

-

3.

Based upon these estimates, the various optimization problems are solved and the updated portfolio weights are updated at every first trading day of each month, and the rebalancing is done to construct a portfolio that achieves the desired investment objective.

-

4.

The estimates of are then used to calculate out-of-sample returns and portfolio performance over the next month. A total of out-of-sample returns are produced for each model, with being the total number of observations.

-

5.

These out-of-sample returns and portfolio weights are analyzed using a range of performance metrics and statistical measures that are reported for each model, respectively. For example, one can examine the cumulative returns resulting from a one dollar initial investment after a specified end date.

In this standard procedure, we note that as the covariance matrix is calculated globally, no explicit consideration is taken of any potential asymmetries in the return distribution. Our idea is now to utilize the local Gaussian correlation, and one should expect, to be able to improve the total portfolio return. In practice, all steps above are equal, except that in Step 2, the rolling sampling windows of historical returns are used to estimate a local covariance matrix in the gridpoint , by using the pairwise approach described in the last section. More specifically, step 2 is replaced by the following;

-

2.’

During each month , starting from , returns from the previous months are used to calculate the one month ahead local covariance matrix , consisting of the pairwise local covariances and local standard deviations in the gridpoint with being the bandwidth in the local Gaussian approximation. As new information arrives at month , we update these estimates. This process is repeated by incorporating the return for each month going forward and ignoring the earliest one, as previously mentioned. The one month ahead expected return vector is calculated as in step 2 above (i.e. using the global estimate).

Thus, our model is specified to account for asymmetries by specifying the gridpoint to use. But the key question is then; what gridpoint and hence which corresponding local covariance matrix should be used for solving the optimization problem for each time period? In practice, a regular grid is placed across the area of interest, and then an investor can pick any gridpoint based on her preferences. For instance, a risk-averse investor can guard against large losses by selecting a gridpoint representing the asset returns during crisis periods. In this way, the corresponding estimated local covariance matrix will reflect the (historical) dependence structure during crisis periods. However, the selection of the gridpoint can also be dynamic. For instance, the gridpoint may correspond to a subjective meaning of where the investor thinks the market of a particular asset is going to be in the following trading month.

In the empirical analysis in section 5, we opt for a simple data-driven selection of gridpoints, where the gridpoint is selected by computing the average of the three last months recorded return observations. Thus the gridpoint will change from one month to the next. More specifically, the ”moving-grid” point at time is defined for all pairs of assets as

| (3.2) |

This is a simple way of letting the covariance matrix dynamically adapt to the dependence structure of the market under the näive assumption that the dependence structure between asset returns in month corresponds to the dependence structure of asset returns in the neighbourhood of the three months moving average of observed previous returns.

4 Data

Our data set consists of monthly closing prices on six US dollar-denominated indices sourced from Thompson Reuters Datastream. The sample period extends from February 1980 to August 2018, yielding 463 monthly return observations. The included time series are FTSE Actuaries All Share Index, (FTALLSH), Standard and Poor’s 500 Index (S&P500), UK Benchmark 10 Year DS government bond Index (BMUK10Y), US Benchmark 10 Year DS government bond Index (BMUS10Y), Thomson Reuters Equal Weight Commodity Index (EWCI), and Standard and Poor’s GSCI Gold Index (GSGCSPT).

| Name | Description |

|---|---|

| FTALLSH | FTSE Actuaries All Share Index |

| S&P500 | Standard and Poor’s 500 Index |

| BMUK10Y | UK Benchmark 10 Year DS government bond Index |

| BMUS10Y | US Benchmark 10 Year DS government bond Index |

| EWCI | Thomson Reuters Equal Weight Commodity Index |

| GSGCSPT | Standard and Poor’s GSCI Gold Index |

From the descriptive statistics in Table 2, we note that all of the returns are skewed and show relatively high kurtosis. Normality is rejected with the Jarque-Bera test, which is significant on the level for all series. A departure from the Gaussian assumption suggests the multivariate normal distribution with a global covariance matrix may not be a sufficient description of the dependence structure, particularly in the distribution’s tails.

