On a limit behaviour of a random walk penalised in the lower half-plane

A. Pilipenko

Institute of Mathematics, National Academy of Sciences of Ukraine, 3 Tereshchenkivska str., 01601, Kyiv, Ukraine; National Technical University of Ukraine “Igor Sikorsky Kyiv Polytechnic Institute”, Kyiv, Ukraine

pilipenko.ay@gmail.com and O. O. Prykhodko

National Technical University of Ukraine “Igor Sikorsky Kyiv Polytechnic Institute”, Department of Physics and Mathematics, 03056, Kyiv, Ukraine, 37, Peremohy ave.

o.prykhodko@yahoo.com

Abstract.

We consider a random walk which has different increment distributions in positive and

negative half-planes. In the upper half-plane the increments are

mean-zero i.i.d. with finite variance.

In the lower half-plane we consider two cases: increments are positive i.i.d. random variables with either

a slowly

varying tail or with a finite expectation. For the distributions with a slowly varying tails,

we show that has no weak limit in ; alternatively,

the weak limit is a reflected

Brownian motion.

Key words and phrases:

Invariance principle, Reflected Brownian motion

2000 Mathematics Subject Classification:

60F17; 60G50

A.Pilipenko was partially supported by the Alexander von Humboldt Foundation within

the Research Group Linkage Programme Singular diffusions: analytic and stochastic approaches,

the DFG Project Stochastic Dynamics with Interfaces (PA 2123/7-1),

and

the National Research

Foundation of Ukraine (project 2020.02/0014 “Asymptotic regimes of perturbed random walks:

on the edge of modern and classical probability”).

1. Introduction and main results

Let random variables be i.i.d. with a generic copy and ; are positive i.i.d., independent from the previous ones and with a generic copy .

We consider a random walk :

(1)

Figure 1. Sample path of (up to interpolation). Red vertical lines show when the jump is distributed as .

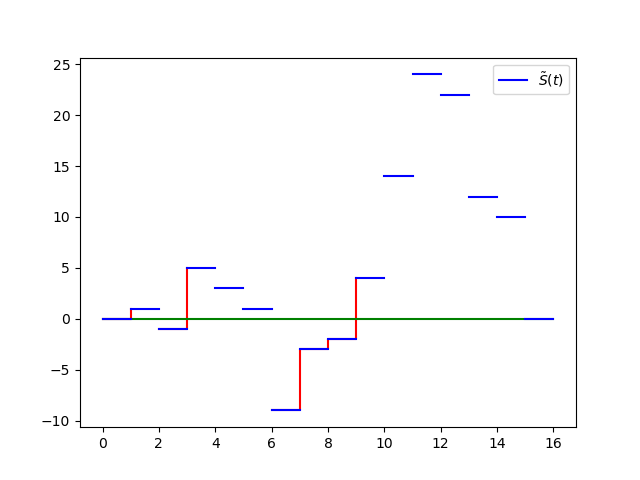

If , then the random walk has increments distributed as and on as .

Jumps pushes the random walk up from the negative half-plane. This can be interpreted as some non-immediate reflection to the positive half-plane. Similar approach

for stochastic differential equations is called the penalization method and

leads to a reflected diffusion if penalizations below zero are big enough, see for example

[Men83] or [Pil14, §1.4].

An interpretation of this model comes from the evaporation of gas from liquid in physics, for example, a model of ballistic evaporation [JLF14]. The usual form of speed distribution of a particle in a medium is Maxwell distribution. But in case when there is a medium change (a particle bounces off liquid) several papers have indicated that super- or sub-Maxwell distributions could apply [JLF14], [HKF16], [KS16].

Another interpretation is the following.

Consider an online shop with a warehouse. Assume that the warehouse is replenished every day (e.g. under a long-term contract) and also that the expectation of supply equals the expectation of demand. So,

the increments of the number of goods in the warehouse are mean-zero random variables if the warehouse is non-empty.

In case when the virtual amount of goods in stock is negative, i.e., the warehouse is empty and we

have unsatisfied orders, the shop seeks

to refill the warehouse by buying batches of goods until it has a positive balance.

In our model this refilling corresponds to the sequence . If we consider a regular shop or a traditional queueing

model, then the unsatisfied orders would be discarded and the walk couldn’t overjump a zero-level.

While the shortage is not overcome (which may take some time), the shop does not sell any goods.

Our goal is to analyse the limit of the scaled sequence of the processes as .

