A Neural Frequency-Severity Model and Its Application to Insurance Claims

Abstract

This paper proposes a flexible and analytically tractable class of frequency-severity models based on neural networks to parsimoniously capture important empirical observations. In the proposed two-part model, mean functions of frequency and severity distributions are characterized by neural networks to incorporate the non-linearity of input variables. Furthermore, it is assumed that the mean function of the severity distribution is an affine function of the frequency variable to account for a potential linkage between frequency and severity. Within our modelling framework, we provide explicit closed-form formulas for the mean and variance of the aggregate loss. Components of the proposed model including parameters of neural networks and distribution parameters can be estimated by minimizing the associated negative log-likelihood functionals with neural network architectures. Furthermore, we leverage the Shapely value and recent developments in machine learning to interpret the outputs of the model. Applications to a synthetic dataset and insurance claims data illustrate that our method outperforms the existing methods in terms of interpretability and predictive accuracy. Keywords: frequency-severity model; dependence modelling;aggregate risk losses; interpretable machine learning

1 Introduction

When we deal with a dataset that involves a joint distribution of frequency and severity such as insurance claims, health care expenditures and operational risk losses, frequency-severity models are widely considered. For example, Chavez-Demoulin et al. [2006], Dahen and Dionne [2010] and Brechmann et al. [2014] developed frequency-severity models to quantify and analyze operational losses, and Frees et al. [2011a] used the aggregate loss model for predicting health care expenditures. In particular, they are a fundamental tool for risk management and assessment in insurance business. This paper proposes a novel modelling framework based on neural networks which unifies neural networks and frequency-severity models to address fundamental empirical observations. We call this new framework the neural frequency-severity model, which we abbreviate to NeurFS.

The first observation is that severity is positively(or negatively) related to frequency. Motivated by the empirical feature, two approaches have been mainly explored in the generalized linear model(GLM) framework. Gschlöl and Czado [2007], Frees et al. [2011a] and Garrido et al. [2016] used the frequency variable, which is the number of claims in the context of actuarial science, as an additional covariate to model the severity distribution, allowing to incorporate the dependence between frequency and severity. On the other hand, the traditional GLM has been extended by combining marginal distributions for frequency and severity via a bivariate copula, for example, see Czado et al. [2012] and Kramer et al. [2013]. Two ideas are extensively reviewed and compared to traditional independent models in Shi et al. [2015].

Despite such developments in the literature, the GLM based models have their obvious limitation in the sense that mean functions of marginal distributions are restricted to a linear form, which is not enough to accommodate complex relations in covariates. For example, Kelly and Nielson [2006] found that the severity against age is ‘U’ shaped in North American auto insurance data, indicating the strong evidence on the nonlinear relationship between severity and age. In response to the fact, the second feature this paper considers is that input variables can be non-linearly related to frequency and/or severity. Recently, there is a growing body of literature extending frequency-severity models based on machine learning techniques to capture the nonlinearity. For example, Yang et al. [2018] introduced a gradient boosting algorithm for the nonlinear Tweedie model and Zhou et al. [2020] extended it to the zero-inflated Tweedie model. Huang and Meng [2019] investigated several machine learning techniques in predicting frequency and severity based on telematics driving data. However, these models need to assume that frequency and severity are independent. In addition, Guelman [2012] and Su and Bai [2020] applied the gradient boosting to modelling frequency and severity distributions that allows their dependency. But, in their models, it is impossible to compute and analyze the aggregate loss, which is the most important quantity in analyzing frequency-severity data. More importantly, these models rely on the feature importance measure and dependence plot to interpret the outputs of models. Unfortunately, many researchers have revealed that these tools are inconsistent and inaccurate, resulting in misleading decision-making when deploying the model in a real business, see Lundberg and Lee [2017].

The goal of our modelling is to overcome the limitations stated above by combining the advantages of the existing models and nonlinear regression based on neural networks. In particular, the use of neural networks allows our model to automatically extract complex relations in data and efficiently handle high-dimensional and large scale data. Also, the feasibility of NeurFS is fully supported by the availability of massive data, increase in computing power and storage capacity, and advanced machine learning algorithms.

The key contributions of our work are summarized as follows:

-

•

Analytical tractability: We provide the explicit closed-form solutions for mean and variance of the aggregate loss in the presence of the nonlinearity and dependence structure in data.

-

•

Flexibility: A wide range of probability distributions can be utilized for marginal frequency and severity distributions in our modelling framework. This paper mainly considers the exponential family of distributions due to its popularity.

-

•

Efficient estimation: We suggest efficient neural network architectures to estimate parameters of the model. In our training scheme, the parameters of neural networks and distribution parameters are simultaneously estimated by solving the associated optimization problems.

-

•

Interpretability: The main components of NeurFS are neural networks, of which the great expressivity is strength in modelling, but weakness in interpreting the result. We improve the interpretability of our models by applying the Shapley value-based explanation method, proposed by Lundberg and Lee [2017].

This paper is organized as follows. In Section 2, we develop NeurFS with some assumptions. In Section 3, we present some background on neural networks and notations. Also, we describe the estimation process and the network architecture. Section 4 demonstrates the accuracy and effectiveness of our model through an artificial example. In Section 5, we apply NeurFS to real insurance claim data and explain the results via the SHAP model.

2 Neural frequency-severity model

2.1 Marginal distributions and assumptions

This subsection introduces two marginal distributions of frequency-severity models with associated regularities to develop NeurFS. Let be the number of claim counts for a fixed time period. We interchangeably use the term, frequency, to represent the random variable . We assume that there exists some constant such that for ,

We note that the moment-generating function is well-defined within the interval with and the endpoints may be included. In particular, we have the following useful identity for the th order derivative of the moment generating function of :

| (1) |

for . A common and popular candidate for is the Poisson distribution. In addition, several parametric count distributions have been discussed to capture the excess zero observations and over-dispersion observed in frequency data. Without additional effort, our approach can utilize these distributions as the frequency part. We list some count distributions and their moment generating functions in Table 6 and 7.

Consider the aggregate loss random variable during the given time period

where is the size of the individual claim(or severity). Define when by convention. We further define the average claim size(or average severity) as

| (2) |

and then we have . Traditionally, many studies assumed that is independent of ’s to exploit the favorable fact that the mean of the aggregate loss can be computed by the product of and . However, the model without taking account of the dependence effect between frequency and severity is inevitably faced with model risk. Indeed, various papers have revealed that the average claim size is positively(or negatively) related to the number of claims in non-life insurances. For example, see Shi et al. [2015] and Garrido et al. [2016]. NeurFS incorporates the dependence structure by describing the average severity in terms of covariates as well as the frequency.