The two top panels in Table 2 show the global and local correlation matrices over the entire sampling period. The latter is constructed for a bear market scenario by using the lower percentiles for the grid point selection in the pairwise calculation approach described above. Globally, the strongest positive correlation can be found between the stock indices FTALLSH and S&P500, and the strongest negative between EWCI and BMUS10Y. Both stock indices show a positive, but close to zero correlation with gold. Locally in the bear market scenario, the positive stock market correlation is larger, , and the negative relation between commodities and US interest rate markets enhanced to . Here, both stock indices are negatively correlated with gold, with and for FTALLSH and S&P500, respectively. Intuitively, this seems reasonable, as gold historically has been considered a safe haven in times of turmoil. Such asymmetries in the returns data will be accounted for by calculating local covariance matrices with the moving-grid approach at each time step for the asset allocation below.

| FTALLSH | S&P500 | BMUK10Y | BMUS10Y | EWCI | GSGCSPT | |

| Global correlation matrix | ||||||

| FTALLSH | ||||||

| S&P500 | ||||||

| BMUK10Y | ||||||

| BMUS10Y | - | - | ||||

| EWCI | - | - | ||||

| GSGCSPT | ||||||

| Local correlation matrix, bear market (lower 5% percentiles) | ||||||

| FTALLSH | ||||||

| S&P500 | ||||||

| BMUK10Y | - | |||||

| BMUS10Y | ||||||

| EWCI | - | - | ||||

| GSGCSPT | - | - | ||||

| Descriptive statistics | ||||||

| Observations | ||||||

| Mean | ||||||

| Std.Dev. | ||||||

| Variance | ||||||

| Skewness | - | - | - | - | ||

| Kurtosis | ||||||

| Jarque-Bera | ||||||

| Sharpe ratio | ||||||

| Max. drawdown | ||||||

| Min | - | - | - | - | - | - |

| 1 Quartile | - | - | - | - | - | - |

| Median | - | |||||

| 3 Quartile | ||||||

| Max | ||||||

5 Empirical results

Our analysis 111Reproduce results or perform new studies with: https://gitlab.com/sleire/lgportf compares the portfolio performance for all MV strategies listed in Table 3 by evaluating outcomes when the optimization is performed with (a) the global covariance matrix and (b) the local covariance matrix calculated with the moving-grid approach. The naive weighted portfolio strategy is used as the benchmark model in the analysis, and we perform the study with sampling windows of and months.

The model distributes weights equally across the portfolio at the start of the sampling period, and is left unadjusted for the rest of the investment horizon. The MVS strategy is the classic approach where historical mean returns and the covariance matrix are used to determine the weights for each out-of-sample period, where no consideration is given within the optimization rule to adjust for estimation error in any form. MVSC is the constrained version, where only positive weights are allowed. The MIN strategy aims to minimize portfolio risk measured as variance of portfolio returns. Finally, MINC is the constrained version, where only positive weights are allowed. All strategies allowing short sales have a lower limit on portfolio weights equal to .

| Strategy | Description |

|---|---|

| EW | without rebalancing |

| MVS | Mean-variance with short sales |

| MVSC | Mean-variance with short sales constraint |

| MIN | Minimum variance |

| MINC | Minimum variance with short sales constraint |

When implemented with the local covariance matrix, the strategies are presented as MVS-L, MVSC-L, MIN-L, MINC-L. The local covariance matrices have been constructed by pairwise correlations with the moving-grid approach, where a simple moving average of length is used to predict gridpoints for the next month. In the event that the resulting covariance matrix is not positive definite, it is adjusted with the method described in Higham (2002).

Inspired by the procedure in Low et al. (2013), we continue with a descriptive analysis of out-of-sample results, followed by an evaluation of portfolio rebalancing, terminal wealth and risk-adjusted performance for each of the strategies.

5.1 Descriptive statistics portfolio strategies

Descriptive statistics of the portfolio strategies out-of-sample returns are shown in Table 4. We report mean, standard deviation, skewness, kurtosis, minimum value, maximum value, and the maximum portfolio drawdown, which is the maximum observed loss from a peak to a trough of the portfolio, before a new peak is attained, for window size (top) and (bottom).

The mean return tends to increase with the different local Gaussian approaches, and all portfolios achieve moderately higher average returns. In the case, MVS-L reaches the highest mean, followed by MVSC-L, MIN-L, MINC-L, MVS, MVSC, MIN, MVSC and EW. For the window size, the average return ranking is MIN-L, MINC-L, MVS-L, MVSC-L/MINC, MIN, MVS, MVSC and EW. These findings indicate that the local Gaussian approach may be able to capture asymmetries and outperform the corresponding benchmark models.