Depending on the distribution of we want to distinguish two cases:

(1)

has a finite expectation:

(2)

the distribution of has a slowly varying tail

where a set of slowly varying functions (check definition 1.4.2 in [BGT87]).

Remark 1.

Another interesting case is when the tail of is regularly varying, i.e., belongs to the domain of attraction of an -stable distribution. This case was studied in [PP14] with the restriction on to be in and greater than or equal to . We conjecture that the limit process should be the same as in [PP14], although we postpone the proof for the future paper.

For the case we assume that is linearly interpolated for :

Theorem 1.

A sequence of processes

converges weakly in to a reflected Brownian motion:

Remark 2.

It is well-known that has the same distribution as the absolute value of a Brownian motion , see for example Theorem 1.3.2 in [Pil14].

For the second case we assume has a flat-right interpolation for :

Theorem 2.

For a sequence of processes

there is no weak limit in . Moreover for any

(2)

Our results show that intuitively understandable things happen: when has an expectation, the process behaves like a Brownian motion with a reflection; otherwise when has a slowly varying tail, the process blows up at the beginning.

Note that model (1) is equivalent (up to recounting of and ) to the following

(3)

where is the number of visits to before the time :

(4)

We work only with this representation in the paper further.

Denote

(5)

So

(6)

We set by definition for all

Although the cases we discuss are very different, we tried to pick out common traits in

Section 2.

In Section 3 we prove Theorem 1. We aim to show that converges to and do so by showing that the latter lies neatly between and .

The proof of the second case can be found in Section 4 and is based on the

observation that the overshoots above level of the random walk are much larger than . This is a known property, proved by Rogozin, see for example Theorem 8.8.2

in [BGT87]. Thus we need to show that this overshoot happens before because only

in this way it could affect .

2. Proof: shared part

Let be a (sign flipped) running minimum of :

(7)

Lemma 1.

For each

(8)

Proof.

The left inequality is trivial when . Assume that and that for some

(9)

Take , such that and . This is always possible since .

Thus

From (9) we infer that . Therefore which contradicts with our choice of .

As for the right hand side inequality, observe that

jumps downwards at only when and jumps downwards. Thus for every

Hence

Taking maximum over of both sides of the last inequality we get

∎

By the Donsker theorem

meaning a weak convergence in . By the Skorokhod Representation theorem (Theorem 6.7 in [Bil99]) we can construct a probability space which supports random elements and such that

and the uniform convergence holds

(10)

for .

To emphasize that we work on this new space we will write a

whenever we use random variables dependent on .

Without loss of generality we may assume that this new probability space is reach enough and contains

a copy of the sequence . We leave the same notation and assume that

the original sequence belongs to this probability space.

Using sequences and

we construct copies of similarly to formulas (4), (7),

(6).

Note that in this constructions sequences

depend on but

does not. Often we will leave out indexing by , that is becomes .

[BGT87]

N. H. Bingham, C. M. Goldie, and J. L. Teugels.

Regular variation.

Cambridge University Press, Cambridge, 1987.

[Bil99]

P. Billingsley.

Convergence of Probability Measures.

Wiley, 1999.

[Gut13]

A. Gut.

Probability: A Graduate Course.

Springer New York, 2013.

[HKF16]

C. Hahn, Z. R. Kann, J. A. Faust, J. L. Skinner, and G. M. Nathanson.

Super-Maxwellian helium evaporation from pure and salty water.

The Journal of Chemical Physics, 144(4):044707, January 2016.

[JLF14]

A. M. Johnson, D. K. Lancaster, J. A. Faust, C. Hahn, A. Reznickova, and G. M.

Nathanson.

Ballistic evaporation and solvation of helium atoms at the surfaces

of protic and hydrocarbon liquids.

The Journal of Physical Chemistry Letters, 5(21):3914–3918,

October 2014.

[KS16]

Z. R. Kann and J. L. Skinner.

Sub- and super-Maxwellian evaporation of simple gases from liquid

water.

The Journal of Chemical Physics, 144(15):154701, April 2016.

[Men83]

J. L. Menaldi.

Stochastic variational inequality for reflected diffusion.

Indiana University mathematics journal, 32(5):733–744, 1983.

[Pil14]

A. Pilipenko.

An introduction to stochastic differential equations with

reflection.

Potsdam:Universitatsverlag, 09 2014.

[PP14]

A. Pilipenko and Yu. Prykhodko.

Limit behaviour of a simple random walk with non-integrable jump from

a barrier.

Theory of Stochastic Processes, 19 (35)(1):52–61, 2014.