We suppose that ’s are mutually independent conditional on . Notice that the assumption does not imply and are independent of . While the flexibility of our approach allows us to use a wide spectrum of distributions for the severity, we mainly consider the exponential family of distributions throughout this paper due to its generality and popularity in actuarial science. If the distribution of belongs to the exponential family of distributions, we write and the probability density is defined by

where is the canonical parameter and is the dispersion parameter. The normalizing function and the cumulant function are determined from the actual probability function. Expectation and variance of the random variable are expressed as

and

where and are the first and second derivatives of with respect to , respectively, and is called the variance function.

One useful property of the exponential family of distributions is that they are closed under the convolution operation. That is, the average claim size also belongs to the exponential family of distributions with a different dispersion parameter. Specifically, if , conditional on , we then have . This well-known property can be easily confirmed by using the moment generating function of the exponential family of distributions. We refer to Frees [2014]. As a result, one can identify the average severity based on the knowledge about the individual severity distribution that is well documented in the literature. For example, is given by

| (3) |

where is the variance function of .

2.2 Dependent and nonlinear model

This subsection develops NeurFS and compute the mean and variance of the aggregate loss random variable. Let be the set of covariates that explains the -th observation, be the number of claims and be the average severity. We model the mean function of random variable in terms of a regression function with the log link :

| (4) |

or equivalently, where is the exposure variable.

Next, the mean function of random variable is specified by a regression function and

| (5) |

or equivalently,

where is a parameter that controls the dependency of the frequency and severity.111 The range of the dependence parameter is dependent on the frequency distribution of interest It is worth noting that we do not impose any linearity or other restrictions on and to incorporate the non-linearity of covariates. Instead, and are represented by neural networks that can approximate any complex functions thanks to the universal approximation theorem. Henceforth, we call the triplet of as the neural frequency-severity model.

NeurFS is fully analytically tractable in the sense that once we have estimated and , we can obtain explicit closed form solutions for the mean and variance of the aggregate loss of , which are important quantities for analyzing frequency-severity data. In particular, these statistics are essential for managing insurance portfolios. Given , the mean of the aggregate loss is given by

where is defined in (1). Note that is always well-defined when .

The variance of the aggregate loss of can be also derived analytically. From the law of total variance and (3), one calculates that

where is defined in (1), which is also well-defined for .

The following theorem summarizes the mean and variance of the aggregate loss for within NeurFS.

Theorem 2.1.

Given the neural frequency-severity model, ), the mean and variance of the aggregate loss are given by

and

for where is the moment-generating function of the random variable , and and are the first and second-order derivative of defined in (1). and are the dispersion parameter and variance function of the individual claim loss , respectively.

When , the NeurFS model reduces to a nonlinear prediction model under the independent assumption between frequency and severity distributions. , , and for popular distributions in actuarial science can be found in Table 6 and 7.

Example 2.1.

Suppose that frequency and severity follow the zero-inflated Poisson distribution and Gamma distribution, respectively. That is, and . Then, we obtain

and

| (6) |

Moreover, we remark that it is straightforward to consider , and are also dependent on . However, it is assumed that these values are constants throughout our analysis to keep our model being parsimonious.

3 Neural network and estimation

This section discusses an estimation procedure for and associated distribution parameters. Before proceed, we present some background on neural networks. Simply speaking, the (feed-forward) neural network is constructed by the composition of affine transformations and non-linear functions, so called the activation function. One of the key reasons for the success of neural networks lies on the universal approximation theorem which states that they can approximate any function provided that the number of layers and neurons is sufficient. In a statistical model context, the expressive power of neural networks enables the proposed model to capture complex non-linearity in inputs.

3.1 Definitions and notations

Over the two past decades, various types of neural network architecture have been developed to deal with different data features and tasks arising in science and engineering. In this paper, we focus on the feed-forward neural network(also known as the fully connected network), which is one of the fundamental architectures.

Let and be the number of hidden layers and the number of neurons in each layer, respectively. Here, and represent the dimension of input and output layers, respectively and are the dimensions of hidden layers. In this paper, we will set and where is the number of covariates. Let denote the activation function and define

| x |

for where is the weight matrix between the -th layer and -th layer and is the bias term. The parameters of the neural network, the set of trainable parameters of all weight matrices and bias terms in the network, are denoted by where is a parameter space of the neural network and . Then, the neural network is defined by

| (7) |

with where the activation function is applied element-wise. In particular, the case when is called “deep” neural network.

Theoretical properties of neural networks as function approximators have been extensively studied in the literature. See Hornik et al. [1989], Hornik [1991] and Barron [1993]. To make our paper self-contained, we record the following theorem from Hornik et al. [1989].

Theorem 3.1.

(Universal approximation theorem, Hornik et al. [1989]) Suppose the activation function is bounded and nonconstant then, for any finite measure , multilayer feedforward networks can approximate any function in (the space of all functions on such that ) arbitrarily well, provided that sufficiently many hidden layers are available.

Moreover, if the activation function is continuous, bounded and nonconstant then, for arbitrary compact subsets , multilayer feedforward networks can approximate any continuous function on arbitrary well with respect to uniform norm, provided that sufficiently many hidden layers are available.

Remark 3.1.

The sigmoid and tanh activation functions satisfy the condition in Theorem 3.1. On the other hand, in practice, it is common to use piecewise-linear functions such as Rectified Linear Units(ReLUs) and its variants as an activation function. We refer to Pan and Vivek [2016] for the expressiveness of feed-forward neural networks with ReLu activations.

3.2 Estimation of , and model parameters

Suppose that we construct a dataset from independent observations:

where is the feature set of covariates, is the number of claims, is the observed period and is the average severity. Let be the density of the frequency distribution with the mean function and a vector of other parameters . For example, is the proportion of structural zeros for the zero-inflated Poisson distribution and is the empty set for one-parameter distributions like the Poisson distribution. Also, we denote the conditional density of the average severity given the number of claims by with the mean function and the dispersion parameter for the severity distribution. Given , then, the log-likelihood functional of the frequency model is given by

where is a neural network for the frequency model, which is defined in (7). Similarly, the log-likelihood functional of the average severity model can be written as

where is the second neural network for the severity model. Then, the mean function for the frequency model is defined as by minimizing the negative log-likelihood(NLL) functional:

| (8) |

where is the parameter space of the neural network of the frequency model and is the set of possible values for . Notice that we have used the entire dataset to estimate the frequency model. On the other hand, the subset of the dataset for which the number of claims is positive is only used for estimating , and . More specifically, the mean function for the severity model is defined as where

| (9) |

where and is the parameter space of the neural network of the severity model.