The lowest standard deviation for is achieved by MINC-L. This is however an exception, as all other strategies have slightly higher values when the local Gaussian method is applied. For , all local Gaussian portfolios have moderately higher standard deviations, with the exception of MINC-L. As noted in Low et al. (2013), this can be due to a larger upside variation, which is desirable for investors. We will follow their approach and include downside risk measures when evaluating performance below.

| Mean | Std.dev. | Skewness | Kurtosis | Min | Max | Max. drawdown | |

| Window size M = 120 | |||||||

| EW | - | - | |||||

| MVS | - | - | |||||

| MVSC | - | - | |||||

| MIN | - | - | |||||

| MINC | - | - | |||||

| MVS-L | - | - | |||||

| MVSC-L | - | - | |||||

| MIN-L | - | - | |||||

| MINC-L | - | - | |||||

| Window size M = 240 | |||||||

| EW | - | - | |||||

| MVS | - | - | |||||

| MVSC | - | - | |||||

| MIN | - | - | |||||

| MINC | - | - | |||||

| MVS-L | - | - | |||||

| MVSC-L | - | - | |||||

| MIN-L | - | ||||||

| MINC-L | - | ||||||

All strategy returns exhibit slight negative skewness, except for MIN-L and MINC-L for the window, with values of and respectively. Disregarding the EW strategies, the largest negative skew of can be found in MVSC, for . Hence, the strategies are all moderately skewed, or approximately symmetric.

The MIN-L for holds the largest kurtosis value in the analysis. When examining the minimum and maximum returns for this strategy, we observe larger values for both. The MIN-L also achieves the lowest drawdown for . The smallest maximum drawdown for is produced by MINC-L. Overall, the local gaussian strategies all have lower maximum drawdowns when compared to their benchmarks, in both windows.

5.2 Portfolio rebalancing and terminal wealth

The primary goal of a rebalancing strategy is to minimize risk relative to the target asset allocation produced by the trading strategy. According to Tokat and Wicas (2007), the asset manager needs to consider 1) frequency of rebalancing; 2) how large deviations to accept before triggering rebalancing; and 3) whether to restore a portfolio to its target or to some intermediate allocation. Inability to fully rebalance towards the target portfolio weights will lead to sub-optimal diversification. A decision-maker facing practical limitations such as regulatory requirements and periods with weak market liquidity will find strategies with stable target portfolio weights easier to implement relative to those who require more trading, DeMiguel et al. (2009). In our study, portfolios are fully rebalanced to target weights on a monthly basis. We evaluate differences in required trading activity and associated transaction costs.

Table 5 provides a summary of the portfolio rebalancing analysis and the terminal wealth reached by each of the strategies. It shows the average standard deviation within target portfolio weights, maximum positive and maximum negative adjustments of weights, average turnover, and terminal wealth of a hypothetical investment of $ 1 for each strategy. The average standard deviation within target portfolio weights across the entire out-of-sample time period is calculated as follows:

| (5.1) |

where

| (5.2) |

where is is the portfolio weight for asset in a portfolio of assets for strategy based upon a window sampling of months, and is the average portfolio weight across the assets in the portfolio. The maximum values for positive and negative weight adjustments are selected by identifying the largest positive and negative weight changes on the asset level. Following DeMiguel et al. (2009), we also report the average turnover, which is calculated as the average sum of the absolute value of the transactions over the assets with:

| (5.3) |

where is the number of assets in the portfolio, is the full length of the returns series, is the window size, is the target weight for asset at time for strategy , and is the corresponding asset weight before rebalancing. Terminal wealth is calculated assuming no transaction costs, and with a transaction cost of basis point.

| Max. adj. | Min. adj. | Avg.turnover | Wealth | Wealth incl.tcost | ||

| Window size M = 120 | ||||||

| EW | ||||||

| MVS | - | |||||

| MVSC | - | |||||

| MIN | - | |||||

| MINC | - | |||||

| MVS-L | - | |||||

| MVSC-L | - | |||||

| MIN-L | - | |||||

| MINC-L | - | |||||

| Window size M = 240 | ||||||

| EW | ||||||

| MVS | - | |||||

| MVSC | - | |||||

| MIN | - | |||||

| MINC | - | |||||

| MVS-L | - | |||||

| MVSC-L | - | |||||

| MIN-L | - | |||||

| MINC-L | - | |||||

The variability of portfolio weights reported in Table 5 shows the larges values for the MIN-L strategy, both for and . Results for the remaining strategies are mixed. The local Gaussian models does not seem to systematically achieve either higher or lower average standard deviation in target portfolio weights compared to their benchmarks. Looking at the maximum and minimum adjustments of portfolio weights however, there are clear differences. The local Gaussian strategies require adjustments of larger magnitude, in both directions. This is particularly the case for the unconstrained models allowing short sales. For example, during a period of large market moves, the MIN-L strategy exploit nearly it’s full mandate with a maximum negative weight adjustment of for one of the assets in the window. This is a significant adjustment, that does generate additional costs. Viewed across all strategies, we see larger and more frequent adjustments, resulting in an average turnover times higher than the classical MV portfolios when the lowest negative weight allowed is set to . For the long only portfolios, the differences are smaller, but still significant. Average turnover is increased by a factor of .

