Deo, Murthy

EFFICIENT BLACK-BOX IMPORTANCE SAMPLING FOR VaR AND CVaR ESTIMATION

ABSTRACT

This paper considers Importance Sampling (IS) for the estimation of tail risks of a loss defined in terms of a sophisticated object such as a machine learning feature map or a mixed integer linear optimization formulation. Assuming only black-box access to the loss and the distribution of the underlying random vector, the paper presents an efficient IS algorithm for estimating the Value at Risk and Conditional Value at Risk. The key challenge in any IS procedure, namely, identifying an appropriate change-of-measure, is automated with a self-structuring IS transformation that learns and replicates the concentration properties of the conditional excess from less rare samples. The resulting estimators enjoy asymptotically optimal variance reduction when viewed in the logarithmic scale. Simulation experiments highlight the efficacy and practicality of the proposed scheme.

1 INTRODUCTION

Value at Risk (VaR) and Conditional Value at Risk (CVaR) constitute two widely used measures of tail risk in quantitative risk management [McNeil et al. (2015)]. Desirable properties such as subaddivity, convexity, etc., have allowed CVaR to further flourish as a vehicle for introducing risk aversion in planning problems in operations and machine learning (see, for example, \shortciteNProckafellar2000optimization,bienstock2014chance,ban2018machine,tamar2016sequential). The value at risk at a tail probability level is the -th quantile of the loss distribution. CVaR at level is the expected value of the loss over its largest fraction of outcomes and is relatively more challenging to estimate than VaR [Lim et al. (2011)]. With a limited fraction of data representing the loss distribution tail, estimation of VaR/CVaR via simulation is executed typically with a rare event simulation technique such as importance sampling, splitting, conditional Monte Carlo or control variates for the purposes of variance reduction and accelerated estimation [Glasserman (2013)].

As we explain imminently in the context of importance sampling (IS), efficient use of these simulation techniques rely often on leveraging the structure of the loss at hand and the distribution of the underlying random vector. In terms of general methodology, \citeNPglynn1996importance demonstrates how variance reduction using IS in tail estimation can be translated to efficient estimation of VaR. \citeNPsun2010asymptotic develop asymptotic representations for VaR/CVaR which yield conveniently applicable characterizations of asymptotic variances for VaR and CVaR. \shortciteNPbardou2008computation,egloff2010quantile and, more recently, \shortciteNPhe2021adaptive develop adaptive algorithms which incorporate generic IS changes of measure in estimation of VaR/CVaR. While generically applicable, it is not within the scope of these works to provide specific prescriptions of IS changes of measure that offer variance reduction guarantees. In this regard, \shortciteNPglasserman2000variance,glasserman2002portfolio,BJZWSC demonstrate how the properties of multivariate normal and distributions can be exploited to reap substantial variance reduction in portfolio risk estimation contexts. These algorithms critically utilize the specific structural properties of the loss, such as the linear-quadratic or the sum of indicators structure, and are restricted to settings involving multivariate normal and distributions.

In a number of operations and risk management contexts, the underlying loss often involves a sophisticated structure. Planning problems typically specify a loss in terms of an optimization formulation involving numerous constraints. In the rapidly growing instances of operations and risk management models which use machine learning tools, a suitable loss is written in terms of a feature-map (or) a feature-based decision rule specified, for example, in terms of representation-learning devices such as kernels or deep neural networks (see \shortciteNPban2019big,SmartPredictOpt and references therein). Given the rich modelling power of these loss instances, it is impractical to explicitly tailor the IS change of measure to the problem considered. Adaptive IS methods, which utilize the estimator variance (or) cross-entropy criterion [Rubinstein and Kroese (2013)] to search for the best parameter choice within a chosen IS distribution family, remain the most common approach to address this challenge. The performance of the adaptive approaches is however determined crucially by the IS family distribution family initially chosen and may additionally involve systematic underestimation \shortcitearief2021deep.