We emphasize that our estimating process is more efficient and easier to be implemented compared to the existing non-linear(but independent) models of Yang et al. [2018]. In the model of Yang et al. [2018], a prediction function and other distribution parameters have to be estimated separately. Thus, one needs to sequentially solve three optimization problems when there are two distribution parameters. In contrast, the frequency mean estimate and are simultaneously obtained by solving the optimization problem (8) in our learning process. Likewise, the severity mean estimate and two parameters and are computed at once from the optimization problem (9). This property is extremely useful when there are many parameters associated with frequency and severity distributions to be estimated.

In the specification of Example 2.1, the above estimation process is stated as follows:

| (10) | |||||

| (11) | |||||

We give details about training specification and neural network architectures. For simplicity’s sake, we focus on training the frequency model (10). The severity model (11) can be similarly treated. Let denote the objective function in (10).

To train neural networks, it is common to use stochastic gradient descent(SGD) algorithm which updates parameters at each iteration as follows: for ,

where is mini-batch size and is randomly chosen from the dataset. Along with the great success of nerual networks, several variants of SGD such as ADAM of Kingma and Ba [2015] and AMSGrad of Reddi et al. [2018] have been proposed to boost the speed and stability of the convergence. The network parameter w is initialized according to the rule proposed by He et al. [2015] and the initial value for is uniformly distributed on . We use the exponential linear unit(ELU) of Clevert et al. [2016] defined as

for all experiments in this paper.

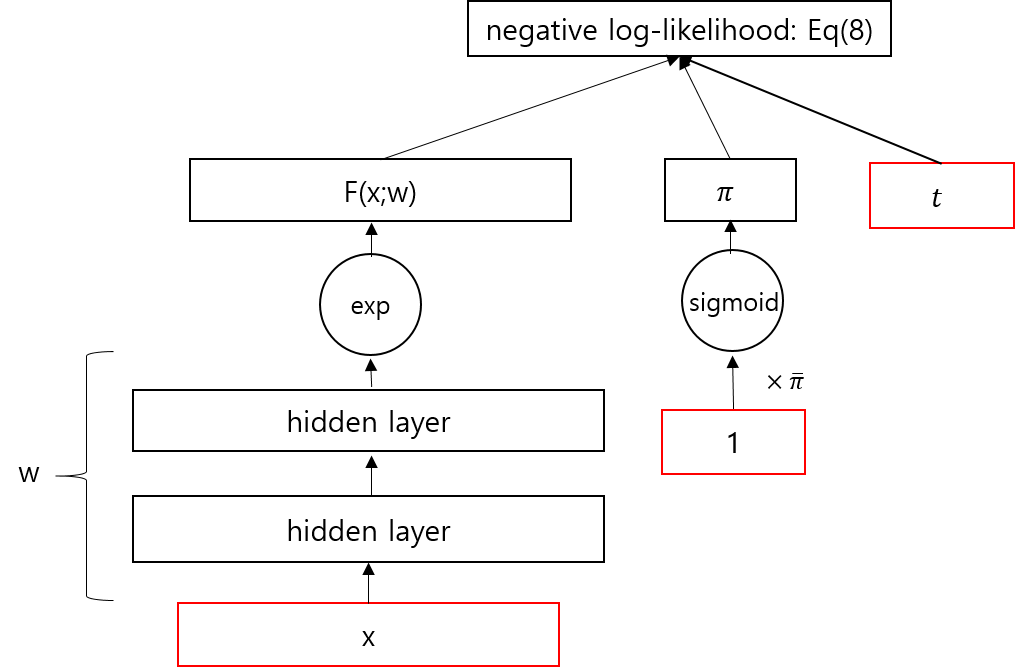

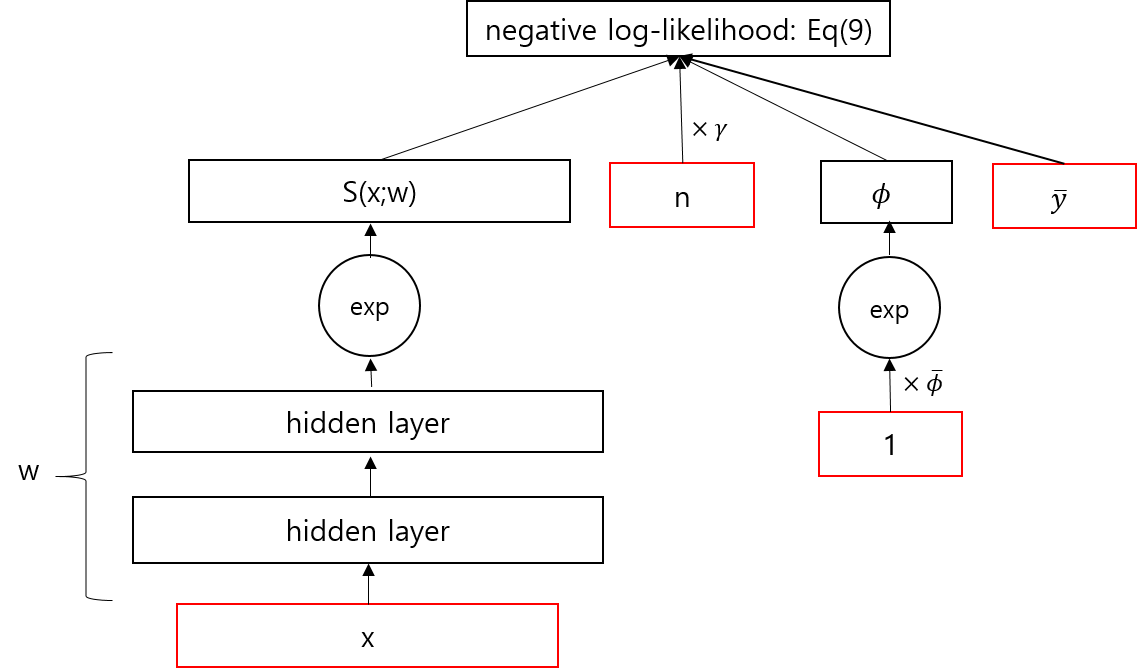

Distribution parameters are often restricted to some pre-specified domains. For example, the proportion of structural zeros in the zero-inflated Poisson distribution has a value between and and the dispersion parameter in the severity distribution has a positive value. To ensure these parameters to stay within given domains, we apply proper transformations such as for positive parameters and for -valued parameters at the last layer. As a result, is expressed by with some trainable parameter . The final networks for the frequency model and severity model are visualized in Figure 1 and 2.