The increase in traded volume translates into lower terminal wealth when transaction costs are included in the analysis. While all local Gaussian strategies achieve larger terminal wealth when disregarding costs of trade, the MIN-L for shows weakest performance when 1 basis point is added as a transaction fee. The remaining local Gaussian strategies still reach a larger terminal wealth. Top-ranked strategies ex. costs are MVS-L () and MIN-L (). When costs are included, these are replaced by the long only portfolios MVSC-L and MINC-L. These two achieve a final wealth which of and larger than their classical MV benchmarks.

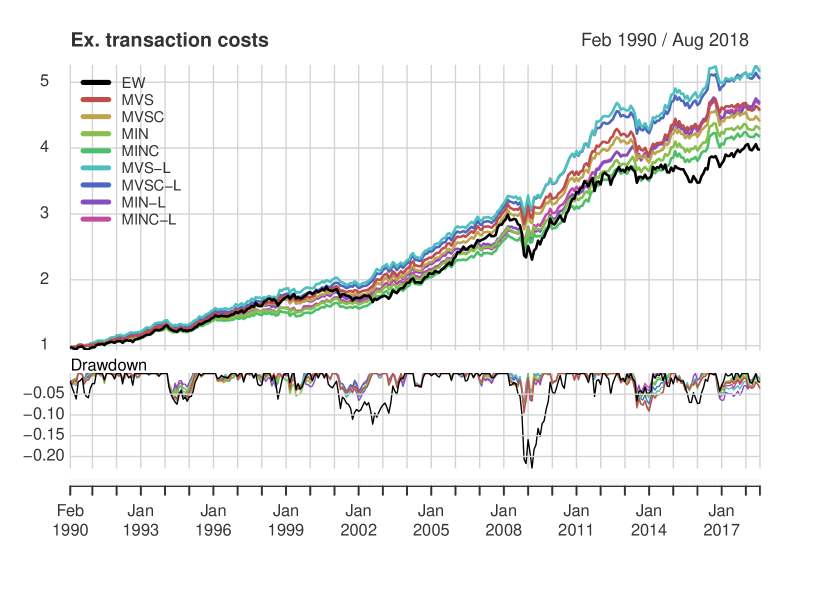

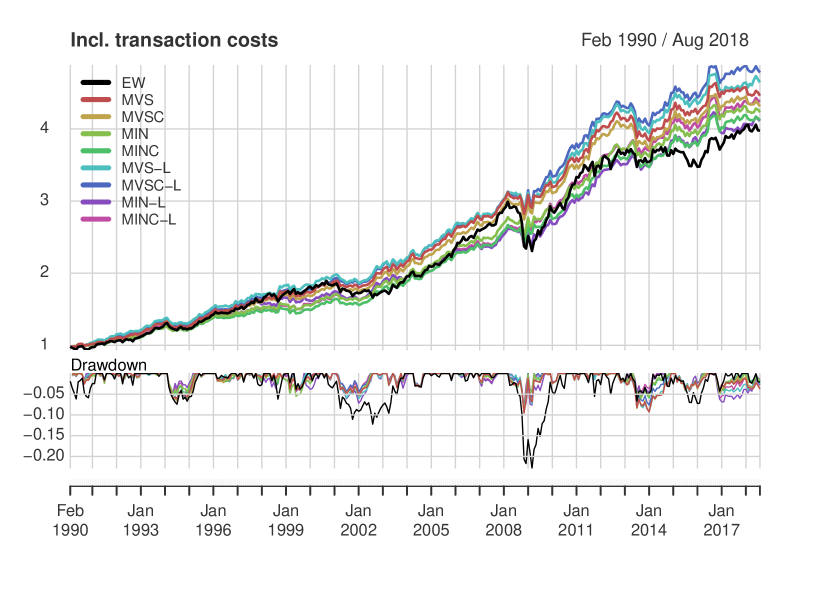

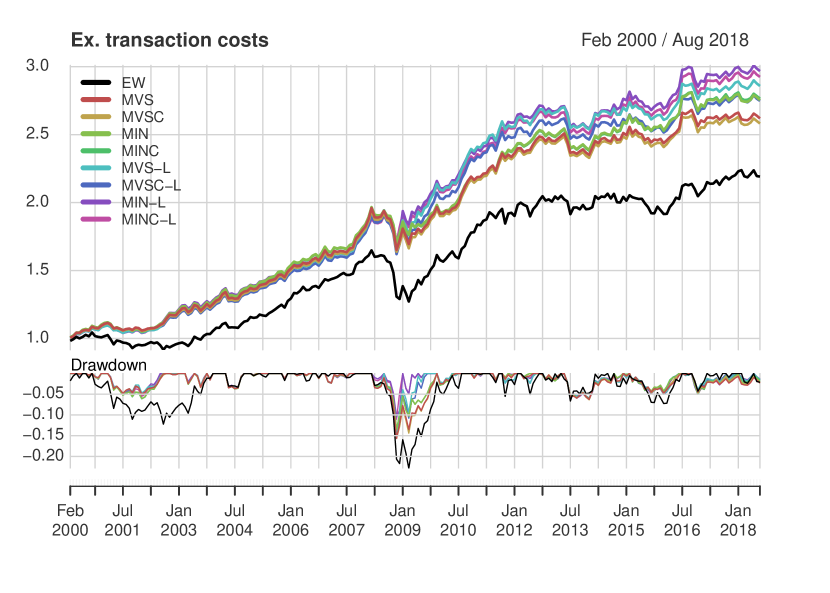

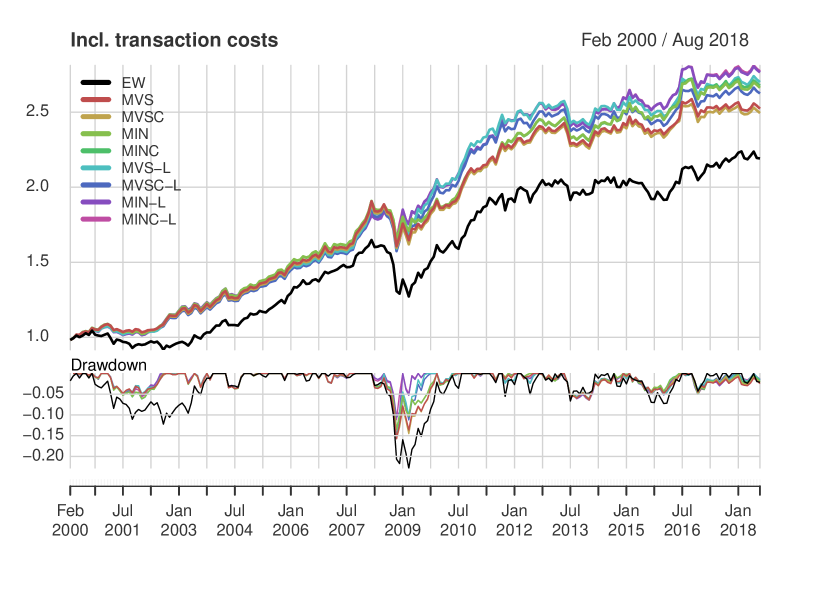

Figure 1 shows wealth accumulation and drawdowns for the hypothetical investment of $ 1 in each of the nine strategies included in the analysis when a sampling window of is used. As seen in the upper part of the figure, the local Gaussian MVS-L produces the largest final wealth when disregarding costs of trade. It remains top-ranked during most months in the sample, and suffers from smaller drawdowns in volatile periods such as the 2008 financial crisis. When transaction costs are considered, the strategy still performs well, but is pushed down from the top position by the constrained MVSC-L, which has lower turnover. A similar illustration for can be found in Figure 2.

5.3 Evaluation of risk-adjusted performance