This paper aims to tackle the challenges in marrying efficiency with black-box IS for VaR/CVaR estimation. Restricting to multivariate normal distributions, \shortciteNPbai2020rare,arief2021deep utilise the machinery of dominating points to algorithmically arrive at efficient IS mixture distributions for estimation of distribution tails of losses that can be either directly written or approximated with a piece-wise linear structure. Assuming only a black box access to the evaluations of loss and the distribution of the underlying random vector we present here an efficient IS algorithm (Algorithm 1) to jointly estimate VaR/CVaR of . The IS scheme in this paper builds upon a generically applicable large deviations framework and the IS scheme developed in \citeNPdeo2021achieving for the estimation of distribution tails. Exploiting the self-similarity in conditional excess distributions at different thresholds, the novel approach informs a suitable IS measure by extrapolating excess loss samples observed at less rare thresholds. We show that the proposed IS scheme offers asymptotically optimal variance reduction, when viewed at a logarithmic scale, for a broad class of useful losses and multivariate distributions. Specifically, given any we show that the sample complexity for estimating CVaR at a tail probability level scales as with the proposed IS scheme. It is instructive to contrast this with the scaling of obtained for the case of naive estimation without IS. We complement the variance reduction guarantees with numerical experiments that validate the efficacy and generic applicability of the proposed scheme.

We note that an attempt at black box CVaR estimation is made by \citeNPdeo2020optimizing for the case where has regularly varying tails (that is, when , for ). While their scheme bears some similarity to Algorithm 1, it relies heavily on the weak convergence properties of regularly varying densities, and does not result in asymptotically optimal variance reduction.

Notation: We use to denote convergence in distribution. Boldface letters denote vectors. Likewise for a function , . We let denote a normal variable with mean and variance . Let denote the norm of a vector and denote the -metric ball of radius centred at . For an increasing function , we let denote its left-inverse. For real valued functions and , we say that as if there exist positive constants such that for all , . We say that if for some .

2 PROBLEM DESCRIPTION

Suppose denotes the loss incurred when the underlying random vector realizes the value . Let denote the distribution function of , that is, , and let be its density. Given a confidence level , denote the Value at Risk (VaR) and Conditional Value at Risk (CVaR) of the loss at level as,

respectively. Our objective is to enable efficient estimation of the VaR and CVaR for values of close to 0. Assumption 1 below imposes a mild regularity condition on the function whose evaluation may be available only via a black-box.

Assumption 1.

The function satisfies the following conditions:

-

(i)

the set is contained in for all sufficiently large and

-

(ii)

for any sequence of satisfying we have

where is a positive constant and the limiting function is such that the cone is nonempty.

Assumption 1 stipulates that the loss incurred, denoted by is large when at least one of components of takes large values. Besides commonly considered examples such as piecewise affine and linear-quadratic losses, Assumption 1 is satisfied for a wide-class of operations and quantitative risk management models that motivate our study. These include cases where is written as the value of a suitable mixed integer linear program or a quadratic program, and instances in prescriptive analytics where a suitable is written in terms of feature maps or decision-rules specified by a neural network with ReLU activation units. We refer the reader to \citeNP[Section 2]deo2021achieving for a precise description of these examples for which Assumption 1 is readily satisfied. Notably, Assumption 1 does not require the loss to be convex or possess specific combinatorial structure.

Monte-Carlo estimation without any change of measure. Given independent samples of , let denote the empirical cumulative distribution function (c.d.f.) formed from the samples . Then the VaR and CVaR at level can be estimated as,

| (1) |

respectively. These estimators satisfy asymptotic normality under nominal assumptions (see, for example, \citeNP[pg. 75]serfling2009approximation and \shortciteNP[Theorem 2]trindade2007financial):

| (2) |

where

| (3) |

The asymptotic variances indicate the price paid in terms of sample complexity when Observe that (2) and (3) imply that with the error in CVaR estimation with samples is roughly . It can be seen that (see for example, (23)). Therefore, estimating within a relative error of with confidence necessarily requires samples of when using the above sample-average based estimators; see also \citeNPsun2010asymptotic. Since this sample requirement is impractically large when is small, importance sampling is typically considered in order to reduce mean square error (MSE) to a lower order than

3 THE PROPOSED IS ALGORITHM

We begin by describing the IS scheme presented in Algorithm 1 below. To circumvent the issue of limited relevant observations in tail exceedance events of the form IS typically involves obtaining samples from an alternate distribution under which these exceedance events are less rare. To accomplish this in our context, define the -valued function , where is a decreasing function of explicitly identified in Algorithm 1 and

| (4) |

Exponentiation is done component-wise in the above expression for as in, In Algorithm 1, we use independent samples of as the samples from IS distribution specified implicitly via The map can be shown to be invertible almost everywhere on (see \citeNP[Proposition 1]deo2021achieving) and the resulting vector has a probability density if has a density. Letting and denote the respective densities of and the likelihood ratio resulting from this change-of measure is given by,

| (5) |

An explicit expression of the Jacobian, in the above expression, is given in Algorithm 1. With this change-of-measure, we have the following unbiased estimator for the c.d.f.