4 Simulation study

This subsection examines the performance of NeurFS by estimating the mean functions of frequency, severity and aggregate loss, and associated parameters from a synthetic dataset. To demonstrate the importance of taking into account non-linearity and dependence in covariates, we compare the proposed algorithm to two existing models in the literature; 1. linear and independent model(GLM) 2. linear but dependent model(dGLM) of Garrido et al. [2016].

Let be a vector of covariates for the -th observation. For simplicity, we set for all observations. Define and . Moreover, suppose that the number of claims follows the zero-inflated Poisson distribution with the mean function

| (12) |

and . Also, assume that the average severity is generated from the Gamma distribution with the mean function

| (13) |

and the dispersion parameter , and . Then, from Theorem 2.1 and Example 2.1, we can analytically compute the true mean of the aggregate loss

We generate 40,000 samples

with for and , i.e., for .

The dataset exhibits both the nonlinearity of covariates and the dependency between frequency and severity. Thus, it is able to identify the impact of model misspecification stemmed from the lack of non-linearity and dependence by comparing the three different models.

Under GLM, the estimation errors come from both the linear assumption in covariates and the independent assumption between frequency and severity. It is expected that dGLM works well when there is a linear relationship among variables and the average severity is linearly dependent on the frequency. However, dGLM is still exposed to the presence of non-linearity in covariates like GLM. In contrast, our model remains valid even when the non-linearity and the dependency are present in the data.

Frequency model

To estimate the mean function , we use a neural network with hidden layers and neurons in each layer. The trained mean function is obtained by solving (10) with AMSGrad of Reddi et al. [2018] for epochs. For AMSGrad, the initial learning rate is set to and decays by a constant factor every epochs. The mini-batch size is 512.

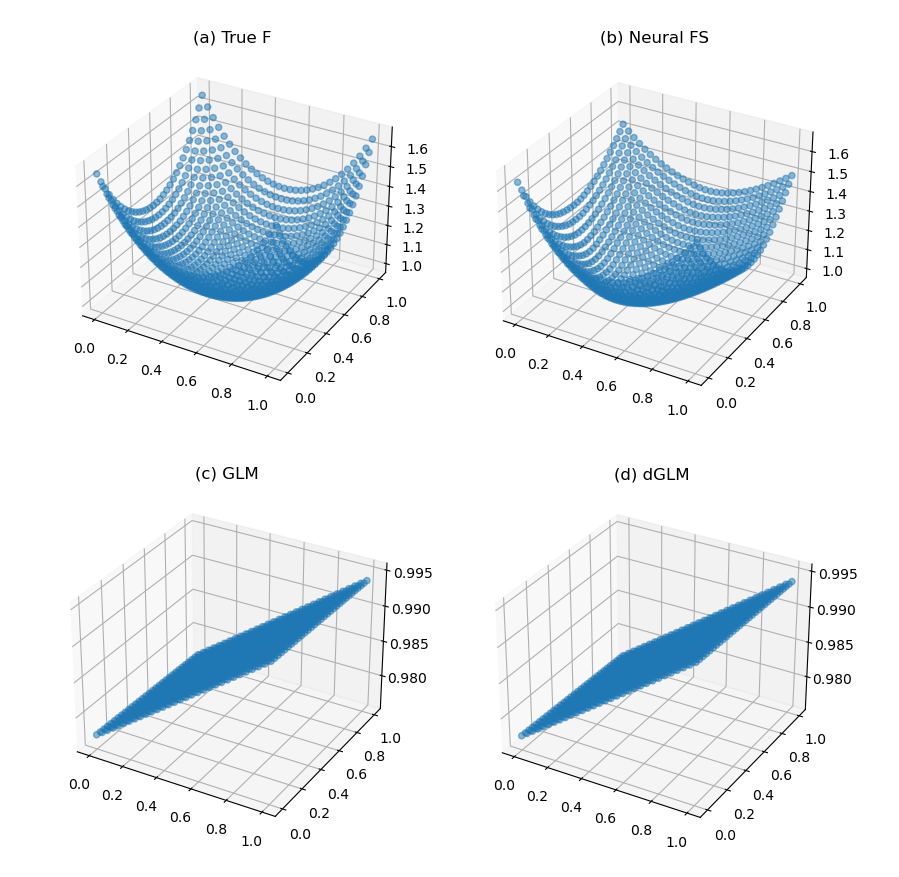

Figure 3 shows that the true mean function and the estimated functions obtained from three different models. It is apparent that the NeurFS model replicates the true mean function accurately, but GLM and dGLM generate completely different mean functions. Note that GLM and dGLM produce the equivalent mean function for the frequency model. To quantify the accuracy of models, we compute mean absolute error(MAE) and root mean squared error(RMSE) for , that measures and norm of the prediction error on the grid , respectively. Table 1 displays MAE and RMSE of NeurFS, GLM and dGLM, showing that the proposed method significantly performs better than other two models in terms of given measures.

| GLM | dGLM | NeurFS | |

| Frequency model | |||

| MAE | 0.2456 | 0.2456 | |

| RMSE | 0.2920 | 0.2920 | |

| 0.2591(29.55%) | 0.2591(29.55%) | ||

| Severity model | |||

| MAE | 4.1135 | 0.2065 | |

| RMSE | 4.4662 | 0.2867 | |

| 2.1888(118.88%) | 1.0300(3%) | ||

| N/A | 0.5190(3.8%) | ||

| Aggregate loss | |||

| MAE | 3.3289 | 2.7832 | |

| RMSE | 5.1093 | 4.5908 | |

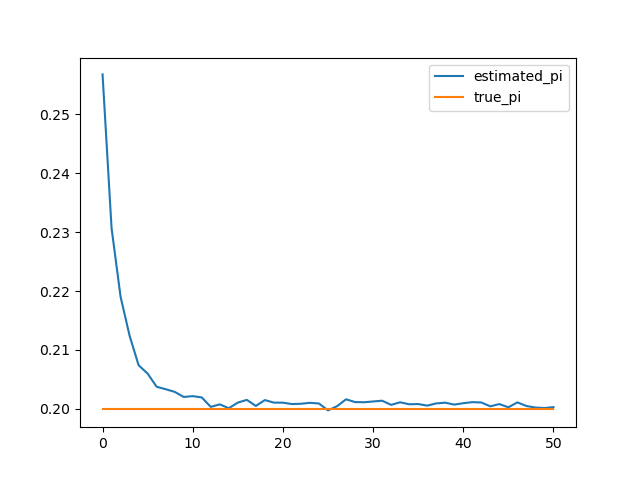

Figure 4 plots how is estimated in NuerFS as training progresses. It is observed that starting from about tends to converge to the true value as the number of epochs increases. On the other hands, GLM and dGLM considerably overestimate to compensate the non-linearity, resulting in large prediction error.