Table 6 reports out-of-sample performance by evaluating portfolio strategy returns using a range of risk-adjusted metrics. The traditional Sharpe ratio was introduced as a measure for mutual fund performance in Sharpe (1966) under the term reward-to-variability ratio. The ratio is a risk-adjusted measure of return using standard deviation to represent risk. As standard deviation also will penalize upside deviations in returns, several modifications have been suggested. In VaR Sharpe and ES Sharpe, the Value at Risk and Expected Shortfall are used as risk measures. The Certainty Equivalent (CEQ) assuming quadratic utility with a risk aversion parameter equal to is also included. The Sortino ratio introduced in Sortino and Price (1994) penalize downside standard deviation only. Finally, the Omega ratio from Keating and Shadwick (2002) is calculated as a probability-weighted ratio of gains versus losses for a threshold return target (here set to zero), without making any assumptions regarding investors utility or risk aversion. All metrics produce high values for the best-performing strategies.

Results excluding transaction costs are reported in Panel A. The classic Sharpe ratio using standard deviation as risk measure is higher for all portfolios with the local Gaussian approach, and the largest value is attained by the MINC-L in both windows. This is also reflected in the annualized Sharpe ratio. For windows and , the other top rankings are: MINC-L and MIN-L (VaR Sharpe), MINC-L and MIN-L (ES Sharpe ratio), MVS-L and MIN-L (CEQ), MINC-L and MIN-L (Sortino ratio), MINC-L and MIN-L (Omega ratio). With the exception of MVS-L, all the top-ranked strategies are of type minimum-variance, optimized with the local covariance matrix. In a total of 14 top rankings, 8 are held by strategies with a long-only constraint. For , 6 out of 7 are long-only, while for , 2 out of 7 does not allow short sales.