| (6) |

where are drawn i.i.d. from , and . Subsequent IS estimation of involves a routine computation of VaR and CVaR from the given IS estimator for the c.d.f. and is described precisely in Algorithm 1 below.

| (7) |

| (8) | ||||

| (9) |

A key feature of Algorithm 1 is that it is agnostic to the specific forms of both the loss and the distribution of and it requires only a black-box access to evaluations of and This is in sharp contrast to most existing literature requiring careful tailoring of the IS density to the underlying distribution and the loss considered. Building on the self-structuring IS procedure introduced in \citeNPdeo2021achieving for estimating tail probabilities of the form Algorithm 1 below offers a suitable adaptation to the root-finding task required to estimate VaR. In contrast to estimating for a fixed large , VaR/CVaR estimation requires that the extrapolation parameter is chosen carefully as a function of such that variance reduction is pronounced even if the precise range of over which root-finding has to be conducted for quantile estimation is not known apriori. The choice of hyperparameter can be made either with a cross-validation based approach we demonstrate in numerical experiments, or with recursive schemes such as those considered in \citeNPbardou2008computation or \shortciteNPhe2021adaptive.

4 VARIANCE REDUCTION GUARANTEES FOR ALGORITHM 1

Let , where denotes the hazard function of component We say that is regularly varying if for all ,

for some (see \citeNP[Definition B.1.1]de2007extreme). In this case, we write Letting we see that vector has standard exponential distribution as marginals. Just as in the use of copula models, standardization of marginals allows to state the main result without getting distracted by the differing marginal distributions.

Assumption 2.

The marginal distribution of is such that each of are eventually strictly increasing and for some The joint distribution, when written in terms of the probability density of admits the form,

| (10) |

where the functions satisfy the following: There exists a limiting function such that,

| (11) |

for any sequence of satisfying and

A wide variety of parametric and nonparametric multivariate distributions, including normal, exponential family, elliptical, log-concave distributions and Archimedian copula models satisfy Assumption 2. Marginal distributions which satisfy include all distributions that are either Weibull-type heavy-tailed or possess lighter tails (such as exponential, normal, etc.). See \citeNP[Appendix B]deo2021achieving for further details and sufficient conditions directly in terms of the distribution of

Choice of the IS density. A cornerstone of VaR/CVaR estimation is the accurate estimation of the loss tail distribution, for large values of . In elementary examples, this is typically achieved by choosing an IS density with features suitably mirroring the conditional distribution of over (see \citeNP[Section 4.2]bucklew2013introduction). A central component in this endeavour is to utilize large deviations to identify the most likely way in which the loss becomes large. For the broad family of losses and distributions specified by Assumptions 1 and 2 above, \citeNPdeo2021achieving show that the sequence of random vectors satisfy (i) the following large deviations principle (LDP),

| (12) |

and (ii) consequently, satisfy the tail asymptotic,

| (13) |

for some positive constant (see \citeNP[Theorems 3.3 and 4.1]deo2021achieving).

The lack of explicit dependence on parameter in the right-hand side of (13) suggests that the concentration of the target conditional distribution of may be approximated from the conditional samples of where and as the tail probability level The requirements on ensure that the event though rare by itself, is significantly less rare than the target event and is observed more often in the samples. Letting the map in Algorithm 1 suitably replicates these more frequent samples from the less rare region onto the target set Specifically, the distribution of can be roughly written as approximating the conditional distribution of given as in,

| (14) |

Example 1.

To see (14) by means of an example, suppose has a multivariate exponential distribution with density , , for some and (see \citeNP[Section 4]lu1990some). Changing variable to and letting we obtain

as and over in the region

Indeed the approximating feature of demonstrated in Example 1 can be shown to hold more generally for any satisfying Assumption 2; see \citeNP[Proposition 5.1]deo2021achieving for a precise statement of this self-structuring feature of the map and the accompanying figures. The following asymptotic variance reduction guarantees for the proposed VaR/CVaR estimation are obtained as a consequence.