Severity model

Let us focus on the severity model defined in (13). We train a neural network with hidden layers and neurons in each layer to estimate . See Figure 2 for the whole neural network structure. The optimization problem (11) for the severity model is solved using AMSGrad for epochs with the same setting done in the frequency model except for the initial learning rate .

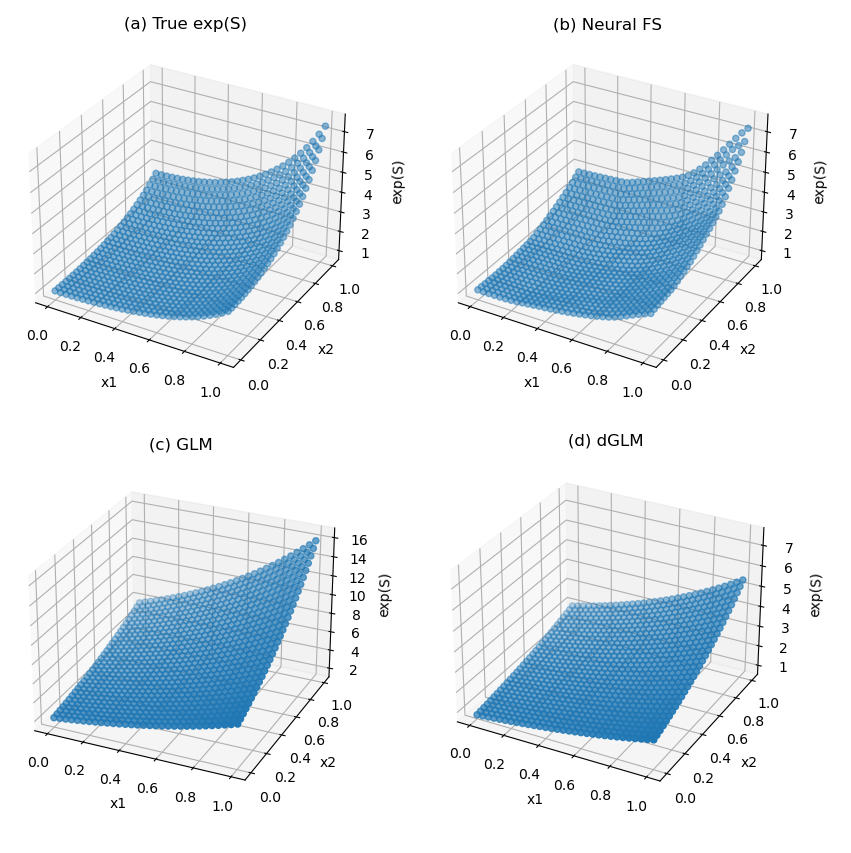

Figure 5 plots the true function, , and the fitted curves, , under the three different models. The NeurFS model generates the highly accurate estimated function, but GLM(and dGLM) overestimates(and underestimates) when and are close to . Table 1 summarizes simulation results and their accuracy measures, showing that our model is superior to GLM and dGLM. The proposed model achieves the lowest MAE and RMSE and recovers accurate distribution parameters, and , with and relative errors, respectively.

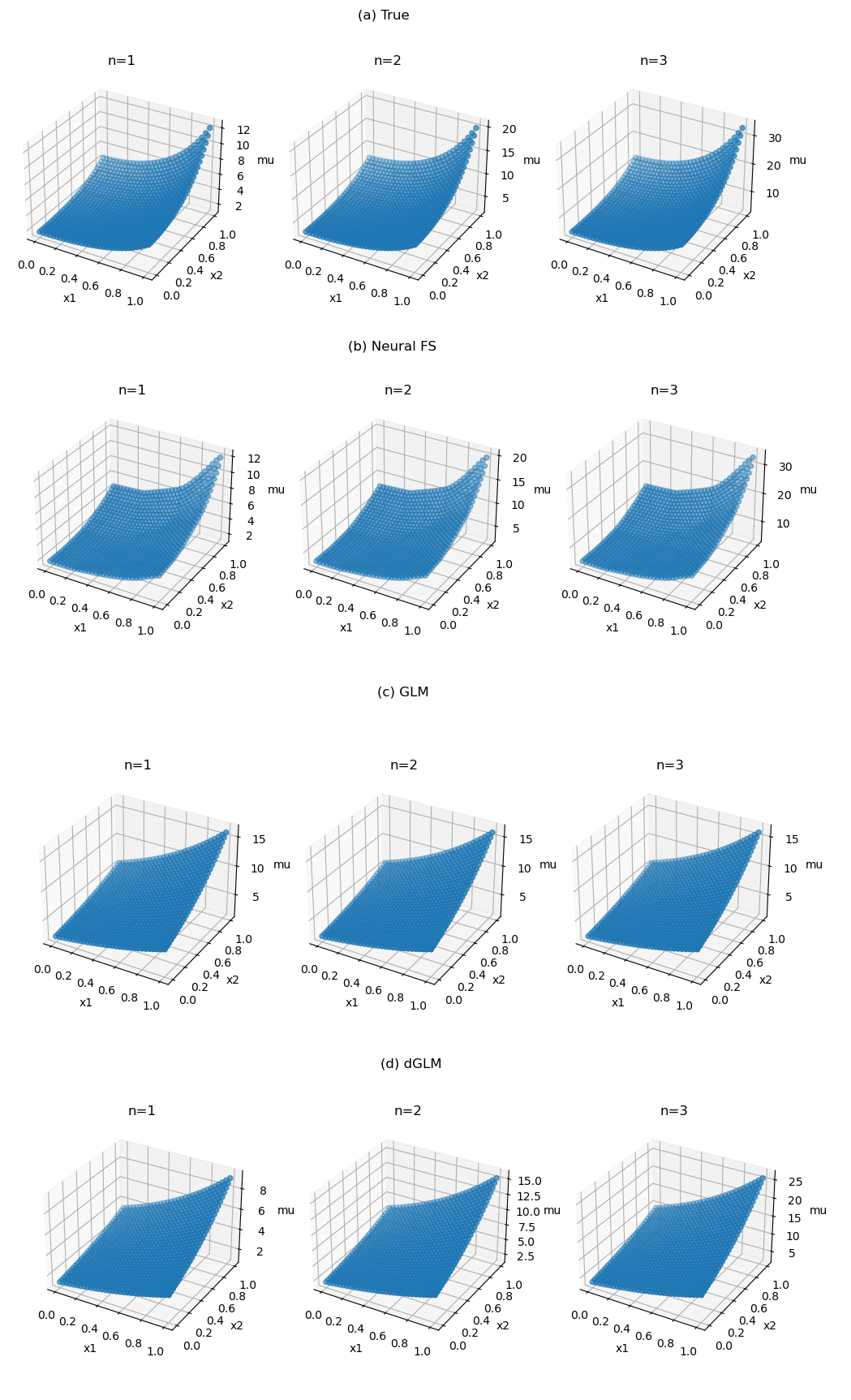

We also plot the mean function of the average severity, , with and the estimated curves to investigate the dependence structure in Figure 6. It is observed that the estimated mean functions of the average severity in our model and dGLM are positively correlated to . However, the mean function in GLM does not change with respect to due to the independence assumption between frequency and severity.