Results including transaction costs are reported in Panel B. Here, the MINC-L still produces the largest Sharpe ratio in both windows. Improvements in Sharpe ratios are reduced for some of the unconstrained strategies in the window. The MVS-L and MIN-L do not manage to achieve larger scores than their benchmarks evaluated with Sharpe, VaR Sharpe, ES Sharpe, Sortino and Omega ratios. In the window, all local Gaussian models still perform slightly better than their benchmarks.

| Sharpe | VaR Sharpe | ES Sharpe | Ann. Sharpe | CEQ | Sortino | Omega | |

| Panel A: Ex. transaction costs | |||||||

| Window size M = 120 | |||||||

| EW | |||||||

| MVS | |||||||

| MVSC | |||||||

| MIN | |||||||

| MINC | |||||||

| MVS-L | 0.479 | ||||||

| MVSC-L | |||||||

| MIN-L | |||||||

| MINC-L | 0.328 | 0.250 | 0.168 | 1.141 | 0.587 | 2.340 | |

| Window size M = 240 | |||||||

| EW | |||||||

| MVS | |||||||

| MVSC | |||||||

| MIN | |||||||

| MINC | |||||||

| MVS-L | |||||||

| MVSC-L | |||||||

| MIN-L | 0.317 | 0.317 | 0.489 | 0.567 | 2.303 | ||

| MINC-L | 0.309 | 1.070 | |||||

| Panel B: Incl. transaction costs | |||||||

| Window size M = 120 | |||||||

| EW | |||||||

| MVS | |||||||

| MVSC | |||||||

| MIN | |||||||

| MINC | |||||||

| MVS-L | |||||||

| MVSC-L | 0.464 | ||||||

| MIN-L | |||||||

| MINC-L | 0.320 | 0.242 | 0.162 | 1.111 | 0.568 | 2.295 | |

| Window size M = 240 | |||||||

| EW | |||||||

| MVS | |||||||

| MVSC | |||||||

| MIN | |||||||

| MINC | |||||||

| MVS-L | |||||||

| MVSC-L | |||||||

| MIN-L | 0.291 | 0.291 | 0.534 | 2.214 | |||

| MINC-L | 0.299 | 1.035 | 0.468 | ||||

For windows and , the remaining top rankings are: MINC-L and MIN-L (VaR Sharpe), MINC-L and MIN-L (ES Sharpe ratio), MVSC-L and MINC-L (CEQ), MINC-L and MIN-L (Sortino ratio), MINC-L and MIN-L (Omega ratio).

In this analysis, the local Gaussian approach seems to improve performance. This suggests that challenges related to return asymmetries may be handled in a familiar and well-established framework for portfolio management by replacing the global covariance matrix with it’s a local cousin. Improved performance and simplicity is some of the appeal with the local Gaussian approach to portfolio management in the MV setting. There are however matters to keep in mind when implementing the approach. The selection of gridpoints for calculating the pairwise local correlations will affect the local Gaussian covariance matrix. We have evaluated alternative approaches to the moving gridpoint selection without observing substantial changes in results and conclusions. A more thorough analysis of these effects is left for future studies.

6 Summary and conclusion

In this paper, we investigate whether the asymmetries typically found in financial returns data can be modeled using a new non-parametric measure of local dependence to improve asset allocation in a traditional Mean-Variance portfolio setting. Markowitz (1952) explicitly recommends the use of a probability model to generate the model inputs. Our study focuses on improving the covariance matrix used as input to a range of MV optimization rules by utilizing a model-based approach, namely the local Gaussian correlation.

We investigate the performance of the benchmark and four MV portfolio strategies in a six-asset portfolio consisting of indices exposed to stocks, commodities and interest rates. The strategies are implemented both with the global covariance matrix and the corresponding local covariance matrix calculated with a moving-grid method. The analysis is performed on monthly returns data with sampling windows of and observations. The strategies are evaluated out-of-sample based on need for portfolio rebalancing, turnover, terminal wealth and risk-adjusted performance.