Theorem 1

Considering the proposed change of measure for the example of CVaR estimation, Theorem 1 guarantees a sample complexity of as where can be made arbitrarily small. Thus the asymptotic variance reduction is optimal when viewed in the logarithmic scale (see \shortciteNPBJZWSC). In contrast, naive estimation without any change of measure requires samples. With the variance reduction guarantee holding for any choice of hyperparameter an effective can be chosen via cross-validation without incurring a change of scaling in sample complexity. The numerical experiments below demonstrate this by illustrating the relative insensitivity of variance reduction to various choices of

5 NUMERICAL EXAMPLES

For a given loss and the random vector we adopt the following procedure across all the experiments. Following Algorithm 1, we take independent samples to arrive at the IS c.d.f. estimate in (6) and subsequently use it to arrive at the IS VaR estimate and the IS CVaR estimate in (9). For every choice of considered, the hyper-parameter is chosen by performing cross-validation over the observed coefficient of variation. Each experiment involves computation of CVaR as above from independent samples of and we report the relative root-mean square error = (root mean-square error of CVaR observed across 50 independent experiments)/(average of CVaR observed across 50 experiments). To enable comparison with naive estimation without IS, we also report its sample complexity for attaining the same precision offered by the IS algorithm. We observe the following across the experiments: 1) the proposed IS has a significantly smaller relative error and a lower sample complexity when compared to estimation without any change of measure, and 2) the errors obtained using IS do not increase as the problem is made increasingly difficult by considering smaller values of These observations align with the conclusions of Theorem 1. The specific details of the experiments are given below.

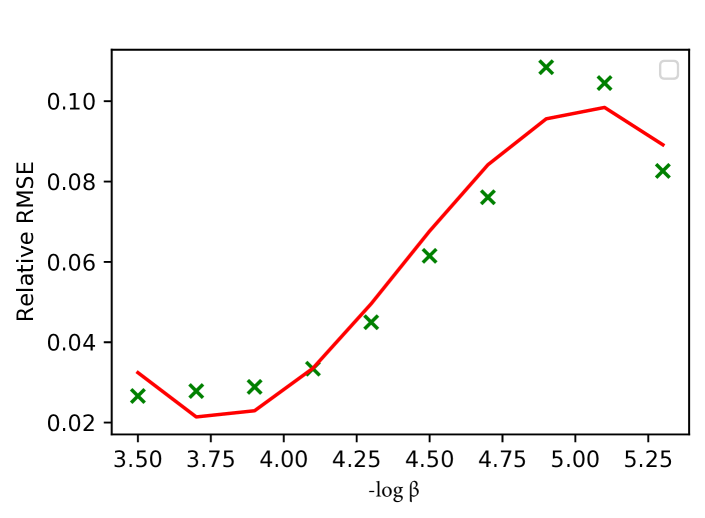

5.1 PERT Network:

We consider a PERT network where the project completion time is generally written as the value of a mixed integer linear program. We consider an example with tasks and take . Here is taken to be completion time of the PERT network when the individual task completion times realise the values . To demonstrate performance for heavier than exponential delays, we assume that the marginal distribution of each delay is and their joint dependence is through a Gaussian copula whose correlation matrix is given by

| (15) |

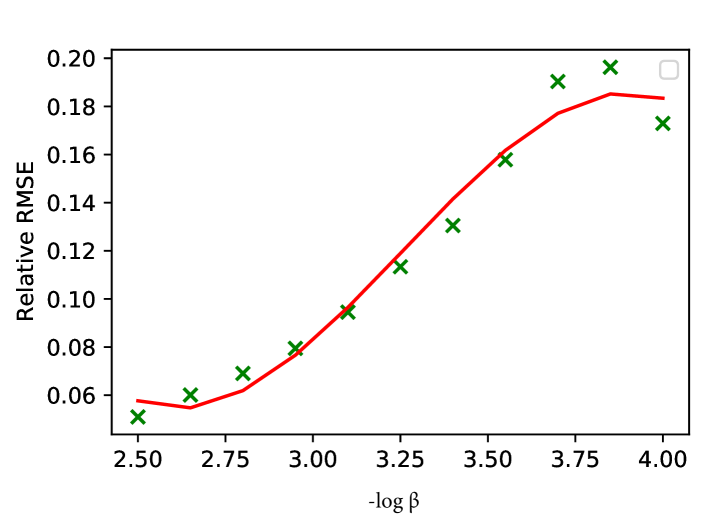

In each experiment, we take samples to compute VaR/CVaR using the IS estimator. We plot the observed root mean square errors (observed across 50 independent experiments) in Figure 1 as a function of the tail probability level . The parameter is selected as . Figure 1(a) details the results. Contrast this to estimation without IS which requires samples to attain a relative error similar to the IS scheme at (see Figure 1(b)).