Aggregate Loss

Predicting the aggregate loss is primary purpose of frequency-severity models. The performance of our model in predicting the aggregate loss is compared with GLM and dGLM in Table 1. Our model significantly reduces prediction error for the aggregate loss. These remarkable results demonstrate that the NeurFS model is effectively able to extract complex relations in response and explanatory variables and dependence structure between frequency and severity distributions. Furthermore, we find that the impact of model misspecification can cause substantial prediction errors and cannot be negligible when we deal with nonlinear and dependent frequency-severity data.

5 Application to insurance claims

This section is devoted to applying our method to real insurance claims data and to interpreting the results of the model. This empirical study will show the feasibility and effectiveness of the NeurFS model in practice.

5.1 Data description

We consider the auto-insurance claim data from “freMTPL2freq” and “freMTPL2sev” in the R package “CASdatasets”, which is also used in Su and Bai [2020]. After deleting missing data, we have 668,897 records and each record includes 9 explanatory variables as well as the number of claims , the average severity and exposure . See Table 2 for the description of explanatory variables, which is available at “http://cas.uqam.ca/pub/R/web/CASdatasets-manual.pdf”.

| Variable | Type | Description |

|---|---|---|

| VehPower | C | The power of the car (6 classes) |

| VehAge | C | The vehicle age in years. ((0,1], (1,4], (4,10], (10, )) |

| DrivAge | C | The driver age in years |

| ([18,21], (21,25], (25,35],(35,45], (45,55],(55,70], (70,)) | ||

| VehBrand | C | The car brand (14 classes) |

| VehGas | C | The car gas (diesel or regular) |

| Region | C | The policy region in France (22 classes) |

| Area | C | The density value of the city community where |

| the car driver lives in (6 classes) | ||

| Density | N | the density of inhabitants in the city the driver of the car lives in |

| BonusMalus | N | Bonus/malus, between 50 and 350 |

| : means bonus, means malus in France. |

The dataset is split into samples as training set to train models and samples as test set to evaluate the trained model. For neural networks, one-hot encoding is used for converting categorical variables and max-min normalization is used to scale numeric variables. In addition, the intercept is included for GLM and dGLM.

5.2 Result analysis

We use a fully connected feed forward network with 2 hidden layers and 100 neurons on each layers for both frequency and severity models. i.e, , , and (See the notations in subsection 3.1). Furthermore, we employ dropout (Srivastava et al. [2015]) and batch normalization (Ioffe and Szegedy [2015]) to prevent our models from overfitting and boost the training speed. Other hyperparameters including the number of epochs, learning rate, learning decay schedule and so on can be found in Table 3.

| Frequency model | Severity model | |

|---|---|---|

| The number of epochs | 100 | 100 |

| Optimizer | AMSGrad | AMSGrad |

| Learning rate | 0.001 | 0.005 |

| Batch size | 256 | 128 |

| Dropout rate | 0.25 | 0 |

| Batch Normalization | True | False |

| Activation function | ELU | ELU |

| Early stopping - patience | 5 | 5 |

| Early stopping - learning decay factor | 0.5 | 0.5 |

In order to compare the accuracy of models, we measure the mean absolute error in predicting the frequency and the average severity as follows:

and

where is the number of test set, is the observed number of claims, is the model’s prediction of , is the observed average severity and is the model’s prediction of . That is, for the NeurFS model, and are written as and , respectively. In addition, we report the root mean squared error with respect to the actual observations. Table 4 shows that NeurFS provides the lowest performance measures for predicting both frequency and severity, confirming that our model outperforms GLM and dGLM.

| GLM | dGLM | Neural FS | |

| Frequency | |||

| MAE | 0.0720 | 0.0720 | |

| RMSE | 0.2047 | 0.2047 | |

| Severity model | |||

| MAE | 2023 | 1566 | |

| RMSE | 2919 | 2510 | |

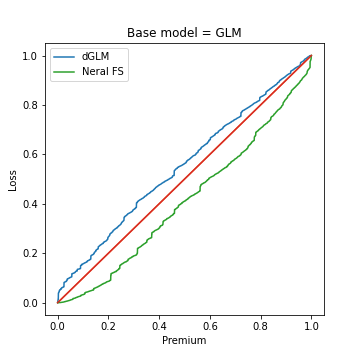

Predicting the aggregate loss is particularly important for an insurer because the insurer that charges a mispriced premium is prone to adverse selection in a competitive market (Cohen and Siegelman [2010] and Frees et al. [2014]). However, when it comes to assessing models in predicting the aggregate loss, a special care needs to be taken because the distribution of the aggregate loss is not only zero-inflated, but also heavily skewed. The obstacles make the MAE or RMSE to be not appropriate for evaluating the accuracy of the predicted aggregate loss. Alternatively, this paper adopts the ordered Lorenz curve and the associated Gini index, proposed by Frees et al. [2011b], as a statistical measure for examining predictions of the aggregate loss distribution.

Define the relative premium as where is the predicted aggregate loss of a base model and is the predicted aggregate loss of a competing model. Then, the ordered premium distribution, taking values between , is given by

and the ordered loss distribution, taking values between , is

where is the indicator function. The graph of is called the ordered Lorenz curve and the -degree line is known as the line of equality. The Gini index is computed by twice the area between the ordered Lorenz curve and the line of equality. A larger Gini index implies that the competing model is superior to the base model in identifying risk groups. We compute the Gini indices by successively selecting the base model and the competing model among GLM, dGLM and NFS.