Our findings suggest that the local Gaussian approach to portfolio management improves the traditional MV portfolio optimization when asymmetries are present in asset returns data. When investigating portfolio rebalancing, we find that the local Gaussian strategies do require higher turnover. After transactions costs have been taken into account, seven out of eight strategies achieve higher terminal wealth relative to their MV-benchmarks. In the risk-adjusted performance evaluation disregarding transaction costs, all local Gaussian strategies outperform the corresponding MV-models. When the cost of trade is included, six out of eight strategies improve upon their benchmarks, and the top-performing strategies are of local Gaussian type. This suggests the proposed methodology may be a viable and straightforward approach for improving asset allocation when asymmetries are present in returns data.

Acknowledgements

This work has been partly supported by the Finance Market Fund (Norway).

References

- Aït-Sahalia and Brandt [2001] Y. Aït-Sahalia and M. W. Brandt. Variable selection for portfolio choice. The Journal of Finance, 56(4):1297–1351, 2001.

- Ang and Chen [2002] A. Ang and J. Chen. Asymmetric correlations of equity portfolios. Journal of Financial Economics, 63(3):443–494, March 2002.

- Aslanidis and Casas [2013] N. Aslanidis and I. Casas. Nonparametric correlation models for portfolio allocation. Journal of Banking & Finance, 37(7):2268–2283, 2013.

- Bampinas and Panagiotidis [2017] G. Bampinas and T. Panagiotidis. Oil and stock markets before and after financial crises: A local gaussian correlation approach. Journal of Futures Markets, 37(12):1179–1204, 2017.

- Bekiros et al. [2015] S. Bekiros, J. A. Hernandez, S. Hammoudeh, and D. K. Nguyen. Multivariate dependence risk and portfolio optimization: An application to mining stock portfolios. Resources Policy, 46:1 – 11, 2015.

- Berentsen and Tjøstheim [2014] G. D. Berentsen and D. Tjøstheim. Recognizing and visualizing departures from independence in bivariate data using local Gaussian correlation. Statistics and Computing, 24(5):785–801, 2014.

- Berentsen et al. [2014] G.D. Berentsen, B. Støve, D. Tjøstheim, and T. Nordbø. Recognizing and visualizing copulas: an approach using local gaussian approximation. Insurance: Mathematics and Economics, 57:90–103, 2014.

- Campbell et al. [2002] R. Campbell, K. Koedijk, and P. Kofman. Increased correlation in bear markets. Financial Analysts Journal, 58(1):87–94, January 2002.

- Chollete et al. [2009] L. Chollete, A. Heinen, and A. Valdesogo. Modeling international financial returns with a multivariate regime switching copula. Journal of Financial Econometrics, 7:437–480, 2009.

- DeMiguel et al. [2009] V. DeMiguel, L. Garlappi, and R. Uppal. Optimal versus naive diversification: How inefficient is the 1/n portfolio strategy? The Review of Financial Studies, 22(5):1915–1953, 2009.

- Engle and Colacito [2006] R. Engle and R. Colacito. Testing and valuing dynamic correlations for asset allocation. Journal of Business & Economic Statistics, 24(2):238–253, 2006.

- Francis and Kim [2013] J.C. Francis and D. Kim. Modern portfolio theory: Foundations, analysis, and new developments. John Wiley & Sons, 2013.

- Garcia and Tsafack [2011] R. Garcia and G. Tsafack. Dependence structure and extreme comovements in international equity and bond markets. Journal of Banking and Finance, 35:1954–1970, 2011.

- Glosten et al. [1993] L. R. Glosten, R. Jagannathan, and D. E. Runkle. On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance, 48(5):1779–1801, 1993.

- Han et al. [2017] Y. Han, P. Li, and Y. Xia. Dynamic robust portfolio selection with copulas. Finance Research Letters, 21:190–200, 2017.

- Hatherley and Alcock [2007] A. Hatherley and J. Alcock. Portfolio construction incorporating asymmetric dependence structures: a user’s guide. Accounting & Finance, 47(3):447–472, 2007.

- Higham [2002] N.J. Higham. Computing the nearest correlation matrix—a problem from finance. IMA journal of Numerical Analysis, 22(3):329–343, 2002.

- Hjort and Jones [1996] N.L. Hjort and M.C. Jones. Locally parametric nonparametric density estimation. Annals of Statistics, 24(4):1619–1647, 1996.

- Hong et al. [2007] Y. Hong, J. Tu, and G. Zhou. Asymmetries in stock returns: Statistical tests and economic evaluation. Review of Financial Studies, 20(5):1547–1581, 2007.

- Jones [1996] M. Chris Jones. The local dependence function. Biometrika, 83(4):899–904, 1996.

- Jordanger and Tjøstheim [2020] L.A. Jordanger and D. Tjøstheim. Nonlinear spectral analysis: A local gaussian approach. Journal of the American Statistical Association, pages 1–55, 2020.