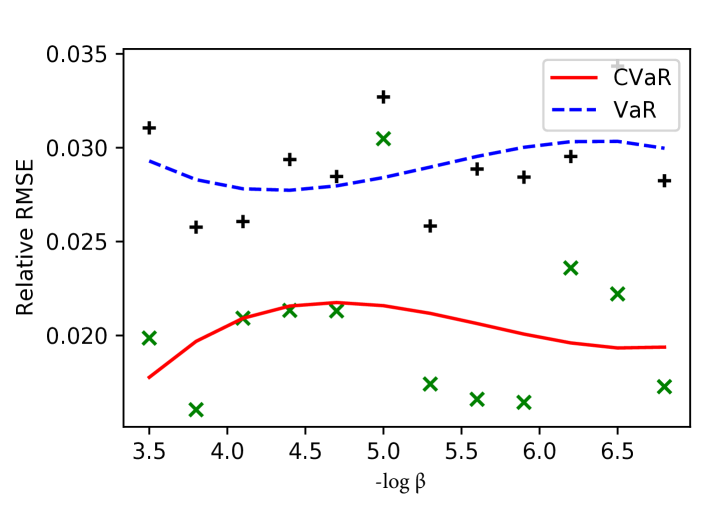

5.2 Linear portfolios:

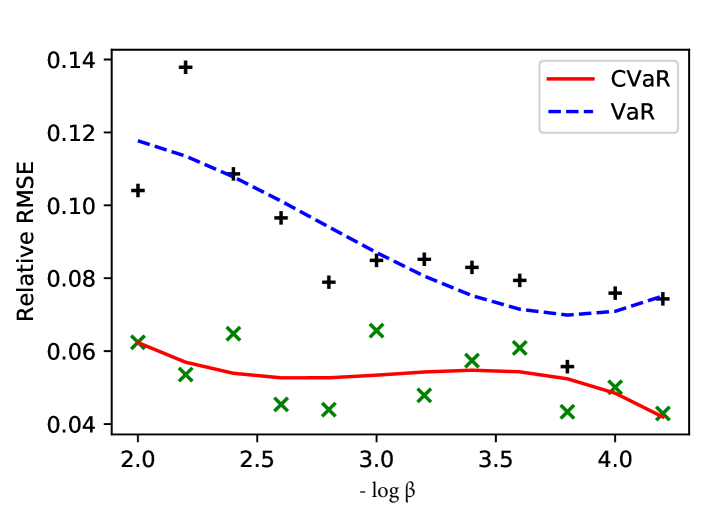

We consider the equally weighted linear portfolio loss in this example. To illustrate performance in a case where the marginal distributions of the components of are different, we consider the marginal c.d.f.s where for , and for . Dependence among the components of is introduced through a Gaussian copula for which the correlation matrix is specified by the off-diagonal entries for , and diagonal entries for . Figure 2(a) below presents details on cross-validation by plotting the relative error of estimation observed for different choices of hyper-parameter considered. With the relative RMSE staying less than throughout the interval we note that the error reduction is robust and the estimator variance is relatively less sensitive to the choice of parameter Notice from Figure 2(b) that a relative error between is obtained with only samples upon use of the IS algorithm, and that this error is constant even as the target level is varied from to . Note that to obtain a relative error at level , estimation without IS requires samples.