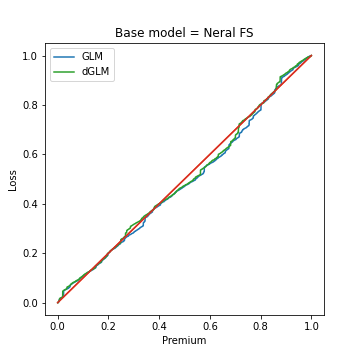

Figure 7 shows the ordered Lorenz curves of all possible pairs of models. It is clear that the area between the ordered Lorenz curve and the line of equality is larger when the competing model is NeurFS. On the other hand, if NeurFS is chosen as the base model, the areas between the ordered Lorenz curve and the line of equality are close to zero for GLM and dGLM as the competing model, meaning that GLM and dGLM does not improve the model performance against NeurFS. We record the corresponding Gini indices in Table 5. These results suggest that our model that takes account of nonlinearity and dependency provides effective risk segmentation, and outranks the existing methods.

| Alternative score | |||

| Base score | GLM | dGLM | Neural FS |

| GLM | - | -0.1037 | |

| dGLM | 0.1557 | - | |

| Neural FS | - | ||

5.3 Model interpretation

We introduce an excellent tool for explaining outputs of neural networks based on Shapely value. The Shapley value proposed by Shapley [1953] is one of the most important object in cooperative game theory to explain marginal contributions of players. Given a set of players , a cooperative game is characterized by a finite set and a characteristic function with where is the set of all possible subset of . Simply speaking, maps to the sum of payoffs that can be obtained from given players. Then, the Shapely value is given by

Lundberg and Lee [2017] proposed Shapley additive explanation(SHAP) to interpret a prediction of highly complex models such as neural networks, Gradient Boost, XGBoost, by combining local explanation models of Riberiro et al. [2016] and Shapley values. In their seminal work, it is shown that SHAP provides the unique additive feature importance values that satisfy three desirable properties: local accuracy, missingness and consistency. Also, it is proven that SHAP values are more consistent with human intuition than other methods such as the dependence plot, the feature importance and saliency map in the literature. We refer the interested readers to Lundberg and Lee [2017] and Adebayo et al. [2018].

In the SHAP, each player is considered as each input variable in the model and is the output of the model of interest. SHAP specifies the explanation model defined as

| (14) |

where is the importance of a input variable and , so called the base value, is the prediction value without any features. That is, SHAP value represents the contribution of each feature to the prediction. We build two SHAP models for and .

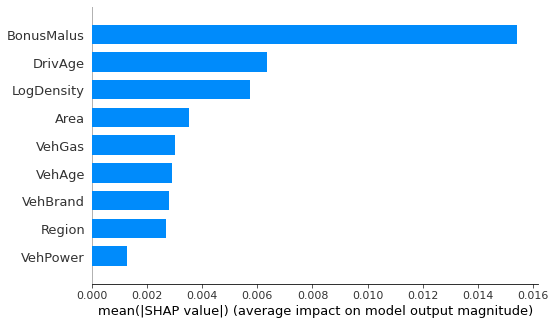

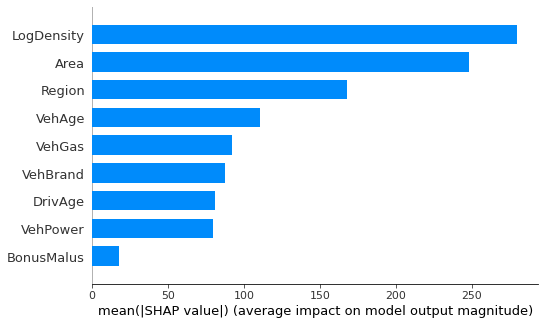

First of all, we investigate the global importance of each feature, which is computed by the mean absolute value of that feature over given samples. Figure 8 shows the global feature importance of the 9 explanatory variables for the frequency and severity models. One can observe that significant variables of the frequency and severity models are completely different. For example, BonusMalus is the most influential variable for the frequency model. It is quite natural and intuitive since BonusMalus, also known as the no-claim discount, is directly determined by the driver’s claim history. More importantly, it is indirectly verified that a driver with a low BonusMalus is likely to avoid a car accident due to the driver’s skill or defensive driving, which giving the justification of a BonusMalus system. Next, it is well recognized that the age of the driver is an important variable in the frequency model. We can see that the impact of Driver’s age is second most influential for explaining the predicted frequency. LogDensity, Area and Region are the most three relevant variables for the severity model. This result is consistent with a general consensus that the risk of fatal injury in rural areas is less than that in urban areas (Castro-Nuno and Arevalo-Quijada [2018]). On the other hand, BonusMalus is the least important factor. This is because severity is a quantity conditional on the occurrence of the accident.

We now perform an individual risk analysis by looking SHAP values for each observation’s prediction. Imagine that one sample is randomly chosen. We then compute SHAP values for the frequency model. The model’s output is approximately . Figure 9 illustrates how SHAP values for each feature contribute to the model’s output. The base value defined in (14) is , which is the predicted frequency without any information on features of the observation. To reach the model’s prediction , SHAP values of all features are added. In this example, the fact that the driver lives in Area6 increases the frequency rate. In contrast, the predicted value is negatively associated with BonusMalus of the driver.

6 Conclusion

NeurFS offers several advantages over the existing methods in the literature. We provide explicit formulas for the mean and variance of the aggregate loss when the model takes account of the nonlinearity and the dependency. A wide range of distributions studied in the literature can be utilized for marginal distributions without additional effort. We also propose an efficient estimation process with detailed neural network architectures. To interpret the results of NeurFS, we apply the SHAP which is a more consistent and accurate tool for explaining machine learning models. Numerical experiments including the artificial example and the real dataset confirm the effectiveness and accuracy of our model. It is also worth noting that application of NeurFS is not limited to the insurance claim prediction.

This scalable but transparent model can be an important alternative to the traditional GLM in insurance business where the large volume of data is available, but strict regulations are imposed. In particular, our research output will contribute to maintaining the competitiveness of an insurer by predicting insurance claims accurately, and avoiding adverse selection. Lastly, the proposed model can be applied to analyzing operations losses, health care expenditures or credit assessment data where a joint distribution of frequency and severity is involved.

| Frequency distributions | ||||

|---|---|---|---|---|

| Models | ||||

| Binomial | ||||

| Poisson | ||||

| ZIP | ||||

| Severity distributions | ||||

| Models | ||||

| Gamma | ||||

| Inverse Gaussian | ||||

| Normal | ||||

| Frequency distributions | |||

|---|---|---|---|

| Models | |||

| Binomial | |||

| Poisson | |||

| ZIP | |||

References

- Adebayo et al. [2018] J. Adebayo, J. Gilmer, M. Muelly, I. Goodfellow, M. Hardt, and B. Kim. Sanity checks for saliency maps. Working paper, 2018.