- Kakouris and Rustem [2014] I. Kakouris and B. Rustem. Robust portfolio optimization with copulas. European Journal of Operational Research, 235(1):28–37, 2014.

- Kalotychou et al. [2014] E. Kalotychou, S. K. Staikouras, and G. Zhao. The role of correlation dynamics in sector allocation. Journal of Banking & Finance, 48:1–12, 2014.

- Keating and Shadwick [2002] C. Keating and W.F. Shadwick. A universal performance measure. Journal of performance measurement, 6(3):59–84, 2002.

- Lacal and Tjøstheim [2017] V. Lacal and D. Tjøstheim. Local gaussian autocorrelation and tests of serial dependence. Journal of Time Series Analysis, 38(1):51–71, 2017.

- Lacal and Tjøstheim [2019] V. Lacal and D. Tjøstheim. Estimating and testing nonlinear local dependence between two time series. Journal of Business and Economic Statistics, 37(4):648–660, 2019.

- Low et al. [2013] R. K. Low, J. Alcock, R. Faff, and T. Brailsford. Canonical vine copulas in the context of modern portfolio management: Are they worth it? Journal of Banking & Finance, 37(8):3085–3099, 2013.

- Low et al. [2016] R. K. Y. Low, R. Faff, and K. Aas. Enhancing mean–variance portfolio selection by modeling distributional asymmetries. Journal of Economics and Business, 85:49–72, 2016.

- Markowitz [1952] H. Markowitz. Portfolio selection. The Journal of Finance, 7(1):77–91, 1952.

- Nguyen et al. [2020] Q.N. Nguyen, S. Aboura, J. Chevallier, Z. Lyuyuan, and B. Zhu. Local gaussian correlations in financial and commodity markets. European Journal of Operational Research, 2020.

- Okimoto [2008] T. Okimoto. New evidence of asymmetric dependence structures in international equity markets. Journal of Financial and Quantitative Analysis, 43(3):787–816, September 2008.

- Otneim and Tjøstheim [2017] H. Otneim and D. Tjøstheim. The locally Gaussian density estimator for multivariate data. Statistics and Computing, 27(6):1595–1616, 2017.

- Otneim and Tjøstheim [2018] H. Otneim and D. Tjøstheim. Conditional density estimation using the local gaussian correlation. Statistics and Computing, 28(2):303–321, 2018.

- Otneim and Tjøstheim [2021] H. Otneim and D. Tjøstheim. The locally gaussian partial correlation. Journal of Business & Economic Statistics, pages 1–13, 2021.

- Patton [2004] A. J. Patton. On the out-of-sample importance of skewness and asymmetric dependence for asset allocation. Journal of Financial Econometrics, 2(1):130–168, 2004.

- Sharpe [1966] W. F. Sharpe. Mutual fund performance. The Journal of business, 39(1):119–138, 1966.

- Silvapulle and Granger [2001] P. Silvapulle and C. W. J. Granger. Large returns, conditional correlation and portfolio diversification: a value-at-risk approach. Quantitative Finance, 1(5):542–551, 2001.

- Sortino and Price [1994] F.A. Sortino and L.N. Price. Performance measurement in a downside risk framework. the Journal of Investing, 3(3):59–64, 1994.

- Støve and Tjøstheim [2014] B. Støve and D. Tjøstheim. Measuring asymmetries in financial returns: An empirical investigation using local gaussian correlation. In M. Meitz N. Haldrup and P. Saikkonen, editors, Essays in Nonlinear Time Series Econometrics, pages 307–329. Oxford University Press, Oxford, 2014.

- Støve et al. [2014] B. Støve, D. Tjøstheim, and K.O. Hufthammer. Using local gaussian correlation in a nonlinear re-examination of financial contagion. Journal of Empirical Finance, 25:785–801, 2014.

- Tjøstheim and Hufthammer [2013] D. Tjøstheim and K.O. Hufthammer. Local Gaussian correlation: A new measure of dependence. Journal of Econometrics, 172:33–48, 2013.

- Tjøstheim et al. [2021] D. Tjøstheim, H. Otneim, and B. Støve. Statistical dependence: Beynd pearson’s . Statistical Science, to appear, 2021.

- Tokat and Wicas [2007] Y. Tokat and N.W. Wicas. Portfolio rebalancing in theory and practice. The Journal of Investing, 16(2):52–59, 2007.

- Tu and Zhou [2011] J. Tu and G. Zhou. Markowitz meets talmud: A combination of sophisticated and naive diversification strategies. Journal of Financial Economics, 99(1):204–215, 2011.

- Yao and Fan [2015] Q. Yao and J. Fan. The Elements of Financial Econometrics. Cambridge University Press, 2015.