5.3 Forest fires data-set

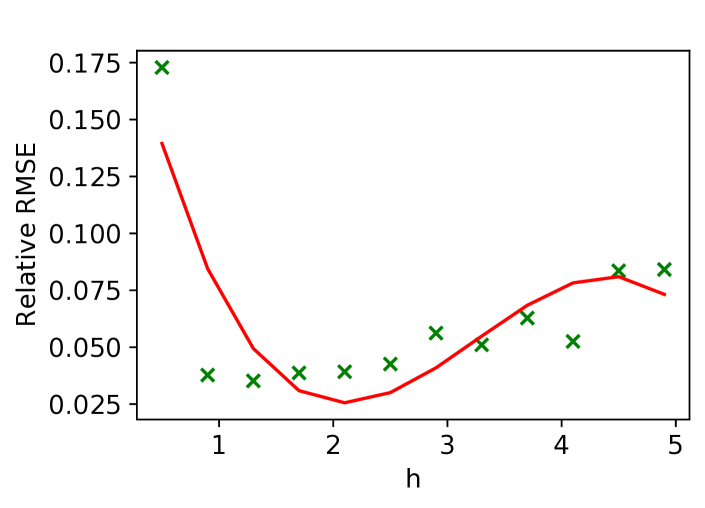

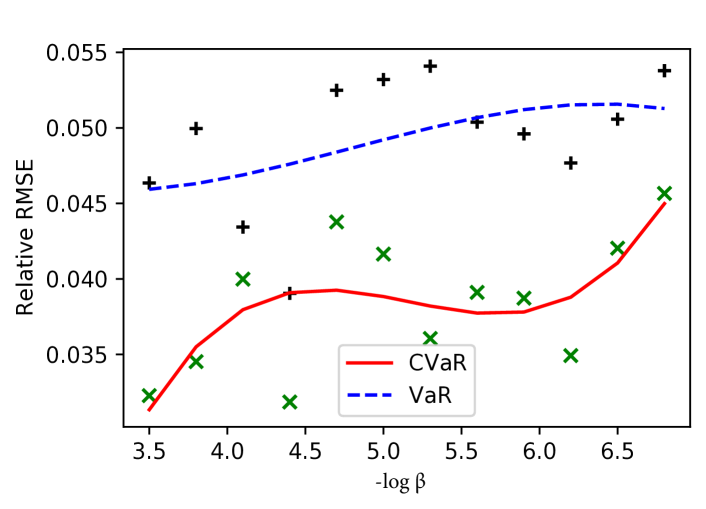

We consider a loss trained from the forest fires dataset used in \citeNPcortez2007data in this example. The input covariates consist of climatic factors such as wind speed, daily rainfall, temperature, humidity etc. The output is the area of forest fires, in hectares, corresponding to the respective climatic data. We train a deep neural network (DNN) network to learn the function , which maps the covariates to the log of the area of the forest fire. The DNN has one hidden layer consisting of 12 neurons with ReLU link. The parameters are learnt via stochastic gradient descent. We consider the following example distribution for covariates for the sake of the experiment: The marginal distribution of the components are given by and the dependence structure is informed via a Gaussian copula whose correlation matrix is given as in (15). For the purpose of this experiment, we choose in (9) to match the size of the input data-set. As before, we cross validate over the parameter (see Figure 3(a)), and then using in Algorithm 1, jointly estimate VaR / CVaR for . Figure 3(b) gives the result of our experiment. It is worthwhile to note that although the loss is a black box, our algorithm still produces estimates of VaR/CVaR with a small relative error (4-6% for CVaR and 7-10% for VaR). Contrast this to MC estimation, which requires samples to give a relative error of in CVaR estimation at .

6 PROOF OF THEOREM 1

For ease of presentation, we focus on variance reduction in CVaR estimation and assume that has identical marginals (that is, for all ). The proof for the case where has heterogeneous marginals can be similarly accomplished by introducing a vector for capturing differing relative tail heaviness as in the results in \citeNPdeo2021achieving. To begin, we recall \citeNP[Corollary 2]sun2010asymptotic, as applicable to our IS estimator:

| (16) |

where and the likelihood ratio is defined as in (5). To present the main ideas in deconstructing the above variance term, we postpone the verification of the technical conditions required for applying \citeNP[Corollary 2]sun2010asymptotic towards the end of this section.

For any and , let be a ball of radius centred at under the norm. Denote by . Define be the component-wise inverse, and . Let denote the hazard rate of and Define . Finally, let . For notational convenience, let denote the second moment of . For , let denote its characteristic function; that is, if and if . Further, for a function and let denote the super-level set of Let .