- Barron [1993] A. Barron. Universal approximation bounds for superpositions of a sigmoidal function. IEEE Transactions on Information theory, 39:930–945, 1993.

- Brechmann et al. [2014] E. Brechmann, C. Czado, and S. Paterlini. Flexible dependence modeling of operational risk losses and its impact on total capital requirements. Journal of Banking & Finance, 40:271–285, 2014.

- Castro-Nuno and Arevalo-Quijada [2018] M. Castro-Nuno and M. Teresa Arevalo-Quijada. Assessing urban road safety through multidimensional indexes: Application of multicriteria decision making analysis to rank the spanish provinces. Transport policy, 68, 2018.

- Chavez-Demoulin et al. [2006] V. Chavez-Demoulin, P. Embrechts, and J. Nešlehová. Quantitative models for operational risk: extremes, dependence and aggregation. Journal of Banking & Finance, 30(10), 2006.

- Clevert et al. [2016] D-A. Clevert, T. Unterthiner, and S. Hochreiter. Fast and accurate deep network learning by exponential linear units (elus). International Conference on Learning Representations(ICLR), 2016.

- Cohen and Siegelman [2010] A. Cohen and P. Siegelman. Testing for adverse selection in insurance markets. Journal of Risk and insurance, 77(1), 2010.

- Czado et al. [2012] C. Czado, R. Kastenmeier, E. C. Brechmann, and A. Min. A mixed copula model for insurance claims and claim sizes. Scandinavian Actuarial Journal, 4, 2012.

- Dahen and Dionne [2010] H. Dahen and G. Dionne. Scaling models for the severity and frequency of external operational loss data. Journal of Banking & Finance, 34(7), 2010.

- Frees [2014] E. W. Frees. Ch6. Frequency and severity models in Predictie Modeling Applications in Actuarial Science. Cambridge University Press, 2014.

- Frees et al. [2011a] E. W. Frees, J. Gao, and M. A. Rosenberg. Predicting the frequency and amount of health care expenditures. North American Actuarial Journal, 15(3):377–392, 2011a.

- Frees et al. [2011b] E. W. Frees, G. Meyers, and A. D. Cummings. Summarizing insurance scores using a gini index. Journal of the American Statistical Association, 106(495):1085–1098, 2011b.

- Frees et al. [2014] E. W. Frees, G. Meyers, and A. D. Cummings. Insurance ratemaking and a gini index. Journal of Risk and Insurance, 81(2):335–366, 2014.

- Garrido et al. [2016] J. Garrido, C. Genest, and J. Schulz. Generalized linear models for dependent frequency and severity of insurance claims. Insurance: Mathematics and Economics, 70:205–215, 2016.

- Gschlöl and Czado [2007] S. Gschlöl and C. Czado. Spatial modelling of claim frequency and claim size in non-life insurance. Scandinavian Actuarial Journal, 3:202–225, 2007.

- Guelman [2012] L. Guelman. Graient boosting trees for auto insurance loss cost modeling and prediction. Expert Systems with Applications, 39:3659–3667, 2012.

- He et al. [2015] K. He, X. Zhang, S. Ren, and J. Sun. Delving deep into rectifiers: Surpassing human-level performance on imagenet classification. Proceedings of the IEEE international conference on computer vision(ICCV), 2015.

- Hornik [1991] K. Hornik. Approximation capabilities of multilayer feedforward networks. Neural Networks, 4:251–257, 1991.

- Hornik et al. [1989] K. Hornik, M. Stinchcombe, and H. White. Multilayer feedforward networks are universal approximators. Neural Networks, 2:359–366, 1989.

- Huang and Meng [2019] Y. Huang and S. Meng. Automobile insurance classification ratemaking based on telematics driving data. Decision Support Systems, 127, 2019.

- Ioffe and Szegedy [2015] S. Ioffe and C. Szegedy. Batch normalization: Accelerating deep network training by reducing internal covariate shift. International conference on machine learning, pages 448–456, 2015.

- Kelly and Nielson [2006] M. Kelly and N. Nielson. Age as a variable in insurance pricing and risk classification. The Geneva Papers on Risk and Insurance-Issues and Practice, 31(2):212–232, 2006.

- Kingma and Ba [2015] D. Kingma and J. Ba. Adam: A method for stochastic optimization. International Conference on Learning Representations(ICLR), 2015.

- Kramer et al. [2013] N. Kramer, E. Brechmann, D. Silversrini, and C. Czado. Total loss estimation using copula-based regression models. Insurance: Mathematics and Economics, 53:829–839, 2013.

- Lundberg and Lee [2017] S. Lundberg and S. Lee. A unified approach to interpreting model predictions. Advances in neural information processing systems(NeurIPS), 2017.

- Pan and Vivek [2016] X. Pan and S. Vivek. Expressiveness of rectifier networks. International Conference on Machine Learning(ICML), pages 2427–2435, 2016.

- Reddi et al. [2018] S. Reddi, S. Kale, and S. Kumar. On the convergence of ADAM and beyond. International Conference on Learning Representations(ICLR), 2018.

- Riberiro et al. [2016] M. T. Riberiro, S. Singh, and C. Guestrin. Why should i trust you?: Explaining the predictions of any classifier. 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 1135–1144, 2016.

- Shapley [1953] L. Shapley. A value for n-person games. Contributions to the Theory of Games, 2:307–317, 1953.

- Shi et al. [2015] P. Shi, X. Feng, and A. Ivantsova. Dependent frequency-severity modeling of insurance claims. Insurance: Mathematics and Economics, 64:417–428, 2015.

- Srivastava et al. [2015] N. Srivastava, G. Hinton, A. Krizhevsky, I. Sutskever, and R. Salakhutdinov. Dropout: a simple way to prevent neural networks from overfitting. The journal of machine learning research, 15:1929–1958, 2015.

- Su and Bai [2020] X. Su and M. Bai. Stochastic gradient boosting frequency-severity model of insurance claims. PloS one, 15, 2020.

- Yang et al. [2018] Y. Yang, W. Qian, and H. Zou. Insurance premium prediction via gradient tree-boosted Tweedie compound Poisson models. Journal of Business & Economic Statistics, 36(3):456–470, 2018.

- Zhou et al. [2020] H. Zhou, W. Qian, and Y. Yang. Tweedie gradient boosting for extremely unbalanced zero-inflated data. Communications in Statistics-Simulation and Computation, online:1–23, 2020.