With this notation, see that . Changing variables from to in the expectation below (see (EC.16) onward in the proof of Lemma EC.6 of \citeNPdeo2021achieving for detailed steps in a similar change of variables exercise), we obtain

| (17) |

| (18a) | |||

| (18b) | |||

| (18c) | |||

| (18d) |

Notice that is well defined for all . Observe that from (13), . Next, recall that and that . Hence, from \citeNP[Proposition B.1.9 (viii)]de2007extreme, . Therefore, and as . Hence, the following conclusions of \citeNP[Lemmas A.8-A.11 and Corollary A.3]deo2021achieving hold: for , for all sufficiently small enough ,

| (19a) | |||

| (19b) | |||

| (19c) |

whenever Let be the unit vector in the direction of . Rewrite

uniformly over ; the second equality in the above is obtained upon noting that , and using the continuous convergence of as specified in Assumption 1. Further, as , for any ,

Therefore, (19b) suggests that uniformly over , for all sufficiently small. Further, since for all small enough

| (20) |

Now for any from the bounds in (19a), (19c) and (20), one obtains that whenever as ,

Noting that satisfies an LDP with rate function , an application of the general Varadhan’s integral lemma (see \citeNP[Theorem 2.2]LD_Varadhan) yields,

| (21) |

Since has standard exponential marginals, for all (see \citeNP[Lemma 3.4 (d)]deo2021achieving). The infimum in (21) therefore occurs in a compact set. As above is arbitrary, we have

| (22) |

Next, as a consequence of (13), as . With we have With the choice of being arbitrary, we therefore have for any . Finally, for the Monte Carlo estimator without change-of-measure, . Notice that

| (23) |

Further, notice that following the analysis from (17), for any , . Hence, . Thus, we have that for all ,

Verification of the conditions of \citeNP[Corollaries 1 and 2 ]sun2010asymptotic: Here we perform the pending verification of \citeNP[Assumption 2]sun2010asymptotic. Notice that existence of automatically implies that \citeNP[Assumption 1]sun2010asymptotic holds, which is a sufficient condition for the central limit theorem to hold. Fix any . Notice that using a similar change of variables arguments as in the beginning of the proof (with denoting expectation under the IS measure), is bounded above by

| (24) |

AUTHOR BIOGRAPHIES

ANAND DEO is a Senior Research Assistant at Singapore University of Technology and Design. His research interests span applied probability, quantitative risk management, operations research, and machine learning. Formerly, he was a PhD student at the Tata Institute of Fundamental Research, Mumbai. His e-mail address is .

KARTHYEK MURTHY is an Assistant Professor in Singapore University of Technology and Design. His research centers around building models and methods for incorporating competing considerations such as risk, robustness, and fairness in data-driven optimization problems affected by uncertainty. Before joining SUTD, he was a postdoctoral researcher at IEOR deparment, Columbia University and a PhD student at the Tata Institute of Fundamental Research, Mumbai. His e-mail address is .

ACKNOWLEDGEMENTS

Support from Singapore Ministry of Education grant MOE2019-T2-2-163 is gratefully acknowledged.

References

- Arief et al. (2021) Arief, M., Z. Huang, G. K. S. Kumar, Y. Bai, S. He, W. Ding, H. Lam, and D. Zhao. 2021. “Deep Probabilistic Accelerated Evaluation: A Robust Certifiable Rare-Event Simulation Methodology for Black-Box Safety-Critical Systems”. In International Conference on Artificial Intelligence and Statistics, 595–603. PMLR.

- Bai et al. (2020) Bai, Y., Z. Huang, H. Lam, and D. Zhao. 2020. “Rare-Event Simulation for Neural Network and Random Forest Predictors”. arXiv preprint arXiv:2010.04890.

- Ban et al. (2018) Ban, G.-Y., N. El Karoui, and A. E. Lim. 2018. “Machine learning and portfolio optimization”. Management Science 64(3):1136–1154.

- Ban and Rudin (2019) Ban, G.-Y., and C. Rudin. 2019. “The big data newsvendor: Practical insights from machine learning”. Operations Research 67(1):90–108.

- Bardou et al. (2008) Bardou, O., G. Pagès, and N. Frikha. 2008. “Computation of VaR and CVaR using stochastic approximations and unconstrained importance sampling”. arXiv preprint arXiv:0812.3381.

- Bassamboo et al. (2005) Bassamboo, A., S. Juneja, and A. Zeevi. 2005. “Expected shortfall in credit portfolios with extremal dependence”. In Proceedings of the Winter Simulation Conference, 2005., 10 pp.–.

- Bienstock et al. (2014) Bienstock, D., M. Chertkov, and S. Harnett. 2014. “Chance-constrained optimal power flow: Risk-aware network control under uncertainty”. Siam Review 56(3):461–495.

- Bucklew (2013) Bucklew, J. 2013. Introduction to rare event simulation. Springer Science & Business Media.

- Cortez and Morais (2007) Cortez, P., and A. d. J. R. Morais. 2007. “A data mining approach to predict forest fires using meteorological data”.

- de Haan and Ferreira (2007) de Haan, L., and A. Ferreira. 2007. Extreme value theory: an introduction. Springer Science & Business Media.

- Deo and Murthy (2020) Deo, A., and K. Murthy. 2020. “Optimizing tail risks using an importance sampling based extrapolation for heavy-tailed objectives”. In 2020 59th IEEE Conference on Decision and Control (CDC), 1070–1077. IEEE.

- Deo and Murthy (2021) Deo, A., and K. Murthy. 2021. “Achieving Efficiency in Black Box Simulation of Distribution Tails with Self-structuring Importance Samplers”. arXiv preprint arXiv:2102.07060.

- Egloff and Leippold (2010) Egloff, D., and M. Leippold. 2010. “Quantile estimation with adaptive importance sampling”. The Annals of Statistics 38(2):1244–1278.

- Elmachtoub and Grigas (2021) Elmachtoub, A. N., and P. Grigas. 2021. “Smart “Predict, then Optimize””. Management Science 0(0):null.

- Glasserman (2013) Glasserman, P. 2013. Monte Carlo methods in financial engineering, Volume 53. Springer Science & Business Media.

- Glasserman et al. (2000) Glasserman, P., P. Heidelberger, and P. Shahabuddin. 2000. “Variance reduction techniques for estimating value-at-risk”. Management Science 46(10):1349–1364.

- Glasserman et al. (2002) Glasserman, P., P. Heidelberger, and P. Shahabuddin. 2002. “Portfolio value-at-risk with heavy-tailed risk factors”. Mathematical Finance 12(3):239–269.

- Glynn (1996) Glynn, P. W. 1996. “Importance sampling for Monte Carlo estimation of quantiles”. In Mathematical Methods in Stochastic Simulation and Experimental Design: Proceedings of the 2nd St. Petersburg Workshop on Simulation, 180–185. Citeseer.

- He et al. (2021) He, S., G. Jiang, H. Lam, and M. C. Fu. 2021. “Adaptive Importance Sampling for Efficient Stochastic Root Finding and Quantile Estimation”. arXiv preprint arXiv:2102.10631.

- Lim et al. (2011) Lim, A. E., J. G. Shanthikumar, and G.-Y. Vahn. 2011. “Conditional value-at-risk in portfolio optimization: Coherent but fragile”. Operations Research Letters 39(3):163–171.

- Lu and Bhattacharyya (1990) Lu, J.-C., and G. K. Bhattacharyya. 1990. “Some new constructions of bivariate Weibull models”. Annals of the Institute of Statistical Mathematics 42(3):543–559.

- McNeil et al. (2015) McNeil, A. J., R. Frey, and P. Embrechts. 2015. Quantitative risk management: concepts, techniques and tools-revised edition. Princeton university press.

- Rockafellar et al. (2000) Rockafellar, R. T., S. Uryasev et al. 2000. “Optimization of conditional value-at-risk”. Journal of risk 2:21–42.

- Rubinstein and Kroese (2013) Rubinstein, R. Y., and D. P. Kroese. 2013. The cross-entropy method: a unified approach to combinatorial optimization, Monte-Carlo simulation and machine learning. Springer Science & Business Media.

- Serfling (2009) Serfling, R. J. 2009. Approximation theorems of mathematical statistics, Volume 162. John Wiley & Sons.

- Sun and Hong (2010) Sun, L., and L. J. Hong. 2010. “Asymptotic representations for importance-sampling estimators of value-at-risk and conditional value-at-risk”. Operations Research Letters 38(4):246–251.

- Tamar et al. (2016) Tamar, A., Y. Chow, M. Ghavamzadeh, and S. Mannor. 2016. “Sequential decision making with coherent risk”. IEEE Transactions on Automatic Control 62(7):3323–3338.

- Trindade et al. (2007) Trindade, A. A., S. Uryasev, A. Shapiro, and G. Zrazhevsky. 2007. “Financial prediction with constrained tail risk”. Journal of Banking & Finance 31(11):3524–3538.

- Varadhan (1988) Varadhan, S. R. S. 1988. “Large deviations and applications”. In École d’Été de Probabilités de Saint-Flour XV–XVII, 1985–87, edited by P.-L. Hennequin, 1–49. Berlin, Heidelberg: Springer Berlin Heidelberg.